© 2013 Cengage Learning. All rights reserved. CHAPTER 7 GLOBAL2 PENG © J Marshall—Tribaleye Images/Alamy

© 2013 Cengage Learning. All rights reserved. CHAPTER 7 GLOBAL2 PENG © J Marshall—Tribaleye Images/Alamy.

Dec 24, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

© 2013 Cengage Learning. All rights reserved.

CHAPTER 7

GLOBAL2 PENG

© J

Mar

shal

l—T

ribal

eye

Imag

es/A

lam

y

© 2013 Cengage Learning. All rights reserved.

CHAPTER 7 LEARNING OBJECTIVES

After studying this chapter, you should be able to:

1. List the factors that determine foreign exchange rates.

2. Articulate and explain the steps in the evolution of the international monetary system.

3. Identify strategic responses firms can take to deal with foreign exchange movements.

4. Identify three things you need to know about currency when doing business internationally.

Foreign exchange rate

Price of one currency in terms of another

• An appreciation is an increase in the value of the currency.

• A depreciation is a loss in the value of the currency.

© 2013 Cengage Learning. All rights reserved.

EXAMPLE OF KEY EXCHANGE RATES (4/6/11)

Source: These examples are from April 6, 2011. Adapted from “Key currency cross rates,” Wall Street Journal, 6 April 2011, available at http://www.wsj.com [accessed 6 April 2011]. Copyright © 2011 Dow Jones & Company, Inc. All Rights Reserved. Reading vertically, the first column means US$1 = C$0.96 = ¥85 = Mexican Peso 11.81 = SFr 0.92 = £0.61 = €0.70. Reading horizontally, the last row means €1 = US$1.43; £1 = US$1.63; SFr 1 = US$1.09; Mexican Peso 1 = US$0.08; ¥1 = US$0.01; C$1 = US$1.04.

© 2013 Cengage Learning. All rights reserved.

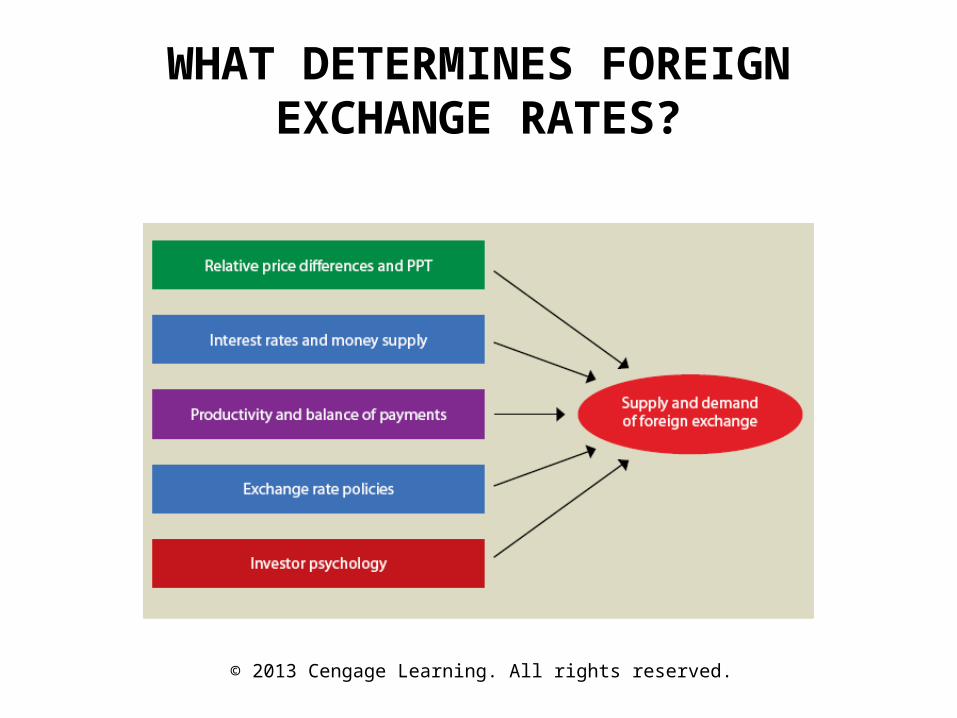

WHAT DETERMINES FOREIGN EXCHANGE RATES?

© 2013 Cengage Learning. All rights reserved.

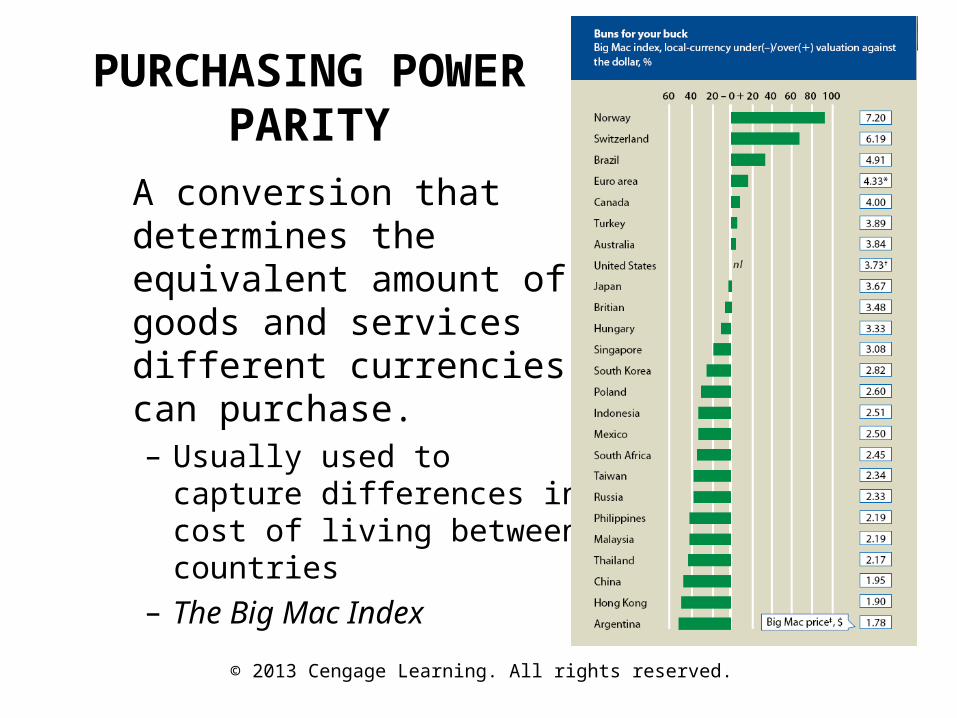

PURCHASING POWER PARITY

A conversion that determines the equivalent amount of goods and services different currencies can purchase.– Usually used to capture

differences in cost of living between countries

– The Big Mac Index

© 2013 Cengage Learning. All rights reserved.

PURCHASING POWER PARITY

Some countries have expensive prices, while others have cheap ones. The effect of these differences on the exchange rate is measured by the purchasing power parity (PPP).

© 2013 Cengage Learning. All rights reserved.

INTEREST RATES AND MONEY SUPPLY

– If one country’s interest rates are high relative to the interest rates of other countries, it will attract foreign funds.

– Inflation causes currency to depreciate.

© 2013 Cengage Learning. All rights reserved.

PRODUCTIVITY

– Rise in a country’s productivity brings increase of FDI, fueling demand for its home currency.

PRODUCTIVITY AND BALANCE OF PAYMENTS

Balance of payments

A country’s international transaction statement (includes merchandise trade, service trade, and capital movement)

Current Account balance

Current account = balance of trade + net factor income from abroad + net unilateral transfers from abroad

© 2013 Cengage Learning. All rights reserved.

BALANCE OF PAYMENTS

EXCHANGE RATE POLICIES

Floating (or flexible) exchange rate policy

Willingness of a government to let demand and supply conditions determine exchange rates

• Clean (or free) float– Pure market solution to determine exchange rates

• Dirty (or managed) float– Using selective government intervention to determine

exchange rates

EXCHANGE RATE POLICIES

Fixed rate policy

Setting the exchange rate of a currency relative to other currencies

•Peg– Stabilizing policy of linking a developing country’s currency to a key

currency

Target exchange rates (crawling bands)

Specified upper or lower bounds within which an exchange rate is allowed to fluctuate (range)

INVESTOR PSYCHOLOGY

bandwagon effectEffect of investors moving in the same direction at the

same time (as in “jumping on the…”)

capital flightPhenomenon in which a large number of individuals and

companies exchange domestic currencies for a foreign currency

© 2013 Cengage Learning. All rights reserved.

THE EVOLUTION OF THE INTERNATIONAL MONETARY SYSTEM

• The Gold Standard (1870-1914)– Gold used as common

denominator• CD: Currency or

commodity to which the value of all currencies are pegged

© iS

tock

phot

o.co

m/T

alaj

© 2013 Cengage Learning. All rights reserved.

THE EVOLUTION OF THE INTERNATIONAL MONETARY SYSTEM

• The Bretton Woods System (1944-1973)– US dollar as common denominator

© iS

tock

phot

o.co

m/A

nton

Vak

hlac

hev

© 2013 Cengage Learning. All rights reserved.

THE EVOLUTION OF THE INTERNATIONAL MONETARY SYSTEM

• The Post-Bretton Woods System (1973-present)– System of flexible exchange rate regimes.– No common denominator; diversity of

exchange rates.

A STRONG DOLLAR VS A WEAK DOLLAR

International Monetary Fund (IMF)

An international organization established to promote international monetary cooperation, exchange stability, and orderly exchange arrangements

© 2013 Cengage Learning. All rights reserved.

INTERNATIONAL MONETARY FUND (IMF)

• Legacy of Bretton Woods system.• Lender of last resort for countries experiencing

balance of payments problems. • Each member country assigned a quota that

determines required contribution. – Quota: Weight a member country carries within the

IMF, which determines the amount of its financial contribution (its “subscription”), and its capacity to borrow from the IMF, and its voting power

• Loans typically require long-term policy reforms.

© 2013 Cengage Learning. All rights reserved.

STRATEGIC RESPONSES TO FOREIGN EXCHANGE MOVEMENTS

Strategies for Financial Companies:Main goal – to profit from foreign exchange market.

• Spot transactions – single-shot exchange of one currency for another (ex: vacation).

• Forward transactions –purchase or sale of currencies for future delivery.

• Currency swap – conversion of one currency into another at Time 1, with agreement to revert it back to original currency at Time 2 in the future.

STRATEGIES FOR FINANCIAL COMPANIES

TWO TYPES OF FOREIGN TRANSACTIONS:• Forward discount

Condition under which the forward rate of one currency relative to another currency is higher than the spot rate

• Forward premium

Condition under which the forward rate of one currency relative to another currency is lower than the spot rate

© 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

© 2013 Cengage Learning. All rights reserved.

STRATEGIC RESPONSES TO FOREIGN EXCHANGE MOVEMENTS

Strategies for Non-Financial Companies

• Invoicing in their own currencies (big advantage to US firms)

• Currency hedging

• Strategic hedging

STRATEGIES FOR NONFINANCIAL COMPANIES

Currency risk

Potential for loss associated with fluctuations in the foreign exchange market

Currency hedging

A transaction that protects trades and investors from exposure to the fluctuations of the spot (daily) exchange rate.

Strategic hedging

Spreading out activities in a number of countries in different currency zones to offset any currency losses in one region through gains in other regions

© 2013 Cengage Learning. All rights reserved.

THREE THINGS TO KNOW ABOUT CURRENCIES

• Fostering foreign exchange literacy is a must.

• Risk analysis of any country must include an analysis of its currency risks.

• A currency risk-management strategy is necessary—via invoicing in one’s own currency, currency hedging, or strategic hedging.

Related Documents