Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

2Copyright © 2017 Aquaa Partners Limited.

All Rights Reserved.

Contents

1. DIsRUPtIon ABoUnDs - ALL CoMPAnIes ARe “GoInG teCH” 4

THE DISRUPTIVE PAST IS DEAD. LONG LIVE THE DISRUPTIVE PAST. 6

M&A AS A STRATEGIC TOOL 9

TECHNOLOGY M&A GOES DEEP AND WIDE 10

2. FUnDAMentAL DRIVeRs oF teCHnoLoGY CoMPAnY M&A 16

EXPONENTIAL CHANGE MEANS COMPANIES AND THEIR PRODUCTS NEED TO CHANGE 22

3. HoW Do CoMPAnIes DeAL WItH tHese DIsRUPtIVe CHAnGes? 26

“THIS IS A MOVEMENT” 29

M&A IS A SOLUTION – BUT THERE ARE BUMPS IN THE ROAD 32

4. FIVe oF tHe Most CoMMon MIstAKes CoRPoRAtes MAKe WHen ACQUIRInG A teCHnoLoGY CoMPAnY 37

5. tHe GooD neWs – tHeRe Is A sCIenCe to ACQUIRInG A teCHnoLoGY CoMPAnY 43

“Neither RedBox nor Netflix are even on the

radar screen in terms of competition.” – Blockbuster CEO Jim Keyes, speaking to the Motley Fool in 2008.

3Copyright © 2017 Aquaa Partners Limited.

All Rights Reserved.

JPMorgan CEO Jamie Dimon opined plainly

in late 2015 that bitcoin will not survive:

“This is my personal opinion, there will be no real, non-controlled

currency in the world,”

said Dimon.

“There is no government that’s going to put up with it for long … there will be no currency that gets

around government controls.”

4Copyright © 2017 Aquaa Partners Limited.

All Rights Reserved.

DIsRUPtIon ABoUnDs - ALL CoMPAnIes ARe “GoInG teCH”

“(In 2016), the number of technology companies sold to non-

tech companies surpassed those acquired by tech companies for

the first time since the internet era began, according to data

compiled by Bloomberg. Excluding private equity buyers,

682 tech companies were purchased by a company in an

industry other than technology, while 655 were acquired by

tech companies.” – The New York Times, 2 Jan 2017

Increasingly, digital technology for companies is like water, air or electricity – a company has to have it – just to survive.

Rob Carter, CIO, FedEx Corporation says “the digital revolution is underway and survival requires way more than surface level tactics.”

However, survival isn’t enough. Technological advances are not only speeding up, but they are speeding up exponentially.

Customers across the world today are demanding and expecting more value, in the form of an outcome or experience, which tends to contain the following elements:

a) a more advanced product / service / solution, that hasb) more features and benefits, whichc) costs less and d) is simple to use and whiche) is available 24/7f) in all aspects of their daily lives.

When the customer demands more, it doesn’t just affect pricing, or product. It affects everything.

“We are a technology company”

– Goldman Sachs CEO,

Lloyd Blankfein

1.

5Copyright © 2017 Aquaa Partners Limited.

All Rights Reserved.

Higher customer expectations affect every facet of the organisation – R&D, production, operations, IT, sales and marketing, HR. No department or business function is safe.

In a recent survey of 600 large-cap corporate executives from around the world, EY reported that 90% of the executives surveyed said their companies faced increased competition from businesses that have already embraced digital technology1.

As the WSJ recently reported, new venture capital arms of large corporations seem to sprout up every few months, enabling their executives to mingle and hunt for partnerships and acquisitions. Entrants in 2016 included Campbell Soup Co., Kellogg Co., Jet-Blue Airways Corp. and Airbus Group SE, the last two located in Silicon Valley.2

1 EY, “Dealing in a digital world”, June 2016

2 The Wall Street Journal, 30 Dec 2016, “Old-Line Companies Like Wal-Mart and GM Acquire Taste for Tech

Start-Ups”

6Copyright © 2017 Aquaa Partners Limited.

All Rights Reserved.

Gartner Fellow, Mark Raskino, says “every industry will be digitally remastered.”

This “remastering” is already happening.

THE DISRUPTIVE PAST IS DEAD. LONG LIVE THE DISRUPTIVE PAST.

Kodak was once the world’s largest film company, with 145,000 worldwide employees in the late 1980s, and generating nearly $16 billion annual revenue in 1996. It had a market cap of approxi-mately $30 billion at its peak in 1997. “Kodak” was regularly rated as one of the world’s five most valuable brands.

In 1976, more than 90% of photographic film and more than 85% of cameras sold in the US were made by Kodak.3

But even this mightiest oak of oaks, Kodak, fell victim to technol-ogy disruption. In 2011 its share price fell by more than 80% and, in 2012, after 128 years of history, it filed for bankruptcy.

Steve Sasson, the Kodak engineer who invented the first digital camera in 1975, characterized the initial corporate response to his invention this way:

“But it was filmless photography, so management’s

reaction was, ‘that’s cute—but don’t tell anyone about it.’”

Kodak management’s inability to see digital photography as a dis-ruptive technology, even as its researchers extended the boundaries of the technology, would continue for decades. As late as 2007, a Kodak marketing video felt the need to trumpet that “Kodak is back “ and that Kodak “wasn’t going to play grab ass anymore” with digital.4

If disruption can destroy Kodak, it can destroy anyone.

3 The Independent, “The moment it all went wrong for Kodak”, 20 Jan 2012 and The Economist, “The last

Kodak moment?” 14 Jan 2012

4 Forbes, “How Kodak Failed”, Chunka Mui, 18 Jan 2012

“Every discussion we have now is

about technology”

– Deutsche Bank CEO,

John Cryan

7Copyright © 2017 Aquaa Partners Limited.

All Rights Reserved.

Most executives are generally aware of the disruption that technol-ogy has wielded over the past 15 years or so on so many traditional industries such as music, newspapers, travel agencies, books, trans-port and photographic film.

The already crippled industries who have been infected over so many years by digital technology disruption continue to attract wounds and battle scars.

For example, even in late 2016, after years and years of battering from digital disruption such as online classifieds, newspaper com-panies’ revenue continued to decline quite substantially.

A case in point is The Wall Street Journal, part of News Corp’s Dow Jones division, which in in Q3 2016 suffered a 21% decline in ad revenue.

The New York Times, Financial Times, Gannett (which owns USA Today), and Tronc (which owns the LA Times and Chicago Tri-bune), all suffered similar declines.

Gerry Baker, Editor-In-Chief of The Wall Street Journal, com-mented in November 2016 on the continuing consequences of dis-ruption from technology:

“The fall in advertising has been much faster

this year than anyone had expected.” 5

Pearson, the multinational publishing and education company, has faced a similar challenge from digital disruption. Revenues in Pear-son’s US higher education division – which accounts for 60% of profits and revenues – fell by 30% in Q4 2016.

When this news was announced on 18 Jan 2017 Pearson’s share price fell 29% in one day.

However the disruption we have witnessed in these industries over the past 15 years is not finished. Some would argue the disruption is just getting started.

5 Financial Times, “Wall Street Journal slims to tackle falling ad sales”, 16 Nov 2016

8Copyright © 2017 Aquaa Partners Limited.

All Rights Reserved.

From here it only gets worse – not only for the already disrupted industries, but also for those industries that are about to get dis-rupted, potentially even more painfully and swiftly than the indus-tries that were vulnerable to disruption during the genesis of digital technology 15 to 20 years ago.

As non-tech growth-focused companies now begin to feel the pres-sure of digital disruption they are starting to see the inevitable real-ity of their predicament.

The question is how does a growth-focused traditional company build the capabilities required to create more value and guard against disruption?

How does it keep up with continually rising customer expecta-tions? How does it generate more revenue? How does it maintain and increase its margins? How does it enhance the customer expe-rience? How does it continually manage its operating costs down in the face of ever-increasing globalisation?

Does a company need to build all these capabilities organically? Or should it acquire them? Or both?

These are monumental challenges that companies face today. But they can, and are, being met.

“A pessimist sees the difficulty in every opportunity; an optimist

sees the opportunity in every difficulty.” - Winston Churchill

Companies can take actions to future-proof themselves. If they are bold and capable enough, they can even go from “disruptee” to “disruptor”.

The most forward-thinking companies (think Netflix not Block-buster), are making changes – they are becoming technology companies.

It is not just the newspaper, books and music industries that are being remastered by technological change. All industries are under pressure.

“An iPhone belongs in your

pocket, not on the road,”

said Porsche CEO Oliver

Blume said.

9Copyright © 2017 Aquaa Partners Limited.

All Rights Reserved.

For many companies devising technological solutions and digital expertise and innovation in-house to combat the digital threat is no longer enough.

Corporates are beginning to manage this disruptive change, to their advantage, by acquiring technology companies.

M&A AS A STRATEGIC TOOL

The acquisition of the right technology company is becoming increasingly important to the success of a traditional growth-fo-cused company.

For much of the past 50 or 60 years, companies in industries rang-ing from manufacturing to retail generally avoided high-tech, Sili-con Valley-type “startups”, instead choosing to build their own new products or buy established companies.

But a combination of factors—fear of seeing business disrupted, struggles to find growth, changes that require new skills—are lead-ing more of these more traditional companies to search for tech-nology acquisitions.

Take the example of a traditional company that has successfully navigated the choppy waters of technology company acquisitions – Harman International Industries.

Harman, a traditional manufacturer of speakers and other audio gear, announced in November 2016 that it is being acquired by Samsung for $8 billion in an all-cash deal.

Why?

Because Harman, as a growth-focused company, created more value and guarded against disruption by expanding over the past several years into technology – specifically software development and components for connected cars – such as WiFi connectivity and navigation systems.

10Copyright © 2017 Aquaa Partners Limited.

All Rights Reserved.

Harman created much of its well-directed growth and expansion by acquiring tech companies, such as the $780m acquisition in 2015 of software-services company, Symphony Teleca Corp.

Simply put, Harman played to the future, not to where it was.

And what about Samsung itself? Harman is a rare large acquisi-tion for the company, since Samsung has traditionally preferred to develop technologies in-house. So why Harman and why now?

Cars are increasingly becoming “connected cars” and Samsung views Harman as a connected car technology company. Samsung’s strategy chief, Young Sohn, points out, “we think technology is more critical than being in the metal-bending business.”6

John Casesa, who runs global strategy for Ford Motor Co. says “we are in an era in our industry where M&A will be a frequently used instrument.”7 (Ford recently acquired a San Francisco-based startup commuter shuttle service called Chariot for $65m).

TECHNOLOGY M&A GOES DEEP AND WIDE

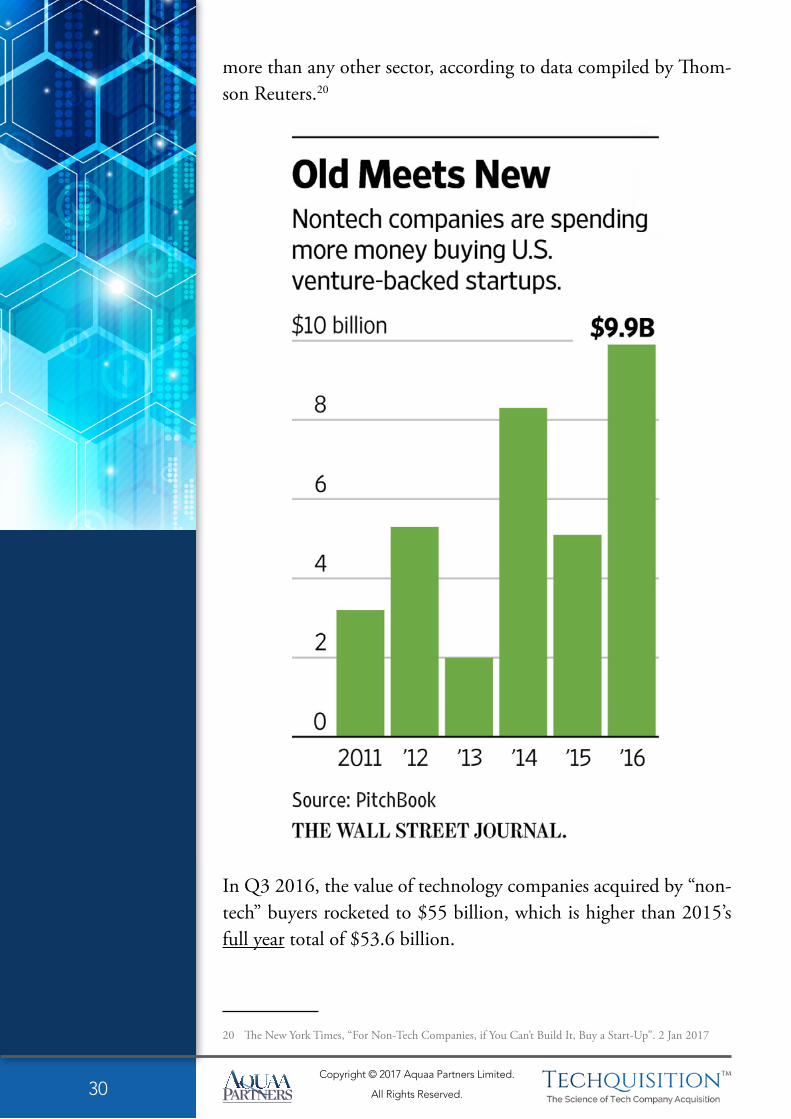

Exactly how widespread is M&A of technology companies being used today as a tool for growth-focused companies to respond to digital disruption?

EY states that more than 67% of global executives now plan to use M&A to upgrade their digital capabilities in responding to height-ened competition and a disruptive environment.

The chart below (from EY’s June 2016 “Dealing in a digital world” study) shows that the 90% of executives who are concerned about their competition having already embraced digital technology believe that 62% of this competition have achieved their competi-tive position via M&A or inorganic means.

6 WSJ, 15 Nov 2016, “Samsung Charges Into Auto Tech With $8 Billion Deal for Harman”

7 WSJ, 30 Dec 2016, “Old-Line Companies Like Wal-Mart and GM Acquire Taste for Tech Start-Ups”

“It’s our recognition that if you go to bed as an industrial company, you’re going to wake

up as a software and analytics company. The

notion that there’s a huge separation

between the industrial world and the world

of digitalization – those days are

over…”

– Jeffrey Immelt,

Chairman and CEO, GE

11Copyright © 2017 Aquaa Partners Limited.

All Rights Reserved.

Acquisitions of technology companies are impacting all elements of acquirers’ businesses – logistics/supply chain, back office, inventory management, cost of goods reduction, quality of goods enhance-ment, big data customer analytics, new product extensions and improvements, enhanced customer / user experience – this list goes on and on.

BBVA, Mastercard and Boeing, for example, have made seven, eight and 10 technology company acquisitions, respectively, since 2011 according to PwC.

In this time Siemens has acquired or invested in at least 26 technol-ogy companies, GE at least 22.

Companies in non-digital industries completed 48% more tech-nology company acquisitions in 2015 than they did in 2011.

Of the roughly 20,000 technology company acquisitions announced between 2011 and 2015, about a third involved a non-tech, non-telecom acquirer. (PwC)

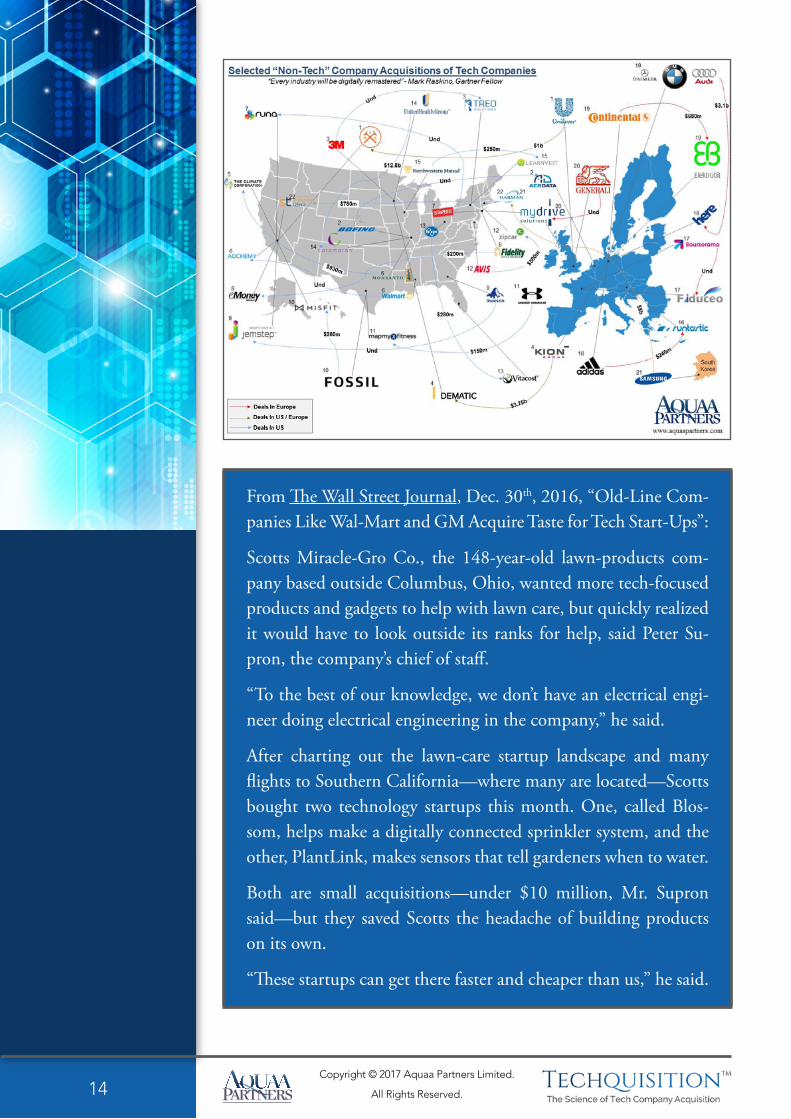

The infographic below highlights the trend of “non-tech” compa-nies acquiring “tech” companies as they, and their respective indus-tries, go more and more tech.

12Copyright © 2017 Aquaa Partners Limited.

All Rights Reserved.

“There is no reason anyone would

want a computer in their home,”

said Ken Olsen, founder

of Digital Equipment

Corporation, 1977.

13Copyright © 2017 Aquaa Partners Limited.

All Rights Reserved.

A few of the more interesting technology company acquisi-tions made by more traditional companies include the following transactions:

�� Samsung acquiring audio systems company, Harman ($8b; Nov 2016)

�� John Wiley & Sons acquiring SaaS content delivery to publishers company, Atypon Systems ($120m; Aug 2016)

�� Telus Health acquiring cloud-based EHR and PM solutions company, Nightingale Informatix ($14m; Jul 2016)

�� Mars Petcare acquiring dog fitness tracking company, Whistle ($117m; Apr 2016)

�� GM acquiring self-driving tech start-up, Cruise Automation ($1b; Mar 2016)

�� Adidas acquiring app tracking company, Runtastic ($240m; Aug 2015)

�� Hello Curry fast food chain acquiring software company Fire42 (und; Jun 2015)

�� Under Armour acquiring fitness and nutrition tracking platform, MapMyFitness ($150m; Feb 2015)

�� Harman acquiring software-services company, Symphony Teleca ($780m; Jan 2015)

�� Capital One acquiring user experience consultancy, Adaptive Path (und; Oct 2014)

�� Monsanto acquiring weather big data company, Climate Corp. ($930m; Oct 2013)

Highlighted below in a map format are a few of the more interest-ing technology company acquisitions executed by traditional com-panies over the past few years:

“We don’t consider customers cargo,”

said Jaguar’s head of

R&D, Wolfgang Epple,

in 2015.

“We don’t want to build a robot that delivers the cargo from A to

B.”

14Copyright © 2017 Aquaa Partners Limited.

All Rights Reserved.

From The Wall Street Journal, Dec. 30th, 2016, “Old-Line Com-panies Like Wal-Mart and GM Acquire Taste for Tech Start-Ups”:

Scotts Miracle-Gro Co., the 148-year-old lawn-products com-pany based outside Columbus, Ohio, wanted more tech-focused products and gadgets to help with lawn care, but quickly realized it would have to look outside its ranks for help, said Peter Su-pron, the company’s chief of staff.

“To the best of our knowledge, we don’t have an electrical engi-neer doing electrical engineering in the company,” he said.

After charting out the lawn-care startup landscape and many flights to Southern California—where many are located—Scotts bought two technology startups this month. One, called Blos-som, helps make a digitally connected sprinkler system, and the other, PlantLink, makes sensors that tell gardeners when to water.

Both are small acquisitions—under $10 million, Mr. Supron said—but they saved Scotts the headache of building products on its own.

“These startups can get there faster and cheaper than us,” he said.

“I personally don’t want my blood pressure and blood sugar values stored in the cloud, or on servers in Silicon Valley

… I cannot accept the responsibility of whether my device warns a customer

in time before a heart attack.”

– Swatch executive Nick Hayek Jr.,

speaking to The Guardian

16Copyright © 2017 Aquaa Partners Limited.

All Rights Reserved.

FUnDAMentAL DRIVeRs oF teCHnoLoGY CoMPAnY M&A

To understand what is fundamentally driving this growing trend of traditional companies acquiring technology companies, it helps to go back in time to gain perspective on where we are today.

Twenty-five years ago there were no cellphones, digital music play-ers, digital cameras, cloud computing, YouTube, iPhone, tablets, Dropbox, Google, Facebook, texting, Siri, Instagram, Google Maps, LinkedIn or augmented reality games. In fact, the “Internet” and “email” were just in their infancy.

A kid in Africa with a cellphone today has more access to accurate information than the President of the United States did 15 years ago.

Within the last five years we’ve learned how to reprogram stem cells to rebuild the hearts of heart attack victims. The stem cells are harvested from skin cells, not human embryos.

Even investing has changed, quite dramatically.

Back in 1992, mutual funds charged about 8% sale commissions – even on dividends reinvested in the fund – and annual expenses of at least 1% of assets.

If you put $10,000 into a mutual fund then, only $9,200 would go to work for you, and you would pay at least $100 a year in expenses on that.

Today, you can buy exchange-traded funds, commission free, with annual expenses as low as 0.03%. Invest $10,000 and $9,997 stays in your own pocket. For small investors, the costs of buying and selling individual stocks also have shrunk towards zero8.

8 “Some of the Wisest Words Even Spoken About Investing”, Jason Zweig, The Wall Street Journal, 25

Nov 2016

These mobile games are “candidly

disposable from a consumer standpoint,”

said Nintendo president

Reggie Fils-Aime,

speaking

in 2011.

2.

17Copyright © 2017 Aquaa Partners Limited.

All Rights Reserved.

And what about the next 10 years?

In the next 10 years, everything we know - and do - will change. The ways in which we shop, work, sleep, eat, travel, communicate, bank, entertain ourselves, conduct warfare, manufacture, design, distribute, create, transact, and maintain our own health – will all change. It will all be different9.

For example, if we can turn off genes, then why not turn off the ones in cancer cells that enable them to pursue unlimited repro-duction, until they kill its host? That development would cure all cancers, and is probably only a decade off10.

Compared to the next 10 years, the advances we’ve seen in the last 25 years are just incremental improvements; just a foundation for the revolution of exponential technology-based metamorphosis we are about to experience.

Most of us are familiar with Sir Isaac Newton’s comment to scien-tist Robert Hooke in 1675: “If I have seen further it is by standing on ye shoulders of Giants.”

9 “Over the Next 10 Years Fortunes Will Be Made”, Bonner & Partners, 26 Nov 2016

10 Stocks to Buy for the Coming Roaring Twenties, John Thomas

18Copyright © 2017 Aquaa Partners Limited.

All Rights Reserved.

But progress in science and innovation goes deeper.

Humans evolved to become linear thinking animals (eg we saw gazelles running right to left and that’s where we threw the spear). We tend to project and forecast growth and change at a linear rate.

But science / technology / innovation grows at an exponential rate.

The difference between linear and exponential is the difference between night and day.

Exponential growth is just like compound interest.

“Compound interest is the eighth wonder of the

world. He who understands it, earns it ... he who

doesn’t ... pays it.” – Albert Einstein

Andy Kessler describes it well below (WSJ, 8 November 2016):

“In 1970, Intel pioneered integrated memory chips to replace

wire-wrapped diodes. The 3101 was a 64 bit SRAM chip

that IBM and others could buy for $40 each. Let’s call it a buck

a bit. Today…you’re carrying around an iPhone or Android

with at least 32 gigabytes of memory. At a buck a bit, that’s

. . . wow, congratulations! You’re a billionaire! We all are…

this is progress on steroids and is coming faster and faster…”

These exponential technological advances are speeding up custom-ers’ expectations, which in turn are affecting consumer behaviours, which in turn affect behaviour in the enterprise.

Whether we like it or not, our society is rapidly – exponentially – advancing to a brave new “Westworld” singularity.

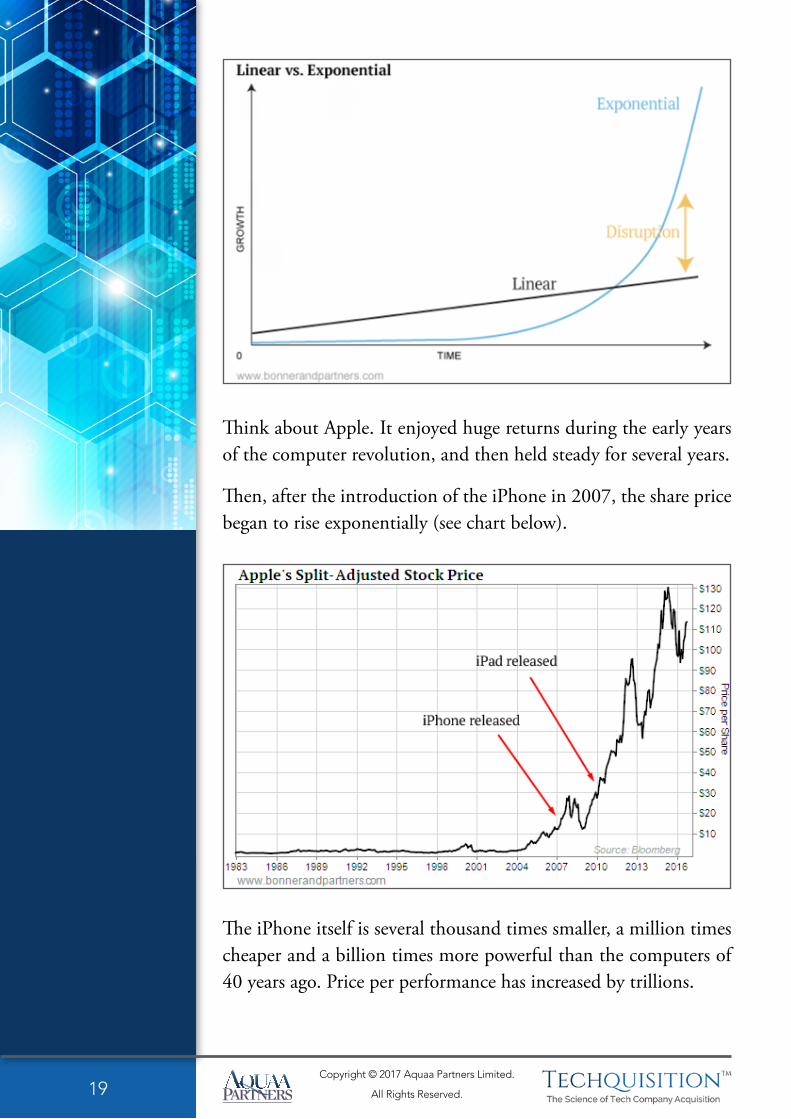

The problem with identifying an exponential change is that in the early stages it looks the same as ordinary linear change.

As shown in the graphic below, exponential changes grow slowly in the early stages. But when they reach a certain tipping point they take off like a rocket.

“Microsoft will roll [Salesforce]

over,”

Thomas Siebel of Siebel

Systems flatly told

Bloomberg in 2003.

“They get Zambonied.”

19Copyright © 2017 Aquaa Partners Limited.

All Rights Reserved.

Think about Apple. It enjoyed huge returns during the early years of the computer revolution, and then held steady for several years.

Then, after the introduction of the iPhone in 2007, the share price began to rise exponentially (see chart below).

The iPhone itself is several thousand times smaller, a million times cheaper and a billion times more powerful than the computers of 40 years ago. Price per performance has increased by trillions.

20Copyright © 2017 Aquaa Partners Limited.

All Rights Reserved.

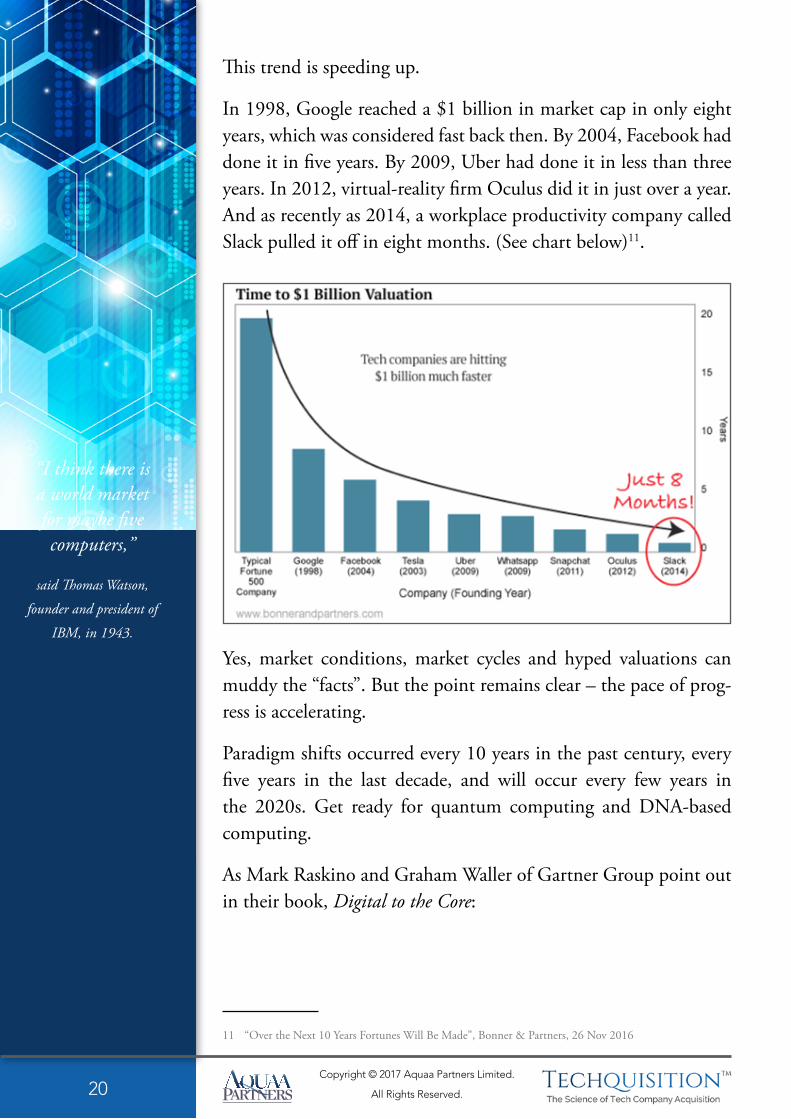

This trend is speeding up.

In 1998, Google reached a $1 billion in market cap in only eight years, which was considered fast back then. By 2004, Facebook had done it in five years. By 2009, Uber had done it in less than three years. In 2012, virtual-reality firm Oculus did it in just over a year. And as recently as 2014, a workplace productivity company called Slack pulled it off in eight months. (See chart below)11.

Yes, market conditions, market cycles and hyped valuations can muddy the “facts”. But the point remains clear – the pace of prog-ress is accelerating.

Paradigm shifts occurred every 10 years in the past century, every five years in the last decade, and will occur every few years in the 2020s. Get ready for quantum computing and DNA-based computing.

As Mark Raskino and Graham Waller of Gartner Group point out in their book, Digital to the Core:

11 “Over the Next 10 Years Fortunes Will Be Made”, Bonner & Partners, 26 Nov 2016

“I think there is a world market for maybe five computers,”

said Thomas Watson,

founder and president of

IBM, in 1943.

21Copyright © 2017 Aquaa Partners Limited.

All Rights Reserved.

“Leaders from traditional industries should not

underestimate how fast the art of what is technically

possible can tip, nor its disruptive power. Sometimes the

change just ahead of you feels like science fiction.”

By 2020 super-computer capability (which surpasses human brain computational ability) will be available on a low end laptop. By 2050, this single laptop will have the same computing power of the entire human race, about 9 billion individuals. It will also be small enough to implant in our brains.

Stock analysts, investors and many corporate senior executive deci-sion makers make a fatal flaw in estimating future company earn-ings based on linear trends of the past, instead of on the exceptional exponential growth that will occur in the future.

Based on the growth of stock market indices of the last century (eg the Dow rose from 100 to 10,000, an increase of 100x), the current stock indices are actually currently lagging the historical trend – the Dow is only up 3.2% a year in the last 16 years into the new century.

After the next major market crash/correction, which we expect will happen sometime during 2017-2019 (for further views on this coming crash click here), the stock indices will play catch-up in a major way during the 2020s, when economic growth begins to accelerate (could be from 2% to 4-5% a year in the US), thanks to the effects of massively accelerating technological change.

As an example, just consider solar energy use, which is on an expo-nential path. It’s now only 1% of the world’s energy supply, but is also only 7 doublings away from becoming 100%. Then we’ll consume only one 10,000th of the sunlight hitting the earth. Geo-thermal offers similar opportunities.

Food is another example of disruption from exponential innovation.

In 1790, farm jobs accounted for 90% of all US jobs, compared to < 2% today.

22Copyright © 2017 Aquaa Partners Limited.

All Rights Reserved.

Still, in 2016, it took 63 billion land animals to feed 7 billion humans. Land animals occupy one-third of the non-ice landmass, use 8% of our water supply and generate 18% of all greenhouse gases.

In the near future, bio-printing of meat (beef, chicken, pork) would allow us to feed the world with 99% less land, 96% less water and 96% fewer greenhouse gases and 45% less energy.

Cloned muscle tissue of cows will be produced in factories, dis-ease-free, at a fraction of the present cost.

In addition, 70% of a food’s final retail price comes from trans-portation, storage and handling. Vertical farming, already a $1 bil-lion industry in 2015, will help eliminate this cost. One acre of a vertical farm can produce 10-20x that of a traditional farm. Food delivery will be disrupted by food on demand and drone delivery.

Food preparation is another massive opportunity. The US consumes nearly 1 billion meals per day and spends an average of 11 million minutes per day on food prep and clean up. Food preparation and clean-up will be disrupted by 3D printed food, personalised nutri-tion and AI-designed recipes12.

The ultimate upshot is that these technologies will relatively rapidly help eliminate poverty around the world.

EXPONENTIAL CHANGE MEANS COMPANIES AND THEIR PRODUCTS NEED TO CHANGE

The rapidly increasing, exponential path of change that we are on means every industry will need to continually re-invent its business model, or disappear.

Raskino and Waller of Gartner again:

12 “Reinventing Food”, Nov 2016, Peter Diamandis

“Screw the Nano. What the hell does the Nano do? Who

listens to 1,000 songs?”

said Motorola CEO Ed

Zander, speaking at a

conference in 2006.

23Copyright © 2017 Aquaa Partners Limited.

All Rights Reserved.

“…the technology tipping point conundrum, which has

previously been restricted to ‘tech’ companies, now extends

to all companies because the next generation of everyday

products will likely include digital capability…

…Over the past twenty years of IT advancement, most

businesses have changed everything but the product. Even

if they now possess advanced, Internet-enabled business

models, they are actually making and selling pretty much

the same kind of products they were making in 1994…

...Changing the product is the final step, and the biggest shock

of all. Internet-connected and embedded digital functions

will become a key part of your product and the value your

customer buys. This value may represent 20%, 40% or

60% of what the customer acknowledges and pays for.”13

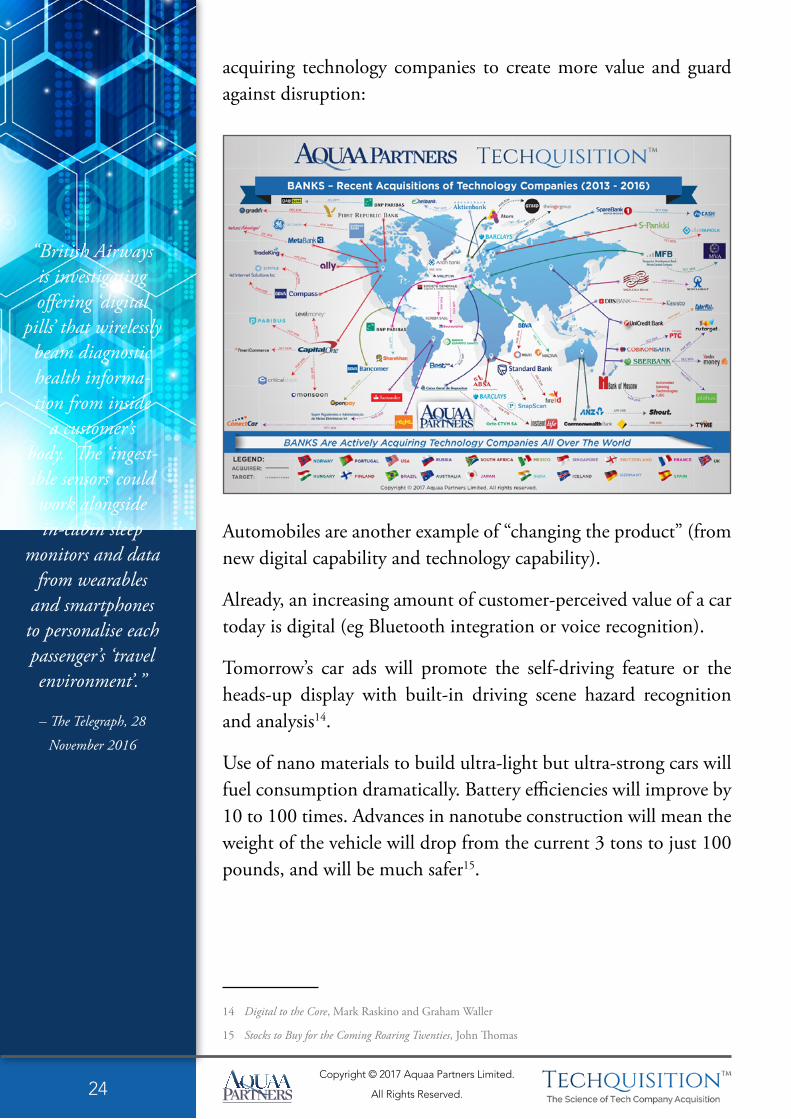

The banking industry is an example of where the product, and ser-vice, must change.

In November 2015 Anthony Jenkins, the former CEO of the world’s 16th largest bank, Barclays Bank, said that the IT systems of all of Britian’s big four banks are “antiquated and inefficient”.

Jenkins warns that if banks fail to deliver superior services to com-pete with Fintech companies then the banks “risk losing revenue” and even risk “being displaced”.

Given Jenkins’ credible insight and the fact that technology spend in the banking industry represents the largest IT spend of any industry, this is a serious affirmation of the importance of technol-ogy in industry today.

Indeed, as one can see from the map below, many banks all over the world understand the threat of technology, and they are actively

13 Digital to the Core, Mark Raskino and Graham Waller

24Copyright © 2017 Aquaa Partners Limited.

All Rights Reserved.

acquiring technology companies to create more value and guard against disruption:

Automobiles are another example of “changing the product” (from new digital capability and technology capability).

Already, an increasing amount of customer-perceived value of a car today is digital (eg Bluetooth integration or voice recognition).

Tomorrow’s car ads will promote the self-driving feature or the heads-up display with built-in driving scene hazard recognition and analysis14.

Use of nano materials to build ultra-light but ultra-strong cars will fuel consumption dramatically. Battery efficiencies will improve by 10 to 100 times. Advances in nanotube construction will mean the weight of the vehicle will drop from the current 3 tons to just 100 pounds, and will be much safer15.

14 Digital to the Core, Mark Raskino and Graham Waller

15 Stocks to Buy for the Coming Roaring Twenties, John Thomas

“British Airways is investigating offering ‘digital

pills’ that wirelessly beam diagnostic health informa-tion from inside

a customer’s body. The ‘ingest-ible sensors’ could work alongside in-cabin sleep

monitors and data from wearables

and smartphones to personalise each passenger’s ‘travel environment’.”

– The Telegraph, 28

November 2016

“The development of mobile phones will follow a similar path

to that followed by PCs,”

said Nokia’s Chief Strategy Officer

Anssi Vanjoki, in a German interview

(translated through Google Translate).

“Even with the Mac, Apple attracted a lot of attention at first, but they have

remained a niche manufacturer. That will be their role in mobile phones as well.”

26Copyright © 2017 Aquaa Partners Limited.

All Rights Reserved.

HoW Do CoMPAnIes DeAL WItH tHese DIsRUPtIVe CHAnGes?

With all these changes ahead of us, how can each industry, and the companies within an industry, “continuously reinvent” their busi-ness model?

Norbert Schwieters of PwC puts it this way:

“If your company is falling into the trap of thinking that it

can stay in the same industry forever, or even for the next two

decades, you risk losing out to more flexible competitors.

You can avoid this trap by taking on an outcomes mind-

set. Instead of thinking of your company as providing

a particular type of product or service — electric

power, health records management, or automobile

components — think of it as a producer of outcomes.

The customer needs to get somewhere, so you’re not a

car company; you’re a facilitator of that outcome. The

house is cold, so you help make it warm, possibly without

supplying the necessary fuel. Many of the changes taking

place today have come about because a few leading

companies have replaced their products with outcomes.

Customers, in turn, are making fewer purchases to

accumulate physical things and more purchases to

achieve outcomes, convenience, and value.”16

But still, what are the ways to execute on this “outcome” thinking? How can a company make it happen?

16 “The End of Conventional Industry Sectors”, PwC, strategy+business, 3 Jan 2017

“It’s a little bit like, is the

Albanian army going to take over the world? I don’t

think so,”

said Time Warner CEO

Jeffrey L Bewkes, when

asked in 2010 what he

thought about Netflix’s

push toward licensed

content.

3.

27Copyright © 2017 Aquaa Partners Limited.

All Rights Reserved.

An increasing number of corporate executives see the acquisition of technology companies as the fastest and the most efficient and productive way to accelerate their corporate transformation.

One reason non-tech executives have become more active in tech-nology deal making is that they have become more comfortable with technology itself. They now understand “software” and “the cloud” etc.

GE has moved its headquarters to Boston, more of a hub for tech and start-ups than its previous home in Fairfield, Conn. The com-pany’s recent commercials feature the tagline: “The digital com-pany. That’s also an industrial company.”

As previously mentioned, a recent EY survey17 showed that 67% of corporate executives believe acquiring a technology company, ie acquiring digital capabilities, assets and technologies, can “bridge gaps and accelerate growth”. A similar number see “rapid response” as essential.

17 “Dealing in a Digital World”, EY, June 2016

28Copyright © 2017 Aquaa Partners Limited.

All Rights Reserved.

Of course, acquiring a technology company has significant challenges.

Historically, non-tech companies have not felt comfortable paying the high prices that many technology companies can claim and often achieve. Older, mature companies that are not as rapidly growing tend to trade at lower valuations relative to measures like revenue and earnings, compared with young tech companies that sometimes do not even have earnings.

Wal-Mart, for example, has a market capitalisation about 65 times that of what it paid for Jet.com, and it has roughly $480 billion in revenue compared with what it said was $1 billion in annualized revenue for Jet.com.

But Wal-Mart is facing ever-more competition from Amazon.com and other retailers, and executives at the company have said Jet.com will allow them to expand their e-commerce at a much faster rate.18

While boards and CEOs of non-tech companies now have a better understanding of tech company valuation, one of the next chal-lenges for many of these companies is in integrating their technol-ogy company acquisitions with the main business.

Shareholders are increasingly judging and expecting their manage-ment teams to be bold and to play to the future and make strong long-term strategic moves, rather than short-term tactical fixes.

An additional emerging challenge for would-be tech company acquirers is that the deal environment today for digital companies or tech companies is becoming so much more competitive – not only from tech companies themselves as acquirers but also from tra-ditional non-tech strategic buyers in all industries who want tech.

More and more traditional companies that are growth-focused are now thinking “How can we protect against disruption? How can

18 WSJ, Dec. 30th, 2016, “Old-Line Companies Like Wal-Mart and GM Acquire Taste for

Tech Start-Ups”

29Copyright © 2017 Aquaa Partners Limited.

All Rights Reserved.

we deliver more value? How can we deliver better outcomes? How can we meet and beat our customers’ expectations?”

Most interestingly some are even asking “How can we be a disrup-tor ourselves, rather than be a disruptee?”

These companies are taking action. They are acquiring technology companies, among many other organic initiatives.

The idea of having a “disruptor” mentality is growing in indus-try. Rapid advances in technology – which include AI, Blockchain, IoT, 3D printing, Augmented Reality and Virtual Reality – now allow for the possibility for everyone to think this way – if they choose to do so.

Raskino and Waller of Gartner relate the consequences of digital transformation:

“Your company, and many others in your industry, are facing a

future in which digital technologies will become integral parts

of your products and services – not just in the marketing of

them. If you don’t make that happen, someone else will.”19

The industry remastering is happening now and it is happening in “fast-motion” – 2x, 4x, 8x, 16x….infinity.

If executives do not pay attention to this trend of exponentially advancing digital technology becoming an integral part of a com-pany’s core products and services then they should not be surprised when it (eg a “Netflix”) stampedes all over them (eg a “Block-buster”) and crushes them into road kill.

“THIS IS A MOVEMENT”

Of the 45,416 transactions announced in 2016, approximately 6,660, or 15 percent, were acquisitions of technology companies,

19 Mark Raskino and Graham Waller, “Digital to the Core”

“Digital transfor-mation marches

on. Tech and non-tech com-panies alike are

being disrupted by innovative digital technologies and are turning to

M&A in search of solutions.”

– EY Global Technology

M&A Report: 3Q 2016

30Copyright © 2017 Aquaa Partners Limited.

All Rights Reserved.

more than any other sector, according to data compiled by Thom-son Reuters.20

In Q3 2016, the value of technology companies acquired by “non-tech” buyers rocketed to $55 billion, which is higher than 2015’s full year total of $53.6 billion.

20 The New York Times, “For Non-Tech Companies, if You Can’t Build It, Buy a Start-Up”. 2 Jan 2017

31Copyright © 2017 Aquaa Partners Limited.

All Rights Reserved.

In other words, in the three months of Q3 2016 the value of tech companies acquired by non-tech acquirers was greater than all 12 months of last year’s value of tech companies acquired by non-tech acquirers.

As Donald Trump might say, “this is a movement.”

At $93.2 billion of tech companies acquired by non-tech compa-nies through the first nine months of 2016, non-tech acquirers of tech companies are 74% ahead of full-year 2015 – this represents 27% of all 2016 aggregate global tech M&A value.21

In fact, CB Insights reported on 15 Dec 2016 that:

“Non-Tech Acquirers Are Suddenly More Common

Than Tech Companies in Deals For $1B+ Startups”

This is an astounding development.

The chart below shows the eight non-tech companies that have acquired a venture capital-backed U.S. “startup” in 2016 YTD for $1 billion or more, vs only one tech company acquirer (Cisco).22

21 EY Global Technology M&A Report:3Q 2016

22 CB Insights, “Non-Tech Acquirers Are Suddenly More Common Than Tech Companies In Deals For

$1B + Startups”, 15 Dec 2016

“We’ve learned and struggled for a few years here figuring out how to make a decent phone … PC guys are not going to just figure this

out,”

Palm CEO Ed Colligan

in 2006, after news that

Apple was developing a

phone.

“They’re not going to just walk in.”

32Copyright © 2017 Aquaa Partners Limited.

All Rights Reserved.

CB Insights commented: “…the make-up of buyers appears to be shifting as incumbents across industries ranging from consumer pack-aged goods to auto to insurance buy into venture-backed companies.”

As evidence of the “movement”, in late 2016 Accel Partners coun-seled the founders of its invested startup companies to become more familiar with these older, more traditional companies, an apparent gesture to the disdain that startup founders often express about their corporate counterparts.23

M&A IS A SOLUTION – BUT THERE ARE BUMPS IN THE ROAD

The ultimate cause and core driver now of these technology com-pany acquisitions by non-tech companies is summed up well by Raskino and Waller:

23 WSJ, 30 Dec 2016, “Old-Line Companies Like Wal-Mart and GM Acquire Taste for Tech Start-Ups”

“Technology is in such a state of rapid evolution,

and tech and most other industries are so deep into disruptive dig-ital technology

transformations, that buyers know they can’t wait for markets to smooth themselves out.”1

– EY, November 2016

1 EY Global Technology

M&A Report: 3Q16

33Copyright © 2017 Aquaa Partners Limited.

All Rights Reserved.

“Over the past twenty years of IT advancement, most businesses

have changed everything but the product. Even if they now possess

advanced, Internet-enabled business models, they are actually

making and selling pretty much the same kind of products they

were making in 1994. Changing the product is the final step,

and the biggest shock of all. Internet-connected and embedded

digital functions will become a part of your product and the

value your customer buys. This value may represent 20%, 40%

or 60% of what the customer acknowledges and pays for.”24

It is the product or service itself that is now being transformed. As companies embed more and more digital and Internet-connected functionality into their core products and services, they inevitably create more value, guard against disruption and enhance the cus-tomer experience.

Indeed, as mentioned earlier, several of these growth-focused com-panies will become disruptors themselves.

Acquiring a technology company – the right technology company – accelerates this value creation and prevents against being disrupted.

When an acquirer gets a technology acquisition right it can be truly transformative for the whole company.

An example of this potential game-changing transformation that can come from acquiring a technology company is evidenced by Alexa Von Tobel, the CEO of seven-year-old startup LearnVest, which was acquired by Northwestern Mutual for a reported $250m in 201525, describing the post-acquisition culture of the company a year after the acquisition:

24 Raskino and Waller, “Digital to the Core”

25 RIABiz, 1 April 2015, “The real reasons Northwestern Mutual paid a reported $250m for LearnVest”

34Copyright © 2017 Aquaa Partners Limited.

All Rights Reserved.

“The really exciting thing about bringing together a

106-year-old company and a seven-year-old data-driven,

fast-moving start-up is the chance to create a third culture,

which makes innovative, data-driven decisions, and does

them at scale. I think it’s going really, really well so far,

because our core values are completely aligned.”26

When a traditional growth-focused company acquires a technology company it can achieve at least some or all of the following:

�� Create new products and services (that would not otherwise be possible)

�� Produce a higher quality of goods

�� Improve inventory turns

�� Reduce costs

�� Squeeze more productivity and efficiency from your assets

�� Make your customers a lot happier than they were before

�� Get some really talented and able new staff

�� Catalyse a culture change

However, a corporate acquirer has to acknowledge that acquiring a technology company can be very tricky, with a lot of moving parts.

Acquiring a tech company is not like buying a house or an oil field or a factory.

It’s more like buying a Formula One team – think engine, driver, tyres, weather, equipment, fuel, design, pit crew, track, other driv-ers, manager, tech support staff – and then mix it all up together.

If a company doesn’t have its act together on each of the individual disciplines as well as on the overall web of disciplines seamlessly

26 McKinsey & Company, “How a culture survives when a start-up merges with an incumbent”, November

2016

Steve Jobs:

“It doesn’t matter how good or bad

the (Amazon Kindle) is, the fact is that people don’t

read anymore.”

35Copyright © 2017 Aquaa Partners Limited.

All Rights Reserved.

interconnecting with each other, then forget it – the company will lose. There is no point even trying.

It’s the same with acquiring a technology company. If one approaches it in an ad-hoc, opportunistic or unplanned manner then failure is likely.

In fact, there are probably 1,000 ways a technology acquisition can go wrong.

If an acquirer does get it wrong, then it can cost the acquirer mil-lions and millions of dollars (or euros, pounds or yen), and months and months, and sometimes years, of painful undoing.

Microsoft CEO Steve Ballmer had this to say

about the iPhone’s lack of a physical keyboard:

“500 dollars? Fully subsidized? With a plan? I said that is the most expensive

phone in the world. And it doesn’t appeal to business customers because it doesn’t have a keyboard. Which makes

it not a very good email machine.”

37Copyright © 2017 Aquaa Partners Limited.

All Rights Reserved.

FIVe oF tHe Most CoMMon MIstAKes CoRPoRAtes MAKe WHen ACQUIRInG A teCHnoLoGY CoMPAnY

Five of the most common mistakes we see corporates making when acquiring a technology company include the following:

MISTAKE # 1 - ACQUIRING THE WRONG COMPANY

Too often a corporate will acquire a target company because it was relatively easy, or “it was there”, instead of ensuring that it was the right company after undertaking an exhaustive search and review. Acquiring the wrong company can happen for many reasons, including the following:

a. The CEO knows the target and its management, and overly influences the other executives on his or her man-agement team without properly scrutinising the target

b. One of the company’s leaders likes a company from his or her historical relationship and pushes it through without doing a thorough review of the target’s competitors or peers and of other alternatives (including other targets or joint ventures, partnerships and strategic investments).

c. The CFO, Head of M&A or Head of Corporate Devel-opment has been tasked by the CEO or board with mak-ing one or more “acquisitions”, but is under-resourced, and relies only on internal leads rather than being able to reach out externally for support and advice, including sourcing fresh ideas, leads and guidance.

d. The management team is “sold” on a target by an invest-ment bank leading an auction of the target. The bank pro-motes the target’s “scarcity value” and claims that “your competitors will own it if you don’t” etc. The acquiring management and board succumbs.

RIM’s co-CEO, Jim

Balsillie, wrote off the

iPhone almost completely:

“It’s kind of one more entrant into an already very busy space with lots of choice for

consumers … But in terms of a sort of a sea-change

for BlackBerry, I would think that’s

overstating it.”

4.

38Copyright © 2017 Aquaa Partners Limited.

All Rights Reserved.

e. Management wrongly believes it needs the target based on the wrong assumptions it has made about its own stra-tegic imperatives.

MISTAKE # 2 - NOT BUILDING A RELATIONSHIP WITH THE TARGET’S FOUNDERS / MANAGEMENT

If a corporate doesn’t build a relationship with the founders or management team of a target technology company, then sometimes the founders or leaders of the target will leave the acquiring or merged company, even before the earn-out period is completed.

Founders of technology companies are often sensitive, particu-larly to their own products, services or creations. If the acquir-ing company executives don’t show that they appreciate this sensitivity – both before and after a deal completes – then they can lose the top executives of the target company, which could cause other valued employees to leave, which could cause value destruction of the asset acquired.

Technology company executives need to know they are valued. They need to know that they and their talented staff matter, and that they will make an important impact on the acquiring com-pany. They cannot be forgotten. Building a relationship with the founders and management team of the target technology com-pany can be as important to the acquirer’s success as any asset of the target company.

MISTAKE # 3 - ASSUMING THE EARN-OUT, PERFORMANCE-BASED DEFERRED CONSIDERATION MATTERS MORE THAN THE UPFRONT PRICE PAID AT CLOSING

Founders and technology company leaders have typically spent years and years secreting blood, sweat and tears working early mornings, late nights, weekends, and experiencing lost custom-ers, lost employees and other painful disasters. Sometimes they

39Copyright © 2017 Aquaa Partners Limited.

All Rights Reserved.

just want out. Often they will leave before they receive their full earn-out deferred consideration, particularly if they are feeling especially unloved, tired or frustrated.

Sometimes acquirers can increase the offered upfront consider-ation amount only slightly while relatively dramatically reducing the long-term incentive consideration and compensation. This might seem counter-intuitive, but it’s all about getting inside of the heads of the founders and leaders of a tech company.

MISTAKE # 4 – NOT ARTICULATING WELL ENOUGH WHY YOU WANT TO ACQUIRE THE COMPANY

If the founders / leaders of a technology company believe that you don’t understand them, they might balk at your approach. Even if you offer an attractive price, or package of value as terms, they might accept another offer instead. Alternatively, you might agree terms with them, but they might just take the cash and then leave.

Fundamentally, the founders and leaders of technology compa-nies want to be understood. They want to feel that an acquirer appreciates them and their products or services and what they have created. They want to know what the acquirer’s strategy is: “What do you intend to do with us and our product/service and why?” They want to know the big picture. They want to be inspired. They want to know how their product will help change the world by your owning it instead of them.

If the founders and leaders of a tech company are going to sell their “baby”, they want to know that it will be in good, safe hands, and that it will grow. Show them how you intend to treat the baby, and how you intend to nourish it, and grow it, so that the original “parents” can be proud as the baby grows up.

Early on in Google’s

ascendancy, Steve Ballmer

of Microsoft made his

disdain for the search

giant known, up to and

including discounting its

very status as a company.

“Google’s not a real company. It’s a house of cards.”

40Copyright © 2017 Aquaa Partners Limited.

All Rights Reserved.

MISTAKE # 5 – NOT PAYING ENOUGH ATTENTION TO “PEOPLE”

Of course “technology” is about “technology”.

But technology is also about people. Technology does not exist without people. People create technology. Technology doesn’t create technology…at least not yet.

If people create technology, and people form a company around the technology, then when one acquires that company it is not just acquiring the technology, it is acquiring the people that are intimately involved and intertwined with that technology.

Perhaps one the main reasons that technology acquisitions go wrong is not because of “overpaying” on price, but rather because of “underpaying” on people.

41Copyright © 2017 Aquaa Partners Limited.

All Rights Reserved.

When an acquirer underpays on people, or gets the culture fit wrong, then the target company starts to bleed. First it bleeds people, then it bleeds fans and customers, and then it bleeds product quality. When a technology begins to bleed on product quality, then that is the beginning of the end. This is the point at which everyone begins saying it was a “bad deal” and “that deal should never have been done” and the most famous of all, “they overpaid”.

“We have not seen a direct effect [from Airbnb] in any of our hotels … We don’t feel it’s having any impact on our

results or that it has hit our radar

as of yet,”

said Richard Jones,

senior VP and COO

of Hospitality Ventures

Management Group, in

2014.

Stan Shih of Acer claimed that Apple’s foray

into computers was an aberration and that the

company would fail to make a niche for itself:

“Apple is like a mutant virus, escaping from the traditional structure of the PC industry,

but the industry will still eventually build up immunity, thus further blocking this

trend, and we believe the size of the non-Apple camp will exceed Apple’s, because

this is how the industry normally evolves.”

43Copyright © 2017 Aquaa Partners Limited.

All Rights Reserved.

tHe GooD neWs – tHeRe Is A sCIenCe to ACQUIRInG A teCHnoLoGY CoMPAnY

There is a solution to many of these challenges. It involves convert-ing the art of acquiring a technology company into a science – a science we call TechquisitionTM.

There are 12 essential steps to the TechquisitionTM method of tech-nology company acquisition. These steps – when properly executed – will help any acquirer to create and retain maximum value from a technology company acquisition.

Described below in brief are the 12 steps of the TechquisitionTM method, which a prospective acquirer can deploy to acquire the right tech company to create more value, guard against disruption and enhance the customer experience:

In 1876, Western Union

Telegraph company

was offered the chance

to purchase the patent

on Alexander Graham

Bell’s telephone. William

Orton, President of

Western Union, failed to

see the value of the newly

invented device:

“What use could this company make of an

electrical toy?”

5.

44Copyright © 2017 Aquaa Partners Limited.

All Rights Reserved.

1. QUALIFY – In the initial and critically important step of TechquisitionTM – “Qualify” – you will want to thoroughly assess and sense check your strategic imperatives against the industry and market trends, the competitive environment and your positioning in it, the capabilities you need, cus-tomer demands and the evolving technological landscape. Take the time to review your board’s decision and specifi-cations to acquire a technology company; ideally you will confirm the consensus opinion and specifications via a third party adviser.

2. SEARCH – In step 2, “Search”, you will want to undertake a comprehensive global search to identify all the potential available target companies in the world that fit the speci-fication determined in the Qualify phase. Leave no stone unturned. Assume nothing. Use every resource available. Saving nickels and dimes in the Search step can cost you millions in the end, particularly if you acquired a company that was less than the ideal company because you didn’t find the company that you should have acquired. Your perfect target is out there. Find it.

3. DIAGNOSE – In step 3 of TechquisitionTM – “Diagnose” – you should review and analyze the candidate target com-panies identified in the Search phase against a long list of criteria, including company size, profitability, growth, geog-raphy, competitive positioning, quality of product/solution, protected IP, scalability of the IP, potential fit (strategic and operational), management team, likely valuation range, shareholding, relationships with your networks and your advisers’ networks, etc. Don’t assume too much or discount companies too early in the Diagnose step – you don’t know what you don’t know, until you start making calls and get-ting the real scoop.

4. TARGET – In step 4 – “Target” – you will want to review and discuss the target companies from the Diagnose phase, assessing not only the traditional “pros” and “cons”, but also critically asking the questions internally of each candidate target company “What makes this target company special? What makes it special for us? Why? How well does it fit into our ecosystem?” If you’re not sure of the answers to these

45Copyright © 2017 Aquaa Partners Limited.

All Rights Reserved.

questions then go get the answers – make the calls you need to make to collect the intel you need to inject into the dis-cussion. Once you’re satisfied that you have the answers you need to the critical questions above, then rank and prioritise the target companies. Create a shortlist of the most appropri-ate companies to contact in the next step.

5. CONTACT – Step 5 – “Contact” – is when TechquisitionTM starts to get interesting. For each candidate identified as a priority target in the Target step you will want to create a bespoke script (the Chalk TalkTM script), based on what was determined as “special” about the target from the Target phase. This is when you can start to leverage your network and your advisers’ networks of relationships to contact the right people at the target company and articulate the oppor-tunity to them via the Chalk TalkTM script. If you get trac-tion with the target company then you’ll want to arrange for NDAs to be signed and obtain additional critical informa-tion on the target company.

6. ENGAGE – Step 6 of TechquisitionTM – “Engage” – is when the process starts to get real. This is when you start to spend serious time and money on the project, which is why Step 1 (Qualify) is so important.

(Unless you are from Step 1 committed to achieving a suc-cessful, game-changing result from TechquisitionTM then there is little point going through the “expensive” Engage phase – it would be like paying for a joy ride in a private jet rather than paying to go in that jet from point A to point B as quickly and as productively as possible).

In the Engage step, after having further qualified the target company from the Contact step, begin a dialogue between your management team and the target company manage-ment / founders and/or shareholders. Your best line (vs staff) executives should lead the discussions, if possible. Identify the target’s key staff early (which often will not include the CEO) and build a relationship with them. This is the stage at which the “culture check” begins. Initial meetings can be informal, but craft a specific agenda for more formal meet-ings between the key staff of the target company and your

Daryl Zanuck,

co-founder of 20th

Century Fox thought that

the TV itself wouldn’t

catch on:

“Television won’t be able to hold

onto any market it captures after the first six months. People will soon

get tired of staring at a plywood box

every night.”

46Copyright © 2017 Aquaa Partners Limited.

All Rights Reserved.

management. Ensure that you are still engaging simultane-ously with several target companies from the shortlist in the Target phase as “beggars can’t be choosers” – ie sometimes no matter what you do, even after increasing the price, you can’t get what you want, so you have to decide if you can still get what you need. Keep more than one door open.

7. VALUE ASSESS – Step 7 of TechquisitionTM – “Value Assess” – is when you start to seriously consider making an offer for the target company. After the initial meeting(s) with the target company and further qualification after each meeting or call during the Engage phase, you can then pre-pare an indicative valuation of the target company, including its IP and talent assets, and also an analysis of the strategic fit, including the pros and cons of a transaction, a risk anal-ysis and the risk mitigation actions. Note that fast-growing innovative companies attract a crowd and can be snapped up quickly by other bidders. Lead from the front; don’t find out the bad news the hard way.

8. VALUE RETAIN – Many acquirers focus early in the process

47Copyright © 2017 Aquaa Partners Limited.

All Rights Reserved.

on the value they can “get” rather than the value they can “retain” after the acquisition is complete. This would be a mistake. Step 8 of TechquisitionTM – “Value Retain” – aims to eliminate this problem. Assuming a target company still qualifies for a formal acquisition approach after the “Value Assess” step, the culture fit decision must be made. Often it’s “no fit, no deal”. With tech companies culture can be everything.

Beyond assessing culture fit you can qualify and confirm four additional key success factors to achieve a “Bleed-FreeTM” acquisition:

(a) can the target’s key talent be retained and if so how?

(b) can full ownership of the target’s IP be secured and can all IP rights be protected?

(c) will the target’s customers genuinely be happy with this acquisition (why and, specifically, how?) and

(d) will our customers genuinely be happy with this acquisi-tion (why and, specifically, how?)

9. OFFER – Getting to this step 9 – “Offer” – can take a lot of time and effort (as steps 1-8 of TechquisitionTM do require time and effort). But it is worth it. Based on (a) the outcome from the “Value Assess” and “Value Retain” phases, (b) any timing constraints you and the target company might be fac-ing, and (c) your available alternatives to acquiring the target that meet the specs (from the Qualify phase), you can now draft the conditional offer to be made to the shareholders of the target company.

Ensure that the offer leads with a thorough articulation of what has inspired your approach to the target company. This is critically important, because the vendor(s) often form a view on your offer and decide for several different reasons, not just “money”. The decision makers are human, not robots, and humans are emotional beings, so make the emotion count. Use emotion to your advantage. If you are motivated and sincere, and note that a modification of the original Chalk TalkTM might still apply here, then you will

48Copyright © 2017 Aquaa Partners Limited.

All Rights Reserved.

be welcomed with open ears. Include why you are so excited about the business combination and the strategic fit as well as the benefits you see for the target company stakehold-ers. Remember in tech company acquisitions the “why” can often matter more than the “price”.

10. AGREE – Negotiation is the essence of step 10 of TechquisitionTM – “Agree”. We believe it is by far best to make your offer during a physical face to face meeting with the vendor(s), but we know this is not always possible. So, if your offer is not made during a meeting with the target com-pany, then after sharing your offer with the target (usually via email and/or video conference or conference call), then plan a meeting (which does not need to be called a “negotiation” meeting) regardless of the target company’s response to your offer. You’ve made it this far, so be sure to keep talking, and realize that there is almost always more than one way to skin a cat.

Before your meeting, or otherwise during the meeting, above all seek first to understand, imparting as much “pre-suasion” as possible before you enter detailed discussions. (Note that agents can be quite helpful here). Negotiation of a tech com-pany acquisition is all about agreeing the package of value and terms, not just about agreeing the “price”. Price is just one of many terms, and many of them can be as equally important as “price”. Negotiate with power first and fore-most. Always start with power. Default to creativity if nec-essary as a supplementary or supporting mechanism. Most negotiators start with reason, but we advise using reason only as a last resort, and only if you are certain it will help.

11. CLOSE – After you have negotiated the terms and formally agreed the package of terms (via a binding Letter of Intent or Heads of Terms etc that includes exclusivity arrangements), then you have entered step 11 of Techqui-sitionTM – “Close”. To close the transaction you will want to initiate confirmatory due diligence and documentation of the final definitive agreements.

Many executives forget to ensure well in advance of the Offer step that all their supporting team members (ie your

“…..Every company will

need to become a technology company.”

– Mark Raskino and

Graham Waller, Gartner

Group

49Copyright © 2017 Aquaa Partners Limited.

All Rights Reserved.

advisers) are in place to support you in the Agree and Close phases as appropriate. Preparation is everything. Your advis-ers include financial advisers, legal, accounting, commercial, tax, insurance and PR advisers. Regarding announcements, ensure that any deal announcement (which often happens at the Agree phase) is discussed and agreed by both you and the target company to avoid disagreements and misunderstand-ings before you have even closed the transaction. In fact this is a good proxy for how to operate and manage expectations going forward in the merged companies – communicate early and often. Whenever in doubt, communicate.

12. LEVERAGE – So after 11 well-earned steps of Tech-quistionTM the deal is finally closed. But does that mean your job is complete? No, the post-completion action plan of a tech company acquisition is critical to remaining Bleed-FreeTM and to creating shareholder value, particularly for the first 100 days and particularly for those targets that you intend to integrate with your core operations. Step 12 of TechquisitionTM – “Leverage” – is when it all comes together.

The subject of “People” might not have been the most import-ant value element during the first 11 steps, but it certainly is among the most important value elements post-completion. You’ll want to ensure early on in the process (usually by the Offer phase) that you have the proper post-completion sup-porting mechanisms in place. Usually the most effective of these mechanisms is employing a specialist post-completion consultant, particularly one that has a very strong compe-tency in “People” and IP and significant experience in tech company acquisitions. Leverage this consultant, as well as the selected staff on your team and the key staff at the target to make the magic happen.

Successfully completing the essential 12 steps of TechquisitionTM can deliver an acquisition that can transform the acquirer’s busi-ness and protect and create shareholder value. In many cases it can convert a company from a “disruptee” to becoming a “disruptor”.

The TechquisitionTM method can be a bit overwhelming to achieve as an organisation. However the result for the acquirer can be

50Copyright © 2017 Aquaa Partners Limited.

All Rights Reserved.

truly phenomenal and is worth it. Creating exceptional results and growth like this is why leaders are in business.

The truth is most companies need a partner or adviser to help them with the TechquisitionTM process, whether it’s us or someone else.

If you’d like to know more about how to use the TechquisitionTM method then reach out to us directly at [email protected]. We’ll be happy to help.

Remember, every company is going digital now. Bold companies confident of controlling their future are acquiring technology com-panies. Get it right. Use the TechquisitionTM method.

Your board and shareholders expect it.

51Copyright © 2017 Aquaa Partners Limited.

All Rights Reserved.

1-6 Yarmouth Place, London W1J 7BUTel : +44 203 725 6451 . Fax : +44 203 170 8101

Authorised and Regulated by the Financial Services Authority

“We enable growth-focused companies to create more value and guard against disruption by

acquiring the right tech companies.”

www.aquaapartners.com

Related Documents