© 2004 The McGraw-Hill Companies, Inc. McGraw-Hill/Irwin Chapter 15 Leases Leases

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Chapter 15

LeasesLeases

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-2

Basic Lease Terms

A lease is an agreement where the A lease is an agreement where the lessorlessor conveys the right to use property, plant, conveys the right to use property, plant, or equipment, usually for a stated period or equipment, usually for a stated period

of time, to the of time, to the lesseelessee..

Lessor = Owner of propertyLessor = Owner of propertyLessor = Owner of propertyLessor = Owner of property

Lessee = RenterLessee = RenterLessee = RenterLessee = Renter

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-3

Lease Classifications

Lessee Lessor

Operating lease Operating lease

Capital lease Direct financing lease

Sales-type lease

Lessee Lessor

Operating lease Operating lease

Capital lease Direct financing lease

Sales-type lease

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-4

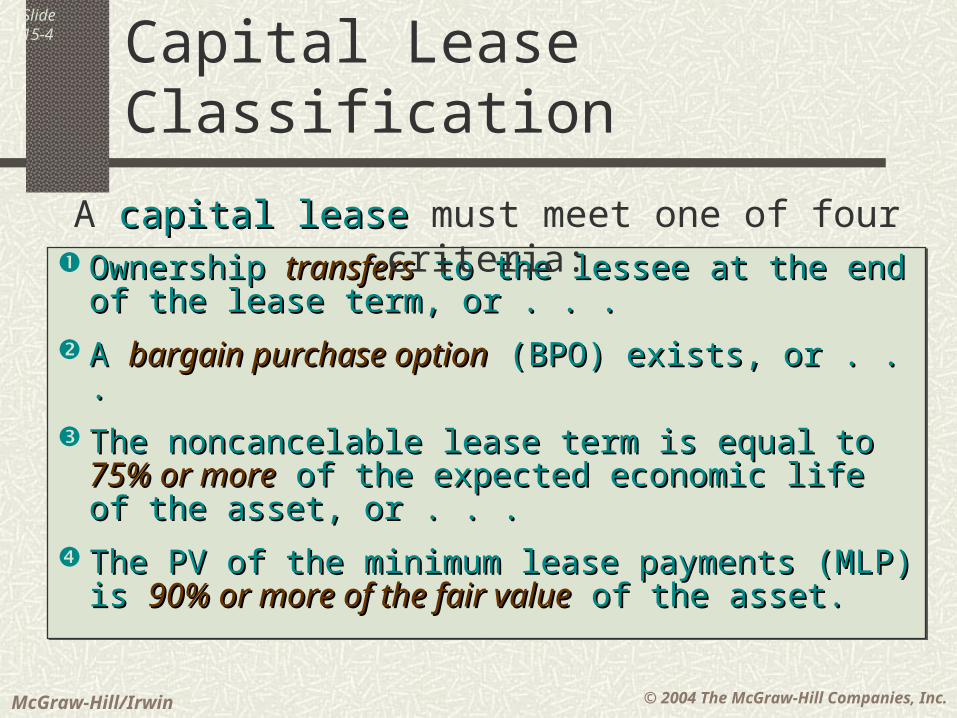

Capital Lease Classification

OwnershipOwnership transferstransfers to the lessee at the end of to the lessee at the end of the lease term, or . . . the lease term, or . . .

A A bargain purchase optionbargain purchase option (BPO) exists, or . . .(BPO) exists, or . . .

The noncancelable lease term is equal to The noncancelable lease term is equal to 75% or 75% or moremore of the expected economic life of the asset, of the expected economic life of the asset, or . . .or . . .

The PV of the minimum lease payments (MLP) is The PV of the minimum lease payments (MLP) is 90% or more of the fair value90% or more of the fair value of the asset.of the asset.

OwnershipOwnership transferstransfers to the lessee at the end of to the lessee at the end of the lease term, or . . . the lease term, or . . .

A A bargain purchase optionbargain purchase option (BPO) exists, or . . .(BPO) exists, or . . .

The noncancelable lease term is equal to The noncancelable lease term is equal to 75% or 75% or moremore of the expected economic life of the asset, of the expected economic life of the asset, or . . .or . . .

The PV of the minimum lease payments (MLP) is The PV of the minimum lease payments (MLP) is 90% or more of the fair value90% or more of the fair value of the asset.of the asset.

A capital leasecapital lease must meet one of four criteria:

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-5

Capital Lease Classification

A A bargain purchase option (BPO)bargain purchase option (BPO) gives the lessee the right to gives the lessee the right to purchase the leased asset at a price sufficiently lower than the purchase the leased asset at a price sufficiently lower than the expected fair value of the property and the exercise of the option expected fair value of the property and the exercise of the option appears reasonably assured.appears reasonably assured.

A A bargain purchase option (BPO)bargain purchase option (BPO) gives the lessee the right to gives the lessee the right to purchase the leased asset at a price sufficiently lower than the purchase the leased asset at a price sufficiently lower than the expected fair value of the property and the exercise of the option expected fair value of the property and the exercise of the option appears reasonably assured.appears reasonably assured.

The The lease termlease term is normally considered to be the noncancelable is normally considered to be the noncancelable term of the lease plus any periods covered by term of the lease plus any periods covered by bargain renewal bargain renewal optionsoptions. If the inception of the lease occurs during the last 25% of . If the inception of the lease occurs during the last 25% of an asset’s economic life, this criterion does not apply.an asset’s economic life, this criterion does not apply.

The The lease termlease term is normally considered to be the noncancelable is normally considered to be the noncancelable term of the lease plus any periods covered by term of the lease plus any periods covered by bargain renewal bargain renewal optionsoptions. If the inception of the lease occurs during the last 25% of . If the inception of the lease occurs during the last 25% of an asset’s economic life, this criterion does not apply.an asset’s economic life, this criterion does not apply.

For the lessee, a capital lease is treated as the For the lessee, a capital lease is treated as the purchase of an asset – the lessee records both an purchase of an asset – the lessee records both an

asset and liability at inception of the lease.asset and liability at inception of the lease.

For the lessee, a capital lease is treated as the For the lessee, a capital lease is treated as the purchase of an asset – the lessee records both an purchase of an asset – the lessee records both an

asset and liability at inception of the lease.asset and liability at inception of the lease.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-6

Additional Lessor Conditions

The four conditions discussed apply to both the The four conditions discussed apply to both the lessee and lessor. However, the lessor must lessee and lessor. However, the lessor must

meet two additional conditions for the lease to meet two additional conditions for the lease to be classified as either a direct financing or sales-be classified as either a direct financing or sales-

type lease:type lease:

1.1. The collectibility of the lease payments must be The collectibility of the lease payments must be reasonably predictable.reasonably predictable.

2.2. If any costs to the lessor have yet to be incurred If any costs to the lessor have yet to be incurred they are reasonably predictable. Performance they are reasonably predictable. Performance by the lessor is substantially complete.by the lessor is substantially complete.

The four conditions discussed apply to both the The four conditions discussed apply to both the lessee and lessor. However, the lessor must lessee and lessor. However, the lessor must

meet two additional conditions for the lease to meet two additional conditions for the lease to be classified as either a direct financing or sales-be classified as either a direct financing or sales-

type lease:type lease:

1.1. The collectibility of the lease payments must be The collectibility of the lease payments must be reasonably predictable.reasonably predictable.

2.2. If any costs to the lessor have yet to be incurred If any costs to the lessor have yet to be incurred they are reasonably predictable. Performance they are reasonably predictable. Performance by the lessor is substantially complete.by the lessor is substantially complete.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-7

Operating Leases

Criteria for a capital Criteria for a capital lease not met.lease not met.

Criteria for a capital Criteria for a capital lease not met.lease not met.

Lease agreement Lease agreement exists.exists.

Lease agreement Lease agreement exists.exists.

Record lease as an Record lease as an Operating LeaseOperating Lease

Record lease as an Record lease as an Operating LeaseOperating Lease

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-8

Operating Leases

On December 26, 2003, Matrix, Inc. On December 26, 2003, Matrix, Inc. signed a two-year operating lease signed a two-year operating lease

with RentPro, Inc. for office with RentPro, Inc. for office equipment. The lease called for equipment. The lease called for $500 per month, payable at the $500 per month, payable at the

beginning of each month.beginning of each month.

The first payment was due on January The first payment was due on January 1, 2004. Matrix paid three months 1, 2004. Matrix paid three months

of rent in advance on December 26.of rent in advance on December 26.

On December 26, 2003, Matrix, Inc. On December 26, 2003, Matrix, Inc. signed a two-year operating lease signed a two-year operating lease

with RentPro, Inc. for office with RentPro, Inc. for office equipment. The lease called for equipment. The lease called for $500 per month, payable at the $500 per month, payable at the

beginning of each month.beginning of each month.

The first payment was due on January The first payment was due on January 1, 2004. Matrix paid three months 1, 2004. Matrix paid three months

of rent in advance on December 26.of rent in advance on December 26.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-9

Operating Leases

Prepare the entry on the books of Matrix on Prepare the entry on the books of Matrix on December 26.December 26.

GENERAL JOURNAL

Date Description Debit Credit

Dec 26 Prepaid rent 1,500 Cash 1,500

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-10

Operating Leases

Prepare the entry the RentPro would make to Prepare the entry the RentPro would make to record receipt of the December 26. record receipt of the December 26.

GENERAL JOURNAL

Date Description Debit Credit

Dec 26 Cash 1,500 Unearned Rent Revenue 1,500

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-11

Operating LeasesThe January 31 adjustment by Matrix.The January 31 adjustment by Matrix.

GENERAL JOURNAL

Date Description Debit Credit

Jan 31 Rent expense 500 Prepaid rent 500

The January 31 adjustment by RentPro.The January 31 adjustment by RentPro.

GENERAL JOURNAL

Date Description Debit Credit

Jan 31 Unearned rent revenue 500 Rent revenue 500

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-12

We’ll look at We’ll look at non-operating non-operating

leases for lessee leases for lessee and Lessor in and Lessor in some detail.some detail.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-13

Nonoperating Leases - Lessee

The amount recorded (capitalized) is the present The amount recorded (capitalized) is the present value of the minimum lease payment. However, the value of the minimum lease payment. However, the amount recorded cannot exceed the fair value of the amount recorded cannot exceed the fair value of the

leased asset.leased asset.

The amount recorded (capitalized) is the present The amount recorded (capitalized) is the present value of the minimum lease payment. However, the value of the minimum lease payment. However, the amount recorded cannot exceed the fair value of the amount recorded cannot exceed the fair value of the

leased asset.leased asset.

In calculating the present value of the minimum In calculating the present value of the minimum lease payment, the interest rate used by the lessee lease payment, the interest rate used by the lessee

is the lower of:is the lower of:

1.1. Its incremental borrowing rate, orIts incremental borrowing rate, or

2.2. The implicit interest rate used by the lessor.The implicit interest rate used by the lessor.

In calculating the present value of the minimum In calculating the present value of the minimum lease payment, the interest rate used by the lessee lease payment, the interest rate used by the lessee

is the lower of:is the lower of:

1.1. Its incremental borrowing rate, orIts incremental borrowing rate, or

2.2. The implicit interest rate used by the lessor.The implicit interest rate used by the lessor.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-14

Nonoperating Leases - Lessor

When the lessor is a manufacturer or dealer, the fair When the lessor is a manufacturer or dealer, the fair value of the property at the inception of the lease is value of the property at the inception of the lease is

likely to be its normal selling price.likely to be its normal selling price.

When the lessor is a manufacturer or dealer, the fair When the lessor is a manufacturer or dealer, the fair value of the property at the inception of the lease is value of the property at the inception of the lease is

likely to be its normal selling price.likely to be its normal selling price.

If the lessor is not a manufacturer or dealer, the fair If the lessor is not a manufacturer or dealer, the fair value of the leased assets is typically the lessor’s value of the leased assets is typically the lessor’s

cost.cost.

If the lessor is not a manufacturer or dealer, the fair If the lessor is not a manufacturer or dealer, the fair value of the leased assets is typically the lessor’s value of the leased assets is typically the lessor’s

cost.cost.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-15

Nonoperating Leases

On January 1, 2002, Matrix, Inc. signed a 5-year lease On January 1, 2002, Matrix, Inc. signed a 5-year lease with RentPro, Inc. for equipment. The lease calls for with RentPro, Inc. for equipment. The lease calls for

$6,000 per year, payable at the beginning of each $6,000 per year, payable at the beginning of each year starting on January 1, 2002.year starting on January 1, 2002.

The equipment has a economic life of 7 years and a fair The equipment has a economic life of 7 years and a fair value of $25,873. The equipment reverts to RentPro value of $25,873. The equipment reverts to RentPro

at the end of the lease, unless Matrix buys the at the end of the lease, unless Matrix buys the equipment for $4,500, the expected fair value. equipment for $4,500, the expected fair value.

Matrix has an incremental borrowing rate of 8%, Matrix has an incremental borrowing rate of 8%, which is the same implicit rate used by RentPro to which is the same implicit rate used by RentPro to

calculate the annual payment.calculate the annual payment.

On January 1, 2002, Matrix, Inc. signed a 5-year lease On January 1, 2002, Matrix, Inc. signed a 5-year lease with RentPro, Inc. for equipment. The lease calls for with RentPro, Inc. for equipment. The lease calls for

$6,000 per year, payable at the beginning of each $6,000 per year, payable at the beginning of each year starting on January 1, 2002.year starting on January 1, 2002.

The equipment has a economic life of 7 years and a fair The equipment has a economic life of 7 years and a fair value of $25,873. The equipment reverts to RentPro value of $25,873. The equipment reverts to RentPro

at the end of the lease, unless Matrix buys the at the end of the lease, unless Matrix buys the equipment for $4,500, the expected fair value. equipment for $4,500, the expected fair value.

Matrix has an incremental borrowing rate of 8%, Matrix has an incremental borrowing rate of 8%, which is the same implicit rate used by RentPro to which is the same implicit rate used by RentPro to

calculate the annual payment.calculate the annual payment.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-16

Nonoperating Leases - Lessee

The lease term does not meet the “75% of The lease term does not meet the “75% of the economic life” test.the economic life” test.

YearsEconomic life 775% of economic life 5.25

Lease Term 5

Lease Term (5 years) is less than 75% of the economiclife of the equipment (5.25 years). This test is not met.

YearsEconomic life 775% of economic life 5.25

Lease Term 5

Lease Term (5 years) is less than 75% of the economiclife of the equipment (5.25 years). This test is not met.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-17

Minimum Lease Payments per Year 6,000$ Present Value of Annuity Due factor (5 periods @ 8%) × 4.31213

Present Value of the MLP 25,872.78$

FMV of the equipment at lease inception 25,873$ 90% of the FMV of the equipment at lease inception 23,286$

The present value of the MLP > 90% of the FMV of theequipment. This test is met.

Minimum Lease Payments per Year 6,000$ Present Value of Annuity Due factor (5 periods @ 8%) × 4.31213

Present Value of the MLP 25,872.78$

FMV of the equipment at lease inception 25,873$ 90% of the FMV of the equipment at lease inception 23,286$

The present value of the MLP > 90% of the FMV of theequipment. This test is met.

Nonoperating Leases - Lessee

The PV of the minimum lease payments (MLP) The PV of the minimum lease payments (MLP) 90% of the equipment’s fair value?90% of the equipment’s fair value?

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-18

Nonoperating Leases - Lessee

Matrix makes the following entries at Matrix makes the following entries at inception of the lease.inception of the lease.

GENERAL JOURNAL

Date Description Debit Credit

Jan 1 Leased equipment 25,873 Lease payable 25,873

Lease payable 6,000 Cash 6,000

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-19

Nonoperating Leases - Lessor

In addition to the information given earlier, the In addition to the information given earlier, the lessor (RentPro) knows that the collectibility lessor (RentPro) knows that the collectibility

of the lease payments is reasonably of the lease payments is reasonably predictable, and there are no future cost to be predictable, and there are no future cost to be

incurred. RentPro’s performance is incurred. RentPro’s performance is substantially complete at far as the lease is substantially complete at far as the lease is

concerned. RentPro is not a manufacturer or concerned. RentPro is not a manufacturer or dealer and its cost of the equipment is dealer and its cost of the equipment is

$25,872.78. $25,872.78.

In addition to the information given earlier, the In addition to the information given earlier, the lessor (RentPro) knows that the collectibility lessor (RentPro) knows that the collectibility

of the lease payments is reasonably of the lease payments is reasonably predictable, and there are no future cost to be predictable, and there are no future cost to be

incurred. RentPro’s performance is incurred. RentPro’s performance is substantially complete at far as the lease is substantially complete at far as the lease is

concerned. RentPro is not a manufacturer or concerned. RentPro is not a manufacturer or dealer and its cost of the equipment is dealer and its cost of the equipment is

$25,872.78. $25,872.78.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-20

Nonoperating Leases - Lessor

Because the cost of the asset in the hands of the Because the cost of the asset in the hands of the lessor is equal fair market value, the lease is lessor is equal fair market value, the lease is

classified as a classified as a Direct Financing LeaseDirect Financing Lease..

Because the cost of the asset in the hands of the Because the cost of the asset in the hands of the lessor is equal fair market value, the lease is lessor is equal fair market value, the lease is

classified as a classified as a Direct Financing LeaseDirect Financing Lease..

GENERAL JOURNAL

Date Description Debit Credit

Jan 1 Lease receivable 30,000 Inventory of equipment 25,873 Unearned interest revenue 4,127

$6,000 $6,000 × 5 = × 5 = $30,000$30,000

$6,000 $6,000 × 5 = × 5 = $30,000$30,000

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-21

Nonoperating Leases - Lessor

Because the cost of the asset in the hands of the Because the cost of the asset in the hands of the lessor is equal fair market value, the lease is lessor is equal fair market value, the lease is

classified as a classified as a Direct Financing LeaseDirect Financing Lease..

Because the cost of the asset in the hands of the Because the cost of the asset in the hands of the lessor is equal fair market value, the lease is lessor is equal fair market value, the lease is

classified as a classified as a Direct Financing LeaseDirect Financing Lease..

GENERAL JOURNAL

Date Description Debit Credit

Jan 1 Cash 6,000 Lease receivable 6,000

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-22

Period PaymentInterest Income

Asset Recovery

Unrecovered Balance

25,873$ 1 6,000$ -$ (6,000)$ 19,873 2 6,000 1,590 (4,410) 15,463 3 6,000 1,237 (4,763) 10,700 4 6,000 856 (5,144) 5,556 5 6,000 444 (5,556) 0

Lease Amortization Schedule

Period PaymentInterest Income

Asset Recovery

Unrecovered Balance

25,873$ 1 6,000$ -$ (6,000)$ 19,873 2 6,000 1,590 (4,410) 15,463 3 6,000 1,237 (4,763) 10,700 4 6,000 856 (5,144) 5,556 5 6,000 444 (5,556) 0

Lease Amortization Schedule

Lease Amortization Schedule

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-23

Nonoperating LeasesDecember 31, 2002, adjustment by Matrix.December 31, 2002, adjustment by Matrix.

GENERAL JOURNAL

Date Description Debit Credit

Dec 31 Interest expense 1,590 Interest payable 1,590

December 31, 2002, adjustment by RentPro.December 31, 2002, adjustment by RentPro.

GENERAL JOURNAL

Date Description Debit Credit

Dec 31 Unearned interest revenue 1,590 Interest revenue 1,590

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-24

Depreciation by Lessee

Depreciation expense is recorded in a manner Depreciation expense is recorded in a manner consistent with the company’s usual policy concerning consistent with the company’s usual policy concerning

depreciation of other operational assets.depreciation of other operational assets.

Depreciation expense is recorded in a manner Depreciation expense is recorded in a manner consistent with the company’s usual policy concerning consistent with the company’s usual policy concerning

depreciation of other operational assets.depreciation of other operational assets.

If title passes to the lessee at the enter or If title passes to the lessee at the enter or the lease term, or the lease contains a the lease term, or the lease contains a bargain purchase option, the asset is bargain purchase option, the asset is

depreciated over the depreciated over the asset’s economic lifeasset’s economic life; ; otherwise, it is depreciated over the otherwise, it is depreciated over the lease lease

termterm..

If title passes to the lessee at the enter or If title passes to the lessee at the enter or the lease term, or the lease contains a the lease term, or the lease contains a bargain purchase option, the asset is bargain purchase option, the asset is

depreciated over the depreciated over the asset’s economic lifeasset’s economic life; ; otherwise, it is depreciated over the otherwise, it is depreciated over the lease lease

termterm..

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-25

Depreciation by Lessee

At December 31, 2002, Matrix At December 31, 2002, Matrix prepares the following entry to prepares the following entry to

recognize depreciation expense for recognize depreciation expense for the year.the year.

GENERAL JOURNAL

Date Description Debit Credit

Dec 31 Depreciation expense 5,175 Accumulated depreciation 5,175

$25,87$25,8733

5 years5 years

= = $5,175$5,175

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

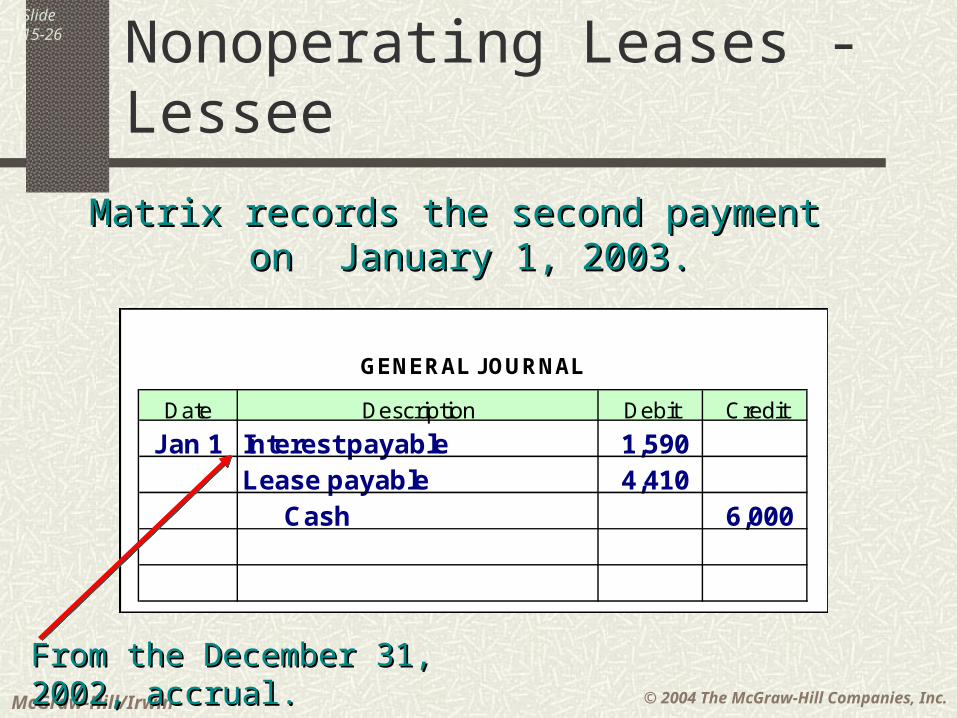

Slide15-26

Nonoperating Leases - Lessee

Matrix records the second payment on Matrix records the second payment on January 1, 2003.January 1, 2003.

GENERAL JOURNAL

Date Description Debit Credit

Jan 1 Interest payable 1,590Lease payable 4,410 Cash 6,000

From the December 31, 2002, accrual.From the December 31, 2002, accrual.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-27

Nonoperating Leases - Lessor

GENERAL JOURNAL

Date Description Debit Credit

Jan 1 Cash 6,000 Lease receivable 6,000

RentPro records the second receipt on RentPro records the second receipt on January 1, 2003.January 1, 2003.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-28

Now let’s Now let’s look at look at

sales-type sales-type leases.leases.

Nonoperating Leases

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-29

Sales-Type Lease

Because the lessor is a manufacturer or Because the lessor is a manufacturer or dealer, the FMV of the leased asset dealer, the FMV of the leased asset is not is not

equal to theequal to the Cost of the asset. Cost of the asset.

At inception of the lease, the lessor will At inception of the lease, the lessor will record the record the Cost of Goods SoldCost of Goods Sold as well as as well as

the the Sales RevenueSales Revenue (PV of MLP). (PV of MLP).

At inception of the lease, the lessor will At inception of the lease, the lessor will record the record the Cost of Goods SoldCost of Goods Sold as well as as well as

the the Sales RevenueSales Revenue (PV of MLP). (PV of MLP).

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-30

Sales-Type Lease

On 1/1/02, RentPro, Inc. signed a 3-year lease On 1/1/02, RentPro, Inc. signed a 3-year lease agreement with Matrix, Inc. for equipment. The agreement with Matrix, Inc. for equipment. The

lease calls for payments of $117,296 at the end of lease calls for payments of $117,296 at the end of each of the next three years.each of the next three years.

The equipment has a 5-year economic life, a fair value The equipment has a 5-year economic life, a fair value of $300,000 and cost to RentPro of $222,500. The of $300,000 and cost to RentPro of $222,500. The lease contains a $4,000 bargain purchase option. lease contains a $4,000 bargain purchase option.

RentPro requires a 9% return on leased equipment. RentPro requires a 9% return on leased equipment. Matrix has an incremental borrowing rate of 11%, but Matrix has an incremental borrowing rate of 11%, but

knows RentPro’s implicit rate. The collectability of knows RentPro’s implicit rate. The collectability of the MLP is certain and there are no costs yet to be the MLP is certain and there are no costs yet to be incurred by RentPro in connection with the lease.incurred by RentPro in connection with the lease.

On 1/1/02, RentPro, Inc. signed a 3-year lease On 1/1/02, RentPro, Inc. signed a 3-year lease agreement with Matrix, Inc. for equipment. The agreement with Matrix, Inc. for equipment. The

lease calls for payments of $117,296 at the end of lease calls for payments of $117,296 at the end of each of the next three years.each of the next three years.

The equipment has a 5-year economic life, a fair value The equipment has a 5-year economic life, a fair value of $300,000 and cost to RentPro of $222,500. The of $300,000 and cost to RentPro of $222,500. The lease contains a $4,000 bargain purchase option. lease contains a $4,000 bargain purchase option.

RentPro requires a 9% return on leased equipment. RentPro requires a 9% return on leased equipment. Matrix has an incremental borrowing rate of 11%, but Matrix has an incremental borrowing rate of 11%, but

knows RentPro’s implicit rate. The collectability of knows RentPro’s implicit rate. The collectability of the MLP is certain and there are no costs yet to be the MLP is certain and there are no costs yet to be incurred by RentPro in connection with the lease.incurred by RentPro in connection with the lease.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-31

Sales-Type Lease

This is a This is a sales-type leasesales-type lease because the because the agreement contains a bargain purchase agreement contains a bargain purchase option, the MLP will be collected, and no option, the MLP will be collected, and no further costs will be incurred by RentPro.further costs will be incurred by RentPro.

Matrix treats this as a Matrix treats this as a capital leasecapital lease because it because it contains a bargain purchase option.contains a bargain purchase option.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-32

Sales-Type Lease

Calculation of the lease payment.Calculation of the lease payment.

Fair value of asset 300,000$

End of period payment 4,000$

PV $1 factor 0.77218 (3,089)

Recovered through lease payments 296,911

PV annuity $1, n=3, i=9% ÷ 2.53129

Lease payment 117,296$

Fair value of asset 300,000$

End of period payment 4,000$

PV $1 factor 0.77218 (3,089)

Recovered through lease payments 296,911

PV annuity $1, n=3, i=9% ÷ 2.53129

Lease payment 117,296$

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-33

Sales-Type Lease

Lease Amortization TableLease Amortization Table

Asset Carrying Year Payment Interest Recovery Value

Initial value………………………………………….. 300,000$ 1 117,296$ 27,000$ 90,296$ 209,704 2 117,296 18,873 98,423 111,281 3 117,296 10,015 107,281 4,000

Totals 351,888$ 55,888$ 296,000$

Asset Carrying Year Payment Interest Recovery Value

Initial value………………………………………….. 300,000$ 1 117,296$ 27,000$ 90,296$ 209,704 2 117,296 18,873 98,423 111,281 3 117,296 10,015 107,281 4,000

Totals 351,888$ 55,888$ 296,000$

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-34

Sales-Type Lease - Lessor

Entry at inception of the leaseEntry at inception of the lease

GENERAL JOURNAL

Date Description Debit Credit

Jan 1 Lease receivable 355,888Cost of goods sold 222,500 Sales revenue 300,000 Unearned interest revenue 55,888 Inventory of equipment 222,500

($117,296 ($117,296 × 3) + $4,000 = $355,888× 3) + $4,000 = $355,888($117,296 ($117,296 × 3) + $4,000 = $355,888× 3) + $4,000 = $355,888

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-35

Capital Lease - Lessee

Entry at inception of the leaseEntry at inception of the lease

GENERAL JOURNAL

Date Description Debit Credit

Jan 1 Leased equipment 300,000 Lease payable 300,000

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-36

Sales-Type Lease - LesseeFirst payment First payment

GENERAL JOURNAL

Date Description Debit Credit

Dec 31 Lease payable 90,296Interest expense 27,000 Cash 117,296

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-37

Sales-Type Lease - LesseeRecord first year depreciationRecord first year depreciation

GENERAL JOURNAL

Date Description Debit Credit

Dec 31 Depreciation expense 60,000 Accumulated depreciation 60,000

$300,000 $300,000 ÷ 5 (economic life) = $60,000÷ 5 (economic life) = $60,000$300,000 $300,000 ÷ 5 (economic life) = $60,000÷ 5 (economic life) = $60,000

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-38

Sales-Type Lease - LessorFirst receiptFirst receipt

GENERAL JOURNAL

Date Description Debit Credit

Dec 31 Lease receivable 117,296 Cash 117,296

Unearned interest revenue 27,000 Interest revenue 27,000

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-39

Sales-Type Lease

On December 31, 2004, the end of the lease term, On December 31, 2004, the end of the lease term, Matrix exercises the BPO.Matrix exercises the BPO.

GENERAL JOURNAL

Date Description Debit Credit

Dec 31 Lease payable 4,000 Cash 4,000

Matrix, Inc.Matrix, Inc.

GENERAL JOURNAL

Date Description Debit Credit

Dec 31 Cash 4,000 Lease receivable 4,000

RentPro, Inc.RentPro, Inc.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-40

Let’s look at Let’s look at how we how we handle handle residual residual value.value.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-41

Residual Value

The residual value of a leased asset is an The residual value of a leased asset is an estimate of what its estimate of what its commercial valuecommercial value will will be at the end of the lease term. Let’s see be at the end of the lease term. Let’s see

how residual value impacts the accounting how residual value impacts the accounting for leases by both the lessee and lessor.for leases by both the lessee and lessor.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-42

Residual Value

The only impact on the lessee is The only impact on the lessee is the determination of the determination of depreciationdepreciation expense. The cost of the asset will expense. The cost of the asset will

be reduced by the estimated be reduced by the estimated residual value and depreciated residual value and depreciated

over the economic life of the asset.over the economic life of the asset.

Lessee Obtains Title to Leased Lessee Obtains Title to Leased Asset.Asset.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-43

Residual Value

In determining the lease payment, In determining the lease payment, the lessor will reduce the fair value the lessor will reduce the fair value of the asset by the of the asset by the present value present value of the residual valueof the residual value. The reduced . The reduced fair value becomes the value used fair value becomes the value used

to calculate the lease payment.to calculate the lease payment.

Lessor Retains Title to Leased Lessor Retains Title to Leased Asset.Asset.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-44

Residual Value

On January 1, 2002, RentPro, Inc. signed a 10-On January 1, 2002, RentPro, Inc. signed a 10-year direct financing lease with Matrix, Inc. for year direct financing lease with Matrix, Inc. for equipment. The lease requires end-of-period equipment. The lease requires end-of-period

payments. The equipment has a fair value and payments. The equipment has a fair value and cost to RentPro of $500,000. Title to the cost to RentPro of $500,000. Title to the

equipment is retained by RentPro and it is equipment is retained by RentPro and it is estimated that at the end of the lease the asset estimated that at the end of the lease the asset will have a residual value of $35,000. RentPro will have a residual value of $35,000. RentPro requires an 8% return on leased equipment.requires an 8% return on leased equipment.

Let’s calculate the lease payment!Let’s calculate the lease payment!

On January 1, 2002, RentPro, Inc. signed a 10-On January 1, 2002, RentPro, Inc. signed a 10-year direct financing lease with Matrix, Inc. for year direct financing lease with Matrix, Inc. for equipment. The lease requires end-of-period equipment. The lease requires end-of-period

payments. The equipment has a fair value and payments. The equipment has a fair value and cost to RentPro of $500,000. Title to the cost to RentPro of $500,000. Title to the

equipment is retained by RentPro and it is equipment is retained by RentPro and it is estimated that at the end of the lease the asset estimated that at the end of the lease the asset will have a residual value of $35,000. RentPro will have a residual value of $35,000. RentPro requires an 8% return on leased equipment.requires an 8% return on leased equipment.

Let’s calculate the lease payment!Let’s calculate the lease payment!

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-45

Residual Value

Calculation of the lease payment.Calculation of the lease payment.

Fair value of asset 500,000$

Residual value 35,000$

PV $1 factor, n=10, i=8% 0.46319 (16,212)

Recovered through lease payments 483,788

PV annuity $1, n=10, i=8% ÷ 6.71008

Lease payment 72,099$

Fair value of asset 500,000$

Residual value 35,000$

PV $1 factor, n=10, i=8% 0.46319 (16,212)

Recovered through lease payments 483,788

PV annuity $1, n=10, i=8% ÷ 6.71008

Lease payment 72,099$

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-46

Residual Value Guaranteed by Lessee

Lessee pays any difference between guaranteed Lessee pays any difference between guaranteed residual value and the appraised value.residual value and the appraised value.

On 1/1/02, RentPro, Inc. signed a 5-year direct financing On 1/1/02, RentPro, Inc. signed a 5-year direct financing lease with Matrix, Inc. for equipment. Matrix lease with Matrix, Inc. for equipment. Matrix

guarantees a residual value of $3,500. The lease guarantees a residual value of $3,500. The lease requires beginning-of-period payments. The requires beginning-of-period payments. The

equipment has a fair value and cost to RentPro of equipment has a fair value and cost to RentPro of $100,000. Title to the equipment is retained by $100,000. Title to the equipment is retained by

RentPro. The lease payment is based on a 8% return.RentPro. The lease payment is based on a 8% return.

Let’s calculate the lease payment!Let’s calculate the lease payment!

On 1/1/02, RentPro, Inc. signed a 5-year direct financing On 1/1/02, RentPro, Inc. signed a 5-year direct financing lease with Matrix, Inc. for equipment. Matrix lease with Matrix, Inc. for equipment. Matrix

guarantees a residual value of $3,500. The lease guarantees a residual value of $3,500. The lease requires beginning-of-period payments. The requires beginning-of-period payments. The

equipment has a fair value and cost to RentPro of equipment has a fair value and cost to RentPro of $100,000. Title to the equipment is retained by $100,000. Title to the equipment is retained by

RentPro. The lease payment is based on a 8% return.RentPro. The lease payment is based on a 8% return.

Let’s calculate the lease payment!Let’s calculate the lease payment!

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-47

Residual Value Guaranteed by Lessee

Calculation of the lease payment.Calculation of the lease payment.

Fair value of asset 100,000$

Guaranteed residual value 3,500$

PV $1 factor, n=5, i=8% 0.68058 (2,382)

Recovered through lease payments 97,618

PV annuity due $1, n=5, i=8% ÷ 4.31213

Lease payment 22,638$

Fair value of asset 100,000$

Guaranteed residual value 3,500$

PV $1 factor, n=5, i=8% 0.68058 (2,382)

Recovered through lease payments 97,618

PV annuity due $1, n=5, i=8% ÷ 4.31213

Lease payment 22,638$

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-48

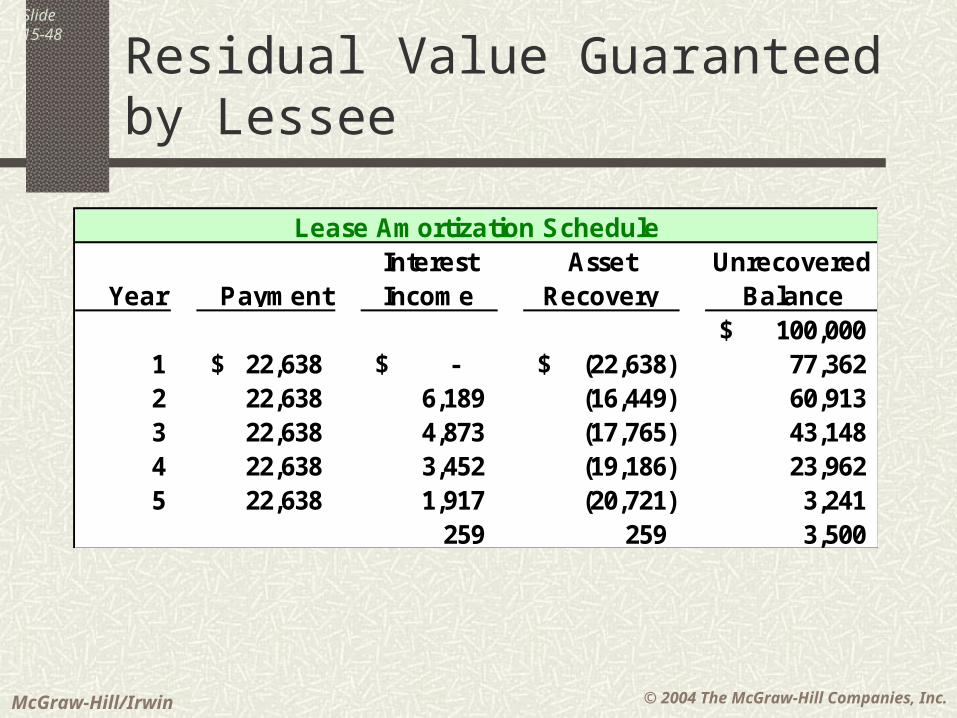

Residual Value Guaranteed by Lessee

Year PaymentInterest Income

Asset Recovery

Unrecovered Balance

100,000$ 1 22,638$ -$ (22,638)$ 77,362 2 22,638 6,189 (16,449) 60,913 3 22,638 4,873 (17,765) 43,148 4 22,638 3,452 (19,186) 23,962 5 22,638 1,917 (20,721) 3,241

259 259 3,500

Lease Amortization Schedule

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-49

Residual Value Guaranteed by Lessee

The accounting for this direct financing lease will be the The accounting for this direct financing lease will be the same as previously discussed. There are two same as previously discussed. There are two

exceptions:exceptions:

1.1. The lessee reduces the cost basis of the asset by $3,500 The lessee reduces the cost basis of the asset by $3,500 to calculate depreciation expense, to calculate depreciation expense, andand

2.2. If at the end of the lease term the appraised value of the If at the end of the lease term the appraised value of the asset is less than $3,500, the lessee must pay the asset is less than $3,500, the lessee must pay the difference between appraised value and guaranteed difference between appraised value and guaranteed residual value to the lessor.residual value to the lessor.

The accounting for this direct financing lease will be the The accounting for this direct financing lease will be the same as previously discussed. There are two same as previously discussed. There are two

exceptions:exceptions:

1.1. The lessee reduces the cost basis of the asset by $3,500 The lessee reduces the cost basis of the asset by $3,500 to calculate depreciation expense, to calculate depreciation expense, andand

2.2. If at the end of the lease term the appraised value of the If at the end of the lease term the appraised value of the asset is less than $3,500, the lessee must pay the asset is less than $3,500, the lessee must pay the difference between appraised value and guaranteed difference between appraised value and guaranteed residual value to the lessor.residual value to the lessor.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-50

Executory Costs

Executory costs include cost of ownership like Executory costs include cost of ownership like maintenance, insurance, taxes, and other costs. If maintenance, insurance, taxes, and other costs. If the lease agreement makes the lessee responsible the lease agreement makes the lessee responsible

for the executory costs, they are treated as for the executory costs, they are treated as expenses by the lessee.expenses by the lessee.

In some cases, the lessor pay executory costs, and In some cases, the lessor pay executory costs, and the lessee will reimburse the lessor through higher the lessee will reimburse the lessor through higher periodic lease payments. These costs are excluded periodic lease payments. These costs are excluded

in determining the minimum lease payment.in determining the minimum lease payment.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-51

Initial Direct Costs

Incremental costs incurred by the lessor in Incremental costs incurred by the lessor in negotiating and consummating a lease agreement.negotiating and consummating a lease agreement.

Operating LeasesOperating Leases −− Capitalize and amortize over Capitalize and amortize over the lease term by the lessor.the lease term by the lessor.

Direct Financing LeasesDirect Financing Leases −− Include as part of Include as part of investment balance.investment balance.

Incremental costs incurred by the lessor in Incremental costs incurred by the lessor in negotiating and consummating a lease agreement.negotiating and consummating a lease agreement.

Operating LeasesOperating Leases −− Capitalize and amortize over Capitalize and amortize over the lease term by the lessor.the lease term by the lessor.

Direct Financing LeasesDirect Financing Leases −− Include as part of Include as part of investment balance.investment balance.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-52

Contingent Rentals

Sometimes rental payment may be increased (or Sometimes rental payment may be increased (or decreased) at some future time during the lease decreased) at some future time during the lease

term, depending on whether or not some specified term, depending on whether or not some specified event occurs.event occurs.

Contingent rentals are not included in the minimum Contingent rentals are not included in the minimum lease payments. However, they are disclosed in the lease payments. However, they are disclosed in the

notes to the financial statements.notes to the financial statements.

Sometimes rental payment may be increased (or Sometimes rental payment may be increased (or decreased) at some future time during the lease decreased) at some future time during the lease

term, depending on whether or not some specified term, depending on whether or not some specified event occurs.event occurs.

Contingent rentals are not included in the minimum Contingent rentals are not included in the minimum lease payments. However, they are disclosed in the lease payments. However, they are disclosed in the

notes to the financial statements.notes to the financial statements.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-53

Lessee Disclosures

For capital leases, discloseFor capital leases, disclose Gross amount of assets recorded under Gross amount of assets recorded under

capital leases.capital leases. Future MLP in the aggregate and for each Future MLP in the aggregate and for each

of the five succeeding years.of the five succeeding years. Total minimum sublease rentals to be Total minimum sublease rentals to be

received in the future under noncancelable received in the future under noncancelable subleases.subleases.

Total contingent rentals.Total contingent rentals.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-54

Lessee Disclosures

For operating leases in excess of one year, For operating leases in excess of one year, disclosedisclose Future minimum rental payments required in the Future minimum rental payments required in the

aggregate and for each of the five succeeding aggregate and for each of the five succeeding fiscal years.fiscal years.

Total of minimum rentals to be received in the Total of minimum rentals to be received in the future under noncancelable subleases.future under noncancelable subleases.

For all operating leases, disclose rental expense, For all operating leases, disclose rental expense, with separate amounts for minimum rentals, with separate amounts for minimum rentals, contingent rentals, and sublease rentals.contingent rentals, and sublease rentals.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-55

Lessee Disclosures

Provide a description of the lessee’s leasing Provide a description of the lessee’s leasing arrangements including, but not limited to arrangements including, but not limited to The basis on which contingent rental payments The basis on which contingent rental payments

are determined.are determined. The existence and terms of renewal or purchase The existence and terms of renewal or purchase

options and escalation clauses.options and escalation clauses. Restrictions imposed by lease agreements, such Restrictions imposed by lease agreements, such

as those concerning dividends, additional debt, as those concerning dividends, additional debt, and further leasing.and further leasing.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-56

Lessor Disclosures

For sales-type and direct financing leases, For sales-type and direct financing leases, disclosedisclose

Components of the net investment in sales-Components of the net investment in sales-type and direct financing leasestype and direct financing leases

1.1. Future MLP to be received.Future MLP to be received.

2.2. Unguaranteed residual values.Unguaranteed residual values.

3.3. Unearned Interest Revenue.Unearned Interest Revenue. Future MLP to be received for each of the five Future MLP to be received for each of the five

succeeding fiscal years.succeeding fiscal years. Total contingent rentals included in income.Total contingent rentals included in income.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-57

Lessor Disclosures

For operating leases, discloseFor operating leases, disclose Cost and carrying amount of property on lease or Cost and carrying amount of property on lease or

held for leasing. held for leasing. Minimum future rentals on noncancelable leases Minimum future rentals on noncancelable leases

in the aggregate and for each of the five in the aggregate and for each of the five succeeding years.succeeding years.

Total contingent rentals included in income.Total contingent rentals included in income.

Provide a general description of the lessor’s Provide a general description of the lessor’s leasing arrangements.leasing arrangements.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-58

Balance Sheet & Income Statement

Lease transactions impact several financial Lease transactions impact several financial ratios:ratios:

1.1. Debt to equity ratio – Lease liabilities are Debt to equity ratio – Lease liabilities are recorded.recorded.

2.2. Rate of return on assets – Lease assets Rate of return on assets – Lease assets are recorded.are recorded.

Whether leases are capitalized or treated as Whether leases are capitalized or treated as an operating lease affects the income an operating lease affects the income statement and balance sheet. The most statement and balance sheet. The most impact is on the balance sheet.impact is on the balance sheet.

Lease transactions impact several financial Lease transactions impact several financial ratios:ratios:

1.1. Debt to equity ratio – Lease liabilities are Debt to equity ratio – Lease liabilities are recorded.recorded.

2.2. Rate of return on assets – Lease assets Rate of return on assets – Lease assets are recorded.are recorded.

Whether leases are capitalized or treated as Whether leases are capitalized or treated as an operating lease affects the income an operating lease affects the income statement and balance sheet. The most statement and balance sheet. The most impact is on the balance sheet.impact is on the balance sheet.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-59

Statement of Cash Flows

Operating leasesOperating leases - Rent expense is a cash - Rent expense is a cash outflow to the lessee and a cash inflow to outflow to the lessee and a cash inflow to the lessor.the lessor.

Capital & Direct Financing LeasesCapital & Direct Financing Leases – Lessee – Lessee reports interest expense as an outflow reports interest expense as an outflow from operating activities and principal from operating activities and principal payment as an outflow from financing payment as an outflow from financing activities. The lessor has a cash inflow activities. The lessor has a cash inflow from operating activities and investing from operating activities and investing activities.activities.

Operating leasesOperating leases - Rent expense is a cash - Rent expense is a cash outflow to the lessee and a cash inflow to outflow to the lessee and a cash inflow to the lessor.the lessor.

Capital & Direct Financing LeasesCapital & Direct Financing Leases – Lessee – Lessee reports interest expense as an outflow reports interest expense as an outflow from operating activities and principal from operating activities and principal payment as an outflow from financing payment as an outflow from financing activities. The lessor has a cash inflow activities. The lessor has a cash inflow from operating activities and investing from operating activities and investing activities.activities.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-60

Statement of Cash Flows

Sales-type leasesSales-type leases – The lessor recognizes – The lessor recognizes the interest revenue in the operating the interest revenue in the operating activities section of the statement and the activities section of the statement and the principal reduction in the investing principal reduction in the investing section. In addition, the lessor has sales section. In addition, the lessor has sales revenue and cost of goods sold revenue and cost of goods sold recognized in the operating activities recognized in the operating activities section.section.

Sales-type leasesSales-type leases – The lessor recognizes – The lessor recognizes the interest revenue in the operating the interest revenue in the operating activities section of the statement and the activities section of the statement and the principal reduction in the investing principal reduction in the investing section. In addition, the lessor has sales section. In addition, the lessor has sales revenue and cost of goods sold revenue and cost of goods sold recognized in the operating activities recognized in the operating activities section.section.

© 2004 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide15-61

End of Chapter 15

Related Documents