© 2002 Pearson Education Canada Inc. Slide 14-1 Management Control Systems and Responsibility Accounting 14

© 2002 Pearson Education Canada Inc. Slide 14-1 Management Control Systems and Responsibility Accounting 14.

Dec 19, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

© 2002 Pearson Education Canada Inc. Slide 14-1

Management Control Systems and

Responsibility Accounting

14

© 2002 Pearson Education Canada Inc. Slide 14-2

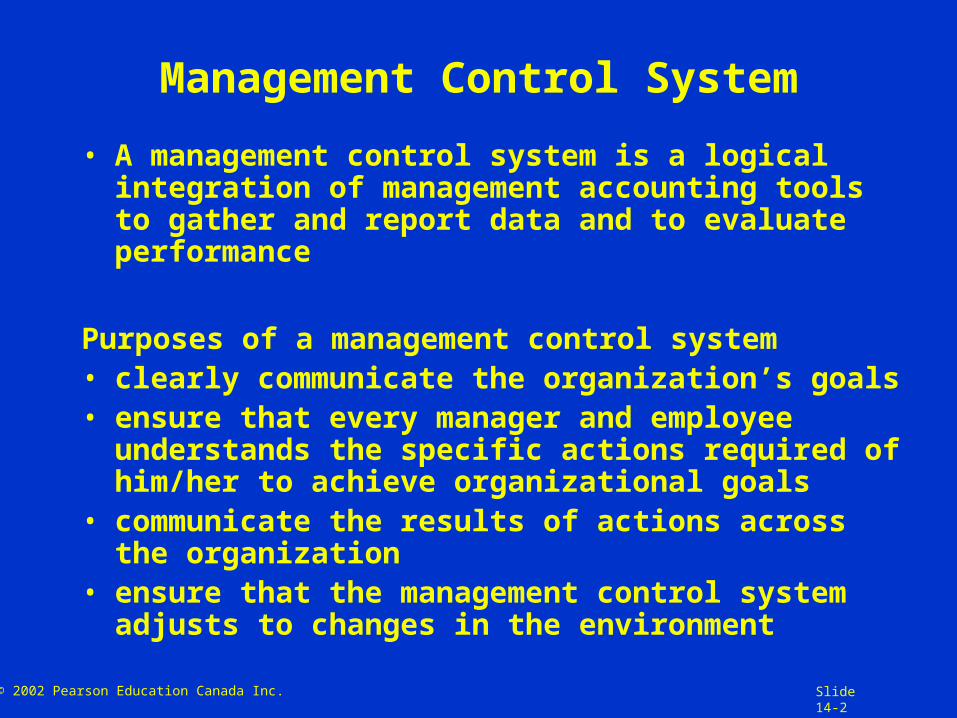

Management Control System

• A management control system is a logical integration of management accounting tools to gather and report data and to evaluate performance

Purposes of a management control system• clearly communicate the organization’s goals• ensure that every manager and employee

understands the specific actions required of him/her to achieve organizational goals

• communicate the results of actions across the organization

• ensure that the management control system adjusts to changes in the environment

© 2002 Pearson Education Canada Inc. Slide 14-3

Management Control System Steps

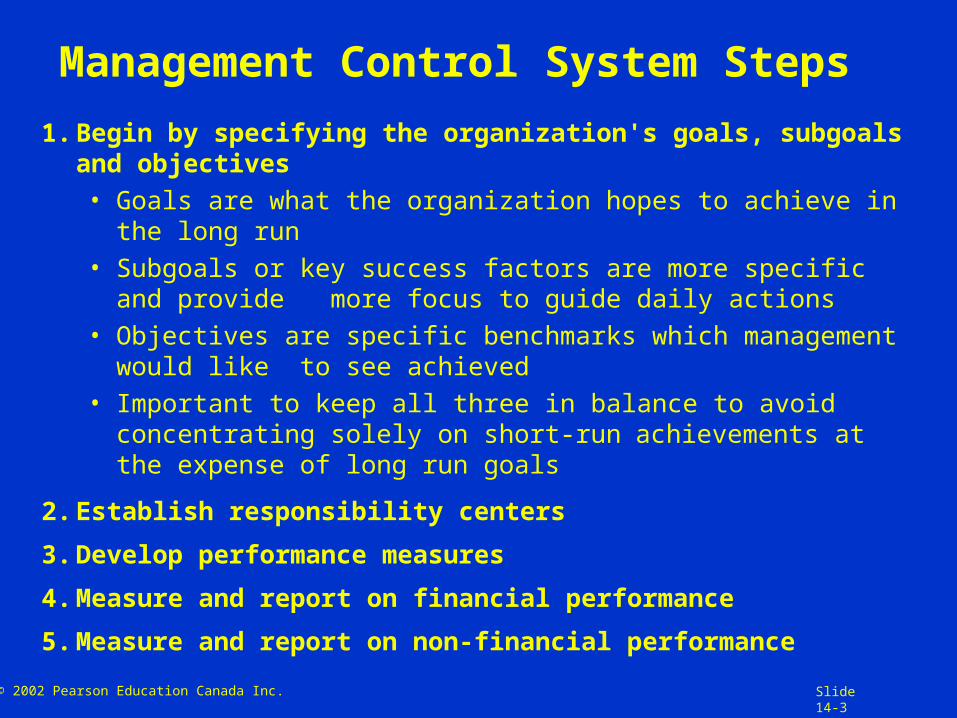

1. Begin by specifying the organization's goals, subgoals and objectives• Goals are what the organization hopes to achieve in the long run• Subgoals or key success factors are more specific and provide

more focus to guide daily actions• Objectives are specific benchmarks which management would like

to see achieved• Important to keep all three in balance to avoid concentrating solely

on short-run achievements at the expense of long run goals

2. Establish responsibility centers

3. Develop performance measures

4. Measure and report on financial performance

5. Measure and report on non-financial performance

© 2002 Pearson Education Canada Inc. Slide 14-4

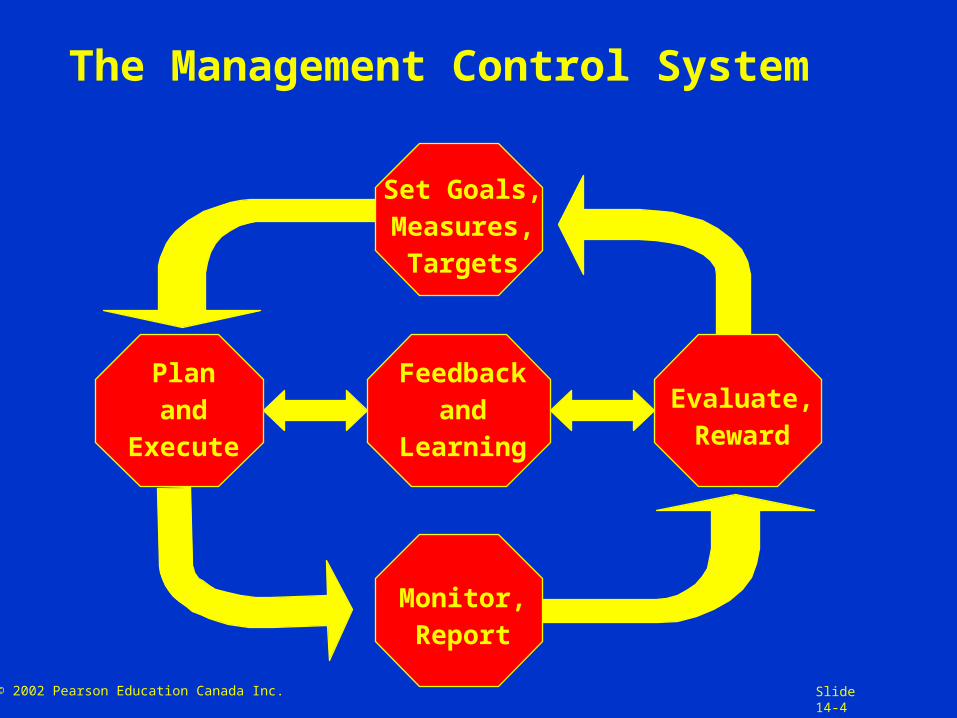

The Management Control System

Set Goals,Measures,

Targets

Feedbackand

Learning

Monitor,Report

Planand

Execute

Evaluate,Reward

© 2002 Pearson Education Canada Inc. Slide 14-5

Setting Goals, Objectives and Performance Measures

Top management develops organization-wide goals, measuresand targets. They also identify the critical processes.

Top management develops organization-wide goals, measuresand targets. They also identify the critical processes.

Top management and critical process managers developcritical success factors and performance measures.

They also specify objectives

Top management and critical process managers developcritical success factors and performance measures.

They also specify objectives

Critical process managers and lower-level managersdevelop performance measures for objectives.

Critical process managers and lower-level managersdevelop performance measures for objectives.

© 2002 Pearson Education Canada Inc. Slide 14-6

Forms of Organizational Structure

VPProduction

VPMarketing

VPHuman Resources

VPFinance

StaffFunctional

Staff

VPDivision B

VPDivision A

VPDivision C

President

Divisional

Functional VPs

DivisionalVPs

Matrix

A

B

C

Mkt. Prod. H.R. Fin.

President

President

© 2002 Pearson Education Canada Inc. Slide 14-7

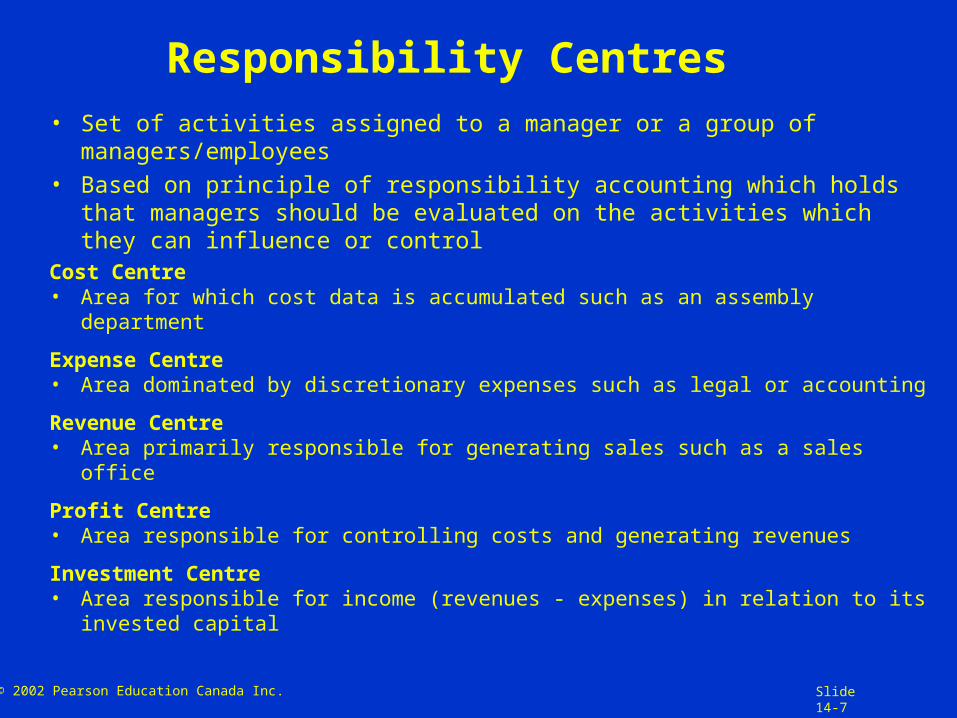

Responsibility Centres

• Set of activities assigned to a manager or a group of managers/employees

• Based on principle of responsibility accounting which holds that managers should be evaluated on the activities which they can influence or control

Cost Centre• Area for which cost data is accumulated such as an assembly department

Expense Centre• Area dominated by discretionary expenses such as legal or accounting

Revenue Centre• Area primarily responsible for generating sales such as a sales office

Profit Centre• Area responsible for controlling costs and generating revenues

Investment Centre• Area responsible for income (revenues - expenses) in relation to its invested

capital

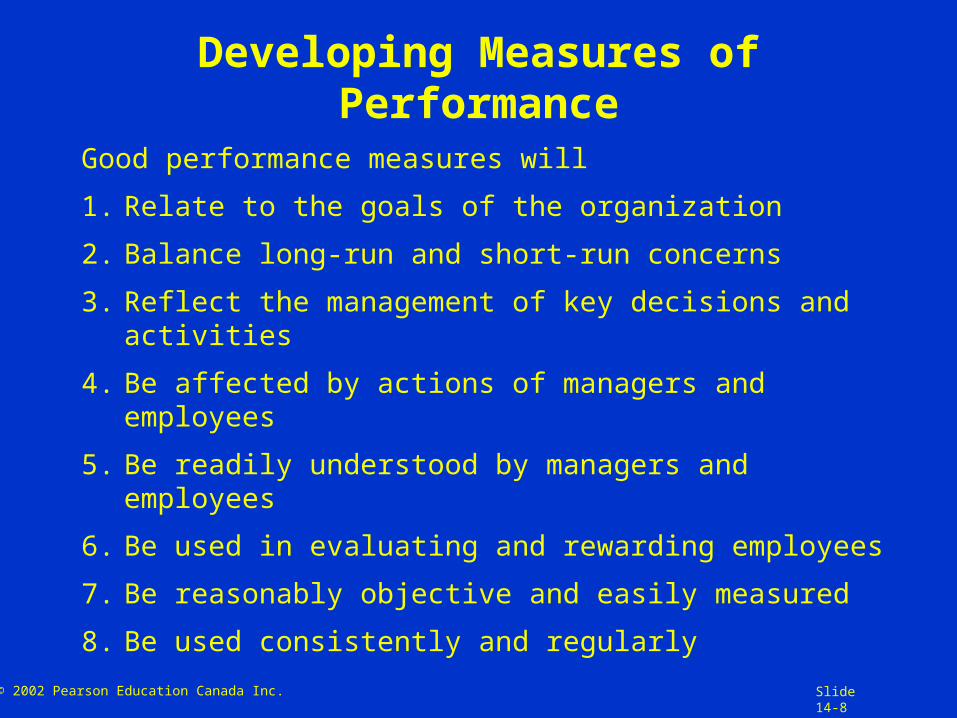

© 2002 Pearson Education Canada Inc. Slide 14-8

Developing Measures of Performance

Good performance measures will

1. Relate to the goals of the organization

2. Balance long-run and short-run concerns

3. Reflect the management of key decisions and activities

4. Be affected by actions of managers and employees

5. Be readily understood by managers and employees

6. Be used in evaluating and rewarding employees

7. Be reasonably objective and easily measured

8. Be used consistently and regularly

© 2002 Pearson Education Canada Inc. Slide 14-9

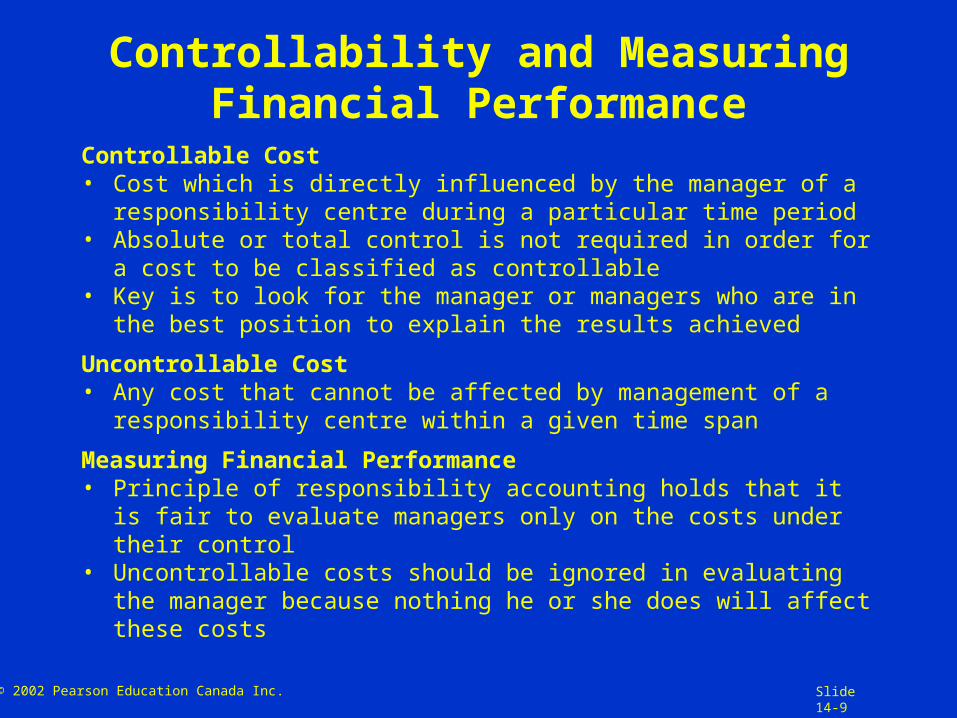

Controllability and MeasuringFinancial Performance

Controllable Cost• Cost which is directly influenced by the manager of a

responsibility centre during a particular time period• Absolute or total control is not required in order for a cost to be

classified as controllable • Key is to look for the manager or managers who are in the best

position to explain the results achieved

Uncontrollable Cost• Any cost that cannot be affected by management of a

responsibility centre within a given time span

Measuring Financial Performance• Principle of responsibility accounting holds that it is fair to

evaluate managers only on the costs under their control• Uncontrollable costs should be ignored in evaluating the

manager because nothing he or she does will affect these costs

© 2002 Pearson Education Canada Inc. Slide 14-10

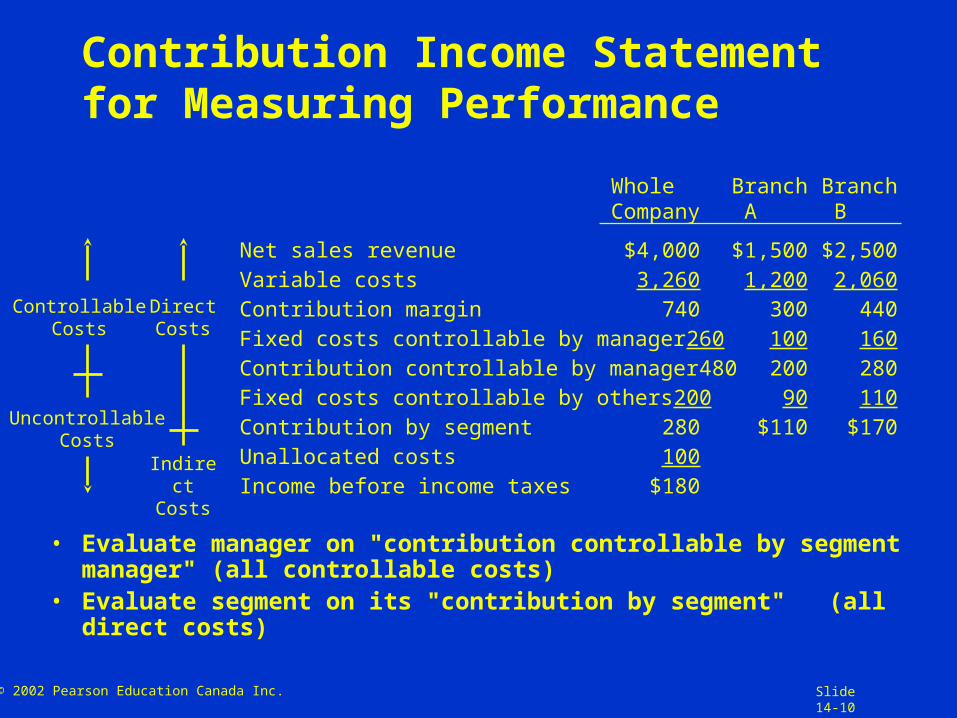

Contribution Income Statement for Measuring Performance

• Evaluate manager on "contribution controllable by segment manager" (all controllable costs)

• Evaluate segment on its "contribution by segment" (all direct costs)

Whole Branch BranchCompany A B

Net sales revenue $4,000 $1,500 $2,500Variable costs 3,260 1,200 2,060Contribution margin 740 300 440Fixed costs controllable by manager 260 100 160Contribution controllable by manager 480 200 280Fixed costs controllable by others 200 90 110Contribution by segment 280 $110 $170Unallocated costs 100Income before income taxes $180

ControllableCosts

DirectCosts

IndirectCosts

UncontrollableCosts

© 2002 Pearson Education Canada Inc. Slide 14-11

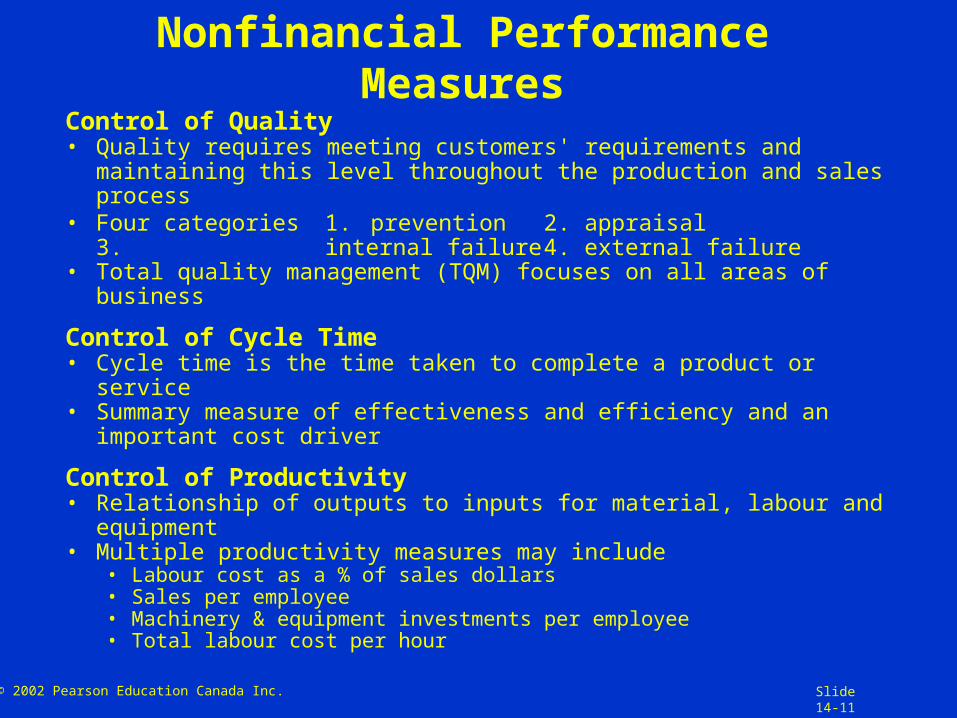

Nonfinancial Performance Measures

Control of Quality• Quality requires meeting customers' requirements and maintaining

this level throughout the production and sales process• Four categories 1. prevention 2. appraisal

3. internal failure 4. external failure• Total quality management (TQM) focuses on all areas of business

Control of Cycle Time• Cycle time is the time taken to complete a product or service• Summary measure of effectiveness and efficiency and an important

cost driver

Control of Productivity• Relationship of outputs to inputs for material, labour and equipment• Multiple productivity measures may include

• Labour cost as a % of sales dollars• Sales per employee• Machinery & equipment investments per employee• Total labour cost per hour

© 2002 Pearson Education Canada Inc. Slide 14-12

Successful Organizations and Measures of Achievement

CUSTOMER SATISFACTIONCUSTOMER SATISFACTION

BUSINESSS PROCESS IMPROVEMENTSBUSINESSS PROCESS IMPROVEMENTS

ORGANIZATIONAL LEARNINGORGANIZATIONAL LEARNING

FINANCIALSTRENGTH

FINANCIALSTRENGTH

© 2002 Pearson Education Canada Inc. Slide 14-13

Balanced Scorecard

• Performance reporting approach which links organizational strategy to actions of managers and employees

• Combines financial and operating measures• Links performance to rewards• Recognizes diversity in organizational goals

FinancialStrength

CustomerSatisfaction

Business ProcessImprovement

OrganizationalLearning

© 2002 Pearson Education Canada Inc. Slide 14-14

Management Control Systems in Service, Government and Nonprofit Organizations

• Control systems are more difficult to implement and maintain:• Outputs are more difficult to measure• Quality ratings are less clear

• Important to properly train and motivate employees to achieve organization's goals and consistent monitoring of objectives in accordance with critical subgoals

• Government and nonprofit organizations face further problems:• Goals and objectives are less clear• Professionals less receptive to control systems• Lack of profit measure makes measurements more difficult• Less pressure to improve from "owners"• Budgeting is more of a bargaining game to acquire additional funding and

less of a planning tool• Motivations and incentives of organizational employees are often

drastically different from for-profit organizations

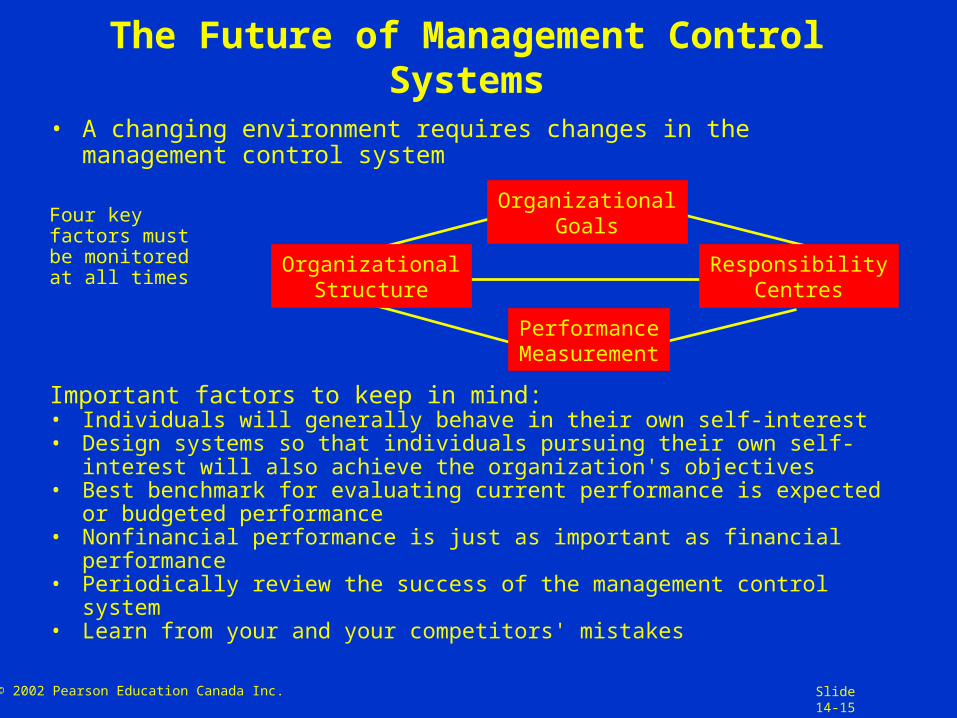

© 2002 Pearson Education Canada Inc. Slide 14-15

The Future of Management Control Systems

ResponsibilityCentres

OrganizationalGoals

OrganizationalStructure

PerformanceMeasurement

• A changing environment requires changes in the management control system

Four key factors mustbe monitoredat all times

Important factors to keep in mind:• Individuals will generally behave in their own self-interest• Design systems so that individuals pursuing their own self-interest will also

achieve the organization's objectives • Best benchmark for evaluating current performance is expected or budgeted

performance• Nonfinancial performance is just as important as financial performance• Periodically review the success of the management control system• Learn from your and your competitors' mistakes

Related Documents