Your future. Our Mission. Student Financial Assistance Office

Your future. Our Mission.

Feb 25, 2016

Your future. Our Mission. Student Financial Assistance Office. Repaying Student Loans. – Take inventory your federal student loans – Explore repayment plans available – Understand the basics of consolidation – Learn about deferment and forbearance . Taking Inventory. - PowerPoint PPT Presentation

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Your future. Our Mission.Student Financial Assistance Office

Repaying Student Loans

– Take inventory your federal student loans– Explore repayment plans available– Understand the basics of consolidation– Learn about deferment and forbearance

Taking InventoryWhere can I obtain information on my

federal loans?

• – National Student Loan Data System (NSLDS)http://www.nslds.ed.gov/

Provides loan amounts, loan holders, and loan servicers

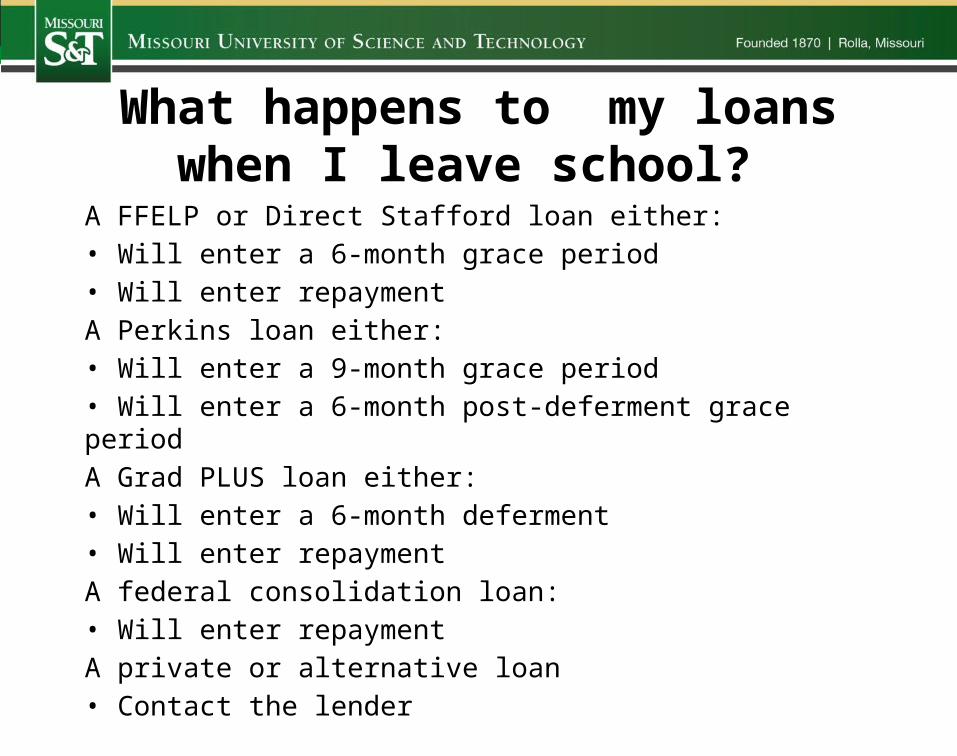

What happens to my loans when I leave school?

A FFELP or Direct Stafford loan either:• Will enter a 6-month grace period• Will enter repaymentA Perkins loan either:• Will enter a 9-month grace period• Will enter a 6-month post-deferment grace periodA Grad PLUS loan either:• Will enter a 6-month deferment• Will enter repaymentA federal consolidation loan:• Will enter repaymentA private or alternative loan• Contact the lender

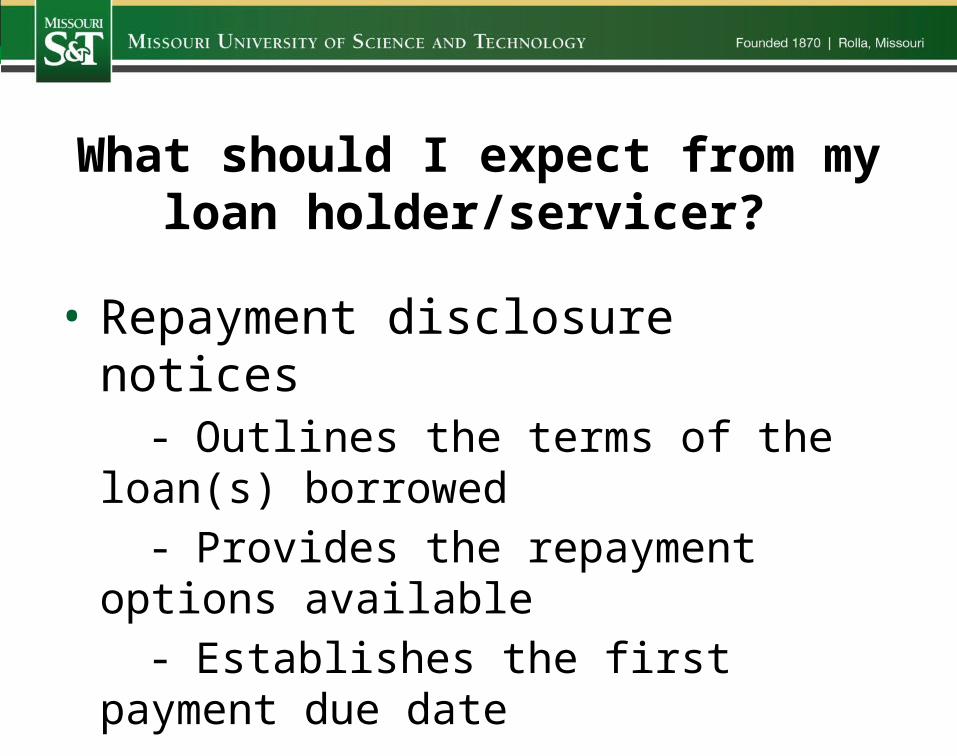

What should I expect from my loan holder/servicer?

• Repayment disclosure notices- Outlines the terms of the loan(s)

borrowed- Provides the repayment options

available- Establishes the first payment due

date

What does my loan holder/servicer expect from me?

- To select a repayment plan- To make timely payments on your

loans- To provide updated contact

information whenever it changes- To contact the loan holder whenever

you are having difficulty managing repayment

Learn Moresfa.mst.edu

Can I pre-pay on my loans?

Learn Moresfa.mst.edu

Yes…- If sending in a prepayment, make sure

you inform the lender to apply the prepayment to the principal of the

loan balance

- There is no prepayment penalty

What repayment plans are available? - Standard- Graduated- Extended- Income-sensitive (FFELP only)- Income-contingent (FDLP only)- Income-based

Overview of repayment plans

Learn Moresfa.mst.edu

How do repayment plans work?• Standard:

- Lowest total loan cost. - Regular payments of both principal and interest are due

monthly, excluding periods of deferment and forbearance- Minimum monthly payment is $50 with 10 yr repayment

• Graduated: - Monthly payments are smaller at the start of the repayment

period and gradually increase every two years- 10-year repayment term- Total amount paid in interest will be greater than under the

standard repayment plan

Repayment Plans con’t• Extended: - Lengthens repayment term up to 25 years

- Available to borrowers with more than $30,000 in federal student loans (per program)

- Total interest costs may be higher over life of the loan, although monthly payment amount may be lower

Repayment plans con’t• Income-sensitive (FFELP):- Offered only to borrowers under the FFELP- Monthly payment varies according to gross monthly

income- Monthly payment covers at least monthly accruing

interest- Must reapply annually- Total interest costs will be higher over the life of your

loan than with standard repayment- Maximum repayment period is 10 years

Repayment plans con’t• Income-contingent (FDLP):- Offered only to borrowers under the Direct Loan

Program - Monthly payment based on adjusted gross

income, family size, and total Direct Loan debt - Maximum repayment period is 25 years, and any

balance after 25 years (time spent in deferment or forbearance does not count) is forgiven.

What is income-based repayment (IBR)?

Learn Moresfa.mst.edu

- IBR is designed to help borrowers experiencing a “partial financial hardship”.

- Available to Stafford, Grad PLUS, and certain consolidation borrowers.

How do I apply for IBR?Contact loan holder/servicer and request an IBR plan- IBR forms available at:

http://studentaid.ed.gov/PORTALSWebApp/students/english/IBRPlan.jsp

- Borrower must:Apply annually (payment amount may fluctuate)

- Provide permission for IRS to disclose AGI "and other tax return information“

- Certify family size

Basics of Consolidation

– Consolidation enables you to bundle one or more federal student loans into a single new loan.

– At time of consolidation, your consolidating loan holder pays off the outstanding balances of the loans you include in the consolidation.

– No fees.

Who can consolidate?

– Any federal student loan borrower, including:

- Borrowers with student loans.- Borrowers with student & parent loans.

Learn Moresfa.mst.edu

How do I qualify?

– You must be in your grace period or in repayment on each loan being consolidated.

– You can still obtain a Consolidation loan if you are delinquent or in default on one or more of your existing loans.

What loans may be consolidated?

– Federal Family Education Loans– Federal Direct Loans– Federal Perkins Loans– Health Professions Student Loans– Nursing Student Loans– Health Education Assistance Loans

Learn Moresfa.mst.edu

What loans may not be consolidate?

– Private (alternative) education loans– Other consumer debt**Private consolidation loans

– Do not offer the same advantages(i.e., repayment options, deferments, etc.)as a federal consolidation loan– Interest rate will be credit-based and likelyhigher than a federal consolidation loan

Can I ever “Re-consolidate”?

– Generally, no– You may only reconsolidate if you consolidate an existing Consolidation loan with another loan outside the Consolidation loan

Learn Moresfa.mst.edu

Factors to consider in consolidating

+ Bring together loans with multiple loan holder for convenience of one payment.

+ Lower loan payments by lengthening repayment period.

+ May be able to lock in a more favorable interest rate.

- May lose some or all of grace period.- May lose certain borrower benefits- May increase total cost of loan if you lengthen your

repayment period, you will pay more interest in the long run.

Loan Deferment• A deferment is a period of time when payment on a

loan is temporarily postponed.• Interest payment

– Federal government pays the interest during deferments for subsidized loans and for the underlying subsidized loans that were consolidated.

– Borrower is responsible for the interest for unsubsidized Stafford loans, GradPLUS loans, and PLUS loans and for the underlying unsubsidized loans that were consolidated

Types of Deferment• Enrolled at least half-time at an approved postsecondary

school• Study in an approved graduate fellowship program or an

approved rehabilitation training program for the disabled• Unable to find full-time employment (up to 3 years)• Economic Hardship (up to 3 years)• Engages in service listed under discharge/cancellation

conditions (Perkins only)• Active Military Duty, for loans first disbursed on/after July 1,

2001; while borrower is on active duty during a war or other military option, or national emergency (up to 3 years)

• www.studentloans.gov

Forbearance• A period of time during which the borrower is

permitted to temporarily cease making payments or reduce the amount of the payments.

– Borrower is liable for all interest that accrues on the loan.

– Contact your loan holder• Some deferment types require an application

Helpful Resources• www.federalstudentaid.ed.gov/students.html• www.studentloans.gov• www.nslds.ed.gov• www.dl.ed.gov• www.loanconsolidation.ed.gov• www.finaid.org• www.tgslc.org/borrowers

Student Financial Assistance Office

• G-1 Parker Hall• 573-341-4282• 1-800-522-0938• [email protected]• sfa.mst.edu

Related Documents