State of the Video Encoding and Transcoding State of the Video Encoding and Transcoding Industry Industry - 2014 2014 OTT moves towards real monetization for enterprise and M&E alike; OTT moves towards real monetization for enterprise and M&E alike; UltraHD UltraHD and IP redefine contribution; and IP redefine contribution; Analysts run out of cloud puns Analysts run out of cloud puns Avni Rambhia, Industry Principal Digital Media April 15, 2014 © 2014 Frost & Sullivan. All rights reserved. This document contains highly confidential information and is the sole property of Frost & Sullivan. No part of it may be circulated, quoted, copied or otherwise reproduced without the written approval of Frost & Sullivan.

State of the Video and Encoding/Transcoding Industry

Aug 20, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

State of the Video Encoding and Transcoding State of the Video Encoding and Transcoding Industry Industry -- 20142014

OTT moves towards real monetization for enterprise and M&E alike; OTT moves towards real monetization for enterprise and M&E alike; UltraHDUltraHD and IP redefine contribution;and IP redefine contribution;

Analysts run out of cloud punsAnalysts run out of cloud puns

Avni Rambhia, Industry Principal

Digital Media

April 15, 2014

© 2014 Frost & Sullivan. All rights reserved. This document contains highly confidential information and is the sole property of Frost & Sullivan. No part of it may be circulated, quoted, copied or otherwise reproduced without the written approval of Frost & Sullivan.

Today’s Presenter

• Coverage areas:

Avni Rambhia, Industry Principal

Frost & Sullivan

2

• Coverage areas:

•Video encoders & transcoders

•Online video workflows

•Video-enabled devices

•M&E CAS and DRM

•Software DRM and enterprise data security

• Experience: 15 years of R&D, product management and marketing in

media processing and application security

Focus Points

• Market structure: revenue segmentation and forecast

• Drivers and restraints impacting the market

• Growth opportunities: by segment and geography

• Technical trends: today and in the future

• Competitive landscape: by segment

• Strategic imperatives for continued growth

3

• Strategic imperatives for continued growth

• Concluding thoughts

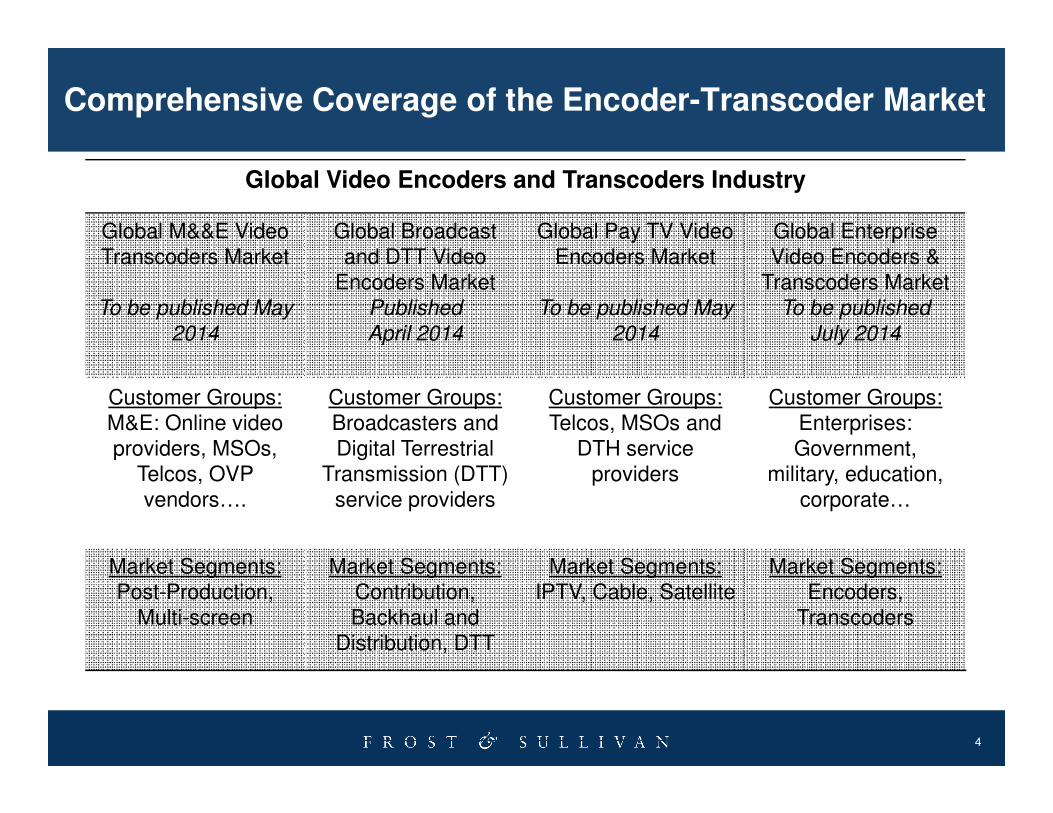

Comprehensive Coverage of the Encoder-Transcoder Market

Global Video Encoders and Transcoders Industry

Global M&&E Video Transcoders Market

To be published May

2014

Global Broadcastand DTT Video

Encoders MarketPublished

April 2014

Global Pay TV Video Encoders Market

To be published May

2014

Global Enterprise Video Encoders &

Transcoders MarketTo be published

July 2014

Customer Groups: Customer Groups: Customer Groups: Customer Groups:

4

Customer Groups:M&E: Online video providers, MSOs,

Telcos, OVP vendors….

Customer Groups:Broadcasters and Digital Terrestrial

Transmission (DTT) service providers

Customer Groups:Telcos, MSOs and

DTH service providers

Customer Groups:Enterprises:Government,

military, education, corporate…

Market Segments:Post-Production,

Multi-screen

Market Segments:Contribution, Backhaul and

Distribution, DTT

Market Segments:IPTV, Cable, Satellite

Market Segments:Encoders,

Transcoders

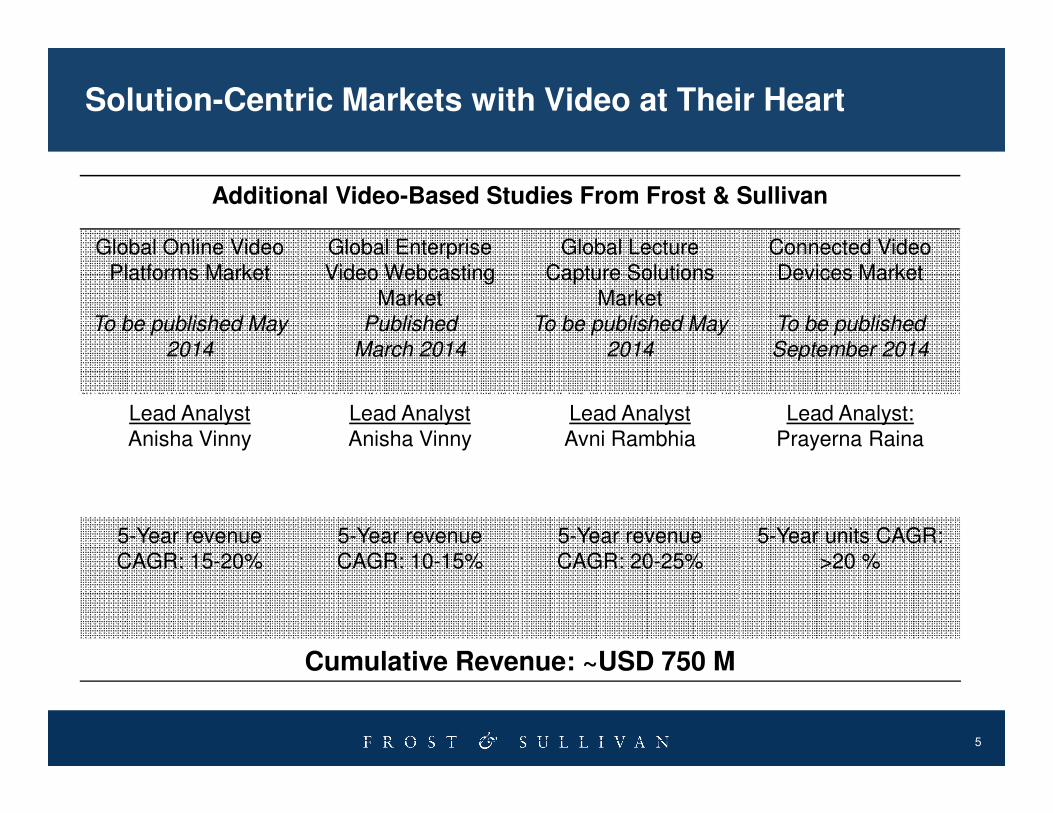

Solution-Centric Markets with Video at Their Heart

Additional Video-Based Studies From Frost & Sullivan

Global Online Video Platforms Market

To be published May

2014

Global Enterprise Video Webcasting

MarketPublished

March 2014

Global Lecture Capture Solutions

MarketTo be published May

2014

Connected Video Devices Market

To be published

September 2014

Lead Analyst Lead Analyst Lead Analyst Lead Analyst:

5

Lead AnalystAnisha Vinny

Lead AnalystAnisha Vinny

Lead AnalystAvni Rambhia

Lead Analyst:Prayerna Raina

5-Year revenue CAGR: 15-20%

5-Year revenue CAGR: 10-15%

5-Year revenue CAGR: 20-25%

5-Year units CAGR: >20 %

Cumulative Revenue: ~USD 750 M

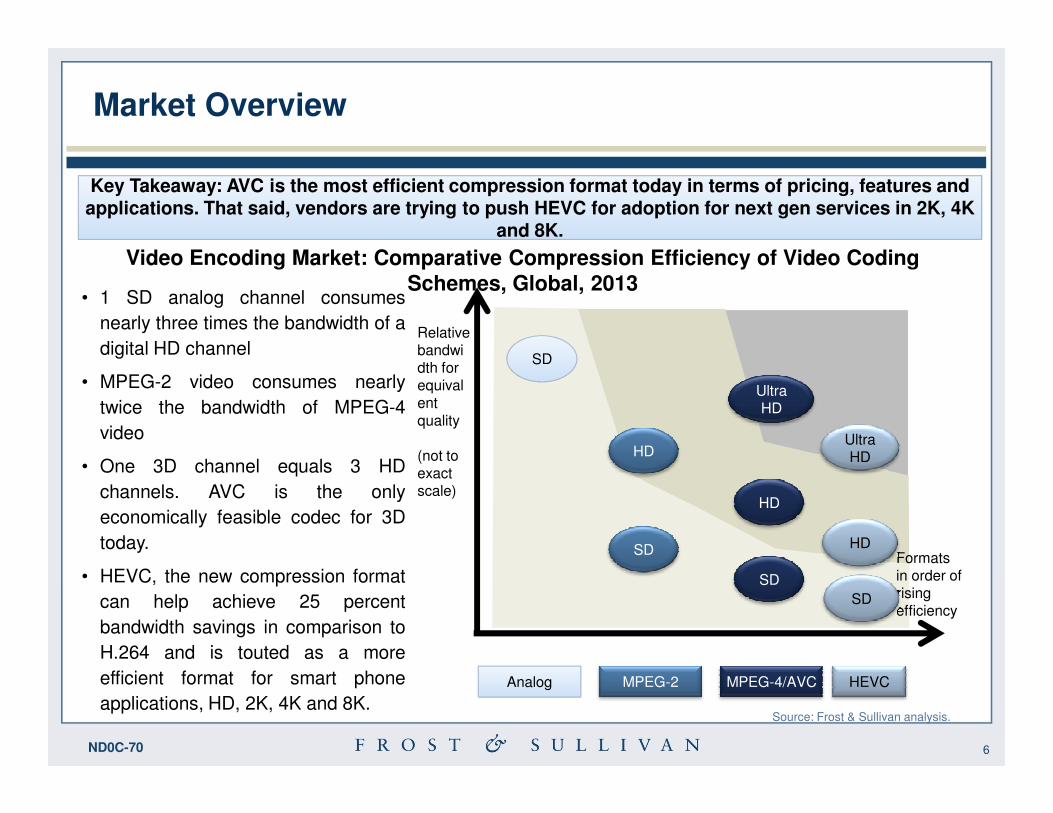

Market Overview

Key Takeaway: AVC is the most efficient compression format today in terms of pricing, features and

and 8K.

Key Takeaway: AVC is the most efficient compression format today in terms of pricing, features and applications. That said, vendors are trying to push HEVC for adoption for next gen services in 2K, 4K

and 8K.

Video Encoding Market: Comparative Compression Efficiency of Video Coding Schemes, Global, 2013

• 1 SD analog channel consumes

nearly three times the bandwidth of a

digital HD channel

• MPEG-2 video consumes nearly

twice the bandwidth of MPEG-4

Relativebandwidth for equivalent

SD

Ultra HD

6ND0C-70

Source: Frost & Sullivan analysis.

twice the bandwidth of MPEG-4

video

• One 3D channel equals 3 HD

channels. AVC is the only

economically feasible codec for 3D

today.

• HEVC, the new compression format

can help achieve 25 percent

bandwidth savings in comparison to

H.264 and is touted as a more

efficient format for smart phone

applications, HD, 2K, 4K and 8K.

ent quality

(not to exact scale)

Formats in order of rising efficiency

Analog MPEG-2 MPEG-4/AVC

SD

HD

HD

SD

HEVC

UltraHD

SD

HD

HD

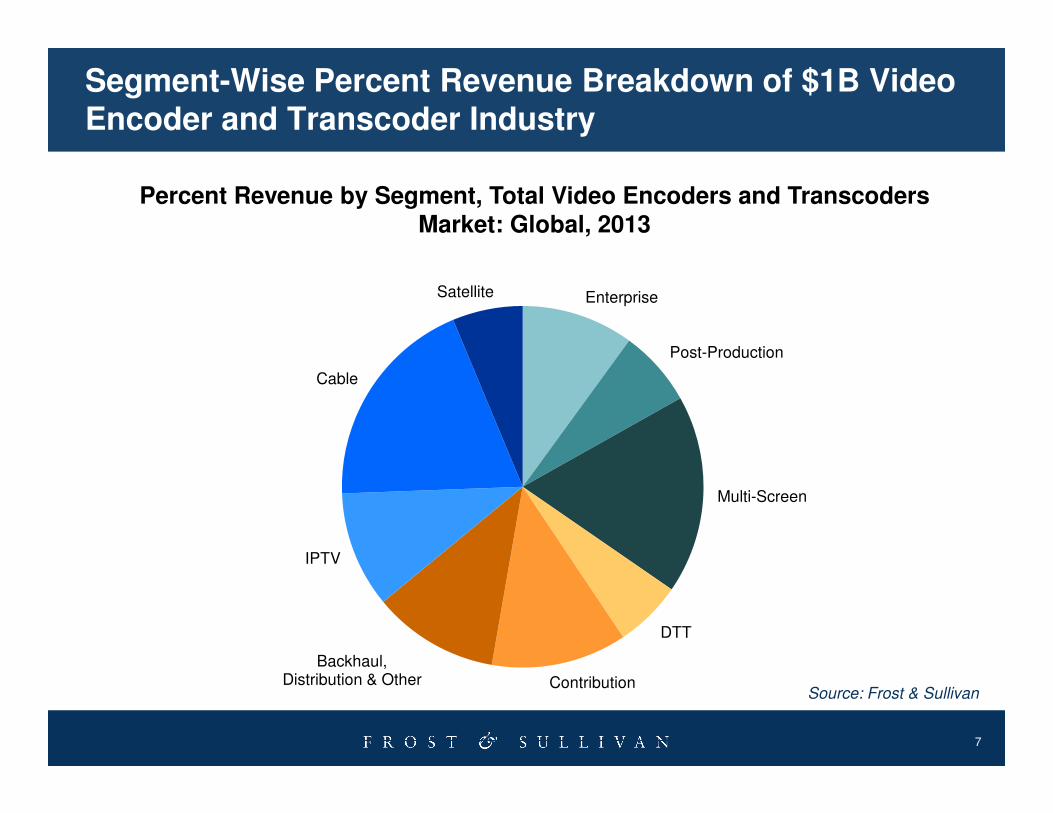

Segment-Wise Percent Revenue Breakdown of $1B Video Encoder and Transcoder Industry

Enterprise

Post-Production

Cable

Satellite

Percent Revenue by Segment, Total Video Encoders and Transcoders Market: Global, 2013

7

Multi-Screen

DTT

Contribution

Backhaul, Distribution & Other

IPTV

Source: Frost & Sullivan

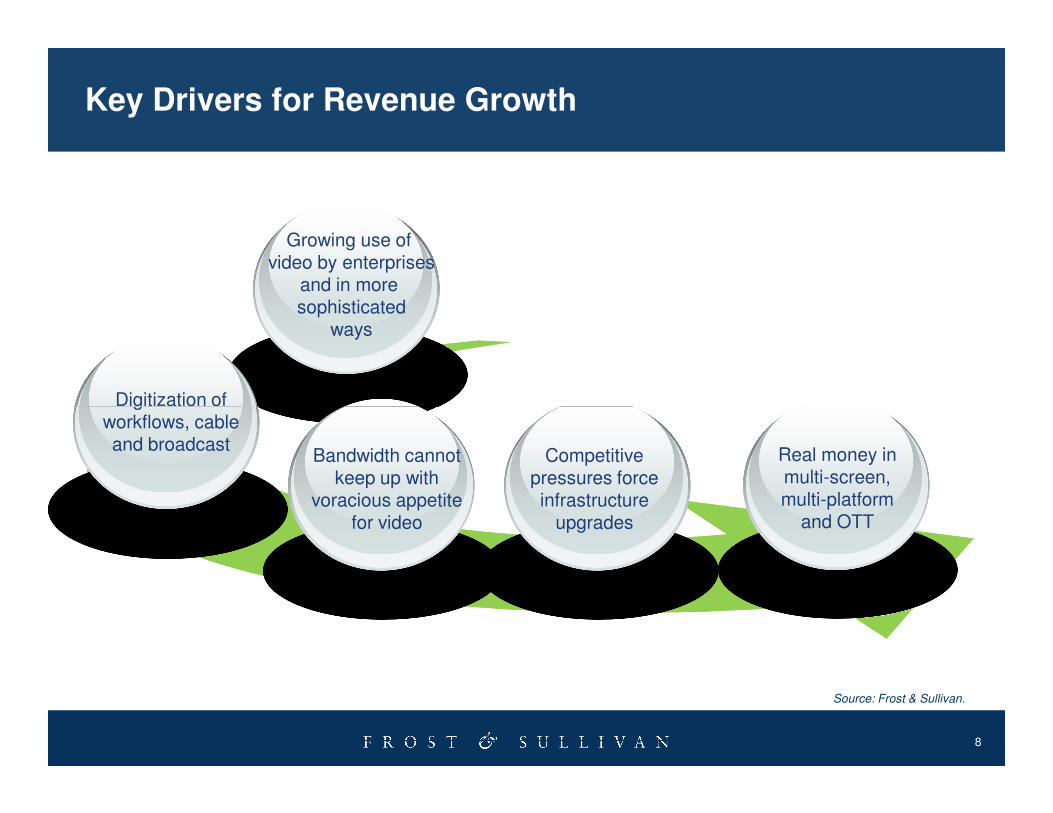

Key Drivers for Revenue Growth

Growing use of video by enterprises

and in more sophisticated

ways

Digitization of

8

Digitization of workflows, cable and broadcast

Competitive pressures force infrastructure

upgrades

Real money in multi-screen, multi-platform

and OTT

Bandwidth cannot keep up with

voracious appetite for video

Source: Frost & Sullivan.

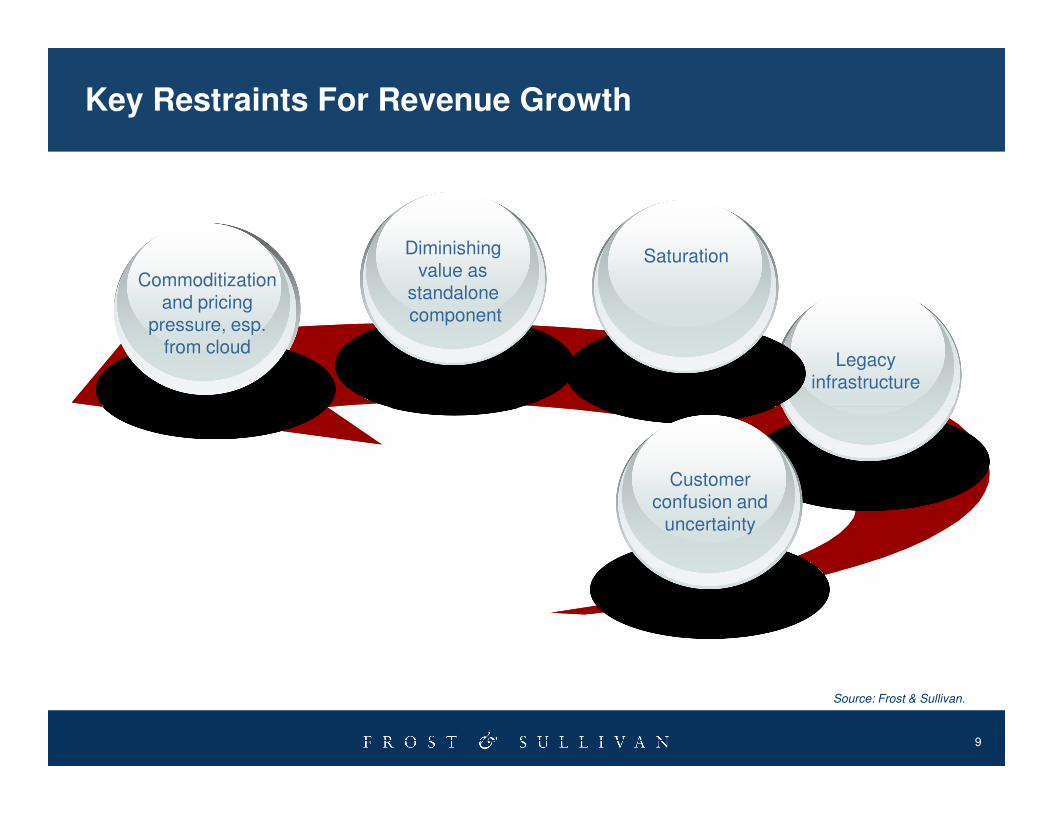

Legacy infrastructure

Commoditization and pricing

pressure, esp. from cloud

Diminishing value as

standalone component

Saturation

Key Restraints For Revenue Growth

9

Customer confusion and

uncertainty

Source: Frost & Sullivan.

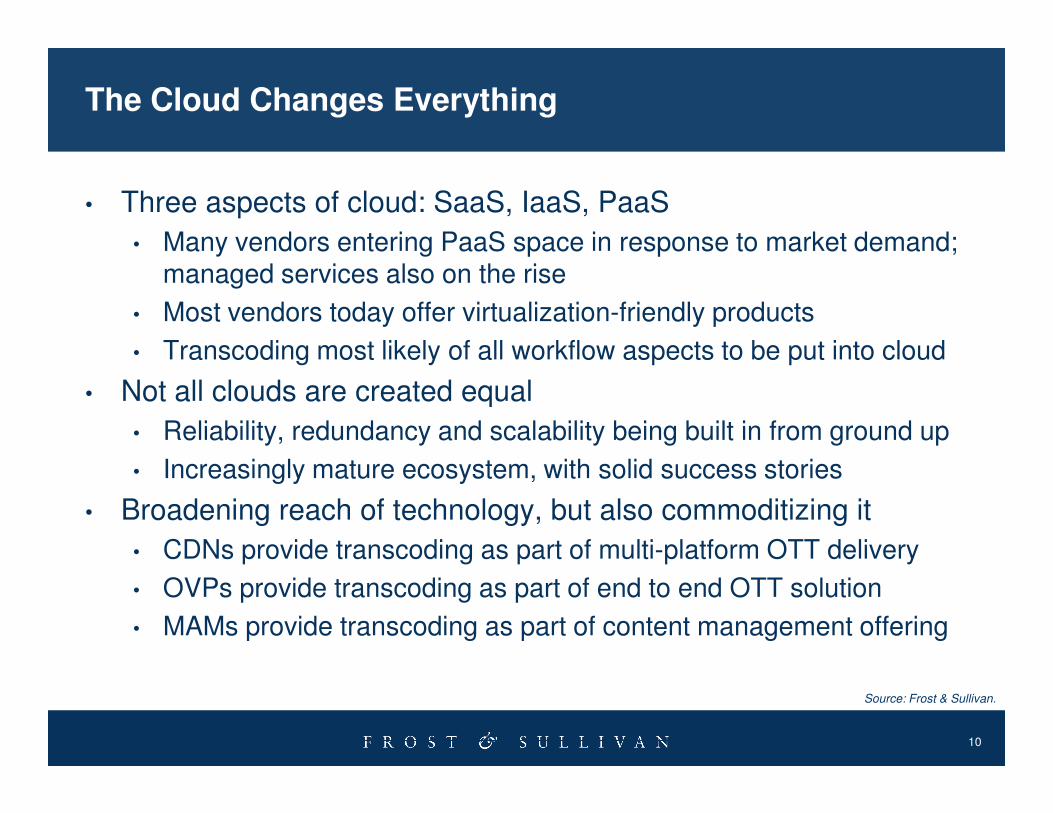

The Cloud Changes Everything

• Three aspects of cloud: SaaS, IaaS, PaaS

• Many vendors entering PaaS space in response to market demand; managed services also on the rise

• Most vendors today offer virtualization-friendly products

• Transcoding most likely of all workflow aspects to be put into cloud

• Not all clouds are created equal

10

Not all clouds are created equal

• Reliability, redundancy and scalability being built in from ground up

• Increasingly mature ecosystem, with solid success stories

• Broadening reach of technology, but also commoditizing it

• CDNs provide transcoding as part of multi-platform OTT delivery

• OVPs provide transcoding as part of end to end OTT solution

• MAMs provide transcoding as part of content management offering

Source: Frost & Sullivan.

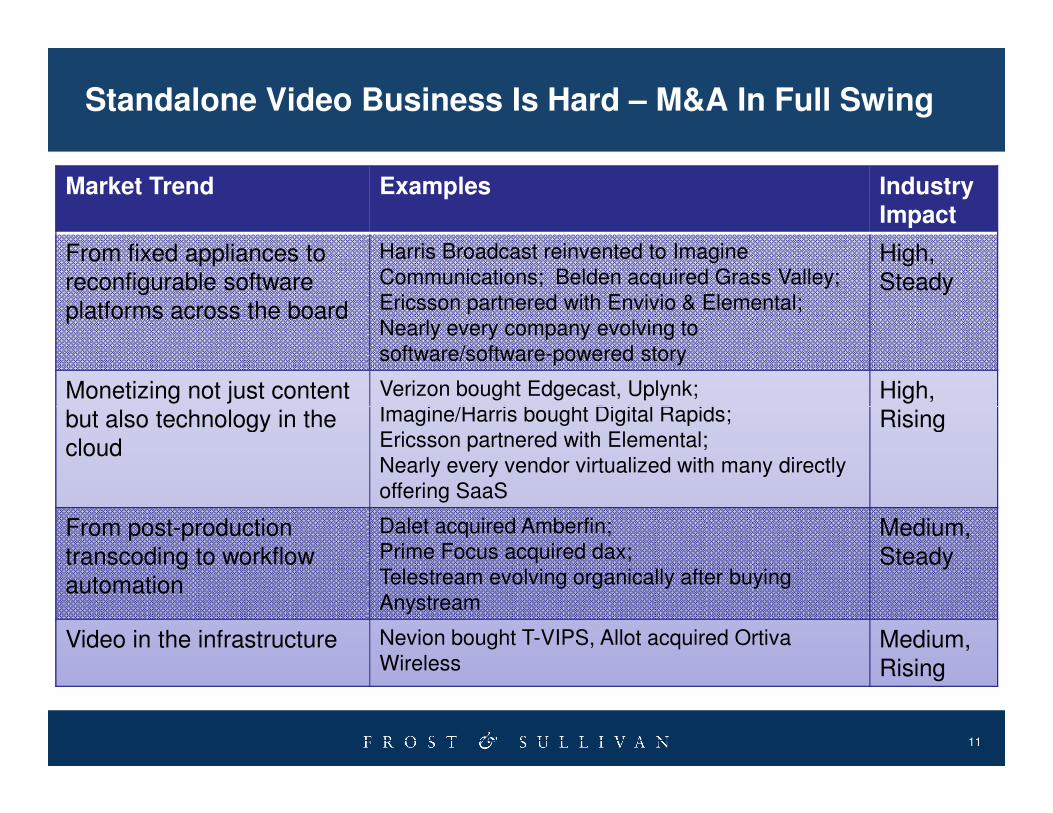

Standalone Video Business Is Hard – M&A In Full Swing

Market Trend Examples Industry Impact

From fixed appliances to reconfigurable software platforms across the board

Harris Broadcast reinvented to Imagine Communications; Belden acquired Grass Valley; Ericsson partnered with Envivio & Elemental; Nearly every company evolving to software/software-powered story

High, Steady

Monetizing not just content but also technology in the

Verizon bought Edgecast, Uplynk;Imagine/Harris bought Digital Rapids;

High, Rising

11

but also technology in the cloud

Imagine/Harris bought Digital Rapids;Ericsson partnered with Elemental; Nearly every vendor virtualized with many directly offering SaaS

Rising

From post-production transcoding to workflow automation

Dalet acquired Amberfin; Prime Focus acquired dax; Telestream evolving organically after buying Anystream

Medium, Steady

Video in the infrastructure Nevion bought T-VIPS, Allot acquired OrtivaWireless

Medium, Rising

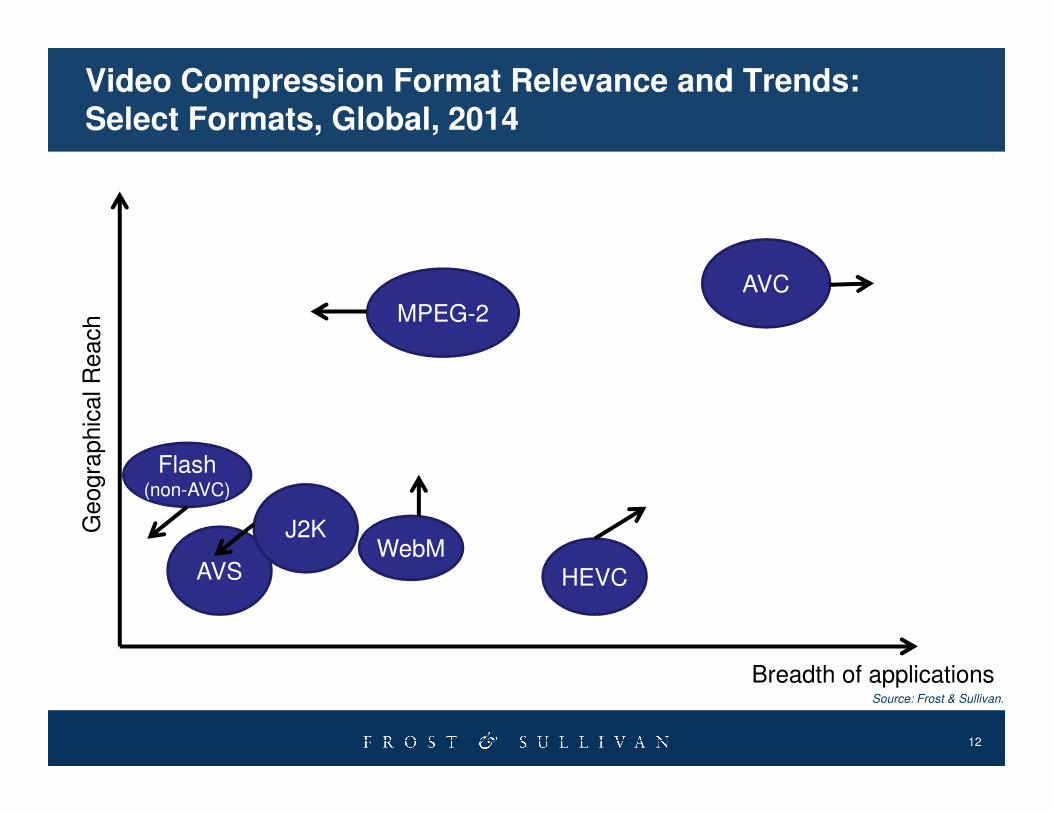

Video Compression Format Relevance and Trends:Select Formats, Global, 2014

Geogra

phic

al R

each

AVCMPEG-2

12

Breadth of applications

Geogra

phic

al R

each

Source: Frost & Sullivan.

AVS

J2K

Flash (non-AVC)

HEVCWebM

Technical Trends – The More Things Change….

• Transcoders

• Commoditization of codecs; emphasis on automated workflows

• Diminishing standalone value; renewed emphasis on throughput

• Scalability & Elasticity – via hybrid or pure cloud architectures

• Mezzanine-to-CDN turnkey solutions in the cloud

• HEVC imminent disruptor, esp. for mobile and UltraHD scenarios

• Broadcast and DTT

13

• Broadcast and DTT

• Growing channel density, falling costs & transition to “software”

• Transition to IP and rise of UltraHD redefining contribution segment

• MPEG-2 -> AVC -> HEVC

• Pay TV

• Multi-screen transcoders and Pay TV encoders converging

• Growing channel density, prices continue to fall

• Appliances remain popular for live linear but cloud services rising

Growth Strategies: Current and Future

• Enable agility and efficiency for major market customers

• “New offerings in minutes” paradigm is crucial

• Optimize bandwidth at every step of the workflow

• Combat pricing pressure by minimizing total cost of ownership

• Complexity of boxes is rising, but that simplifies customer workflow

• Increase density; decrease power consumption; embrace software

Maximize automation to minimize human resource requirements

14

• Maximize automation to minimize human resource requirements

• Educate customers in intelligently evaluating products

• Combat saturation in major markets by focus on growth markets

• LatAm, CEE and Africa continue to offer greenfield opportunities

• India and China continue to expand, v2 upgrades already underway

• Convergence solutions are the need of the day

• In all regions, one-stop vendors with a comprehensive multi-screen, multi-platform, ad-aware product line are seeing fastest growth

Conclusion: Key Take-Aways and Recommendations

• $1.5B+ industry in 2020, with video-powered solutions growing much faster than core video technology revenues. Partnerships, channel strategies and M&A will play a key role in onward growth

• Companies must continue to differentiate on quality and throughput, while positioning themselves as operations partners

• Global footprint is key to sustained and steady revenue streams;

15

Global footprint is key to sustained and steady revenue streams; this requires diverse product portfolio and local relationships with dealerships and system integrators

• HEVC is a valuable buzzword, but customers are looking for comfort in a future-proof investment

• In the very long term, the entire encoders and transcoders industry will continue to converge into a single digital workflow automation market.

Your Feedback is Important to Us

Growth Forecasts?

Competitive Structure?

What would you like to see from Frost & Sullivan?

16

Emerging Trends?

Strategic Recommendations?

Other?

Please inform us by “Rating” this presentation.

Next Steps

Develop Your Visionary and Innovative SkillsGrowth Partnership Service Share your growth thought leadership and ideas or

join our GIL Global Community

17

Join our GIL Community NewsletterKeep abreast of innovative growth opportunities

Follow Frost & Sullivan on Facebook, LinkedIn, SlideShare, and Twitter

http://www.facebook.com/FrostandSullivan

https://www.linkedin.com/groups/Future-Growth-Opportunities-in-ICT-4876870

18

https://twitter.com/FS_ITVision

https://www.linkedin.com/groups/Future-Growth-Opportunities-in-ICT-4876870

http://www.slideshare.net/FrostandSullivan

For Additional Information

Mireya Espinoza

Global Director, Corporate Communications

Digital Media

210-247-3870

Mukul Krishna

Global Research Director

Digital Media

210-247-3850

19

Related Documents