Study on Indian Initial Public Offering (IPO) market and its Regulatory aspect with reference to Religare Securities Ltd Project report Submitted in Partial Fulfillment of the Requirements and for the award of Degree of Post Graduate Diploma in Management (PGDM) BY RADHE SHYAM LAL (Registration No. 09/042) Institute of Computer & Business Management School of Business Excellence Member ACBSE Approved by AICTE Govt. Of India

Project Report on Indian IPO Special Reference With Religare Securites

Nov 29, 2014

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Study on Indian Initial Public Offering (IPO) market and its Regulatory aspect with reference to Religare Securities Ltd

Project report

Submitted in Partial Fulfillment of theRequirements and for the award of Degree of

Post Graduate Diploma in Management(PGDM)

BY

RADHE SHYAM LAL(Registration No. 09/042)

Institute of Computer & Business ManagementSchool of Business Excellence

Member ACBSE

Approved by AICTE Govt. Of India

HYDERABAD-500048

ACKNOWLEDGEMENT

I owe a great many thanks to a great many people who helped and supported me

during the writing of this book.

First of all I would like to convey my sincere gratitude to Dr. S. Zarar and

Mrs. Ritu Zarar, Principal and chairman (Institute for Computers and

Business Management) for their unprecedented support and giving me an

opportunity to do my summer internship program at RELIGARE SECURITIES

LTD, which has been a pure learning experience and has enlightened my

knowledge and skills about financial aspect.

I would also like to express my gratitude to Prof. Jitender Govindani,

Administrative Director, Institute of Computers and Business Management

and my special thanks to finance faculty and my mentor Mr. Ramesh Babu Sir

and Mrs. Annie Kavita Ma’am for his outstanding and undeniable

considerations. I would also like to thank all my friends who have bore with me

during this project, apart from that, those who have helped up in to some way or

the other. Last but not the least I would like to extend my heartfelt thanks to my

parent, who were with me when I was some expensive about the project. Their

help and encouragement also proved to be a handful.

I express my gratefulness to the Mr. Praveen Mahendraker, “associate Vice

President – Investment Banking” in Religare Capital Markets Limited in

Hyderabad for their valuable suggestion, constant encouragement, silent

support & unwavering confidence, without which this project would not have

been possible. It was they who motivated for this cause (to do something

entirely new) and always was present with their expert guidance and disciplined

ideas.

Radhe Shyam Lal

DECLARATION

I hereby declare that the project on “Study on Indian Initial Public Offering (IPO) market and its Regulatory aspect with reference to Religare Securities Ltd in Hyderabad” is completely my work. It has been submitted to ICBM-SCHOOL OF BUSINESS EXCELLENCE for partial fulfillment of the educational session and allotment of marks.

Radhe shyam lal09/42

CERTIFICATE FROM THE ORGANIZATION

CONTENT

SR.NO PARTICULAR PAGE. NO

1 1.1 Introduction 1.2 Objectives of the Project 1.3 Research Methodology 1.4 Scope of the Project 1.5 Limitation 1.6 Review of Literature

1-2345 67

2 INDUSTRY PROFILE 2.1 Initial Public Offer 2.2 SEBI (Regulatory Aspect) 2.3 NSE 2.4 BSE

88-1011-1213-1415-16

3 COMPANY PROFILE 3.1 Name of the Organization 3.2 History and background 3.3 Group structure 3.4 About Religare Sec. limited 3.5 The Religare Edge 3.6 Company IPO

1717181920-2121-2223

4 Indian IPO market 4.1 IPO overview 4.2 Process of IPO 4.3 Role of Regulatory Aspect 4.3.1 SEBI

4.3.2 NSE 4.3.3 BSE

2425-2627-3334-51

5 Data Analysis and interpretation 52-64

6 Conclusion 6.1 Findings 6.2 Suggestions

6566-6768

7 BIBLIOGRAPHY 69

8 ANNEXURE 70-77

INTRODUCTION

This report, as the title “Public issue” suggests, is an attempt to bring forth the

importance of the process of Issue of an Initial Public Offer (IPO).

When a Company issues an IPO, it means it is going public. The issue of an IPO introduces a great degree of transparency in a Company’s operations. All the relevant and updated information pertaining to the company is laid down before the investors so that they may make an investment decision. Again, there are set procedures, rules, regulations and laws to be followed in laying down this information before the investors. A document called the ‘Prospectus’ must be prepared. The Prospectus captures all the necessary information that is to be made available to the investors. Apart from the Prospectus, there are various other company documents that need to be verified and summarized in order to present them before the investors.

Many Intermediaries are appointed for the purpose of managing the public

issue of an IPO of a company. They play a vital role by co-ordinating the

activities of the company, the Regulatory Bodies and Investors. The

following are the responsibilities:

Company, to manage the entire process of issue of its IPO, and to

present the Company’s information before the investors in a concise

and unambiguous form.

Investors, to give them all the relevant and updated information on the

Company, while at the same time protecting their interests

Regulatory Bodies such as the Securities and Exchange Board of

India, to adhere to all secretarial and legal work.

In order to fulfill all their responsibilities well, they must work

diligently. The process through which they verify and summarize the

Company’s information is thus called the process of Due Diligence.

-1-

These Intermediaries must issue “Due Diligence Certificates” at various

points during the issue process, saying that the company documents have

all been verified and are correct.

This report will take the reader through the entire process of the

Issue of an IPO and will lay special emphasis on the dynamic role played

by them.

This report aims at highlighting the key points about an IPO issue by

separating the concrete points regarding an issue from the frills, and

focusing on these concrete points.

-2-

Objectives of the Project

To study and analysis the Indian initial public offering (IPO) market and

Role of its regulatory aspect.

To study and understand the concept of and procedure, problem, benefits,

involved in Initial Public Offers (IPO’s).

To understand the role of intermediaries in managing Initial Public

Offers.

To know various services offered by religare securities.

To study risks faced by investor in primary market.

-3-

Scope of the Project

The following report is an attempt to analyses thoroughly, the behavior and

dynamics of Initial Public Offerings market in India. In other words, it’s a

detailed study on the Primary and secondary Market in India. A long with study

on IPO process and its regulatory aspect. This study takes into account Public

Offerings made by major companies in various sectors, in a period ranging of

last few year. The sectors taken into consideration are-

a) Industrials

b) Consumer goods & retail

c) Technology , media & Telecommunication

d) Real Estate & infrastructure

e) Banking, financial Services & insurance

f) Healthcare & life sciences

g) Power and Energy

The study analyses the behavior of public offerings of companies within each

sector and also attempts to make a comparative analysis among the sectors,

with the purpose of gauging investor preference. Over subscription and under

subscription analysis determines the investor preference at the time of issue.

-4-

Research Methodology

Sources of Study

The data for the project has been collected from both primary and

secondary sources.

Primary data has been collected by:

Consulting the officials “associate Vice President – Investment Banking”

in Religare Capital Markets Limited in Hyderabad.

Also, IPO prospectus and all the necessary documents required for, and

furnished by, the companies for managing the issue of IPO’s and IPO

process have been used as primary data.

Secondary data

It includes, information secured from web sites, magazines and the daily

experience, observations and through newspapers.

Books related to Financial Management.

Web sites were used as the vital information source.

-5-

Limitations of the project

Although Initial Public Offers are issued by many companies, this study is confined to a few companies only. These are companies that fall within limited company.

This study will be limited to the information willingly shared by the

authorities and of RSL.

To understand the overall India IPO market, the period of 45 days is not enough, so finding cannot be generalized for all times.

The data followed in project is partly based on Secondary information and it can’t be held true as 100% correct.

The scope of the study is very vast. It is very difficult to cover and focus on all the areas. Therefore an attempt is made to cover as much as possible.

-6-

Review of Literature

IPO – INITIAL PUBLIC OFFERING is the hottest topic in the current industry, mainly because of India being a developing country and lot of growth in various sectors which leads a country to ultimate success. And when we talk about country’s growth which is dependent on the kind of work and how much importance to which sector is given. And when we say or talk about industries growth which leads the economy of country has to be balanced and given proper finance so as to reach the levels to fulfill the needs of the society. And industries which have massive outflow of work and a big portfolio then its very difficult for any company to work with limited finance and this is where IPO plays an important role.

This report talks about how IPO helps in raising fund for the companies going public, what are its pros and cons, and also it gives us detailed idea why companies go public. How and what are the steps taken by the companies before going for any IPO and also the role of (SEBI) Securities and Exchange Board of India the BSE and NSE , what are primary and secondary markets and also the important terms related to IPO. It gives us idea of how IPO is driven in the market and what are various factors taken into consideration before going for an IPO. And it also tells us how we can more or less judge a good IPO.

IPO has been one of the most important generators of funds for the small companies making them big and given a new vision in past and it is still continuing its work and also for many coming years.

-7-

INDUSTRY PROFILE

INDIAN IPO MARKET

HISTORY

The term initial public offering (IPO) slipped into everyday speech during the tech bull market of the late 1990s. Back then, it seemed you couldn't go a day without hearing about a dozen new dotcom millionaires in Silicon Valley who were cashing in on their latest IPO. The phenomenon spawned the term siliconaire, which described the dotcom entrepreneurs in their early 20s and 30s who suddenly found themselves living large on the proceeds from their internet companies' IPOs.

INVESTORS are still wary of equities in the 1990s, to blame are the excesses in the primary market in the 1990s. Of the thousands of IPOs (initial public offerings) and offers for sale made between 1994 and 1996, less than a hundred were from companies with track record. Even in this shortlist, only a few managed to complete planned projects and deliver value to investors. The rest just frittered the money away.

The primary market of the mid-1990s was merely used as a channel to move public funds into private hands. The Securities and Exchange Board of India (SEBI) was late to wake up to the excesses, but when it did, it improved the disclosure framework, tightened the prerequisites for an IPO, and towards the end of the decade, introduced book-building.

-8-

CURRENT POSITION OF INDIAN IPO MARKET

India is being lauded as the savior of the ailing global IPO market with $3.3 billion worth of proceeds from eight deals. This makes India the largest IPO market in the world so far this year.

India accounts for 49.1% of global IPO proceeds at the moment, compared to just 3.7% same time last year. Significant, given that global IPOs declined 36.1% over the last one year.

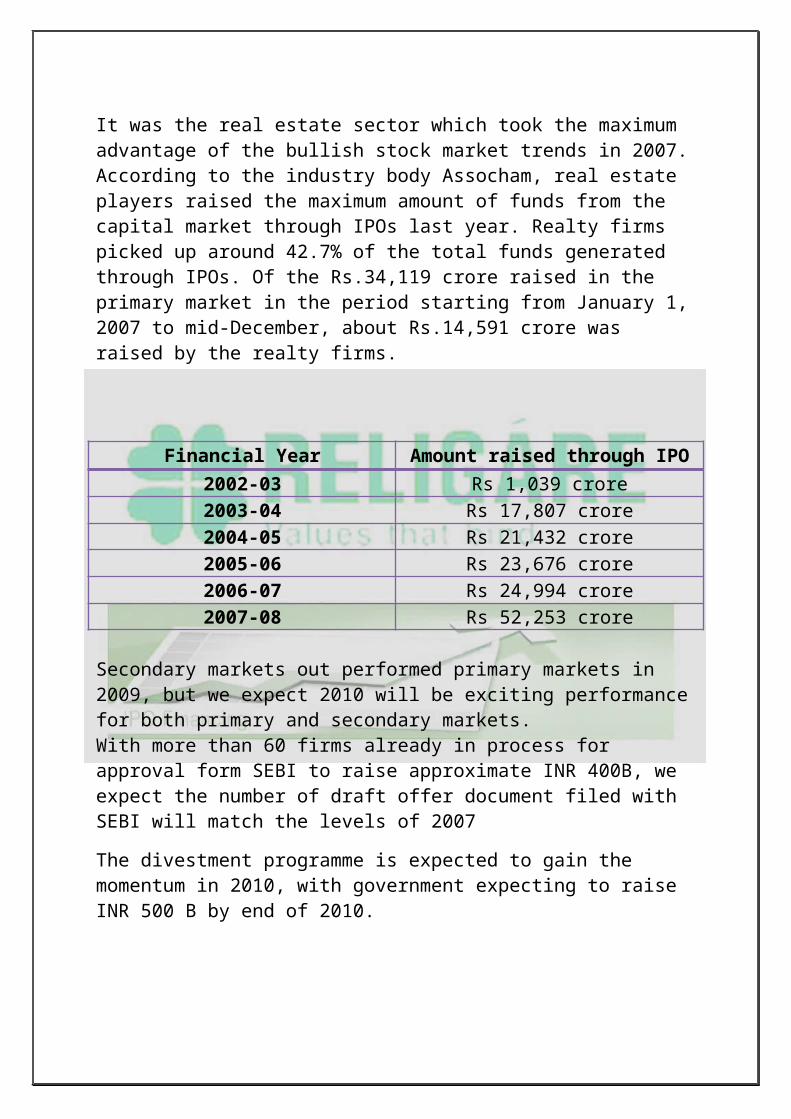

It was the real estate sector which took the maximum advantage of the bullish stock market trends in 2007. According to the industry body Assocham, real estate players raised the maximum amount of funds from the capital market through IPOs last year. Realty firms picked up around 42.7% of the total funds generated through IPOs. Of the Rs.34,119 crore raised in the primary market in the period starting from January 1, 2007 to mid-December, about Rs.14,591 crore was raised by the realty firms.

Financial Year Amount raised through IPO2002-03 Rs 1,039 crore2003-04 Rs 17,807 crore2004-05 Rs 21,432 crore2005-06 Rs 23,676 crore2006-07 Rs 24,994 crore2007-08 Rs 52,253 crore

Secondary markets out performed primary markets in 2009, but we expect 2010 will be exciting performance for both primary and secondary markets.With more than 60 firms already in process for approval form SEBI to raise approximate INR 400B, we expect the number of draft offer document filed with SEBI will match the levels of 2007

The divestment programme is expected to gain the momentum in 2010, with government expecting to raise INR 500 B by end of 2010.

-9-

2010 will see the IPOs of BSNL and RITES and FPO of SAIL.With the handy increase in liquidity in market and stabilization in secondary markets, the companies will raise money with ease in early in 2010.

PRIMARY MARKET AND SECONDARY MARKET

When shares are bought in an IPO it is termed primary market. The primary market does not involve the stock exchanges. A company that plans an IPO contacts an investment banker who will in turn called on securities dealers to help sell the new stock issue.

This process of selling the new stock issues to prospective investors in the primary market is called underwriting.

When an investor buys shares from another investor at an agreed prevailing market price, it is called as buying from the secondary market.

The secondary market involves the stock exchanges and it is regulated by a regulatory authority. In India, the secondary and primary markets are governed by the Security and Exchange Board of India (SEBI).

ADVANTAGES AND DISADVANTAGES OF AN IPO

ADVANTAGES

Increased capital Liquidity Increased Prestige Valuation Increased wealth

DISADVANTAGES

Time and Expense Disclosure Decision based upon stock price Regulatory Review Falling Stock Price -10-

Securities and Exchange Board of India

The Securities and Exchange Board of India was established on April 12, 1992 in accordance with the provisions of the Securities and Exchange Board of India Act,1992.

The PREAMBLE of the Securities and Exchange Board of India describes the basic functions of the Securities and Exchange Board of India as

“…..to protect the interests of investors in securities and to promote the development of, and to regulate the securities market and for matters connected there with or incidental thereto”

The mission of SEBI is to make India as one of the best securities market of the world and SEBI as one of the most respected regulator in the world.

OBJECTIVE

SEBI protect the interests of investors in securities, and promotes the development of Securities Market and it also regulates the securities market.

Another significant event is the approval of trading in stock indices (like Nifty & Sensex) in 2000. A market Index is a convenient and effective product because of the following reasons:

It is used in derivative instruments like index futures and index options;

It can be used for passive fund management as in case of Index Funds.

-11-

FUNCTIONS

The regulation of the capital markets is primarily the responsibility of the Securities and Exchange Board of India (SEBI), which is located in Mumbai. Some of the major functions of SEBI are:

SEBI is expected to regulate the business in stock exchanges and any other securities markets.

Registering and regulating the working of collective investment schemes, including mutual funds is a responsibility of SEBI.

SEBI is responsible for prohibiting fraudulent and unfair trade practices relating to securities markets.

• Prohibiting insider trading in securities, with the imposition of monetary penalties, on erring market intermediaries.

• Regulating substantial acquisition of shares and takeover of companies.

-12-

The National Stock Exchange (NSE) is India's leading stock exchange covering

various cities and towns across the country. NSE was set up by leading

institutions to provide a modern, fully automated screen-based trading system

with national reach. The Exchange has brought about unparalleled transparency,

speed & efficiency, safety and market integrity. It has set up facilities that serve

as a model for the securities industry in terms of systems, practices and

procedures.

The Organization

The National Stock Exchange of India Limited has genesis in the report of the

High Powered Study Group on Establishment of New Stock Exchanges, which

recommended promotion of a National Stock Exchange by financial institutions

(FIs) to provide access to investors from all across the country on an equal

footing. Based on the recommendations, NSE was promoted by leading

Financial Institutions at the behest of the Government of India and was

incorporated in November 1992 as a tax-paying company unlike other stock

exchanges in the country.

On its recognition as a stock exchange under the Securities Contracts

(Regulation) Act, 1956 in April 1993, NSE commenced operations in the

Wholesale Debt Market (WDM) segment in June 1994. The Capital Market

(Equities) segment commenced operations in November 1994 and operations in

Derivatives segment commenced in June 2000.

-13-

Market Segments and Products

NSE provides a trading platform for of all types of securities for investors under one roof – Equity, Corporate Debt, Central and State Government Securities, T-Bills, Commercial Paper (CPs), Certificate of Deposits (CDs), Warrants, Mutual Funds (MFs) units, Exchange Traded Funds (ETFs), Derivatives like Index Futures, Index Options, Stock Futures, Stock Options and Currency Futures.

The Exchange provides trading 5 in 4 different segments viz., Wholesale Debt Market (WDM) segment, Capital Market (CM) segment, Futures & Options (F&O) segment and the Currency Derivatives Segment (trading on which commenced on August 29, 2008)

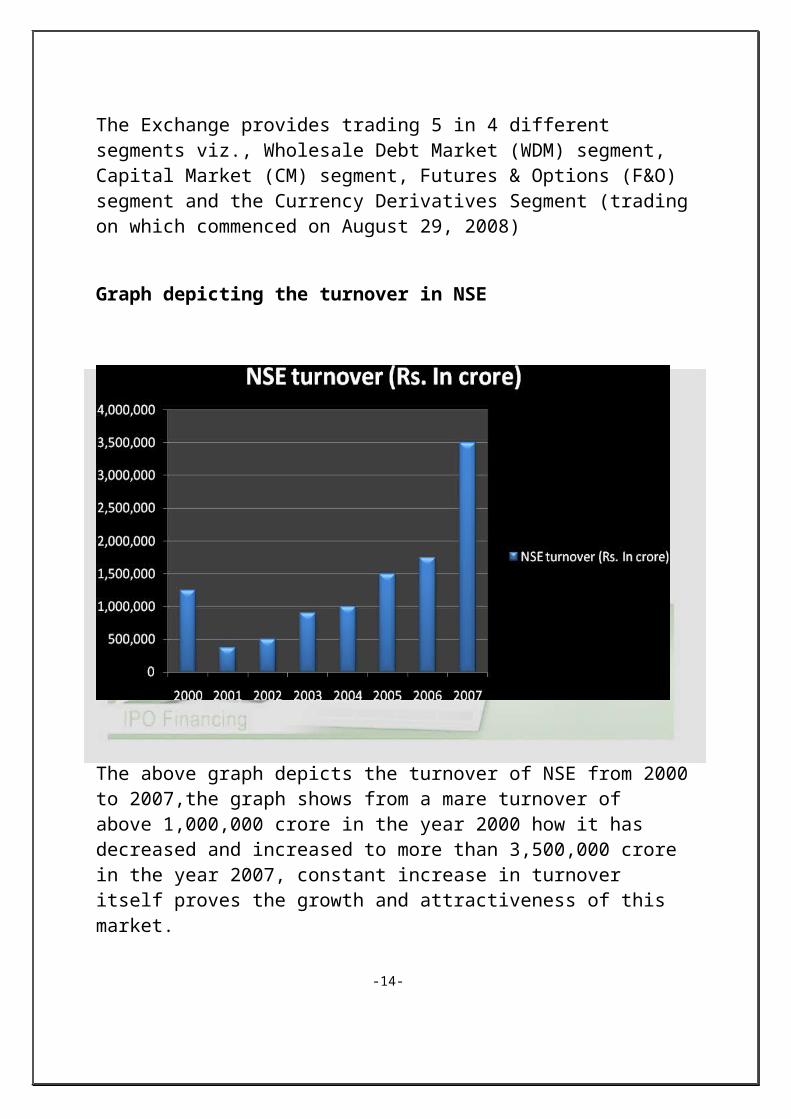

Graph depicting the turnover in NSE

The above graph depicts the turnover of NSE from 2000 to 2007,the graph shows from a mare turnover of above 1,000,000 crore in the year 2000 how it has decreased and increased to more than 3,500,000 crore in the year 2007, constant increase in turnover itself proves the growth and attractiveness of this market.

-14-

Bombay Stock Exchange Limited (the Exchange) is the oldest stock exchange

in Asia with a rich heritage. Popularly known as "BSE", it was established as

"The Native Share & Stock Brokers Association" in 1875. It is the first stock

exchange in the country to obtain permanent recognition in 1956 from the

Government of India under the Securities Contracts (Regulation) Act, 1956.The

Exchange's pivotal and pre-eminent role in the development of the Indian

capital market is widely recognized and its index, SENSEX, is tracked

worldwide. Earlier an Association of Persons (AOP), the Exchange is now a

demutualised and corporatised entity incorporated under the provisions of the

Companies Act, 1956, pursuant to the BSE Scheme, 2005 notified by the

Securities and Exchange Board of India (SEBI).Bombay Stock Exchange

Limited received its Certificate of Incorporation on 8th August, 2005 and

Certificate of Commencement of Business on 12th August, 2005. The 'Due

Date' for taking over the business and operations of the BSE, by the Exchange

was fixed for 19th August, 2005, under the Scheme. The Exchange has

succeeded the business and operations of BSE on going concern basis and its

recognition as an Exchange has been continued by SEBI

The Exchange has a nation-wide reach with a presence in 417 cities and towns

of India. The systems and processes of the Exchange are designed to safeguard

market integrity and enhance transparency in operations. During the year 2004-

2005, the trading volumes on the Exchange showed robust growth.

-15-

Coverage:

The equity shares of 200 selected companies from the specified and non specified lists of this Exchange have been considered for inclusion in the sample for `BSE-200'. The selection of companies has primarily been done on the basis of current market capitalization of the listed scripts on the exchange. Besides market capitalization, the market activity of the companies as reflected by the volumes of turnover and certain fundamental factors were considered for the final selection of the 200 companies.

Choice of Base Year:

The financial year 1989-90 has been chosen as the base year for the price stability exhibited during that year and due to its proximity to the current period.

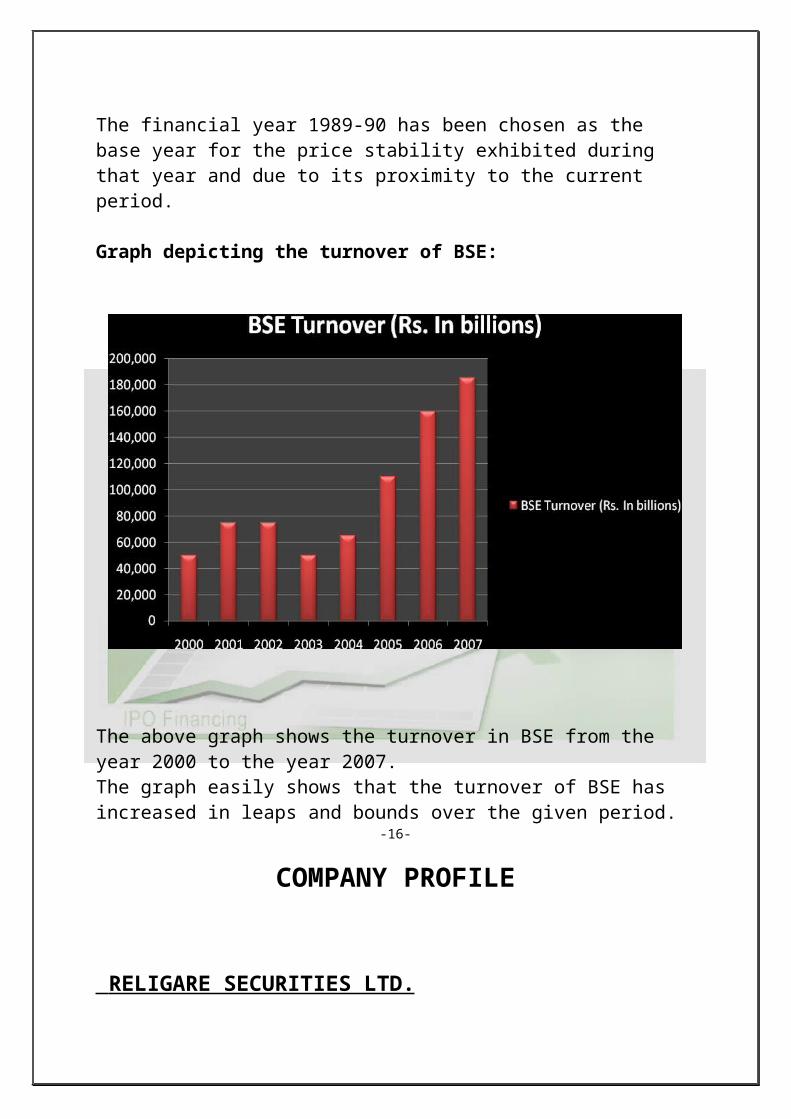

Graph depicting the turnover of BSE:

The above graph shows the turnover in BSE from the year 2000 to the year 2007.

The graph easily shows that the turnover of BSE has increased in leaps and bounds over the given period.

-16-

COMPANY PROFILE

RELIGARE SECURITIES LTD.

SEBI Registration No: INMOOOO11062

Corporate Office:19 Nehru Place, New Delhi – 110019Website: www.religare.inEmail: [email protected]: RELIGARE to 5888

PUNE:Ground Floor, Amar Caliber,BMCC Road, Shivajinagar,Pune – 411004

AHMEDNAGAR:5&6, Himalaya Tower,Opp. Deepak Hospital,Savedi Road,Ahmednagar – 414003

-17-

HISTORY AND BACKGROUND

RELIGARE Securities Ltd. (RSL) is a wholly owned subsidiary of RELIGARE Financial Services Ltd. (RFSL), a Company promoted by the late Dr.Parvinder Singh, Ex-CMD of Ranbaxy Laboratories Ltd.

The primary focus of Religare Securities Ltd. is to cater to services in Capital Market Operations to Institutional Investors. The Company is a member of the National Stock Exchange (NSE) and OTCEI. The growing list of financial institutions with whom RSL is empanelled as approved Broker is a reflection of the high levels of services maintained by the Company.

REL operates from seven domestic regional offices, 43 sub-regional offices, andhas a presence in 498* cities and towns controlling 1,837* business locations allover India.

To make a mark in the global arena, REL acquired UK-based Hichens, Harrison& Co. in 2008 which was subsequently re-named as Religare Hichens HarrisonPLC ("RHH"). Hichens, Harrison & Co. was incorporated in London in the year1803 and is believed to be one of the oldest firms of stockbrokers in the City ofLondon. Pursuant to expansion of REL's business, the company has grown fromlargely an equity trading company into a diversified financial services company.With the addition of RHH the REL group now operates out of multiple globallocations, other than India, (the UK, the USA, Brazil, South Africa, Dubai andSingapore).

RELIGARE was founded with the vision of providing integrated financial care driven by the relationship of trust. The bouquet of services offered by RELIGARE includes Broking (Stocks and Commodities), Depository Participant Service, Advisory on Mutual Fund Investments and Portfolio Management Services.

RELIGARE is a pioneer in the concept of partnership to reach multiple locationsin order to effectively service its large base of individual clients. Besides the reach of RELIGARE, the clients of the company greatly benefit by its strong

research capability, which encompasses fundamentals as well as technical knowledge.

-18-

RELIGARE

ENTERPRISE

LIMITED

Religare Finvest ltd

Religare Finvest ltdReligare

Securities Ltd

Religare Wealth

Mgt Services Ltd

s

Religare Wealth

Mgt Services Ltd

s

Religare capital

Markets Ltd

Religare finance

Ltd

Religare Commodities Ltd

Religare Insurance

Broking Ltd

Religare Venture

Capital Pvt Ltd

Religare Realty

Ltd

-19-

ABOUT RELIGARE SECURITIES LIMITED

BRND IDENTITY

Name

Religare is a Latin word that translates as 'to bind together'. This name has been chosen to reflect the integrated nature of the financial services the company offers.

Symbol

The Religare name is paired with the symbol of a four-leaf clover. Traditionally, it is considered good fortune to find a four-leaf clover as there is only one four-leaf clover for every 10,000 three-leaf clovers found.

For us, each leaf of the clover has a special meaning. It is a symbol of Hope. Trust. Care. Good Fortune. For the world, it is the symbol of Religare.

The first leaf of the clover represents Hope, The aspirations to succeed. The dream of becoming, Of new possibilities, It is the beginning of every step and the foundation on which a person reaches for the stars.

The second leaf of the clover represents Trust, The ability to place one’s own faith in another. To have A relationship as partners in a team. To accomplish a given goal with the balance that brings satisfaction to all, not in the binding, but in the bond that is built.

-20-

The third leaf of the clover represents Care, The secret ingredient that is the cement in every relationship. The truth of feeling that underlines sincerity and the triumph of diligence in every aspect. From it springs true warmth of service and the ability to adapt to evolving environments with consideration to all.

The fourth and final leaf of the clover represents Good Fortune. Signifying that rare ability to meld opportunity and planning with circumstance to generate those often looked for remunerative moments of success.

Hope. Trust. Care. Good Fortune. All elements perfectly combine in the emblematic and rare, four-leaf clover to visually symbolize the values that bind together and form the core of the Religare vision.

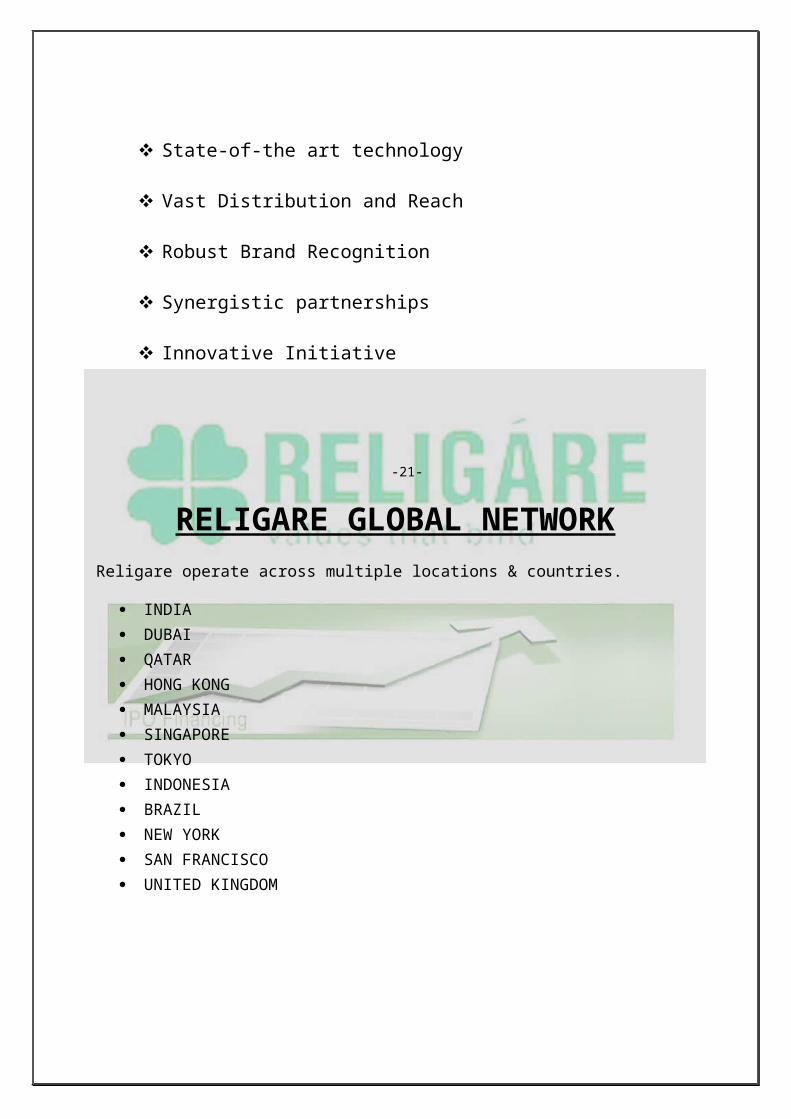

THE RELIGARE EDGE

Diverse offerings

Dynamic Management Team

State-of-the art technology

Vast Distribution and Reach

Robust Brand Recognition

Synergistic partnerships

Innovative Initiative

-21-

RELIGARE GLOBAL NETWORKReligare operate across multiple locations & countries.

INDIA DUBAI QATAR HONG KONG MALAYSIA SINGAPORE TOKYO INDONESIA BRAZIL NEW YORK SAN FRANCISCO UNITED KINGDOM

-22-

Company’s IPO

Sr.No

Name of the issue

Book Running Lead Manager

Date of

issueNo. of

members

No. of biddin

gcenters

Issue Size

FloorPrice

(in Rs)

ExitPric

e(in Rs

1 KAUSAR

INDIA LIMITED

Religare capital

markets limited

Mar 23, 2009 to Mar 25,

20091 30 9,74,26

8

13.00 50.54

2EMMBI

POLYARNS

LIMITED

KEYNOTE CORPORATIO

NSERVICE LIMITED

01/02/2010 TO 03/02/2010

84 51 95.74 40 TO 45

45

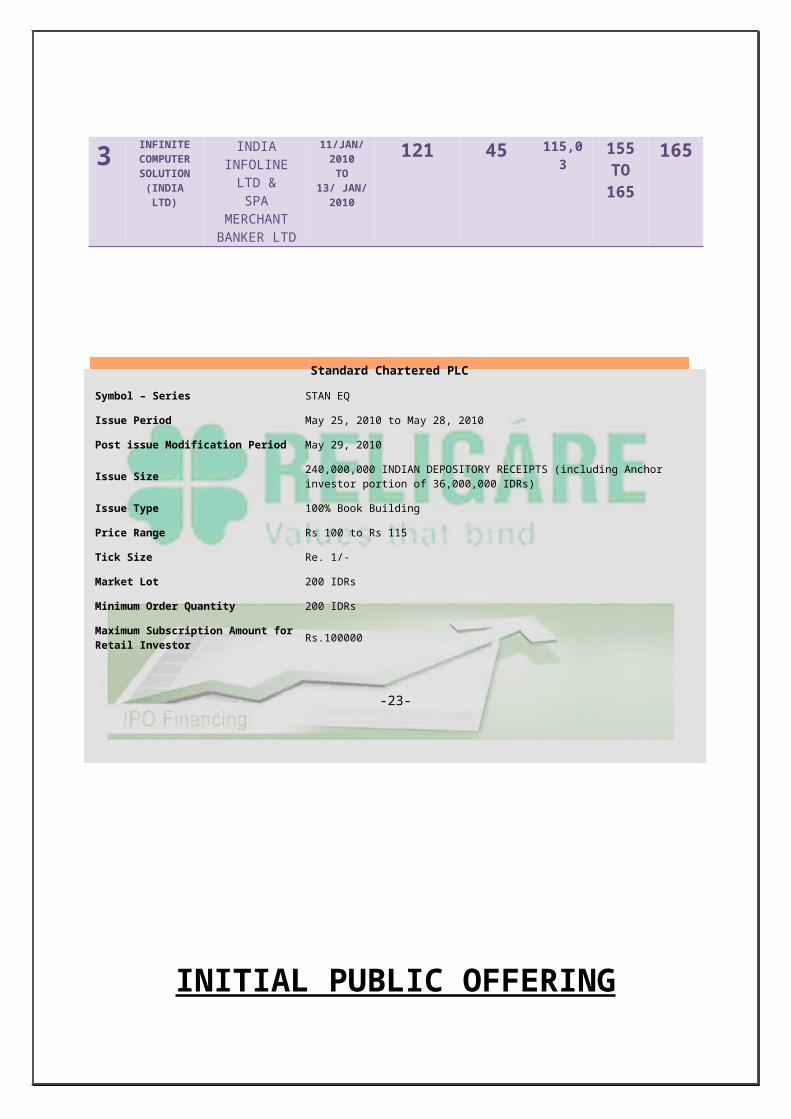

3INFINITECOMPUTE

R SOLUTION

(INDIA LTD)

INDIA INFOLINE LTD

&SPA

MERCHANTBANKER LTD

11/JAN/ 2010TO

13/ JAN/ 2010

121 45 115,03 155 TO 165

165

Standard Chartered PLC

Symbol – Series STAN EQ

Issue Period May 25, 2010 to May 28, 2010

Post issue Modification Period May 29, 2010

Issue Size240,000,000 INDIAN DEPOSITORY RECEIPTS (including Anchor investor portion of 36,000,000 IDRs)

Issue Type 100% Book Building

Price Range Rs 100 to Rs 115

Tick Size Re. 1/-

Market Lot 200 IDRs

Minimum Order Quantity 200 IDRs

Maximum Subscription Amount for Retail Investor

Rs.100000

-23-

INITIAL PUBLIC OFFERING

-24-

AN OVERVIEW OF INITIAL PUBLIC OFFER

An IPO or an Initial Public Offer is a company's first sale of

equity shares to the general public. Shares offered in an IPO are often, but not

always, those of newly setup companies seeking outside equity capital and a

public market for their shares.

An Initial Public Offering (IPO) can be a good investment avenue for

equity investors. While the IPO market is dry these days, a fresh crop is

expected soon. It is important to understand IPO’s and decide whether to invest

in them or not.

Why does a company go for an IPO

Initial Public Offering (IPO) is when an unlisted company makes either a fresh

issue of securities or an offer for sale of its existing securities or both for the

first time to the public. This paves way for listing and trading of the issuer’s

securities.

A company's first sale of stock to the public. Securities offered in an IPO are

often, but not always, those of young, small companies seeking outside equity

capital and a public market for their stock. Investors purchasing stock in IPOs

generally must be prepared to accept very large risks for the possibility of large

gains. IPO's by investment companies (closed end funds) usually contain

underwriting fees which represent a load to buyers.

The basis purpose of an IPO is to facilitate transfer of resources from savers to

entrepreneurs seeking to establish new enterprise or to diversify/expand existing

ones. -25-

Such facilities are of crucial importance in the context of the dichotonomy of

funds available for capital uses form those in whose hands they accumulate, and

those by whom they are applied for capital uses from those in whose hands they

accumulate, and those by whom they are applied to productive uses.

However it should not be conceived as exclusively serving

the purpose of raising finance for new capital expenditure. Infect the

organization and facilities of the market are also utilized for selling concerns to

the public as going concerns through the conversion of existing proprietary

enterprises or private companies in to public companies

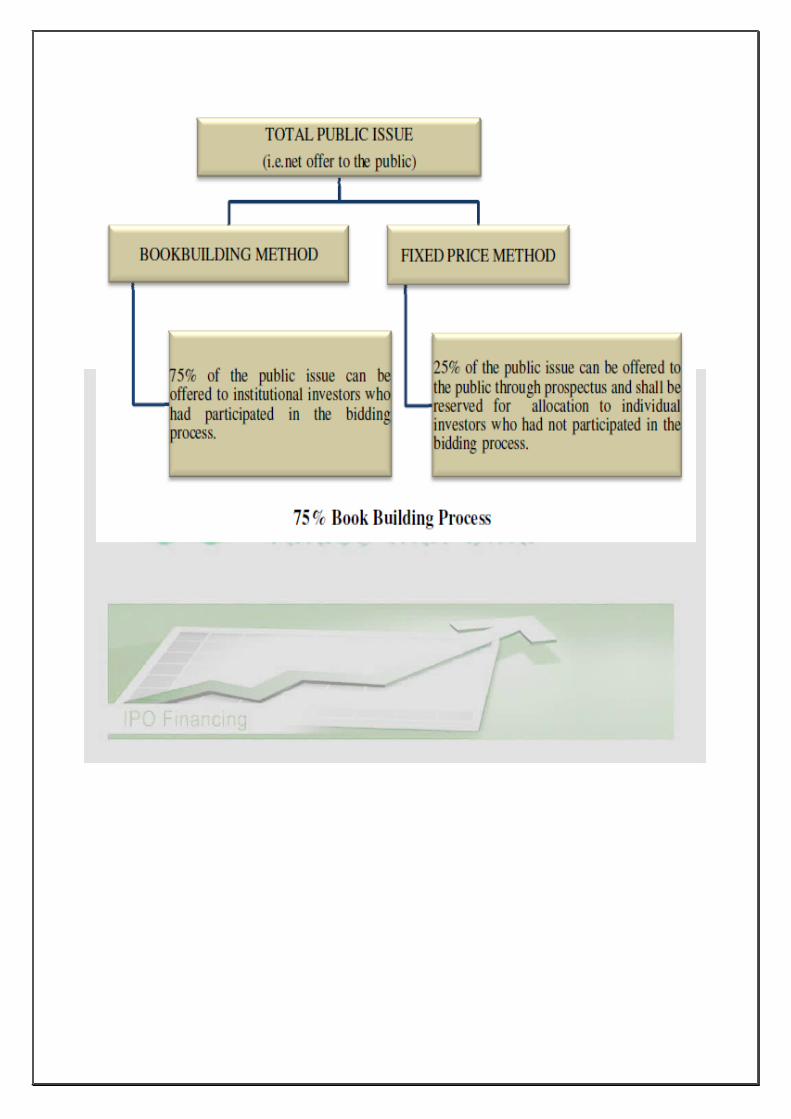

Corporate may raise capital in the primary market by way of an initial public

offer, rights issue or private placement. An Initial Public Offer (IPO) is the

selling of securities to the public in the primary market. This Initial Public

Offering can be made through the fixed price method, book building method or

a combination of both.

In case the issuer chooses to issue securities through the book building route

then as per SEBI guidelines, an issuer company can issue securities in the

following manner:

a) 100% of the net offer to the public through the book building route.

b) 75% of the net offer to the public through the book building process

c) 25% through the fixed price portion.

-26-

PROCESS OF AN IPO

The Process:

The Issuer who is planning an IPO nominates a lead merchant banker as a

'book runner'.

The Issuer specifies the number of securities to be issued and the price

band for orders.

The Issuer also appoints syndicate members with whom orders can be

placed by the investors.

Investors place their order with a syndicate member who inputs the

orders into the 'electronic book'. This process is called 'bidding' and is

similar to open auction.

A Book should remain open for a minimum of 5 days.

Bids cannot be entered less than the floor price.

Bids can be revised by the bidder before the issue closes.

On the close of the book building period the 'book runner evaluates the

bids on the basis of the evaluation criteria which may include -

Price Aggression

Investor quality

Earliness of bids, etc.

-27-

The book runner and the company conclude the final price at which it is

willing to issue the stock and allocation of securities.

Generally, the number of shares are fixed, the issue size gets frozen based

on the price per share discovered through the book building process.

Allocation of securities is made to the successful bidders.

Book Building is a good concept and represents a capital market which is

in the process of maturing.

How does the company fix the price band?

The red herring prospectus may contain either the floor price for the securities

or a price band within which the investors can bid. The spread between the floor

and the cap of the price band shall not be more than 20%. In other words, it

means that the cap should not be more than 120% of the floor price. The price

band can have a revision and such a revision in the price band shall be widely

disseminated by informing the stock exchanges, by issuing press release and

also indicating the change on the relevant website and the terminals of the

syndicate members. In case the price band is revised, the bidding period shall be

extended for a further period of three days, subject to the total bidding period

not exceeding thirteen days

Pricing is critical and the most important process in IPO. Pricing involves lot of

research and calculations. Pricing is done in such a way that investors are

benefited and also the company’s objective is achieved that is its aim for an IPO

is achieved. Thus, pricing is the most important factor in IPO process generally

there are two methods of IPO pricing .-

28-

Fixed Pricing

Book building Process

PROCEDURE

The sale (that is, the allocation and pricing) of shares in an IPO may take

several forms. Common methods include:

Dutch auction

Firm commitment

Best efforts

Bought deal

Self Distribution of Stock

A large IPO is usually underwritten by a "syndicate" of investment banks led by

one or more major investment banks (lead underwriter). Upon selling the

shares, the underwriters keep a commission based on a percentage of the value

of the shares sold. Usually, the lead underwriters, i.e. the underwriters selling

the largest proportions of the IPO, take the highest commissions—up to 8% in

some cases.

Multinational IPOs may have as many as three syndicates to deal with differing

legal requirements in both the issuer's domestic market and other regions. For

example, an issuer based in the E.U. may be represented by the main selling

syndicate in its domestic market, Europe, in addition to separate syndicates or

selling groups for US/Canada and for Asia. Usually, the lead underwriter in the

main selling group is also the lead bank in the other selling groups.

Because of the wide array of legal requirements, IPOs typically involve one or

more law firms with major practices in securities law, such as the Magic Circle

firms of London and the white shoe firms of New York City. -29-

Usually, the offering will include the issuance of new shares, intended to

raise new capital, as well the secondary sale of existing shares. However,

certain regulatory restrictions and restrictions imposed by the lead underwriter

are often placed on the sale of existing shares.

Public offerings are primarily sold to institutional investors, but some shares are

also allocated to the underwriters' retail investors. A broker selling shares of a

public offering to his clients is paid through a sales credit instead of a

commission. The client pays no commission to purchase the shares of a public

offering; the purchase price simply includes the built-in sales credit.

Fixed Pricing

An issuer company is allowed to freely price the issue. The basis of issue price

is disclosed in the offer document where the issuer discloses in detail about the

qualitative and quantitative factors justifying the issue price. Fixed price does

not allow an opportunity to the issuer or the merchant banker to do any

discretionary allotment, which is possible only in a book building issue. So

there is one factor that we should remember which drives book building issue

more.

Book building Process

Book building Process as Mentioned in the SEBI

Book Building is basically a capital issuance process used in Initial Public Offer

(IPO) which aids price and demand discovery. It is a process used for marketing

a public offer of equity shares of a company. It is a mechanism where, during

the period for which the book for the IPO is open, bids are collected from

investors at various prices, which are above or equal to the floor price. The

process aims at tapping both wholesale and retail investors. -30-

The offer/issue price is then determined after the bid closing date based on

certain evaluation criteria.

Guidelines for Book Building

Rules governing book building is covered in Chapter XI of the Securities and

Exchange Board of India (Disclosure and Investor Protection) Guidelines 2000.

Difference between shares offered through book building and offer of shares

through normal public issue:

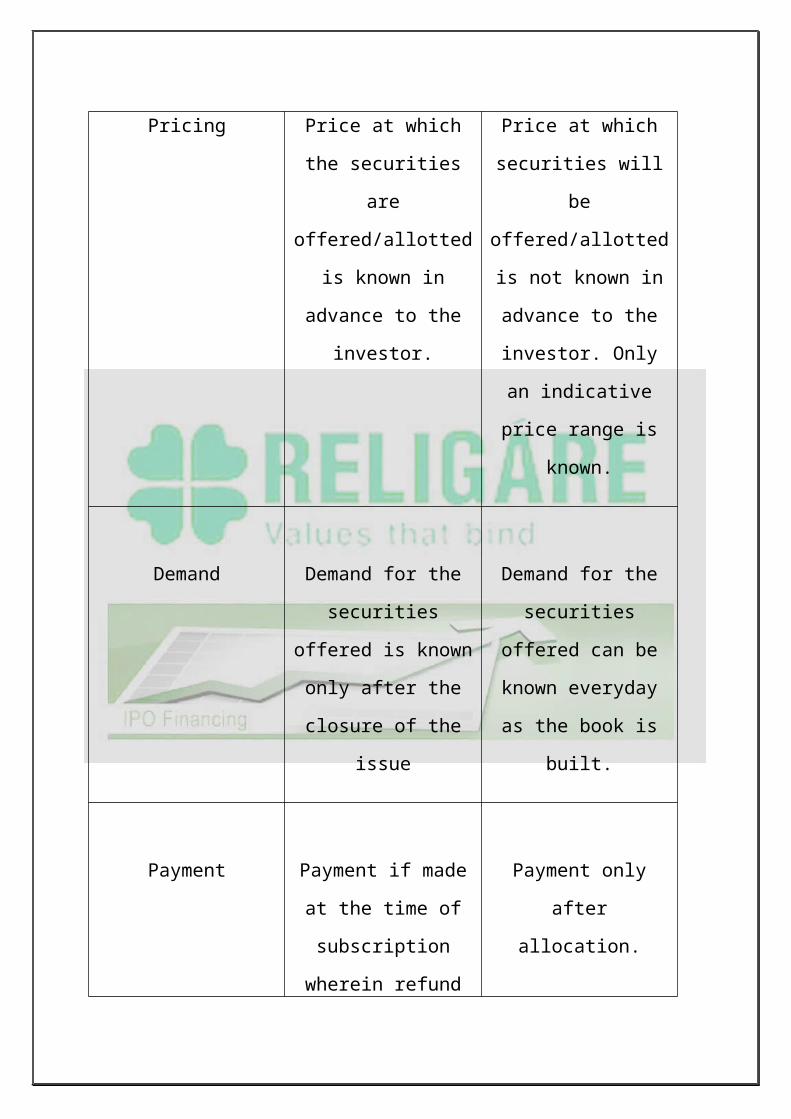

Feature Fixed Price process Book Building process

Pricing Price at which the

securities are

offered/allotted is

known in advance to

the investor.

Price at which

securities will be

offered/allotted is not

known in advance to

the investor. Only an

indicative price range is

known.

Demand Demand for the

securities offered is

known only after the

Demand for the

securities offered can

be known everyday as

closure of the issue the book is built.

Payment Payment if made at the

time of subscription

wherein refund is given

after allocation.

Payment only after

allocation.

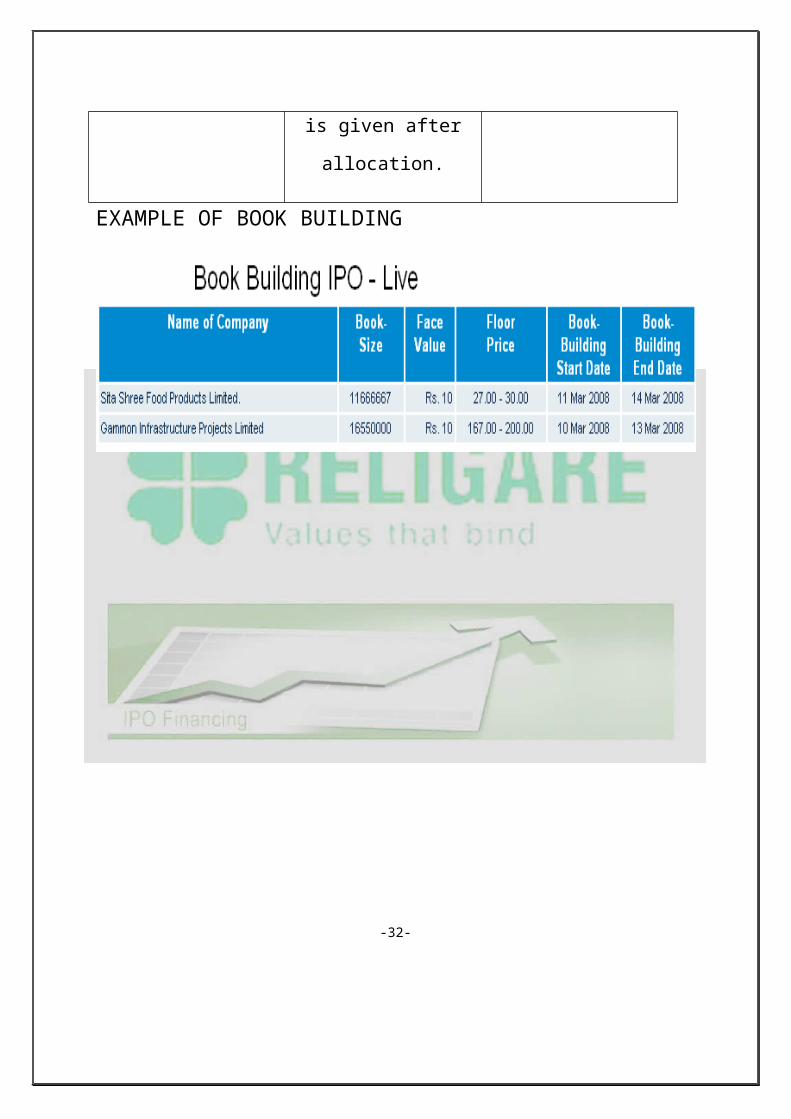

EXAMPLE OF BOOK BUILDING

-32-

-33-

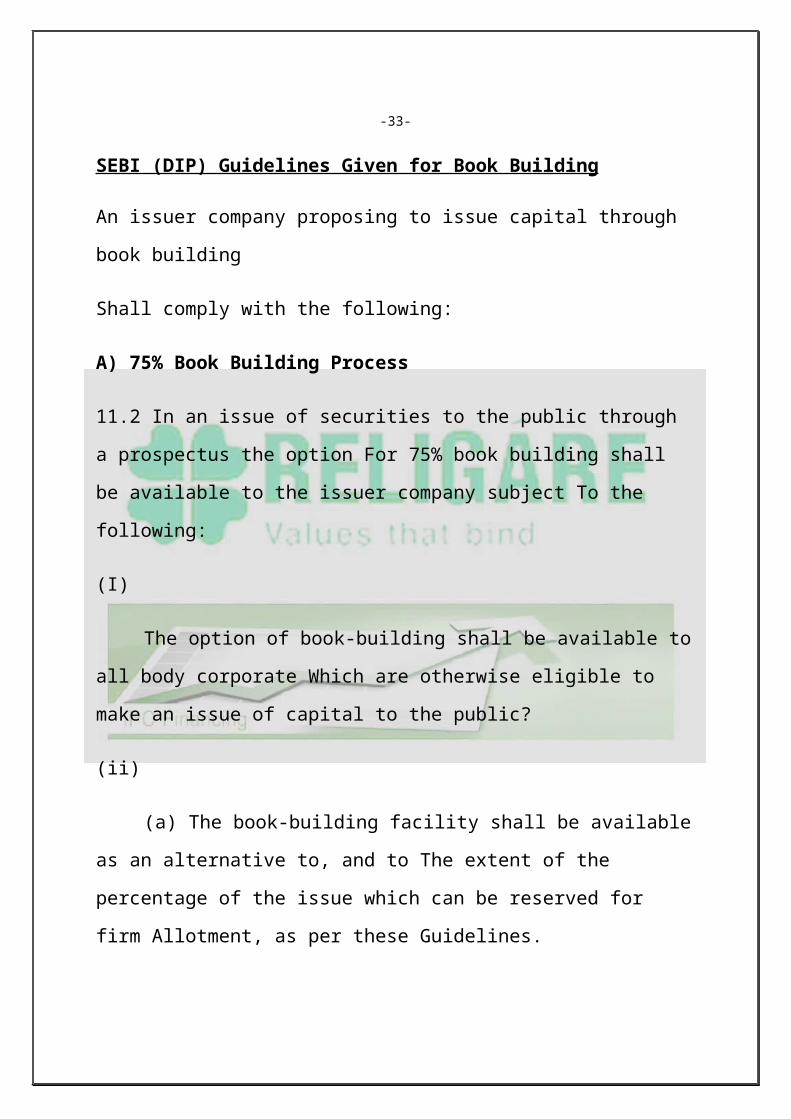

SEBI (DIP) Guidelines Given for Book Building

An issuer company proposing to issue capital through book building

Shall comply with the following:

A) 75% Book Building Process

11.2 In an issue of securities to the public through a prospectus the option For

75% book building shall be available to the issuer company subject To the

following:

(I)

The option of book-building shall be available to all body corporate

Which are otherwise eligible to make an issue of capital to the public?

(ii)

(a) The book-building facility shall be available as an alternative to, and

to The extent of the percentage of the issue which can be reserved for firm

Allotment, as per these Guidelines.

(b) The issuer company shall have an option of either reserving the

Securities for firm allotment or issuing the securities through book building

Process.

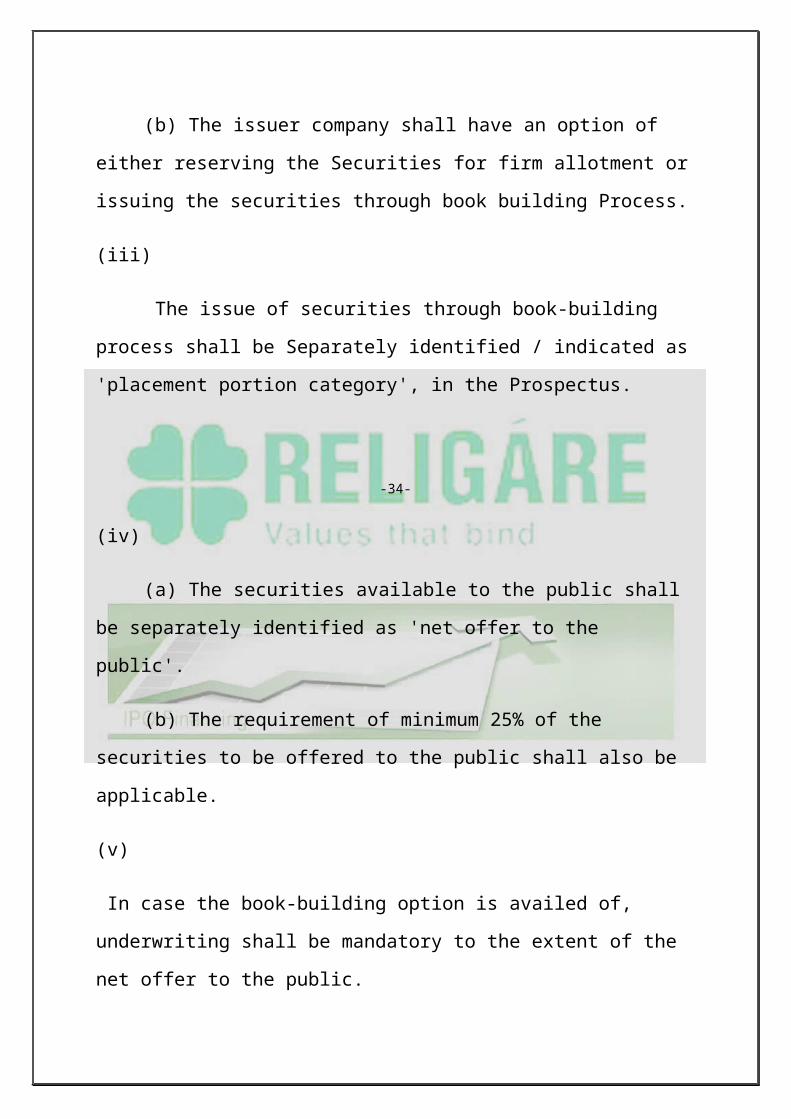

(iii)

The issue of securities through book-building process shall be Separately

identified / indicated as 'placement portion category', in the Prospectus.

-34-

(iv)

(a) The securities available to the public shall be separately identified as

'net offer to the public'.

(b) The requirement of minimum 25% of the securities to be offered to

the public shall also be applicable.

(v)

In case the book-building option is availed of, underwriting shall be mandatory

to the extent of the net offer to the public.

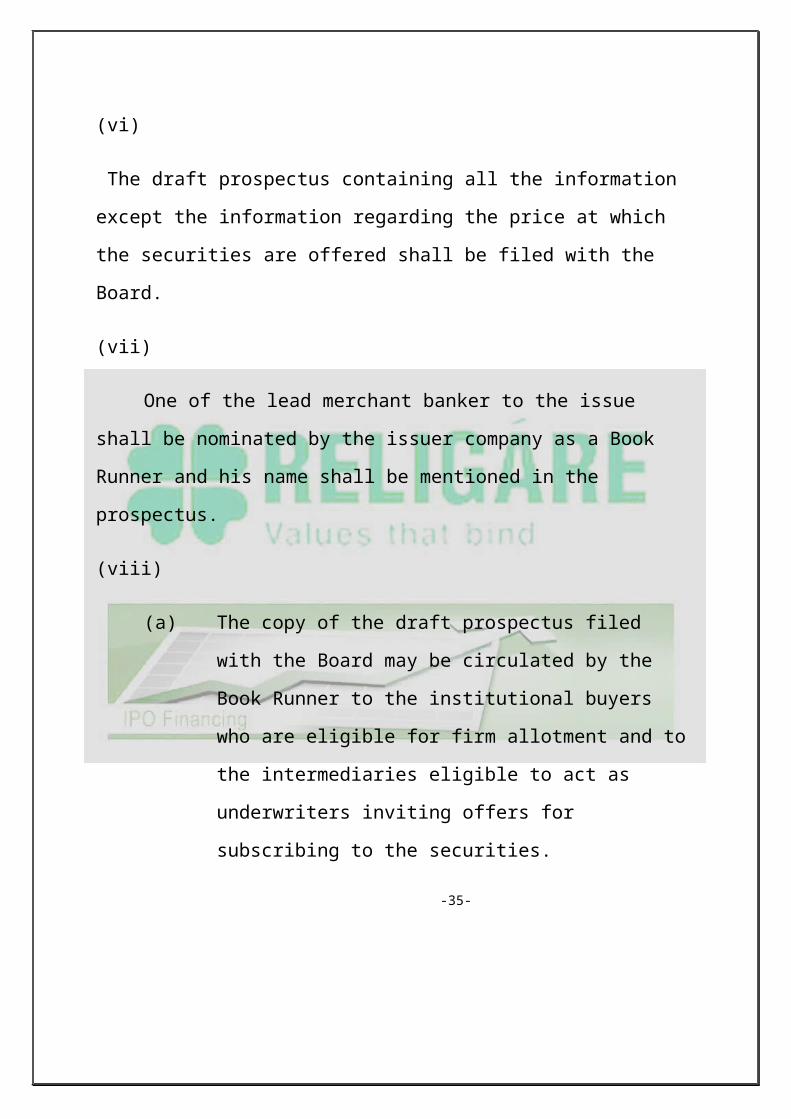

(vi)

The draft prospectus containing all the information except the information

regarding the price at which the securities are offered shall be filed with the

Board.

(vii)

One of the lead merchant banker to the issue shall be nominated by the

issuer company as a Book Runner and his name shall be mentioned in the

prospectus.

(viii)

(a) The copy of the draft prospectus filed with the Board may be

circulated by the Book Runner to the institutional buyers who

are eligible for firm allotment and to the intermediaries eligible

to act as underwriters inviting offers for subscribing to the

securities.

-35-

(b) The draft prospectus to be circulated shall indicate the price band

within which the securities are being offered for subscription.

(ix)

The Book Runner on receipt of the offers shall maintain a record of the

names and number of securities ordered and the price at which the institutional

buyer or underwriter is willing to subscribe to securities under the placement

portion.

(x)

The underwriter(s) shall maintain a record of the orders received by him

for subscribing to the issue out of the placement portion.

Duration of the issue

Subscription list for public issues shall be kept open for at least 3

working days and not more than 10 working days. In case of Book built issues,

the minimum and maximum period for which bidding will be open is 3–7

working days extendable by 3 days in case of a revision in the price band. The

public issue made by an infrastructure company, may be kept open for a

maximum period of 21 working days and Rights issues shall be kept open for at

least 30 days and not more than 60 days.

-36-

B) 195(Offer to Public through Book Building Process)

11.3

196(An issuer company may, subject to the requirements specified in

This chapter, make an issue of securities to the public through a Prospectus in

the following manner:

a.100% of the net offer to the public through book building process, or

b.75% of the net offer to the public through book building process and

25% at the price determined through book building.)

11.3.1

(I) 197(Deleted)

(ii) Reservation or firm allotment to the extent of percentage specified in These

Guidelines shall not be made to categories other than the Categories mentioned

in sub-clause (iii) below.

(iii) Book Building shall be for the portion other than the promoters

Contribution and the allocation made to:

(a) ‘Permanent employees of the issuer company and in the case of a new

Company the permanent employees of the promoting companies';

(b) ‘Shareholders of the promoting companies in the case of a new Company

and shareholders of group companies in the case of an Existing company’ either

on a ‘competitive basis’ or on a ‘firm allotment Bases.

-37-

198

((c) persons who, on the date of filing of the draft offer document with

the Board, have business association, as depositors, bondholders and

Subscribers to services, with the issuer making an initial public offering,

provided that allotment to such persons shall not exceed 5% of the issue

Provided further that no reservation shall be made for the issue management

team, syndicate members, their promoters, directors and employees and for the

group/associate companies of issue management team and syndicate members

and their promoters, directors and employees.)

(iv)

The issuer company shall appoint an eligible Merchant Banker(s) as book

runner(s) and their name(s) shall be mentioned in the draft prospectus.

199

((iv) (a) The issuer company shall enter into an agreement with one or

more of the Stock Exchange(s) which have the requisite system of on-line offer

of securities. The agreement shall specify inter-alia, the rights, duties,

responsibilities and obligations of the company and stock exchange (s) inter se.

The agreement may also provide for a dispute resolution mechanism between

the company and the stock exchange.

(iv) (b) The company may apply for listing of its securities on an

exchange other than the exchange through which it offers its securities to public

through the on-line system.)

-38-

200

(V) The Lead Merchant Banker shall act as the Lead Book Runner.)

201

((v) (a) In case the issuer company appoints more than one 202(merchant

banker(s)), the names of all such (merchant bankers(s)) who have submitted the

due diligence certificate to SEBI, may be mentioned on the front cover page of

the prospectus. A disclosure to the effect that " the investors may contact any of

such (merchant bankers(s)), for any complaint pertaining to the issue" shall be

made in the prospectus, after the "risk factors”.)

203

((v) (b) The lead book runner/issuer may designate, in any manner, the

other Merchant Banker(s), subject to the following;

Eligible for reservation

In a book built issue allocation to Retail Individual Investors (RII’s), Non

Institutional Investors (NII’s) and Qualified Institutional Buyers (QIB’s) is in

the ratio of 35: 15: 50 respectively. In case the book built issues are made

pursuant to the requirement of mandatory allocation of 60% to QIB’s , the

respective figures are 30% for RII’s and 10% for NII’s. This is a transitory

provision pending harmonization of the QIB allocation.

The allotment to the Qualified Institutional Buyers (QIB’s) is on a discretionary

basis. The discretion is left to the Merchant Bankers who first disclose the

parameters of judgment in the Red Herring Prospectus. There are no objective

conditions stipulated as per the DIP Guidelines.

-39-

The Merchant Bankers are free to set their criteria and mention the same in the

Red Herring Prospectus.

Reservation on Competitive Basis is when allotment of shares is made in

proportion to the shares applied for by the concerned reserved categories.

Reservation on competitive basis can be made in a public issue to the

Employees of the company, Shareholders of the promoting companies in the

case of a new company and shareholders of group companies in the case of an

existing company, Indian Mutual Funds, Foreign Institutional Investors

(including non resident Indians and overseas corporate bodies), Indian and

Multilateral development Institutions and Scheduled Banks.

-40-

Book Building at NSE

The NSE has set up nation-wide network for trading whereby members can trade remotely from their offices located all over the country. The NSE trading network spans various cities and towns across India.

NSE decided to offer this infrastructure for conducting online IPOs through the Book Building process. NSE operates a fully automated screen based bidding system called NEAT IPO that enables trading members to enter bids directly from their offices through a sophisticated telecommunication network.

Book Building through the NSE system offers several advantages:

The NSE system offers a nationwide bidding facility in securities.

It provides a fair, efficient & transparent method for collecting bids using latest electronic trading systems

Costs involved in the issue are far less than those in a normal IPO

Procedures

Issuers

Issuers desirous of using NSE's online IPO system are required to comply with the following procedures:

1. Submit a written request as per prescribed format (Letter1, Letter2, BRLM) for usage of electronic facilities and software of NSE

2. Give details regarding Book Running Lead Manager, Co Book Running Lead Managers and Syndicate Members.

3. Pay the requisite charges to NSE.

-41-

Trading Members

The Book Running Lead Manager will give the list of trading members who are eligible to participate in the Book Building process to the Exchange. Members have to submit a one time undertaking to the Exchange. Eligible trading members have to give in the prescribed format details of the user IDs that they would like to use.

Subscribers

Subscribers can approach any of the approved trading members for submitting bids in the NEAT IPO system. On line transaction registration slip are generated automatically after entering the bids in to the system which acts as proof of the registration of each Bid option.

-42-

BSE's Book Building System

BSE offers the book building services through the Book Building

software that runs on the BSE Private network.

This system is one of the largest electronic book building networks

anywhere spanning over 350 Indian cities through over 7000 Trader

Work Stations via eased lines, VSATs and Campus LANS

The software is operated through book-runners of the issue and by the

syndicate member brokers. Through this book, the syndicate member

brokers on behalf of themselves or their clients' place orders.

Bids are placed electronically through syndicate members and the

information is collected on line real-time until the bid date ends.

In order to maintain transparency, the software gives visual graphs

displaying price v/s quantity on the terminals.

Listing Rules for New Companies on BSE /IPO Rules

The following eligibility criteria have been prescribed for the companies seeking permission to get list on the stock exchange, effective August 1st 2006.

The companies are classified into two categories: large cap and Small cap. A company is treated as a large cap company if the issue size is greater than or equal to Rs 10 crore and market capitalization of not less then Rs 25 crore.

-43-

A) In case of large cap companies

The minimum post-issue paid up capital of the applicant company shall be Rs. 3 crore.

The minimum issue size shall be Rs. 10 crore and The minimum market capitalization of the company shall be

Rs. 25 crore

Authorized capital is the amount for which a company has got the authorization from the regulatory body to raise through the issue. A company may or may not want to raise the full amount of authorized capital. Issue size is the amount that a company want to raise funds through the issue. It’s always less than or equal to authorized capital.

Part payment facility may be available for the investors who want to subscribe to an issue. Post-issue paid-up capital is the value of subscriptions (including promoter’s holding) paid at the end of issue date. This will be less than issue size if the total subscriptions are less than the offered shares or when there is part payment facility available for the issue.

Market capitalization is the product of number of shares outstanding (including promoter’s holding) and the market price. In an IPO before the first day of listing the market price is the issue price.

B) In respect of small cap companies

The minimum post issue paid up capital of the company shall be

Rs. 3 crore.

The minimum issue size shall be Rs. 3 crore.

The minimum market capitalization of the company shall be Rs. 5

crore.

The minimum income/turnover of the company shall be Rs. 3 crore

in each of the preceding three 12 month period.

The minimum number of the public shareholder after the issue

shall be 1000.

-44-

A due diligence study may be conducted by an independent team

of chartered Accountant or merchant banker (Investment Banker)

appointed by BSE, the cost of which will be borne by the

company. The requirement of a due diligence study may be waived

if a financial institution or a scheduled commercial bank has

appraised the project in the preceding 12 months.

In addition to this, the issuer company should have a post issue net worth

(equity capital + free reserve excluding revaluation reserve) of Rs 20 crore.

C) For all companies

In respect of the requirement of paid up capital and market

capitalization, the issuers shall be required to include in the

disclaimer clause forming a part of the offer document that in the

event of market capitalization requirement of BSE not being met,

the securities of the issuer would not be listed on BSE.

The applicant, promoters and / or group companies, shall be in

default in compliance of the listing agreement.

The above eligibility criteria would be in additions of the

companies prescribed under SEBI guidelines.

-45-

Listing Fees (BSE)

Particular Amount (Rs)

Initial Listing fees 7500

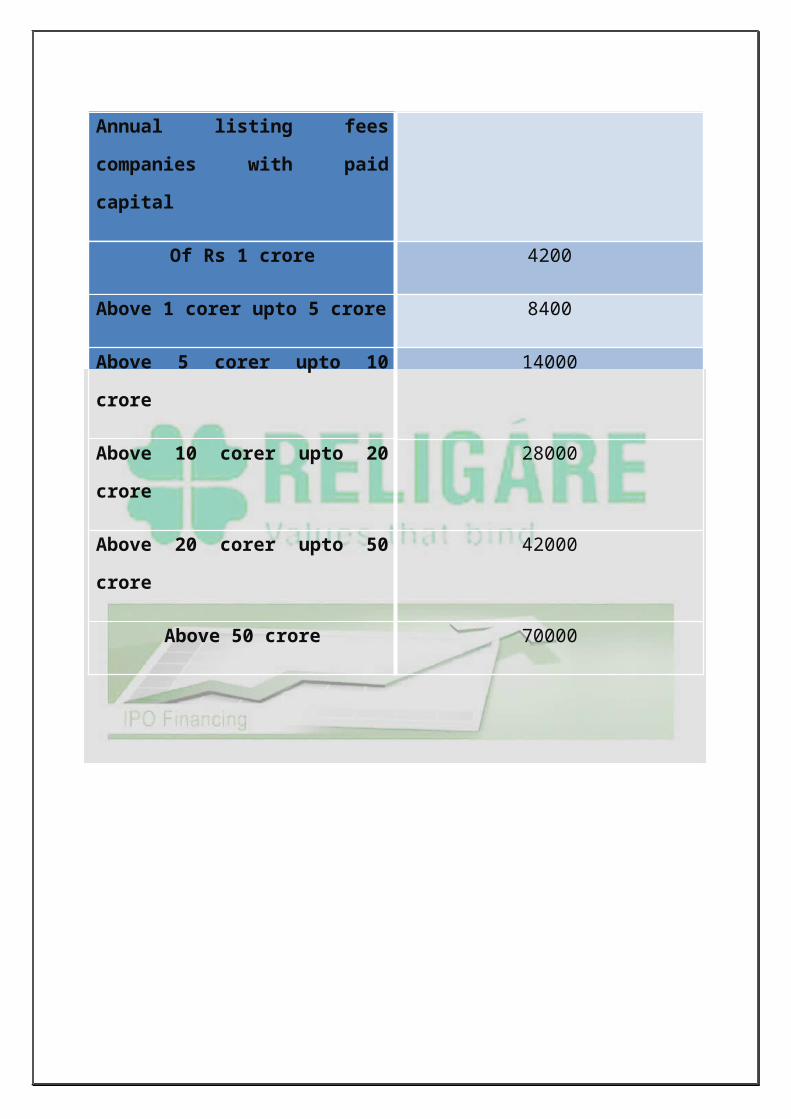

Annual listing fees companies with

paid capital

Of Rs 1 crore 4200

Above 1 corer upto 5 crore 8400

Above 5 corer upto 10 crore 14000

Above 10 corer upto 20 crore 28000

Above 20 corer upto 50 crore 42000

Above 50 crore 70000

-46-

Role of Lead manager

In the pre-issue process, the Lead Manager (LM) takes up the due

diligence of company’s operations/ management/ business plans/ legal etc.

Other activities of the LM include drafting and design of Offer documents,

Prospectus, statutory advertisements and memorandum containing salient

features of the Prospectus. The book running lead manager (BRLMs) shall

ensure compliance with stipulated requirements and completion of prescribed

formalities with the Stock Exchanges, RoC and SEBI including finalisation of

Prospectus and RoC filing. Appointment of other intermediaries viz.,

Registrar(s), Printers, Advertising Agency and Bankers to the Offer is also

included in the pre-issue processes.

The lead manager also draws up the various marketing strategies for the issue.

The post issue activities including management of escrow accounts, coordinate

non-institutional allocation, intimation of allocation and dispatch of refunds to

bidders etc are performed by the LM. The post Offer activities for the Offer will

involve essential follow-up steps, which include the finalization of trading and

dealing of instruments and dispatch of certificates and demat of delivery of

shares, with the various agencies connected with the work such as the

Registrar(s) to the Offer and Bankers to the Offer and the bank handling refund

business. The merchant banker shall be responsible for ensuring that these

agencies fulfill their functions and enable it to discharge this responsibility

through suitable agreements with the Company.

-47-

Role of registrar

The Registrar finalizes the list of eligible allottees after deleting the

invalid applications and ensures that the corporate action for crediting of shares

to the demat accounts of the applicants is done and the dispatch of refund orders

to those applicable are sent. The Lead manager coordinates with the Registrar to

ensure follow up so that that the flow of applications from collecting bank

branches, processing of the applications and other matters till the basis of

allotment is finalized, dispatch security certificates and refund orders completed

and securities listed.

Role of banker to the issue

Bankers to the issue, as the name suggests, carries out all the activities of

ensuring that the funds are collected and transferred to the Escrow accounts.

The Lead Merchant Banker shall ensure that Bankers to the Issue are appointed

in all the mandatory collection centers as specified in DIP Guidelines. The lead

manager also ensures follow-up with bankers to the issue to get quick estimates

of collection and advising the issuer about closure of the issue, based on the

correct figures.

Merchant Banking

Issue Management Services – to act as Book Running Lead

Manager/Lead

Project appraisal

Corporate Advisory Services

underwriting of equity issues

Banker to the Issue/Paying Banker -48-

Refund Banker

Monitoring Agency

Debenture Trustee

Investment Banking

Investment Bank is a financial intermediary that performs a variety of

services which includes underwriting, acting as an intermediary between an

issuer of securities and the investing public, facilitating mergers and other

corporate reorganizations, and also acting as a broker for institutional clients.

Private Equity

Private equities are equity securities of unlisted companies. Private

equities are generally illiquid and thought of as a long-term investment. Private

equity investments are not subject to the same high level of government

regulation as stock offerings to the general public. Private equity is also far less

liquid than publicly traded stock.

Acquisition

Acquisition is the process through which one company takes over the

controlling interest of another company. Acquisition includes obtaining supplies

or services by contract or purchase order with appropriated or non-appropriated

funds, for the use of Federal agencies through purchase or lease.

Venture Capital

Venture Capital is the money and resources made available to startup

firms and small businesses with exceptional growth potential. Most venture

capital money comes from an organized group of wealthy investors.

-49-

Underwriter

Lead Merchant Banker shall ensure that the underwriters appointed or

proposed to be appointed are capable of discharging their obligations under the

Issue.

Clause 5.5.3 requires the Lead Merchant Banker to underwrite a minimum of

5% of the total underwriting commitment of Rs. 25 Lakh, whichever is less.

However, under no situation, a BRLM can underwrite more than 20 times its

Net Worth at any point of time.

Non institutional bidders.

Companies, corporate bodies, Scientific institutions and trusts, resident

Indian Individuals HUF (in the name of Karta) and NRIs (Applying for an

amount exceeding Rs.100000 )

Retail individual bidders

Individuals (including NRIs and HUFs) applying for an amount up to

Rs.100000.

FPO

FPO means following public offer when a company goes for an public

offer after going for an IPO it is known as Following Public Offer(FPO). It may

go for an public offer if it is again in requirement of funds for new projects, for

expansion or for dilution of holding of shares. -50-

IPO Grading

1 An unlisted company making an IPO of equity shares or any other

security which may be converted into or exchanged with equity shares at a later

date may opt to obtain grading for such an IPO from one or more credit rating

agencies.

.2 Where an issuer opts to obtain IPO grading under clause 5.6B.1, it shall

disclose all grades so obtained by it, including unaccepted grades, in the

prospectus and abridged prospectus.

-51-

Data Analysis and interpretation

-52-

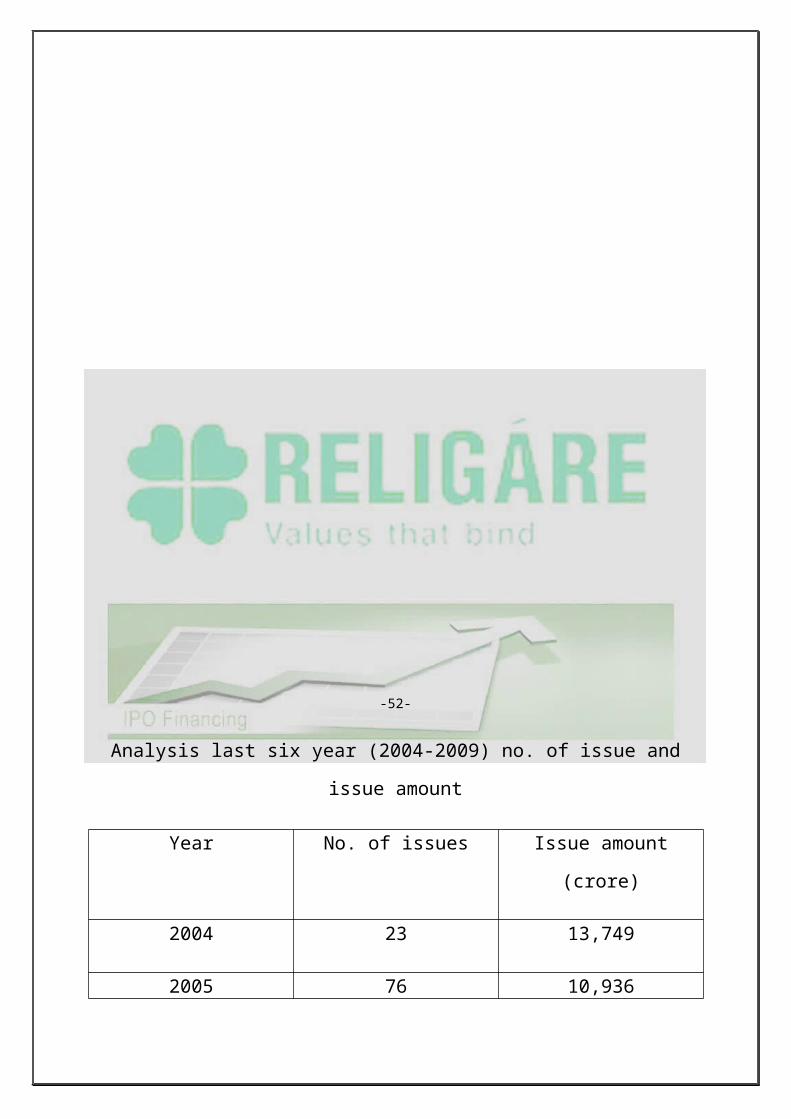

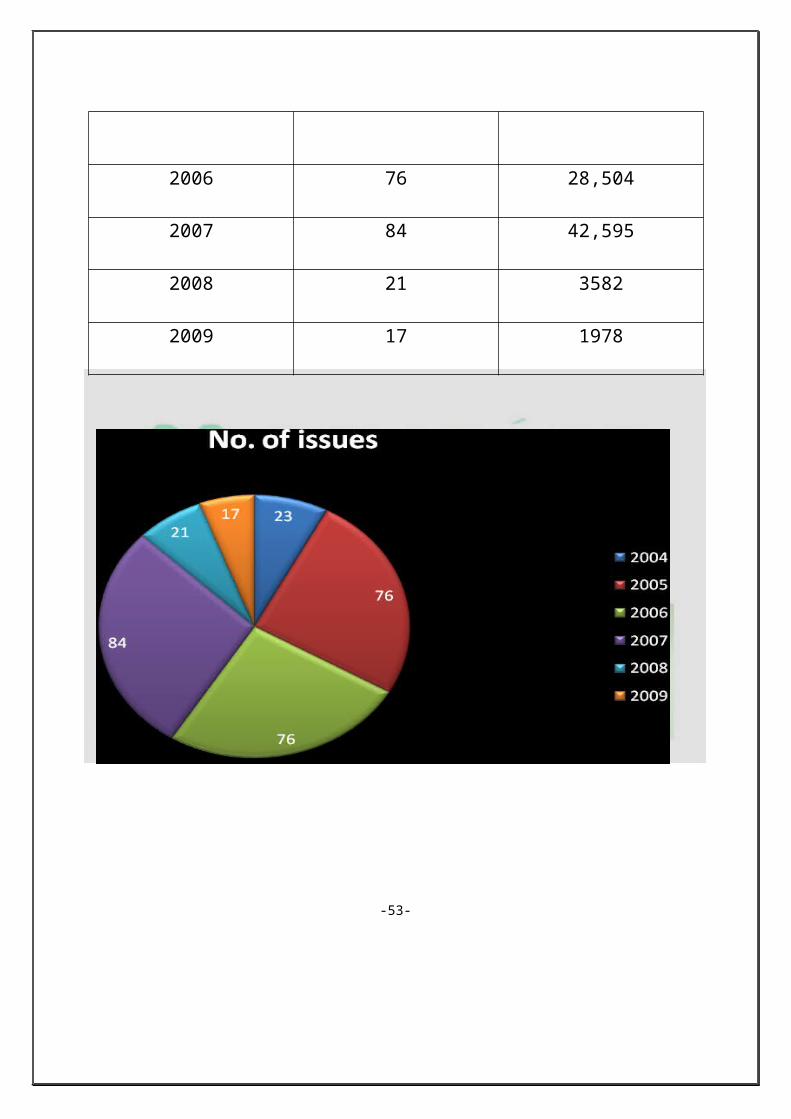

Analysis last six year (2004-2009) no. of issue and issue amount

Year No. of issues Issue amount (crore)

2004 23 13,749

2005 76 10,936

2006 76 28,504

2007 84 42,595

2008 21 3582

2009 17 1978

-53-

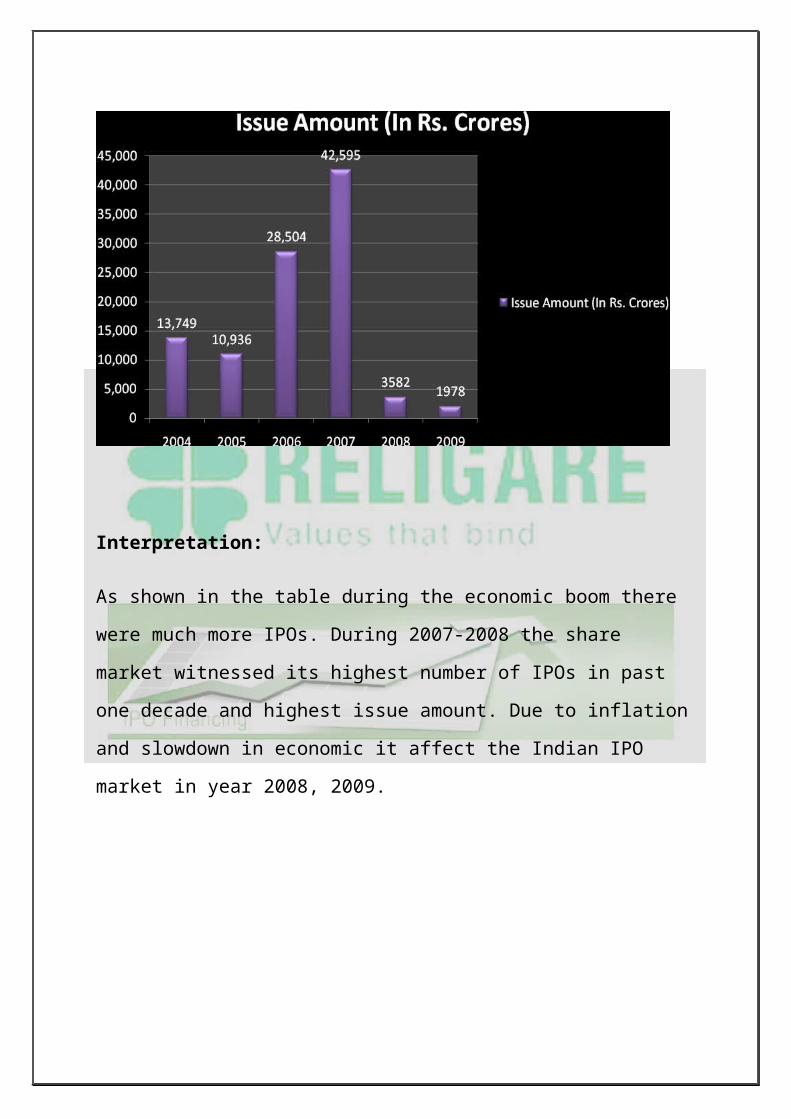

Interpretation:

As shown in the table during the economic boom there were much more IPOs.

During 2007-2008 the share market witnessed its highest number of IPOs in

past one decade and highest issue amount. Due to inflation and slowdown in

economic it affect the Indian IPO market in year 2008, 2009.

-54-

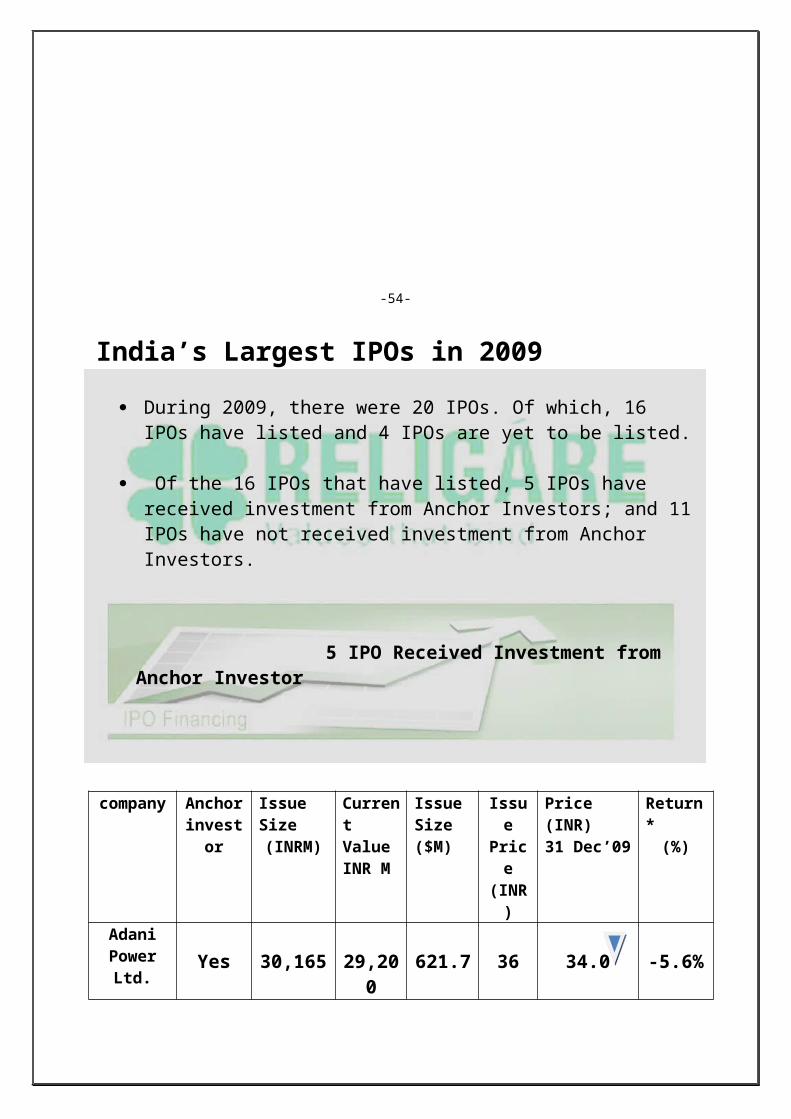

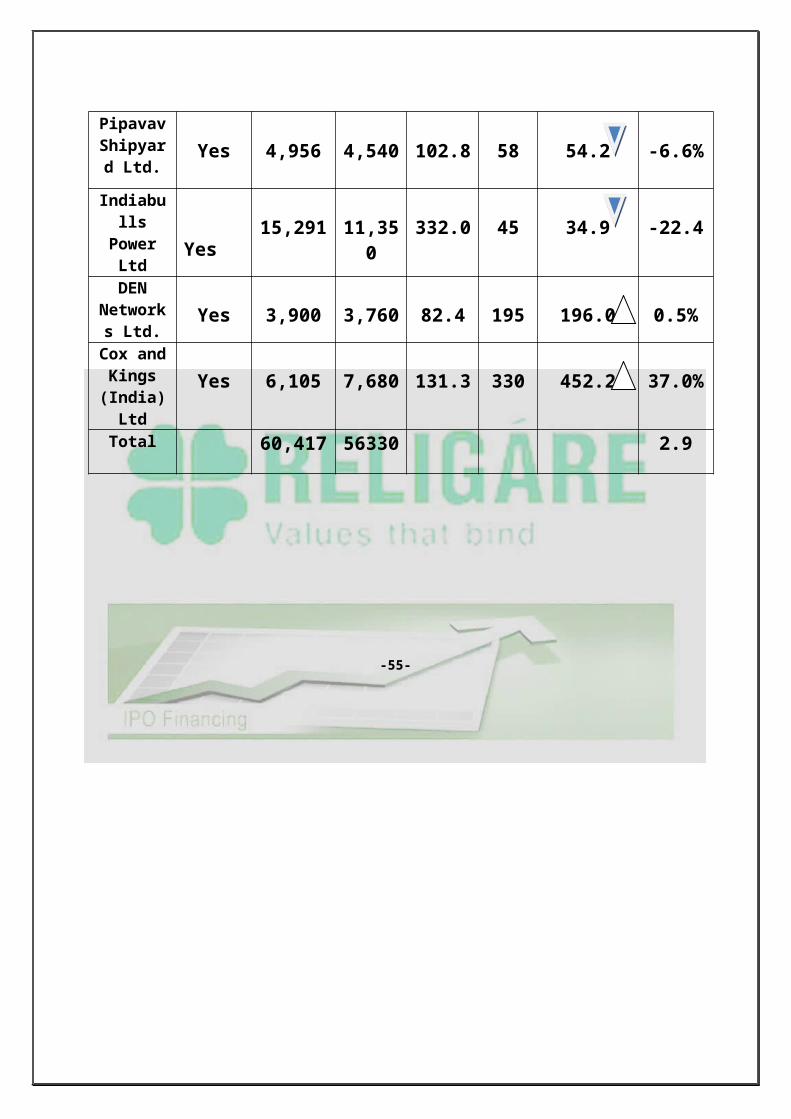

India’s Largest IPOs in 2009

During 2009, there were 20 IPOs. Of which, 16 IPOs have listed and 4 IPOs are yet to be listed.

Of the 16 IPOs that have listed, 5 IPOs have received investment from Anchor Investors; and 11 IPOs have not received investment from Anchor Investors.

5 IPO Received Investment from Anchor Investor

company Anchorinvestor

Issue Size(INRM)

CurrentValueINR M

Issue Size($M)

Issue Price (INR)

Price (INR)31 Dec’09

Return*(%)

Adani Power Ltd.

Yes 30,165 29,200 621.7 36 34.0 -5.6%

Pipavav Shipyard

Ltd.Yes 4,956 4,540 102.8 58 54.2 -6.6%

Indiabulls Power Ltd

Yes 15,291 11,350 332.0 45 34.9 -22.4

DEN Networks

Ltd.Yes 3,900 3,760 82.4 195 196.0 0.5%

Cox and Kings (India)

Ltd

Yes 6,105 7,680 131.3 330 452.2 37.0%

Total 60,417 56330 2.9

-55-

-56-

Interpretation

Of the 5 IPOs that have received investment from Anchor Investors, 3 IPOs are

trading below the issue price (that is 60% of such issues) and only 2 IPO is

trading above the issue price. On an aggregate basis, about Rs. 60417 Crores is

mobilized by such IPOs that have received anchor investors. However, the

current value of such IPOs is down to Rs. 5,6330 Crores, indicating a Mark-to-

Market loss of about Rs. 4087 Crores, indicating current Mark-to-Market profit

of 2.9 %.

11 IPOs have not received investment from Anchor Investors.

Sr.No Company AnchorInvestor

Issue Size(INRM)

Current value

Current MTM Return (%)

Profit Loss

1 Edserv Softsystems Ltd.

No 240 960 304.25% 1 0

2 Mahindra Holiday & Resorts India Ltd.

No 2,780 3,950 42.3% 1 0

3 Excel Infoways Ltd.

No 480 330 -30.88% 0 1

4 Raj Oil Mills Ltd

No 1,140 680 -40.25% 0 1

5 NHPC Ltd. No 60,385 54,350 -10% 0 1

6 Jindal Cotex Ltd.

No 844 1,140 35% 1 0

7 Globus Spirits Ltd.

No 750 710 -5.05% 0 1

8 Oil India Ltd.

No 27,772 32,800 18.10% 1 0

9 Euro Multivision Ltd.

No 660 270 -58.73% 0 1

10 Thinksoft Global Services Ltd.

No 460 1,070 135.36% 1 0

11 Astec Lifesciences Ltd.

No 620 640 3.35% 1 0

Total 96,131 96,900 0.81% 6 5

-58-

Particular Issue size (in Rs. Crs)

Current value (in Rs. Crs)

Return

(%)

IPO in Profit

IPO in Loss

Aggregate of IPOs with participation of Anchor Investors

60,417 56,330 2.9% 2 3

Aggregate of IPOs without participation of Anchor Investors 96,131 96,900 0.81% 6 5

Total 1,56,548 1,53,230 3.71% 8 8

-59-

Interpretation

Outof the 11 IPOs that have not received investment from Anchor investors, about 6 IPOs are trading above the issue price and 5 IPOs are trading below the issue price. The total amount that is mobilized by such IPOs that have not received investment from Anchor investors is about Rs. 9,6131 Crores. And, the current value of such IPOs is increased to about Rs. 9,6900 Crores, indicating a Mark-to-Market gain of about Rs. 769 Crores, indicating current Mark-to Market gain of +0.81%.

On an aggregate basis, total amount that is mobilized by 16 IPOs is about Rs. 1,56,548 Crores. And, the current value of such IPOs is decreased to Rs. 1,53,230 Crores, indicating a Mark-to-Market loss of Rs. 3,318 Crores, indicating current Mark-to-Market loss of 3.71%. In total, of the 16 IPOs, about 8 IPOs are in profit and 8 IPOs are in loss.

Even though the IPO market has tried to stage a comeback during 2009, the listing performances of several high profile companies has been disappointing, raising the concerns about the recovery of the primary market. Further, even the IPOs which could able to attract the anchor investors interest, couldn't able to fare well. In fact, the IPOs which have received the investment from Anchor Investors have underperformed in comparison to the IPOs which have not received the investment from Anchor Investors.

-60-

Sector Wise Comparison (Volume)

-61-

Interpretation

(REI) Healthcare and BFSI sector didn’t have any offering in 2009, but contributed more than 25% (in total volume) in 2008

2IPOs from (REI) and 1 each from (TMT) and Energy & power made their debut in 2009, but are to be listed in 2010

**Banking finance services & Insurance (BFSI)**Technology, Media & Telecommunication (TMT)**Real Estate & Infrastructure (REI)

-62-

IPOs: Sector Wise Comparison in 2009

2010 IPOs Issued and Listed in 2009

Sector* IPO Proceeds(INR M)

% of IPO Proceeds

IPO Volume % of IPO Volume

Energy& Power

105,842 67.5% 3 17.6%

Industrial 34,413 22.0% 5 29.4%

Hospitality 8,884 5.7% 2 11.8%

Telecom, Media & Technology

5,016 3.2% 3 17.6%

Consumer Goods & Retail

1,890 1.2% 2 11.8%

Outsourcing 482 0.3% 1 5.9%

Education 238 0.2% 1 5.9%

Total 156,765 100% 17 100%

IPO Volume

Interpretation

Out of the total Energy proceeds, NHPC IPO contributed 57%

Out of the total Industrial proceeds, OIL India IPO contributed 81%

Out of the total TMT*** proceeds, Den Networks IPO contributed 74%

-64-

Findings

&

Conclusion

-65-

Major Findings

An IPO can be a risky investment. For the individual investor, it is

tough to predict what the stock or shares will do on its initial day

of trading and in the near future since there is often little historical

data with which to analyze the company.

IPO’s are playing major role in the field of investment.

It can be observed that out of 16 companies, only 5 companies

have given positive returns on the date of listing.

Out of 16 companies, 11 IPOs have not received investment from

Anchor Investors.

As per sectors wise comparison out of 7 areas only 3 sector

(Energy & power, Industrial, and Telecom, Media & Technology)

gives better response.

As per sector wise comparison in year 2008 and 2009 out of 7

areas only 3 sectors (Education, energy & power and TMT) give

positive return.

In IPO process Intermediary (SEBI, NSE, BSE) play a vital role in

issue of IPO book building.

-66-

Conclusion

IPO is used by a company to raise its funds. The extra amount obtained from public may be invested in the development o f the company, although it costs a little to a company but it gives a way to get more money for long term investments.

The issue of an IPO by a Company involves a number of stages, each calling for a great deal of verification. The relevant and updated information on the Company has to be captured precisely in the Prospectus. The decision by the Investors on whether to invest in a Company is influenced significantly by the information contained in the Prospectus. The Regulatory Bodies are also involved and there are set procedures that must be followed. Legal compliance has to be maintained. Moreover, the Company’s potential should not be understated in or lost in the Prospectus because of the weight of such rules, regulations and formalities.

.In this project all the aspects of IPO have been studied like IPO norms, IPO

process and its regulatory aspect, Pricing Process, Factors and financial

parameters to watch before investing in an IPO.

Thus the objective of studying is achieved.

-67-

SUGGESTIONS

The investment in IPO can prove too risky because the investor does not know anything about the company because it is listed first time in the market so its performance cannot be measure.

On the other hand it can be said that the higher the risk higher the returns earned. So we can say that the though risky if investment is done then it can give higher returns as well.

Primary market is more volatile than the secondary market because all the companies are listed for the first time in the market so nothing can be said about its performance.

If higher risk is taken, it is always rewarded with the higher returns. So higher the risk the more the returns rewarded for it.

“We can fairly predict the future, but can’t make it happen as it is.”

-68-

BIBLIOGRAPHY

Websites:

www. bseindia.com

www.religareonline.in

www. business-standard.com

www.moneycontrol.com

www.nseindia.com

www.bseindia.com

http://www.theinvestor.tv/money/thebrokerageindustry.htm

http://www.economywatch.com/market/share-market/share-market

trading.html

Books & Journals:

NSE fact book 2009

Raising capital, second edition 2005, “GET THE MONEY YOU NEED

TO GROW YOUR BUSINESS, AUTHOR ANDREW J . SHERMAN

NSE Certification

BSE Certification

SEBI Guidelines- August - 2009

-69-

ANNEXURE

Top Companies: An analysis

Reliance Power IPO has been issued by Reliance Power Limited. Reliance Power IPO was issued on 15th January, 2008 and closed on 18th January, 2008. Reliance Power Limited Company is planning to generate capital worth Rs. 11, 700 crores through the IPO. This makes it the largest IPO in the country as on 17th January, 2008. The price band of the equity

shares of Reliance Power IPO has been fixed at Rs. 405- 450 per equity share.The total size of Reliance Power IPO is around 26 crores equity shares.Reliance Power IPO will be listed on the National Stock Exchange (NSE) and also on the Bombay Stock Exchange (BSE). The lead bankers of Reliance Power IPO are Enam Securities, Kotak Mahindra Capital Co, ABN Amro Rothschild, ICICI Securities, JP Morgan Chase & Co, UBS AG and Deutsche Bank AG.The main objective of Reliance Power IPO is that the proceeds from the issue will be used to fund the power generation projects that the company plans to carry out.

-70-

Kingfisher till date has not launched any IPO, but has expressed its wish to launch one soon. This IPO would be used to fund its aggressiveexpansion plans in India. The accumulated corpus would be utilized to fund its airline business and to payoff debt for its acquired liquor company Shaw Wallace & Company.The brand Kingfisher is being owned by the business conglomerate United Breweries Group. The brand is being used for two business entities – Airlines and Alcoholic Beverage. The Airlines operates under the name of "Kingfisher Airlines" and the alcoholic beverage segment manufactures "Beer" and "Mineral Water" under the same brand name. Till now the company has not launched any IPO to fund its aggressive expansion plans, but plans to launch it in near future to raise capital. Dr Vijay Mallya is the Chairman and CEO of both the segments. The Chief of the United Breweries Holding Ltd (UBHL), Mr Vijay Mallaya, said that the group would come up

with an Initial Public Offering in 2008 and would raise a total corpus of US$ 400 million. The Initial Public Offering of the Kingfisher Airlines would target a corpus of US$ 200 million and the rest would be raised through the IPO of the liquor business. Kingfisher Airline IPO, to be issued for the first time in the year 2008, to finance the airline's expansion and funding of A380s air fleet.

-71

The Maruti IPO has set a price range of Rs. 125 per share above the Floor price of Rs. 115. The subscription for Maruti IPO opened on June 12, 2003 and closed on June 19, 2003. The response to Maruti IPO was overwhelming within the subscription period, which led to an over-subscription of the public offerings of Maruti by more than ten times.

The government decided to shell out 85 percent shares of IPO to the noninstitutional investors and 15 percent shares to the non-institutional high networth individuals. Consequently, government would get Rs.993 crores for 7.94 crores shares. But SEBI recommended that 60 percent can be given to the institutional investors but at least 40 percent should be allotted for the retail investors as well. The government has allotted 60 percent shares to the retail investors and 40 percent shares to the institutional investors. The shares were allotted to the individuals on a pro rata basis. The IPO of Maruti is claimed to be one of the biggest capital market transactions in recent years in India and also the largest Book Built IPO that has been implanted in India till date. Maruti IPO received more than 300,000 applications which is a record in the history of IPO in India. The majority of applicants to these comprise of the Indian retail investors. They received the allotments on the basis of

the price range already fixed by the government. A huge number of institutional investors also paid a lot of importance in investing in Maruti.

-72-

DATA BASE COVERAGE 1990-91 to 2008-09 (19 years)

Year Amount in Rs (Crores)

No. of Issue

1990-1991 2251 2091991-92 3851 3161992-93 12630 4881993-94 9306 3841994-95 6793 3511995-96 6520 2911996-97 2724 1311997-98 1703 491998-99 568 26

1999-2000 1560 282000-01 729 272001-02 1041 132002-03 431 122003-04 1006 222004-05 3616 262005-06 4126 362006-07 3704 382007-08 13519 23

76,078 2,470

-73-

IPO GLOSSARY

A

AllocationThis is the amount of stock in an initial public offering (IPO) granted by the underwriter to an investor.

AftermarketTrading in the IPO subsequent to its offering is called the aftermarket.

Aftermarket Orders Underwriters look favorably on investors who buy IPOs in the days after the IPO first goes public. While underwriters cannot solicit aftermarket orders, some expect investors to purchase two or three times their IPO allocation in the aftermarket.

BBoard of DirectorsThe composition of the Board of Directors is particularly critical for an IPO. Typically, a board is composed of inside and outside directors.

Broken IPOsIf an IPO trades below its IPO price in the aftermarket, it is said to be a broken IPO.

CCalendarThis refers to upcoming IPOs and secondary offerings. Brokerage houses have equity calendars, bond calendars and municipal calendars.

Clearing PriceThe price at which all shares of an IPO can be sold to investors in a Dutch Auction. Sometimes referred to as the “market clearing price”.

-74-

FFirst Day CloseThe closing price at the end of the first day of trading reflects not only how well the lead manager priced and placed the deal, but what the near-term trading is likely to be.

FloatWhen a company is publicly traded, a distinction is made between the total number of shares outstanding and the number of shares in circulation, referred to as the float. The float consists of the company's shares held by the general public.

GGreen ShoeA typical underwriting agreement allows the underwriters to buy up to an additional 15% of shares at the offering price for a period of several weeks after the offering. This option is also called the overallotment and is exercised when the IPO is oversubscribed and trading above its offer price. The term comes from the Green Shoe Company, which was the first to have this option.

HHot IssueWhen there is significantly more demand than supply for an IPO it is said to be a hotissue.

IInitial Public OfferingThis is the event of a company first selling its shares to the public.

InsidersManagement, directors and significant stockholders are regarded as insiders because they are privy to information about the operations of a company not known to the general public.

IPO Price

Individual investors often ask why the price at which an IPO starts trading is different from its offer price. This occurs because the offer price is set by the underwriters before the stock starts trading. Once the stock starts trading, the price is determined by actual supply and demand and can be higher or lower.

-75-

IPO ResearchPrior to the offering, the underwriters involved in the IPO are prohibited from issuing research or recommendations for forty days. Following the IPO, the underwriter is allowed to issue a research report

M-NThe total market value of a firm. It is defined as the product of the company's stock price per share and the total number of shares outstanding

Market ValueThe market value of a company is determined by multiplying the number of shares outstanding by the current price of the stock.

OOffering PriceThis is the price at which the IPO is first sold to the public. It is set by the lead manager, usually after the close of stock market trading the night before the shares are distributed to IPO buyers. In the case of some foreign IPOs, the pricing occurs over the weekend.

OversubscribedWhen a deal has more orders than there are shares available it is said to be oversubscribed.

PPreliminary ProspectusThis is the offering document printed by the company containing a description of the business, discussion of strategy, presentation of historical financial statements, explanation of recent financial results, management and their backgrounds and ownership.

ProceedsCompanies go public to raise money. The money raised is referred to as proceeds.

R

Red HerringThis is the term of art for the preliminary prospectus. It gets its name from the printed red disclaimer on the left side of the prospectus.

-76-

U-VUnderwriterThis is a brokerage firm that raises money for companies using public equity and debt markets. Underwriters are financial intermediaries that buy stock or bonds from an issuer and then sell these securities to the public.

Venture CapitalFunding acquired during the pre-IPO process of raising money for companies. It is done only by accredited investors.

-77-

Related Documents