1 ឯឧបដ គង់ �បុល រប ត ភរជ រ ត បាលលទារបន � កជាអគ� ៃបជាអគ�ជរ ប�បពជ គវលរង ៨:៣០ គល រ � ដ ៃថ�ល រ ២១ ែខ��ៈ ឆាំ២០១៤ នណរ ប ភ�ស រ ែថា ជងអ ភ� (Sofitel Angkor Phuketra) ខបដេរ បេរនំ ត ម�លផ�ស��ជំ� រ រ�ិបព�បពជ្ � ក មជេ ត រប រ ន�រឯឧបដ គង់ �បុល រប ត ភរជ រ ត បាលលទារបន � កជាអគ� ៃបជាអគ�ជរប �បពជ ជ�បមនភាទ� រ ឯឧប�ជាអគ�ង លររប-ជប�ររបគ�ជ រប លររប- ជប�ររប��បពជ ខបដេរ លររប-ជប�ររបម ត ាិ� ប ត ងនប� រ ៃបជាអគ�ជរប�បពជ ល-ល រ បំណងរ�ម �បនំបទប២០៧ ប ត ងបំណងាណរ ប្ � ក ែដា�មឧរប��ថវ តម ត ម�លប។ ក ត នច�រ� ផ ឯឧប� គង់ �បុល រប ត ភរជ រ ត បាលលទារបន � កជាអគ� ៃបជាអគ�ជរប �បពជបបំែដងបភវ ត នច�សាបមនំវប�បរ ឯឧប� លឧរ លរំវ ល-ល រ គង � � បំណងរ�ម �ប ប ត ង ឯឧប� ល-ល រ ថាដ ដ គំ នប� រ �បពជ ប ត ងភ�វ ត ប� ត �ំងជែដា បបជេ� ផ នភាទា � ងជងអ ត ម �លប។ ជាអគ�ជរប�បពជកដរ បា�� ផ �បពែដាបន ត នចារាងរភានំចភា�� ផ �បពៃនា � ង ាររលែដាកែាទ�ដមំបៃបនំចភ ាថវ តមកប ត ែដា� ត បនមនំច�រទងដរ ត នច ប ត ង � ត េ� វប� � ។ រនច � របា ជាអគ�ជរប�បពជ បគ�ជរបរំគនថាណ� ានំបទប៧ ��បពជ ខច�នំបទប ៧ នររប រ ាំ� ប ត ង��បពជខបដនំ បទប ២៣ លភំងរល។ ា � ង�ៈ�ា ៥ ឆ ា ំករបា ប�ង អគ� គ�ជរប�បពជ រភានំចភា�បពជៃនា � ងាររល ផ បឡ ផ ងកាំជរ ា � ងគ ឆា ំ២០០៩ នបប ១.៧៤៥ បលបេា (៤៣៦ លបដ�ល � ត រ ឆាំ ២០១០ នបប ២.០៨៩ បលបេា (៥២២ លបដ�ល � ត រ ឆា ំ២០១១នបប ២.៣៦០ ប ររប រ ាំ�៖ ៃថ�ល រ ២១ ែខ��ៈ ២០១៣ ជ� ជាអគ�ជរប�បពជ

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

ឯឧបដ គង �បល របត ភរជរ តបាលលទារបន�កជាអគ� ៃបជាអគ�ជរ ប�បពជ

គ វល រ ង ៨:៣០ គលរ�ដ ៃថ�លរ២១ ែខ ��ៈ ឆា ២០១៤ នណរ ប ភ�សរែថា ជងអ ភ � (Sofitel Angkor Phuketra) ខបដ េរ ប េរន តម �លផ�ស��ជ�ររ�បព�បពជ�ក មជេតរបរន�រ ឯឧបដ គង �បល របតភ រជរ តបាលលទារបន�កជាអគ� ៃបជាអគ�ជរ ប�បពជរ ជ�បមនភាទ �រ ឯឧប�ជាអគ�ង លររប-ជប�ររបគ�ជរ ប លររប-ជប�ររប��បពជ ខបដ េរ លររប-ជប�ររបម តា�រ បតងនប�ររ ៃបជាអគ�ជរ ប�បពជរ ល- ល រ បណងរ �ម�បនបទប២០៧ បតងបណងាណរ ប�ក ែដា�មឧរប� �ថវ តម

តម �ល ប។ កតនច�រ �ផ រឯឧប�រគង �បល របតភរជរ តបាលលទារបន�កជាអគ� ៃបជាអគ�ជរ បរ

�បពជបបែដងបភវតនច�ស ាបមន វប�បរ ឯឧប� លឧញារ លរ វរ ល- ល ររ គង�� រ បណងរ �ម�បរ បតង ឯឧប� ល- ល រ ថា ដដគរ នប�រ�បពជរ បតង ភ�វតប�ត�ងជ ែដាបបជ េ� ផនភាទ ា�ងជងអ តម �ល បរ។

ជាអគ�ជរ ប�បពជកដរបា� �ផ�បពែដាបនតនចារ ាងរភានចភ ា� �ផ�បពៃន ា�ង

ារ រ លែដាកែាទ�ដម បៃបនចភ ាថវ តមកបត ែដា�តប ន មនច� រ ទង ដរ តនចរ បតងរ

�តេ� វប��។ រនច�របា ជាអគ�ជរ ប�បពជ បគ�ជរ បរគ នថា ណ� ានបទប៧ ��បពជ

ខច� នបទប ៧រ នររបរា �របតង��បពជ ខបដនបទបរ២៣រលភងរ ល។រ

ា�ង�ៈ �ារ ៥រ ឆា ករបា ប�ង អគ�គ�ជរ ប�បពជ រភានចភ ា�បពជៃនា�ងារ រ លរ ផប ឡផងកាជររ ា�ង គរ ឆា ២០០៩រ នបប ១.៧៤៥ បលប េា (៤៣៦រ លបដ�ល� ត រ ឆា ២០១០រ នបប ២.០៨៩ បលប េា (៥២២រលបដ�ល� ត រ ឆា ២០១១រ នបប ២.៣៦០ ប

ររបរ ា �៖រៃថ�លររ២១ ែខ � �ៈ ២០១៣រ ជ�រជាអគ�ជរ ប�បពជ

2

លប េារ(៥៩០រលបដ�ល� ត រឆា ២០១២រ នបប ២.៩៩៧ បលប េា (៧៤៩រលបដ�ល� តរ �ផបដង ១០០.៣%រៃបែបម បតងរឆា ២០១៣ បរ នបប ៣.៥២៥ បលប េា (៨៨១រលបដ�ល� ត រ �ផបដង ១០១.៨%រៃបែបម ។រាតបក ចផ ប ឃផថា�ង�ៈ �ារ៥រឆា ប�ង បរអគ�គ�ជរ ប�បពជ បប េសផឲនចភ ាថវ តមកបត ផប ឡផងកង លសដង ។រ រផ រ�រ េេរ ា�ង�ៈ �ារ១២ ឆា ប�ង អគ�គ�ជរ ប�បពជ រភានចភ ា�បពជ ផប ឡផងកង ១០ដងរ(ឆា ២០០១ នបប ២៩២ បលប េា (៧៣រ លបដ�ល� ត រ �ផរ ១.៨%រ ៃបរ GDP ឆា ២០១២ នបបរច ២.៩៩៧ បលប េា (៧៤៩រលបដ�ល� ត ររ �ផរ៥.១៥%រៃបរGDP បតងរឆា ២០១៣ បរ នបបរច ៣.៥២៥ បលប េា (៨៨១រលបដ�ល� ត ររ �ផរ៥.៧៣% ៃបរGDPរ។ ជ�ែឡា�ងឆា រ២០១២របតង២០១៣រ រផ ររក �កណន�ក បបលលទាងបភវ ប�បដ�លដ របបរ បតងម េរន ប ឆា បះ ជ�រ ជាអគ�ជរ ប �បពជបបរភានចភ ាបប ាផ ែបម�រឆា ករាបា ។រ នចភ ាែដា នបប បទ�នាេ រចកងរ ៨៥%រ រភា ជ�គ�ជរ បារ ាងជា ករ�បពេរ ែដាកគ�ជរ បប ទ�ា�ងន ណគ�ជរ បងរ ៧រ ៃបជាអគ�ជរ ប�បពជរ ែដាបបបតង��ង េសផមារ ាង បតងរភា�បព ាផជាករ�បពេនបទបរច ២.៧៤២ �ប ។

ការ�ង បរ ាគបប�រមជ នរ បភវែចលង �ររ េរ រជរ តបារ ទង ដរតនចរ

បតង�តេ� វប��របតងជាអគ�ជរ ប�បពជរា�ង គបប�រមប លរ ង �ល�ដងរ រសេម�ចនាយករដមម�ន�

�ងករដមម�ន�យសសងេសរដយចច��ងងករ��វត��បតងកែ��ផ ងែដរ ៃបមជប�វប�រ ង ង រខងទបបភវ�វ តេរ ែច

លងមារ ាង�តេ� វប���រចៈែដារសេម�ចអគ�មហេសននវ�េវេត ង�� ែស� គ�ដរ នប�រ ៃប�កណន�ក បបរម ជឲជប�វប��ង�រ ដផែខេាភ ឆា ២០០៤ ែដាា�ង គជាអគ�ជរ ប

�បពជ បបជ នបភវែបម�ន�រ ខ�ទបា�ងមែាជ បាប ប�� �ផ�បព បតងម�ងដងដរ

បា� �ផ�បព ទ បម�ងដង�ងរម�ា វដាជាករ�បពឲមបែបាល ជប�វប��វ តេរ�ររងន

ជាករ�បពតប ប�នពរ ជ�បប េសផមរច�� រណ� ាករករ� ន នប�រ�បពជរ�ងជា ករ�បពរ

ឲបប�ានព ជ�រនពរបតងរលរេ�បដតគគដរ�រ�បពជ តលព បតងជណនរ ដរបា� �ផ�បពរ តលព បតង

មប�ស តនចរ ជាករ�បពរក ដផរ។ា។

ប�ងរ ររជាអគ�ជរ ប�បពជ នបប ការ�ា�ងនតនចរភានចភ ា�បពរភបដររ ង

ណះ ជ� កេនបនច� នខសបទ�នបទបរ ែដាបវ េសផមែលងករបដរគន ររ ដភនកែចលងែា រ

3

នពររដរបា� �ផ�បពរ�ងដងជតបាតនចាលរបតងប� ន�រ ជ��តបតបឲ ឃផ�បទ�នបទបតបបរជប�

វបដបបបដបវបភវនពរ បតងរលរេ�បដតគគដរ�រ�បពជេន ឡផ� ែដាបវឲជាអគ�ជរ ប�បពជ របដ

�ងដងម ជប�វបដែបម�ន�ែចលងដរបា� �ផ�បពរែប� បកលអ �ងដងមជរជាករ�បព

ជ�រនពររ បតងរលរេ�បដតគគដរ�រ�បពជ��ៈម េរន តម �លរ បតង មផ�ស���រ�បព��បន

បរ បតង�ងដងវ តរបម�ររងន ជា ករ�បពែដាតប ប�នពររ ដផ រឲជាករ�បពបមលលទាខ�បវ

ន មប�សតនចរ ខ�ទប។រ លបនដបដង គែដរ ជាអគ�ជរ ប�បពជបបបតង��ងខតបខ�� រ�ភាបាបតបនបដរ�បព

ជឲម� �កជា�ា វដាជាករ�បពរ បតង�ងដងមជប�វបដ រាេនវ តកង ររវៈនបដរ�បពជ ដផ ររ ងផផបម

រឿល�នតបដ�រ�រចៈរប ឲរ� បាប ប�ែចលង �ររ ររ រជរ តបា ជចបដតលរ៥រ

ែដាបរសេម�ចអគ�មហេសននវ�េវេត ង�� ែស� កគ�ដរ នបដររ។

ដផ ររ ងផផបមលលទាខ�បវរ រ ងផផបតនច�របតរបដតមរបតង�ាបភវរ បឿល�នតបដរ កទ�ជាអគ�ជរ បរ�បពជររ �ម�បបវបមប�ស តនចដភនង មរ៖

១. រផលភល�ប� ន�បតង�ាបភវ�បនប�បនន តនចម�បពដាជាអគ�ជរ ប�បពជ។

២.បវបម ឆ�ផ�បរ ជ� �� បង បតងនា ន ម� ទរ នបដរ�បពជ។

៣.�មកទ�ជាអគ�ជរ ប�បពជ ដផ រ ចបបភវរ�� បតងវ តេរ�នដ ដផ រ ជ��បភវរ�� តបរបា ។

៤.បវ�ា�បនបឲប �ា វលជាអគ�ជរ ប�បពជ ា�ងចរ ែដារ�ម�ប��ប�បនប ែដា ាផ � ជ�ជាអគ�ជរ ប�បពជ ដផ រវ តេរទ�ែដាបម�ារងងង។

៥.�មក ទ�ជាអគ�ជរ ប�បពជ ដផ រ ដ ណ�� ទ�ែដាបម�ា រន នច� ន បវរ រេវងរបដបរបតវ តេរ ទប�លម។

៦.បវ រេវងបភវម ាផ � ឬលលទា�បភវម ាផែាង�បពែដា��បែនងា�ងនពរ បតងរលរេ�បដត គគ�រ�រ�បពជ។

៧.របវជប�វបដ�បរបតវ តេរ បតង�បដមែដាបបឯន� ន �ា េសផមកទ�ជាអគ�ជរ ប�បពជ។ ម េរន ឡផងបភវ តម �លដរ�ររ�បព�បពជ�ករ ដាជាករ�បព រចរ ២០៧រ �ប

ែដាបលរ�ងររវ� នា�ង ខបដ េរ តម មនភាទ នបទបរ ៤០០ គ ា�ង បារចង�ងរ បភវម

�ាដដងឲបបលភាលភល�បភវារលរេ�បដតដរ�រ� �ផ�បពរ បតង�ងដងបភវម ប�របតរបដតនពរ ង ប ែដា

កមប�ស តនច បតបបបរ ជាករ�បព មដភនកដរបា� �ផ�បពរ។រ តម �ល បរ �ដ បប ាផមជប�

វបដរ ល�បពបាទ�នបទប ទ ប៖រ �ត រ រ�គ�រចៈរ �ា នរ ាផបៃ�រែប�រ

�បព ាផប រេវបផរបតង�បព ាផបន ចរ�ឆា ែដារ�ម�បងជ ឲបបនព ល ។

��ៈ តម �លៃថ� បរ ជាអគ�ជរ ប�បពជង ដ រ បតង រឿកថ បណងរ �ម�បងជ

លលទាបបន ចដដងថ�រារែប� លេប ដផ រកល�បា�ងម� ទជប�វបដបបបដបវបភវនពរ បតងរលរេ�បដត ដរ�រ�បព

ជ បតងបបលលទាាលព ាាទកលរ �នតបដរ។

អគ�នាយកដា� នពន�ដារ

រពះរជណណចររ រត សារពចណព

អគ�ាណកដ រពក� ណសសងសសដណតជចត ត�រ��តរ

ឧេទ�សនេេដ : ងលណង េស សខ

អនរបនាននាេខេពន�េសរខរ

ឣណ�ងលើ� ណខង (េសរខរ ៃថ�ទ២១ ែពក�ៈ ឆា ២០១៤ )

មតើ

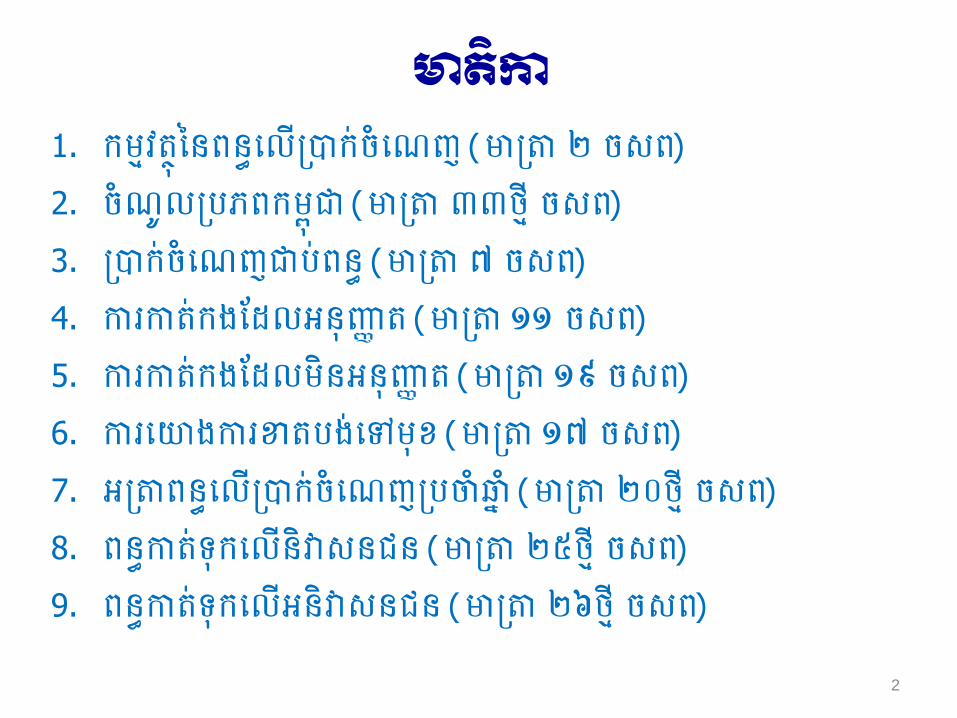

១.ចរោ នងរទរប�ន�ននាេខ ២.នដនដ ៣.អរតកខ នងេនលផ�នោផ�ងោ ៤.កខគណនកោតកខ ៥.កខរងោកោតកខ ៦.េទសទណទ

2

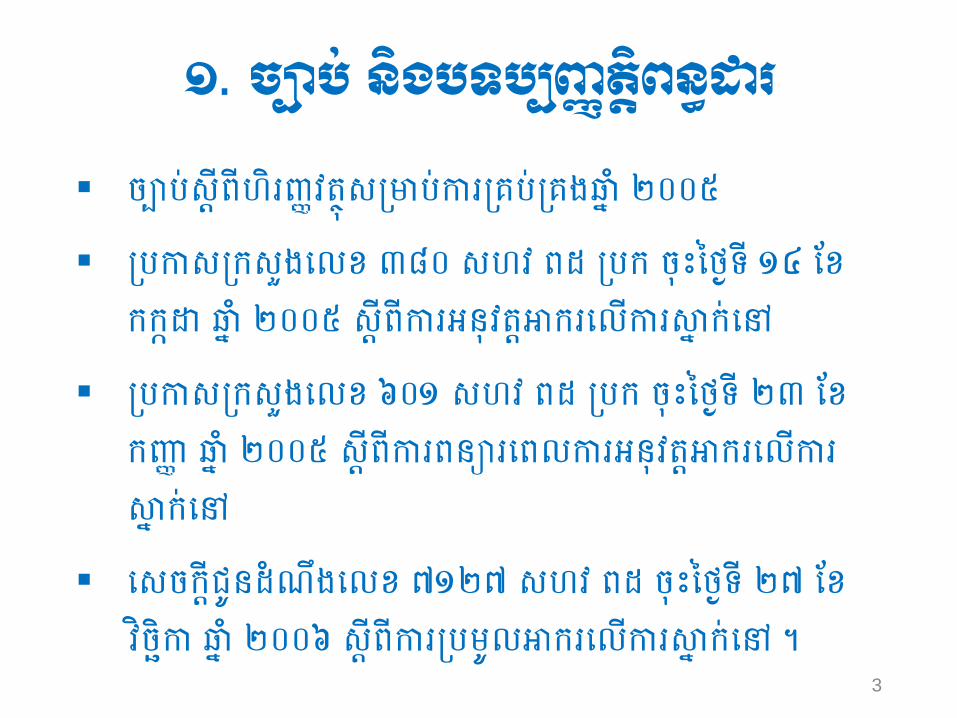

១. ជបខតបងបទរ��តរពក�

ចរោស� នពខប��នវតសសរោកខគរោគងឆា ២០០៥

រកសកសសងេលព ៣៨០ សព� នដ រក ចៃថ�ទ ១៤ ែព កក�េ ឆា ២០០៥ ស� នកខអន�ន�តកខេលលកខាា កោេ�

រកសកសសងេលព ៦០១ សព� នដ រក ចៃថ�ទ ២៣ ែព ក�� ឆា ២០០៥ ស� នកខននពខេនលកខអន�ន�តកខេលលកខ ាា កោេ�

េសចក�ជនដណងេលព ៧១២៧ សព� នដ ចៃថ�ទ ២៧ ែព ��ច�ក ឆា ២០០៦ ស� នកខរលតកខេលលកខាា កោេ� ា

3

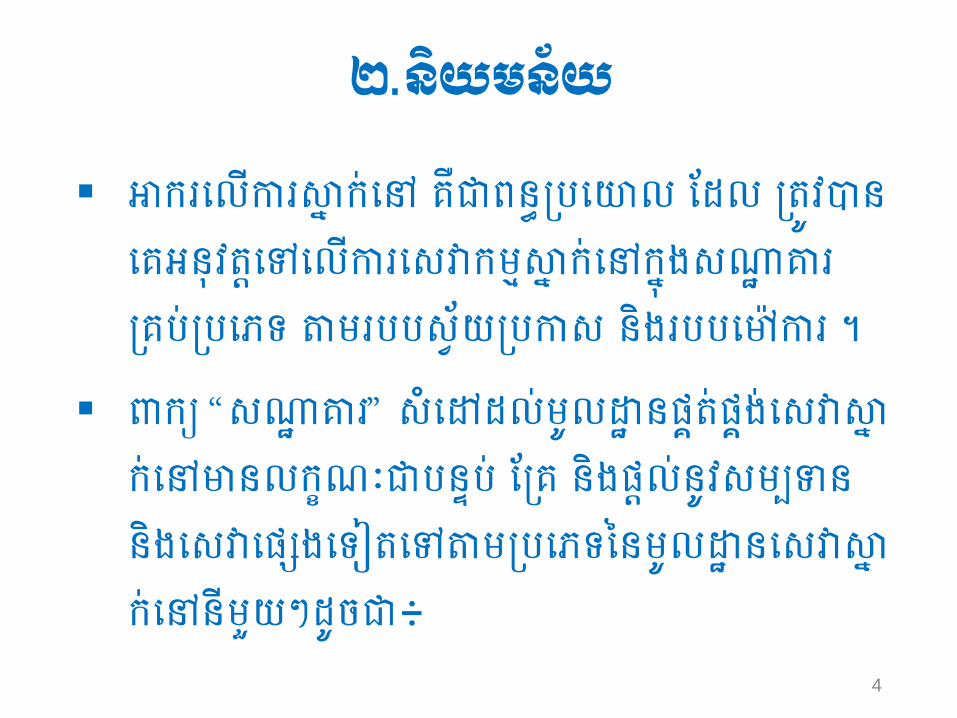

២.តច

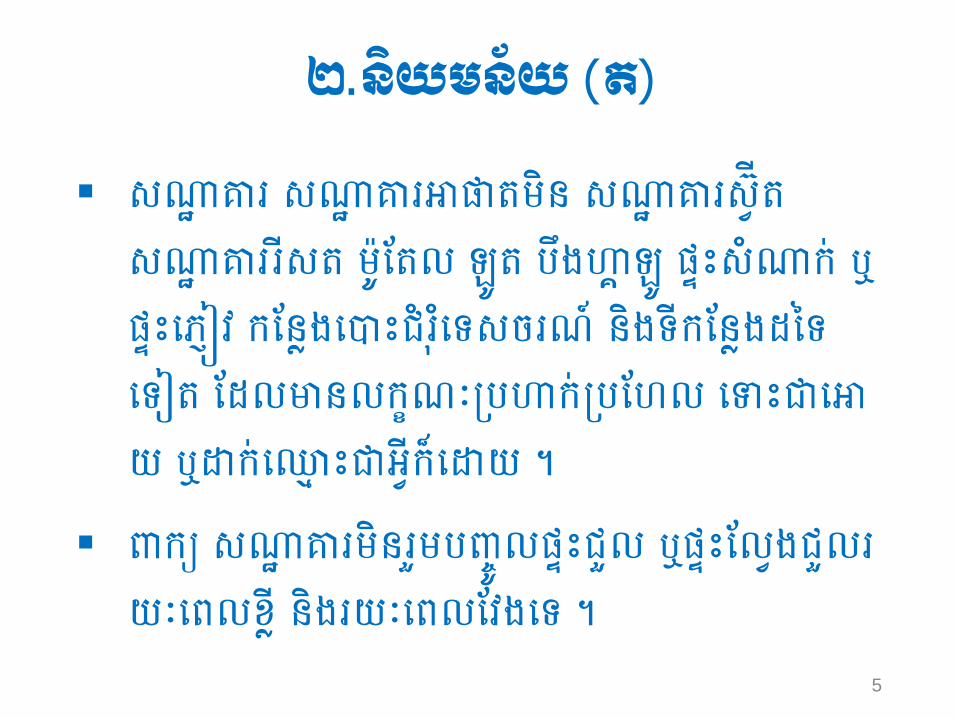

តកខេលលកខាា កោេ� គេននារេពល ែដល នល�នេគអន�ន�េ�េលលកខេសេកាា កោេ�កាតងសក� �ខគរោរេបទ រខររសរ ដរកស នងខររេនកខ ា

ពក “សក� �ខ” សេ�ដលោលេ� នផ�នោផ�ងោេសេាាកោេ�សនលកលណៈេរន�រោ ែគ នងផ�លោន�សទន នងេសេេផផងេទរនេ�ររេបទៃនលេ� នេសេាាកោេ�នសដៗដចេ

4

២.តច()

សក� �ខ សក� �ខត�នន សក� �ខសរ សន សក� �ខខសន ែនល តលន រងប� តល ផ�សកកោ ផ�េប��� កែន�ងេជខរេទសចខណរ នងទកែន�ងដៃទេទរន ែដលសនលកលណៈរបកោរែពល េទេេតដ េកោេេ េអរកអេេដ ា

ពក សក� �ខនខសរបមលលផ�ជសល ផ�ែលរងជសលខដៈេនលព� នងខដៈេនលែ�ងេទ ា

5

៣.អរឣណ�តងរង�ខង�ខ

តកខេលលកខាា កោេ� នល�នកណនោដករអរ ២% (នខភគខដ) េលលៃថ�រន�រោាា កោេ�កាតងសក� �ខ េេដខសរបមលលទងននាតកខ នងរន�តកេសេេផផងៗ (Service

Charge) េលលកែលងែនតកខេលលនៃ�រែនវ នងតកខេលលកខាា កោេ�ព�េនខង ា

កខផ�នោផ�ងោេសេាា កោេ� គេេនលែដលសម សោសក� �ខ អាកនកងនល�េចេ��ក�ដរន េេនលែដលសម សោសក� �ខ អាកនកងនេចេ��ក�ដរន ា

6

៣.អរឣណ�តងរង�ខង�ខ ()

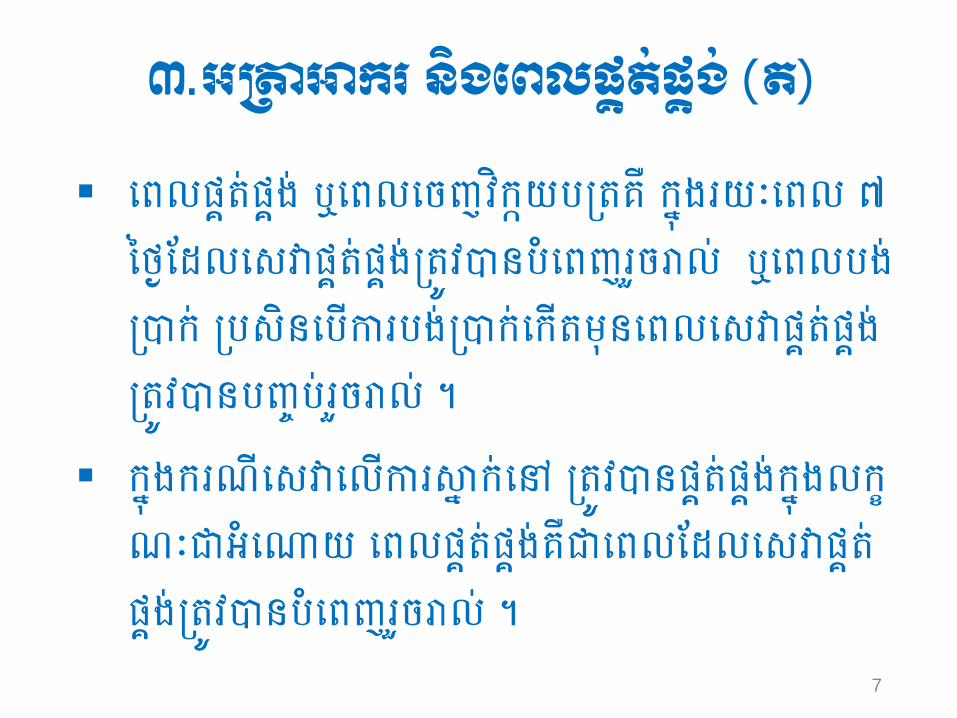

េនលផ�នោផ�ងោ េនលេចេ��ក�ដរនគ កាតងខដៈេនល ៧ៃថ�ែដលេសេផ�នោផ�ងោនល�នរេនេខសចខលោ េនលរងោកោ រសនេរលកខរងោកោេកលននេនលេសេផ�នោផ�ងោនល�នរបមរោខសចខលោ ា

កាតងកខណេសេេលលកខាា កោេ� នល�នផ�នោផ�ងោកាតងលកលណៈេអេកដ េនលផ�នោផ�ងោគេេនលែដលេសេផ�នោផ�ងោនល�នរេនេខសចខលោ ា

7

៤.ើ�គរានណខឣណ�

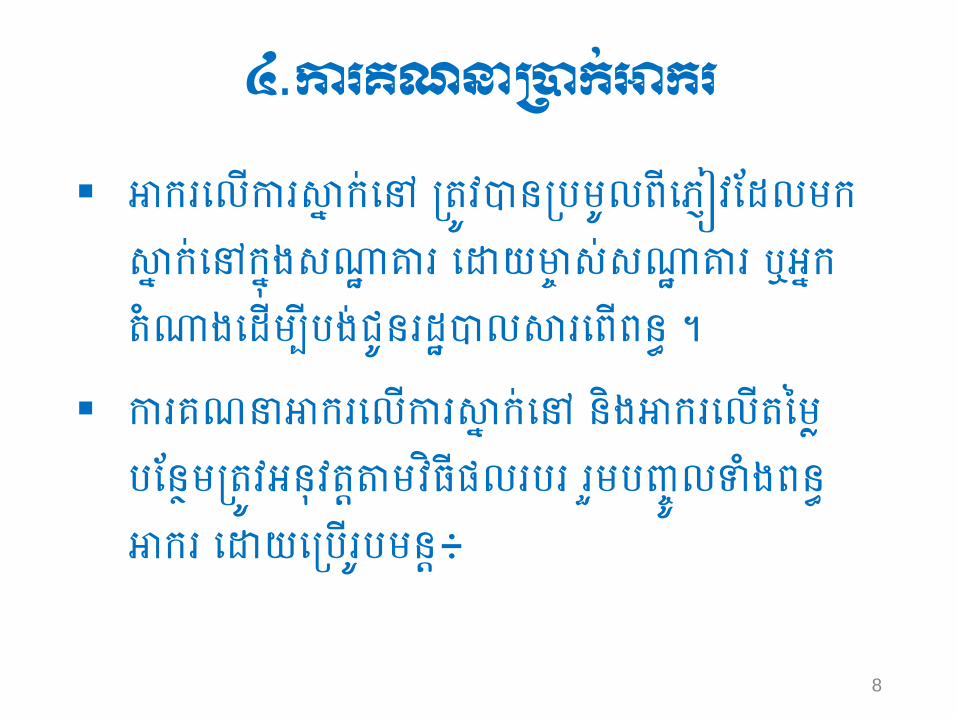

តកខេលលកខាា កោេ� នល�នរលនេប���ែដលកាា កោេ�កាតងសក� �ខ េេដសម សោសក� �ខ អាកនកងេដលរងោជនខដ�លាខេនលននា ា

កខគណនតកខេលលកខាា កោេ� នងតកខេលលនៃ�រែនវនល�អន�ន�រ��មផលខរខ ខសរបមលលទងននា តកខ េេដេរលខរន�

8

៤.ើ�គរានណខឣណ� ()

- សសសនននា-តកខ :

- រភគគនអនរ :

- រភគគនតកខេលលផលខរខ :

- រភគគនតកខេលលកខាា កោេ� :

10 10 1 ------------ = -------- = ------ 10 + 100 110 11

2 2 1 ----------- = --------- = ------- 2 + 100 102 51

2 2 1 ----------- = --------- = ----- 2 + 100 102 51

R Rate ----------- = ----------------- R + 100 Rate + 100

9

៤.ើ�គរានណខឣណ� ()

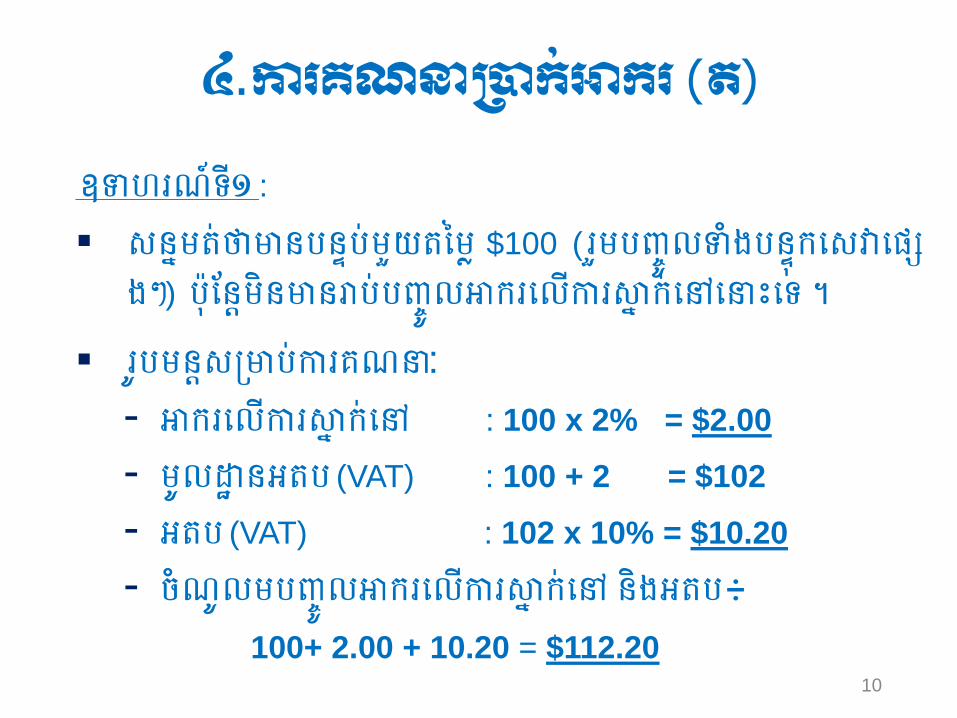

ឧទពខណរទ១ :

សនានោថសនរន�រោសដនៃ� $100 (ខសរបមលលទងរន�តកេសេេផផងៗ) រែន�នសនខរោរបមលលតកខេលលកខាា កោេ�េនេទ ា

ខរន�សសរោកខគណន: - តកខេលលកខាា កោេ� : 100 x 2% = $2.00

- លេ� នអនរ (VAT) : 100 + 2 = $102

- អនរ (VAT) : 102 x 10% = $10.20

- ចណលរបមលលតកខេលលកខាា កោេ� នងអនរ

100+ 2.00 + 10.20 = $112.20 10

៤.ើ�គរានណខឣណ� ()

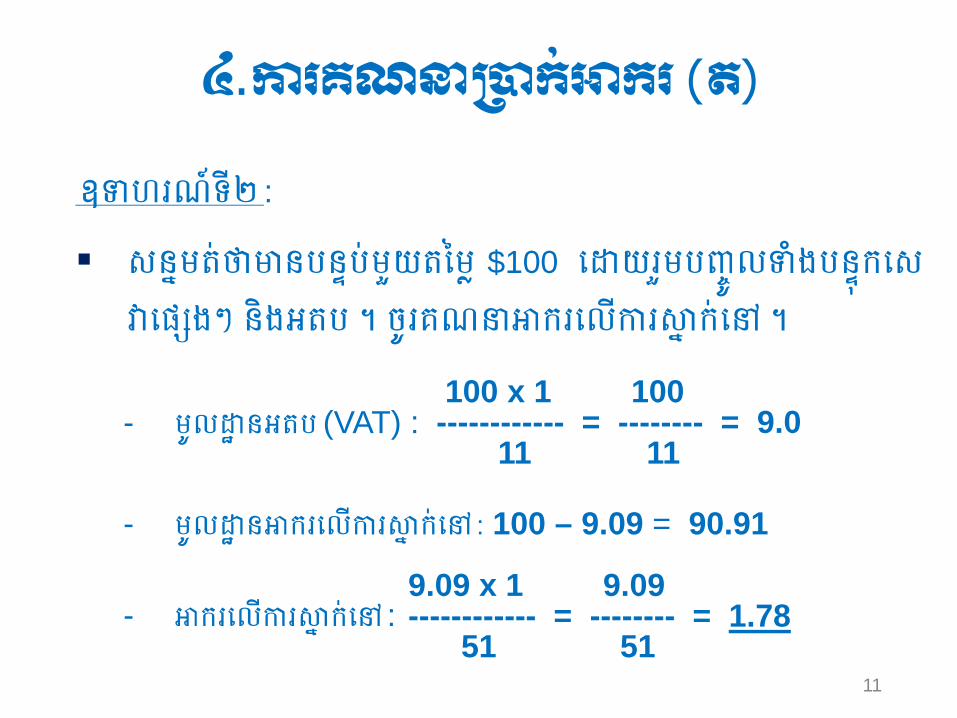

ឧទពខណរទ២ :

សនានោថសនរន�រោសដនៃ� $100 េេដខសរបមលលទងរន�តកេសេេផផងៗ នងអនរ ា ចខគណនតកខេលលកខាា កោេ� ា

- លេ� នអនរ (VAT) :

- លេ� នតកខេលលកខាា កោេ� : 100 – 9.09 = 90.91

- តកខេលលកខាា កោេ� :

100 x 1 100 ------------ = -------- = 9.0 11 11

9.09 x 1 9.09 ------------ = -------- = 1.78 51 51

11

៥.ើ�បខនណខឣណ�

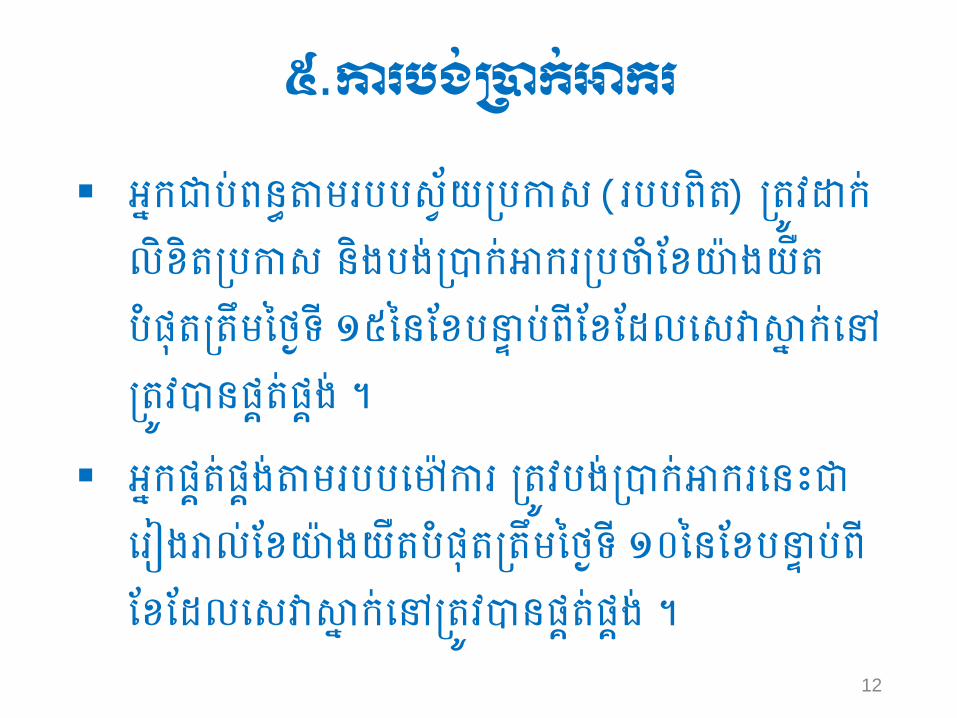

អាកេរោននារខររសរ ដរកស (ខររនន) នល�េកោលពនរកស នងរងោកោតកខរ ែពពងដនរផននៃថ�ទ ១៥ៃនែពរន� រោនែពែដលេសេាា កោេ�នល�នផ�នោផ�ងោ ា

អាកផ�នោផ�ងោរខររេនកខ នល�រងោកោតកខេនេេខរងខលោែពពងដនរផននៃថ�ទ ១០ៃនែពរន� រោនែពែដលេសេាា កោេ�នល�នផ�នោផ�ងោ ា

12

៦.ងទសងរទ

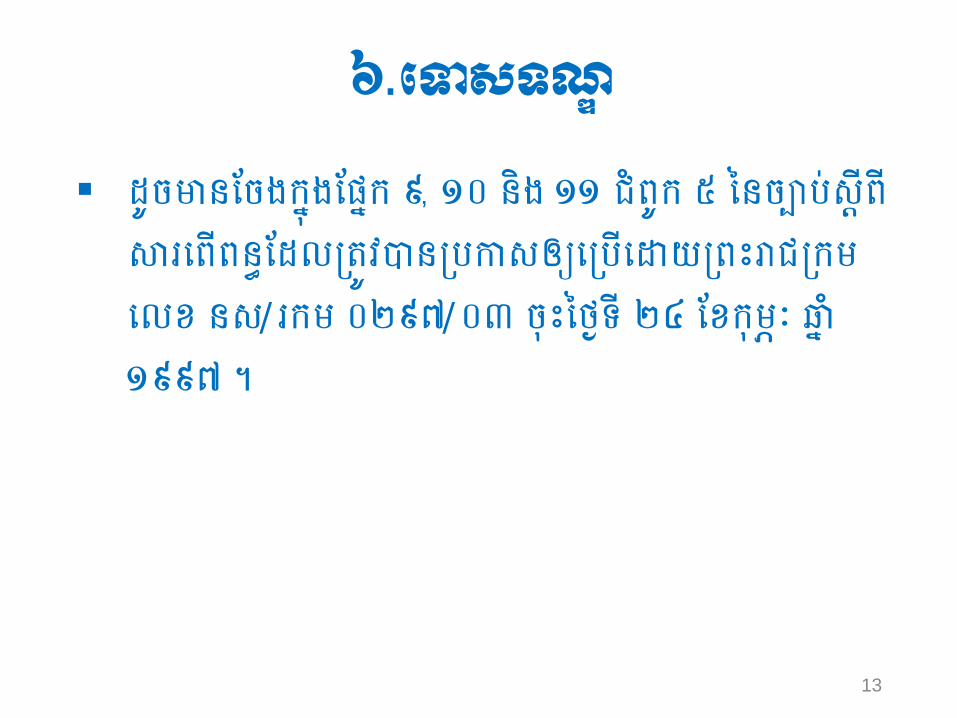

ដចសនែចងកាតងែផាក ៩, ១០ នង ១១ ជនក ៥ ៃនចរោស� នាខេនលននាែដលនល�នរកសនេរលេេដនខជកេលព នស/ខក ០២៩៧/០៣ ចៃថ�ទ ២៤ ែពក�ៈ ឆា១៩៩៧ ា

13

សចអ�គ រ!

14

KINGDOM OF CAMBODIA

NATION RELIGION KING

General Department of Taxation

Ministry of Economy and Finance

Presented by : Mr. Hien Sokhal

Deputy Director of Siem Reap Tax Branch

ACCOMMODATION TAX Siem Reap, 21st February, 2014

CONTENTS

1.Related Law and Regulations

2.Definition

3.Tax Rate and Time of Supply

4.Practical Calculation

5.Payment of Tax

6.Penalty 2

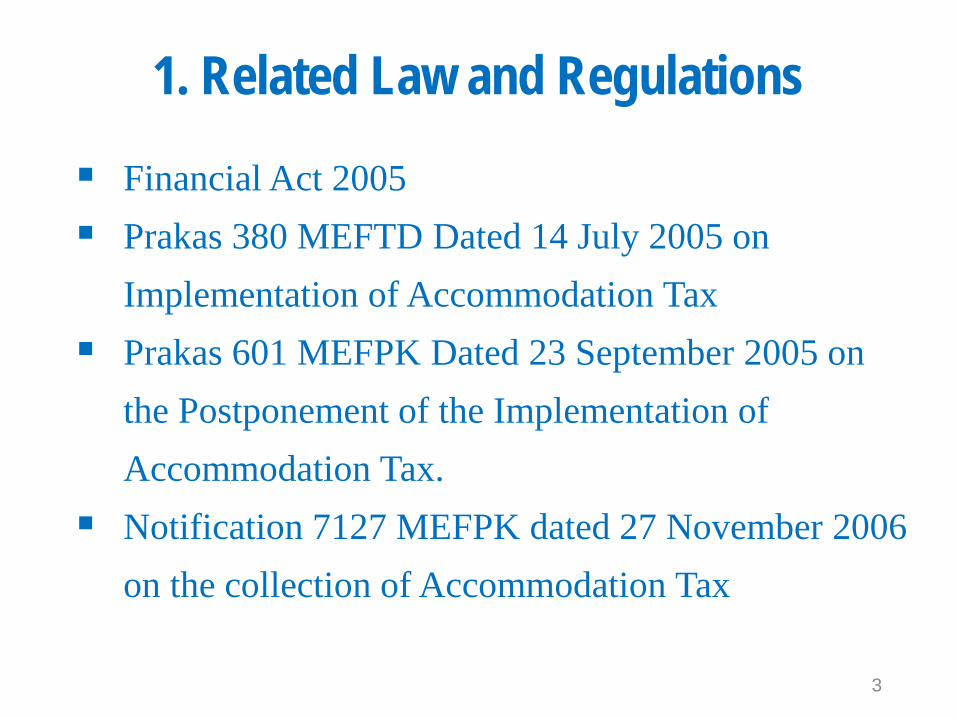

1. Related Law and Regulations

Financial Act 2005 Prakas 380 MEFTD Dated 14 July 2005 on

Implementation of Accommodation Tax Prakas 601 MEFPK Dated 23 September 2005 on

the Postponement of the Implementation of Accommodation Tax.

Notification 7127 MEFPK dated 27 November 2006 on the collection of Accommodation Tax

3

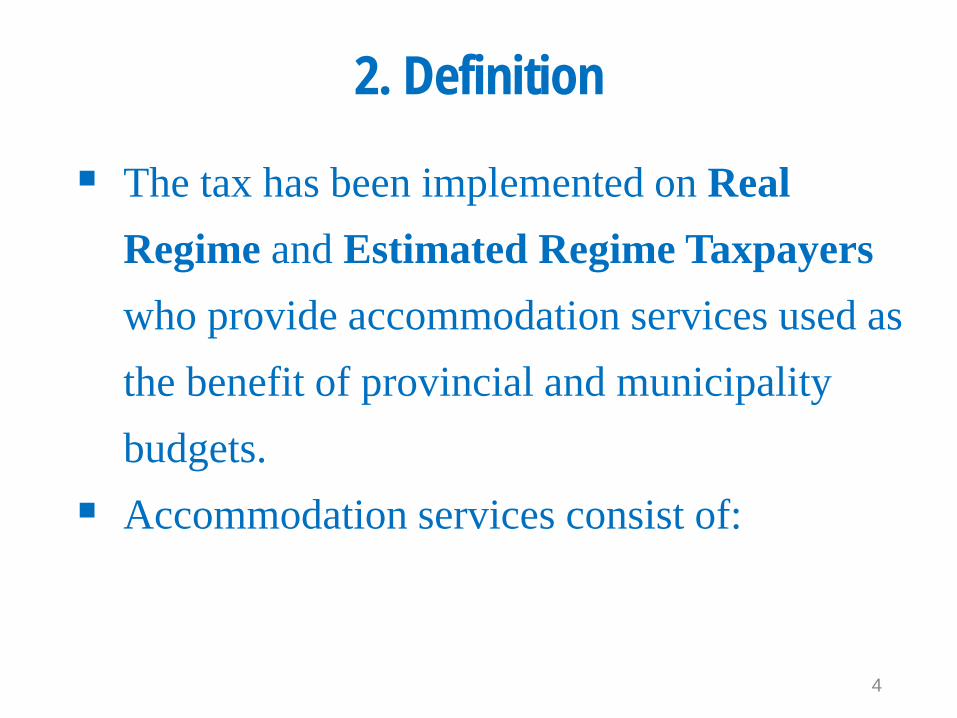

2. Definition

The tax has been implemented on Real Regime and Estimated Regime Taxpayers who provide accommodation services used as the benefit of provincial and municipality budgets.

Accommodation services consist of:

4

2. Definition (cont.)

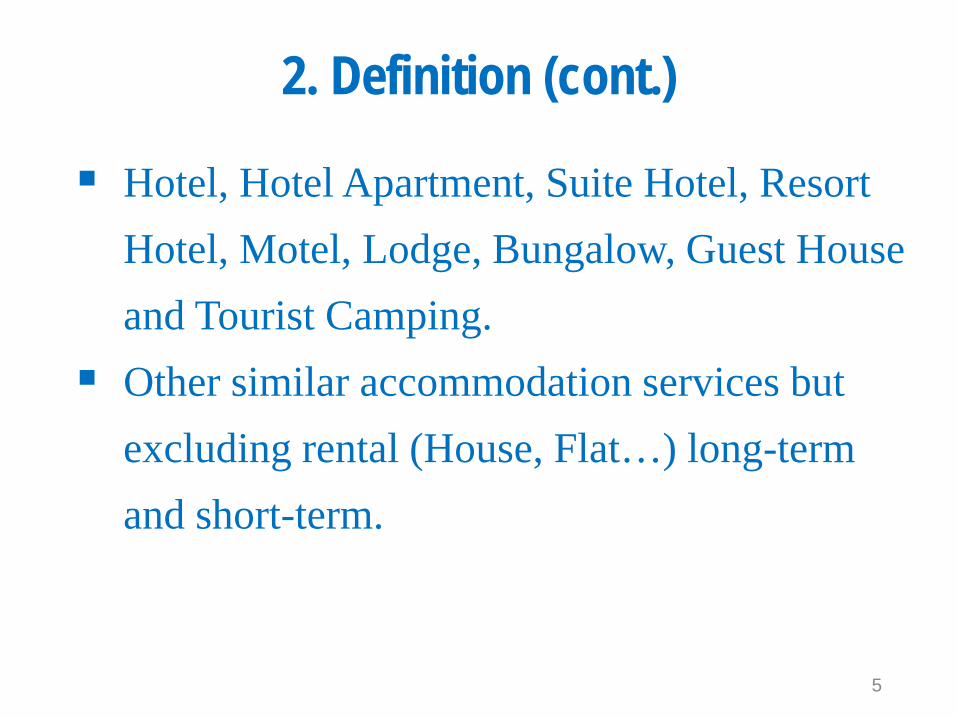

Hotel, Hotel Apartment, Suite Hotel, Resort Hotel, Motel, Lodge, Bungalow, Guest House and Tourist Camping.

Other similar accommodation services but excluding rental (House, Flat…) long-term and short-term.

5

3. Tax Rate and Time of Supply

The tax rate is 2% on taxable value of accommodation services inclusive of service charge and other taxes except AT and VAT.

Time of Supply or Issue an Invoice: within 7 days of the completion of services, or the payment if it is made prior to the completion of services.

6

3. Tax Rate and Time of Supply (cont.)

Where the service is supplied by way of gift, the time at which the performance of the services is completed.

7

4. Practical Calculation

Accommodation tax is collected from guests by hotel’s owner or representative to pay to the General Department of Taxation.

Accommodation tax and VAT are calculated through the following formula:

8

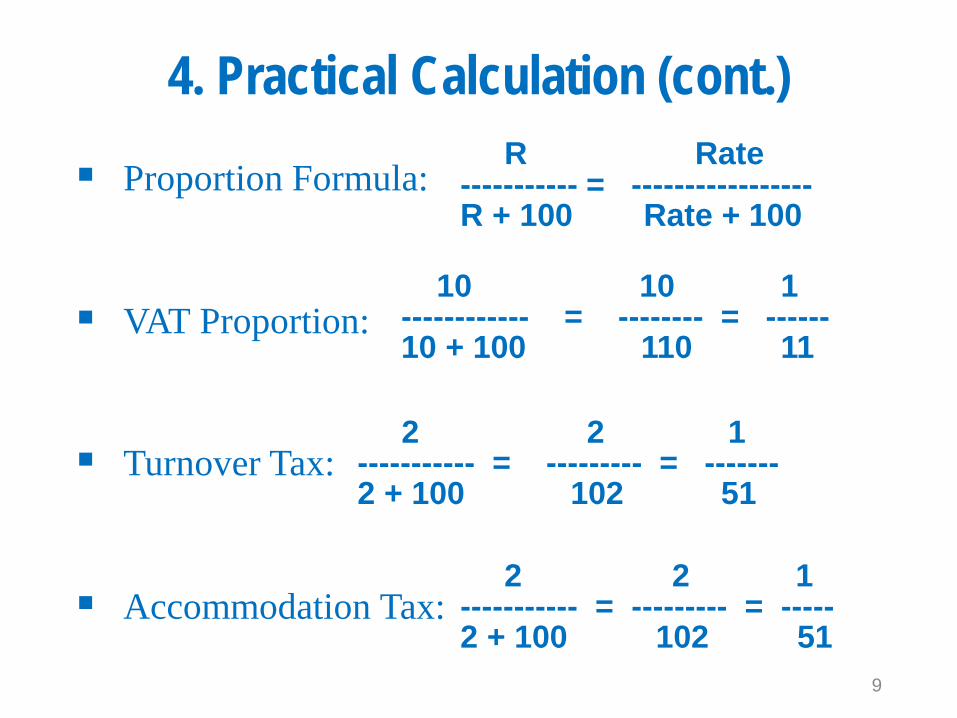

4. Practical Calculation (cont.)

Proportion Formula:

VAT Proportion:

Turnover Tax:

Accommodation Tax:

R Rate ----------- = ----------------- R + 100 Rate + 100

10 10 1 ------------ = -------- = ------ 10 + 100 110 11

2 2 1 ----------- = --------- = ------- 2 + 100 102 51

2 2 1 ----------- = --------- = ----- 2 + 100 102 51

9

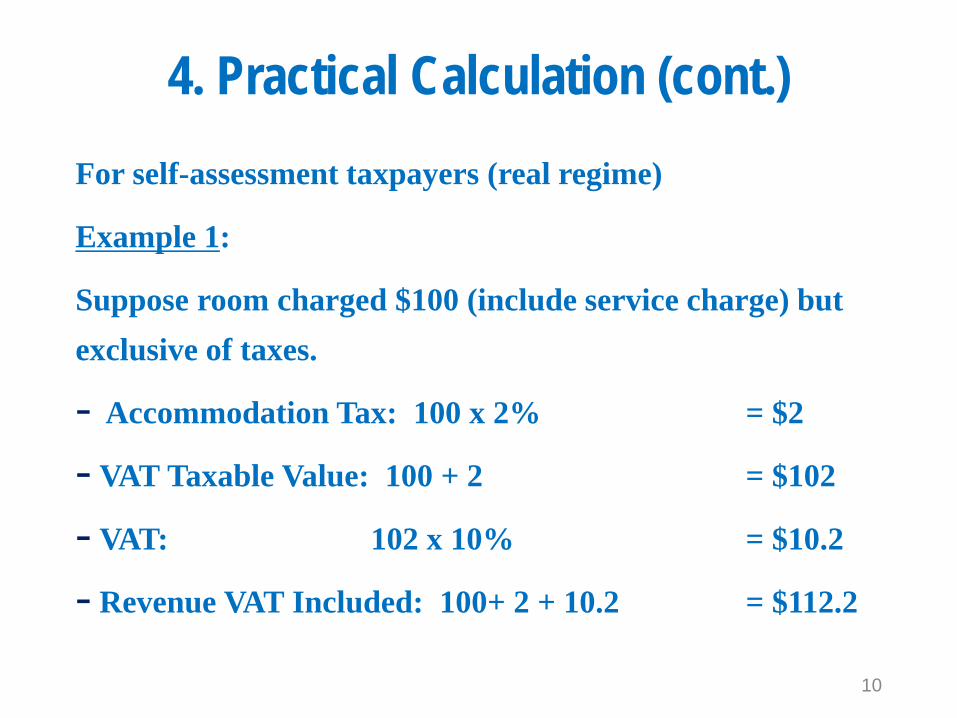

4. Practical Calculation (cont.) For self-assessment taxpayers (real regime)

Example 1:

Suppose room charged $100 (include service charge) but exclusive of taxes.

- Accommodation Tax: 100 x 2% = $2

- VAT Taxable Value: 100 + 2 = $102

- VAT: 102 x 10% = $10.2

- Revenue VAT Included: 100+ 2 + 10.2 = $112.2

10

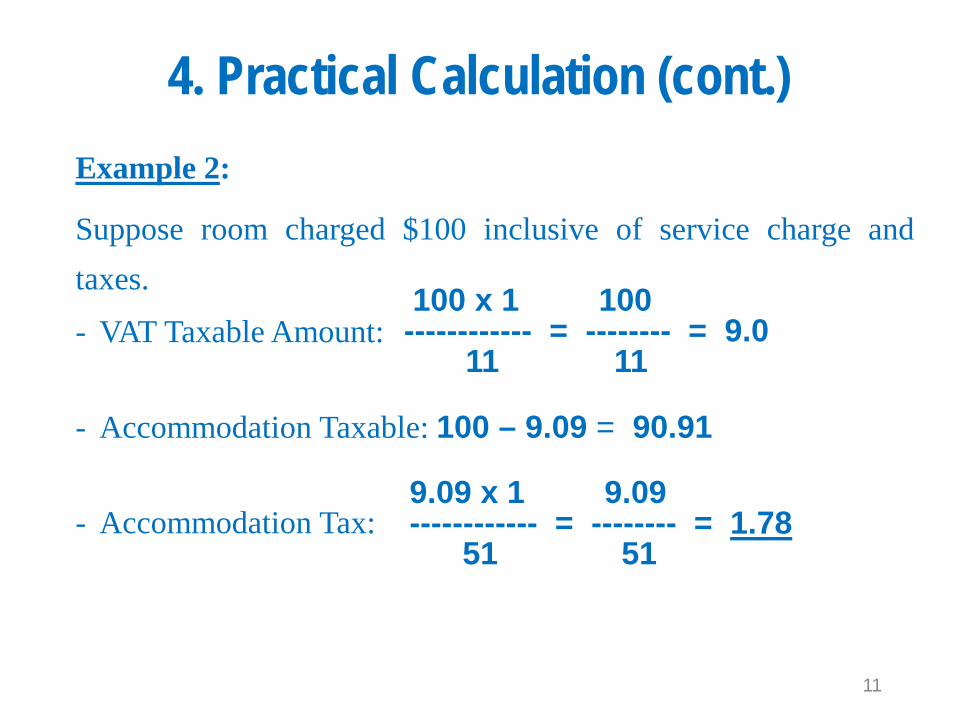

4. Practical Calculation (cont.) Example 2:

Suppose room charged $100 inclusive of service charge and taxes.

- VAT Taxable Amount:

- Accommodation Taxable: 100 – 9.09 = 90.91

- Accommodation Tax:

100 x 1 100 ------------ = -------- = 9.0 11 11

9.09 x 1 9.09 ------------ = -------- = 1.78 51 51

11

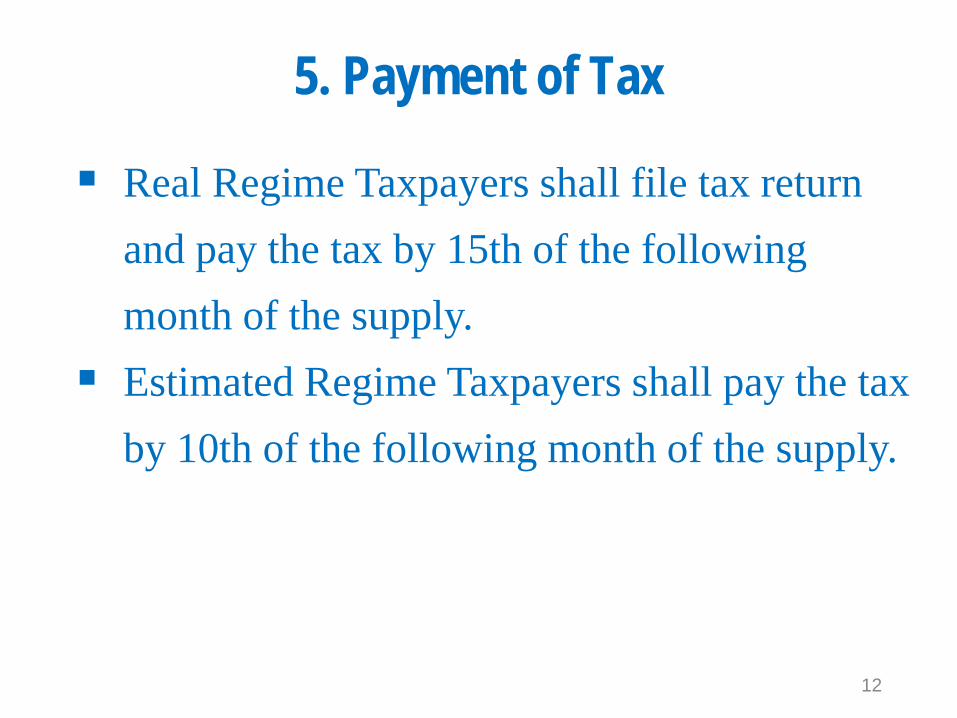

5. Payment of Tax

Real Regime Taxpayers shall file tax return and pay the tax by 15th of the following month of the supply.

Estimated Regime Taxpayers shall pay the tax by 10th of the following month of the supply.

12

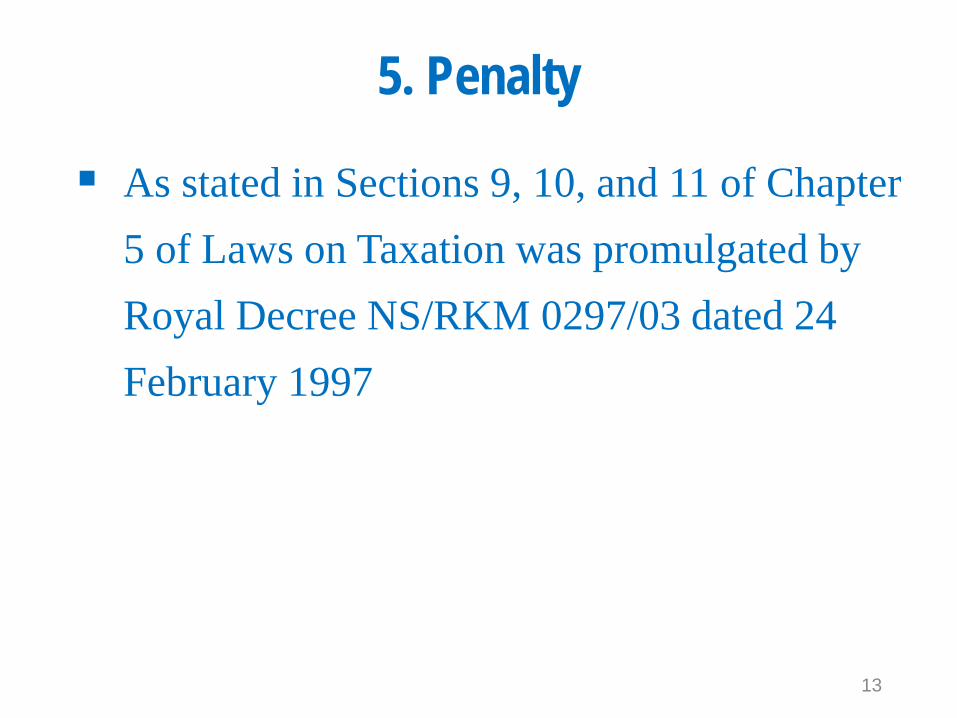

5. Penalty

As stated in Sections 9, 10, and 11 of Chapter 5 of Laws on Taxation was promulgated by Royal Decree NS/RKM 0297/03 dated 24 February 1997

13

THANK YOU!

14

រពះរជណណចររ រត សារពចណព

អគ�ាណកដ រពក� ណសសងសសដណតជចត ត�រ��តរ

ឧេទ�សនេេដ : ងលណង ៀសខល

អនរបនាននាេខេពន�េសរខរ�

ឣណ�រប ភ� ស�ធ (េសរខរ ៃថ�ទ២១�ែពក�ៈ�ឆា ២០១៤ )

មតត

១.កខផ�នផ�ងជរឣកខរ ភ�ាបខណៈ ២.នដនដ ៣.ននវ�ធៃនកខកណនឣកខ ៤.អរឣកខ ៥.�វ�ធគណនឣកខរ ភ�ាបខណៈ ៦.កខរងកឣកខ

2

១.ត���ររឣណ�រប ភ� ស�ធ

កខផ�នផ�ងនវទនញដចងេក�នមវជរឣកខរ ភ�ាបខណៈ�រ�

សខេខរដ

ាេររខ

ខ

3

២.តច

នមវនានជសខេខរដ�ាេររខ�នងខ�រ

�ាេររខ�

ាទពងដបខសស�ខសងាទពងដបខែដលមនរែនែជនសខ

ាែវន�នងាទពងដបខសសេផរងេទរនផរ នខក�ជន�នងាខជនកអរ

េសប�ៈេខរដេផរងេទរន�េលលកែលងទទកេរា នប�នងាស

4

២.តច()

ឣលកលេអទលកសទា�ែដលមនកនជនសខកា�ងឯករចណណេលលសន�៨០% ៃនចណណឬេលលសនេនណ�នងឣលកលេអទលក�េេលដនងេសប�ៈមនជនសខែដលនរងកនសខេដលខរសវ ។

5

២.តច()

ឣលកលេអទលកនរងបនសទាែដលមនកនជនសខកា�ងឯករចណណ�៨០% ៃនចណណ�នងេសប�ៈមនជនសខ�េសប�ៈសវៈងេផរងងេទរន�កខេខររចែកៃចាសខផរ កា�ងរេទែដលេរលសមរផលនេសប�ៈ�។

ខ�ខស�� គររេទ�

6

៣.ត��ធៃត�ណបឣណ�

ឣកខរ ភ�ាបខណៈនមវកណនេតគរដបក�កលៃនកខផ�នផ�ង�នងនមវអនវន�េលលនៃភផ�នផ�ងផលនផលជរឣកខ�ខសរមបមលងននាឣកខនន�េវរខែលងែនឣកខរ ភ�ាបខណៈពភណនឯង�នងឣកខេលលនៃភរែនែ�។

7

៣.ត��ធៃត�ណបឣណ�()

េដលគណនកឣកខនមវរង�រគ�លជរឣកខនមវេធធលកខែរងែចកែចនខវងផលខរខែដលនកនកខផ�នផ�ងសខេខរដ�នងខជរឣកខ�នងផលខរខនកនកខផ�នផ�ងទនញ�េសវដដៃទេទរន�។

8

៤.អរតសណបឣណ�

ឣកខរ ភ�ាបខណៈ�នមវរលរអរ�៣% េលលនៃភសខេខរដ�នងខ�ែដលលកកា�ងណ� លែដនដេពន�ក�ងនសដង�។

ឣកខេនណ�កដនមវអនវន�ផងែដខចេពណកខដកដក�សខេខរដ�នងខសមរនមវកខ � លពភណនខរសរគ�លជរឣកខ�ខរសរគ�លក�ឬសមរននដបន�។

9

៥.��ធគាឣណ�រប ភ� ស�ធ

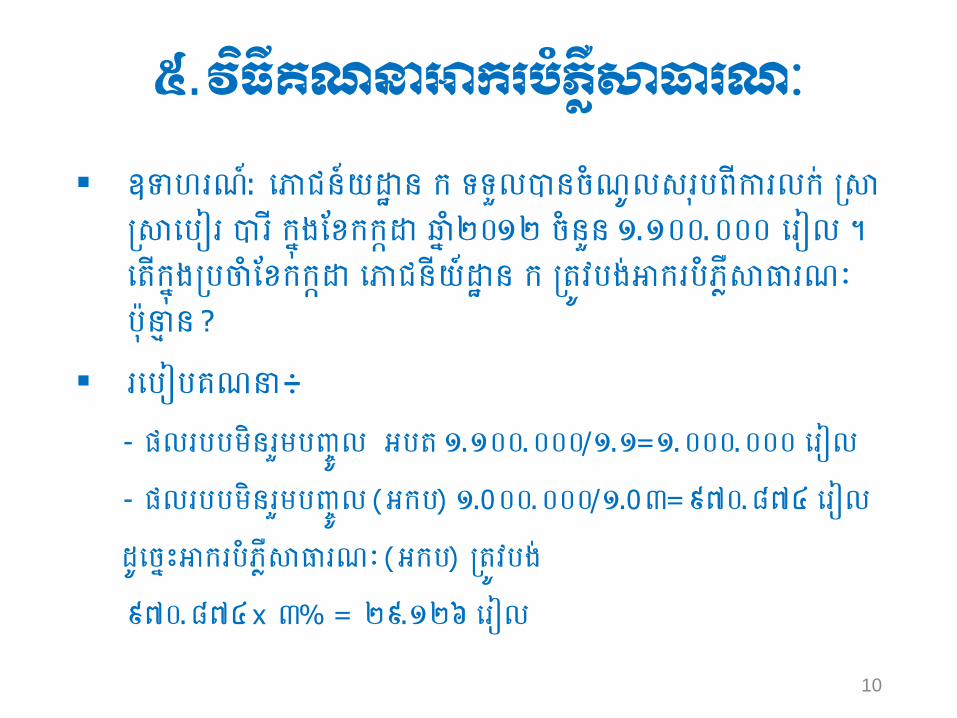

ឧេខណរ: េភបនរដេ ន�ក�ទទសលនចណលសខរនកខលក�ា�ាេររខ�ខ�កា�ងែពកកងេ�ឆា ២០១២�ចនសន�១.១០០.០០០ េខរល ។�េនលកា�ងរាែពកកងេ�េភបនដរ�េ ន�ក�នមវរងឣកខរ ភ���ាបខណៈរន ន ?

ខេរររគណនរ

- ផលខររនខសរមបមល��អរន�១.១០០.០០០/១.១=១.០០០.០០០ េខរល

- ផលខររនខសរមបមល�(អករ) ១.0០០.០០០/១.0៣=៩៧០.៨៧៤�េខរល

ដេចាណឣកខរ ភ�ាបខណៈ�(អករ) នមវរង

៩៧០.៨៧៤�x ៣% = ២៩.១២៦�េខរល

10

៦.ត�រណឣណ�

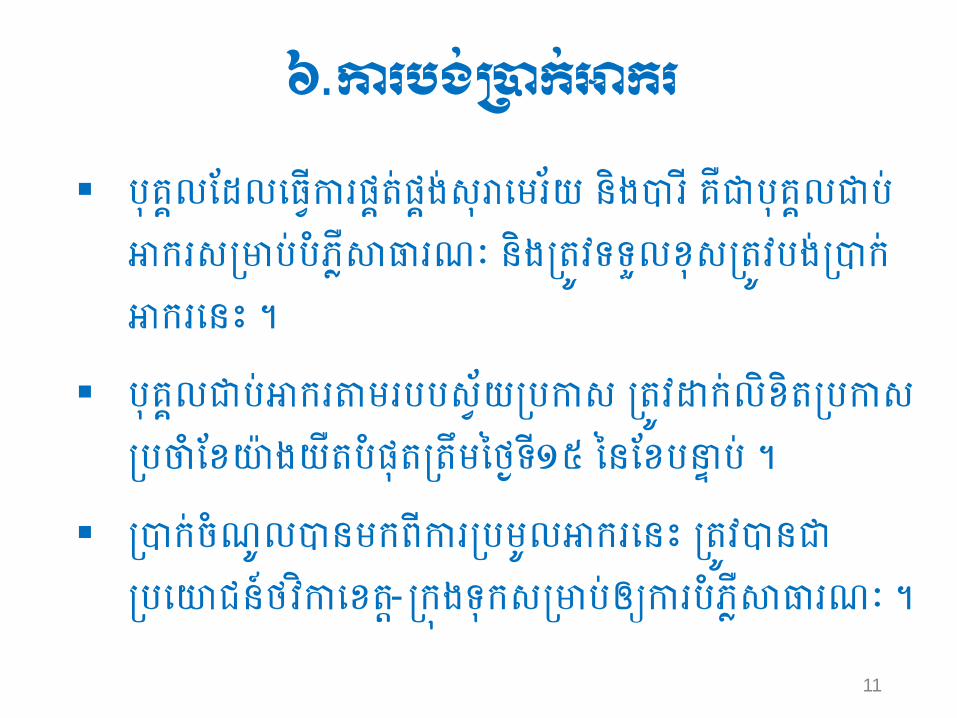

រគ�លែដលេធធលកខផ�នផ�ងសខេខរដ�នងខ�គ�ជរគ�លជរឣកខសមររ ភ�ាបខណៈ�នងនមវទទសលពសនមវរងកឣកខេនណ ។

រគ�លជរឣកខរខររសធដរកស�នមវេកលពន�រកស�រាែពងដ�នរផននទៃថ�ទ១៥�ៃនែពរន� រ�។

កចណលនកនកខរលឣកខេនណ�នមវនជរេបនរថវ�កេពន�-ក�ងទកសមរែចកខរ ភ�ាបខណៈ ។

11

សចអ�គ!

12

KINGDOM OF CAMBODIA

NATION RELIGION KING

General Department of Taxation

Ministry of Economy and Finance

Presented by : Mr. Hien Sokhal

Deputy Director of Siem Reap Tax Branch

PUBLIC LIGHTING TAX Siem Reap, 21st February, 2014

CONTENTS

1.PLT Taxable Supply

2.Definition

3.Procedure of Tax Assessment / Payment

4.Tax Rate

5.Method of Tax Calculation

6.Tax Payment 2

1. PLT Taxable Supply

Shall be taxed on Public Lighting of Supply of Products as follows: Alcoholic Beverages Beers and Cigarettes

3

2. Definition

Shall be determined as alcoholic beverages, beers and cigarettes: - All kinds of beers, - Red wine included alcoholic substance, - Other alcoholic beverages except palm

juice (toddy) and wine - Cigarettes and all kinds of Cigars

4

2. Definition (cont.)

Alcoholic beverages which contains or more than 80% of Alcohol substance, Alcohol beverages which lose its primary alcohol substance, and Other alcohol beverages after any conversion.

5

3. Procedure of Tax Assessment/Payment

Public Lighting Tax (PLT) is imposed on all stages of supplies (of alcoholic Beverages and cigarettes) and shall implement on value of taxable supplies of products inclusive all taxes except Public Lighting Tax itself and Value Added Tax (VAT).

6

3. Procedure of Tax Assessment/Payment (cont.)

In order to calculate taxes to be paid, taxable person shall separately record revenues realized from other taxable supply and other supplies.

7

4. Tax Rate and Tax Payment

Public Lighting Tax shall be collected at the rate of 3% on value of Alcoholic Beverages and Cigarettes sold in each province and municipality.

This tax is also applied for the appropriation Alcoholic Beverages and Cigarettes for his/her own use by taxable person, personnel or for third party.

8

5. Method of Tax Calculation Example “A”: A restaurant realized the total revenue from selling of Wine, Beer and Cigarettes in July, 2012 the amount of 1,100,000 riel. What is tax due for “A” restaurant in July, 2012? Calculating Method: Turnover Exclusive VAT: 1,100,000/1.1 = 1,000,000 Riel Turnover Exclusive PLT: 1,000,000/1.03 = 970,874 Riel Therefore PLT shall be paid for July, 2012: 970,874 x 3% = 29,126 Riel

9

6. Tax Payment

Person who makes taxable supply of Alcoholic Beverages and Cigarettes is a PLT Taxable person and shall be responsible for collection of PLT from customers and pay the tax to the tax administration.

Self-Assessed / Real Regime Taxpayers shall pay the tax no later than 15th of the following month.

Budget collected from this tax shall be the benefit of the provincial and municipal budget for public lighting.

10

THANK YOU!

11

រពះរជណណចររ រត សារពចណព

អគ�ាណកដ រពក� ណសសងសសដណតជចត ត�រ��តរ

ឧេ ទ �ស ន េ េដ : ងលណ ង ៀសខល

អ នរ ប នា ននា េខ េ ពន�េ ស រ ខ រ �

ឣណ�រតងសសងលលើទតតងសសចសជទស (េ ស រ ខ រ ៃថ� ទ ២១�ែពក� ៈ� ឆា ២០១៤ )

មតត

១.កខរ ន�រ ផ�ងរ�កខនេស ស

២.ល េ ន ន នកខនេស ស

៣.អ រ កខនេស ស

៤. �វ�ធន ណនក�កខ

៥. កខរផ�ក�កខ

2

១.ត���រឣណ�រតងសស

ទន ញ� ន ផ េសវងរ�ក ខនេ ស ស េ

ា� ាេររខ� ខប នរ�រេ� ទ� ន ផ េ� សេភ ៈ

ៃថ� លក �សរនតដក េជភ� ន អា ក ត េណ ណខ រ ដន� េ ហា

េសវទខ�សសន�

េសវលែ ែក ាន� េ�ផ ផ

3

១.ត���រឣណ�រតងសស()

េសវលែ ែក ាន� េ

េសវលែ ែក ាន� េ�ផ ផ� ខង ន �េ� ក ខរននន� � គក �េ�� ផ � សែ តផ ឈ នឆ ក � ក ក ដ វ�ក ខ� ន លករ ណ ៈងសក � ភនេ វក � េម កា� ផ ខផរ ាល� ខ驈 អេព� ស� េថក �ទក ែ ន� ផ ាខបខណ ៈ� ក ក ែ ន� ផ ែងដ� ។

4

១.ត���រឣណ�រតងសស()

េសវលែ ែក ាន� �(ន)េ

សែ � ខ� ក េភេន ដេ ន ែ តល ន ក ខរននន� � ក ខសែ តផ ឈ នឆ ក � ក ក ដ វ�ក ខ ន លករ ណ ៈ ខភភ រ�ន ដផេ វក � ខរស�សែ � ខ� ក េភេន ដេ ន � ក យន�វនគន�ទក ងេស វលែ ែក ាន� ែ តខ� ។

ា ស � រែ ខថដន� �Karting រែ ផ ាន� សា� ក �សខ�Bowling េែ រ នរ�រេ� ទ� ក ន េហរ ល� ។

5

២.ចលកដ គតឣណ�រតងសស

ស ែ �ស លន កា�ផ ស �កេ

លេ ន នន កខនេស ស �ន ងៃថ� លក�េកញ នេខ ផក កកន � រ កា�ផ វ�កដ រ ន�( រ �៨៥ � កស ន) ។

ៃថ� លក�េកញ នេខ ផក កកន � រ កា�ផ វ�កដ រ ន�េស� ណន ផ�៦ ៥% ៃន ៃថ� រ ន �រ ផ� ន ខងរជ�� ល�អ រ ន �ែ ត លន កន � រកា�ផ� វ�កដ រ ន តឲ េយ��� អ ន ថ េន េេដ � ន �ននអ នកខរ ជ�� ា ៃថ� េ� ផផេេណដ �( រ កស ��៣ ៤ ៤ �កា ៃថ� ២ ៧/៤/២ ០ ០ ៧) ។

6

២.ចលកដ គតឣណ�រតងសស()

កខរ ន�រ ផ�ព�ខ ន �ផ�ក � ល �អ េែដ េ

កខរ ន�រ ផ�ទន ញ ត ឲព�ខ ន �ផ�ក កខក ល �ងអ េែដ �ក កខល ក�េកនៃ� ទ ខន�វរផ�កខរ នៃ� ទ ខ�។

7

២.ចលកដ គតឣណ�រតងសស()

ស ែ�ស រ ន�រ ផ�េស វកា�ផស �កេ

ល េ ន ន នកខនេស ស េល ណកខរ ន�រ ផ�េស វកា�ផស �កន �ងៃថ� រ ន�រ ផ�េស វន ខងរជ�� ល កខេល ណនែ � រែ ន� �ែ តល ន �កន�រ កា�ផ វ�កដ រនត ឲេយអ នថេន �េវរ ខែ ល ផែ នកខនេស ស �ព�ខ ន�ផ� ។

8

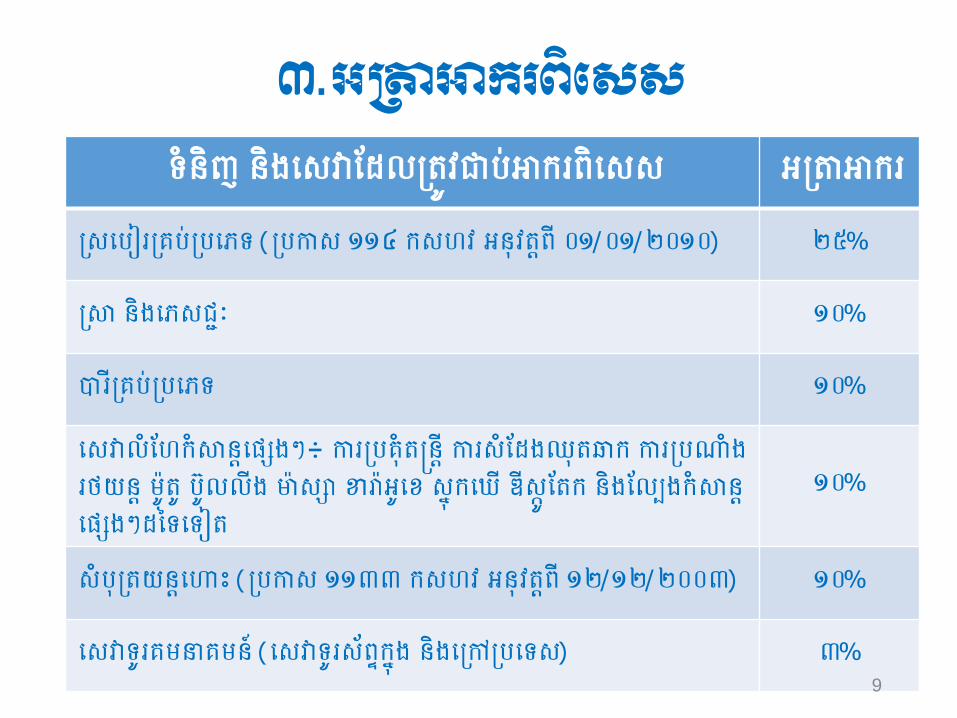

៣.អរឣណ�រតងសស ទ នញ�នផេសវែតលន�វងរ�កខនេសស អរកខ

សេ រ រ ខ នរ � រ េ �ទ�( រ កស� ១១៤ �កសែ វ� អន វន�ន �០១/០១/២០១០) ២៥%

ា�ន ផ េ �សេភ ៈ ១០%

ខប នរ � រ េ �ទ ១០%

េ សវ ល ែ ែ កាន� េ �ផ ផេ កខ រ នន ន� �កខសែ ត ផ ឈ នឆ ក�កខ រ ែ ផខថ ដន� � ាន�រ ល ល ផ � ា ស �ខ驈 អេ ព�សា� កេ � ណ� ស� ែ នក�ន ផ ែ ល ផ កាន�េ �ផ ផត ៃ ទេ ទរ ន�

១០%

សរ នដន� េ ហា�( រ កស ១១៣ ៣�កសែ វ� អន វន�ន �១២/១២/២០០៣) ១០%

េ សវ ទខន ន ន ន ម (េ សវ ទខសសន� កា�ផ � ន ផ េ រ េ ទស) ៣% 9

៤.��ធគណាណឣណ�

ស នន នឲរ ខ ផន ណនកា�ផ�វ�កសដ រសន។

10

៥.ត�ណឣណ�

រនរ ល ែ តល េធ�ណកខរ ន�រ ផ�ងរ�កខនេស ស �ន�វេក�ល ពនរកស ន ផរផ�ក�កខ�រគ ែ ព�យា ផដ នរននដៃថ� ទ�១៥�ៃន ែ ព��រន� រ��។

11

សចអ�គណ!

12

KINGDOM OF CAMBODIA

NATION RELIGION KING

General Department of Taxation

Ministry of Economy and Finance

Presented by : Mr. Hien Sokhal

Deputy Director of Siem Reap Tax Branch

SPECIFIC TAX ON CERTAIN MERCHANDISE AND SERVICES

Siem Reap, 21st February, 2014

CONTENTS

1.Subject to Specific Tax

2.Taxable Amount of Specific Tax

3.Rate of Specific Tax

4.How to Calculate Specific Tax

5.Payment of Specific Tax

2

1. Subject To Specific Tax

Certain merchandise and services are subject to specific tax including: Wines, beers, all kinds of tobacco, and

beverages. Sales of air tickets (passengers). Telecommunication services. Entertainment services.

3

1. Subject To Specific Tax (cont.)

Entertainment Services: Entertainment services include: concert,

playing music, performing sketch or gestures which are related to business activities in bar, karaoke, discotheque in public area or any place.

4

1. Subject To Specific Tax (cont.)

Entertainment Services (Cont.): Hotel or restaurant which consists of playing

concert, performing sketch or gestures related to business activities in hotel or restaurant are subject to be entertainment services.

Massage, car racing, motor racing, snooker, bowling, golf, and other gambling.

5

2. Taxable Amount of Specific Tax

For Local Production Industries: Taxable amount is the sale price which is recorded

on the manufacturing invoice (article 85 Of LOT). Sale price which is recorded on the manufacturing

invoice equals to 65% of the price exclusive VAT recorded on the invoice issued to customers regardless of any discounts (Prakas 344 dated 27 April 2007).

6

2. Taxable Amount of Specific Tax (cont.)

Owner’s use or giving gifts : Owner’s use or giving gifts or sales bellow

market price, the tax must be calculated and paid following the market price of the items.

7

2. Taxable Amount of Specific Tax (cont.)

Local Service Industries: Taxable amount of Specific Tax on local service supplied is the service supplied amount excluding VAT recorded on the invoice issued to customers except Specific Tax itself.

8

3. Rate of Specific Tax

Goods and Services are Subject to Specific Tax Tax Rates

All Kinds of Beers (Prakas 114 MEF on 01 Jan 2010) 25%

Wines and Beverages 10%

All Kinds Of Tobacco 10%

Entertainment Services: Concert, Performing Sketch Car Racing, Motor Racing, Bowling, Massage, Karaoke Snooker, Discotheque, Golf, and Other Gambling. 10%

Air Tickets (Passenger only) 10%

Telecommunication Services 3%

9

4. How to Calculate Specific Tax

Kindly refer to the Calculation List of the invoice.

10

5. Payment of Specific Tax

The entities who are subject to Specific Tax must file a Tax Return and pay the tax no later than 15th day of following month.

11

THANK YOU!

12

រពះរជណណចររ រត សារពចណព

អគ�ាណកដ រពក� ណសសងសសដណតជចត ត�រ��តរ

ឧេទ�សនេេដ : ងលណសរអ �ង��

អនរបននដយេដ នររបររអងយ�របនពន�

រពងលើរណាជកងច (េសៀររ ៃថ�ទ២១�ែខយ�ៈ�ឆង ន២០១៤ )

1

2

1. យ�វត��ៃននេលើរយបនេច�(ម�២��ស) 2. នចលរបយម���(ម�៣៣ថ��ស) 3. រយបនេច�របន�(ម�៧��ស) 4. កាកតបយរែលអនលអ ត�(ម�១១��ស) 5. កាកតបយរែលែនអនលអ ត�(ម�១៩�ស) 6. កាេររកាងតររបេាខ��(ម�១៧��ស) 7. អនេលើរយបនេចរ នឆង ន�(ម�២០ថ��ស) 8. នកតបទយេលើនែនសនន�(ម�២៥ថ���ស) 9. នកតបទយេលើអនែនសនន�(ម�២៦ថ���ស)

មតត

3

10.នេលើរយបនេចរែន�េលើកាែររែយបរែប�(ម�២៣ថ���ស)

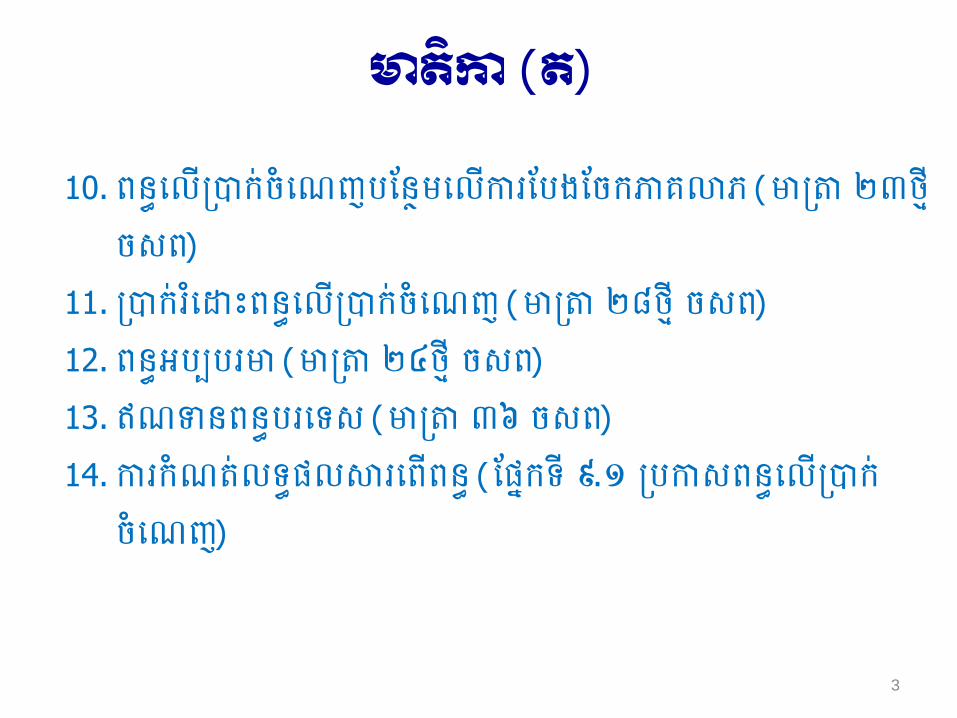

11. រយបាកេេ�នេលើរយបនេច�(ម�២៨ថ��ស) 12.នអររាម�(ម�២៤ថ��ស) 13.ឥចទននរាេទស�(ម�៣៦�ស) 14.កាយនចតបលទទលផាេើន�(ែទងយទ�៩.១�រកសនេលើរយប

នេច)

មតត()

4

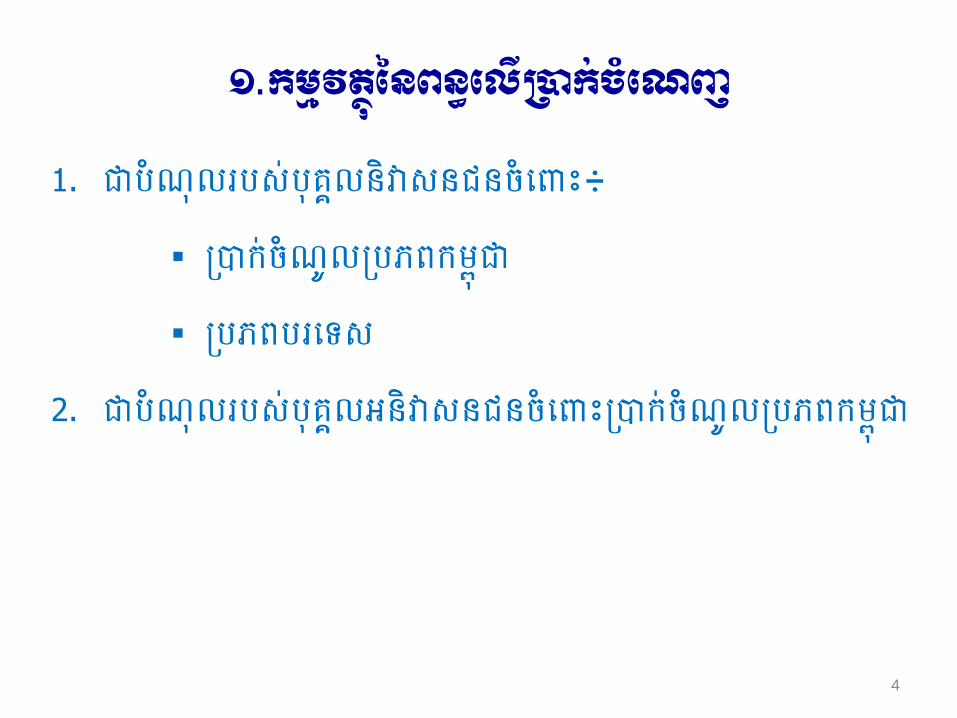

1. �រនចលារសបររគលនែនសនននេ�ព

រយបនចលរបយម���

របរាេទស

2. �រនចលារសបររគលអនែនសនននេ�រយបនចលរបយម��

១.ណច��តរៃរពងលើរណាជកងច

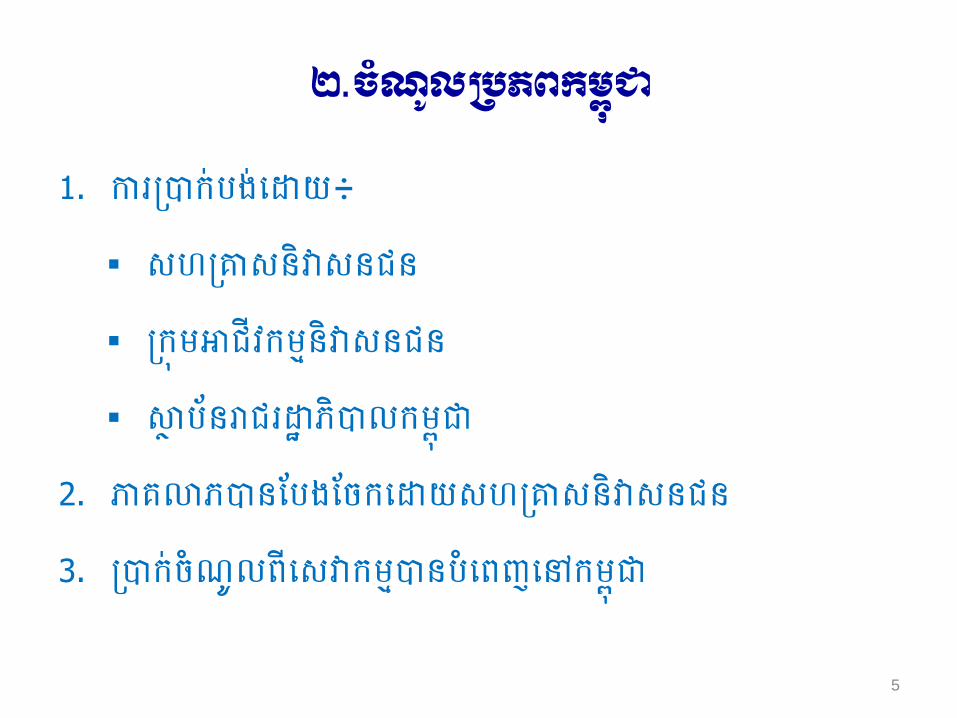

1. ការយបររបេេដព

សហរសនែនសនន�

យ�ឣវយ�នែនសនន��

ផ� រនរាេដ បែរលយម��

2. បរែបរនែររែយេេដសហរសនែនសនន

3. រយបនចលេសនយ�រនរនេេបយម��

5

២.ជកចលរបរណចររ

4. រយបនចល�ការរប ររ នែរ�េសនរេចយេទស�ែលរនទទតប��

េេដររគលនែនសនន

5. រយបនចលលនទព ឬ�អលនទព េរើទពេន�ស� ែតេប���

យម��

6. រយបសកដផារនយកាេរើរសប�ឬ�សែទែេរើរសបទពអារ��

ែលរនទទតបេេដររគលនែនសនន�ឬ�ររគលអនែនសនន

ាដៈ PE នរេបយម���

6

២.ជកចលរបរណចររ()

7. ទលនេច�កាលយបអលនទពស� ែតេបយម�� ឬ�ទលនេច

កាេទ�ាទលរេរនយ�ណកដៃនអលនទពស� ែតេបយម���

8. រ�ែបបនរារបារ�ឬបនរារបាររន�នេ�ងនែបដេបយម��

9. ទលនេចកាលយបលនទព�ែល�នែចយៃនទពឣវយ�

ារសប�PE ារសបអងយ�របនអនែនសននេបយម��

10. រយបនចលសយ�បឣវយ�ារសបររគលអនែនសនន����ា

ដៈ�PE េបយម���

7

២.ជកចលរបរណចររ()

៣.រណាជកងចររារព (ម៧ជសរ/ែផ�ណទ២.២ជសរ)

1. រយបនេចសទរនលទទលទនរអសបៃនរតែរតែកាាកទនរព

តនៃលេលើសរនកាលយបនែចយននៃនទពសយ�យង�រេល

យនររយរឣវយ��ឬេបេលរលចរបឣវយ��

រយបនចលយែចរតែរតែកាហែាលអវត���ឬវតនែេររ��

ការយប�

ៃថ�ឈង� ល�

សកដផា 8

៣.រណាជកងចររារព()

2. រយបនេច�របនេយើតេកាកតបយររង ានរព

នចលល�

នែររន��យទនរអសប

រតែរតែការរបរេបទយង�រេលយនរនេចើាកា�ឬេបេលរលចរប

ឣវយ��

9

៣.រណាជកងចររារព()

3. ននកនលនេអៀរានរតនៃលៃនទពសយ�សទនេលរែទ�នែរេលេរើយ

ៃនាដៈកលកដេេដព

យៈ��ឧរងាតតរែន�

រយៈ�កាយយេរើរសបរ� លបខ��ន

រយៈ�កាកតបយរដយនយង�ររ

10

3.រណាជកងចររារព()

4. តនៃ�េលើសសនេារនយង�រេលយហតទពសតែទ�វរបព

យង�រេលា�រអស�

ឬកាទទកលរយបសនចរបនរារបារ

5. កាលយបទននែ�ឬេសនសពមច សបបរទនៃថ�ទរ�រៃថ�ព�ែល

អនវតនេ�តតែដន

6. កាលរេលរនចលងរអយ�

11

៤.រណាជកងចររារព()

7. កាកតបរន�ដរនចលែលមច សបរនចលរនទលបសពសហរស

8. រចនទនរដៃនទពអយ�ែល�យបែសររ� នកាែត

9. ការេរេើតេតើរវតងរទពសយ�នវខ�របែលេប��េេដេហត

មនកាេយើនេតើរនវទពសយ�សទ�

12

៤.ត�តាណែសលអរល�

(ម១១ជសរ/ែផ�ណទ៥.១/៥.២ជសរ)

1. �រន��យ�ឬនណដ�រនទទតប ឬ តវសរ េបយង�រឆង ន�របនែល

អងយ�របនរនេព�ើេតើរេើរយរឣវយ��

13

៤.ត�តាណែសលអរល� ()

2. នណដរនេព�ើេើរនេាប�ឬ�រេរនយៃនឣវយ� ឣកតបយរ

រនល�ណរនេលយញខច� ៣�ងរេកព

រល� យបអ�ឣរេេដបស�រែលឣត�តែនែតពរន�(�វតយេដរត�

រតែេវទនយរដ�លែខែតេេ�ើដេ�រចែ�យ��យែចសន�ខច រយប�...

ែសរេនវលទទលសយ�បេស ដយែច

តវរនយនចតបសបែសប�(រនេព�ើរចេនដពយ�យង�រ

កាតដរាតេេទ��នែរមនបស�ររល� យបទបយរយប) 14

៤.ត�តាណែសលអរល� ()

រែន�េលើលយញខច� ៣ងរេលើ

1. នណដែនទនបរនទទតបេបនណបឆង នផាេើនព

តវ�រនចលែតរយ

តវមនកាយនហែតទាេេដមច សបរនចល�

ាកបរសសររនចលនបរតវទទតបែតរយ

15

៤.ត�តាណែសលអរល� ()

2. រយបេរៀវតៀែនទនបេរើយតវរនេរើយយង�រអនត�រេល�៦០�ៃថ��ៃនឆង ន

ផាេើនរន� រប

3. នណដែនទនបទទតបនេ�ររគលទយបទែន�នែរតវទទតបយង�រអនត�រ

េល�១៨០�ៃថ��ៃនឆង នផាេើនរន� រប�

16

៤.ត�តាណែសលអរល� ()

នណដែេសសេទៀរេទៀតព

1. ការយបៈ យនហែតតប�៥០% ៃនរយបនេចសទ�េេដព

យៈ�នចលការយប�

យៈ�នណដការយប�

រយៈ�នចលការយបែលរនទទកល�ឬតវរនទទកលយង�រឆង ន�រប

ន ��

ការយបេបសលបឣកតបយររនេបឆង នរនរន� រប�

17

៤.ត�តាណែសលអរល� ()

2. �វតបរទនសរ �ាសព�ែលរនរាត ច រលបព

ផ� រនាេដ បែរល�

អរគកាននេព�ើសយ�បែនែស�រាយរយបនេច �

យនហែតតប�៥% ៃនរយបនេច�របននេលកតបយរវតបរទន����

សរ �ាសព��

3. ាកលសបរបស ផាេើន

4. សនវតបនបននេ�ផ� រនពនរា�

18

៥.ត�តាណែសលចតអរល�

(ម១៩ជសរ/ែផ�ណទ៥.៣ជសរ)

1. កាយនផន�កាសនរយលនែហ�កាទទកលេបាϠវ�ឬកាេរើរសបេព�រដ

ណកដ�របទយបទែននបរសយ�បេន�

2. នណដសមរបកាាសបេបរ� លបខ��ន�ឬយ�រ�ផា�េលើយែលរែតអត�

រេរនយរែន��រយប�ឬ�វត��ែលរយបនរនកតបទយ រទ

រលអតែស នេលើរយបេរៀវតៀ

3. នេលើរយបនេច�នកតបទយ�នេលើរយបេរៀវតៀ�

19

៥.ត�តាណែសលចតអរល� ()

4. កាងតេលើកាលយប�ឬេេ�ាទពសតែេទ�េេដរ� លប�ឬ

រេរលានរររគលទយបទែន

5. នណដននែនទយបទរសយ�បឣវយ�

6. ាកលសប�ឬសនវតបនពនែលយតបខសេរលកាចយ�ឬយតបេលើស�

20

៦.ត�ងរត�ងរាងាចរង

(ម១៧ជសរ/ែផ�ណទ៩.៥TOP)

1. កាងតររបយង�រឆង ន�របនណកដតវតប�រន��យ�នែរកតបេ

រយបនេចយង�រឆង នរន� រប

2. ឣេររេាឆង ន�របនរន� របាហតលបឆង ន�របនទ៥

3. ឣកតបយររនល�ណែតមន�យង�រលែខែតរកស�ន

4. អងយ�របនែលារកាយនចតបន�នយេបរា ដរលផាេើន

ែនអនលអ តសពេររកាងតររបនយកតបយរេទ� 21

៦.ត�ងរត�ងរាងាចរង()

5. ឣកតបយររនល�ណែតមនអ�ឣរេេដរល� រចេនដពស

របេាយនចតប

6. ែនរ� សបរាមច សបសហរស

7. ែនរ� សបរាសយ�បឣវយ��

22

៧.អរព (ម២០ជសរ)

1. ២០% រយបនេចារសបនតែររគល

2. ៣០% រយបនេចេកយែចសន�ែររែរទលលែតទលព

េររកត�

ឧស� នព��តែ�

ពនបនព��តែាកទនរ�ៃេឈើ�ែាាមស�ឬតរថ�មនតៃ�នន

23

៧.អរព (ម២០ជសរ)

3. ៩% រយបនេចារសបរេមរ�រលរ�សនររបអនាកល�៥ឆង ន�រប

ៃថ�រកសេរើរបវតេផពនយ�ៃនរបវតនែេររ

4. ០% រយបនេចារសបរេមរ�រលរ�ស� ែតយង�រាដៈេលេលើយែលរ

ន�

24

បរៃនរយបនេចរ នឆង នតវ�របន អន

0` ដល 6,000,000 ` 0%

ព 6,000,000 ` ដល 15,000,000 ` 5%

ព 15,000,000 ` ដល 102,000,000 10%

ព 102,000,000 ` ដល 150,000,000 ` 15%

េលសព 150,000,000 ` 20%

រយបនេចារសបារវនររគល�នែរនែចយតវែររែយសពសមែយមង យបារសបយ�ឣវយ�ព

៧.អរព ()

25

៨.រពតាទរណងលើតនស (ម២៥ថ�ជសរ)

1. ១៥%

រយបនចលារវនររគលទទកល ការនេេសននន�កា

ររបររ�ឬកាែេរ�េររលប�ឬេសនរងយបរែហល

សកដផាទពអារ នែរបរយ�យង�រពនបនែាា ការយបែលអងយ

�របននែនសននរយរឣវយ� (ែនែន�ពនរាយង�រស�យ)

ររបសពអងយ�របននែនសនន�

26

៨.រពតាទរណងលើតនស ()

2. ១០% រយបនចលកាកលលន ឬអលនទព

3. ៦% ការយបែលពនរា�ររបសពអងយ�របននែនសននមនរចន

រេលអើមនកលយនចតប

4. ៤% ការយបែលពនរា�ររបសពអងយ�របននែនសននមន

រចនសនៀ នរ� នកលយនចតប�

27

៩.រពតាទរណងលើតនស ()

នកតបទយេលើររគលយង�រាររែតរង ព

នច�១.រ�ៃនេសយន នចបរេលខ�០២៨�យសហព

• នកតបទយតវរនយនចតបដយទរែានវនណដេលើការយប�សកដ

ផា�នែរកាកលានរអងយ�របនាររែតរង �

ែទងយទ៨.៦�ៃនរកសស នេលើ រយបនេច�យខច� ទ២�នចយ

• នកតបទយែនតវអនវតេទនេ�រយបនចលការនេេសននន�ាកទនរការរបររ�ឬកាែេរ�េររលប�ឬេសនរងយបរែហលារសបសហរសនតែររគលាររែត�

28

៩.រពតាទរណងលើអតនស (ម២៦ថ�ជសរ)

អងយ�របននែនសននរយរឣវយ��ែលរនទទតបរយបនចលងរេកសពអងយ�របនអនែនសននតវកតបទយ�នែរររបនវរយបន��១៤% ៃនទបយរយបតវេរើយព

1. ការយប

2. សកដផា�ៃថ�ឈង� ល�នែររយបនចលេទៀរទយបទែននបរកាេរើរសប

ទពសតែ

3. កាទទតបនេ�េសនររប ររ�នែរេសនរេចយេទសនន

4. បរែប� 29

១០.រពងលើរណាជកងចរែតចងលើត�ែរែជណបគលប

(ម២៣ថ�ជសរ)

1. ២០% ៃនទបយរយបតវែររែយនេ�ព

កាែររែយរយបនេចាយេទយ�ឬរយបនេចរ នឆង នេកដ

ររបនេលើរយបនេចអ�០%

កាែររែយៃទេទៀត�េលើយែលរនន២�នច៣�ងរេក

នែរការរបសរវតនវលពន�

30

១០.រពងលើរណាជកងចរែតចងលើត�ែរែជណបគលប ()

2. ១១/៩១ ៃនទបយរយបតវែររែយ�នេ�កាែររែយរយបនេច

ាយេទយ�ឬរយបនេចរ នឆង នែលរនររបនេលើរយបនេច

អ�៩%

3. នេលើរយបនេចែនតវអនវតេទនេ�កាែររែយរយប

នេចាយេទយ�ឬរយបនេចរ នឆង នែលរនររបនេលើ រយប

នេចអ�២០% ឬ�៣០%

31

១១.រណា�កងកពរពងលើរណាជកងច (ម២៨ជសរ)

1. សហរស�របនេលើ រយបនេចាររែត�នែរ�រលរ��របនេលើរយបនេចអ�៩% មនកត�យែចររបរយបាកេេ�រ នែខអ�១% ៃនទលាររែតាករលចលទនរនឣយាទនរអសប�េលើយែលរែត�អតរ

2. រលរ�ស� ែតយង�រាដៈេលេលើយែលរនតវរនេលើយែលរការរបរយបាកេេ�េន�

3. រយបាកេេ�នបរតវដយយកតបយរនេលើរយបនេចេបេលេព�ើកាទទតបរ នឆង ន�

32

១២.រពអររ�ម (ម២៤ថ�ជសរ)

1. អនវតនេ�អងយ�របនាររែត�នែរេលើយែលរ�រលរ

2. �នកដេេដែតយ�នែរេទៀរនេលើរយបនេច

3. ១% េលើទលាររ នឆង ន�ាករលចលទនរនឣយានន�េវៀែលរែត��

អតរ

4. តវររបេបេលទទតបនេលើរយបនេចរ នឆង ន�

33

១៣.ឥចទរពរ�ងទស (ម៣៦ជសរ)

1. អងយ�របនទទកលរយបនចលរបរាេទស�នែររនររបន

របនរាេទសតវរនទទកលឥចទនន

2. តវមននយផារល� យបការរបនេបរាេទស

3. ឥចទននែលអនលអ តសពកតបយរសមរបឆង ន�របនរននកនែល

ទរ�រេរយង�រនេណព

យ-រយបនែលរនររប�យបែសរេបរេទសេរណកដ

34

១៣.ឥចទរពរ�ងទស ()

ខ-ននកនែលរនយកាដយរយបនេលើរយបនេចសារររប

របសមរបាដៈេល�កដរង �ែលរចនអនយង�រ

ម២០�រចនបរទលែយានររយបនចលែលរនទទកលេប

រេទសេរេន��នែររយបនចលសារររបរប�

េរើឥចទននមនននកនេលើសរនចលន��ននកនេលើសឣេររ

េាេរើេបឆង នរនរន� របាហតលបឆង នទ៥�

35

១៤.ត�ណកចាលទពផល �ងរើរព (ែផ�ណទ៩.១ជសរ)

ការលចលយវត�នែរកាកតបេេទៀរព

1. រយបនេច�របន�ព�ែនេស� ើរង នបររយបនេច

រចេនដពេទ

2. េើរចនរយបនេច�របនៃនឆង ន�របនណកដ�តវដយ

លទទលរចេនដពៃនឆង ន�របនេន�យែយតវរបនេា

36

១៤.ត�ណកចាលទពផល �ងរើរព ()

សហរសស� ែតេបយង�រាដៈេលេលើយែលរន�តវេព�ើកាែយែរតវ

េររល� ករចេនដព�េេដដយលទទលរចេនដពេាេព�ើកាែយតវ

សពេា�រយបនេច/ងត�របន�សររប�នែររទរលអតែតស

ផាេើន�

37

សចអ�គរច!

38

KINGDOM OF CAMBODIA

NATION RELIGION KING

General Department of Taxation

Ministry of Economy and Finance

Presented by : Mr. SRUN ANGKAREN

Deputy Director of Large Taxpayer Department

TAX ON PROFIT (TOP) Siem Reap, 21st February, 2014

Contents 1. Objectives of Tax on Profit (Article 2 LOT) 2. Cambodian Source Income (Article 33(new) LOT) 3. Taxable Profit (Article 7 LOT) 4. Allowable Deductions (Article 11 LOT) 5. Not allowed as Deductions (Article 19 LOT) 6. Carry Forward of losses ( Article 17 LOT) 7. Annual Tax Rate (Article 20 (new) LOT) 8. Withholding Taxes on Resident Taxpayers (Article 25

(new) LOT) 9. Withholding Taxes on Non-resident Taxpayers (Article

26 (new) LOT)

2

3

10. Additional Profit Tax on Dividend Distributions (Article 23 (new) LOT)

11. Prepayment of Tax on Profit (Article 28 (new) LOT) 12. Minimum Tax (Article 24 (new) LOT) 13. Foreign Tax Credit (Article 36 LOT) 14. Determination of the Taxable Results (Section 9.1 TOP) 15. Determination of the Tax Exemption Period

Contents (cont.)

1-Objectives of Tax on Profit

1. is the debt of a resident person on

income from Cambodian sources and income from foreign sources;

2. is the debt of a non-resident person on income from Cambodian sources.

4

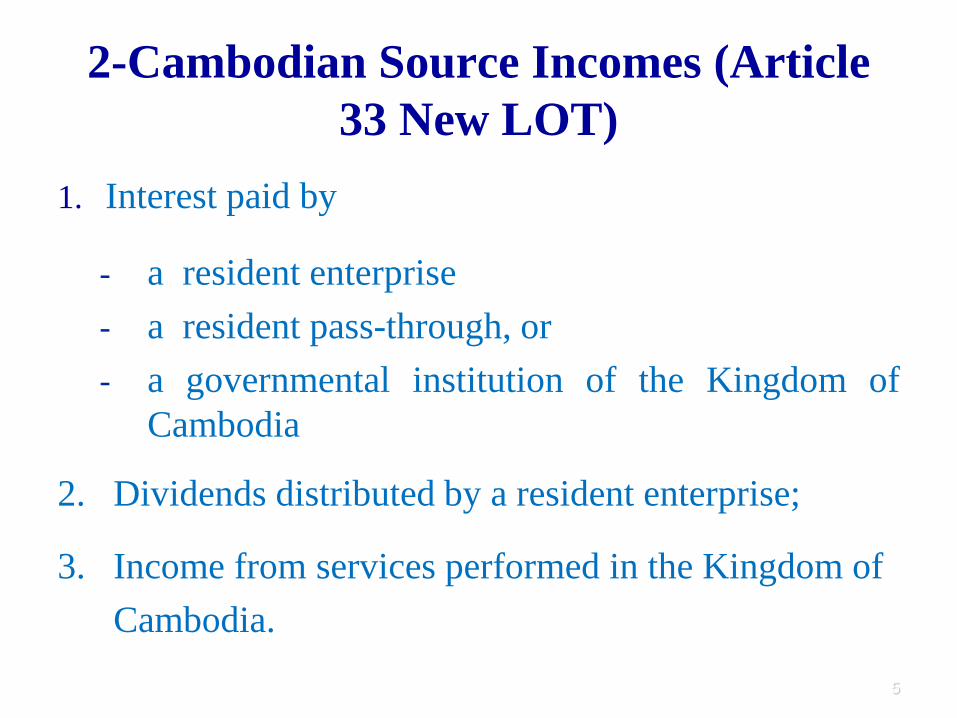

2-Cambodian Source Incomes (Article 33 New LOT)

1. Interest paid by

- a resident enterprise - a resident pass-through, or - a governmental institution of the Kingdom of

Cambodia

2. Dividends distributed by a resident enterprise;

3. Income from services performed in the Kingdom of Cambodia.

5

2-Cambodian Source Incomes (Cont.) 4. Income from Management and Technical Services paid by a resident person.

5. Income from movable or immovable property if such a property situated in the Kingdom of Cambodia.

6. Royalties from the use, or right to use intangible property paid by a resident or by a non-resident through a PE that he maintains in the Kingdom of Cambodia.

6

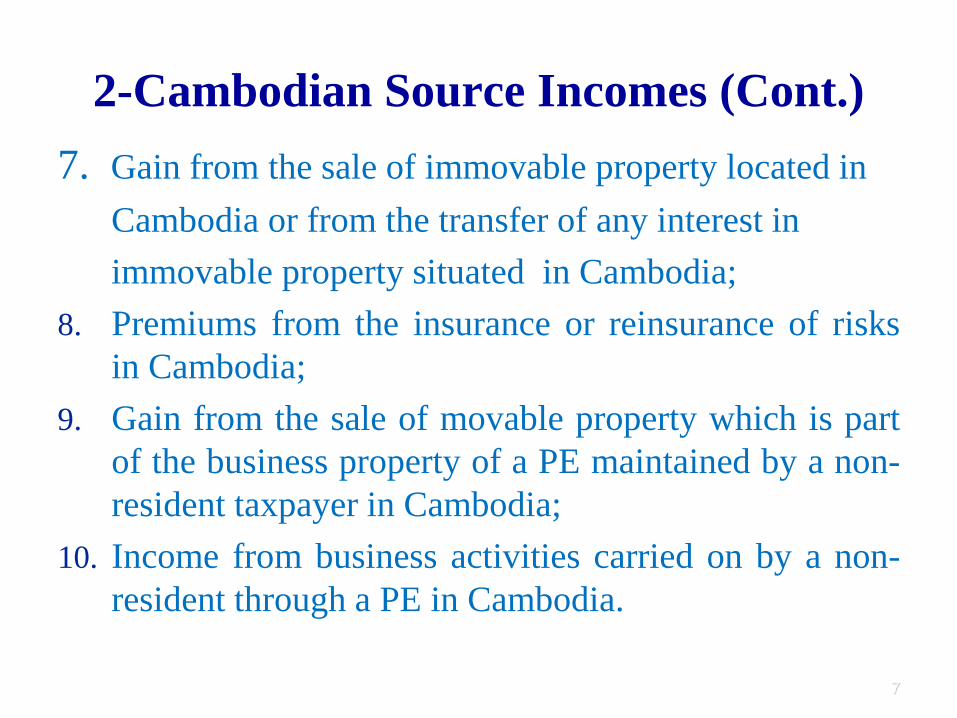

2-Cambodian Source Incomes (Cont.) 7. Gain from the sale of immovable property located in Cambodia or from the transfer of any interest in immovable property situated in Cambodia; 8. Premiums from the insurance or reinsurance of risks

in Cambodia; 9. Gain from the sale of movable property which is part

of the business property of a PE maintained by a non-resident taxpayer in Cambodia;

10. Income from business activities carried on by a non-resident through a PE in Cambodia.

7

3-Taxable Profit (Article 7 LOT/Section 2.2 TOP)

1. Is the net profit obtained from all the results of all types of operations realized by the enterprise including: capital gains from the sale of various parts of the

asset during the operation or at the close of the business

income from financial or investment operations interest rental, and royalty income

8

3-Taxable Profit (Article 7 LOT/Section 2.2 TOP) (Cont.)

9

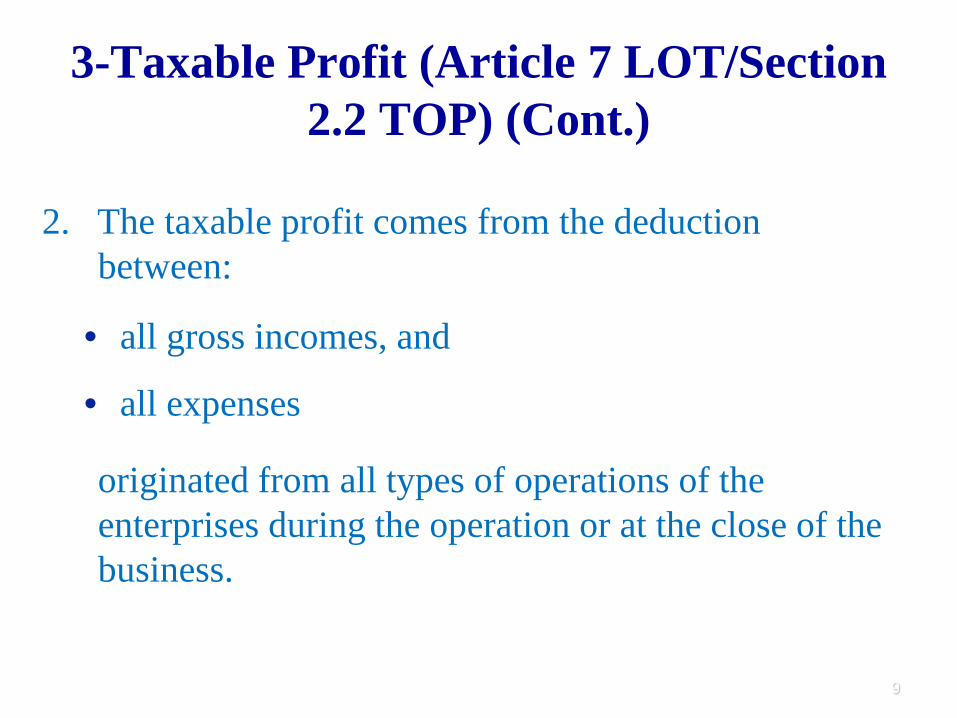

2. The taxable profit comes from the deduction between:

• all gross incomes, and

• all expenses

originated from all types of operations of the enterprises during the operation or at the close of the business.

3-Taxable Profit (Article 7 LOT/Section 2.2 TOP) (cont.)

10

3. is the difference between the values of the shareholders equity at the close and at the beginning of the taxable period by:

deducting : all additional capital contributions

adding up: all appreciations for personal use

adding up: advance deductions in the period

3-Taxable Profit (Article 7 LOT/Section 2.2 TOP) (Cont.)

11

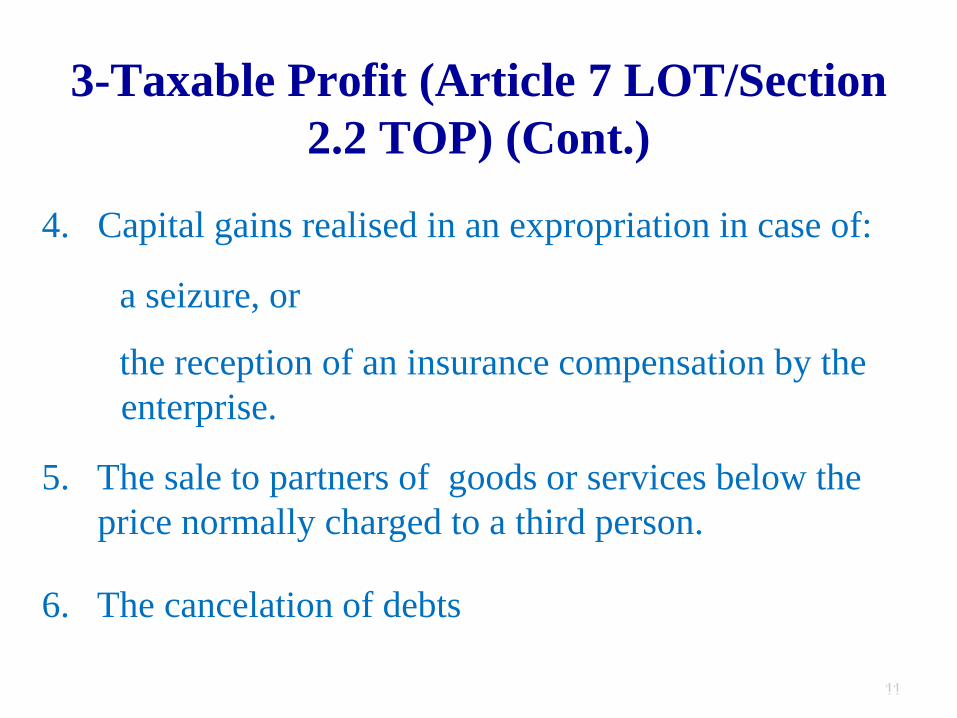

4. Capital gains realised in an expropriation in case of:

• a seizure, or

• the reception of an insurance compensation by the enterprise.

5. The sale to partners of goods or services below the price normally charged to a third person. 6. The cancelation of debts

3-Taxable Profit (Article 7 LOT/Section 2.2 TOP)(Cont.)

7. The reduction of debts that creditors granted.

8. Various liabilities accounts which do not exist in reality.

9. The recording in the assets of missed out items due to the fact that there is an increase in equity.

12

4-Allowable Deductions (Article 11 LOT/Sec. 5.1/5.2 TOP)

1. is a charge or expense which a taxpayer paid or is payable in the tax year to carry on the business.

13

4-Allowable Deductions (Article 11 LOT/Sec.5.1/5.2TOP)(Cont.)

14

2. Expenses incurred to serve the needs of or for the benefits of the business can be allowable unless it meets the following 3 conditions:

• Proven by verifiable evidence (invoice, custom declaration, business letters, loan agreements…)

• The result of economic activities.

• Precisely determined (accounted in the period with accurate evidence).

4-Allowable Deductions (cont.)

In addition to the 3 conditions above:

1. The unpaid expenses at the end of tax year must constitute :

• a genuine liabilities

• with the prove of enforceable claim by the creditor

• with a reasonable expectation that the debts will in fact be paid by the debtors.

15

4-Allowable Deductions (cont.)

2. Unpaid salary must be paid within 60 days of the following tax year.

3. Unpaid expenses to related parties must be paid within 180 days of the following tax year.

16

4-Allowable Deductions (cont.)

Other special expenses: 1. Interest expense : is limited to 50% of net profit

calculated by:

• deducting : interest income • Adding up : interest expense Then add up with interest income received or accrued in the tax year

The remaining interest can be used in the following year

17

4-Allowable Deductions (cont.)

2. Charitable contribution made to

Government institution, or

Non-profit organizations

is limited to 5% of taxable profit before charitable contribution deduction.

18

4-Allowable Deductions (cont.)

For an insurance enterprise:

The level of charitable contribution which is allowable in any one tax year is 5% of the gross premium in that tax year .

The remaining balance can not be carried forward for deduction in another taxable year. (Sec. 5.10 of TOP)

3 Depreciation as per LOT.

4 Provision for bad debts for banking institutions . 19

5-Not allowed as Deductions (Article 19 LOT)

1. Amusement, recreation, entertainment or the use of any means in connection with such an activity.

2. Personal living or family expenses except for fringe benefits in cash or in kind subject to withholding tax according to the provisions for the Tax on Salary.

3. Tax on profit, withholding tax, salary tax.

20

5-Not allowed as Deductions (Cont.)

4. For the loss on any sale or exchange of property, directly or indirectly, between related persons.

5. Any expense that is not related to business activities.

6. Depreciation or provision which is wrongly accounted for or overstated.

21

6-Carrying forward of Losses (Article 17 LOT)

1. A loss in any one tax year, is considered as a charge and deduct in the following tax year.

2. The remaining loss can carry over successively to the following tax year until the fifth tax year.

3. Can be deductible only if it is booked in the tax return.

4. Those with unilateral tax re-assessment are not allowed for deduction.

22

6-Carrying forward of Losses (Cont.)

5. Can be deductible only if it is proved by the account which is properly done in accordance with

the standards.

6. No change in shareholder.

7. No change in business activity.

23

7-Tax Rate (Article 20 LOT)

1. 20 percent for the profit realized by a legal person.

2. 30 percent for the profit realized under

• an oil production sharing contract

• natural gas production sharing contract, and

• the exploration of natural resources including timber, ore, gold, and precious stones.

24

7-Tax Rate (Article 20 LOT) (Cont.)

3. 9 percent for the profit of QIP to be entitled to the 5-year transitional period, starting from the tax year after the date of the promulgation of the Law on on the amendment of the Law on Investment.

4. 0 percent for the profit of QIP during the tax exemption period.

25

7-Tax Rate (Cont.)

The profit realized by a physical person and the distributive share to each member of a pass-through.

26

Parts of the annual taxable profit Tax rate

0 Riels to 6,000,000 Riels 0%

From 6,000,001 Riels to 15,000,000 Riels 5%

From 15,000,001 Riels to 102,000,000 Riels 10%

From 102,000,001 Riels to 150,000,000 Riels 15%

greater than 150,000,000 Riels 20%

7-Tax Rate (Cont.)

For an enterprise having principal activity in the insurance or reinsurance of life, property, or other risks, the tax on profit shall be determined as follows (Article 21):

• 5 percent of the gross premiums received in the tax year for the insurance or reinsurance of risk in the Kingdom of Cambodia,

• According to the rates in Article 20 for other activities that are not insurance or reinsurance.

27

8-Withholding Tax on the Resident Taxpayer (Article 25(new) LOT)

1. 15%

• income received by physical person from the performance of services including management, consulting, and similar services;

• royalties for intangible and interest in minerals, and interest paid by resident taxpayer (other than domestic bank ) to a resident taxpayer.

28

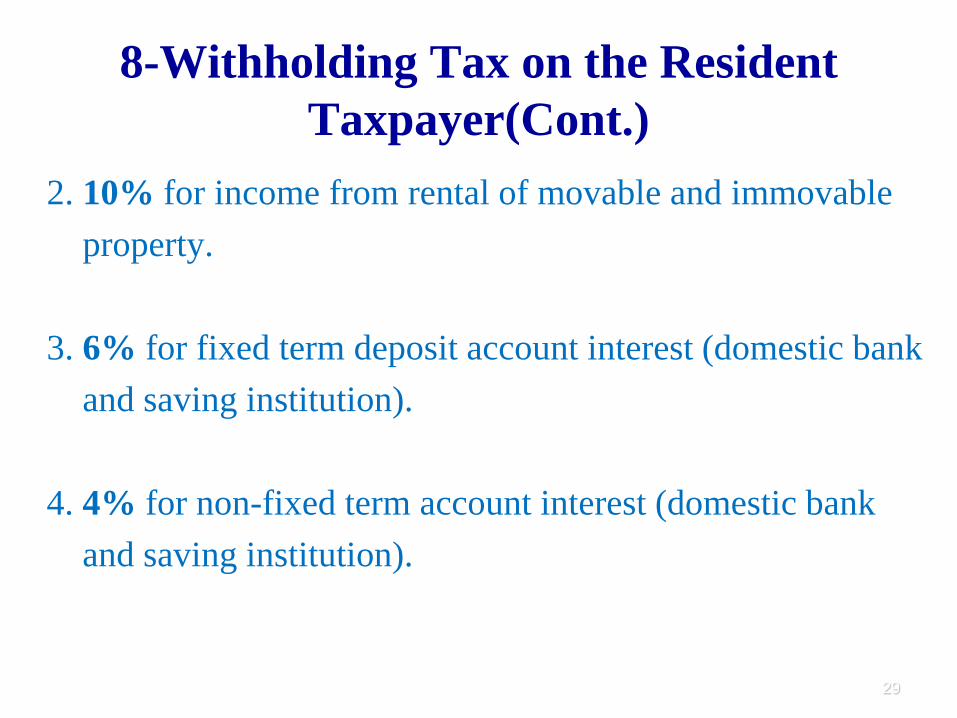

8-Withholding Tax on the Resident Taxpayer(Cont.)

2. 10% for income from rental of movable and immovable property. 3. 6% for fixed term deposit account interest (domestic bank and saving institution). 4. 4% for non-fixed term account interest (domestic bank and saving institution).

29

9-Withholding Tax on the Non-resident Taxpayer (Article 26(new) LOT)

Any resident taxpayer carrying on business and who makes any of the following payments to a non-taxpayer shall withhold, and pay a tax , an amount equal to 14% of the amount paid:

1. interest; 2. royalties, rent , and other income connected with the use of property; 3. compensation for management and technical services; 4. dividend.

30

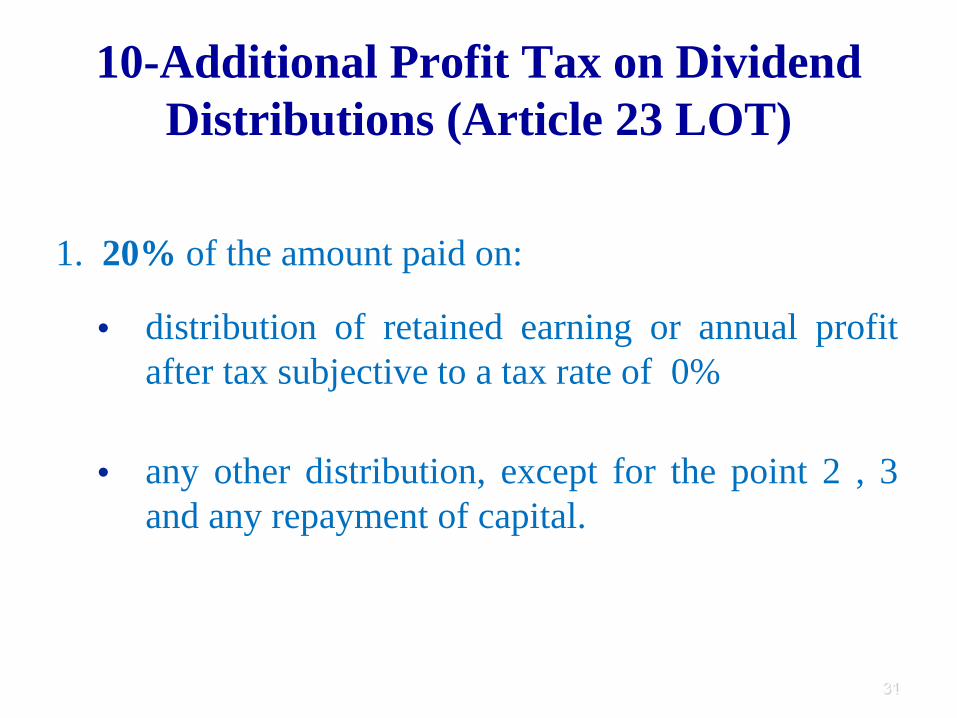

10-Additional Profit Tax on Dividend Distributions (Article 23 LOT)

1. 20% of the amount paid on:

• distribution of retained earning or annual profit after tax subjective to a tax rate of 0%

• any other distribution, except for the point 2 , 3 and any repayment of capital.

31

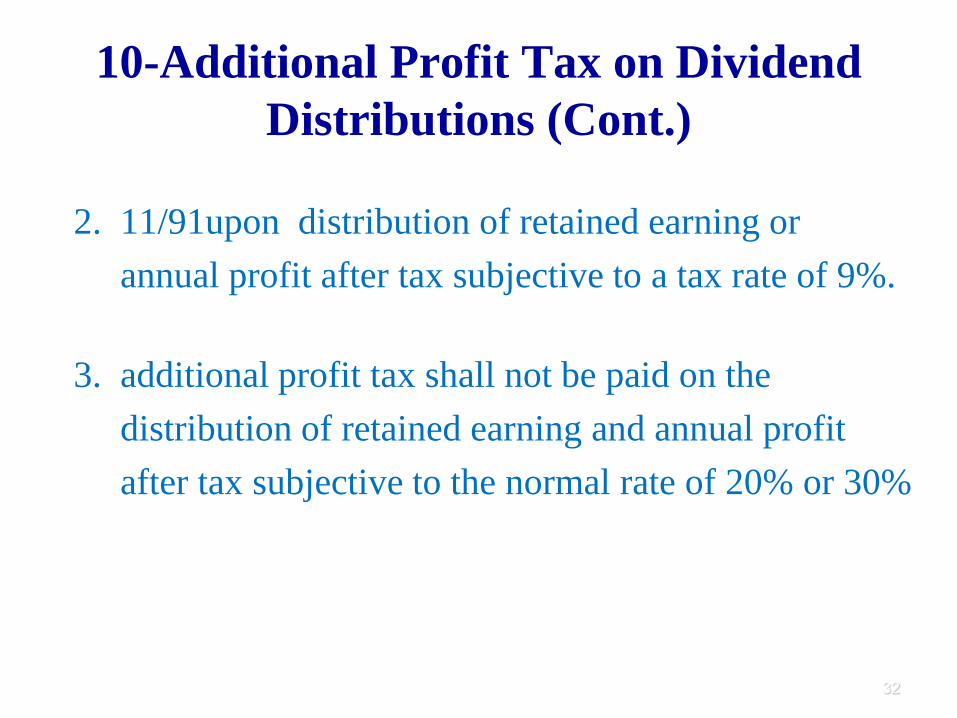

10-Additional Profit Tax on Dividend Distributions (Cont.)

2. 11/91upon distribution of retained earning or annual profit after tax subjective to a tax rate of 9%. 3. additional profit tax shall not be paid on the distribution of retained earning and annual profit after tax subjective to the normal rate of 20% or 30%

32

11-Prepayment of Tax on Profit (Article 28 LOT)

1. An enterprise liable to the tax on profit according to the real regime system of taxation and QIP liable to the tax on profit at the rate of 9%, has the obligation to pay a monthly prepayment at the rate of 1% of the turnover inclusive of all taxes , except VAT. 2. QIP within the exemption period shall be exempted from this prepayment. 3. The prepayment will be deducted from the tax on profit at the annual liquidation of the tax.

33

11-Prepayment of Tax on Profit (Cont.)

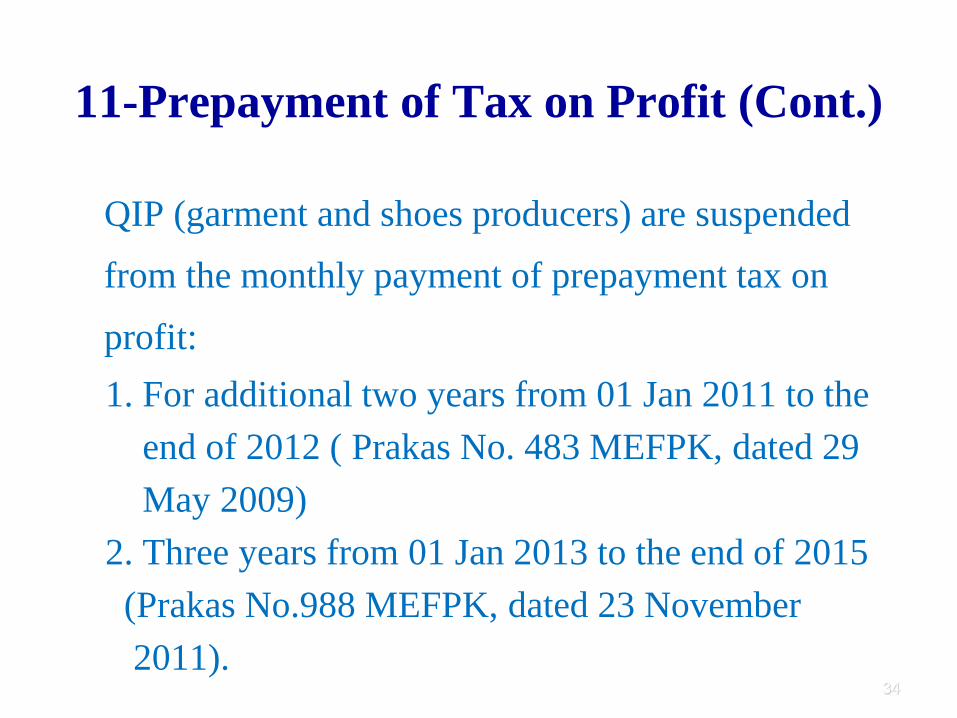

QIP (garment and shoes producers) are suspended

from the monthly payment of prepayment tax on

profit: 1. For additional two years from 01 Jan 2011 to the end of 2012 ( Prakas No. 483 MEFPK, dated 29 May 2009) 2. Three years from 01 Jan 2013 to the end of 2015 (Prakas No.988 MEFPK, dated 23 November 2011).

34

12-Minimum Tax (Article 24)

1. is imposed on taxpayers subject to real regime system except the QIP.

2. is a separate and distinct tax from the tax on profit.

3. 1% of annual turnover inclusive of all taxes, except VAT.

4. is payable at the time of the annual liquidation of the tax on profit.

35

13-Foreign Tax Credit (Article 36 LOT)

1. A resident taxpayer who has received income from foreign sources and who has paid taxes according to the foreign tax law shall receive a tax credit for deduction from the tax on profit. 2. must prove documents confirming this tax was paid abroad. 3. The tax credit to be allowed for deduction in the tax year is the smaller of: A. the tax amount actually paid in a foreign country;

36

13-Foreign Tax Credit (Cont.)

B. the amount obtained by multiplying the total tax on profit from all sources for the same period calculated according to the LOT tax rate in article 20 with the ratio of income received in that foreign country to the total income from all sources. In the case where the tax credit exceeds the tax liability the amount of excess may be carried forward to be used in succeeding years up to the fifth.

37

14-Determination of Taxable Results (Section 9.1 TOP)

Write backs and deductions: 1. Normally, taxable profit is not the same as accounting profit.

2. In order to calculate the taxable profit of a tax year, enterprise must take the accounting results of that

year and carried out various adjustment in according with the law on taxation.

38

14-Determination of Taxable Results (Cont.)

During the exemption period, enterprise shall make adjustments outside its accounting system by adjusting accounting results to taxable profit/loss in accordance with tax law.

39

រពះរជណណចររ រត សារពចណព

អគ�ាណកដ រពក� ណសសងសសដណតជចត ត�រ��តរ

ឧេទ�សនេេដ : ងលណែ ពសឌ អនរបននដយេដ នសវនយ�សហរសា

រពងលើរណាងក�ព (េសៀររ ៃថ�ទ២១ាែខយ�ៈាឆា ២០១៤ )

មតត ១.យ�វត��ៃនពន� ២.នដនដ ៣.រយាេរៀវតេេលយែេលពន� ៤.េេដ ននតពន�ររែខ ៥.រយាេរៀវតសរាពន�ររែខ ៦.កាយណតារយាពន�ររែខារសានេបសត ៧.កាយណតារយាពន�េេលអតើ រេបសនេរែនើ ា៨.កាយណតាពន�េេលរយាេរៀវតារសាអាយសរាពន�អននសនសន ៩.កតពតយការសានេបសយ នលនេបសត

2

១.ណច���រៃរព

ពន�េេលរយាេរៀវតានសពន�ររែខយណតាេេល រយាេរៀវតែែេរនទទនេយា�លយរខណក ៃនការេពសយ�ភពរេាេកាកាារ

ារវន�រន�េននសនសនេេយា�លពររសរកយយច�សាត�វសរាពន�េេល រយាេរៀវតរតពយច�សានលរយាេរៀវតរតពរាេទសារ

ារវន�រន�េអននសនសនាត�វសរាពន�េេល រយាេរៀវតរតពយច�សារ

3

២.តច

សររាេរេេគៃនរទរៃនបត�ស� ពពន�េេលរយាេរៀវតស

១. ពយា“ននសនសន” យា�លយាណែែេេរលកេពរនេបសតាអាយសរាពន�ាារវន�រន�េារននដែែេរនននសនេដ នរនយែននលមា យាេេសេរេេែលេេយា�លពររសរកយយច�សាែែេរនវត�រនេេយា�លពររសរកយយច�សេេលសព១៨២ាៃថ�ាេេយា�លាដៈេពេ១២ាែខារនដែែេរនរនរាយា�លឆា មាេពលពន�កាន� រ

២. ពយា“អននសនសន” រននដារន�េរនដែែេនែនសននសនសនតយខណក ខលេេលានលទទនេរយាេរៀវតរតពយច�ស រ

៣. េវៀាែេលែតរនរទរៃនបត�ត��ដាកាេរលពយនេបសតាអាយសរាពន�ានលារវន�រន�េានសេគែេាទលននសសនានលអននសសន រ

4

២.តច ()

៤. ពយា“នេបសយ” ានរនមើ រនាែដនតរន�េននសនសនាយ�ឣសវយ�ននសនសនានរមើ នអកៃនន�ដេេេយា�លពររសរកយយច�សាអល�កានែសតលាយរយាកេណាារវន�រន�េននសនសនាែែេរយរឣសវយ� រ

៥. ពយា“នេបសត” សេគែេាារវន�រន�េែែេទទនេរនរយាេរៀវតអពសយ�ភពរេាេកាកាារសាខនរនាានរន�េទលអាយទទនេខសត�វអតរេារសាសហរសានន�រសកាានន�េសលសតលេេដកាេររេឆា តាេេលយែេលែតសរសយាែដសភានលពទ�សភ រ

5

២.តច ()

៦. ពយា“រយាេរៀវតរតពយច�សា” រននដារយាេរៀវតែែេរនទទនេយា�លយរខណក ៃនការេពសយ�ភពរេាេកាកាេេយា�លពររសរកយយច�សរាេេដែយកេពររយាេរៀវតាែែេអននសសនរនទទនេយា�លកាត�េាសននដរេកយេទសត�វរតាទយរនរតពេេយា�លរេទសែែេអាយទទតាេនរមា យាេេារ

៧. ពយា“រាេទសា” ស

យ. េពេរេរលសនដារវន�រន�េារននដែែេសអននសសន

ខ. កេពរកាយណតារតពរយាកណេារននដេមពររសរកយយច�សារ

6

២.តច ()

៨. ពយា“រយាេរៀវតា” សេគែេាេរៀវតា តកាារយាររកាារពត តារយាេរលរែនើារយារររវននានលអតើ រេបសនេារែនើែែេរនទទតាែេានេបសតាែែេរនទទតាេែលៃសរេបសនេរ� េាារេបេែេានេបសតកេពរការេពសយ�ភពារេាេកាកាារ

7

៣.រណាងក�ពងលើណែលរព

កាេេលយែេលពន�េេលរយាេរៀវតារសានន�កាទតានលនន�រាេទសែេៃទាេទៀតត�វរនយណតាែកតេ�ស

១. ត�វរនេេលយែេលពន�េេលរយាេរៀវតកេពរស

យ. រយាេរៀវតែែេនន�ានលនេបសតៃនេរសយយ�ទតាយលសេារសារសាេដ តរេរាេទសរនដាែែេកនាេខតឆនលែែនកាទតាតន�វកាារសារេទសេនរារនទទនេយា�លយរខណក ៃនការេពខកាសតន�វកាេេយា�លពររសរកយយច�សារ

8

៣.រណាងក�ពងលើណែលរព()

ខ. រយាេរៀវតែែេតរលនន�ានលនេបសតរាេទសារសាអល�កាអន�ាសតានលារសាទភា យាកាខលសហរតរត�ការេកយេទសៃនាេដ តរេែេៃទេទៀតារនទទនេយា�លយរខណក ៃនការេពខកាសតន�វកាេេយា�លពររសរកយយច�សារ

២. កាេេលយែេលពន�យា�លកនកេនរាត�វវាេេលេរេកាណេរែកាានលាេដ តរេែែេពយាពន�ារ

9

៣.រណាងក�ពងលើណែលរព()

រយាកណេេេលយែេលពន�ារសានេបសតាត�វរនេេលយែេលពន�ាស

១. រយាសណលេេដពតរយែនវករដខលវសខ សវៈាែែេរនរដេេដនេបសតតេសកយ�រក� រាានលសររាសរេបសនេៃននេបសយាេហលដែែេរនរេពេយលខណក ៣ាែកតេ�ស

យ. រនរដយា�លរេបសនេរ� េាានលេកាខតារសាសហរស

ខ. នរក េយលណៈហនសររណស��យស��ហនសេហត

ន. រនរក សតស��តលេេដវយដរតរដេអតានលរនទទតាាេសករកាាេហលដែែេរនេបតលយា�លនអាយរនទទនេរយាសណលនវាករដពតរយែារ

10

៣.រណាងក�ពងលើណែលរព()

រយាកណេេេលយែេលពន�ារសានេបសតាត�វរនេេលយែេលពន�ាស

១. រយាសណលេេដពតរយែនវករដខលវសខ សវៈាែែេរនរដេេដនេបសតតេសកយ�រក� រាានលសររាសរេបសនេៃននេបសយាេហលដែែេរនរេពេយលខណក ៣ាែកតេ�ស

យ. រនរដយា�លរេបសនេរ� េាានលេកាខតារសាសហរស

ខ. នរក េយលណៈហនសររណស��យស��ហនសេហត

ន. រនរក សតស��តលេេដវយដរតរដេអតានលរនទទតាាេសករកាាេហលដែែេរនេបតលយា�លនអាយរនទទនេរយាសណលនវាករដពតរយែារ

11

៣.រណាងក�ពងលើណែលរព()

២. រយាររកាៃនការនររាែេលេបតលកាាយា�លយតែែេរនរនបត�យា�លាករាកាកាារ

៣. តការែនើរនេយលណៈខលសល�យកាយា�លយាណែែេរនរនបត�យា�លករាកាកាារ

៤. កាត�តាត�លាេេដតដយៃថនាដយៃថនទរសលៃថនេែលនវើយសរដ នារាកល ាសររាវសខ សវៈពេសសារ

៥. រយាររកាេេកាសររាករដេរសយយ�ានលកាេបតលែេណលារារយាររកាេនរានត�វតរតរា សនដរយាសណលពតរយែានវករដែករនែកលខលេេលេលដារ

12

៤.ចលកដ គតរពករបែា

េវៀាែេលែតអតើ រេបសនេរែនើាែែេត�វយណតាេេដែយាា េេដ ននតពន�ររែខារសាននសនសនានសរយាេរៀវតសរាពន�េេដរតាេកនវស

១. រយាកតាទយែែេសកតពតយកយា�លការតរត�តករាកាកាាេែលៃរេលលតេរបេមបនានលបនសខរេភពសល�ារ

២. កាទទតាននាែែេត�វរនេេលយែេលពន�ែករនែកលខលេែលារ

13

៥.រណាងក�ពរការពករបែា

រយាេរៀវតសរាពន�ររែខត�វរនយណតាែកតេ�ស

១. រយាេរៀវតសរាពន�ររែខារសានេបសតននសនសនានរនស

យ. រយាេរៀវតែែេរនទទនេពរតពយច�ស

ខ. រយាេរៀវតែែេរនទទនេពរតពរាេទស

ន. រយារេារទនារយាខរយាាេេរែែេនេបសយរនេរលយនេបសតរារយារេារទនារយាខរយាាេេរត�វរយរែនើេេលេរៀវតសរាពន�ៃនែខែែេរយាទលេនររនេរលយាេហលដត�វកតារនើដពរយាេរៀវតយា�លែខែែេនេបសតរនសលាវារ

14

៥.រណាងក�ពរការពករបែា()

២. ែត�យេេលការក តស��តលៃនមើ នភពនរមាានេបសតននសសនរនដែែេរនស

យ. យនសើ តយា�លរន��យនេពេែែេត�វរលាពន�ាត�វរនទទនេនវការនើដេេដ នយណតាពន�កនននា៧៥.០០០ាេាៀេា(រពានរពាពនាេាៀេ) យា�លយនរាយាៗាយា�លនដែខារ

ខ. សហពទ�ែែេេបតលែតេត�រាត�វរនទទនេនវការនើដេេដ នយណតាពន�កនននា៧៥.០០០ាេាៀេា(រពានរពាពនាេាៀេ) សររាែតរា យាយា�លនដែខារ

៣. កេពរអាយសរាពន�អននសនសនារយាេរៀវតសរាពន�ានរនរយាេរៀវតរតពយច�សាែែេត�វសរាពន�តរទរៃនបត�ទលបដាៃនសពយេនរារ

15

៦. ត�ណបការណារពករបែា�កសាតងខរត សររានេបសតននសសនារយាពន�ត�វរលាត�វយណតាេេលរយាេរៀវតសរាពន�ររែខានលត�វកតាទយេេដនេបសយាាតអតយេណលនត ា យាាែកតេ�ស

ភនេរៀវតររែខត�វសរាពន� អតពន�

ព 0 ែេា 500,000 0%

ព 500,001 ែេា

1,250,000 5%

ព 1,250,001 ែេា

8,500,000 10%

ព 8,500,001 ែេា

12,500,000 15%

េេលសព 12,500,000

20% 16

៧.ត�ណបការណារពងលើអតកងខររកែតច

កេពរអតើ រេបសនេរែនើាសេាៀលរេាែខនេបសយត�វកតាទយនលរលារយាពន�តកេយណតាាតអត២០ាភនាដាៃនតៃនសារារសាអតើ រេបសនេរែនើែែេរនត�េា នេបសតទលអសារាតៃនៃនអតើ រេបសនេរែនើានសតៃនទតទាានទលពន�ឣយាទអសាារ

17

៧.ត�ណបការណារពងលើអតកងខររកែតច()

អតើ រេបសនេរែនើែែេនេបាសយត�េាេេដរ� េាាតាដៈតតដសនែេាារវន�រន�េាត�វសរាពន�ាេេលអតើ រេបសនេរែនើរាអតើ រេបសនេរែនើទលេនររនសឣទស

យ. បនសនរនរារេតទ

ខ. �រឣា

ន. េេេេដ នាកាមា យាេេ

ឃ. ទយាេតនលលាទាសព�

ល. អាយរេលកាកាយា�លេេេេដ ន

ក. រយាខដេេដនតការយាទរសលការយាទតទារាអតការយាទតទាែែេត�វដយយអនវត�ត�វយណតាេេដយសនលាសហវ រ

18

៧.ត�ណបការណារពងលើអតកងខររកែតច()

ឆ. កាេយាទនករៃថន

ស. សននដែតាយអរាាសររានេបសតែែេនែនសកែណយរនដាៃនយ�វបរណ�� រររ� េទយាទនរ� េាេ�នលការេពកាកាារសានេបសតេនរ

វ. សននដែតាយអរាាសររាយនារសានេបសត

. រពត តបនរារាាលឣដសវតាសខភពាេេលយែេលែតរនត�េាអតើរេបសនេរែនើែករា ែេានេបសតនរារា េេដរ� នកាែរលែកយតតននទាខកាារ

ែ. កែណយៃនកាឧរតើ�េេលករដែែេនសេហតតេានលនររកាសររាឣសវយ�ារ

19

៧.ត�ណបការណារពងលើអតកងខររកែតច()

ឋ. កនននរយារលាកេេនបសខរេភពសល�ែែេេេលសពយាាតែែេករារនអន�ប ត

ឌ. កនននរយារលាកេេរបេមបនែែេេេលសព១០ាភនាដាៃនរយាេរៀវតររែខរ� នរយអតើ រេបសនេរែនើារសានេបសត

ឍ. ករដសររាកាទទនេេតទ វាកាយមន�ាកាសរយេែហាកាេរលរសាេបរដរនដែែេទយាទននលសយ�ភពទលេនរែែេនែនសកែណយរនដៃនទនយាទនលរេាេកាកាារ

20

៨.ត�ណបការពងលើរណាងក�ព�កសាអសណរការព អតវសរ

សររាអាយសរាពន�អននសនសនារយាពន�ត�វកតាទយេេដអាយេរលយរយាតអត២០ាភនាដាេេលរេាកាទទតារយាេរៀវតសរាពន�រាពន�កតាទយេនរានសពន�កលេកដៃនពន�េេលរយាេរៀវតាសររាអននសនសនាសអាយទទនេរយាេរៀវតារ

21

៩. តរតណតជច�កសាតងខរណតតងខរត

េហតររ� េសរាពន�ាស

កាេរលយេរៀវតារេលលតសេហតររ� េសរាពន�ារ

22

៩. តរតណតជច�កសាតងខរណតតងខរត()

រណេពន�ានលកតពតយកកតាទយរយាពន�ាត�វរនយណតាែកតេ�ៈ

១. ពន�េនរនសរណេារសាារវន�រន�េែែេរនទទនេរយាេរៀវតាានទលារវន�រន�េរាេទសតលាេវៀាែេលែតរនរទរៃនបត�ត��ដាែែេរនែកលយា�លយកពេពលអន�ាសតារ

២. ពន�េេលរយាេរៀវតត�វរេាតាេរៀរកតាទយសនសេាៀលរេាែខេេដនេបសយេេរេាេពេេរលយរយាារ

៣. រសនេរលនេបសយមា យាេេរាេទសាតរលមាេពលពន�េេពររសរកយាែែេនេបសយរនរតាតលានសអាយទទនេភាៈកតាទយពន�េេលរយាេរៀវតានេពេេរលយរយាេរៀវតេ�នេបសតានលរែលតារយាពន�ទលេនរសនាែដារ

23

៩. តរតណតជច�កសាតងខរណតតងខរត()

៤.នេបសយាតរលននសនសនេេពររសរកយយច�សារសានេបសយរាេទសាេហលដនលនេបសតត�វទទនេខសត�វានរា យា�លការលាពន�េេលរយាេរៀវតយា�លពររសរកយាេេដពយណតារយាេរៀវតរនេរលយេេពររសរកយយច�សាេេរាេទសេលដារាយា�លយាណានរនកតាទយរយាពន�េេលរយាេរៀវតានេបសយត�វទទនេខសត�វកេពរខករាេនរាេទររសរយាពន�ត�វរនរលាេេដានេបសតានកេហលដយ�ារ

24

៩. តរតណតជច�កសាតងខរណតតងខរត()

ការលារយាពន�ែែេរនកតាទយស

រយាពន�កតាទយែែេទយាទលែេាកាេរលយរយាេរៀវតេបតលេលលយា�លែខរនដាត�វរលាបលដតរតតេេៃថ�ទ១៥ាៃនែខរន� រាសនេ�ាែដរេាមាេពលពន�េេទយែននលៃនេេេេដ នានរមើ នសេរេេែលៃនអាយទទនេភាៈកតាទយរយាពន�េនរារ

25

៩. តរតណតជច�កសាតងខរណតតងខរត()

នរានេបសយែែេេរលយរយាេរៀវតសរាពន�ាត�វទទនេភាយកស

កតាទយរយាពន�នេពេេរលយរយាេរៀវតារ

រដកាណេសនាែដរេមាេពលពន�ានលនេបសតអពមើ នភពរយាពន�ាែែេរនកតាទយារ

កនាករាានលែថាយទរនខ កាែែេយណតាេេដរកសារសាយសនលេសែដយកានហហានបវតើ�ារ

26

សចអ�គក!

27

KINGDOM OF CAMBODIA

NATION RELIGION KING

General Department of Taxation

Ministry of Economy and Finance

Presented by : Mr. TE JEUDI

Deputy Director of Department of Enterprise Audit

TAX ON SALARY Siem Reap, 21st February, 2014

CONTENTS 1. Objective 2. Definition 3. Salary Exempted 4. Monthly Tax Base 5. Monthly Salary Taxable 6. Determination of the Monthly Tax of Employees 7. Determination of the Tax on Fringe Benefits 8. Determination of the Monthly Tax of Non- Resident 9. Obligation of Employers and Employees

2

1.Objectives

The Tax on salary is a monthly tax imposed on salary that has been received within the frame work of fulfilling employment activities.

A physical resident person in the Kingdom of Cambodia is liable to the tax on salary for Cambodian source and foreign source salary.

A physical non-resident person in the Kingdom of Cambodia is liable to the tax on salary for Cambodian source salary.

3

2. Definition The term “Resident” when used for an employee, taxpayer, or

physical person means has his residence in or his principal place of abode in the Kingdom of Cambodia, or who is present in the Kingdom of Cambodia on more than 182 days in any period of twelve months ending in the current tax year.

The term “Non-Resident” means any person who is not a resident according to paragraph 1 and receives salary from Cambodian source.

Except for contrary provisions, any reference to the terms employee, taxpayer and physical person are references to both resident and non-resident as defined in this article.

4

2. Definition (cont.) The term “Employer” includes any government

institution, any resident legal person, any resident pass-through, any permanent establishment in the Kingdom of Cambodia, any non-profit organization, or any resident physical person carrying on a business.

The term “Employee” means any physical person receiving salary from their employment activity including any responsible officer or director of an enterprise, any governmental officer, any elected official except for members of parliament and senate.

5

2. Definition (cont.) The term “Cambodian Source Salary” means salary

received within the framework of fulfilling employment activities in the Kingdom of Cambodia. As for the salary received by a non-resident for furnishing technical assistance it shall be treated as from sources in the country where the payer of such income resides.

The term “Foreign” means: when used with respect to an physical person means non-

resident for the determination of the source of income, means outside of the Kingdom of Cambodia.

6

2. Definition (cont.)

The term “Salary” in this Law means salary, remuneration, wages, bonuses and overtime, compensations and fringe benefits which are paid to an employee or which are paid for the direct or indirect advantage of the employee for the fulfillment of employment activities.

7

3. Salary Exempted

The tax exemption for the salary of diplomatic and foreign officials shall be as follows: 1- Shall be exempted from the tax on salary:

a. Salaries those officers and employees of a diplomatic or consular mission of foreign government holding a diplomatic or official passport of that government have received within the framework of fulfilling their official function in the Kingdom of Cambodia.

8

3. Salary Exempted (cont.)

b. Salaries those foreign representatives, officials and employees of international organizations and agencies of technical cooperation of other government have received within the framework of fulfilling their official function in the Kingdom of Cambodia.

2- Any tax exemption in this article shall be based on the principle of reciprocity between the government concerned.

9

3. Salary Exempted (cont.)

Real refunds on professional expenses made by the employee under the assignment and for the benefit of the employer and which satisfy the 3 following conditions: Made for the direct and exclusive interest of the

enterprise. Not exaggerated nor extravagant. Supported by detailed invoices already paid and made

in the name of the recipient of the real expense refund.

10

3. Salary Exempted (cont.)

Indemnity for the layoff within the limit as provided in Labor Law.

Additional remuneration with social characteristics where there is provision in Labor Law.

Supply gratis or below acquisition cost of special uniforms or professional equipment.

Flat allowance for mission and travel expenses. This allowance should not be overlap the real expense refund provided in this article.

11

4. Monthly Tax Base

Except for fringe benefits taxable under art.48 of this LOT, the monthly tax base for a resident is the taxable salary from which is deducted: - Withholding obligations as the result of the

compliance with the Labor Law in order to create pension and for the maintenance of social welfare

- Payment which are allowed to be tax exempt in art.44 of this LOT.

12

5. Monthly Taxable Salary

Monthly taxable salary for a resident employee includes: Salary from Cambodian source Salary from Foreign source Advance money, loan or installment made by

employer to employee which shall be added to the taxable salary of the month in which they are paid out and shall be deducted from salary in the month of any repayment made by the employee.

13

5. Monthly Taxable Salary (cont.) Based on the evidence of family situation, any resident

employee with: - Minor dependent children at the time of tax payment is

allowed a reduction in the tax base of 75,000 riel per each.

- Spouse having only an occupation as housewife is allowed a reduction in the tax base of 75,000 riel for one person only per month.

For a non-resident taxpayer taxable salary includes salary from Cambodian sources taxable according to the provisions of this chapter.

14

6. Determination of the Monthly Tax of Employees

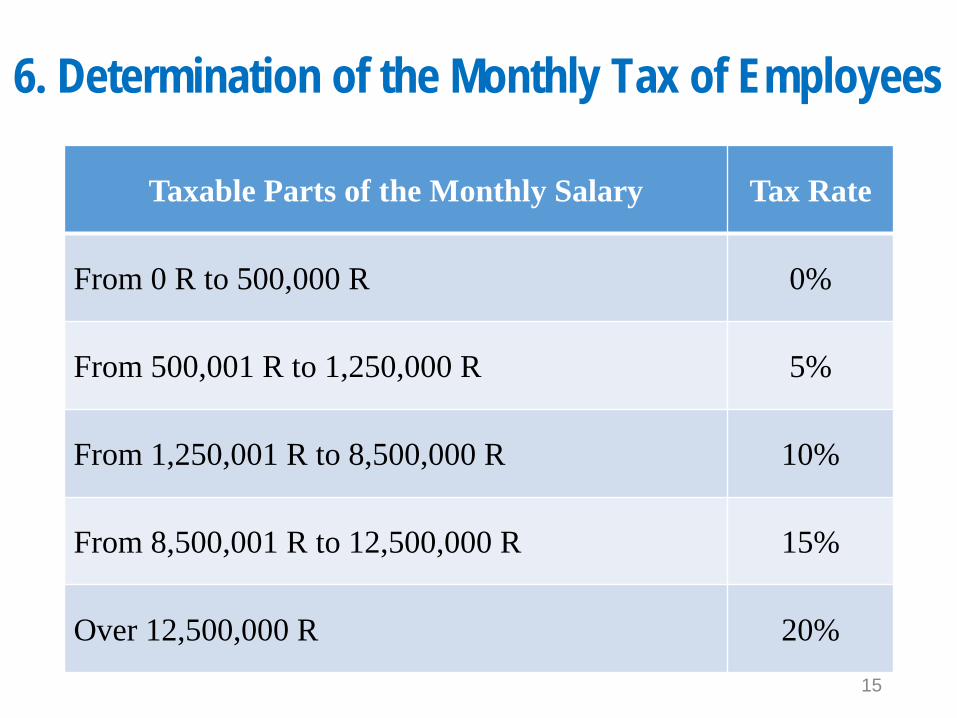

Taxable Parts of the Monthly Salary Tax Rate

From 0 R to 500,000 R 0%

From 500,001 R to 1,250,000 R 5%

From 1,250,001 R to 8,500,000 R 10%

From 8,500,001 R to 12,500,000 R 15%

Over 12,500,000 R 20% 15

7. Determination of the Tax on Fringe Benefits

For Fringe Benefits, every months the employer shall withhold and pay tax by the time specified at the rate of 20% of the total value of fringe benefits given to all employees. The value of fringe benefits is the fair market value inclusive of all taxes.

16

7. Determination of the Tax on Fringe Benefits (cont.)

The Fringe Benefits are as below: Transportations Foods Accommodation Utilities (water, electricity, phone,…) Housekeeper Loan with low interest or no interest Special discount Professional development which is not related to the

business Employee’s children education Life & health insurance, accept for giving equally to all

employee... 17

8. Determination of the Monthly Tax of Non-Residents

For a non-resident taxpayer, the tax shall be withheld by the payer at the rate of 20% on every payment of taxable salary. This withholding tax is the final tax on salary for the non-resident receiving the salary.

18

9. Obligation of Employers and Employees The salary payment is the cause of tax liability This tax is the debt of the physical person

receiving the salary, including foreign physical person, except for contrary provisions as stated in international agreement.

The tax on salary shall be collected through monthly withholding procedure by the employer at the time of each salary payment.

19

9. Obligation of Employers and Employees (cont.)

If the employer resides abroad, the fiscal representative appointed in the Kingdom of Cambodia by the employer is the one in charge of withholding the tax on salary prior to the salary payment to employees and of transferring their taxes to the State.

The employer or the resided representative in the Kingdom of Cambodia of a foreign employer and the employee shall be jointly

20

9. Obligation of Employers and Employees (cont.)

Responsible for the payment of the tax on salary in the Kingdom of Cambodia regardless of whether the salary is paid in the Kingdom of Cambodia or abroad. In the case where no withholding is made on the tax on salary, the employer is held responsible under this law even if the tax is already paid by the employee.

21

THANK YOU!

22

រព ះ រ ជ ណណចរ រ រ ត សា រព ចណព

អ គ� ាណកដ រ ព ក � ណស សងស ស ដណតជច ត ត�រ� �តរ

ឧេទ�សនេេដ : ងលណ ងអ � ា

របធនដយេដ ធររបររគងយ�របធពន�

ឣណ� ងេលតចម �បត ច(អ�) (េសៀររ ៃថ�ទ២១�ែខយ�ៈ�ឆង ន២០១៤ )

ម តត ១. កាផ�តបផ�រប�របឣយា ២. គរឣយា ៣. កាផ�តបផ�របធ�របឣយា ៤. ភខស ង ាារកាផ�តបផ�រប�របឣយារគរសធរ ធរកាផ�តប

ផ�របធ�របឣយា ៥. លយ�ខណ� ៃធកាផរលបលណឥធ គតរ ៦. បតតល ធរបតេតេ ៧. លយ�ខណ� ៃធកាេសង ើសនលណឥធឣយាេលើបតតល ៨. ឣយាេលើបតតលែលធឣតកតបយរាធ ៩. េលផ�តបផ�រប ១០.តៃ��របឣយា

2

ម តត () ១១. ការណនគតរតបររប ឬលណឥធេនរ ១២. គតរេលើបតតលេរើាសបបដតនែណយ�កាផ�តបផ�រប�របគតរ

ធរបដែផងយេទៀត�កាផ�តបផ�របធ�របគតរ ១៣. ការរបលសរាយបឣយា ១៤. លយ�ខណ� ៃធការរបលសរាយបឣយាេលើបតតល ១៥. កតបយតររ�ល�របគតរ ១៦. កតបយតគងយ�របធតនេចគតរ ១៧. តបកាតនេចពយដរតឣយា ១៨. ខ�សាៃធពយដរត ១៩. ធតពពៃធកាេតេពយដរត ២០. ការណនាយបឣយាសរបកាលយបមរេបគងយេរើ ាសប ២១. កាែយតបទយាយបគតរ 3

១.ត� � �� �រ��ឣណ�

កាផ�តបផ�រប�របឣយាឣ

កាផ�តបផ�របទនធេ�ឬេសា�េេដគងយផ�តបផ�រប�របគតរ�េបយង�ររ�តយយ���ម

កាយទនធេយេរើាសបរ� លបខ��ធ

កាផរលប�គនេដ�ឬផ�តបផ�របេកៃថ�េ ើទនធេ�ធរេសាេេដគងយផ�តបផ�រប�របគតរ�ម

កាននតលទនធេយង�ររ�តយយ���ម

4

២.អ រ ឣណ � (តស�រ�៦៤)

គរឣយា�១០% (របភរាដ)ឣ�សរបកាផ�តបផ�រប�របឣយាែលាបធកាផ�តបផ�របយង�រស�យ�ធរកាននតល�ម

គរ�០% (សធរភរាដ)ឣ�សរបកាននេតេទនធេ�ធរេសាែលាធរនេេេបេ�រ�តយយ���ធរកាយដ កបធគធរា�ត�ម

5

៣.ត� � �� �ចតរ��ឣណ� (តស�រ�៦៤)

េសាៃរណដសបាណៈ េសាធ�ាេទរ�ធររ�ធយ�េសាសរេដកសវសរ �ធរទធរសវសរ ��ធរកាលយបទនធេរន� របរធន នសរេដកសវសរ �ធរទធរសវសរ �ែលឥយបទធធរការនេេេសាយមឥនរេធ�ម េសាយដ កបធគងយ នេណើាេេដររធយដ កបធសបាណៈ�ែល�យមសទឥនរស�យារសបា ដ�ម េសាបនររបារ េសា�លេដ ធសរនាហ ត�� កាននតលារសបារាេរើាសបរ� លបខ��ធ�ែលាបតធរដ សយមភធែសបរាយាយបបតនេណេេ ើដរេនដធសបាណៈ កាននតល�ឬទេទនធេសរប�ដយយរនេេខញា�ផ�បកា�ារសបេរសយយមកាទតធរយរសងលរាេទស�គរ�កាគធរា�ត�ឬទភង យបញាសនរតរតរការេតយេទសារសបាេដ រាលនន�ម

6

៤.ភ រ ពស ស � ា ត � � �� �រ � �ឣណ � រច អ រស រ ត ត � � �� �ច តរ � �ឣណ �

(តស�រ�៥៧�៦៥�ធរ�៦៩)

កាផ�តបផ�របរគរសធរឣ រ�កាផ�តបផ�រប�របឣយា�ឣយាេលើបតតលតបាធគធរហ ត�លណឥធ�ឬឣតេសង ើសនររបលសរ

កាផ�តបផ�របទនធេ�ឬេសាសរគតថដធ�របឣយារគរ�០% (កាននេតេ)

កាផ�តបផ�របធ�របឣយាឣ� ធគធរហ តលណឥធឣយាេលើបតតល

ធតបរតឣយាគតថដធធ រលបកាផ�តបផ�របទនធេ�ឬេសា 7

៥. េណ� ណ� តត� រ េ�លណ ឥ អ� (គធយ គតរ រ�២៨)

ទនធេែលេសង ើសនលណឥធ�តបែតាធទេ�ឬននតលយង�រាដៈេល�៦០�ៃថ��ធកាតរ ក �ម

ចយរេសង ើសនលណឥធ�តបេពបើេ�ើររទរបយនណតបេេដគរ�នដយេដ ធធេា�ម

ចយរេសង ើសនលណឥធ�តបភក របេេដបយសារសឯ�ររៃធការរបាយបឣយា�ម

ររ�ល�របឣយាតបាយវបយសាែលឥយបទធធរកាេសង ើសនលណឥធយង�រាដៈ�េល១០ឆង ន ម

8

៦.ធ ពជេ ត ធ ពងជត (តស�រ�៦៥-៦៦)

ទនធេ�ឬេសាែលាធទេតលសរបរយរឣដយមេ�ថ� បតតល

ាយបឣយាែលាធររបេលើទនធេ�ឬេសាែលាធទេេ�ថ� ឣយាេលើបតតល

ទនធេ�ឬេសាែលាធផ�តបផ�របសរគតថដធេ�ថ�បតេតេ�

ាយបឣយាែលាធរតេលើទនធេ�ឬេសាែលាធផ�តបផ�របសរគតថដធ�េ�ថ�ឣយាេលើបតេតេ

ឣយាតបររប����= ឣយាេលើបតេតេ��- ឣយាេលើបតតល�(ឣយាេលើបតេតេពន�រឣយាេលើបតតល)

លណឥធឣយា��= ឣយាេលើបតេតេ��- ឣយាេលើបតតល�(ឣយាេលើបតេតេតត�រឣយាេលើបតតល)

9

៧.េណ� ណ� ត ត � ងសស លសពសលណឥ ឣណ � ងេលធពជេ (តស�រ�៦៨)

គធរហ តសរែតតនេចឣយាែលាធររបេលើទនធេឬេសាែលសរបេរើ�ាសបយង�រកាផ�តបផ�រប�របឣយារងេប

តនេចឣយាេលើបតតលែលឥយបទធធរកាននតល�តបធរតេទធរដ�សរបកាននតលែលររក យបេេដឣ�ក ពារដ

តនេចឣយាេលើបតតលែលឥយបទធធរកាទេយង�រស�យ�តប ធពយដរត�ឣយាែលេតេេេដគងយផ�តបផ�របាធតរ ក � គតរ�ម

10

៨.ឣណ � ងេលធ ពជេបសេចត ឣជត�ណ ា (តស�រ�៦៩)

ឣយាែលាធររបេលើកាតនដទទបលេរកទ�កាយនសធឯឬសយលនែន�េលើយែលរែត�ររ�ល�របឣយារយរឣដយមផ�តបផ�របកាទទបលេរកទ�កាយនសធឯ�ឬសយលនែន�ម

- ចយរ�កាទទបលេរកទ�ធធរដថ�កាផ�តបផ�របតបរឣងា�េរសដកៈ�ថង នដយប�យែធ�រសង យបឣសរដ�ឬរសដ ាយតបដ�

ឣយាែលាធររបេលើកាទេ�ឬកាននតលាថដធឯ�េលើយែលរែតររ�ល�របឣយារយរ�ឣដយមលយបឬ�ដបលាថដធឯឥនរេន

- ចយរ�ាថដធឯ�សនេ�លប�ាថដធឯែលធយែធ�រគរ��ដធេលើស�១០�

ឣយាែលាធររបេលើកាទេផលតផលេតលសេបដតនធបធ�ាបធេររសនរ�េររ� ងសងត�ធរេររាេគលររបរេរទ�េលើយែលរែតររ�ល�របឣយារយរឣដយមផ�តបផ�រប�ផលតផលេតលសេ ម

11

៩.ឣណ � ងេលធ ពជេបសេចត ឣជត �ណ ា (តស�រ�៦៩)

ឣយាែលាធររបេលើកាតនដទទបលេរកទ�កាយនសធឯឬសយលនែន�េលើយែលរែត�ររ�ល�របឣយារយរឣដយមផ�តបផ�របកាទទបលេរកទ�កាយនសធឯ�ឬសយលនែន�ម

- ចយរ�កាទទបលេរកទ�ធធរដថ�កាផ�តបផ�របតបរឣងា�េរសដកៈ�ថង នដយប�យែធ�រសង យបឣសរដ�ឬរសដ ាយតបដ�

ឣយាែលាធររបេលើកាទេ�ឬកាននតលាថដធឯ�េលើយែលរែតររ�ល�របឣយារយរ�ឣដយមលយបឬ�ដបលាថដធឯឥនរេន

- ចយរ�ាថដធឯ�សនេ�លប�ាថដធឯែលធយែធ�រគរ��ដធេលើស�១០�

ឣយាែលាធររបេលើកាទេផលតផលេតលសេបដតនធបធ�ាបធេររសនរ�េររ� ងសងត�ធរេររាេគលររបរេរទ�េលើយែលរែតររ�ល�របឣយារយរឣដយមផ�តបផ�រប�ផលតផលេតលសេ ម

12

១០.ងរ េ� �� � (តស�រ�៦២)

េលផ�តបផ�រប�រ�េលែលាយបឣយាលបយនណតបតបររប

េលផ�តបផ�របទនធេធរេសា�រ�េលែលគងយលយបតបេតេ ពយដរត�ឬ�េលែលគងយ�លយបាធេតេ ពយដរត�រសធេរើ ពយដរតេនតបាធេតេធេលែលគងយលយបតបេតេ� ពយដរត

� ពយដរតឣយាេលើតៃ�រែធ�តបេតេនង រដតរនផត�៧ៃថ��េកដការ កបធទនធេ�ឬកា�រនេេេសា�ឬេកដកាទឥតបយង�រយាណែលកាទឥតបេពបើេ�ើរធការ កបធទនធេ�ឬកា�រនេេេសា

រសធេរើទនធេតបាធយេរើាសប�រ�េលែលទនធេេនតបាធដយេបេរើាសបនររ�

រសធេរើេពបើគនេដ�រ�េលែលទនធេតបាធរ កបធេបេពបើ�គនេដ�ម

13

១០.ងរ េ� �� �() (តស�រ�៦២)

យង�រយាណែលធកាផ�តបផ�របេដ�ន ង ាារទនធេ�ធរេសា�តបយនណតបតតេបឣ

- េលផ�តបផ�របធ េសារន� របរធន នែលាប�បដធរកាផ�តបផ�របទនធេ�រ�តនែណយបដៃធកាផ�តបផ�របទនធេ

- េលផ�តបផ�របធ ទនធេរន� របរធន នែលាប ង �បដធរកាផ�តបផ�របេសា�រ�តនែណយបដៃធកាផ�តបផ�របេសា

- េលផ�តបផ�របធ េសារន� របរធន នែលាប�បដធរននតល�រ�តនែណយបដៃធននតល�ម

14

១១.តចម រ ��ឣណ � (តស�រ�៦១)

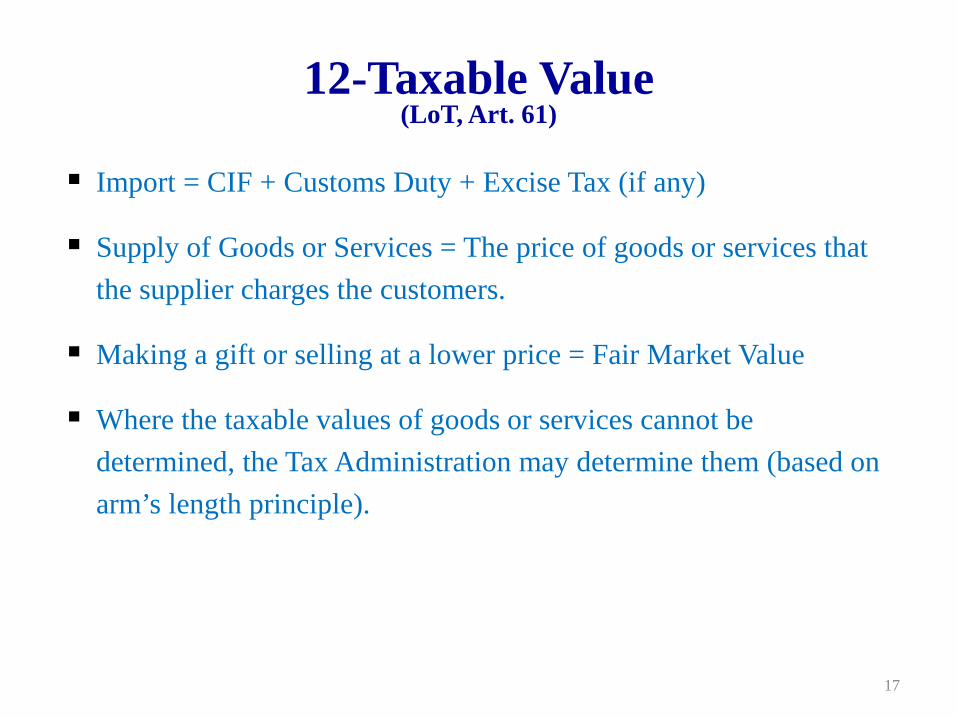

កាននតល�= CIF +ធរដ��+ ឣយាេសសេលើទនធេធរេសាបដតនធបធ

កាផ�តបផ�របទនធេ�ឬេសា�= ៃថ�ែលគងយលយបរតដយគងយទេ�ាបឥនររធ��យេផនរ�ធរឣយាេសសេលើទនធេធរេសាបដតនធបធ�រសធេរើធ

កាេពបើគនេដឬកាលយបេេដរ�ៃថ��= តៃ�តបរតរតៃ�ទផវា�

រសធេរើតៃ�ទនធេឬេសាធឣតយនណតបាធថ�តៃ�តេទ�គរ�នដយេដ ធធេា�ឣតេពបើកាយនណតបតៃ�បដសរបទនធេឬេសាេន�ម

15

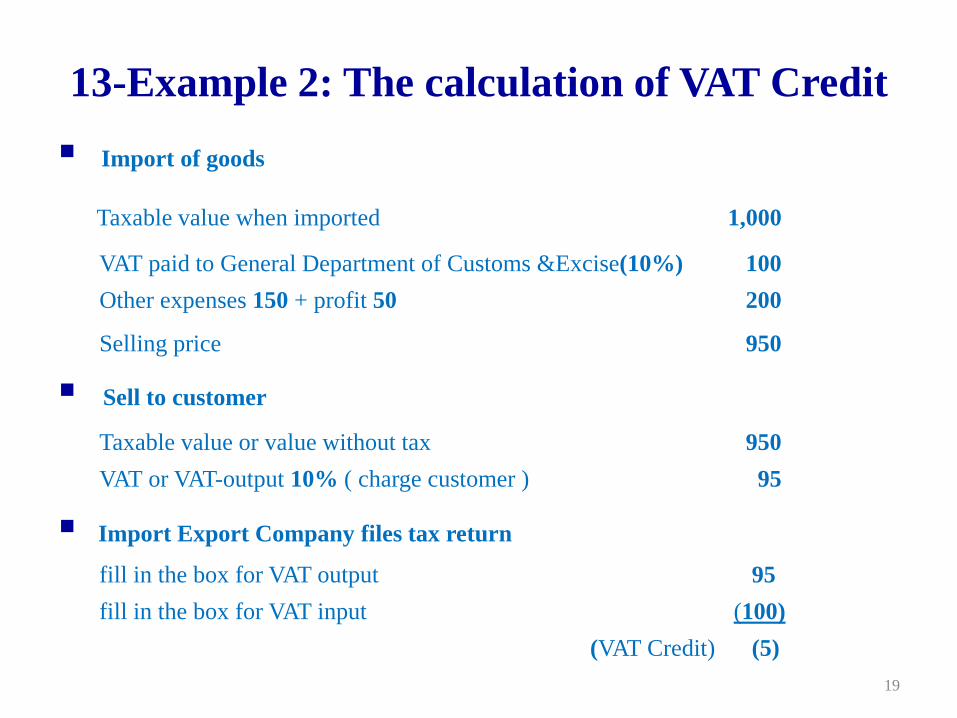

ឧឥ � ណរ ១ ៖អសរ ត � គណា អ� �� �

ននតលទនធេ តៃ�រតឣយាេបេលននតល = ១,០០០ ឣយាេលើតៃ�រែធ�ររបសរគា ១០% = ១០០� តនដេផនរ�១៥០�+ តនេណេ�៥០� = ២០០� ៃថ�លយបេតេ� = ១,២០០ លយបទនធេសរគតថដធ តៃ�រតឣយា�ឬតៃ�ធាបរ កបលឣយា = ១,២០០ ឣយាេលើតៃ�រែធ��ឬឣយាេលើបតេតេ�១០% = ១២០�(រតដយគតថដធ)

យ�នងធននតលទនធេេយបលខតរកស រនេេេបយង�ររគរបសរបឣយាេលើបតេតេ� ១២០ រនេេេបយង�ររគរបសរបឣយាេលើបតតល� ១០០ ២០��ឣយាតបររបសរែថ 16

ឧឥ � ណរ ២៖អសរ ត � គណា អ� �� �()

ននតលទនធេ តៃ�រតឣយាេបេលននតល = ១,០០០ ឣយាេលើតៃ�រែធ�ររបសរគា ១០% = ១០០� តនដេផនរ�១៥០�+ តនេណេ�៥០� = ២០០� ៃថ�លយបេតេ� = ៩៥០ លយបទនធេសរគតថដធ តៃ�រតឣយា�ឬតៃ�ធាបរ កបលឣយា = ៩៥០ ឣយាេលើតៃ�រែធ��ឬឣយាេលើបតេតេ�១០% = ៩៥ (រតដយគតថដធ)

យ�នងធននតលទនធេេយបលខតរកស រនេេេបយង�ររគរបសរបឣយាេលើបតេតេ� ៩៥ រនេេេបយង�ររគរបសរបឣយាេលើបតតល� ១០០ (៥) លណឥធឣយា 17

១២.អ � ងេលធ ពជ េង� លា ស�ច ស ជ សបណណ រ ត �� �� �រ � �អ � ត ច ស ជ សបណណ ងទៀ រ ត �� �� �ច តរ � �អ �

(គធយ គតរ រ�៣៣)

កាផ�តបផ�របារសបររ�ល�របគតរេបយង�រាដៈេល�រប�គតរ�ធបដែផងយ�កាផ�តបផ�រប��រប�គតរ�ធរបដែផងយេទៀត��កាផ�តបផ�របធ�រប�គតរ�តនធបធលណឥធែលឣតផឯលប�សរតបាធរណនរារធឯ�ឣ��យ�x (ខ�/ រ)

យ��ឣ�ទយាយបសារៃធ�គតរ�េលើបតតលយង�រាដៈេល�រប�គតរ

ខ��ឣ�តៃ�សារធឥធបរត�គតរ�ៃធកាផ�តបផ�រប�រប�គតរ

រ��ឣ�តៃ�សារធឥធបរត�គតរ�ៃធកាផ�តបផ�រប�រប�គតរ�ធរកាផ�តប ផ�របធ�រប�គតរ�េលើយែលរែតកាេផ�ាឣដយម�ម

រភរតត�រ�០.០៥�ឣយាបតតលឥនរគសបធតប ាធគធហត�លណឥធ

រភរពន�រ�០.០៩�ឣយាបតតលឥនរគសបតប ាធគធហត�លណឥធ

រភរតេន� �០.០៥�លប�០.០៩�ឣយាបតតលតប ាធគធរហ ត�លណឥធរសតៃធរភរ�ម

18

១៣.ត � � ប តេស ាណ �ឣណ � (តស�រ�៧២ -៧៣)

ររ�ល�របឣយាាធតរ ក�ែលាធរកសកាននេតេេបេលើលខតរកស�ឣតេសង ើ�សនររបលសរឣយាេលើបតតលេលើសេបេលើលខតរកសេន

សនសពធេនរែលាធរកសឣយាេលើបតតលេលើសេបេលើលខតរកស�ឣត�េសង ើសនររបលសរាយបឣយាេបេលើលខតរកសេន

ររ�ល�របឣយាាធតរ ក�ែលធលណឥធឣយាេលើបតតលេលើសចរប�៣ែខ��រប ង េ�ើរេប�ឣតេសង ើសនររបលសរឣយាេលើបតតលេលើសេបនតបែខទ៣�ម

19

១៤.េណ� ណ� ត ត � � ប តេស ាណ �ឣណ � ងេលធពជេ (តស�រ�៦៨)

ររ�ល�របឣយាែលេពបើកាននេតេឣ

- តបធរតេទធរដសរបកាននតលែលររក យបេេដឣ�ក ពារដ

- តបធ ពយរដររតឣយាែលេតេេេដគងយផ�តបផ�របាធតរ ក �គតរ

- តបធរតេទធរដសរបកាននេតេែលររក យបេេដឣ�ក ពារដ�ធរបយសារសឯ�ររៃធកាននេតេ

សនស ពធេនរឣ

- តបធរតេទធរដសរបកាននតលែលររក យបេេដឣ�ក ពារដ

- តបធ ពយរដររតឣយាែលេតេេេដគងយផ�តបផ�របាធតរ ក �គតរ�ម

20

១៥.ត រ បណ តជច �ពគ� េរ ��អ� (គធយ�គតរ�រ�២�-៧)

តបតរ ក �គតរ

េយបរនរ ពរហ រធររតតរ ក �គតរ�េបយែធ�ររយរឣដយម�សនសធបារសបខ�បធ�

រតឣយាេលើកាលយបសរគតថដធចរបរនរកលរាពេតទធរសទភៃធកា�តរ ក �គតរ

េតេ ពយរដររតឣយាលបគតថដធែលាធតរ ក �គតរ�

យតបរកាលយបរដរចនៃថ��ឬេតេ ពយរដររតពមរលបគតថដធែលធាធត�រ ក �គតរ�

តបតរ ក ធធរេពបើកាននតល�ឬននេតេ

21

១៦.ត រ បណ តជច អស ណ រ ��រ ព ជសងច ពអ� (តស�រ�៧៩)

យតបរ�រលបបយសា�យនណតបរ�ធររ ក រណេធដរែលឥយបទធធរកា

ផ�តបផ�រប�រប�គតរ�ធរាយវទយយង�រាដៈេល�១០�ឆង ន�ម

េយបលខតរកស�ធរររបាយបឣយា��េាៀររលបែខ�នង រដតរនផតត

ៃថ��ទ២០�ៃធែខរន� រប�ែខែល�ាដៈេល�របឣយា�ម

ដធនណរលបា ដាលសាេើធ�គនកាែររ�លស� ធភឣដយម�ាប

ឥនរកា�េផ�ាឣដយម�ធរកាេសង ើសនលរេចលកាតរ កផរ�ម

គធរហ តសរវធឯៃធនដយេដ ធធេា�ត�តធតរ�បយសាយនណតបរ�រ ក

រណេធដរ�ធររស� ធឣដយម�ម 22

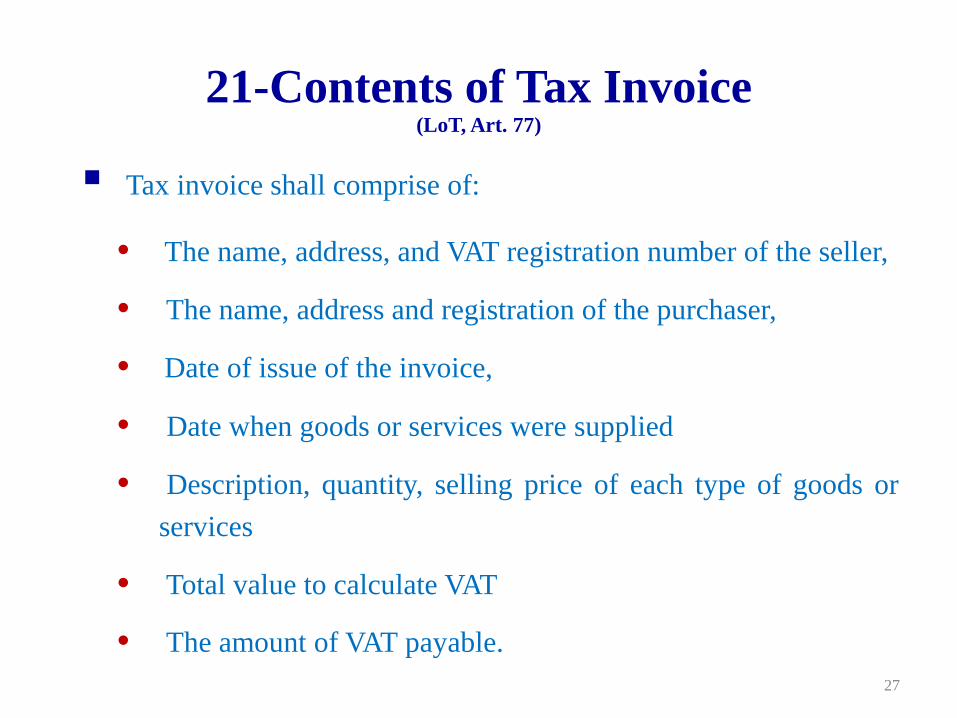

១៧. ច �ត � ជសងច ព �ពណ � ឣណ � (តស�រ�៧៧)

តបេតេពយដរតឣយាេបេលែលេពបើកាផ�តបផ�របេបសរររ�ល

�របឣយាែល�ាធតរ ក �ៃទេទៀត

� ពយដរតឣយាែលាធេតេ�តបធេលខេាៀរត ង តតប

� ពយដរតឣយាតបធតនណរេដើរថ�“� ពយដរតឣយាេលើតៃ�

រែធ�”

ររ�ល�របឣយា�ធសទឥឥាសរររ�ល�របឣយាៃទេទៀត�

េតេពយដរត�ឣយាសរេបេលទទបលកាផ�តបផ�របទនធេ�ឬេសា�ម

23

១៨. មច � ត �ពណ � (តស�រ�៧៧)

� ពយដរតឣយាតបធរដឣ

- េឈម �ឣសដេដ ធ�ធរ�េលខគតឯសរហ ណយម�គតរ�ារសបគងយលយប

- េឈម �ឣសដេដ ធ�ធរ�េលខគតឯសរហ ណយម�គតរ�ារសបគងយទេ

- កលរាពេតទេតេ� ពយដរត

- កលរាពេតទៃធកាផ�តបផ�របទនធេ�ឬេសាតបាធរនេេ

- រាពនដខទនធេ�រាពណ�ៃថ�បយរ�ធរតៃ�ទនធេបដខេលើ� ពយដរត

- តៃ�សារេ ើដរណនឣយាេលើតៃ�រែធ�

- តនធបធទយាយបឣយាេលើតៃ�រែធ� 24

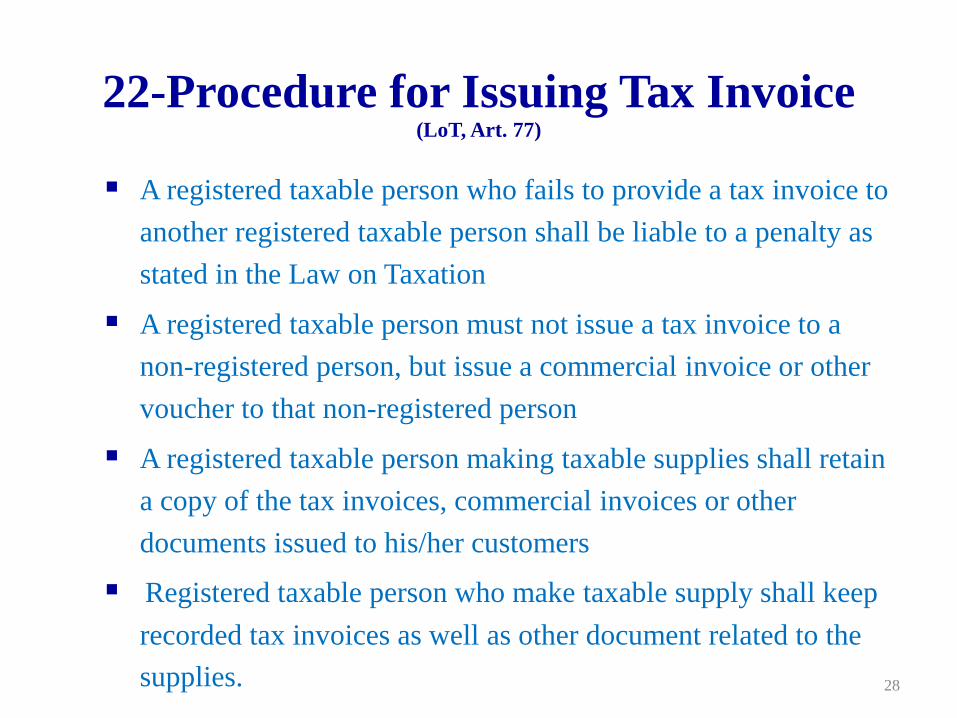

១៩. ត �ពធ ត ត � ងជត �ពណ � (តស�រ�៧៧)

ធែតររ�ល�របឣយាាធតរ ក េទ�ែលឣតេតេ ពយដរតឣយាយង�រកា�លយបទនធេ�ឬេសាេបសរររ�ល�របឣយាាធតរ ក ៃទេទៀត�ម

ររ�ល�របឣយាាធតរ ក �ែលធាធេតេ ពយដរតឣយាេបសរររ�ល��របឣយាាធតរ ក �ៃទេទៀត�តបទទបលារេឥសទណ� រតរប�ម

ររ�ល�របឣយាាធតរ ក �ធតបេតេ ពយដរតឣយា�េបសរររ�លែល�ធាធតរ ក េ�ើដ�ែតតបេតេ ពយរដររតពមរ�ឬរញ ធបៃទទបលាយបេប�សរររ�លេន�ម

ររ�ល�របឣយាាធតរ ក ែលេពបើកាផ�តបផ�រប�របឣយាតបាយវទយតរបត�រ�� ពយដរតឣយា�ឥនរបយសាៃទេទៀតែលឥយបទធេបធរកាផ�តបផ�រប�ម

25

២០.ត � គណា ា ណ �ឣណ � ស ម� �ត � េណ � ម រ ង� អស ណ ង � ល ា ស� (តស�រ�៧៧)

េតេពយដរតពមរ�ែលសារឥនរាយបឣយាេបយង�រតៃ�ផរ

េពបើកាយតបរយង�រយនណតបរសតបាយប�ឬយនណតបរលយបរដសាររចនៃថ��េនើដដយេបរណធរ�រភរឣយា�េ ើដរណនាយាយបឣយា ម

- រភរឣយា�សរបគរឣយា�១០% រ�ឣ

- គរ / (គរ + 100) = 10 / (10 + 100) = 1 / 11

ឧរថទយាយបលយបសាររចនៃថ��= ១១,០០០�(ាបឥនរាយបឣយា)

- ទយាយឣយា��= ១១,០០០�x (1 / 11) = ១,០០០

- តៃ��របឣយា� = ១១,០០០�- ១,០០០� = ១០,០០០

ឬ�១១,០០០�/១.១�= ១០,០០០

ឬាយបឣយា�= ១១,០០០/១.១��x ១០% = ១,០០០ 26

២ ១.ត � បណ ច �ទណ ាណ �អ� (គធយ�គតរ រ�៤៩)

ររ�ល�របគតរែលាធេតេ ពយដរតគតរឬាធេយបលខតរកសរចនែខាបតេនើដ�ឣតេពបើកាែយតបទយាយប�គតរ�េ�ើរ ពេាធេរើសធ�ធេនតកាណ� តសរេកេធាធេយើតេ�ើរឣ

- កាផ�តបផ�របតប ាធលរេចល�ឬ

- តាពតៃធកាផ�តបផ�របតប ាធែររ�ល�ឬាធរ� សបរឯបា�លេដ ធ�ឬ

- គត�រេនដធសរបកាផ�តបផ�របែលាធេទរ ង េលធតបាធែររ�ល�ឬាធរ� សបរឯបាេេដយតេទរថម�បដធរគងយទទបលកាផ�តបផ�របេេដលេនត�ៃធការ�ៃថ��ឬេេដេនតផលេផនរេទៀត�ឬ

- ទនធេឬតនែណយបដៃធទនធេឬសនរយេតខរប�តបាធរ កបធត�របយគងយផ�តបផ�រប� ពេ�ឬេសាធតបាធរនេេាបតរលប�ម

27

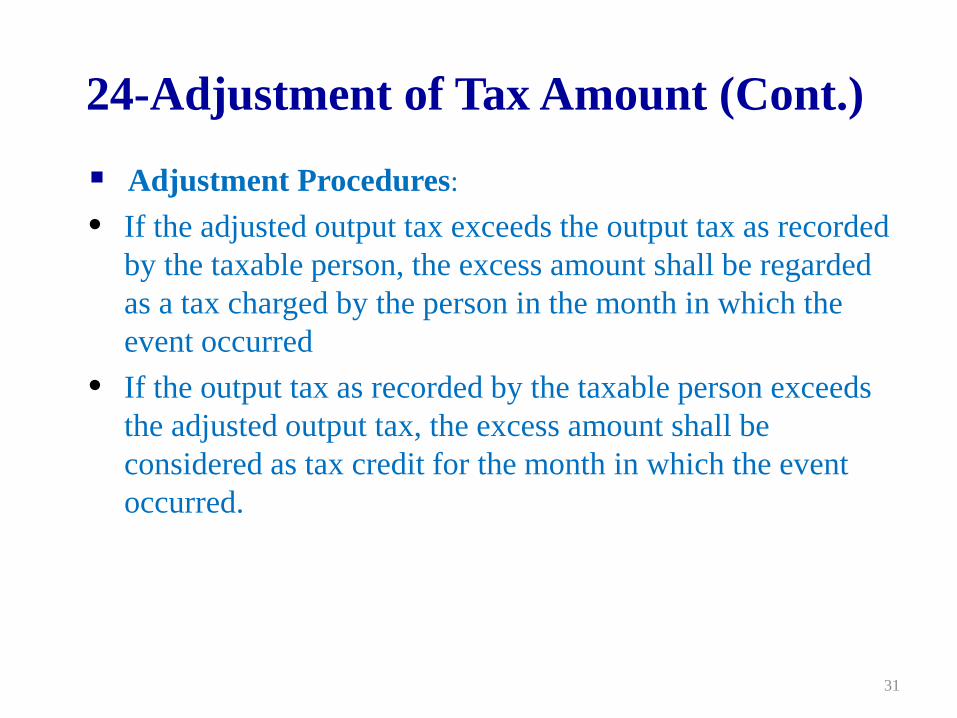

២ ១.ត � បណ ច �ទណ ាណ �អ�() (គធយ�គតរ រ�៤៩)

ាេរៀរែយតបឣ េរើសធ�ាយប�គតរ�េលើបតេតេែយតប�ធតនធបធេលើសាយប�គតរ�េលើ�បតេតេែលររ�ល�រប�គតរ�ាធយតបរ�តនធបធេលើសតបាធចតបទយ�ាយប�គតរ�ែលររ�ល�រប�គតរ�ាធរលេបយង�រែខ�ម

េរើសធ�ាយប�គតរ�េលើបតេតេែលររ�ល�រប�គតរ�ាធយតបរធតនធបធេលើស�ាយប�គតរ�េលើបតេតេែយតប�តនធបធេលើសតបាធចតបទយ�លណឥធ�គតរ�សរបែខ�ម

កាផ�តបផ�របសរររ�លធ�របគតរ�ាយប�គតរ�េលើស�ធតបាធគធរហ ត�លណឥធ�គតរេទ�េលើយែលរែតររ�ល�រប�គតរ�ាធទឥតបសរាយបគតរ�េលើសសរគងយទទបល�កាផ�តបផ�រប ពេ�សតបាយប�ឬកតបយររនណល�ែលគងយទទបលកាផ�តបផ�របដនចយប�ម

28

២ ១.ត � បណ ច �ទណ ាណ �អ�() (គធយ�គតរ រ�៤៩)

ាេរៀរែយតប�(ត)ឣ

ររ�ល�រប�គតរ�ែលាធេតេពយរដររត�គតរ�េនើដតនធបធាយប�គតរ�ែលាធយតបរេលើ ពយរដររតធឣ

- តនធបធេលើសាយប�គតរ�ែយតប�តបផឯលបសរគតថដធធ �េតតលណឥអ�

- តនធបធតត�រាយប�គតរ�ែយតប�តបផឯលបសរគតថដធធ �េតតលណរដ អ�

គងយផ�តបផ�រប�ឬគតថដធែលាធេតេ�ឬាធទទបលលខតលណធ�ឬលខតលណឥធ�គតរ�តបយតបរតលនទយាយបៃធលខតលណធ�ឬលខតលណឥធ�គតរ�ត ង េបធរតលនទយាយបៃធ ពយរដររតគតរែា�ម

29

សចអ �គពណ!

30

KINGDOM OF CAMBODIA

NATION RELIGION KING

General Department of Taxation

Ministry of Economy and Finance

Presented by : Mr. ENG RATANA

Director of Large Taxpayer Department

VALUE ADDED TAX (VAT) Siem Reap, 21st February, 2014

1

1- Taxable Supply 2- Rules and Procedures for VAT Registration 3- Obligation to Register for VAT 4- VAT Rate 5- Non Taxable Supply 6- The Differences Between Zero Rate Supply and Non-

Taxable Supply 7- Conditions for Creditable Input VAT 8- Input and Output 9- Conditions to Claim an Input Tax Credit 10- Input Tax not Allowed as a Tax Credit 11- Time of Supply 12- Taxable Value

2

Contents

13- Example: Calculation of VAT Payable/Credit Carry Forward 14- Input Tax Partly for Taxable Supplies and Partly Non- Taxable Supply 15- VAT Refund 16- Conditions for Refund of Input VAT 17- Taxpayers’ Obligation for VAT Registration 18- Obligation of Taxable Persons 19- Taxpayers’ Obligation for VAT 20- Requirements of Tax Invoice 21- Contents of Tax Invoice 22- Procedure for Issuing Tax Invoice 23- Tax Calculation for Supply to Consumer 24- Adjustment of VAT Amount 3

Contents (cont.)

1-Taxable Supply (LoT, Art. 60)

The taxpayer under self-assessment system who makes taxable supplies shall have obligation to register for VAT Definition of taxable supply:

• The supply of goods or services by a taxable person in the Kingdom of Cambodia;

• The appropriation of goods for his own use by the taxable person;

• The making of a gift or supply at below cost of goods or services by the taxable person;

• The import of goods into the customs territory of the Kingdom of Cambodia.

4

2-Rules and Procedures for VAT Registration (Sd. VAT, Art. 2)

All legal persons, import-export companies and QIPs Other enterprises who have the following turnover

within 3 months: • 125 million riels for those supplying goods • 60 million riels for those providing services • 30 million riels for those under the contract with the royal

government

5

2-Rules and Procedures for VAT Registration (Cont.) (Sd. VAT, Art. 2)

For those who are not legal persons, import-export companies and QIPs, they shall have annual turnover starting from: • 500 million riels for those supplying goods • 250 million riels for those providing services • 125 million riels for those under the contract with the royal

government Other enterprises shall be able to register for VAT voluntarily if they

find it crucial.

6

Persons who meet the criteria for self assessment system and make taxable supplies have the obligation to VAT Registration.

Only the taxable persons with Certificate of VAT Registration are allowed to charge VAT when supplying goods or services.

Registered taxable persons will get VAT Identity Numbers (VATIN) and the certificate of VAT registration.

The General Department of Taxation has the right whether or not to register or cancel the registration.

3-Obligation to Register for VAT (LoT, Art. 76)

7

The rate of 10% ( Ten percent) : on the locally taxable supplies and import

The rate of 0% (Zero percent) : on the taxable value of each taxable supply of goods exported from the Kingdom of Cambodia and of the taxable supply of a service rendered outside of the Kingdom of Cambodia; and, international transportation

4-VAT Rate (LoT, Art. 64)

8

Public postal service Hospital, clinic, medical and dental services and the sale of medical

and dental goods incidental to the performance of such services The service of transportation of passengers by a wholly state owned

public transportation system Insurance services Primary financial services The importation of articles for personal use that are exempt from

custom duties Non profit activities for the public interest The import of goods for official mission by foreign diplomatic and

consular mission, international organizations and agencies of technical cooperation of other governments.

5-Non Taxable Supplies (LoT, Art. 57-58)

9

Supply With Zero Rate:

• the taxable supply with zero rate

• Input tax is allowed as tax credit or can be refunded.

• The supply of goods and services taxable with zero rate is export

Non-taxable supplies

• Not allowed as credit of input tax

• The suppliers shall not charge VAT to customer for all supplies.

6-The Differences Between Zero Rate and Non-Taxable Supply

(Sd. VAT, Art. 57, 64, 65 and 69)

10

7-Conditions for Creditable Input VAT (Sd. VAT, Art. 28)

Goods that can receive VAT credit shall be purchased or imported within 60 days before VAT registration.

Tax credit application shall follow the form prescribed by GDT.

Tax credit application shall be attached with the evidence of VAT payment.

Taxable person shall keep related documents of credit request for 10 years.

11

8-Input and Output (LoT, Art. 65-66)

Goods or services which are purchased for business are called Input.

Tax amounts charged on goods and services purchased are called VAT input.

Goods or services supplied to customers are called Output.

Tax amounts charged on goods or services that are supplied to customers are called VAT output.

Payable tax = VAT output – VAT input (VAT output > VAT input)

VAT Credit = VAT output – VAT input (VAT output < VAT input)

12

9-Conditions to Claim an Input VAT Credit (LoT, Art. 68)

Shall be allowed only for tax paid on goods or services that are used for taxable supplies

For VAT input related to import, there shall be customs declaration certified by customs authorities.