Topic# 3: General Theory of Taxation. Romanian tax system General theory of taxation PROF. ANDREEA STOIAN, PHD | LECTURE 5

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Topic# 3:

General Theory of Taxation.

Romanian tax systemGeneral theory of taxationPROF. ANDREEA STOIAN, PHD | LECTURE 5

Content

General theory

of taxation

Taxes

Principles of taxation

Tax base and tax rate

structure

Learning outcomes

Students will be able to:

• Define the concept of tax

• Know the principle of an efficient and fair taxation

• Understand the basic terminology use to analyze the impact of taxes on the economy,

including the tax base and tax structure

• Discuss issues related to the distribution of the tax burden

Mick Jagger

"I love America,

but I can't spend

the whole year

here. I can't afford

the taxes."

What are

taxes?

Compulsory payments associated with certain activities

Revenues collected through taxation are used to purchase the inputs necessary to produce government-supplied goods or to redistribute the purchasing power among citizens

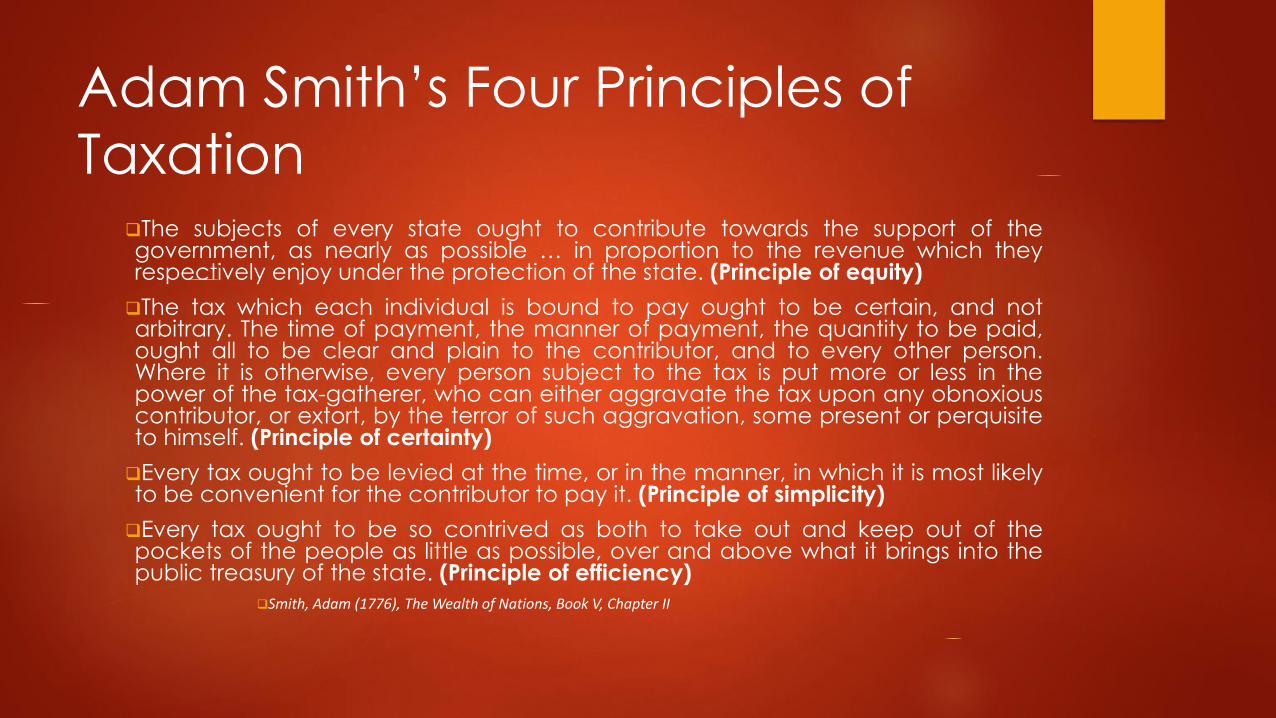

Adam Smith’s Four Principles of

TaxationThe subjects of every state ought to contribute towards the support of thegovernment, as nearly as possible … in proportion to the revenue which theyrespectively enjoy under the protection of the state. (Principle of equity)

The tax which each individual is bound to pay ought to be certain, and notarbitrary. The time of payment, the manner of payment, the quantity to be paid,ought all to be clear and plain to the contributor, and to every other person.Where it is otherwise, every person subject to the tax is put more or less in thepower of the tax-gatherer, who can either aggravate the tax upon any obnoxiouscontributor, or extort, by the terror of such aggravation, some present or perquisiteto himself. (Principle of certainty)

Every tax ought to be levied at the time, or in the manner, in which it is most likelyto be convenient for the contributor to pay it. (Principle of simplicity)

Every tax ought to be so contrived as both to take out and keep out of thepockets of the people as little as possible, over and above what it brings into thepublic treasury of the state. (Principle of efficiency)

Smith, Adam (1776), The Wealth of Nations, Book V, Chapter II

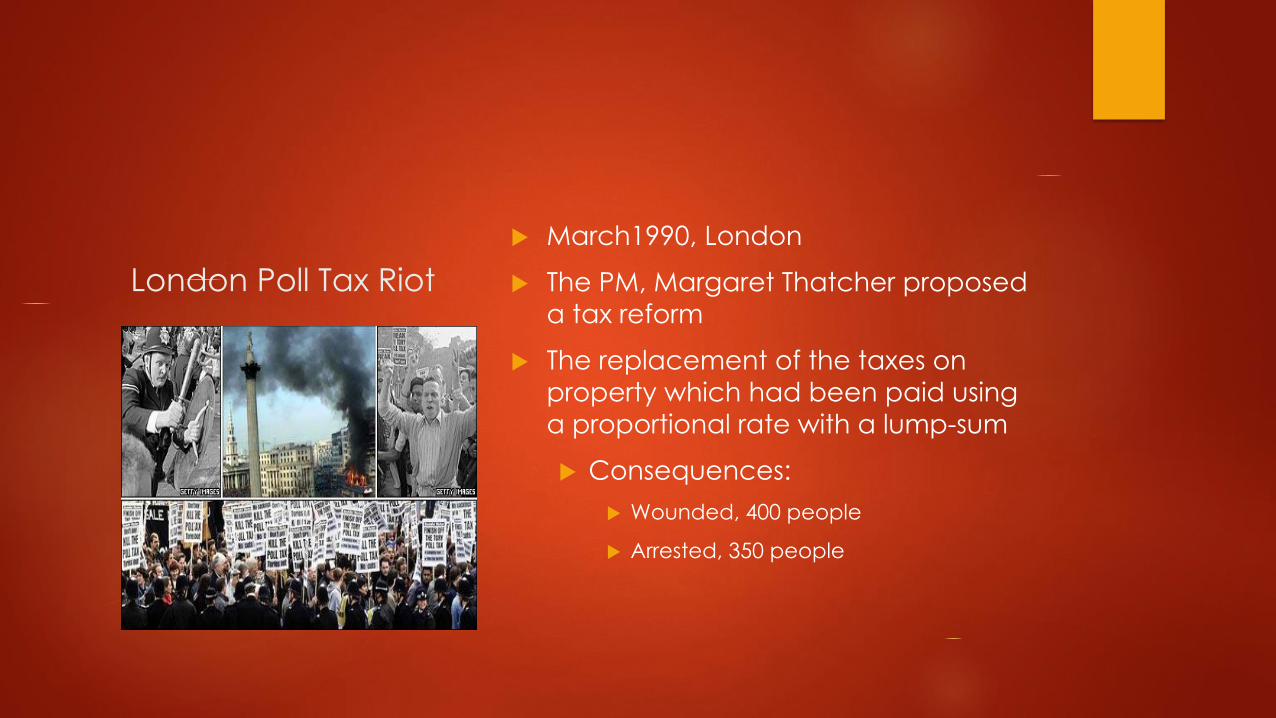

London Poll Tax Riot

March1990, London

The PM, Margaret Thatcher proposed

a tax reform

The replacement of the taxes on

property which had been paid using

a proportional rate with a lump-sum

Consequences:

Wounded, 400 people

Arrested, 350 people

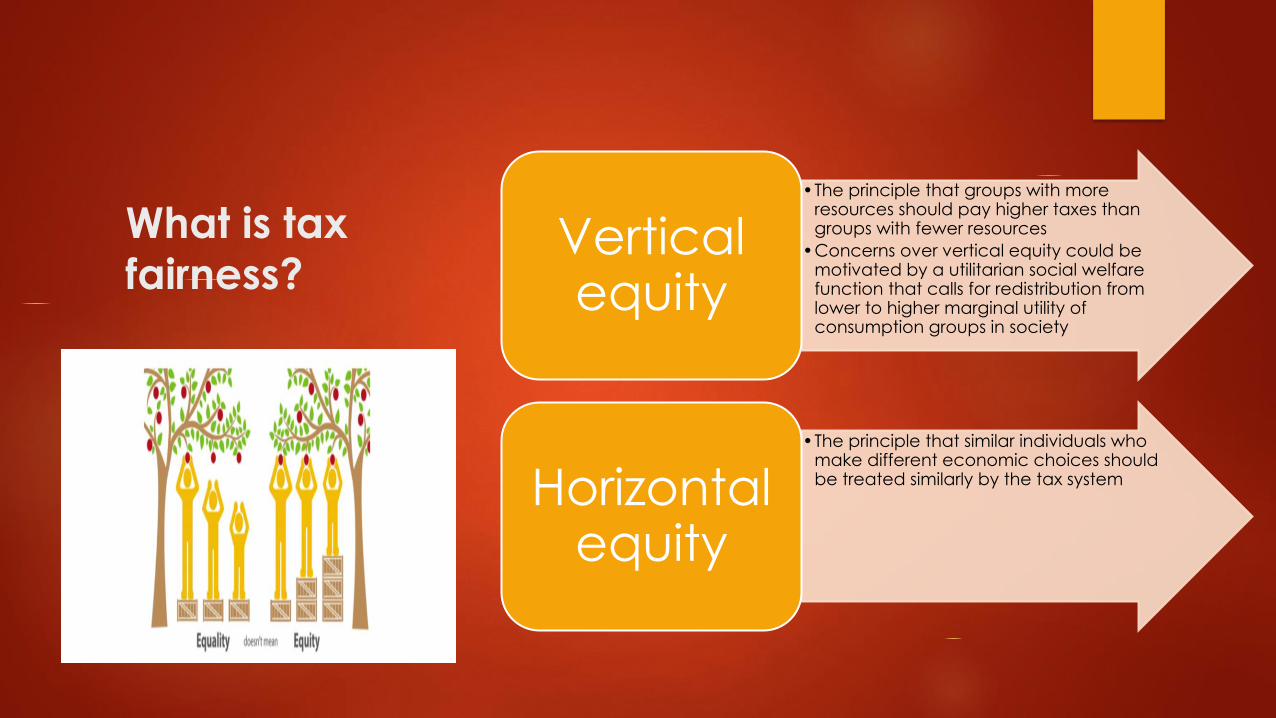

What is tax

fairness?

•The principle that groups with more resources should pay higher taxes than groups with fewer resources

•Concerns over vertical equity could be motivated by a utilitarian social welfare function that calls for redistribution from lower to higher marginal utility of consumption groups in society

Vertical equity

•The principle that similar individuals who make different economic choices should be treated similarly by the tax systemHorizontal

equity

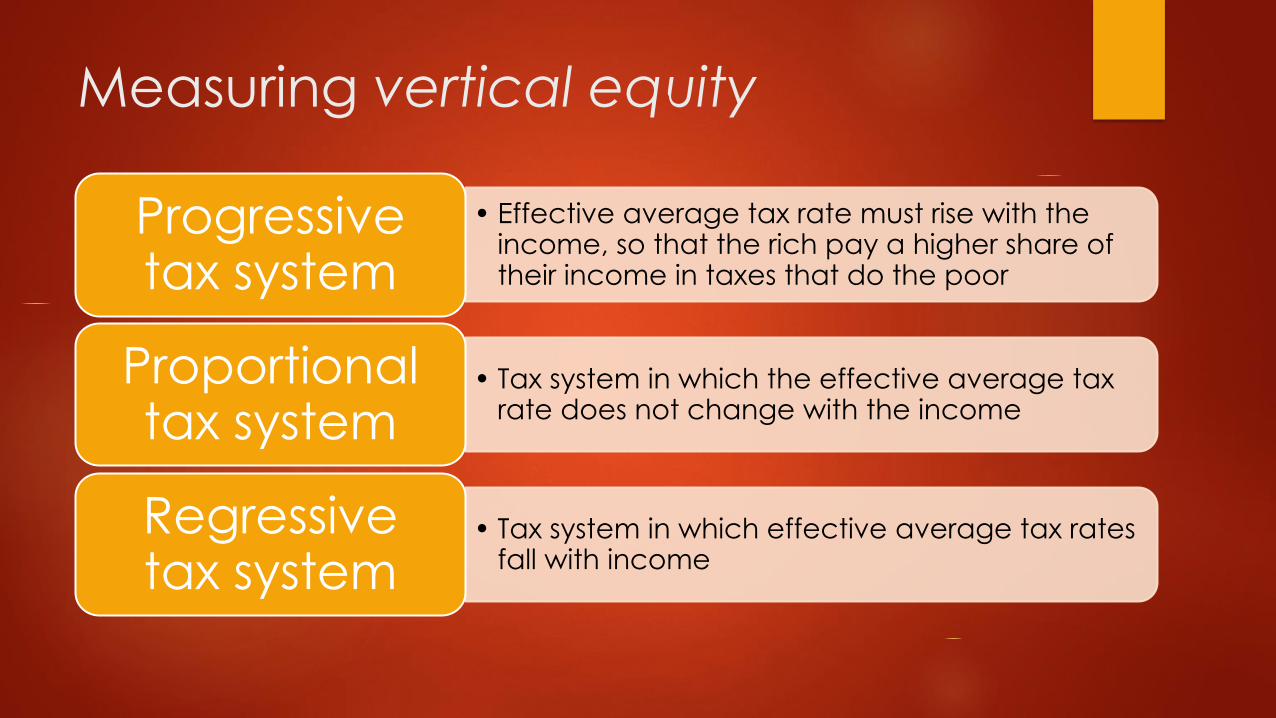

Measuring vertical equity

• Effective average tax rate must rise with the income, so that the rich pay a higher share of their income in taxes that do the poor

Progressive tax system

• Tax system in which the effective average tax rate does not change with the income

Proportional tax system

• Tax system in which effective average tax rates fall with income

Regressive tax system

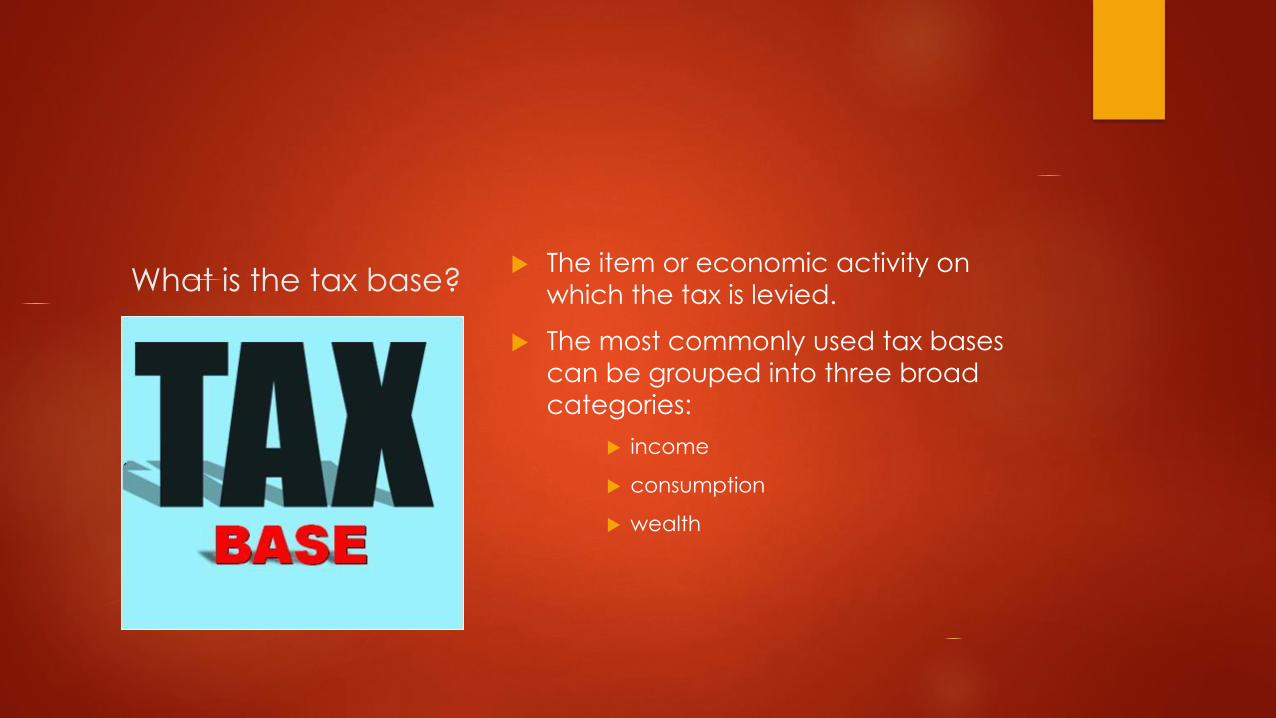

What is the tax base? The item or economic activity on

which the tax is levied.

The most commonly used tax bases

can be grouped into three broad

categories:

income

consumption

wealth

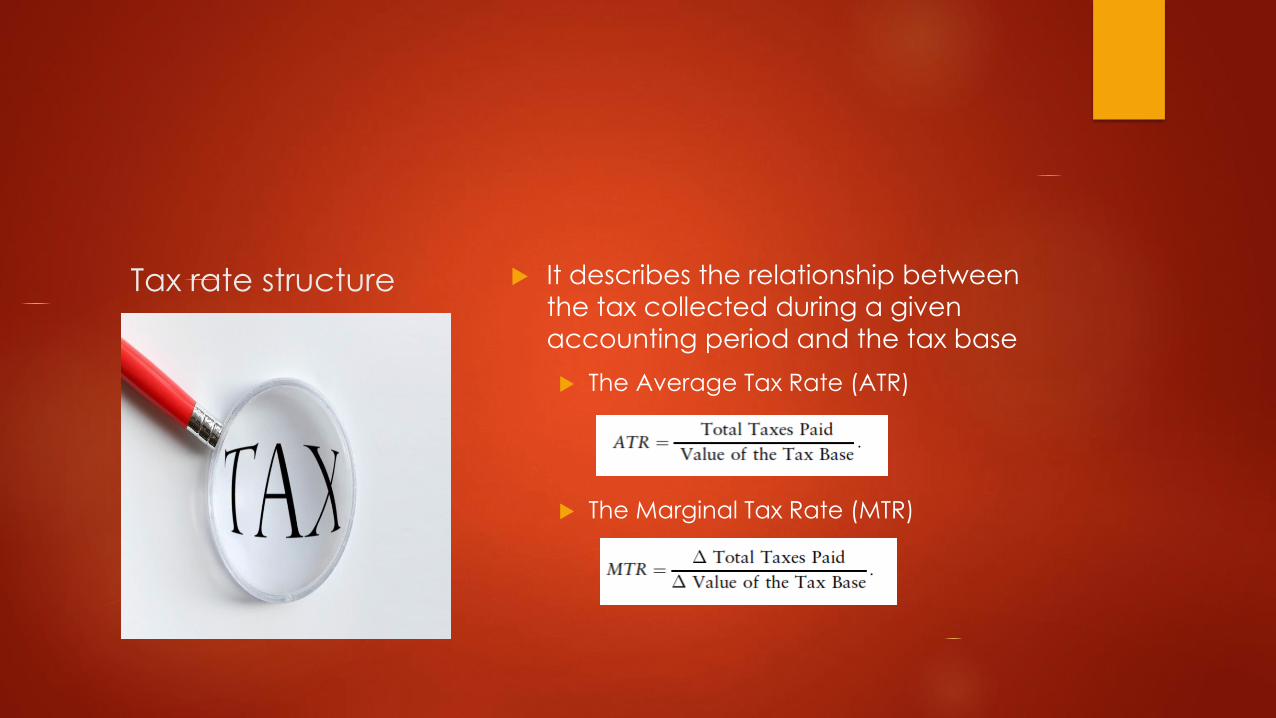

Tax rate structure It describes the relationship between

the tax collected during a given

accounting period and the tax base

The Average Tax Rate (ATR)

The Marginal Tax Rate (MTR)

Exercise Proportional tax rate structure (flat tax

rate)

Progressive tax rate structure

Tax bracket

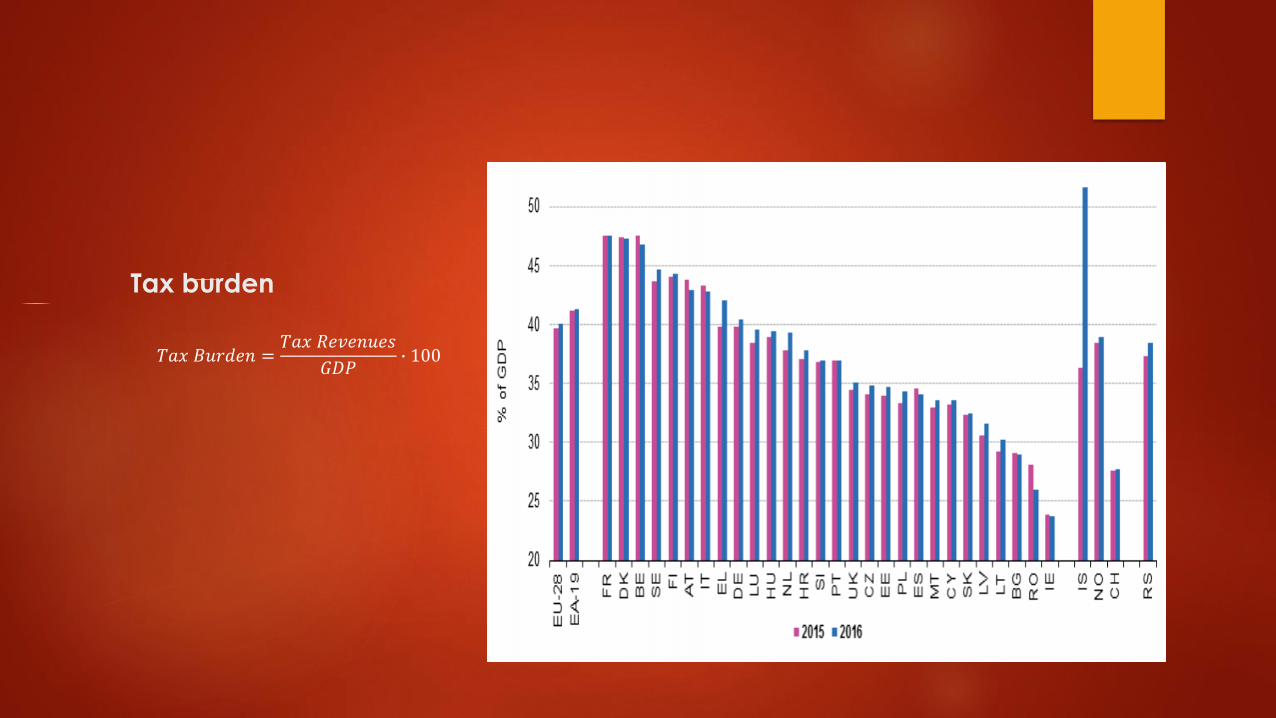

Tax burden

𝑇𝑎𝑥 𝐵𝑢𝑟𝑑𝑒𝑛 =𝑇𝑎𝑥 𝑅𝑒𝑣𝑒𝑛𝑢𝑒𝑠

𝐺𝐷𝑃∙ 100

The benefit principle The means of financing government-

supplied goods and services should

be linked to the benefits that citizens

receive from government

Fees and charges are ideal forms of

government finance

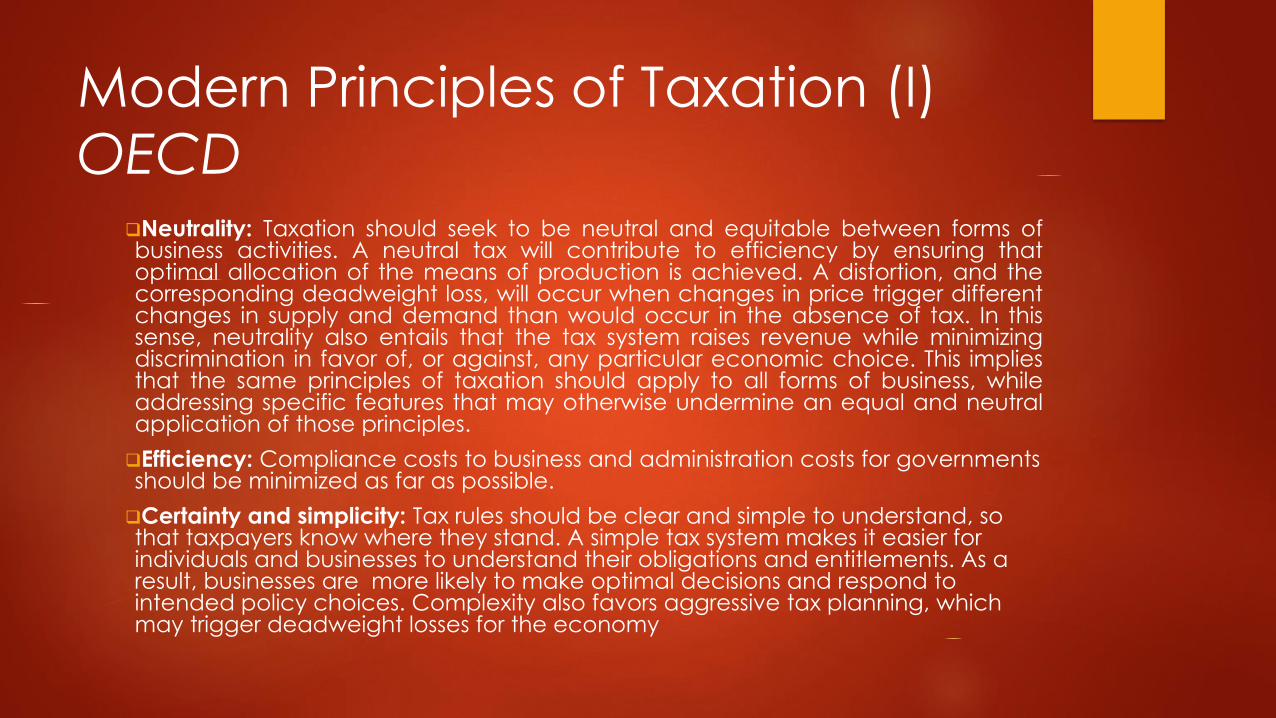

Modern Principles of Taxation (I)

OECDNeutrality: Taxation should seek to be neutral and equitable between forms ofbusiness activities. A neutral tax will contribute to efficiency by ensuring thatoptimal allocation of the means of production is achieved. A distortion, and thecorresponding deadweight loss, will occur when changes in price trigger differentchanges in supply and demand than would occur in the absence of tax. In thissense, neutrality also entails that the tax system raises revenue while minimizingdiscrimination in favor of, or against, any particular economic choice. This impliesthat the same principles of taxation should apply to all forms of business, whileaddressing specific features that may otherwise undermine an equal and neutralapplication of those principles.

Efficiency: Compliance costs to business and administration costs for governments should be minimized as far as possible.

Certainty and simplicity: Tax rules should be clear and simple to understand, so that taxpayers know where they stand. A simple tax system makes it easier for individuals and businesses to understand their obligations and entitlements. As a result, businesses are more likely to make optimal decisions and respond to intended policy choices. Complexity also favors aggressive tax planning, which may trigger deadweight losses for the economy

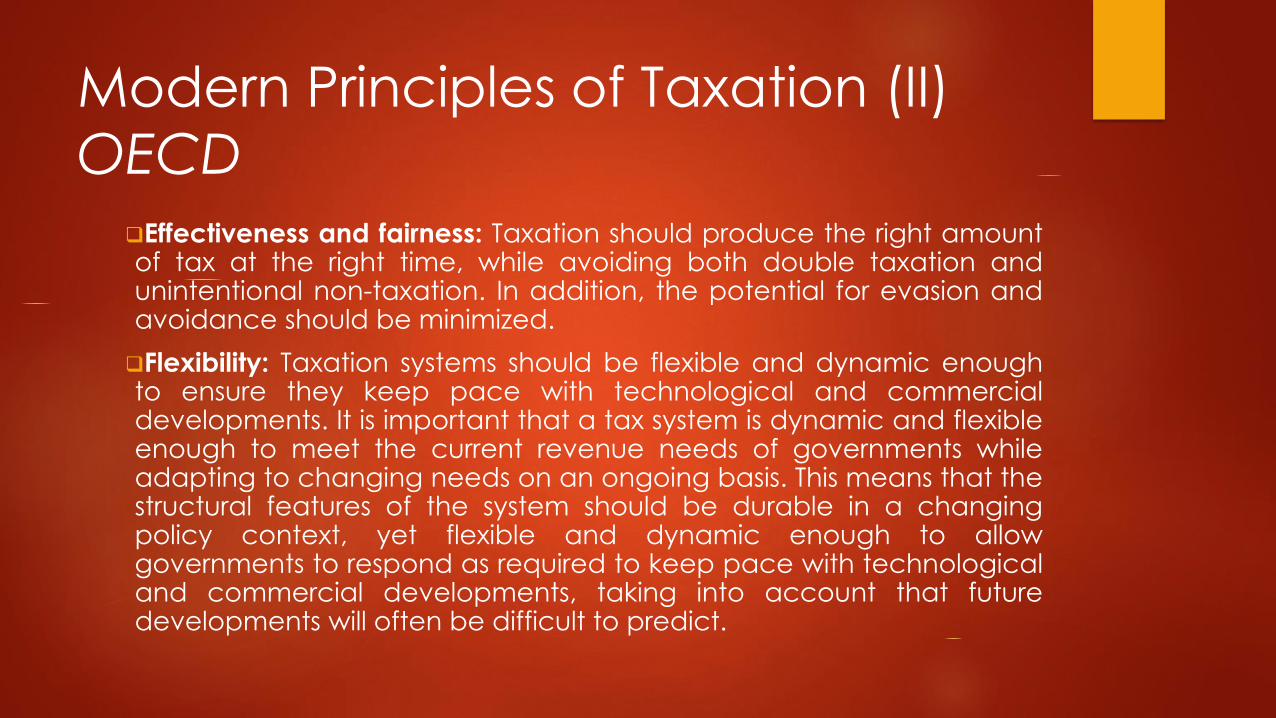

Modern Principles of Taxation (II)

OECD

Effectiveness and fairness: Taxation should produce the right amountof tax at the right time, while avoiding both double taxation andunintentional non-taxation. In addition, the potential for evasion andavoidance should be minimized.

Flexibility: Taxation systems should be flexible and dynamic enoughto ensure they keep pace with technological and commercialdevelopments. It is important that a tax system is dynamic and flexibleenough to meet the current revenue needs of governments whileadapting to changing needs on an ongoing basis. This means that thestructural features of the system should be durable in a changingpolicy context, yet flexible and dynamic enough to allowgovernments to respond as required to keep pace with technologicaland commercial developments, taking into account that futuredevelopments will often be difficult to predict.

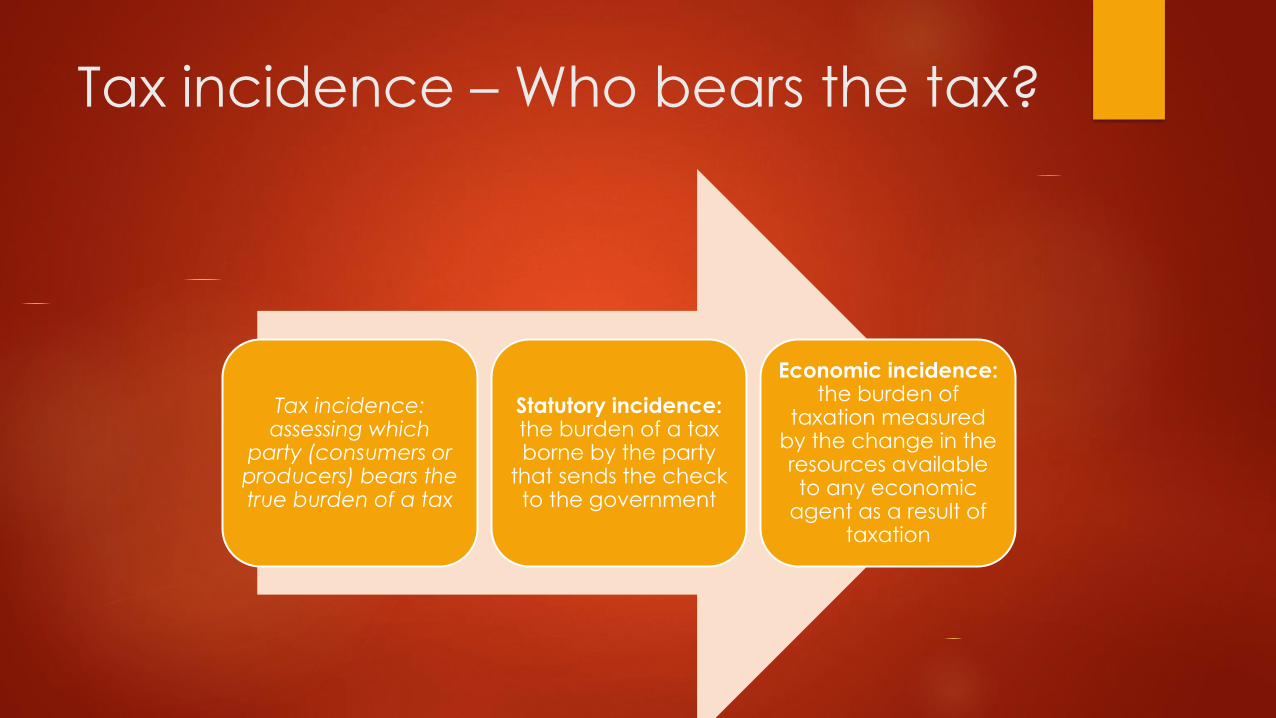

Tax incidence – Who bears the tax?

Tax incidence: assessing which

party (consumers or producers) bears the true burden of a tax

Statutory incidence: the burden of a tax borne by the party

that sends the check to the government

Economic incidence: the burden of

taxation measured by the change in the resources available to any economic

agent as a result of taxation

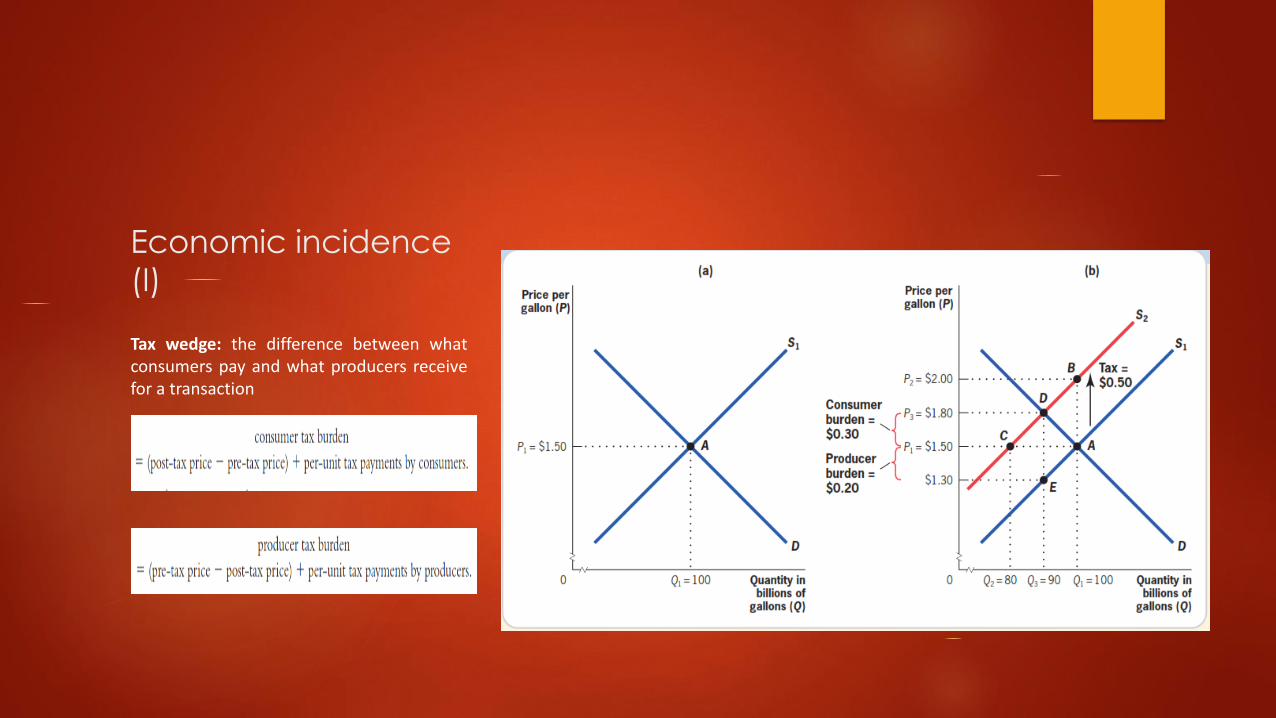

Economic incidence

(I)

Tax wedge: the difference between whatconsumers pay and what producers receivefor a transaction

Economic incidence

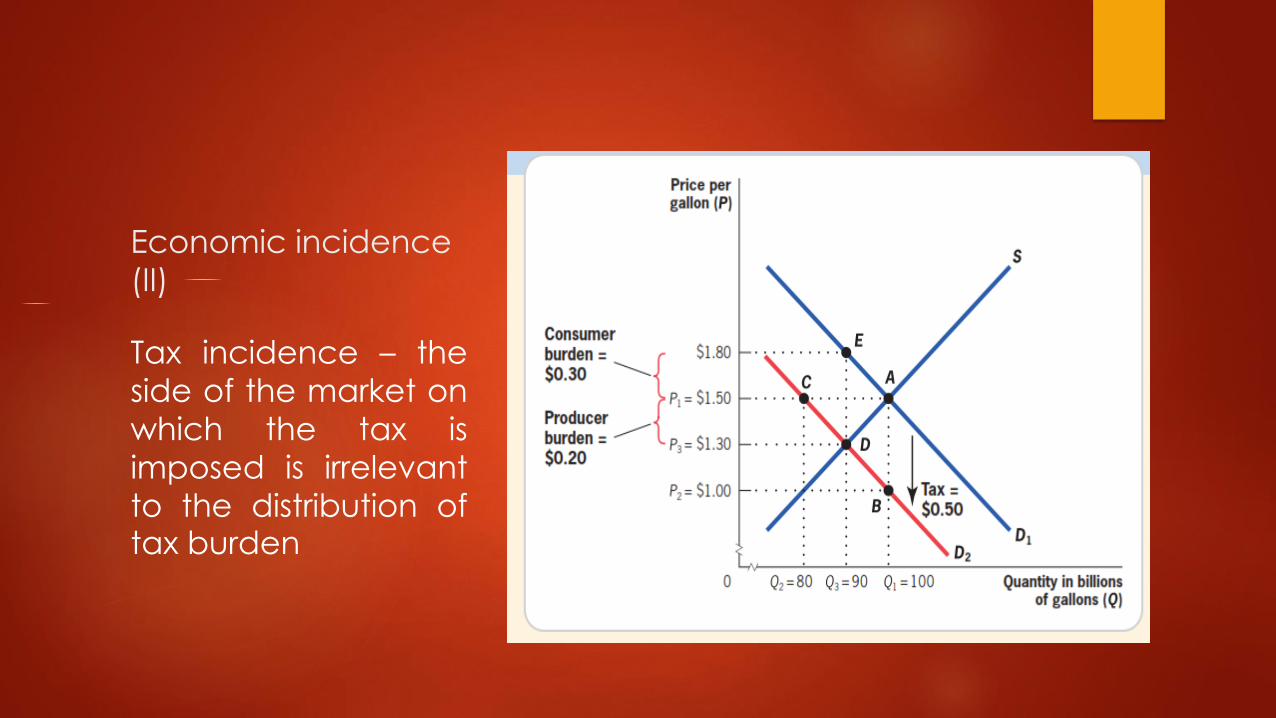

(II)

Tax incidence – the

side of the market on

which the tax is

imposed is irrelevant

to the distribution oftax burden

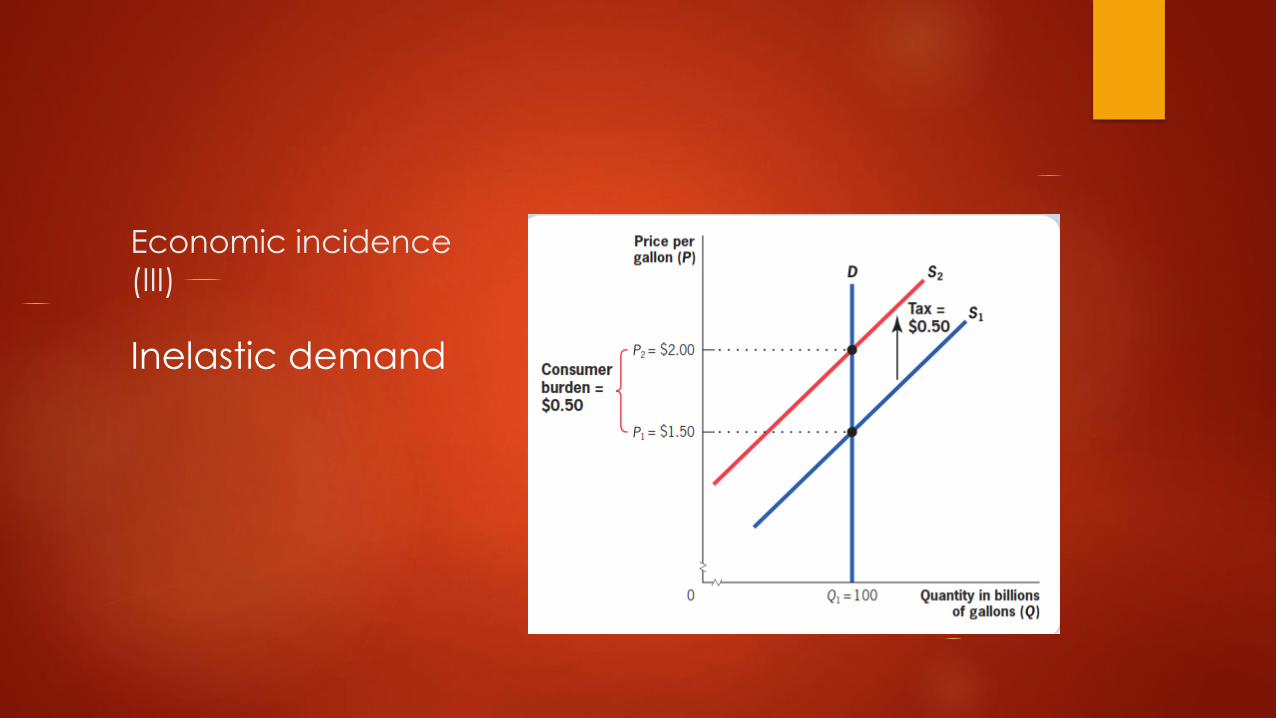

Economic incidence

(III)

Inelastic demand

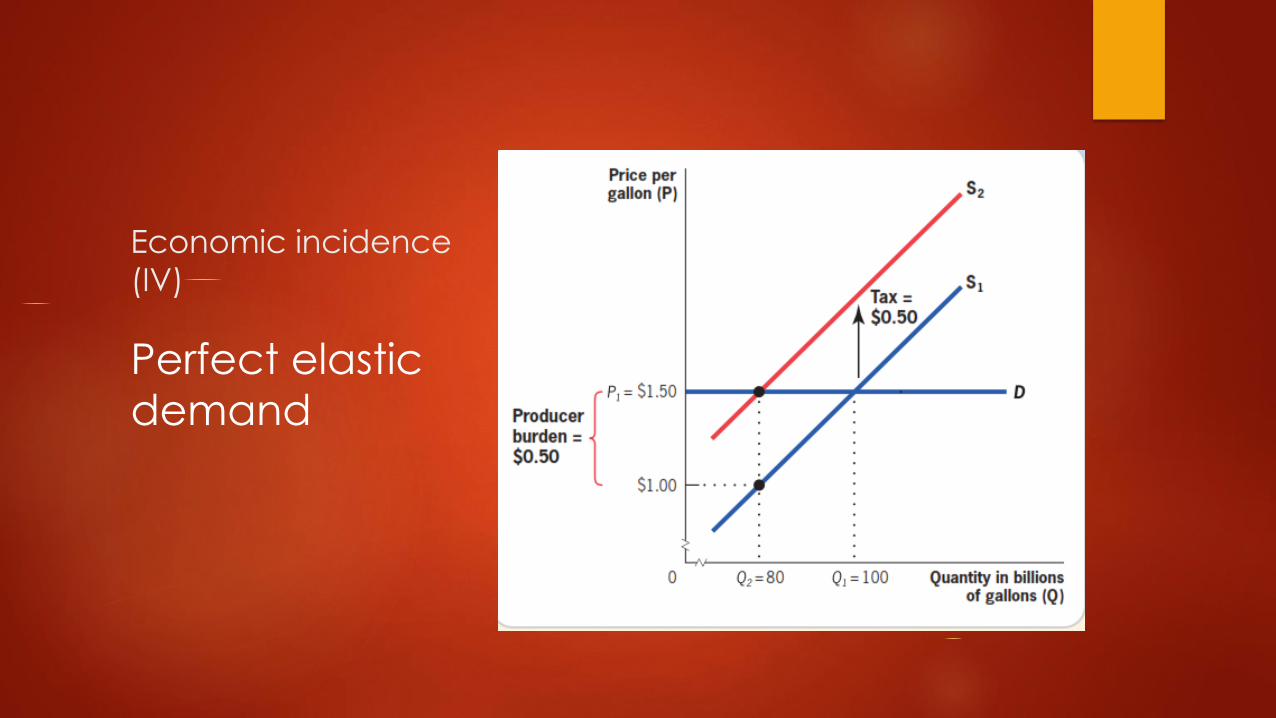

Economic incidence

(IV)

Perfect elastic

demand

Tax incidence - summary

The statutory burden of a tax does notdescribe who really bears the tax

The side of the market on which the tax isimposed is irrelevant to the distribution oftax burden

Parties with inelastic supply or demandbear taxes; parties with elastic supply ordemand avoid them

online.ase.ro PROFESSOR’S Q

Related Documents