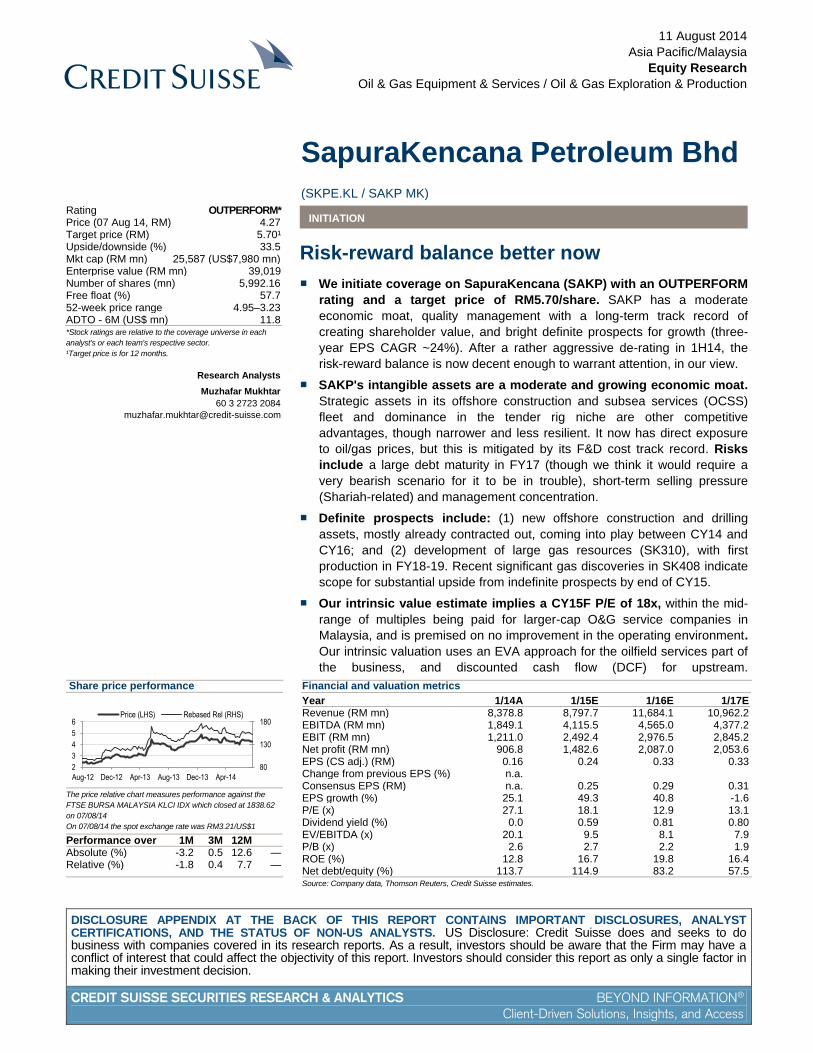

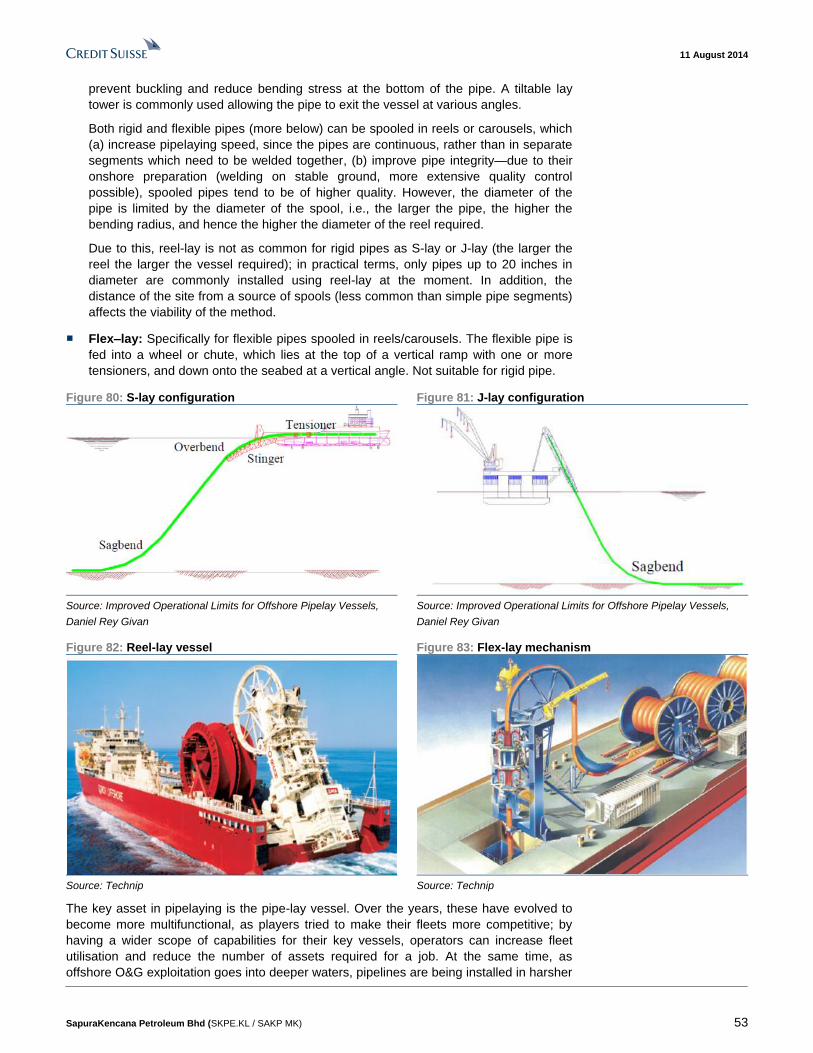

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION ® Client-Driven Solutions, Insights, and Access 11 August 2014 Asia Pacific/Malaysia Equity Research Oil & Gas Equipment & Services / Oil & Gas Exploration & Production SapuraKencana Petroleum Bhd (SKPE.KL / SAKP MK) INITIATION Risk-reward balance better now ■ We initiate coverage on SapuraKencana (SAKP) with an OUTPERFORM rating and a target price of RM5.70/share. SAKP has a moderate economic moat, quality management with a long-term track record of creating shareholder value, and bright definite prospects for growth (three- year EPS CAGR ~24%). After a rather aggressive de-rating in 1H14, the risk-reward balance is now decent enough to warrant attention, in our view. ■ SAKP's intangible assets are a moderate and growing economic moat. Strategic assets in its offshore construction and subsea services (OCSS) fleet and dominance in the tender rig niche are other competitive advantages, though narrower and less resilient. It now has direct exposure to oil/gas prices, but this is mitigated by its F&D cost track record. Risks include a large debt maturity in FY17 (though we think it would require a very bearish scenario for it to be in trouble), short-term selling pressure (Shariah-related) and management concentration. ■ Definite prospects include: (1) new offshore construction and drilling assets, mostly already contracted out, coming into play between CY14 and CY16; and (2) development of large gas resources (SK310), with first production in FY18-19. Recent significant gas discoveries in SK408 indicate scope for substantial upside from indefinite prospects by end of CY15. ■ Our intrinsic value estimate implies a CY15F P/E of 18x, within the mid- range of multiples being paid for larger-cap O&G service companies in Malaysia, and is premised on no improvement in the operating environment . Our intrinsic valuation uses an EVA approach for the oilfield services part of the business, and discounted cash flow (DCF) for upstream. Share price performance 80 130 180 2 3 4 5 6 Aug-12 Dec-12 Apr-13 Aug-13 Dec-13 Apr-14 Price (LHS) Rebased Rel (RHS) The price relative chart measures performance against the FTSE BURSA MALAYSIA KLCI IDX which closed at 1838.62 on 07/08/14 On 07/08/14 the spot exchange rate was RM3.21/US$1 Performance over 1M 3M 12M Absolute (%) -3.2 0.5 12.6 — Relative (%) -1.8 0.4 7.7 — Financial and valuation metrics Year 1/14A 1/15E 1/16E 1/17E Revenue (RM mn) 8,378.8 8,797.7 11,684.1 10,962.2 EBITDA (RM mn) 1,849.1 4,115.5 4,565.0 4,377.2 EBIT (RM mn) 1,211.0 2,492.4 2,976.5 2,845.2 Net profit (RM mn) 906.8 1,482.6 2,087.0 2,053.6 EPS (CS adj.) (RM) 0.16 0.24 0.33 0.33 Change from previous EPS (%) n.a. Consensus EPS (RM) n.a. 0.25 0.29 0.31 EPS growth (%) 25.1 49.3 40.8 -1.6 P/E (x) 27.1 18.1 12.9 13.1 Dividend yield (%) 0.0 0.59 0.81 0.80 EV/EBITDA (x) 20.1 9.5 8.1 7.9 P/B (x) 2.6 2.7 2.2 1.9 ROE (%) 12.8 16.7 19.8 16.4 Net debt/equity (%) 113.7 114.9 83.2 57.5 Source: Company data, Thomson Reuters, Credit Suisse estimates. Rating OUTPERFORM* Price (07 Aug 14, RM) 4.27 Target price (RM) 5.70¹ Upside/downside (%) 33.5 Mkt cap (RM mn) 25,587 (US$7,980 mn) Enterprise value (RM mn) 39,019 Number of shares (mn) 5,992.16 Free float (%) 57.7 52-week price range 4.95–3.23 ADTO - 6M (US$ mn) 11.8 *Stock ratings are relative to the coverage universe in each analyst's or each team's respective sector. ¹Target price is for 12 months. Research Analysts Muzhafar Mukhtar 60 3 2723 2084 [email protected]

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION®

Client-Driven Solutions, Insights, and Access

11 August 2014

Asia Pacific/Malaysia

Equity Research

Oil & Gas Equipment & Services / Oil & Gas Exploration & Production

SapuraKencana Petroleum Bhd

(SKPE.KL / SAKP MK) INITIATION

Risk-reward balance better now

■ We initiate coverage on SapuraKencana (SAKP) with an OUTPERFORM

rating and a target price of RM5.70/share. SAKP has a moderate

economic moat, quality management with a long-term track record of

creating shareholder value, and bright definite prospects for growth (three-

year EPS CAGR ~24%). After a rather aggressive de-rating in 1H14, the

risk-reward balance is now decent enough to warrant attention, in our view.

■ SAKP's intangible assets are a moderate and growing economic moat.

Strategic assets in its offshore construction and subsea services (OCSS)

fleet and dominance in the tender rig niche are other competitive

advantages, though narrower and less resilient. It now has direct exposure

to oil/gas prices, but this is mitigated by its F&D cost track record. Risks

include a large debt maturity in FY17 (though we think it would require a

very bearish scenario for it to be in trouble), short-term selling pressure

(Shariah-related) and management concentration.

■ Definite prospects include: (1) new offshore construction and drilling

assets, mostly already contracted out, coming into play between CY14 and

CY16; and (2) development of large gas resources (SK310), with first

production in FY18-19. Recent significant gas discoveries in SK408 indicate

scope for substantial upside from indefinite prospects by end of CY15.

■ Our intrinsic value estimate implies a CY15F P/E of 18x, within the mid-

range of multiples being paid for larger-cap O&G service companies in

Malaysia, and is premised on no improvement in the operating environment.

Our intrinsic valuation uses an EVA approach for the oilfield services part of

the business, and discounted cash flow (DCF) for upstream.

Share price performance

80

130

180

2

3

4

5

6

Aug-12 Dec-12 Apr-13 Aug-13 Dec-13 Apr-14

Price (LHS) Rebased Rel (RHS)

The price relative chart measures performance against the

FTSE BURSA MALAYSIA KLCI IDX which closed at 1838.62

on 07/08/14

On 07/08/14 the spot exchange rate was RM3.21/US$1

Performance over 1M 3M 12M Absolute (%) -3.2 0.5 12.6 — Relative (%) -1.8 0.4 7.7 —

Financial and valuation metrics

Year 1/14A 1/15E 1/16E 1/17E Revenue (RM mn) 8,378.8 8,797.7 11,684.1 10,962.2 EBITDA (RM mn) 1,849.1 4,115.5 4,565.0 4,377.2 EBIT (RM mn) 1,211.0 2,492.4 2,976.5 2,845.2 Net profit (RM mn) 906.8 1,482.6 2,087.0 2,053.6 EPS (CS adj.) (RM) 0.16 0.24 0.33 0.33 Change from previous EPS (%) n.a. Consensus EPS (RM) n.a. 0.25 0.29 0.31 EPS growth (%) 25.1 49.3 40.8 -1.6 P/E (x) 27.1 18.1 12.9 13.1 Dividend yield (%) 0.0 0.59 0.81 0.80 EV/EBITDA (x) 20.1 9.5 8.1 7.9 P/B (x) 2.6 2.7 2.2 1.9 ROE (%) 12.8 16.7 19.8 16.4 Net debt/equity (%) 113.7 114.9 83.2 57.5

Source: Company data, Thomson Reuters, Credit Suisse estimates.

Rating OUTPERFORM* Price (07 Aug 14, RM) 4.27 Target price (RM) 5.70¹ Upside/downside (%) 33.5 Mkt cap (RM mn) 25,587 (US$7,980 mn) Enterprise value (RM mn) 39,019 Number of shares (mn) 5,992.16 Free float (%) 57.7 52-week price range 4.95–3.23 ADTO - 6M (US$ mn) 11.8

*Stock ratings are relative to the coverage universe in each

analyst's or each team's respective sector.

¹Target price is for 12 months.

Research Analysts

Muzhafar Mukhtar

60 3 2723 2084

11 August 2014

SapuraKencana Petroleum Bhd (SKPE.KL / SAKP MK) 2

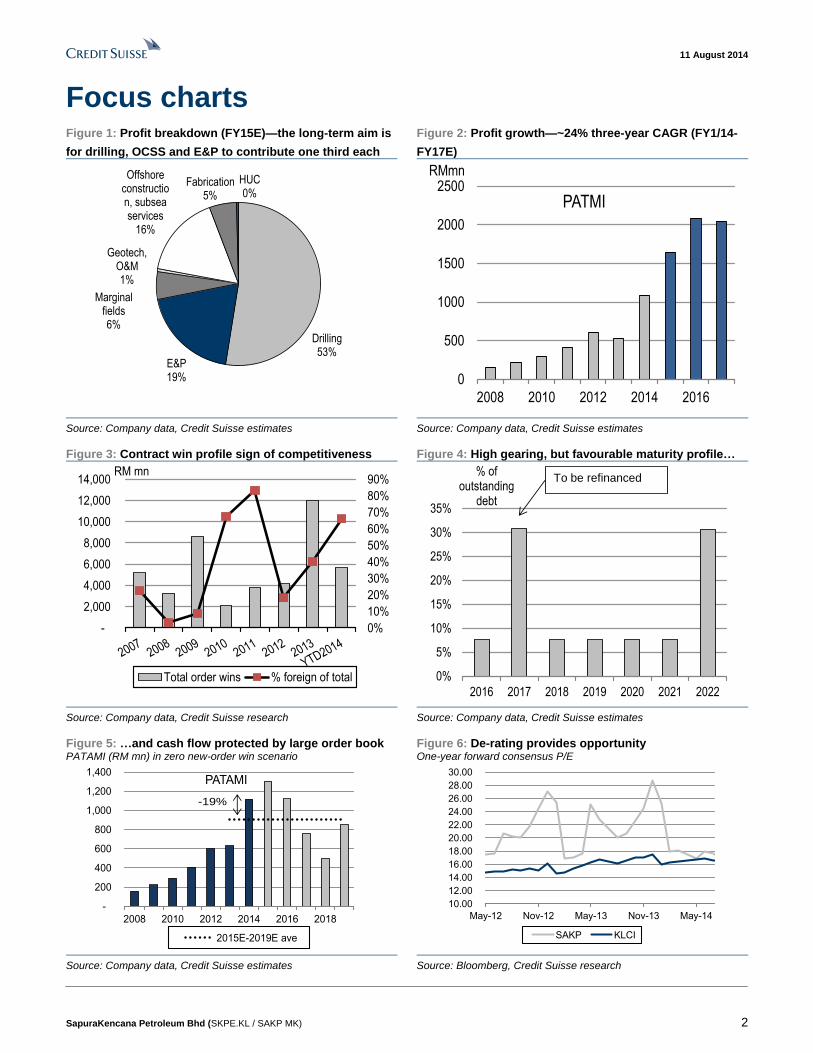

Focus charts Figure 1: Profit breakdown (FY15E)—the long-term aim is

for drilling, OCSS and E&P to contribute one third each

Figure 2: Profit growth—~24% three-year CAGR (FY1/14-

FY17E)

Drilling53%

E&P19%

Marginal fields6%

Geotech, O&M1%

Offshore construction, subsea services

16%

Fabrication5%

HUC0%

0

500

1000

1500

2000

2500

2008 2010 2012 2014 2016

RMmn

PATMI

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Figure 3: Contract win profile sign of competitiveness Figure 4: High gearing, but favourable maturity profile…

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000RM mn

Total order wins % foreign of total

0%

5%

10%

15%

20%

25%

30%

35%

2016 2017 2018 2019 2020 2021 2022

% of outstanding

debt

To be refinanced

Source: Company data, Credit Suisse research Source: Company data, Credit Suisse estimates

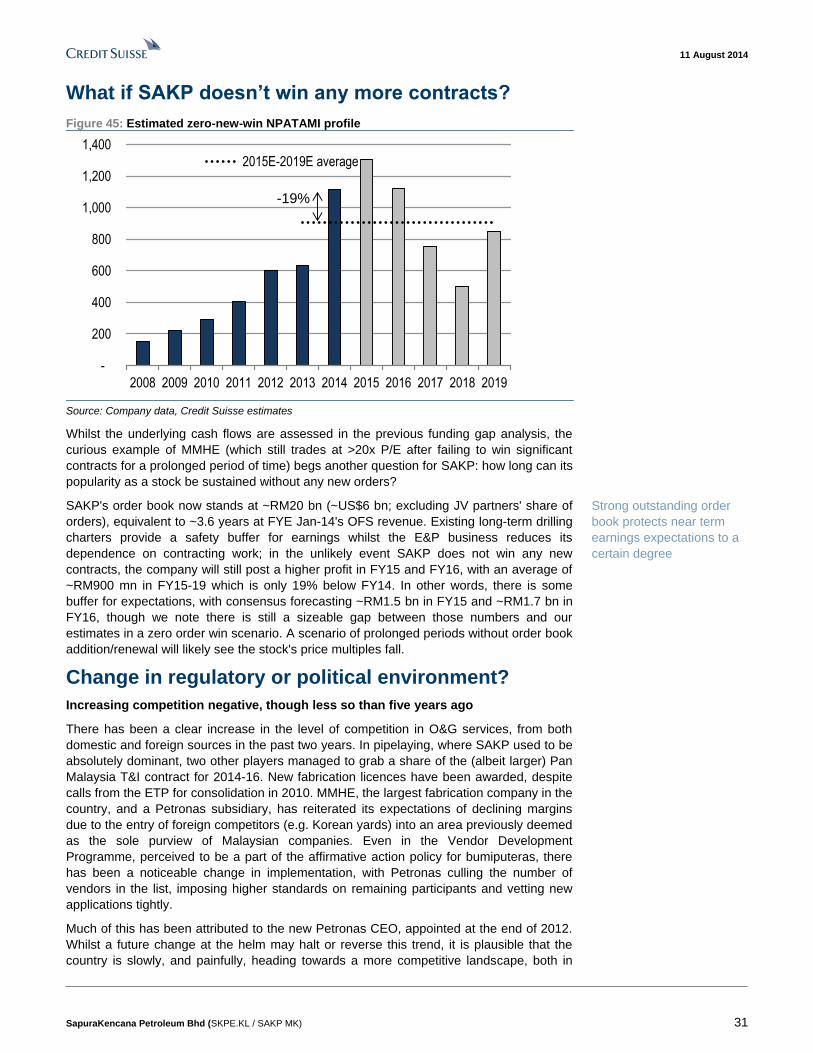

Figure 5: …and cash flow protected by large order book PATAMI (RM mn) in zero new-order win scenario

Figure 6: De-rating provides opportunity One-year forward consensus P/E

-

200

400

600

800

1,000

1,200

1,400

2008 2010 2012 2014 2016 2018

PATAMI

2015E-2019E ave

-19%

10.00

12.00

14.00

16.00

18.00

20.00

22.00

24.00

26.00

28.00

30.00

May-12 Nov-12 May-13 Nov-13 May-14

SAKP KLCI

Source: Company data, Credit Suisse estimates Source: Bloomberg, Credit Suisse research

11 August 2014

SapuraKencana Petroleum Bhd (SKPE.KL / SAKP MK) 3

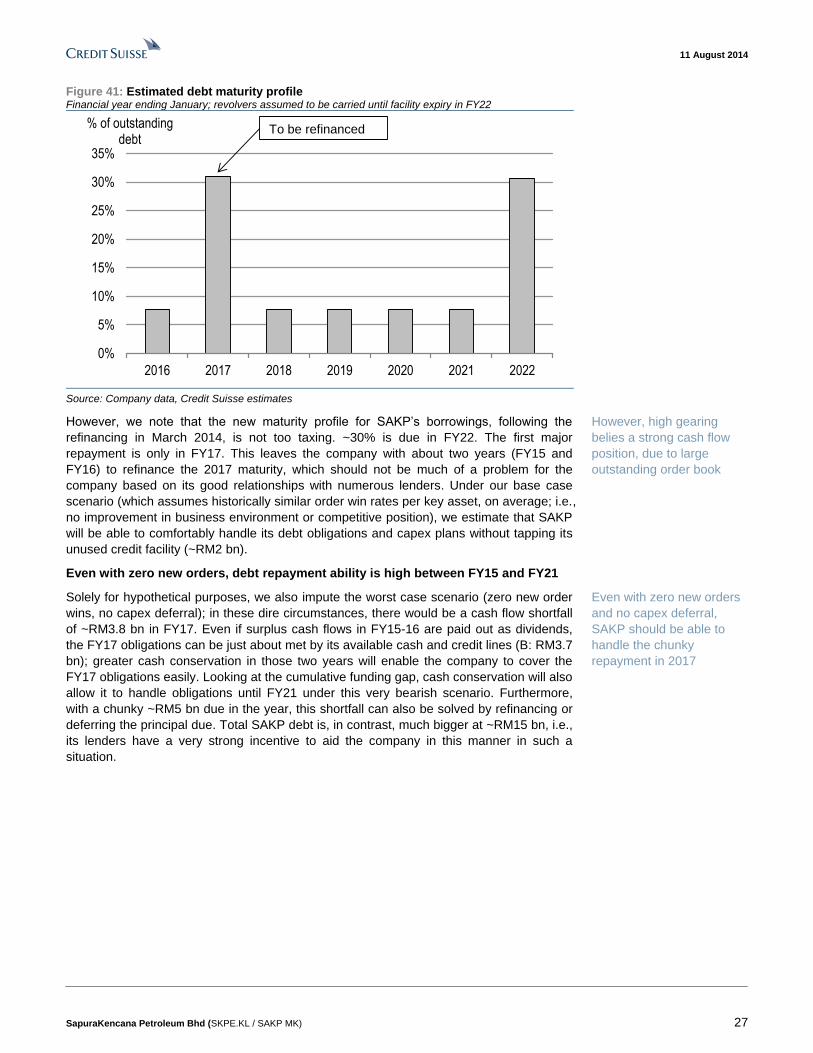

Risk-reward balance better now How does it make money?

SapuraKencana (SAKP) is an integrated upstream oil & gas company, straddling (1)

oilfield services (it is a contractor for offshore development drilling, offshore construction

and subsea services, fabrication, and hook-up and commissioning, with an increasingly

global footprint), (2) exploration and production (SAKP has working interests in oil & gas

blocks under production sharing contracts in Malaysia) and (3) marginal fields—under risk

service contracts, SAKP and its partners develop marginal oil & gas fields in Malaysia and

operate production facilities in return for a fixed payment; Petronas remains the owner.

Are there any economic moats?

SAKP's most valuable assets are intangible: track record, client relationships and

reputation. This moderate but growing economic moat is based on a genuine ability to

compete (~70% of its order book is outside of Malaysia), and is the result of both organic

cultivation and acquisitions. The moat is widest in the Malaysian upstream segment,

where SAKP is a key player across oilfield services, E&P and marginal fields, and within

the tender rig niche, where it holds 44% of global capacity. In EPCIC, however, larger

players still do not see SAKP as a comparable peer, though trends in its order book and

fleet suggest this might only be a matter of time. Its execution track record in OCSS

leverages on advanced assets in its young fleet, which includes several high-spec

strategic assets either already operational or under construction, whilst the niche nature of

tender rigs will likely allow them to maintain their dominance in this profitable, and less

cyclical, segment. These require consistent fleet renewal however; we are a bit more

sceptical on the long-term durability or relative strength of these competitive advantages.

Where can things go wrong?

Our analysis of the various risks facing investors suggests that most potential problems

are adequately mitigated. The only chink in the armour that we see is related to debt

(chunky maturity in two years), though our analysis suggests that only in an extremely

bearish scenario would this be a real problem, due to the strong earnings visibility from the

outstanding order book. Along with a lower dependence on the domestic market, the high

backlog also protects it more from any decline in domestic capex compared to most

Malaysian peers. The E&P business has demonstrated an above-average ability to find

hydrocarbons in Malaysia, and we believe total underlying production costs are within the

lower region of the cost curve, mitigating SAKP's direct exposure to oil/gas prices. In the

near-term, however, there could be downside risk from further selling pressure ahead of

SAKP's removal from the SC's Shariah-compliant list. Management concentration is a

pertinent risk to note, but we are not sure investors would want it to be mitigated.

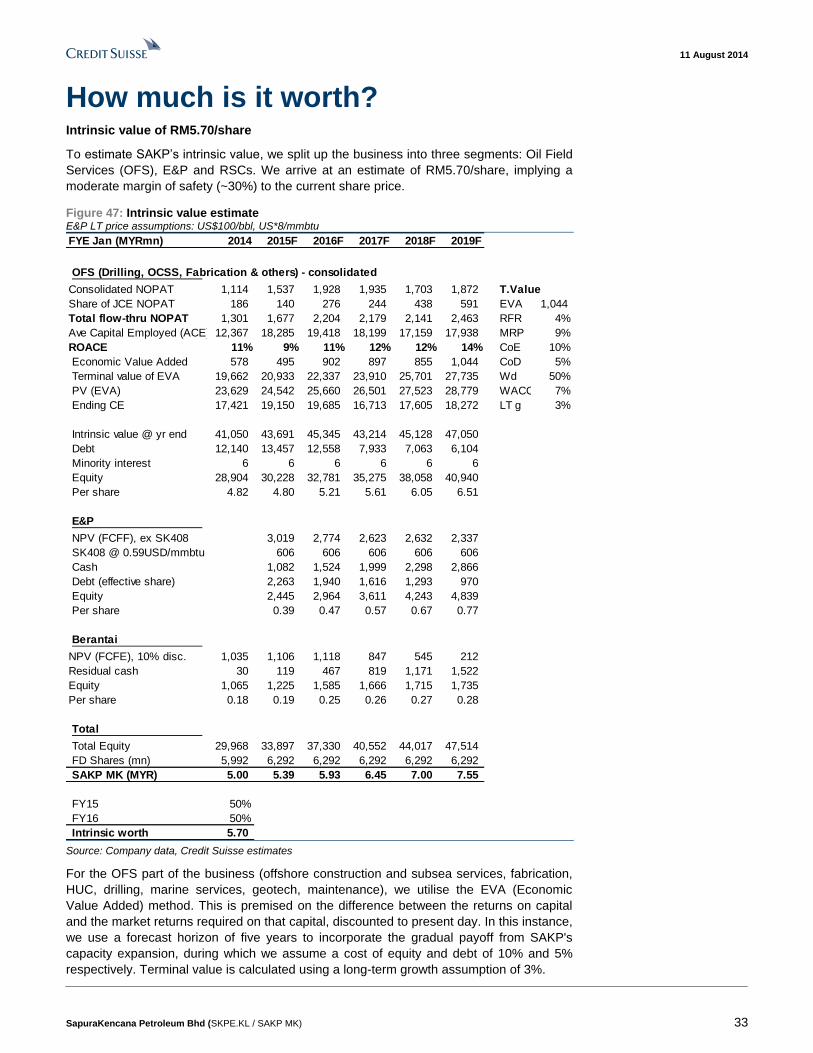

How much is it worth?

Our intrinsic value estimate for SAKP is RM5.70/share, which implies a margin of safety of

~30%. We use an Economic Value Added approach for the oilfield services segments and

mostly DCF for the E&P and marginal field assets. Our target price implies a CY15F P/E

multiple of 18x, well within the mid-range of those seen across the larger-cap O&G-related

stocks in Malaysia, where trapped domestic liquidity with a predilection for liquid names

bids up prices for larger companies. The strength of the business, quality of management

and a decent margin of safety arising from the de-rating in 1H14 (possibly Shariah-related),

combine to form an opportunity in our view. A more logical approach is to wait patiently for a

very wide margin of safety before loading up heavily, but in the absence of the ability to adopt a

concentrated portfolio strategy, we believe the risk-reward balance is good enough at the

moment for investors to contemplate putting their money in.

Key moving parts: offshore

drilling, offshore

construction, E&P

Intangible assets are

moderate but growing

economic moats; OCSS

fleet and tender rig niche

support this, though are

much weaker and less

durable advantages

Most risks are well

mitigated; even with zero

new order wins, cashflow is

strong enough

Decent margin of safety;

intrinsic value of RM5.70

11 August 2014

SapuraKencana Petroleum Bhd (SKPE.KL / SAKP MK) 4

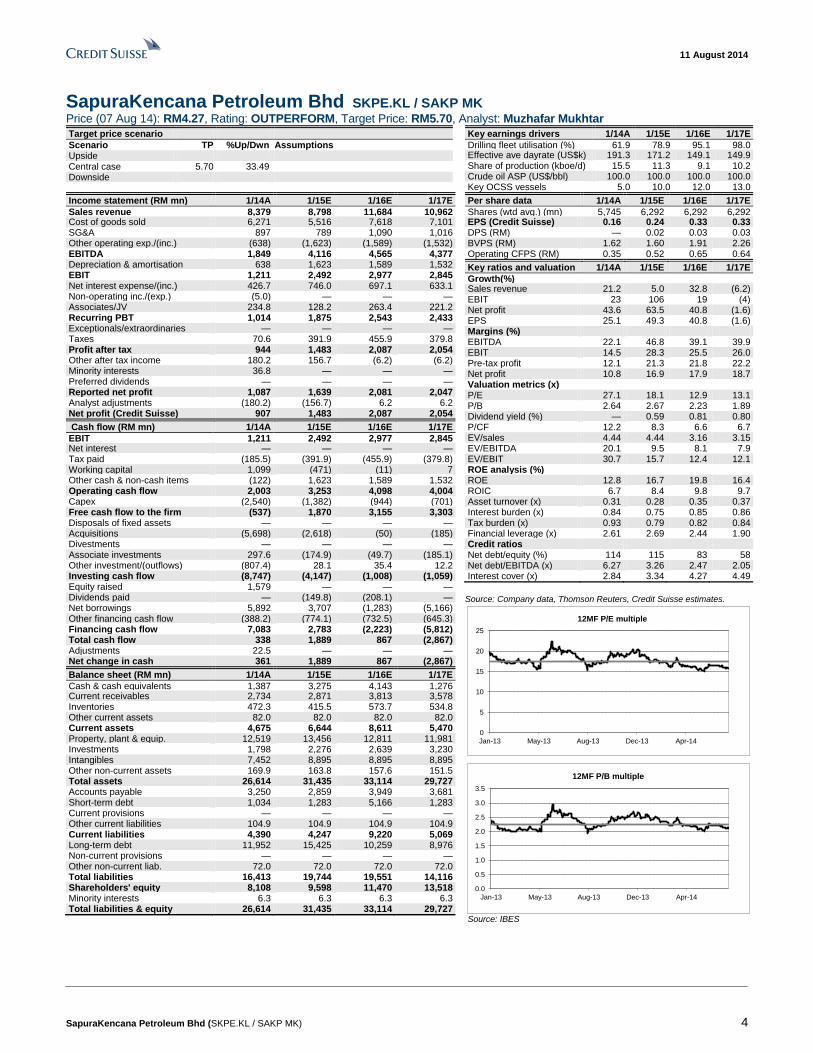

SapuraKencana Petroleum Bhd SKPE.KL / SAKP MK Price (07 Aug 14): RM4.27, Rating: OUTPERFORM, Target Price: RM5.70, Analyst: Muzhafar Mukhtar

Target price scenario

Scenario TP %Up/Dwn Assumptions Upside Central case 5.70 33.49 Downside

Key earnings drivers 1/14A 1/15E 1/16E 1/17E

Drilling fleet utilisation (%) 61.9 78.9 95.1 98.0 Effective ave dayrate (US$k) 191.3 171.2 149.1 149.9 Share of production (kboe/d) 15.5 11.3 9.1 10.2 Crude oil ASP (US$/bbl) 100.0 100.0 100.0 100.0 Key OCSS vessels 5.0 10.0 12.0 13.0

Income statement (RM mn) 1/14A 1/15E 1/16E 1/17E

Sales revenue 8,379 8,798 11,684 10,962 Cost of goods sold 6,271 5,516 7,618 7,101 SG&A 897 789 1,090 1,016 Other operating exp./(inc.) (638) (1,623) (1,589) (1,532) EBITDA 1,849 4,116 4,565 4,377 Depreciation & amortisation 638 1,623 1,589 1,532 EBIT 1,211 2,492 2,977 2,845 Net interest expense/(inc.) 426.7 746.0 697.1 633.1 Non-operating inc./(exp.) (5.0) — — — Associates/JV 234.8 128.2 263.4 221.2 Recurring PBT 1,014 1,875 2,543 2,433 Exceptionals/extraordinaries — — — — Taxes 70.6 391.9 455.9 379.8 Profit after tax 944 1,483 2,087 2,054 Other after tax income 180.2 156.7 (6.2) (6.2) Minority interests 36.8 — — — Preferred dividends — — — — Reported net profit 1,087 1,639 2,081 2,047 Analyst adjustments (180.2) (156.7) 6.2 6.2 Net profit (Credit Suisse) 907 1,483 2,087 2,054

Cash flow (RM mn) 1/14A 1/15E 1/16E 1/17E

EBIT 1,211 2,492 2,977 2,845 Net interest — — — — Tax paid (185.5) (391.9) (455.9) (379.8) Working capital 1,099 (471) (11) 7 Other cash & non-cash items (122) 1,623 1,589 1,532 Operating cash flow 2,003 3,253 4,098 4,004 Capex (2,540) (1,382) (944) (701) Free cash flow to the firm (537) 1,870 3,155 3,303 Disposals of fixed assets — — — — Acquisitions (5,698) (2,618) (50) (185) Divestments — — — — Associate investments 297.6 (174.9) (49.7) (185.1) Other investment/(outflows) (807.4) 28.1 35.4 12.2 Investing cash flow (8,747) (4,147) (1,008) (1,059) Equity raised 1,579 — — — Dividends paid — (149.8) (208.1) — Net borrowings 5,892 3,707 (1,283) (5,166) Other financing cash flow (388.2) (774.1) (732.5) (645.3) Financing cash flow 7,083 2,783 (2,223) (5,812) Total cash flow 338 1,889 867 (2,867) Adjustments 22.5 — — — Net change in cash 361 1,889 867 (2,867)

Balance sheet (RM mn) 1/14A 1/15E 1/16E 1/17E

Cash & cash equivalents 1,387 3,275 4,143 1,276 Current receivables 2,734 2,871 3,813 3,578 Inventories 472.3 415.5 573.7 534.8 Other current assets 82.0 82.0 82.0 82.0 Current assets 4,675 6,644 8,611 5,470 Property, plant & equip. 12,519 13,456 12,811 11,981 Investments 1,798 2,276 2,639 3,230 Intangibles 7,452 8,895 8,895 8,895 Other non-current assets 169.9 163.8 157.6 151.5 Total assets 26,614 31,435 33,114 29,727 Accounts payable 3,250 2,859 3,949 3,681 Short-term debt 1,034 1,283 5,166 1,283 Current provisions — — — — Other current liabilities 104.9 104.9 104.9 104.9 Current liabilities 4,390 4,247 9,220 5,069 Long-term debt 11,952 15,425 10,259 8,976 Non-current provisions — — — — Other non-current liab. 72.0 72.0 72.0 72.0 Total liabilities 16,413 19,744 19,551 14,116 Shareholders' equity 8,108 9,598 11,470 13,518 Minority interests 6.3 6.3 6.3 6.3 Total liabilities & equity 26,614 31,435 33,114 29,727

Per share data 1/14A 1/15E 1/16E 1/17E

Shares (wtd avg.) (mn) 5,745 6,292 6,292 6,292 EPS (Credit Suisse) (RM)

0.16 0.24 0.33 0.33 DPS (RM) — 0.02 0.03 0.03 BVPS (RM) 1.62 1.60 1.91 2.26 Operating CFPS (RM) 0.35 0.52 0.65 0.64

Key ratios and valuation 1/14A 1/15E 1/16E 1/17E

Growth(%) Sales revenue 21.2 5.0 32.8 (6.2) EBIT 23 106 19 (4) Net profit 43.6 63.5 40.8 (1.6) EPS 25.1 49.3 40.8 (1.6) Margins (%) EBITDA 22.1 46.8 39.1 39.9 EBIT 14.5 28.3 25.5 26.0 Pre-tax profit 12.1 21.3 21.8 22.2 Net profit 10.8 16.9 17.9 18.7 Valuation metrics (x) P/E 27.1 18.1 12.9 13.1 P/B 2.64 2.67 2.23 1.89 Dividend yield (%) — 0.59 0.81 0.80 P/CF 12.2 8.3 6.6 6.7 EV/sales 4.44 4.44 3.16 3.15 EV/EBITDA 20.1 9.5 8.1 7.9 EV/EBIT 30.7 15.7 12.4 12.1 ROE analysis (%) ROE 12.8 16.7 19.8 16.4 ROIC 6.7 8.4 9.8 9.7 Asset turnover (x) 0.31 0.28 0.35 0.37 Interest burden (x) 0.84 0.75 0.85 0.86 Tax burden (x) 0.93 0.79 0.82 0.84 Financial leverage (x) 2.61 2.69 2.44 1.90 Credit ratios Net debt/equity (%) 114 115 83 58 Net debt/EBITDA (x) 6.27 3.26 2.47 2.05 Interest cover (x) 2.84 3.34 4.27 4.49

Source: Company data, Thomson Reuters, Credit Suisse estimates.

0

5

10

15

20

25

Jan-13 May-13 Aug-13 Dec-13 Apr-14

12MF P/E multiple

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Jan-13 May-13 Aug-13 Dec-13 Apr-14

12MF P/B multiple

Source: IBES

11 August 2014

SapuraKencana Petroleum Bhd (SKPE.KL / SAKP MK) 5

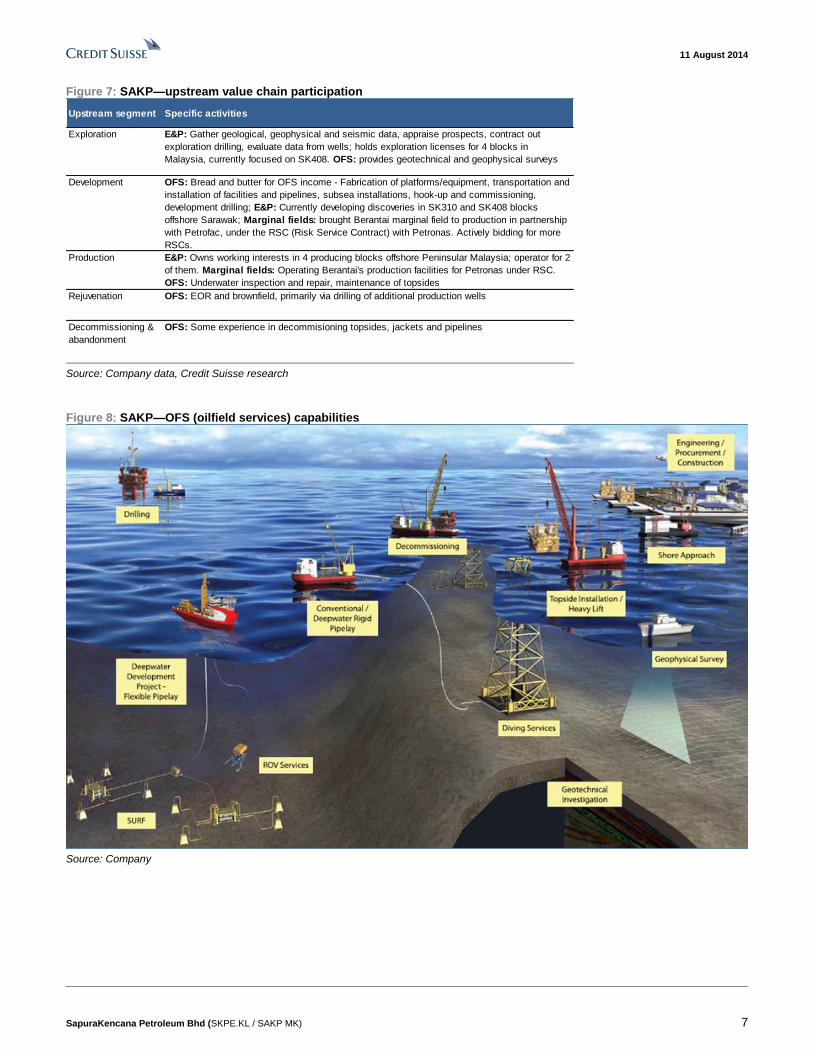

How does it make money? Integrated upstream oil & gas company primarily in drilling, offshore construction

and E&P. SAKP is involved in both E&P (exploration and production), and providing

oilfield services (OFS) for other oil companies. It was born from the merger in early 2012

between the two then-rapidly growing Malaysian oilfield services contractors: SapuraCrest

Petroleum (involved in offshore construction, subsea services and offshore drilling) and

Kencana Petroleum (fabrication, marine services and offshore drilling). The management

team is being led by Tan Sri Shahril Shamsuddin (with a 17% stake), who first entered the

O&G industry in 2003 when the Sapura Group acquired a controlling stake in SapuraCrest

(then known as Crest Petroleum, active in O&G since 1991).

The company bought Seadrill’s tender rig business in April 2013 and extended its reach up

the value chain by acquiring Newfield’s Malaysian E&P business in February 2014.

Throughout this transformative period, SAKP has also been organically increasing its fleet

of offshore construction vessels and drilling rigs. The company reports its business

segments as below (with CS-estimated FY15E profit contribution):

Drilling and energy services (~79% of FY15E profit):

■ Drilling (~53%): The biggest contributor to profits, and the most profitable OFS line.

SAKP owns and operates 19 tender rigs, under contract with E&P companies. Tender

rigs are used only for development drilling (i.e. production wells, not exploration wells);

those on barges are suitable only for shallow waters, whilst the semi-subs (a third of

its fleet) can venture further out up to ~6,500 feet of water. Currently, the fleet is

operating mostly in Southeast Asia and West Africa. EBIT margins are wide at ~40-

50%, and firm charters tend to run for at least a year, going as far out as five years

historically. This segment began with a JV with Seadrill in the early 1990s, and

culminated in the acquisition of Seadrill’s entire tender rig business (i.e., including

management) in 2013. SAKP now controls ~44% of global capacity within the tender

rig sector of the global drilling fleet. We estimate its fleet’s cumulative utilisation rate to

be at an impressive 94% so far. One additional tender rig under construction will be

ready in 2015; we have also assumed one of the older rigs will be scrapped by then.

■ E&P (~19%): In February 2014, SAKP completed the acquisition of the Malaysian

business of US-listed Newfield Exploration. The division has a good track record for

exploration and bringing assets to production quickly. It now has interests in eight

blocks across East Malaysia and Eastern Peninsular Malaysia (plus 1 EOR alliance

contract); the portfolio consists of a good mix of producing, development and

exploration assets. Whilst the production profile will naturally decline between FY15

and FY18, we estimate the existing cash balance and the net free cash flows from

producing assets should be more than sufficient to cover both planned development

and exploration capex. By FY18, the current development play (~3tcf of gas initially in

place in SK310) is scheduled to come into production and will eventually be strongly

cash flow positive. At the moment, the project is awaiting the signature of the gas

sales agreement with Petronas. The existing exploration prospect (block SK408)

provides substantial upside potential, with four major gas finds already announced in

June 2014, about half the size of the SK310 resources, and close to the existing

infrastructure. One well has been completed with the results yet to be announced, and

another five wells will be drilled by the end of CY15 in SK408.

■ Marginal fields (~6%): SAKP was awarded the first of the Risk Service Contracts

(RSCs) in Malaysia in 2011 for the Berantai field, in partnership with Petrofac (50:50).

Under the Berantai RSC, the contractors will develop the field at their own cost and

operate the production facilities; in return, they will receive fixed payments for nine

years, based on several key performance indicators including time to first gas, cost

versus budget, production levels, which can result in project IRRs of 12-22%; capex

Integrated upstream oil

company transformed by

M&A in past two years, but

with roots stretching back

two decades ago

Three key moving parts:

offshore drilling, offshore

construction, and E&P.

Dominant player in tender

rig niche, after acquiring

Seadrill's tender rig

business

E&P focused on existing oil

production from four blocks

in Malaysia, and future

development of gas

resources in two blocks off

Sarawak

Marginal field development

in Malaysia under RSCs

offer an good risk-reward

balance

11 August 2014

SapuraKencana Petroleum Bhd (SKPE.KL / SAKP MK) 6

recovery is guaranteed by Petronas. The oil & gas resources remain under Petronas

ownership. On an average, this particular RSC provides only ~5% of profits, according

to our estimate. However, following the success of Berantai, SAKP will continue to bid

for more RSCs, of which at least ~five are still available. The risk-reward balance of

the RSC model is attractive, and the pool of potential domestic participants is limited

(eligibility requirements include a strong execution track record in O&G, financial

strength, and public listing). SAKP has a strong ability to mitigate execution risk with

its solid field development experience as a contractor, newly acquired E&P capabilities

and existing tie-up with Petrofac, which has proven itself to be very successful with the

Cendor and Berantai marginal fields. This segment is quite promising for the group.

■ Geotech, operations & maintenance (~1%): This includes the chartering out of four

surveying vessels, repairing of General Electric gas turbines, repairs/refurbishment of

single-buoy moorings and valves, and the supply/installation/maintenance of the POS

system used by Petronas Dagangan Bhd’s petrol stations. Profit contribution is very

small in this sub-segment.

Offshore construction and subsea services (~16%):

■ Offshore construction (~16%): One of its traditional bread and butter businesses;

practically all of the profit contribution for OCSS comes from installation of pipeline and

production facilities (IPF). SAKP uses a core fleet of wholly- and jointly-owned vessels

(six derrick lay vessels); partners include Subsea 7, Larsen & Toubro and Seadrill. Due

to the limited global availability of these high-cost vessels, particularly for deepwater,

the consolidated EBIT margin for this activity (i.e., with wholly-owned vessels) can be

quite substantial, up to ~25% in Malaysia and ~40% for deepwater work in Brazil, on

our estimates. In Malaysia, SAKP is dominant and routinely secures the lion’s share of

installation contracts. Internationally, the group has a proven competitive ability and (via

its 50:50 JV with Seadrill) has secured two multi-year charters for six hi-spec PLSVs

(pipe-laying support vessels) from Petrobras worth ~US$4.1 bn. The first vessel is

already completed (ahead of original schedule) and should begin contributing to the

bottom line by 3QFYE Jan-15. Additionally, SAKP provides sub-sea installation

services, and underwater inspection/repair/maintenance, using its own diving support

vessels, saturation diving systems and internally-built ROVs.

■ Marine services: This primarily supports SAKP's offshore construction business, with

a small fleet of accommodation work barges, anchor handling tugs, two MOPUs and a

semi-submersible barge.

Fabrication, hook-up and commissioning (~5%):

■ Fabrication (~5%): SAKP is one of the six major offshore fabricator licensees in

Malaysia; it operates a fabrication yard in Lumut on Peninsular Malaysia, which has a

substantial capacity of 90kmt p.a., and holds 50% stake in the 36kmt p.a. Labuan

Shipyard (LSE) in Sabah, East Malaysia. The Lumut yard generally focuses on

offshore platforms, jackets, equipment skids and other O&G structures, whilst LSE's

main business has previously been the construction and repair of vessels, but with an

increasing bias to O&G-related fabrication. In the recent year, this business segment

has been relatively weak due to the delay in major fabrication contracts previously

expected domestically, with the Lumut yard running at less than 50% utilisation;

however, this should begin to pick up to ~80% with the award of recent contracts.

Profit contribution is small; EBIT margins are typically 10-20%.

■ HUC (<1%): Additionally, SAKP can perform hook-up and commissioning (HUC) for

offshore facilities. It currently has a contract to provide ExxonMobil Malaysia with HUC

services between May 2013 and May 2018, worth ~RM300-500 mn.

OCSS is a key engine for

growth, and where SAKP's

strong reputation has its

roots

11 August 2014

SapuraKencana Petroleum Bhd (SKPE.KL / SAKP MK) 7

Figure 7: SAKP—upstream value chain participation

Upstream segment Specific activities

Exploration E&P: Gather geological, geophysical and seismic data, appraise prospects, contract out

exploration drilling, evaluate data from wells; holds exploration licenses for 4 blocks in

Malaysia, currently focused on SK408. OFS: provides geotechnical and geophysical surveys

Development OFS: Bread and butter for OFS income - Fabrication of platforms/equipment, transportation and

installation of facilities and pipelines, subsea installations, hook-up and commissioning,

development drilling; E&P: Currently developing discoveries in SK310 and SK408 blocks

offshore Sarawak; Marginal fields: brought Berantai marginal field to production in partnership

with Petrofac, under the RSC (Risk Service Contract) with Petronas. Actively bidding for more

RSCs.

Production E&P: Owns working interests in 4 producing blocks offshore Peninsular Malaysia; operator for 2

of them. Marginal fields: Operating Berantai's production facilities for Petronas under RSC.

OFS: Underwater inspection and repair, maintenance of topsides

Rejuvenation OFS: EOR and brownfield, primarily via drilling of additional production wells

Decommissioning &

abandonment

OFS: Some experience in decommisioning topsides, jackets and pipelines

Source: Company data, Credit Suisse research

Figure 8: SAKP—OFS (oilfield services) capabilities

Source: Company

11 August 2014

SapuraKencana Petroleum Bhd (SKPE.KL / SAKP MK) 8

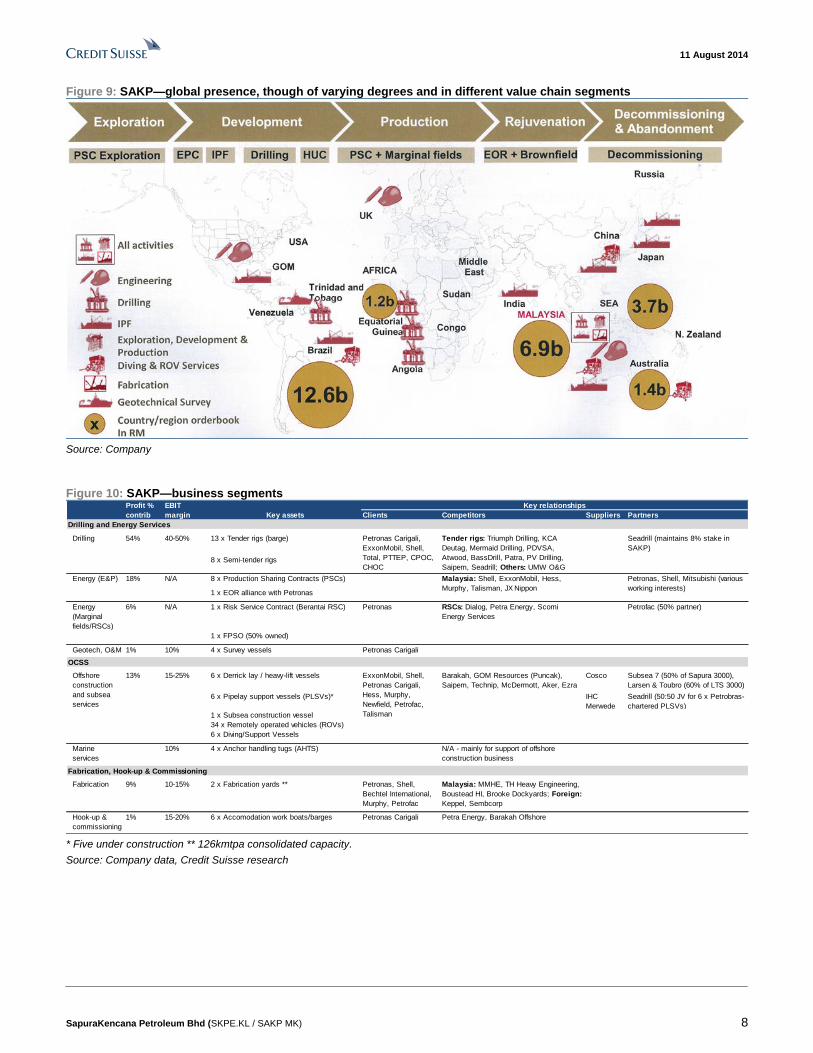

Figure 9: SAKP—global presence, though of varying degrees and in different value chain segments

Source: Company

Figure 10: SAKP—business segments

Clients Competitors Suppliers Partners

Drilling and Energy Services

Drilling 54% 40-50% 13 x Tender rigs (barge) Seadrill (maintains 8% stake in

SAKP)

8 x Semi-tender rigs

Energy (E&P) 18% N/A 8 x Production Sharing Contracts (PSCs)

1 x EOR alliance with Petronas

Energy

(Marginal

fields/RSCs)

6% N/A 1 x Risk Service Contract (Berantai RSC) Petronas Petrofac (50% partner)

1 x FPSO (50% owned)

Geotech, O&M 1% 10% 4 x Survey vessels Petronas Carigali

OCSS

13% 15-25% 6 x Derrick lay / heavy-lift vessels Cosco Subsea 7 (50% of Sapura 3000),

Larsen & Toubro (60% of LTS 3000)

6 x Pipelay support vessels (PLSVs)* IHC

Merwede

Seadrill (50:50 JV for 6 x Petrobras-

chartered PLSVs)

1 x Subsea construction vessel

34 x Remotely operated vehicles (ROVs)

6 x Diving/Support Vessels

Marine

services

10% 4 x Anchor handling tugs (AHTS)

Fabrication, Hook-up & Commissioning

Fabrication 9% 10-15% 2 x Fabrication yards ** Petronas, Shell,

Bechtel International,

Murphy, Petrofac

Malaysia: MMHE, TH Heavy Engineering,

Boustead HI, Brooke Dockyards; Foreign:

Keppel, Sembcorp

Hook-up &

commissioning

1% 15-20% 6 x Accomodation work boats/barges Petronas Carigali Petra Energy, Barakah Offshore

N/A - mainly for support of offshore

construction business

Petronas Carigali,

ExxonMobil, Shell,

Total, PTTEP, CPOC,

CHOC

Tender rigs: Triumph Drilling, KCA

Deutag, Mermaid Drilling, PDVSA,

Atwood, BassDrill, Patra, PV Drilling,

Saipem, Seadrill; Others: UMW O&G

EBIT

margin

Profit %

contrib

Malaysia: Shell, ExxonMobil, Hess,

Murphy, Talisman, JX Nippon

Offshore

construction

and subsea

services

Petronas, Shell, Mitsubishi (various

working interests)

RSCs: Dialog, Petra Energy, Scomi

Energy Services

ExxonMobil, Shell,

Petronas Carigali,

Hess, Murphy,

Newfield, Petrofac,

Talisman

Key relationships

Key assets

Barakah, GOM Resources (Puncak),

Saipem, Technip, McDermott, Aker, Ezra

* Five under construction ** 126kmtpa consolidated capacity.

Source: Company data, Credit Suisse research

11 August 2014

SapuraKencana Petroleum Bhd (SKPE.KL / SAKP MK) 9

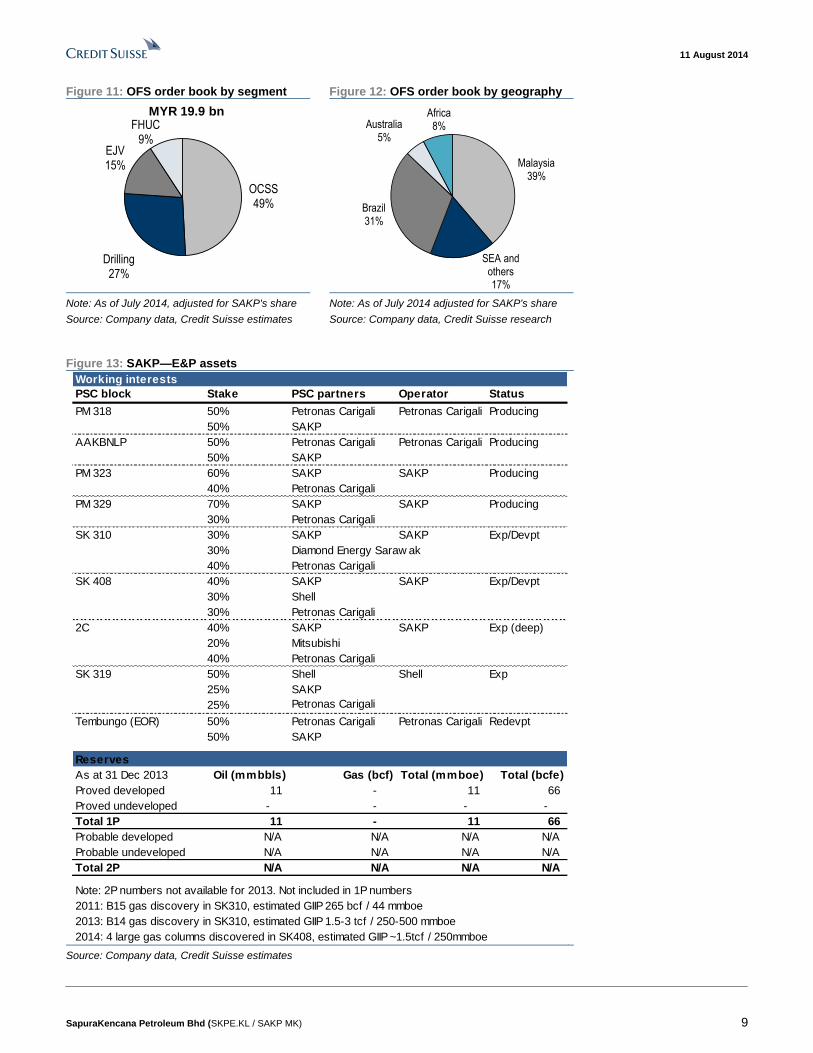

Figure 11: OFS order book by segment Figure 12: OFS order book by geography

OCSS49%

Drilling27%

EJV15%

FHUC9%

MYR 19.9 bn

Malaysia39%

SEA and others17%

Brazil31%

Australia5%

Africa8%

Note: As of July 2014, adjusted for SAKP's share

Source: Company data, Credit Suisse estimates

Note: As of July 2014 adjusted for SAKP's share

Source: Company data, Credit Suisse research

Figure 13: SAKP—E&P assets

Working interests

PSC block Stake PSC partners Operator Status

PM 318 50% Petronas Carigali Petronas Carigali Producing

50% SAKP

AAKBNLP 50% Petronas Carigali Petronas Carigali Producing

50% SAKP

PM 323 60% SAKP SAKP Producing

40% Petronas Carigali

PM 329 70% SAKP SAKP Producing

30% Petronas Carigali

SK 310 30% SAKP SAKP Exp/Devpt

30% Diamond Energy Saraw ak

40% Petronas Carigali

SK 408 40% SAKP SAKP Exp/Devpt

30% Shell

30% Petronas Carigali

2C 40% SAKP SAKP Exp (deep)

20% Mitsubishi

40% Petronas Carigali

SK 319 50% Shell Shell Exp

25% SAKP

25% Petronas Carigali

Tembungo (EOR) 50% Petronas Carigali Petronas Carigali Redevpt

50% SAKP

Reserves

As at 31 Dec 2013 Oil (mmbbls) Gas (bcf) Total (mmboe) Total (bcfe)

Proved developed 11 - 11 66

Proved undeveloped - - - -

Total 1P 11 - 11 66

Probable developed N/A N/A N/A N/A

Probable undeveloped N/A N/A N/A N/A

Total 2P N/A N/A N/A N/A

Note: 2P numbers not available for 2013. Not included in 1P numbers

2011: B15 gas discovery in SK310, estimated GIIP 265 bcf / 44 mmboe

2013: B14 gas discovery in SK310, estimated GIIP 1.5-3 tcf / 250-500 mmboe

2014: 4 large gas columns discovered in SK408, estimated GIIP ~1.5tcf / 250mmboe Source: Company data, Credit Suisse estimates

11 August 2014

SapuraKencana Petroleum Bhd (SKPE.KL / SAKP MK) 10

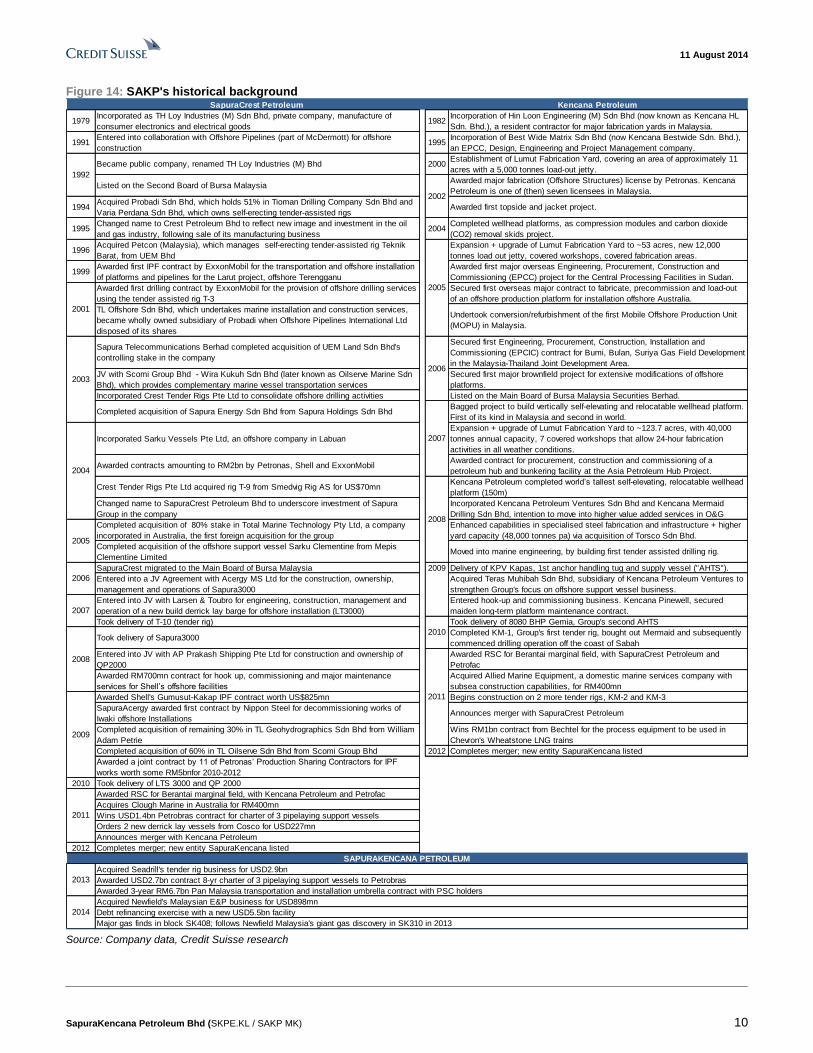

Figure 14: SAKP's historical background SapuraCrest Petroleum Kencana Petroleum

1979Incorporated as TH Loy Industries (M) Sdn Bhd, private company, manufacture of

consumer electronics and electrical goods1982

Incorporation of Hin Loon Engineering (M) Sdn Bhd (now known as Kencana HL

Sdn. Bhd.), a resident contractor for major fabrication yards in Malaysia.

1991Entered into collaboration with Offshore Pipelines (part of McDermott) for offshore

construction1995

Incorporation of Best Wide Matrix Sdn Bhd (now Kencana Bestwide Sdn. Bhd.),

an EPCC, Design, Engineering and Project Management company.

Became public company, renamed TH Loy Industries (M) Bhd 2000Establishment of Lumut Fabrication Yard, covering an area of approximately 11

acres with a 5,000 tonnes load-out jetty.

Listed on the Second Board of Bursa MalaysiaAwarded major fabrication (Offshore Structures) license by Petronas. Kencana

Petroleum is one of (then) seven licensees in Malaysia.

1994Acquired Probadi Sdn Bhd, which holds 51% in Tioman Drilling Company Sdn Bhd and

Varia Perdana Sdn Bhd, which owns self-erecting tender-assisted rigsAwarded first topside and jacket project.

1995Changed name to Crest Petroleum Bhd to reflect new image and investment in the oil

and gas industry, following sale of its manufacturing business2004

Completed wellhead platforms, as compression modules and carbon dioxide

(CO2) removal skids project.

1996Acquired Petcon (Malaysia), which manages self-erecting tender-assisted rig Teknik

Barat, from UEM Bhd

Expansion + upgrade of Lumut Fabrication Yard to ~53 acres, new 12,000

tonnes load out jetty, covered workshops, covered fabrication areas.

1999Awarded first IPF contract by ExxonMobil for the transportation and offshore installation

of platforms and pipelines for the Larut project, offshore Terengganu

Awarded first major overseas Engineering, Procurement, Construction and

Commissioning (EPCC) project for the Central Processing Facilities in Sudan.

Awarded first drilling contract by ExxonMobil for the provision of offshore drilling services

using the tender assisted rig T-3

Secured first overseas major contract to fabricate, precommission and load-out

of an offshore production platform for installation offshore Australia.

TL Offshore Sdn Bhd, which undertakes marine installation and construction services,

became wholly owned subsidiary of Probadi when Offshore Pipelines International Ltd

disposed of its shares

Undertook conversion/refurbishment of the first Mobile Offshore Production Unit

(MOPU) in Malaysia.

Sapura Telecommunications Berhad completed acquisition of UEM Land Sdn Bhd's

controlling stake in the company

Secured first Engineering, Procurement, Construction, Installation and

Commissioning (EPCIC) contract for Bumi, Bulan, Suriya Gas Field Development

in the Malaysia-Thailand Joint Development Area.

JV with Scomi Group Bhd - Wira Kukuh Sdn Bhd (later known as Oilserve Marine Sdn

Bhd), which provides complementary marine vessel transportation services

Secured first major brownfield project for extensive modifications of offshore

platforms.

Incorporated Crest Tender Rigs Pte Ltd to consolidate offshore drilling activities Listed on the Main Board of Bursa Malaysia Securities Berhad.

Completed acquisition of Sapura Energy Sdn Bhd from Sapura Holdings Sdn BhdBagged project to build vertically self-elevating and relocatable wellhead platform.

First of its kind in Malaysia and second in world.

Incorporated Sarku Vessels Pte Ltd, an offshore company in Labuan

Expansion + upgrade of Lumut Fabrication Yard to ~123.7 acres, with 40,000

tonnes annual capacity, 7 covered workshops that allow 24-hour fabrication

activities in all weather conditions.

Awarded contracts amounting to RM2bn by Petronas, Shell and ExxonMobil Awarded contract for procurement, construction and commissioning of a

petroleum hub and bunkering facility at the Asia Petroleum Hub Project.

Crest Tender Rigs Pte Ltd acquired rig T-9 from Smedvig Rig AS for US$70mnKencana Petroleum completed world’s tallest self-elevating, relocatable wellhead

platform (150m)

Changed name to SapuraCrest Petroleum Bhd to underscore investment of Sapura

Group in the company

Incorporated Kencana Petroleum Ventures Sdn Bhd and Kencana Mermaid

Drilling Sdn Bhd, intention to move into higher value added services in O&G

Completed acquisition of 80% stake in Total Marine Technology Pty Ltd, a company

incorporated in Australia, the first foreign acquisition for the group

Enhanced capabilities in specialised steel fabrication and infrastructure + higher

yard capacity (48,000 tonnes pa) via acquisition of Torsco Sdn Bhd.

Completed acquisition of the offshore support vessel Sarku Clementine from Mepis

Clementine LimitedMoved into marine engineering, by building first tender assisted drilling rig.

SapuraCrest migrated to the Main Board of Bursa Malaysia 2009 Delivery of KPV Kapas, 1st anchor handling tug and supply vessel ("AHTS").

Entered into a JV Agreement with Acergy MS Ltd for the construction, ownership,

management and operations of Sapura3000

Acquired Teras Muhibah Sdn Bhd, subsidiary of Kencana Petroleum Ventures to

strengthen Group's focus on offshore support vessel business.

Entered into JV with Larsen & Toubro for engineering, construction, management and

operation of a new build derrick lay barge for offshore installation (LT3000)

Entered hook-up and commissioning business. Kencana Pinewell, secured

maiden long-term platform maintenance contract.

Took delivery of T-10 (tender rig) Took delivery of 8080 BHP Gemia, Group's second AHTS

Took delivery of Sapura3000Completed KM-1, Group's first tender rig, bought out Mermaid and subsequently

commenced drilling operation off the coast of Sabah

Entered into JV with AP Prakash Shipping Pte Ltd for construction and ownership of

QP2000

Awarded RSC for Berantai marginal field, with SapuraCrest Petroleum and

Petrofac

Awarded RM700mn contract for hook up, commissioning and major maintenance

services for Shell’s offshore facilities

Acquired Allied Marine Equipment, a domestic marine services company with

subsea construction capabilities, for RM400mn

Awarded Shell's Gumusut-Kakap IPF contract worth US$825mn Begins construction on 2 more tender rigs, KM-2 and KM-3

SapuraAcergy awarded first contract by Nippon Steel for decommissioning works of

Iwaki offshore InstallationsAnnounces merger with SapuraCrest Petroleum

Completed acquisition of remaining 30% in TL Geohydrographics Sdn Bhd from William

Adam Petrie

Wins RM1bn contract from Bechtel for the process equipment to be used in

Chevron's Wheatstone LNG trains

Completed acquisition of 60% in TL Oilserve Sdn Bhd from Scomi Group Bhd 2012 Completes merger; new entity SapuraKencana listed

Awarded a joint contract by 11 of Petronas’ Production Sharing Contractors for IPF

works worth some RM5bnfor 2010-2012

2010 Took delivery of LTS 3000 and QP 2000

Awarded RSC for Berantai marginal field, with Kencana Petroleum and Petrofac

Acquires Clough Marine in Australia for RM400mn

Wins USD1.4bn Petrobras contract for charter of 3 pipelaying support vessels

Orders 2 new derrick lay vessels from Cosco for USD227mn

Announces merger with Kencana Petroleum

2012 Completes merger; new entity SapuraKencana listed

2002

2010

2011

2009

1992

2001

2003

2004

2007

2005

2007

2008

2005

2006

2006

2011

2008

Debt refinancing exercise with a new USD5.5bn facility

Major gas finds in block SK408; follows Newfield Malaysia's giant gas discovery in SK310 in 2013

2013

2014

SAPURAKENCANA PETROLEUM

Acquired Seadrill's tender rig business for USD2.9bn

Awarded USD2.7bn contract 8-yr charter of 3 pipelaying support vessels to Petrobras

Awarded 3-year RM6.7bn Pan Malaysia transportation and installation umbrella contract with PSC holders

Acquired Newfield's Malaysian E&P business for USD898mn

Source: Company data, Credit Suisse research

1

1 A

ug

us

t 20

14

Sa

pu

raK

en

ca

na P

etro

leu

m B

hd

(SK

PE

.KL / S

AK

P M

K)

11

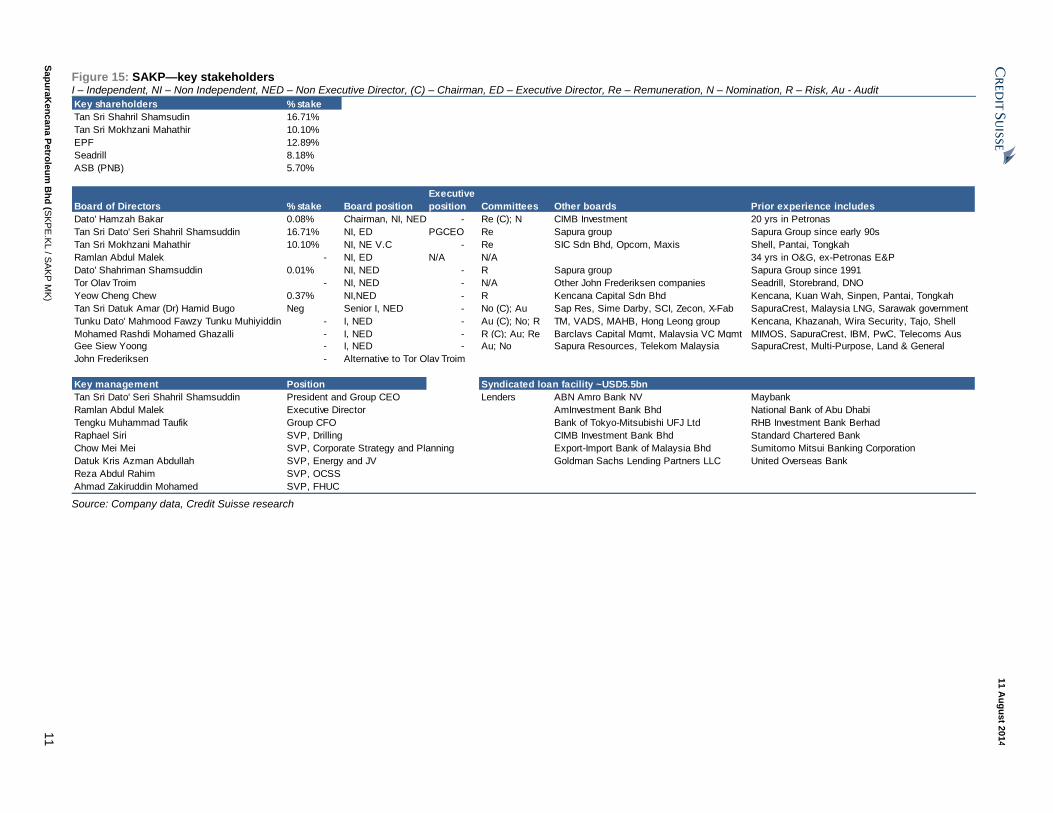

Figure 15: SAKP—key stakeholders I – Independent, NI – Non Independent, NED – Non Executive Director, (C) – Chairman, ED – Executive Director, Re – Remuneration, N – Nomination, R – Risk, Au - Audit

Key shareholders % stake

Tan Sri Shahril Shamsudin 16.71%

Tan Sri Mokhzani Mahathir 10.10%

EPF 12.89%

Seadrill 8.18%

ASB (PNB) 5.70%

Board of Directors % stake Board position

Executive

position Committees Other boards Prior experience includes

Dato' Hamzah Bakar 0.08% Chairman, NI, NED - Re (C); N CIMB Investment 20 yrs in Petronas

Tan Sri Dato' Seri Shahril Shamsuddin 16.71% NI, ED PGCEO Re Sapura group Sapura Group since early 90s

Tan Sri Mokhzani Mahathir 10.10% NI, NE V.C - Re SIC Sdn Bhd, Opcom, Maxis Shell, Pantai, Tongkah

Ramlan Abdul Malek - NI, ED N/A N/A 34 yrs in O&G, ex-Petronas E&P

Dato' Shahriman Shamsuddin 0.01% NI, NED - R Sapura group Sapura Group since 1991

Tor Olav Troim - NI, NED - N/A Other John Frederiksen companies Seadrill, Storebrand, DNO

Yeow Cheng Chew 0.37% NI,NED - R Kencana Capital Sdn Bhd Kencana, Kuan Wah, Sinpen, Pantai, Tongkah

Tan Sri Datuk Amar (Dr) Hamid Bugo Neg Senior I, NED - No (C); Au Sap Res, Sime Darby, SCI, Zecon, X-Fab SapuraCrest, Malaysia LNG, Sarawak government

Tunku Dato' Mahmood Fawzy Tunku Muhiyiddin - I, NED - Au (C); No; R TM, VADS, MAHB, Hong Leong group Kencana, Khazanah, Wira Security, Tajo, Shell

Mohamed Rashdi Mohamed Ghazalli - I, NED - R (C); Au; Re Barclays Capital Mgmt, Malaysia VC Mgmt MIMOS, SapuraCrest, IBM, PwC, Telecoms Aus

Gee Siew Yoong - I, NED - Au; No Sapura Resources, Telekom Malaysia SapuraCrest, Multi-Purpose, Land & General

John Frederiksen - Alternative to Tor Olav Troim

Key management Position Syndicated loan facility ~USD5.5bn

Tan Sri Dato' Seri Shahril Shamsuddin President and Group CEO Lenders ABN Amro Bank NV Maybank

Ramlan Abdul Malek Executive Director AmInvestment Bank Bhd National Bank of Abu Dhabi

Tengku Muhammad Taufik Group CFO Bank of Tokyo-Mitsubishi UFJ Ltd RHB Investment Bank Berhad

Raphael Siri SVP, Drilling CIMB Investment Bank Bhd Standard Chartered Bank

Chow Mei Mei SVP, Corporate Strategy and Planning Export-Import Bank of Malaysia Bhd Sumitomo Mitsui Banking Corporation

Datuk Kris Azman Abdullah SVP, Energy and JV Goldman Sachs Lending Partners LLC United Overseas Bank

Reza Abdul Rahim SVP, OCSS

Ahmad Zakiruddin Mohamed SVP, FHUC Source: Company data, Credit Suisse research

11 August 2014

SapuraKencana Petroleum Bhd (SKPE.KL / SAKP MK) 12

Are there any economic moats? These are the sustainable competitive advantages which will over time produce returns on

capital in excess of returns typically expected on that capital. Moats are not easy to find

and vary in both width and durability, fluctuate with time, and can be eliminated by

competitive destruction (usually in the form of disruptive technology). They result in the

company’s ability to have either strong control over pricing or lower cost (or both) as

compared to peers (more often than not, with some kind of regulatory help). In the case of

SAKP, we believe there is a moderate but growing key economic moat: its intangible

assets (reputation, track record and client relationships). Its possession of hi-spec assets

in the pipe-laying segment and fleet scale in the tender rig segment are also a growing,

though much narrower, economic moat.

Intangible assets: Moderate but growing

Steadily growing track record, reputation, client relationships

Despite its favoured position, SAKP and its precursors (SCRES and KEPB) have not just

relied on protectionism to grow the business; over the past decade, a solid execution track

record with clients has been developed. The most dramatic example of management’s

commitment to clients occurred in 2007. That year, SCRES (mostly involved in OCSS,

back then, plus an offshore drilling JV with Seadrill) incurred its first loss since its takeover

by current SAKP President & CEO Tan Sri Shahril, due to fuel cost volatility and adverse

weather conditions, which had not been sufficiently hedged against. Despite the certainty

of this loss throughout this period (the company lost RM18 mn at the end of the year, after

a profit of RM74 mn the year before), management ensured commitments to clients were

kept. This did not go unnoticed, and TL Offshore (SAKP’s installation subsidiary) has

consistently won the bulk of the Pan-Malaysia installation umbrella contracts since then,

with new contract clauses and ownership of strategic pipe-laying vessels to better control

costs.

Figure 16: Contract wins primarily from outside Malaysia now—sign of growing

reputation and execution ability

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

2007 2008 2009 2010 2011 2012 2013 YTD2014

RM mn Total % foreign of total

Source: Company data, Credit Suisse estimates

Delivery of key OCSS assets between 2008 and 2010 (most notably Sapura3000), also

allowed SAKP to enter foreign markets more aggressively. Foreign orders now contribute

the bulk of its contract wins (~70% YTD). The substantial wins from the competitive market

in Brazil (~US$4.1 bn for six PLSVs for Petrobras in 2013, via JV with Seadrill) were clear

indications of SAKP's growing ability to compete globally. Its acquisition of the Seadrill

Valuable intangible assets

cultivated organically and

acquired, based on genuine

competitiveness

11 August 2014

SapuraKencana Petroleum Bhd (SKPE.KL / SAKP MK) 13

tender rig business in 2013 entailed taking on valuable intangible assets, which have in

the past translated into the sustained high utilisation rate seen for the offshore drilling fleet

(cumulative average now stands at ~94%). The acquisition of Newfield's Malaysian E&P

operations was also that of a business with significant intangible assets—our discussions

with industry players indicate that it has a strong reputation for finding and exploiting

hydrocarbon reserves successfully in Malaysia.

Figure 17: SAKP acquired dominant franchise in tender

rig niche, with 44% of global capacity (includes rigs under

construction)—As of July 2014

Figure 18: These rigs have been contracted for ~94% of

their life, on average

SAKP44%

Atlantica9%

Mermaid8%

Triumph8%

Energy6%

KCA6%

Seadrill6%

Others (5)14%

0%10%20%30%40%50%60%70%80%90%

100%

Utilisation Average

Source: Rigzone data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

To us, these are all clear signs that its client relationships and reputation are not only

deepening and widening (organically and inorganically), but are based on a growing

genuine ability to deliver, rather than protectionism and Petronas handouts.

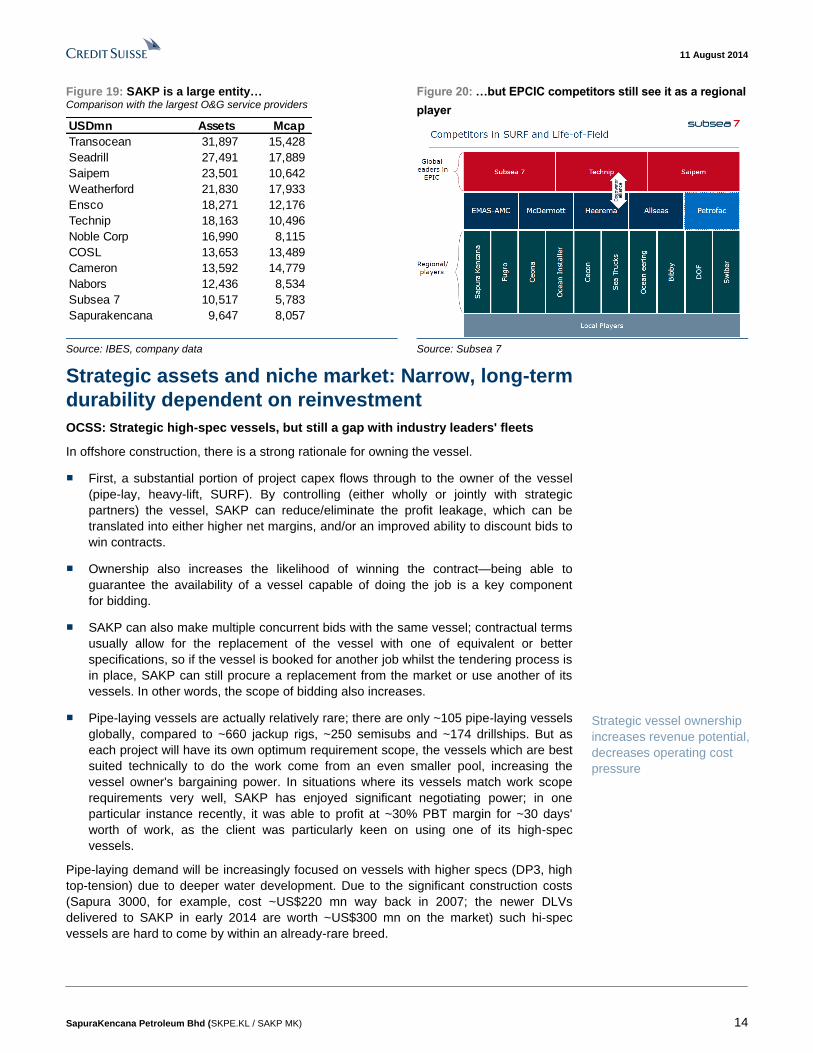

This moat is very wide in Malaysia, across EPCIC (engineering, procurement, construction,

installation & commissioning), E&P and offshore drilling, but is narrower in foreign markets,

in varying degrees. Despite being one of the biggest upstream O&G contractors in terms of

total assets, with its relatively short history, SAKP’s global brand is naturally not yet as strong

as some of its competitors, who still view it as a regional EPCIC/OCSS player. The brand is

stronger outside of Malaysia within the tender rig niche, where it is the dominant player

globally and is clearly visible in the key tender rig markets of Southeast Asia and West Africa.

The reputation of the E&P business is less relevant in foreign markets, since operations

have been confined to Malaysia (although clearly other intangible assets such as its

expertise in finding and exploiting oil are also applicable elsewhere).

Apart from the obvious benefits, strong client relationships have multiple spill-over effects

which also directly translate into better volumes and pricing (i.e., order wins): (1) key

clients such as Shell and ExxonMobil are global players with company-wide standards and

fairly independent of protectionist policies. Successfully delivering in Malaysia (a

significant resource base within Asia-Pacific) enhances SAKP's ability to win contracts

from the same client elsewhere around the world. (2) It is only natural that companies will

gravitate towards providers whom they are confident, from past experience, can do the job

safely within the cost and time constraints. Switching from a familiar, reliable contractor to

a new entrant incurs a risk on the decision-maker. The high premium on safety in the oil &

gas industry amplifies this form of switching cost, which basically translates into better

pricing power for SAKP (i.e., new entrants would have to drop prices substantially to justify

the risk of switching seen by the client).

Spill-over effects from

strong client relationships

11 August 2014

SapuraKencana Petroleum Bhd (SKPE.KL / SAKP MK) 14

Figure 19: SAKP is a large entity… Comparison with the largest O&G service providers

Figure 20: …but EPCIC competitors still see it as a regional

player

USDmn Assets Mcap

Transocean 31,897 15,428

Seadrill 27,491 17,889

Saipem 23,501 10,642

Weatherford 21,830 17,933

Ensco 18,271 12,176

Technip 18,163 10,496

Noble Corp 16,990 8,115

COSL 13,653 13,489

Cameron 13,592 14,779

Nabors 12,436 8,534

Subsea 7 10,517 5,783

Sapurakencana 9,647 8,057

Source: IBES, company data Source: Subsea 7

Strategic assets and niche market: Narrow, long-term

durability dependent on reinvestment

OCSS: Strategic high-spec vessels, but still a gap with industry leaders' fleets

In offshore construction, there is a strong rationale for owning the vessel.

■ First, a substantial portion of project capex flows through to the owner of the vessel

(pipe-lay, heavy-lift, SURF). By controlling (either wholly or jointly with strategic

partners) the vessel, SAKP can reduce/eliminate the profit leakage, which can be

translated into either higher net margins, and/or an improved ability to discount bids to

win contracts.

■ Ownership also increases the likelihood of winning the contract—being able to

guarantee the availability of a vessel capable of doing the job is a key component

for bidding.

■ SAKP can also make multiple concurrent bids with the same vessel; contractual terms

usually allow for the replacement of the vessel with one of equivalent or better

specifications, so if the vessel is booked for another job whilst the tendering process is

in place, SAKP can still procure a replacement from the market or use another of its

vessels. In other words, the scope of bidding also increases.

■ Pipe-laying vessels are actually relatively rare; there are only ~105 pipe-laying vessels

globally, compared to ~660 jackup rigs, ~250 semisubs and ~174 drillships. But as

each project will have its own optimum requirement scope, the vessels which are best

suited technically to do the work come from an even smaller pool, increasing the

vessel owner's bargaining power. In situations where its vessels match work scope

requirements very well, SAKP has enjoyed significant negotiating power; in one

particular instance recently, it was able to profit at ~30% PBT margin for ~30 days'

worth of work, as the client was particularly keen on using one of its high-spec

vessels.

Pipe-laying demand will be increasingly focused on vessels with higher specs (DP3, high

top-tension) due to deeper water development. Due to the significant construction costs

(Sapura 3000, for example, cost ~US$220 mn way back in 2007; the newer DLVs

delivered to SAKP in early 2014 are worth ~US$300 mn on the market) such hi-spec

vessels are hard to come by within an already-rare breed.

Strategic vessel ownership

increases revenue potential,

decreases operating cost

pressure

11 August 2014

SapuraKencana Petroleum Bhd (SKPE.KL / SAKP MK) 15

Vessels which are more flexible in work scope (i.e. capable of doing several types of jobs)

are also strategic, allowing owners a greater ability to maximise utilisation; the flipside is

that these tend to require a larger capital investment upfront.

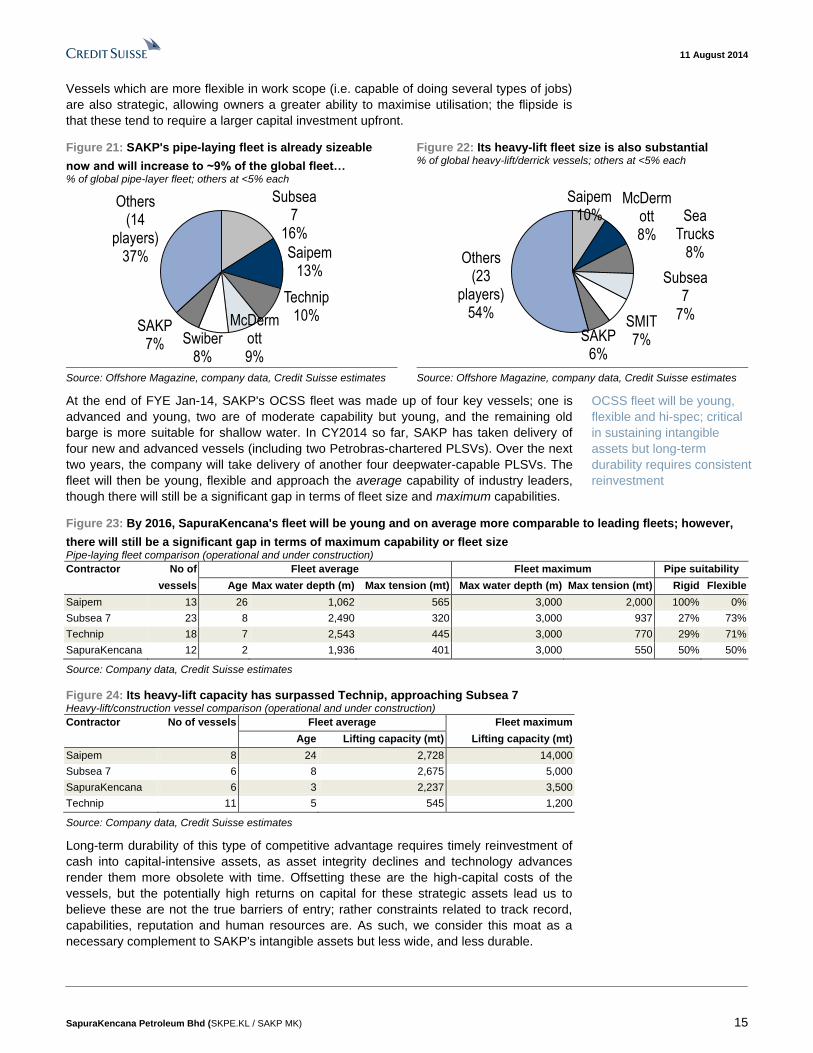

Figure 21: SAKP's pipe-laying fleet is already sizeable

now and will increase to ~9% of the global fleet… % of global pipe-layer fleet; others at <5% each

Figure 22: Its heavy-lift fleet size is also substantial % of global heavy-lift/derrick vessels; others at <5% each

Subsea 7

16%

Saipem13%

Technip10%McDerm

ott9%

Swiber 8%

SAKP7%

Others (14

players)37%

Saipem10%

McDermott8%

Sea Trucks

8%

Subsea 7

7%SMIT7%SAKP

6%

Others (23

players)54%

Source: Offshore Magazine, company data, Credit Suisse estimates Source: Offshore Magazine, company data, Credit Suisse estimates

At the end of FYE Jan-14, SAKP's OCSS fleet was made up of four key vessels; one is

advanced and young, two are of moderate capability but young, and the remaining old

barge is more suitable for shallow water. In CY2014 so far, SAKP has taken delivery of

four new and advanced vessels (including two Petrobras-chartered PLSVs). Over the next

two years, the company will take delivery of another four deepwater-capable PLSVs. The

fleet will then be young, flexible and approach the average capability of industry leaders,

though there will still be a significant gap in terms of fleet size and maximum capabilities.

Figure 23: By 2016, SapuraKencana's fleet will be young and on average more comparable to leading fleets; however,

there will still be a significant gap in terms of maximum capability or fleet size Pipe-laying fleet comparison (operational and under construction)

Contractor No of Fleet average Fleet maximum Pipe suitability

vessels Age Max water depth (m) Max tension (mt) Max water depth (m) Max tension (mt) Rigid Flexible

Saipem 13 26 1,062 565 3,000 2,000 100% 0%

Subsea 7 23 8 2,490 320 3,000 937 27% 73%

Technip 18 7 2,543 445 3,000 770 29% 71%

SapuraKencana 12 2 1,936 401 3,000 550 50% 50%

Source: Company data, Credit Suisse estimates

Figure 24: Its heavy-lift capacity has surpassed Technip, approaching Subsea 7 Heavy-lift/construction vessel comparison (operational and under construction)

Contractor No of vessels Fleet average Fleet maximum

Age Lifting capacity (mt) Lifting capacity (mt)

Saipem 8 24 2,728 14,000

Subsea 7 6 8 2,675 5,000

SapuraKencana 6 3 2,237 3,500

Technip 11 5 545 1,200

Source: Company data, Credit Suisse estimates

Long-term durability of this type of competitive advantage requires timely reinvestment of

cash into capital-intensive assets, as asset integrity declines and technology advances

render them more obsolete with time. Offsetting these are the high-capital costs of the

vessels, but the potentially high returns on capital for these strategic assets lead us to

believe these are not the true barriers of entry; rather constraints related to track record,

capabilities, reputation and human resources are. As such, we consider this moat as a

necessary complement to SAKP's intangible assets but less wide, and less durable.

OCSS fleet will be young,

flexible and hi-spec; critical

in sustaining intangible

assets but long-term

durability requires consistent

reinvestment

11 August 2014

SapuraKencana Petroleum Bhd (SKPE.KL / SAKP MK) 16

Tender rigs: niche with decent prospects, but deeper water evolution unavoidable

In offshore drilling (~50% of earnings), SAKP specialises specifically in tender rigs—these

house the equipment and manpower in a separate hull and requires the transportation of

the drilling package onto a production platform, which eliminates the concept as a feasible

alternative in hydrocarbon exploration, but does provide for a cost-effective alternative in

development drilling compared to jackups, semisubs and platform rigs (drilling packages

integrated into the production platform).

There are 48 tender rigs operating and under construction in the world; in comparison

there are ~660 jackups, ~250 semi-subs and ~250 platform rigs. The reason for that is

because their application, as described above, is very limited in scope. Within this niche

market, SAKP is clearly the dominant player, controlling almost half of the global tender rig

fleet. What this translates into is natural protection from larger players in the overall

offshore drilling market who have little incentive in competing for such a small segment,

already dominated by a single player. The tender rig market is also less cyclical, since it is

geared to development drilling, which provides for more stable income, but with less

upside potential (which arise during cycle up-turns in other market segments)

Figure 25: SAKP's drilling presence is focused on the

tender rig niche… % of global drilling fleet (tender and all types of rigs)

Figure 26: Where income stability has been attractive, but

with less potential upside Average annual dayrates for various offshore drilling rigs

Tender Total

SAKP 44% Transocean 7%

Atlantica 8% ENSCO 5%

Mermaid Drilling 8% Nabors 5%

Triumph Drilling 8% Seadrill 4%

Energy Drilling 6% KCA Deutag 3%

KCA Deutag 6% Diamond 3%

Seadrill 6% COSL 3%

Others (5) 13% Hercules 3%

Shelf 3%

Maersk 2%

PDVSA 2%

Archer 2%

SAKP 1%

Others (60) 58%

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

500,000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

USD/day

Drillship Tender Jackup Semisubmersible

Source: Rigzone, company data, Credit Suisse estimates Source: IHS Petrodata

Opportunities in West Africa and SEA will still be plentiful for tender rigs in the medium

term, including in Malaysia where Petronas is increasingly focused on brownfield activities

for fields (mature fields are mostly in shallow waters off the Peninsula's east coast,

followed by Sarawak). Semisub hulls also allow the same concept to be utilised in deeper

waters. However, in our opinion, prospects are not so bright that larger players will begin

to muscle into this segment, as can be seen from a comparison of the key players in the

tender and overall offshore drilling markets.

The long-term durability of this narrow economic moat may be questionable however, as

discoveries are increasingly in deeper waters; whilst semi-tenders can theoretically work

up to ~6,500 feet / ~2,000 metres of water depth, ~65% of SAKP's fleet is barge units.

Semi-tenders will also see the transfer of people and equipment to and from the

production platform via a walkway; harsh conditions (wind, current, swell) tend to result in

high down-times. To maintain the relevance of its fleet in the long term, SAKP will have to

upgrade it continuously, and possibly eventually venture into more capital-intensive

segments of the offshore-drilling market.

Niche nature of tender rigs

and lower potential return

deters bigger players from

competing

Niche market offers

protection for now but

relevance of fleet requires

continuous reinvestment

into deeper-water units

11 August 2014

SapuraKencana Petroleum Bhd (SKPE.KL / SAKP MK) 17

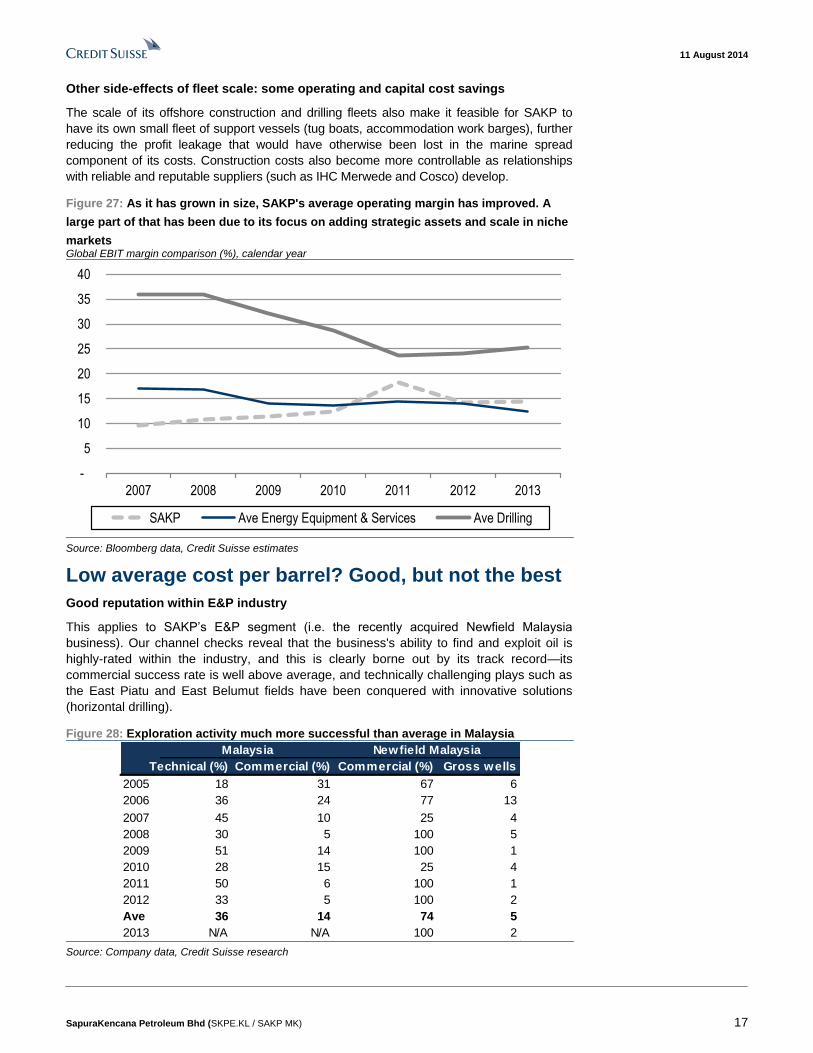

Other side-effects of fleet scale: some operating and capital cost savings

The scale of its offshore construction and drilling fleets also make it feasible for SAKP to

have its own small fleet of support vessels (tug boats, accommodation work barges), further

reducing the profit leakage that would have otherwise been lost in the marine spread

component of its costs. Construction costs also become more controllable as relationships

with reliable and reputable suppliers (such as IHC Merwede and Cosco) develop.

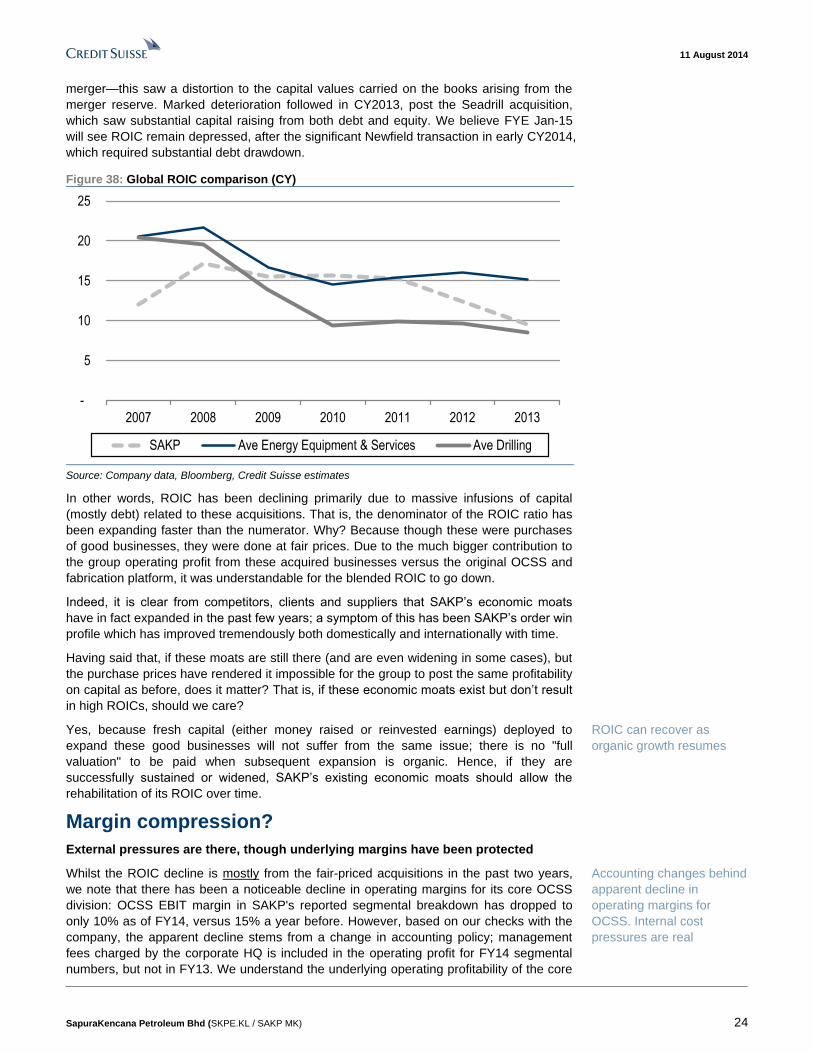

Figure 27: As it has grown in size, SAKP's average operating margin has improved. A

large part of that has been due to its focus on adding strategic assets and scale in niche

markets Global EBIT margin comparison (%), calendar year

-

5

10

15

20

25

30

35

40

2007 2008 2009 2010 2011 2012 2013

SAKP Ave Energy Equipment & Services Ave Drilling

Source: Bloomberg data, Credit Suisse estimates

Low average cost per barrel? Good, but not the best

Good reputation within E&P industry

This applies to SAKP’s E&P segment (i.e. the recently acquired Newfield Malaysia

business). Our channel checks reveal that the business's ability to find and exploit oil is

highly-rated within the industry, and this is clearly borne out by its track record—its

commercial success rate is well above average, and technically challenging plays such as

the East Piatu and East Belumut fields have been conquered with innovative solutions

(horizontal drilling).

Figure 28: Exploration activity much more successful than average in Malaysia

Technical (%) Commercial (%) Commercial (%) Gross wells

2005 18 31 67 6

2006 36 24 77 13

2007 45 10 25 4

2008 30 5 100 5

2009 51 14 100 1

2010 28 15 25 4

2011 50 6 100 1

2012 33 5 100 2

Ave 36 14 74 5

2013 N/A N/A 100 2

Malaysia Newfield Malaysia

Source: Company data, Credit Suisse research

11 August 2014

SapuraKencana Petroleum Bhd (SKPE.KL / SAKP MK) 18

Figure 29: Exploration success also stacks up well versus reputable peers in Asia Talisman data includes Vietnam for a few years

SAKP Murphy Talisman Shell Exxon Chevron Total BP Ave

2006 73 66 57 61 83 88 na 50 71

2007 61 71 54 51 67 75 98 42 67

2008 69 60 22 58 63 70 81 52 65

2009 63 51 11 70 43 72 76 37 60

2010 57 65 22 64 29 74 66 43 55

2011 37 85 70 34 20 77 53 50 47

2012 24 87 100 21 25 75 55 66 49

2013 67 82 81 9 36 81 39 73 48

Net productive exploratory w ells / Total net exploratory w ells (3 year rolling)

AsiaMalaysia

Source: Company data, Credit Suisse estimates

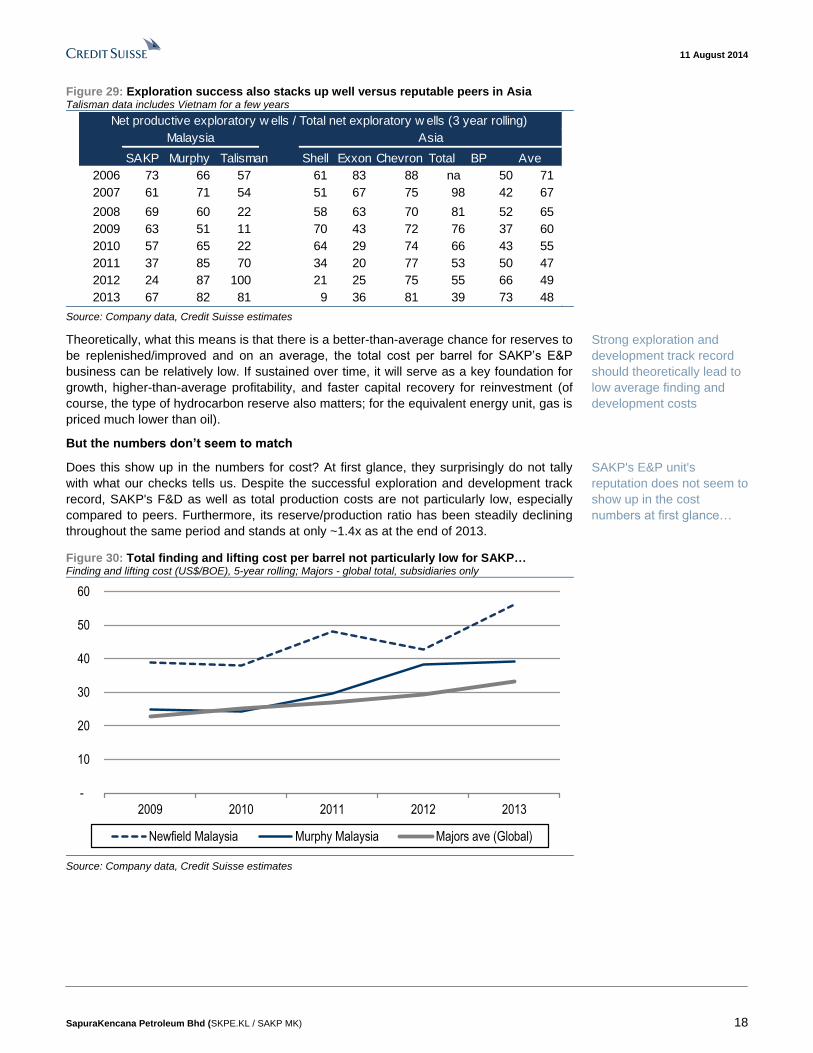

Theoretically, what this means is that there is a better-than-average chance for reserves to

be replenished/improved and on an average, the total cost per barrel for SAKP’s E&P

business can be relatively low. If sustained over time, it will serve as a key foundation for

growth, higher-than-average profitability, and faster capital recovery for reinvestment (of

course, the type of hydrocarbon reserve also matters; for the equivalent energy unit, gas is

priced much lower than oil).

But the numbers don’t seem to match

Does this show up in the numbers for cost? At first glance, they surprisingly do not tally

with what our checks tells us. Despite the successful exploration and development track

record, SAKP's F&D as well as total production costs are not particularly low, especially

compared to peers. Furthermore, its reserve/production ratio has been steadily declining

throughout the same period and stands at only ~1.4x as at the end of 2013.

Figure 30: Total finding and lifting cost per barrel not particularly low for SAKP… Finding and lifting cost (US$/BOE), 5-year rolling; Majors - global total, subsidiaries only

-

10

20

30

40

50

60

2009 2010 2011 2012 2013

Newfield Malaysia Murphy Malaysia Majors ave (Global)

Source: Company data, Credit Suisse estimates

Strong exploration and

development track record

should theoretically lead to

low average finding and

development costs

SAKP's E&P unit's

reputation does not seem to

show up in the cost

numbers at first glance…

11 August 2014

SapuraKencana Petroleum Bhd (SKPE.KL / SAKP MK) 19

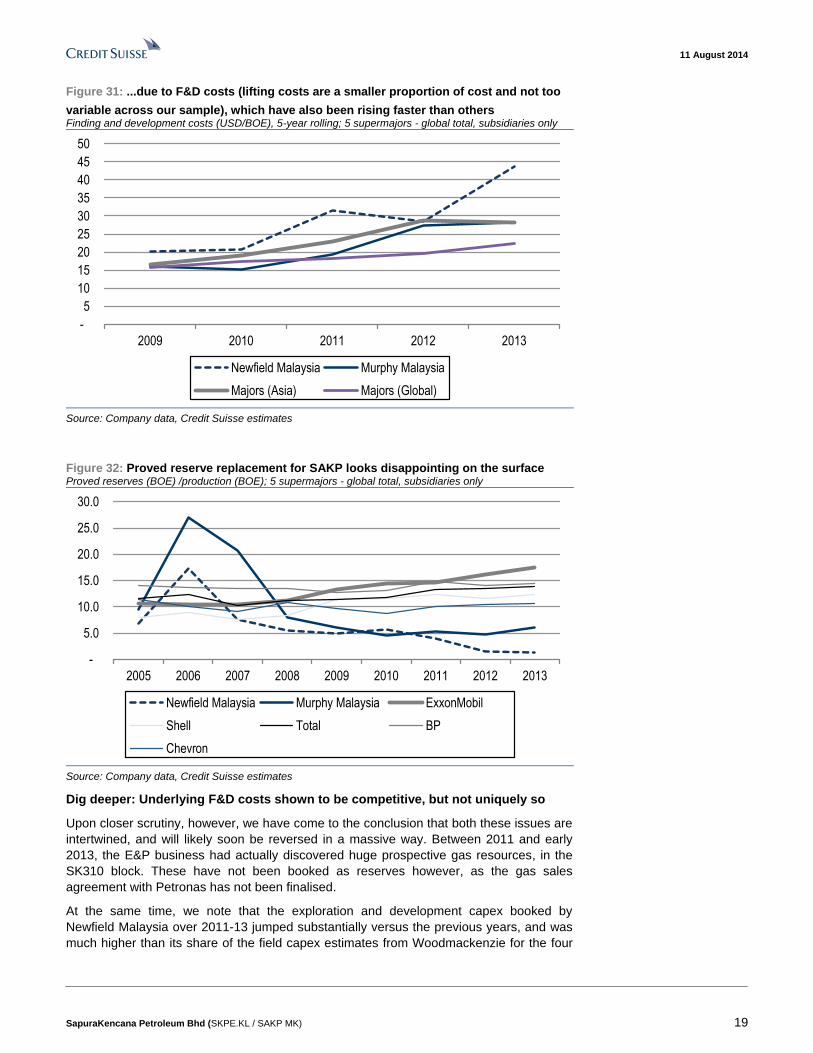

Figure 31: ...due to F&D costs (lifting costs are a smaller proportion of cost and not too

variable across our sample), which have also been rising faster than others Finding and development costs (USD/BOE), 5-year rolling; 5 supermajors - global total, subsidiaries only

-

5

10

15

20

25

30

35

40

45

50

2009 2010 2011 2012 2013

Newfield Malaysia Murphy Malaysia

Majors (Asia) Majors (Global)

Source: Company data, Credit Suisse estimates

Figure 32: Proved reserve replacement for SAKP looks disappointing on the surface Proved reserves (BOE) /production (BOE); 5 supermajors - global total, subsidiaries only

-

5.0

10.0

15.0

20.0

25.0

30.0

2005 2006 2007 2008 2009 2010 2011 2012 2013

Newfield Malaysia Murphy Malaysia ExxonMobil

Shell Total BP

Chevron

Source: Company data, Credit Suisse estimates

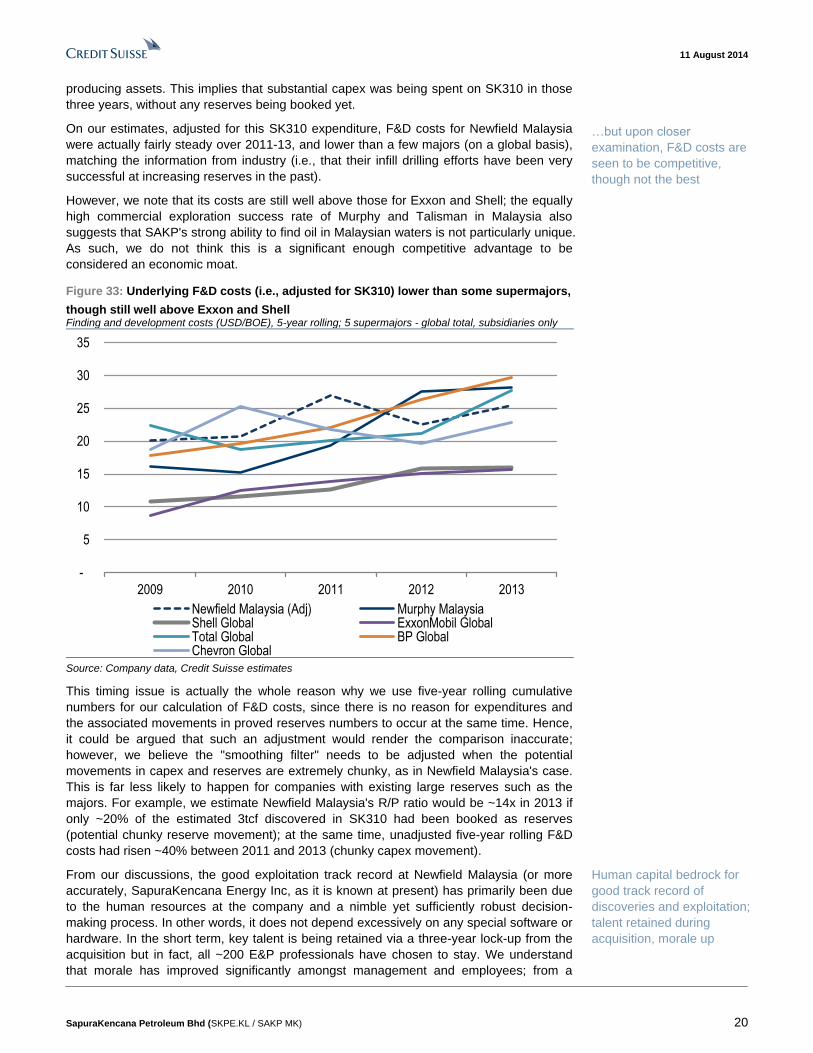

Dig deeper: Underlying F&D costs shown to be competitive, but not uniquely so

Upon closer scrutiny, however, we have come to the conclusion that both these issues are

intertwined, and will likely soon be reversed in a massive way. Between 2011 and early

2013, the E&P business had actually discovered huge prospective gas resources, in the

SK310 block. These have not been booked as reserves however, as the gas sales

agreement with Petronas has not been finalised.

At the same time, we note that the exploration and development capex booked by

Newfield Malaysia over 2011-13 jumped substantially versus the previous years, and was

much higher than its share of the field capex estimates from Woodmackenzie for the four

11 August 2014

SapuraKencana Petroleum Bhd (SKPE.KL / SAKP MK) 20

producing assets. This implies that substantial capex was being spent on SK310 in those

three years, without any reserves being booked yet.

On our estimates, adjusted for this SK310 expenditure, F&D costs for Newfield Malaysia

were actually fairly steady over 2011-13, and lower than a few majors (on a global basis),

matching the information from industry (i.e., that their infill drilling efforts have been very

successful at increasing reserves in the past).

However, we note that its costs are still well above those for Exxon and Shell; the equally

high commercial exploration success rate of Murphy and Talisman in Malaysia also

suggests that SAKP's strong ability to find oil in Malaysian waters is not particularly unique.

As such, we do not think this is a significant enough competitive advantage to be

considered an economic moat.

Figure 33: Underlying F&D costs (i.e., adjusted for SK310) lower than some supermajors,

though still well above Exxon and Shell Finding and development costs (USD/BOE), 5-year rolling; 5 supermajors - global total, subsidiaries only

-

5

10

15

20

25

30

35

2009 2010 2011 2012 2013

Newfield Malaysia (Adj) Murphy MalaysiaShell Global ExxonMobil GlobalTotal Global BP GlobalChevron Global

Source: Company data, Credit Suisse estimates

This timing issue is actually the whole reason why we use five-year rolling cumulative

numbers for our calculation of F&D costs, since there is no reason for expenditures and

the associated movements in proved reserves numbers to occur at the same time. Hence,

it could be argued that such an adjustment would render the comparison inaccurate;

however, we believe the "smoothing filter" needs to be adjusted when the potential

movements in capex and reserves are extremely chunky, as in Newfield Malaysia's case.

This is far less likely to happen for companies with existing large reserves such as the

majors. For example, we estimate Newfield Malaysia's R/P ratio would be ~14x in 2013 if

only ~20% of the estimated 3tcf discovered in SK310 had been booked as reserves

(potential chunky reserve movement); at the same time, unadjusted five-year rolling F&D

costs had risen ~40% between 2011 and 2013 (chunky capex movement).

From our discussions, the good exploitation track record at Newfield Malaysia (or more

accurately, SapuraKencana Energy Inc, as it is known at present) has primarily been due

to the human resources at the company and a nimble yet sufficiently robust decision-

making process. In other words, it does not depend excessively on any special software or

hardware. In the short term, key talent is being retained via a three-year lock-up from the

acquisition but in fact, all ~200 E&P professionals have chosen to stay. We understand

that morale has improved significantly amongst management and employees; from a

…but upon closer

examination, F&D costs are

seen to be competitive,

though not the best

Human capital bedrock for

good track record of

discoveries and exploitation;

talent retained during

acquisition, morale up

11 August 2014

SapuraKencana Petroleum Bhd (SKPE.KL / SAKP MK) 21

business that was expected to simply pay out cash to its US parent, management is now

dealing with a shareholder keen on having them grow the business.

We take comfort in SAKP management’s success in talent retention in previous

acquisitions (Seadrill tender rigs: 2,000 professionals; Clough: 100). Equally as importantly,

SAKP's top management has made it clear that the E&P business will be allowed to

operate on a standalone basis, with as little intervention from the group as possible. The

only addition to the E&P management team has been a financial controller who will focus

on the overall Group's interests. Furthermore, an attractive shadow share option scheme

is in place to align the financial interests of SapuraKencana Energy's management with

the Group's shareholders.

Regulatory protection? Not so relevant anymore

Oil & gas activity is usually highly regulated; in Malaysia, all upstream activity is governed

by Petronas, which is appointed the sole custodian of Malaysia’s oil & gas resources. All

services and goods must be procured from licensees. Due to the strategic importance of

the sector, and the obvious benefits of pro-domestic policy, there is also a requirement for

substantial local content/equity across the industry: the cabotage policy, bumiputera

vendor programme, and bumiputera equity requirement are examples of this. This facet of

protection will likely endure in Malaysia, making it easier for SAKP to continue winning

contracts domestically and expand vertically in its key market, since it has developed a

strong working relationship with Petronas, and is controlled by bumiputera shareholders.

Whilst this protection does not extend beyond Malaysia, a strong home base will continue

to provide a firm experiential and financial platform from which SAKP can keep venturing

into other markets overseas.

However, despite our belief that it is highly unlikely that this form of protection will reverse

completely, there are already clear signs that it is being slowly relaxed. And even amongst

those enjoying this protection, a greater degree of competition is being fostered. For

example, in the Pan Malaysia T&I (Transport and Installation) contract award for 2010-12,

SAKP bagged almost all of the packages available; only one small package was awarded

to Global Offshore Malaysia (GOM). In the latest round however, for 2014-16, SAKP still

grabbed the lion's share, but a greater proportion of the work was awarded to two other

domestic competitors (GOM and Barakah Offshore Petroleum). As for engineering and

construction, MMHE (the largest fabrication yard in Malaysia, and a subsidiary of

Petronas) has been finding it hard to win jobs. To a large part this has been the result of

stronger competition seen in contracts tendered out in Malaysia, where foreign players

have been allowed in; projects previously deemed to be "for Malaysians only" were

opened up, resulting in the trend of lower margins seen across the board.

As such, we believe this factor is not durable or strong enough to be considered an

economic moat; furthermore, the considerations that go into license award are not readily

clear, and the potential for manipulation in a tightly-regulated sector is always there. In any

case, SAKP's increasingly foreign exposure makes this less relevant with time.

11 August 2014

SapuraKencana Petroleum Bhd (SKPE.KL / SAKP MK) 22

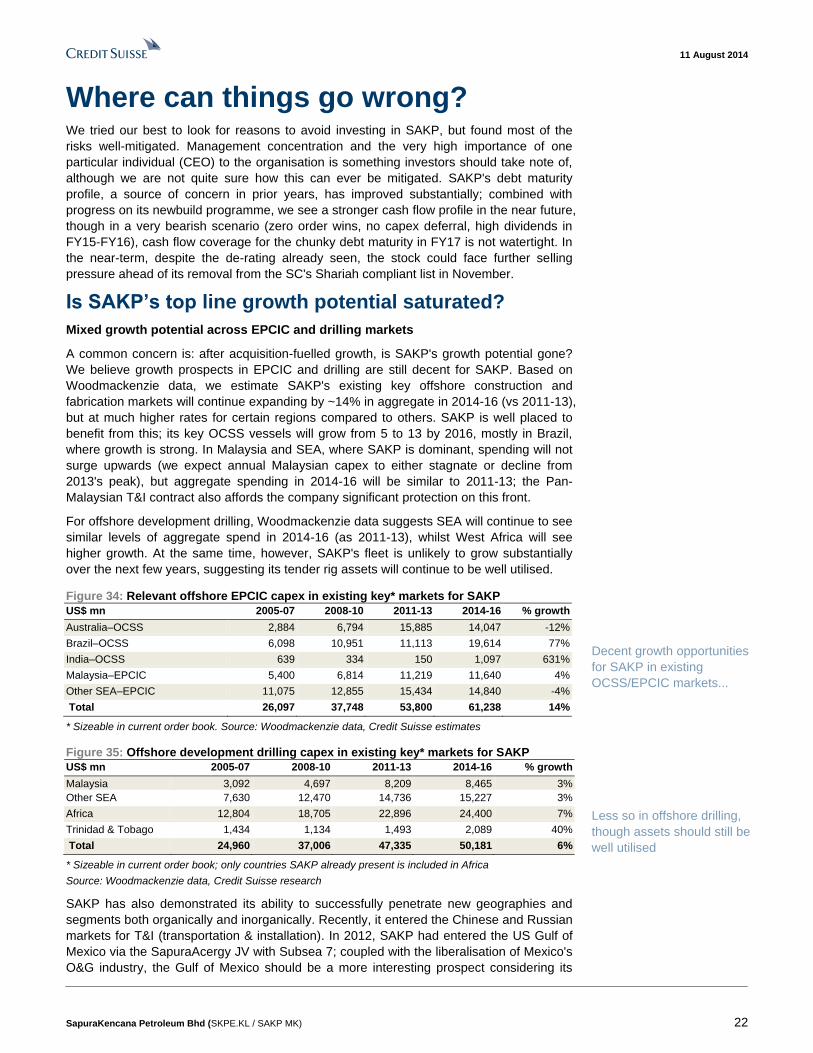

Where can things go wrong? We tried our best to look for reasons to avoid investing in SAKP, but found most of the

risks well-mitigated. Management concentration and the very high importance of one

particular individual (CEO) to the organisation is something investors should take note of,

although we are not quite sure how this can ever be mitigated. SAKP's debt maturity

profile, a source of concern in prior years, has improved substantially; combined with

progress on its newbuild programme, we see a stronger cash flow profile in the near future,

though in a very bearish scenario (zero order wins, no capex deferral, high dividends in

FY15-FY16), cash flow coverage for the chunky debt maturity in FY17 is not watertight. In