© 2004 HFI On the Web Introduction to Manufactured Housing August 10, 2005

© 2004 HFI On the Web Introduction to Manufactured Housing August 10, 2005.

Dec 25, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

© 2004 HFI On the Web

Introduction to Manufactured

Housing

August 10, 2005

© 2004 HFI On the Web

Before We Begin, Please…

• Put your phone on mute except when you want to ask a question

• Don’t put your phone on hold during the seminar

• Wait until the end of the seminar to print out the presentation

THANK YOU!

© 2004 HFI On the Web

Your Instructor Today

Kelly VespucciKelly VespucciSenior Underwriting

Consultant

© 2004 HFI On the Web

Your Subject Matter Expert

Virginia MahoneySenior Risk Manager

Single Family Business

© 2004 HFI On the Web

• Introduction & Definition of Manufactured Housing

• Review of Eligibility Parameters & Underwriting Requirements

• Examine new Appraisal Requirements • Explore Title Issues and Lien Requirements • Offer Servicing Guidance

Objectives for this Session

© 2004 HFI On the Web

• Manufactured homes make up approximately .5 % of our total book of business

• Volumes have been low, however, we have seen a significant increase in the past 2 years

Introduction & Definition

© 2004 HFI On the Web

• Mortgages secured by manufactured homes default at higher rates and have higher losses than mortgages secured by comparable site-built homes

• Our previous guidelines for manufactured housing allowed for mortgage characteristics that did not match the asset

Introduction & Definition(continued)

© 2004 HFI On the Web

Introduction & Definition(continued)

• Modifying our requirements and providing additional guidance for lenders will • Reduce the likelihood of default• Help ensure that borrowers have every

opportunity to become and remain successful homeowners

• Fannie Mae remains committed to providing liquidity to this important segment of the housing market

© 2004 HFI On the Web

Built on a permanent chassis and attached to a permanent foundation system

Definition of Manufactured Housing

© 2004 HFI On the Web

• Built in compliance with Federal Manufactured Home Construction and Safety Standards - June 15, 1976

• A one-family dwelling, legally classified as real property.

• The land must be owned as fee simple. Leasehold estates are not eligible.

• “On-Frame” modular homes built on a permanent chassis must meet the HUD Code to be eligible for delivery.

Eligibility Parameters

© 2004 HFI On the Web

Eligibility Parameters(continued)

• Multi-width may be located on an individual lot

in a co-op, condo or PUD

• Single-width manufactured homes are eligible

only if located in a co-op, condo, or PUD

• Project acceptance is required for

cooperative or condominium

PUD if a single-width manufactured home

© 2004 HFI On the Web

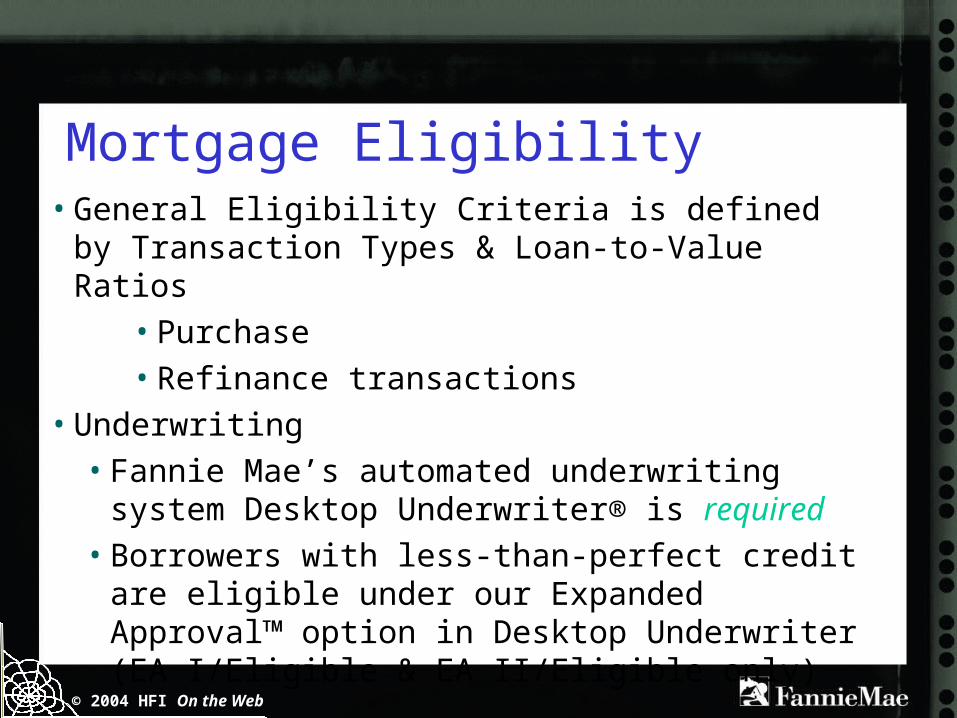

Mortgage Eligibility• General Eligibility Criteria is defined by Transaction Types

& Loan-to-Value Ratios

• Purchase

• Refinance transactions

• Underwriting

• Fannie Mae’s automated underwriting system Desktop Underwriter® is required

• Borrowers with less-than-perfect credit are eligible under our Expanded Approval™ option in Desktop Underwriter (EA I/Eligible & EA II/Eligible only)

© 2004 HFI On the Web

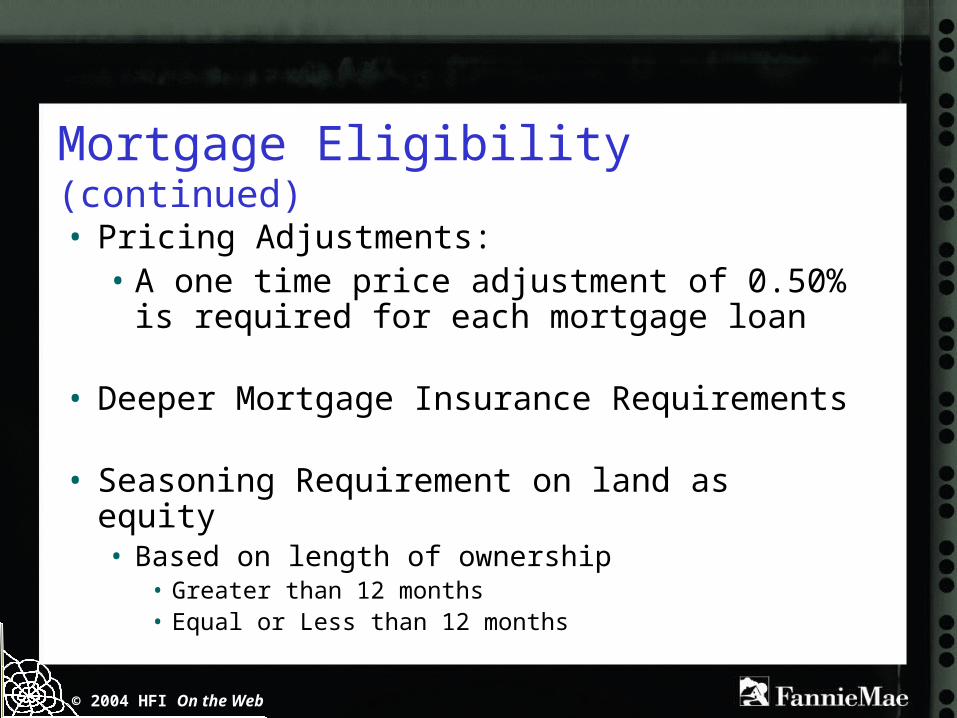

Mortgage Eligibility (continued)• Pricing Adjustments:

• A one time price adjustment of 0.50% is required for each mortgage loan

• Deeper Mortgage Insurance Requirements

• Seasoning Requirement on land as equity • Based on length of ownership

• Greater than 12 months• Equal or Less than 12 months

© 2004 HFI On the Web

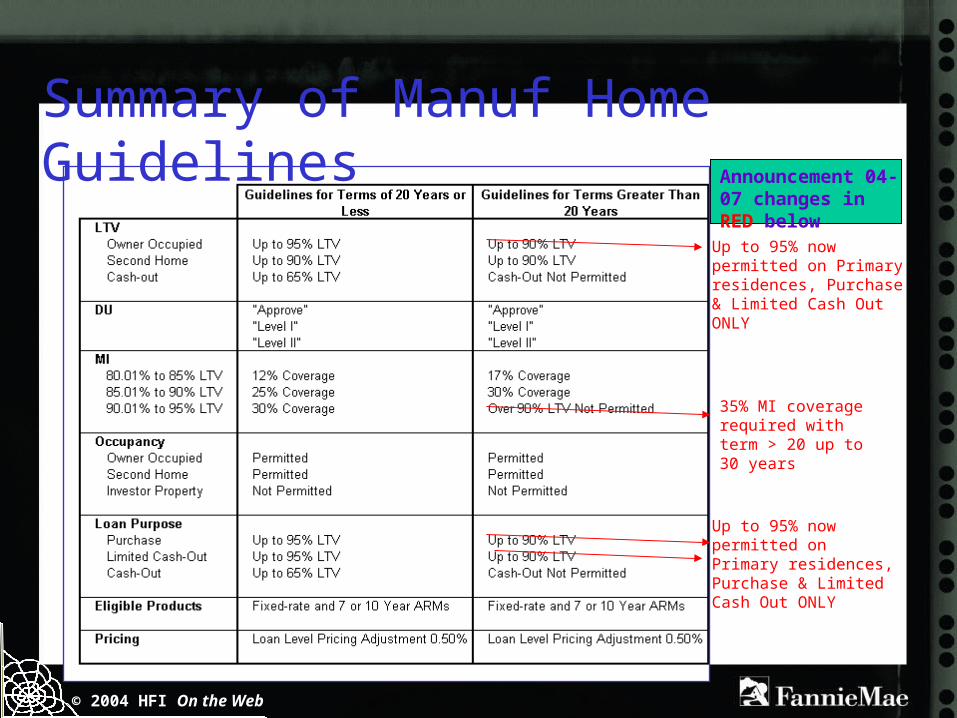

Summary of Manuf Home Guidelines

Up to 95% now permitted on Primary residences, Purchase & Limited Cash Out ONLY

35% MI coverage required with term > 20 up to 30 years

Up to 95% now permitted on Primary residences, Purchase & Limited Cash Out ONLY

Announcement 04-07 changes in RED below

© 2004 HFI On the Web

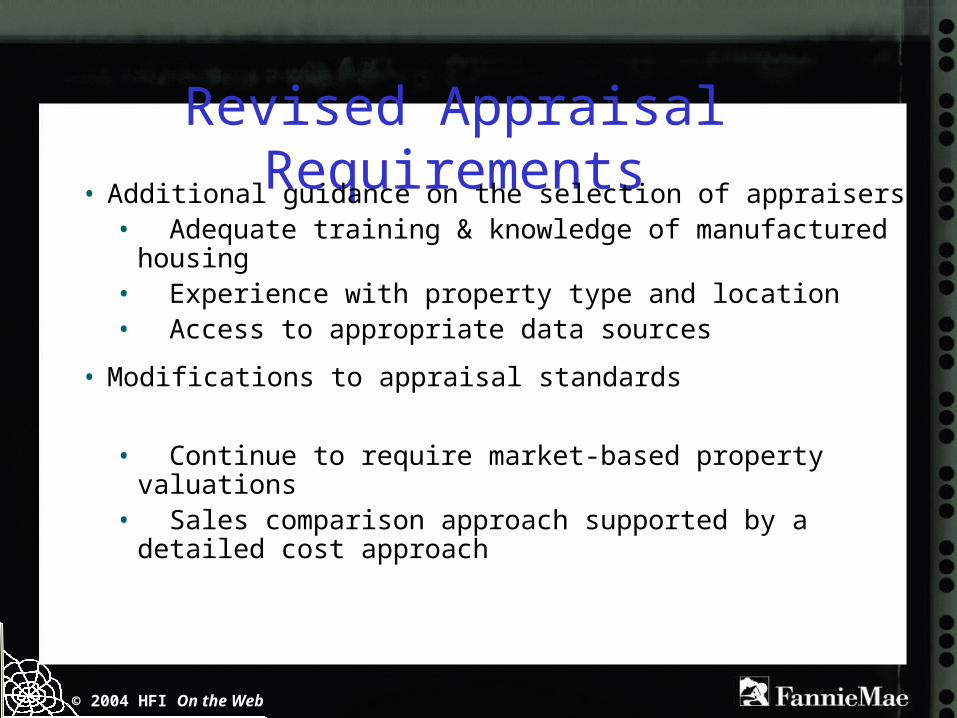

Revised Appraisal Requirements• Additional guidance on the selection of appraisers

• Adequate training & knowledge of manufactured housing • Experience with property type and location• Access to appropriate data sources

• Modifications to appraisal standards

• Continue to require market-based property valuations• Sales comparison approach supported by a detailed cost

approach

© 2004 HFI On the Web

Revised Appraisal Requirements (continued)

• Enhanced appraisal reporting requirements with new Manufactured Home Appraisal Report Addendum (Form 1004C)

• Addendum reinforces existing valuation and reporting requirements

• Addendum also implements revised requirements• New certifications by the appraiser

© 2004 HFI On the Web

Revised Appraisal Requirements (continued)

• Sources of manufactured housing data

• N.A.D.A. Manufactured Housing Appraisal Guide

• Marshall & Swift Residential Cost Handbook• Manufactured home dealer costs

© 2004 HFI On the Web

Title Issues and Lien Requirements• Overview

• Did not previously provide much guidance related to titling

• Previously, we required properties to be secured by a single lien on both the home and land

• Fannie Mae requires that manufactured housing loans be secured by a lien on real property

© 2004 HFI On the Web

Title Issues & Lien Requirements (cont’d)• Guidance on Fannie Mae’s website to assist lenders

• state-specific• does not relieve lenders of responsibility for reps and

warranties (Consult with your own legal counsel)• available on www.efanniemae.com

• Legal requirements covered in Announcement 03-06 • titling properties as real estate • use of standard instruments that support characteristics of

properties as real estate and specifies information that must be included on the security instrument (VIN #, Serial #, make model and size of unit)

• recorded affidavit from lender & borrower that home will be a permanent part of real property that secures the loan

© 2004 HFI On the Web

Title Issues and Lien Requirements (continued)

Link to Titling information Resources on www.efanniemae.com

http://www.efanniemae.com/singlefamily/mortgage_products/manufactured_housing.jhtml

© 2004 HFI On the Web

• Clarifies existing servicing requirements & addresses issues unique to manufactured home mortgages

• Stresses the need for servicers to identify mortgages as manufactured homes on their internal systems & to notify Fannie Mae if the servicer discovers a mortgage not delivered with the Special Feature Code

• Specifies collateral documents to be retained by servicer

Servicing Requirements

© 2004 HFI On the Web

Servicing Requirements (continued)• Addresses collection of personal property taxes if they

are assessed

• Addresses loan modifications completed as part of loss mitigation efforts

• Requires the servicer to notify the attorney in advance of foreclosure and bankruptcy proceedings that a property is a manufactured home

© 2004 HFI On the Web

Additional ResourcesLink to Titling Information Resources on www.efanniemae.com

http://www.efanniemae.com/singlefamily/mortgage_products/manufactured_housing.jhtml

Announcement 03-06

Link to Manufactured Housing Appraisal Addendum

http://www.efanniemae.com/singlefamily/pdf/1004c.pdf

© 2004 HFI On the Web

Questions?

Related Documents