Marke&ng Proposal Group 28 -‐ Think Like A Brand

KLEUR TONACITY

PRODUCT BRIEF

MARKET OPPORTUNITY

CUSTOMER PERSONA

CUSTOMER JOURNEY CAMPAIGN METRICS

The Product Kleur Tonacity – “You’re The Professional” High-end Home Hair Colouring Product Good Quality, Lasting Colour Ammonia Free Bespoke Application Tool First Truly Multi Tonal Salon Effect at Home No Direct Competitors

Our PresentaAon Market Opportunity & SWOT Analysis Customer Personas Customer Journey - Traditional & Digital Together Content Plan Paid Search Online Display Social Media Driving Sales Through Digital Innovation Metrics

Our Aims To establish Kleur Tonacity as a recognisable brand in the UK To create acceptance of a high end hair colouring price point & product To educate the UK consumer that it is possible to achieve a salon result at home To generate sales and return on Kleur’s investment

KLEUR TONACITY

PRODUCT BRIEF

MARKET OPPORTUNITY

CUSTOMER PERSONA

CUSTOMER JOURNEY CAMPAIGN METRICS

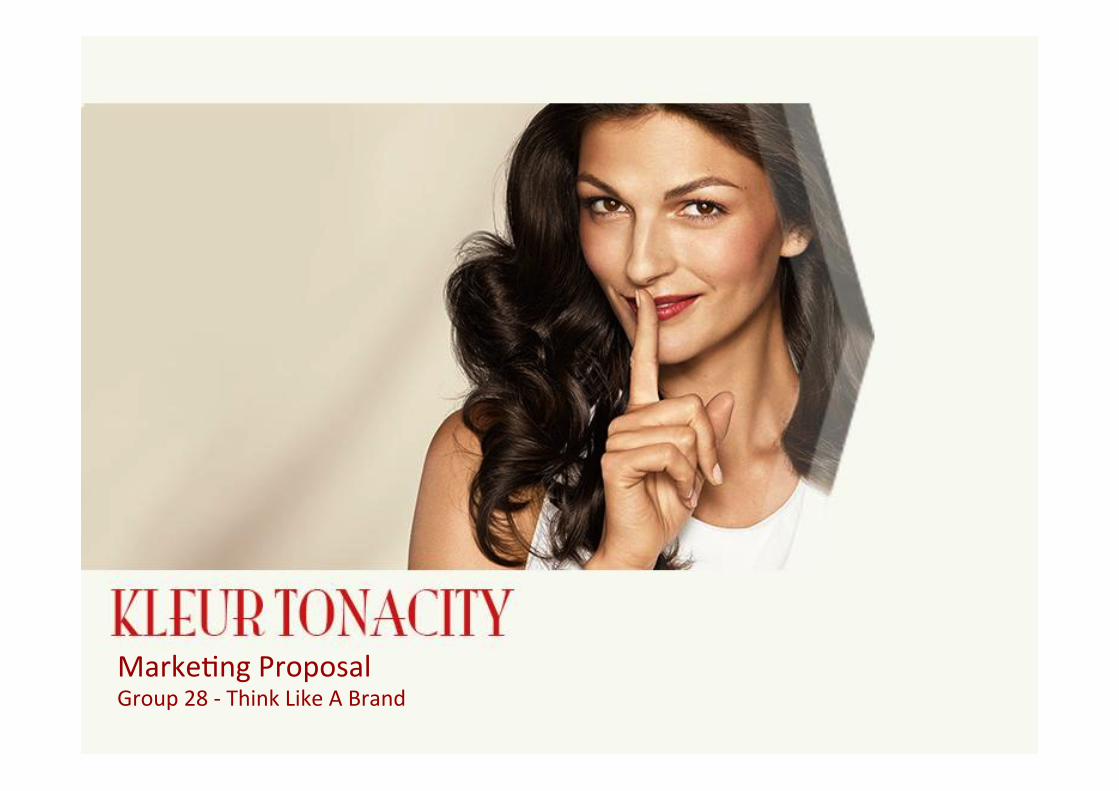

Market Opportunity

Customers do not want to spend reduced disposable income on luxury salon appointments But they are s&ll willing to buy a premium product that will give a professional look and finish, whilst also saving them &me

0

50

100

2013 2015 2017 2019 2021

Strengths Niche product Clear poten&al market Good brand name Links to well-‐known high street stores

OpportuniAes Large market, predicted to grow from 2015-‐2020 Opportunity to build market share First to market advantage

Weaknesses Customers need to be educated about products at this price point Will take &me to build strong & recognisable brand Lots of well-‐known brand names at lower price point

Threats Other entrants if KT is successful Aggressive strategies from well-‐known brands as a market response

SWOT

Global hair care market set to increase year-‐on-‐year to $94.5 billion in 2021

Disposable income for UK households 2010 -‐ 2015

UK hairdressing & beauty treatment revenue

2010 -‐ 2015

UK Hairdressing &

Beauty Treatment Market:

£4bn

KLEUR TONACITY

PRODUCT BRIEF

MARKET OPPORTUNITY

CUSTOMER PERSONA

CUSTOMER JOURNEY CAMPAIGN METRICS

Laura 35 years old Single Architect Rental Accommoda&on London

Lifestyle ² Social network presence: Facebook, Pinterest;

YouTube subscriber ² Ac&ve social life ² Mobile and tablet user ² Love shopping online but buy beauty products in

store ² Online magazine: Glamour, Elle, Vogue

AZtude to hair care ² Likes fashionable style but

budget conscious ² Willing to consider a

convenient salon alterna&ve

Helen 45 years old Married – 2 children Finance Director Home owner Manchester

Lifestyle ² Modern working mother with hec&c life ² Enjoys spending &me with family and friends ² Likes checking beauty products online but

prefers to buy in store ² Print magazines: Good Housekeeping, Marie

Claire

AZtude to hair care ² Concerned with her grey

hair, wants natural hair dye product that gives salon quality results and saves her &me

Key Influencers: Family 33% Friends 46%

Magazine Advice 75%

90% Buy Beauty

products Offline

Top reason to shop with retailer

Daily Usage 16.4 mins 15.8 mins 12.1 mins

Target Audience: Affluent Professional Women

We have iden&fied two “Beauty Enthusiast” personas who care about appearance and want to look and feel good about themselves.

Age Group 25-39

Age Group 40-59

KLEUR TONACITY

PRODUCT BRIEF

MARKET OPPORTUNITY

CUSTOMER PERSONA

CUSTOMER JOURNEY

CAMPAIGN METRICS

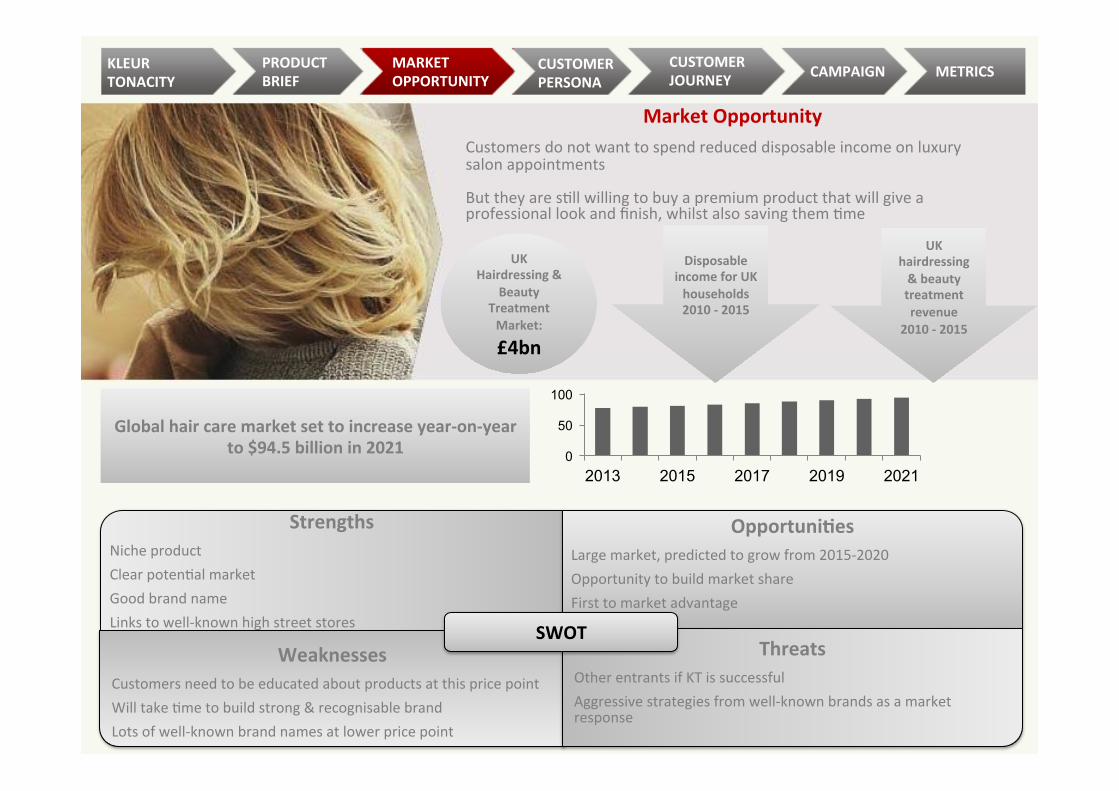

Traditional & Digital Working Together Total weekly hours spent online has doubled in last 10 years

Adults now split their media usage: TV 36.5 hrs; Mobile 23.3 hrs; Online 18.0 hrs; Radio 10.9 hrs; Print 3.5 hrs

73% of shoppers go online to research first before purchasing in store. Our Strategy is therefore: Generate awareness of brand across multiple traditional and digital channels Drive customers to website/social pages, then in store to experience Tonacity Build advocacy through innovative use of social media and website

AWARENESS

CONSIDERATION

EVALUATION

EXPERIENCE

LOYALTY

TV Ads Outdoor Display Fashion & Beauty Magazines, Weekend Supplements Online Display – Sponsored Social, Tenancies, Email Paid Search Blogger Outreach (Pixiwoo, Lise Eldridge etc) First Hero Video Content Social Media Sponsored New Feed Ads PR AcAvity Dept. Store & Shopping Mall Roadshow Interac&ve Digital & Window Display

Tonacity Website & App Fashion & Beauty Magazines Paid Search Tonacity Social Media Pages Online Display – Contextual & Behavioural Banners Online Display – Retarge&ng

Partner Dept. Stores / Shopping Mall Roadshow Pop Up Stores Tonacity Website Retail Partner Websites

Product Quality & EffecAveness Customer Service Line Website Chat Tonacity Social Media Pages

Tonacity Social Media Pages Tonacity Website Forum Retailer website review pages Consumer magazines/sites (e.g. Which?)

Traditional Digital

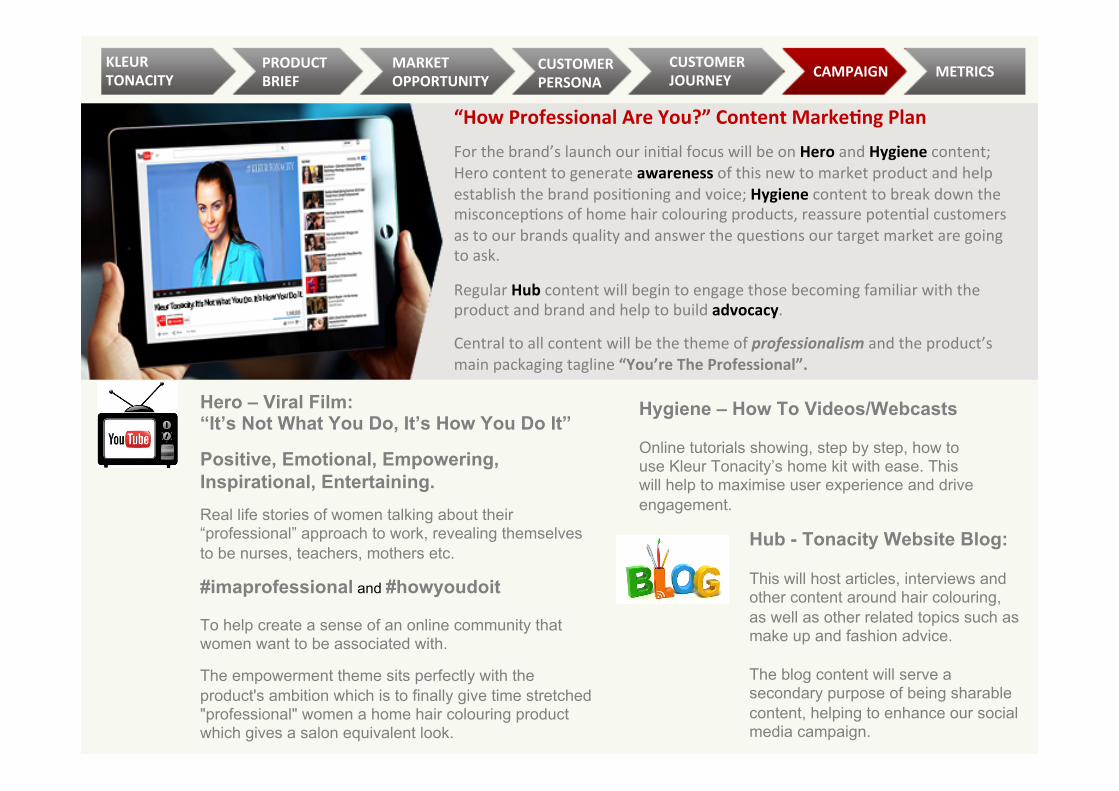

“How Professional Are You?” Content MarkeAng Plan

For the brand’s launch our ini&al focus will be on Hero and Hygiene content; Hero content to generate awareness of this new to market product and help establish the brand posi&oning and voice; Hygiene content to break down the misconcep&ons of home hair colouring products, reassure poten&al customers as to our brands quality and answer the ques&ons our target market are going to ask.

Regular Hub content will begin to engage those becoming familiar with the product and brand and help to build advocacy.

Central to all content will be the theme of professionalism and the product’s main packaging tagline “You’re The Professional”.

Hero – Viral Film: “It’s Not What You Do, It’s How You Do It”

Positive, Emotional, Empowering, Inspirational, Entertaining.

Real life stories of women talking about their “professional” approach to work, revealing themselves to be nurses, teachers, mothers etc.

#imaprofessional and #howyoudoit To help create a sense of an online community that women want to be associated with. The empowerment theme sits perfectly with the product's ambition which is to finally give time stretched "professional" women a home hair colouring product which gives a salon equivalent look.

Hub - Tonacity Website Blog: This will host articles, interviews and other content around hair colouring, as well as other related topics such as make up and fashion advice. The blog content will serve a secondary purpose of being sharable content, helping to enhance our social media campaign.

Hygiene – How To Videos/Webcasts

Online tutorials showing, step by step, how to use Kleur Tonacity’s home kit with ease. This will help to maximise user experience and drive engagement.

KLEUR TONACITY

PRODUCT BRIEF

MARKET OPPORTUNITY

CUSTOMER PERSONA

CUSTOMER JOURNEY CAMPAIGN METRICS

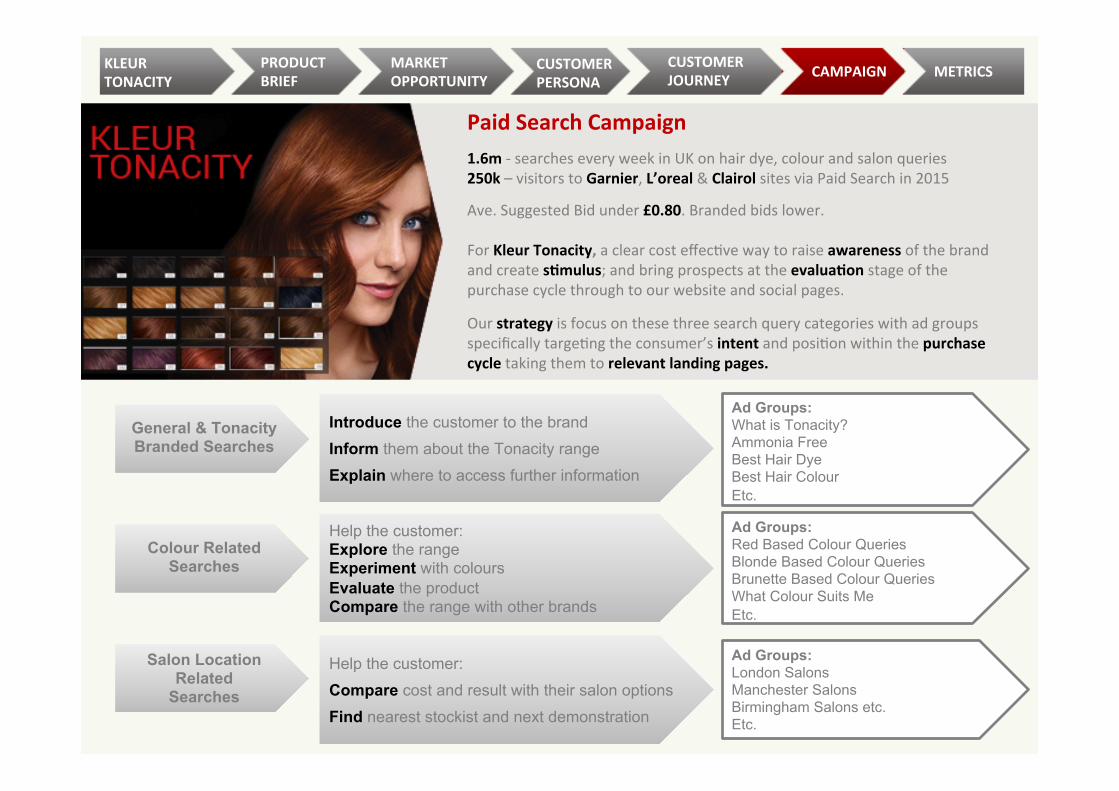

Paid Search Campaign

1.6m -‐ searches every week in UK on hair dye, colour and salon queries 250k – visitors to Garnier, L’oreal & Clairol sites via Paid Search in 2015

Ave. Suggested Bid under £0.80. Branded bids lower. For Kleur Tonacity, a clear cost effec&ve way to raise awareness of the brand and create sAmulus; and bring prospects at the evaluaAon stage of the purchase cycle through to our website and social pages.

Our strategy is focus on these three search query categories with ad groups specifically targe&ng the consumer’s intent and posi&on within the purchase cycle taking them to relevant landing pages.

General & Tonacity Branded Searches

Colour Related Searches

Salon Location Related

Searches

Introduce the customer to the brand

Inform them about the Tonacity range

Explain where to access further information

Help the customer: Explore the range Experiment with colours Evaluate the product Compare the range with other brands

Help the customer:

Compare cost and result with their salon options

Find nearest stockist and next demonstration

Ad Groups: What is Tonacity? Ammonia Free Best Hair Dye Best Hair Colour Etc. Ad Groups: Red Based Colour Queries Blonde Based Colour Queries Brunette Based Colour Queries What Colour Suits Me Etc.

Ad Groups: London Salons Manchester Salons Birmingham Salons etc. Etc.

KLEUR TONACITY

PRODUCT BRIEF

MARKET OPPORTUNITY

CUSTOMER PERSONA

CUSTOMER JOURNEY CAMPAIGN METRICS

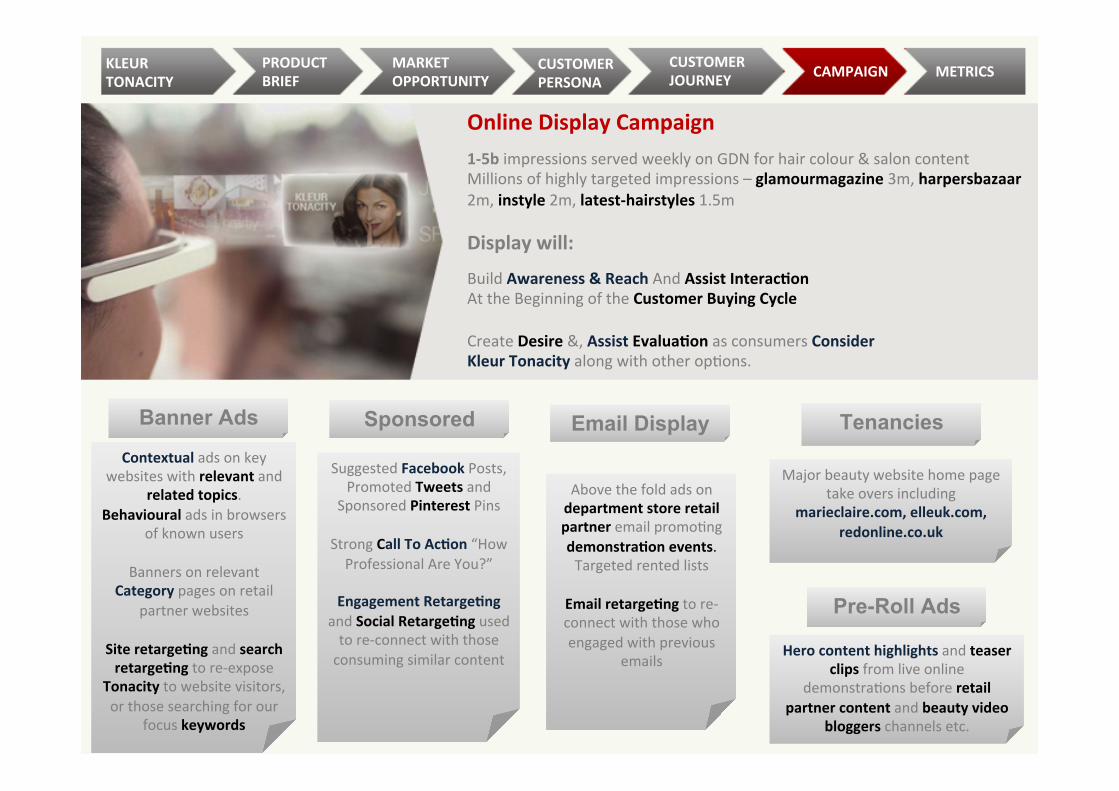

Online Display Campaign

1-‐5b impressions served weekly on GDN for hair colour & salon content Millions of highly targeted impressions – glamourmagazine 3m, harpersbazaar 2m, instyle 2m, latest-‐hairstyles 1.5m Display will:

Build Awareness & Reach And Assist InteracAon At the Beginning of the Customer Buying Cycle Create Desire &, Assist EvaluaAon as consumers Consider Kleur Tonacity along with other op&ons.

Banner Ads Sponsored

Email Display

Tenancies

Pre-Roll Ads

Contextual ads on key websites with relevant and

related topics. Behavioural ads in browsers

of known users

Banners on relevant Category pages on retail

partner websites

Site retargeAng and search retargeAng to re-‐expose

Tonacity to website visitors, or those searching for our

focus keywords

Suggested Facebook Posts, Promoted Tweets and

Sponsored Pinterest Pins

Strong Call To AcAon “How Professional Are You?”

Engagement RetargeAng

and Social RetargeAng used to re-‐connect with those consuming similar content

Above the fold ads on department store retail partner email promo&ng demonstraAon events. Targeted rented lists

Email retargeAng to re-‐connect with those who engaged with previous

emails

Major beauty website home page take overs including

marieclaire.com, elleuk.com, redonline.co.uk

Hero content highlights and teaser clips from live online

demonstra&ons before retail partner content and beauty video

bloggers channels etc.

KLEUR TONACITY

PRODUCT BRIEF

MARKET OPPORTUNITY

CUSTOMER PERSONA

CUSTOMER JOURNEY CAMPAIGN METRICS

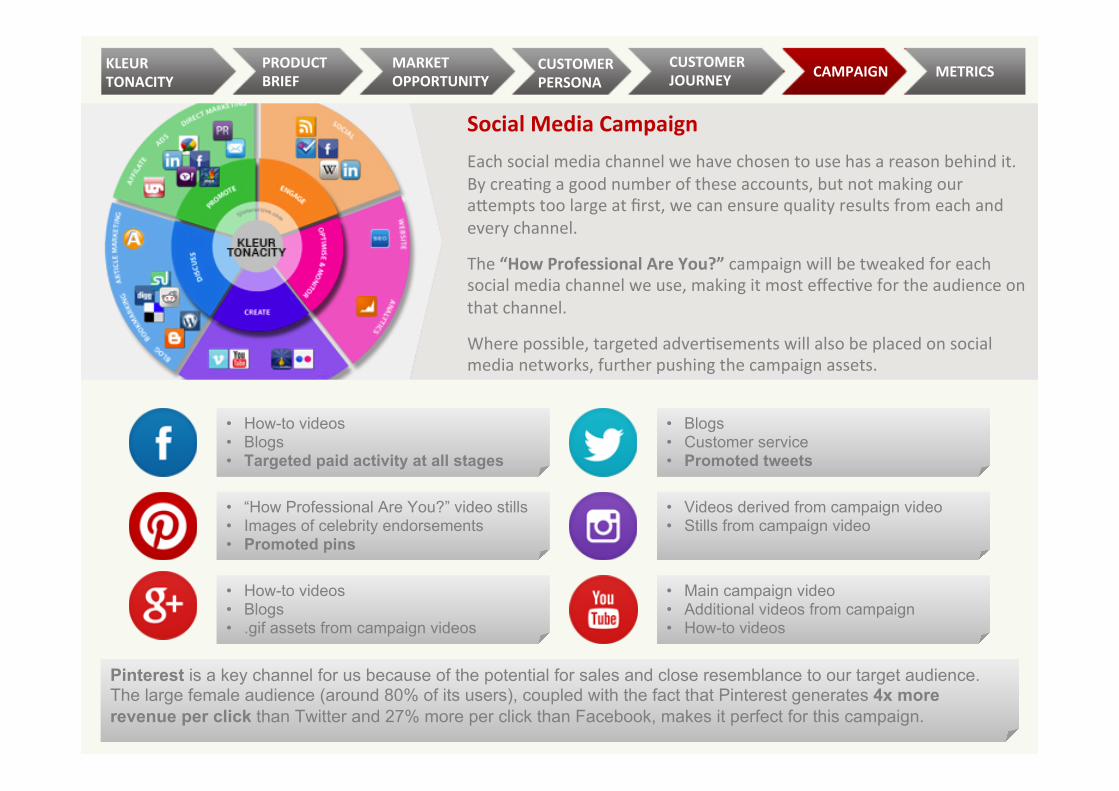

• How-to videos • Blogs • Targeted paid activity at all stages

Social Media Campaign

Each social media channel we have chosen to use has a reason behind it. By crea&ng a good number of these accounts, but not making our amempts too large at first, we can ensure quality results from each and every channel.

The “How Professional Are You?” campaign will be tweaked for each social media channel we use, making it most effec&ve for the audience on that channel.

Where possible, targeted adver&sements will also be placed on social media networks, further pushing the campaign assets.

• Blogs • Customer service • Promoted tweets

• “How Professional Are You?” video stills • Images of celebrity endorsements • Promoted pins

• Videos derived from campaign video • Stills from campaign video

• How-to videos • Blogs • .gif assets from campaign videos

• Main campaign video • Additional videos from campaign • How-to videos

Pinterest is a key channel for us because of the potential for sales and close resemblance to our target audience. The large female audience (around 80% of its users), coupled with the fact that Pinterest generates 4x more revenue per click than Twitter and 27% more per click than Facebook, makes it perfect for this campaign.

KLEUR TONACITY

PRODUCT BRIEF

MARKET OPPORTUNITY

CUSTOMER PERSONA

CUSTOMER JOURNEY CAMPAIGN METRICS

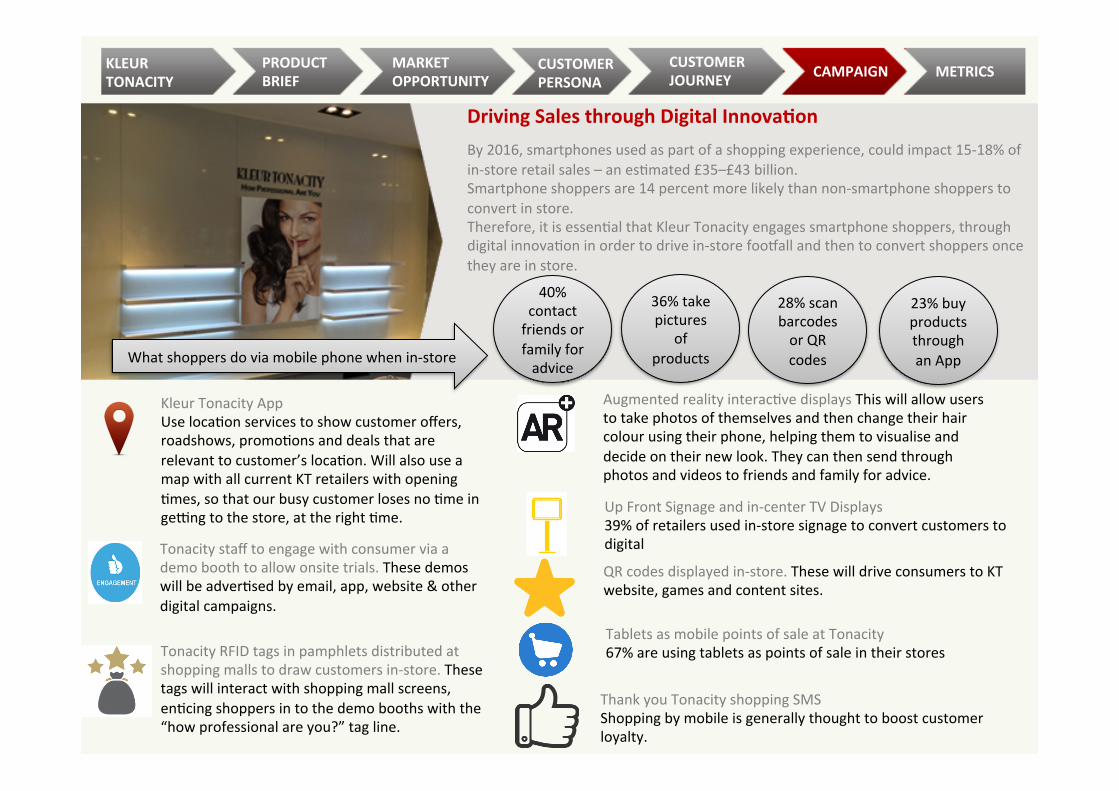

Driving Sales through Digital InnovaAon

By 2016, smartphones used as part of a shopping experience, could impact 15-‐18% of in-‐store retail sales – an es&mated £35–£43 billion. Smartphone shoppers are 14 percent more likely than non-‐smartphone shoppers to convert in store. Therefore, it is essen&al that Kleur Tonacity engages smartphone shoppers, through digital innova&on in order to drive in-‐store foooall and then to convert shoppers once they are in store.

Tonacity staff to engage with consumer via a demo booth to allow onsite trials. These demos will be adver&sed by email, app, website & other digital campaigns.

Tonacity RFID tags in pamphlets distributed at shopping malls to draw customers in-‐store. These tags will interact with shopping mall screens, en&cing shoppers in to the demo booths with the “how professional are you?” tag line.

Up Front Signage and in-‐center TV Displays 39% of retailers used in-‐store signage to convert customers to digital

Tablets as mobile points of sale at Tonacity 67% are using tablets as points of sale in their stores

QR codes displayed in-‐store. These will drive consumers to KT website, games and content sites.

Thank you Tonacity shopping SMS Shopping by mobile is generally thought to boost customer loyalty.

Kleur Tonacity App Use loca&on services to show customer offers, roadshows, promo&ons and deals that are relevant to customer’s loca&on. Will also use a map with all current KT retailers with opening &mes, so that our busy customer loses no &me in gerng to the store, at the right &me.

Augmented reality interac&ve displays This will allow users to take photos of themselves and then change their hair colour using their phone, helping them to visualise and decide on their new look. They can then send through photos and videos to friends and family for advice.

40% contact friends or family for advice

What shoppers do via mobile phone when in-‐store

36% take pictures

of products

28% scan barcodes or QR codes

23% buy products through an App

KLEUR TONACITY

PRODUCT BRIEF

MARKET OPPORTUNITY

CUSTOMER PERSONA

CUSTOMER JOURNEY CAMPAIGN METRICS

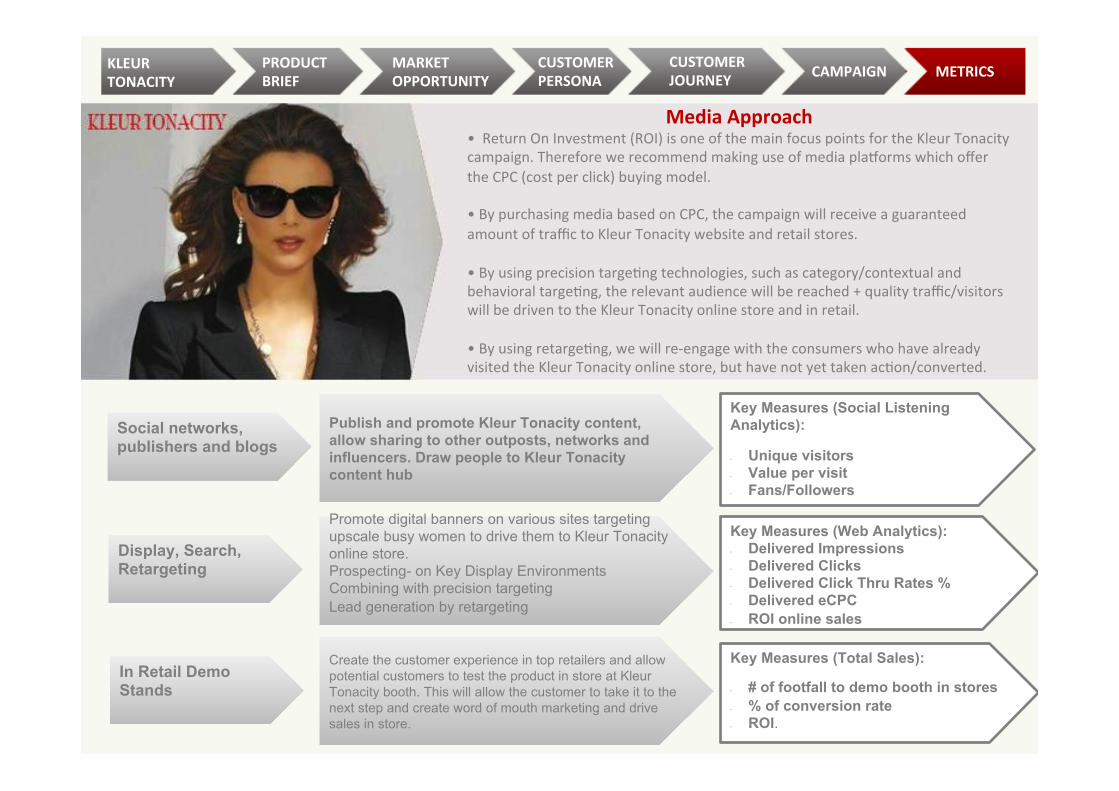

Media Approach • Return On Investment (ROI) is one of the main focus points for the Kleur Tonacity campaign. Therefore we recommend making use of media plaoorms which offer the CPC (cost per click) buying model. • By purchasing media based on CPC, the campaign will receive a guaranteed amount of traffic to Kleur Tonacity website and retail stores. • By using precision targe&ng technologies, such as category/contextual and behavioral targe&ng, the relevant audience will be reached + quality traffic/visitors will be driven to the Kleur Tonacity online store and in retail. • By using retarge&ng, we will re-‐engage with the consumers who have already visited the Kleur Tonacity online store, but have not yet taken ac&on/converted.

Social networks, publishers and blogs

Display, Search, Retargeting

In Retail Demo Stands

Publish and promote Kleur Tonacity content, allow sharing to other outposts, networks and influencers. Draw people to Kleur Tonacity content hub

Promote digital banners on various sites targeting upscale busy women to drive them to Kleur Tonacity online store. Prospecting- on Key Display Environments Combining with precision targeting Lead generation by retargeting

Create the customer experience in top retailers and allow potential customers to test the product in store at Kleur Tonacity booth. This will allow the customer to take it to the next step and create word of mouth marketing and drive sales in store.

Key Measures (Social Listening Analytics): • Unique visitors • Value per visit • Fans/Followers Key Measures (Web Analytics): • Delivered Impressions • Delivered Clicks • Delivered Click Thru Rates % • Delivered eCPC • ROI online sales Key Measures (Total Sales):

• # of footfall to demo booth in stores • % of conversion rate • ROI.

KLEUR TONACITY

PRODUCT BRIEF

MARKET OPPORTUNITY

CUSTOMER PERSONA

CUSTOMER JOURNEY CAMPAIGN METRICS

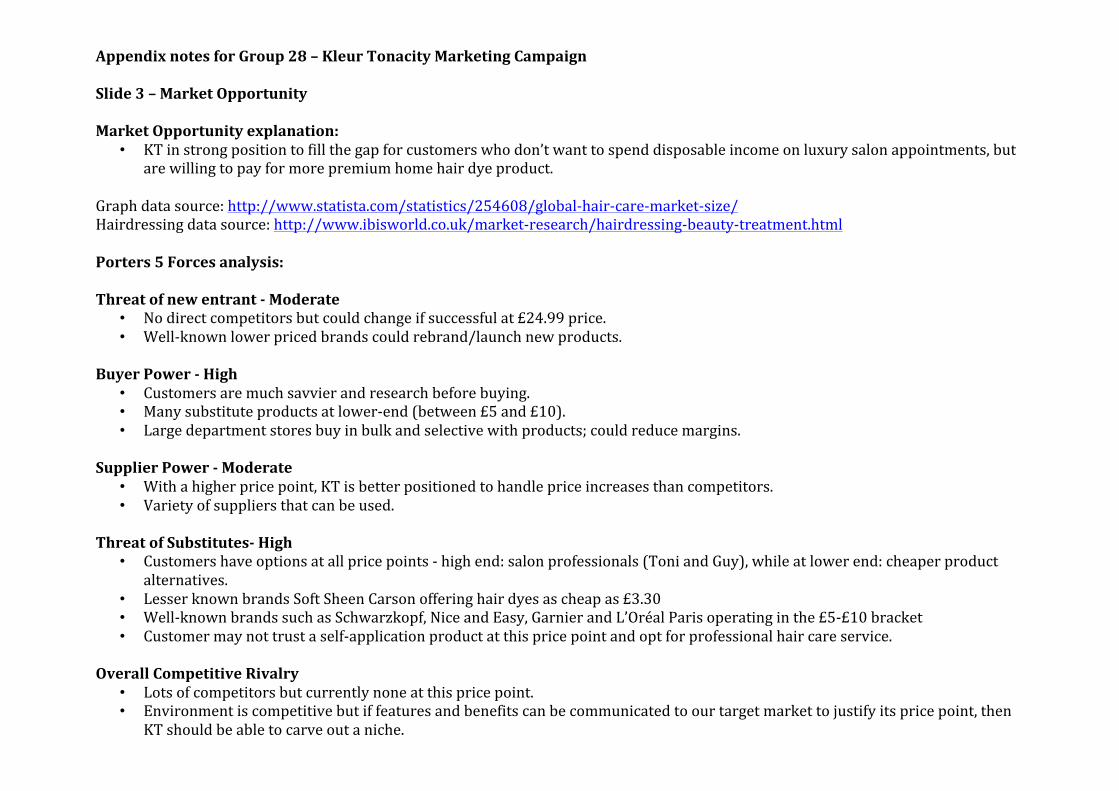

Appendix notes for Group 28 – Kleur Tonacity Marketing Campaign Slide 3 – Market Opportunity Market Opportunity explanation:

• KT in strong position to fill the gap for customers who don’t want to spend disposable income on luxury salon appointments, but are willing to pay for more premium home hair dye product.

Graph data source: http://www.statista.com/statistics/254608/global-‐hair-‐care-‐market-‐size/ Hairdressing data source: http://www.ibisworld.co.uk/market-‐research/hairdressing-‐beauty-‐treatment.html Porters 5 Forces analysis: Threat of new entrant -‐ Moderate

• No direct competitors but could change if successful at £24.99 price. • Well-‐known lower priced brands could rebrand/launch new products.

Buyer Power -‐ High

• Customers are much savvier and research before buying. • Many substitute products at lower-‐end (between £5 and £10). • Large department stores buy in bulk and selective with products; could reduce margins.

Supplier Power -‐ Moderate

• With a higher price point, KT is better positioned to handle price increases than competitors. • Variety of suppliers that can be used.

Threat of Substitutes-‐ High

• Customers have options at all price points -‐ high end: salon professionals (Toni and Guy), while at lower end: cheaper product alternatives.

• Lesser known brands Soft Sheen Carson offering hair dyes as cheap as £3.30 • Well-‐known brands such as Schwarzkopf, Nice and Easy, Garnier and L’Oréal Paris operating in the £5-‐£10 bracket • Customer may not trust a self-‐application product at this price point and opt for professional hair care service.

Overall Competitive Rivalry

• Lots of competitors but currently none at this price point. • Environment is competitive but if features and benefits can be communicated to our target market to justify its price point, then

KT should be able to carve out a niche.

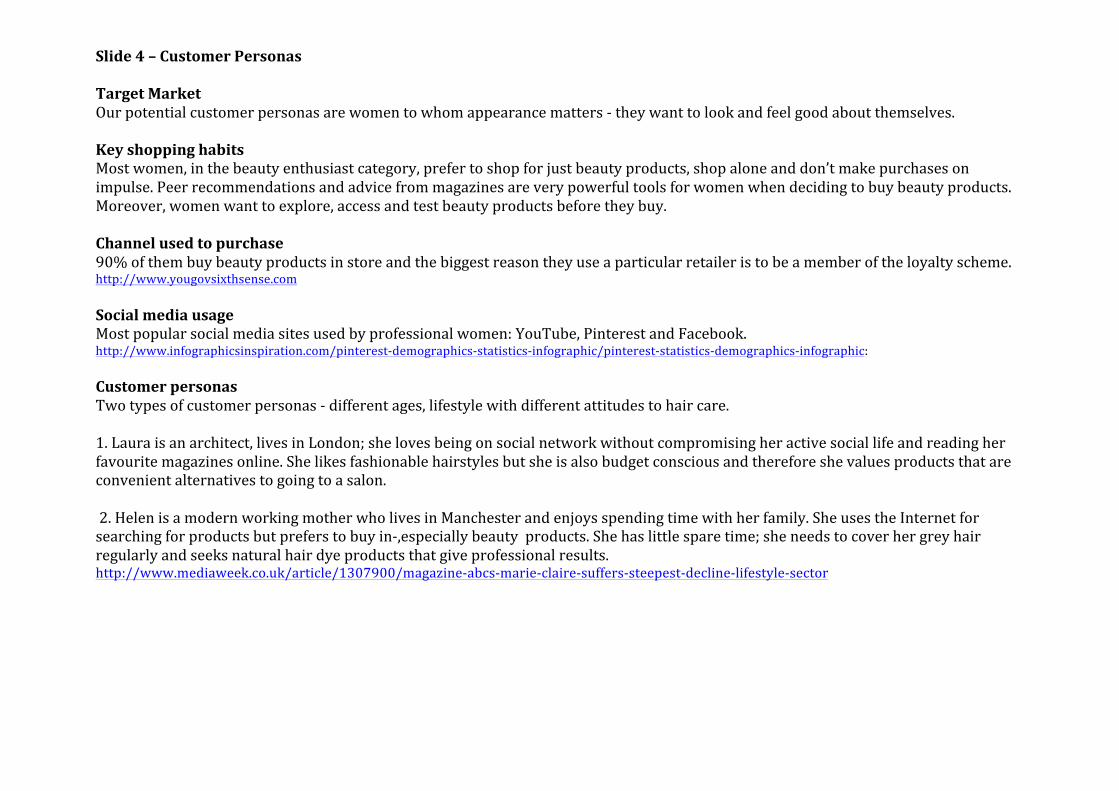

Slide 4 – Customer Personas Target Market Our potential customer personas are women to whom appearance matters -‐ they want to look and feel good about themselves. Key shopping habits Most women, in the beauty enthusiast category, prefer to shop for just beauty products, shop alone and don’t make purchases on impulse. Peer recommendations and advice from magazines are very powerful tools for women when deciding to buy beauty products. Moreover, women want to explore, access and test beauty products before they buy. Channel used to purchase 90% of them buy beauty products in store and the biggest reason they use a particular retailer is to be a member of the loyalty scheme. http://www.yougovsixthsense.com Social media usage Most popular social media sites used by professional women: YouTube, Pinterest and Facebook. http://www.infographicsinspiration.com/pinterest-‐demographics-‐statistics-‐infographic/pinterest-‐statistics-‐demographics-‐infographic: Customer personas Two types of customer personas -‐ different ages, lifestyle with different attitudes to hair care. 1. Laura is an architect, lives in London; she loves being on social network without compromising her active social life and reading her favourite magazines online. She likes fashionable hairstyles but she is also budget conscious and therefore she values products that are convenient alternatives to going to a salon. 2. Helen is a modern working mother who lives in Manchester and enjoys spending time with her family. She uses the Internet for searching for products but prefers to buy in-‐,especially beauty products. She has little spare time; she needs to cover her grey hair regularly and seeks natural hair dye products that give professional results. http://www.mediaweek.co.uk/article/1307900/magazine-‐abcs-‐marie-‐claire-‐suffers-‐steepest-‐decline-‐lifestyle-‐sector

Slide 5 – Customer Journey TOP 10 MOST UK INFLUENTIAL BEAUTY BLOGGERS as per http://www.cision.com/uk/social-‐media-‐index/top-‐10-‐uk-‐beauty-‐blogs/ Pixiwoo.com Lisa Eldridge A Model Recommends British Beauty Blogger Zoella London Beauty Queen ReallyRee essie-‐button Vivianna Does Makeup Hello October Ten Largest Shopping Centres in UK by Sq ft.: Westfield Stratford 1.9m John Lewis Metrocentre 1.8m Debenhams / HOF

Trafford Centre 1.8m Debenhams / J Lewis / Selfridges

Milton Keynes Centre 1.8m HOF / J Lewis

Bluwater 1.65m HOF / J Lewis Westfield London 1.6m Debenhams / HOF Princess Charles Sq Meadowhall 1.5m Debenhams / HOF Cabot Circus 1.5m HOF Victoria Gate 1.4m J Lewis 9 out of 10 are anchored by our retail partners offering a major tactical advantage through use of each centres prime shopping throughways where we can set up demonstration stands. Media usage among UK adults: http://stakeholders.ofcom.org.uk/binaries/research/media-‐literacy/media-‐lit-‐10years/2015_Adults_media_use_and_attitudes_report.pdf Research online, buy in store: http://www.fierceretail.com/story/73-‐consumers-‐browse-‐online-‐purchase-‐store/2015-‐02-‐10

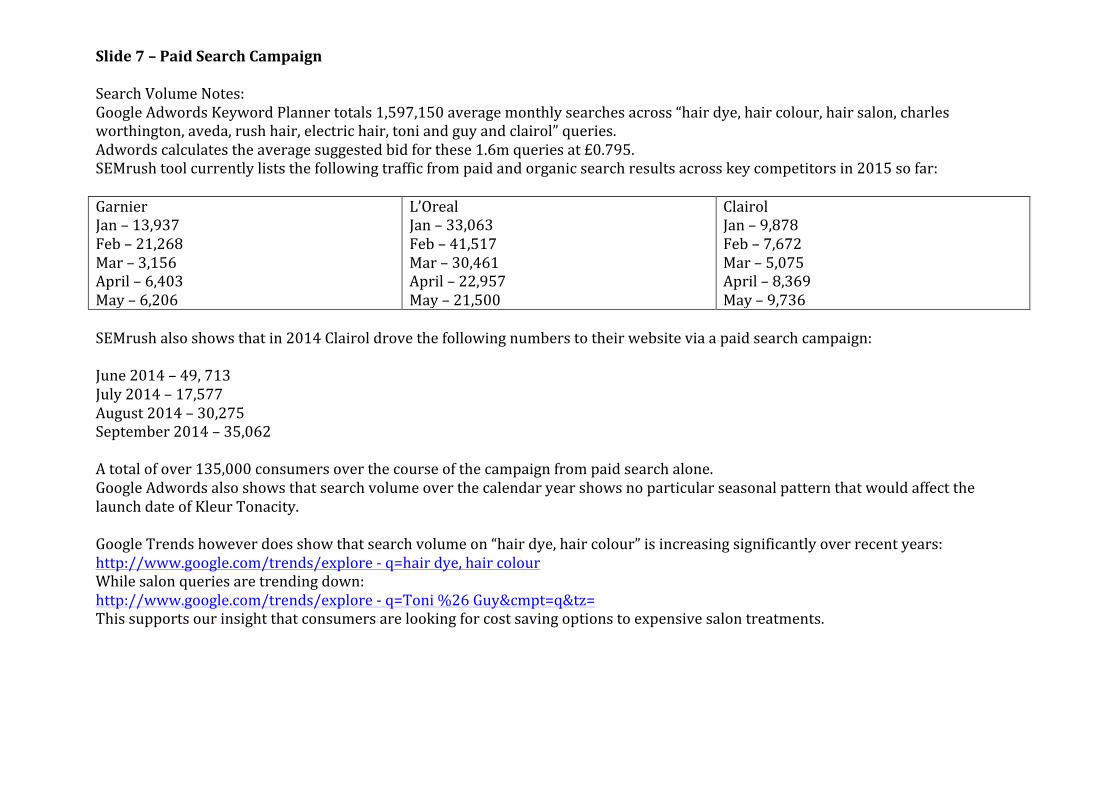

Slide 7 – Paid Search Campaign Search Volume Notes: Google Adwords Keyword Planner totals 1,597,150 average monthly searches across “hair dye, hair colour, hair salon, charles worthington, aveda, rush hair, electric hair, toni and guy and clairol” queries. Adwords calculates the average suggested bid for these 1.6m queries at £0.795. SEMrush tool currently lists the following traffic from paid and organic search results across key competitors in 2015 so far: Garnier Jan – 13,937 Feb – 21,268 Mar – 3,156 April – 6,403 May – 6,206

L’Oreal Jan – 33,063 Feb – 41,517 Mar – 30,461 April – 22,957 May – 21,500

Clairol Jan – 9,878 Feb – 7,672 Mar – 5,075 April – 8,369 May – 9,736

SEMrush also shows that in 2014 Clairol drove the following numbers to their website via a paid search campaign: June 2014 – 49, 713 July 2014 – 17,577 August 2014 – 30,275 September 2014 – 35,062 A total of over 135,000 consumers over the course of the campaign from paid search alone. Google Adwords also shows that search volume over the calendar year shows no particular seasonal pattern that would affect the launch date of Kleur Tonacity. Google Trends however does show that search volume on “hair dye, hair colour” is increasing significantly over recent years: http://www.google.com/trends/explore -‐ q=hair dye, hair colour While salon queries are trending down: http://www.google.com/trends/explore -‐ q=Toni %26 Guy&cmpt=q&tz= This supports our insight that consumers are looking for cost saving options to expensive salon treatments.

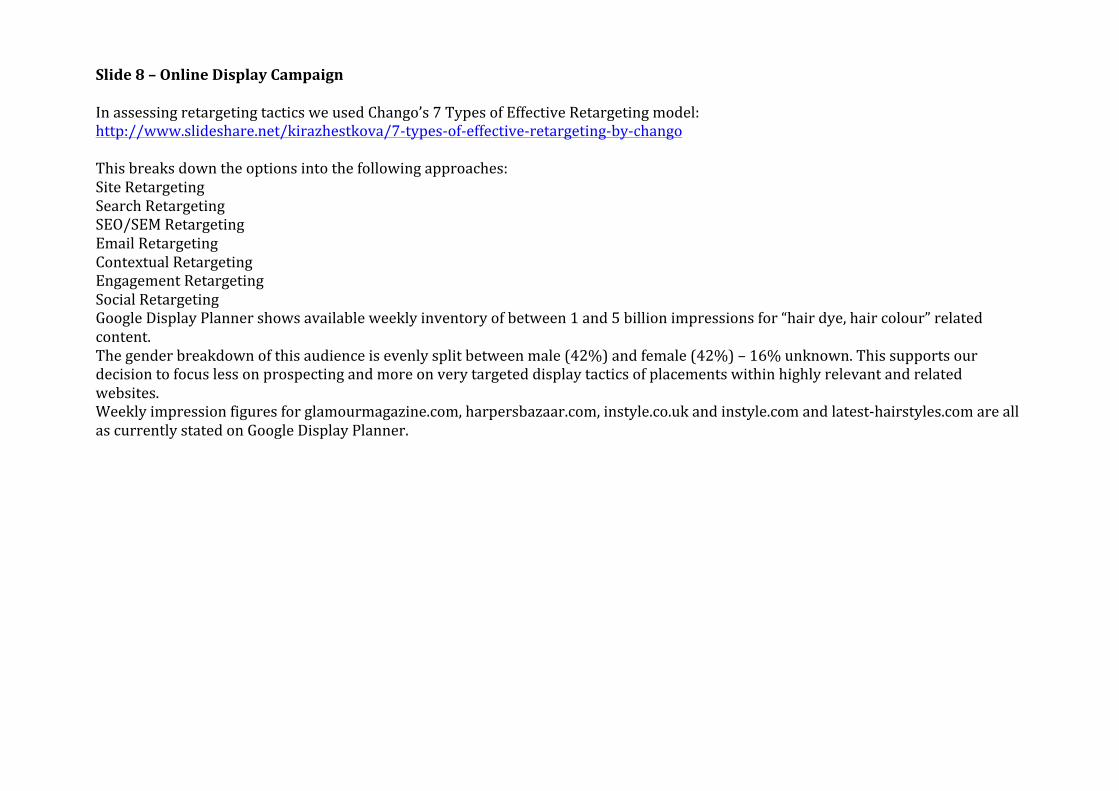

Slide 8 – Online Display Campaign In assessing retargeting tactics we used Chango’s 7 Types of Effective Retargeting model: http://www.slideshare.net/kirazhestkova/7-‐types-‐of-‐effective-‐retargeting-‐by-‐chango This breaks down the options into the following approaches: Site Retargeting Search Retargeting SEO/SEM Retargeting Email Retargeting Contextual Retargeting Engagement Retargeting Social Retargeting Google Display Planner shows available weekly inventory of between 1 and 5 billion impressions for “hair dye, hair colour” related content. The gender breakdown of this audience is evenly split between male (42%) and female (42%) – 16% unknown. This supports our decision to focus less on prospecting and more on very targeted display tactics of placements within highly relevant and related websites. Weekly impression figures for glamourmagazine.com, harpersbazaar.com, instyle.co.uk and instyle.com and latest-‐hairstyles.com are all as currently stated on Google Display Planner.

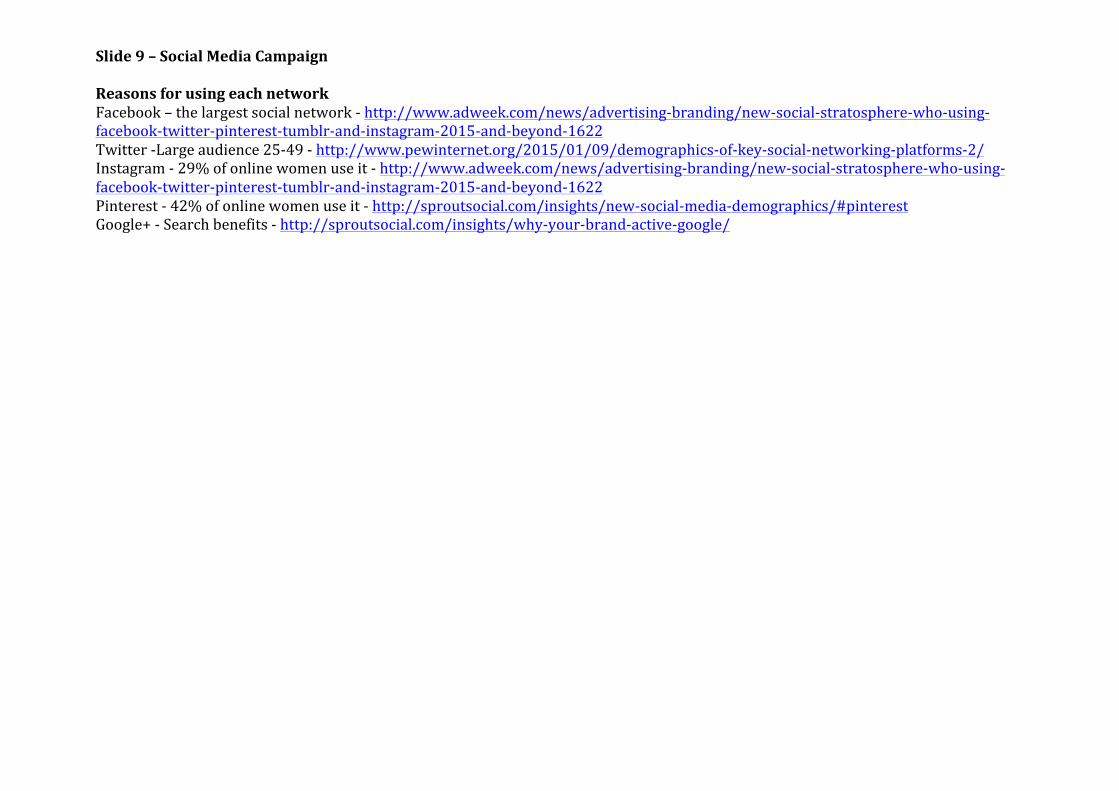

Slide 9 – Social Media Campaign Reasons for using each network Facebook – the largest social network -‐ http://www.adweek.com/news/advertising-‐branding/new-‐social-‐stratosphere-‐who-‐using-‐facebook-‐twitter-‐pinterest-‐tumblr-‐and-‐instagram-‐2015-‐and-‐beyond-‐1622 Twitter -‐Large audience 25-‐49 -‐ http://www.pewinternet.org/2015/01/09/demographics-‐of-‐key-‐social-‐networking-‐platforms-‐2/ Instagram -‐ 29% of online women use it -‐ http://www.adweek.com/news/advertising-‐branding/new-‐social-‐stratosphere-‐who-‐using-‐facebook-‐twitter-‐pinterest-‐tumblr-‐and-‐instagram-‐2015-‐and-‐beyond-‐1622 Pinterest -‐ 42% of online women use it -‐ http://sproutsocial.com/insights/new-‐social-‐media-‐demographics/#pinterest Google+ -‐ Search benefits -‐ http://sproutsocial.com/insights/why-‐your-‐brand-‐active-‐google/

Slide 10 – Driving Sales Through Digital Innovation By 2016 we expect the influence of mobile will have significantly changed the UK retail channel landscape. In fact, we project the mobile influence factor will reach 15-‐18% of total retail sales, amounting to £35–£43billion in mobile-‐influenced store sales by 2016. We must allow customers to maintain control of their information. Whilst 76% of smartphone users will use their phones GPS or location based services, customers are uncomfortable with retailers knowing when they are near/ in their store: only 21% would be happy for a retailer to know they are nearby & 27% happy for retailer to know they are inside a store. Even though the integrated phone technology would have to be switched on, people are uncomfortable with their movements being monitored. Omni-‐Channel Insights: Customer experience accounts for 47% of customer loyalty Smartphones influenced $159 billion in U.S. store sales in 2012 8 in 10 smartphone shoppers use mobile in-‐store to help with shopping The Future of Retail Marketing 77% of consumers prefer email for permission-‐based promotional messaging 39% of retailers used in-‐store signage to convert customers to digital 44% of retailers do email acquisition at point-‐of-‐purchase Reference Links http://blog.gfk.com/2015/04/shoppers-‐bringing-‐online-‐competition-‐inside-‐bricks-‐and-‐mortar-‐stores/ http://www.shopify.com/blog/14210261-‐10-‐slideshare-‐presentations-‐on-‐the-‐future-‐of-‐omni-‐channel-‐retail http://www2.deloitte.com/content/dam/Deloitte/uk/Documents/consumer-‐business/deloitte-‐uk-‐the-‐dawn-‐of-‐mobile-‐influence-‐final.pdf https://www.downtowndevelopment.com/pdf/2_us_retail_Mobile_Influence.pdf http://mediazone.brighttalk.com/comm/sitedata/c52f1bd66cc19d05628bd8bf27af3ad6/download/13983_MobileReport_lowres%20%281%29.pdf http://www.accenture.com/sitecollectiondocuments/accenture-‐customer-‐desires-‐vs-‐retailer-‐capabilities.pdf