NEW ISSUE Non-rated Book Entry Only This Final Official Statement is dated November 10, 2005. In the opinion of Ice Miller, Indianapolis, Indiana (“Bond Counsel”), under existing laws, regulations, judicial decisions and rulings, interest on the Bonds, as defined herein, is excludable from gross income under Section 103 of the Internal Revenue Code of 1986, as amended (the “Code”) for federal income tax purposes. Such exclusion is conditioned on continuing compliance with the Tax Covenants (hereinafter defined). In the opinion of Ice Miller, Indianapolis, Indiana, under existing laws, regulations, judicial decisions and rulings, interest on the Bonds is exempt from income taxation in the State of Indiana. See “TAX MATTERS,” herein. The Bonds are not bank qualified. $ 7,295,000 HAMILTON COUNTY (INDIANA) REDEVELOPMENT DISTRICT TAX INCREMENT REVENUE BONDS OF 2005 (Village Park Economic Development Area) Dated: Date of Delivery Due: February 1st and August 1st as shown on the inside cover page The Hamilton County (Indiana) Redevelopment Commission (the “Commission”), acting in the name of Hamilton County, Indiana (the “County”), is issuing $7,295,000 of Redevelopment District Tax increment Revenue Bonds of 2005 (the “Bonds”) to finance the construction of road improvements (the “Project”), and to pay costs of issuance. The Project will serve and benefit the Village Park Economic Development Area (the “Area”). The Bonds will be issued pursuant to the Final Bond Resolution (the “Bond Resolution”) adopted by the Commission on October 14, 2005, and subject to the provisions of the Act (herein defined). There are currently bonds payable out of real property tax revenues collected in the Area, designated Redevelopment District Tax Increment Refunding Revenue Bonds of 1993, dated June 1, 1993 (the “1993 Bonds”), originally issued in the amount of $4,140,000 now outstanding in the amount of $225,000 and maturing on February 1, 2006. The 1993 Bonds will be defeased at the time of delivery of the Bonds with funds on hand. Debt Service on the Bonds will be payable from Tax Increment, as more fully described herein. Additional security will be provided through the funding of a debt service reserve from funds on hand. THE BONDS DO NOT CONSTITUTE A CORPORATE OBLIGATION OF THE COUNTY, BUT CONSTITUTE A LIMITED OBLIGATION OF THE HAMILTON COUNTY REDEVELOPMENT DISTRICT (THE “DISTRICT”), AS A SPECIAL TAXING DISTRICT, IN THE NAME OF THE COUNTY, PAYABLE SOLELY FROM THE TRUST ESTATE. THE DISTRICT IS NOT OBLIGATED TO PAY THE DEBT SERVICE ON THE BONDS FROM ANY SOURCE OTHER THAN THE TRUST ESTATE. NEITHER THE FULL FAITH AND CREDIT NOR THE TAXING POWER OF THE DISTRICT OR THE COUNTY IS PLEDGED TO THE PAYMENT OF THE PRINCIPAL OF OR THE INTEREST ON THE BONDS. The Bonds will be issued only as fully registered bonds and, when issued, will be registered in the name of Cede & Co., as nominee for the Depository Trust Company, New York, New York (“DTC”). Purchases of beneficial interests in the Bonds will be made in book-entry-only form, in the denomination of $5,000 or any integral multiple thereof. Purchasers of beneficial interests in the Bonds (the “Beneficial Owners”) will not receive physical delivery of certificates representing their interests in the Bonds. Interest on the Bonds is payable semiannually February 1st and August 1st of each year commencing August 1, 2006, by check mailed one business day prior to each interest payment date to the registered owners or, if payment is made to a depository, by wire transfer of immediately available funds on the interest payment date. Principal is payable semiannually on February 1st and August 1st in the amounts shown on the inside cover page hereof at the principal corporate trust office of J.P. Morgan Trust Company, National Association, in the City of Dallas, Texas (the “Trustee”, “Registrar” or “Paying Agent”) or by wire transfer to depositories. Interest on, together with principal of, the Bonds will be paid directly to DTC by the Paying Agent so long as DTC or its nominee is the registered owner of the Bonds. The final disbursements of such payments to the Beneficial Owners of the Bonds will be the responsibility of DTC Participants and the Indirect Participants. See “BOOK-ENTRY-ONLY SYSTEM”. The Bonds are subject to optional redemption beginning August 1, 2015, as more fully described herein. The Bonds may be issued as “Term Bonds” at the Underwriter’s (herein defined) discretion and any bonds issued as Term Bonds will be subject to mandatory sinking fund redemption as a more fully described. This cover page contains certain information for guide reference only. It is not a summary of this issue. Investors must read the entire Official Statement to obtain information essential in the making of an informed investment decision.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

NEW ISSUE Non-ratedBook Entry Only

This Final Official Statement is dated November 10, 2005.

In the opinion of Ice Miller, Indianapolis, Indiana (“Bond Counsel”), under existing laws, regulations, judicial decisions and rulings, interest on the Bonds, as defined herein, is excludable from gross income under Section 103 of the Internal Revenue Code of 1986, as amended (the “Code”) for federal income tax purposes. Such exclusion is conditioned on continuing compliance with the Tax Covenants (hereinafter defined). In the opinion of Ice Miller, Indianapolis, Indiana, under existing laws, regulations, judicial decisions and rulings, interest on the Bonds is exempt from income taxation in the State of Indiana. See “TAX MATTERS,” herein. The Bonds are not bank qualified.

$ 7,295,000 HAMILTON COUNTY (INDIANA) REDEVELOPMENT DISTRICT

TAX INCREMENT REVENUE BONDS OF 2005(Village Park Economic Development Area)

Dated: Date of Delivery Due: February 1st and August 1st as shown on the inside cover page

The Hamilton County (Indiana) Redevelopment Commission (the “Commission”), acting in the name of Hamilton County, Indiana (the “County”), is issuing $7,295,000 of Redevelopment District Tax increment Revenue Bonds of 2005 (the “Bonds”) to finance the construction of road improvements (the “Project”), and to pay costs of issuance. The Project will serve and benefit the Village Park Economic Development Area (the “Area”). The Bonds will be issued pursuant to the Final Bond Resolution (the “Bond Resolution”) adopted by the Commission on October 14, 2005, and subject to the provisions of the Act (herein defined). There are currently bonds payable out of real property tax revenues collected in the Area, designated Redevelopment District Tax Increment Refunding Revenue Bonds of 1993, dated June 1, 1993 (the “1993 Bonds”), originally issued in the amount of $4,140,000 now outstanding in the amount of $225,000 and maturing on February 1, 2006. The 1993 Bonds will be defeased at the time of delivery of the Bonds with funds on hand.

Debt Service on the Bonds will be payable from Tax Increment, as more fully described herein. Additional security will be provided through the funding of a debt service reserve from funds on hand.

THE BONDS DO NOT CONSTITUTE A CORPORATE OBLIGATION OF THE COUNTY, BUT CONSTITUTE A LIMITED OBLIGATION OF THE HAMILTON COUNTY REDEVELOPMENT DISTRICT (THE “DISTRICT”), AS A SPECIAL TAXING DISTRICT, IN THE NAME OF THE COUNTY, PAYABLE SOLELY FROM THE TRUST ESTATE. THE DISTRICT IS NOT OBLIGATED TO PAY THE DEBT SERVICE ON THE BONDS FROM ANY SOURCE OTHER THAN THE TRUST ESTATE. NEITHER THE FULL FAITH AND CREDIT NOR THE TAXING POWER OF THE DISTRICT OR THE COUNTY IS PLEDGED TO THE PAYMENT OF THE PRINCIPAL OF OR THE INTEREST ON THE BONDS.

The Bonds will be issued only as fully registered bonds and, when issued, will be registered in the name of Cede & Co., as nominee for the Depository Trust Company, New York, New York (“DTC”). Purchases of beneficial interests in the Bonds will be made in book-entry-only form, in the denomination of $5,000 or any integral multiple thereof. Purchasers of beneficial interests in the Bonds (the “Beneficial Owners”) will not receive physical delivery of certificates representing their interests in the Bonds. Interest on the Bonds is payable semiannually February 1st and August 1st of each year commencing August 1, 2006, by check mailed one business day prior to each interest payment date to the registered owners or, if payment is made to a depository, by wire transfer of immediately available funds on the interest payment date. Principal is payable semiannually on February 1st and August 1st in the amounts shown on the inside cover page hereof at the principal corporate trust office of J.P. Morgan Trust Company, National Association, in the City of Dallas, Texas (the “Trustee”, “Registrar” or “Paying Agent”) or by wire transfer to depositories. Interest on, together with principal of, the Bonds will be paid directly to DTC by the Paying Agent so long as DTC or its nominee is the registered owner of the Bonds. The final disbursements of such payments to the Beneficial Owners of the Bonds will be the responsibility of DTC Participants and the Indirect Participants. See “BOOK-ENTRY-ONLY SYSTEM”. The Bonds are subject to optional redemption beginning August 1, 2015, as more fully described herein. The Bonds may be issued as “Term Bonds” at the Underwriter’s (herein defined) discretion and any bonds issued as Term Bonds will be subject to mandatory sinking fund redemption as a more fully described.

This cover page contains certain information for guide reference only. It is not a summary of this issue. Investors must read the entire Official Statement to obtain information essential in the making of an informed investment decision.

Maturity Principal *Interest

Rate Price CUSIP

8/1/2006 40,000$ 3.25% 100.00$ DC92/1/2007 100,000 3.50% 100.00 DD78/1/2007 100,000 3.50% 100.00 DE52/1/2008 105,000 3.75% 100.00 DF28/1/2008 105,000 3.75% 100.00 DG02/1/2009 105,000 4.00% 100.00 DH88/1/2009 110,000 4.00% 100.00 DJ42/1/2010 110,000 4.10% 100.00 DK18/1/2010 115,000 4.10% 100.00 DL92/1/2011 115,000 4.20% 100.00 DM78/1/2011 120,000 4.20% 100.00 DN52/1/2012 120,000 4.30% 100.00 DP08/1/2012 125,000 4.30% 100.00 DQ82/1/2013 125,000 4.40% 100.00 DR68/1/2013 130,000 4.40% 100.00 DS42/1/2014 130,000 4.50% 100.00 DT28/1/2014 135,000 4.50% 100.00 DU9

$880,000 of Term Bonds @ 4.60% due August 1, 2017, Price: $98.661, CUSIP DV7$4,525,000 of Term Bonds @ 5.00% due February 1, 2025, Price: $100.00, CUSIP DW5

MATURITY SCHEDULE(Base CUSIP* 40722K)

Term Bonds

*Copyright 2004, American Banker Association. CUSIP data herein provided by Standard & Poor’s, CUSIP Service Bureau, a division of The McGraw-Hall Companies, Inc.

The Bonds are offered when, as and if issued and received by the Underwriter (hereinafter defined) and subject to approval of legality by Ice Miller, Indianapolis, Indiana, Bond Counsel. Certain legal matters will be passed on by Mr. Michael A. Howard, Attorney at Law, Howard & Associates, Noblesville, Indiana as counsel to the County. The Bonds are expected to be available for delivery in Indianapolis, Indiana, on or about November 30, 2005.

IN CONNECTION WITH THIS OFFERING, THE UNDERWRITER MAY OVER-ALLOT OR EFFECT TRANSACTIONS WHICH STABILIZE OR MAINTAIN THE MARKET PRICE OF THE BONDS OFFERED HEREBY AT A LEVEL ABOVE THAT WHICH MIGHT OTHERWISE PREVAIL IN THE OPEN MARKET, AND SUCH STABILIZING, IF COMMENCED, MAY BE DISCONTINUED AT ANY TIME.

No dealer, broker, salesperson or other person has been authorized by the Commission to give any information or to make any representations other than those contained in this Official Statement, and if given or made, such other information or representations must not be relied upon as having been authorized by the Commission. This Official Statement does not constitute an offer to sell or the solicitation of an offer to buy nor shall there be any sale of securities, described herein by any person in any jurisdiction in which it is unlawful for such person to make such an offer, solicitation or sale. The information set forth herein has been obtained from the Commission, and other sources which are believed to be reliable, but it is not guaranteed as to accuracy or completeness. The information and expressions of opinion herein are subject to change without notice and neither the delivery of the Official Statement nor any sale made hereunder shall under any circumstances create any implication that there has been no change in the affairs of the County since the date thereof. However, upon delivery of the securities, the Commission will provide a certificate stating that there have been no material changes in the information contained in the Final Official Statement since its delivery.

THE UNDERWRITER HAS PROVIDED THE FOLLOWING SENTENCE FOR INCLUSION IN THIS OFFICIAL STATEMENT. THE UNDERWRITER HAS REVIEWED THE INFORMATION IN THIS OFFICIAL STATEMENT IN ACCORDANCE WITH, AND AS PART OF, THEIR RESPECTIVE RESPONSIBILITIES TO INVESTORS UNDER THE FEDERAL SECURITIES LAWS AS APPLIED TO THE FACTS AND CIRCUMSTANCE OF THIS TRANSACTION, BUT THE UNDERWRITER DOES NOT GUARANTEE THE ACCURACY OR COMPLETENESS OF SUCH INFORMATION.

THE BONDS HAVE NOT BEEN REGISTERED WITH THE SECURITIES AND EXCHANGE COMMISSION UNDER THE SECURITIES ACT OF 1933, AS AMENDED. IN MAKING AN INVESTMENT DECISION, INVESTORS MUST RELY ON THEIR OWN EXAMINATION OF THE COUNTY AND THE TERMS OF THE OFFERING, INCLUDING THE MERIT AND RISK INVOLVED. THE BONDS HAVE NOT BEEN RECOMMENDED BY ANY FEDERAL OR STATE SECURITIES COMMISSION OR REGULATORY AUTHORITY. FURTHERMORE, THE FOREGOING AUTHORITIES HAVE NOT CONFIRMED THE ACCURACY OR DETERMINED THE ADEQUACY OF THIS DOCUMENT. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

Pursuant to continuing disclosure requirements promulgated by the Securities and Exchange Commission in Securities and Exchange Commission Rule 15c2-12, as amended, the County will enter into a Continuing Disclosure Undertaking Agreement. For a description of the Continuing Disclosure Undertaking Agreement, see “CONTINUING DISCLOSURE”.

[REMAINDER OF PAGE INTENTIONALLY LEFT BLANK]

[THIS PAGE INTENTIONALLY LEFT BLANK]

TABLE OF CONTENTS

PROJECT PERSONNEL

Introduction to the Official Statement ............................................................................................................... 1-3 Securities Being Offered Authorization................................................................................................................................................ 3 Sources and Uses of Funds ........................................................................................................................... 3 Schedule of Amortization of $7,295,000 of Redevelopment District, Tax Increment Revenue Bonds of 2005................................................................................................... 4 Project Description ....................................................................................................................................... 5 The Economic Development Area (“Area”)................................................................................................. 5 Security and Sources of Payment ................................................................................................................. 5-6 Investment of Funds ..................................................................................................................................... 6 Risks to Bondholders.................................................................................................................................... 6-7 Additional Bonds.......................................................................................................................................... 7-8 Redemption Provisions................................................................................................................................. 8-9 Interest Payable............................................................................................................................................. 9 Book-Entry-Only System .................................................................................................................................. 10-11 Procedures for Property Assessment, Tax Levy and Collection........................................................................ 12-13 Original Issue Discount ..................................................................................................................................... 13-14 Continuing Disclosure ....................................................................................................................................... 14-15 Underwriting...................................................................................................................................................... 15 Litigation ........................................................................................................................................................... 15 Certain Legal Matters ........................................................................................................................................ 15 Verification........................................................................................................................................................ 15 Legal Opinions and Enforceability of Remedies ............................................................................................... 16

Appendices:

A General Information B Accounting Report C Bond Resolution D Legal Opinion and Tax Matters

PROJECT PERSONNEL

Names and positions of the County officials and professionals who have taken part in the planning of the proposed bond issue are:

Hamilton County Redevelopment Commission

Gary Meunier, President William G. Crandall, Vice President Art Levine, Secretary Stephen K. Andrews Charlotte Swain

Hamilton County Commissioners

Christine Altman Steven C. Dillinger Steven A. Holt

Hamilton County Council

Brad Beaver James J. Belden Meredith Carter John Hiatt Judy Levine Rick McKinney Steve Schwartz

Auditor

Robin M. Mills

Bond Counsel

Ice Miller One American Square Box 82001 Indianapolis, IN 46204

County Attorney

Mr. Michael Howard, Attorney at Law Howard & Associates 694 Logan Street Noblesville, Indiana 46060

Underwriter

City Securities Corporation 30 South Meridian Street Suite 600 Indianapolis, Indiana 46204

Financial Advisor

O.W. Krohn & Associates, LLP 231 E. Main Street Westfield, Indiana 46074

Fiscal Consultant

Michael A. Reuter

1

FINAL OFFICIAL STATEMENT

$7,295,000

HAMILTON COUNTY (INDIANA) REDEVELOPMENT DISTRICT

TAX INCREMENT REVENUE BONDS OF 2005

INTRODUCTION TO THE OFFICIAL STATEMENT

This Official Statement sets forth certain information concerning the issuance of $7,295,000 of Hamilton County Redevelopment District Tax Increment Revenue Bonds of 2005 (the “Bonds”) by the Hamilton County Redevelopment Commission (the “Commission”) on behalf of Hamilton County, Indiana (the “County”).

SECURITY AND SOURCES OF PAYMENT

The Bonds will be issued as provided in the Final Bond Resolution of the Commission adopted on October 14, 2005 (the “Bond Resolution”). Debt Service on the Bonds will be payable solely from Tax Increment (as defined below) collected in the Village Park Economic Development Area (the “Area”) and any cash or securities held in the funds and accounts established under the Bond Resolution and investment earnings theron (the “Trust Estate”). Additional security will be provided through the funding of a debt service reserve from funds on hand.

The Bonds do not constitute a corporate obligation of the County, but constitute a limited obligation of the Hamilton County Redevelopment District (the “District”), as a special taxing district, in the name of the County, payable solely from the Trust Estate. The District is not obligated to pay the debt service on the Bonds from any source other than the Trust Estate. Neither the full faith and credit nor the taxing power of the District or the County is pledged to the payment of the principal of or the interest on the Bonds. Additional security will be provided through the funding of a debt service reserve from funds on hand.

PURPOSE

The Bonds are being issued for the purpose of financing the construction of road improvements (the “Project”), and to pay costs of issuance. The Project will serve and benefit the Area .

REDEMPTION PROVISIONS

The Bonds are subject to optional redemption beginning August 1, 2015, as more fully described herein. The Bonds may be issued as Term Bonds and subject to mandatory sinking fund redemption as more fully described herein.

DENOMINATIONS

The Bonds are being issued in the denomination of $5,000 or integral multiples thereof.

REGISTRATION AND EXCHANGE FEATURES

Each Bond shall be transferable or exchangeable only upon the books of the Commission, kept for that purpose at the office of the Registrar, J.P. Morgan Trust Company, National Association, located in Indianapolis, Indiana, by registered owner in person, or by its attorney duly authorized in writing, upon surrender of such Bonds together with written instrument of transfer or exchange satisfactory to the Registrar. A further description of the registration and exchange features of the Bonds can be found in Section 3 of the Bond Resolution.

2

PROVISIONS FOR PAYMENT

The principal on the Bonds shall be payable at the principal corporate trust office of the Registrar and Paying Agent, J.P. Morgan Trust Company, National Association, located in Dallas, Texas, or by wire transfer to the Depository Trust Company (“DTC”) or any successor depository. All payments of interest on the Bonds shall be paid by check, mailed one business day prior to the interest payment date to the registered owners as the names appear as of the fifteenth day preceding the interest payment date and at the addresses as the appear on the registration books kept by the Registrar or at such other address as is provided to the Registrar or at such other address as is provided to the Registrar or by wire transfer to DTC or any successor depository. If payment of principal or interest is made to DTC or any successor depository, payment shall be made by wire transfer on the payment date in same-day funds. If the payment date occurs on a date when financial institutions are not open for business, the wire transfer shall be made on the next succeeding business day. The Registrar shall be instructed to wire transfer payments by 1:00 pm (New York City time). Payments on the Bonds shall be made in lawful money of the United States of America, which, on the date of such payment, shall be legal tender.

So long as DTC or its nominee is the registered owner of the Bonds, principal and interest on the Bonds will be paid directly to DTC by the Paying Agent. (The financial disbursement of such payments to the beneficial owners of the Bonds will be responsibility of the DTC participants and Indirect Participants, as defined and more fully described herein).

TAX MATTERS

In the opinion of Ice Miller, Bond Counsel, interest on the Bonds is excludable from gross income for federal income tax purposes. Such exclusion is conditioned on continuing compliance with the Tax Covenants, hereinafter defined. In the opinion of Ice Miller, interest on the Bonds is exempt from income taxation in the State of Indiana. See Appendix D. The Bonds are not bank qualified.

AUTHORIZATION AND DELIVERY OF THE BONDS

The Bonds are to be issued under the authority of Indiana law, including, without limitation, IC 36-7-14 and IC 36-7-25, as in effect on the issue date of the Bonds (collectively, the “Act”), and pursuant to the Bond Resolution.

The Bonds are anticipated to be available for delivery in Indianapolis, Indiana on or about November 30, 2005.

THE 1993 BONDS

The defeasance of the 1993 Bonds will be accomplished by creating an irrevocable escrow and trust account (“Trust Account”) pursuant to an Escrow Agreement between the Commission and J.P. Morgan Trust Company, National Association, Indianapolis, Indiana, as escrow trustee (the “Escrow Agreement”) and depositing therein cash currently held in the 1993 Bond Principal and Interest Account. The 1993 Bonds will be payable from the Trust Account on February 1, 2006.

MISCELLANEOUS

The information contained in this Official Statement has been compiled from records and other materials provided by County officials and other sources deemed to be reliable, and while not guaranteed as to completeness or accuracy, it is believed to be correct as of this date. However, the Official Statement speaks only as of its date, and the information contained herein is subject to change.

The references, excerpts, and summaries of valid documents referred to herein do not purport to be complete statements of the provisions of such documents, and reference is directed to all such documents for full and complete statements of all matters of fact relating to the Bonds, the security for the payment of the Bonds and the rights and obligations of the owners thereof. Additional information may be requested from the Auditor, Hamilton County, One Hamilton County Square, Suite L21, Noblesville, Indiana 46060, phone (317) 776-8402.

3

MISCELLANEOUS (CONTINUED)

Any statements made in this Official Statement involving matters of opinion or of estimates, whether or not so expressly stated, are set forth as such and not as representations of fact, and no representation is made that any of the estimates will be realized. Neither this Official Statement nor any statement which may have been made orally or in writing is to be construed as a contract with the owners of the Bonds.

The County will, upon request of any bondholder, provide current financial statements for review by the bondholder. The financial statements of the County will be available at reasonable times for inspection by any bondholder or its authorized agent as provided in the Bond Resolution.

SECURITIES BEING OFFERED

AUTHORIZATION

The Bonds are being issued under the authority of Indiana law, including without limitation, the Act and all laws amendatory thereof and supplemental thereto as in effect on the issue date of the Bonds and pursuant to the Bond Resolution. (See Appendix C)

The County created a five member Commission to undertake redevelopment and economic development efforts in the County in accordance with the Act. On August 15, 1989, the Commission adopted a Declaratory Resolution, as confirmed by a Confirmatory Resolution on September 26, 1989 to establish the Area for purposes of capturing all incremental real property tax revenues. The Project will serve and benefit the Area.

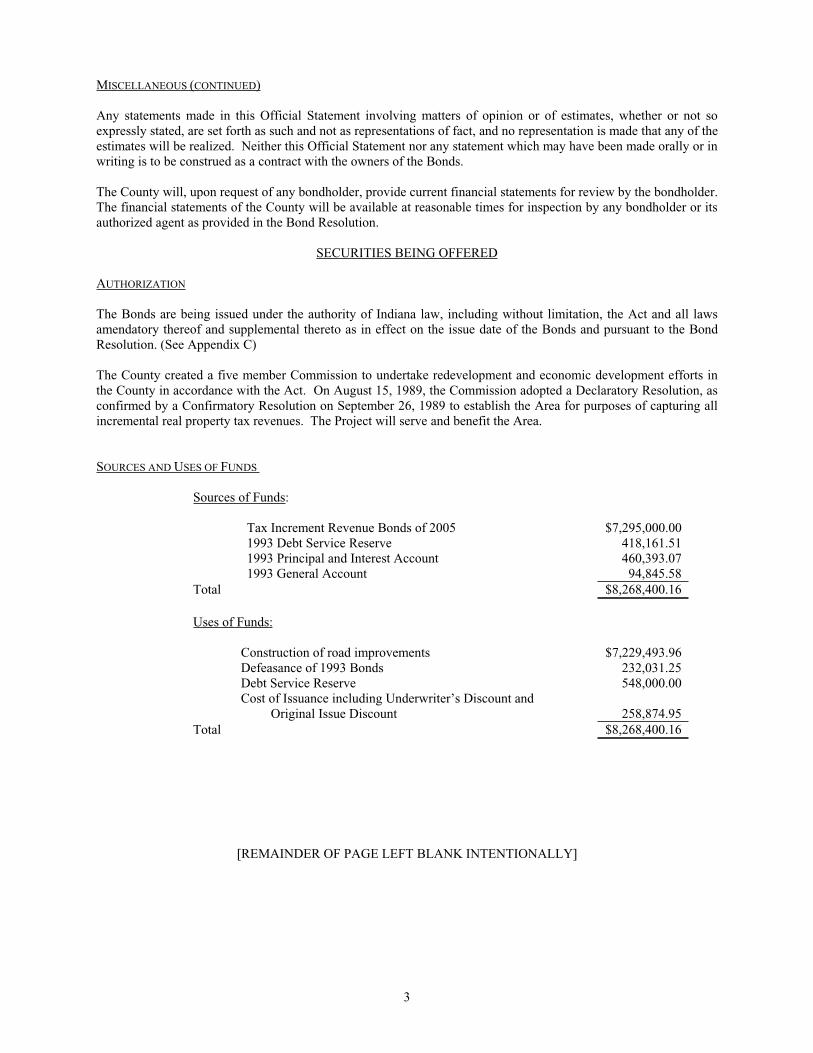

SOURCES AND USES OF FUNDS

Sources of Funds:

Tax Increment Revenue Bonds of 2005 1993 Debt Service Reserve 1993 Principal and Interest Account 1993 General Account

$7,295,000.00 418,161.51460,393.0794,845.58

Total $8,268,400.16

Uses of Funds:

Construction of road improvements Defeasance of 1993 Bonds Debt Service Reserve Cost of Issuance including Underwriter’s Discount and Original Issue Discount

$7,229,493.96 232,031.25548,000.00

258,874.95Total $8,268,400.16

[REMAINDER OF PAGE LEFT BLANK INTENTIONALLY]

4

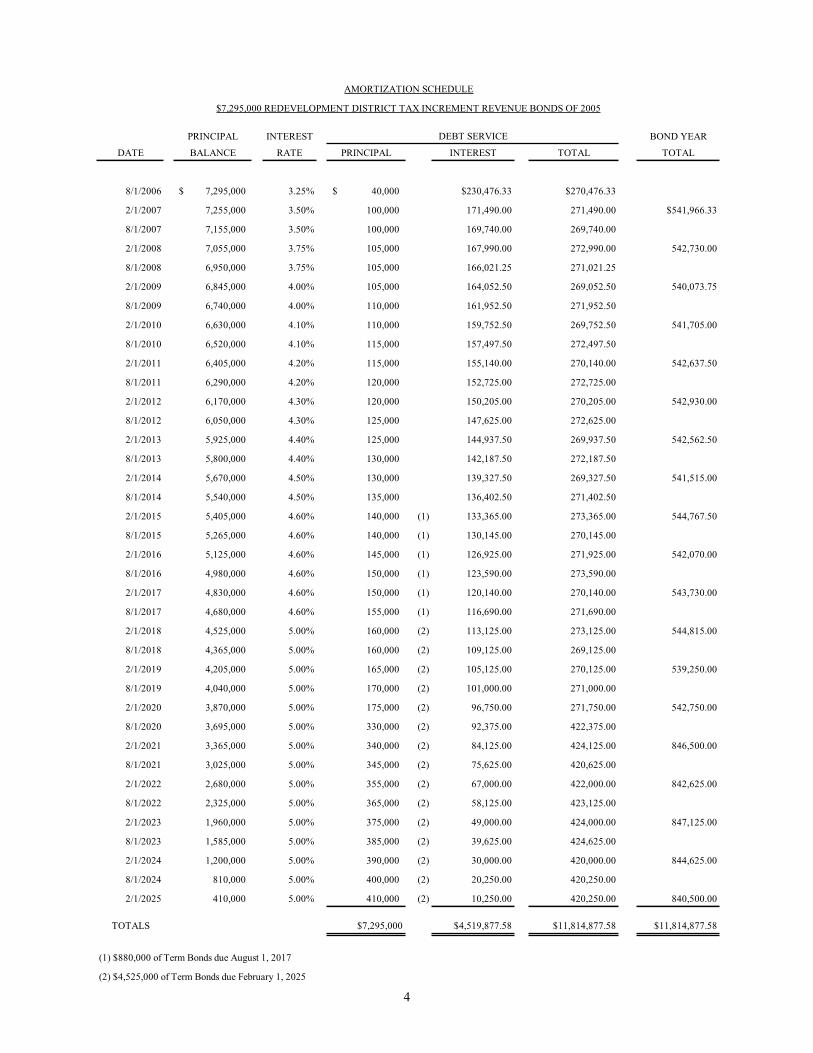

PRINCIPAL INTEREST BOND YEAR

DATE BALANCE RATE PRINCIPAL INTEREST TOTAL TOTAL

8/1/2006 7,295,000$ 3.25% 40,000$ $230,476.33 $270,476.33

2/1/2007 7,255,000 3.50% 100,000 171,490.00 271,490.00 $541,966.33

8/1/2007 7,155,000 3.50% 100,000 169,740.00 269,740.00

2/1/2008 7,055,000 3.75% 105,000 167,990.00 272,990.00 542,730.00

8/1/2008 6,950,000 3.75% 105,000 166,021.25 271,021.25

2/1/2009 6,845,000 4.00% 105,000 164,052.50 269,052.50 540,073.75

8/1/2009 6,740,000 4.00% 110,000 161,952.50 271,952.50

2/1/2010 6,630,000 4.10% 110,000 159,752.50 269,752.50 541,705.00

8/1/2010 6,520,000 4.10% 115,000 157,497.50 272,497.50

2/1/2011 6,405,000 4.20% 115,000 155,140.00 270,140.00 542,637.50

8/1/2011 6,290,000 4.20% 120,000 152,725.00 272,725.00

2/1/2012 6,170,000 4.30% 120,000 150,205.00 270,205.00 542,930.00

8/1/2012 6,050,000 4.30% 125,000 147,625.00 272,625.00

2/1/2013 5,925,000 4.40% 125,000 144,937.50 269,937.50 542,562.50

8/1/2013 5,800,000 4.40% 130,000 142,187.50 272,187.50

2/1/2014 5,670,000 4.50% 130,000 139,327.50 269,327.50 541,515.00

8/1/2014 5,540,000 4.50% 135,000 136,402.50 271,402.50

2/1/2015 5,405,000 4.60% 140,000 (1) 133,365.00 273,365.00 544,767.50

8/1/2015 5,265,000 4.60% 140,000 (1) 130,145.00 270,145.00

2/1/2016 5,125,000 4.60% 145,000 (1) 126,925.00 271,925.00 542,070.00

8/1/2016 4,980,000 4.60% 150,000 (1) 123,590.00 273,590.00

2/1/2017 4,830,000 4.60% 150,000 (1) 120,140.00 270,140.00 543,730.00

8/1/2017 4,680,000 4.60% 155,000 (1) 116,690.00 271,690.00

2/1/2018 4,525,000 5.00% 160,000 (2) 113,125.00 273,125.00 544,815.00

8/1/2018 4,365,000 5.00% 160,000 (2) 109,125.00 269,125.00

2/1/2019 4,205,000 5.00% 165,000 (2) 105,125.00 270,125.00 539,250.00

8/1/2019 4,040,000 5.00% 170,000 (2) 101,000.00 271,000.00

2/1/2020 3,870,000 5.00% 175,000 (2) 96,750.00 271,750.00 542,750.00

8/1/2020 3,695,000 5.00% 330,000 (2) 92,375.00 422,375.00

2/1/2021 3,365,000 5.00% 340,000 (2) 84,125.00 424,125.00 846,500.00

8/1/2021 3,025,000 5.00% 345,000 (2) 75,625.00 420,625.00

2/1/2022 2,680,000 5.00% 355,000 (2) 67,000.00 422,000.00 842,625.00

8/1/2022 2,325,000 5.00% 365,000 (2) 58,125.00 423,125.00

2/1/2023 1,960,000 5.00% 375,000 (2) 49,000.00 424,000.00 847,125.00

8/1/2023 1,585,000 5.00% 385,000 (2) 39,625.00 424,625.00

2/1/2024 1,200,000 5.00% 390,000 (2) 30,000.00 420,000.00 844,625.00

8/1/2024 810,000 5.00% 400,000 (2) 20,250.00 420,250.00

2/1/2025 410,000 5.00% 410,000 (2) 10,250.00 420,250.00 840,500.00

TOTALS $7,295,000 $4,519,877.58 $11,814,877.58 $11,814,877.58

(1) $880,000 of Term Bonds due August 1, 2017

(2) $4,525,000 of Term Bonds due February 1, 2025

DEBT SERVICE

AMORTIZATION SCHEDULE

$7,295,000 REDEVELOPMENT DISTRICT TAX INCREMENT REVENUE BONDS OF 2005

PROJECT DESCRIPTION

The proposed Project includes roadway improvements, engineering costs and related right of way acquisition for streets serving and benefiting the Area. Planned roadway improvements for Greyhound Pass, Western Way and 151st Street include reconstruction, lane additions or widening and traffic signals. The Project also includes construction of a new four lane access road on the east side of the Area connecting Greyhound Pass to 151st Street. Bond proceeds will also be used to pay costs of issuance.

THE ECONOMIC DEVELOPMENT AREA

The Commission established the Area and allocation area (coterminous with the Area) by adopting a Declaratory Resolution on August 15, 1989 and a Confirmatory Resolution on September 26, 1989. The Area was subsequently annexed by the Town of Westfield (the “Town”) and is comprised of approximately 126 acres within the Town located north of 146th Street, south of 151st Street and east of Meridian Street (US 31). The Area is currently occupied by a variety of retail businesses anchored by a strip mall owned and leased by Simon Property Group d/b/a Village Developers. Tenants and owner occupied retail establishments in the Area include but are not limited to the following: Walmart, Bed Bath and Beyond, Marsh Supermarkets, Ashley Furniture, Kohls Department Store, Menards and various other restaurants and retail businesses. The Town has consented to the issuance of the Bonds.

SECURITY AND SOURCES OF PAYMENT

The Bonds do not constitute a corporate obligation of the County. The Bonds shall constitute an indebtedness of the Commission payable in accordance with the terms of the Bond Resolution and secured by the pledge of the funds and accounts defined therein, including the Tax Increment, the debt service reserve and any interest earnings (collectively, the “Trust Estate”). (Please refer to the Bond Resolution shown in Appendix C, and also to the section entitled “Risks to Bondholders” contained in this Official Statement).

The District is not obligated to pay the debt service on the Bonds from any source other than the sources described above. Neither the full faith and credit nor the taxing power of the District or the County is pledged to the payment of the principal of or the interest on the Bonds.

FROM TAX INCREMENT:

Tax Increment consists of the tax proceeds attributable to 50% of real property assessed value within the Area, as of the assessment date in excess of the base assessed value, as defined in IC 36-7-14-39(b)(1) (referred to throughout this Official Statement as the “Tax Increment”). Tax Increment is not currently reduced by the additional credit (the “Additional Credit”) provided for in IC 36-7-14-39.5. The base assessed value means the net assessed value of all the property in the Area as finally determined for the assessment date immediately preceding the effective date of the declaratory resolution pursuant to IC 36-7-14-19 establishing the allocation areas. The base assessment date of the Area is March 1, 1989. Unless there is a draw on the Debt Service Reserve Account (as described below) the remaining 50% of the incremental assessed value of real property will be passed through to the overlapping taxing units. Under IC 6-1.1-21.2, beginning with property taxes payable if 2003, the portion of the State-paid Property Tax Replacement Credit (PTRC) for school general funds was increased from 20% to 60% of the school general fund tax rate. The increase in the Additional Credit (equal to this increased PTRC) would, if paid, result in a reduction in Tax Increment. The new law allows for the potentially lost Tax Increment to be replaced by a State-imposed property tax levy on the District (the “TIF Replacement Levy”). This TIF Replacement Levy is imposed annually by the Department of Local Government Finance (DLGF), unless the County Commissioners eliminate the TIF Replacement Levy. Although is it anticipated that the Replacement Levy will not be eliminated, the schedules in Appendix B have not included this amount in the future projected tax increment revenues.

For additional information on the Tax Increment as it relates to the Bonds, please refer to the “Accounting Report” in Appendix B.

Allocation Fund:

In the Allocation Fund, there will be established by the Trustee a Bond Principal and Interest Account and a Debt Service Reserve Account. The Allocation Fund and the Accounts created thereunder will be held by the Trustee. The Tax Increment distributions will be deposited into the Accounts in the Allocation Fund in the following order of priority.

5

6

SECURITY AND SOURCES OF PAYMENT (CONTINUED)

(1) Bond Principal and Interest Account. Upon each semiannual distribution of Tax increment, the Auditor shall immediately pay to the Trustee for deposit into the Bond Principal and Interest Account, an amount sufficient, when taking into account moneys already on deposit in the Bond Principal and Interest Account, to pay the principal and interest due on the Bonds on the next February 1 or August 1 payment date. No deposit need to be made to the Bond Principal and Interest Account to the extent that the amount contained therein is at least equal to the principal and interest becoming due and payable on all outstanding Bonds on the next February 1 and August 1.

(2) Debt Service Reserve Account. Cash on hand in an amount equal to the Debt Service Reserve Requirement shall be deposited in the Debt Service Reserve Account, upon issuance of the Bonds. The Debt Service Reserve Requirement is $548,000. Moneys deposited and maintained in the Debt Service Reserve Account shall be applied to the payment of the principal of and interest on the Bonds to the extent that amounts in the Bond Principal and Interest Account and the Surplus Fund are insufficient to pay Debt Service when due and payable. If moneys in the Debt Service Reserve Account are transferred to the Bond Principal and Interest Account to pay Debt Service on the Bonds, the depletion of the balance in the Debt Service Reserve Account shall be made up from any moneys in the Surplus Fund and from the next available Tax Increment after the required deposits to the Bond Principal and Interest Account are made. If Tax Increment is required to be deposited in the Debt Service Reserve Account, Tax Increment shall be defined to include all real property tax proceeds from 100% of the assessed value as long as necessary to replenish the Debt Service Reserve Account. Any moneys in the Debt Service Reserve Account in excess of the Debt Service Reserve Requirement shall be deposited in the Bond Principal and Interest Account and applied as described above.

The Redevelopment Capital Fund: The proceeds in the Capital Fund and investment earnings thereon shall be expended to pay the costs of the Project including bond issuance expenses. The Auditor shall administer the moneys in the Capital Fund. After payment of all claims, any funds remaining in the Capital Fund will be transferred to the Bond Principal and Interest Account to pay debt service on the Bonds, or, as directed by the Commission, for the same purpose or type of project for which the Bonds were issued.

The Commission, acting in the name of the County, represents and warrants that there are no prior liens, encumbrances or other restrictions on the Tax Increment except for the 1993 Bonds or on the County’s ability to pledge the Tax Increment for the benefit of the owners of the Bonds. The 1993 Bonds will be defeased upon issuance of the Bonds.

For greater detail of flow of funds and accounts, refer to the Bond Resolution provided in Appendix C.

INVESTMENT OF FUNDS

Pursuant to the Bond Resolution, all funds shall be invested in “Qualified Investments”. Qualified Investments are direct obligations of the United States of America or other investments in which the Commission is permitted to invest under Indiana law.

RISKS TO BONDHOLDERS

Prospective investors in the Bonds should be aware that there are risk factors associated with the Bonds:

The Commission will pay debt service solely from the Trust Estate, including Tax Increment. The estimated Tax Increment available to pay debt service is based on capturing revenues generated by 50% of the incremental real property assessed value in the Area. The estimate of Tax Increment is dependent on certain assumptions as to future events, the occurrence of which cannot be guaranteed. In relying on estimates of Tax Increment contained herein, consideration should be given to risk factors, which could result in reduction in the estimated Tax Increment. Risk factors include, but are not limited to, the following:

(1) (a) General Risks of Tax Increment include: (i) destruction of property in the Area caused by natural disaster; (ii) delinquent taxes or adjustments of or appeals on assessments by property owners in the Area;

7

RISKS TO BONDHOLDERS (CONTINUED)

(iii) a decrease in the assessed value of properties in the Area due to increase in depreciation, obsolescence or other factors by the assessor; (iv) acquisition of property in the Area by a tax-exempt entity; (v) removal or demolition of real property improvements by property owners in the Area; (vi) delayed billing, collection, or distribution of Tax Increment by the County auditor; (vii) a decrease in property tax rates or increase in the State of Indiana’s (“State”) PTRC which would increase the Additional Credit (if paid) applied to Tax Increment; (viii) the General Assembly, the courts, the DLGF or other administrative agencies with jurisdiction in the matter could enact new laws or regulations or interpret, amend, alter, change or modify the laws or regulations governing the calculation, collection, definition or distribution of Tax Increment including laws or regulations relating to reassessment, or a revision in the property tax system; or (ix) a change in any of the civil unit’s funding mechanisms (i.e. no longer funding it with property taxes) could adversely affect Tax Increment. Any such changes could cause the Tax Increment to fall below the levels set forth in the “Comparison of Estimated Tax Increment and Debt Service” schedule shown in Appendix B.

(b) Reduction of Tax Rates or Tax Collection Rates. Any substantial increase in the State or Federal aid or other sources of local revenues which would reduce local required fiscal support for certain public programs or any substantial increase in assessments outside the Area could reduce the rates of taxation by the taxing bodies levying taxes upon property within the Area and have an adverse effect on the amount of Tax Increment received by the Commission. Economic conditions or administrative action could reduce the collection rate achieved by the County within its jurisdiction, including the Area.

(c) Reassessment. The next general reassessment of property in the State is scheduled to be effective for property assessed March 1, 2011, for taxes payable in 2012. Reassessments are scheduled to occur every four years thereafter. The DLGF is required by law to make a one-time adjustment to neutralize the effect of a reassessment on property within tax increment allocation areas, including the Area, so the owners of obligations secured by tax increment revenues will not be adversely affected. Delays in the reassessment process, the inability to neutralize the effect of reassessment, or appeals of reassessments could adversely affect the Tax Increment.

(d) Additional Credit and Tax Rates Assumed in the Tax Increment Estimate. The estimate also assumes that the gross property tax will remain at approximately the same level as the certified 2005 tax rates, for the tax districts within the Area, through the term of the Bonds, and that the Commission will not grant the Additional Credit to taxpayers in the Area. The Commission could decide to grant the Additional Credit in future years. If the Additional Credit is granted, the amount of the PTRC (on which the calculation of the Additional Credit is based) could change if, among other things, property taxes are levied to pay debt service on bonds issued by any taxing units overlapping the Area. The General Assembly could also enact legislation changing the method of calculating, or the size of, the PTRC. Any decease in the tax rate or increase in the PTRC could result in a decrease in the amount of Tax Increment available to pay debt service, if the Additional Credit is granted by the Commission.

(e) Tax Increment Replacement Levy. Beginning with taxes payable in 2003, under IC 6-1.1-21-2, real property receives an increased PTRC on the school general fund from 20% to 60%. IC 6-1.1-21-2, also authorizes a property tax levy in the District to replace the Tax Increment lost from the increase in the PTRC unless the local legislative body acts to eliminate or reduce the TIF Replacement Levy. It is assumed that the County Commissioners will not rescind or reduce this State imposed TIF Replacement Levy. There can be no assurance that the TIF Replacement Levy will continue to be collected.

(2) In the event of delayed billing, collection or distribution by the county auditor of ad valorem property taxes levied on the District, sufficient funds may not be available to the Commission in time to pay debt service when due. This risk is inherent in all property-tax supported obligations and the debt service reserve account could be used to pay debt service under those circumstances.

ADDITIONAL BONDS

Parity Obligations-Tax Increment:

Pursuant to the Bond Resolution, the Commission reserves the right to authorize and issue parity obligations of the Commission (payable from Tax Increment), acting in the name of the County, for the purpose of raising money for

8

ADDITIONAL BONDS (CONTINUED)

future local public improvements or economic development projects in, serving or benefiting the Area or to refund the Bonds or other parity obligations. The authorization and issuance of such parity obligations payable from Tax Increment, shall be subject to the following conditions precedent:

(1) All principal and interest payments with respect to all obligations payable from Tax Increment shall be current to date in accordance with the terms thereof, with no payment in arrears.

(2) For parity obligations payable from Tax Increment without a special benefits tax levy under IC 36-7-14-27 or a pledge of local option income taxes, the Commission and the Trustee shall have received a certificate prepared by an independent, qualified accountant or feasibility consultant ("Certifier") certifying the amount of the Tax Increment estimated to be received in each succeeding year, adjusted as provided below, which estimated amount shall be at least equal to one hundred twenty-five percent (125%) of the lease rental and debt service requirements with respect to the outstanding Bonds and the proposed parity obligations, for each respective year during the term of the outstanding Bonds. In estimating the Tax Increment to be received in any future year, the Certifier shall base the calculation on assessed valuation actually assessed or estimated to be assessed as of the assessment date immediately preceding the issuance of the parity obligations; provided, however, the Certifier shall adjust such assessed values for the current and future reductions of real property tax abatements granted to property owners in the Area. If the parity obligations are secured by a special benefits tax levy under IC 36-7-14-27 or a pledge of local option income taxes, this test does not need to be met.

(3) Payments of any parity obligations or junior obligations shall be payable semiannually in approximately equal installments on February 1 and August 1.

Subordinate Obligations:

Subordinate obligations may be issued in accordance with terms set forth in a resolution of the Commission with semiannual payments on February 1 and August 1.

REDEMPTION PROVISIONS

Optional Redemption:

The Bonds are redeemable at the option of the Commission on any date, on thirty (30) days’ notice, in whole or in part, in such order of maturity as the Commission shall direct and by lot within maturities on any date not earlier than August 1, 2015, at face value, plus accrued interest to the date fixed for redemption.

Notice of Redemption:

Notice of redemption shall be mailed to the registered owners of all Bonds to be redeemed at least 30 days prior to the date fixed for such redemption. If any of the Bonds are so called for redemption, and payment therefore is made to the Paying Agent in accordance with the terms of the bond resolution, then such Bonds shall cease to bear interest from and after the date fixed for redemption in the call. The redemption price of the Bonds is payable at the principal corporate trust operations office of the Paying Agent.

Mandatory Redemption Provisions:

The Bonds maturing August 1, 2017 and February 1, 2025 (collectively, the “Term Bonds”) are subject to mandatory sinking fund redemption prior to maturity at a redemption price equal to the principal amount thereof plus accrued interest to the date of redemption and on the dates and in the amounts in accordance with the following schedules:

REDEMPTION PROVISIONS (CONTINUED):

Date Amount2/1/2015 140,000$ 8/1/2015 140,0002/1/2016 145,0008/1/2016 150,0002/1/2017 150,0008/1/2017 155,000 *

Date Amount2/1/2018 160,000$ 8/1/2018 160,0002/1/2019 165,0008/1/2019 170,0002/1/2020 175,0008/1/2020 330,0002/1/2021 340,0008/1/2021 345,0002/1/2022 355,0008/1/2022 365,0002/1/2023 375,0008/1/2023 385,0002/1/2024 390,0008/1/2024 400,0002/1/2025 410,000 *

* Final Maturity

August 1, 2017 Term Bonds

February 1, 2025 Term Bonds

The Paying Agent shall credit against the mandatory sinking fund requirement for the Term Bonds, and corresponding mandatory redemption obligation, in the order determined by the Commission, any Term Bonds which have previously been redeemed (otherwise than as a result of a previous mandatory redemption requirement) or delivered to the Registrar for cancellation or purchased for cancellation by the Paying Agent and not theretofore applied as a credit against any redemption obligation. Each Term Bond so delivered or canceled shall be credited by the Paying Agent at 100% of the principal amount thereof against the mandatory sinking fund obligation or that series on such mandatory redemption date, and any excess of such amount shall be credited on future redemption obligations, and the principal amount of the Bonds to be redeemed by operation of the mandatory sinking fund requirement shall be accordingly reduced. If fewer than all of the Bonds are called for redemption at one time, the Bonds shall be redeemed in such amounts and order of maturity as the Commission shall direct, and by lot within maturity. Each $5,000 principal amount shall be considered a separate Bond for purposes of optional and mandatory redemption. If some Bonds are to be redeemed by optional redemption and mandatory sinking fund redemption on the same date, the Paying Agent shall select by lot the Bonds for optional redemption before selecting Bonds by lot for the mandatory sinking fund redemption.

INTEREST PAYABLE

Interest shall be calculated on the basis of a 360-day year consisting of twelve 30-day months.

9

10

BOOK-ENTRY-ONLY SYSTEM

The Bonds will be available only in book-entry form in the principal amount of $5,000 or any integral multiple thereof. DTC will act as the initial securities depository for the Bonds. The ownership of one fully registered Bond will be registered in the name of Cede & Co., as nominee for DTC.

SO LONG AS CEDE & CO., AS NOMINEE OF DTC, IS THE REGISTERED OWNER OF THE BONDS, REFERENCES IN THIS OFFICIAL STATEMENT TO THE REGISTERED OWNERS (OR THE OWNERS) WILL MEAN CEDE & CO. AND WILL NOT MEAN THE BENEFICIAL OWNERS.

The Depository Trust Company (“DTC”), New York, New York, will act as securities depository for the Bonds. The Bonds will be issued as fully registered securities registered in the name of Cede & Co. (DTC’s partnership nominee) or such other name as may be requested by an authorized representative of DTC. One fully-registered Bond will be issued for the Bonds, in the aggregate principal amount of such issue, and will be deposited with DTC.

DTC, the world’s largest depository, is a limited-purpose trust company organized under the New York Banking Law, a “banking organization” within the meaning of the New York Banking Law, a member of the Federal Reserve System, a “clearing corporation” within the meaning of the New York Uniform Commercial Code, and a “clearing agency” registered pursuant to the provisions of Section 17A of the Securities Exchange Act of 1934. DTC holds and provides asset servicing for over 2 million issues of U.S. and non-U.S. equity issues, corporate and municipal debt issues, and money market instruments from over 85 countries that DTC’s participants (“Direct Participants”) deposit with DTC. DTC also facilitates the post-trade settlement among Direct Participants of sales and other securities transactions in deposited securities, through electronic computerized book-entry transfers and pledges between Direct Participants’ accounts. This eliminates the need for physical movement of securities certificates. Direct Participants include both U.S. and non-U.S. securities brokers and dealers, banks, trust companies, clearing corporations, and certain other organizations. DTC is a wholly-owned subsidiary of The Depository Trust & Clearing Corporation (“DTCC”). DTCC, in turn, is owned by a number of Direct Participants of DTC and Members of the National Securities Clearing Corporation, Government Securities Clearing Corporation, MBS Clearing Corporation, and Emerging Markets Clearing Corporation, (NSCC, GSCC, MBSCC, and EMCC, also subsidiaries of DTCC), as well as by the New York Stock Exchange, Inc., the American Stock Exchange LLC, and the National Association of Securities Dealers, Inc. Access to the DTC system is also available to others such as both U.S. and non-U.S securities brokers and dealers, banks, trust companies and clearing corporations that clear through or maintain a custodial relationship with a Direct Participant, either directly or indirectly (“Indirect Participants”). DTC has Standard & Poor’s highest rating: AAA. The DTC Rules applicable to its Participants are on file with the Securities and Exchange Commission. More information about DTC can be found at www.dtcc.com.

Purchases of the Bonds under the DTC system must be made by or through Direct Participants, which will receive a credit for the Bonds on DTC’s records. The ownership interest of each actual purchaser of each Bond (“Beneficial Owner”) is in turn to be recorded on the Direct and Indirect Participants’ records. Beneficial Owners will not receive written confirmation from DTC of their purchase, but Beneficial Owners are expected to receive written confirmations providing details of the transaction, as well as periodic statements of their holdings, from the Direct or Indirect Participant through which the Beneficial Owner entered into the transaction. Transfers of ownership interests in the Bonds are to be accomplished by entries made on the books of Direct and Indirect Participants acting on behalf of Beneficial Owners. Beneficial Owners will not receive certificates representing their ownership interests in the Bonds, except in the event that use of the book-entry system for the Bonds is discontinued.

To facilitate subsequent transfers, all of the Bonds deposited by Direct Participants with DTC are registered in the name of DTC’s partnership nominee, Cede & Co. or such other name as may be requested by an authorized representative of DTC. The deposit of the Bonds with DTC and their registration in the name of Cede & Co. or such other DTC nominee do not effect any change in beneficial ownership. DTC has no knowledge of the actual Beneficial Owners of the Bonds; DTC’s records reflect only the identity of the Direct Participants to whose accounts such Bonds are credited, which may or may not be the Beneficial Owners. The Direct and Indirect Participants will remain responsible for keeping account of their holdings on behalf of their customers.

Conveyance of notices and other communications by DTC to Direct Participants, by Direct Participants to Indirect Participants, and by Direct Participants and Indirect Participants to Beneficial Owners will be governed by arrangements among them, subject to any statutory and regulatory requirements as may be in effect from time to time.

11

BOOK-ENTRY-ONLY SYSTEM (CONTINUED)

Redemption notices shall be sent to DTC. If less than all of the Bonds within a maturity are being redeemed, DTC’s practice is to determine by lot the amount of the interest of each Direct Participant in such maturity to be redeemed.

Neither DTC nor Cede & Co. (nor such other DTC nominee) will consent or vote with respect to the Bonds unless authorized by a Direct Participant in accordance with DTC’s procedures. Under its usual procedures, DTC mails an Omnibus Proxy to the Commission as soon as possible after the record date. The Omnibus Proxy assigns Cede & Co.'s consenting or voting rights to those Direct Participants to whose accounts for the Bonds are credited on the record date (identified in a listing attached to the Omnibus Proxy).

Principal of and interest payments on the Bonds will be made to Cede & Co., or such other nominee as may be requested by an authorized representative of DTC. DTC’s practice is to credit Direct Participants accounts, upon DTC’s receipt of funds and corresponding detail information from the Commission or the Paying Agent, on the payable date in accordance with their respective holdings shown on DTC’s records. Payments by Participants to Beneficial Owners will be governed by standing instructions and customary practices, as is the case with securities held for the accounts of customers in bearer form or registered in “street name,” and will be the responsibility of such Participant and not of DTC (nor its nominee), the Paying Agent, any other Fiduciary or the Commission, subject to any statutory or regulatory requirements as may be in effect from time to time. Payments of principal and interest to Cede & Co. (or such other nominee as may be requested by an authorized representative of DTC) is the responsibility of the Commission or the Paying Agent, or any other Fiduciary, disbursement of such payments to Direct Participants shall be the responsibility of DTC, and disbursement of such payments to the Beneficial Owners shall be the responsibility of Direct and Indirect Participants.

DTC may discontinue providing its services as securities depository with respect to the Bonds at any time by giving reasonable notice to the Commission or the Paying Agent. Under such circumstances, in the event that a successor securities depository is not obtained, Bond certificates are required to be printed and delivered.

The Commission may decide to discontinue use of the system of book-entry transfers through DTC (or a successor securities depository). In that event, Bond certificates will be printed and delivered. The information contained in this section concerning DTC and DTC’s book-entry system has been obtained from sources that the Commission believes to be reliable, but neither the Commission nor the Underwriter takes any responsibility for the accuracy thereof.

In the event that the book-entry system for the Bonds is discontinued, the Paying Agent will provide for the registration of the Bonds in the name of the Beneficial Owners thereof. The Commission, the Trustee, the Paying Agent and any other Fiduciary would treat the person in whose name any Bond is registered as the absolute owner of such Bond for the purposes of making and receiving payment of the principal thereof and interest thereon, and for all other purposes, and none of these parties would be bound by any notice or knowledge to the contrary.

REVISION OF BOOK-ENTRY SYSTEM

In the event that either (1) the Commission receives notice from DTC to the effect that DTC is unable or unwilling to discharge its responsibilities as a clearing agency for the Bonds or (2) the Commission elects to discontinue its use of DTC as a clearing agency for the Bonds, then the Commission and the Paying Agent will do or perform or cause to be done or performed all acts or things, not adverse to the rights of the holders of the Bonds, as are necessary or appropriate to discontinue use of DTC as a clearing agency for the Bonds and to transfer the ownership of each of the Bonds to such person or persons, including any other clearing agency, as the holder of such Bonds may direct in accordance with the Bond Resolution. Any expenses of such a discontinuation and transfer, including any expenses of printing new certificates to evidence the Bonds will be paid by the Commission.

12

PROCEDURES FOR PROPERTY ASSESSMENT, TAX LEVY AND COLLECTION

The Bonds are payable solely from the Trust Estate, including the Tax Increment. Real and personal property in the State is assessed each year as of March 1. On or before August 1st each year, the County Auditor must submit to each underlying taxing unit a statement of (i) the estimated assessed value of the taxing unit as of March 1st of that year, and (ii) an estimate of the taxes to be distributed to the taxing unit during the last six months of the current budget year. The estimated value is based on property tax lists delivered to the Auditor by the Township Assessors in Marion County and the County Assessor in all other counties on or before July 1.

The estimated value is used when the governing body of a local taxing unit meets to establish its budget for the next fiscal year (January 1 through December 31), and to set tax rates and levies. By statute, the budget, tax rate and levy must be established no later than the last meeting of the fiscal body in September for Marion County; no later than September 30th for all second class cities; and no later than September 20th for most other units. The budget, tax levy and tax rate are subject to review and revision by the Department of Local Government Finance (DLGF) which, under certain circumstances, may revise, reduce or increase the budget, tax rate, or levy of a taxing unit. The DLGF must complete its actions on or before February 15.

On or before March 1, the County Auditor prepares and delivers the tax duplicate, which is a roll of property taxes payable in that year, to the County Treasurer. Upon receipt of the tax duplicate, the County Treasurer publishes notice of the tax rate in accordance with Indiana statues. The County Treasurer mails tax statements at least 15 days prior to the date that the first installment is due (due dates may be delayed due to a general reassessment or other factors). Property taxes are due and payable to the County Treasurer in two installments on May 10 and November 10, unless a later due date is established by order of the DLGF. If an installment of taxes is not completely paid on or before the due date, a penalty of 10% of the amount delinquent is added to the amount due. On May 10 and November 10 of each year thereafter, an additional penalty equal to 10% of any taxes remaining unpaid is added. The penalties are imposed only on the principal amount of the delinquency. Property becomes subject to tax sale procedures after 15 months of delinquency. The County Auditor distributes property taxes collected to the various taxing units on or about June 30 after the May 10 payment date and December 31 and after the November 10 payment date.

Pursuant to State law, personal property is assessed at its actual historical cost less depreciation. Real property is valued for assessment purposes at its “true tax value” as defined in Real Property Assessment Rule, 50 IAC 2.3, the 2002 Real Property Assessment Manual (“Manual”), as incorporated into 50 IAC 2.3, and the 2002 Real Property Assessment Guidelines, Version A (“Guidelines”), as adopted by the DLGF. The Manual defines “true tax value” as “the market value in use of property for its current use, as reflected by the utility received by the owner or a similar user from that property”. The Manual permits assessing officials in each county to choose any acceptable mass appraisal method to determine true tax value, taking into consideration the ease of administration and the uniformity of the assessments produced by that method. The Guidelines were adopted to provide assessing officials with an acceptable appraisal methodology, although the Manual makes it clear that assessing officials are free to select from any number of appraisal methods, provided that they are capable of producing accurate and uniform values throughout the jurisdiction and across all classes of property. The Manual specifies the standards for accuracy and validation that the DLGF will use to determine the acceptability of any alternate appraisal method.

“Net Assessed Value” or “Taxable Value” represents the “Gross Assessed Value” less certain deductions for, mortgages, veterans, the aged, the blind, economic revitalization, resource recovery systems, rehabilitated residential property, solar energy systems, wind power devices, coal conservation systems, hydroelectric systems, geothermal devices, inventory in enterprise zone and tax-exempt property. The “Net Assessed Value” or “Taxable Value” is the value used to determination of tax rates. If an assessing official changes the assessed value of property, a notice of that change is sent by either the township assessor or the County Property Tax Assessment Board of Appeals to the affected property owner. The property owner may appeal the assessment by filing a Petition for Review of Assessment within 45 days of the date the notice was mailed. While the appeal is pending, the taxpayer may pay taxes based on the current year’s tax rate and the previous or current year’s assessed value.

A State property tax replacement credit (PTRC) is applied to the property tax liability of a taxpayer. The maximum amount of the PTRC is: (a ) sixty percent (60%) of a taxpayer’s real and personal property tax liability for the general fund levy imposed by the school corporation; and (b) approximately twenty percent (20%) of a taxpayer’s real property tax liability for the general fund levies imposed by the taxing units in the taxing district (less sixty percent (60%) of a taxpayer’s property tax liability for the general fund levy imposed by the school corporation); and (c) approximately twenty percent (20%) of taxpayer’s personal property that is not business personal property

13

PROCEDURES FOR PROPERTY ASSESSMENT, TAX LEVY AND COLLECTION (CONTINUED)

tax liability for the general fund levies imposed by the taxing units in the taxing district (less sixty percent 60% of the taxpayer’s property tax liability for the general fund levy imposed by the school corporation). Legislation enacted in 2005 may have the effect of reducing the amount of State PTRC payment paid to the County. A State homestead credit is also applied to the property tax liability of an owner of a primary residence in the State. The amount of the State homestead credit is equal to approximately 20% of the taxpayer’s property tax liability for the general fund levies imposed by all of the taxing units in the taxing district (less the State property tax replacement credit).

The State does not pay the PTRC on Tax Increment. However, IC 36-7-14-39.5(c) entitles taxpayers in an allocation area to the Additional Credit payable from Tax Increment in an amount equal to the State PTRC unless the County Commissioners deny the Additional Credit, as they have done in the Area. Since 2003, under 6-1.1-21.2, the portion of the State PTRC relating to school general funds has been increased from 20% to 60% of the school general fund tax rate. The Tax Increment lost from this increase in the Additional Credit (equal to the PTRC) (if paid) may be replaced by a property tax levy throughout the District (the “TIF Replacement Levy”). This TIF Replacement Levy will be initiated annually by the State of Indiana, unless the County Commissioners reduce or eliminate the TIF Replacement Levy. The County Commissioners have not taken action to eliminate or reduce the TIF Replacement levy since its inception. The schedules estimating Tax Increment contained in Appendix B assume that the County Commissioners will not take action to reduce or eliminate the TIF Replacement Levy.

ORIGINAL ISSUE DISCOUNT

The initial public offering price of the Bonds maturing on August 1, 2017 (such Bonds, the “Discount Bonds”) is less than the principal amount payable at maturity. The Discount Bonds will be considered to be issued with original issue discount. The difference between the initial public offering price of the Discount Bonds, as set forth on the cover page of this Official Statement (assuming it is the first price at which a substantial amount of that maturity is sold) (the “Issue Price” for such maturity), and the amount payable at maturity of the Discount Bonds, will be treated as “original issue discount.” The original issue discount on each of the Discount Bonds is treated as accruing daily over the term of such Bond on the basis of the yield to maturity determined on the basis of compounding at the end of each six-month period (or shorter period from the date of the original issue) ending on February 1 and August 1 (with straight line interpolation between compounding dates). An owner who purchases a Discount Bond in the initial public offering at the Issue Price for such maturity will treat the accrued amount of original issue discount as interest which is excludable from the gross income of the owner of that Discount Bond for federal income tax purposes.

Section 1288 of the Code provides, with respect to tax-exempt obligations such as the Discount Bonds, that the amount of original issue discount accruing each period will be added to the owner’s tax basis for the Discount Bonds. Such adjusted tax basis will be used to determine taxable gain or loss upon disposition of the Discount Bonds (including sale, redemption or payment at maturity). Owners of Discount Bonds who dispose of Discount Bonds prior to maturity should consult their tax advisors concerning the amount of original issue discount accrued over the period held and the amount of taxable gain or loss upon the sale or other disposition of such Discount Bonds prior to maturity.

The original issue discount that accrues in each year to an owner of a Discount Bond may result in certain collateral federal income tax consequences. Owners of any Discount Bonds should be aware that the accrual of original issue discount in each year may result in a tax liability from these collateral tax consequences even though the owners of such Discount Bonds will not receive a corresponding cash payment until a later year.

Owners who purchase Discount Bonds in the initial public offering but at a price different from the Issue Price for such maturity should consult their own tax advisors with respect to the tax consequences of the ownership of the Discount Bonds.

The Code contains certain provisions relating to the accrual of original issue discount in the case of subsequent purchasers of Bonds such as the Discount Bonds. Owners who do not purchase Discount Bonds in the initial offering should consult their own tax advisors with respect to the tax consequences of the ownership of the Discount Bonds.

14

ORIGINAL ISSUE DISCOUNT (CONTINUED)

Owners of Discount Bonds should consult their own tax advisors with respect to the state and local tax consequences of owning the Discount Bonds. It is possible under the applicable provisions governing the determination of state or local income taxes that accrued interest on the Discount Bonds may be deemed to be received in the year of accrual even though there will not be a corresponding cash payment until a later year.

CONTINUING DISCLOSURE

Pursuant to continuing disclosure requirements promulgated by the Securities and Exchange Commission in SEC Rule 15c2-12, as amended (the “Rule”), the County will enter into a Continuing Disclosure Undertaking Agreement (the “Agreement”), to be dated the dated the date of initial delivery of the Bonds are outstanding, to provide the following information:

Audited Financial Statements. To each nationally recognized municipal securities information repository (“NRMSIR”) then in existence and to the Indiana state information depository then in existence, if any (“SID”), when and if available, the comprehensive annual financial report of the County (“CAFR”) for each twelve (12) month period, beginning with the twelve (12) month period ending December 31, 2005, together with the opinion of such accountants and all notes thereto, within sixty (60) days of receipt; and

Financial Information in this Official Statement. To each NRMSIR then in existence and to the SID, within 180 days of each December 31, beginning with the calendar year ending December 31, 2005, unaudited annual financial information for the County for such calendar year including (1) unaudited financial statements of the County, including the CAFR; (ii) operating data including (a) a statement of Tax Increment collected in the preceding year for payment of the Bonds and (b) information included under the following headings in Appendix A and Appendix B of the Official Statement (collectively, the “Annual Information”):

APPENDIX A

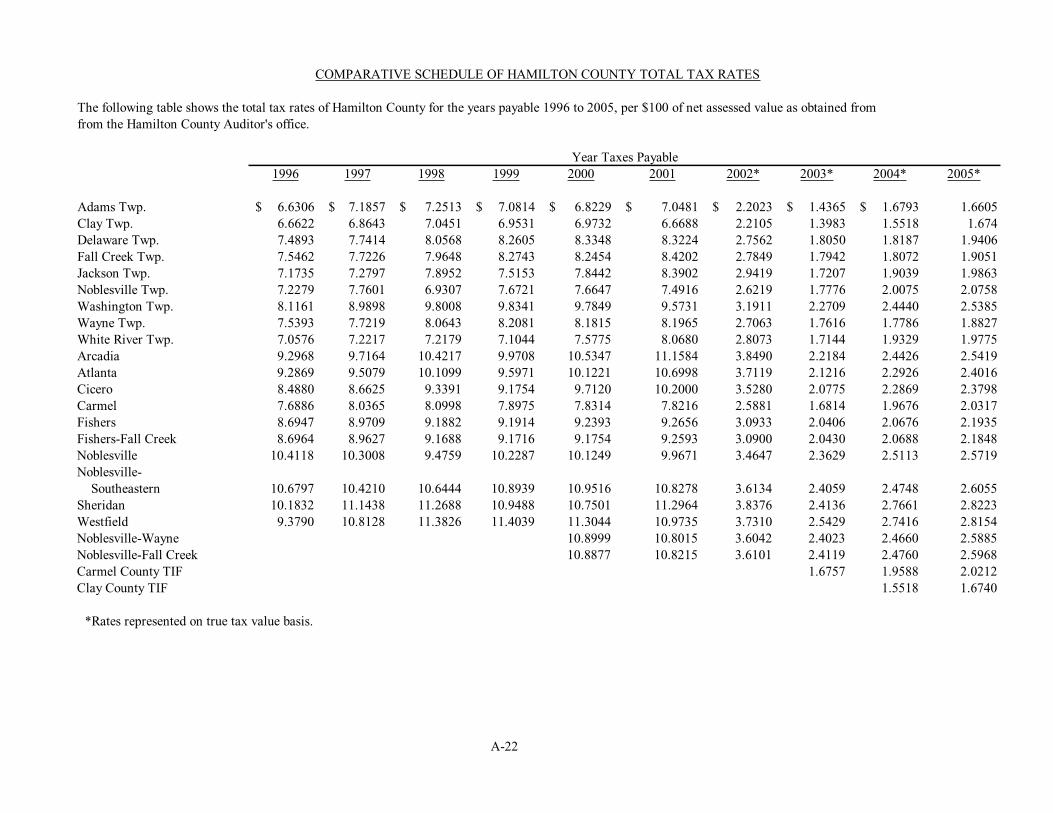

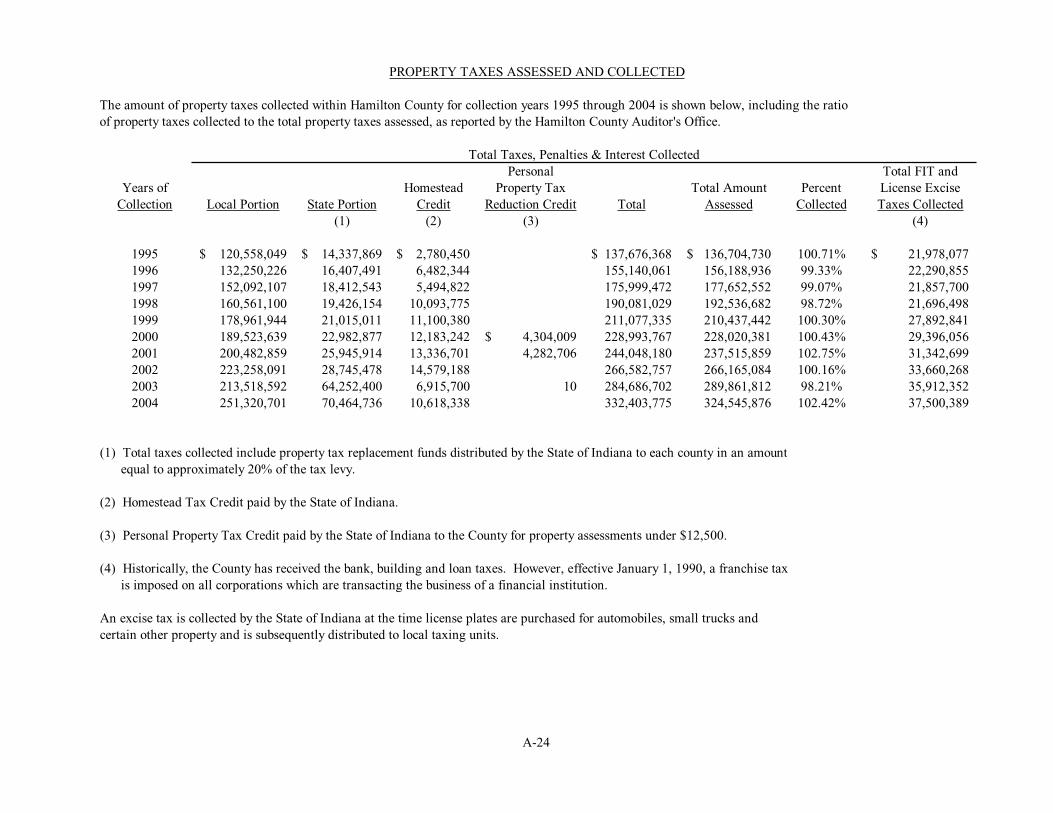

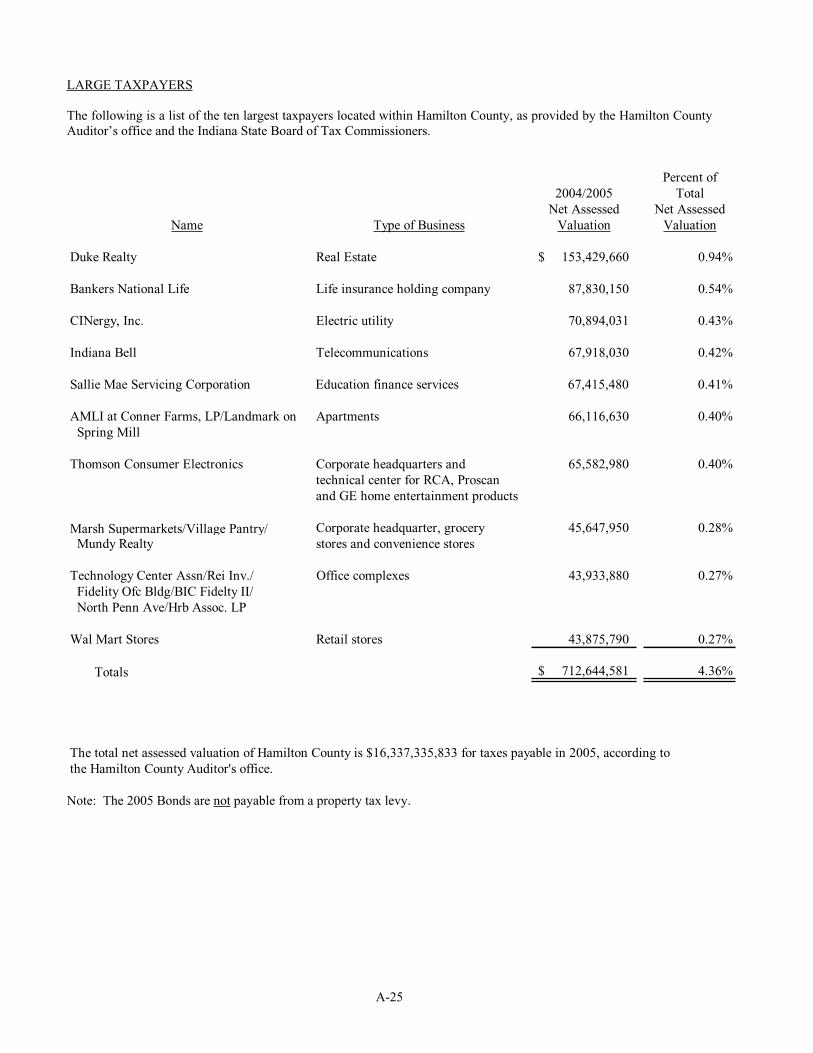

GENERAL ECONOMIC AND FINANCIAL INFORMATION - Historical Net Assessed Valuation of Hamilton County - Comparative Schedule of Hamilton County Tax Rates - Property Taxes Assessed and Collected - Large Taxpayers - Combined Statement of Revenues, Expenditures and Changes in Fund Balance

APPENDIX B

- Schedule of Historical Tax Increment

Event Notices. In a timely manner, to each NRMSIR or to the Municipal Securities Rulemaking Board (“MSRB”), and to the SID notice of certain events listed in the Rule, if material with respect to the Bonds (which determination of materiality shall be made by the County in accordance with the standards established by federal securities laws).

Failure to Disclose. In a timely manner, to each NRMSIR or to the MSRB, and to the SID notice of the County failing to provide the annual financial information as described above.

The County may, from time to time, amend or modify the Agreement without the consent of or notice to the owners of the Bonds if either (a)(i) such amendments, waiver, or modification is made in connection with a change in circumstances that arises from a change in legal requirements, change in law or change in the identity, nature, or status of the County, or type of business conducted; (ii) the Agreement, as so amended or modified, would have complied with the requirements of the Rule on the date of execution of the Agreement, after taking into account any

15

CONTINUING DISCLOSURE (CONTINUED)

amendments or interpretations of the Rule, as well as any change in circumstances; and (iii) such amendment or modification does not materially impair the interests of the holders of the Bonds, as determined either by (A) any nationally recognized bond counsel or (B) an approving vote of the bondholders at the time of such amendment or modification or (b) such amendment or modification (including an amendment or modification which rescinds the Agreement) is permitted by the SEC Rule, as then in effect.

The County may, at its sole discretion, use an agent in connection with the dissemination of any financial information required to be provided by the County pursuant to the terms of the Rule and this Agreement.

The purpose of the Agreement is to enable the Underwriter to purchase the Bonds by providing for an undertaking by the County in satisfaction of the Rule. The Agreement is solely for the benefit of the owners of the Bonds and creates no new contractual or other rights for the SEC, underwriters, brokers, dealers, municipal securities dealers, potential customers, other obligated persons or any other third party. The sole remedy against the County for any failure to carry out any provision of the Agreement shall be for specific performance of the County’s disclosure obligations under and not for money damages of any kind or in any amount or any other remedy. The County’s failure to honor its covenants hereunder shall not constitute a breach or default of the Bonds, the Bond Resolution, or any other agreement to which the County or the Commission is a party.

UNDERWRITING

The Bonds are being purchased by City Securities Corporation (the “Underwriter”) at a purchase price of $7,181,125.05 (which is $7,295,000, the original principal amount of the Bonds, less $102,091.75 in Underwriter’s Discount and $11,783.20 in Original Issue Discount). The Bond Purchase Agreement provides that all of the Bonds will be purchased by the Underwriter if any of such Bonds are purchased.

The Underwriter intends to offer the Bonds to the public at the offering prices set forth on the cover page of this Official Statement. The Underwriter may allow concessions to certain dealers (including dealers in a selling group of the Underwriter and other dealers depositing the Bonds into investment trusts), who may re-allow concessions to other dealers. After the initial public offering, the public offering price may be varied from time to time by the Underwriter.

LITIGATION

To the knowledge of the officers and counsel for the Commission and the County, there is no litigation pending, or threatened, against the Commission or the County, which in any way questions or affects the validity of the Bonds, or the Bond Resolution, or any proceedings or transactions relating to the issuance, sale or delivery of the Bonds or the collection of Tax Increment (except as described under “Risks to Bondholders”) to pay debt service.

The counsel for the County has stated that no litigation has been instituted, nor to its knowledge is there any litigation pending or threatened, which individually or in the aggregate will have a materially adverse effect upon the financial position of the County.

CERTAIN LEGAL MATTERS

Legal matters incident to the authorization and issuance of the Bonds are subject to the unqualified approving opinion of Ice Miller, Indianapolis, Indiana, Bond Counsel, whose approving opinion will be available at the time of delivery of the Bonds. Ice Miller has not been asked nor has it undertaken to review the accuracy or sufficiency of this Official Statement, and will express no opinion thereon. The form of opinion of Bond Counsel is included as Appendix D of the Official Statement.

VERIFICATION

The mathematical calculations of the adequacy of the deposit to the Trust Account to pay the principal of and accrued interest on all the outstanding 1993 Bonds on February 1, 2006 will be verified by O.W. Krohn & Associates, Certified Public Accountants, LLP. Such recomputations will be based upon information, assumptions and calculations supplied by the Underwriter.

16

LEGAL OPINIONS AND ENFORCEABILITY OF REMEDIES

The various legal opinions to be delivered concurrently with the delivery of the Bonds express the professional judgment of the attorneys rendering the opinion as to the legal issues explicitly addressed therein. By rendering a legal opinion, the opinion giver does not become an insurer or guarantor of that expression of professional judgment, of the transaction opined upon, or of the future performance of parties to such transaction. Nor does the rendering of an opinion guarantee the outcome of any legal dispute that may arise out of the transaction.