SOCIAL SECURITY & PENSION REFORM Baron Furstenburg Head: Pension Reform Strategy Liberty Corporate 8 & 9 September 2009

SOCIAL SECURITY & PENSION REFORM

Jan 14, 2016

SOCIAL SECURITY & PENSION REFORM. Baron Furstenburg Head: Pension Reform Strategy Liberty Corporate 8 & 9 September 2009. STRUCTURE OF PRESENTATION. Treasury position – 2007 Dept of Social Development – 2007 The World Kept Turning ... Process Areas of agreement ? - PowerPoint PPT Presentation

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

SOCIAL SECURITY & PENSION REFORM

Baron Furstenburg

Head: Pension Reform Strategy

Liberty Corporate

8 & 9 September 2009

STRUCTURE OF PRESENTATION

(1) Treasury position – 2007

(2) Dept of Social Development – 2007

(3) The World Kept Turning ...

(4) Process

(5) Areas of agreement ?

(6) Possible impacts & issues

TREASURY – FEB 2007

Core proposals:

• Introduce National Social Security Fund (NSSF)• mandatory contributions to bridge gap between social old age grant and tax

incentivised retirement savings

• DC as opposed to DB

• Individualised accounts

• Caters for savings and basic risk benefits

• Silent on “opting-out”

• Additional mandatory contributions to private occupational arrangements

• Supplementary voluntary savings

• Complement with a wage subsidy

DEPT OF SOCIAL DEVELOPMENT – 2007

Core proposals:

• The National Social Security Fund (NSSF) should be:

• Totally DB (based on average career earnings) or 50% DB and 50% DC split

• Individualised accounts

• No “opting out” up to for instance R150 000 p.a. (but threshold debatable)

• Additional mandatory and voluntary contributions to “accredited retirement institutions”

• Essentially a fully portable, individual environment much like Chile

• Remove tax incentives and redeploy the revenue gain to other social needs

• Wage subsidy debate should be seen separately

• Most of 2008 spent on conducting research work and reconciling conflicting departmental viewpoints: trying to find a “meeting of the minds”

• Different ideological positions

PROCESS

THE WORLD STILL TURNS .....

• People resigning to access retirement funds

• People divorcing to access retirement funds

• Some employers delaying implementation of a scheme

• Why? Financial crisis, uncertainty of the national scheme, both?

• Most people are staying the course though

ON THE GROUND ...

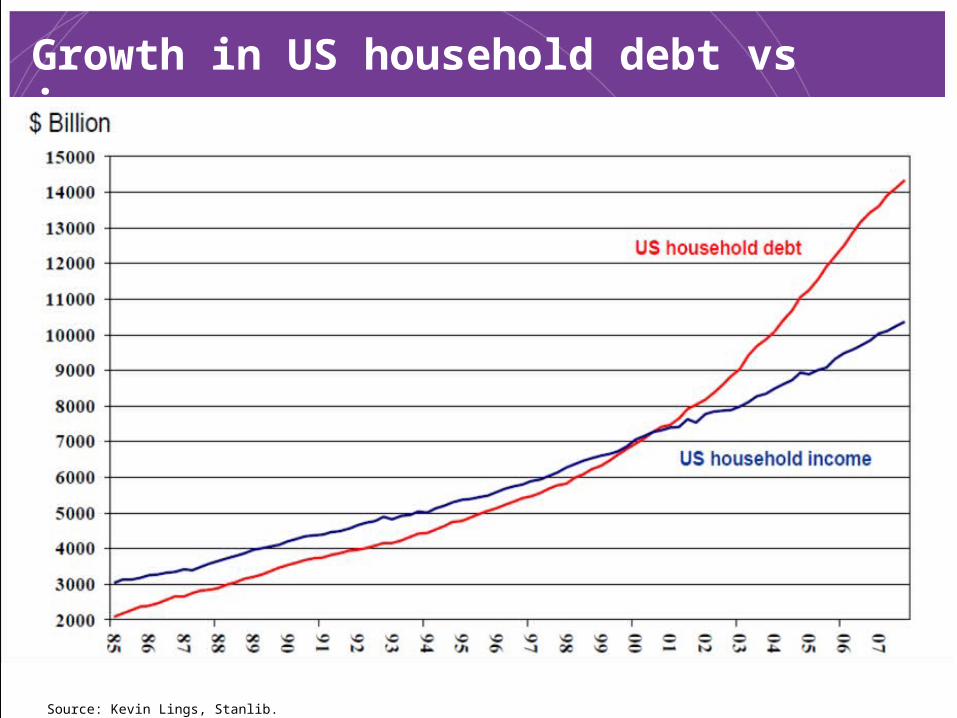

Growth in US household debt vs income

Source: Kevin Lings, Stanlib.

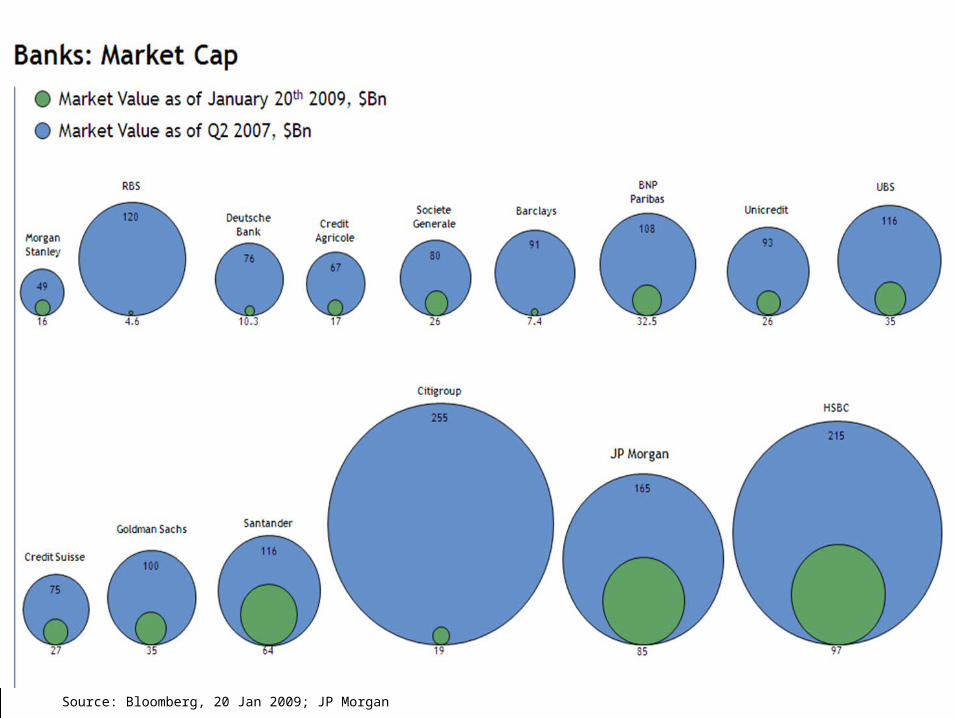

Source: Bloomberg, 20 Jan 2009; JP Morgan

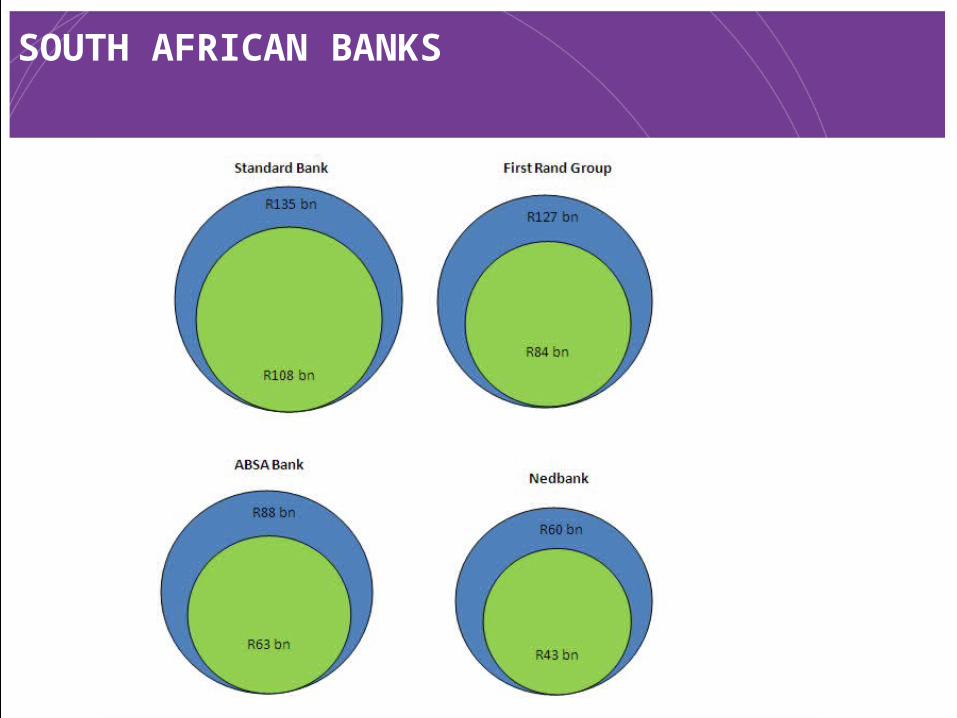

SOUTH AFRICAN BANKS

• Despite the Press: Don’t act on rumour and speculation

• Optimistic scenario:

• Finalisation of proposals end 2009.

• Commence drafting of legislation and passing through Parliament 2010/11.

• Implementation phased-in from 2012.

• The elections have come and gone ...

Who will be responsible for policy .....?

PROCESS

PROCESS

Are there any areas of agreement ...?

• Substantially revise “means test”

• Farm out asset management of national fund to private sector

• Improve governance and regulation (accreditation process)

• Improve disclosure and restrict charges – restricting the types of permissible charges (1st best) or charge caps (2nd best)

• Retirees need a pension for life, so some form of compulsory annuitisation, but not 100%.

• Review role of “living annuities”

AREAS OF AGREEMENT

AREAS OF AGREEMENT

• Compulsory preservation on merely change employ & assistance mechanisms integrated with UIF given loss of employ.

• Increase competition in the pension funds space (ie. open up to banks, CIS)

• Limits to individual choice to prevent confusion. Possibly ... • No / little choice in the national fund

• Limited choice in accredited funds

• Greater choice in the individual retirement fund environment

• Limit switching

• “A little learning is a dangerous thing” Alexander Pope (1711)

• Debate continues on “one stop shop” (independence)

THE CRYSTAL BALL ...

What is likely going forward and ...

What are the hot issues?

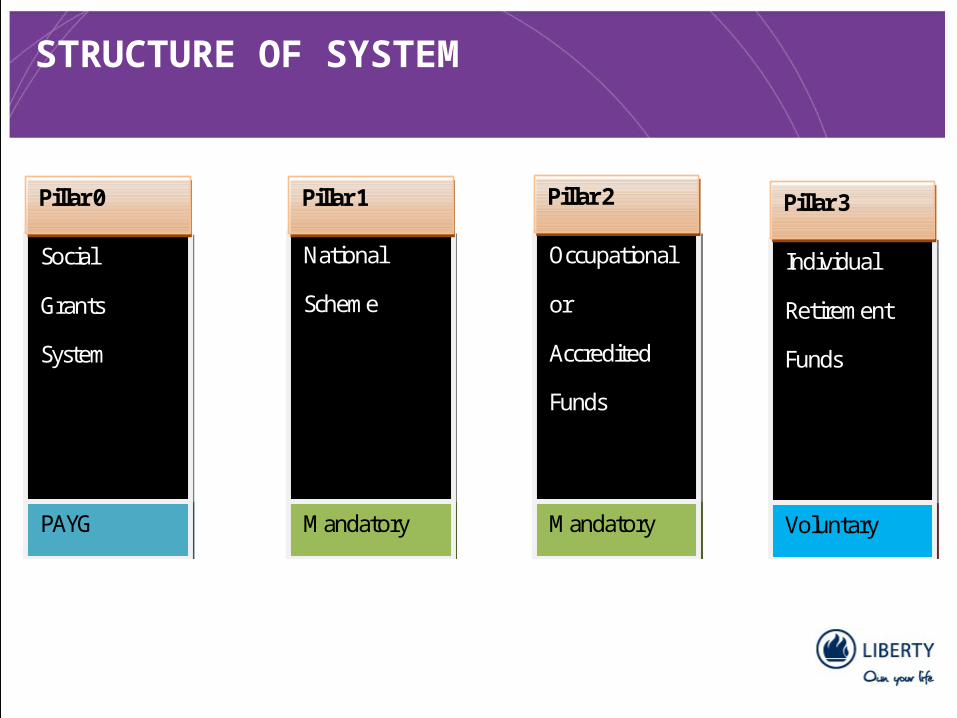

STRUCTURE OF SYSTEM

Social

Grants

System

National

Scheme

Occupational

or

Accredited

Funds

Individual

Retirement

Funds

Pillar 0 Pillar 1 Pillar 2 Pillar 3

Voluntary Mandatory Mandatory PAYG

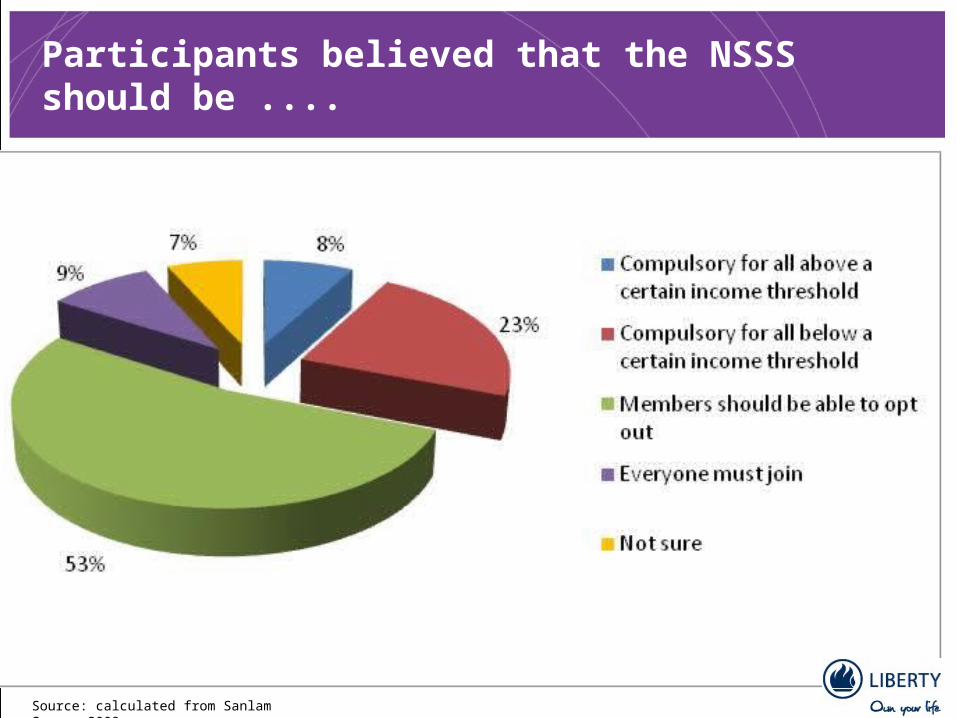

Participants believed that the NSSS should be ....

Source: calculated from Sanlam Survey 2009

Participation

• Allow “opting out” for savings into accredited arrangements, but not basic risk

• Allow the NSSF to serve as benchmark / default fund

• DC with a guarantee much more realistic than an obscure DB model

• Opting out more viable & Unions wont like a “loss of control”

• Possibility of auto-enrolment

• Members can get additional top-up risk cover in their accredited arrangement

• Require mandatory contribution but only up to some earnings level, beyond which participation is voluntary

POSSIBLE IMPACTS AND ISSUES

Participation

• Additional top-up savings through “individual retirement funds”

• Essentially RAs in fully portable form

• Limit on tax deductibility

• Collections done by SARS? Central clearinghouse? [eg. Sweden, Mexico]

• De-linking of the wage subsidy debate from social security:

• Wage subsidies are usually targeted and tweaked over time but ...

• Pensions are long-term

• Thinking around co-contributions likely

• Large cost of wage subsidy vs benefit

POSSIBLE IMPACTS AND ISSUES

Assets

• Larger pool of retirement assets. Growth of national fund will be exponential.

• Govt will seek increased participation of black asset managers

• SRI debate in the SA context still to be had

POSSIBLE IMPACTS AND ISSUES

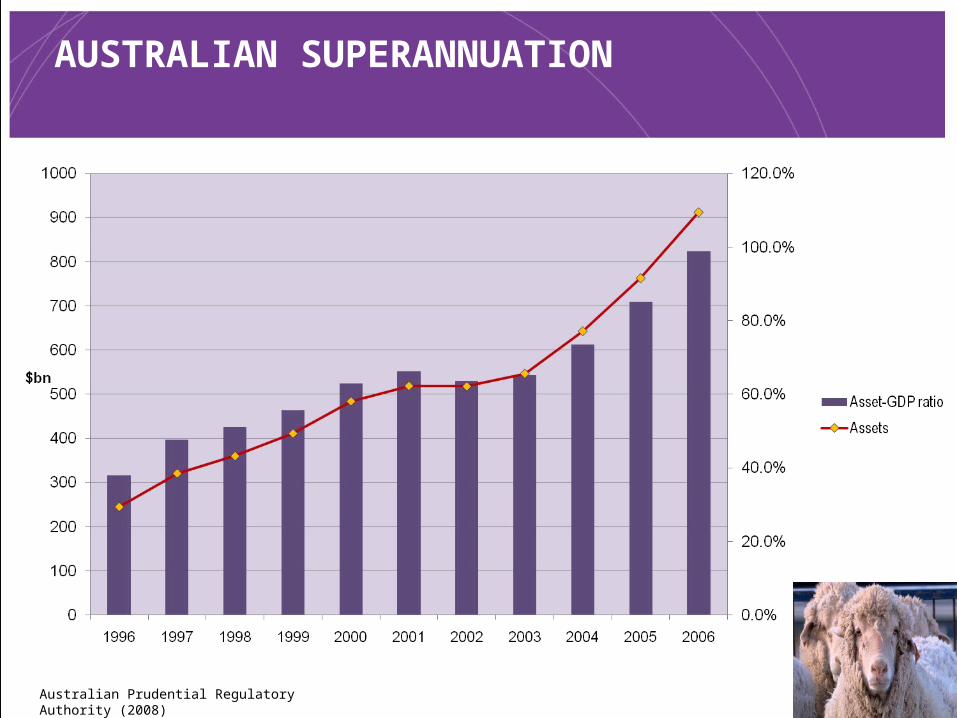

AUSTRALIAN SUPERANNUATION

Australian Prudential Regulatory Authority (2008)

Regulation & Governance

• Continued move towards umbrella and industry funds (but issues: conflicts of interests and transparency)

• Fewer funds implies better regulation & disclosure.

• Little chance of a Chilean system – ie. one totally based on individual choice. SA not ready for it, but the model is not totally out the window just yet

• Fewer trustees required – a greater role for independent trustees & greater “professionalization” of the trustee role

POSSIBLE IMPACTS AND ISSUES

Annuitisation

• Compulsory annuitisation implies innovation in the annuity market;

• “The first marriage is to please one’s parents, the second marriage to please oneself” (Chinese idiom)

• Possibility joint life annuities for married people

• Likely prescription of an inflation-linked annuity

• Circumscribed scope for living annuities (don’t provide longevity insurance; possible Govt may require a conventional annuity up to a point, then more individual freedom thereafter)

• Will a national fund provide annuities? How?

• Chile: SCOMP system

POSSIBLE IMPACTS AND ISSUES

POSSIBLE IMPACTS AND ISSUES

Advisors: food for thought

• Diversify sources of income?

• As-and-when commission implies building a book of clients even of greater importance

• Service and service partners increasingly important

• Continuing professionalism

• Regulatory change

There is no pensions blue-print ...

We will have a home-grown, tailored solution ...

... And its going to take some time...

END OF PRESENTATION

Related Documents