Time Series “ “ The Art of The Art of Forecasting” Forecasting”

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Time Series

““The Art of Forecasting”The Art of Forecasting”

Time Series• An ordered sequence of values of a variable

at equally sp• Applications: The usage of time series

models is twofold: Obtain an understanding of the underlying forces and structure that produced the observed data

• Fit a model and proceed to forecasting, monitoring or even feedback and feedforward control.

• aced time intervals.

• Time Series Analysis is used for many applications such as: Economic Forecasting

• Sales Forecasting• Budgetary Analysis• Stock Market Analysis• Yield Projections• Process and Quality Control• Inventory Studies• Utility Studies• Census Analysis• and many, many more...

Time Series Components

Time Series Components

TrendTrend

Time Series Components

TrendTrend CyclicalCyclical

Time Series Components

TrendTrend

SeasonalSeasonal

CyclicalCyclical

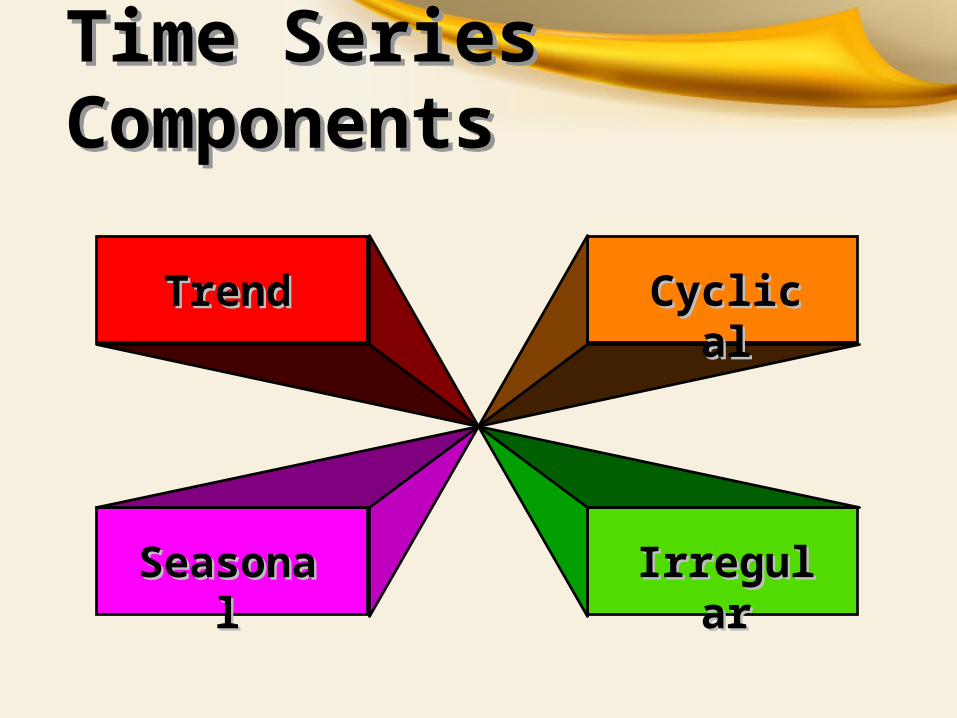

Time Series Components

TrendTrend

SeasonalSeasonal

CyclicalCyclical

IrregularIrregular

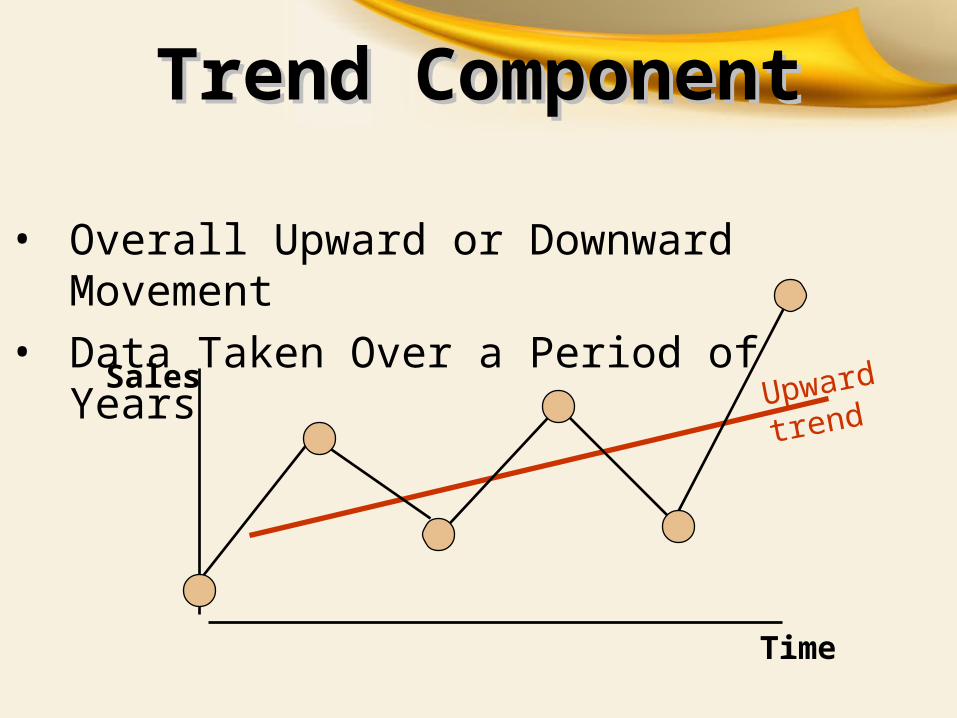

Trend ComponentTrend Component

• Overall Upward or Downward Movement• Data Taken Over a Period of Years

Sales

Time

Upward trend

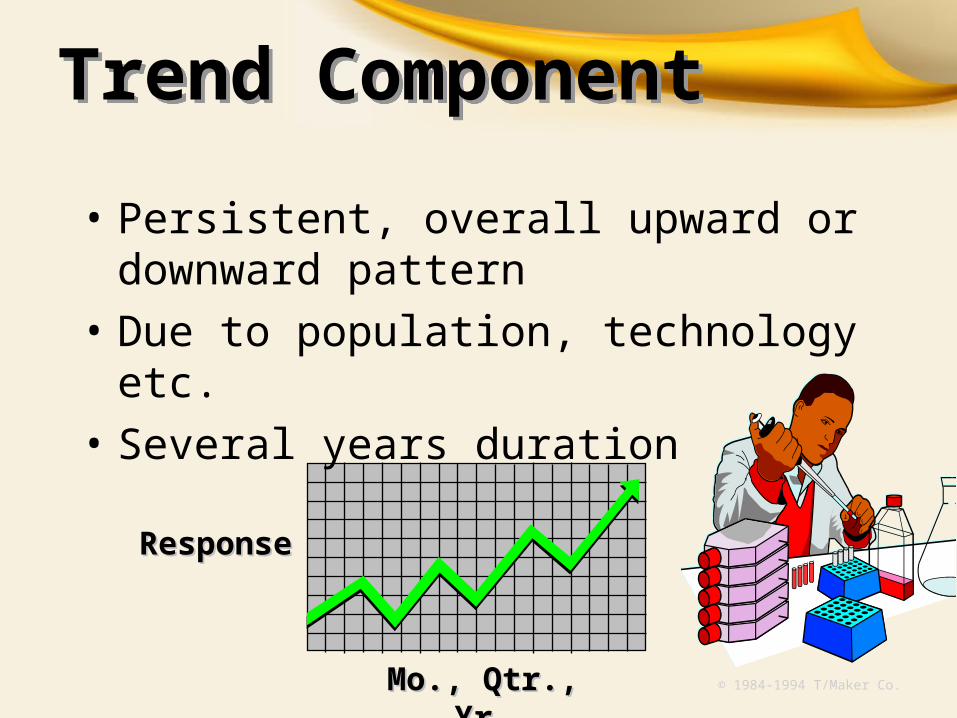

Trend Component

• Persistent, overall upward or downward pattern

• Due to population, technology etc.• Several years duration

Mo., Qtr., Yr.Mo., Qtr., Yr.

ResponseResponse

© 1984-1994 T/Maker Co.

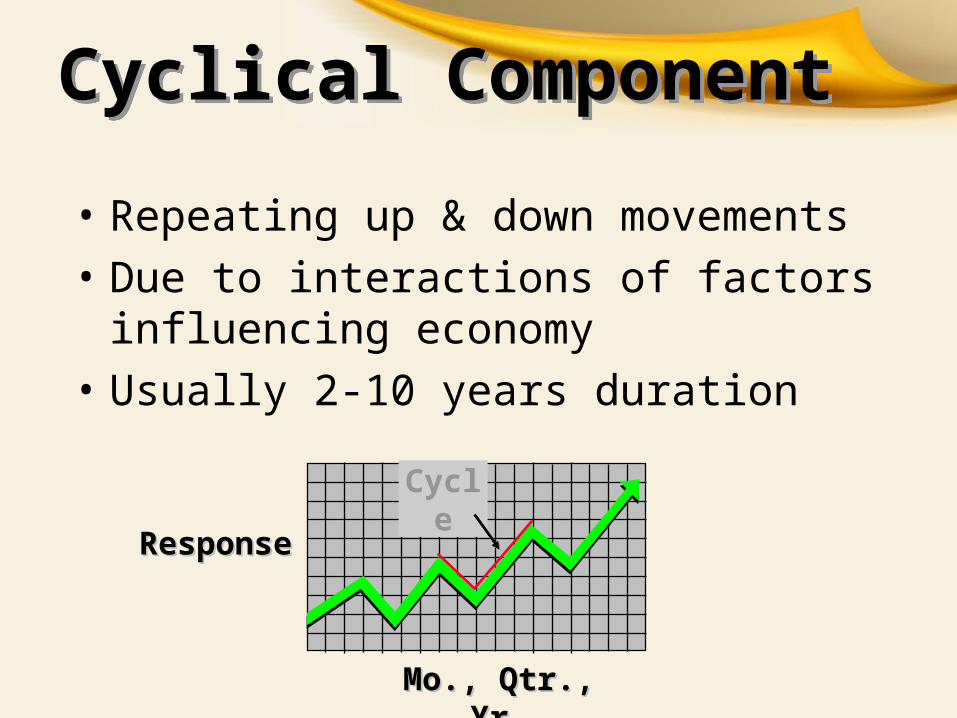

Cyclical Component

• Repeating up & down movements• Due to interactions of factors influencing

economy• Usually 2-10 years duration

Mo., Qtr., Yr.Mo., Qtr., Yr.

ResponseResponseCycle

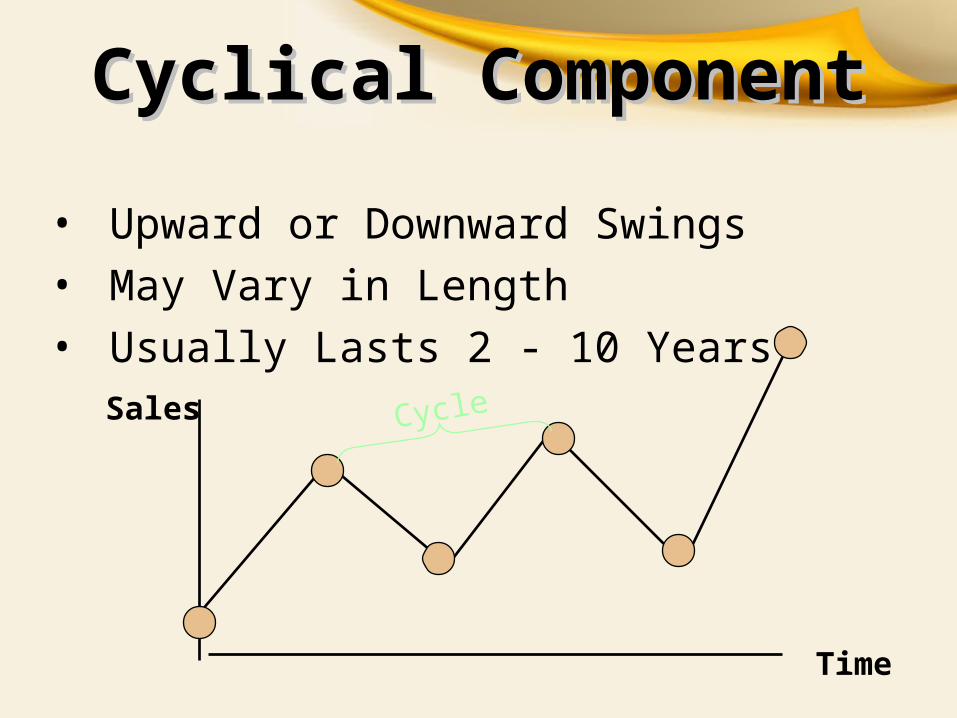

Cyclical ComponentCyclical Component

• Upward or Downward Swings• May Vary in Length• Usually Lasts 2 - 10 Years

Sales

Time

Cycle

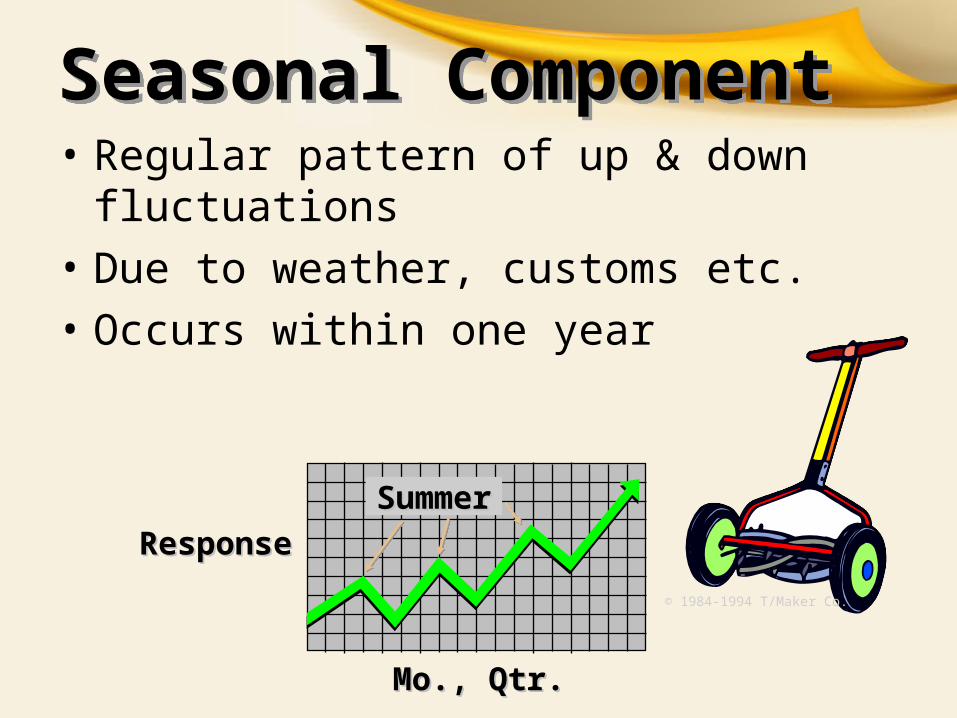

Seasonal Component• Regular pattern of up & down fluctuations• Due to weather, customs etc.• Occurs within one year

Mo., Qtr.Mo., Qtr.

ResponseResponseSummerSummer

© 1984-1994 T/Maker Co.

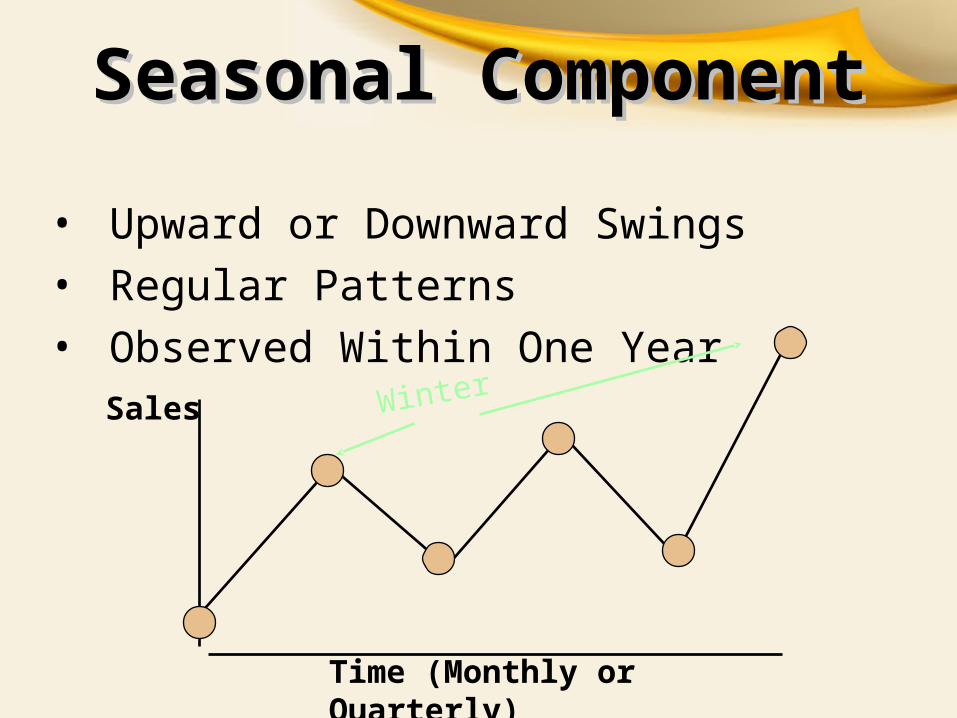

Seasonal ComponentSeasonal Component

• Upward or Downward Swings• Regular Patterns• Observed Within One Year

Sales

Time (Monthly or Quarterly)

Winter

Irregular Component• Erratic, unsystematic, ‘residual’

fluctuations• Due to random variation or unforeseen

events– Union strike– War

• Short duration & nonrepeating

© 1984-1994 T/Maker Co.

Random or Irregular Random or Irregular ComponentComponent

• Erratic, Nonsystematic, Random, ‘Residual’ Fluctuations

• Due to Random Variations of – Nature

– Accidents

• Short Duration and Non-repeating

What Is Forecasting?What Is Forecasting?• Process of predicting a

future event• Underlying basis of

all business decisions– Production– Inventory– Personnel– Facilities

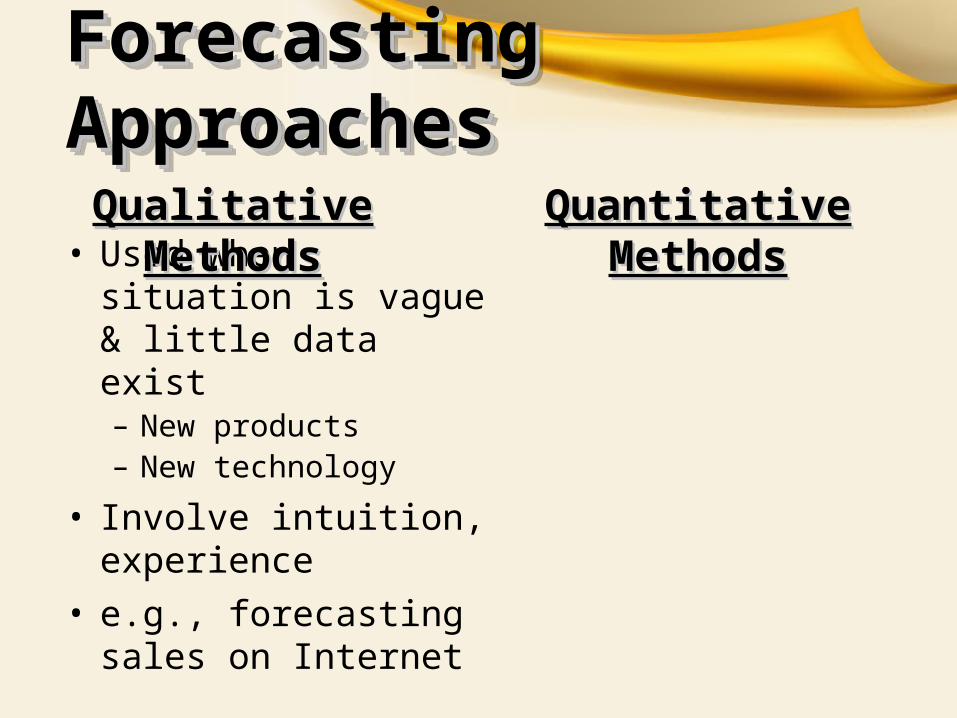

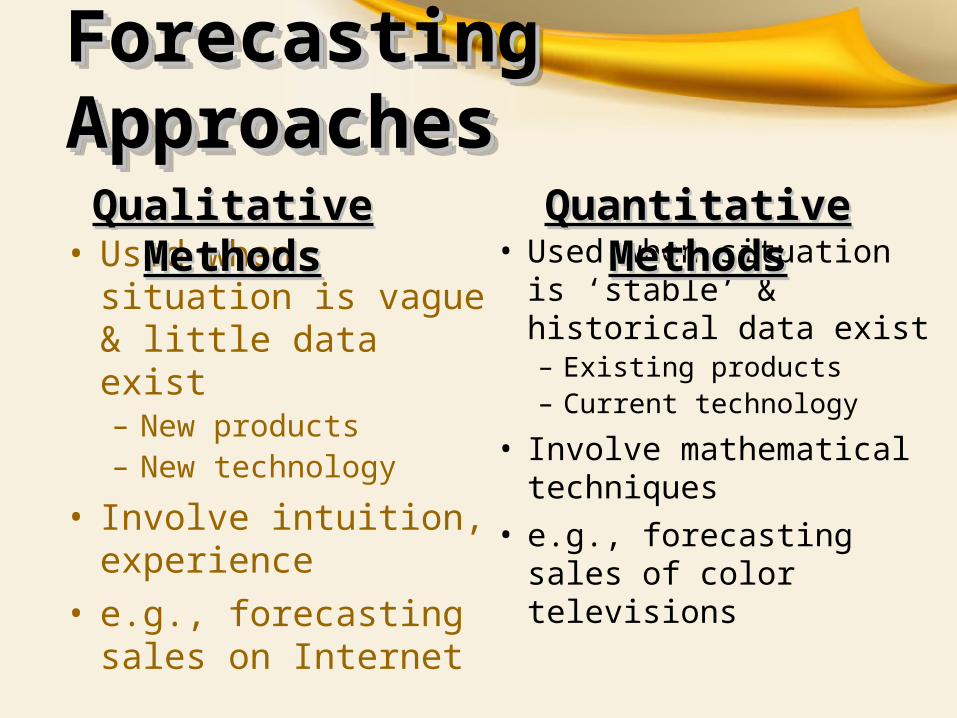

• Used when situation is vague & little data exist– New products– New technology

• Involve intuition, experience

• e.g., forecasting sales on Internet

Qualitative MethodsQualitative Methods

Forecasting ApproachesForecasting ApproachesQuantitative MethodsQuantitative Methods

• Used when situation is ‘stable’ & historical data exist– Existing products– Current technology

• Involve mathematical techniques

• e.g., forecasting sales of color televisions

Quantitative MethodsQuantitative Methods

Forecasting ApproachesForecasting Approaches

• Used when situation is vague & little data exist– New products– New technology

• Involve intuition, experience

• e.g., forecasting sales on Internet

Qualitative MethodsQualitative Methods

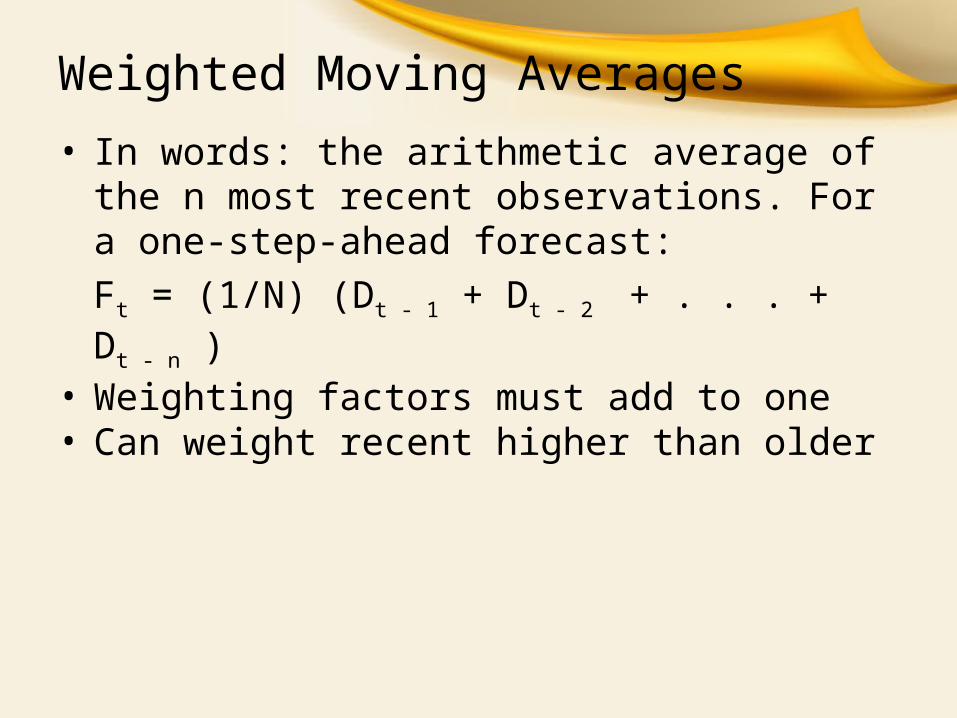

Weighted Moving Averages• In words: the arithmetic average of the n most

recent observations. For a one-step-ahead forecast: Ft = (1/N) (Dt - 1 + Dt - 2 + . . . + Dt - n )

• Weighting factors must add to one• Can weight recent higher than older

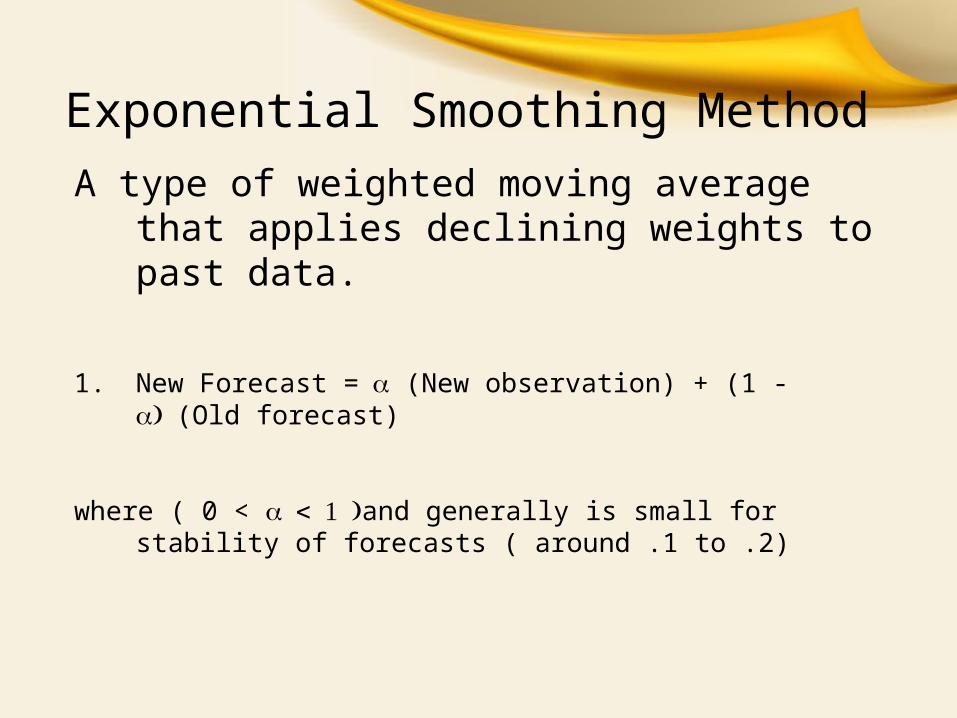

Exponential Smoothing MethodA type of weighted moving average that applies

declining weights to past data.

1. New Forecast = (New observation) + (1 - (Old forecast)

where ( 0 < and generally is small for stability of forecasts ( around .1 to .2)

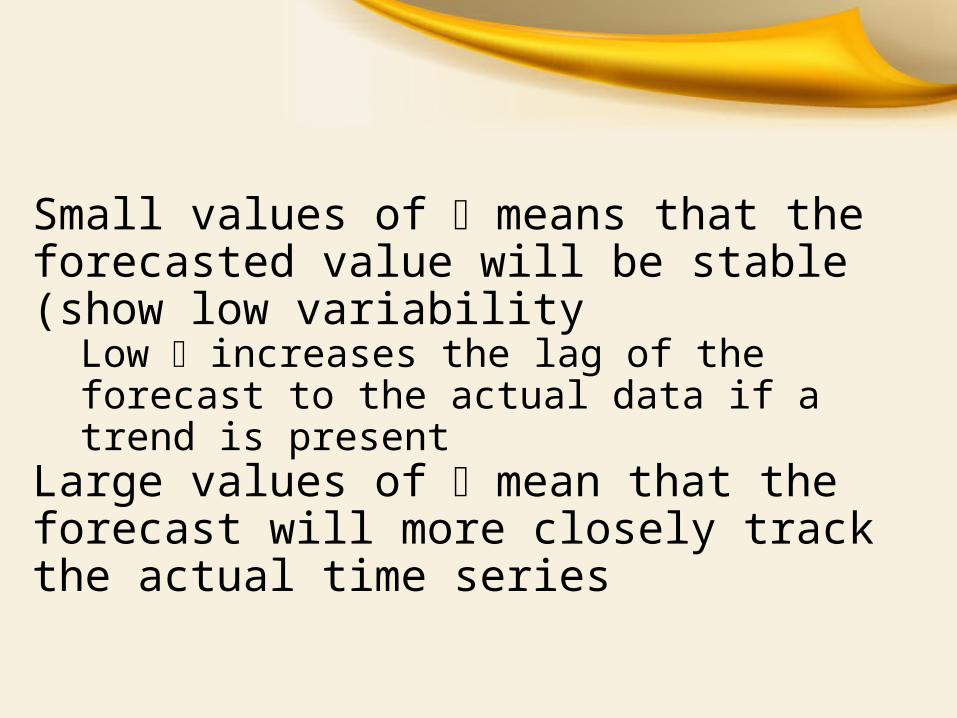

Small values of means that the forecasted value will be stable (show low variability

Low increases the lag of the forecast to the actual data if a trend is present

Large values of mean that the forecast will more closely track the actual time series

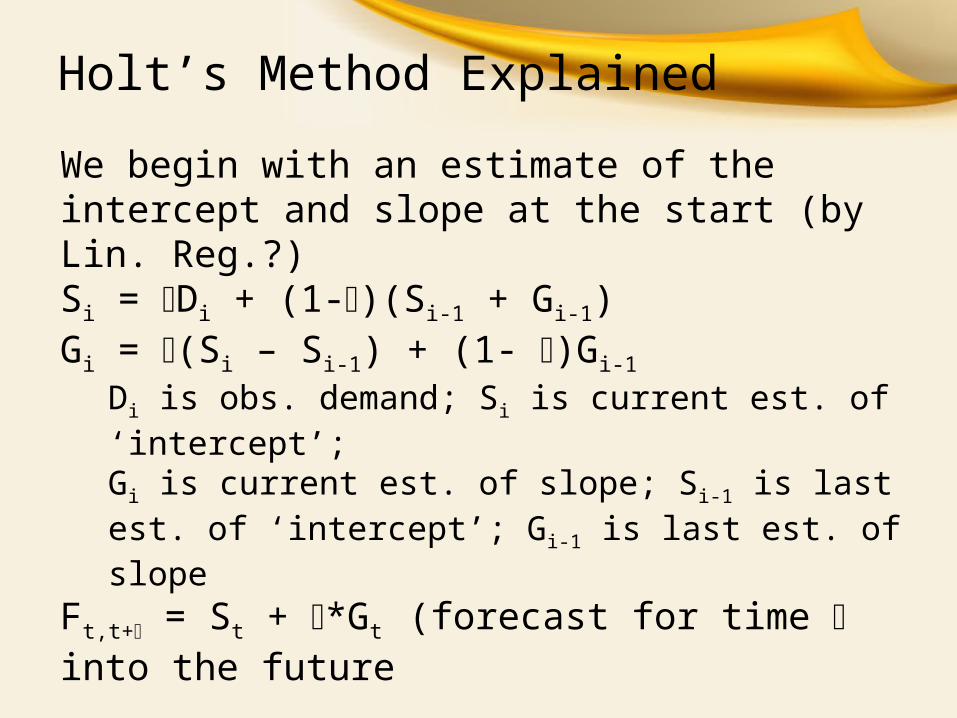

Holt’s Method Explained

We begin with an estimate of the intercept and slope at the start (by Lin. Reg.?)Si = Di + (1-)(Si-1 + Gi-1)Gi = (Si – Si-1) + (1- )Gi-1

Di is obs. demand; Si is current est. of ‘intercept’;Gi is current est. of slope; Si-1 is last est. of ‘intercept’; Gi-1 is last est. of slope

Ft,t+ = St + *Gt (forecast for time into the future

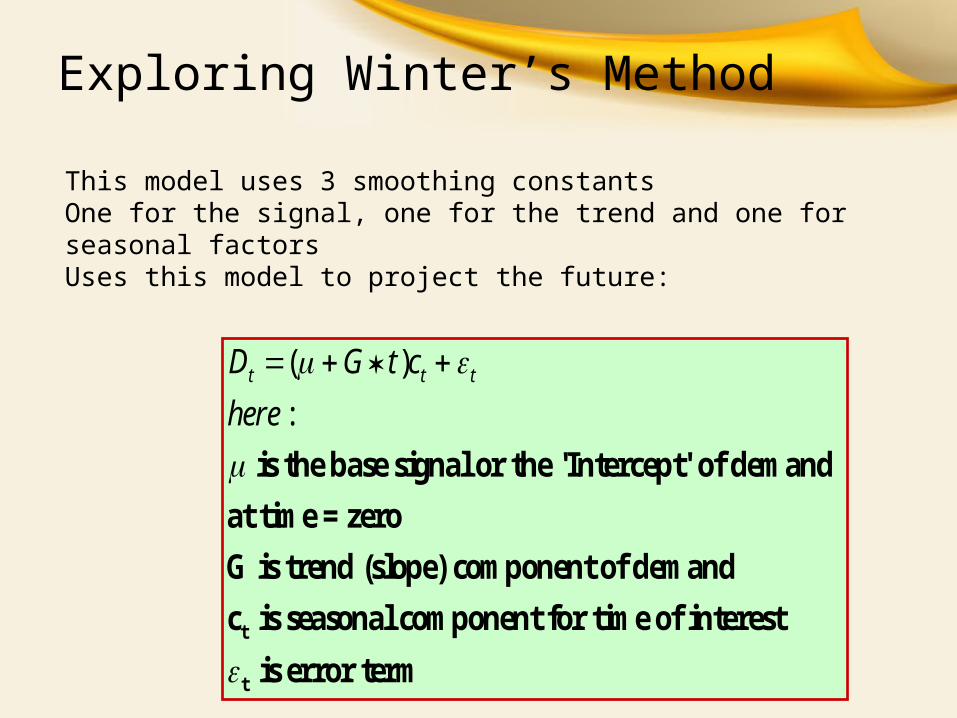

Exploring Winter’s Method

This model uses 3 smoothing constantsOne for the signal, one for the trend and one for seasonal factorsUses this model to project the future:

( ):

t

t

is the base signal or the 'Intercept' of demand at time = zeroG is trend (slope) component of demandc is seasonal component for time of interest

is error term

t t tD G t chere

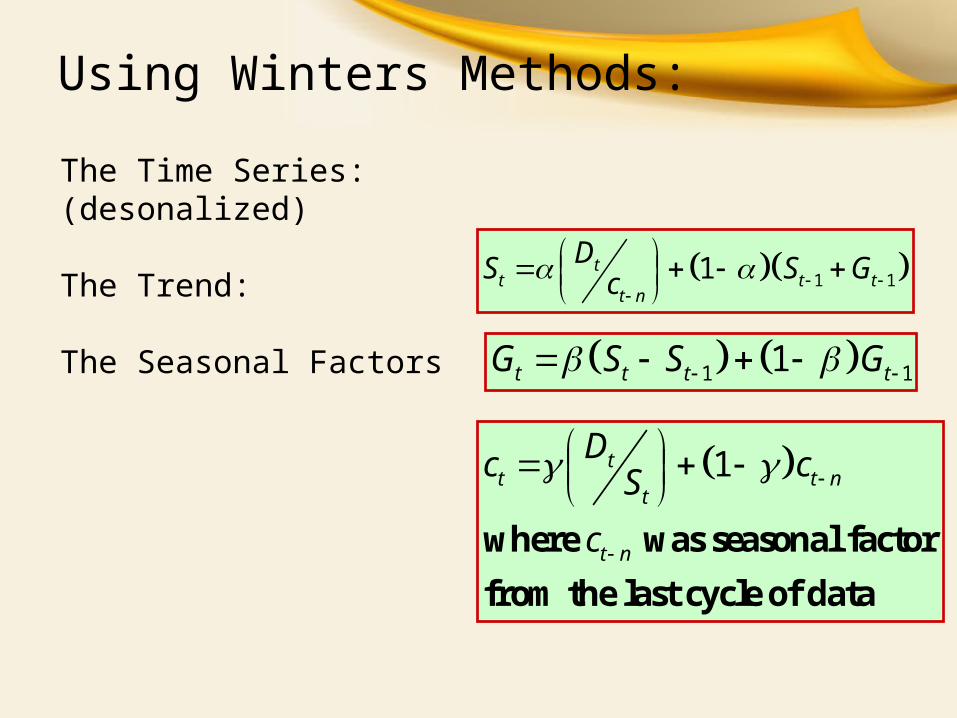

Using Winters Methods:

The Time Series:(desonalized)

The Trend:

The Seasonal Factors

1 11tt t t

t n

DS S Gc

1 11t t t tG S S G

1

where was seasonal factorfrom the last cycle of data

tt t n

t

t n

Dc cS

c

Thank you

Related Documents