choose HEALTH develop CAREER grow WEALTH 2014 RUSH BENEFITS GUIDE

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Rush is a not-for-profit health care, education and research enterprise comprising Rush University Medical Center, Rush University, Rush Oak Park Hospital and Rush Health.

I-2900 10/13

choose H E A L T H develop C A R E E Rgrow W E A L T H

2014

RUSH BENEFITS

GUIDE

CHANGES TO RUSH EMPLOYEE BENEFITS FOR 2014

Rush provides you with a full range of affordable employee benefits to enhance your health, help you prepare for retirement and protect you and your family against the unexpected. It’s one of the many ways we’re working to be an employer of choice in the Chicagoland area.

This enrollment guide provides important details about your employee benefits for 2014, including several changes to your benefits options.

Introducing the new Health Savings Advantage PlanIn addition to the medical plans that are currently available, you will have a new medical plan option for 2014, the Health Savings Advantage plan. This plan is a special kind of PPO that provides you with 100 percent coverage for preventive and wellness care as well as financial protection against significant medical expenses. It is the only type of plan that enables you to open a Health Savings Account (HSA). Having an HSA gives you a tax-advantaged way to save for current and future health care costs — even costs you might incur in retirement. Plus, Rush helps you fund your HSA by contributing money you can use to help pay your current deductible or save for future medical expenses ($750 per year for individual coverage or $1,500 per year for employee + spouse, employee + children, or family coverage). That’s a real advantage.

Dental Plan Improvements Rush offers a choice between a Dental PPO and Dental HMO plan. Both plans cover preventive care and minor and major restorative care. In 2014, the Dental PPO plan will change in two important ways:

• WithanewPreventiveAdvantageProgram,in-networkpreventivechargeswillnotcounttowardtheannual maximum benefit.

• Additionally,newhiresenrolledintheDentalPPOplanwillnotneedtowait12monthsbeforetheyreceive coverage for major dental procedures.

1

choose HE

ALT

Hdevelop C

AR

EE

Rgrow

WE

ALT

Hbalance L

IFE

Your Online Benefits ResourceAs a Rush employee, you can go to https://Rushbenefits.HRintouch.com anytime, anywhere for all your benefit needs.• EnrollinyourRushbenefits

• Viewyourcurrentbenefitelectionsandcosts

• Viewbeneficiaryanddependentinformation

• Makechangesduringtheyearafterqualifyingevents(suchasthebirthofachild)

• GetdetailsaboutRushbenefitsandwellnessprogramsthatcanhelpyouimproveyourtotalhealth—your physical, financial and personal well-being

Use Rush Providers and SaveAs an employee of Rush, you receive significant discounts when you use Rush Health physicians and facilities. This includes Rush University Medical Center, Rush Oak Park Hospital and Rush Copley Medical Center. Keep in mind, you still receive in-network benefits if you use a provider in the Cigna network, you just pay less if it’s a Rush Health provider.

In addition to lower costs, you’ll get to experience Rush from the inside. As an employee, this is important because it can help you better understand our patients and what they experience when they visit a Rush provider or facility.

Asyoumayknow,Rushiswidelyconsideredoneofthebestmedicalcentersinthenation.Auniquecombinationofresearch and patient care has earned Rush national rankings in nine of the 16 specialty areas in U.S. News & World Report’s 2013-14 America’s Best Hospitalsissue,amongotherrecognitionsofourqualityofcareandaccreditations.Why not make Rush your home for health care?

Wehopeyoufindthisbenefitsguidetobehelpfulandinformative.Asalways,shouldyouhaveanyquestionsregard-ing your Rush benefits, please don’t hesitate to contact human resources at (312) 942-6637, Monday through Friday, 8a.m.to4p.m.,orcontactourbenefitsprovidersthroughtheinformationlistedonpage55.Wevalueyouandyourservice to Rush and our patients. Please read this guide carefully and Put Rush Rewards to Work for You.

2

choo

se H

EA

LTH

deve

lop

CA

RE

ER

grow

WE

ALT

Hba

lanc

e L

IFE

3

WHAT’S INSIDE

GENERAL INFORMATION ON RUSH BENEFITS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6 Eligibility. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6 Table of eligibility start dates for new employees . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6 New Federal Rule about Same-Sex Marriage . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

Definition of a dependent. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6 Civil Union coverage . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6 Coverage levels . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7 Table of benefits and eligibility. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7 Information on when you can make benefit changes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8 Keeping your information current . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8 Choose Health . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

RUSH MEDICAL PLANS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10 Rush medical plans. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10 Coverage differences between the health plans . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10 Benefits provided by the health plans . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11 Understanding the new Health Savings Advantage Plan. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

The Triple Tax Advantage. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12 HowtheMedicalPlanandHSAWorkTogether . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12 WhoisEligible. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

Using Your HSA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13 Maximum Contributions to Your HSA for 2014 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13 Basic,Premier,HealthSavingsAdvantageorSelectEPO:Whichisrightforyou?. . . . . . . . . . . . . . . . . . . . . . . . . . . 14 WhattheBasic,PremierandHealthSavingsAdvantagehaveincommon . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15 How the Basic, Premier and Health Savings Advantage differ from one another . . . . . . . . . . . . . . . . . . . . . . . . . . . 15 Example:Avisittothedoctor. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

YOUR ANNUAL DEDUCTIBLE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17 Comparisonchart:Basic,Premier,HealthSavingsAdvantageandEPOPlans . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

ExpressScriptsPharmacy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22 Prescription coverage with the Health Savings Advantage plan . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22 Prescription out-of-pocket maximum costs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

Using your prescription drug benefits to your best advantage . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23 Infertility prescription and treatment coverage . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23 Smoking cessation prescription coverage . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23 2014 Non-Union Tobacco Free Medical Rates per pay period . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

2014 Non-Union Tobacco User Medical Rates per pay period . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25 DENTAL PLANS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

Comparison chart: PPO and Dental HMO . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27 2014 employee dental insurance rates per pay period. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

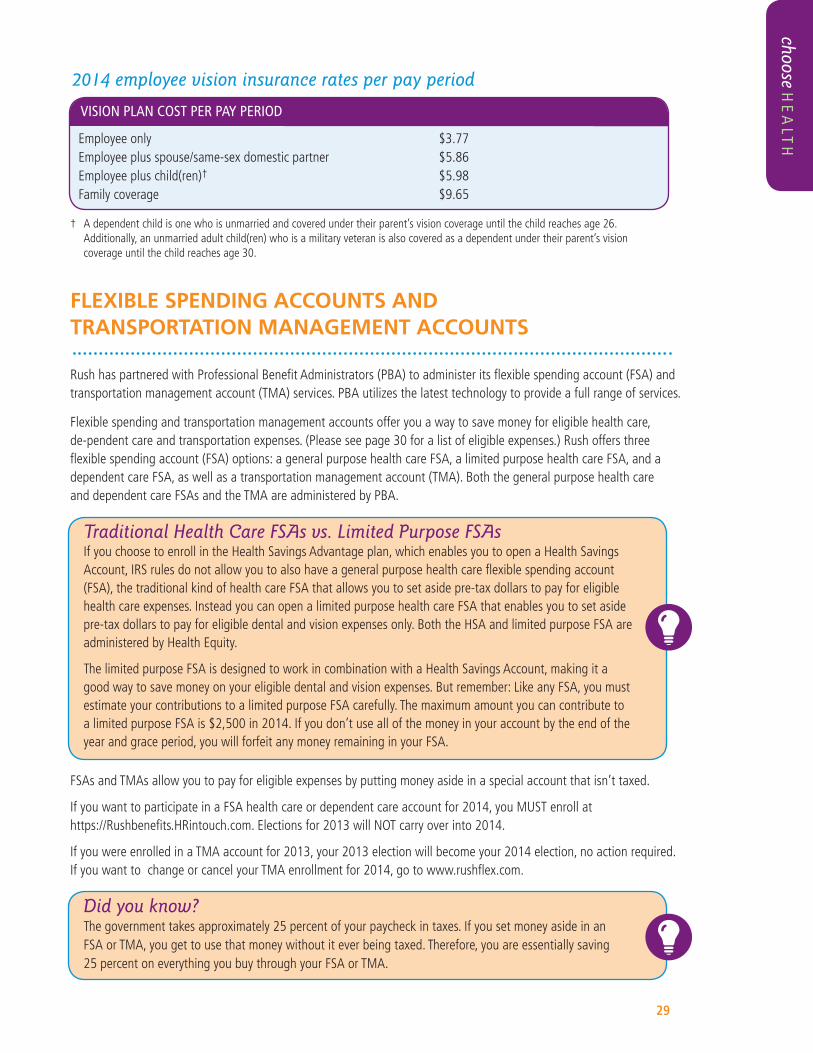

VISION PLAN. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28 Visionplancoveredservices. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28 2014 employee vision insurance rates per pay period . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

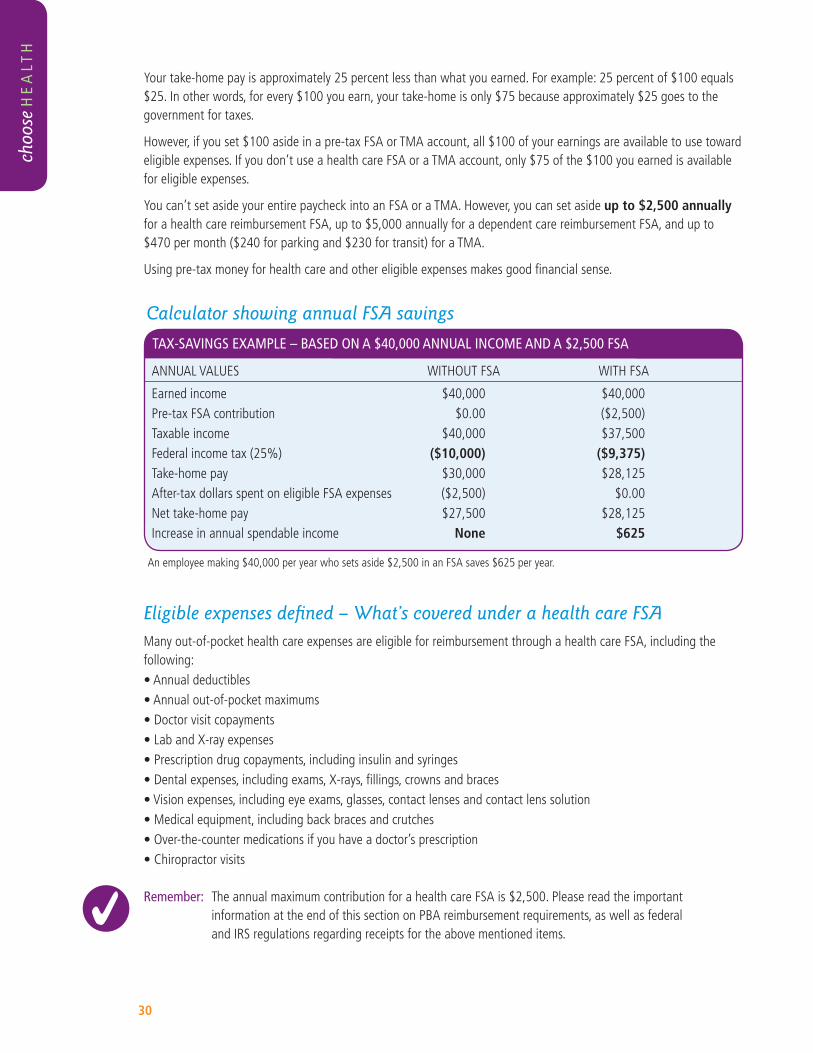

FLEXIBLE SPENDING ACCOUNTS (FSAs) AND TRANSPORTATION MANAGEMENT ACCOUNTS (TMAs) . . . . . . . . 29 Calculator showing annual FSA savings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

choose HE

ALT

Hdevelop C

AR

EE

Rgrow

WE

ALT

Hbalance L

IFE

4

Eligibleexpensesdefined . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30 Health care FSAs are easy to use. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31 Signing up for Direct Deposit. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31 Dependent care FSAs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31 Reimbursement for dependent care FSAs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

Transportation management accounts (TMAs) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32 Reimbursement options for TMAs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32

How deductions are made for FSAs and TMAs. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32How to enroll . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32

Separation from Rush and your FSA/TMA accounts. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32 Federal laws and IRS regulations regarding FSAs and TMAs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33 Save your receipts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

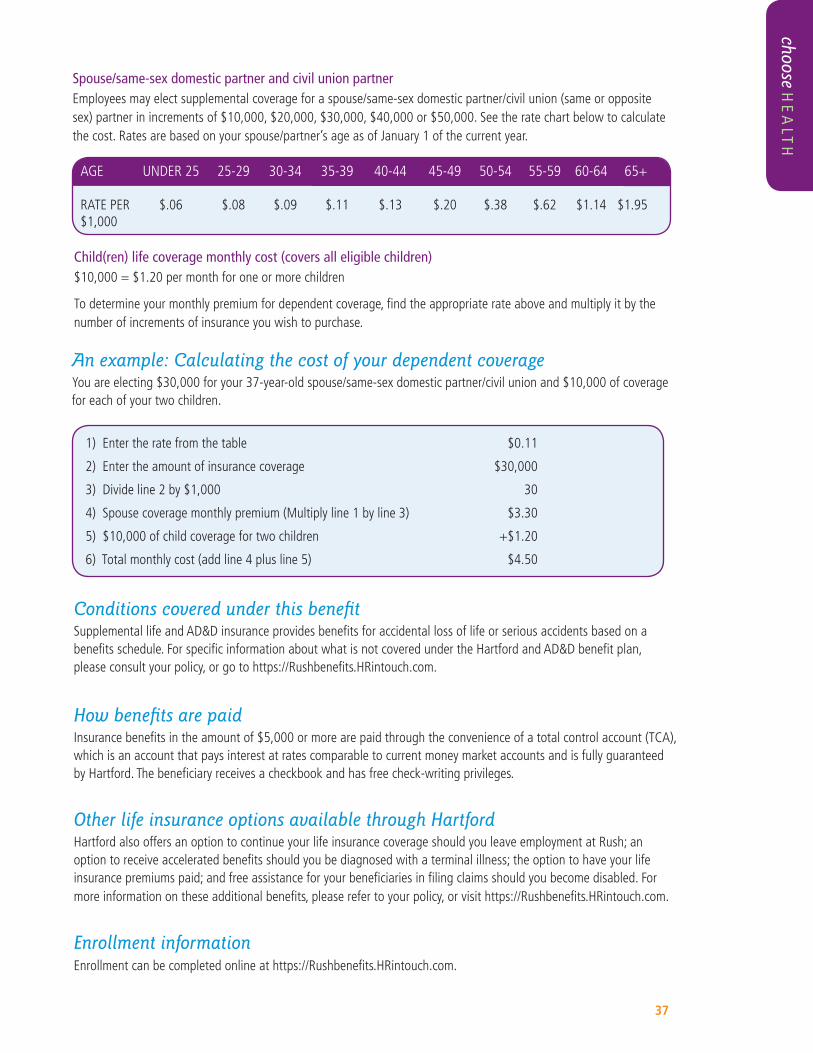

LIFE AND ACCIDENTAL DEATH AND DISMEMBERMENT (AD&D) INSURANCE . . . . . . . . . . . . . . . . . . . . . . . . . . . 34 GeneralinformationabouttheRushlifeinsuranceandAD&Dbenefit. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34 Whoiseligibleforsupplementalcoverage . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35 Determining the amount of supplemental coverage you may need . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35 Supplemental life insurance coverage amounts. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35 Evidenceofhealthformsfornewandexistingemployees . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36 Spouse/same-sex domestic or civil union partner (same or opposite)/child . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36 Determining the cost of supplemental coverage. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36 How to calculate your supplemental life insurance premium . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36 An example: Calculating the cost of your dependent coverage . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37 Conditions covered under this benefit. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37

How benefits are paid . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37 Other life insurance options available through Hartford. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37 Enrollmentinformation. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37

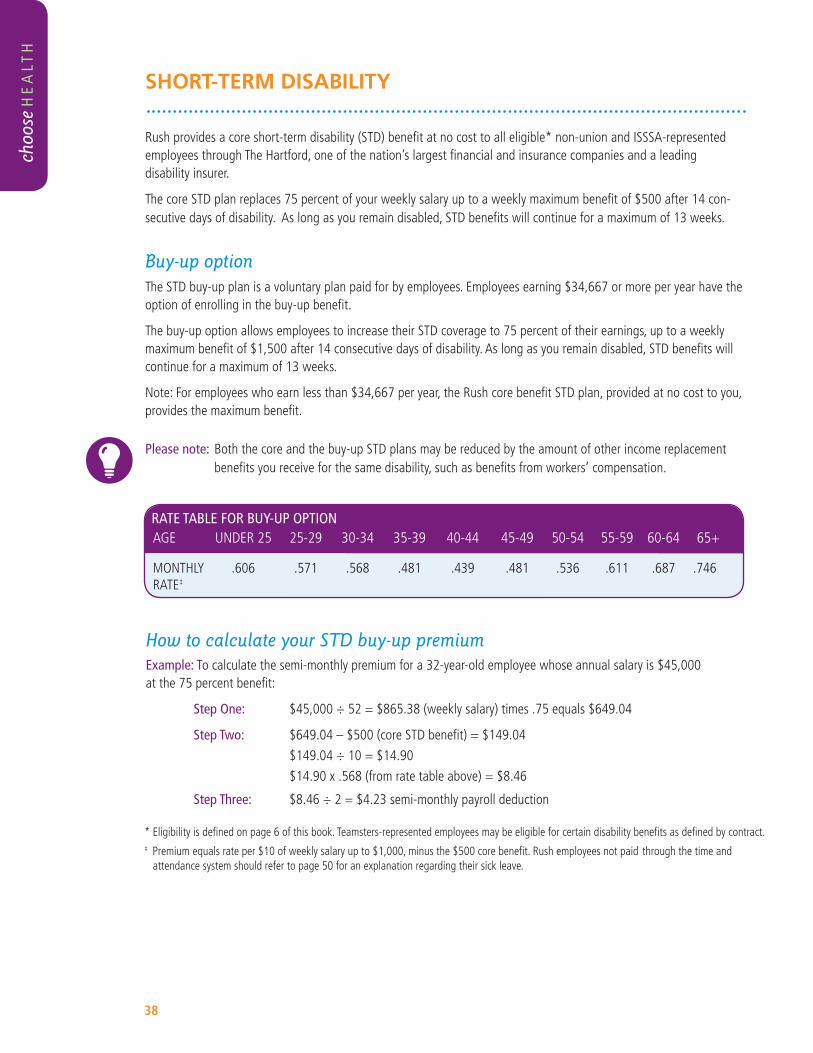

SHORT-TERM DISABILITY. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38 Buy-up option . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

Rate table for buy-up option . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38 How to calculate your STD premium . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

Pre-existing condition limitation for disability (applies to STD and LTD core plans and both buy-up plans) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39

Definition of disability . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39 Eliminationperiod . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39 Taxability. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39 Additional information. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39

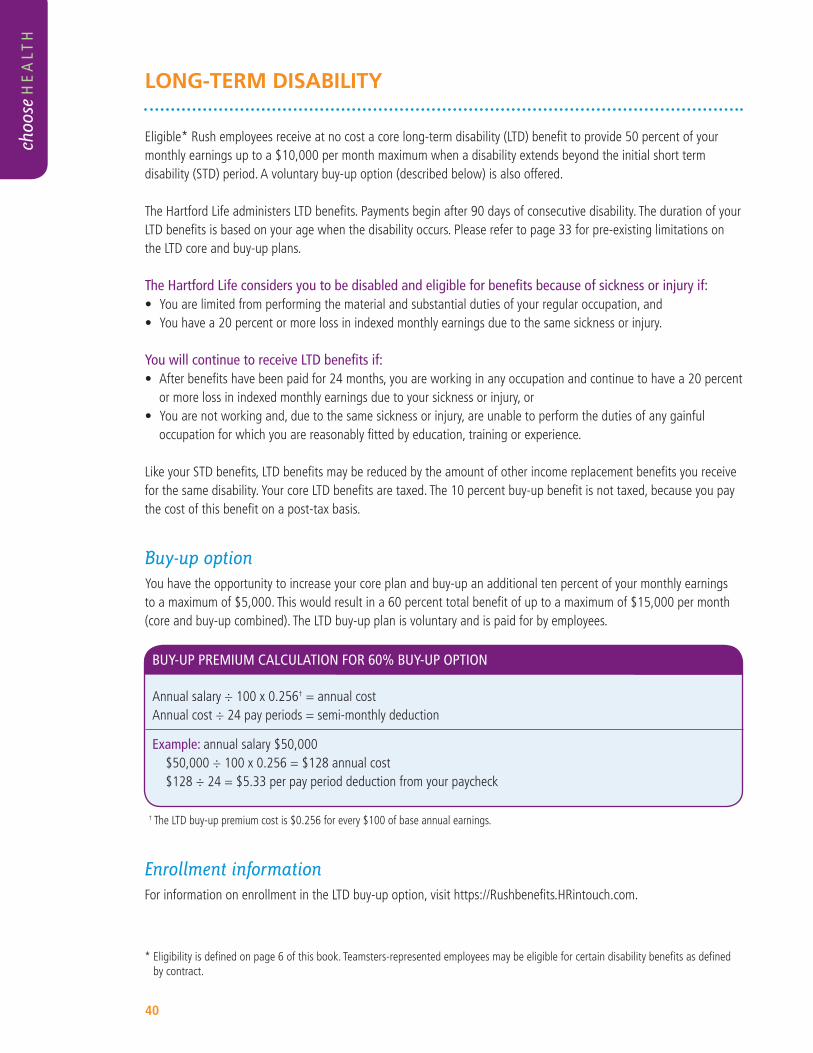

LONG-TERM DISABILITY. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40 Buy-up option. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40 Buy-up premium calculation. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40 Enrollmentinformation. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40

RETIREMENT BENEFITS. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41 The 403(b) Retirement Savings Plan. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41 Whoiseligibletoparticipate. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41 Vestinginthe403(b)RetirementSavingsPlan . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41 Compensation on which contributions are based . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41 Investments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42

choo

se H

EA

LTH

deve

lop

CA

RE

ER

grow

WE

ALT

Hba

lanc

e L

IFE

Important:This guide contains only a brief overview of the medical and other benefit options available to you. For more information about any Rush benefit plan, please refer to the applicable summary plan description. Although every effort has been made to ensure that the information in this guide is accurate, if there is any conflict between this guide and the terms of a benefit plan as described in the summary plan descrip-tion, the latter must control. Summary plan descriptions are available in human resources and online at https://Rushbenefits.HRintouch.com.

5

Investment funds. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42 Employeecontributions. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42

Contribution limits. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42 Criteria for financial hardship. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43 Whenpaymentsbegin. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43

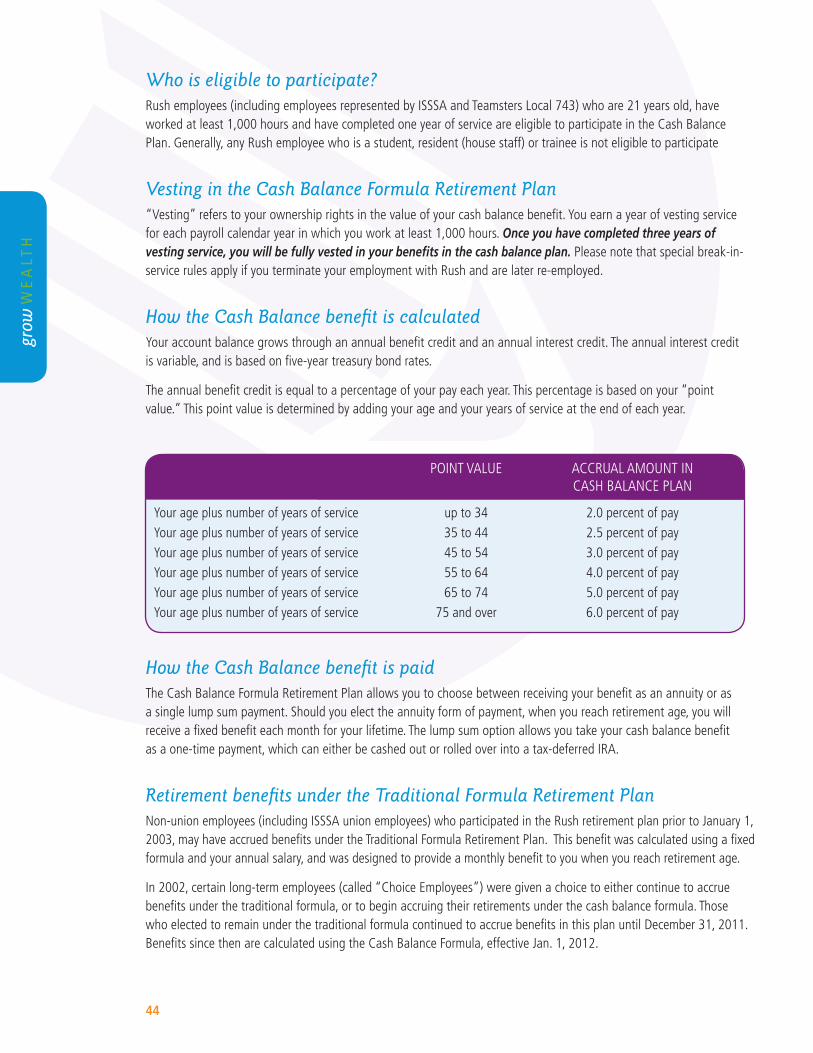

Additional provisions in the 403(b) Retirement Savings Plan . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43 The Cash Balance Formula Retirement Plan. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43 Whoiseligibletoparticipate. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44

VestingintheCashBalanceFormulaRetirementPlan . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44 How the Cash Balance benefit is calculated . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44 How the Cash Balance benefit is paid. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44 Retirement benefits under the Traditional Formula Retirement Plan . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44 Commencing payment of your retirement benefits. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45 The Pension Plan (Teamsters-represented employees only). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45 Whoiseligibletoparticipate. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45 VestinginthePensionPlan. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45 How the Pension benefit is paid. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46

For additional information and assistance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46 EMPLOYEE EDUCATION THROUGH LEAP. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47PAID TIME OFF (PTO). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48

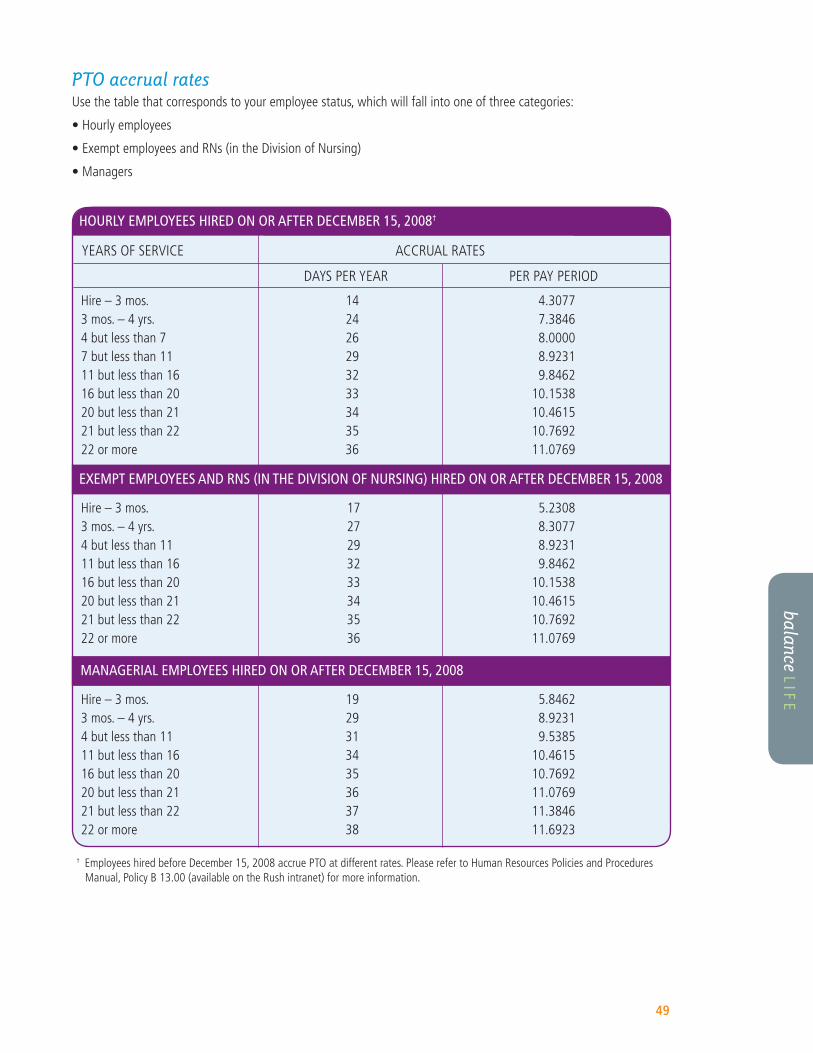

How PTO accrual is calculated . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48 PTO accrual rates. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49 PTO maximum accrual banks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 50

Checking your PTO balance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 50 Recognized holidays . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 50

PTO exceptions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 50

EMPLOYEE ASSISTANCE PROGRAM (EAP). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51 Work-liferesourceandreferralprogram . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51

OtherEAPservices . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51

ADDITIONAL SERVICES AVAILABLE THROUGH RUSH. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52 PerkSpot . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52

On-site child care (LADS) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52

GLOSSARY OF TERMS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 53

NEED MORE INFORMATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 55

choose HE

ALT

Hdevelop C

AR

EE

Rgrow

WE

ALT

Hbalance L

IFE

6

GENERAL INFORMATION ON RUSH BENEFITS

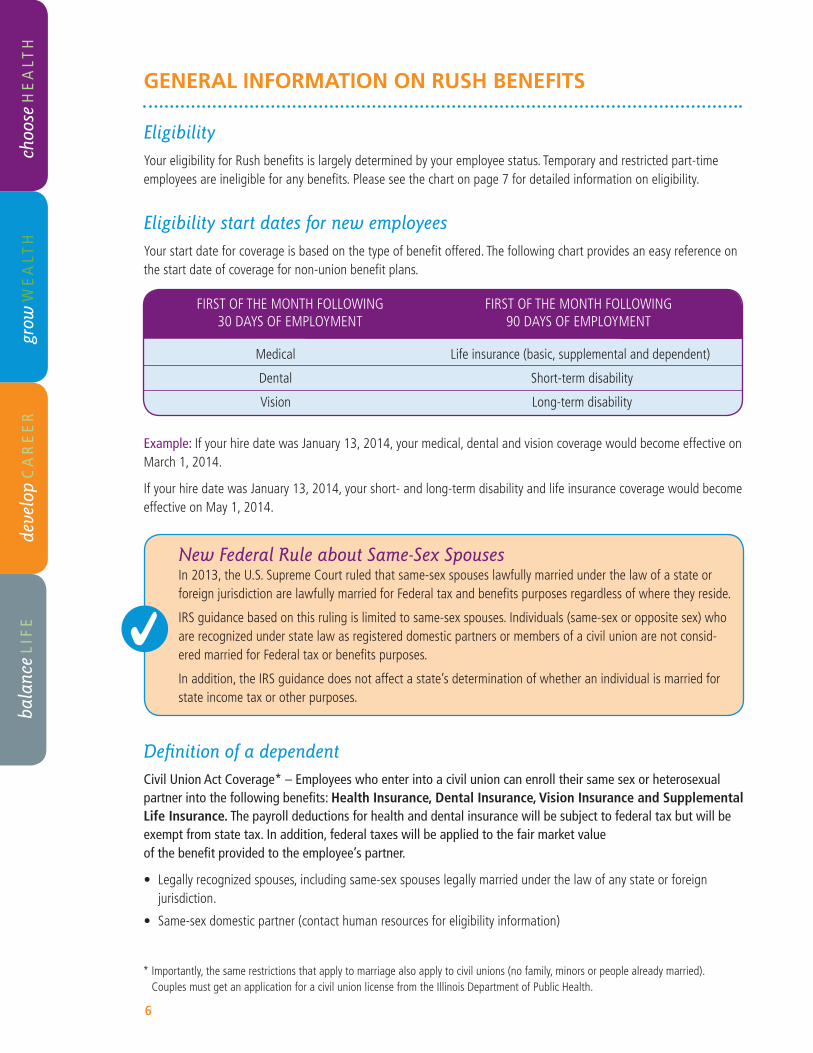

Eligibility Your eligibility for Rush benefits is largely determined by your employee status. Temporary and restricted part-time employees are ineligible for any benefits. Please see the chart on page 7 for detailed information on eligibility.

Eligibility start dates for new employeesYour start date for coverage is based on the type of benefit offered. The following chart provides an easy reference on the start date of coverage for non-union benefit plans.

Definition of a dependentCivil Union Act Coverage* – Employees who enter into a civil union can enroll their same sex or heterosexual partner into the following benefits: Health Insurance, Dental Insurance, Vision Insurance and Supplemental Life Insurance. The payroll deductions for health and dental insurance will be subject to federal tax but will be exempt from state tax. In addition, federal taxes will be applied to the fair market value of the benefit provided to the employee’s partner.

• Legallyrecognizedspouses,includingsame-sexspouseslegallymarriedunderthelawofanystateorforeign jurisdiction.

•Same-sexdomesticpartner(contacthumanresourcesforeligibilityinformation)

Example: If your hire date was January 13, 2014, your medical, dental and vision coverage would become effective on March 1, 2014.

If your hire date was January 13, 2014, your short- and long-term disability and life insurance coverage would become effective on May 1, 2014.

FIRSTOFTHEMONTHFOLLOWING30DAYSOFEMPLOYMENT

FIRSTOFTHEMONTHFOLLOWING90DAYSOFEMPLOYMENT

Life insurance (basic, supplemental and dependent)

Short-term disability

Long-term disability

Medical

Dental

Vision

choo

se H

EA

LTH

deve

lop

CA

RE

ER

grow

WE

ALT

Hba

lanc

e L

IFE

New Federal Rule about Same-Sex SpousesIn 2013, the U.S. Supreme Court ruled that same-sex spouses lawfully married under the law of a state or foreign jurisdiction are lawfully married for Federal tax and benefits purposes regardless of where they reside.

IRS guidance based on this ruling is limited to same-sex spouses. Individuals (same-sex or opposite sex) who are recognized under state law as registered domestic partners or members of a civil union are not consid-ered married for Federal tax or benefits purposes.

In addition, the IRS guidance does not affect a state’s determination of whether an individual is married for state income tax or other purposes.

* Importantly, the same restrictions that apply to marriage also apply to civil unions (no family, minors or people already married). Couples must get an application for a civil union license from the Illinois Department of Public Health.

7

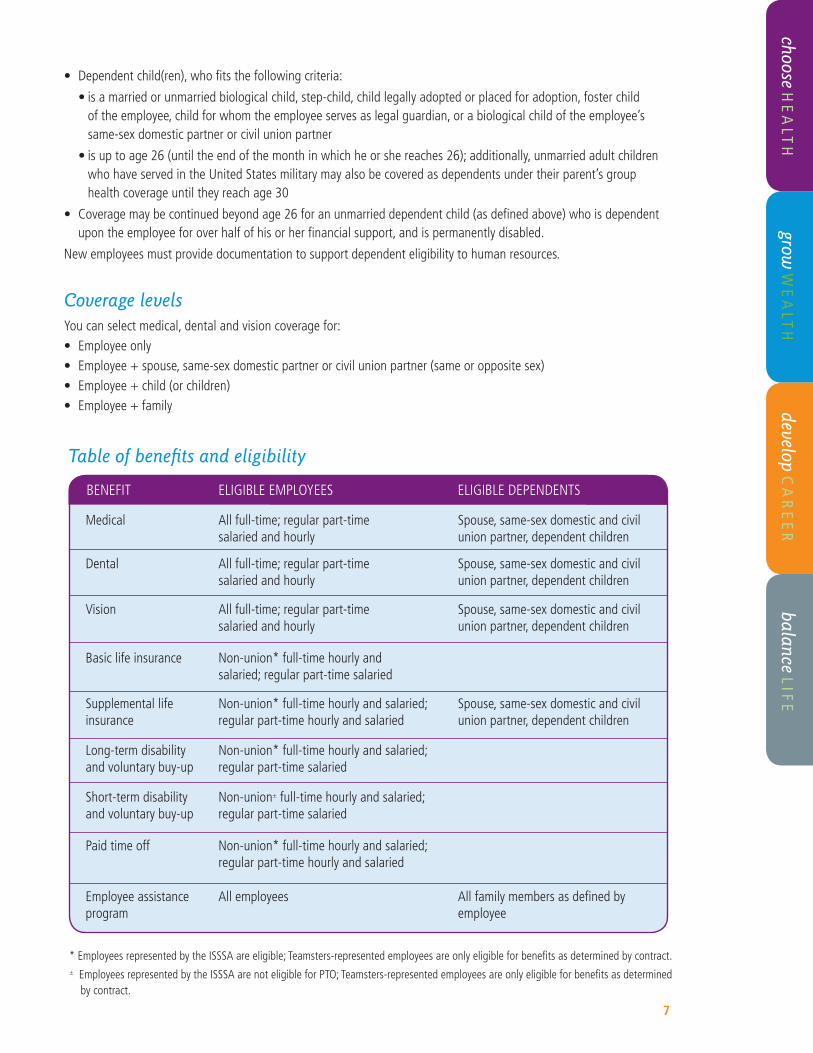

• Dependentchild(ren),whofitsthefollowingcriteria:

•isamarriedorunmarriedbiologicalchild,step-child,childlegallyadoptedorplacedforadoption,fosterchild of the employee, child for whom the employee serves as legal guardian, or a biological child of the employee’s same-sex domestic partner or civil union partner

•isuptoage26(untiltheendofthemonthinwhichheorshereaches26);additionally,unmarriedadultchildren who have served in the United States military may also be covered as dependents under their parent’s group health coverage until they reach age 30

• Coveragemaybecontinuedbeyondage26foranunmarrieddependentchild(asdefinedabove)whoisdependent upon the employee for over half of his or her financial support, and is permanently disabled.

New employees must provide documentation to support dependent eligibility to human resources.

Coverage levelsYou can select medical, dental and vision coverage for:• Employeeonly• Employee+spouse,same-sexdomesticpartnerorcivilunionpartner(sameoroppositesex)• Employee+child(orchildren)• Employee+family

Table of benefits and eligibility

BENEFIT ELIGIBLEEMPLOYEES ELIGIBLEDEPENDENTS

Medical

Dental

Vision

Supplemental life insurance

Long-term disability and voluntary buy-up

Short-term disability and voluntary buy-up

Paid time off

Employeeassistanceprogram

Basic life insurance

Allfull-time;regularpart-time salaried and hourly

Allfull-time;regularpart-time salaried and hourly

Allfull-time;regularpart-time salaried and hourly

Non-union*full-timehourlyandsalaried;regular part-time hourly and salaried

Non-union*full-timehourlyandsalaried;regular part-time salaried

Non-union±full-timehourlyandsalaried;regular part-time salaried

Non-union*full-timehourlyandsalaried;regular part-time hourly and salaried

All employees

Non-union* full-time hourly andsalaried;regularpart-timesalaried

Spouse, same-sex domestic and civil union partner, dependent children

Spouse, same-sex domestic and civil union partner, dependent children

Spouse, same-sex domestic and civil union partner, dependent children

Spouse, same-sex domestic and civil union partner, dependent children

All family members as defined by employee

*EmployeesrepresentedbytheISSSAareeligible;Teamsters-representedemployeesareonlyeligibleforbenefitsasdeterminedbycontract.±EmployeesrepresentedbytheISSSAarenoteligibleforPTO;Teamsters-representedemployeesareonlyeligibleforbenefitsasdetermined by contract.

choose HE

ALT

Hdevelop C

AR

EE

Rgrow

WE

ALT

Hbalance L

IFE

8

Information on when you can make benefit changesGenerallyspeaking,youmaymakechangestoyourbenefitsonlyduringtheannualopenenrollmentperiod.*

After open enrollment, you can only change your benefits coverage from January 1 through December 31, if youhaveaqualifiedlifeeventorachangeinstatus.

Qualified life events and changes in status that permit coverage changes include:

•Employeemovesfrompart-timetofull-timeemploymentorviceversa

•Employeegainsaneligibledependent,e.g.,throughbirth,legaladoptionorlegalguardianship

•Marriage,same-sexdomesticpartnerorcivilunionpartner(sameoroppositesex)

•Divorce,annulmentorlegalseparation

•Dissolutionofasame-sexdomesticpartnerorcivilunionpartner(sameoroppositesex)relationship

•Spouse,same-sexdomesticpartner,civilunionpartner(sameoroppositesex)ordependentgainsorlosescoveragedue to gaining or losing employment/eligibility with his/her current employer

•Deathofaspouseorsame-sexdomesticpartnerorcivilunionpartner(sameoroppositesex)

•Deathofadependentchild

•Spouse/same-sexdomesticpartner/civilunionpartner(sameoroppositesex)/dependentbecomesMedicare/Medicaid eligible or ineligible

Any changes you make for yourself and your dependents must be consistent with, and on account of, your change in status. For example, you can enroll your newborn in medical coverage, but you cannot drop coverage for your spouse, same-sex domestic partner or civil union partner (same or opposite sex) or change medical options because of the birth of your child.

Keeping your information currentIfyouhaveaqualifiedlifeeventorachangeinstatus,youmustmakeyourbenefitchangeswithin31days of the actual event by logging onto https://Rushbenefits.HRintouch.com. Otherwise you cannot make changes until the next open enrollment period.

Please note: You must log onto https://Rushbenefits.HRintouch.com to add your newborn within 31 days of birth. Failure to do so may result in unpaid claims.

Mostcoveragechangesduetoaqualifiedlifeeventorchangeinstatusareeffectiveontheeventdate.

If you move or change your primary contact number, you must notify your manager as soon as this change takes place. This is especially important for keeping you up-to-date on any important changes within the Rush benefits program and for income tax purposes.

*ChangesinqualifiedTMAparkingandmasstransitexpensereimbursementchoicesmaybemadeatanytime.

choo

se H

EA

LTH

deve

lop

CA

RE

ER

grow

WE

ALT

Hba

lanc

e L

IFE

9

Choose HealthChoose Health is a comprehensive, voluntary wellness program for all employees participating in Rush medical plans. Participating in the Choose Health wellness program can help employees understand their health risks and take actions to make the most of life. Choose Health focuses on prevention and management of chronic disease.

To get started in Choose Health, employees take part in a free health screening that is held at Rush each year. The program then provides events and classes to help employees reduce their health risks and achieve their wellness goals. Choose Health also offers the OnTrack health condition management and health coaching program to help employees manage chronic medical conditions such as diabetes, asthma and high blood pressure and to provide special assistance for pregnant women. Additionally, Choose Health partners with the Rush employee medical plan to provide coverage for preventive screenings and treatment of illness and injury.

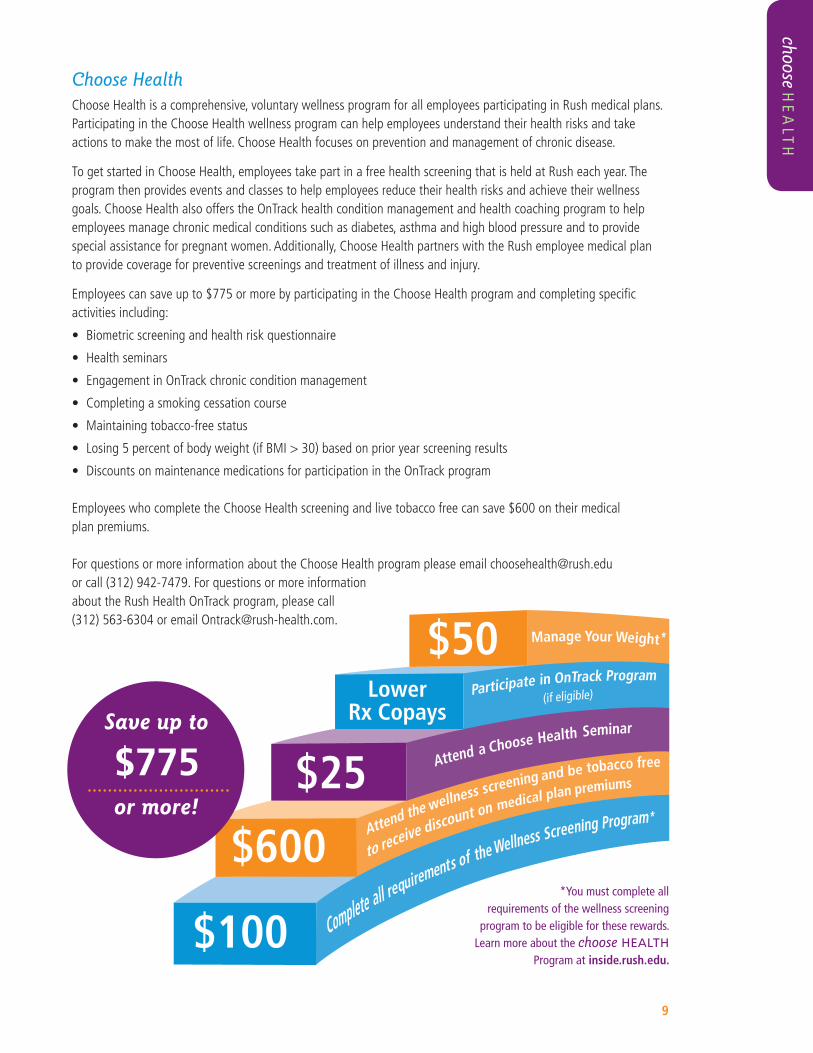

Employeescansaveupto$775ormorebyparticipatingintheChooseHealthprogramandcompletingspecific activities including:

•Biometricscreeningandhealthriskquestionnaire

• Healthseminars

• EngagementinOnTrackchronicconditionmanagement

• Completingasmokingcessationcourse

• Maintainingtobacco-freestatus

• Losing5percentofbodyweight(ifBMI>30)basedonprioryearscreeningresults

• DiscountsonmaintenancemedicationsforparticipationintheOnTrackprogram

EmployeeswhocompletetheChooseHealthscreeningandlivetobaccofreecansave$600ontheirmedical plan premiums.

ForquestionsormoreinformationabouttheChooseHealthprogrampleaseemailchoosehealth@rush.edu orcall(312)942-7479.Forquestionsormoreinformation about the Rush Health OnTrack program, please call (312)[email protected].

choose HE

ALT

H

*You must complete all requirements of the wellness screening

program to be eligible for these rewards. Learn more about the choose HEALTH

Program at inside.rush.edu.

Save up to

$775or more!

10

Coverage differences between the health plans

choo

se H

EA

LTH

RUSH MEDICAL PLANS

Rush medical plans are administered by Cigna. Cigna offers many services and online support through its website for Rushemployeesatwww.askallegiance.com/rush.Employeescanreceiveconfidentialandpersonalizedinformationon:•Coverageandbenefitsdetails•Providerresources,includinglocatingaRushorin-networkphysiciantomeetyourneeds•Claimpaymentinformationand details

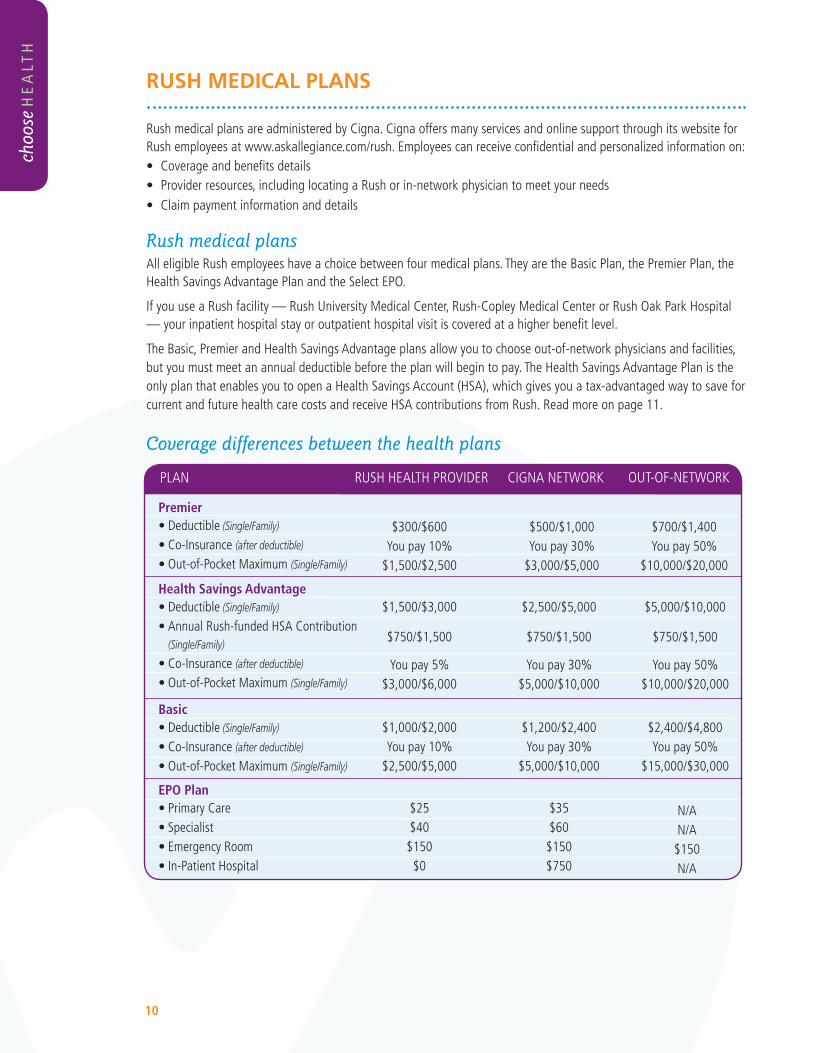

Rush medical plansAll eligible Rush employees have a choice between four medical plans. They are the Basic Plan, the Premier Plan, the HealthSavingsAdvantagePlanandtheSelectEPO.

If you use a Rush facility — Rush University Medical Center, Rush-Copley Medical Center or Rush Oak Park Hospital — your inpatient hospital stay or outpatient hospital visit is covered at a higher benefit level.

The Basic, Premier and Health Savings Advantage plans allow you to choose out-of-network physicians and facilities, but you must meet an annual deductible before the plan will begin to pay. The Health Savings Advantage Plan is the only plan that enables you to open a Health Savings Account (HSA), which gives you a tax-advantaged way to save for current and future health care costs and receive HSA contributions from Rush. Read more on page 11.

Premier•Deductible (Single/Family)

•Co-Insurance(after deductible)

•Out-of-PocketMaximum(Single/Family)

Basic•Deductible (Single/Family)

•Co-Insurance(after deductible)

•Out-of-PocketMaximum(Single/Family)

Health Savings Advantage •Deductible (Single/Family)

•AnnualRush-fundedHSAContribution(Single/Family)

•Co-Insurance(after deductible)

•Out-of-PocketMaximum(Single/Family)

EPO Plan•PrimaryCare•Specialist•EmergencyRoom•In-PatientHospital

$300/$600You pay 10%

$1,500/$2,500

$1,000/$2,000You pay 10%

$2,500/$5,000

$1,500/$3,000

$750/$1,500

You pay 5%$3,000/$6,000

$25$40$150$0

$500/$1,000You pay 30%

$3,000/$5,000

$1,200/$2,400You pay 30%

$5,000/$10,000

$2,500/$5,000

$750/$1,500

You pay 30%$5,000/$10,000

$35$60$150$750

$700/$1,400You pay 50%

$10,000/$20,000

$2,400/$4,800You pay 50%

$15,000/$30,000

$5,000/$10,000

$750/$1,500

You pay 50%$10,000/$20,000

N/AN/A

$150N/A

PLAN RUSHHEALTHPROVIDER CIGNANETWORK OUT-OF-NETWORK

11

choose HE

ALT

H

1 A “true emergency” is defined by “the prudent layperson standard,” meaning the situation or illness would be considered to be an emergency by a prudent (cautious and sensible) non-medically trained person.

Benefits provided by the health plansAll four plans provide many of the same benefits, such as the opportunity to see a specialist without a referral from your primary care physician. In addition, the plans provide an out-of-pocket maximum to protect you from financial hardship resulting from health care costs. All plans provide varying levels of prescription drug coverage and all plans include an infertility drug and medical treatment benefit, as well as smoking cessation prescription coverage.

Themaindifferencebetweentheplans(Basic,PremierandHealthSavingsAdvantage)andtheSelectEPOisthatundertheSelectEPOtherewillbenomedicalbenefitspaidifyouchoosetogotoanout-of-networkphysicianorfacility(exceptin the case of a true emergency).1 The other big difference between the plans is only the Health Savings Advantage Plan enables participants to open a Health Savings Account (HSA).

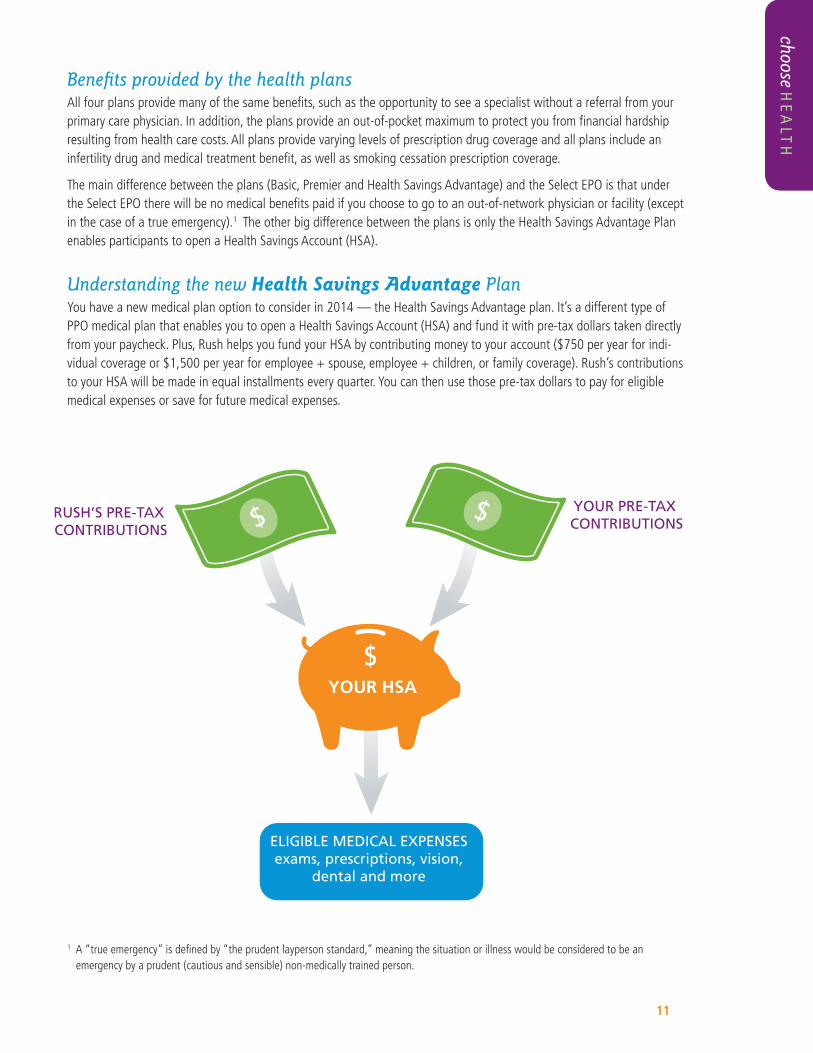

Understanding the new Health Savings Advantage PlanYou have a new medical plan option to consider in 2014 — the Health Savings Advantage plan. It’s a different type of PPO medical plan that enables you to open a Health Savings Account (HSA) and fund it with pre-tax dollars taken directly from your paycheck. Plus, Rush helps you fund your HSA by contributing money to your account ($750 per year for indi-vidual coverage or $1,500 per year for employee + spouse, employee + children, or family coverage). Rush’s contributions toyourHSAwillbemadeinequalinstallmentseveryquarter.Youcanthenusethosepre-taxdollarstopayforeligiblemedical expenses or save for future medical expenses.

$

$ $

The Triple Tax AdvantageThe HSA works to pay for your health care in the same way a 401(k) or 403(b) savings plan works to pay for your retirement. But unlike a 401(k) or 403(b), your HSA contributions provide three tax advantages.

1. Your contributions are deposited tax-free (from federal taxes),

2. They earn interest tax-free, and

3. They can be withdrawn to pay for eligible health care expenses tax-free.

That’s a triple tax benefit!

Investment OptionsOnce you have $2,000 in your HSA, you can choose to allocate some of your funds to various investment options that may help you grow your account and save for eligible medical expenses in retirement.

How the Medical Plan and HSA Work TogetherThe Health Savings Advantage plan consists of two parts: the PPO medical plan and the HSA.

12

choo

se H

EA

LTH

The PPO Medical Plan

The Health Savings Account (HSA)

The Health Savings Advantage plan is a PPO medical plan that enables you to open a HSA. Like other PPO options, the medical plan gives you access to a wide range of physicians and providers.

The plan provides you with 100 percent coverage for preventive and wellness care as well as financial protection against significant medical expenses. You’ll have a deductible to meet before the medical plan begins sharing the cost of medical care or prescription drugs through coinsurance or copayments. For drugs classified as preventive, you won’t have to meet the deductible before you start sharing the cost through copayments.

The medical plan is considered a “high deductible health plan” by the federal government, which is what enables you to open a HSA with it. But Rush helps to offset the higher deductibles by making tax-free contributions to your HSA. You can use these contributions from Rush to help cover eligible medical expenses and meet your deductible.

A Health Savings Account (HSA) is a special type of savings account that can be used to pay for eligible health care expenses with pre-tax dollars. Your HSA contributions are deposited tax-free (from federal taxes), earn interest tax-free, and are withdrawn to pay for eligible health care expenses tax-free.

Plus,RushhelpsyoufundyourHSAbycontributingmoneytoyouraccountonaquarterlybasis ($750 per year for individual coverage or $1,500 per year for employee + spouse, employee + children, or family coverage).

You own your HSA and the money in it. It is yours to keep, even if you choose to leave Rush. You decide whether to use your HSA funds to help pay for your deductible and cur-rent eligible health care expenses or let the funds grow tax-free year after year to pay for future eligible medical expenses — even expenses you might incur in retirement.

Unlike a Flexible Spending Account (FSA), the money in your HSA rolls over from year to year. There’s no need to worry about losing money if you don’t use it by the end of the year.

Using Your HSAYourHSAwillbeadministeredbyHealthEquity.HealthEquityprovidesyouwith powerful tools you can use to access and manage your account, including:

• Adebitcard

• Onlinetools

• Afreemobileapp

• Telephoneaccess

YoucanuseyourHealthEquityaccesstoolsto:

• Checkyouraccountbalance

• Reviewyourtransactions

• Reviewclaims

• Submitnewclaimsordocuments

• Sendpaymentsandreimbursements

• Accesstaxdocuments

If you select the Health Savings Advantage plan, Health Equity will send you additional information about using your HSA in December 2013.

13

choose HE

ALT

H

Who is Eligible?To establish a Health Saving Account, you:• MustbecoveredONLYbyanHSA-qualifiedhealthplan

– Having other health coverage (including Medicare, a traditional health plan, or even a general purposeHealthCareFlexibleSpendingAccount)maydisqualifyyou

• Cannotbeclaimedasadependentonsomeoneelse’staxreturn

If you enroll in a HSA, you won’t be able to have a traditional Health Care FSA, but you can open a Limited-Purpose Health Care FSA. A Limited-Purpose FSA is much like a typical, general-purpose Health CareFSA,buteligibleexpensesarelimitedtoqualifyingdental and vision expenses.

Maximum Contributions to Your HSA for 2014The IRS limits the amount of money you and your employer can contribute to your HSA. The maximum HSA contributions for 2014 are:• $3,300forsinglecoverage

• $6,550forfamilycoverage

If you are age 55 or older, you can contribute an additional $1,000 to your HSA annually.

14

choo

se H

EA

LTH

Basic, Premier, Health Savings Advantage or Select EPO: Which plan is right for you?Indeterminingwhetheroneoftheplans(Basic,PremierorHealthSavingsAdvantage)ortheSelectEPOplanisarightchoiceforyouandyourfamily,therearemanyfactorsyouwillwanttoconsider.Everyone’smedicalsituationisdiffer-ent and we urge you to investigate your options thoroughly before making your decision on what medical coverage to go with for 2014.

Whilewerealizethattheunexpectedcanhappenatanytime,thequestionsbelowareexamplesofitemsthatshould be taken into consideration when choosing your plan:

•DoyouutilizeRushfacilities?

•Howoftendoyouseeyourphysicianduringtheyear?Isitmainlyforwellnessexams?

•Areyoucurrentlybeingtreatedforachronicillness?

•Areyouplanninganyupcomingsurgeries,orareyouhavingababyin2014?

•Doyouoryourfamilymembersrequiremultipleorcostlyprescriptiondrugs?

•Whatareyourannualpaycheckcontributionscomparedtoyourout-of-pocketexpensesthroughouttheyear (e.g.,deductibles,copayments,andcoinsurance)?

With the Basic, Premier and Health Savings Advantage Plans: •YourpaycheckdeductionislowerthantheEPObutyouwillbesubjecttoadeductibleandcoinsurancefor

non-preventive care services such as diagnostic procedures (e.g., labs, X-rays, MRI and CT scans), inpatient hospital stays and specialty services. (Preventive services are covered at 100 percent.)

•Youhaveanout-of-networkbenefitthatcoversyouifyouseekservicesoutsidetheCignanetwork.

•Youhavecomprehensiveprescriptioncoverageoptionswithamaximumout-of-pocketexpenselimit.Thiswill be helpful if you or a family member take an extensive amount of prescription medication.

With the Select EPO plan:•Youwillhavethehighestpaycheckdeduction,butyouwillnothaveadeductibletosatisfyanditpays100percent

after applicable copayments are made. You may find this option preferable if you or a family member have a chronic medical condition or you know of an upcoming surgery or hospital stay in 2014.

•Youarenotrequiredtochooseaprimarycareprovider.However,youmustuseaproviderwithintheSelect EPOnetwork.

•Youdonothaveanyout-of-networkbenefits,onlyin-networkprovidersarecovered.Inaddition,noreferralis neededforspecialistcarewithintheSelectEPOnetwork.

•Yourprescriptioncoveragedoesnothaveanout-of-pocketmaximum,meaningprescriptioncostsmaybe more expensive.

DetailsabouttheplansandSelectEPOarelistedinthissectionandweencourageyoutoreviewtheminmoredetail asyoumakeyourdecision.Ifyouhaveanyquestions,logontohttps://Rushbenefits.HRintouch.com.

Did you know that even if your primary care physician is not a Rush physician, you can still utilize the services of onsite physicians, facilities, laboratory services and specialty care. Accessing these onsite services will help you save time and money!

To find a Rush physician, please visit the Rush Health Internet site, http://doctors.rush.edu/. If you are unsure whether or not your current physician is in-network or out-of-network, please visit the Cigna website at www.askallegiance.com/rush.

15

choose HE

ALT

H

What the Basic, Premier and Health Savings Advantage Plans have in common 1. Choosing a doctor•Youmaychoosetoseeanyprovider

•Youarenotrequiredtochooseaprimarycareprovider

•Youdon’tneedtoobtainreferralsforcare

•Youreceivein-networkandout-of-networkbenefits,whichmeans:

•Yourout-of-pocketcostsarelowerifyouchooseRushandin-networkproviders.WhenyouuseaRushor in-network provider, you do not have to file a claim — your provider will file a claim directly with Cigna. Depending on the type of service you receive, you pay a copayment (to a Rush or in-network physician for an office visit) or coinsurance, and the plan pays the remaining covered amount.

•Youcanreceivecarefromprovidersoutsideofthenetwork,butyourshareofthecostishigherandyouare responsibleforpayinganyexpensesthatexceedtheusual,customaryandreasonable(UCR)limits.Whenyou use an out-of-network provider, you pay the full cost to the provider and file a claim to be reimbursed a percentage of the covered expenses for medically necessary services, after you meet your annual deductible.

2. Meeting the deductibleOnce you meet your annual deductible, the Basic, Premier and Health Savings Advantage Plans pay a percentage of covered medical expenses. This percentage is the coinsurance. These amounts that you pay are called out-of-pocket expenses. Only the Health Savings Advantage enables you to have a Health Savings Account to help cover the cost of your deductible.

3. Out-of-pocket maximumsThe out-of-pocket maximum is your financial responsibility in any calendar year for coinsurance and deductible expenses. Your copayments do not count toward your out-of-pocket maximum for any year. Once you reach the annual out-of-pocket maximum, the Basic, Premier and Health Savings Advantage Plans pay most expenses at 100 percent. The limitations are dependent on which plan you choose, and how much coverage you need.

If you use a Rush Health doctor or Rush network facility, you pay a lower deductible and coinsurance.

How the Basic, Premier and Health Savings Advantage Plans differ from one another Basic Plan: •YourdeductibleamountishigherthanthePremierPlan.

• You pay lower payroll contributions in this plan than the Premier Plan.

•Thisplanmayworkbestforyouifyouandyourfamilyarenotfrequenthealthcareusers.

Health Savings Advantage Plan:• YourdeductibleamountishigherthanthePremierorBasicPlans,butyouwillhaveaHealthSavingsAccount

funded by tax-free contributions from Rush to help cover the deductible.

• You pay lower payroll contributions in this plan than the Premier Plan. Your payroll contributions will be slightly higher than the Basic Plan.

• ThisplanmayworkbestifyouandyourfamilywanttoenjoythetaxadvantagesofaHealthSavingsAccounttohelp pay your deductible and current eligible health care expenses or let the funds grow tax-free year after year to pay for future eligible medical expenses — even expenses you might incur in retirement.

16

* Charges for additional services that are performed during an office visit may be subject to your plan deductible and coinsurance.

choo

se H

EA

LTH

Premier Plan: • YourdeductibleamountislowerthantheBasicPlan.

•You pay higher payroll contributions in this plan than the Basic Plan.• Ifyouandyourfamilyarefrequenthealthcareusers,thisplanmaybebestforyou.

Example: A visit to the doctorThe amount you pay when you visit the doctor depends on the plan you participate in and the type of provider you choose.

If you choose a Rush or Cigna doctor — whether you choose the Basic or Premier Plan — you pay a $20 copayment for an office visit with a primary care doctor (or a $40 copayment for an office visit with a specialist), then the plan pays 100 percent.* Your office visit copayment does not apply toward your deductible.

If you choose an out-of-network provider, your out-of-network annual deductible applies. This means if you haven’t met your out-of-network annual deductible, you pay the full cost of your office visit. Once you meet the out-of-net-work deductible, the plan will share your expenses. Specifically, when you visit the doctor, you will pay 50 percent of the cost and the plan will pay 50 percent.

WiththeHealthSavingsAdvantagePlan,ifyouchooseaRushorCignadoctor,youwillpaythetotalcostofyourcareuntil you meet the annual deductible. Then you will pay coinsurance (5% for an office visit with a Rush doctor or 30% for an office visit with a Cigna doctor.) Once you meet your annual out-of-pocket maximum, the plan will pay 100% of the cost.

Please note:Whenyouuseanout-of-networkprovider,youmayberesponsibleforadditionalchargesbeyond usual, customary and reasonable (UCR).

17

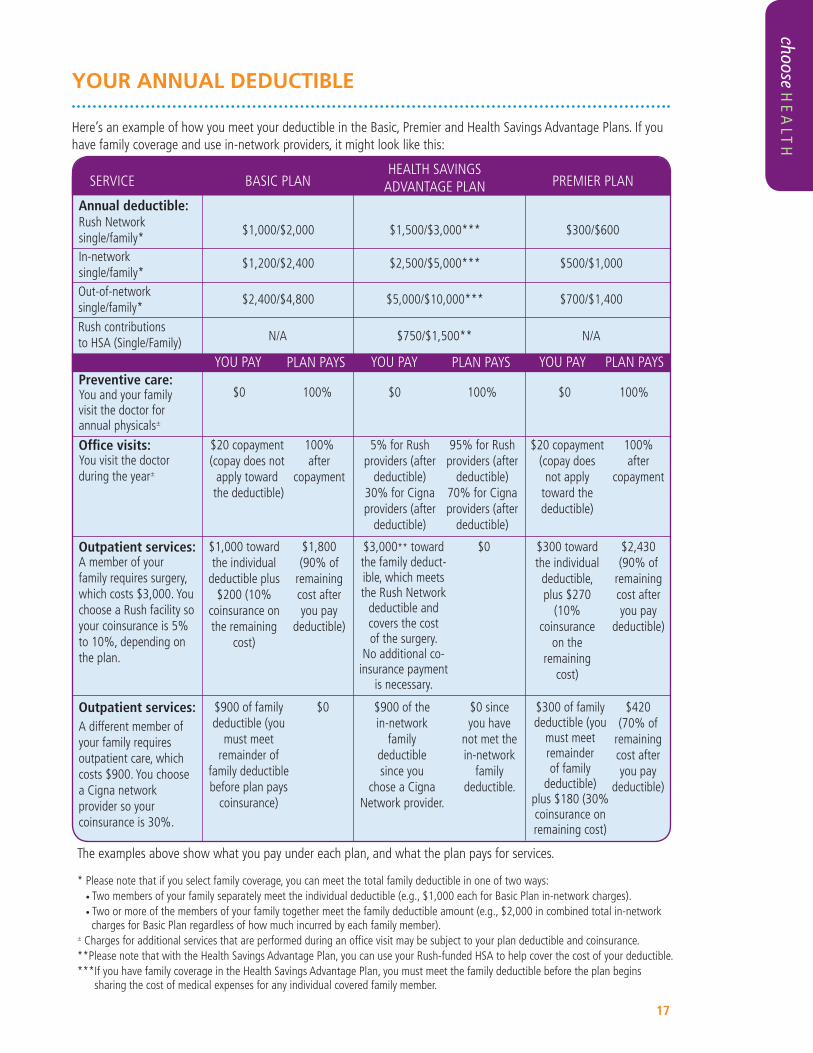

YOUR ANNUAL DEDUCTIBLE

Here’s an example of how you meet your deductible in the Basic, Premier and Health Savings Advantage Plans. If you have family coverage and use in-network providers, it might look like this:

SERVICE BASIC PLANHEALTHSAVINGS ADVANTAGEPLAN PREMIERPLAN

Annual deductible:

Preventive care:

Office visits:

Outpatient services:

Outpatient services:

In-network single/family*

Rush Network single/family*

You and your family visit the doctor for annual physicals±

You visit the doctor during the year±

A member of your familyrequiressurgery,which costs $3,000. You choose a Rush facility so your coinsurance is 5% to 10%, depending on the plan.

A different member of yourfamilyrequires outpatient care, which costs $900. You choose a Cigna network provider so your coinsurance is 30%.

$1,200/$2,400 $2,500/$5,000***

$1,000/$2,000 $1,500/$3,000***

$0 $0

$20 copayment(copay does not

apply toward the deductible)

5% for Rush providers (after

deductible)30% for Cigna providers (after

deductible)

$1,000 toward the individual

deductible plus $200 (10%

coinsurance on the remaining

cost)

$3,000** toward the family deduct-ible, which meets the Rush Network

deductible and covers the cost of the surgery.

No additional co-insurance payment

is necessary.

$900 of familydeductible (you

must meet remainder of

family deductiblebefore plan pays

coinsurance)

$900 of the in-network

family deductible since you

chose a Cigna Network provider.

$20 copayment(copay does not apply

toward the deductible)

$300 toward the individual

deductible, plus $270

(10% coinsurance

on the remaining

cost)

$300 of family deductible (you

must meet remainder of family

deductible)plus $180 (30% coinsurance on remaining cost)

$0100% 100%

100% after

copayment

95% for Rush providers (after

deductible)70% for Cigna providers (after

deductible)

$1,800(90% of

remaining cost after you pay

deductible)

$0

$0 $0 since you have

not met the in-network

family deductible.

100% after

copayment

$2,430(90% of

remaining cost after you pay

deductible)

$420(70% of

remaining cost after you pay

deductible)

100%

$500/$1,000

$300/$600

Out-of-network single/family*

Rush contributions to HSA (Single/Family)

$2,400/$4,800

N/A

$5,000/$10,000***

$750/$1,500**

$700/$1,400

N/A

YOU PAY YOU PAY YOU PAYPLAN PAYS PLAN PAYS PLAN PAYS

The examples above show what you pay under each plan, and what the plan pays for services.

* Please note that if you select family coverage, you can meet the total family deductible in one of two ways: • Two members of your family separately meet the individual deductible (e.g., $1,000 each for Basic Plan in-network charges). • Two or more of the members of your family together meet the family deductible amount (e.g., $2,000 in combined total in-network charges for Basic Plan regardless of how much incurred by each family member).± Charges for additional services that are performed during an office visit may be subject to your plan deductible and coinsurance.**Please note that with the Health Savings Advantage Plan, you can use your Rush-funded HSA to help cover the cost of your deductible.***If you have family coverage in the Health Savings Advantage Plan, you must meet the family deductible before the plan begins sharing the cost of medical expenses for any individual covered family member.

choose HE

ALT

H

18

SERVICEDESCRIPTION

RUSHNETWORK

(INCLUDESRUSHPHYSICIANS)

NON-RUSHIN-NETWORK

FACILITY

OUT-OF-NETWORKFACILITY

IN-NETWORKPHYSICIAN

OUT-OF- NETWORK PHYSICIAN

BASIC PLAN

HEALTHSAVINGSADVANTAGEPLAN

BASIC PLAN

BASIC PLAN

BASIC PLAN

PREMIERPLAN

PREMIERPLAN

HEALTHSAVINGSADVANTAGEPLAN

PREMIERPLAN

HEALTHSAVINGSADVANTAGEPLAN

PREMIERPLAN

HEALTHSAVINGSADVANTAGEPLAN

SELECTEPO

SELECTEPO

SELECTEPO

SELECTEPO

Single: $2,500Family: $5,000

Single: $3,000Family: $6,000

$150 copay, plan pays 90% after deductible

Plan pays 90% after deductible‡

Single: $1,500Family: $2,500

Single: $6,350 Family: $12,700

$150 copay, plan pays 90% after deductible

Plan pays 95% after deductible

Plan pays 90% after deductible‡

Plan pay 95% after deductible

Copayment waived

Plan pays 100%

Single: $5,000 Family: $10,000

Single: $5,000 Family: $10,000

$300 copay, plan pays 70% after deductible

Plan pays 70% after deductible

Single: $3,000Family: $5,000

Single: $6,350 Family: $12,700

$300 copay, plan pays 70% after deductible

Plan pays 70% after deductible

Plan pays 70% after deductible

Plan pays 70% after deductible

$750 copay, plan then pays 100%

Plan pays 100%

Single: $15,000Family: $30,000

Single: $10,000Family: $20,000

$600 copay, plan pays 50% after deductible

N/A

N/A

N/A

Plan pays 50% after deductible

Single: $10,000Family: $20,000

N/A

$600 copay, plan pays 50% after deductible

Plan pays 50% after deductible

Single: $750 Family: $1,500

Plan pays 50% after deductible

Plan pays 50% after deductible

Not covered

Not covered

Single: $5,000Family: $10,000

Single: $5,000Family: $10,000

Plan pays 70% after deductible

Plan pays 70% after deductible

Single: $3,000Family: $5,000

Single: $6,350 Family: $12,700

Plan pays 70% after deductible

Plan pays 70% after deductible

Plan pays 70% after deductible

Plan pays 70% after deductible

Plan pays 100%

Plan pays 100%

Single: $15,000Family: $30,000

Single: $10,000Family: $20,000

Plan pays 50% after deductible

Plan pays 50% after deductible

Single: $10,000Family: $20,000

N/A

Plan pays 50% after deductible

Plan pays 50% after deductible

Plan pays 50% after deductible

Plan pays 50% after deductible

Not covered

Not covered

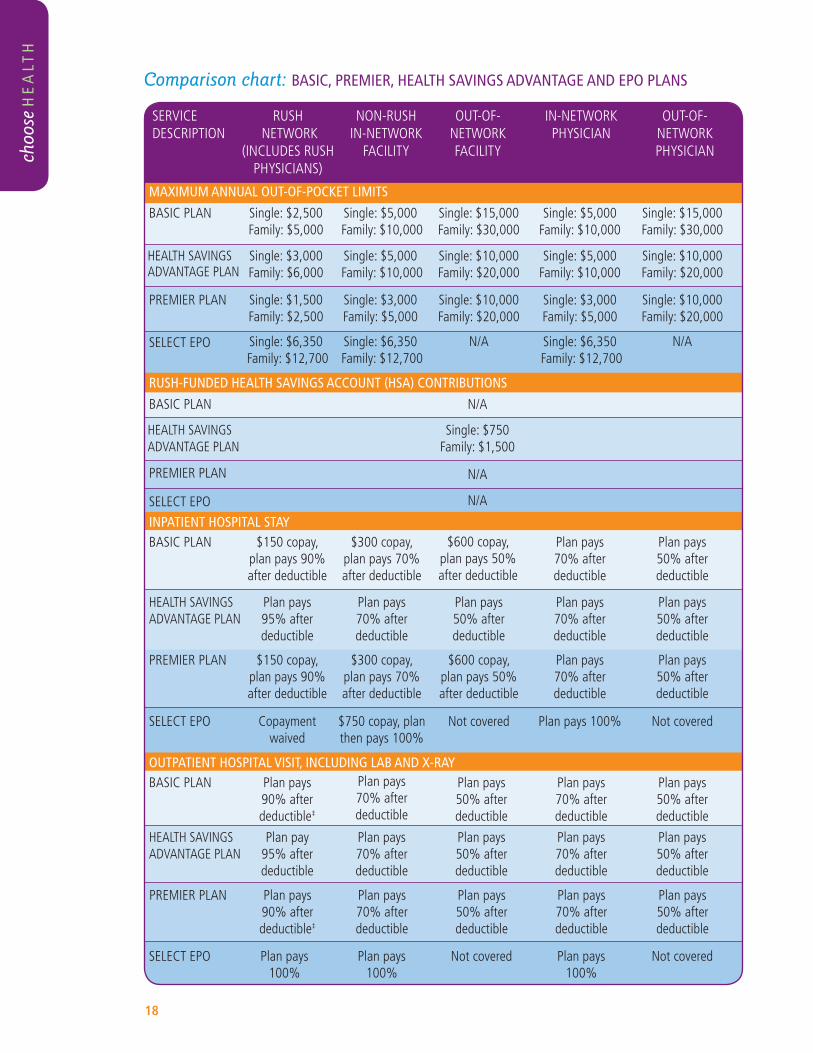

MAXIMUM ANNUAL OUT-OF-POCKET LIMITS

INPATIENT HOSPITAL STAY

RUSH-FUNDED HEALTH SAVINGS ACCOUNT (HSA) CONTRIBUTIONS

OUTPATIENT HOSPITAL VISIT, INCLUDING LAB AND X-RAY

Comparison chart: BASIC, PREMIER, HEALTH SAVINGS ADVANTAGE AND EPO PLANS

choo

se H

EA

LTH

19

Comparison chart: BASIC, PREMIER, HEALTH SAVINGS ADVANTAGE AND EPO PLANS (continued)

SERVICEDESCRIPTION

RUSH FACILITY

(INCLUDESRUSHPHYSICIANS)

NON-RUSHIN-NETWORK

FACILITY

OUT-OF-NETWORKFACILITY

IN-NETWORKPHYSICIAN

OUT-OF- NETWORK PHYSICIAN

BASIC PLAN

PREMIERPLAN

HEALTHSAVINGSADVANTAGEPLAN

SELECTEPO

$20 copay, plan then pays 100%*

$20 copay, plan then pays 100%*

Plan pays 95% after deductible

$25 copay, plan then pays 100%

$20 copay, plan then pays 100%*

$20 copay, plan then pays 100%*

Plan pays 70% after deductible

$35 copay, plan then pays 100%

Plan pays 50% after deductible

Plan pays 50% after deductible

Plan pays 50% after deductible

Not covered

$20 copay, plan then pays 100%*

$20 copay, plan then pays 100%*

Plan pays 70% after deductible

$35 copay, plan then pays 100%

Plan pays 50% after deductible

Plan pays 50% after deductible

Plan pays 50% after deductible

Not covered

OFFICE VISIT TO A PRIMARY CARE PHYSICIAN

BASIC PLAN

PREMIERPLAN

HEALTHSAVINGSADVANTAGEPLAN

SELECTEPO

$150 copay, plan then pays 100%

$150 copay, plan then pays 100%

Plan pays 70% after deductible

$150 copay, plan then pays 100%

$150 copay, plan then pays 100%

$150 copay, plan then pays 100%

Plan pays 70% after deductible

$150 copay, plan then pays 100%

$150 copay, plan then pays 100%

$150 copay, plan then pays 100%

Plan pays 70% after deductible

$150 copay, plan then pays 100%

$150 copay, plan then pays 100%

$150 copay, plan then pays 100%

Plan pays 70% after deductible

$150 copay, plan then pays 100%

$150 copay, plan then pays 100%

$150 copay, plan then pays 100%

Plan pays 70% after deductible

$150 copay, plan then pays 100%

EMERGENCY ROOM††† (TRUE EMERGENCY BASED ON PRUDENT LAYPERSON STANDARD)**

BASIC PLAN

PREMIERPLAN

HEALTHSAVINGSADVANTAGEPLAN

SELECTEPO

$40 copay, plan then pays 100%

$40 copay, plan then pays 100%

Plan pays 95% after deductible

$40 copay, plan then pays 100%

$40 copay, plan then pays 100%

$40 copay, plan then pays 100%

Plan pays 70% after deductible

$60 copay, plan then pays 100%

Plan pays 50% after deductible

Plan pays 50% after deductible

Plan pays 50% after deductible

Not covered

$40 copay, plan then pays 100%

$40 copay, plan then pays 100%

Plan pays 70% after deductible

$60 copay, plan then pays 100%

Plan pays 50% after deductible

Plan pays 50% after deductible

Plan pays 50% after deductible

Not covered

URGENT CARE CENTER

* Charges for additional services that are performed during an office visit may be subject to your plan deductible and coinsurance.‡ 90percentforallservicesbilledthroughRushfacility;70percentforservicesbilledindependently.††† Copay waived if admitted.

** The “prudent layperson standard” means the situation or illness would be considered to be an emergency by a prudent (cautious and sensible) non-medically trained person.

choose HE

ALT

H

continued on next page

SERVICEDESCRIPTION

RUSH FACILITY

(INCLUDESRUSHPHYSICIANS)

NON-RUSHIN-NETWORK

FACILITY

OUT-OF-NETWORKFACILITY

IN-NETWORKPHYSICIAN

OUT-OF- NETWORK PHYSICIAN

BASIC PLAN

BASIC PLAN

BASIC PLAN

BASIC PLAN

PREMIERPLAN

HEALTHSAVINGSADVANTAGEPLAN

PREMIERPLAN

HEALTHSAVINGSADVANTAGEPLAN

PREMIERPLAN

HEALTHSAVINGSADVANTAGEPLAN

PREMIERPLAN

HEALTHSAVINGSADVANTAGEPLAN

SELECTEPO

SELECTEPO

SELECTEPO

SELECTEPO

$40 copay, plan then pays 100%*

Plan pays 90% after deductible

Plan pays 100%*

Plan pays 100%*

$40 copay, plan then pays 100%*

Plan pays 95% after deductible

Plan pays 90% after deductible

Plan pays 95% after deductible

Plan pays 100%*

Plan pays 100%

Plan pays 100%*

Plan pays 100%

$40 copay, plan then pays 100%*

Plan pays 100%

Plan pays 100%

Plan pays 100%

$40 copay, plan then pays 100%*

Plan pays 70% after deductible

Plan pays 100%*

Plan pays 100%*

$40 copay, plan then pays 100%*

Plan pays 70% after deductible

Plan pays 70% after deductible

Plan pays 70% after deductible

Plan pays 100%*

Plan pays 100%

Plan pays 100%*

Plan pays 100%

$60 copay, plan then pays 100%*

Plan pays 100%

Plan pays 100%

Plan pays 100%

Plan pays 50% after deductible

Plan pays 50% after deductible

Plan pays 50% after deductible

Plan pays 50% after deductible

Plan pays 50% after deductible

Plan pays 50% after deductible

Plan pays 50% after deductible

Plan pays 50% after deductible

Plan pays 50% after deductible

Plan pays 50% after deductible

Plan pays 50% after deductible

Plan pays 50% after deductible

Not covered

Not covered

Not covered

Not covered

$40 copay, plan then pays 100%*

Plan pays 70% after deductible

Plan pays 100%*

Plan pays 100%*

$40 copay, plan then pays 100%*

Plan pays 70% after deductible

Plan pays 70% after deductible

Plan pays 70% after deductible

Plan pays 100%*

Plan pays 100%

Plan pays 100%*

Plan pays 100%

$60 copay, plan then pays 100%*

Plan pays 100%

Plan pays 100%

Plan pays 100%

Plan pays 50% after deductible

Plan pays 50% after deductible

Plan pays 50% after deductible

Plan pays 50% after deductible

Plan pays 50% after deductible

Plan pays 50% after deductible

Plan pays 50% after deductible

Plan pays 50% after deductible

Plan pays 50% after deductible

Plan pays 50% after deductible

Plan pays 50% after deductible

Plan pays 50% after deductible

Not covered

Not covered

Not covered

Not covered

DIAGNOSTIC TESTS, LABS, X-RAYS PERFORMED OUTSIDE OF PHYSICIAN OFFICE

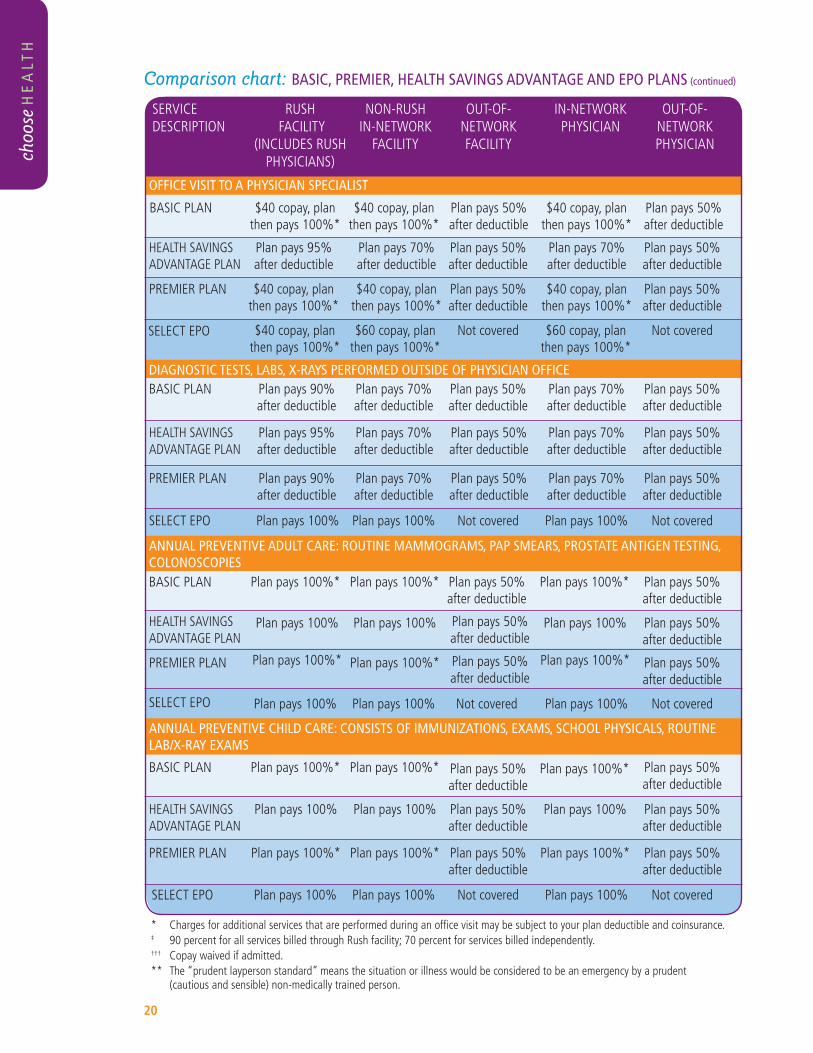

OFFICE VISIT TO A PHYSICIAN SPECIALIST

ANNUAL PREVENTIVE ADULT CARE: ROUTINE MAMMOGRAMS, PAP SMEARS, PROSTATE ANTIGEN TESTING, COLONOSCOPIES

ANNUAL PREVENTIVE CHILD CARE: CONSISTS OF IMMUNIZATIONS, EXAMS, SCHOOL PHYSICALS, ROUTINE LAB/X-RAY EXAMS

* Charges for additional services that are performed during an office visit may be subject to your plan deductible and coinsurance.‡ 90percentforallservicesbilledthroughRushfacility;70percentforservicesbilledindependently.††† Copay waived if admitted.** The “prudent layperson standard” means the situation or illness would be considered to be an emergency by a prudent (cautious and sensible) non-medically trained person.

choo

se H

EA

LTH

20

Comparison chart: BASIC, PREMIER, HEALTH SAVINGS ADVANTAGE AND EPO PLANS (continued)

Comparison chart: BASIC, PREMIER, HEALTH SAVINGS ADVANTAGE AND EPO PLANS (continued)

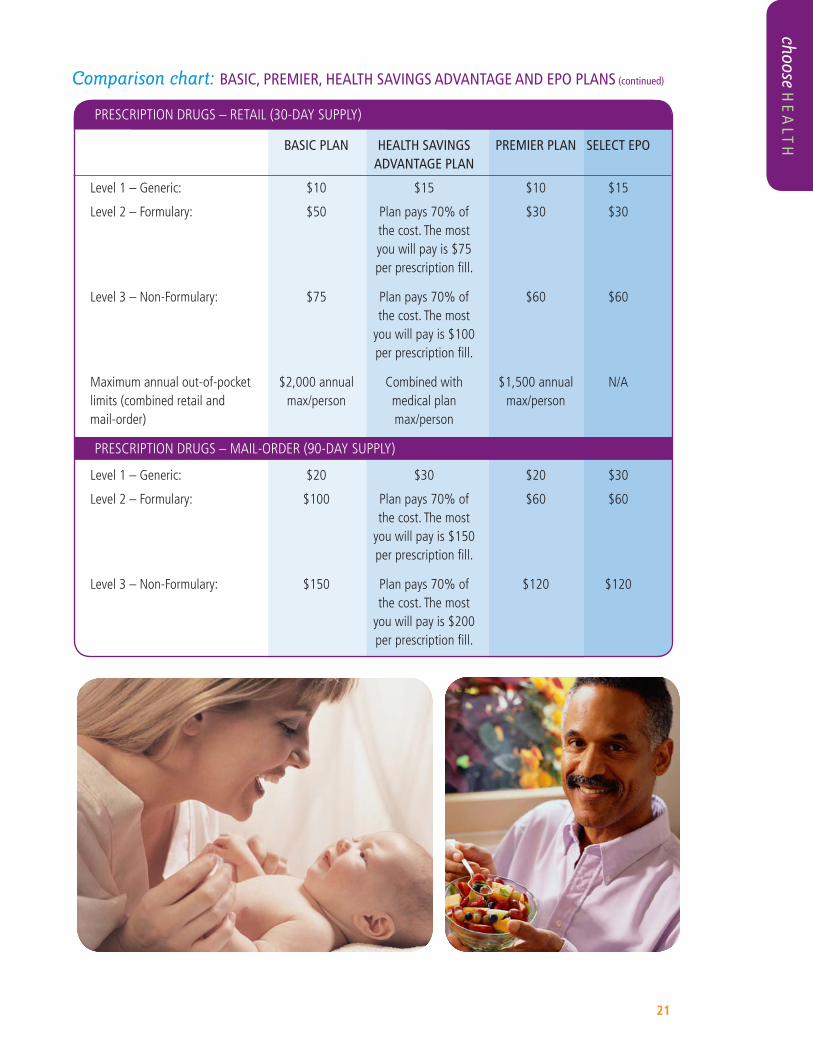

PRESCRIPTIONDRUGS–RETAIL(30-DAYSUPPLY)

BASIC PLAN HEALTH SAVINGS PREMIER PLAN SELECT EPO ADVANTAGE PLAN

Level1–Generic: $10 $15 $10 $15

Level 2 – Formulary: $50 Plan pays 70% of $30 $30 the cost. The most you will pay is $75 per prescription fill.

Level 3 – Non-Formulary: $75 Plan pays 70% of $60 $60 the cost. The most you will pay is $100 per prescription fill.

Maximum annual out-of-pocket $2,000 annual Combined with $1,500 annual N/A limits (combined retail and max/person medical plan max/person mail-order) max/person

Level1–Generic: $20 $30 $20 $30

Level 2 – Formulary: $100 Plan pays 70% of $60 $60 the cost. The most you will pay is $150 per prescription fill.

Level 3 – Non-Formulary: $150 Plan pays 70% of $120 $120 the cost. The most you will pay is $200 per prescription fill.

PRESCRIPTIONDRUGS–MAIL-ORDER(90-DAYSUPPLY)

21

choose HE

ALT

H

22

Prescription out-of-pocket maximum costs for Basic and Premier plansAnnual out-of-pocket costs are capped at $2,000 for the Basic Plan and $1,500 for the Premier Plan. This means that once your prescription costs exceed the cap in any given calendar year, your prescriptions are covered at 100 percent for the rest of the year (applies to each covered individual).

Please note that the cap only applies to covered prescriptions. A list of covered prescriptions can be found on the ExpressScriptswebsite,www.express-scripts.com.ExpressScripts’2014PreferredPrescriptionsMemberGuidewill beavailableinmid-December2013ontheExpressScriptswebsite,www.express-scripts.com.

Example:YousubscribetothePremierPlan.Youaretakingtwonon-formularydrugsthatcostyou$75eachpermonth ($150 per month). After 10 months, your annual out-of-pocket costs are $1,500. All of your prescriptions for the rest of the calendar year will be provided at no cost. The $1,500 cap ($2,000 for Basic Plan members) applies to each covered individual.

ExpressScriptsannuallyreviewsitsdruglist(formulary)andmaymakechangesthataffectyourcoverage.Thesechanges may include:

•Shiftingadrugtoadifferentlevel,whichcouldresultinahighercopayment.

•Changingthedispensinglimits,whichmayrequireyourphysiciantocontactExpressScriptsdirectlyat (866) 814-7106.

•Requiringpre-certification,whichmeansthatyourdoctorwouldneedtocontactExpressScriptsfirstbeforewritingyour prescription.

•Implementinga“steptherapy”protocolinwhichyoumightberequiredtotryacourseofalessexpensivedrugthat has proven to be effective before “stepping up” to a higher-priced drug.

choo

se H

EA

LTH

Prescription coverage with the Health Savings Advantage planThe prescription drug coverage available with the Health Savings Advantage Plan works a little differently thanthecoverageyoureceivewiththeothermedicalplanoptions.WiththeHealthSavingsAdvantage:

•Yourdeductibleforprescriptioncostsiscombinedwithyourmedicalplandeductible,whichmeansyou’ll reach the deductible faster.

•Yourannualmaximumprescriptiondrugout-of-pocketexpensesarealsocombinedwithyourannualmaximum medical plan expenses.

•Ifyouchoosetohaveyourprescriptionfilledatanout-of-networkpharmacy,you’llpay60%ofthecost after the deductible.

Express Scripts PharmacyRushpartnerswithExpressScriptsPharmacytohandleallprescriptiondrugcoverage.ExpressScriptsservesnearly60 million people nationwide and has pioneered innovations in personalized medicine, dispensing technology, and patientcarethathelplowercostsandimprovelives.ExpressScriptshasbeenrecognizedbyindependentresearchorganizations for delivering the highest member satisfaction of any prescription benefit manager.

FormoreinformationonExpressScripts,pleasegototheirwebsite,www.express-scripts.com.

23

Using your prescription drug benefits to your best advantageUsingyourprescriptiondrugbenefitseffectivelybytakingsuchstepsasrequestinggenericdrugsandordering maintenancedrugsthroughthemail-orderprogramwillhelpbothyouandRushmanageexpenses.Genericdrugs arechemicallyequivalenttobrand-namedrugsandtypicallyprovidethesameresultsasbrand-namedrugsbut usuallycost30percentto70percentless.Whenyourdoctorprescribesadrug,askifagenericequivalentisavailableand appropriate for your needs.

Infertility prescription and treatment coverageRush offers comprehensive infertility benefits for all covered health plan members. Benefits are limited to a $50,000 lifetime maximum of combined medical and self-injectible fertility drugs. Benefits paid each year will carry over and apply to the $50,000 lifetime maximum. (For Basic, Premier and Health Savings Advantage Plans, annual deductibles and coinsurance will apply.) Note: for self-injectible infertility medications, your physician must communicate the prescription to the Professional Building pharmacy via telephone at (312) 563-2246 or via fax at (312) 563-2247. Any associated shipping charges will be at the expense of the member. For further information on the Rush infertility benefit, please refer to the summary plan description available on the Benefits website at https://Rushbenefits.HRintouch.com.

Smoking cessation prescription coverageRush prescription drug benefits include smoking-deterrent medications as a covered benefit (with the applicable copayment and subject to a six-month lifetime limitation). Smoking cessation programs, counseling and prescription drug copayments are also reimbursable expenses under the flexible spending account program for health care.

Did you know:DISCOUNTSEmployeesreceivea$3discountoneachprescriptionwhenyoufillyourprescriptionatoneofthetwo Rush pharmacies at the following locations:•TheRushProfessionalBuilding(fourthfloor)•TheOakParkMedicalOfficeBuilding

MAIL-ORDER PROGRAM OFFERS EVEN GREATER SAVINGSForevenmoresavings,youmayobtainprescriptiondrugsthroughExpressScripts’homedeliverymail-orderprogram. You receive a 90-day supply at the same cost as a 60-day supply.

Formoreinformation,membersmaygototheExpressScriptswebsiteatwww.express-scripts.comorcallExpressScripts’customerservicedepartmentat(866)814-7106.

choose HE

ALT

H

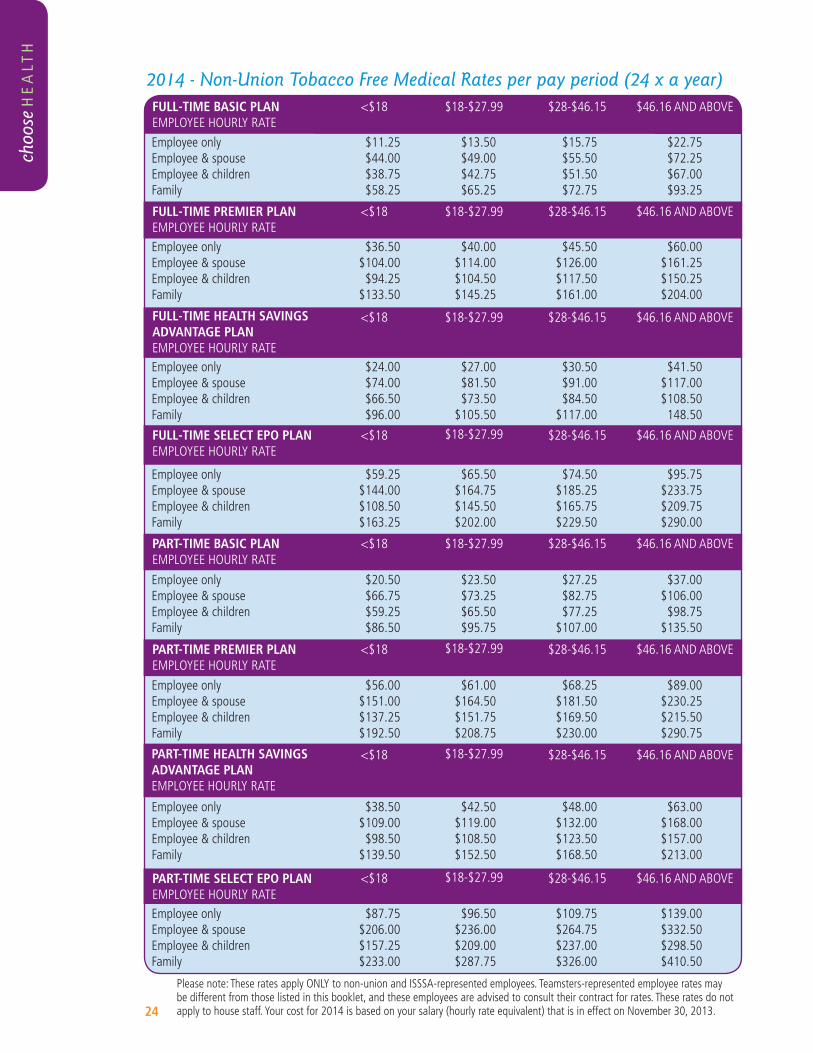

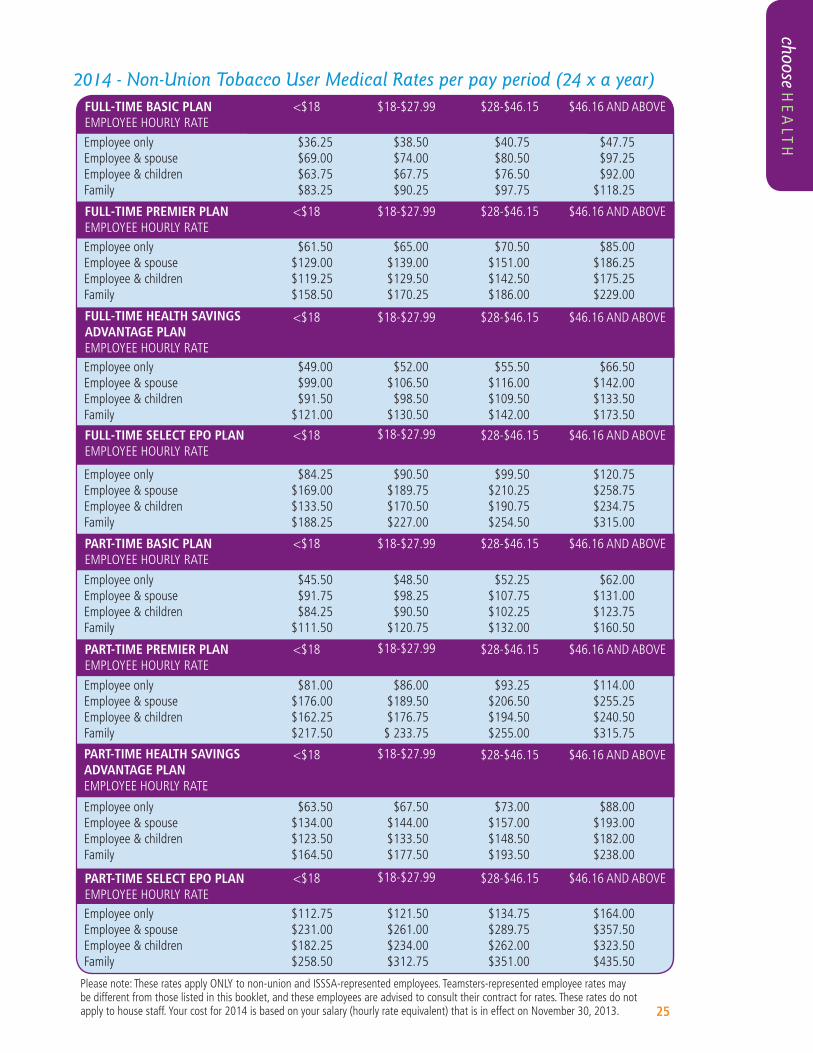

2014 - Non-Union Tobacco Free Medical Rates per pay period (24 x a year)

24

FULL-TIME BASIC PLANEMPLOYEEHOURLYRATE

<$18 $18-$27.99 $28-$46.15 $46.16ANDABOVE

Employeeonly $11.25 $13.50 $15.75 $22.75Employee&spouse $44.00 $49.00 $55.50 $72.25Employee&children $38.75 $42.75 $51.50 $67.00Family $58.25 $65.25 $72.75 $93.25

Employeeonly $36.50 $40.00 $45.50 $60.00Employee&spouse $104.00 $114.00 $126.00 $161.25Employee&children $94.25 $104.50 $117.50 $150.25Family $133.50 $145.25 $161.00 $204.00

Employeeonly $20.50 $23.50 $27.25 $37.00Employee&spouse $66.75 $73.25 $82.75 $106.00Employee&children $59.25 $65.50 $77.25 $98.75Family $86.50 $95.75 $107.00 $135.50

Employeeonly $56.00 $61.00 $68.25 $89.00Employee&spouse $151.00 $164.50 $181.50 $230.25Employee&children $137.25 $151.75 $169.50 $215.50Family $192.50 $208.75 $230.00 $290.75

Employeeonly $38.50 $42.50 $48.00 $63.00Employee&spouse $109.00 $119.00 $132.00 $168.00Employee&children $98.50 $108.50 $123.50 $157.00Family $139.50 $152.50 $168.50 $213.00

Employeeonly $24.00 $27.00 $30.50 $41.50Employee&spouse $74.00 $81.50 $91.00 $117.00Employee&children $66.50 $73.50 $84.50 $108.50Family $96.00 $105.50 $117.00 148.50

Employeeonly $87.75 $96.50 $109.75 $139.00Employee&spouse $206.00 $236.00 $264.75 $332.50Employee&children $157.25 $209.00 $237.00 $298.50Family $233.00 $287.75 $326.00 $410.50

Employeeonly $59.25 $65.50 $74.50 $95.75Employee&spouse $144.00 $164.75 $185.25 $233.75Employee&children $108.50 $145.50 $165.75 $209.75Family $163.25 $202.00 $229.50 $290.00

FULL-TIME PREMIER PLANEMPLOYEEHOURLYRATE

PART-TIME BASIC PLANEMPLOYEEHOURLYRATE

FULL-TIME HEALTH SAVINGS ADVANTAGE PLANEMPLOYEEHOURLYRATE

PART-TIME PREMIER PLANEMPLOYEEHOURLYRATE

PART-TIME SELECT EPO PLANEMPLOYEEHOURLYRATE

PART-TIME HEALTH SAVINGS ADVANTAGE PLANEMPLOYEEHOURLYRATE

FULL-TIME SELECT EPO PLAN EMPLOYEEHOURLYRATE

<$18

<$18

<$18

<$18

<$18

<$18

<$18

$18-$27.99

$18-$27.99

$18-$27.99

$18-$27.99

$18-$27.99

$18-$27.99

$18-$27.99

$28-$46.15

$28-$46.15

$28-$46.15

$28-$46.15

$28-$46.15

$28-$46.15

$28-$46.15

$46.16ANDABOVE

$46.16ANDABOVE

$46.16ANDABOVE

$46.16ANDABOVE

$46.16ANDABOVE

$46.16ANDABOVE

$46.16ANDABOVE

Please note: These rates apply ONLY to non-union and ISSSA-represented employees. Teamsters-represented employee rates may be different from those listed in this booklet, and these employees are advised to consult their contract for rates. These rates do not applytohousestaff.Yourcostfor2014isbasedonyoursalary(hourlyrateequivalent)thatisineffectonNovember30,2013.

choo

se H

EA

LTH

2014 - Non-Union Tobacco User Medical Rates per pay period (24 x a year)

25

FULL-TIME BASIC PLANEMPLOYEEHOURLYRATE

<$18 $18-$27.99 $28-$46.15 $46.16ANDABOVE

Employeeonly $36.25 $38.50 $40.75 $47.75Employee&spouse $69.00 $74.00 $80.50 $97.25Employee&children $63.75 $67.75 $76.50 $92.00Family $83.25 $90.25 $97.75 $118.25

Employeeonly $61.50 $65.00 $70.50 $85.00Employee&spouse $129.00 $139.00 $151.00 $186.25Employee&children $119.25 $129.50 $142.50 $175.25Family $158.50 $170.25 $186.00 $229.00

Employeeonly $45.50 $48.50 $52.25 $62.00Employee&spouse $91.75 $98.25 $107.75 $131.00Employee&children $84.25 $90.50 $102.25 $123.75Family $111.50 $120.75 $132.00 $160.50

Employeeonly $81.00 $86.00 $93.25 $114.00Employee&spouse $176.00 $189.50 $206.50 $255.25Employee&children $162.25 $176.75 $194.50 $240.50Family $217.50 $ 233.75 $255.00 $315.75

Employeeonly $63.50 $67.50 $73.00 $88.00Employee&spouse $134.00 $144.00 $157.00 $193.00Employee&children $123.50 $133.50 $148.50 $182.00Family $164.50 $177.50 $193.50 $238.00

Employeeonly $49.00 $52.00 $55.50 $66.50Employee&spouse $99.00 $106.50 $116.00 $142.00Employee&children $91.50 $98.50 $109.50 $133.50Family $121.00 $130.50 $142.00 $173.50

Employeeonly $112.75 $121.50 $134.75 $164.00Employee&spouse $231.00 $261.00 $289.75 $357.50Employee&children $182.25 $234.00 $262.00 $323.50Family $258.50 $312.75 $351.00 $435.50

Employeeonly $84.25 $90.50 $99.50 $120.75Employee&spouse $169.00 $189.75 $210.25 $258.75Employee&children $133.50 $170.50 $190.75 $234.75Family $188.25 $227.00 $254.50 $315.00

FULL-TIME PREMIER PLANEMPLOYEEHOURLYRATE

PART-TIME BASIC PLANEMPLOYEEHOURLYRATE

FULL-TIME HEALTH SAVINGS ADVANTAGE PLANEMPLOYEEHOURLYRATE

PART-TIME PREMIER PLANEMPLOYEEHOURLYRATE

PART-TIME SELECT EPO PLANEMPLOYEEHOURLYRATE

PART-TIME HEALTH SAVINGS ADVANTAGE PLANEMPLOYEEHOURLYRATE

FULL-TIME SELECT EPO PLAN EMPLOYEEHOURLYRATE

<$18

<$18

<$18

<$18

<$18

<$18

<$18

$18-$27.99

$18-$27.99

$18-$27.99

$18-$27.99

$18-$27.99

$18-$27.99

$18-$27.99

$28-$46.15

$28-$46.15

$28-$46.15

$28-$46.15

$28-$46.15

$28-$46.15

$28-$46.15

$46.16ANDABOVE

$46.16ANDABOVE

$46.16ANDABOVE

$46.16ANDABOVE

$46.16ANDABOVE

$46.16ANDABOVE

$46.16ANDABOVE

Please note: These rates apply ONLY to non-union and ISSSA-represented employees. Teamsters-represented employee rates may be different from those listed in this booklet, and these employees are advised to consult their contract for rates. These rates do not applytohousestaff.Yourcostfor2014isbasedonyoursalary(hourlyrateequivalent)thatisineffectonNovember30,2013.

choose HE

ALT

H

26

choo

se H

EA

LTH

DENTAL PLANS

Dentalcoverage,providedbyGuardian:FirstCommonwealth,helpsyouandyourfamilymanagethecostofmaintain-ing good dental health and treating dental disease or injury.

You have a choice of two dental plans. The PPO allows you to see any dentist you choose. Once you meet the deduct-ible you pay coinsurance, a percentage of the total cost, when you seek dental care. However, you’ll always save moneyifyouchooseoneofthe2,500GuardianparticipatingprovidersintheChicagoarea—thesedentistsanddental specialists have agreed to discount their fees so you pay a percentage of a lower total cost. Also, by utilizing a network dentist, your deductible for preventive care services is waived. If you go out of network, preventive services are covered at 100 percent only after you have satisfied your annual deductible.

NEW FOR 2014:WithanewPreventiveAdvantageProgram,in-networkpreventivechargeswillnotcounttowardthe annual maximum benefit. Additionally, new hires enrolled in the Dental PPO plan will not need to wait 12 months before they receive coverage for major dental procedures.

Did you know:Guardian’sMaximumRolloverAccount(MRA)allowsemployeesenrolledinthePPOdentalplantosaveapercentage of the annual dental maximum ($1,250) in order to cover expensive procedures in upcoming years. For example, if you do not reach your annual maximum in a plan year, the MRA allows you to rollover a percentage of this money for use in the future to help cover oral surgery, implants or other costly services.Additionally,ifyouusetheservicesofin-networkprovidersexclusivelyduringthebenefityear,Guardian will increase the percentage credited to your MRA account.