© Center for Tax and Budget Accountability 200 1 CENTER FOR TAX AND BUDGET ACCOUNTABILITY 70 E. Lake Street Suite 1700 Chicago, Illinois 60601 direct: 312.332.1049 Email: [email protected] 2008 Legal Aid Conference For: Thursday, November 13, 2008; 1:30 pm Renaissance Chicago Hotel 1 West Wacker Drive Chicago, IL Presented by: Ralph Martire Executive Director

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

© Center for Tax and Budget Accountability 2008

1

CENTER FOR TAX AND BUDGET ACCOUNTABILITY70 E. Lake Street Suite 1700 Chicago, Illinois 60601 direct: 312.332.1049 Email: [email protected]

2008 Legal Aid Conference

For: Thursday, November 13, 2008; 1:30 pm

Renaissance Chicago Hotel1 West Wacker Drive

Chicago, IL

Presented by:Ralph MartireExecutive Director

© Center for Tax and Budget Accountability 2008

2

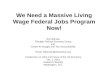

Fed Shapshot Pre-Meltdown

TO

TA

L F

ED

#’S

TO

TA

L F

ED

#’S

2007 Actual

2008 Estimated

2009 projected

GDP $13.668 T $14.312 T(+5%)

$15.027 T (+5%)

2007 Actual

2008 Enacted

2009 projected

Total Fed Budget

$2.730 T $2.931 T (+7%)

$3.107 T (+6%)

Disc Fed Budget

$880 B $9.41.4 B (+7%)

$987.6 B (+5%)

© Center for Tax and Budget Accountability 2008

3

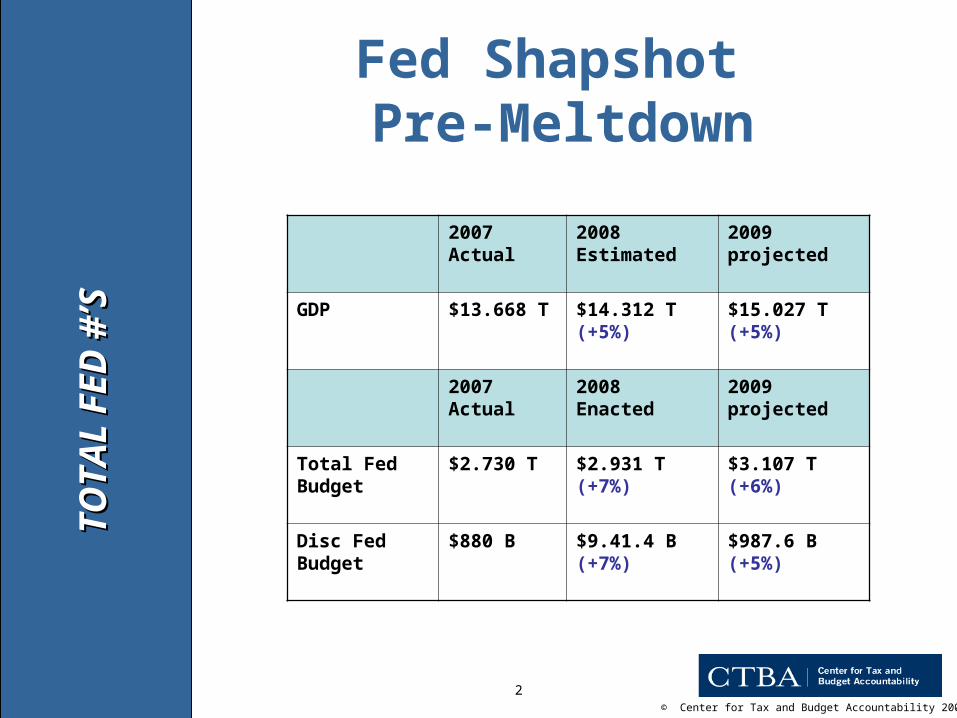

Pre-Bailout/Meltdown

2007 Actual

2008 Projected

2009 Estimated

Revenue 2.568 T $2.521 T(-2%)

$2.7T (+7%)

Deficit (they report, that is)

-$162 B -$410 B -$407 B

Real, On-Budget Deficit

-$343 B -$602 B -$611 BFE

D #

’SF

ED

#’S

How’s that Work……

© Center for Tax and Budget Accountability 2008

4

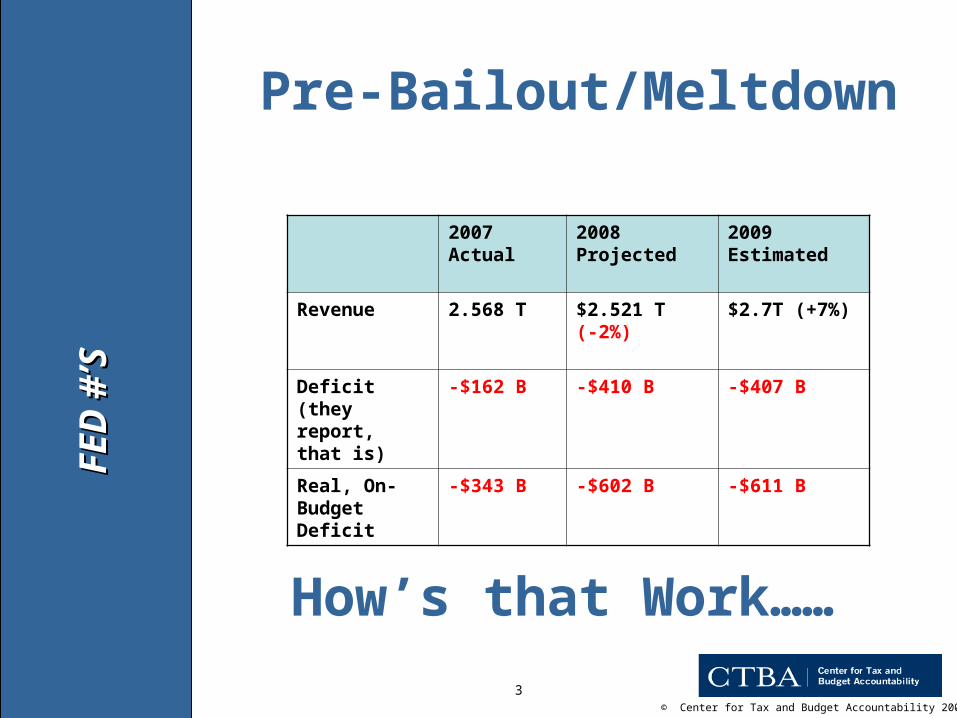

2007 Actual

2008 Enacted

2009 Requested/projected

Social Security Expenditures

$581 B $610 B $644 B

Social Security Revenue

$869 B $910 B $949 B

Social Security SURPLUS!

+$288 B +$300 B +$305 B

SO

CIA

L S

EC

UR

ITY

!S

OC

IAL

SE

CU

RIT

Y !

© Center for Tax and Budget Accountability 2008

5

2007 Actual

2008 Enacted

2009 Requested

Medicare $371 B $391 B $408 B

Medicaid + SCHIP

$197 B $211 B $224 B

Interest on Fed Debt

$237 B $244 B $260 B

TOTAL FED DEBT

$8.966 T $9.629 T $10.388 T

OT

HE

R M

AN

DA

TO

RY

O

TH

ER

MA

ND

AT

OR

Y

BU

DG

ET

IT

EM

S O

F N

OT

EB

UD

GE

T I

TE

MS

OF

NO

TE

© Center for Tax and Budget Accountability 2008

6

2007 Actual

2008 Enacted 2009 Requested

TOTAL $880 B $941.4 B (+7%)

$987.6 (+5%)

Defense + HLS

$441.4 B (50.2%)

$514.4 B (+17%) (55%)

$553 B (+8%) (56%)

Education $54.4 B $57.2 B $59.2 B

HHS $69.1 B $71.9 B $70.4 B

HUD $33.6 B $37.4 B $38.5 B

EPA $7.3 B $7.5 B $7.1 B

Priorities? $164.4 B (18.6%)

$174 B (+5%) (18.4%)

$175.2 B (.6%) (17.7%)

DIS

C. B

RE

AK

DO

WN

DIS

C. B

RE

AK

DO

WN

© Center for Tax and Budget Accountability 2008

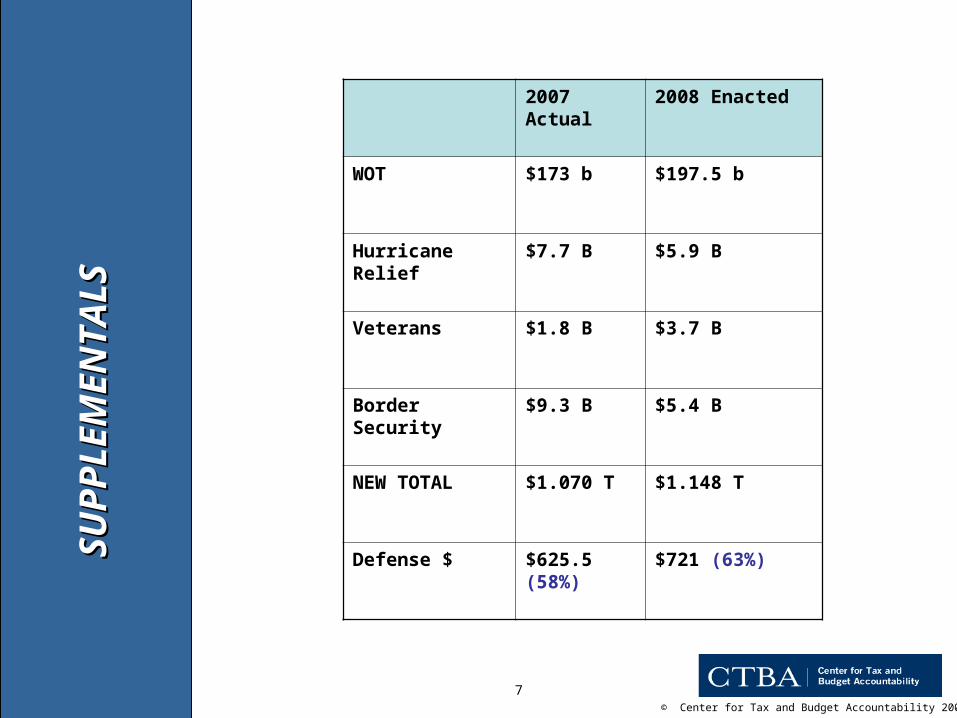

7

2007 Actual

2008 Enacted

WOT $173 b $197.5 b

Hurricane Relief

$7.7 B $5.9 B

Veterans $1.8 B $3.7 B

Border Security

$9.3 B $5.4 B

NEW TOTAL $1.070 T $1.148 T

Defense $ $625.5 (58%)

$721 (63%)SU

PP

LE

ME

NT

AL

SS

UP

PL

EM

EN

TA

LS

© Center for Tax and Budget Accountability 2008

8

BIG ‘N RICH

• In 2007, Illinois ranked fifth nationally with a Gross State Product in excess of $609 billion.

• That would be the 27th largest economy of any nation in the world-greater than Egypt, Saudi Arabia, Colombia, Belgium, Sweden, Greece, Ireland, Portugal, Norway and Nigeria, to name a few.

ILL

INO

IS’

EC

ON

OM

Y

ILL

INO

IS’

EC

ON

OM

Y

IS L

AR

GE

IS L

AR

GE

© Center for Tax and Budget Accountability 2008

9

Illinois GDP Growth Lags

TH

E I

LL

INO

IS E

CO

NO

MY

TH

E I

LL

INO

IS E

CO

NO

MY

71.7%

49.4% 48.1%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

US Midwest States Illinois

But, IL Gross State Product Grew Less than U.S. or Midwest States, 1990-2007

Source: Bureau of Economic Analysis, US Dept. of Commerce

© Center for Tax and Budget Accountability 2008

10

• Between 1990 and 2008, Illinois lost 27% - 249,000 - of its manufacturing industry jobs.

• This loss was worse than both the Midwest (-23.2%) and the Nation (-23.9%).

MA

NU

FA

CT

UR

ING

M

AN

UF

AC

TU

RIN

G

DE

CL

INE

DE

CL

INE

© Center for Tax and Budget Accountability 2008

11

All job growth in Illinois came in the service sector.

For the most part, service sector jobs that pay less than manufacturing

On average, most of these service jobs pay 29% less than the manufacturing jobs they replace

LO

W-E

ND

SE

RV

ICE

LO

W-E

ND

SE

RV

ICE

JOB

S G

RO

WJO

BS

GR

OW

In Fact…

© Center for Tax and Budget Accountability 2008

12

This Transition has been Dramatic

CH

AN

GIN

G

CH

AN

GIN

G

EM

PL

OY

ME

NT

E

MP

LO

YM

EN

T

PA

TT

ER

NS

PA

TT

ER

NS

In 1990, Manufacturing in Illinois employed more workers than any other sector, 20.4%.

By 2007, only 13.1% of the state’s workers were employed in Manufacturing―while low wage service sectors accounted for over 31% of all jobs.

© Center for Tax and Budget Accountability 2008

13

EM

PL

OY

ER

-PR

OV

IDE

D

EM

PL

OY

ER

-PR

OV

IDE

D

BE

NE

FIT

SB

EN

EF

ITS

Employer-provided health insurance benefits have been steadily declining in Illinois since 1980.

By 2006, over 40% of the workforce didn’t have employer provided insurance

Hispanics especially hard hit–over 57% do not have employer-provided insurance

TODAY, 27% of the Illinois population is either on Medicaid or uninsured

© Center for Tax and Budget Accountability 2008

14

• In 1981, 55.6% of the state’s workers were covered by private sector employer-provided pension plans.

• By 2007, only 43.8% of the workforce had private retirement benefits.

PE

NS

ION

ER

OS

ION

PE

NS

ION

ER

OS

ION

© Center for Tax and Budget Accountability 2008

15

• Why the Economic Problems?– NOT TAX BURDEN OR WASTEFUL

SPENDING

• Illinois’ total state AND local tax burden, as a percentage of personal income ranks only 45th in the nation.

• The second lowest tax burden in the Midwest to Missouri (Missouri is all of one-tenth of one percent lower).

• Illinois also ranks only 42nd in spending among the statesIL

LIN

OIS

IS

LO

W T

AX

IL

LIN

OIS

IS

LO

W T

AX

O

VE

RA

LL

OV

ER

AL

L

© Center for Tax and Budget Accountability 2008

16

Education now matters more than ever to economic prosperity:

unemployment rates are highest

for those with the least education. Wages are also tied to education levels.

EX

HIB

IT “

A”

IS E

DU

CA

TIO

NE

XH

IBIT

“A

” IS

ED

UC

AT

ION

© Center for Tax and Budget Accountability 2008

17

Impact of Education on Wages

In real (2006) dollars, between 1980 and 2006, only those with at least a college degree experienced any gain in hourly income, with growth of 14.3%

Real median hourly wages for all other education categories declinedLess than a high school diploma fell by 28.7%Only a high school education declined 8.7%Some college but no degree declined 4.3%You gotta learn to earn!

WA

GE

DIF

FE

RE

NC

ES

WA

GE

DIF

FE

RE

NC

ES

© Center for Tax and Budget Accountability 2008

18

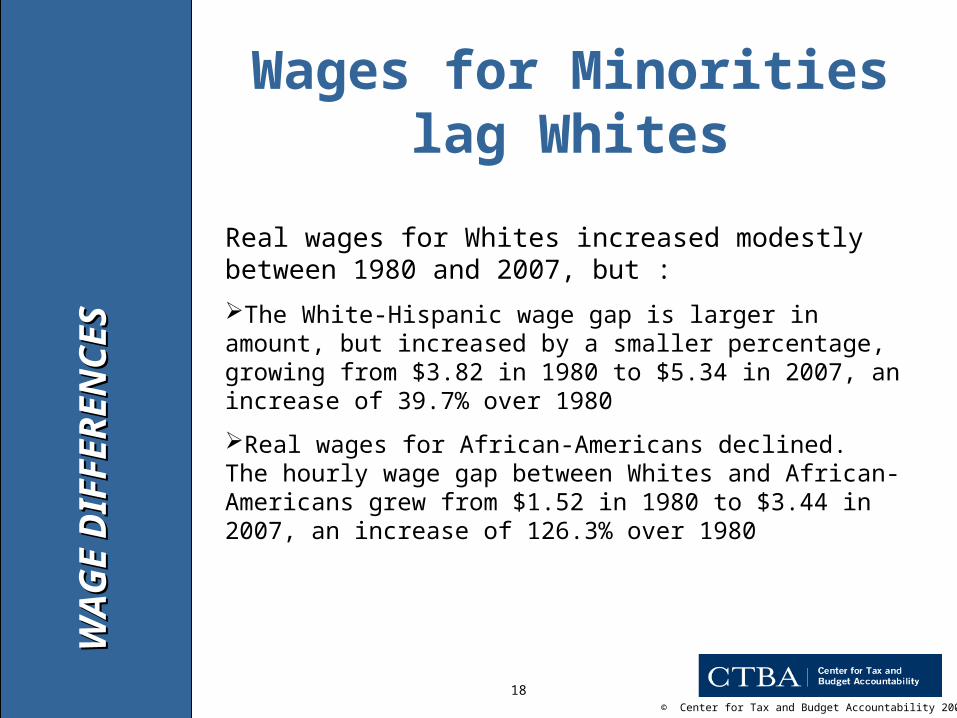

Wages for Minorities lag Whites

Real wages for Whites increased modestly between 1980 and 2007, but :

The White-Hispanic wage gap is larger in amount, but increased by a smaller percentage, growing from $3.82 in 1980 to $5.34 in 2007, an increase of 39.7% over 1980

Real wages for African-Americans declined. The hourly wage gap between Whites and African-Americans grew from $1.52 in 1980 to $3.44 in 2007, an increase of 126.3% over 1980

WA

GE

DIF

FE

RE

NC

ES

WA

GE

DIF

FE

RE

NC

ES

© Center for Tax and Budget Accountability 2008

19

Still Separate. . . . Illinois is the third most

segregated state in K-12 education for blacks

82% of black children attend majority/minority schools

90% of white children attend virtually all white schools

(*Source: 2006 Education Trust study on segregation)

SE

GR

EG

AT

ION

SE

GR

EG

AT

ION

© Center for Tax and Budget Accountability 2008

20

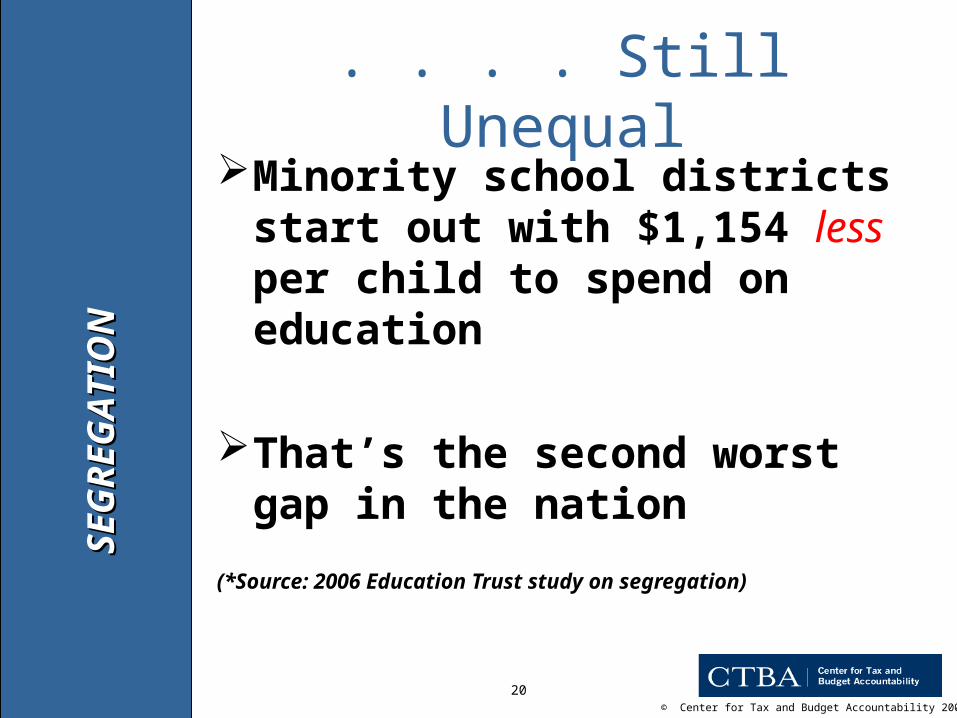

. . . . Still UnequalMinority school districts

start out with $1,154 less per child to spend on education

That’s the second worst gap in the nation

(*Source: 2006 Education Trust study on segregation)

SE

GR

EG

AT

ION

SE

GR

EG

AT

ION

© Center for Tax and Budget Accountability 2008

21

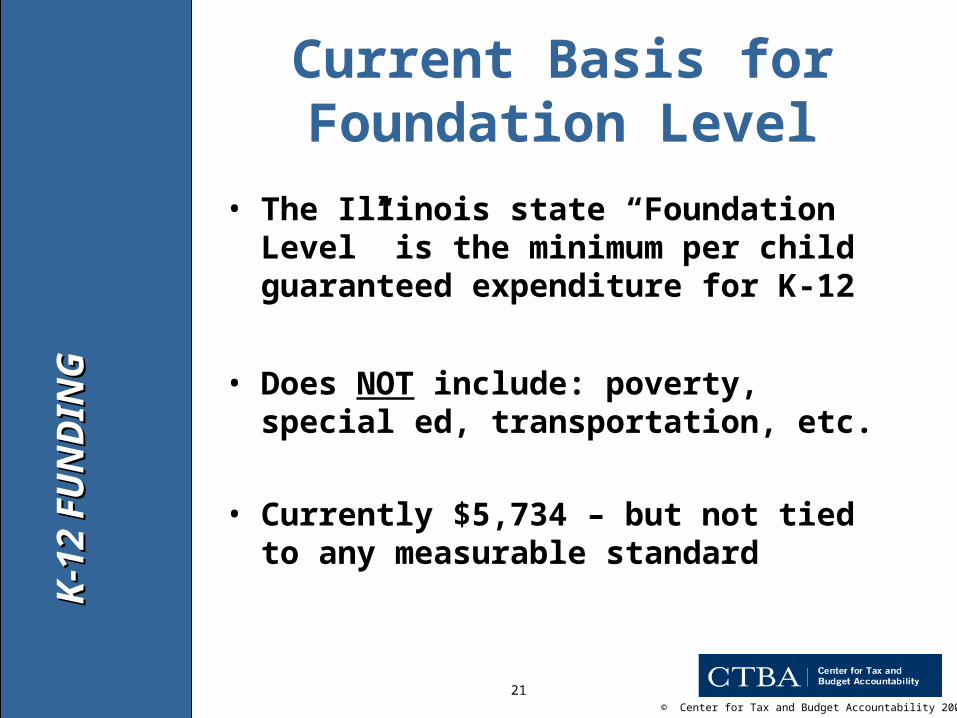

Current Basis for Foundation Level

• The Illinois state “Foundation Level” is the minimum per child guaranteed expenditure for K-12

• Does NOT include: poverty, special ed, transportation, etc.

• Currently $5,734 – but not tied to any measurable standard

K-1

2 F

UN

DIN

GK

-12

FU

ND

ING

© Center for Tax and Budget Accountability 2008

22

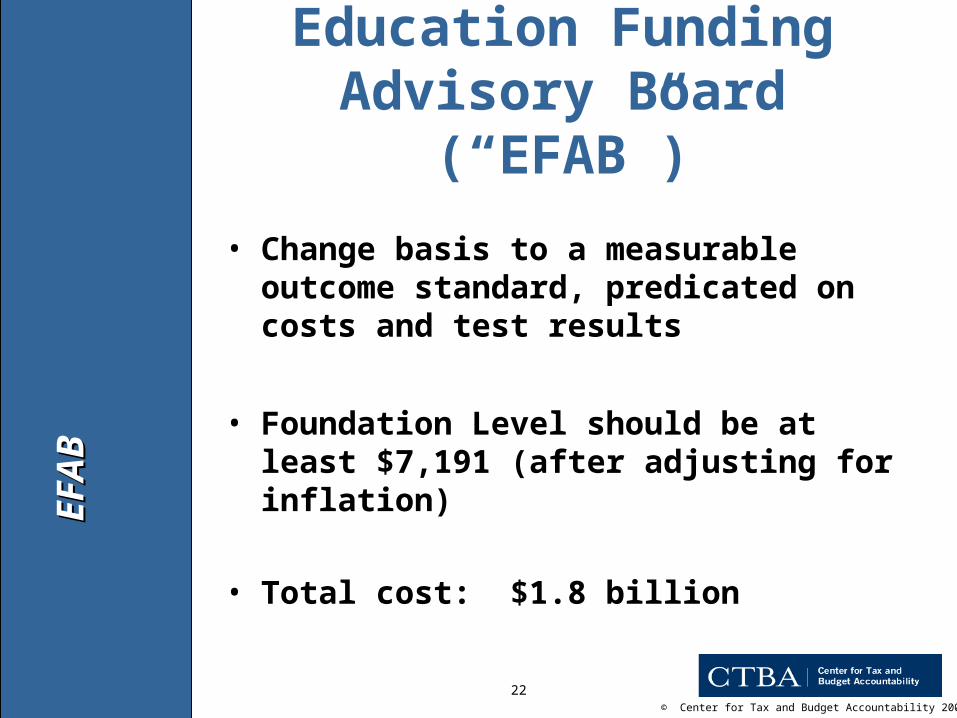

Education Funding Advisory Board

(“EFAB”)

• Change basis to a measurable outcome standard, predicated on costs and test results

• Foundation Level should be at least $7,191 (after adjusting for inflation)

• Total cost: $1.8 billion

EF

AB

EF

AB

© Center for Tax and Budget Accountability 2008

23

• Based upon the ability to pay Foundation Level with property tax revenue, school districts are divided into three groups.

• Flat Grant: districts whose property tax revenue exceeds 175% of the Foundation level of funding. Just over four percent of all Illinois districts, educating about 4.5% of all students, fall into this funding category.

• Alternative: districts whose property tax revenue funds between 93 and 175% of the Foundation level of funding. Fifteen percent of all districts, or 18% of all students, fall into this funding system.

• Foundation: Districts whose property tax revenue is able to fund 93% or less of the Foundation Level. Eighty-one percent of all districts, or 77% of all students, fall into this funding category.

FU

ND

ING

SY

ST

EM

DE

FIN

ITIO

NS

FU

ND

ING

SY

ST

EM

DE

FIN

ITIO

NS

© Center for Tax and Budget Accountability 2008

24

42.12%

2.84%

17.41%

0.83%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

45.00%

1990-2005 2000-2005

Illinois Total Property Tax Revenue Growth Vs. State Median Income Growth

Total Property TaxRevenue Growth

State Median IncomeGrowth

TH

E B

UR

DE

N I

S T

OU

GH

TH

E B

UR

DE

N I

S T

OU

GH

All data inflation adjusted to 2008

Income Data: US Department of Census

Property Tax Data: IL Department of Revenue

© Center for Tax and Budget Accountability 2008

25

83.25%75.58%

45.66%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Property Taxes as a Percentage of District

Revenue

Flat Grant

Alternative Formula

Foundation Formula

Foundation formula districts receive significantly less than the amount received by flat grant and alternative formula districts in property tax revenue, meaning they rely far more heavily on state support. http://www.isbe.net – “2007 IL Report Card”

PR

OP

ER

TY

TA

XE

SP

RO

PE

RT

Y T

AX

ES

© Center for Tax and Budget Accountability 2008

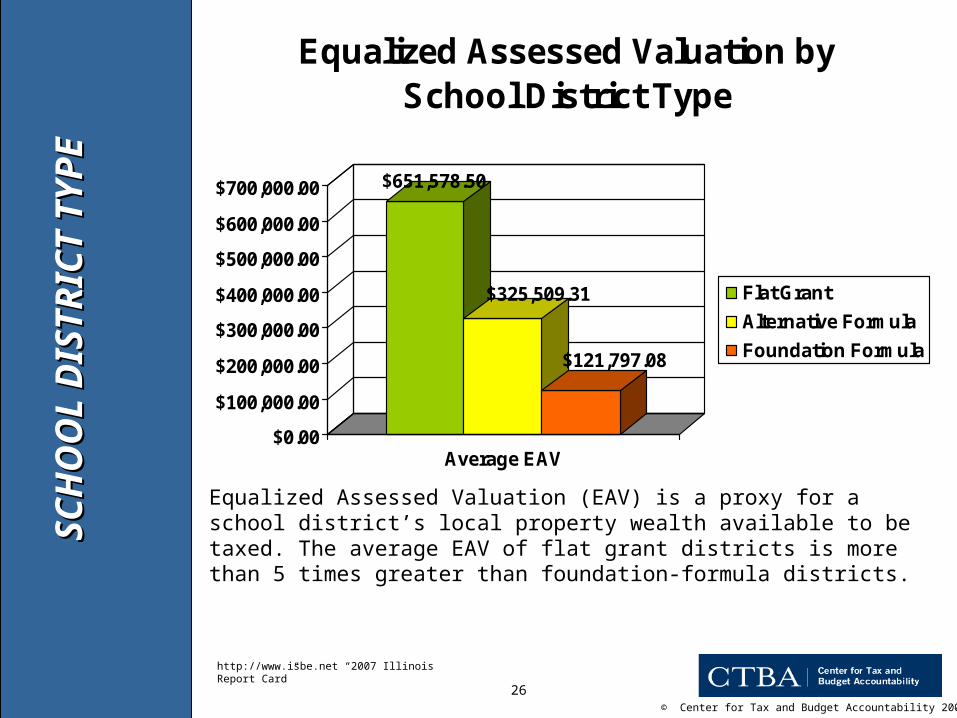

26

$651,578.50

$325,509.31

$121,797.08

$0.00

$100,000.00

$200,000.00

$300,000.00

$400,000.00

$500,000.00

$600,000.00

$700,000.00

Average EAV

Equalized Assessed Valuation by School District Type

Flat Grant

Alternative Formula

Foundation Formula

Equalized Assessed Valuation (EAV) is a proxy for a school district’s local property wealth available to be taxed. The average EAV of flat grant districts is more than 5 times greater than foundation-formula districts.S

CH

OO

L D

IST

RIC

T T

YP

ES

CH

OO

L D

IST

RIC

T T

YP

E

http://www.isbe.net “2007 Illinois Report Card”

© Center for Tax and Budget Accountability 2008

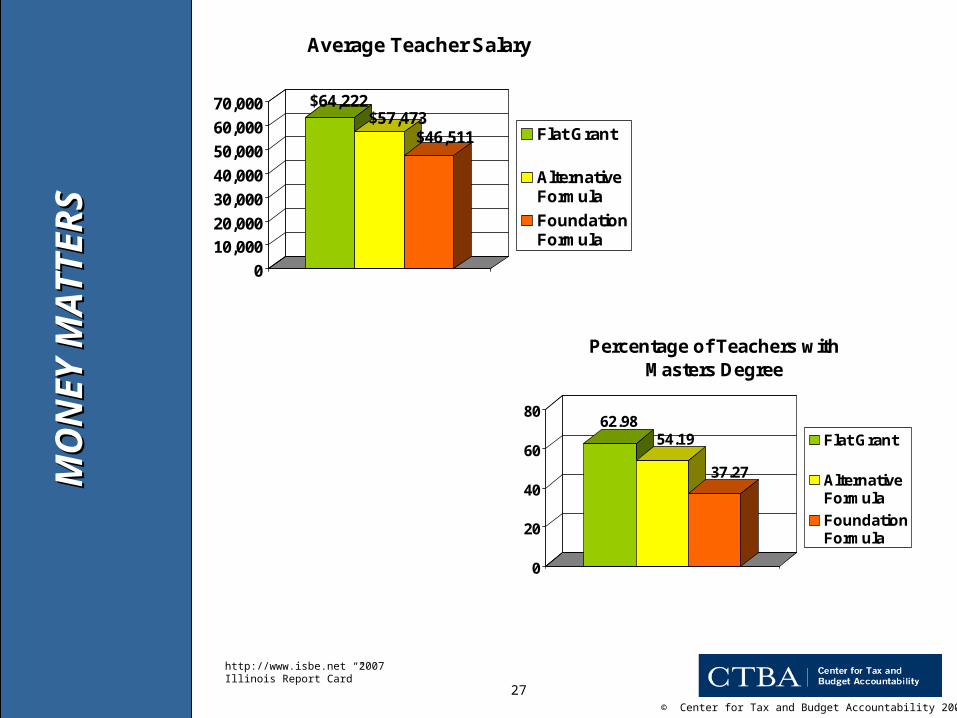

27

$64,222$57,473

$46,511

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

Average Teacher Salary

Flat Grant

AlternativeFormula

FoundationFormula

62.9854.19

37.27

0

20

40

60

80

Percentage of Teachers with Masters Degree

Flat Grant

AlternativeFormula

FoundationFormula

MO

NE

Y M

AT

TE

RS

MO

NE

Y M

AT

TE

RS

http://www.isbe.net “2007 Illinois Report Card”

© Center for Tax and Budget Accountability 2008

28

MO

NE

Y M

AT

TE

RS

MO

NE

Y M

AT

TE

RS

http://www.isbe.net “2006 Illinois Report Card”

90%86%

80%90% 87%

80%

0%10%20%30%40%50%60%70%80%90%

100%

Reading Math

Percentage of students meeting or exceeding ISAT Standards (Grade 8, 2006)

Flat Grant

Alternative Formula

Foundation Formula

© Center for Tax and Budget Accountability 2008

29

163

160

157

163

159

156

164

160

157

150

152

154

156

158

160

162

164

Reading Math Science

PSAE Average Score (2006)

Flat Grant

Alternative Formula

Foundation Formula

MO

NE

Y M

AT

TE

RS

MO

NE

Y M

AT

TE

RS

http://www.isbe.net “2007 Illinois Report Card”

© Center for Tax and Budget Accountability 2008

30

Total and Instructional Spending Differentials

On average, Flat Grant districts spend $4186 more in total per pupil spending than Foundation Formula school districts.

When it comes to instructional expenses, Flat Grant districts spend $2324 more per student on average than do Foundation Formula districts.

MO

NE

Y M

AT

TE

RS

MO

NE

Y M

AT

TE

RS

http://www.isbe.net “2007 Illinois Report Card”

© Center for Tax and Budget Accountability 2008

31

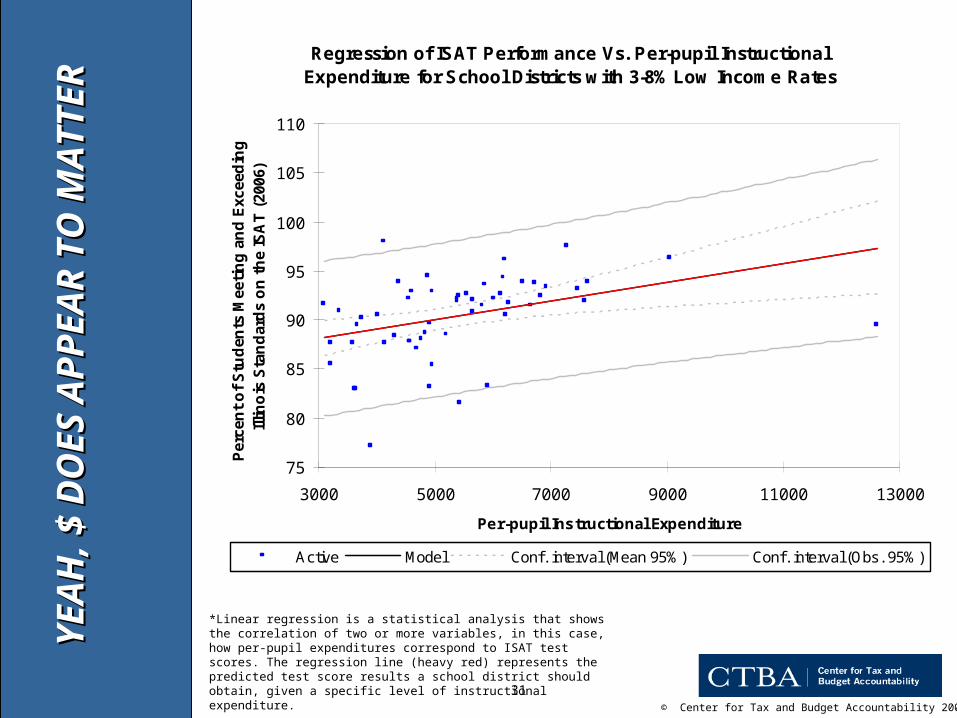

Regression of ISAT Performance Vs. Per-pupil Instructional Expenditure for School Districts with 3-8% Low Income Rates

75

80

85

90

95

100

105

110

3000 5000 7000 9000 11000 13000

Per-pupil Instructional Expenditure

Per

cen

t o

f S

tud

ents

Mee

tin

g a

nd

Exc

eed

ing

Ill

ino

is S

tan

dar

ds

on

th

e IS

AT

(20

06)

Active Model Conf. interval (Mean 95%) Conf. interval (Obs. 95%)

YE

AH

, $ D

OE

S A

PP

EA

R T

O M

AT

TE

RY

EA

H, $

DO

ES

AP

PE

AR

TO

MA

TT

ER

*Linear regression is a statistical analysis that shows the correlation of two or more variables, in this case, how per-pupil expenditures correspond to ISAT test scores. The regression line (heavy red) represents the predicted test score results a school district should obtain, given a specific level of instructional expenditure.

© Center for Tax and Budget Accountability 2008

32

$445,930

$81,422

$0

$100,000

$200,000

$300,000

$400,000

$500,000

Average EAV

Low Income FocusEqualized Assessed Valuation

Lowest Poverty (0-4% LIR)

Highest Poverty (68-100% LIR)

The EAV of school districts with the greatest amount of low income is 5 times less than that of the percentage of the districts with the smallest low income population.

*LIR – means Low Income Rate

http://www.isbe.net “2007 Illinois Report Card”

PO

VE

RT

Y A

ND

SC

HO

OL

SP

OV

ER

TY

AN

D S

CH

OO

LS

© Center for Tax and Budget Accountability 2008

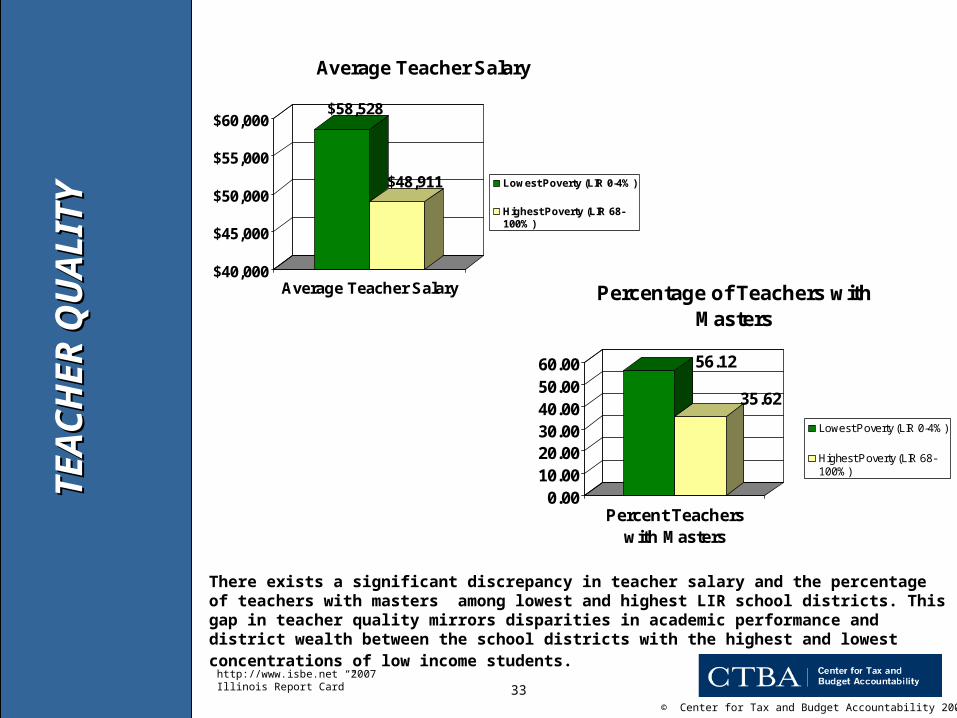

33

56.12

35.62

0.0010.0020.0030.0040.0050.0060.00

Percent Teacherswith Masters

Percentage of Teachers with Masters

Lowest Poverty (LIR 0-4%)

Highest Poverty (LIR 68-100%)

$58,528

$48,911

$40,000

$45,000

$50,000

$55,000

$60,000

Average Teacher Salary

Average Teacher Salary

Lowest Poverty (LIR 0-4%)

Highest Poverty (LIR 68-100%)

There exists a significant discrepancy in teacher salary and the percentage of teachers with masters among lowest and highest LIR school districts. This gap in teacher quality mirrors disparities in academic performance and district wealth between the school districts with the highest and lowest concentrations of low income students.

TE

AC

HE

R Q

UA

LIT

YT

EA

CH

ER

QU

AL

ITY

http://www.isbe.net “2007 Illinois Report Card”

© Center for Tax and Budget Accountability 2008

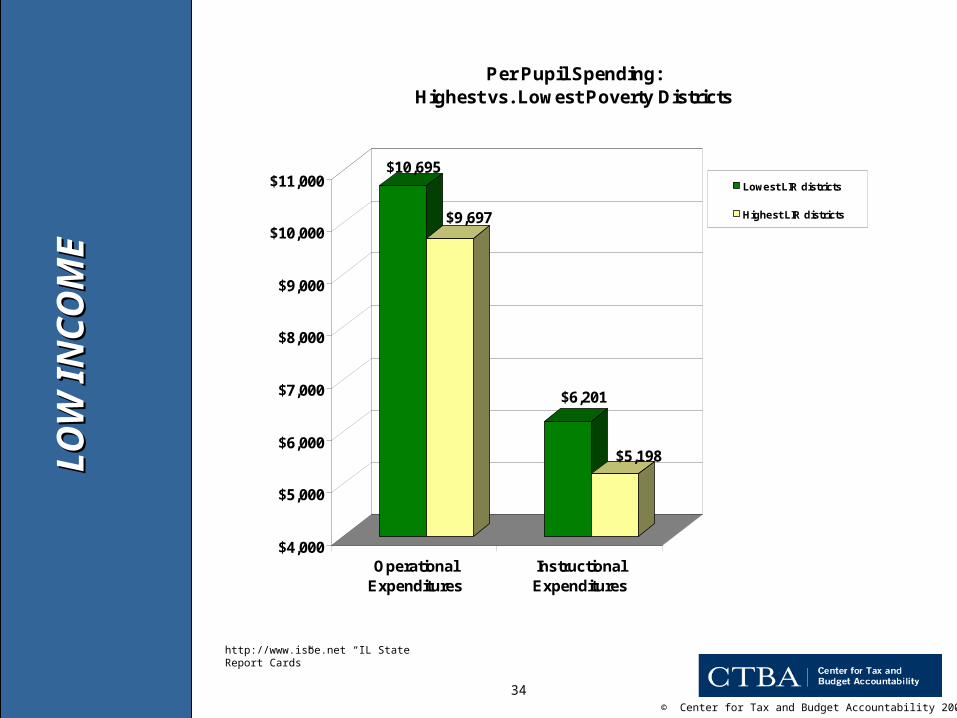

34

$10,695

$9,697

$6,201

$5,198

$4,000

$5,000

$6,000

$7,000

$8,000

$9,000

$10,000

$11,000

OperationalExpenditures

InstructionalExpenditures

Per Pupil Spending: Highest vs. Lowest Poverty Districts

Lowest LIR districts

Highest LIR districts

http://www.isbe.net “IL State Report Cards”

LO

W I

NC

OM

EL

OW

IN

CO

ME

© Center for Tax and Budget Accountability 2008

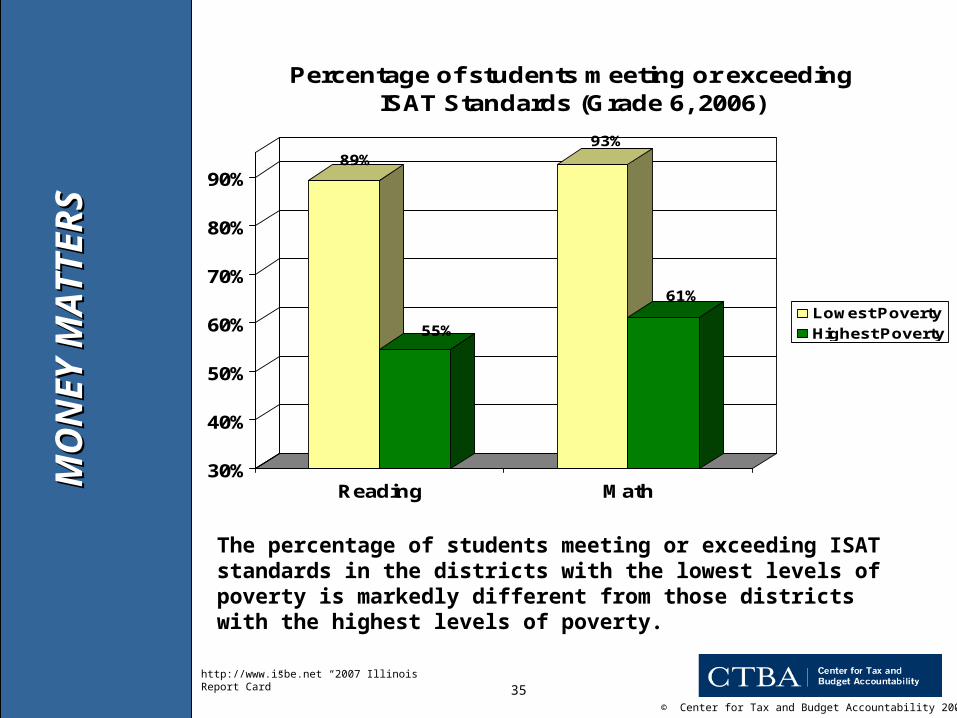

35

The percentage of students meeting or exceeding ISAT standards in the districts with the lowest levels of poverty is markedly different from those districts with the highest levels of poverty.

89%

55%

93%

61%

30%

40%

50%

60%

70%

80%

90%

Reading Math

Percentage of students meeting or exceeding ISAT Standards (Grade 6, 2006)

Lowest Poverty

Highest Poverty

MO

NE

Y M

AT

TE

RS

MO

NE

Y M

AT

TE

RS

http://www.isbe.net “2007 Illinois Report Card”

© Center for Tax and Budget Accountability 2008

36

63.7

26.1

0.0

20.0

40.0

60.0

80.0

% Meet plus exceed

Percentage Meeting plus exceeding PSAE (2006)

Lowest Poverty

Highest Poverty

PO

VE

RT

Y M

AT

TE

RS

PO

VE

RT

Y M

AT

TE

RS

http://www.isbe.net “2007 Illinois Report Card”

© Center for Tax and Budget Accountability 2008

37

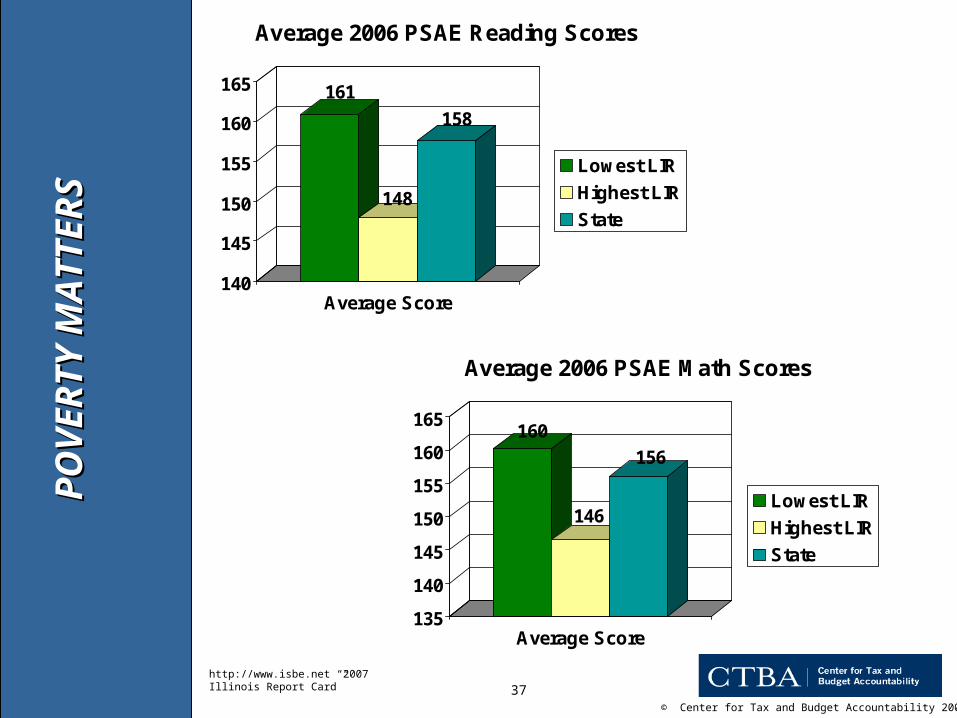

161

148

158

140

145

150

155

160

165

Average Score

Average 2006 PSAE Reading Scores

Lowest LIR

Highest LIR

State

160

146

156

135

140

145

150

155

160

165

Average Score

Average 2006 PSAE Math Scores

Lowest LIR

Highest LIR

State

PO

VE

RT

Y M

AT

TE

RS

PO

VE

RT

Y M

AT

TE

RS

http://www.isbe.net “2007 Illinois Report Card”

© Center for Tax and Budget Accountability 2008

38

Lowest LIR Districts Making AYP

4%

96%

No

Yes

Highest LIR Districts Making AYP

71%

29%

No

Yes

The disparity between those districts meeting AYP corresponds directly to a school district’s LIR.

LO

W I

NC

OM

E M

AT

TE

RS

LO

W I

NC

OM

E M

AT

TE

RS

http://www.isbe.net “2007 Illinois Report Card”

© Center for Tax and Budget Accountability 2008

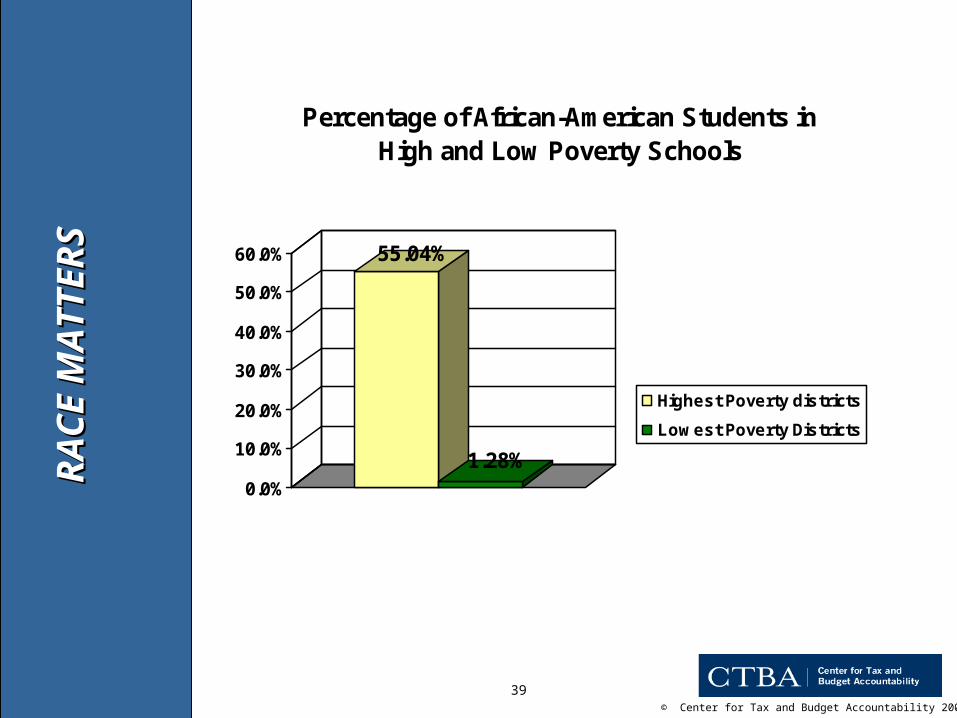

39

55.04%

1.28%0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

Percentage of African-American Students in High and Low Poverty Schools

Highest Poverty districts

Lowest Poverty Districts

RA

CE

MA

TT

ER

SR

AC

E M

AT

TE

RS

© Center for Tax and Budget Accountability 2008

40

21.60%

92.83%

66.45%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

90.00%

100.00%

%White of Total White Pop %Black of Total Black Pop %Hispanic of Total Hispanic Pop

Percentage of Students in Districts with Poverty Rate of 30% or Greater

RA

CE

MA

TT

ER

SR

AC

E M

AT

TE

RS

© Center for Tax and Budget Accountability 2008

41

Racial Breakdown of Flat Grant Districts

Hispanic8%

African American5%

Caucasian76%

Other2%

Asian/Pacific Islander

9%

Native American0%

RA

CE

MA

TT

ER

SR

AC

E M

AT

TE

RS

© Center for Tax and Budget Accountability 2008

42

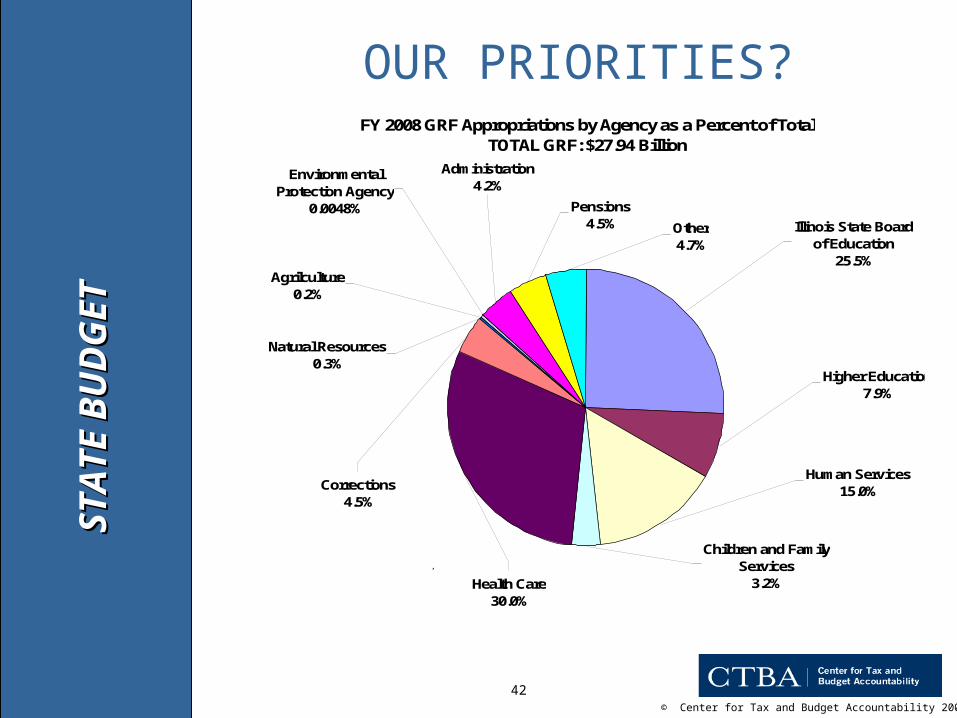

FY 2008 GRF Appropriations by Agency as a Percent of Total TOTAL GRF: $27.94 Billion

Agrilculture0.2%

Administration4.2%

Natural Resources0.3%

Corrections4.5%

Environmental Protection Agency

0.0048%

Health Care30.0%

Children and Family Services

3.2%

Human Services15.0%

Higher Education7.9%

Pensions4.5% Other

4.7%Illinois State Board

of Education25.5%

Source: Illinois Commission on Government Forecasting and Accountability, FY 2008 Budget Summary

-ISBE and Higher Ed does not include pension contributions-Pension contributions include FY 2008 GRF appropriated-Health Care includes Public Health and Health Care and Family Services-Administration includes all boards, commissions, agencies, authorities, districts, councils, OMB, Revenue, CMS, Inspector General and all legislative, constitutional and judicial offices

ST

AT

E B

UD

GE

TS

TA

TE

BU

DG

ET

OUR PRIORITIES?

© Center for Tax and Budget Accountability 2008

43

WHAT ABOUT REVENUE GROWTH

$$

$$

NE

W $

$$ ?

NE

W $

$$ ?

© Center for Tax and Budget Accountability 2008

44

N

OT

SO

MU

CH

NO

T S

O M

UC

HIllinois State Major Tax Revenues Have Not Kept Up With

Inflation by Over $7 Billion Since 2000

-$179.30

-$1,274.10

-$1,873.03-$1,953.03

-$1,369.20

-$576.40

$17

-$2,500

-$2,000

-$1,500

-$1,000

-$500

$0

$500

2001 2002 2003 2004 2005 2006 2007$

in M

illio

ns

Includes: Personal and Corporate Income, State Sales, and Public Utility Taxes. Source, Illinois Commission on Government Forecasting and Accountability. Inflation based on Bureau of Labor Statistics, CPI.

THERE ISN’T ANY

© Center for Tax and Budget Accountability 2008

45

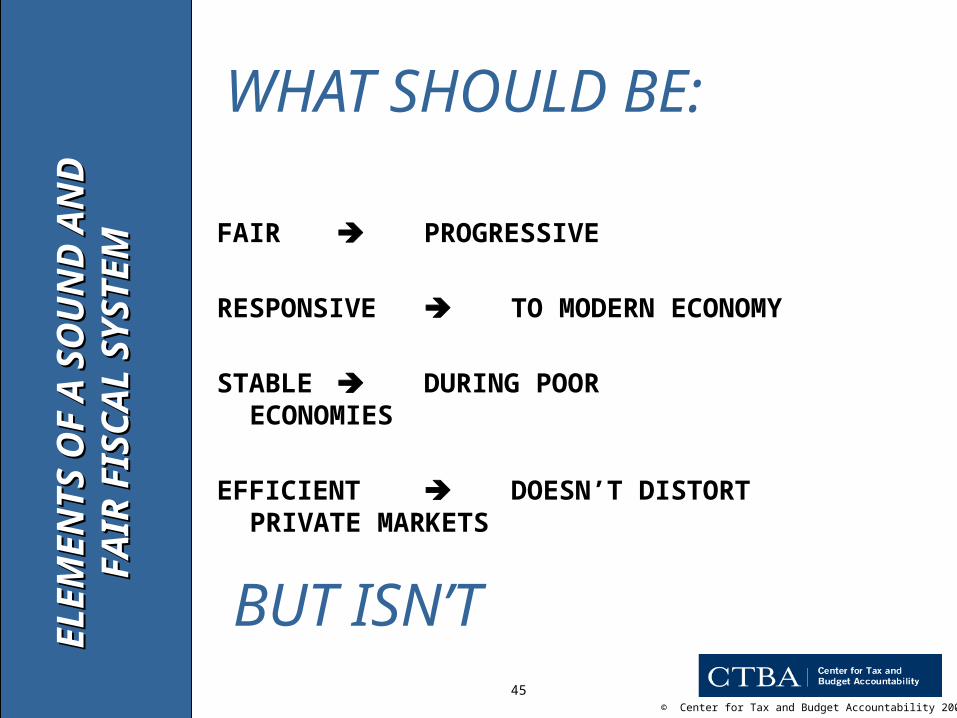

FAIR PROGRESSIVE

RESPONSIVE TO MODERN ECONOMY

STABLE DURING POORECONOMIES

EFFICIENT DOESN’T DISTORTPRIVATE MARKETS

EL

EM

EN

TS

OF

A S

OU

ND

AN

D

EL

EM

EN

TS

OF

A S

OU

ND

AN

D

FA

IR F

ISC

AL

SY

ST

EM

FA

IR F

ISC

AL

SY

ST

EM

WHAT SHOULD BE:

BUT ISN’T

© Center for Tax and Budget Accountability 2008

46

*Adjusts solely for historic rates of inflation and population growth, and assumes normal economic growth.

ST

RU

CT

UR

AL

DE

FIC

ITS

TR

UC

TU

RA

L D

EF

ICIT

The Illinois Structural Deficit (How Revenue Growth Will Not Keep Pace With The Cost of Current Services)

20062007

20082009

20102011

20122013

20142015

20162017

20182019

20202021

20222023

20242025

2026

Revenue

Expenditures

$24 Billion

$49 Billion

$44 Billion

$39 Billion

$34 Billion

$29 Billion

© Center for Tax and Budget Accountability 2008

47

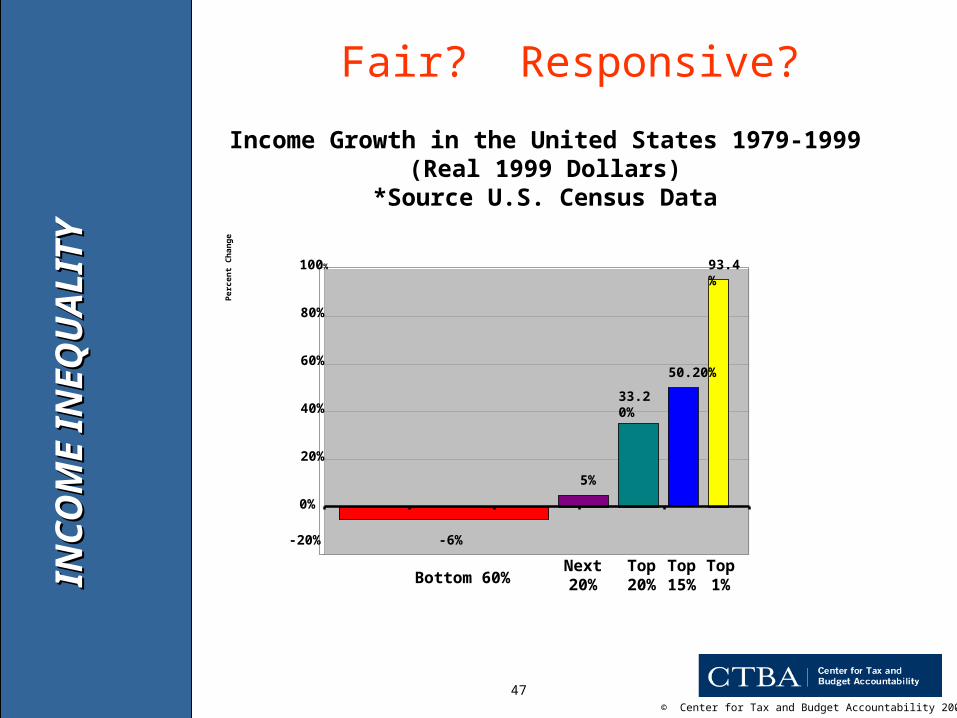

-6%

5%

33.20%

50.20%

93.4%

-20%

0%

20%

40%

60%

80%

100%

Bottom 60% Next20%

Top20%

Top15%

Top1%

Income Growth in the United States 1979-1999(Real 1999 Dollars)

*Source U.S. Census DataP

erce

nt

Ch

ang

e

INC

OM

E I

NE

QU

AL

ITY

INC

OM

E I

NE

QU

AL

ITY

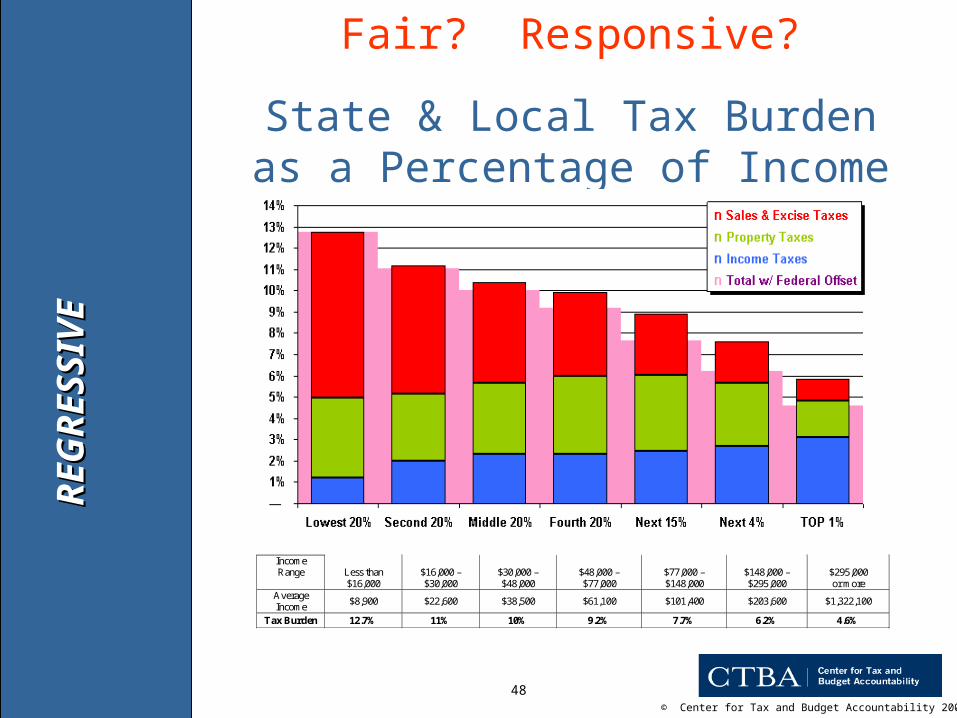

Fair? Responsive?

© Center for Tax and Budget Accountability 2008

48

State & Local Tax Burden as a Percentage of Income

Income Range

Less than $16,000

$16,000 – $30,000

$30,000 – $48,000

$48,000 – $77,000

$77,000 – $148,000

$148,000 – $295,000

$295,000 or more

Average Income

$8,900 $22,600 $38,500 $61,100 $101,400 $203,600 $1,322,100

Tax Burden 12.7% 11% 10% 9.2% 7.7% 6.2% 4.6%

RE

GR

ES

SIV

ER

EG

RE

SS

IVE

Fair? Responsive?

© Center for Tax and Budget Accountability 2008

49

INCOME TAX INCREASE

3% 5%

3% 2% =5%

2/3 = 67%

*Note, corporate rate goes up from 4.8% to 8%, but―overall corporate tax burden goes down!

SB

750

SB

750

© Center for Tax and Budget Accountability 2008

50

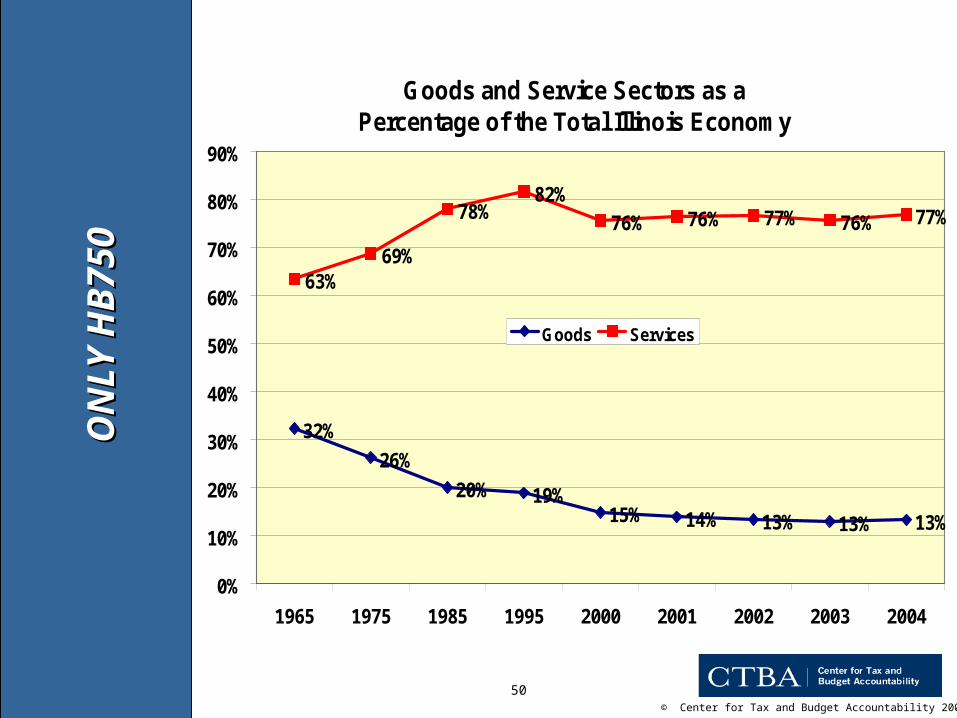

Goods and Service Sectors as a Percentage of the Total Illinois Economy

32%

26%

20% 19%15% 14% 13% 13% 13%

63%69%

78%82%

76% 76% 77% 76% 77%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

1965 1975 1985 1995 2000 2001 2002 2003 2004

Goods Services

ON

LY

HB

750

ON

LY

HB

750

© Center for Tax and Budget Accountability 2008

51

For More Information:

Center for Tax and Budget Accountabilitywww.ctbaonline.org

Ralph M. MartireExecutive Director(312) [email protected]

Chrissy A. ManciniDirector of Budget and Policy Analysis(312) [email protected]

Yerik KaslowResearch Associate(312) [email protected]

Fu

rth

er I

nfo

rmat

ion

Fu

rth

er I

nfo

rmat

ion

Related Documents