The International CAPM Redux Brusa-Ramadorai-Verdelhan Discussion by Anusha Chari (UNC-Chapel Hill & NBER) November 2014

The International CAPM Redux Brusa-Ramadorai-Verdelhan Discussion by Anusha Chari (UNC-Chapel Hill & NBER) November 2014.

Dec 25, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

The International CAPM ReduxBrusa-Ramadorai-Verdelhan

Discussion by Anusha Chari

(UNC-Chapel Hill & NBER)

November 2014

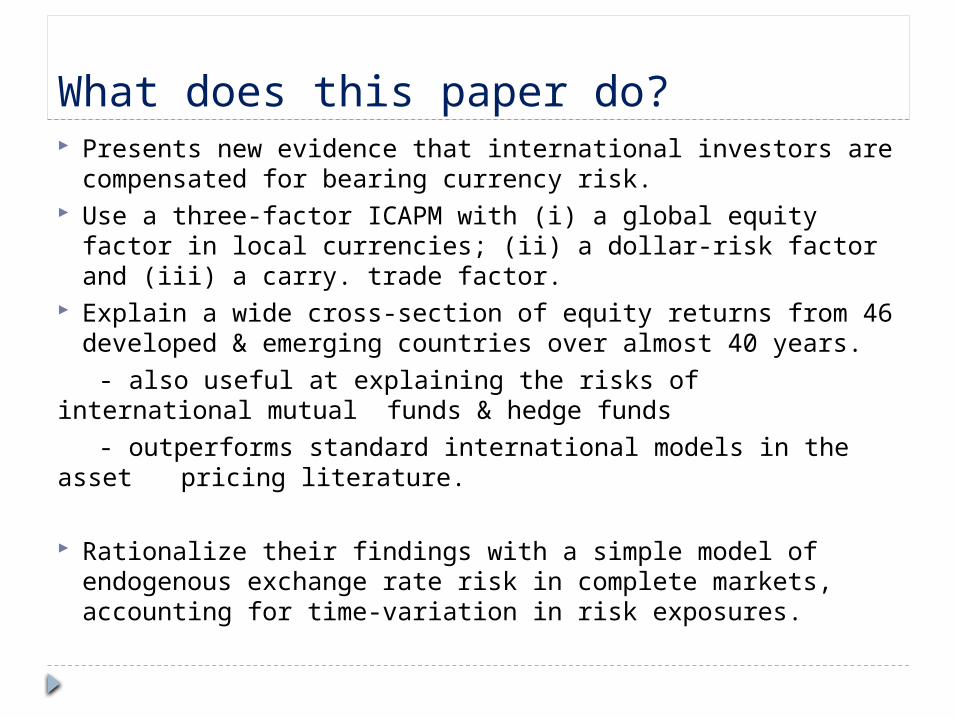

What does this paper do? Presents new evidence that international investors are

compensated for bearing currency risk. Use a three-factor ICAPM with (i) a global equity factor in

local currencies; (ii) a dollar-risk factor and (iii) a carry. trade factor.

Explain a wide cross-section of equity returns from 46 developed & emerging countries over almost 40 years.

- also useful at explaining the risks of international mutual funds & hedge funds

- outperforms standard international models in the asset pricing literature.

Rationalize their findings with a simple model of endogenous exchange rate risk in complete markets, accounting for time-variation in risk exposures.

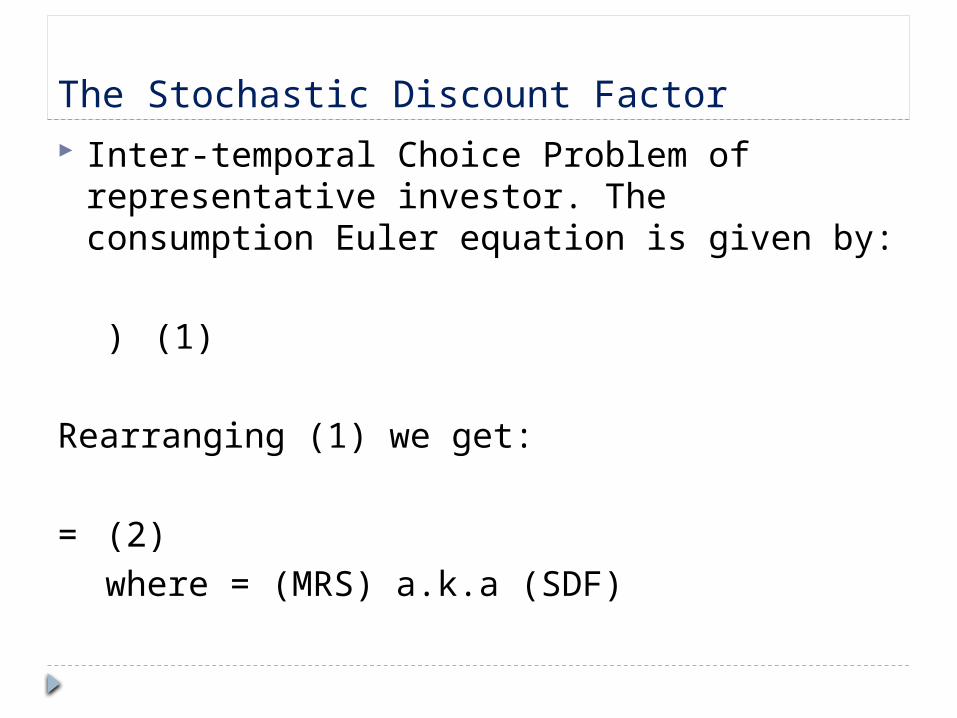

The Stochastic Discount Factor Inter-temporal Choice Problem of

representative investor. The consumption Euler equation is given by:

) (1)

Rearranging (1) we get:

= (2)where = (MRS) a.k.a (SDF)

Excess Returns Depend on Consumption Covariance Risk

Rewriting (2) as a product of expectations and rearranging we get:

and so that ())

Excess Returns Depend on Consumption Covariance Risk With power utility, joint conditional lognormality &

homoskedasticity of asset returns & consumption:

The log risk premium on any asset depends on the covariance between asset returns & consumption growth.

)

For power utility, the SDF associated with the consumption based CAPM is:

Intuitively, an asset with a high consumption covariance tends to have low returns when consumption is low or marginal utility is high. Such an asset is risky and commands a high risk premium.

Factors that enter the exponent as proxies for introduce risk premia into asset pricing equations. Therefore the only factor in the SDF in equilibrium is real consumption growth– pinned

down by the consumption Euler equation in an inter-temporal choice problem (MRS). If we cannot measure consumption or it is unobserved, we use proxies that are

correlated with real consumption growth and see how these proxy factors price the return on assets.

Any factor that goes into the exponent which proxies MRS for consumption will introduce a risk premium that enters into the pricing equation for an asset which is the expected present discounted value of CF, correlation drive + or -, hedging factor more valuable

CF is unrelated to any factor, then the discount factor is simply the risk free rate. Anything that shows up in the exponent will generate a risk premium on variables in

the CFs that are correlated with that factor. Adhoc basis say volatility is imp. Add into the exponent. The components of CFs that

are correlated with volatility will carry risk premium. Why are the CFs are earning risk premium? Because correlated with something in

exponent. Asset price is expected discounted value (SDF*CF) –depends on factors in the exponent

that are correlated with some component of CFs.

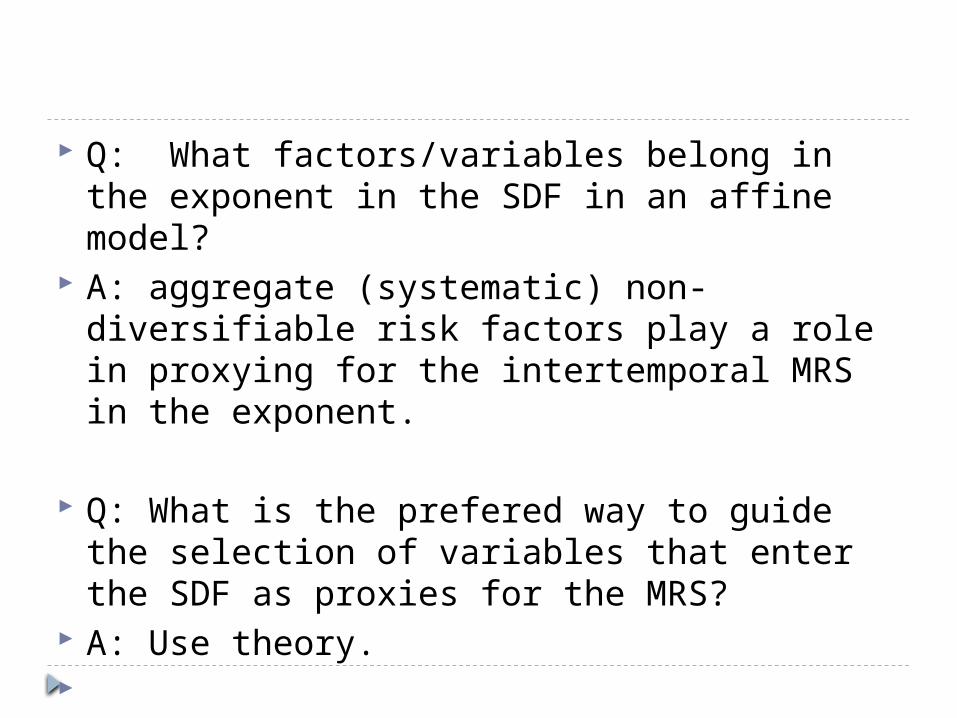

Q: What factors/variables belong in the exponent in the SDF in an affine model?

A: aggregate (systematic) non-diversifiable risk factors play a role in proxying for the intertemporal MRS in the exponent.

Q: What is the prefered way to guide the selection of variables that enter the SDF as proxies for the MRS?

A: Use theory.

One could argue that the paper is uses econometric theory to guide how variables (shocks, underlying state variables) enter the SDF, i.e., with state-dependent multiplicative factors that generate time varying risk prices.

The conditional volatility of the SDFs are governed by two underlying state variables.

There are four shocks (one country-specific and three global) that have different properties in the way they are priced across countries.

1. A country specific shock 2. A global shock that is a common innovation priced differentially across

countries by a scaling factor. (the only source of parameter heterogeneity across countries).

3. A global shock priced differentially across countries even though the exposure is the same.

4. An equity specific global shock that is priced the same across countries.

For some reason inflation risk is not priced even though differences in real returns drive the differences in expectations in the ICAPM through deviations from PPP.

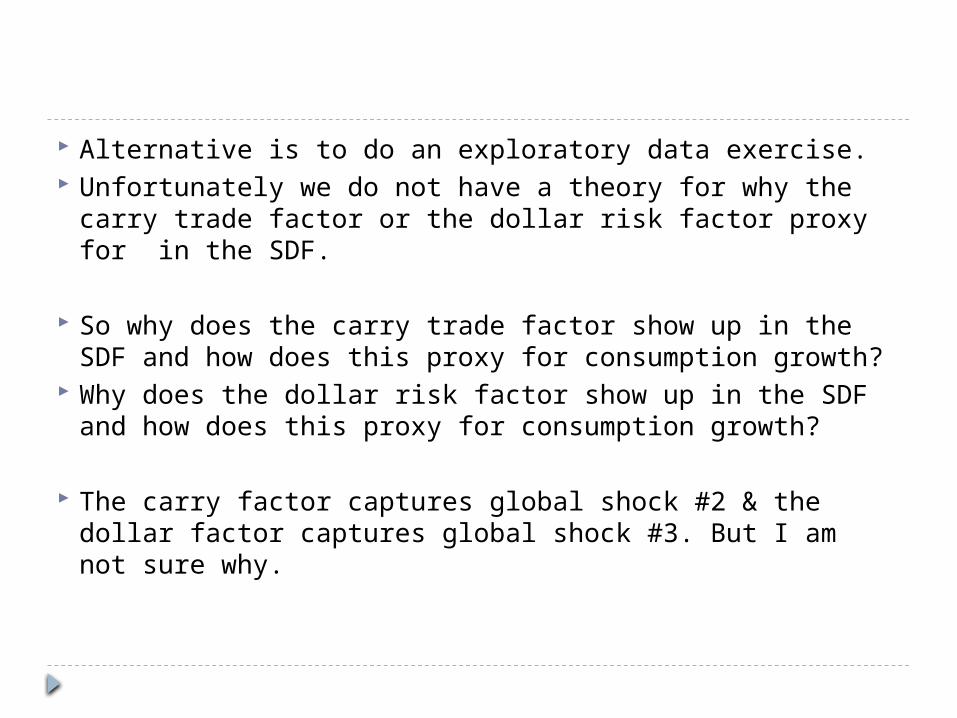

Alternative is to do an exploratory data exercise. Unfortunately we do not have a theory for why the

carry trade factor or the dollar risk factor proxy for in the SDF.

So why does the carry trade factor show up in the SDF and how does this proxy for consumption growth?

Why does the dollar risk factor show up in the SDF and how does this proxy for consumption growth?

The carry factor captures global shock #2 & the dollar factor captures global shock #3. But I am not sure why.

Push the authors to think seriously for why these factors are used in the estimating equation.

If risk premia are priced it’s because of the properties of the covariance between the returns and the factors that enter into the SDF (Carry Trade, $ Risk). In order for a factor to generate excess returns it has to play a role in the SDF.

But we need a theory for why a factor proxies for .

Otherwise analysis smacks of an empirical fishing expedition. Hazards with reaching empirical conclusions

Global equilibrium connects that SDFs. Cannot tie together them together if there is market segmentation. the specification does not take market segmentation into account which as we know can wreak havoc with the aggregation, separation and asset pricing results in portfolio theory a problem that is particularly salient in the international context given that international investors face heterogeneous investment opportunity sets. Misses heterogeneous opportunities given investability restrictions.

Volatility risk premium Ang-Bekaert measure vol. put into pricing equation. Drive out other traditional factors. Endogenously generate volatility risk premium. Are the carry trade and $-risk factors proxies for volatility risk rather than correlation risk?

The paper seems to ignore a lot of recent work on the volatility risk premium,the pricing of idiosyncratic volatility, and correlation risk. Lai Xu who examined the volatility risk premium in a world context. The bottom line seems to be that many studies overlook volatility risk which is proxied by the variables actually used in the study.

Idiosyncratic volatility proxies for aggregate volatility

(unobservable) gets priced.Ang Bekaert. Shows up in pricing returns. Proxying for aggregate volatility.

Related Documents