© 2007 The Williams Companies, Inc. All rights reserved. Building Critical Energy Infrastructure… A Global Challenge Phil Wright, Williams Gas Pipeline 27 th USAEE/IAEE North American Conference September 17th, 2007

© 2007 The Williams Companies, Inc. All rights reserved. Building Critical Energy Infrastructure… A Global Challenge Phil Wright, Williams Gas Pipeline.

Dec 17, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

© 2007 The Williams Companies, Inc. All rights reserved.

Building Critical Energy Infrastructure… A Global ChallengePhil Wright, Williams Gas Pipeline27th USAEE/IAEE North American ConferenceSeptember 17th, 2007

© 2007 The Williams Companies, Inc. All rights reserved. 2

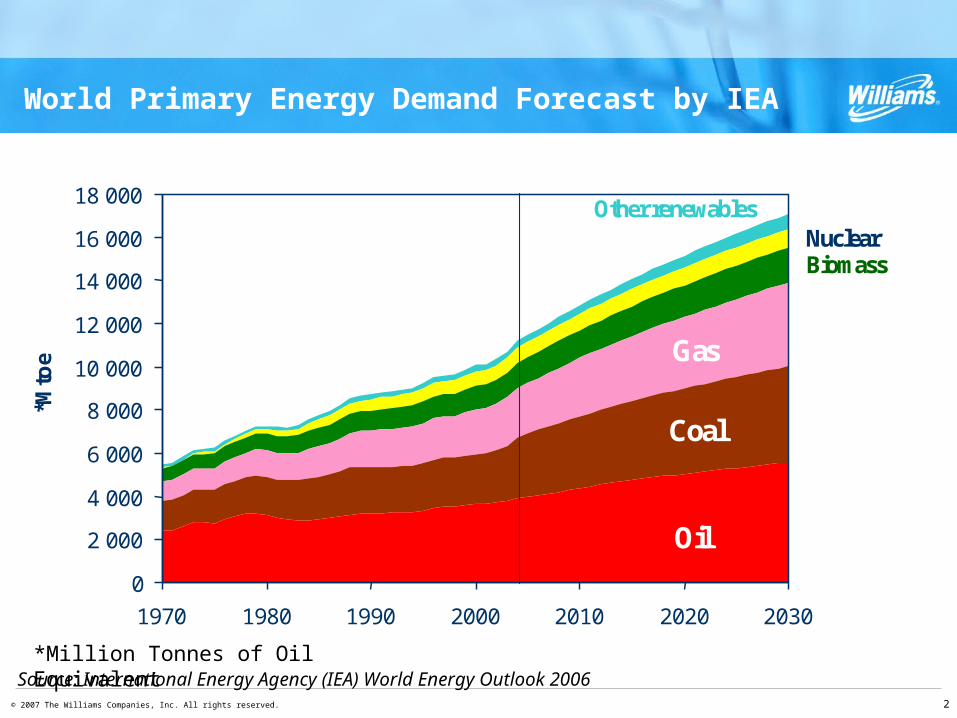

Oil

Coal

Gas

BiomassNuclear

Other renewables

0

2 000

4 000

6 000

8 000

10 000

12 000

14 000

16 000

18 000

1970 1980 1990 2000 2010 2020 2030

*Mto

e

World Primary Energy Demand Forecast by IEA

Source: International Energy Agency (IEA) World Energy Outlook 2006*Million Tonnes of Oil Equivalent

© 2007 The Williams Companies, Inc. All rights reserved. 3

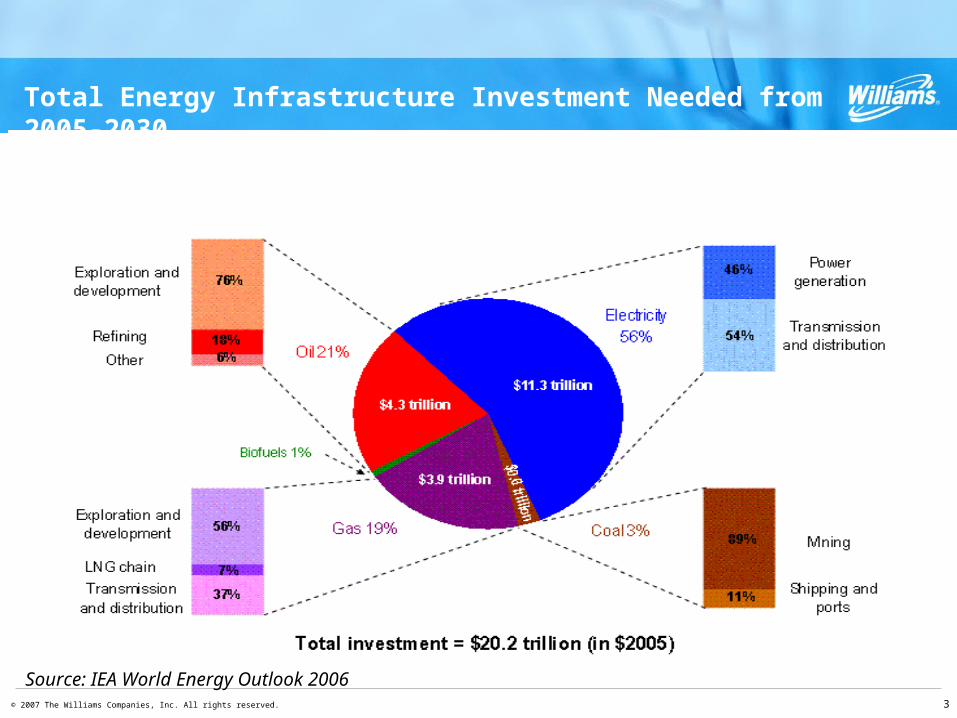

Total Energy Infrastructure Investment Needed from 2005-2030

Source: IEA World Energy Outlook 2006

© 2007 The Williams Companies, Inc. All rights reserved. 4

Natural Gas Infrastructure Needs

> Large amount of infrastructure work

> Large capital commitments for expansion as well as maintaining current infrastructure – and stable and fair regulatory climate to attract capital

> Increased demand for labor, materials and engineering services to put the infrastructure into place

> Land Use, Right of Way Access (ROW), and Regulatory affects

© 2007 The Williams Companies, Inc. All rights reserved. 5

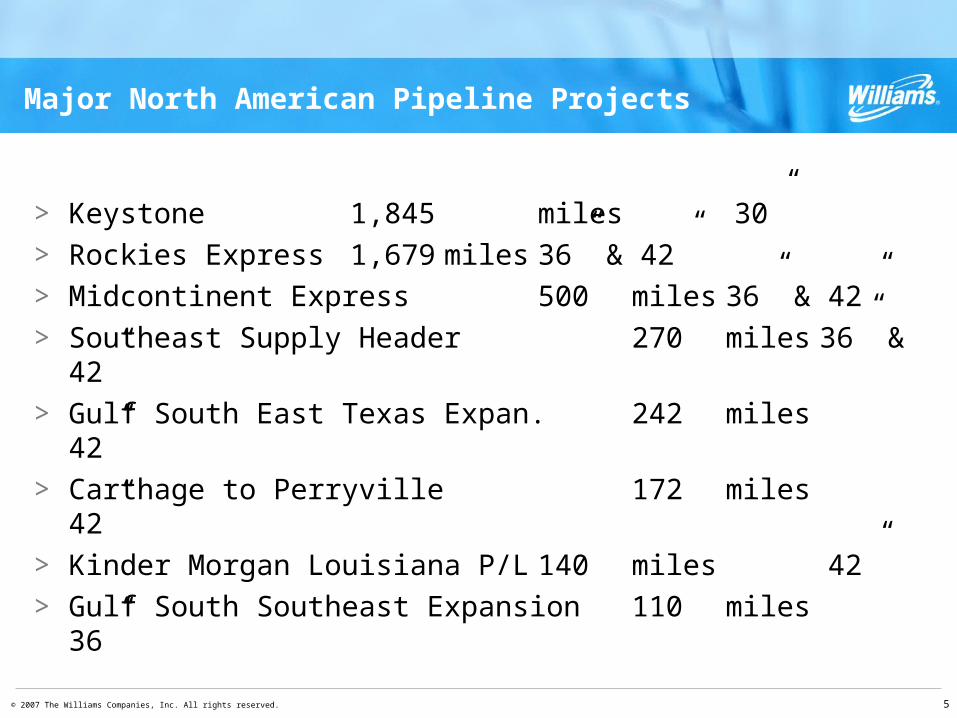

Major North American Pipeline Projects

> Keystone 1,845 miles 30”

> Rockies Express 1,679 miles 36” & 42”

> Midcontinent Express 500 miles 36” & 42”

> Southeast Supply Header 270 miles 36” & 42”

> Gulf South East Texas Expan. 242 miles 42”

> Carthage to Perryville 172 miles 42”

> Kinder Morgan Louisiana P/L 140 miles 42”

> Gulf South Southeast Expansion 110 miles 36”

© 2007 The Williams Companies, Inc. All rights reserved. 6

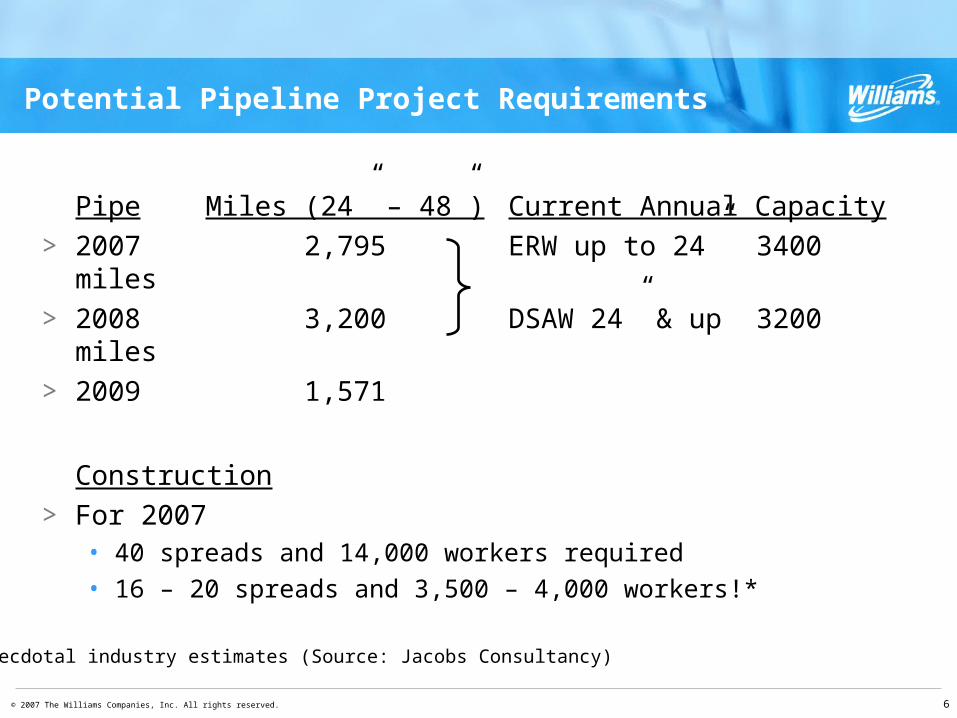

Potential Pipeline Project Requirements

Pipe Miles (24” – 48”) Current Annual Capacity

> 2007 2,795 ERW up to 24” 3400 miles

> 2008 3,200 DSAW 24” & up 3200 miles

> 2009 1,571

Construction

> For 2007 • 40 spreads and 14,000 workers required • 16 – 20 spreads and 3,500 – 4,000 workers!*

*Anecdotal industry estimates (Source: Jacobs Consultancy)

© 2007 The Williams Companies, Inc. All rights reserved. 7

Hurdles to Building Critical Infrastructure

> Costs have risen significantly in recent years for labor, materials and services

© 2007 The Williams Companies, Inc. All rights reserved. 8

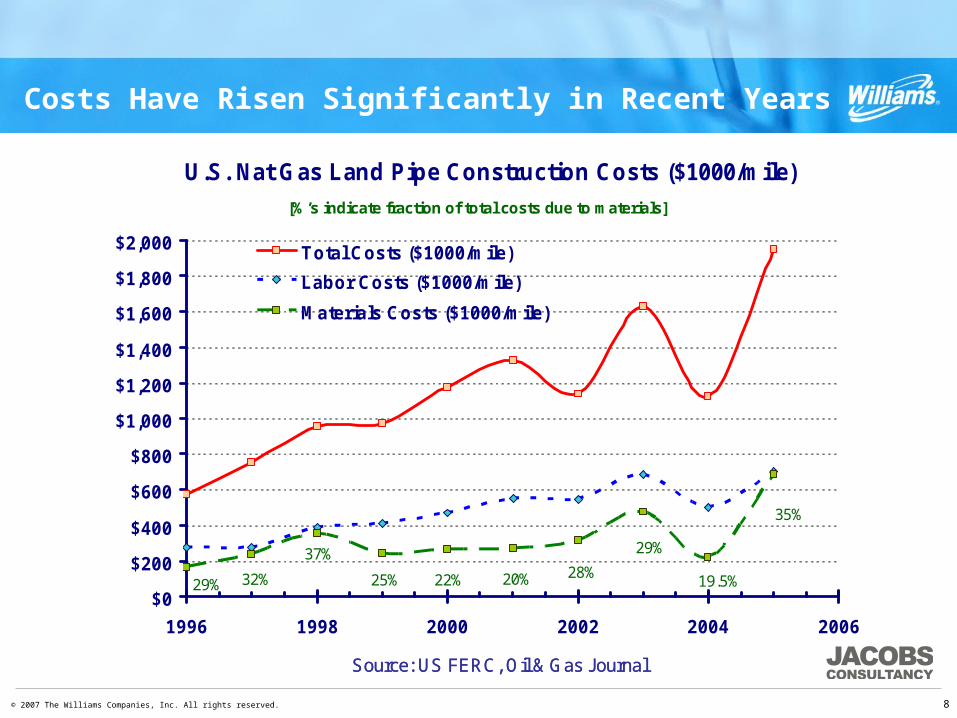

Costs Have Risen Significantly in Recent Years

U.S. Nat Gas Land Pipe Construction Costs ($1000/mile)

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

$2,000

1996 1998 2000 2002 2004 2006

Total Costs ($1000/mile)

Labor Costs ($1000/mile)

Materials Costs ($1000/mile)

37%

29% 25% 22% 20% 28%

29%

19.5%

35%

32%

[%’s indicate fraction of total costs due to materials]

Source: US FERC, Oil & Gas Journal

U.S. Nat Gas Land Pipe Construction Costs ($1000/mile)

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

$2,000

1996 1998 2000 2002 2004 2006

Total Costs ($1000/mile)

Labor Costs ($1000/mile)

Materials Costs ($1000/mile)

37%

29% 25% 22% 20% 28%

29%

19.5%

35%

32%

[%’s indicate fraction of total costs due to materials]

Source: US FERC, Oil & Gas Journal

© 2007 The Williams Companies, Inc. All rights reserved. 9

Hurdles to Building Critical Infrastructure

> Costs have risen significantly in recent years for labor, materials and services

> Strain on qualified technical and construction talent

© 2007 The Williams Companies, Inc. All rights reserved. 10

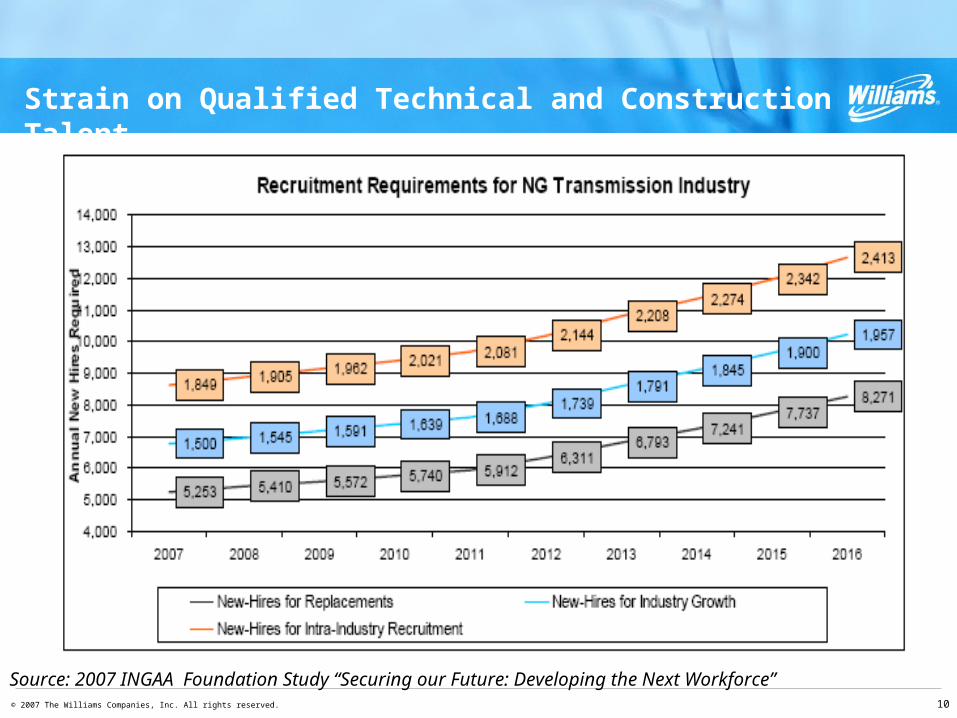

Strain on Qualified Technical and Construction Talent

Source: 2007 INGAA Foundation Study “Securing our Future: Developing the Next Workforce”

© 2007 The Williams Companies, Inc. All rights reserved. 11

Hurdles to Building Critical Infrastructure

> Costs have risen significantly in recent years for labor, materials and services

> Strain on qualified technical and construction talent

> Competition globally for materials and services

© 2007 The Williams Companies, Inc. All rights reserved. 12

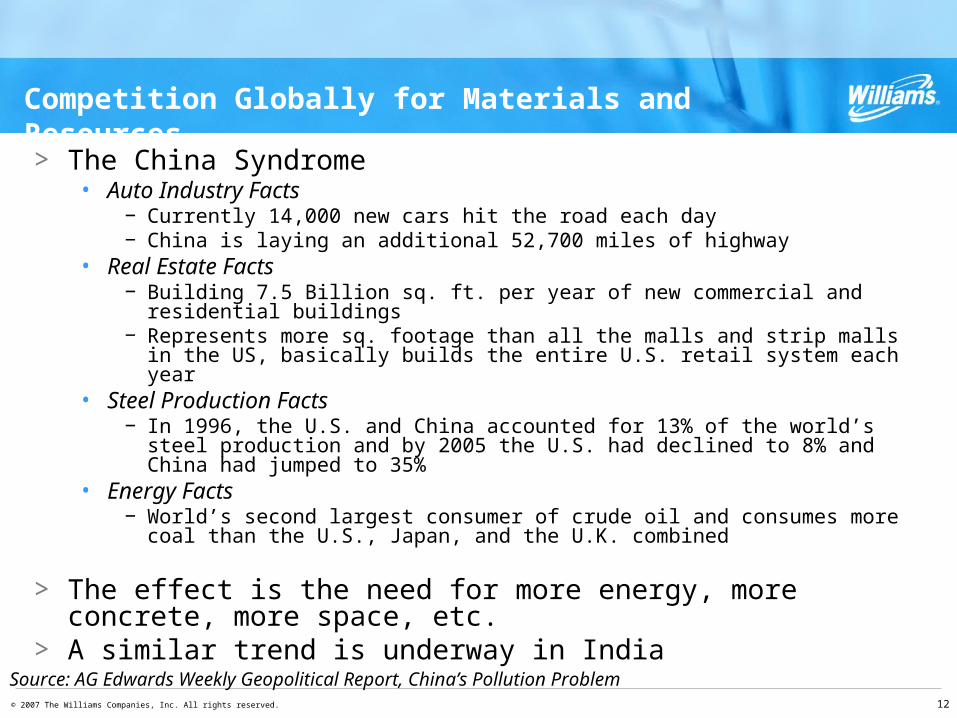

Competition Globally for Materials and Resources

> The China Syndrome• Auto Industry Facts

− Currently 14,000 new cars hit the road each day− China is laying an additional 52,700 miles of highway

• Real Estate Facts− Building 7.5 Billion sq. ft. per year of new commercial and residential buildings− Represents more sq. footage than all the malls and strip malls in the US, basically

builds the entire U.S. retail system each year• Steel Production Facts

− In 1996, the U.S. and China accounted for 13% of the world’s steel production and by 2005 the U.S. had declined to 8% and China had jumped to 35%

• Energy Facts− World’s second largest consumer of crude oil and consumes more coal than the

U.S., Japan, and the U.K. combined

> The effect is the need for more energy, more concrete, more space, etc.

> A similar trend is underway in India

Source: AG Edwards Weekly Geopolitical Report, China’s Pollution Problem

© 2007 The Williams Companies, Inc. All rights reserved. 13

Hurdles to Building Critical Infrastructure

> Costs have risen significantly in recent years for labor, materials and services

> Strain on qualified technical and construction talent

> Competition globally for materials and services

> Land use and ROW restrictions

© 2007 The Williams Companies, Inc. All rights reserved. 14

Land Use and ROW Restrictions

> Restriction on leasing of land for exploration • 100+ TCF already restricted from exploration and development in

the U.S. alone

> A recent experience :• We followed procedure to received FERC approval for a project• Numerous Open Houses with the public• After we received approval a landowner objected to the project and

threatened legal action• As a result, FERC reopened the process and cost $ millions more!

© 2007 The Williams Companies, Inc. All rights reserved. 15

We can lower these hurdles by…

> In the interim• Leverage global markets to supplement domestic resources ( e.g.

sunset of protective tariffs on pipe)• Encourage students not interested in four year colleges to pursue

technical school degrees / career path – joint industry / academic effort initiative

− IPAA and Houston Area High School Technology Program

• Open dialog between state and local governments and special interest groups regarding land and ROW access

• Engender sense of urgency

© 2007 The Williams Companies, Inc. All rights reserved. 16

We can lower these hurdles by…

> Long Term• Supporting efforts to encourage enrollment in engineering and

science at the university level and promoting our industry to future workforce

• Educating government that all out effort is essential for maintaining affordable energy

− Efficiency

− Renewables

− Clean coal technology

− And a lot of gas and oil

© 2007 The Williams Companies, Inc. All rights reserved. 17

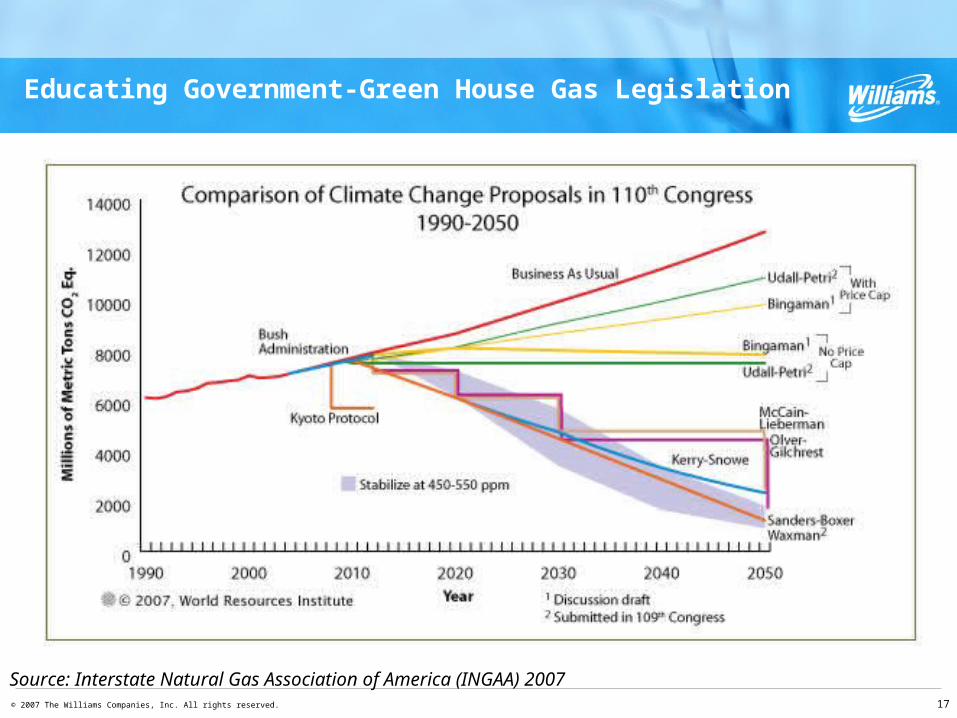

Educating Government-Green House Gas Legislation

Source: Interstate Natural Gas Association of America (INGAA) 2007

© 2007 The Williams Companies, Inc. All rights reserved. 18

Conclusions

> Projected demand growth for energy calls for $20 trillion cumulative global infrastructure investment through 2030

> Significant incremental talent required to execute the largest build out since post- WWII era expansion

> Excessive hurdles complicate building necessary infrastructure

> Overcoming these hurdles will require creativity and efficient resource management

Related Documents

![Walter Wright - Mitchell Williams · Walter Wright From: Kendra Akin Jones [kendra.jones©arkansasag.gov] Sent: Thursday, December 01, 2011 3:12 PM To: Walter Wright Subject: FW:](https://static.cupdf.com/doc/110x72/5b301fc77f8b9ac06e8dee02/walter-wright-mitchell-walter-wright-from-kendra-akin-jones-kendrajonesarkansasaggov.jpg)