Taiwan in View

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Taiwan in View

contentsI. The Pay-TV industry data TV Households and the terrestrial TV market 4

The Cable TV market 4

The IPTV market 9

Satellite TV usage 10

Broadband penetration 10

II. The rise of internet TV services Types of OTT (Over The Top) services in Taiwan 13

OTTservicesofferedlegallyinTaiwan 14

Estimation of OTT market size 14

Major players in OTT services 17

Households having access to streaming

TV as compared to cable TV and IPTV 18

III. Business models and market forecasts Prospects for further development and change of

business models in the pay-TV industry 19

Subscriber growth trends for major platforms 19

Growth constraints 21

IV. Programming and pricing Channel programmers and their agents 22

Approvedtariffs 24

Advertising revenues of major media sectors 25

V. Pay-TV Regulatory Environment Regulatory Frameworks 26

Current policy issues 27

VI. The future and challenges for pay-TV services Lack of must-have digital content and applications 30

Copyright and piracy concerns 30

Substitute relationship between pay-TV and OTT services? 30

VII. Appendix List of OTT providers in Taiwan 32

List of pay-TV operators and channels 39

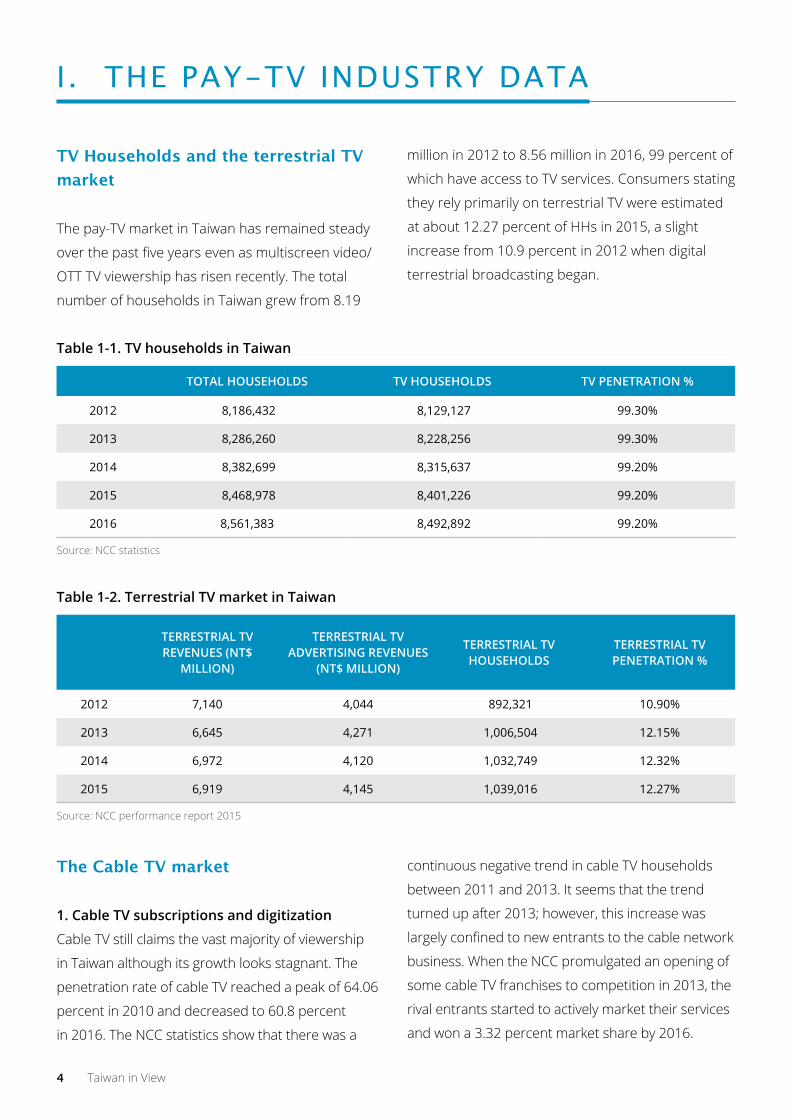

4 Taiwan in View

TV Households and the terrestrial TV market

The pay-TV market in Taiwan has remained steady

over the past five years even as multiscreen video/

OTT TV viewership has risen recently. The total

number of households in Taiwan grew from 8.19

million in 2012 to 8.56 million in 2016, 99 percent of

which have access to TV services. Consumers stating

they rely primarily on terrestrial TV were estimated

at about 12.27 percent of HHs in 2015, a slight

increase from 10.9 percent in 2012 when digital

terrestrial broadcasting began.

I . the Pay-tV Industry data

Table 1-1. TV households in Taiwan

TOTAL HOUSEHOLDS TV HOUSEHOLDS TV PENETRATION %

2012 8,186,432 8,129,127 99.30%

2013 8,286,260 8,228,256 99.30%

2014 8,382,699 8,315,637 99.20%

2015 8,468,978 8,401,226 99.20%

2016 8,561,383 8,492,892 99.20%

Source: NCC statistics

Table 1-2. Terrestrial TV market in Taiwan

TERRESTRIAL TVREVENUES (NT$

MILLION)

TERRESTRIAL TVADVERTISING REVENUES

(NT$ MILLION)

TERRESTRIAL TV HOUSEHOLDS

TERRESTRIAL TV PENETRATION %

2012 7,140 4,044 892,321 10.90%

2013 6,645 4,271 1,006,504 12.15%

2014 6,972 4,120 1,032,749 12.32%

2015 6,919 4,145 1,039,016 12.27%

Source: NCC performance report 2015

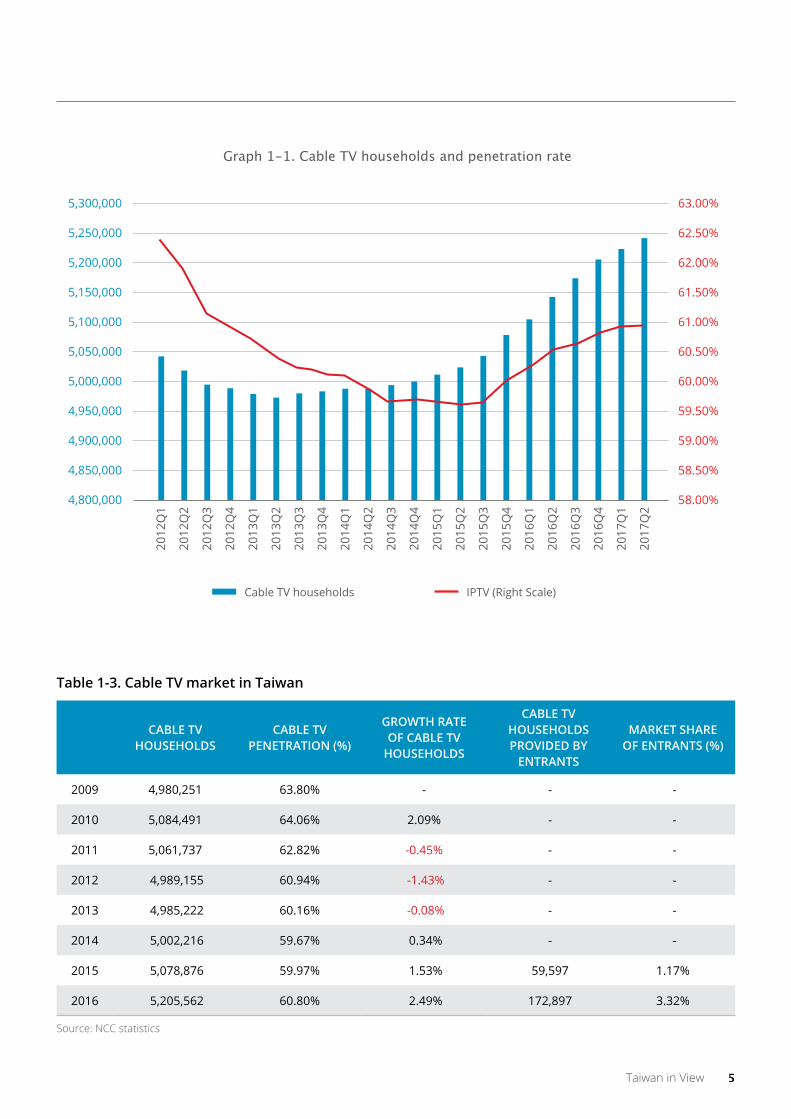

The Cable TV market

1. Cable TV subscriptions and digitization

Cable TV still claims the vast majority of viewership

in Taiwan although its growth looks stagnant. The

penetration rate of cable TV reached a peak of 64.06

percent in 2010 and decreased to 60.8 percent

in 2016. The NCC statistics show that there was a

continuous negative trend in cable TV households

between 2011 and 2013. It seems that the trend

turned up after 2013; however, this increase was

largely confined to new entrants to the cable network

business. When the NCC promulgated an opening of

some cable TV franchises to competition in 2013, the

rival entrants started to actively market their services

and won a 3.32 percent market share by 2016.

Taiwan in View 5

Table 1-3. Cable TV market in Taiwan

CAbLE TV HOUSEHOLDS

CAbLE TV PENETRATION (%)

GROwTH RATE Of CAbLE TV

HOUSEHOLDS

CAbLE TV HOUSEHOLDS PROVIDED by

ENTRANTS

MARkET SHARE Of ENTRANTS (%)

2009 4,980,251 63.80% - - -

2010 5,084,491 64.06% 2.09% - -

2011 5,061,737 62.82% -0.45% - -

2012 4,989,155 60.94% -1.43% - -

2013 4,985,222 60.16% -0.08% - -

2014 5,002,216 59.67% 0.34% - -

2015 5,078,876 59.97% 1.53% 59,597 1.17%

2016 5,205,562 60.80% 2.49% 172,897 3.32%

Source: NCC statistics

5,300,000

5,250,000

5,200,000

5,150,000

5,100,000

5,050,000

5,000,000

4,950,000

4,900,000

4,850,000

4,800,000

63.00%

62.50%

62.00%

61.50%

61.00%

60.50%

60.00%

59.50%

59.00%

58.50%

58.00%

2012

Q1

2012

Q2

2012

Q3

2012

Q4

2013

Q1

2013

Q2

2013

Q3

2013

Q4

2014

Q1

2014

Q2

2014

Q3

2014

Q4

2015

Q1

2015

Q2

2015

Q3

2015

Q4

2016

Q1

2016

Q2

2016

Q3

2016

Q4

2017

Q1

2017

Q2

Cable TV households IPTV (Right Scale)

Graph 1-1. Cable TV households and penetration rate

6 Taiwan in View

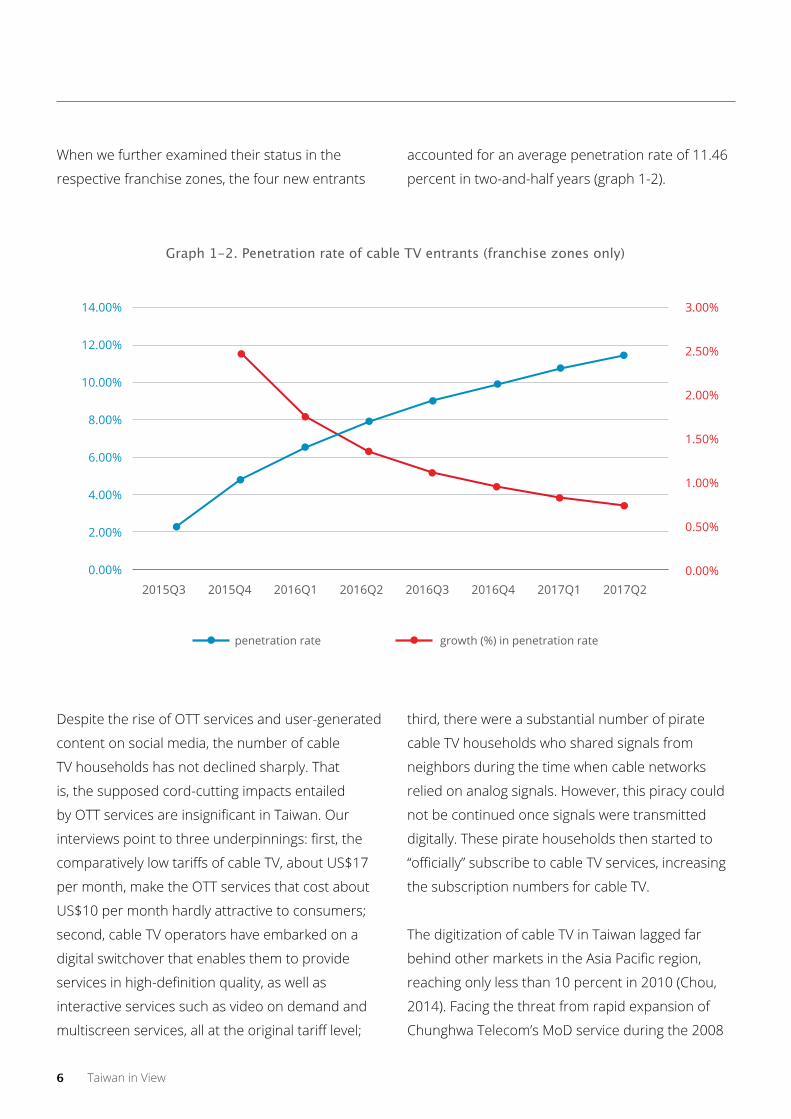

When we further examined their status in the

respective franchise zones, the four new entrants

accounted for an average penetration rate of 11.46

percent in two-and-half years (graph 1-2).

14.00%

12.00%

10.00%

8.00%

6.00%

4.00%

2.00%

0.00%

3.00%

2.50%

2.00%

1.50%

1.00%

0.50%

0.00%2015Q3 2015Q4 2016Q1 2016Q2 2016Q3 2016Q4 2017Q1 2017Q2

penetration rate growth (%) in penetration rate

Graph 1-2. Penetration rate of cable TV entrants (franchise zones only)

Despite the rise of OTT services and user-generated

content on social media, the number of cable

TV households has not declined sharply. That

is, the supposed cord-cutting impacts entailed

by OTT services are insignificant in Taiwan. Our

interviews point to three underpinnings: first, the

comparatively low tariffs of cable TV, about US$17

per month, make the OTT services that cost about

US$10 per month hardly attractive to consumers;

second, cable TV operators have embarked on a

digital switchover that enables them to provide

services in high-definition quality, as well as

interactive services such as video on demand and

multiscreen services, all at the original tariff level;

third, there were a substantial number of pirate

cable TV households who shared signals from

neighbors during the time when cable networks

relied on analog signals. However, this piracy could

not be continued once signals were transmitted

digitally. These pirate households then started to

“officially” subscribe to cable TV services, increasing

the subscription numbers for cable TV.

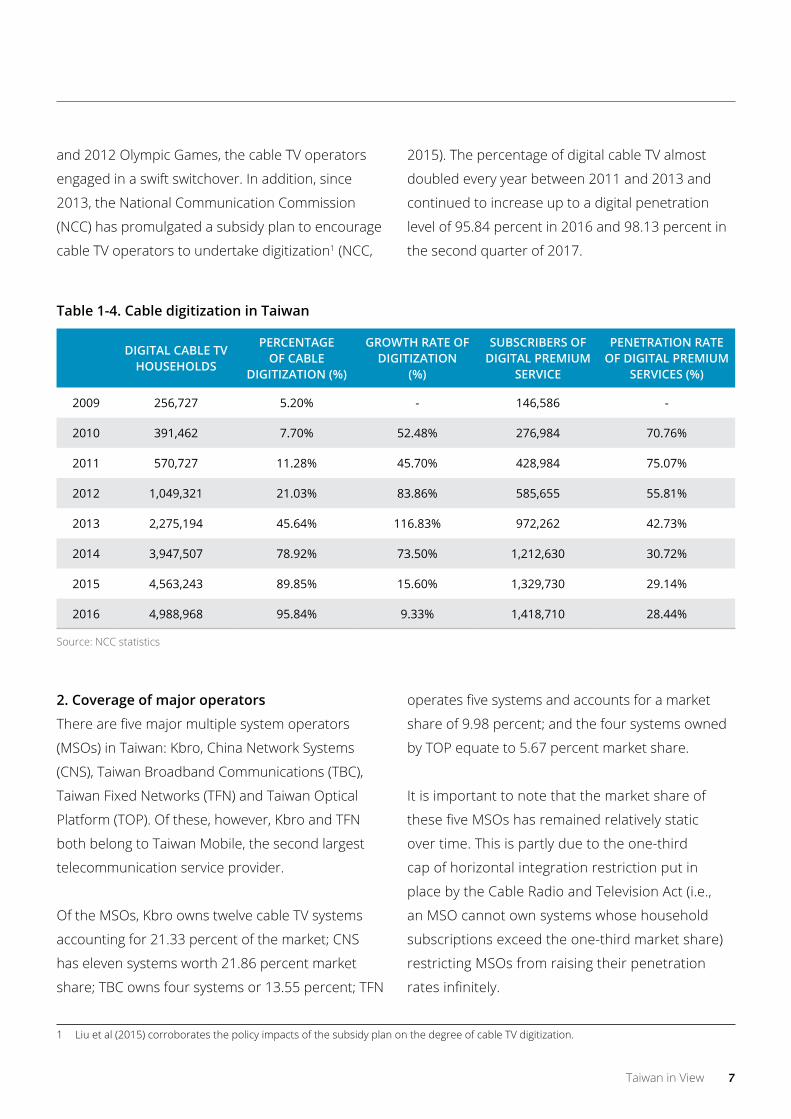

The digitization of cable TV in Taiwan lagged far

behind other markets in the Asia Pacific region,

reaching only less than 10 percent in 2010 (Chou,

2014). Facing the threat from rapid expansion of

Chunghwa Telecom’s MoD service during the 2008

Taiwan in View 7

and 2012 Olympic Games, the cable TV operators

engaged in a swift switchover. In addition, since

2013, the National Communication Commission

(NCC) has promulgated a subsidy plan to encourage

cable TV operators to undertake digitization1 (NCC,

2015). The percentage of digital cable TV almost

doubled every year between 2011 and 2013 and

continued to increase up to a digital penetration

level of 95.84 percent in 2016 and 98.13 percent in

the second quarter of 2017.

Table 1-4. Cable digitization in Taiwan

DIGITAL CAbLE TVHOUSEHOLDS

PERCENTAGE Of CAbLE

DIGITIZATION (%)

GROwTH RATE Of DIGITIZATION

(%)

SUbSCRIbERS Of DIGITAL PREMIUM

SERVICE

PENETRATION RATE Of DIGITAL PREMIUM

SERVICES (%)

2009 256,727 5.20% - 146,586 -

2010 391,462 7.70% 52.48% 276,984 70.76%

2011 570,727 11.28% 45.70% 428,984 75.07%

2012 1,049,321 21.03% 83.86% 585,655 55.81%

2013 2,275,194 45.64% 116.83% 972,262 42.73%

2014 3,947,507 78.92% 73.50% 1,212,630 30.72%

2015 4,563,243 89.85% 15.60% 1,329,730 29.14%

2016 4,988,968 95.84% 9.33% 1,418,710 28.44%

Source: NCC statistics

2. Coverage of major operators

There are five major multiple system operators

(MSOs) in Taiwan: Kbro, China Network Systems

(CNS), Taiwan Broadband Communications (TBC),

Taiwan Fixed Networks (TFN) and Taiwan Optical

Platform (TOP). Of these, however, Kbro and TFN

both belong to Taiwan Mobile, the second largest

telecommunication service provider.

Of the MSOs, Kbro owns twelve cable TV systems

accounting for 21.33 percent of the market; CNS

has eleven systems worth 21.86 percent market

share; TBC owns four systems or 13.55 percent; TFN

operates five systems and accounts for a market

share of 9.98 percent; and the four systems owned

by TOP equate to 5.67 percent market share.

It is important to note that the market share of

these five MSOs has remained relatively static

over time. This is partly due to the one-third

cap of horizontal integration restriction put in

place by the Cable Radio and Television Act (i.e.,

an MSO cannot own systems whose household

subscriptions exceed the one-third market share)

restricting MSOs from raising their penetration

rates infinitely.

1 Liu et al (2015) corroborates the policy impacts of the subsidy plan on the degree of cable TV digitization.

8 Taiwan in View

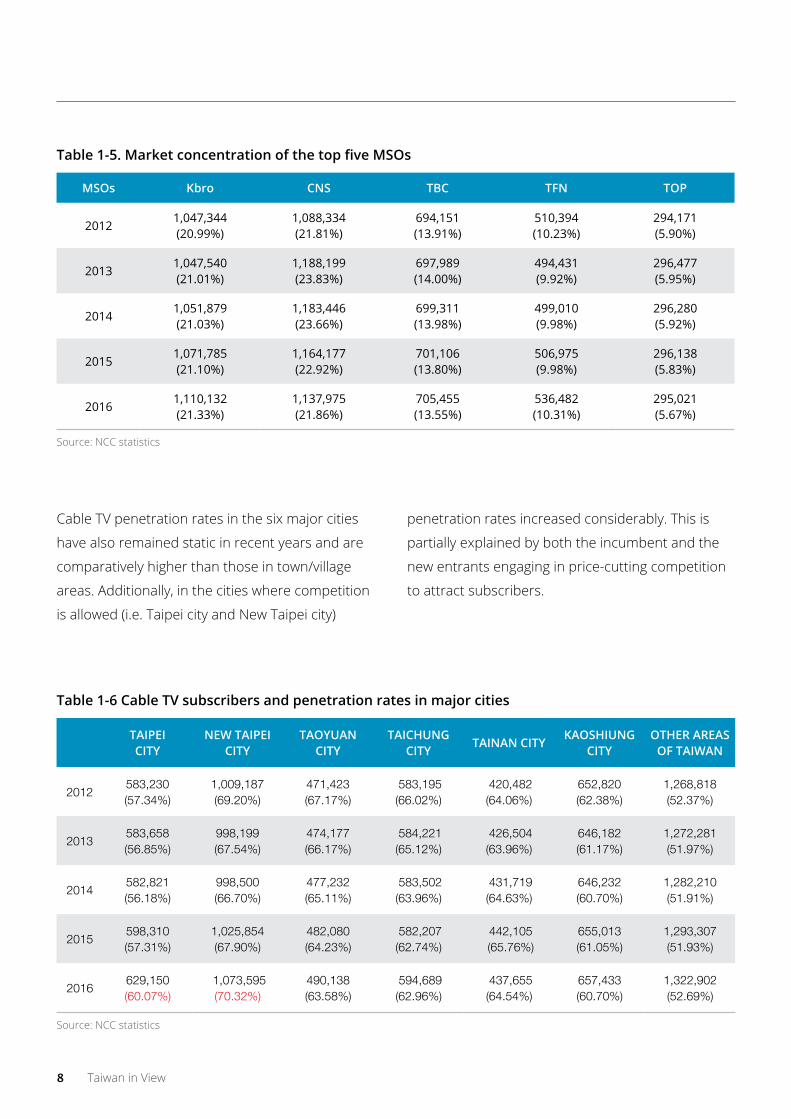

Table 1-5. Market concentration of the top five MSOs

MSOs kbro CNS TbC TfN TOP

20121,047,344 (20.99%)

1,088,334 (21.81%)

694,151 (13.91%)

510,394 (10.23%)

294,171 (5.90%)

20131,047,540(21.01%)

1,188,199 (23.83%)

697,989 (14.00%)

494,431 (9.92%)

296,477 (5.95%)

20141,051,879 (21.03%)

1,183,446 (23.66%)

699,311 (13.98%)

499,010 (9.98%)

296,280 (5.92%)

20151,071,785 (21.10%)

1,164,177 (22.92%)

701,106 (13.80%)

506,975 (9.98%)

296,138 (5.83%)

20161,110,132(21.33%)

1,137,975 (21.86%)

705,455 (13.55%)

536,482 (10.31%)

295,021 (5.67%)

Source: NCC statistics

Cable TV penetration rates in the six major cities

have also remained static in recent years and are

comparatively higher than those in town/village

areas. Additionally, in the cities where competition

is allowed (i.e. Taipei city and New Taipei city)

penetration rates increased considerably. This is

partially explained by both the incumbent and the

new entrants engaging in price-cutting competition

to attract subscribers.

Table 1-6 Cable TV subscribers and penetration rates in major cities

TAIPEI CITy

NEw TAIPEI CITy

TAOyUAN CITy

TAICHUNG CITy

TAINAN CITykAOSHIUNG

CITyOTHER AREAS

Of TAIwAN

2012583,230(57.34%)

1,009,187(69.20%)

471,423(67.17%)

583,195(66.02%)

420,482(64.06%)

652,820(62.38%)

1,268,818(52.37%)

2013583,658(56.85%)

998,199(67.54%)

474,177(66.17%)

584,221(65.12%)

426,504(63.96%)

646,182(61.17%)

1,272,281(51.97%)

2014582,821(56.18%)

998,500(66.70%)

477,232(65.11%)

583,502(63.96%)

431,719(64.63%)

646,232(60.70%)

1,282,210(51.91%)

2015598,310(57.31%)

1,025,854(67.90%)

482,080(64.23%)

582,207(62.74%)

442,105 (65.76%)

655,013(61.05%)

1,293,307(51.93%)

2016629,150(60.07%)

1,073,595(70.32%)

490,138(63.58%)

594,689(62.96%)

437,655(64.54%)

657,433(60.70%)

1,322,902(52.69%)

Source: NCC statistics

Taiwan in View 9

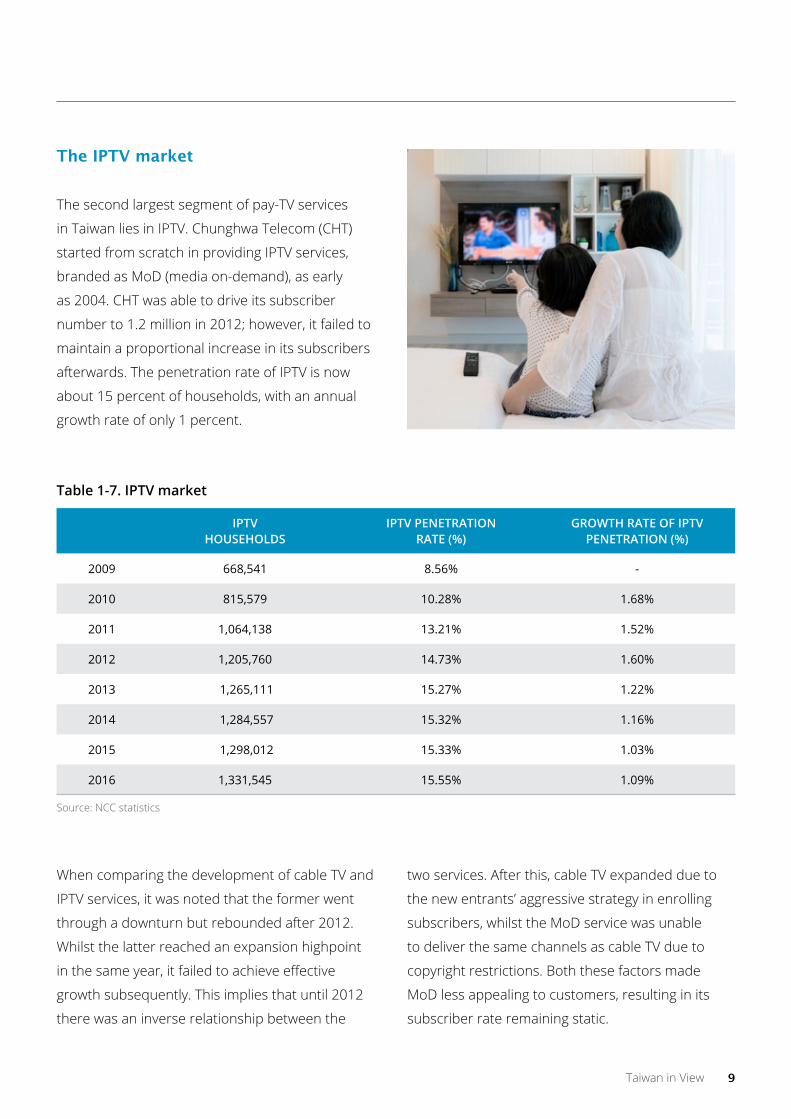

The IPTV market

The second largest segment of pay-TV services

in Taiwan lies in IPTV. Chunghwa Telecom (CHT)

started from scratch in providing IPTV services,

branded as MoD (media on-demand), as early

as 2004. CHT was able to drive its subscriber

number to 1.2 million in 2012; however, it failed to

maintain a proportional increase in its subscribers

afterwards. The penetration rate of IPTV is now

about 15 percent of households, with an annual

growth rate of only 1 percent.

Table 1-7. IPTV market

IPTV HOUSEHOLDS

IPTV PENETRATION RATE (%)

GROwTH RATE Of IPTV PENETRATION (%)

2009 668,541 8.56% -

2010 815,579 10.28% 1.68%

2011 1,064,138 13.21% 1.52%

2012 1,205,760 14.73% 1.60%

2013 1,265,111 15.27% 1.22%

2014 1,284,557 15.32% 1.16%

2015 1,298,012 15.33% 1.03%

2016 1,331,545 15.55% 1.09%

Source: NCC statistics

When comparing the development of cable TV and

IPTV services, it was noted that the former went

through a downturn but rebounded after 2012.

Whilst the latter reached an expansion highpoint

in the same year, it failed to achieve effective

growth subsequently. This implies that until 2012

there was an inverse relationship between the

two services. After this, cable TV expanded due to

the new entrants’ aggressive strategy in enrolling

subscribers, whilst the MoD service was unable

to deliver the same channels as cable TV due to

copyright restrictions. Both these factors made

MoD less appealing to customers, resulting in its

subscriber rate remaining static.

10 Taiwan in View

Satellite TV usage

Despite the fact that satellite TV (DBS) is popular

in the Asia Pacific region, satellite TV operators

never achieved a critical mass in providing the

service in Taiwan. The historical data as of 2012

showed that the number of subscribers was less

than 35,000.

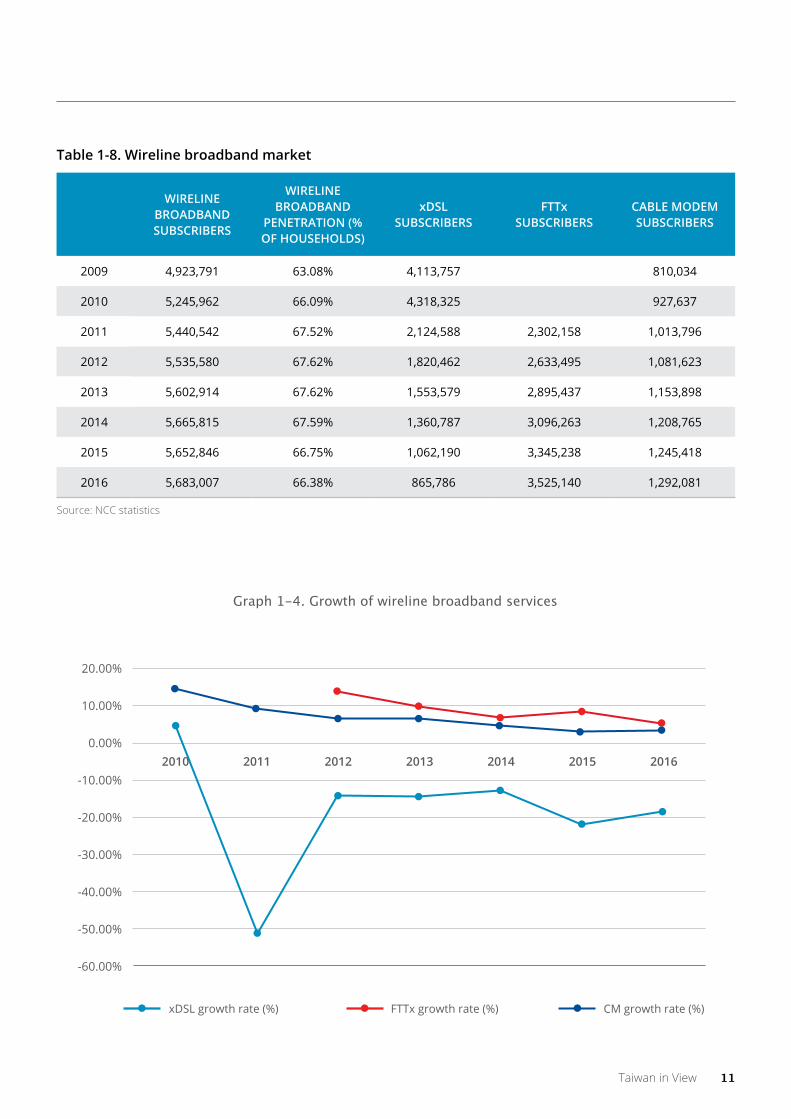

Broadband penetration

The total number of wireline broadband subscribers

was 5.7 million in 2016, up 700,000 from 5 million

in 2009. This equates to a 66.38 percent household

penetration rate. There are three technologies used

for wireline broadband provision: xDSL, FTTx, and

cable modem. The first two are mainly provided

by CHT, while cable modem service is delivered

via cable TV operators. Overall, as xDSL and FTTx

are almost a perfect substitute, the total number

of wireline broadband subscriptions does not

significantly grow even though the number of FTTx

subscriptions continues to surge since its launch in

2011. Meanwhile, cable modem service subscribers

increased only marginally.

3.00%

2.50%

2.00%

1.50%

1.00%

0.50%

0.00%

-0.50%

-1.00%

-1.50%

-2.00%

Cable TV households IPTV

Graph 1-3. Growth rates of cable TV and IPTV services

growth rate (%)

2009 2010 2014 2015 20162011 2012 2013

Taiwan in View 11

Table 1-8. wireline broadband market

wIRELINE bROADbAND SUbSCRIbERS

wIRELINE bROADbAND

PENETRATION (% Of HOUSEHOLDS)

xDSL SUbSCRIbERS

fTTx SUbSCRIbERS

CAbLE MODEM SUbSCRIbERS

2009 4,923,791 63.08% 4,113,757 810,034

2010 5,245,962 66.09% 4,318,325 927,637

2011 5,440,542 67.52% 2,124,588 2,302,158 1,013,796

2012 5,535,580 67.62% 1,820,462 2,633,495 1,081,623

2013 5,602,914 67.62% 1,553,579 2,895,437 1,153,898

2014 5,665,815 67.59% 1,360,787 3,096,263 1,208,765

2015 5,652,846 66.75% 1,062,190 3,345,238 1,245,418

2016 5,683,007 66.38% 865,786 3,525,140 1,292,081

Source: NCC statistics

20.00%

10.00%

0.00%

-10.00%

-20.00%

-30.00%

-40.00%

-50.00%

-60.00%

xDSL growth rate (%) FTTx growth rate (%)

Graph 1-4. Growth of wireline broadband services

2014 2015 20162011 2012 2013

CM growth rate (%)

2010

12 Taiwan in View

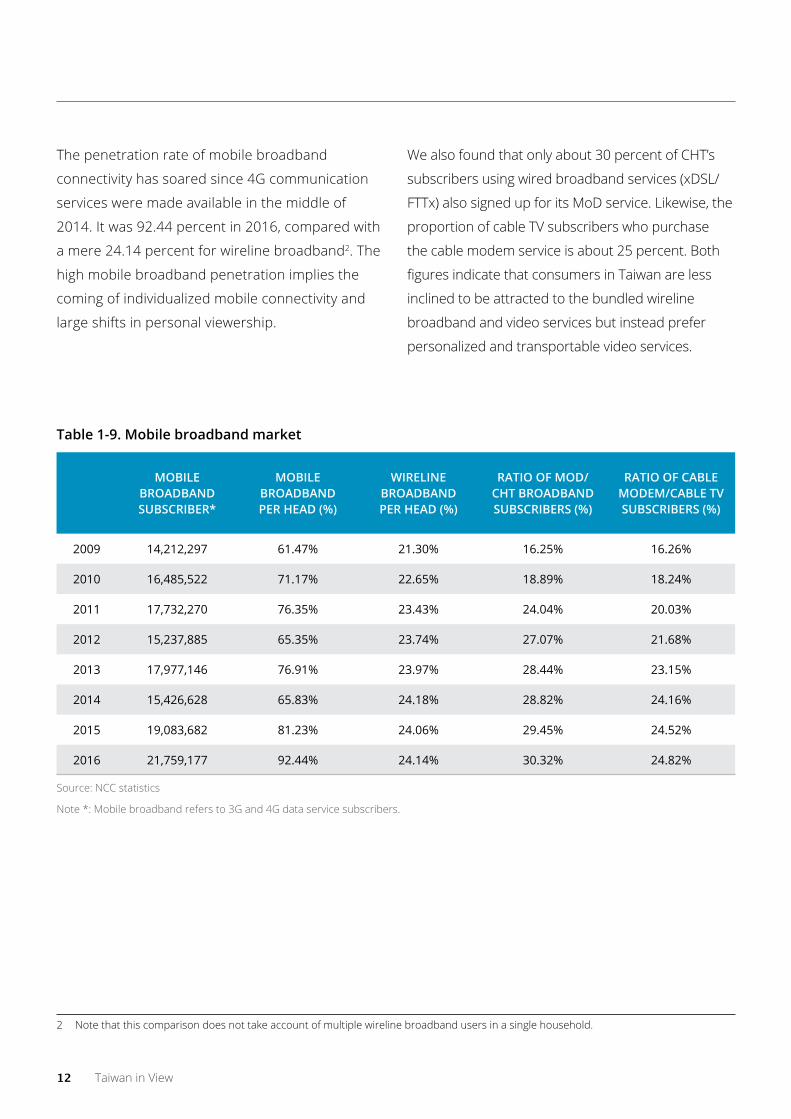

The penetration rate of mobile broadband

connectivity has soared since 4G communication

services were made available in the middle of

2014. It was 92.44 percent in 2016, compared with

a mere 24.14 percent for wireline broadband2. The

high mobile broadband penetration implies the

coming of individualized mobile connectivity and

large shifts in personal viewership.

We also found that only about 30 percent of CHT’s

subscribers using wired broadband services (xDSL/

FTTx) also signed up for its MoD service. Likewise, the

proportion of cable TV subscribers who purchase

the cable modem service is about 25 percent. Both

figures indicate that consumers in Taiwan are less

inclined to be attracted to the bundled wireline

broadband and video services but instead prefer

personalized and transportable video services.

Table 1-9. Mobile broadband market

MObILE bROADbAND SUbSCRIbER*

MObILE bROADbAND PER HEAD (%)

wIRELINE bROADbAND PER HEAD (%)

RATIO Of MOD/CHT bROADbAND SUbSCRIbERS (%)

RATIO Of CAbLE MODEM/CAbLE TV SUbSCRIbERS (%)

2009 14,212,297 61.47% 21.30% 16.25% 16.26%

2010 16,485,522 71.17% 22.65% 18.89% 18.24%

2011 17,732,270 76.35% 23.43% 24.04% 20.03%

2012 15,237,885 65.35% 23.74% 27.07% 21.68%

2013 17,977,146 76.91% 23.97% 28.44% 23.15%

2014 15,426,628 65.83% 24.18% 28.82% 24.16%

2015 19,083,682 81.23% 24.06% 29.45% 24.52%

2016 21,759,177 92.44% 24.14% 30.32% 24.82%

Source: NCC statistics

Note *: Mobile broadband refers to 3G and 4G data service subscribers.

2 Note that this comparison does not take account of multiple wireline broadband users in a single household.

Taiwan in View 13

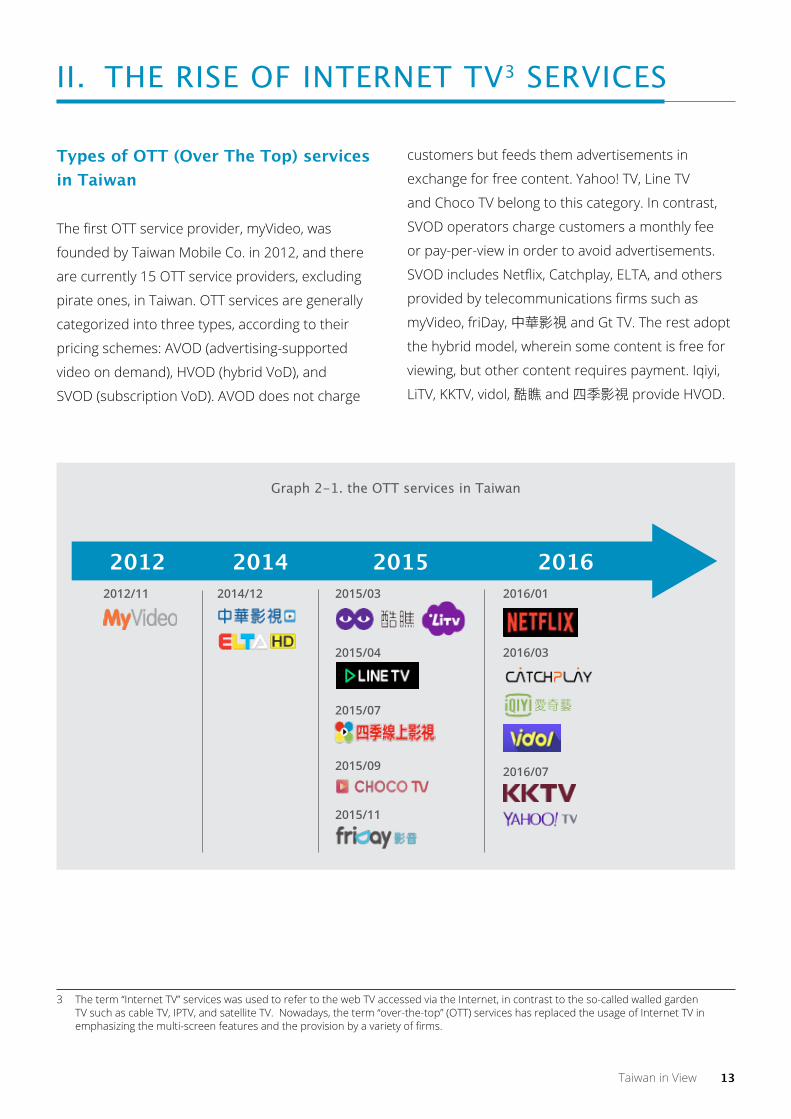

Types of OTT (Over The Top) services in Taiwan

The first OTT service provider, myVideo, was

founded by Taiwan Mobile Co. in 2012, and there

are currently 15 OTT service providers, excluding

pirate ones, in Taiwan. OTT services are generally

categorized into three types, according to their

pricing schemes: AVOD (advertising-supported

video on demand), HVOD (hybrid VoD), and

SVOD (subscription VoD). AVOD does not charge

customers but feeds them advertisements in

exchange for free content. Yahoo! TV, Line TV

and Choco TV belong to this category. In contrast,

SVOD operators charge customers a monthly fee

or pay-per-view in order to avoid advertisements.

SVOD includes Netflix, Catchplay, ELTA, and others

provided by telecommunications firms such as

myVideo, friDay, 中華影視 and Gt TV. The rest adopt

the hybrid model, wherein some content is free for

viewing, but other content requires payment. Iqiyi,

LiTV, KKTV, vidol, 酷瞧 and 四季影視 provide HVOD.

3 The term “Internet TV” services was used to refer to the web TV accessed via the Internet, in contrast to the so-called walled garden TV such as cable TV, IPTV, and satellite TV. Nowadays, the term “over-the-top” (OTT) services has replaced the usage of Internet TV in emphasizing the multi-screen features and the provision by a variety of firms.

II. the rIse of Internet tV3 serVIces

2012/11 2014/12

Graph 2-1. the ott services in taiwan

2015/03

2015/04

2015/07

2015/09

2015/11

2016/01

2016/03

2016/07

2012 2014 2015 2016

14 Taiwan in View

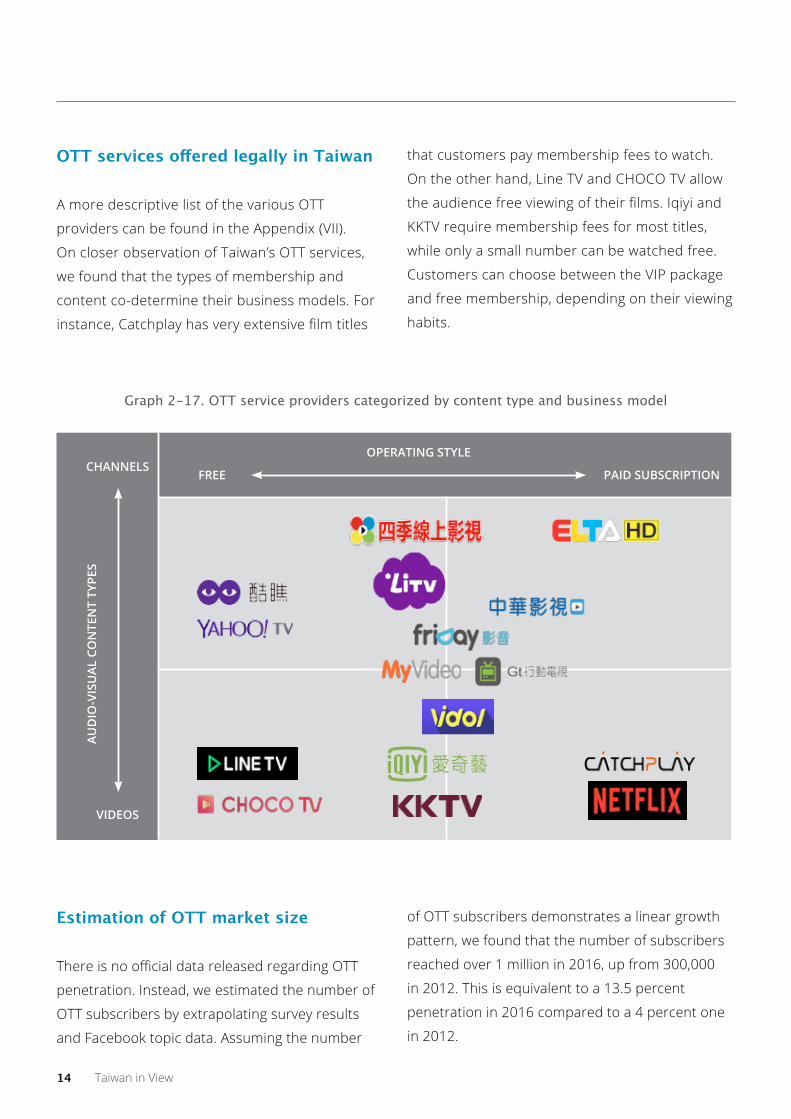

OTT services offered legally in Taiwan

A more descriptive list of the various OTT

providers can be found in the Appendix (VII).

On closer observation of Taiwan’s OTT services,

we found that the types of membership and

content co-determine their business models. For

instance, Catchplay has very extensive film titles

that customers pay membership fees to watch.

On the other hand, Line TV and CHOCO TV allow

the audience free viewing of their films. Iqiyi and

KKTV require membership fees for most titles,

while only a small number can be watched free.

Customers can choose between the VIP package

and free membership, depending on their viewing

habits.

Estimation of OTT market size

There is no official data released regarding OTT

penetration. Instead, we estimated the number of

OTT subscribers by extrapolating survey results

and Facebook topic data. Assuming the number

of OTT subscribers demonstrates a linear growth

pattern, we found that the number of subscribers

reached over 1 million in 2016, up from 300,000

in 2012. This is equivalent to a 13.5 percent

penetration in 2016 compared to a 4 percent one

in 2012.

CHANNELS

VIDEOS

AUD

IO-V

ISU

AL C

ON

TEN

T Ty

PES

fREE PAID SUbSCRIPTION

OPERATING STyLE

Graph 2-17. ott service providers categorized by content type and business model

Taiwan in View 15

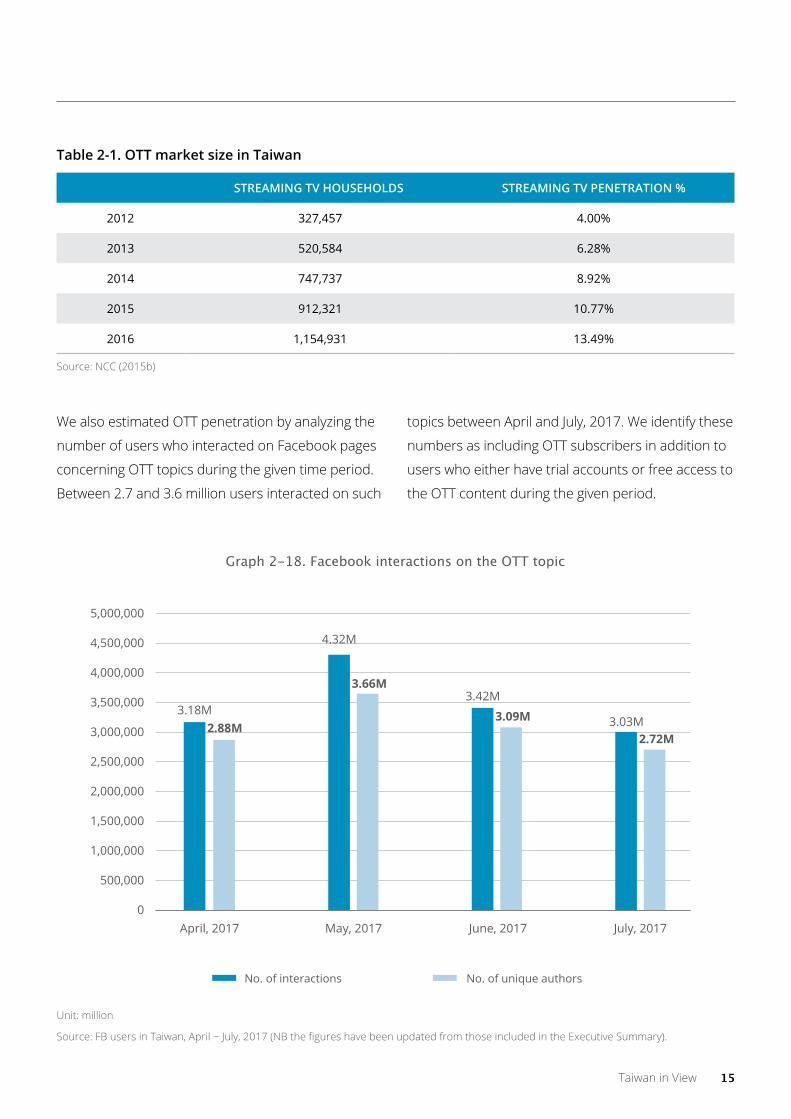

Table 2-1. OTT market size in Taiwan

STREAMING TV HOUSEHOLDS STREAMING TV PENETRATION %

2012 327,457 4.00%

2013 520,584 6.28%

2014 747,737 8.92%

2015 912,321 10.77%

2016 1,154,931 13.49%

Source: NCC (2015b)

We also estimated OTT penetration by analyzing the

number of users who interacted on Facebook pages

concerning OTT topics during the given time period.

Between 2.7 and 3.6 million users interacted on such

topics between April and July, 2017. We identify these

numbers as including OTT subscribers in addition to

users who either have trial accounts or free access to

the OTT content during the given period.

5,000,000

4,500,000

4,000,000

3,500,000

3,000,000

2,500,000

2,000,000

1,500,000

1,000,000

500,000

0

3.18M2.88M

4.32M

3.66M3.42M

3.09M 3.03M2.72M

April, 2017 May, 2017 June, 2017 July, 2017

No. of interactions No. of unique authors

Graph 2-18. Facebook interactions on the OTT topic

Unit: million

Source: FB users in Taiwan, April ~ July, 2017 (NB the figures have been updated from those included in the Executive Summary).

16 Taiwan in View

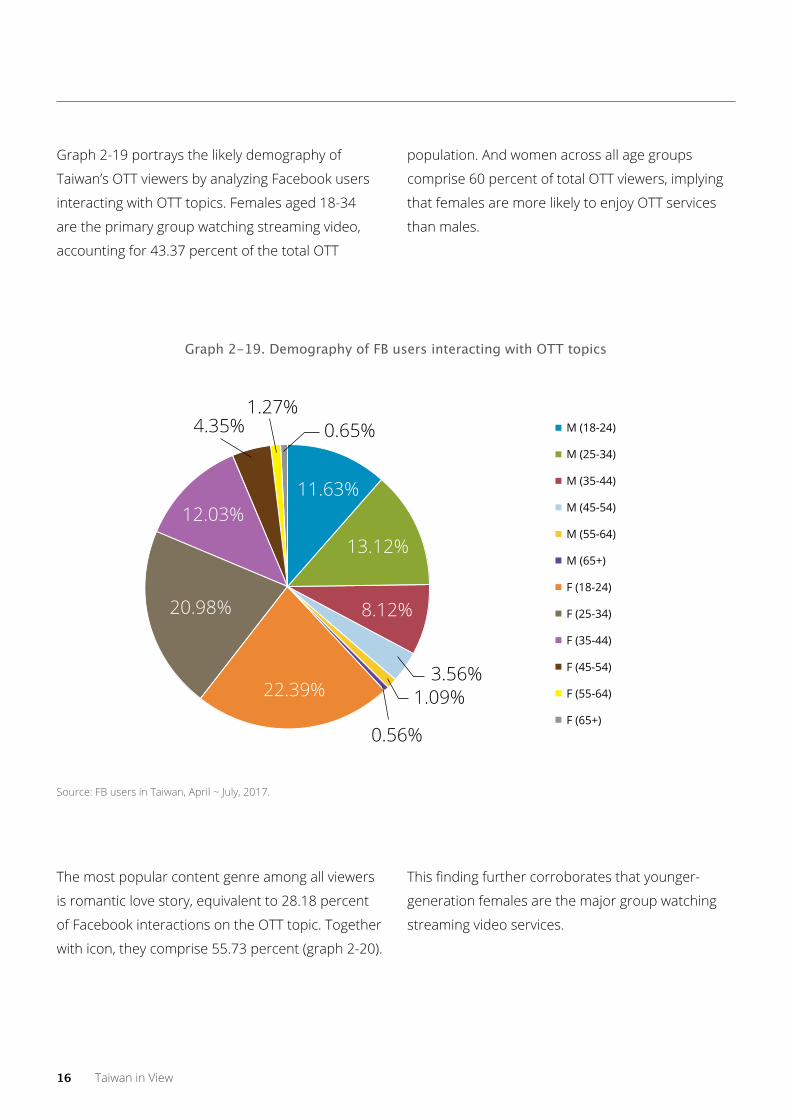

Graph 2-19 portrays the likely demography of

Taiwan’s OTT viewers by analyzing Facebook users

interacting with OTT topics. Females aged 18-34

are the primary group watching streaming video,

accounting for 43.37 percent of the total OTT

population. And women across all age groups

comprise 60 percent of total OTT viewers, implying

that females are more likely to enjoy OTT services

than males.

Source: FB users in Taiwan, April ~ July, 2017.

Graph 2-19. demography of fB users interacting with ott topics

12.03%

20.98%

22.39%3.56%

M (18-24)

M (25-34)

M (35-44)

M (45-54)

M (55-64)

M (65+)

F (18-24)

F (25-34)

F (35-44)

F (45-54)

F (55-64)

F (65+)

1.09%

0.56%

8.12%

13.12%

11.63%

4.35%1.27%

0.65%

The most popular content genre among all viewers

is romantic love story, equivalent to 28.18 percent

of Facebook interactions on the OTT topic. Together

with icon, they comprise 55.73 percent (graph 2-20).

This finding further corroborates that younger-

generation females are the major group watching

streaming video services.

Taiwan in View 17

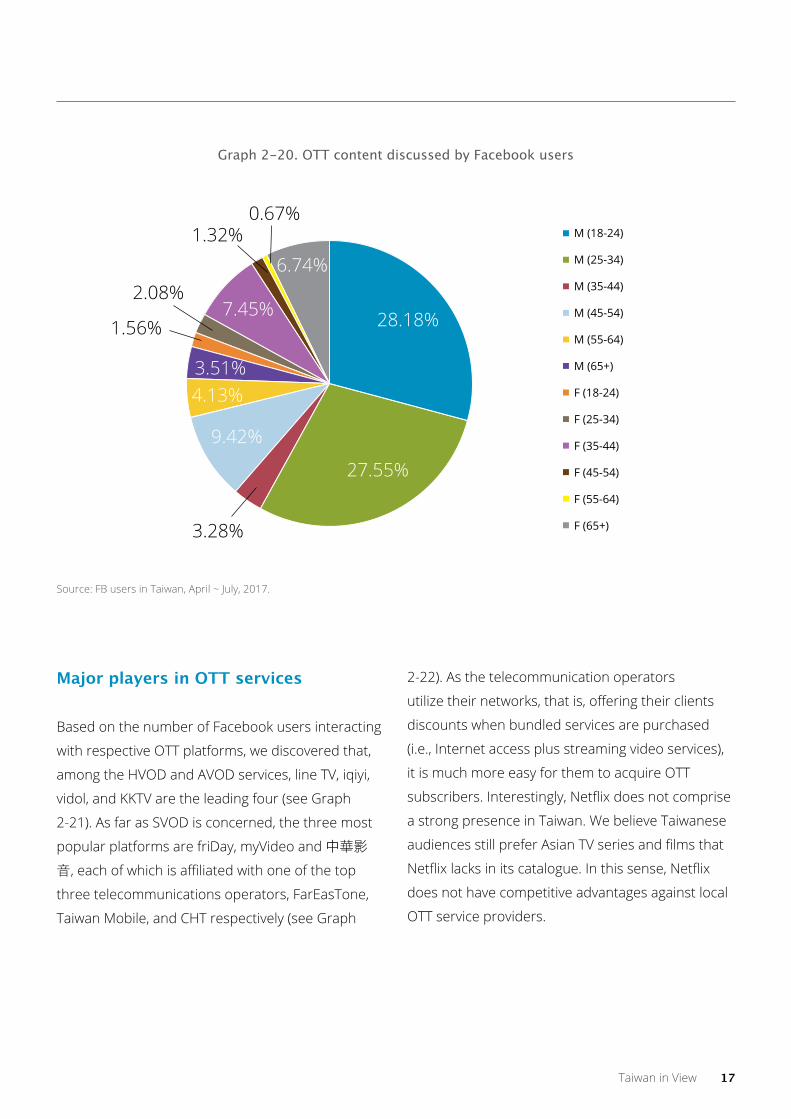

Major players in OTT services

Based on the number of Facebook users interacting

with respective OTT platforms, we discovered that,

among the HVOD and AVOD services, line TV, iqiyi,

vidol, and KKTV are the leading four (see Graph

2-21). As far as SVOD is concerned, the three most

popular platforms are friDay, myVideo and 中華影

音, each of which is affiliated with one of the top

three telecommunications operators, FarEasTone,

Taiwan Mobile, and CHT respectively (see Graph

2-22). As the telecommunication operators

utilize their networks, that is, offering their clients

discounts when bundled services are purchased

(i.e., Internet access plus streaming video services),

it is much more easy for them to acquire OTT

subscribers. Interestingly, Netflix does not comprise

a strong presence in Taiwan. We believe Taiwanese

audiences still prefer Asian TV series and films that

Netflix lacks in its catalogue. In this sense, Netflix

does not have competitive advantages against local

OTT service providers.

Source: FB users in Taiwan, April ~ July, 2017.

M (18-24)

M (25-34)

M (35-44)

M (45-54)

M (55-64)

M (65+)

F (18-24)

F (25-34)

F (35-44)

F (45-54)

F (55-64)

F (65+)

0.67%1.32%

1.56%

3.28%

2.08%

Graph 2-20. ott content discussed by facebook users

28.18%

27.55%

9.42%

4.13%3.51%

7.45%

6.74%

18 Taiwan in View

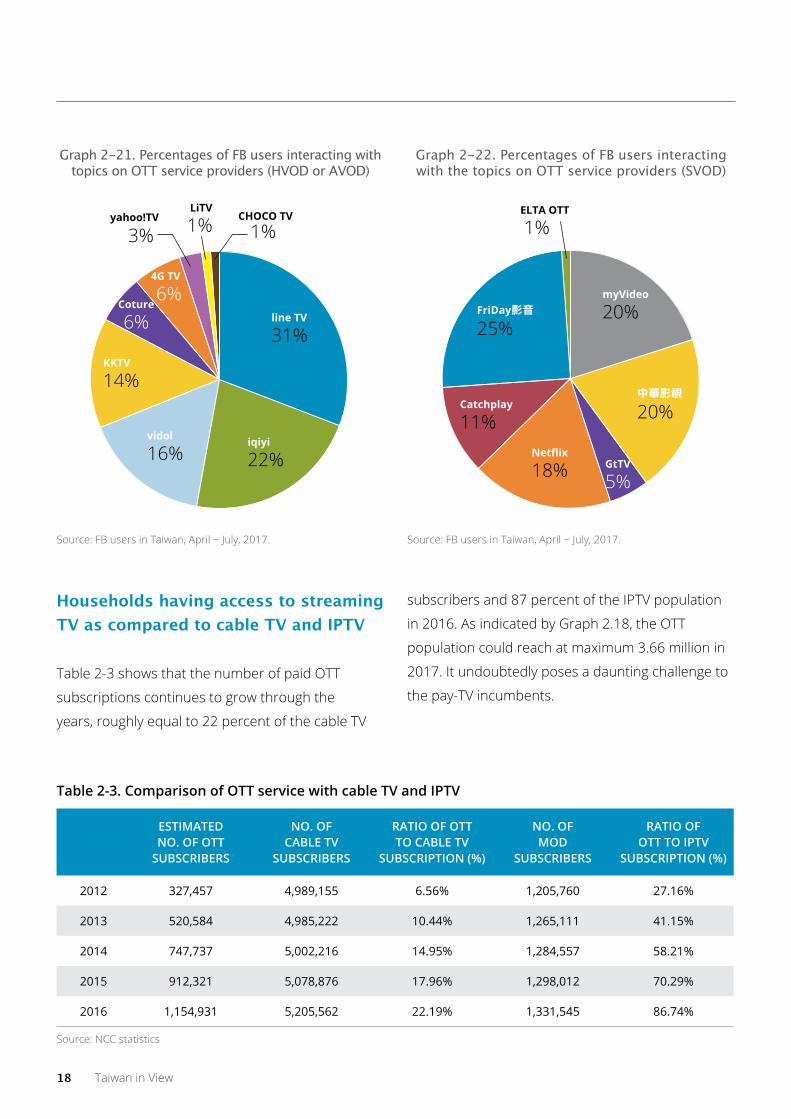

Households having access to streaming TV as compared to cable TV and IPTV

Table 2-3 shows that the number of paid OTT

subscriptions continues to grow through the

years, roughly equal to 22 percent of the cable TV

subscribers and 87 percent of the IPTV population

in 2016. As indicated by Graph 2.18, the OTT

population could reach at maximum 3.66 million in

2017. It undoubtedly poses a daunting challenge to

the pay-TV incumbents.

Graph 2-21. Percentages of fB users interacting with topics on ott service providers (hVod or aVod)

Graph 2-22. Percentages of fB users interacting with the topics on ott service providers (sVod)

3% 1% 1%1%

Source: FB users in Taiwan, April ~ July, 2017. Source: FB users in Taiwan, April ~ July, 2017.

Table 2-3. Comparison of OTT service with cable TV and IPTV

ESTIMATED NO. Of OTT

SUbSCRIbERS

NO. Of CAbLE TV

SUbSCRIbERS

RATIO Of OTT TO CAbLE TV

SUbSCRIPTION (%)

NO. Of MOD

SUbSCRIbERS

RATIO Of OTT TO IPTV

SUbSCRIPTION (%)

2012 327,457 4,989,155 6.56% 1,205,760 27.16%

2013 520,584 4,985,222 10.44% 1,265,111 41.15%

2014 747,737 5,002,216 14.95% 1,284,557 58.21%

2015 912,321 5,078,876 17.96% 1,298,012 70.29%

2016 1,154,931 5,205,562 22.19% 1,331,545 86.74%

Source: NCC statistics

line TV

myVideo

GtTVNetflix

Catchplay

FriDay影音

中華影視

iqiyividol

KKTV

Coture

4G TV

yahoo!TVLiTV ELTA OTTCHOCO TV

31%20%

5%18%

11%

25%

20%

22%16%

14%

6%6%

Taiwan in View 19

III. BusIness models and market forecasts

Prospects for further development and change of business models in the pay-TV industry

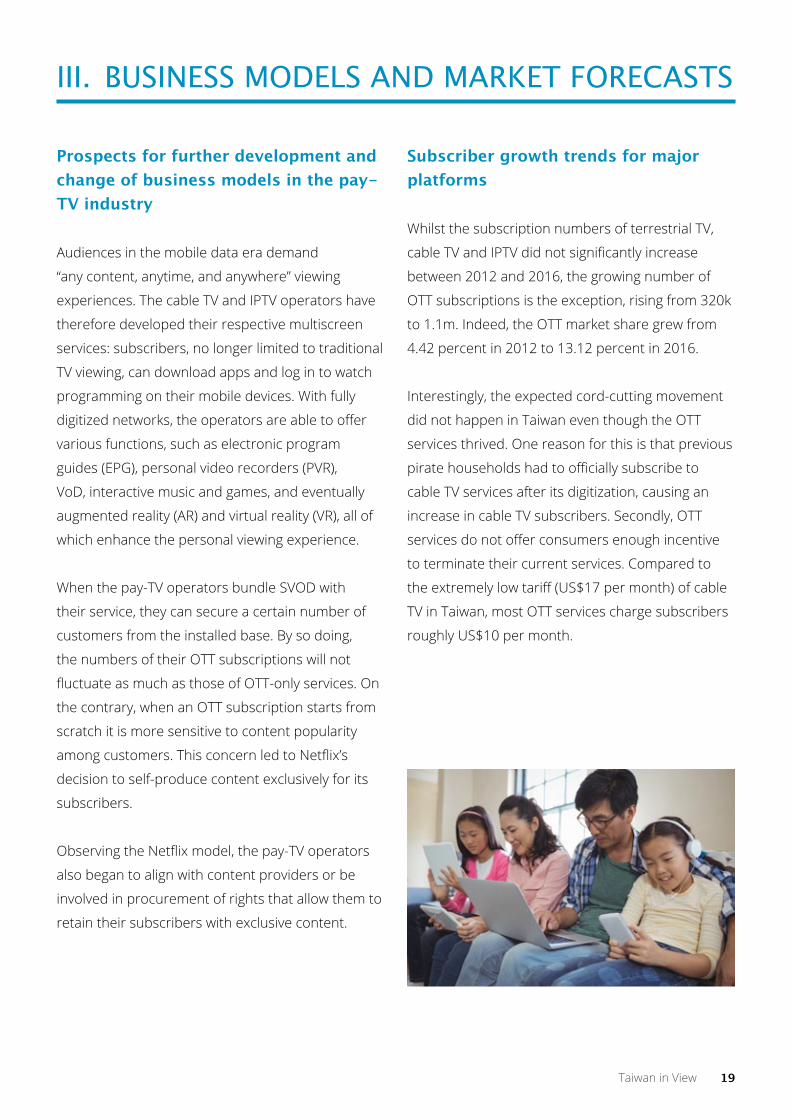

Audiences in the mobile data era demand

“any content, anytime, and anywhere” viewing

experiences. The cable TV and IPTV operators have

therefore developed their respective multiscreen

services: subscribers, no longer limited to traditional

TV viewing, can download apps and log in to watch

programming on their mobile devices. With fully

digitized networks, the operators are able to offer

various functions, such as electronic program

guides (EPG), personal video recorders (PVR),

VoD, interactive music and games, and eventually

augmented reality (AR) and virtual reality (VR), all of

which enhance the personal viewing experience.

When the pay-TV operators bundle SVOD with

their service, they can secure a certain number of

customers from the installed base. By so doing,

the numbers of their OTT subscriptions will not

fluctuate as much as those of OTT-only services. On

the contrary, when an OTT subscription starts from

scratch it is more sensitive to content popularity

among customers. This concern led to Netflix’s

decision to self-produce content exclusively for its

subscribers.

Observing the Netflix model, the pay-TV operators

also began to align with content providers or be

involved in procurement of rights that allow them to

retain their subscribers with exclusive content.

Subscriber growth trends for major platforms

Whilst the subscription numbers of terrestrial TV,

cable TV and IPTV did not significantly increase

between 2012 and 2016, the growing number of

OTT subscriptions is the exception, rising from 320k

to 1.1m. Indeed, the OTT market share grew from

4.42 percent in 2012 to 13.12 percent in 2016.

Interestingly, the expected cord-cutting movement

did not happen in Taiwan even though the OTT

services thrived. One reason for this is that previous

pirate households had to officially subscribe to

cable TV services after its digitization, causing an

increase in cable TV subscribers. Secondly, OTT

services do not offer consumers enough incentive

to terminate their current services. Compared to

the extremely low tariff (US$17 per month) of cable

TV in Taiwan, most OTT services charge subscribers

roughly US$10 per month.

20 Taiwan in View

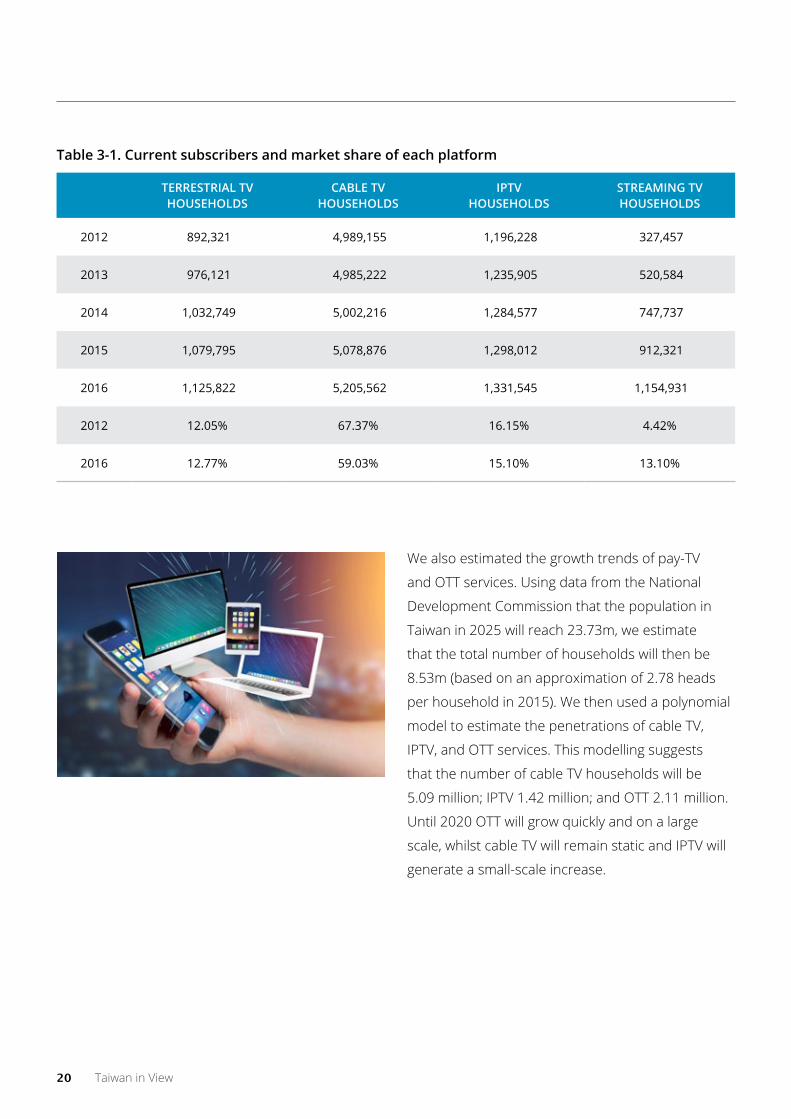

Table 3-1. Current subscribers and market share of each platform

TERRESTRIAL TV HOUSEHOLDS

CAbLE TV HOUSEHOLDS

IPTV HOUSEHOLDS

STREAMING TV HOUSEHOLDS

2012 892,321 4,989,155 1,196,228 327,457

2013 976,121 4,985,222 1,235,905 520,584

2014 1,032,749 5,002,216 1,284,577 747,737

2015 1,079,795 5,078,876 1,298,012 912,321

2016 1,125,822 5,205,562 1,331,545 1,154,931

2012 12.05% 67.37% 16.15% 4.42%

2016 12.77% 59.03% 15.10% 13.10%

We also estimated the growth trends of pay-TV

and OTT services. Using data from the National

Development Commission that the population in

Taiwan in 2025 will reach 23.73m, we estimate

that the total number of households will then be

8.53m (based on an approximation of 2.78 heads

per household in 2015). We then used a polynomial

model to estimate the penetrations of cable TV,

IPTV, and OTT services. This modelling suggests

that the number of cable TV households will be

5.09 million; IPTV 1.42 million; and OTT 2.11 million.

Until 2020 OTT will grow quickly and on a large

scale, whilst cable TV will remain static and IPTV will

generate a small-scale increase.

Taiwan in View 21

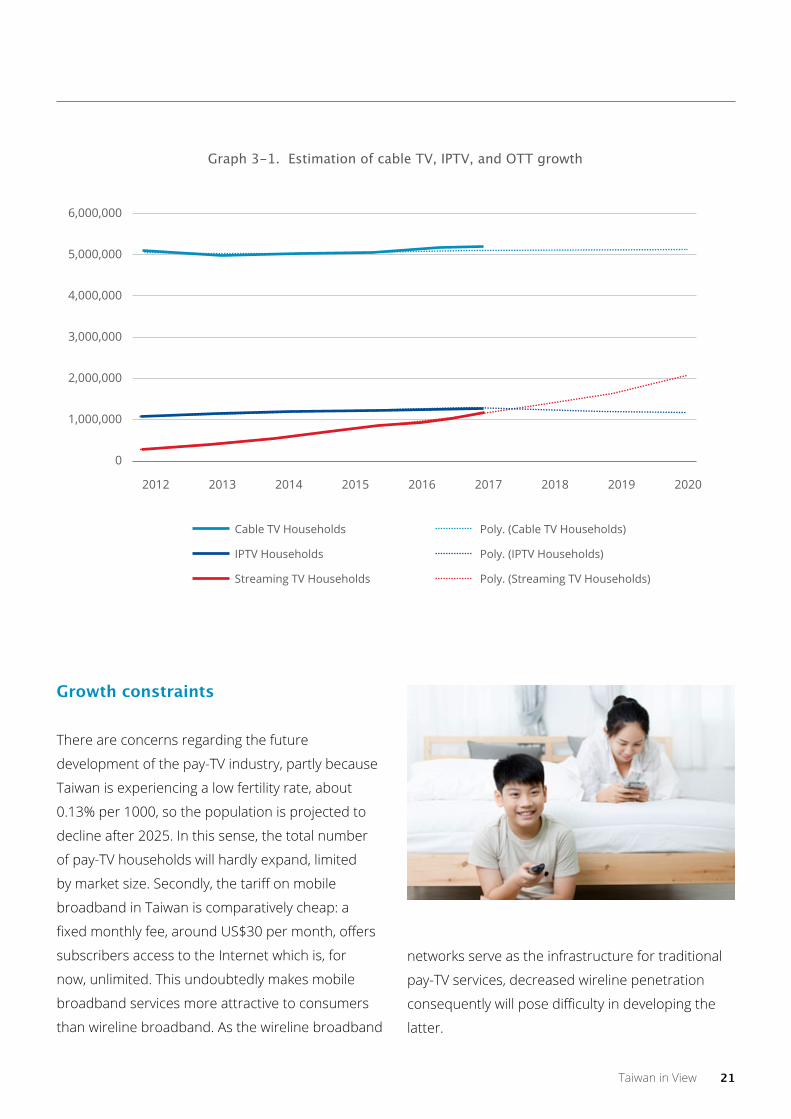

Growth constraints

There are concerns regarding the future

development of the pay-TV industry, partly because

Taiwan is experiencing a low fertility rate, about

0.13% per 1000, so the population is projected to

decline after 2025. In this sense, the total number

of pay-TV households will hardly expand, limited

by market size. Secondly, the tariff on mobile

broadband in Taiwan is comparatively cheap: a

fixed monthly fee, around US$30 per month, offers

subscribers access to the Internet which is, for

now, unlimited. This undoubtedly makes mobile

broadband services more attractive to consumers

than wireline broadband. As the wireline broadband

6,000,000

5,000,000

4,000,000

3,000,000

2,000,000

1,000,000

0

2012 2013 2014 2015 2016 2017 2018 2019 2020

Cable TV Households

Poly. (IPTV Households)

Graph 3-1. Estimation of cable TV, IPTV, and OTT growth

Poly. (Cable TV Households)

Streaming TV Households

IPTV Households

Poly. (Streaming TV Households)

networks serve as the infrastructure for traditional

pay-TV services, decreased wireline penetration

consequently will pose difficulty in developing the

latter.

22 Taiwan in View

Channel programmers and their agents

The NCC mandates that all channels broadcast

on pay-TV platforms must file for (satellite) TV

channel licenses. The combined number of channel

programmers, domestic and international, was 126

in 2016 holding a total of 304 channel licenses, 71

up compared to 233 in 2009.

Of these 304 licenses, however, only 118 of them

resulted in programming which could be accessed

via major pay-TV platforms; some are carried on

MoD and some are not used at all. One reason for

this lies in the fact that any change in the channels

delivered over the platforms must be approved

by the NCC. That is, the operators do not have

much freedom in adjusting the channels they offer.

The other is due to the negotiating power of their

agents with pay-TV operators. Since large agents

are affiliated with the MSOs, they easily reach

consensus with the MSOs to maintain the status

quo to avoid any variation in revenue streams (table

4-2). These two factors led to minimal changes

in the TV channels delivered over the platforms

through the years.

IV. ProGrammInG and PrIcInG

Table 4-1 Pay-TV channels in Taiwan

NO. Of DOMESTIC Channel programmers

NO. Of INTERNATIONAL Channel programmers

TOTAL NUMbER Of TV CHANNELS

2009 79 30 233

2010 82 30 268

2011 80 29 263

2012 80 29 269

2013 84 30 280

2014 86 29 280

2015 93 30 299

2016 93 33 304

Source: NCC statistics

Taiwan in View 23

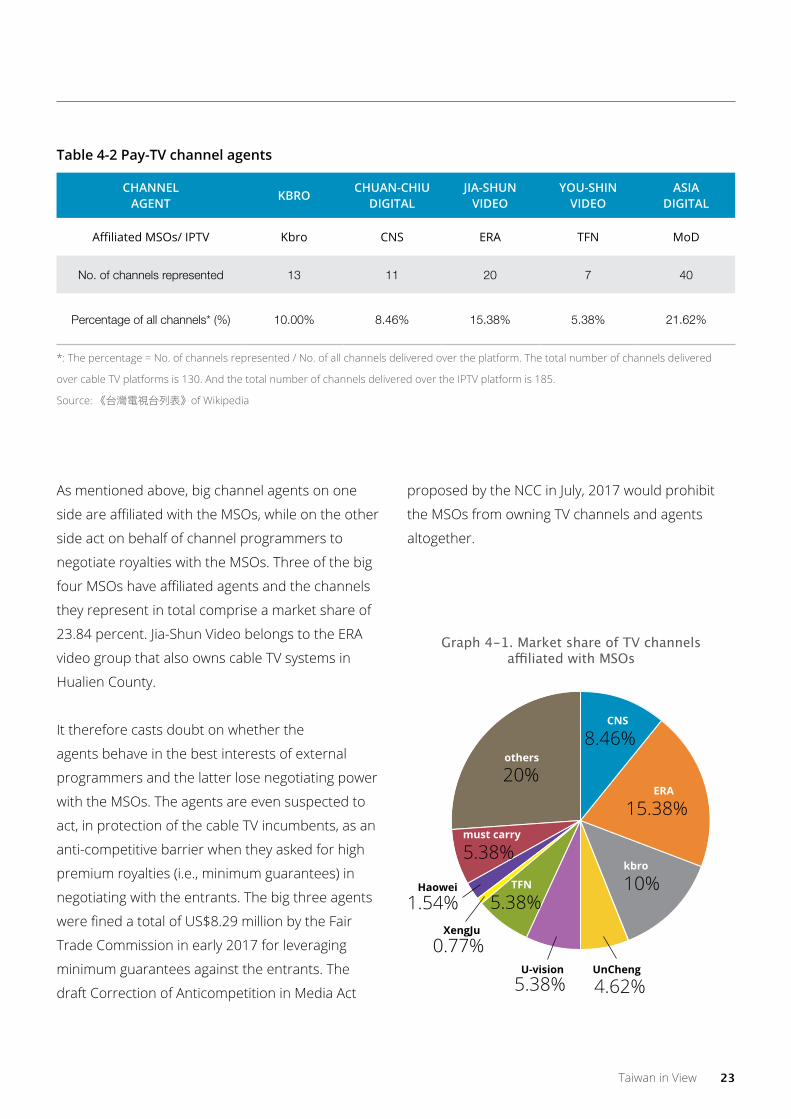

Table 4-2 Pay-TV channel agents

CHANNEL AGENT

kbROCHUAN-CHIU

DIGITALJIA-SHUN

VIDEOyOU-SHIN

VIDEOASIA

DIGITAL

AffiliatedMSOs/IPTV Kbro CNS ERA TFN MoD

no. of channels represented 13 11 20 7 40

percentage of all channels* (%) 10.00% 8.46% 15.38% 5.38% 21.62%

*: The percentage = No. of channels represented / No. of all channels delivered over the platform. The total number of channels delivered

over cable TV platforms is 130. And the total number of channels delivered over the IPTV platform is 185.

Source: 《台灣電視台列表》of Wikipedia

As mentioned above, big channel agents on one

side are affiliated with the MSOs, while on the other

side act on behalf of channel programmers to

negotiate royalties with the MSOs. Three of the big

four MSOs have affiliated agents and the channels

they represent in total comprise a market share of

23.84 percent. Jia-Shun Video belongs to the ERA

video group that also owns cable TV systems in

Hualien County.

It therefore casts doubt on whether the

agents behave in the best interests of external

programmers and the latter lose negotiating power

with the MSOs. The agents are even suspected to

act, in protection of the cable TV incumbents, as an

anti-competitive barrier when they asked for high

premium royalties (i.e., minimum guarantees) in

negotiating with the entrants. The big three agents

were fined a total of US$8.29 million by the Fair

Trade Commission in early 2017 for leveraging

minimum guarantees against the entrants. The

draft Correction of Anticompetition in Media Act

proposed by the NCC in July, 2017 would prohibit

the MSOs from owning TV channels and agents

altogether.

Graph 4-1. market share of tV channels affiliated with MSOs

0.77%

1.54%

CNS

ERA

kbro

UnCheng

TFN

U-vision

must carry

others

XengJu

Haowei

8.46%

15.38%

10%

4.62%

5.38%

5.38%

5.38%

20%

24 Taiwan in View

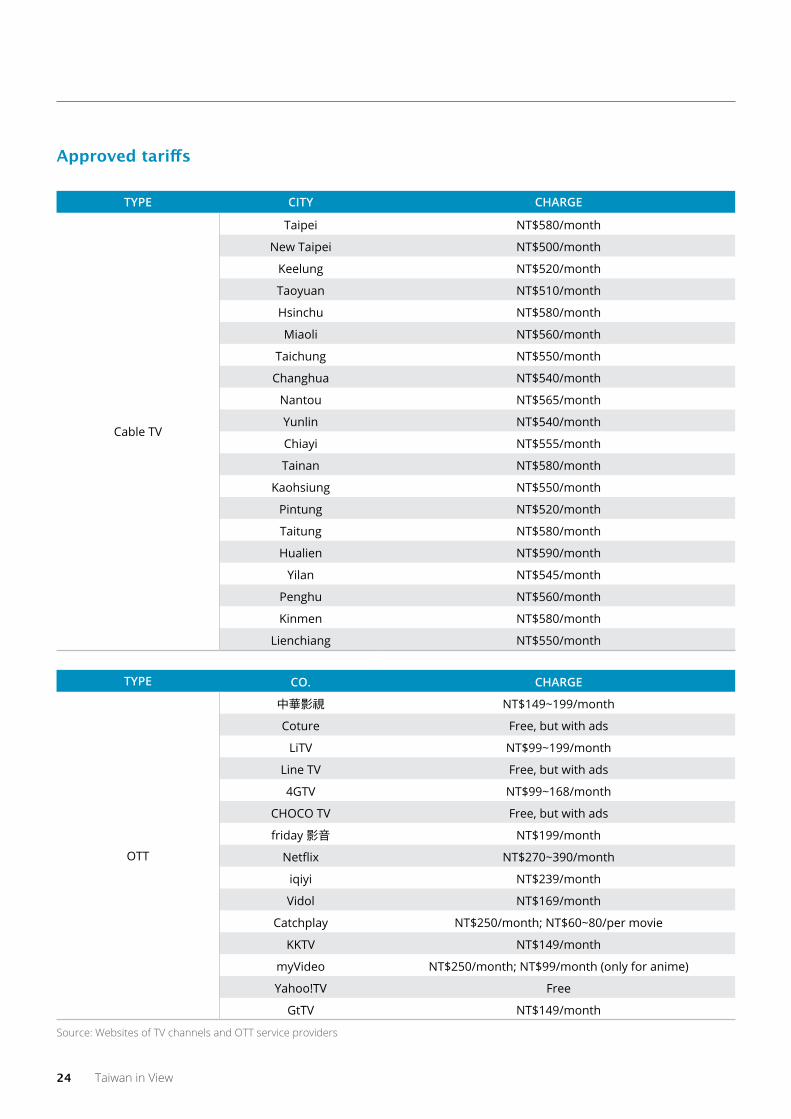

Approved tariffs

TyPE CITy CHARGE

Cable TV

Taipei NT$580/month

New Taipei NT$500/month

Keelung NT$520/month

Taoyuan NT$510/month

Hsinchu NT$580/month

Miaoli NT$560/month

Taichung NT$550/month

Changhua NT$540/month

Nantou NT$565/month

Yunlin NT$540/month

Chiayi NT$555/month

Tainan NT$580/month

Kaohsiung NT$550/month

Pintung NT$520/month

Taitung NT$580/month

Hualien NT$590/month

Yilan NT$545/month

Penghu NT$560/month

Kinmen NT$580/month

Lienchiang NT$550/month

TyPE CO. CHARGE

OTT

中華影視 NT$149~199/month

Coture Free, but with ads

LiTV NT$99~199/month

Line TV Free, but with ads

4GTV NT$99~168/month

CHOCO TV Free, but with ads

friday 影音 NT$199/month

Netflix NT$270~390/month

iqiyi NT$239/month

Vidol NT$169/month

Catchplay NT$250/month;NT$60~80/permovie

KKTV NT$149/month

myVideo NT$250/month;NT$99/month(onlyforanime)

Yahoo!TV Free

GtTV NT$149/month

Source: Websites of TV channels and OTT service providers

Taiwan in View 25

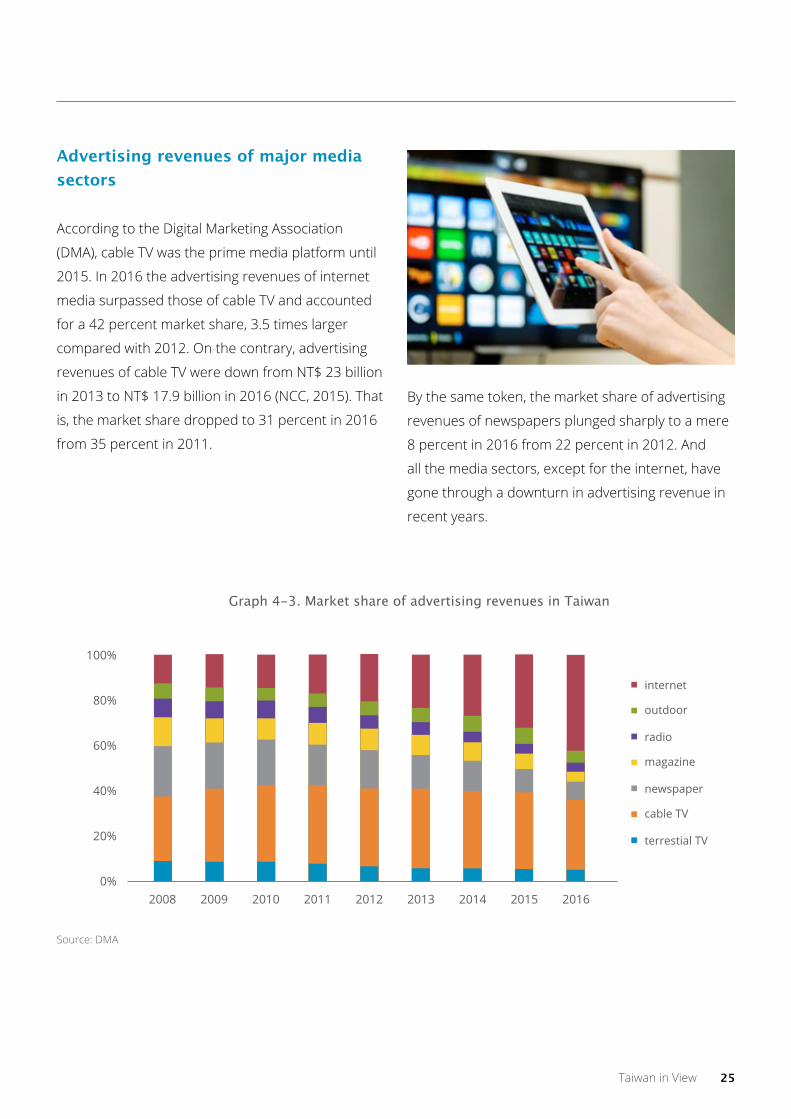

Advertising revenues of major media sectors

According to the Digital Marketing Association

(DMA), cable TV was the prime media platform until

2015. In 2016 the advertising revenues of internet

media surpassed those of cable TV and accounted

for a 42 percent market share, 3.5 times larger

compared with 2012. On the contrary, advertising

revenues of cable TV were down from NT$ 23 billion

in 2013 to NT$ 17.9 billion in 2016 (NCC, 2015). That

is, the market share dropped to 31 percent in 2016

from 35 percent in 2011.

By the same token, the market share of advertising

revenues of newspapers plunged sharply to a mere

8 percent in 2016 from 22 percent in 2012. And

all the media sectors, except for the internet, have

gone through a downturn in advertising revenue in

recent years.

100%

80%

60%

40%

20%

0%

Graph 4-3. Market share of advertising revenues in Taiwan

internet

outdoor

2008 2009 2010 2011 2012 2013 2014 2015 2016

radio

magazine

newspaper

cable TV

terrestial TV

Source: DMA

26 Taiwan in View

Regulatory Frameworks

In Taiwan, there are 3 TV broadcasting statutes and

one telecommunications statute, namely, the Radio

and Television Act (RTA), Cable Radio and Television

Act (CRTA), Satellite Radio and Television Act (SRTA),

and Telecommunications Act (Telecom Act). The

competent authority for the above statutes is the

“National Communication Commission” (NCC). Cable

TV and IPTV services are regulated by the CRTA

and Telecom Act, respectively. OTT TV services are

essentially unregulated.

1. Cable Radio and Television Act (CRTA)

The first version of the CRTA was enacted in 1993,

with wholescale amendments in 1999, and most

recently in 2016.

Cable system operators are awarded regional

licenses. Before 2012, there were 51 cable TV

regions. The number of cable regions was reduced

to 22 in 2012, which matches the number of cities

and counties in Taiwan. In other words, the size

of cable regions were “enlarged”. Currently there

are 61 cable operators in total. 36 cable operators

belong to five major MSOs (multiple system

operators), while the remaining 25 operators are

presumed to be independent. As of the end of

2016, five MSOs controlled 73 percent of nationwide

cable subscribers, making cable TV a horizontally

concentrated industry.

Each year, cable operators are required to pay a

franchise fee, which equates to 1 percent of their

annual sales. Cable operators are subject to retail

price regulation, which local governments review

every year. Since 1998, the price has been set

between NT $500 to $600 (US $17 to $20). There is

also a “must-carry” regulation that cable operators

must re-transmit signals of all (5) terrestrial wireless

TV stations to their audience. The “must-carry” rule

waives the requirement for cable operators to pay

copyright royalties to wireless TV stations.

For more than 20 years, not only have a majority

of cable operators been owned by conglomerates

(MSOs), but many programming channels have

also been owned by conglomerates and traded in

groups. Furthermore, a few top MSOs are vertically

integrated with programming conglomerates.

Vertical integration, associated with horizontal

concentration, resulted in anti-competitive practices

such as programming cut-off and unjust tie-in sales

in the 1990s. Consequently, two anti-concentration

provisions, modeled after the US Cable Television

Consumer Protection and Competition Act of 1992,

were added to the CRTA in 1999. These provisions

were:

(1) Restrictions on horizontal integration. By law,

the size of cable conglomerates (MSO) shall not

exceed 1/3 of nationwide subscribers.

(2) Restrictions on vertical integration. When a

cable operator is vertically integrated with a

programming conglomerate, the operator shall

not carry the conglomerate’s programming at a

proportion over 1/4 of its channel occupancy.

2. Telecommunications Act (Telecom Act)

“IPTV” is a multi-channel programming service

provided by a telecommunications carrier via its

telecommunications network (not via the Internet).

Chunghwa Telecom, the incumbent fixed network

carrier, is the sole operator providing IPTV (under

the brand name “MoD”) in Taiwan. IPTV used to

V. Pay-tV reGulatory enVIronment

Taiwan in View 27

be regulated by the CRTA, and Chunghwa Telecom

obtained a cable TV license in 2004. After 2006,

however, the IPTV service is regulated by the

Telecom Act. (Reason see infra section V b.3.)

Pursuant to a regulation authorized by the

Telecom Act, an IPTV operator is characterized as

a “multimedia carriage platform”. A multimedia

carriage platform is an open platform over which all

programming channels may elect to be broadcast.

By contrast, a cable operator has the editorial

control to decide which programming channel(s) to

carry. Since the CRTA does not apply to multimedia

carriage platforms, they are not subject to regional

licensing, paying a franchise fee, must-carry, or

anti-concentration regulation. As an open network,

however, a multimedia carriage platform is

required to –

• provide fair and non-discriminatory treatment to

(potential) programming channels;

• allow programming channels to set retail prices

chargeable to subscribers; and,

• allow subscribers to purchase programming

channels on an individual basis, or à la carte.

Current policy issues

There are 4 major regulatory/policy issues

confronting the pay-TV industry:

1. Price regulation and tiering of cable

programming

The basic tier of cable TV is subject to price

regulation. The basic tier contains over 100

channels and the price cap is very low, charging

only US $20 or less which makes Taiwan’s cable

tariffs one of the lowest in the world. Under the low

price regulation for the past 20 years, the quality

of programming services has been gradually

deteriorating.

From 2013 to early 2016, the NCC proposed to

reform the pricing tiers. The proposal had several

prongs. First, the rate-regulated basic tier would be

divided into two tiers, i.e. the universal basic tier and

combination basic tier. Second, the universal basic tier

would contain only 11 channels, mainly must-carry

channels (price: NT $200). Third, in the combination

basic tier, cable systems would provide 3 sets of

channels (price for each set: NT $130). Subscribers

would be free to purchase one, two, or three sets of

channel combinations, in addition to the universal

basic tier. Fourth, the price ceiling for all 3 sets of

channels, along with the universal basic tier, would

be NT $500. Reform of the basic tier was to provide

greater flexibility for cable operators, but industry

players are divided by the reform proposals.

However, in 2016 there was a change of the

Central Government in Taiwan and 5 new

NCC commissioners (5 out of 7), including the

Chairperson, assumed their offices in August 2016.

28 Taiwan in View

The new Chairperson and commissioners so far

have not yet disclosed any views either supporting

or rejecting the pricing reform proposal.

2. Reform of the must-carry rule

In 1999, a must-carry rule was added to the CRTA.

The rule stipulates that cable operators must re-

transmit signals of all (5) wireless TV stations to

their audience. Among the 5 wireless TV stations,

2 are public TV stations, i.e. Public Television Service

(PTS) and Chinese Television System (CTS); and 3 are

private commercial stations – Taiwan Television

(TTV), China Television (CTV), and Formosa Television

(FTV). The must-carry rule faced a challenge when

programming of wireless TV stations was converted

to digital transmission (“digital switch-over”) in 2012.

Each wireless TV station thereafter provided 3 or 4

digital channels. The legal issue became how many

channels for each terrestrial TV station should cable

operators be required to carry, one or many?

In response, the NCC in 2012 tentatively adopted a

resolution that cable operators shall carry only one

channel (the main channel) per each wireless TV

station although a new must-carry rule still needs

to be passed by the legislature to solve the issue

ultimately.

The executive branch in 2012 then proposed a

must-carry amendment according to which all

channels of public TV should be carried, along with

one channel of each commercial TV. Although the

industry of cable TV operators essentially agreed

with the executive branch, the wireless TV industry

asked for more than that. The wireless industry

provided a proposal which included all channels of

public TV, and two channels of each commercial TV.

The association of cable programming channels,

however, was fiercely opposed, only accepting the

must-carry requirement for public TV and rejecting

any free carriage of commercial TV on the ground

that they are essentially competitors.

Must-carry amendment A (The executive branch)

(industry of cable operators)

Must-carry amendment b(wireless TV industry)

Must-carry amendment C (association of programming

channels)

Section 33Cable TV operators shall carry, without charge, – • all channels of public TV stations• one channel of each private

wireless TV.

Section 33Cable TV operators shall carry, without charge, – • all channels of public TV stations• two channel of each private

wireless TV.

Section 33Cable TV operators shall carry, without charge, – • all channels of public TV stations.

From 2013 to 2015, debates and negotiations

among the concerned parties took place in many

public hearings and, through their agents, in the

parliament. Parties were so divided that eventually

no consensus was reached and none of the

proposed amendments of section 33 passed the

legislature. Thus, the current section 33 of the must-

carry rule remains in place.

Taiwan in View 29

3. “No state/party ownership” rule

The “no state/party ownership” statute became

effective in 2005. It prohibits any government

agencies, political parties, or elected officials

from investing either directly or indirectly in cable

system operators or TV channels. The rule had

an immediate impact on Chunghwa Telecom (the

IPTV operator) which received a cable TV license

in 2004. By that time, the Central Government, via

the Ministry of Transportation and Communication,

controlled 40 percent of the total shares in

Chunghwa Telecom. In response, the NCC had to

create a new regulatory regime, “open platform”, for

Chunghwa Telecom. (Details see supra section 1.2.)

The no state/party ownership rule is so strict that

not even a single share ownership is allowed.

Furthermore, the term “indirectly” is construed so

broadly that even a few government shares in a

shareholder of a shareholder of a shareholder… (no

matter how many tiers) of cable system operators

are still prohibited. Such a rigid rule has rendered

several merger proposals between telecom carriers

and cable MSOs impossible, such as the attempt of

Far Eastone to acquire CNS Cable. This was because,

when a small number of shares of telecom carriers

in a stock market are acquired by any state-owned

corporations, such carriers are deemed to have

state ownership and thus shall not control any cable

operators. The executive branch in 2012 proposed

an amendment to relax the state/party ownership

rule – setting a new threshold of 10 percent of total

shares of cable operators. However, the amendment

did not pass the legislature, and for now the no

state/party ownership rule remains rigid and

absolute. Recently in May 2017, Vice Chairman P.T.

Wong of the NCC announced that the Commission

will propose a relaxing amendment again.

4. “Digital Communication Act” and network

neutrality

In April 2017, the NCC drafted a new “Digital

Communication Act” (DCA), in which a few sections

seem to address the issue of neutrality. The term

“net neutrality” may have different meanings,

and needs a good definition. The U.S. Federal

Communications Commission in its 2015 Rule

defines “net neutrality” with three principles – no

blocking, no throttling, and no paid prioritization (no

fast lanes).

Section 6 of the draft DCA provides that ISPs shall

manage network communication and access to

achieve “best performance”, and “shall not impose

any limitations which are obviously unfair”. Section 7

of the Act demands ISPs manage network resources

in a reasonable manner, and shall not impose

“barriers to interfere with choices of users”. This

section resembles the FCC’s “no blocking” rule,

which requires that an ISP may not block lawful

content, applications, or services. The meaning of

“best performance” in section 6 is quite unclear, and

therefore nothing can be said as to whether section

6 is for or against the “no fast lanes” rule.

The draft is expected to be discussed in the

Legislative Yuan later this year.

30 Taiwan in View

Lack of must-have digital content and applications

Table 1.4 shows that the percentage of digital

premium service subscriptions continuously

dwindles when more and more subscribers are

able to receive other (non-premium) service

digitally. Only 28.44 percent of cable TV households

subscribe to premium services beyond the basic

one. This means that cable TV subscribers are

less interested in obtaining premium services

even if they are able to do so. This pattern may

jeopardize the financial health of the industry in

the future because – should it persist – revenue

streams are constrained to only those of the basic

tier. Likewise, the IPTV penetration rate remains

at 15 percent through recent years. It is said that

CHT MoD lacks the mainstream news channels

that can drive subscriptions. Therefore, it seems

that a priority for the pay-TV industry must lie in

developing and providing must-have content and

applications.

Copyright and piracy concerns

The intensive competition among the OTT services

highlights the winning formulas: either mass

content; or, exclusive must-have content. The

MSOs and CHT consequently engage in seeking

to acquire content rights. Nevertheless, both

mass content and exclusive must-have content

are costly to acquire. Unrestrained piracy, which

sees copyrighted content illegally accessible via

cross-border websites, further deteriorates the

business model. Like OTT service providers, pay-

TV operators are now beginning to consider the

production of their own content as a hedge against

piracy and pricey copyrights.

Substitute relationship between pay-TV and OTT services?

As can be seen in section III b. the data corroborates

that the rise of OTT services until now has not

caused substitution impacts on cable TV and IPTV.

It seems that we can assume a complementary

relationship between them.

However, on closer examination, generational

differences appear important. The revolutionary

change in viewing habits is particularly evident

among young generations. Graph 2.19 showed

that the largest group of OTT users are young

women aged 18-34, about 43 percent of total

users. Together with males aged 18-34, the age

group of 18-34 accounts for almost 70 percent of

OTT users.

VI. the future and challenGes for Pay-tV serVIces

Taiwan in View 31

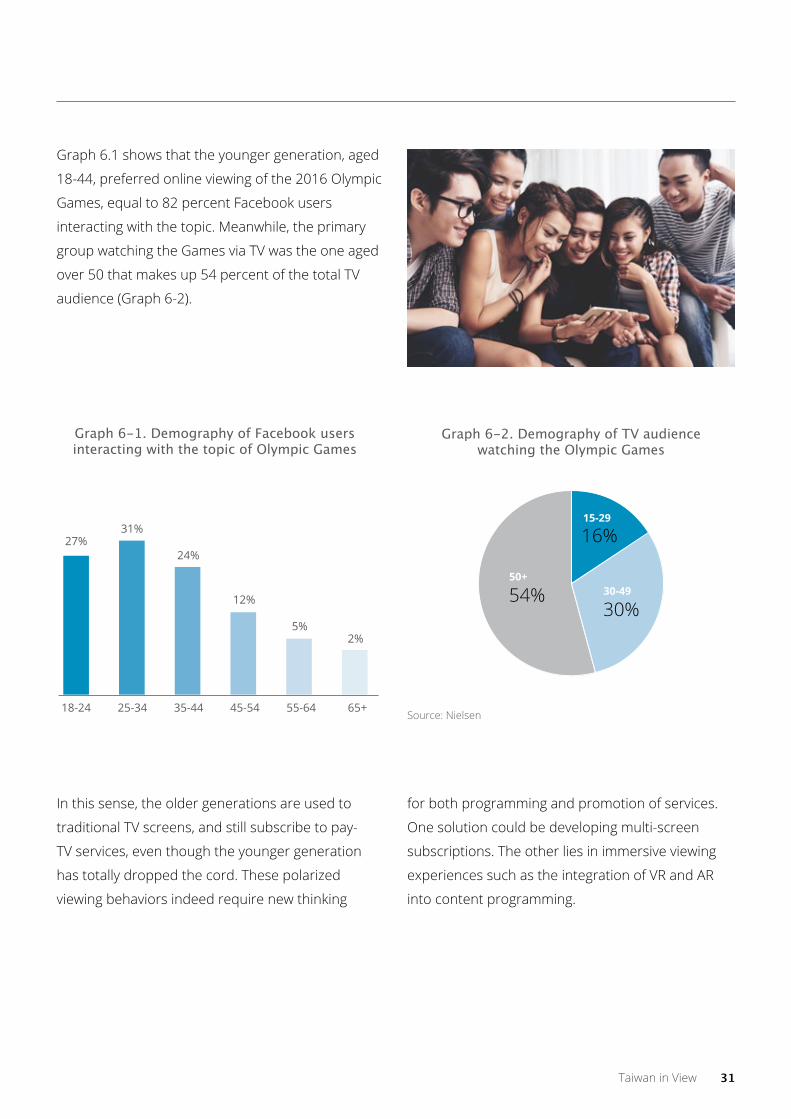

Graph 6.1 shows that the younger generation, aged

18-44, preferred online viewing of the 2016 Olympic

Games, equal to 82 percent Facebook users

interacting with the topic. Meanwhile, the primary

group watching the Games via TV was the one aged

over 50 that makes up 54 percent of the total TV

audience (Graph 6-2).

18-24

27%

25-34 35-44 45-54 55-64 65+

31%

24%

12%

5%2%

Graph 6-1. Demography of Facebook users interacting with the topic of Olympic Games

Graph 6-2. demography of tV audience watching the olympic Games

Source: Nielsen

15-29

16%

30-4950+

30%54%

In this sense, the older generations are used to

traditional TV screens, and still subscribe to pay-

TV services, even though the younger generation

has totally dropped the cord. These polarized

viewing behaviors indeed require new thinking

for both programming and promotion of services.

One solution could be developing multi-screen

subscriptions. The other lies in immersive viewing

experiences such as the integration of VR and AR

into content programming.

32 Taiwan in View

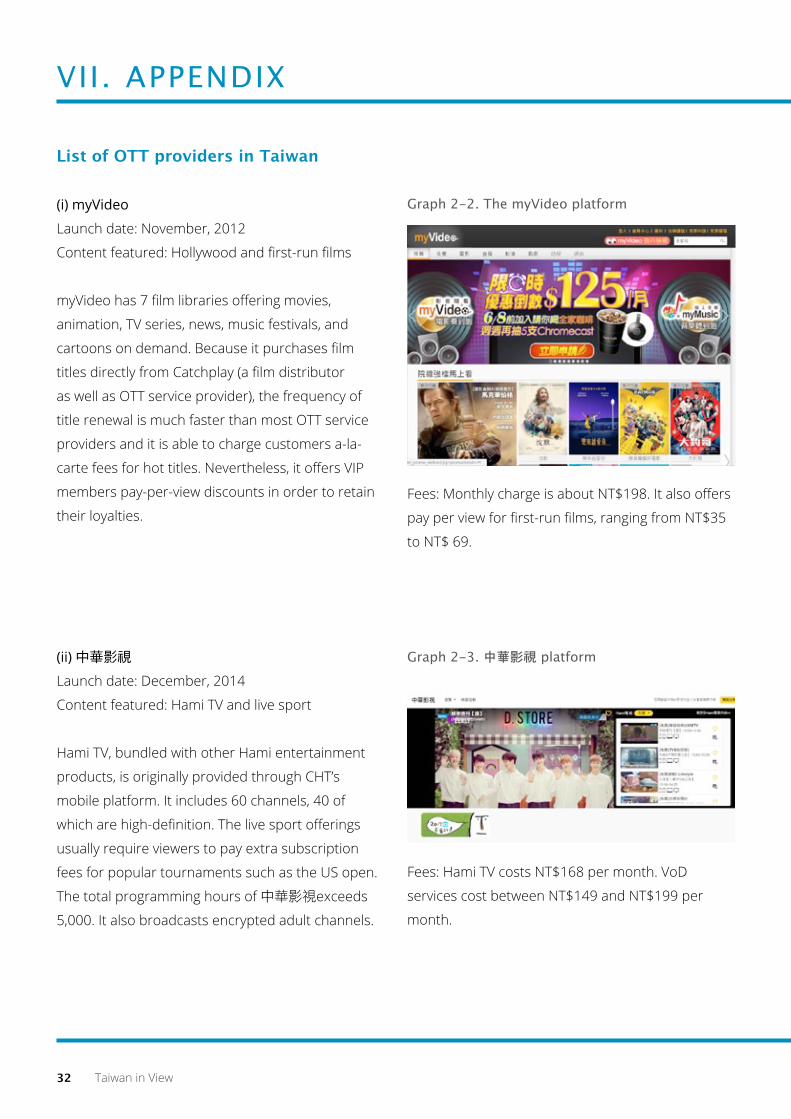

List of OTT providers in Taiwan

(i) myVideo

Launch date: November, 2012

Content featured: Hollywood and first-run films

myVideo has 7 film libraries offering movies,

animation, TV series, news, music festivals, and

cartoons on demand. Because it purchases film

titles directly from Catchplay (a film distributor

as well as OTT service provider), the frequency of

title renewal is much faster than most OTT service

providers and it is able to charge customers a-la-

carte fees for hot titles. Nevertheless, it offers VIP

members pay-per-view discounts in order to retain

their loyalties.

VII. aPPendIx

Graph 2-2. the myVideo platform

Fees: Monthly charge is about NT$198. It also offers

pay per view for first-run films, ranging from NT$35

to NT$ 69.

(ii) 中華影視

Launch date: December, 2014

Content featured: Hami TV and live sport

Hami TV, bundled with other Hami entertainment

products, is originally provided through CHT’s

mobile platform. It includes 60 channels, 40 of

which are high-definition. The live sport offerings

usually require viewers to pay extra subscription

fees for popular tournaments such as the US open.

The total programming hours of 中華影視exceeds

5,000. It also broadcasts encrypted adult channels.

Graph 2-3. 中華影視 platform

Fees: Hami TV costs NT$168 per month. VoD

services cost between NT$149 and NT$199 per

month.

Taiwan in View 33

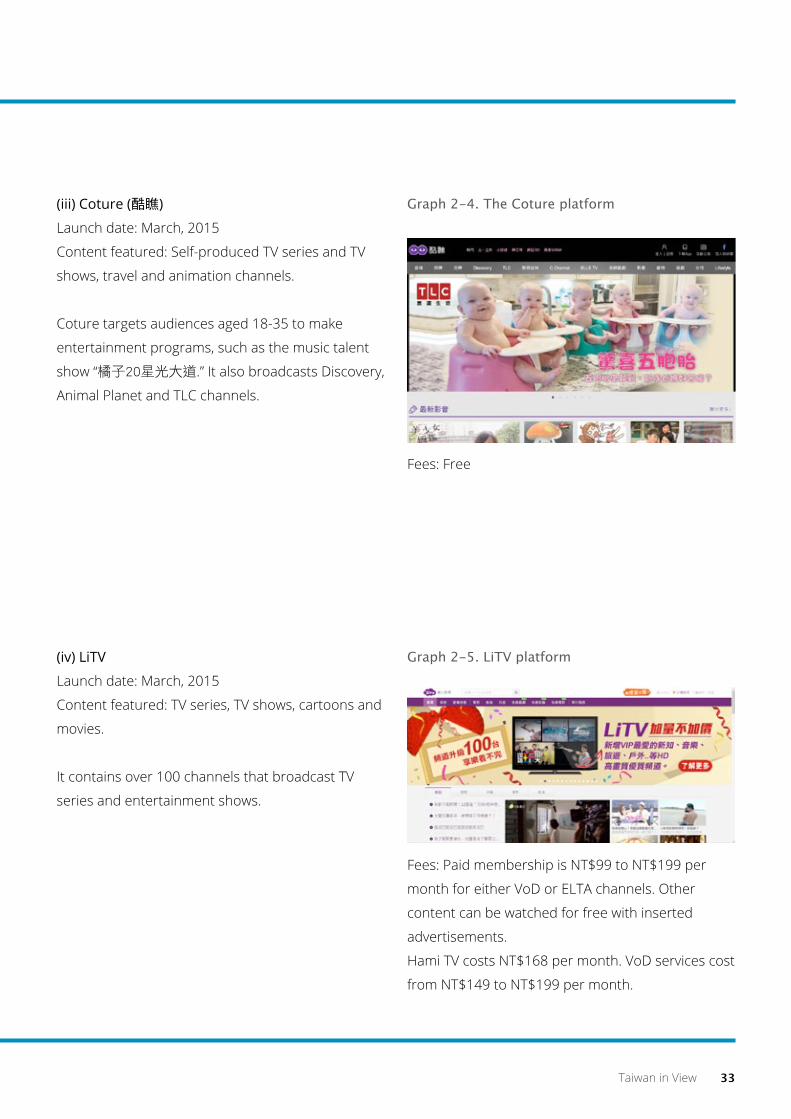

(iii) Coture (酷瞧)

Launch date: March, 2015

Content featured: Self-produced TV series and TV

shows, travel and animation channels.

Coture targets audiences aged 18-35 to make

entertainment programs, such as the music talent

show “橘子20星光大道.” It also broadcasts Discovery,

Animal Planet and TLC channels.

Graph 2-4. the coture platform

Fees: Free

(iv) LiTV

Launch date: March, 2015

Content featured: TV series, TV shows, cartoons and

movies.

It contains over 100 channels that broadcast TV

series and entertainment shows.

Graph 2-5. litV platform

Fees: Paid membership is NT$99 to NT$199 per

month for either VoD or ELTA channels. Other

content can be watched for free with inserted

advertisements.

Hami TV costs NT$168 per month. VoD services cost

from NT$149 to NT$199 per month.

34 Taiwan in View

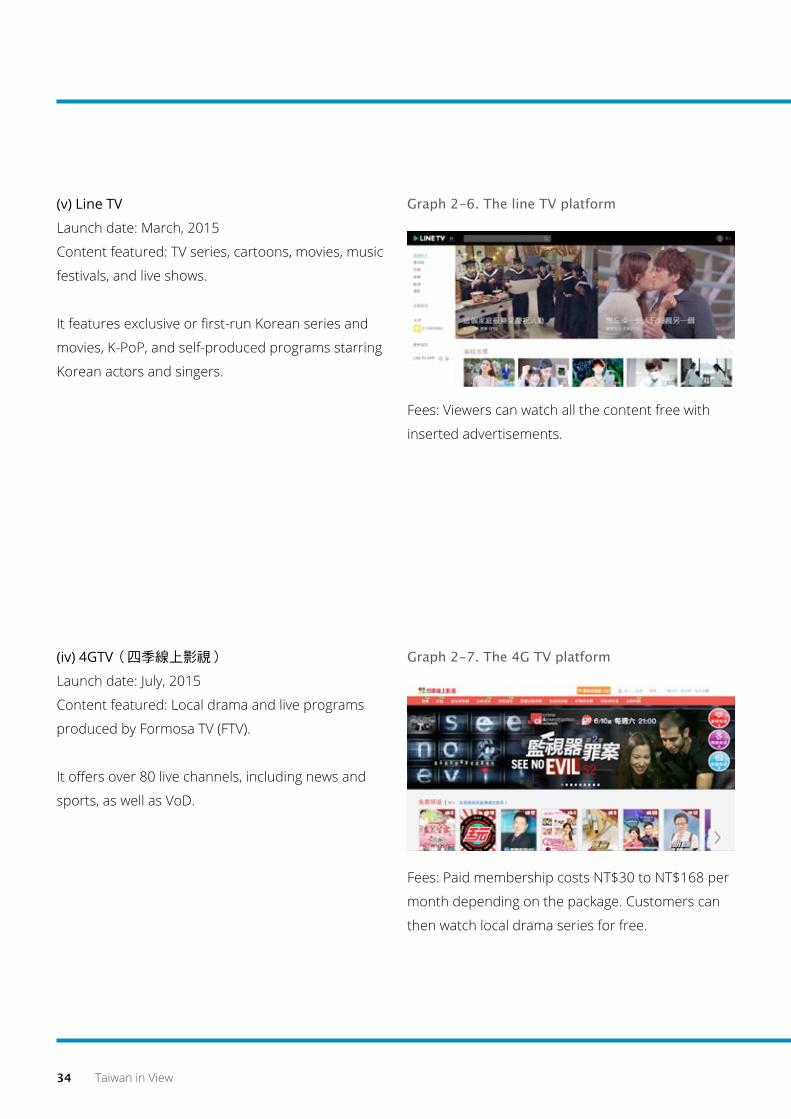

(v) Line TV

Launch date: March, 2015

Content featured: TV series, cartoons, movies, music

festivals, and live shows.

It features exclusive or first-run Korean series and

movies, K-PoP, and self-produced programs starring

Korean actors and singers.

Graph 2-6. the line tV platform

Fees: Viewers can watch all the content free with

inserted advertisements.

(iv) 4GTV(四季線上影視)

Launch date: July, 2015

Content featured: Local drama and live programs

produced by Formosa TV (FTV).

It offers over 80 live channels, including news and

sports, as well as VoD.

Graph 2-7. the 4G tV platform

Fees: Paid membership costs NT$30 to NT$168 per

month depending on the package. Customers can

then watch local drama series for free.

Taiwan in View 35

(vii) CHOCO TV

Launch date: September, 2015

Content featured: TV drama series

It offers a variety of Taiwanese, Korean, and Chinese

series, although the titles may not be up to date. It

also invests in and produces short TV series whose

topics the mainstream TV channels do not yet dare

to touch. The series include “Oba (我們是歐爸),”

“Unknown Lovers (X情人),” and “在一起,就好.”Fees: Free

Graph 2-8. the choco tV platform

(viii) friDay影音

Launch date: November, 2015

Content featured: TV series, entertainment shows,

movies, and live channels

It offers Taiwanese, Korean, and Chinese TV series

and films. However, the film titles are mostly second

run.

Fees: membership is NT$199 per month.

Graph 2-9. the friday影音 platform

36 Taiwan in View

(ix)Netflix

Launch date: January, 2016

Content featured: self-produced TV series and films.

Until recently, Netflix provided similar programming

across the globe. It is now starting to differentiate

individual markets by providing local content.

Fees: Netflix charges subscribers NT$240 for SD

quality and a single device; NT$270 for HD quality

and two devices; and NT$300 for HD quality and

four devices. It offers one-month free trial accounts.

Graph 2-10. The Netflix platform

(x) CatchPlay

Launch date: March, 2016

Content: Hollywood and first-run movies.

As film distributor, Catchplay is able to present its

members with over 15,000 titles via its OTT platform

and to provide a clear catalogue that reduces the

viewers’ burden in searching for titles they desire. It

even offers film commentaries written by film critics

on its platform. Fees: It costs NT$250 per month to sign up for the

“movie lovers” membership that allows members

unlimited viewing of films. However, some selected

first-run films require pay-per-view.

Graph 2-11. the catchplay platform

Taiwan in View 37

b.11 iqiyi (愛奇藝)

Launch date: March, 2016

Content featured: Chinese TV series, TV shows, and

films.

iqiyi Taiwan broadcasts 13 channels, including

drama, films, shows, animation, comedy,

documentary, travel, and self-produced programs. It

also offers Taiwanese and Hong Kong drama series.

Graph 2-12. the iqiyi platform

Fees: VIP membership costs NT$239 per month and

allows unlimited viewing of all programs without

advertisements, whilst the unpaid members watch

programs with inserted advertisements.

(xi) Vidol

Launch date: March, 2015

Content featured: SET TV series, SET TV shows, and

live channels.

SET TV is famous for self-produced Taiwanese

drama. It is the OTT service enjoying the highest

number of self-produced programming hours.

Vidol also does live broadcasts of cast members

interacting with fans and offers exclusive off-screen

clips, alongside the screening of the TV series, in

order to create “a fan economy”.

Fees: It costs members NT$169 per month to watch

all the content without inserted advertisements.

Free viewing is allowed in exchange for inserted

advertisements.

Graph 2-13 the Vidol platform

38 Taiwan in View

(xii) 13 KKTV

Launch date: July, 2016

Content featured: Korean, Taiwanese, Chinese, and

Japanese TV series.

Invested by the parent company of KKbox (the

streaming music service, equivalent to Spotify),

KKTV provides better viewing quality than the rest

of the OTT service providers, including 1080p Full

HD, seamless handover to other devices, offline

watching, etc.

Graph 2-14. the kktV platform

Fees: VIP membership costs NT$169 per month,

with a one-month free trial account.

(xiii) yahoo! TV

Launch date: July, 2016

Content featured: live programs.

Yahoo! TV’s programs mostly cover news,

entertainment, sports and leisure.

Fees: Free

Graph 2-15. the yahoo! tV platform

Taiwan in View 39

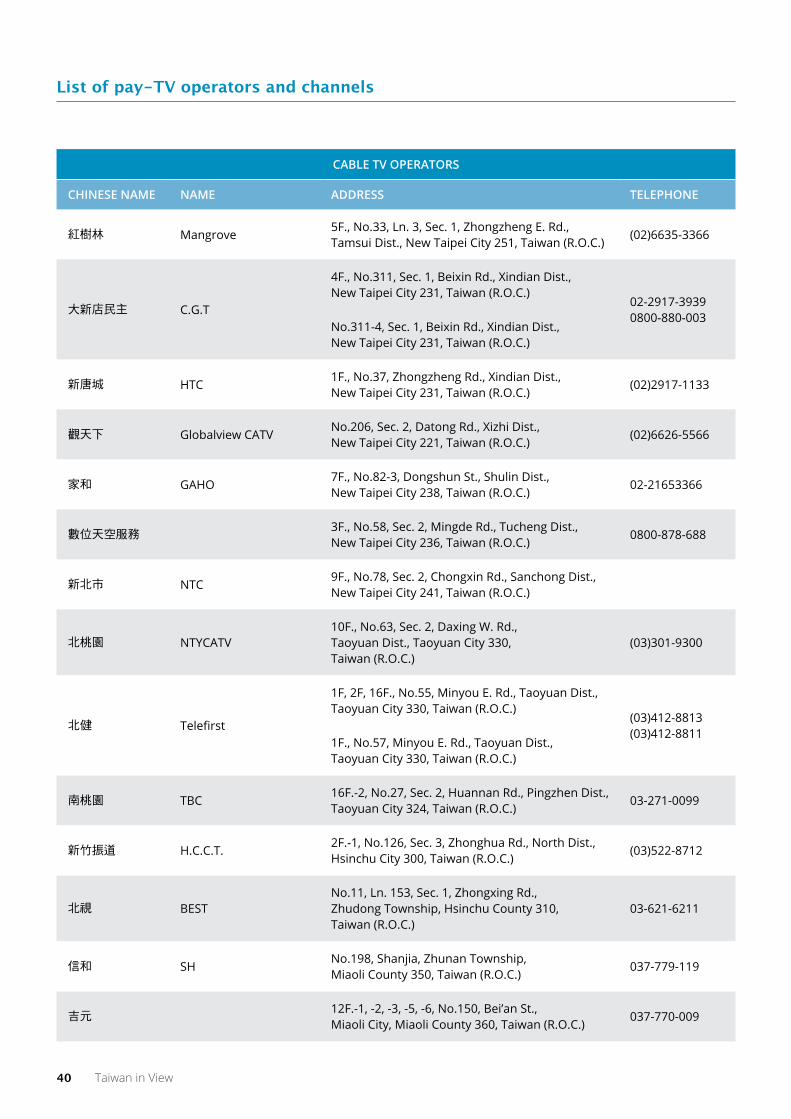

CAbLE TV OPERATORS

CHINESE NAME NAME ADDRESS TELEPHONE

吉隆 ProsperityNo.6, Chongxiao St., Qidu Dist., Keelung City 206, Taiwan (R.O.C.)

02-216531250800-050-027

長德 Everlasting1F., No.345, Jilin Rd., Zhongshan Dist., Taipei City 104, Taiwan (R.O.C.)

02-216531530800-088-909

金頻道 KINGCATV8F., No.260, Sec. 2, Bade Rd., Zhongshan Dist., Taipei City 104, Taiwan (R.O.C.)

(02)8791-1234

大安文山 DAWSNo.15, Ln. 204, Sec. 2, Muzha Rd., Wenshan Dist., Taipei City 116, Taiwan (R.O.C.)

(02)8791-1000

萬象1F., No.96, Ln. 109, Sec. 4, Xinglong Rd., Wenshan Dist., Taipei City 116, Taiwan (R.O.C.)

02-216531560800-600-608

寶福 POWER FULL4F., No.151, Sec. 2, Changsha St., Wanhua Dist., Taipei City 108, Taiwan (R.O.C.)

2311-63780800363999

聯維 NET WAVE4F., No.91, Sec. 2, Changsha St., Wanhua Dist., Taipei City 108, Taiwan (R.O.C.)

02-23118899 0800231021

陽明山 YMS5F.-1, No.13, Sec. 2, Beitou Rd., Beitou Dist., Taipei City 112, Taiwan (R.O.C.)

(02)8791-0099

新台北 NTTV12F.-2, No.412, Sec. 5, Zhongxiao E. Rd., Xinyi Dist., Taipei City 110, Taiwan (R.O.C.)

(02)8792-1999

麗冠 Liguan3F.-1, No.399, Ruiguang Rd., Neihu Dist., Taipei City 114, Taiwan (R.O.C.)

02-216531570800-222-868

北都數位 Bei Du5F., No.260, Sec. 2, Bade Rd., Zhongshan Dist., Taipei City 104, Taiwan (R.O.C.)

0809-096-111

永佳樂 Y. J. L10F.,No.651-5, Zhongzheng Rd., Xinzhuang Dist., New Taipei City 242, Taiwan (R.O.C.)

(02)6635-6699

大豐 Dafeng TV Ltd.5F., No.207, Sec. 2, Zhonghua Rd., Tucheng Dist., New Taipei City 236, Taiwan (R.O.C.)

02-82538999

全國數位 DCTV13F., No.210, Sec. 1, Sanmin Rd., Banqiao Dist., New Taipei City 220, Taiwan (R.O.C.)

02-8071-7039

台灣數位寬頻 DigiTai TV9F., No.5, Ln. 163, Xinyi Rd., Banqiao Dist., New Taipei City 220, Taiwan (R.O.C.)

02-28538988

新視波 NVW

16F., No.343, Zhonghe Rd., Yonghe Dist., New Taipei City 234, Taiwan (R.O.C.)

02-2165368816F., No.345, Zhonghe Rd., Yonghe Dist., New Taipei City 234, Taiwan (R.O.C.)

天外天 TWT10F., No.78, Sec. 2, Chongxin Rd., Sanchong Dist., New Taipei City 241, Taiwan (R.O.C.)

(02)2974-55110800-213-061

List of pay-TV operators and channels

40 Taiwan in View

CAbLE TV OPERATORS

CHINESE NAME NAME ADDRESS TELEPHONE

紅樹林 Mangrove5F., No.33, Ln. 3, Sec. 1, Zhongzheng E. Rd., Tamsui Dist., New Taipei City 251, Taiwan (R.O.C.)

(02)6635-3366

大新店民主 C.G.T

4F., No.311, Sec. 1, Beixin Rd., Xindian Dist., New Taipei City 231, Taiwan (R.O.C.)

02-2917-3939 0800-880-003

No.311-4, Sec. 1, Beixin Rd., Xindian Dist., New Taipei City 231, Taiwan (R.O.C.)

新唐城 HTC1F., No.37, Zhongzheng Rd., Xindian Dist., New Taipei City 231, Taiwan (R.O.C.)

(02)2917-1133

觀天下 Globalview CATVNo.206, Sec. 2, Datong Rd., Xizhi Dist., New Taipei City 221, Taiwan (R.O.C.)

(02)6626-5566

家和 GAHO7F., No.82-3, Dongshun St., Shulin Dist., New Taipei City 238, Taiwan (R.O.C.)

02-21653366

數位天空服務3F., No.58, Sec. 2, Mingde Rd., Tucheng Dist., New Taipei City 236, Taiwan (R.O.C.)

0800-878-688

新北市 NTC9F., No.78, Sec. 2, Chongxin Rd., Sanchong Dist., New Taipei City 241, Taiwan (R.O.C.)

北桃園 NTYCATV10F., No.63, Sec. 2, Daxing W. Rd., Taoyuan Dist., Taoyuan City 330, Taiwan (R.O.C.)

(03)301-9300

北健 Telefirst

1F, 2F, 16F., No.55, Minyou E. Rd., Taoyuan Dist., Taoyuan City 330, Taiwan (R.O.C.)

(03)412-8813 (03)412-8811

1F., No.57, Minyou E. Rd., Taoyuan Dist., Taoyuan City 330, Taiwan (R.O.C.)

南桃園 TBC16F.-2, No.27, Sec. 2, Huannan Rd., Pingzhen Dist., Taoyuan City 324, Taiwan (R.O.C.)

03-271-0099

新竹振道 H.C.C.T.2F.-1, No.126, Sec. 3, Zhonghua Rd., North Dist., Hsinchu City 300, Taiwan (R.O.C.)

(03)522-8712

北視 BESTNo.11, Ln. 153, Sec. 1, Zhongxing Rd., Zhudong Township, Hsinchu County 310, Taiwan (R.O.C.)

03-621-6211

信和 SHNo.198, Shanjia, Zhunan Township, Miaoli County 350, Taiwan (R.O.C.)

037-779-119

吉元12F.-1, -2, -3, -5, -6, No.150, Bei’an St., Miaoli City, Miaoli County 360, Taiwan (R.O.C.)

037-770-009

List of pay-TV operators and channels

Taiwan in View 41

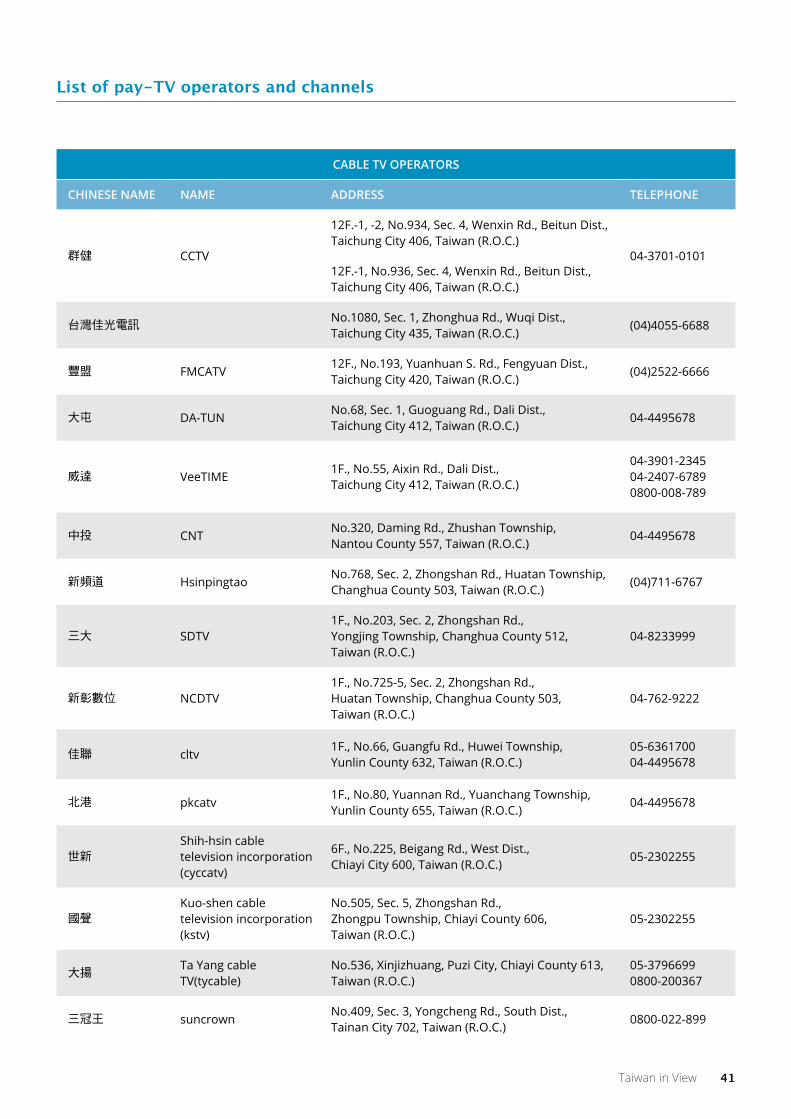

CAbLE TV OPERATORS

CHINESE NAME NAME ADDRESS TELEPHONE

群健 CCTV

12F.-1, -2, No.934, Sec. 4, Wenxin Rd., Beitun Dist., Taichung City 406, Taiwan (R.O.C.)

04-3701-010112F.-1, No.936, Sec. 4, Wenxin Rd., Beitun Dist., Taichung City 406, Taiwan (R.O.C.)

台灣佳光電訊No.1080, Sec. 1, Zhonghua Rd., Wuqi Dist., Taichung City 435, Taiwan (R.O.C.)

(04)4055-6688

豐盟 FMCATV12F., No.193, Yuanhuan S. Rd., Fengyuan Dist., Taichung City 420, Taiwan (R.O.C.)

(04)2522-6666

大屯 DA-TUNNo.68, Sec. 1, Guoguang Rd., Dali Dist., Taichung City 412, Taiwan (R.O.C.)

04-4495678

威達 VeeTIME1F., No.55, Aixin Rd., Dali Dist., Taichung City 412, Taiwan (R.O.C.)

04-3901-234504-2407-67890800-008-789

中投 CNTNo.320, Daming Rd., Zhushan Township, Nantou County 557, Taiwan (R.O.C.)

04-4495678

新頻道 HsinpingtaoNo.768, Sec. 2, Zhongshan Rd., Huatan Township, Changhua County 503, Taiwan (R.O.C.)

(04)711-6767

三大 SDTV1F., No.203, Sec. 2, Zhongshan Rd., Yongjing Township, Changhua County 512, Taiwan (R.O.C.)

04-8233999

新彰數位 NCDTV1F., No.725-5, Sec. 2, Zhongshan Rd., Huatan Township, Changhua County 503, Taiwan (R.O.C.)

04-762-9222

佳聯 cltv1F., No.66, Guangfu Rd., Huwei Township, Yunlin County 632, Taiwan (R.O.C.)

05-636170004-4495678

北港 pkcatv1F., No.80, Yuannan Rd., Yuanchang Township, Yunlin County 655, Taiwan (R.O.C.)

04-4495678

世新Shih-hsin cable television incorporation(cyccatv)

6F., No.225, Beigang Rd., West Dist., Chiayi City 600, Taiwan (R.O.C.)

05-2302255

國聲Kuo-shen cabletelevision incorporation(kstv)

No.505, Sec. 5, Zhongshan Rd., Zhongpu Township, Chiayi County 606, Taiwan (R.O.C.)

05-2302255

大揚Ta Yang cable TV(tycable)

No.536, Xinjizhuang, Puzi City, Chiayi County 613, Taiwan (R.O.C.)

05-37966990800-200367

三冠王 suncrownNo.409, Sec. 3, Yongcheng Rd., South Dist., Tainan City 702, Taiwan (R.O.C.)

0800-022-899

List of pay-TV operators and channels

42 Taiwan in View

CAbLE TV OPERATORS

CHINESE NAME NAME ADDRESS TELEPHONE

雙子星 twinstarsNo.60, Ln. 186, Beicheng Rd., North Dist., Tainan City 704, Taiwan (R.O.C.)

02-412-88120800281999

新永安 HYA Cable TvNo.3, Ln. 95, Guangxing St., Yongkang Dist., Tainan City 710, Taiwan (R.O.C.)

06-27189580800-005988

南天 NtnNo.537, Sec. 2, Changrong Rd., Xinying Dist., Tainan City 730, Taiwan (R.O.C.)

(06)656-7587

慶聯 clcatvNo.42, Liwen Rd., Zuoying Dist., Kaohsiung City 813, Taiwan (R.O.C.)

(07)340-1001

港都 gdcatv3F., No.59, Minquan 1st Rd., Lingya Dist., Kaohsiung City 802, Taiwan (R.O.C.)

(07)340-1998

南國NAN-KUO CATV CO., Ltd.

No.158, Gangshan Rd., Gangshan Dist., Kaohsiung City 820, Taiwan (R.O.C.)

07-6227737

鳳信 phoenixcatvNo.312, Fengping 1st Rd., Daliao Dist., Kaohsiung City 831, Taiwan (R.O.C.)

(07)969-7011

新高雄 NKHTV30F.-1, No.175, Zhongzheng 2nd Rd., Lingya Dist., Kaohsiung City 802, Taiwan (R.O.C.)

0800-250-999

觀昇 ksgNo.10, Gongye Rd., Pingtung City, Pingtung County 900, Taiwan (R.O.C.)

(08)723-4000

屏南No.26-69, Chuantou Rd., Donggang Township, Pingtung County 928, Taiwan (R.O.C.)

(08)-8354567

東台 ttcatv7F., No.396, Changsha St., Taitung City, Taitung County 950, Taiwan (R.O.C.)

089-347450

聯禾 unioncatvNo.179, Sec. 1, Nuzhong Rd., Yilan City, Yilan County 260, Taiwan (R.O.C.)

(03)905-7999

洄瀾Hualien Cable Tv Network. (hlcatv)

No.135, Sec. 1, Ji’an Rd., Ji’an Township, Hualien County 973, Taiwan (R.O.C.)

0800-529-999

東亞T.Y. CableCO., Ltd.

No.365-1, Zhonghua Rd., Yuli Township, Hualien County 981, Taiwan (R.O.C.)

03-888-276503-888-2591

澎湖Penghu CableTV.CO.LTD

2F, 3F., No.17, Zhongzheng Rd., Magong City, Penghu County 880, Taiwan (R.O.C.)

06-9261234

東台播送 ttbNo.1, Zhongxiao Rd., Chishang Township, Taitung County 958, Taiwan (R.O.C.)

089-854-686

名城事業1F., No.43, 44, Ren’aixincun, Jinning Township, Kinmen County 892, Taiwan (R.O.C.)

08 231 2345

祥通播送No.88, Fuwo Vil., Nangan Township, Lienchiang County 209, Taiwan (R.O.C.)

List of pay-TV operators and channels

Taiwan in View 43

(SATELLITE) CHANNEL PROGRAMMERS

CHINESE NAME NAME ADDRESS TELEPHONE

九太科技股份

有限公司JEOU TAI TECHNOLOGY

CO,LTD3F.-3, No.268, Liancheng Rd., Zhonghe Dist., New Taipei City 235, Taiwan (R.O.C.)

02-8228-0678

八大電視股份

有限公司GTV

No.455, Ruiguang Rd., Neihu Dist., Taipei City 114, Taiwan (R.O.C.)

02-2650-6666

十方法界實業

股份有限公司COSMOS BUDDHIST

MISSIONARY TV3F., No.247, Minsheng 1st Rd., Xinxing Dist., Kaohsiung City 800, Taiwan (R.O.C.)

07-2229-665

三大有線電視

股份有限公司San Da Cable TV

1F., No.203, Sec. 2, Zhongshan Rd., Yongjing Township, Changhua County 512, Taiwan (R.O.C.)

04-8238-778

三立電視股份

有限公司Sanlih E-Television Inc.

No.159, Sec. 1, Jiuzong Rd., Neihu Dist., Taipei City 114, Taiwan (R.O.C.)

02-8792-8888

大大寬頻股份

有限公司6F., No.209, Sec. 2, Zhonghua Rd., Tucheng Dist., New Taipei City 236, Taiwan (R.O.C.)

02-8253-8866

中天電視股份

有限公司CTI Television Inc.

7F., No.132, Dali St., Wanhua Dist., Taipei City 108, Taiwan (R.O.C.)

02-6600-7766

亞洲衛星電視

股份有限公司AsiaDigital MediaGroup

10F., No.232, Sec. 2, Bade Rd., Zhongshan Dist., Taipei City 104, Taiwan (R.O.C.)

02-2772-8988

幸福空間數位匯

流股份有限公司No.10, Aly. 21, Ln. 106, Sec. 3, Minquan E. Rd., Songshan Dist., Taipei City 105, Taiwan (R.O.C.)

02-2716-1191

東森電視事業

股份有限公司Eastern Broadcasting Co., Ltd.

12F., No.4, Sec. 1, Zhongxiao W. Rd., Zhongzheng Dist., Taipei City 100, Taiwan (R.O.C.)

02-2311-8000

台灣優視媒體科

技股份有限公司Taiwan WinTV Media Co,Ltd

9F., No.260, Sec. 2, Bade Rd., Zhongshan Dist., Taipei City 104, Taiwan (R.O.C.)

02-6638-1602

年代網際事業

股份有限公司Era Group 2F., No.39, Ruihu St., Neihu Dist.,

Taipei City 114, Taiwan (R.O.C.)02-8751-8599

松視事業股份

有限公司SONSEETV

4F.-2, No.12, Ln. 270, Sec. 3, Beishen Rd., Shenkeng Dist., New Taipei City 222, Taiwan (R.O.C.)

02-8662-6003

飛凡傳播股份

有限公司UNIQUE BROADCASTING INC.

5F., No.35, Ln. 11, Guangfu N. Rd., Songshan Dist., Taipei City 105, Taiwan (R.O.C.)

02-2766-2888

國興傳播股份

有限公司goldsuntv

7F.-2, No.16, Sec. 5, Nanjing E. Rd., Songshan Dist., Taipei City 105, Taiwan (R.O.C.)

02-5577-7126

惟達科技股份

有限公司7F., No.531-1, Zhongzheng Rd., Xindian Dist., New Taipei City 231, Taiwan (R.O.C.)

02-8978-2500

List of pay-TV operators and channels

44 Taiwan in View

(SATELLITE) CHANNEL PROGRAMMERS

CHINESE NAME NAME ADDRESS TELEPHONE

博斯數位股份有

限公司sportcast 10F., No.232, Sec. 2, Bade Rd., Zhongshan Dist.,

Taipei City 104, Taiwan (R.O.C.)02-8662-6259

朝禾事業股份有

限公司10F., No.46, Sec. 1, Nanjing E. Rd., Zhongshan Dist., Taipei City 104, Taiwan (R.O.C.)

02-2523-0900

愛爾達科技股份

有限公司ELTA Technology Co., Ltd.

4F., No.41, Sec. 1, Zhonghua Rd., Zhongzheng Dist., Taipei City 100, Taiwan (R.O.C.)

02-2341-1100

超級傳播股份有

限公司12F., No.4, Sec. 1, Zhongxiao W. Rd., Zhongzheng Dist., Taipei City 100, Taiwan (R.O.C.)

02-2388-5918

新唐人亞太電視

股份有限公司New Tang Dynasty Television (NTDTV)

3F.-1, No.102, Songlong Rd., Xinyi Dist., Taipei City 110, Taiwan (R.O.C.)

02-5571-3838

靖天傳播國際事

業股份有限公司Golden 11F., No.19-3, Sanchong Rd., Nangang Dist.,

Taipei City 115, Taiwan (R.O.C.)02-2655-2111

優視傳播股份有

限公司11F., No.98, Zhouzi St., Neihu Dist., Taipei City 114, Taiwan (R.O.C.)

02-6601-2345

緯來電視網股份

有限公司Videoland Television Network

10F., No.1, Sec. 4, Nanjing E. Rd., Songshan Dist., Taipei City 105, Taiwan (R.O.C.)

02-8797-2879

衛星娛樂傳播股

份有限公司Satellite Entertainment Communication Co., Ltd

2F., No.39, Ruihu St., Neihu Dist., Taipei City 114, Taiwan (R.O.C.)

02-5559-9933

龍祥育樂多媒體

股份有限公司

Long-Sheng Entertainment Maltimedia Co, Ltd

3F.-1, No.113, Sec. 2, Hankou St., Wanhua Dist., Taipei City 108, Taiwan (R.O.C.)

02-2361-6022

龍華數位媒體科

技股份有限公司7F., No.232, Sec. 2, Bade Rd., Zhongshan Dist., Taipei City 104, Taiwan (R.O.C.)

02-2731-3899

霹靂國際多媒體

股份有限公司Pili International Multimedia Co., Ltd.

6F., No.209, Sec. 1, Nangang Rd., Nangang Dist., Taipei City 115, Taiwan (R.O.C.)

02-8978-0555

聯利媒體股份有

限公司TVBS Media Inc 11F., No.451, Ruiguang Rd., Neihu Dist.,

Taipei City 114, Taiwan (R.O.C.)02-2162-8168

壹傳媒電視廣播

股份有限公司Next TV Broadcasting Limited

2F., No.16, Sec. 6, Minquan E. Rd., Neihu Dist., Taipei City 114, Taiwan (R.O.C.)

02-7745-9888

List of pay-TV operators and channels

Taiwan in View 45

OTT SERVICE PROVIDERS

CHINESE NAME NAME ADDRESS TELEPHONE

中華電信Chunghwa Telecom Co., Ltd.

No.42, Sec. 1, Ren’ai Rd., Zhongzheng Dist., Taipei City 100, Taiwan (R.O.C.)

02-2344-2485

VidolNo.159, Sec. 1, Jiuzong Rd., Neihu Dist., Taipei City 114, Taiwan (R.O.C.)

02-8792-8888

科科電速股份有

限公司KKTV

1F., No.19-3, Sanchong Rd., Nangang Dist., Taipei City 115, Taiwan (R.O.C.) 02-2655-0369

FriDay1F., No.220, Gangqian Rd., Neihu Dist., Taipei City 114, Taiwan (R.O.C.)

0918-510662(凃吟儀)

歐銻銻(台灣愛

奇藝)7F., No.550, Ruiguang Rd., Neihu Dist., Taipei City 114, Taiwan (R.O.C.)

02-8178-3156

立視線上影視 LiTV8F.-2, No.760, Sec. 4, Bade Rd., Songshan Dist., Taipei City 105, Taiwan (R.O.C.)

02-7707-0708

CHANNEL AGENTS

凱擘股份有限公司 KBRO CO., LTD12F., No.98, Zhouzi St., Neihu Dist., Taipei City 114, Taiwan (R.O.C.)

0809-006-899

允誠多媒體有限

公司Uncheng

No.46, Sec. 1, Nanjing E. Rd., Zhongshan Dist., Taipei City 104, Taiwan (R.O.C.)

02 2571 2210

台灣優視媒體科

技股份

有限公司

Taiwan Win TV Media CO., Ltd

4F., No.96, Zhouzi St., Neihu Dist., Taipei City 114, Taiwan (R.O.C.)

02-6607-5588

佳訊錄影視聽企業

有限公司Jia-Shun

4F., No.69, Sec. 4, Xinyi Rd., Da’an Dist., Taipei City 106, Taiwan (R.O.C.)

02 2705 0633

永鑫多媒體公司 You-ShinRm. 2108, 21F., No.333, Sec. 1, Keelung Rd., Xinyi Dist., Taipei City 110, Taiwan (R.O.C.)

02 2757 6813

List of pay-TV operators and channels

Bibliography Chou, Yuntsai (2014). The stalemate of cable digital switchover:

A study of competition effects and deregulation.

Telecommunications Policy, 38(4), 393-405

NCC (2015a) The NCC Performance Report 2015.

NCC (2015b) The Report on the Consumer Usage in Communications Services, 2015.

About CASBAACASBAA is the Asia Pacific region’s largest non-profit media association, serving the multi-channel audio-visual content creation and distribution industry. Established in 1991, CASBAA has grown with the industry to include digital multichannel television, content, platforms, advertising, and video delivery. Encompassing some 500 million connections within a footprint across the region, CASBAA works to be the authoritative voice for multichannel TV; promoting even-handed and market-friendly regulation, IP protection and revenue growth for subscription and advertising, while promoting global best practices. For more information, visit www.casbaa.com