Takeover cases • 1

Takeover cases 1. Unocal Corporation v. Mesa Petroleum Co. 493 A.2d 946(Del.1985).

Dec 15, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Takeover cases

• 1

Unocal Corporation v. Mesa Petroleum Unocal Corporation v. Mesa Petroleum Co.Co.

493 A.2d 946(Del.1985).493 A.2d 946(Del.1985).

Unocal Corporation v. Mesa Petroleum Unocal Corporation v. Mesa Petroleum Co.Co.

493 A.2d 946(Del.1985).493 A.2d 946(Del.1985).

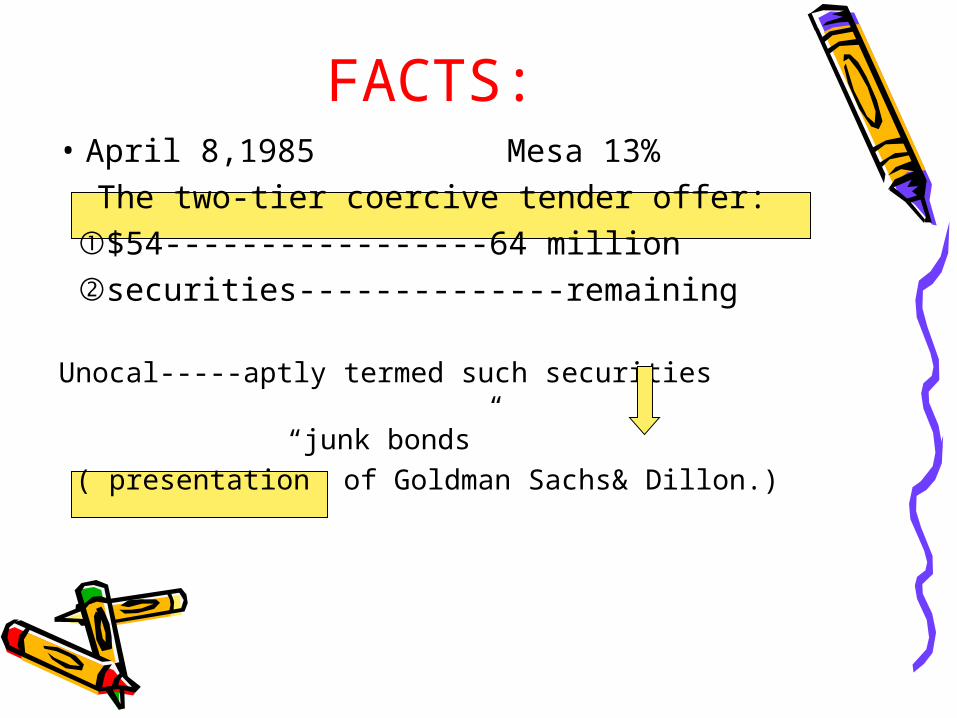

FACTS:• April 8,1985 Mesa 13% The two-tier coercive tender offer: ①$54-----------------64 million ②securities--------------remaining

Unocal-----aptly termed such securities “junk bonds”

( presentation of Goldman Sachs& Dillon.)

The Court of Chancery:• the Sachs presentation was designed to

apprise the directors of the scope of the analyses performed rather than the facts and numbers used in reaching the conclusion that Mesa’s tender offer price was inadequate.

• • BOD not informed

Defensive measure

April 15 $72 ----remaining 49%

1. Mesa Purchase Condition 64M purchased by Mesa----50M

2. Mesa Exclusion Mesa can not tender to Unocal

Injunction

FUNDAMENTAL ISSUES

1. Did the Unocal board have the power and duty to take a defensive measure to oppose a takeover threat?

2. Is its action here entitled to the protection of the business judgment rule?

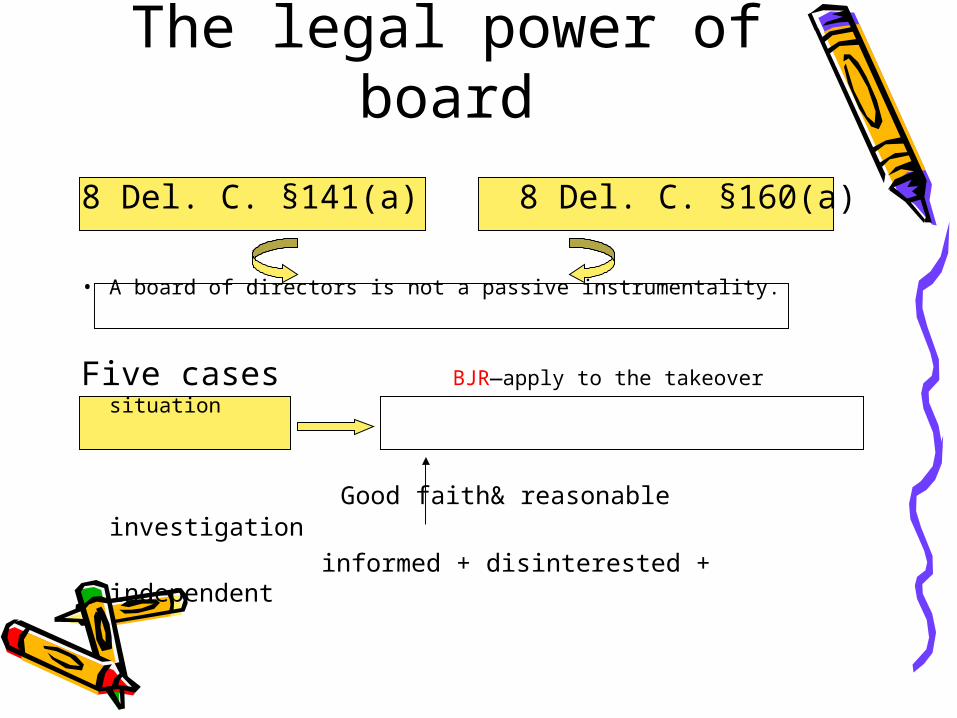

The legal power of board

8 Del. C. §141(a) 8 Del. C. §160(a)

• A board of directors is not a passive instrumentality.

Five cases BJR—apply to the takeover situation

Good faith& reasonable investigation

informed + disinterested + independent

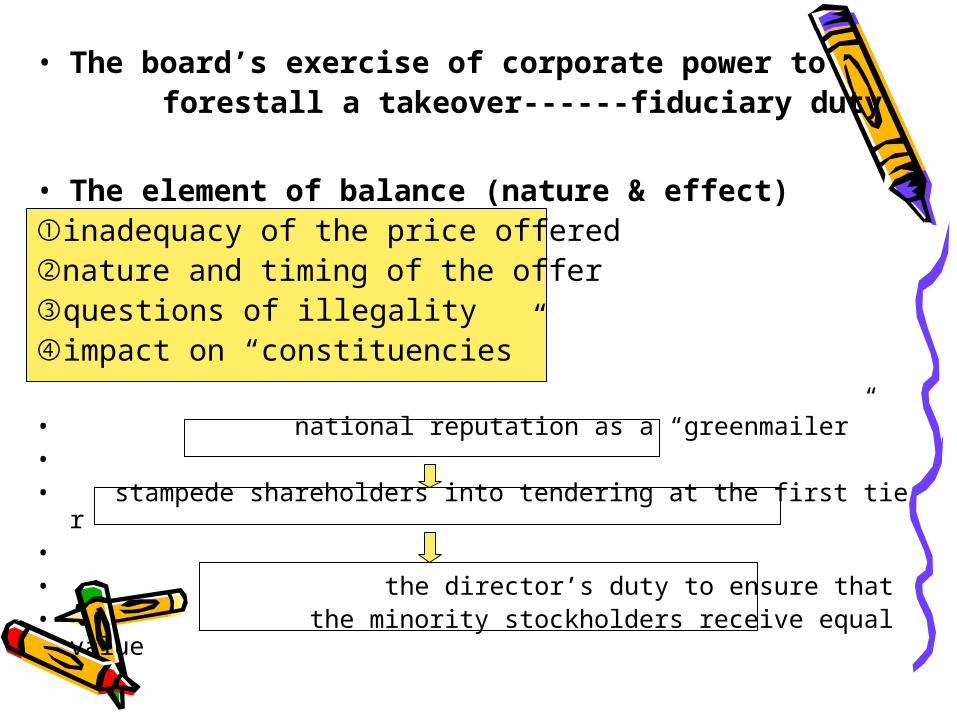

• The board’s exercise of corporate power to forestall a takeover------fiduciary duty.

• The element of balance (nature & effect)①inadequacy of the price offered②nature and timing of the offer③questions of illegality④impact on “constituencies”

• national reputation as a “greenmailer”• • stampede shareholders into tendering at the first tier• • the director’s duty to ensure that• the minority stockholders receive equal value

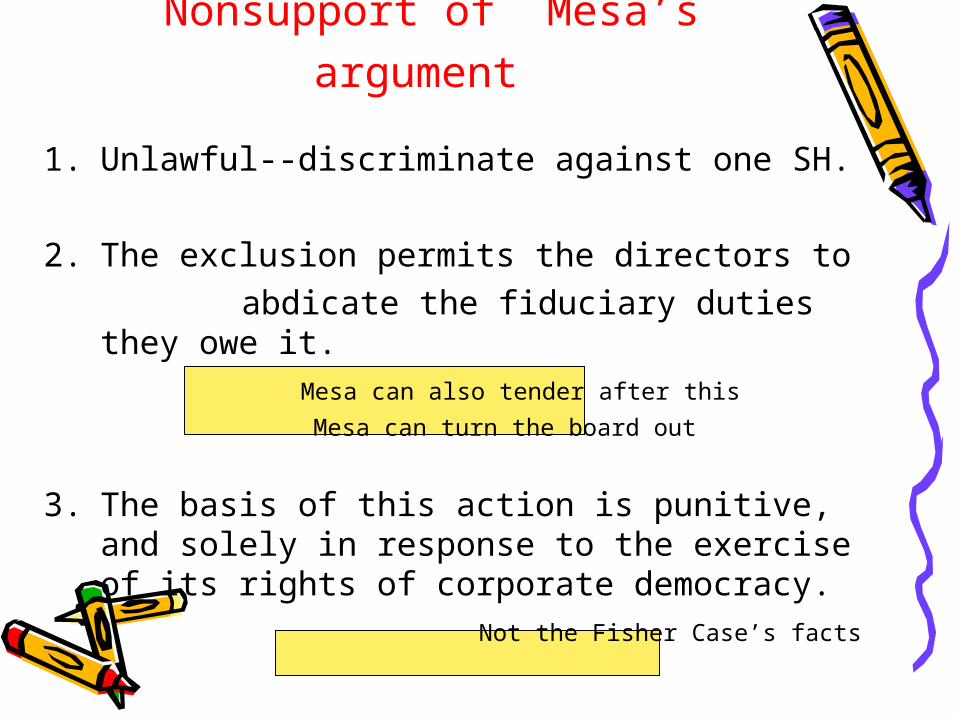

Nonsupport of Mesa’s argument

1. Unlawful--discriminate against one SH. 2. The exclusion permits the directors to abdicate the fiduciary duties they owe

it. Mesa can also tender after this

Mesa can turn the board out

3. The basis of this action is punitive, and solely in response to the exercise of its rights of corporate democracy.

Not the Fisher Case’s facts

The Result • There was a directorial power to oppose the

Mesa tender offer.• The selective stock repurchase plan chosen

by Unocal is rational & reasonable. • The board’s action is entitled to the protec

tion of the BJR.

The decision of the Court of Chancery:REVERSEDThe preliminary injunction:VACATED

ATTENTION:

The reasoning of common law.

The compare of the facts in the proceed of reasoning.

Takeover cases

• 2

Revlon Revlon CaseCase

Revlon Revlon CaseCase

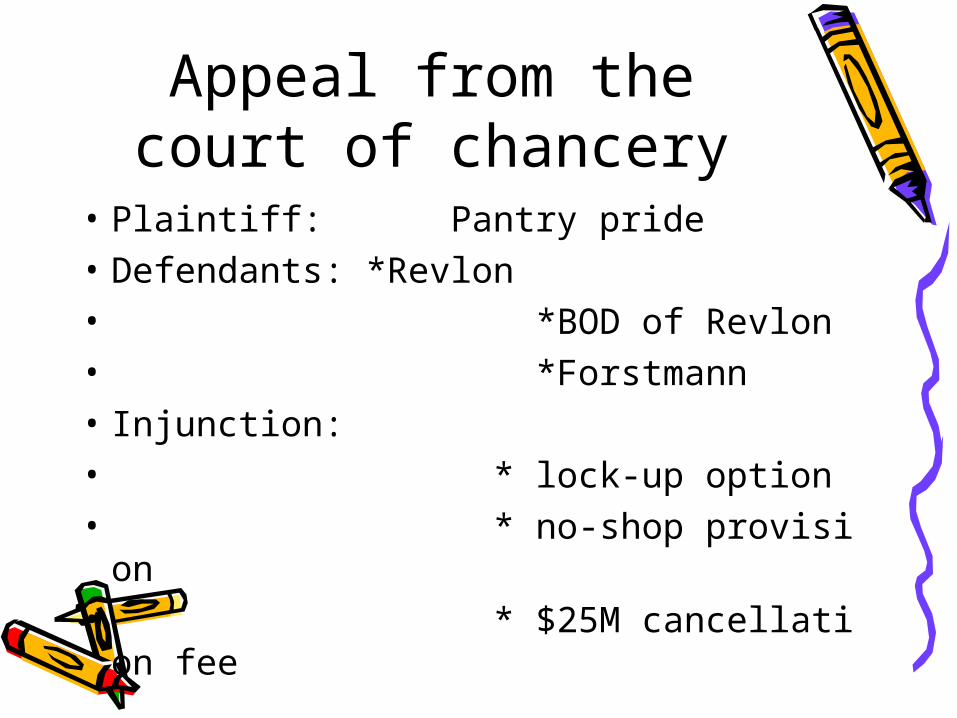

Appeal from the court of chancery

• Plaintiff: Pantry pride• Defendants: *Revlon• *BOD of Revlon• *Forstmann• Injunction: • * lock-up option• * no-shop provision• * $25M cancellation fee

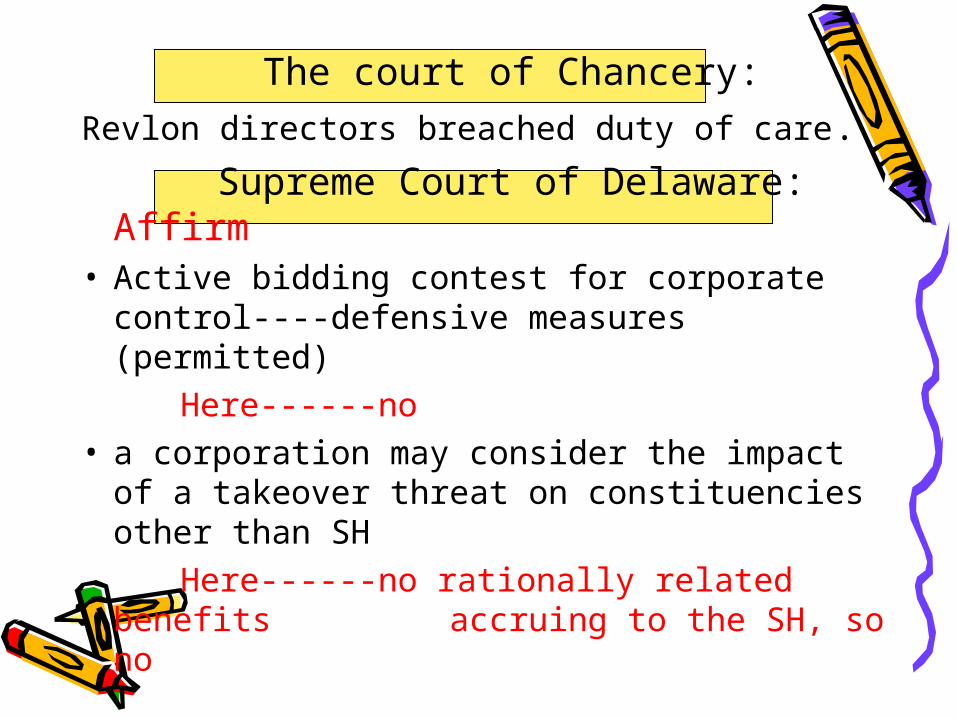

The court of Chancery:Revlon directors breached duty of care. Supreme Court of Delaware:

Affirm• Active bidding contest for corporate

control----defensive measures (permitted) Here------no• a corporation may consider the impact of

a takeover threat on constituencies other than SH

Here------no rationally related benefits accruing to the SH, so no

Facts:• June 1985 $40-50• Mr. Perelman Mr. Bergerac• Pantry Pride Revlon (NO)

• August 141. Negotiation: $42-$43 per S.2. Hostile tender offer: $45

Defensive measures

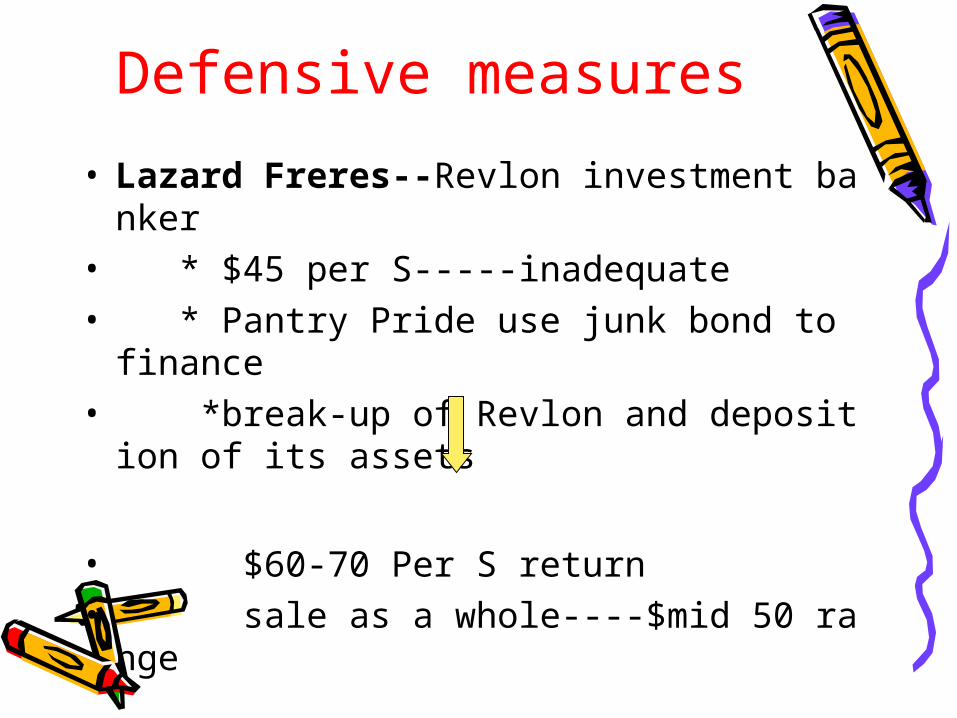

• Lazard Freres--Revlon investment banker• * $45 per S-----inadequate• * Pantry Pride use junk bond to finance• *break-up of Revlon and deposition of its

assets

• $60-70 Per S return• sale as a whole----$mid 50 range

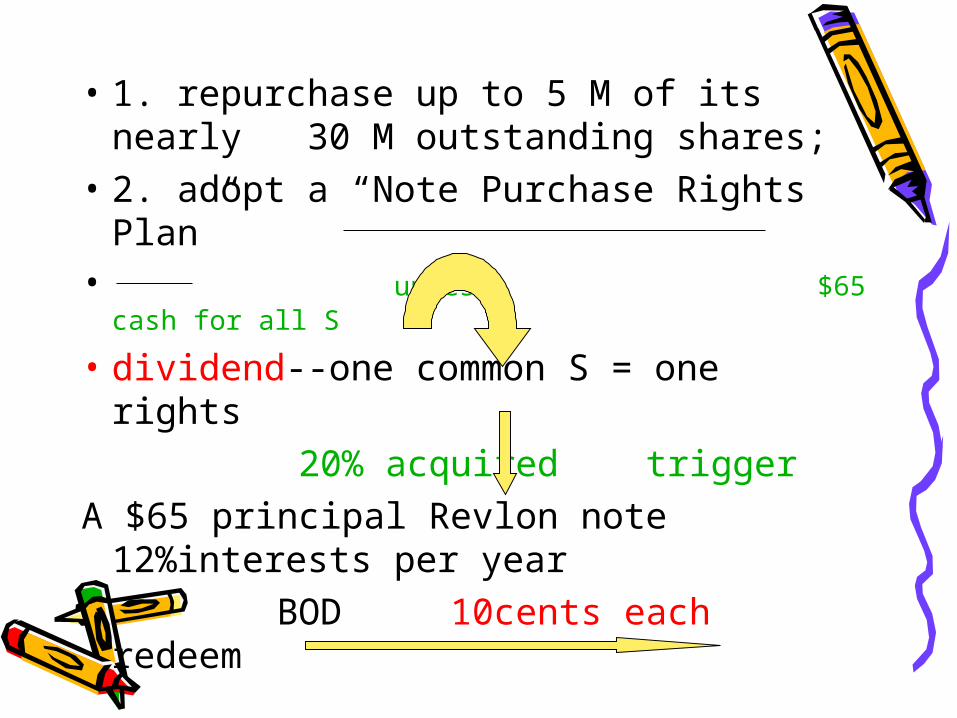

• 1. repurchase up to 5 M of its nearly 30 M outstanding shares;

• 2. adopt a “Note Purchase Rights Plan”

• unless $65 cash for all S

• dividend--one common S = one rights 20% acquired triggerA $65 principal Revlon note

12%interests per year BOD 10cents each redeem

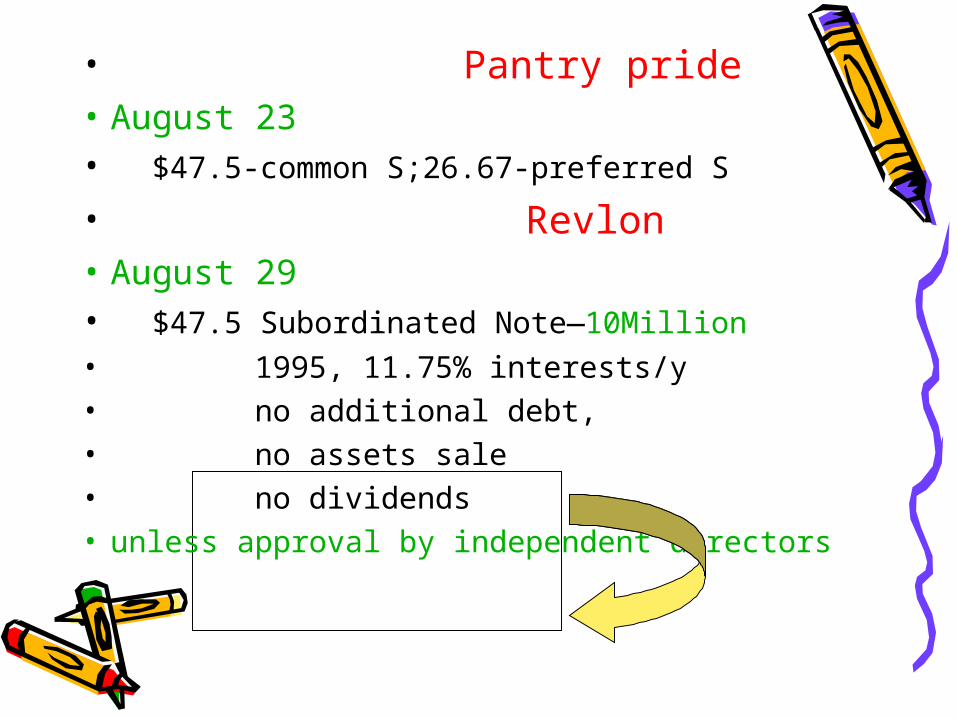

• Pantry pride• August 23• $47.5-common S;26.67-preferred S

• Revlon• August 29• $47.5 Subordinated Note—10Million• 1995, 11.75% interests/y• no additional debt,• no assets sale• no dividends • unless approval by independent directors

• Pantry pride• Sept. 16 second cash bid----$42• increase price if no “rights”• Sept.27 $50• Oct.1 $53• Oct.7 $56.25• • Revlon BOD reject all its offers.• Leverage buyout by Forstmann.

• Revlon SH--$56 cash• waive the Notes covenants • Finance by:• Revlon “golden parachutes”• sell cosmetics and fragrance division for $9

05M • Forstmann assume $475M debts—sell Revl

on’s two divisions for $335M

• Notes from par value$100--$87.5• noteholders----threat to suit

Forstmann’s privileges:1. Access to certain Revlon financial data;2. lock-up option: purchase one divisions for $525M which is $100-175M belo

w its value if other acquiror get 40% of Revlon’s shares;

3. Rights and Notes covenants ---removed4. No-shop provision5. Cancellation fee $25M to be placed in escrow if this agreement terminated o

r if another acquiror get 19.9% of Revlon’s shares. $57.5

No Revlon management involved support the par value of the Notes

Revlon BOD’s reasons:

1. Higher price than the Pantry Pride bid;2. Protect the noteholders;3. Forstmann’s financing was firmly in

place.

should consider time value of moneyNo

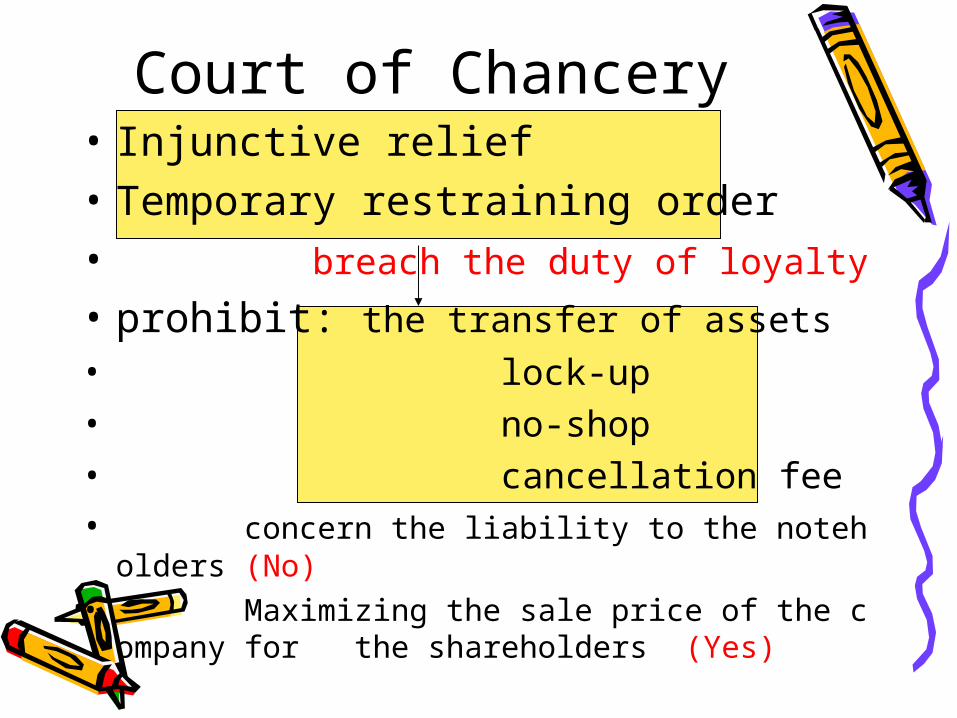

Court of Chancery• Injunctive relief• Temporary restraining order• breach the duty of loyalty • prohibit: the transfer of assets• lock-up• no-shop• cancellation fee• concern the liability to the noteholders (No)• Maximizing the sale price of the company for t

he shareholders (Yes)

Regarding the preliminary injunction

• 1. Plaintiff must demonstrate a reasonable probability of success on the merits;

• 2.some irreparable harm would occur if absent the injuntion.

recognition

Change to

BOD role• Defenders auctioneers

• no Unocal test here

Preservation of Revlon as a corporate entity

Revlon board negotiate a merger or buyout with Forstmann

Revlon for sale

Maximize the company value at a sale for SH benefits

Lock-up• Legal under Delaware Law

• Citing Thompson V. Enstar Corp.

1. Some lock-up options may be beneficial to the SH

Such as those that induce a bidder to compete for the control of a corporation

2. Some may be harmful Such as those that effectively preclude the bidders from co

mpeting with the optionee bidder

Not to foster bidding----but destroy it(here, illegal)

• Preferring the noteholders

• Ignoring the duty of loyalty to the SH intent

•At the expense of the SH

rights of noteholders were fixed by contract, need no further protection

protect the directors against a perceived litigation threat from the creditors

No-shop provision• Like the lock-up, not per se illegal.

• Impermissible under the Unocal standards when a board’s primary duty becomes that of an auctioneer responsible for selling the company to the highest bidder.

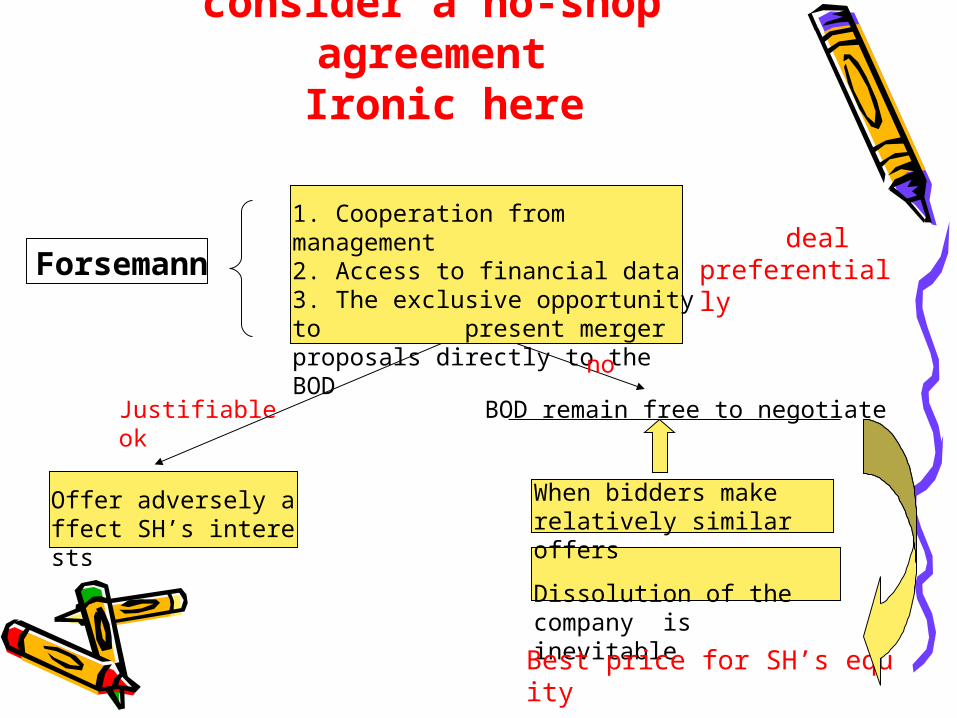

consider a no-shop agreement Ironic here

1. Cooperation from management2. Access to financial data3. The exclusive opportunity to present merger proposals directly to the BOD

Offer adversely affect SH’s interests

Justifiable ok

When bidders make relatively similar offers

Dissolution of the company is inevitable

BOD remain free to negotiate

deal preferentiallyForsemann

Best price for SH’s equity

no

Takeover cases

• 3

Paramount v. Paramount v. TimeTime

Paramount v. Paramount v. TimeTime

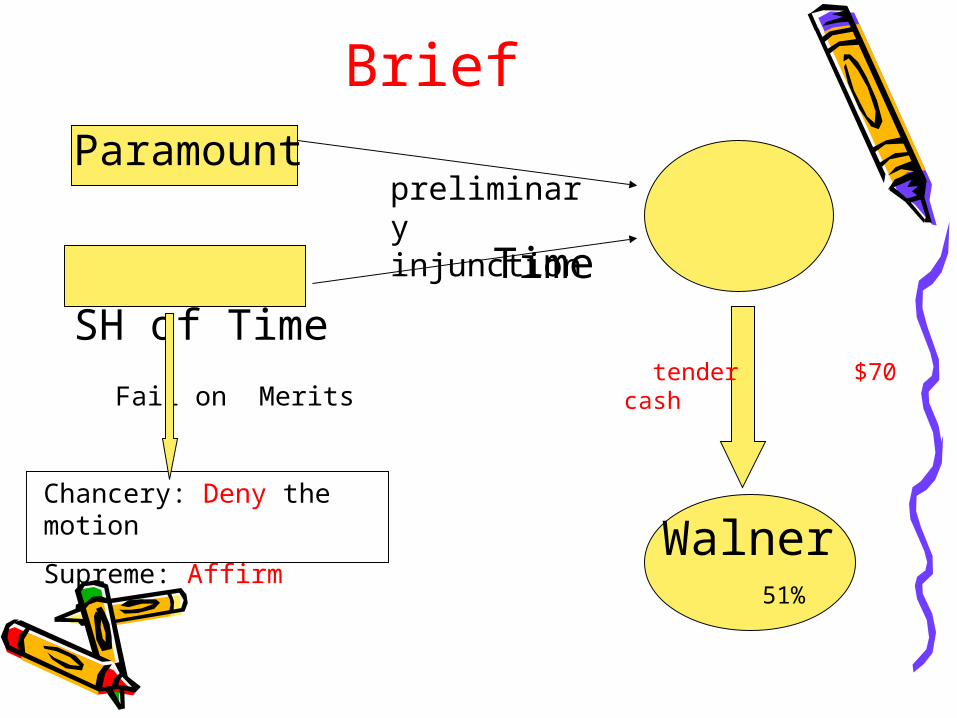

BriefParamount TimeSH of Time

preliminary injunction

Walner 51%

tender $70 cash Fail on Merits

Chancery: Deny the motion

Supreme: Affirm

Two important facts

Time

outside directors

Inside Directors

4

8

Henry R. Luce III

dominated by

(1) (2) Since 1983-1989

considerable time study the merger

Warner

Best fit

Time control

the BOD

Preserve a management culture (journalistic integrity)

Not report to top officer

Report to a committee of BOD

Care Profits (no)

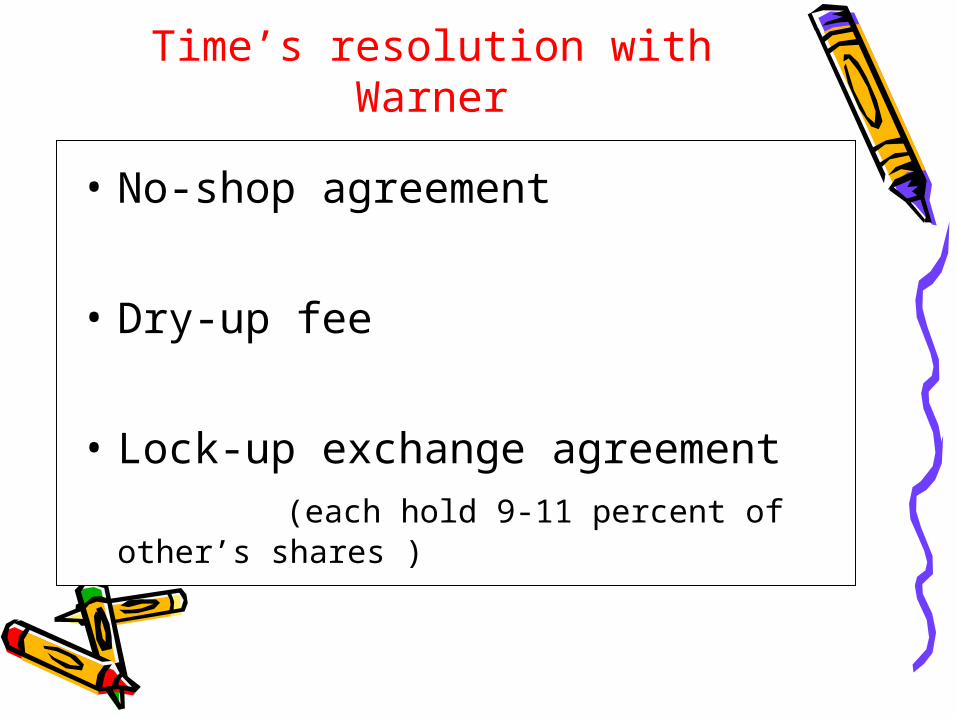

Time’s resolution with Warner

• No-shop agreement

• Dry-up fee

• Lock-up exchange agreement (each hold 9-11 percent of other’s

shares )

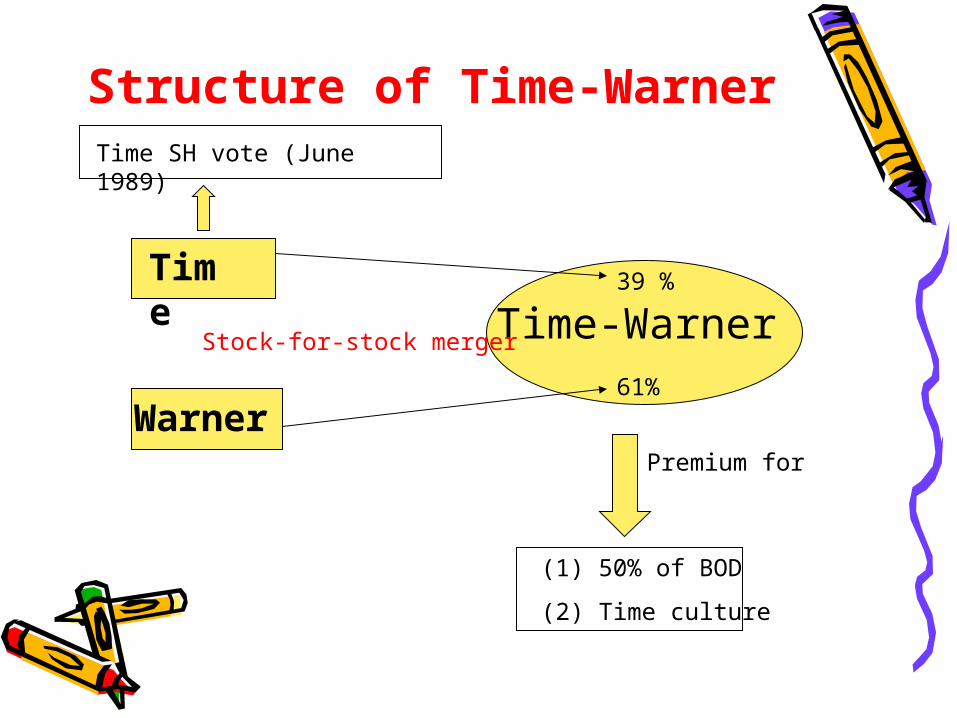

Structure of Time-Warner

Time

Warner

Time-Warner39 %

61%

(1) 50% of BOD

(2) Time culture

Premium for

Time SH vote (June 1989)

Stock-for-stock merger

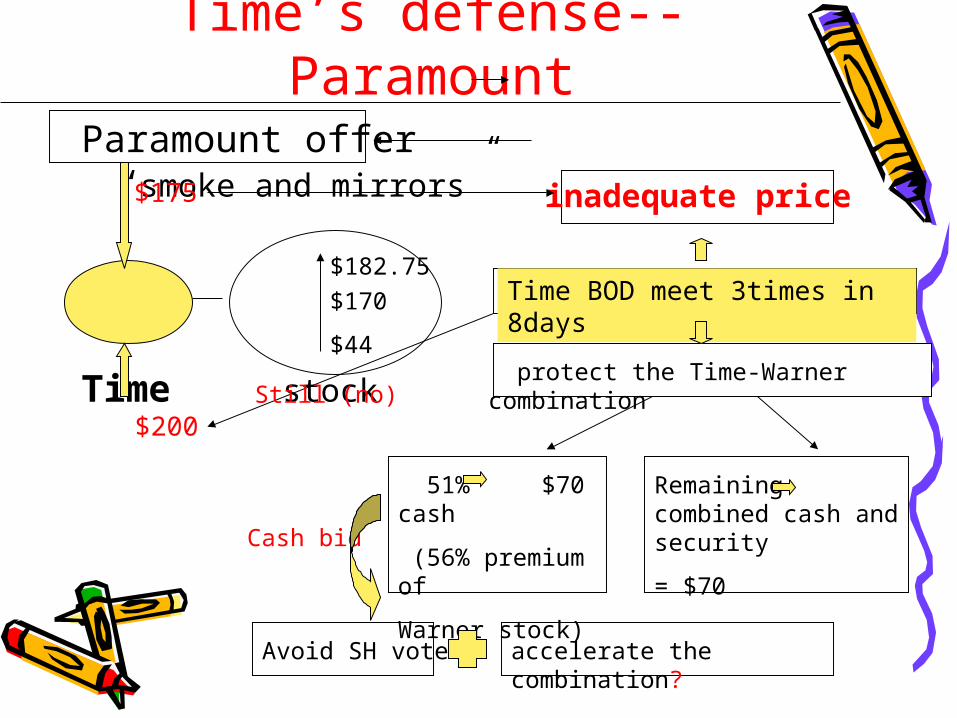

Time’s defense--Paramount

Paramount offer “smoke and mirrors”

Time stock

$182.75$170

$44

$175 inadequate price

Time BOD meet 3times in 8days

protect the Time-Warner combination

$200

51% $70 cash

(56% premium of

Warner stock)

Remaining combined cash and security

= $70

Avoid SH vote

Cash bid

accelerate the combination?

Still (no)

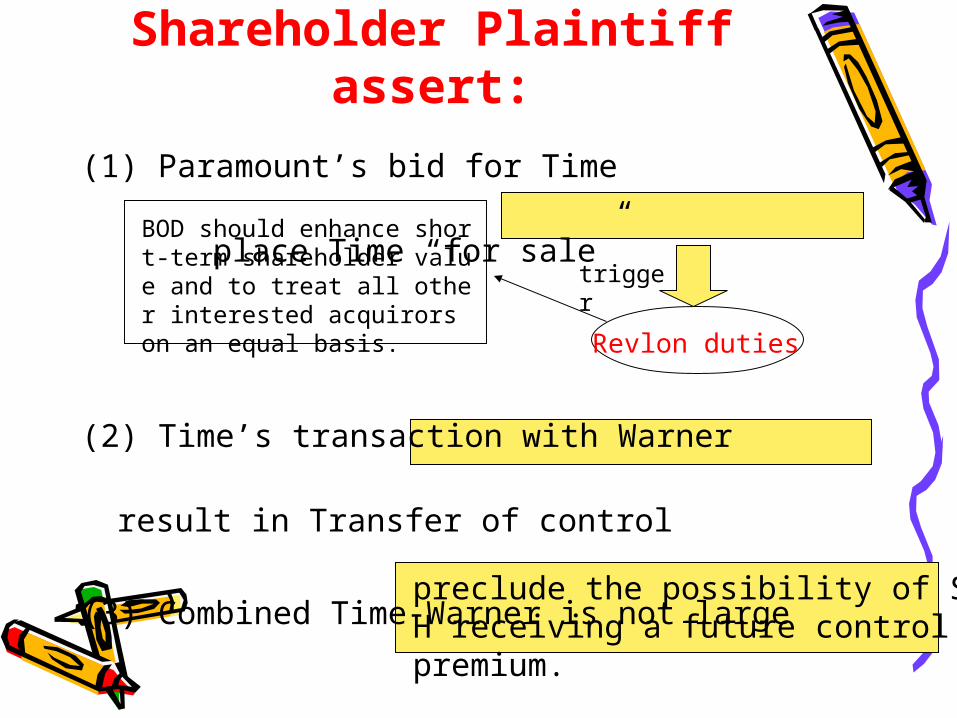

Shareholder Plaintiff assert:

(1) Paramount’s bid for Time place Time “for

sale”

(2) Time’s transaction with Warner result in Transfer of

control

(3) Combined Time-Warner is not large

BOD should enhance short-term shareholder value and to treat all other interested acquirors on an equal basis.

Revlon duties

preclude the possibility of SH receiving a future control premium.

trigger

Chancery and Supreme court:

(1) Del 141(a):

(2) If not under Revlon

BOD has conferred authority to manage corporation business to enhance profitabilityNo fixed investment horizon

Not put the corporation’s future in the hands of its SH

BOD should act in an informed manner

no duty to maximize SH value in the short term

Pivotal Issue: Time—”up for sale”?

No Revlon here:(1) Corporation initiate an active bidding process

seeking to sell or reorganization involving a clear break-up of the company. (here no)

(2) In response to a bidder’s offer, a target abandons its long-term strategy and seeks an alternative transaction also involving the break-up of the company. (here no)

Here: control of the corporation existed in a fluid aggregation of unaffiliated SH

(Control in the Market)

Apply Unocal here:

Safety

devices

Lock-upNo-shopDry-up fee

Not prevent SH from

a control premium

Properly subject to

a Unocal analysis

Merger agreement before Mar.3----BJR okRevised transaction on June 16----Under Unocal

Plaintiff: two-tier offer ---------- threat all cash, all share offer------- no

threat Court: Wrong Unocal

*inadequacy of the price*nature and timing of the offer*questions of illegality*the impact on contingencies other than SH*The risk of nonconsummation *quality of securities

how to

evaluating threat:

Unocal 1: where is the threat

Threat:(1) Paramount’s 11 hour offer upset the SH to

consider the Time-Warner merger vote(2) Paramount offer a degree of uncertainty

BOD informed (1) long time investigation for Warner (2) 12/ 16 are outside directors

Unocal 2: Is this a reasonable defensive action?

Paramount:Assuming threat there, Time’s response was

unreasonable in precluding SH accepting the a control premium.

Court:Directors are not obliged to abandon a

deliberately conceived corporate plan for a short-term SH Profit unless there is clearly no basis to sustain the corporate strategy.

Paramount can still make an offer for the combined Time-Warner

Heavy debts incur to finance the acquisition of Warner----Fine

Related Documents