Slide to accompany Blank and Tarquin Basics of Engineering Economy, 2008 3 - 1 © 2008 McGraw-Hill All rights reserved Lecture slides to Lecture slides to accompany accompany Basics of Engineering Basics of Engineering Economy Economy by by Leland Blank and Anthony Leland Blank and Anthony Tarquin Tarquin Chapter 3 Chapter 3 Nominal and Effective Nominal and Effective Interest Rates Interest Rates

© 2008 McGraw-Hill All rights reserved Slide to accompany Blank and Tarquin Basics of Engineering Economy, 2008 3 - 1 Lecture slides to accompany Basics.

Dec 21, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Slide to accompany Blank and TarquinBasics of Engineering Economy, 2008 3 - 1 © 2008 McGraw-Hill

All rights reserved

Lecture slides to accompanyLecture slides to accompany

Basics of Engineering EconomyBasics of Engineering Economybyby

Leland Blank and Anthony Tarquin Leland Blank and Anthony Tarquin

Chapter 3Chapter 3

Nominal and Effective Nominal and Effective

Interest RatesInterest Rates

Slide to accompany Blank and TarquinBasics of Engineering Economy, 2008 3 - 2 © 2008 McGraw-Hill

All rights reserved

Chapter 3 – Nominal & Effective Interest

PURPOSE

Perform calculations for interest rates and

cash flows that occur on a time basis

other than yearly

TOPICS

Recognize nominal and effective rates

Effective interest ratesPayment period (PP) and

compounding period (CP)Single amounts with

PP ≥ CPSeries with PP ≥ CPSingle and series with

PP < CPSpreadsheet use

Slide to accompany Blank and TarquinBasics of Engineering Economy, 2008 3 - 3 © 2008 McGraw-Hill

All rights reserved

Sec 3.1 – Nominal and Effective Rate Statements

Nominal rates• Interest rate per time

period without regard to compounding frequency

• Some nominal statements:– 8% per year compounded

monthly– 2% per month compounded

weekly– 8% per year compounded

quarterly– 5% per quarter compounded

monthly

Effective rates• Interest rate is compounded

more frequently than once per year

• Some statements indicating an effective rate:– 15% per year– effective 8.3% per year

compounded monthly– 2% per month compounded

monthly– effective 1% per week

compounded continuously

Slide to accompany Blank and TarquinBasics of Engineering Economy, 2008 3 - 4 © 2008 McGraw-Hill

All rights reserved

Sec 3.2 – Effective Interest Rate Formula

• i = effective rate per some stated period, e.g., quarterly, annually

• r = nominal rate for same time period

• m = frequency of compounding per same time period

Slide to accompany Blank and TarquinBasics of Engineering Economy, 2008 3 - 5 © 2008 McGraw-Hill

All rights reserved

Sec 3.2 – Effective Interest Rate

Compounding frequency

Period for effective i

Time period for r

m must equal

Annual annual year 1

Semi-annual annual year 2

Quarterly annual year 4

Monthly annual year 12

Daily annual year 365

Monthly semi-annual 6 months 6

Weekly quarterly quarter 12

Slide to accompany Blank and TarquinBasics of Engineering Economy, 2008 3 - 6 © 2008 McGraw-Hill

All rights reserved

Sec 3.2 – Effective Interest Rate

Example: Find i per year, if m = 4 for quarterly compounding, and

r = 12% per year

Stated period for i is YEAR

i = (1 + 0.12/4)4 - 1 = 12.55%

rEffective i = (1+ ) 1

mm

Slide to accompany Blank and TarquinBasics of Engineering Economy, 2008 3 - 7 © 2008 McGraw-Hill

All rights reserved

Sec 3.2 – Nominal and Effective RatesNominal

r = rate/period × periods

Example: Rate is 1.5% per month. Determine nominal rate per quarter, year, and over 2 years

Qtr: r = 1.5 × 3 mth = 4.5%

Year: r = 1.5 ×12 mth = 18% = 4.5 × 4 qtr = 18%

2 yrs: r =1.5 × 24 mth = 36% = 18 × 2 yrs = 36%

Effective

Example: Credit card rate is 1.5% per month compounded monthly. Determine effective rate per quarter and per year

Period is quarter: r = 1.5 × 3 mth = 4.5% m = 3 i = (1 + 0.045/3)3 – 1 = 4.57% per quarter

Period is year: r = 18% m = 12

i = (1 + 0.18/12)12 - 1) = 19.6% per year

rEffective i = (1+ ) 1

mm

Slide to accompany Blank and TarquinBasics of Engineering Economy, 2008 3 - 8 © 2008 McGraw-Hill

All rights reserved

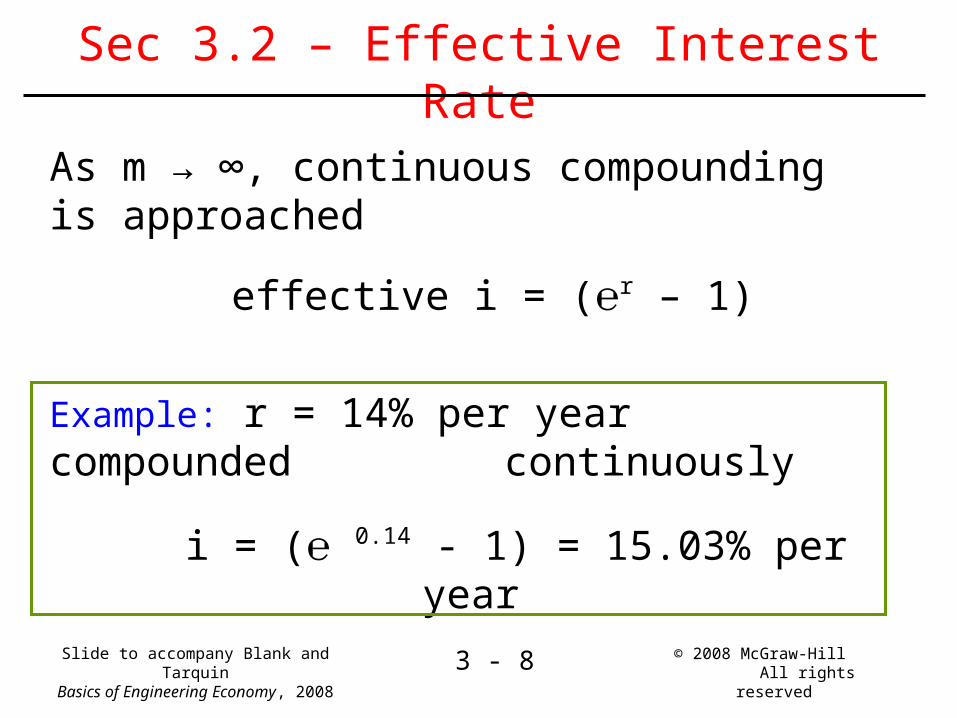

Sec 3.2 – Effective Interest Rate

As m → ∞, continuous compounding is approached

effective i = (℮r – 1)

Example: r = 14% per year compounded continuously

i = (℮ 0.14 - 1) = 15.03% per year

Slide to accompany Blank and TarquinBasics of Engineering Economy, 2008 3 - 9 © 2008 McGraw-Hill

All rights reserved

Sec 3.2 – Nominal and Effective Rates

Using Excel functions to find rates

Slide to accompany Blank and TarquinBasics of Engineering Economy, 2008 3 - 10 © 2008 McGraw-Hill

All rights reserved

Sec 3.3 – Payment Periods (PP)and Compounding Periods (CP)

• PP – how often cash flows occur• CP – how often interest in compounded• If PP = CP, no problem concerning effective i rate

Examples where effective i is involved: Monthly deposit, quarterly compounding (PP < CP)Semi-annual payment, monthly compounding (PP > CP)

Slide to accompany Blank and TarquinBasics of Engineering Economy, 2008 3 - 11 © 2008 McGraw-Hill

All rights reserved

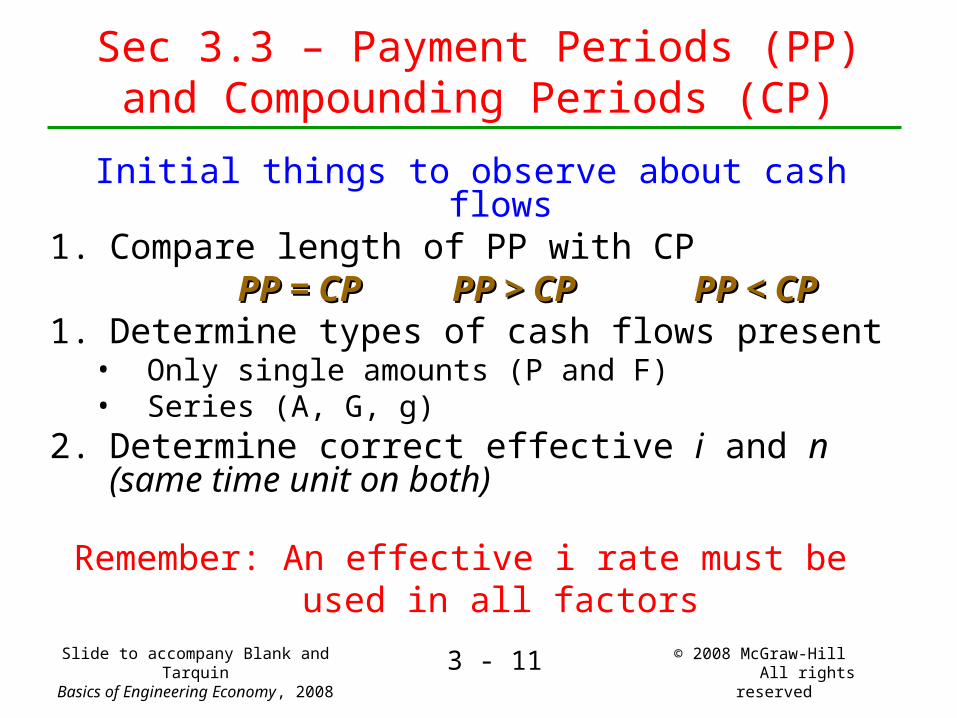

Sec 3.3 – Payment Periods (PP)and Compounding Periods (CP)

Initial things to observe about cash flows1. Compare length of PP with CP PP = CP PP > CP PP < CPPP = CP PP > CP PP < CP1. Determine types of cash flows present

• Only single amounts (P and F)• Series (A, G, g)

2. Determine correct effective i and n (same time unit on both)

Remember: An effective i rate must be used in all factors

Slide to accompany Blank and TarquinBasics of Engineering Economy, 2008 3 - 12 © 2008 McGraw-Hill

All rights reserved

Sec 3.4 – Equivalence with Single Amounts

If only P and F cash flows are present, equivalence relations are

P = F(P/F, effective i per period, # of periods) [1] F = P(F/P, effective i per period, # of periods) [2]

Example: Find equivalent F in 10 years if P is $1000 now. Assume r = 12% per year compounded semi-annually.

- PP = year and CP = 6 months; period is 6 months - Only single amount cash flows - Use relation [2] above to find F

F = 1000(F/P, 6% semi-annually, 20 periods) = 1000(3.2071) = $3207

Slide to accompany Blank and TarquinBasics of Engineering Economy, 2008 3 - 13 © 2008 McGraw-Hill

All rights reserved

Sec 3.5 – Equivalence with Series and PP ≥ CP

• Count number of payments. This is n• Determine effective i over same time

period as n• Use these i and n values in factors

Example: $75 per month for 3 years at 12% per year compounded monthlyPP = CP = monthn = 36 monthseffective i = 1% per month

Relation: F = A(F/A,1%,36)

Slide to accompany Blank and TarquinBasics of Engineering Economy, 2008 3 - 14 © 2008 McGraw-Hill

All rights reserved

Sec 3.5 – Equivalence with Series and PP ≥ CP

• Count number of payments. This is n• Determine effective i over same time period as n• Use these i and n values in factors

Example: $5000 per quarter for 6 years at 12% per year compounded monthlyPP = quarter and CP = month → PP > CPn = 24 quartersi = 1% per month or 3% per quarterm = 3 CP per quartereffective i per quarter = (1 + 0.03/3)3 – 1 = 3.03%

Relation: F = A(F/A,3.03%,24)

Slide to accompany Blank and TarquinBasics of Engineering Economy, 2008 3 - 15 © 2008 McGraw-Hill

All rights reserved

Sec 3.5 – Equivalence with Series and PP ≥ CP

0

P = $3M

• First step: Find P for n = 10 annual payments• Period is year• CP = 6 months; PP = year; PP > CP• Effective i per year = (1 + 0.08/2)2 – 1 = 8.16% Relation: P = 3M + 200,000(P/A,8.16%,10) = $4,332,400

(continued →)

Slide to accompany Blank and TarquinBasics of Engineering Economy, 2008 3 - 16 © 2008 McGraw-Hill

All rights reserved

Sec 3.5 – Equivalence with Series and PP ≥ CP

0

P = $3M

• Second step: Find A for n = 20 semi-annual amounts• Period is six months• CP = 6 months; PP = 6 months; PP = CP• Effective i per 6 months = 8%/2 = 4% Relation: A = 4,332,400(A/P,4%,20) = $318,778

Slide to accompany Blank and TarquinBasics of Engineering Economy, 2008 3 - 17 © 2008 McGraw-Hill

All rights reserved

Sec 3.6 – Equivalence with Series and PP < CP

Example: deposits monthly (PP) with interest compounded semi-annually (CP)

Result: PP < CP

Usually, interest is not paid on interperiod deposits

For equivalence computations: Cash flows are ‘moved’ to match CP time period

Slide to accompany Blank and TarquinBasics of Engineering Economy, 2008 3 - 18 © 2008 McGraw-Hill

All rights reserved

Sec 3.6 – Equivalence with Series and PP < CP

APPROACH NORMALLY TAKEN

Move cash flows not at end of a compounding period: Deposits ( minus cash flows) - to end of period Withdrawals (plus cash flows) - to beginning of same

period (which is the end of last period)

Example (next slide): move monthly deposits to match quarterly compounding. Now, PP = CP = quarter

Find P, F or A using effective i per quarter

Slide to accompany Blank and TarquinBasics of Engineering Economy, 2008 3 - 19 © 2008 McGraw-Hill

All rights reserved

Sec 3.6 – Equivalence with Series and PP < CPMoving cash flows turns top cash flow diagram into bottom

Qtr 1 Qtr 2 Qtr 3 Qtr4

Slide to accompany Blank and TarquinBasics of Engineering Economy, 2008 3 - 20 © 2008 McGraw-Hill

All rights reserved

Sec 3.7 – Spreadsheet UsageSpreadsheet function format and structure:

Fine effective rate: = EFFECT(nom r%, m)Nominal r is over same time period as effective i

Find nominal rate: = NOMINAL(eff i%, m)Result of nominal is always per year

Example: Deposits are planned as follows: $1000 now, $3000 after 4 years, $1500 after 6 years. Find F after 10 years. Interest is 12% per year compounded semiannually

Slide to accompany Blank and TarquinBasics of Engineering Economy, 2008 3 - 21 © 2008 McGraw-Hill

All rights reserved

Sec 3.7 – Spreadsheet Usage

Related Documents

![Engineering Economy 7th Edition Solution Manual [Blank & Tarquin]](https://static.cupdf.com/doc/110x72/55cf9c0e550346d033a86730/engineering-economy-7th-edition-solution-manual-blank-tarquin-56a0a1152740c.jpg)