2008, Cambridge Energy Research Associates, Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written cons 1 CERA_London RT_November 2008 Higher School of Economics Moscow October 27 2008 The Outlook for Russian Oil Supply Thane Gustafson CERA

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

© 2008, Cambridge Energy Research Associates, Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

1

CERA_London RT_November 2008

Higher School of EconomicsMoscowOctober 27 2008

The Outlook for Russian Oil Supply

Thane GustafsonCERA

© 2008, Cambridge Energy Research Associates, Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

2

CERA_London RT_November 2008

1. A Brief Look Back:— The “Russian Oil Miracle” 1999-2004— The Slow-Down 2005-2007— The Stagnation 2008--?

2. What is the Industry Suffering From?— Capital Starvation— A Shortage of Profitable Opportunities— Excess Taxation

3. Will Tax Relief Be Enough?— No: Too Small— No: Wrong Problem

4. The Real Problem: the Era of High Rents is Over (Gas Too)— The next generation of oil and gas will be higher-cost— Too many claimants and too little rent— The state will have to cut back its share—but can it do so?

Outline of Presentation

© 2008, Cambridge Energy Research Associates, Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

3

CERA_London RT_November 2008

During the Period 1999–2005, Russian Oil Output Grew Strongly (Led by a Resurgence in West Siberia), Coming as a Major (but Welcome) Surprise for Global Oil Markets

0

100

200

300

400

500

600

1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007*

mil

lio

n m

etri

c to

ns

Russian Crude Oil Production

West Siberian Oil Production

*Projected; Eurasian Oil Export Outlook (November 2007 update).

Source: Cambridge Energy Research Associates.

© 2008, Cambridge Energy Research Associates, Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

4

CERA_London RT_November 2008

After Rising at Double-Digit Rates in 2000–2004, Russia’s Monthly Growth Rate Falls to Only ~2% in 2005–2007 … and Declines Slightly in 2008

• After growing 8.9% in 2004, Russian output rose only 2.4% in 2005 to 470.0 mt (9.5 mbd) and 2.2% in 2006, to 480.5 mt (9.71 mbd)

• Up by 2.3% in 2007 to 491.5 mt (9.83 mbd)

— Main boost came from Sakhalin-1 project in Jan-Feb

•Onshore production up only ~0.6%— Little growth in second half of 2007

• In 2008, production in first 9 months down 0.5%, to 365.5 mt (9.74 mbd)

— Output in April slid to 9.68 mbd, but back up slightly to ~9.8 mbd in August and September

• Companies been warning for some time that decline imminent due to squeeze on investment from high taxes and rising costs

Monthly Russian Oil Production, 1999–2008

(Month of Previous Year = Index of 100)

85

90

95

100

105

110

115

Jan-

99Ju

n-99

Nov-9

9Apr

-00

Sep-0

0Feb

-01

Jul-0

1Dec

-01

May

-02

Oct-

02M

ar-0

3Aug

-03

Jan-

04Ju

n-04

Nov-0

4Apr

-05

Sep-0

5Feb

-06

Jul-0

6Dec

-06

May

-07

Oct-

07M

ar-0

8Aug

-08

Source: Cambridge Energy Research Associates.

© 2008, Cambridge Energy Research Associates, Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

5

CERA_London RT_November 2008

A Look Back at the “Oil Miracle” 1999-2004

• “A Handful of New Fields Producing More, Hundreds of Old Fields Losing Less”

• The Secret to Slowing Decline Rates: “Pumps, Fracs, and Floods”

• A One-Time Harvesting of the “Soviet Dividend”

© 2008, Cambridge Energy Research Associates, Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

6

CERA_London RT_November 2008

… and Regions: Russian Crude Oil Production by Major Region, First Half 2008 Versus 2007

Source: Cambridge Energy Research Associates.81003-22

0

20

40

60

80

100

120

140

160

180

WestSiberia

Volga-Urals

Timan-Pechora

East Siberiaand Sakhalin

Other

MillionMetricTons

1st Half 2007

1st Half 2008

© 2008, Cambridge Energy Research Associates, Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

7

CERA_London RT_November 2008

Russian Tax Code’s Petroleum Taxation Regime: “One Size Fits All”

• Oil Taxation Remains Highly Regressive: Focused on Revenues/Production Volumes, Not Profits

— Such systems invariably unstable due to need to adjust for changing prices and costs

• Original Plan for New Tax Code: Profits-Based, Self-Regulating Mechanism and Predictable Environment for Investors

— Relatively low royalty— Normal corporate profit tax— Plus excess-profit tax— Plans for special regime for low-flow wells

• But New Tax Code of January 2002 Opted for Simple and Enforceable (but Regressive) Taxes

— Replacement of royalty, mineral restoration tax, and excise tax with single “mineral resource extraction tax” (MRET)

— MRET set at 340 R/ton for crude oil, but linked to international export prices for Urals Blend with sliding-scale formula

— Export taxes on crude oil and refined products• For crude oil and products, sliding-scale formulae linked to international export prices

for Urals Blend (with subsequent revisions in effect in 2005)– Profit tax = 35% of profits (according to Russian accounting standards)

© 2008, Cambridge Energy Research Associates, Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

8

CERA_London RT_November 2008

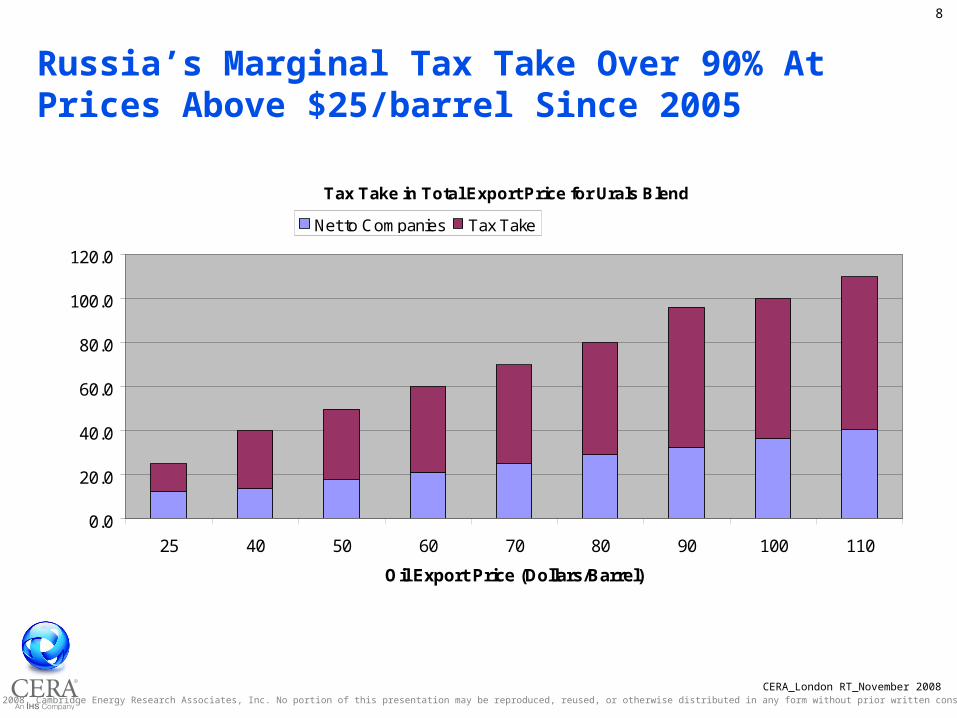

Russia’s Marginal Tax Take Over 90% At Prices Above $25/barrel Since 2005

Tax Take in Total Export Price for Urals Blend

0.0

20.0

40.0

60.0

80.0

100.0

120.0

25 40 50 60 70 80 90 100 110

Oil Export Price (Dollars/Barrel)

Net to Companies Tax Take

© 2008, Cambridge Energy Research Associates, Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

9

CERA_London RT_November 2008

Comparison of Oil Company Profitability

Source: Cambridge Energy Research Associates.81003-11

0

5

10

15

20

25

30

35

40

45

2003 2004 2005 2006 2007

Net Incomeper Barrel of

Production

Lukoil

TNK-BP

Rosneft

Big Five IOCs (average)

Shell

Chevron

Gazprom NeftExxonMobilBPTotal

RussianOilCompanies

InternationalOilCompanies

© 2008, Cambridge Energy Research Associates, Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

10

CERA_London RT_November 2008

2007-2008: Government Offers Limited Tax Relief

• January 2007: As Oil Production Growth Slowed in 2005-2006, Government Granted Two Forms of Modest Tax Relief:

— Holiday from MRET for upstream projects in Sakha, Irkutsk, and Krasnoyarsk

• Really done to provide oil for ESPO — Modest differentiation: 70% MRET reduction for “hard-to-recover” oil

in selected fields (more than 80% depleted)— But impact largely symbolic: less than $250 million in 2007

• Because of technical quirk, companies unable to take advantage of “hard-to-recover” measure

• January 2009: Additional Measures Go into Effect:— Threshold of MRET raised from $9/bbl to $15/bbl— Number of regions eligible for MRET holidays expanded— Finance Minister Kudrin estimates new package worth 100 billion

rubles/year (~$3.7 billion) in tax savings to industry• “Not enough,” says Oil Industry:

— By April 2008, companies calling for higher MRET threshold and cuts in export duty

— Kudrin still opposed to further cuts—for now

© 2008, Cambridge Energy Research Associates, Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

11

CERA_London RT_November 2008

What’s Wrong with Government’s Tax-Relief Program to Date?

• Too Modest in Scale:— $4 billion in tax cuts small compared to the industry’s total upstream

capital spending of nearly $23 billion in 2007— Government reluctant to cut export taxes, by far larger issue

• Aimed at Wrong Problem:— Aimed at stimulating new development in frontier provinces— No incentive to add and produce reserves-in-place from existing fields

• Does Not Correct Basic Flaw:— System taxes production (gross revenues) instead of profits— Too blunt an instrument: “one size fits all”— Fails to encourage efficient production of higher-cost oil

© 2008, Cambridge Energy Research Associates, Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

12

CERA_London RT_November 2008

Collapse of Prices Since July 2008 Has Cut Russia’s Oil Export Earnings Essentially in Half:From ~$1 billion per day to ~$500 million per day

Daily Prices for Urals Blend Crude Oil

$0

$20

$40

$60

$80

$100

$120

$140

$160

Jan-

02Ju

l-02

Jan-

03Ju

l-03

Jan-

04

Jul-0

4Ja

n-05

Jul-0

5Ja

n-06

Jul-0

6Ja

n-07

Jul-0

7Ja

n-08

Jul-0

8

© 2008, Cambridge Energy Research Associates, Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

13

CERA_London RT_November 2008

What Will Be The Impact of Falling Prices On The Oil Industry?

• Government Will Be Hurt More than Industry— “Regressive on the way up, progressive on the way down”: State took

90% of price increase; it will now absorb 90% of price decline• Decline of Ruble Providing Mild “Devaluation Dividend”

— Offsets some of current ~14% inflation• Declining Commodity Prices and Economic Slowdown May

Help to Contain Cost Pressures— Particularly cost of steel

• But “Stickiness” in Tax Scale Becomes Big Problem if Prices Fall Fast

— Because export taxes adjusted only every two months• BOTTOM LINE: Oil companies’ Net Income and Cash Flow Will

Suffer, But Not as Much as Might Seem at First Glance— Still, companies likely to cut their dividends and their capex budgets

for 2008— While rerouting their investment resources to “brownfields”

© 2008, Cambridge Energy Research Associates, Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

14

CERA_London RT_November 2008

The Russian Oil Industry—and the State--Are at a Fundamental Divide

• Era of Rapid, Low-Cost Growth in Production is Over:— Low-cost “post-Soviet” legacy opportunities running out— From now on, new oil will be much more costly

• Next Generation of Russian Oil Will Generate Less Rent— Rents historically divided among three main claimants: the state, the

industry (for reinvestment), and its shareholders— If reinvestment needs go up, then share remaining for shareholders

and the state will have to go down— Yet returns to shareholders are already much lower than international

norms— Lower oil prices only aggravate the basic problem

• Two Bottom-line Implications: — As profits and dividends decline (while capex goes up), company

market values (and therefore share prices) will remain low— State revenues from oil will decline sharply; a new tax reform, to re-

broaden the tax base, will be essential• This Will Be Politically Very Painful: Will The State Actually

Leave the Oil Industry the Investment Capital It Will Need?

If you have any questions about this presentation orCERA in general, please feel free to contact

Tatyana Ustyantseva+1 617 866 5000

55 Cambridge ParkwayCambridge, Massachusetts 02142, USA

www.cera.com

BeijingSan Francisco

Washington, DC

Cambridge, MA

Calgary

Mexico City

Rio de Janeiro

Paris

Oslo

Moscow

Johannesburg

Mumbai

Singapore

Bangkok

Tokyo

Houston

Related Documents