Economic Update – The Good News! (…and the bad & ugly) Rohan Kerr Director Kerr Allan Financial 17 th April 2012

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Economic Update – The Good News! (…and the bad & ugly)

Rohan KerrDirectorKerr Allan Financial17th April 2012

Kerr Allan FinancialDisclaimer

This presentation has been prepared and issued by Kerr Allan Financial Pty Ltd, (“Kerr Allan Financial” or “Company”) to assist it in informing interested parties about the Company. The information in this document is in summary form and should not be relied upon as a complete and accurate representation of any matters that a potential investor should consider in evaluating Kerr Allan Financial. While management has taken every effort to ensure the accuracy of the material in the presentation, neither the Company nor its advisers has verified the accuracy or completeness of the information, or any statements and opinions contained in this presentation. This presentation is provided for information purposes only, and to the maximum extent permitted by law, Kerr Allan Financial, its officers and management exclude and disclaim any liability in respect of the authenticity, validity, accuracy, suitability or completeness of, or any errors in or omission from, any information, statement or opinion contained in this presentation or anything done in reliance on the presentation. This presentation may contain forward looking statements. The words 'anticipate', 'believe', 'expect', 'project', 'forecast', 'estimate', 'likely', 'intend', 'should', 'could', 'may', 'target', 'plan‘ and other similar expressions are intended to identify forward-looking statements. Indications of, and guidance on, future earnings and financial position and performance are also forward-looking statements. Forward-looking statements are subject to risk factors associated with the Company’s business, many of which are beyond the control of the Company. It is believed that the expectations reflected in these statements are reasonable but they may be affected by a variety of variables and changes in underlying assumptions which could cause actual results or trends to differ materially from those expressed or implied in such statements. There can be no assurance that actual outcomes will not differ materially from these statements. You should not place undue reliance on forward-looking statements and neither Kerr Allan Financial nor any of its directors, employees, servants, advisers or agents assume any obligation to update such information. This presentation should not be considered as an offer or invitation to subscribe or purchase any securities in the Company or as an inducement to make an offer or invitation with respect to those securities. No agreement to subscribe for securities in the Company will be entered into on the basis of this presentation. You should not act and refrain from acting in reliance on this presentation material. Nothing contained in this presentation constitutes investment, legal, tax or other advice. This overview of Kerr Allan Financial does not purport to be all inclusive or to contain all information which its recipients may require in order to make an informed assessment of its investment prospects. Before making an investment decision, you should conduct, with the assistance of your broker, planner or other financial or professional adviser, your own investigation in light of your particular investment needs, objectives and financial circumstances and perform your own analysis in order to satisfy yourself as to the accuracy and completeness of the information, statements and opinions contained in this presentation and making any investment decision. References to dollars, cents or $ in this presentation are to Australian currency, unless otherwise stated.

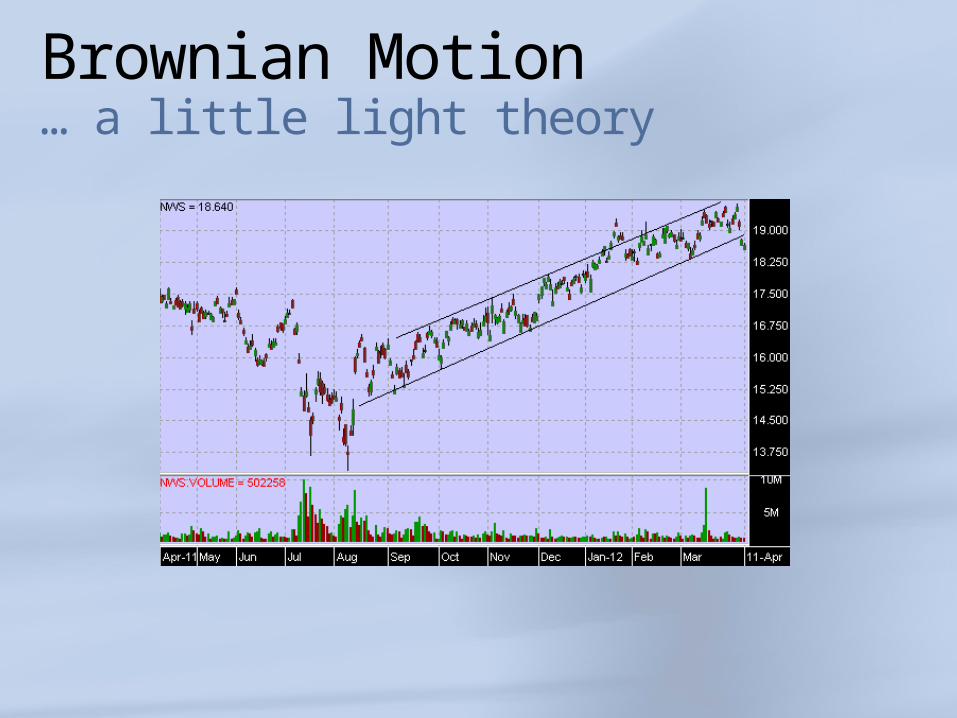

Brownian Motion… a little light theory

Brownian Motion, Robert Brown 1827Under a microscope pollen grains in water were in a constant state of agitationEinstein’s explanation 1909 “a pollen grain is buffeted by collisions with water molecules moving randomly in all directions” At different times a pollen grain is hit more on one side than another, hence the random nature of the motion (basis of random theory)

Significance: The mathematical model of Brownian motion has several real-world applications. An often quoted example is stock market fluctuations.

Brownian Motion… a little light theory

R Merton / P Samuelson “assets have continuous prices evolving continuously in time and are driven by Brownian motion processes”Certain assumptions: perfectly divisible assets, costless markets, no market surprisesSome electronic model based trading funds (eg Macq Winton?) use this base theory of randomly fluctuating components. Trading short options positions also uses this theory

Brownian Motion… a little light theory

Tough Investing EnvironmentRisks to a recovery

Europe is a generational debt problemUS is not recovering fast enough for BernankeThe Australian Governments instability is deterring overseas investors – the “Gillard” effectResource oversupply looming – possible capex cutbacksRBA inflation mandate appears outdatedOther potential black swans

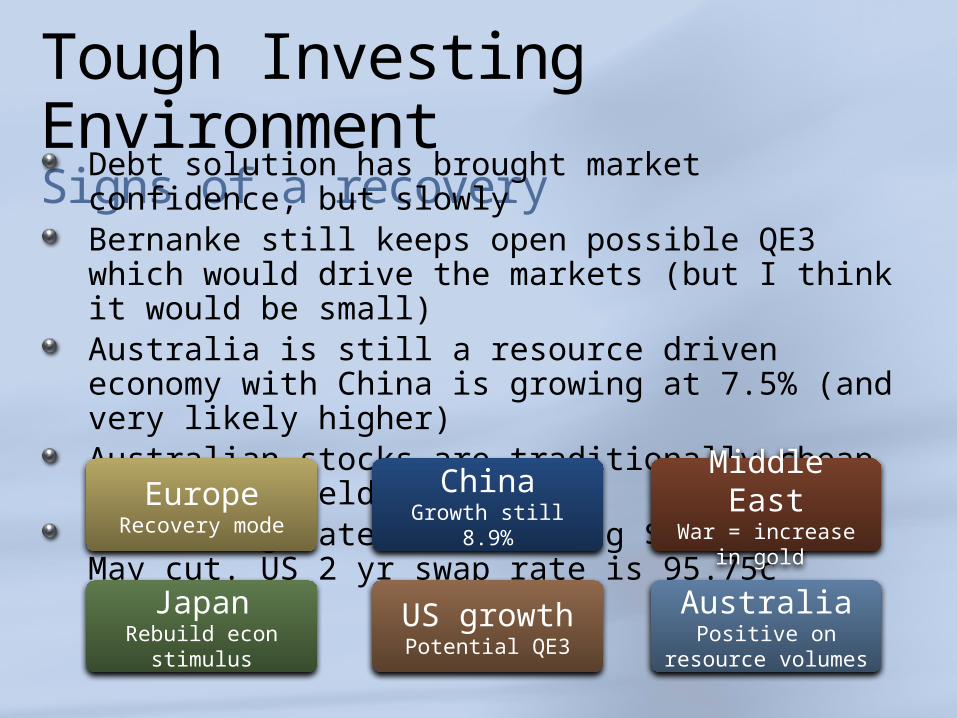

Tough Investing EnvironmentSigns of a recovery

Debt solution has brought market confidence, but slowlyBernanke still keeps open possible QE3 which would drive the markets (but I think it would be small)Australia is still a resource driven economy with China is growing at 7.5% (and very likely higher)Australian stocks are traditionally cheap with good yieldsDecreasing rates and falling $A is key – May cut. US 2 yr swap rate is 95.75c

Middle EastWar = increase in gold

ChinaGrowth still 8.9%

EuropeRecovery mode

AustraliaPositive on resource

volumes

US growthPotential QE3

JapanRebuild econ stimulus

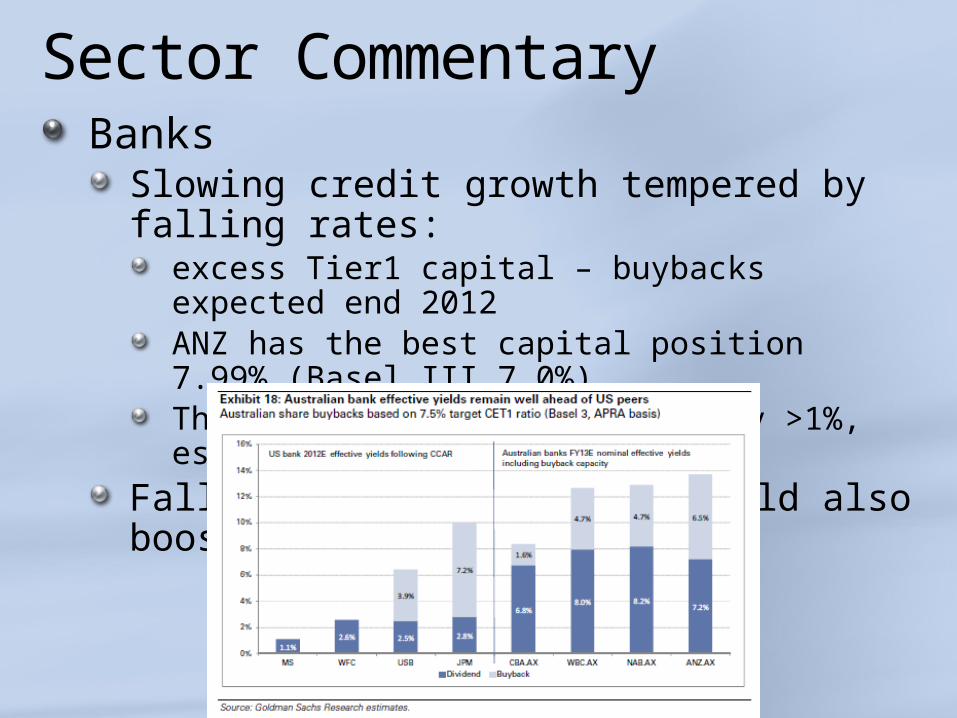

Sector CommentaryBanks

Slowing credit growth tempered by falling rates:excess Tier1 capital – buybacks expected end 2012ANZ has the best capital position 7.99% (Basel III 7.0%)This would boost ROE / yield by >1%, est 2013 ROE 17%

Falling cost of capital should also boost profits

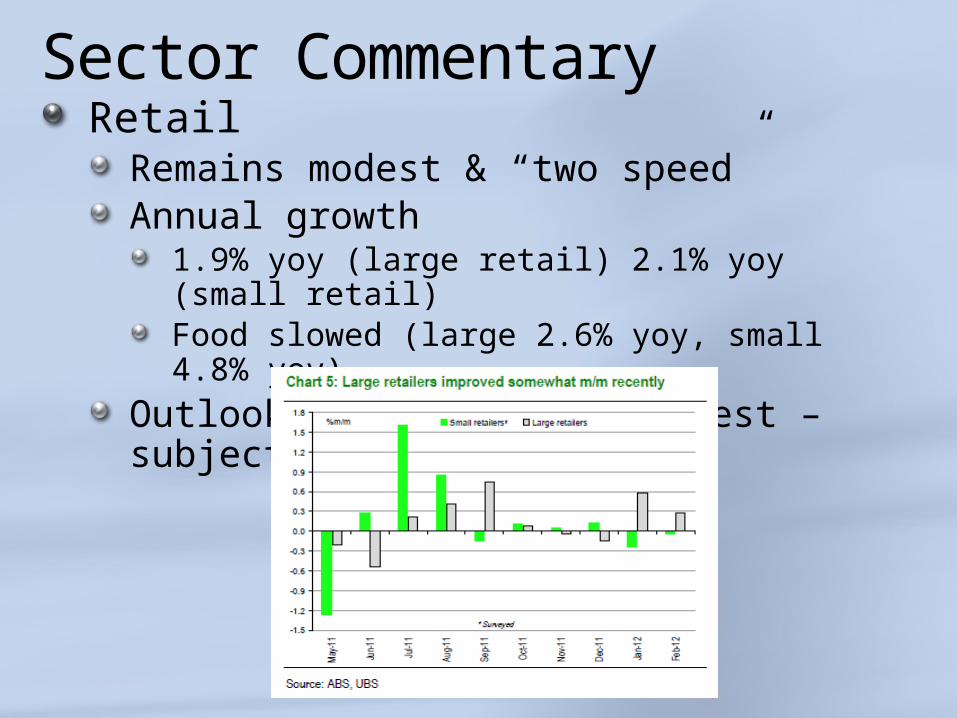

Sector CommentaryRetail

Remains modest & “two speed”Annual growth

1.9% yoy (large retail) 2.1% yoy (small retail)Food slowed (large 2.6% yoy, small 4.8% yoy)

Outlook expected to be modest – subject to IR’s

Sector CommentaryInsurance

Underlying margin improvement expected, but may the level may disappoint. Higher re-insurance costsFierce competition / lack of affordabilityLow but rising bond yields but narrowing credit spreads. Bond yields may retreat again (target 3%)

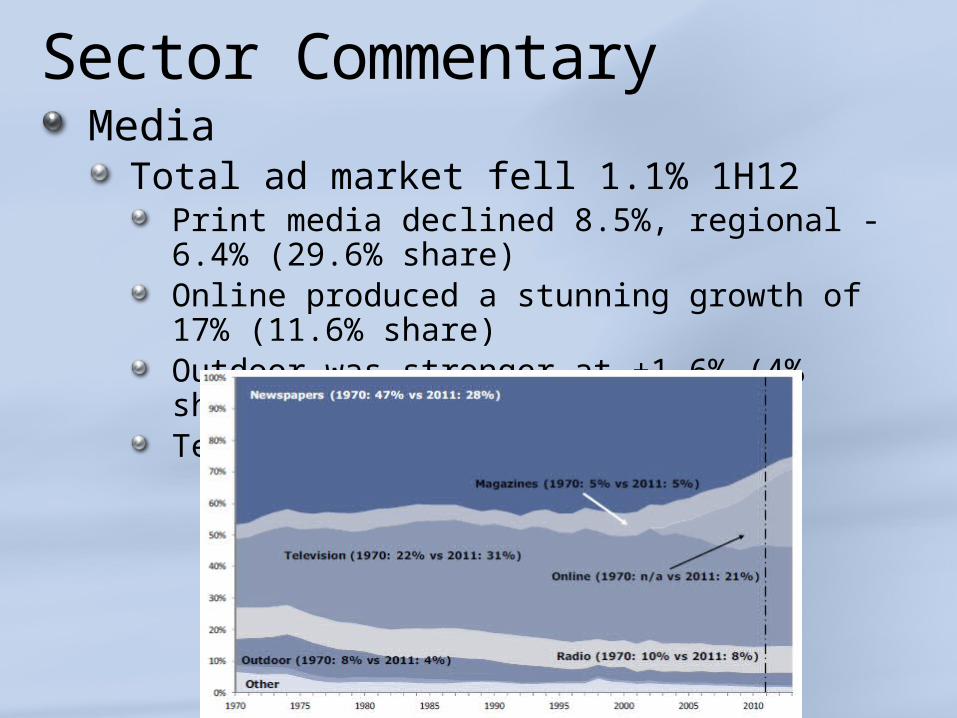

Sector CommentaryMedia

Total ad market fell 1.1% 1H12Print media declined 8.5%, regional -6.4% (29.6% share)Online produced a stunning growth of 17% (11.6% share)Outdoor was stronger at +1.6% (4% share)Television stable (21% share)

Sector CommentaryMiners

Worst performing sector this yearLarge vs small miners (cash flow vs not)Negatives:

Chinese growth slowingGrowth mix changing – less investment demand at the moment globallyChinese equities weakeningGlobal growth sluggish & commodity prices above long run averageDevelopment costs increased ~50% over 2 years, this will continue

Sector CommentaryMiners cont.

PositivesStable pricesChina more likely to pickupCheap valuationsUS economy picking up

Continue underweight & continuous assessment

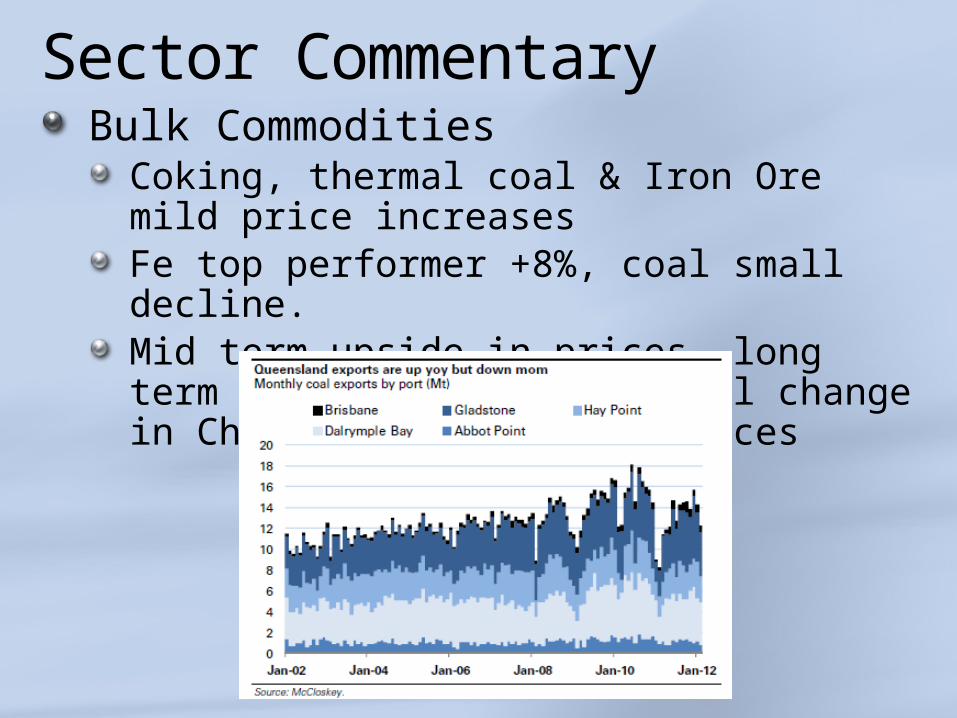

Sector CommentaryBulk Commodities

Coking, thermal coal & Iron Ore mild price increasesFe top performer +8%, coal small decline.Mid term upside in prices, long term oversupply / structural change in China may depress LR prices

Sector CommentaryTelco’s – TLS dominant

9% yield with EPS growth 11% expected. Mobile handset growth & gaining high margins (34%)Growth industry with the explosion in tablets, higher bundles volume & marginsAnalysts predict capital management next catalyst

Investment Strategy… key theme’s

Solid EPS profile (cash flow is king)low earnings volatility, strong cash flow operations

WES, NWS, CSL

International exposure (falling $A)AMC, NWS, CSL

Deep value plays (market turnaround)AWC, BHP (half weight)

Banks – (yield & growth)ANZ, WBC, CBA

Stable conservatives (yield & stability)APA, RHC, TLS

Questions

Related Documents