THINK OUTSIDE. Global Market Brief & Labor Risk Index 2011 1 METHODOLOGY SAMPLE REPORT ONLY

Q1 2011 Global Market Brief & Labor Risk Index

Oct 21, 2014

Brief and Labor Risk Index is joint production between KellyOCG and Eurasia

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Think ouTside.

Global Market Brief & Labor Risk Index

2011 1meThodology sample reporT only

Global Market Brief & Labor Risk Index

2011

This is meThodology sample reporT only.

To subscribe to the global market Brief & labor risk index, visit kellyocg.com/marketbrief

1

conTenTs

This material was produced by Eurasia Group in collaboration with KellyOCG. This is intended as general background research and is not intended to constitute advice on any particular commercial investment, trade matter, or issue, and should not be relied upon for such purposes. Eurasia Group is a private research and consulting firm. © 2011 KellyOCG and Eurasia Group.

3 preface: rolf kleiner, senior Vice-president, kelly ocg & ian Bremmer, president, eurasia group

4 methodology

72 about sponsors

The Americas6 overview

7 risk index

8 argentina

9 Brazil

10 canada

11 chile

12 colombia

13 mexico

14 panama

15 united states

Asia Pacific17 overview

18 risk index

19 australia

20 china

21 hong kong

22 india

23 indonesia

24 Japan

25 malaysia

26 new Zealand

27 philippines

28 singapore

29 south korea

30 sri lanka

31 Thailand

32 Vietnam

Europe and Eurasia34 overview

35 risk index

36 Baltics

37 Belgium

38 Bulgaria

39 czech republic

40 denmark

41 France

42 germanu

43 hungary

44 ireland

45 italy

46 luxembourg

47 netherlands

48 norway

49 poland

50 portugal

51 romania

52 russia

53 spain

54 sweden

55 switzerland

56 Turkey

57 ukraine

58 united kingdom

Middle East and Africa60 overview

61 risk index

62 algeria

63 egypt

64 israel

65 kenya

66 kuwait

67 morocco

68 Qatar

69 saudi arabia

70 south africa

71 united arab emirates

cover: horseshoe Falls, niagara Falls, ontario, canada © 2006 Frank Leung

4 | gloBal markeT BrieF & laBor risk index Q1 2011

Preface

rolf kleiner,senior Vice-president, kellyocg

ian Bremmer,president, eurasia group

conTenTs

preFace

meThodology

The americas

asia paciFic

europe and eurasia

middle easT and aFrica

aBouT sponsors

some convergence, the variation

in growth rates will lead to

different economic and labor

policy concerns.

The Asia-Pacific region, led by

China, continues to grow strongly.

In addition, most of the emerging

economies in the Americas, Middle

East, and Africa appear set for

continued growth—although

the protests in Egypt and other

countries are causing instability and

could dampen growth prospects.

As a result, labor markets in some

countries are tightening and there is

upward pressure on wages. In some

cases, such as Brazil, governments

will likely take an active role in

negotiating wage contracts in 2011.

Governments in strong-growth

countries will also be concerned

with controlling inflation—

especially if it threatens to hurt

the purchasing power of poorer

populations and possibly incite

unrest. China, for instance, has

already begun to tighten monetary

policy, and will likely continue to

do so in 2011.

In developed markets the risks

will come from weak economic

recovery or continued high

unemployment despite economic

growth. And throughout much

of Europe, austerity measures

will continue to weigh on growth

prospects. This is particularly true in

the eurozone periphery—Greece,

Ireland, Portugal, and Spain—

where austerity is likely to be the

most severe. On the bright side,

although potential labor market

reforms may spark social unrest in

the short-term, they could improve

competitiveness and prospects for

long-term growth.

■ ■ ■

➔ The coming year is likely

to see a continuation of the two-

speed economic recovery of 2010

with emerging market nations set

to again outperform developed

economies. However, growth rates

are likely to converge somewhat

in 2011, as growth in emerging

markets is likely to moderate while

the recovery in some developed

markets—such as Norway and the

US—may gain traction. Despite

5 | gloBal markeT BrieF & laBor risk index Q1 2011

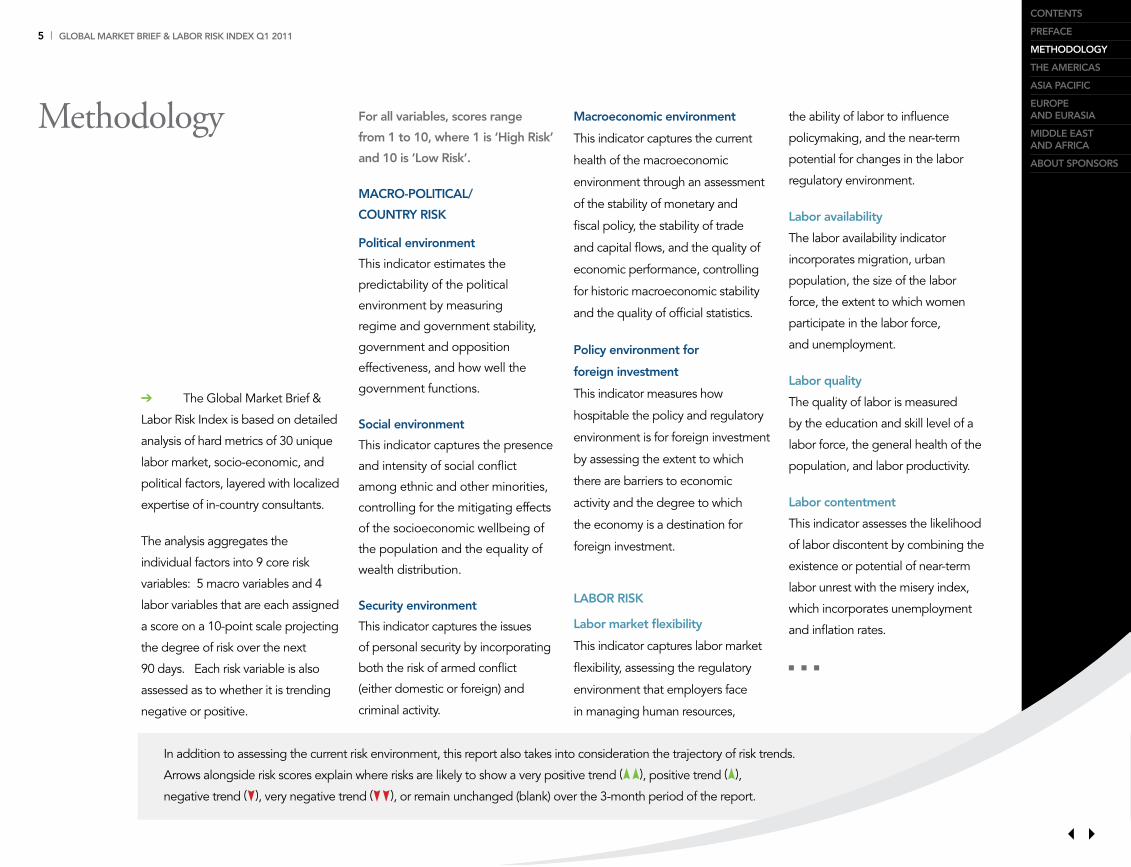

Methodology

In addition to assessing the current risk environment, this report also takes into consideration the trajectory of risk trends.

Arrows alongside risk scores explain where risks are likely to show a very positive trend (X X), positive trend (X),

negative trend (Y), very negative trend (Y Y), or remain unchanged (blank) over the 3-month period of the report.

conTenTs

preFace

meThodology

The americas

asia paciFic

europe and eurasia

middle easT and aFrica

aBouT sponsors

➔ The Global Market Brief &

Labor Risk Index is based on detailed

analysis of hard metrics of 30 unique

labor market, socio-economic, and

political factors, layered with localized

expertise of in-country consultants.

The analysis aggregates the

individual factors into 9 core risk

variables: 5 macro variables and 4

labor variables that are each assigned

a score on a 10-point scale projecting

the degree of risk over the next

90 days. Each risk variable is also

assessed as to whether it is trending

negative or positive.

macroeconomic environment

This indicator captures the current

health of the macroeconomic

environment through an assessment

of the stability of monetary and

fiscal policy, the stability of trade

and capital flows, and the quality of

economic performance, controlling

for historic macroeconomic stability

and the quality of official statistics.

policy environment for

foreign investment

This indicator measures how

hospitable the policy and regulatory

environment is for foreign investment

by assessing the extent to which

there are barriers to economic

activity and the degree to which

the economy is a destination for

foreign investment.

laBor risk

labor market flexibility

This indicator captures labor market

flexibility, assessing the regulatory

environment that employers face

in managing human resources,

the ability of labor to influence

policymaking, and the near-term

potential for changes in the labor

regulatory environment.

labor availability

The labor availability indicator

incorporates migration, urban

population, the size of the labor

force, the extent to which women

participate in the labor force,

and unemployment.

labor quality

The quality of labor is measured

by the education and skill level of a

labor force, the general health of the

population, and labor productivity.

labor contentment

This indicator assesses the likelihood

of labor discontent by combining the

existence or potential of near-term

labor unrest with the misery index,

which incorporates unemployment

and inflation rates.

■ ■ ■

For all variables, scores range

from 1 to 10, where 1 is ‘high risk’

and 10 is ‘low risk’.

macro-poliTical/

counTry risk

political environment

This indicator estimates the

predictability of the political

environment by measuring

regime and government stability,

government and opposition

effectiveness, and how well the

government functions.

social environment

This indicator captures the presence

and intensity of social conflict

among ethnic and other minorities,

controlling for the mitigating effects

of the socioeconomic wellbeing of

the population and the equality of

wealth distribution.

security environment

This indicator captures the issues

of personal security by incorporating

both the risk of armed conflict

(either domestic or foreign) and

criminal activity.

6 | gloBal markeT BrieF & laBor risk index Q1 2011

Overview: The Americas

conTenTs

preFace

meThodology

The americas

overview

risk index

argentina

Brazil

canada

chile

colombia

mexico

panama

united states

asia paciFic

europe and eurasia

middle easT and aFrica

aBouT sponsors

wages in Argentina, Brazil, and

Chile. In other countries, such as

Colombia, Canada, and the US,

high levels of unemployment have

continued to plague governments

that have struggled to foster more

job creation. In Argentina, Brazil,

and Colombia, governments will

likely take an active role in helping

to negotiate next year’s wage

agreements with labor unions.

Despite pressures from unions for

higher pay, most governments

will show some restraint as they

try to keep inflation and spending

pressures in check and address

concerns from the private sector.

➔ Many countries in the

Americas outperformed economic

expectations in 2010, though growth

is expected to slightly moderate

in 2011 as governments tighten

monetary policies, cut back on

spending, or manage the impact

of recent natural disasters. Strong

growth and an uptick in inflation

have led to some labor shortages

and increased demands for higher

Growth in the US and Canada is

expected to remain in the low single

digits. While Canada outperformed

the US in 2010, its growth rate is

now expected to lag as officials in

Ottawa begin to tighten fiscal policy

and tapped-out consumers start to

rein in their spending. Meanwhile,

in the US, an $858 billion tax-cut

compromise hashed out by the

White House and Republicans is

expected to boost the economy by

as much as an additional percentage

point of GDP.

■ ■ ■

7 | gloBal markeT BrieF & laBor risk index Q1 2011

conTenTs

preFace

meThodology

The americas

overview

risk index

argentina

Brazil

canada

chile

colombia

mexico

panama

united states

asia paciFic

europe and eurasia

middle easT and aFrica

aBouT sponsors

very positive trend

positive trend

negative trend

very negative trend

For all variables, scores range from 1 to 10, where 1 is ‘high risk’ and 10 is ‘low risk’.

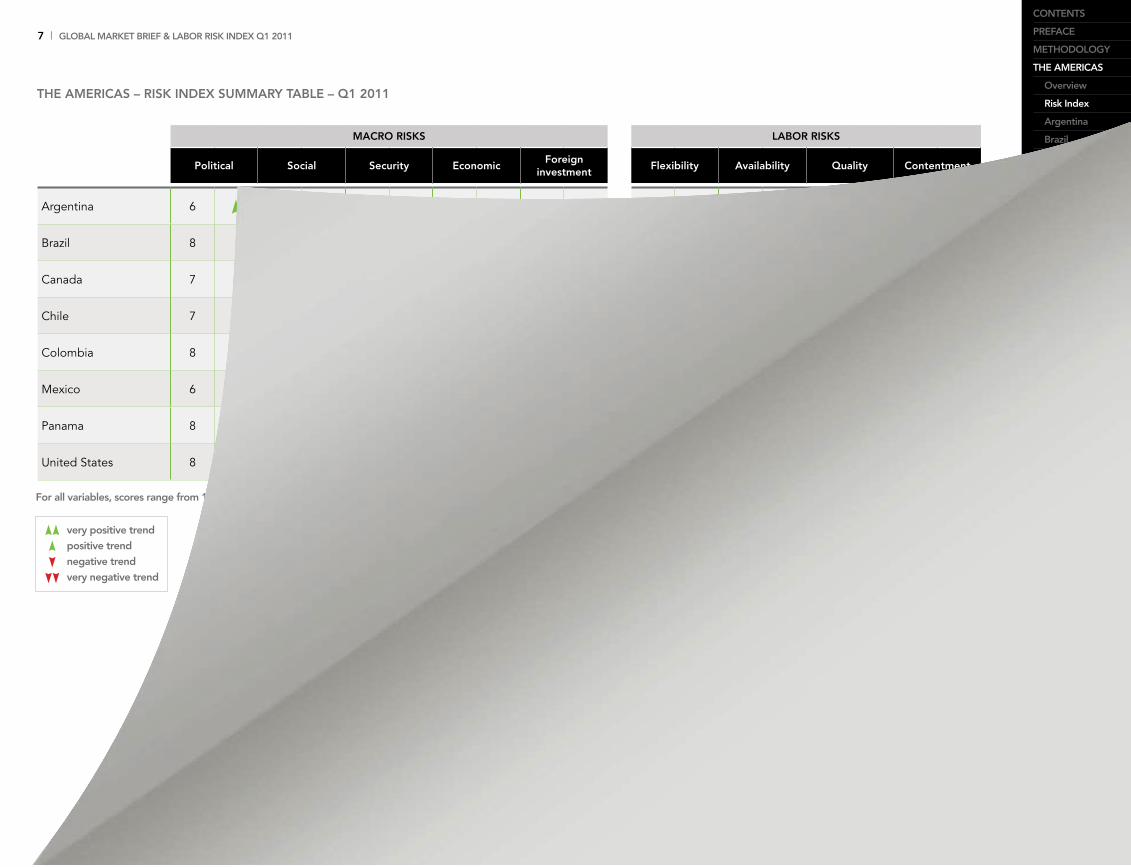

The americas – risk index summary TaBle – Q1 2011

macro risks laBor risks

political social security economicForeign

investmentFlexibility availability Quality contentment

Argentina 6 X 7 8 4 X 5 5 4 7 4

Brazil 8 6 6 X 7 5 X 4 5 5 6

Canada 7 8 10 5 Y 8 7 7 9 5

Chile 7 6 9 7 X 7 7 5 8 6 Y

Colombia 8 5 3 6 Y 6 7 6 X 6 5

Mexico 6 6 5 Y 6 X 7 5 5 6 7

Panama 8 Y 6 7 6 7 4 4 5 4

United States 8 X 8 9 8 X 9 8 9 9 7

8 | gloBal markeT BrieF & laBor risk index Q1 2011

very positive trend

positive trend

negative trend

very negative trend

current quarter

prior quarter

current quarter

prior quarter

low risk

high risk

In an effort to control the pace of current expenditure growth, Rousseff will push for approval of a reform that would limit the real rate of public servant salary increases to 2.5% per year. Wages for public servants have risen at an unsustainable pace in recent years, and Rousseff ’s economic team believes restraining such growth is crucial to its efforts to roll back the pace of spending and executing other government priorities such as increasing public investment.

Brazil

0

1

2

3

4

5

6

7

8

9

10

Political Social Security

MACRO RISKS LABOR RISKS

Economic Foreign Investment

Flexibility Availability Quality Contentment

NXÇÅ

conTenTs

preFace

meThodology

The americas

overview

risk index

argentina

Brazil

canada

chile

colombia

mexico

panama

united states

asia paciFic

europe and eurasia

middle easT and aFrica

aBouT sponsors

in the first quarter of 2011. But

more moderate growth projections

of 4.5% for 2011, coupled with

President Dilma Rousseff’s

commitment to more austere fiscal

policies for this year, could detract

from labor’s negotiating power.

A key policy decision that will affect

wage pressure is the debate over

the minimum wage. Government

economists view the minimum wage

as a driver for inflation in service

sector wages. Despite the fact

that fewer workers in the country’s

more prosperous southern region

are actually paid the minimum

wage, any increases have a ripple

effect at the higher end of the

➔ Economic growth in

2010 likely exceeded earlier GDP

growth forecasts of 7.5%, while the

central bank increased its inflation

expectations for the year from 5.85%

to 5.88% in a survey released on

17 December. Sectors as varied

as finance, engineering, and

construction are experiencing labor

shortages, helping push down the

unemployment rate in November

to a record low of 5.7%, from 6.1%

in October. All of these factors

will contribute to labor pressure

for significant real wage increases

pay scale. Rousseff will likely

restrain the minimum wage hike

for 2011, or grant a small real

increase in exchange for a smaller

amount in 2012.

Nonetheless, the overall context of

high growth and labor shortages

will favor labor in wage negotiations

during Rousseff’s first year in office.

Private companies will continue

to struggle to find adequate labor

supply, while the government

will move forward with ambitious

infrastructure projects, potentially

further strengthening labor’s hand.

■ ■ ■

9 | gloBal markeT BrieF & laBor risk index Q1 2011

very positive trend

positive trend

negative trend

very negative trend

current quarter

prior quarter

current quarter

prior quarter

low risk

high risk

The federal deficit—around 9% of GDP—will constrain the ability of the government to provide additional stimulus in 2011. Republicans won control of the House of Representatives in part by pledging to cut spending; both sides are wary of adding to the deficit given public concern. As a result, Congress is unlikely to pass additional stimulus—and may begin to cut programs—given political concern about the US fiscal position.

0

1

2

3

4

5

6

7

8

9

10

Political Social Security

MACRO RISKS LABOR RISKS

Economic Foreign Investment

Flexibility Availability Quality Contentment

NXÇÅ

conTenTs

preFace

meThodology

The americas

overview

risk index

argentina

Brazil

canada

chile

colombia

mexico

panama

united states

asia paciFic

europe and eurasia

middle easT and aFrica

aBouT sponsors

United States forecasts. Before the tax deal was

reached, the consensus forecast was

for 2.6% growth and it is now firmly

over 3%.

The unemployment insurance

extension ($56 billion) and payroll

tax cut ($112 billion) will provide

an immediate infusion of cash to

consumers. The unemployed tend

to spend their money right away

on basic goods, while workers

will see more money in their

paychecks as a result of reduced

Social Security withholding. A

worker earning $50,000 could see

as much as $1,000 more this year,

while someone earning twice that

much would see around $2,000.

➔ Congress’s approval of an

$858 billion tax-cut compromise

negotiated between President

Barack Obama and Republicans

in December spurred the upward

revision of forecasts for 2011

economic growth. In return for a

two-year extension of the Bush-era

tax cuts, Obama secured 13 extra

months of unemployment insurance

as well as a one-year payroll tax cut

for workers, from 6.2% to 4.2%. Both

measures were unexpected and

their stimulative nature resulted in

most economists upping their 2011

This provision makes an incremental

difference in each paycheck, which

makes it more likely to be spent

right away.

On other indicators, forecasts are

holding steady. Unemployment

dropped to 9.4% in December 2010

and is expected to fall slightly in

2011. The Federal Reserve is likely

to keep its Federal Funds target rate

between zero and 0.25%, and it

said in a 14 December statement

that the recovery has been

disappointingly slow. Inflation is

projected to stay below 2%.

■ ■ ■

10 | gloBal markeT BrieF & laBor risk index Q1 2011

Overview: Asia Pacific

conTenTs

preFace

meThodology

The americas

asia paciFic

overview

risk index

australia

china

hong kong

india

indonesia

Japan

malaysia

new Zealand

philippines

singapore

south korea

sri lanka

Thailand

Vietnam

europe and eurasia

middle easT and aFrica

aBouT sponsors

countries such as Indonesia and the

Philippines are still contemplating

action, while Thailand maintains

price caps on certain food

essentials and commodities.

This bout of inflation is the

consequence of robust growth

in much of the region last year.

Healthy domestic demand, rising

commodity prices, and stimulus

initiatives buoyed regional growth.

China continues to lead the way,

but countries ranging from South

Korea to Australia also put up solid

growth numbers in 2010. Although

countries are projecting lower

growth rates for 2011, the slowdown

so far seems modest. The question

for this year, then, is whether Asia

will remain a global growth engine.

➔ With the notable exceptions

of Japan and New Zealand,

numerous Asia-Pacific countries are

beset by inflationary pressures and

expectations at the outset of 2011.

As a result, the policy emphasis—at

least in the first quarter—will

focus more intensively on taming

inflation, especially in countries

that have large, poor populations.

While China has already hiked

interest rates twice, Southeast Asian

A bright spot for growth appears

to be continued investment

and upgrading of infrastructure,

particularly in Southeast Asia,

China, and India. Malaysia and

Indonesia, for instance, want to

vigorously jumpstart investment

in infrastructure, as their current

deficiencies could eventually limit

economic activity. For Beijing, its

massive investment in rail projects,

including high-speed lines, will

proceed apace, with an estimated

$100 billion in 2011. These projects

will provide a new source of jobs

at a time when some countries are

facing upward wage pressures in

traditional manufacturing sectors.

■ ■ ■

11 | gloBal markeT BrieF & laBor risk index Q1 2011

conTenTs

preFace

meThodology

The americas

asia paciFic

overview

risk index

australia

china

hong kong

india

indonesia

Japan

malaysia

new Zealand

philippines

singapore

south korea

sri lanka

Thailand

Vietnam

europe and eurasia

middle easT and aFrica

aBouT sponsors

very positive trend

positive trend

negative trend

very negative trend

For all variables, scores range from 1 to 10, where 1 is ‘high risk’ and 10 is ‘low risk’.

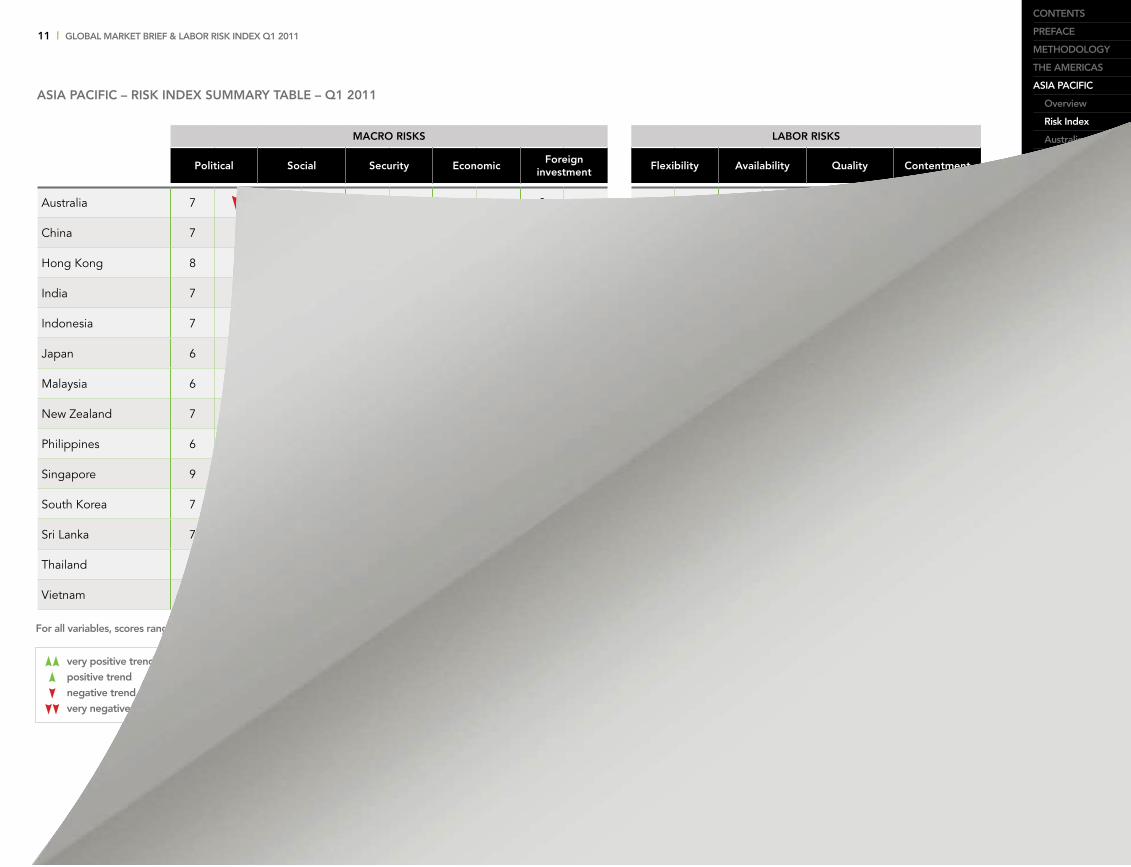

asia paciFic – risk index summary TaBle – Q1 2011

macro risks laBor risks

political social security economicForeign

investmentFlexibility availability Quality contentment

Australia 7 Y 9 9 8 9 8 7 9 8

China 7 5 8 7 Y 6 4 X 6 Y 6 5

Hong Kong 8 7 10 7 Y 10 7 6 Y 8 7

India 7 4 7 6 XX 5 5 5 1 3

Indonesia 7 6 7 5 4 3 5 3 4 YJapan 6 9 9 Y 5 7 5 6 8 Y 7

Malaysia 6 Y 4 9 6 7 6 4 6 6

New Zealand 7 9 10 6 8 7 7 8 7 YPhilippines 6 X 4 7 5 X 4 4 5 4 6

Singapore 9 8 9 8 10 6 5 Y 8 8

South Korea 7 9 6 Y 7 7 3 5 7 6 XSri Lanka 7 X 4 8 5 X 5 6 4 5 5 YThailand 5 Y 4 7 5 7 7 5 4 8

Vietnam 7 X 5 8 4 5 6 5 4 6 Y

12 | gloBal markeT BrieF & laBor risk index Q1 2011

very positive trend

positive trend

negative trend

very negative trend

current quarter

prior quarter

current quarter

prior quarter

low risk

high risk

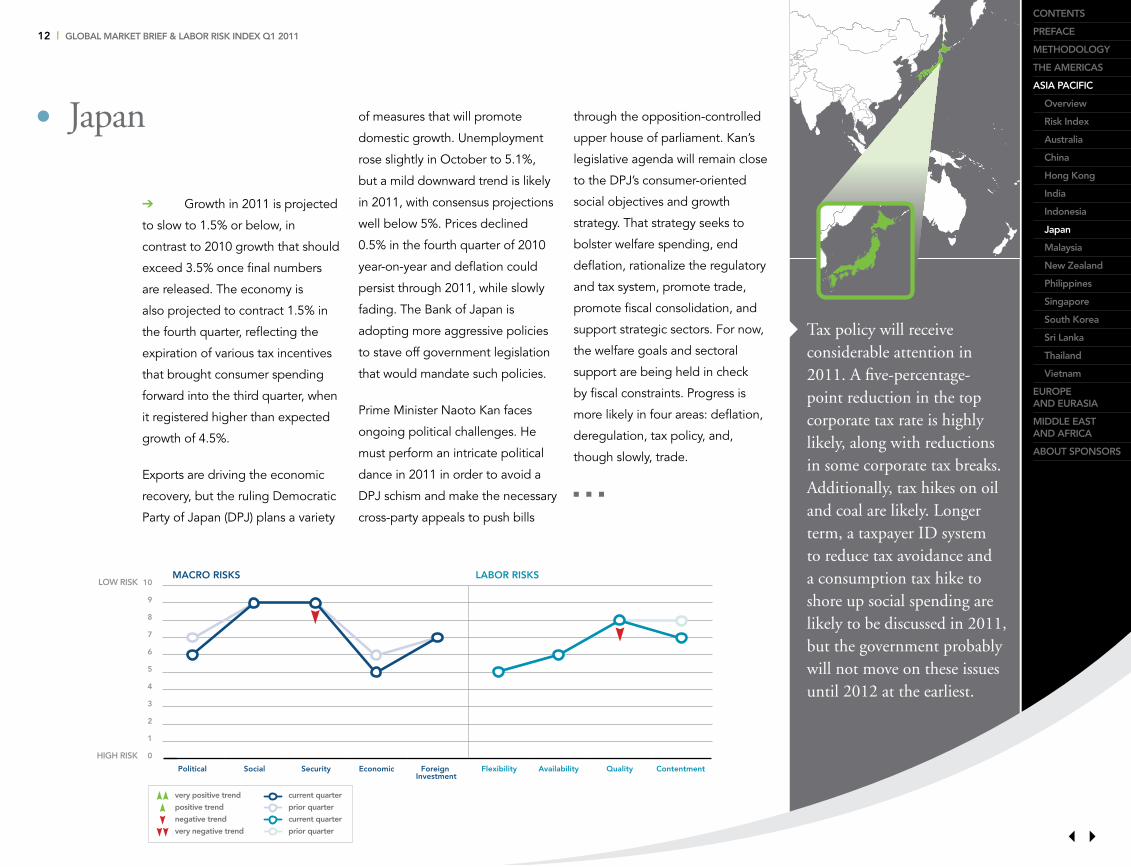

Tax policy will receive considerable attention in 2011. A five-percentage-point reduction in the top corporate tax rate is highly likely, along with reductions in some corporate tax breaks. Additionally, tax hikes on oil and coal are likely. Longer term, a taxpayer ID system to reduce tax avoidance and a consumption tax hike to shore up social spending are likely to be discussed in 2011, but the government probably will not move on these issues until 2012 at the earliest.

0

1

2

3

4

5

6

7

8

9

10

Political Social Security

MACRO RISKS LABOR RISKS

Economic Foreign Investment

Flexibility Availability Quality Contentment

NXÇÅ

conTenTs

preFace

meThodology

The americas

asia paciFic

overview

risk index

australia

china

hong kong

india

indonesia

Japan

malaysia

new Zealand

philippines

singapore

south korea

sri lanka

Thailand

Vietnam

europe and eurasia

middle easT and aFrica

aBouT sponsors

Japan of measures that will promote

domestic growth. Unemployment

rose slightly in October to 5.1%,

but a mild downward trend is likely

in 2011, with consensus projections

well below 5%. Prices declined

0.5% in the fourth quarter of 2010

year-on-year and deflation could

persist through 2011, while slowly

fading. The Bank of Japan is

adopting more aggressive policies

to stave off government legislation

that would mandate such policies.

Prime Minister Naoto Kan faces

ongoing political challenges. He

must perform an intricate political

dance in 2011 in order to avoid a

DPJ schism and make the necessary

cross-party appeals to push bills

➔ Growth in 2011 is projected

to slow to 1.5% or below, in

contrast to 2010 growth that should

exceed 3.5% once final numbers

are released. The economy is

also projected to contract 1.5% in

the fourth quarter, reflecting the

expiration of various tax incentives

that brought consumer spending

forward into the third quarter, when

it registered higher than expected

growth of 4.5%.

Exports are driving the economic

recovery, but the ruling Democratic

Party of Japan (DPJ) plans a variety

through the opposition-controlled

upper house of parliament. Kan’s

legislative agenda will remain close

to the DPJ’s consumer-oriented

social objectives and growth

strategy. That strategy seeks to

bolster welfare spending, end

deflation, rationalize the regulatory

and tax system, promote trade,

promote fiscal consolidation, and

support strategic sectors. For now,

the welfare goals and sectoral

support are being held in check

by fiscal constraints. Progress is

more likely in four areas: deflation,

deregulation, tax policy, and,

though slowly, trade.

■ ■ ■

13 | gloBal markeT BrieF & laBor risk index Q1 2011

very positive trend

positive trend

negative trend

very negative trend

current quarter

prior quarter

current quarter

prior quarter

low risk

high risk

General elections scheduled for 2011 may reignite political turmoil. If allies of former prime minister Thaksin Shinawatra poll well ahead of the election, then speculation will mount about the military’s reaction. It may, with the help of the current civilian government, find a way to maneuver an election defeat for Thaksin’s allies or even prevent the election from taking place. Any sense that the government was undermining the elections would likely bring the opposition out into the streets in large numbers.

Thailand

0

1

2

3

4

5

6

7

8

9

10

Political Social Security

MACRO RISKS LABOR RISKS

Economic Foreign Investment

Flexibility Availability Quality Contentment

NXÇÅ

conTenTs

preFace

meThodology

The americas

asia paciFic

overview

risk index

australia

china

hong kong

india

indonesia

Japan

malaysia

new Zealand

philippines

singapore

south korea

sri lanka

Thailand

Vietnam

europe and eurasia

middle easT and aFrica

aBouT sponsors

higher inflation in the first quarter.

First, a tight labor market led to

wage hikes in early December,

when the government granted

an increase in the daily minimum

wage by an average of 6.7%

nationwide to 176.30 baht ($5.84).

The move, which was largely

politically motivated, will further

add to investor complaints of

rising labor costs in Thailand.

Second, manufacturers in industries

such as auto batteries, electrical

wires, steel, chemical fertilizer,

palm oil for cooking, and pork,

submitted applications for price

hikes ranging from 3% to 25%.

The government sets price caps

for several types of basic goods

➔ Thailand’s exports surged

in November, raising expectations

that exports for 2010 could reach

$90 billion, about 27% more than

2009 and almost 10% more than

2008, before the financial crisis

fully hit Western demand. The

export sector’s strong performance

will help Thailand reach 8%

growth for 2010. With economic

expansion remaining robust, the

government’s attention is likely to

turn to rising prices.

Two factors could contribute to

and commodities, so these firms

need administrative approval to

raise them. The government, facing

possible elections and worried

that rising inflation might force it

to raise interest rates (which would

further strengthen the baht), will

likely freeze the prices of several

products (or allow for only minimal

increases). But the manufacturers’

requests reflect the wider price

pressures in the economy. The

higher prices may eventually cause

Thai authorities to raise interest

rates, which could slow demand in

the industrial sector and weaken the

outlook for manufacturing jobs.

■ ■ ■

14 | gloBal markeT BrieF & laBor risk index Q1 2011

Overview:Europe and Eurasia

conTenTs

preFace

meThodology

The americas

asia paciFic

europe and eurasia

overview

risk index

Baltics

Belgium

Bulgaria

czech republic

denmark

France

germany

hungary

ireland

italy

luxembourg

netherlands

norway

poland

portugal

romania

russia

spain

sweden

switzerland

Turkey

ukraine

united kingdom

middle easT and aFrica

aBouT sponsors

likely increase social unrest

and political instability in the

European periphery (Greece,

Ireland, Spain, and Portugal).

Meanwhile, Germany’s export-

based growth will continue to

make it the economic locomotive

of the continent, with some help

from the Nordic nations. Eastern

Europe presents a mixed outlook.

While economic prospects are

positive for almost all countries,

these are dependent upon the

wider eurozone. Therefore, poor

performance in some western

European economies might

undermine growth momentum

in the entire region. Moreover,

unemployment will remain

elevated and economic measures

taken by countries such as

➔ The situation in Europe

will remain complicated. Many

countries will enact austerity

measures that will not support

growth and employment.

Furthermore, several governments

will likely face funding constraints

in financial markets, which might

prompt the activation of additional

EU/IMF rescue packages, requiring

further cuts.

The implementation of structural

reforms in areas such as labor

regulations and pensions will

Hungary might undermine

investor confidence.

In contrast, steady growth will likely

boost political stability in Eurasian

countries. In the case of Russia,

the government will face minimal

internal frictions, as the risk of

social unrest that rose following

the financial crisis recedes. Stability

will be also the norm for Turkey

because the government will

try to avoid any move that may

undermine its popularity ahead of

parliamentary election to be held

in June. Finally, Ukraine will likely

also profit from a continued surge

in domestic demand, although a

reform of the labor code might

cause social instability.

■ ■ ■

15 | gloBal markeT BrieF & laBor risk index Q1 2011

conTenTs

preFace

meThodology

The americas

asia paciFic

europe and eurasia

overview

risk index

Baltics

Belgium

Bulgaria

czech republic

denmark

France

germany

hungary

ireland

italy

luxembourg

netherlands

norway

poland

portugal

romania

russia

spain

sweden

switzerland

Turkey

ukraine

united kingdom

middle easT and aFrica

aBouT sponsors

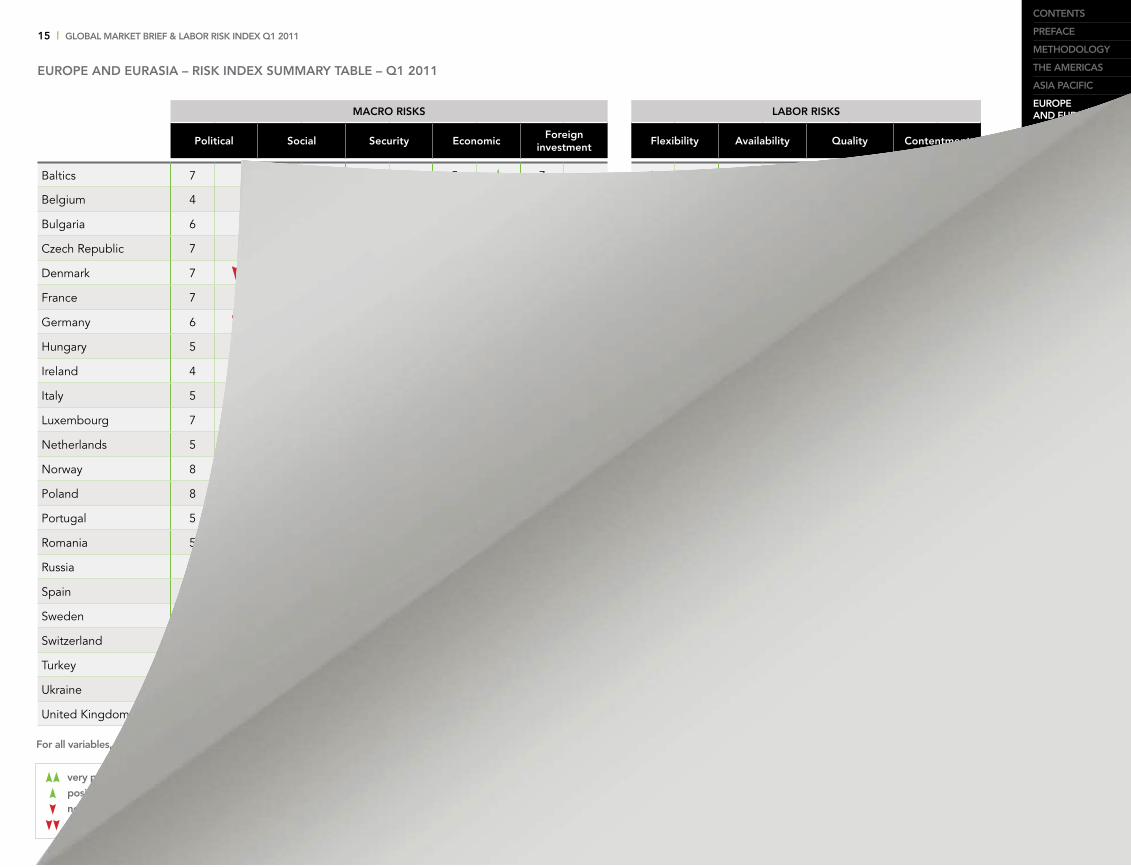

europe and eurasia – risk index summary TaBle – Q1 2011

very positive trend

positive trend

negative trend

very negative trend

For all variables, scores range from 1 to 10, where 1 is ‘high risk’ and 10 is ‘low risk’.

macro risks laBor risks

political social security economicForeign

investmentFlexibility availability Quality contentment

Baltics 7 7 8 5 X 7 5 6 7 4

Belgium 4 6 8 5 Y 7 5 6 7 4

Bulgaria 6 7 7 4 7 6 X 5 6 4

Czech Republic 7 7 Y 9 7 6 8 X 7 7 5

Denmark 7 Y 9 8 6 9 6 5 8 5

France 7 8 7 6 8 4 6 8 3 YGermany 6 Y 9 8 6 8 3 6 9 5

Hungary 5 6 9 4 Y Y 6 Y Y 6 6 7 5

Ireland 4 Y 8 8 4 8 6 7 8 2

Italy 5 Y 8 8 5 6 4 6 7 4

Luxembourg 7 9 8 6 X 9 4 5 9 6

Netherlands 5 7 8 6 8 3 5 Y 7 5

Norway 8 9 8 7 X 8 3 5 8 7

Poland 8 8 9 5 Y 6 Y 6 6 8 5

Portugal 5 Y 8 8 4 Y 7 4 X 6 6 3

Romania 5 6 6 5 X 7 5 5 7 4

Russia 6 5 Y 5 5 6 5 7 5 6

Spain 6 6 7 X 5 7 4 X 7 7 2

Sweden 6 8 8 7 8 4 6 8 6 XSwitzerland 8 9 9 7 Y 8 6 5 9 8

Turkey 6 5 7 7 X 6 5 5 X 5 6

Ukraine 6 5 8 4 X 6 5 6 5 4

United Kingdom 9 8 Y 8 6 9 7 6 Y 9 6 Y

16 | gloBal markeT BrieF & laBor risk index Q1 2011

very positive trend

positive trend

negative trend

very negative trend

current quarter

prior quarter

current quarter

prior quarter

low risk

high risk

conTenTs

preFace

meThodology

The americas

asia paciFic

europe and eurasia

overview

risk index

Baltics

Belgium

Bulgaria

czech republic

denmark

France

germany

hungary

ireland

italy

luxembourg

netherlands

norway

poland

portugal

romania

russia

spain

sweden

switzerland

Turkey

ukraine

united kingdom

middle easT and aFrica

aBouT sponsors

The reforms agreed under the EU/IMF bailout will likely spark more protests from trade unions. The government is expected to adopt new legislation in May to reduce the national minimum wage by €1.00 per hour and reform unemployment and welfare benefits systems. Furthermore, it will also have to present plans to increase state pension eligibility to 66 years in 2014, 67 in 2021, and 68 in 2028.

Ireland

0

1

2

3

4

5

6

7

8

9

10

Political Social Security

MACRO RISKS LABOR RISKS

Economic Foreign Investment

Flexibility Availability Quality Contentment

NXÇÅ

of an economic and financial

adjustment package to correct

Ireland’s significant fiscal deficit of

14.4% of GDP.

These conditions are reflected in

the budget for 2011, which the

parliament is currently discussing

and which will likely be passed

in the first quarter. The four-year

austerity plan includes €15 billion

of budget cuts by 2014, of which

€6 billion (equivalent to about 4%

of GDP) will be implemented as

early as 2011.

The country will probably undergo

a major political shift in 2011.

The ruling Fianna Fail could face

➔ The Irish economy

expanded only 0.5% in the third

quarter of 2010 compared to the

previous quarter after contracting

1% in the previous quarter, and it

continued to have the third highest

unemployment rate in the eurozone

at 14.1% in October. Moreover,

concerns about the solvency of Irish

banks led the government to apply

for external financial assistance in

November. The approval of an €85

billion bailout by the EU and the

IMF was subject to the adoption

a virtual wipeout in this year’s

early elections (which will take

place in late February), while

opposition parties Fine Gael and

Labor will very likely form the next

government. These two parties

have backed the radical fiscal

retrenchment, but insist that they

will not be bound by the strict

terms and conditions attached

to the EU/IMF bailout. A more

significant risk will be the ability

of the new coalition government

to implement the reforms that the

IMF and EU have asked for. The

public backlash against the rescue

package could break the unity of

the incoming government.

■ ■ ■

17 | gloBal markeT BrieF & laBor risk index Q1 2011

very positive trend

positive trend

negative trend

very negative trend

current quarter

prior quarter

current quarter

prior quarter

low risk

high risk

There are many reservations about the government’s proposed labor code, unveiled this fall. Unions argue the law weakens their rights and those of employees and does not meet ILO standards; meanwhile some businesses claim the law expands the rights of employees at their expense. Fears of demonstrations were likely behind the decision to delay consideration until this year. Regardless of whether officials revise the bill in response to the complaints, a vote is likely in the first half of 2011.

Ukraine

0

1

2

3

4

5

6

7

8

9

10

Political Social Security

MACRO RISKS LABOR RISKS

Economic Foreign Investment

Flexibility Availability Quality Contentment

NXÇÅ

conTenTs

preFace

meThodology

The americas

asia paciFic

europe and eurasia

overview

risk index

Baltics

Belgium

Bulgaria

czech republic

denmark

France

germany

hungary

ireland

italy

luxembourg

netherlands

norway

poland

portugal

romania

russia

spain

sweden

switzerland

Turkey

ukraine

united kingdom

middle easT and aFrica

aBouT sponsors

Natural gas tariff increases in the

spring and fall will be one of the

main factors to affect prices. The

IMF will require the National Bank

of Ukraine to further liberalize its

exchange rate policy as part of its

$15 billion loan program with the

government. This will make the

hryvnia potentially more vulnerable

to exchange rate fluctuations.

The government will engage in

a series of reforms in 2011 that

will affect all employers. Tax

reform, which went into effect

on 1 January, is generally

positive for Ukraine’s largest

employers, who will enjoy

lower tax rates, while it is mixed

➔ There is little concern

among outside observers that

Ukraine’s economic recovery will

slow this year. Estimates of GDP

growth range from 3.7% to above

4%. A revival in domestic demand

is expected to continue, a factor

that may help the government

address unemployment

that remains around 9% by

International Labor Organization

(ILO) standards. Inflation will be

lower than before the financial

crisis, but estimates for 2011 are

generally between 10% and 11%.

for small- and medium-sized

enterprises. Protests against the

tax code in November caught

the government by surprise, and

will affect how it approaches

upcoming changes to the pension

system and the labor code.

Nevertheless, these developments

are considered necessary—pension

reform is a requirement of the

IMF loan—and likely will be

implemented in early 2011. Large

and small businesses alike will

be affected by the restructuring,

though the full impact will not

be clear until the cabinet and

parliament finalize the proposals.

■ ■ ■

18 | gloBal markeT BrieF & laBor risk index Q1 2011

Overview:Middle East and Africa

conTenTs

preFace

meThodology

The americas

asia paciFic

europe and eurasia

middle easT and aFrica

overview

risk index

algeria

egypt

israel

kenya

kuwait

morocco

Qatar

saudi arabia

south africa

united arab emirates

aBouT sponsors

countries will benefit from more

robust hydrocarbon exports given

the more stable outlook of the

global economy.

Across Africa and the Middle East,

domestic politics and policies will

drive growth. For instance, Qatar’s

winning bid to host the 2022

FIFA World Cup will help spur the

construction and infrastructure

sectors, as well as the tourism

industry. And in Kenya, effective

monetary policies have supported

economic growth.

But, as recent events have shown,

politics can also delay and even

derail the limited successes that

many of these emerging markets

have achieved. It is unlikely that

➔ The Middle East and

Africa entered 2011 in a profound

state of disarray as protests shook

the region and long-entrenched

dictators wobbled and fell.

Despite this, the two regions are

broadly poised for growth barring

further dislocation. Many of the

energy-dependent economies are

diversifying in order to address

longer-term socioeconomic

concerns such as unemployment.

And in the short term, these

many countries in the Middle

East and Africa will succeed in

addressing structural problems in

2011, such as corruption and the

lack of democracy, and most also

have difficult policy choices to

make. Egypt had weathered the

global financial crisis relatively well,

and was poised to benefit from

the global recovery. But the mid-

January fall of the Tunisian president

pushed rising social discontent

to the fore as protests shook the

regime of President Hosni Mubarak;

the Egyptian stock market tanked

as the military nervously stood

between protesters and the regime.

If Mubarak falls, it will have serious

consequences for Egypt and for the

broader Middle East.

■ ■ ■

19 | gloBal markeT BrieF & laBor risk index Q1 2011

conTenTs

preFace

meThodology

The americas

asia paciFic

europe and eurasia

middle easT and aFrica

overview

risk index

algeria

egypt

israel

kenya

kuwait

morocco

Qatar

saudi arabia

south africa

united arab emirates

aBouT sponsors

very positive trend

positive trend

negative trend

very negative trend

For all variables, scores range from 1 to 10, where 1 is ‘high risk’ and 10 is ‘low risk’.

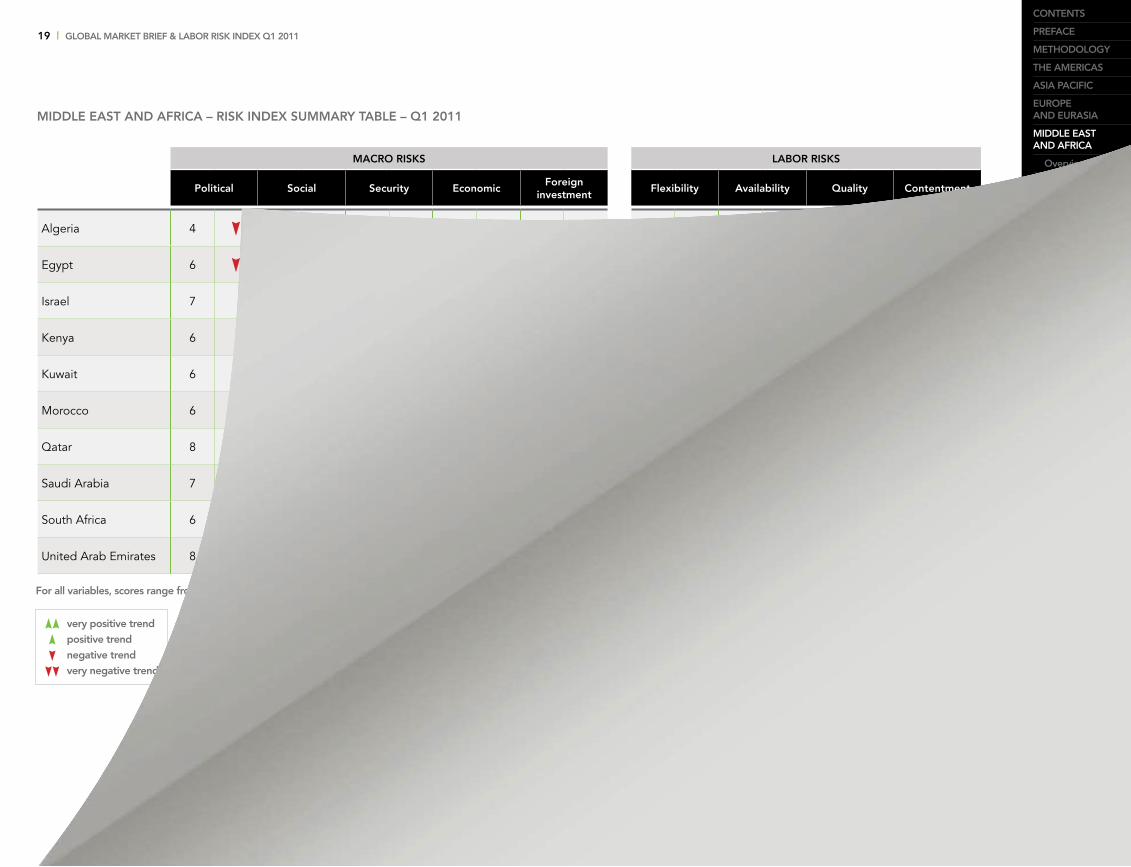

middle easT and aFrica – risk index summary TaBle – Q1 2011

macro risks laBor risks

political social security economicForeign

investmentFlexibility availability Quality contentment

Algeria 4 Y 4 YY 4 Y 3 3 2 5 5 1 Y

Egypt 6 Y 6 YY 8 Y 5 5 4 4 2 2

Israel 7 6 Y 7 7 Y 8 5 6 Y 8 7

Kenya 6 2 X 6 5 X 6 X 6 5 4 4

Kuwait 6 X 6 Y 7 6 5 8 4 7 7 X

Morocco 6 5 Y 8 4 5 3 4 2 4

Qatar 8 X 6 8 7 XX 6 7 5 7 6 Y

Saudi Arabia 7 6 Y 7 6 X 6 7 4 5 5

South Africa 6 Y 3 6 6 X 7 4 Y 7 4 2

United Arab Emirates 8 7 6 7 X 6 X 6 6 7 7 X

20 | gloBal markeT BrieF & laBor risk index Q1 2011

very positive trend

positive trend

negative trend

very negative trend

current quarter

prior quarter

current quarter

prior quarter

low risk

high risk

conTenTs

preFace

meThodology

The americas

asia paciFic

europe and eurasia

middle easT and aFrica

overview

risk index

algeria

egypt

israel

kenya

kuwait

morocco

Qatar

saudi arabia

south africa

united arab emirates

aBouT sponsors

The Netanyahu government is relatively stable. While coalition politics are an ongoing source of policy volatility, a government collapse is unlikely in the near term. Authorities are likely to use this stability to focus on the economy, while avoiding serious engagement in the peace process. If the government does run into trouble, Netanyahu could look to the centrist Kadima party for support, though such a move would necessitate greater engagement in the peace process.

Israel

0

1

2

3

4

5

6

7

8

9

10

Political Social Security

MACRO RISKS LABOR RISKS

Economic Foreign Investment

Flexibility Availability Quality Contentment

NXÇÅ

could stoke inflation and will likely

push the Bank of Israel to raise

interest rates.

Housing prices have soared

dramatically over the last five

years, spurring concerns about a

possible real estate bubble. Prime

Minister Benjamin Netanyahu

recently highlighted the issue,

linking the hike in prices to the

limited supply of land for residential

construction and low interest rates.

The central bank, however, says

there are signs that the housing

boom is slowing. Officials will watch

late 2010 and early 2011 housing

numbers carefully.

➔ Israel’s economic outlook

remains relatively strong, though

growth is expected to be weaker

in 2011 than had been previously

expected. Recent estimates put

GDP growth at 3.2%, more than

one percentage point down from

the 4.5% estimated for 2010.

There are two causes for the

moderate slowdown: Slower

growth of the global economy is

adversely affecting export growth (a

principal driver of Israel’s economy),

while a developing housing bubble

Illegal immigration will remain an

important political issue, with the

number of Africans crossing into

Israel from Egypt likely to increase

beyond the current 13,000 per

year. These illegal laborers are

needed in the southern resorts and

in construction work, but the calls

for curbing migrants will grow as

the unemployment rate is at 6.6%,

high by Israeli standards. Efforts

in 2010 to reform employment

and labor laws will continue in

2011, but will remain contentious.

Nevertheless, the central bank

expects unemployment to return to

the 5%–6% range in 2011.

■ ■ ■

21 | gloBal markeT BrieF & laBor risk index Q1 2011

very positive trend

positive trend

negative trend

very negative trend

current quarter

prior quarter

current quarter

prior quarter

low risk

high risk

Qatar will spend about $57 billion over the next decade for infrastructure developments related to the 2022 World Cup. Project work in preparation for the event presents a lucrative investment opportunity for large-scale multinationals. The infrastructure, hospitality, and real estate sectors are expected to be the biggest beneficiaries. Over the next few years there will be an incremental rise in the number of migrant construction workers. Market research and financial feasibility studies for pipeline projects are expected to begin in 2011.

Qatar

0

1

2

3

4

5

6

7

8

9

10

Political Social Security

MACRO RISKS LABOR RISKS

Economic Foreign Investment

Flexibility Availability Quality Contentment

NXÇÅ

conTenTs

preFace

meThodology

The americas

asia paciFic

europe and eurasia

middle easT and aFrica

overview

risk index

algeria

egypt

israel

kenya

kuwait

morocco

Qatar

saudi arabia

south africa

united arab emirates

aBouT sponsors

State spending for the fiscal

year 2010–2011, which started

in April, is expected to increase

to $32.4 billion. Expenditure on

infrastructure projects is projected

to account for 40% of the budget

through 2016.

Human capital development will

likely be a central theme in the

government’s future economic

and social development policy. In

the first quarter of 2011, Qatar is

expected to accelerate the rollout

of its National Development

Strategy (2011–2016). Building

domestic labor capacity, expanding

the private sector’s role in the

economy, and facilitating the

growth of entrepreneurship

➔ Qatar’s economic prosperity

continues to exceed market

expectations. GDP is projected

to grow 18.5% in 2010 and 20%

in 2011. Natural gas continues to

play a critical role in the country’s

economic plans with LNG

production capacity reaching

77 million tons per year. In 2011,

the government will likely expand

economic diversification projects

to enlarge the non-oil and gas

sector share of GDP (particularly

in finance, industry, construction,

and real estate).

and small- and medium-sized

enterprises will represent tangible

challenges. Government policy

will continue to emphasize the

expansion of educational and

research institutions along with on-

the-job training programs.

Labor laws are currently under

review, but no change is expected

in 2011. The sponsorship system,

which restricts job transfers

without consent of the current

employer, remains the foundation

for employment contracts. Qatar’s

successful 2022 soccer World

Cup bid will heighten pressure to

modernize the legal code, although

no changes are anticipated in 2011.

■ ■ ■

22 | gloBal markeT BrieF & laBor risk index Q1 2011

About this Report

The Global Market Brief & Labor Risk Index is jointly developed by KellyOCG, the Outsourcing and Consulting Group of human resources provider,

Kelly Services and Eurasia Group, the global political risk consultancy. The report, a proprietary blend leveraging Kelly’s labor market knowledge with

Eurasia Group’s expertise in political and socio-economic risk analysis, delivers a groundbreaking resource for companies as they assess market

investments and global labor strategies.

Published on a quarterly basis, the Global Market Brief & Labor Risk Index is segmented by four geographies: the Americas, Asia-Pacific, Europe and Eurasia,

and the Middle East and Africa, with detailed insights for 55 of the world’s most important economies.

About Eurasia Group

Eurasia Group is the world’s leading global political risk research and consulting firm. Since 1998, it has helped clients make informed business decisions in

countries where understanding the political landscape is critical. The firm’s research analysts are trained social scientists with post-graduate degrees, extensive

professional experience, and a diverse range of language capabilities. Headquartered in New York, it also has offices in Washington and London, as well as a

network of experts around the world. For more information, please visit www.eurasiagroup.net.

About KellyOCG

KellyOCG is the Outsourcing and Consulting Group of Fortune 500 human resources solutions provider, Kelly Services, Inc. KellyOCG is a global leader in

innovative talent management solutions in the areas of Recruitment Process Outsourcing (RPO), Business Process Outsourcing (BPO), Contingent Workforce

Outsourcing (CWO), including Independent Contractor Solutions, Human Resources Consulting, Career Transition and Organizational Effectiveness, and

Executive Search. Visit www.kellyocg.com.

To Receive this Report

This report is available on an annual subscription basis. To access a complimentary report abstract, and for full subscription details, visit www.kellyocg.com/marketbrief

More Information

To find out more about how the KellyOCG / Eurasia Group partnership can add insight to your global planning, please contact [email protected]

Related Documents