PRESENTATION 10: REPORT OUTCOMES OF FINANCIAL PLANS

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

PRESENTATION 10: REPORT OUTCOMES OF FINANCIAL PLANS

PRESENTATION 10 OUTLINE

The following areas are covered in this presentation:

• Records of Financial Performance are Maintained

• Journals and Ledgers

• Balance Sheet

• Profit and Loss Statement

• Cash Flow Statement

RECORDS OF FINANCIAL PERFORMANCE ARE MAINTAINED

• To enable correct, current and accurate reporting of financial

performance of the budget and associated plans it is crucial that

all records of the company are maintained for both internal use

and external auditing.

• Every financial or accounting or personnel transaction within the

company must be recorded and utilised both for the above

purposes as well as for legal reporting such as taxation returns

and reports, workers compensation insurance and employee

superannuation guarantee reporting.

RECORDS OF FINANCIAL PERFORMANCE ARE MAINTAINED

• The day-to-day paperwork of a company should be collected and

collated within a suitable system. Day-to-day paperwork can

include:

− Data detailing expenditure

− Payrolls

− Income from sales

− Overheads

− Purchases

− Deposits

RECORDS OF FINANCIAL PERFORMANCE ARE MAINTAINED

• The quality of the data and the maintenance of records is crucial if

accurate reports are to be produced. The use of the Chart of

Accounts is a crucial tool to correctly classify every transaction

both in and out of the company.

• Typically, any of the following are examples of the type of

documents and records that will be used:

− Bank statements

− Payroll records

− Tax records

− Purchase orders and associated delivery dockets

RECORDS OF FINANCIAL PERFORMANCE ARE MAINTAINED

• Other records would include:

− Petty cash vouchers

− Credit card statements (a common form of creditor payment

and one off expenditure these days)

− Sales invoices

− Contracts (useful for predicting with some accuracy future

income)

− Job sheets

• One thing to remember when recording important information is

rubbish in equals rubbish out – an old accounting saying that

is apt when recording accounting information.

JOURNALS AND LEDGERS

A journal is used by a business to enter their day to day transactions.

Separate journals are kept for recording the different groups of

transactions:

• Sales journal

• Sales returns journal

• Purchases journal

• Purchase returns journal

• Cash receipts journal

• Cash payments journal

• General journal

JOURNALS AND LEDGERS

• This enables like information to be summarised before being

entered into the ledgers.

• A ledger keeps all the information about the accounts of the

business. The information from the journals is summarised and

entered into the ledger on a daily basis following the double entry

rule. Electronic Ledger

Paper Ledger

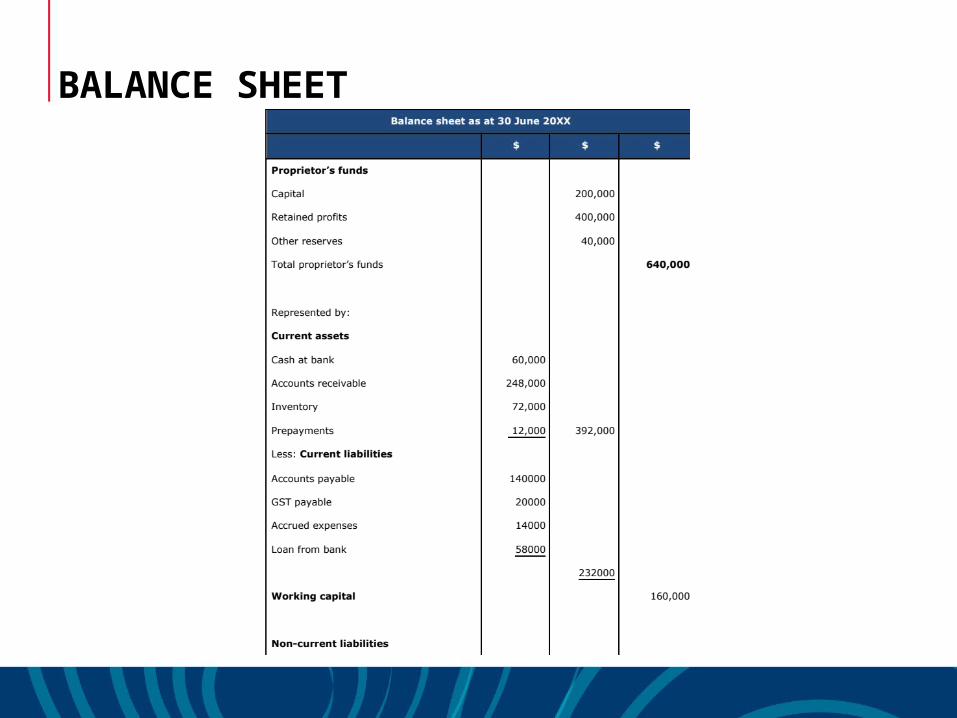

BALANCE SHEET

• A balance sheet is a financial statement regarding the financial

position of the business at a defined point in time, listing assets,

liabilities and owner’s equity of a business. It details the balance

of income and expenditure over the preceding period.

BALANCE SHEET

PROFIT AND LOSS STATEMENT

• Also known as income statements, detail the movement of sales

and expenses

• Assesses the financial position of the company and summarises

the income, costs and expenses incurred by the organisation over

a specific timeframe. They do not record cash flows.

• A financial report used extensively in financial planning and

budgeting phases of any business. It is important to understand

that the statement provides a summary of income, costs and

expenses incurred during a specific timeframe. It also shows the

profitability of the business during a specific time

Sales – Expense = Profit

PROFIT AND LOSS STATEMENT

Income statements work with the following kinds of profit:Gross ProfitThe difference between revenue and the cost of making a product

or providing a service (before deducting overheads, payroll,

taxation and interest payments) Gross profit = Sales minus

Cost of goods sold Or

Gross profit = Total revenue minus variable costs

Operating ProfitProfit earned from a firm's

normal core business operations, also known as earnings before

interest and tax (EBIT). This value does not include -any

profit earned from firm's investments (e.g. earnings from

other firms in which the company has partial interest), or the effects of interest and taxes.

PROFIT AND LOSS STATEMENTNet ProfitAlso referred to as bottom line,

net income or net earnings. Represents the number of sales dollars left after these amounts

have been deducted from a company's total revenue.

The formula for net profit is: Net Profit = TR – COGS –

operating expenses – other financial costs (i.e. interest

and tax)

Total Revenue (TW)Total income the business

receives from sales of goods/services.

Total revenue = price multiplied by quantity

Total Revenue (like total costs) increases as more products and services are produced and sold.

PROFIT AND LOSS STATEMENT

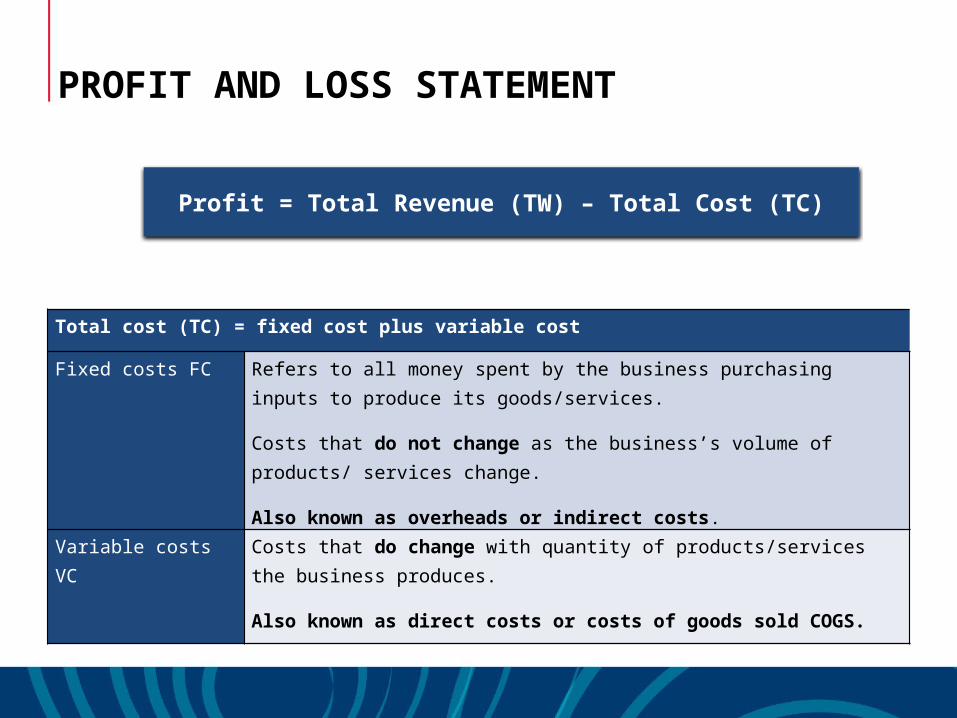

Profit = Total Revenue (TW) – Total Cost (TC)

Total cost (TC) = fixed cost plus variable cost

Fixed costs FC Refers to all money spent by the business purchasing inputs to produce its goods/services.

Costs that do not change as the business’s volume of products/ services change.

Also known as overheads or indirect costs.

Variable costs VC

Costs that do change with quantity of products/services the business produces.

Also known as direct costs or costs of goods sold COGS.

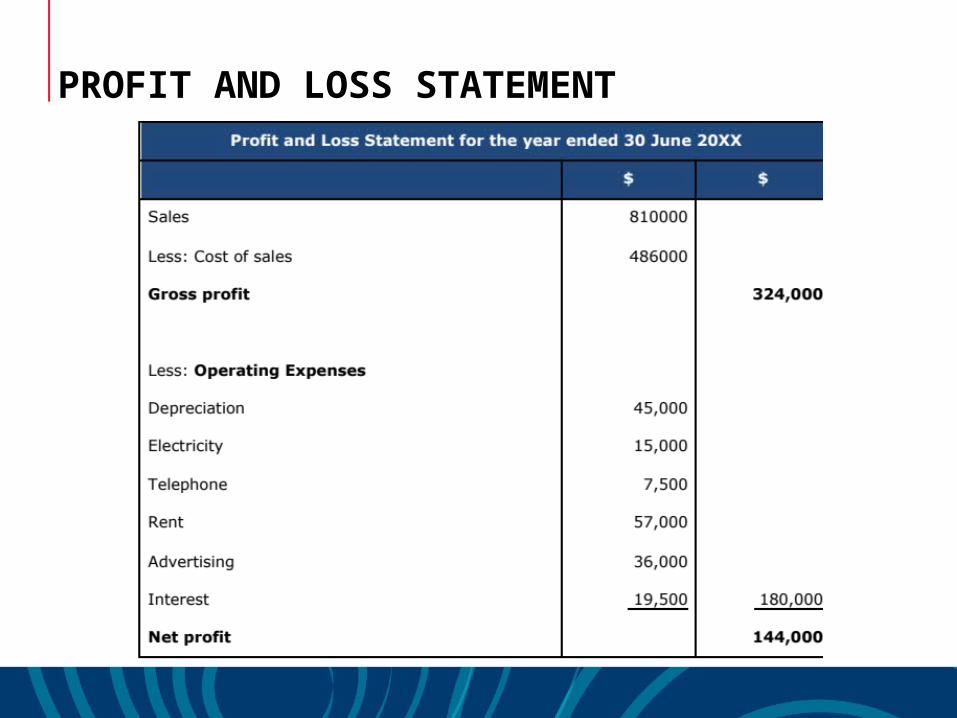

PROFIT AND LOSS STATEMENT

CASH FLOW STATEMENT

• Profit and cash are not the same thing

• Neither past net profit nor future budgeted net profits tell us about

cash flow, because net profit:

− Includes non-cash expenses such as depreciation (remember

the term EBITDA – earnings before interest, tax and

depreciation)

− Does not take into account when money is flowing in and out

− Excludes some payments like loan repayments and purchases

of new equipment (these are reported on the balance sheet –

to be explained later)

(Source: Department of Business Industry and Trade, Government of South Australia)

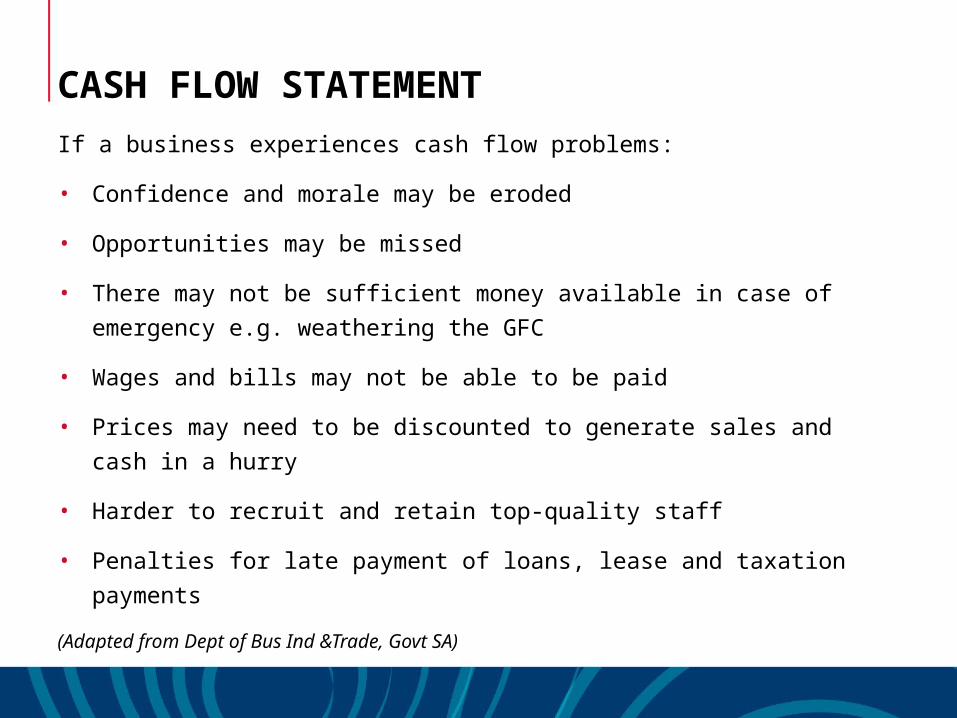

CASH FLOW STATEMENT

If a business experiences cash flow problems:

• Confidence and morale may be eroded

• Opportunities may be missed

• There may not be sufficient money available in case of emergency

e.g. weathering the GFC

• Wages and bills may not be able to be paid

• Prices may need to be discounted to generate sales and cash in a

hurry

• Harder to recruit and retain top-quality staff

• Penalties for late payment of loans, lease and taxation payments

(Adapted from Dept of Bus Ind &Trade, Govt SA)

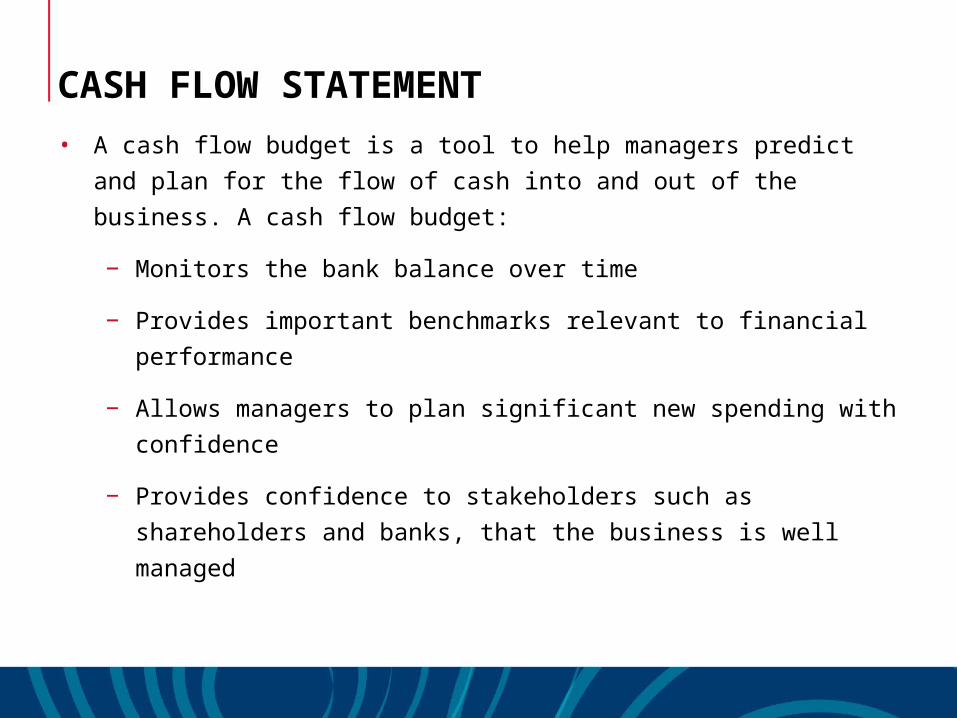

CASH FLOW STATEMENT

• A cash flow budget is a tool to help managers predict and plan for

the flow of cash into and out of the business. A cash flow budget:

− Monitors the bank balance over time

− Provides important benchmarks relevant to financial

performance

− Allows managers to plan significant new spending with

confidence

− Provides confidence to stakeholders such as shareholders and

banks, that the business is well managed

CASH FLOW STATEMENT

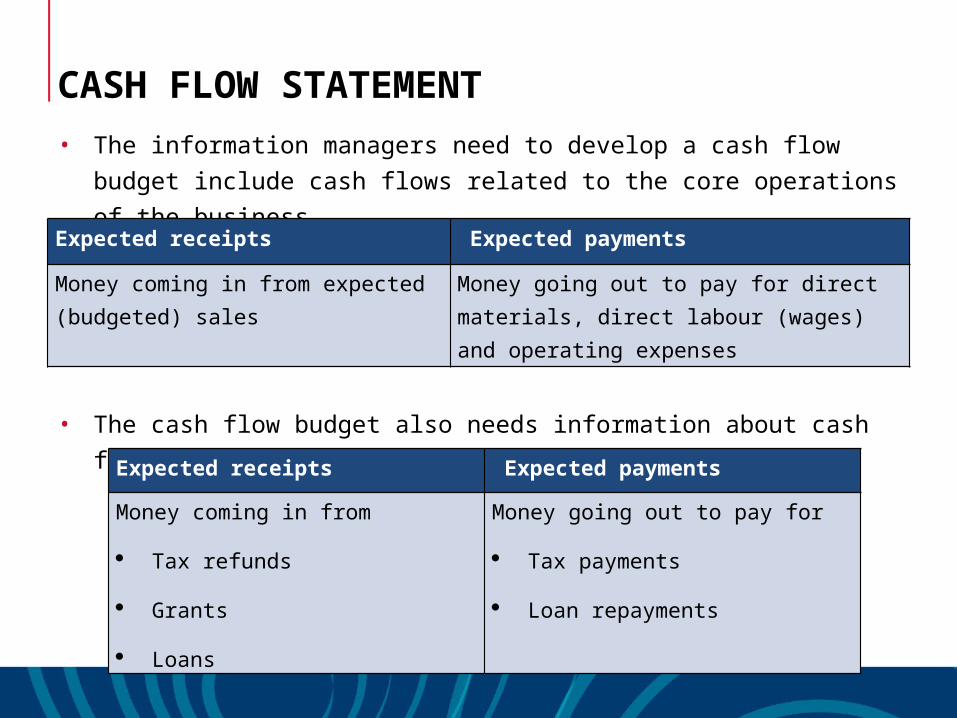

• The information managers need to develop a cash flow budget

include cash flows related to the core operations of the business

• The cash flow budget also needs information about cash flows

from non-core business sources.

Expected receipts Expected payments

Money coming in from expected (budgeted) sales

Money going out to pay for direct materials, direct labour (wages) and operating expenses

Expected receipts Expected payments

Money coming in from

Tax refunds

Grants

Loans

Money going out to pay for

Tax payments

Loan repayments

CASH FLOW STATEMENT

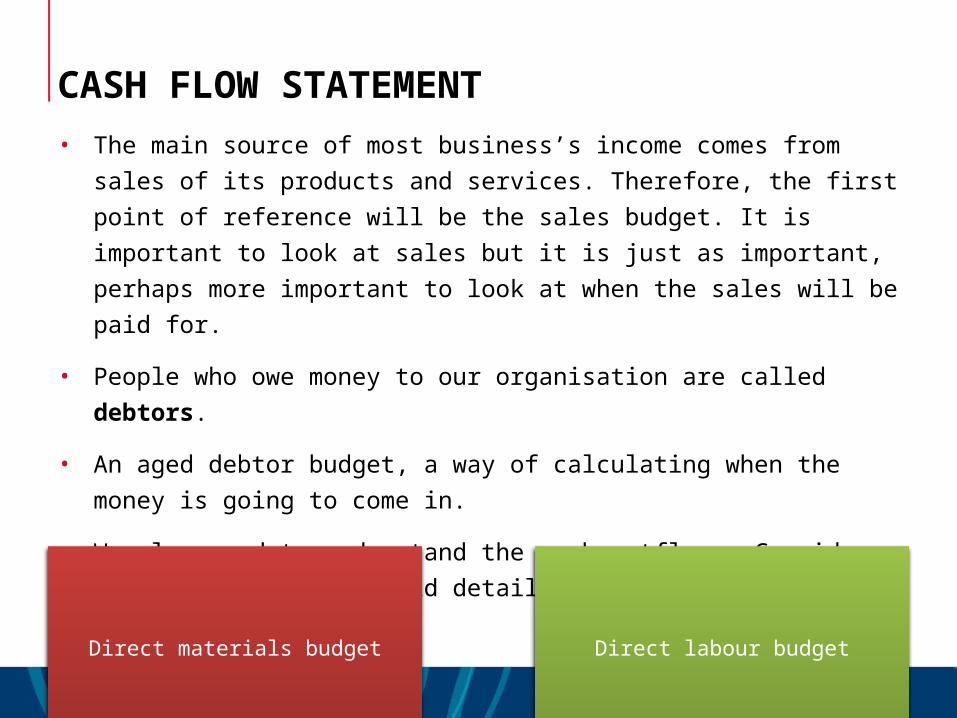

• The main source of most business’s income comes from sales of

its products and services. Therefore, the first point of reference

will be the sales budget. It is important to look at sales but it is

just as important, perhaps more important to look at when the

sales will be paid for.

• People who owe money to our organisation are called debtors.

• An aged debtor budget, a way of calculating when the money is

going to come in.

• We also need to understand the cash outflows. Consider three

budgets that would detail costs:

Direct materials budget Direct labour budget

CASH FLOW STATEMENT

• As with revenue, a monthly budget for cash outflows must be

planned.

• In order to put together the elements of the cash flow budget.

Include the following:

− Opening balance

− Cash inflows

− Cash outflow

− Closing balance

Manage cash flow

• You can’t manage a problem well unless you first see it coming,

and you won’t see a cash flow problem in advance unless you go

looking for it

CASH FLOW STATEMENT

How to improve your cash flow

Increase cash inflow by:

• Increasing the proportion of cash sales

• Send out invoices earlier

• Evaluate customers’ credit worthiness

• Establish and communicate a stricter accounts payable policy

• Chase bad debts sooner and more actively

• Offer discounts for cash or earlier payment of accounts

• Shifting excess cash into higher interest bank accounts

CASH FLOW STATEMENTReduce your costs by:

• Rationalising human resource practices by minimising overtime worked

and using more casual staff or consider using sub-contractors

• Reducing the amount of working capital (money) tied up in

unnecessarily high stock levels

• Negotiate discounts on purchases

• Buying used rather than new machinery

• Manage the rate and timing of payments by:

• Arranging to pay large annual bills in smaller, more frequent payments

(e.g. monthly premiums for insurance)

• Setting aside cash each month to meet tax bills

• Using credit cards for the of interest free periods and delayed payments

CASH FLOW STATEMENT

• Petty cash is a small (petty) amount of cash that helps onsite for

paying small amounts owed. The business determines an amount

to be held in cash on the premises. Creating a procedure to

manage the flow of these monies involves a reconciliation of the

money into and out of the petty cash fund

Simply this involves:

Reconcile the account: does the money taken equal the receipts left? If you are asked to purchase an item using petty cash you will be required to replace the cash taken with a tax

invoice to represent the money spent

An accounts payable staff member will request the invoices and a copy

of the reconciliation statement

Replace the money via a cheque from the bank account to the petty cash account. Petty cash payments are recorded in the general ledger as

expense in the general ledger, and then files the form and attached vouchers or petty cash dockets

CASH FLOW STATEMENT

• In terms of managing the disbursements from petty cash:

− Monitor the spending, only for minor business expense

− Store petty cash in a secure location

− Complete a voucher to itemise the expense, who is

responsible, when and for how much. Attach receipts to the

voucher. Knowing all this information results in clear allocation

of costs to the correct accounts

− Disburse cash – the cash taken must be counted and checked

and recorded

• Different size organisations will deal with these systems differently

depending on their own needs and systems. Some businesses

may use a credit card in lieu of cash. Regardless of the system it is

important to know how the money is being used and why.

CASH FLOW STATEMENT

Related Documents