© 2001 Prentice Hall 9-1 International Business by Daniels and Radebaugh Chapter 9 The Foreign-Exchange Market

© 2001 Prentice Hall9-1 International Business by Daniels and Radebaugh Chapter 9 The Foreign-Exchange Market.

Jan 15, 2016

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

© 2001 Prentice Hall 9-1

International Businessby

Daniels and Radebaugh

Chapter 9The Foreign-ExchangeMarket

© 2001 Prentice Hall 9-2

ObjectivesTo learn the fundamentals of foreign exchangeTo identify the major characteristics of the foreign-

exchange market and how governments control the flow of currencies across national borders

To understand why companies deal in foreign exchangeTo describe how the foreign-exchange market worksTo examine the different institutions that deal in foreign

exchange

© 2001 Prentice Hall 9-3

IntroductionFundamental difference between payment transactions

• Domestic transaction—use only one curency• Foreign transaction—use two or more currencies

Foreign exchange— money denominated in the currency of another group of nations

• Foreign-exchange market—made up of:– over-the-counter (OTC)

» commercial and investment banks» majority of foreign-exchange activity

– security exchanges» trade certain types of foreign-exchange

instrumentsExchange rate—price of a currency

• Number of units of one currency that buys one unit of another currency

• Exchange rate can change daily

© 2001 Prentice Hall 9-4

Foreign-Exchange InstrumentsSpot transactions —exchange rate quoted for transactions that

require either immediate delivery or delivery within two days• Spot rate— settlement rate for the transaction

Outright forward—exchange currency beyond three days at a fixed exchange rate

• Single purchase or sale of a currency for future delivery• Forward rate—settlement rate for transaction

FX swap—a simultaneous spot and forward transactionCurrency swaps—involve interest-bearing financial instruments

• Exchange of principal and interest payments• Options—the right but not the obligation to trade foreign

currency in the future• Futures contract—agreement to buy or sell a currency in

the future at a particular price

© 2001 Prentice Hall 9-5

The Foreign-Exchange MarketSize of foreign-exchange market

• $1.5 trillion daily in traditional instruments• $110 billion daily in other OTC and exchange-traded

instruments• Spot transactions are only 40%t of total transactions

U.S. dollar is the most important currency because it is:• An investment currency in many capital markets• A reserve currency held by many central banks• A transaction currency in many international commodity

markets• An invoice currency in many contracts• An intervention currency employed by monetary

authorities to influence their exchange ratesLondon—the biggest market for foreign exchange

© 2001 Prentice Hall 9-6

1,190

1,500

590

820

0

200

400

600

800

1000

1200

1400

1600

U.S

. dol

lars

(bi

llio

ns)

1989 1992 1995 1998

Average Daily Volume in World Foreign-Exchange Markets, 1989–1998

Years

© 2001 Prentice Hall 9-7

$350.90

$78.60

$81.70

$94.30

$148.60

$637.30

$139

$451.20

United States Hong Kong Switzerland Germany

Japan United Kingdom Singapore Others

Average Daily Volume of Foreign-Exchange Transactions

© 2001 Prentice Hall 9-8Hours

0

5000

10000

15000

20000

25000

30000

35000

40000

45000

100 300 500 700 900 1100 1300 1500 1700 1900 2100 2300

Ele

ctro

nic

co

nve

rsat

ion

s/ho

ur

Peak

Average

Circadian Rhythms of the FX Market

© 2001 Prentice Hall 9-9

Key Foreign-Exchange Terms for the Spot MarketBid—price at which traders are willing to buy foreign currencyOffer—price at which traders are willing to sell foreign currencySpread—difference between bid and offer price

• Profit margin for the traderDirect quote—the number of U.S. dollars per unit of foreign

currency• American terms—perspective of U.S. trader

Indirect quote—the number of units of foreign currency per U.S. dollar

• European terms—perspective of European trader– base currency—U.S. dollar– terms currency—other currency in exchange

Cross rate—exchange rate between non–U.S. dollar currencies

© 2001 Prentice Hall 9-10

The Forward MarketMost widely traded currencies

• British pound, Canadian dollar, French franc, German mark, Japanese yen, and U.S. dollar

• Many currencies do not have a forward market due to the small size and volume of transactions

Forward rate—the rate quoted for transactions after two days• Forward discount—the forward rate for foreign currency

is less than the spot rate• Forward premium—the forward rate for foreign currency

is greater than the spot rate

OptionsOption—the right but not the obligation to trade a foreign

currency at a specific exchange rate• Can be purchased OTC or from an exchange• Forward contract is cheaper but less flexible than an

option

© 2001 Prentice Hall 9-11

FuturesFutures contract—specifies in advance the exchange rate to be

used in exchanging currency• Tailored to the amount and time frame needed• Not as flexible as a forward contract and, therefore, is

less valuable

Foreign-Exchange ConvertibilityFully convertible currencies—government permits both

residents and nonresidents to purchase in unlimited amountsHard currency—currencies that are fully convertible

• Relatively stable and strongSoft currencies—currencies that are not fully convertible

• Typically currencies of developing countriesNonresident convertibility—foreigners can convert their

currency into the local currency and can convert back into their currency

© 2001 Prentice Hall 9-12

Governmental Restrictions on Foreign-Exchange ConvertibilityRestrictions used to conserve scarce foreign exchange

• Licensing—government regulates all foreign-exchange transactions

– those who receive foreign currency required to sell it to its central bank at the official buying rate

– central bank rations foreign currency• Multiple exchange-rate system—different exchange

rates set for different transactions• Advance import deposit—requires importers to

make a deposit with central bank covering price of goods they would purchase from abroad

• Quantity controls—limit the amount of currency that resident can purchase for foreign travel

Currency controls increase the cost of international business and reduce overall international trade

© 2001 Prentice Hall 9-13

How Companies Use Foreign ExchangeMost foreign-exchange transactions involve international

departments of commercial banks• Banks buy and sell foreign currency; banks collect and

pay money in transaction with foreign buyers and sellers• Banks lend money in foreign currency

Companies use foreign-exchange market for:• Import and export transactions• Financial transactions such as FDI

Arbitrage—purchase of foreign currency on one market for immediate resale on another market

• Arbitragers hope to profit from price discrepancy• Interest arbitrage—investing in debt instruments in

different countriesSpeculation—buying or selling foreign currency has both risk

and high profit potential

© 2001 Prentice Hall 9-14

Foreign-Exchange Trading ProcessCompanies work through their local banks to settle foreign-

exchange balances• Commercial banks in major money centers became

intermediaries for small banksMost foreign-exchange activity takes place in traditional

instruments • Commercial and investment banks and other financial

institutions handle spot, outright forward, and FX swaps• Foreign-exchange market made up of about 2,000 dealer

institutions worldwide• Most foreign-exchange takes place in OTC market

Dealers can trade foreign exchange:• Directly with other dealers• Through voice brokers• Through electronic brokerage systems

– Internet trades of currency are more popular

© 2001 Prentice Hall 9-15

Foreign-ExchangeBroker

OTCInterbank

Market

Major Banks(spot and forward

transactions)

SecuritiesBroker

SecuritiesBrokerSecurities Exchange

Client buys marks with $ U.S.

Client buys $ U.S. with marks

CME(futures)

PSE(options)

Structure of Foreign-Exchange Markets

© 2001 Prentice Hall 9-16

VoiceBrokers

Foreign-Exchange Dealers

Reuters EBS

MNE

Internet

AutomatedBrokers

Direct toInterbank

Counterparty

Foreign-Exchange Transactions

© 2001 Prentice Hall 9-17

Commercial and Investment BanksGreatest volume of foreign-exchange activity takes place with

the big banks• Top banks in the interbank market in foreign exchange

are so ranked because of their ability to:– trade in specific market locations– engage in major currencies and cross-trades– deal in specific currencies– handle derivatives

» forwards, options, future swaps– conduct key market research

• Banks may specialize in geographic areas, instruments, or currencies

– exotic currency—currency of a developing country» often unstable, weak, and unpredictable

© 2001 Prentice Hall 9-18

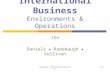

Bank 1. Citibank/Salomon Smith Barney 2. Deutsche Bank 3. Chase Manhattan Bank 4. Warburg Dillon Read 5. Goldman Sachs 6. Bank of America 7. JP Morgan 8. HSBC 9. ABN Amro10. Merrill Lynch

EstimatedMarket Share %

7.757.12

7.09

6.444.864.394.003.753.373.27

Best InLondon

13

2 6=

6=10=

4

Best InNew York

12

3

5=104

7

5=

Best InTrading

Euro/Dollar

21

3

7

6

549

Best InTrading

Euro/Dollar

13

2

6

4

5

8

Top OTC Commercial and Investment Banks inForeign-Exchange Trades

© 2001 Prentice Hall 9-19

Chicago Mercantile Exchange (CME)A not-for-proft corporation owned by its membersCreated the International Monetary Market (IMM)

• Deals primarily in futures contracts, CME futures contracts

• Ready market even with fixed maturity dates • Tend to be for small amounts

CME is losing business• Struggling to find a niche in currency markets

Philadelphia Stock Exchange (PHLX)The only exchange in the U.S. that trades foreign-

currency options• Offers standardized options and customized options• Provide greater flexibility and convenience than

futuresPHLX growing faster than the CME

Related Documents