Broadband Issues Perspective Mike Furby Systems Engineering Manager Redback Networks

Slide title 40 pt Slide subtitle 24 pt Slide title 40 pt Slide subtitle 24 pt Broadband Issues Perspective Mike Furby Systems Engineering Manager Redback.

Dec 25, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Slide title40 pt

Slide subtitle 24 pt

Slide title40 pt

Slide subtitle 24 pt

Broadband Issues PerspectiveMike Furby

Systems Engineering Manager

Redback Networks

© Copyright Redback Networks Inc. 2007. All rights reserved. - 2 -

Top right corner for field-mark, customer or partner logotypes.

Slide title 40 pt

Slide subtitle 24 pt

Text 24 pt

Bullets level 220 pt

Bullets level 3-516 pt

© Copyright Redback Networks Inc. 2007. All rights reserved. - 2 -

Top right corner for field-mark, customer or partner logotypes.

Slide title 40 pt

Slide subtitle 24 pt

Text 24 pt

Bullets level 220 pt

Bullets level 3-516 pt

Redback Networks, An Ericsson Company

• Founded 1996 • Headquarters: San Jose, CA• Wholly owned subsidiary

of Ericsson• Tier 1 Customer Base– 500+ service providers– 16 of Top 25 globally

• Fastest growing SP router company• Support over 50MM DSL Lines• $400MM+ Investment in Next-

Generation Multi-Service Routing Portfolio

© Copyright Redback Networks Inc. 2007. All rights reserved. - 3 -

Top right corner for field-mark, customer or partner logotypes.

Slide title 40 pt

Slide subtitle 24 pt

Text 24 pt

Bullets level 220 pt

Bullets level 3-516 pt

© Copyright Redback Networks Inc. 2007. All rights reserved. - 3 -

Top right corner for field-mark, customer or partner logotypes.

Slide title 40 pt

Slide subtitle 24 pt

Text 24 pt

Bullets level 220 pt

Bullets level 3-516 pt

Multiple Applications

In Top 20

Residential Triple Play

Business Networks

Mobile Broadband

Internet& VOD IPTV VoIP VPN

(L2/3)MetroE

(Agg/VPLS)Wi-Fi/WiMax

3G Data/MPBN

SmartEdge Highlights

© Copyright Redback Networks Inc. 2007. All rights reserved. - 4 -

Top right corner for field-mark, customer or partner logotypes.

Slide title 40 pt

Slide subtitle 24 pt

Text 24 pt

Bullets level 220 pt

Bullets level 3-516 pt

© Copyright Redback Networks Inc. 2007. All rights reserved. - 4 -

Top right corner for field-mark, customer or partner logotypes.

Slide title 40 pt

Slide subtitle 24 pt

Text 24 pt

Bullets level 220 pt

Bullets level 3-516 pt

Broadband Issues

• Waves of change across the industry• Market dynamics & changing traffic patterns – Per subscriber traffic growth – Market saturation, growth is slowing– Service evolution– Increasing competition– Subscriber loyalty & the need to differentiate– Pressure on service margins & the need to reduce OPEX/CAPEX– P2P, DPI & QoS

• 21CN Wholesale Broadband Connect– Single step WBC strategy

© Copyright Redback Networks Inc. 2007. All rights reserved. - 5 -

Top right corner for field-mark, customer or partner logotypes.

Slide title 40 pt

Slide subtitle 24 pt

Text 24 pt

Bullets level 220 pt

Bullets level 3-516 pt

© Copyright Redback Networks Inc. 2007. All rights reserved. - 5 -

Top right corner for field-mark, customer or partner logotypes.

Slide title 40 pt

Slide subtitle 24 pt

Text 24 pt

Bullets level 220 pt

Bullets level 3-516 pt

Technology EvolutionBroadband Capacity

1990 2000 2010 Year

ADSL

ADSL2+

SDSL

VDSL

VDSL2

FTTH

GPON

Last mileBandwidth

500kbps

2Mbps

10Mbps

100Mbps

1Gbps

CapacityBRAS/BNG

1st gen BRAS

Eth BNG

Next-gen Eth MSER

10Gbps

240Gbps

480Gbps

50x

2000x

© Copyright Redback Networks Inc. 2007. All rights reserved. - 6 -

Top right corner for field-mark, customer or partner logotypes.

Slide title 40 pt

Slide subtitle 24 pt

Text 24 pt

Bullets level 220 pt

Bullets level 3-516 pt

© Copyright Redback Networks Inc. 2007. All rights reserved. - 6 -

Top right corner for field-mark, customer or partner logotypes.

Slide title 40 pt

Slide subtitle 24 pt

Text 24 pt

Bullets level 220 pt

Bullets level 3-516 pt

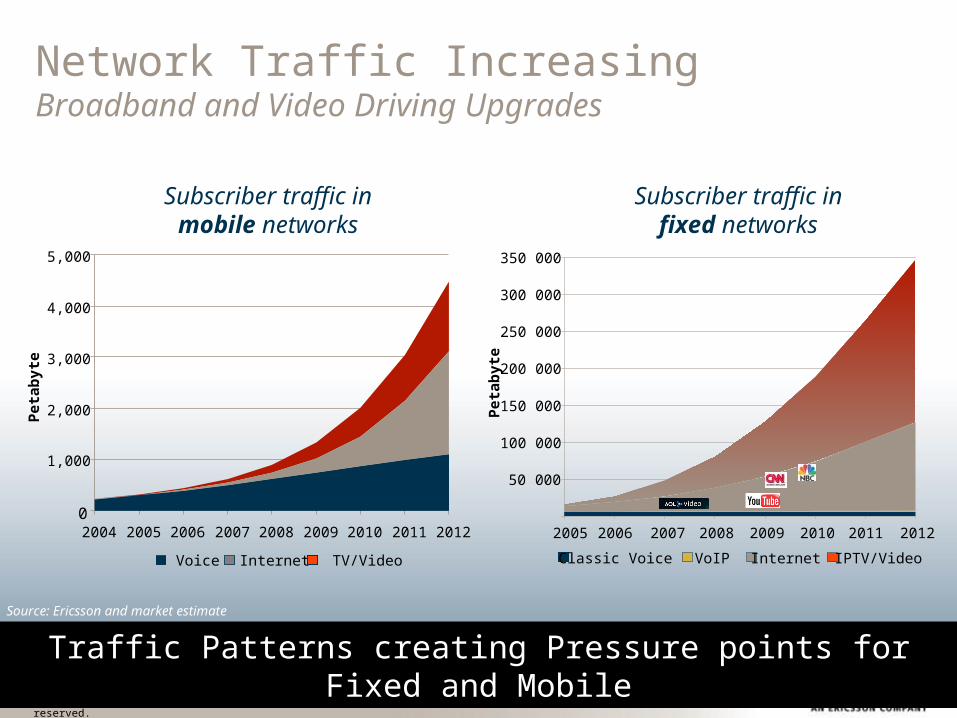

Network Traffic IncreasingBroadband and Video Driving Upgrades

Subscriber traffic in mobile networks

Traffic Patterns creating Pressure points for Fixed and Mobile

Subscriber traffic in fixed networks

50 000

100 000

150 000

200 000

250 000

300 000

350 000

2005 2006 2007 2008 2009 2010 2011 2012

Pet

abyt

e

Classic Voice Internet IPTV/VideoVoIP

Source: Ericsson and market estimate

0

1,000

2,000

3,000

4,000

5,000

2004 2005 2006 2007 2008 2009 2010 2011 2012

Pet

abyt

e

Voice Internet TV/Video

© Copyright Redback Networks Inc. 2007. All rights reserved. - 7 -

Top right corner for field-mark, customer or partner logotypes.

Slide title 40 pt

Slide subtitle 24 pt

Text 24 pt

Bullets level 220 pt

Bullets level 3-516 pt

© Copyright Redback Networks Inc. 2007. All rights reserved. - 7 -

Top right corner for field-mark, customer or partner logotypes.

Slide title 40 pt

Slide subtitle 24 pt

Text 24 pt

Bullets level 220 pt

Bullets level 3-516 pt

0%

5%

10%

15%

Q2C Y 06 Q3C Y 06 Q4C Y 06 Q1C Y 07 Q2C Y 07

DSL Cable FTTX

WorldwideAmericas

EMEA APAC

Source: Point-Topic as of Q1 2007

0%

10%

20%

30%

Q2C Y 06 Q3C Y 06 Q4C Y 06 Q1C Y 07 Q2C Y 07

DSL Cable FTTX

0%

5%

10%

15%

Q2C Y 06 Q3C Y 06 Q4C Y 06 Q1C Y 07 Q2C Y 07

DSL Cable FTTX

-5%

0%

5%

10%

15%

Q2C Y 06 Q3C Y 06 Q4C Y 06 Q1C Y 07 Q2C Y 07

DSL Cable FTTX

Broadband Growth by Technology

© Copyright Redback Networks Inc. 2007. All rights reserved. - 8 -

Top right corner for field-mark, customer or partner logotypes.

Slide title 40 pt

Slide subtitle 24 pt

Text 24 pt

Bullets level 220 pt

Bullets level 3-516 pt

© Copyright Redback Networks Inc. 2007. All rights reserved. - 8 -

Top right corner for field-mark, customer or partner logotypes.

Slide title 40 pt

Slide subtitle 24 pt

Text 24 pt

Bullets level 220 pt

Bullets level 3-516 pt

Service EvolutionsP2P Technology & Internet Video

2002 – 2006P2P dominates Internet traffic

(Video accounts for 60%)

2007HTTP overtakes P2P again

(YouTube accounts for 20%)

iPlayer

Driving the world towards adopting P2P as a commercial video distribution technologyDriving the world towards adopting P2P as a commercial video distribution technology

Source: Cachelogic

Source: Ellacoya

© Copyright Redback Networks Inc. 2007. All rights reserved. - 9 -

Top right corner for field-mark, customer or partner logotypes.

Slide title 40 pt

Slide subtitle 24 pt

Text 24 pt

Bullets level 220 pt

Bullets level 3-516 pt

© Copyright Redback Networks Inc. 2007. All rights reserved. - 9 -

Top right corner for field-mark, customer or partner logotypes.

Slide title 40 pt

Slide subtitle 24 pt

Text 24 pt

Bullets level 220 pt

Bullets level 3-516 pt

BT Transformation

BRASSubscriber CP

Cisco 10k or JNPR ERX

20CN MSiP

(ATM network)

20CN Colossus

(IP network)

20C IP-stream

BRASSubscriber CP

SE800

20CN Colossus

(IP network)

21CN

(Ethernet MPLS)

21C IP-stream

BRASSubscriber CP

SE800

21CN

(Ethernet MPLS)

21CN

(Ethernet MPLS)

21C WBC

© Copyright Redback Networks Inc. 2007. All rights reserved. - 10 -

Top right corner for field-mark, customer or partner logotypes.

Slide title 40 pt

Slide subtitle 24 pt

Text 24 pt

Bullets level 220 pt

Bullets level 3-516 pt

© Copyright Redback Networks Inc. 2007. All rights reserved. - 10 -

Top right corner for field-mark, customer or partner logotypes.

Slide title 40 pt

Slide subtitle 24 pt

Text 24 pt

Bullets level 220 pt

Bullets level 3-516 pt

Summary

• The way Broadband is being delivered is changing• Internet traffic is both increasing and changing shape• Growth is slowing– Driving the need to differentiate– Driving the need to reduce costs

• Redback is a key supplier to the industry– 16 of the top 25 DSL suppliers are Redback customers

Slide title40 pt

Slide subtitle 24 pt

Slide title40 pt

Slide subtitle 24 pt

Spare Slides

© Copyright Redback Networks Inc. 2007. All rights reserved. - 12 -

Top right corner for field-mark, customer or partner logotypes.

Slide title 40 pt

Slide subtitle 24 pt

Text 24 pt

Bullets level 220 pt

Bullets level 3-516 pt

© Copyright Redback Networks Inc. 2007. All rights reserved. - 12 -

Top right corner for field-mark, customer or partner logotypes.

Slide title 40 pt

Slide subtitle 24 pt

Text 24 pt

Bullets level 220 pt

Bullets level 3-516 pt

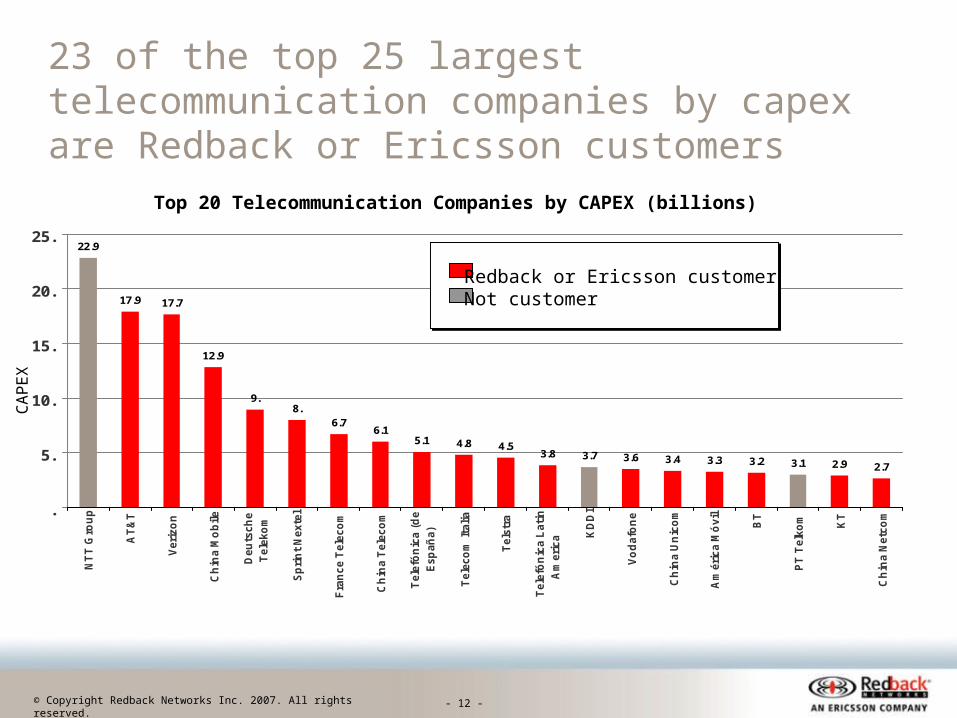

23 of the top 25 largest telecommunication companies by capex are Redback or Ericsson customers

22.9

17.9 17.7

12.9

9.8.

6.76.1

5.1 4.8 4.53.8 3.7 3.6 3.4 3.3 3.2 3.1 2.9 2.7

.

5.

10.

15.

20.

25.

NT

T G

rou

p

AT

&T

Veri

zo

n

Ch

ina M

ob

ile

Deu

tsch

e

Tele

ko

m

Sp

rin

t N

exte

l

Fra

nce T

ele

co

m

Ch

ina T

ele

co

m

Tele

fón

ica (

de

Esp

añ

a)

Tele

co

m Ita

lia

Tels

tra

Tele

fón

ica L

ati

n

Am

eri

ca KD

DI

Vo

dafo

ne

Ch

ina U

nic

om

Am

éri

ca M

óvil

BT

PT

Telk

om KT

Ch

ina N

etc

om

Top 20 Telecommunication Companies by CAPEX (billions)

Redback or Ericsson customerNot customer

CA

PE

X

© Copyright Redback Networks Inc. 2007. All rights reserved. - 13 -

Top right corner for field-mark, customer or partner logotypes.

Slide title 40 pt

Slide subtitle 24 pt

Text 24 pt

Bullets level 220 pt

Bullets level 3-516 pt

© Copyright Redback Networks Inc. 2007. All rights reserved. - 13 -

Top right corner for field-mark, customer or partner logotypes.

Slide title 40 pt

Slide subtitle 24 pt

Text 24 pt

Bullets level 220 pt

Bullets level 3-516 pt

16 of the top 25 DSL operators by subscribers are Redback customers

23

13.4 13.2

8.88 7.3

6.6 6.65.2 5.1 4.7 4.3 3.9 3.7 3.3 3.2 3 2.6 2.4 2.4 2.4 2.2 2.2 2 1.9

0

5

10

15

20

25

Ch

ina T

ele

co

m

Ch

ina N

etc

om

AT

&T

(S

BC

)

BT

Deu

tsch

e T

ele

ko

m

Tele

co

m Ita

lia

Veri

zo

n

Ora

ng

e -

Fra

nce

NT

T

Yah

oo

Jap

an

Tele

fon

ica d

e E

sp

an

a

Ko

rea T

ele

co

m

Ch

un

gh

wa T

ele

co

m

Tu

rk T

ele

ko

m

Tels

tra

Ch

ina T

ieto

ng

Neu

fCeg

ete

l

Fre

e

KP

N T

ele

co

m

Qw

est

Telm

ex

Arc

or

Tele

co

m Ita

lia G

erm

an

y

Bell C

an

ad

a

eA

ccess

Top 25 DSL Operators by Subscribers (millions)

Redback or Ericsson customerNot customer

Su

bsc

ribe

rs

Related Documents