PROJECT ON MCB BANK LIMITED 03143046412 MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

PROJECT ON MCB BANK LIMITED 03143046412

MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 1

PROJECT ON MCB BANK LIMITED 03143046412

PROJECT: BANKING SECTOR MCB BANK (Ltd.)

SUBMITTED TO:

DR. MOHAMMAD KHANPROFESSOR OF MANAGEMENT OF SEIENCES

MOHI-UD-DIN ISLAMIC UNIVERSTIYAZAD JMMU & KASHIR

SUBMITTED BY:

Muhammad AamirMBA (Finance)

ROLL NO. 220046

SESSION: 2009-2010

REGISTERATION NO.

08-PFD-8721

MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 2

PROJECT ON MCB BANK LIMITED 03143046412

Dedicated to

MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 3

Holy Prophet (PBUH)[Greatest Reformer]

&

My Precious Parents

PROJECT ON MCB BANK LIMITED 03143046412

No.

Title Pages

1 Definition 052 History Of Bank 063 History Of MCB Bank 094 Vision 135 Mission 146 Management Committee 157 Marketing Mix 208 Product Mix & Prices 219 Placing Strategies 3010 Departments 3311 First Two Weeks 4812 Next Two Weeks 5413 Last Two Weeks 5614 Financial Statement Analysis 5915 Time Series Analysis 7516 Swot Analysis 7617 Suggestions 7818 References 81

MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 4

PROJECT ON MCB BANK LIMITED 03143046412

DEFINITION OF BANK

The term 'bank' is being used for a long time, yet it has no precise definition. The basic reason is that the commercial banks perform not just one but many types of functions. The term bank has been defined differently by different authors. Some are as follows:

According to Crowther, "Bank is a dealer in debts—his own and of other people."

According to G.W. Gilbert, "A banker is a dealer in capital or more properly a dealer in money. He is an intermediate party between the borrower and the lender. He borrows from one party and lends to another."

According To Bamkinh Companies OrdinanceU/s3 (B) of Banking Companies Ordinance 1962 "Banker means person transacting the business of accepting for the purpose of lending or investment, of deposits of money from the public, repayable on demand or otherwise and withdraw able by cheque, draft, order or otherwise and includes any Post Office Savings Bank."

HISTORY OF BANKING IN PAKISTAN

MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 5

PROJECT ON MCB BANK LIMITED 03143046412

The interesting point which I observed during the span of mine internship was the historical background of Banking & Financial sector which is the one in which great improvement and growth is observed since the formation of Pakistan. For studying the growth of this sector we can divide it into three stages, which are as followsa) Pre-Nationalization Erab) Nationalization Erac) Post Nationalization Era

A) Pre Nationalization Era There were only two Muslim banks in Indo Pak before partition, they were;Habib Bank Ltd. (estd. in 1941 at Bombay) & Australia Bank Ltd. (estd. In 1944 at Lahore). Hindus or Foreigners either owned all other banks, at that time.At the time of partition there were 631 bank branches in area, which came under Pakistani control. But due to blood shed and violence at large scale, mostly branches were closed and the disparity can be assessed from the fact that on July 1948 there were 195 branches with deposits of Rs.88 crore (880 million) only. Also a factor lagging in Pakistani industry was a central bank of its own, by that time Reserve Bank of India was acting as central bank for both countries and same currency notes were used in both territories. But Reserve Bank of India was biased and Set down Pakistan on many occasions such as the issue of funds transfer etc.The private sector also responded to these changes and some very positive changes were observed. Some of the steps taken by the government in this regard were as under:

i. Inauguration of State Bank of Pakistan (SBP) on 1st July, 1948.

ii. Setting up of National Bank of Pakistan in November, 1949 to control the 'jute' export in East Pakistan and to act as agent of SBP.

iii. Larger powers were given to SBP through SBP Act (1956) for controlling purposes.

MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 6

PROJECT ON MCB BANK LIMITED 03143046412

iv. Banking Companies Ordinance 1962 for protection and guidance to banks.

v. Establishment of specialized banks, such as ADBP (1952); a) HBFC (Nov, 1952); b) P1CIC (Oct, 1957) c) IDBP (Aug. 1961); d) NDFC (Jan, 1973).

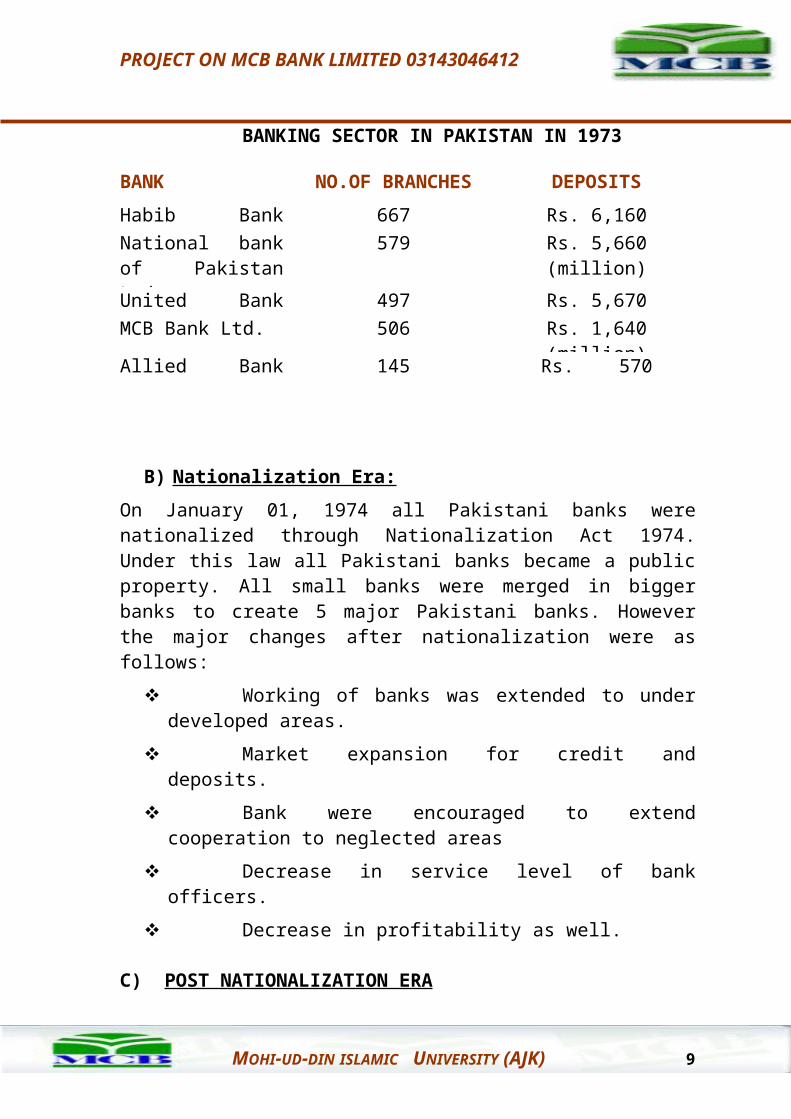

These were the steps, which built a strong banking sector in Pakistan. This is also obvious from the facts that by 1973 there were almost 10 foreign banks were working in Pakistan and all over deposit position was around Rs.2300 crore (23,000 million). A bird eye view of 5 top banks was as given below:

BANKING SECTOR IN PAKISTAN IN 1973

BANK NO.OF BRANCHES DEPOSITSHabib Bank Ltd. 667 Rs. 6,160 (million)National bank of Pakistan Ltd.

579 Rs. 5,660 (million)

United Bank Ltd 497 Rs. 5,670 (million)MCB Bank Ltd. 506 Rs. 1,640 (million)Allied Bank Ltd. 145 Rs. 570 (million)

B) Nationalization Era: On January 01, 1974 all Pakistani banks were nationalized through Nationalization Act 1974. Under this law all Pakistani banks became a public property. All small banks were merged in bigger banks to create 5 major Pakistani banks. However the major changes after nationalization were as follows:

Working of banks was extended to under developed areas.

MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 7

PROJECT ON MCB BANK LIMITED 03143046412

Market expansion for credit and deposits. Bank were encouraged to extend cooperation to

neglected areas Decrease in service level of bank officers. Decrease in profitability as well.

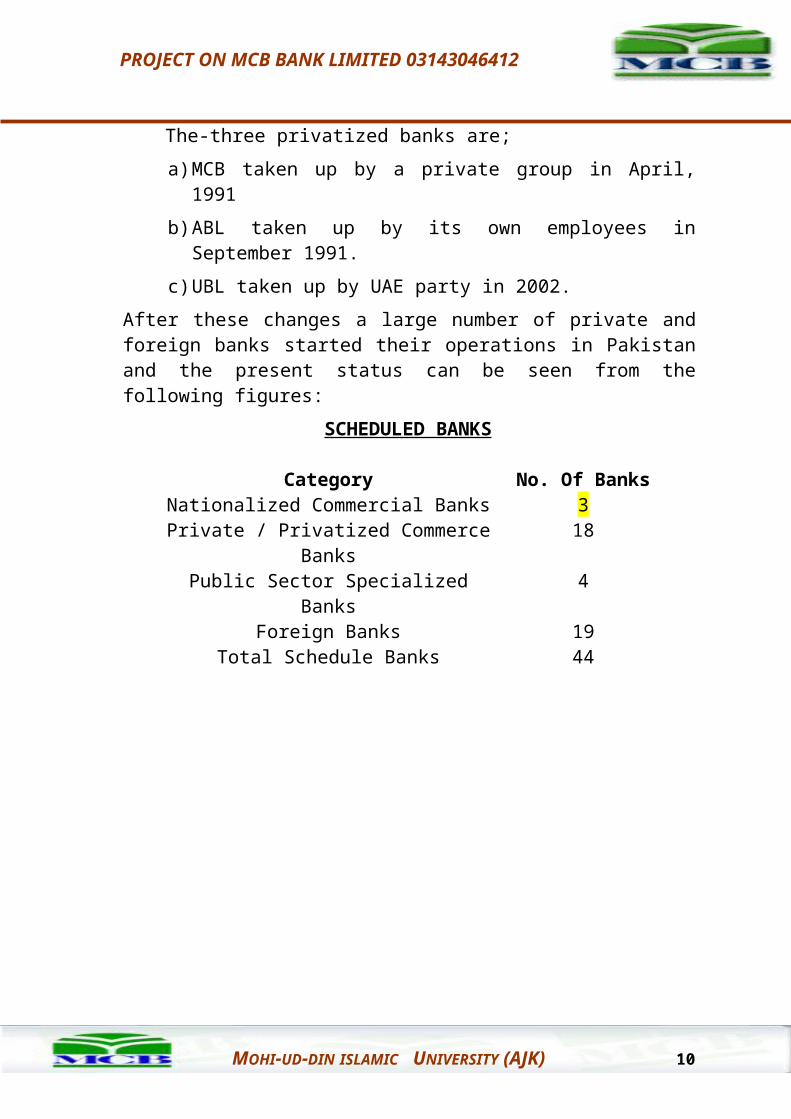

C) POST NATIONALIZATION ERAThe-three privatized banks are; a) MCB taken up by a private group in April, 1991b) ABL taken up by its own employees in September

1991.c) UBL taken up by UAE party in 2002.

After these changes a large number of private and foreign banks started their operations in Pakistan and the present status can be seen from the following figures:

SCHEDULED BANKS

Category No. Of BanksNationalized Commercial Banks 3Private / Privatized Commerce

Banks18

Public Sector Specialized Banks 4Foreign Banks 19

Total Schedule Banks 44

MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 8

PROJECT ON MCB BANK LIMITED 03143046412

HISTORY OF THE MCB BANK LIMITED

Before separation of Indo Pak, the need for more Muslim banks was felt. And Muslims having strong financial capacity were thinking to invest in this sector as well. This was the idea which paved the way for setting up MCB Bank Ltd known as MCB. This was the third Muslim bank in the subcontinent.HISTORYThis bank was incorporated under companies’ act 1913 on 9 th July, 1947 (just before partition) at Calcutta. But due to changing scenario of the region, the certificate of incorporation was issued on 17 th August, 1948 with a delay of almost 1 year; the certificate was issued at Chitagong. The first Head office of the company was established at Dacca and Mr. G.M. Adamjee was appointed its first chairman. It was incorporated with an authorized capital of Rs. 15 million.After some time the registered office of the company was shifted to Karachi on August 23rd, 1956 through a special resolution, now recently the Head office of MCB has been transferred to Islamabad in July, 1999 and now Head office is termed as Principle Office. This institute was nationalized with other on January 1st, 1974. At that time it had 506 branches and deposits amounting to Rs. 1,640 million. Although. MCB has a reputation of a conservative bank but nationalization also left its effects on this institute as well and by end of year 1991 in which it was privatized the total number of branches were 1.287 and deposits amounting to as high as Rs. 35,029 million

MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 9

PROJECT ON MCB BANK LIMITED 03143046412

PRIVATIZATIONWhen privatization policy was announced in 1990, MCB was the first to be privatized upon recommendations of World Bank and IMF. The reason for this choice was the better profitability condition of the organization and less risky credit portfolio which made'' it a good choice for investors. On April 8th, 1991, the management control was handed over to National Group (the highest bidders). Initially only 26% of shares were sold to private sector at Rs. 56 per share. AFTER PRIVATIZATIONTen years after privatization, MCB is now in a consolidation stage designed to lock in the gains made in recent years and prepare the groundwork for future growth. The bank has restructured its asset portfolio and rationalized the cost structure in order to remain a low cost producer. After privatization, the growth in every department of the bank has been observed. Following are some key developments:

Launching of different deposit schemes to increase saving level.

Increased participation on foreign trade. Betterment of branches and staff service level. Introduction of Rupee Traveler Cheques & Photo Credit

Card for the first time in Pakistan.

MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 10

PROJECT ON MCB BANK LIMITED 03143046412

MCB BANK TODAYMCB today, represents a bank that has grown with time, experience and Pakistan. A major financial institution, in scope and size, it symbolizes a fully growing tree evergreen, strong, and firmly rooted.

FOREIGN TRADEThe bank conducted import business during the year amounting to RS. 54.0 billion As compare to RS. 56.4 Billion In 2009. The export business slightly improves to RS. 36.9 Billion From RS. 35.1 Billion. In 2009. Home remittances decline to RS. 16.7 Billion From 30.7 Billion the decline in home remittances business was due to freezing of Foreign Currency Accounts, which has affected the confidence of Pakistanis working overseas.

YEAR 2009 COMPLIANCEMCB’s strength lies in providing a technological base at the gross root level of the society with a challenge to educate and assimilate such systems across vast cultural and economic backgrounds. With over 768 automated branches, 263 online branches, over 151 MCB ATMs in 27 cities nationwide and a network of over 16 banks on the MNET ATM switch and now in 2010 all branches become online, MCB continuously innovates new products and services that harness technology for the customer’s benefits.

SOCIAL SECTORThe bank activity participating in the Prime Minister self-employment Scheme. The application received from various applicants is being processed on merit and disposed off as quickly as possible.

THE BUSINESS MCB is in it’s over 50 years of operation. It has a network of over 1,000 branches all over the country with business establishments in Sri Lanka and Bahrain. The branch break- MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 11

PROJECT ON MCB BANK LIMITED 03143046412

up province wise is Punjab (57%), Sindh (21%), NWFP (19%) and Blochistan (3%) respectively. MCB has an edge over other local banks, as it was the first privatized bank. The State Bank of Pakistan has restricted the number of branches that can be opened by foreign banks, an advantage that MCB capitalizes because of its extensive branch network. Nineteen years after privatization, MCB is now in a consolidation stage designed to lock in the gains made in recent years and prepare the groundwork for future growth. The bank has restructured its asset portfolio and rationalized the cost structure in order to remain a low cost producer. MCB now focuses on three core businesses namely Corporate, Commercial and Consumer Banking. Corporate clientele includes public sector companies as well as large local and multi national concerns. MCB is also catering to the growing middle class. MCB looks with confidence at year 2010 and beyond, making strides towards fulfillment of its mission, "to become the preferred provider of quality financial services in the country with profitability and responsibility and to be the best place to work".A major achievement of MCB is that the state bank of Pakistan has issued a license to MCB to start Islamic banking. MCB was setting up a 1st Islamic banking branch at 1st floor shaheen complex, Karachi. This complex was started working from September 1, 2003.

Vision StatementTO BE THE LEADING FINANCIAL SERVICE PROVIDOR

PARTANING WITH OUR CUSTOMER FOR A MORE

PROSPER AND SECURE FUTURE

MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 12

PROJECT ON MCB BANK LIMITED 03143046412

MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 13

PROJECT ON MCB BANK LIMITED 03143046412

Mission StatementTo become the preferred provider of quality financial services in our country with the profitability and responsibility and to be best place to work

Management Committee

MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 14

PROJECT ON MCB BANK LIMITED 03143046412

MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 15

PROJECT ON MCB BANK LIMITED 03143046412

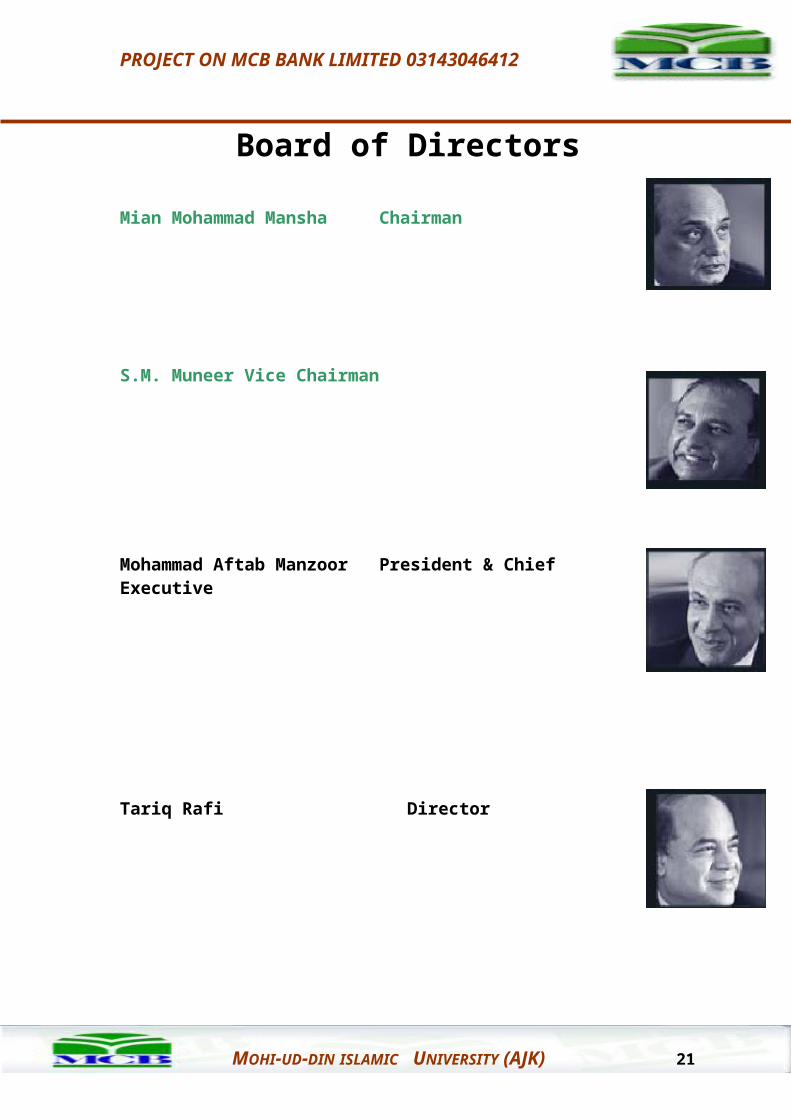

Board of DirectorsMian Mohammad Mansha Chairman

S.M. Muneer Vice Chairman

Mohammad Aftab Manzoor President & Chief Executive

Tariq Rafi Director

MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 16

PROJECT ON MCB BANK LIMITED 03143046412

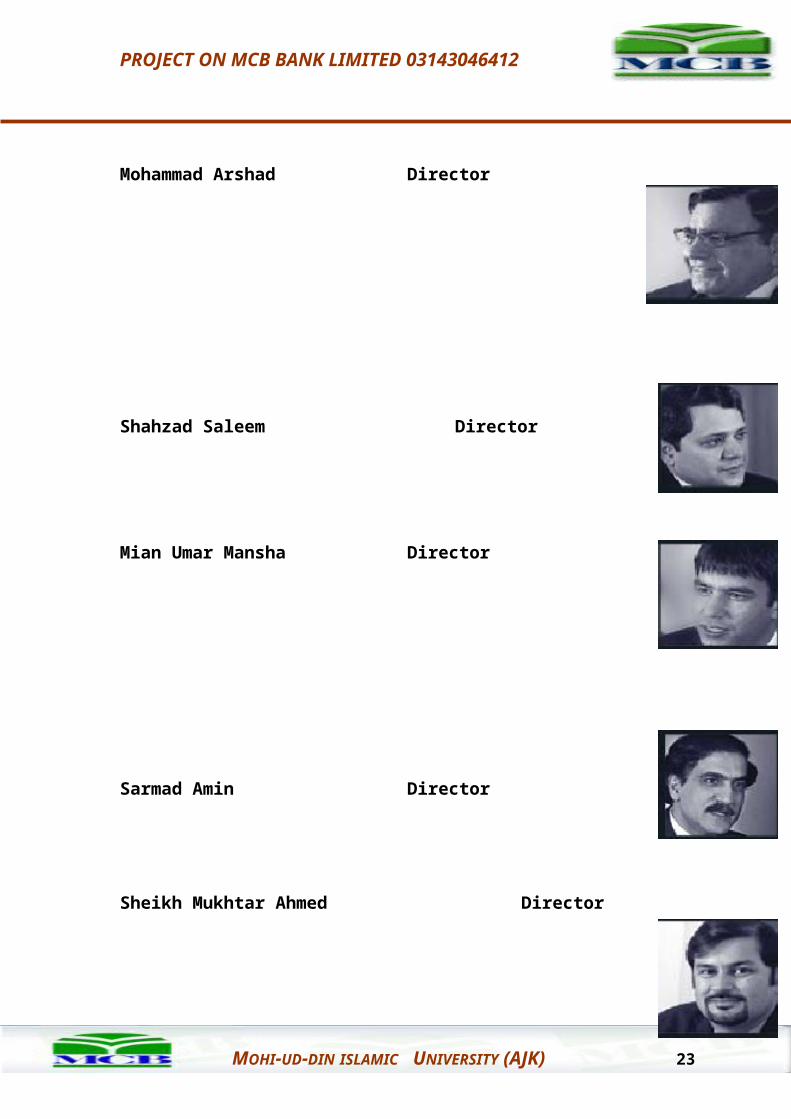

Mohammad Arshad Director

Shahzad Saleem Director

Mian Umar Mansha Director

Sarmad Amin Director

Sheikh Mukhtar Ahmed Director

MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 17

PROJECT ON MCB BANK LIMITED 03143046412

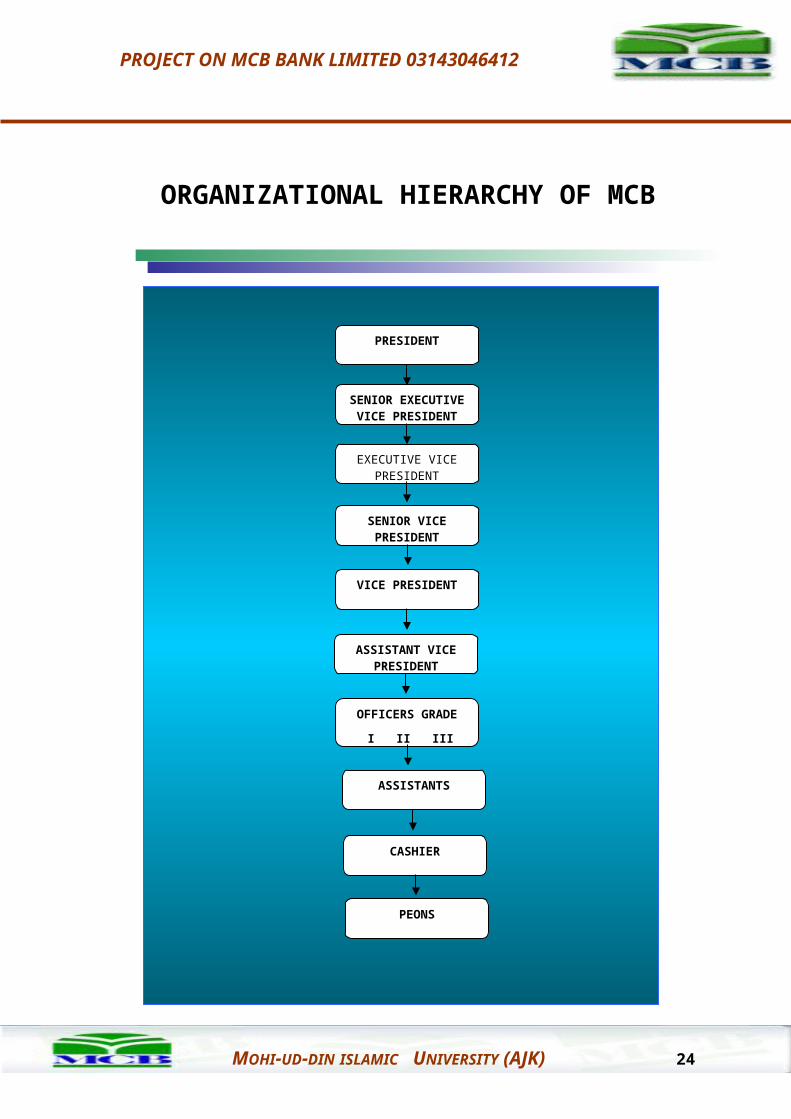

ORGANIZATIONAL HIERARCHY OF MCB

MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 18

PRESIDENT

EXECUTIVE VICE PRESIDENT

SENIOR EXECUTIVE VICE PRESIDENT

SENIOR VICE PRESIDENT

OFFICERS GRADE

I II III

VICE PRESIDENT

ASSISTANT VICE PRESIDENT

CASHIER

ASSISTANTS

PEONS

PROJECT ON MCB BANK LIMITED 03143046412

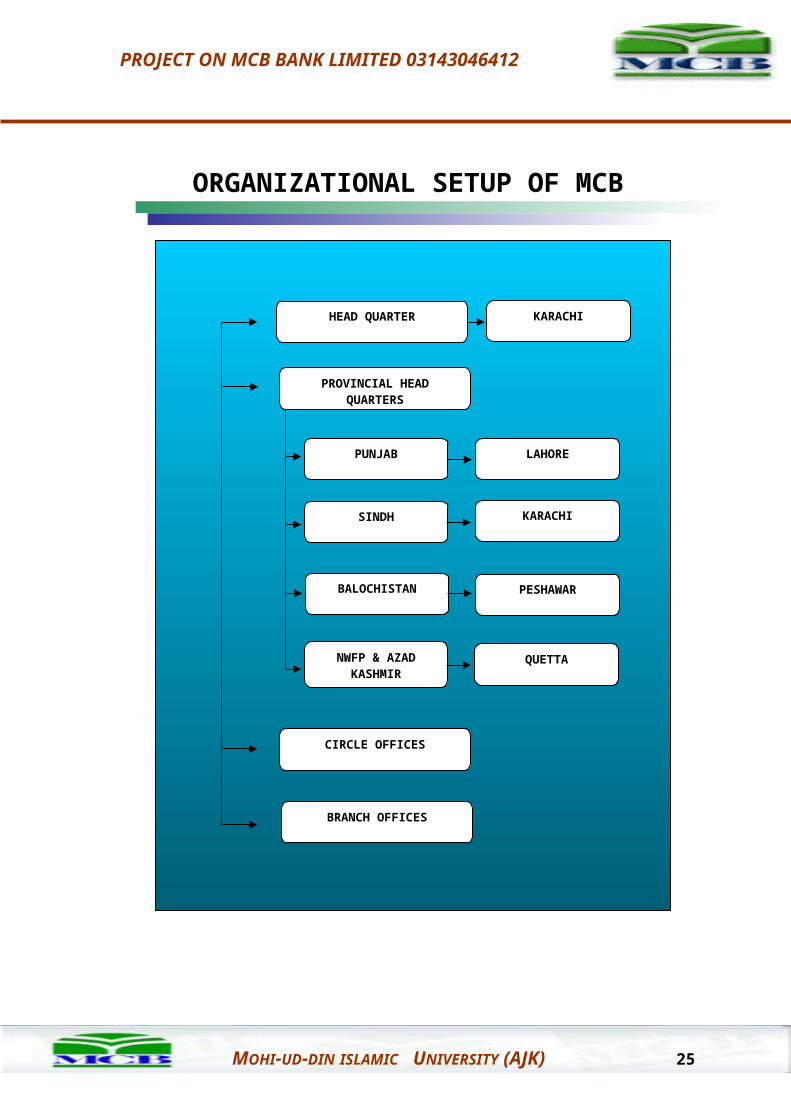

ORGANIZATIONAL SETUP OF MCB

MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 19

PUNJAB

NWFP & AZAD KASHMIR

SINDH

BALOCHISTAN

KARACHI

LAHORE

PESHAWAR

PROVINCIAL HEAD QUARTERS

QUETTA

HEAD QUARTER

CIRCLE OFFICES

BRANCH OFFICES

KARACHI

PROJECT ON MCB BANK LIMITED 03143046412

MARKETING MIX OF MCB BANK LIMITED

Marketing is the task of creating, promoting and delivering goods and services to consumers and businesses. Organizations identify and profile distinct group of buyers who might prefer or require varying products and marketing mixes. The customer seeks for value and satisfaction. The organizations can increase the value of the customer offering in several ways e.g. raising benefits, reducing costs etc. marketing mix is a set of marketing tools that the firm uses to pursue its marketing objectives in the target market. These marketing tools are known as 4 ps of marketing. These four marketing tools are viewed as 4c’s by the consumers.

4 P’s 4 C’sProduct/ Service Customer Solution

Price Customer CostPlace Convenience

Promotion CommunicationTo identify the customer needs and fulfilling hem is the basic objective of an organization. Marketing is not just satisfying your customers, you have to delight them and this can be done by acting upon this phrase. “Under Promise and Over Deliver”MCB Bank provides a winning combination of products and services to its prime customers. It is one of the country’s leading commercial banks, which ensures complete security, and reliability in all-financial transactions.

MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 20

PROJECT ON MCB BANK LIMITED 03143046412

PRODUCT MIX & PRICES OF MCB BANK

1.MCB Rupee Traveler Cheque

MCB Rupee Travelers Cheques are as good as cash, infact better. Better because with Rupee Travelers Cheques you have the power to purchase and a feeling of security that should you lose them, you will get a refund.MCB Rupee Travelers Cheques are accepted at major shops, travel agents, hotels, business establishments and MCB branches all over Pakistan. You don't have to be an MCB account holder to buy the Rupee Traveler Cheques. Anybody can purchase them. It's a safe and convenient way to conduct everyday business. At a time when thefts and robberies are on the increase, you are better off carrying Travelers Cheques rather than money.

2.Mahnama Khushali SchemeA 5- year fixed Deposit Scheme, targeted to persons with small savings who would desire a regular monthly return on their investment.

Salient Features Minimum amount of investment shall be Rs.0.010m and

the maximum amount of investment would be Rs. 1.000m.

Khushali Certificates can be purchased by individuals (singly or jointly) or by the Proprietorship/Partnership concerns or Companies, etc. in their name

The Khushali Certificate will be of five years maturity. The interim rate of profit offered will be minimum 1%

per month. If the profit declared by the bank is higher, additional profit will be paid.

MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 21

PROJECT ON MCB BANK LIMITED 03143046412

Zakat will be deducted wherever applicable on yearly basis whether you will be receiving your profit or encashing your certificates.

As per Government Directions, tax on the profit / return is to be deducted by MCB branches at the time of payment.

3.MCB Khushali Bachat Account

Salient Features 8% rate of return per annum. Returns calculated on daily. Average balance and paid half yearly. Introduced first time in Pakistan. The facility of helping account holders pays utility bills

(electricity, telephone and gas) through their account. No queues. No delays.

4.Prime Currency Account Scheme Launched to attract deposits in foreign currencies. US Dollars, Pound Sterling, Euro and Japanese Yen.Salient Features

Owing foreign currency account under the Prime Currency Scheme allows you to earn attractive rates of interest in foreign currency.

You have a choice between opening this account in your personal name and opening it under joint names.

Whether you are a resident or a non-resident Pakistan, MCB Prime Currency Scheme invites all to operate a foreign currency account.

Foreign nationals and foreign companies can also open a foreign currency account under the Prime Currency Scheme.

MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 22

PROJECT ON MCB BANK LIMITED 03143046412

Your foreign currency account can be opened in four global currencies: The United States Dollar, the Pound Sterling, the Japanese Yen and the Euro.

Travellers Cheques and Foreign Currency Notes can also be issued to holders of personal and Joint accounts.

Rupee Loan facility will also available against this account.

You can draw any amount of foreign exchange from your foreign currency account and transfer or remit the amount freely to any part of the world without any restrictions.

The restrictions imposed by the State of Pakistan for the opening of foreign currency accounts in case of passport; Work-permit and resident Visa have been withdrawn. Your account will be restriction free.

The Prime Currency Scheme is exempt from all forms of taxes including Income Tax, Wealth Tax and Zakat deductions.

MCB Prime Currency Scheme is a world in itself.

5.Hajj Mubarak Scheme A saving scheme, of 2/3 years duration, for the convenience of persons, with a limited income, who desire to perform Hajj was introduced.Under the 2 years scheme, a monthly deposit of Rs.2800 is required, whereas under the 3 years scheme, the required monthly deposit is only Rs.2200

6.Capital Growth Certificate Scheme For long term depositors under which the amount deposited almost doubles at the end of 5 years. For the scheme, the minimum amount of deposits is Rs. 100000 while there is no maximum limit.

MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 23

PROJECT ON MCB BANK LIMITED 03143046412

In case of premature encashment of the certificate, the depositor will profit at the same rates as that of PL Saving Account.

7.Fund Management Scheme This scheme is offered to corporate and customers and is aimed at providing better rate of return up to 15% per annum. One of the objectives of the scheme is to develop secondary market for Government Securities.

8.Consultancy Services In the process of privatization of public sector units, prospective buyers need professional assistance and MCB, with its expertise, offers to them specialized service for valuation of the market value of the industrial unit, preparing bid documents and arranging finance for the purchase of the unit.

9.Self Supporting Scheme For the benefits of genuine worker/borrowers who are poor and needy and for small entrepreneur the bank as evolved a self supporting scheme: maximum amount of loan Rs.25000 and minimum Rs.5000 per individual. Loan will be totally free of mark-up.

10. Fax Press This product was first of its kind introduced by using modem technology of The Fax Machine. It facilitates speedy transfer of funds within Pakistan. The service guarantees transfer of from one city to another, within an hour.

11. Utility Bill Collection With the aim of extending this service to wider range of customers, the number of MCB branches collecting Utility Bills more than 900.

12. MCB Mobile Banking

MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 24

PROJECT ON MCB BANK LIMITED 03143046412

At the forefront of technological excellence, MCB proudly introduces MCB MOBILE BANKING*. The convenience of accessing account balance information and mini statements whenever want or wherever may need them, with comfort and peace of mind.MCB Mobile Banking service is available to all MCB ATM cardholders, 24 hours - 365 days.

MOBILE BANKING AT A GLANCEMCB Mobile Banking gives easy and quick access to account(s) at a time find convenient, including all holidays.

WITH MCB MOBILE BANKING· Check balance· View the last 4 transactions of your MCB account(s).

A FREE SERVICE MCB Mobile Banking is a free service for MCB account holders who have an ATM card of an SMS message if charged by the service provider.

BANKING AT FINGERTIPS Dial in anytime to get information regarding balance and mini statements.

13. MCB Islamic Banking Services Islamic banking services through exclusive units/branches offering a range of liability and asset based Sharia compliant products like Musharika, Murabaha, Ijara and Istasana.

14. MCB Car Cash Car financing and leasing at competitive rates with flexible options Car cash finances both semi-commercial and non-commercial vehicles for personal and business use.

15. MCB Locker

MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 25

PROJECT ON MCB BANK LIMITED 03143046412

The best protection for your valuables. Lockers of different capacities are available nationwide

16. MCB Master Card THE FUTURE OF MONEY Since the beginning of time, people have tried to find more convenient ways to pay, from gold to paper money and checks. Today, money is moving away from distinct hard currencies and towards universal payment products that transcend national borders, time zones, and, with the Internet, even physical space.Plastic or "virtual" money, credit, debit, and electronic cash products, inevitably will displace cash and checks as the money of the future.

MasterCard International has expanded globally in more locations in the world than any other card. The card was introduced by MCB Bank Limited in 1995 and now offers card members over 15 million outlets in 232 countries.

MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 26

PROJECT ON MCB BANK LIMITED 03143046412

Photo security- The first bank in Pakistan to introduce the enhanced feature of photograph on the card limiting fraud in case of card loss.

Welcomed at over 3, 000 outlets in Pakistan.

Provides up-to 45 days Free Credit.

Joining and Annual Fees to suit you.

24 Hour Customer Services- Call 111-700-700 and you can get information from our customer services representatives on new card application or have your queries resolved anytime of the day.

Cash Advance Facilities

Available in Pakistan and worldwide with a network of over 1,000 branches and a team of dedicated professionals, MCB is Pakistan’s largest private sector commercial bank.Our Consumer Banking provides customers with innovative saving schemes, products and services. Our ATM network is the largest in Pakistan and our Pak Rupee Travelers Cheques are market leaders. We were the first to introduce the photo card with the introduction of the MasterCard.Our Corporate Banking ensures assistance from a dedicated team of professional financial advisors for underwriting, project finance or corporate advisory services.When it comes to banking practices, you can depend on us. We’ve been around for over fifty years.

17. MCB Smart Card MCB now brings you MCB SmartCard -a secure and convenient instrument of payment with unmatched functionalities. It provides 24-hour direct access to your bank account

The convenience and flexibility of MCB SmartCard will help live a smarter life. It not only helps you manage your expenses, but also avoids undue interest on your day to day credit card transactions. MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 27

PROJECT ON MCB BANK LIMITED 03143046412

Your balance is always within your reach and you spend accordingly.

MCB is the only bank to introduce a debit card that gives the option to choose from domestic and international card for local and global usage respectively

18. Remit Express Fastest to Pakistan. Anywhere in Pakistan.

The fastest way of getting your money across to Pakistan. Remit Express offers low cost remittance from U.A.E. and Saudi Arabia. Your relatives, friends or business associates receive drafts within 72 hours. MCB Remit Express has been specifically designed to meet the needs of the expatriate Pakistani community residing in the Gulf countries.

19. Easy Personal Loan Helping You Do MoreMCB Easy Personal Loan provides you with the financial advantage to do things you've always wanted to but never had the sufficient funds for. Take that much-needed holiday. Buy a car. Refurnish your house. Purchase a new TV. Finance a better education for your children.

20. MCB Pyara Ghar MCB gives dream home at the lowest and best possible mark-up rates. You can choose either one of our two mark-up rate options- fixed or variable.Early repayment option tailor-made to allow making partial prepayments at dates that suit. Who Can Apply Anyone who fulfills the following criteria is eligible to apply:

Pakistani national residing in the city and area where the product is launched.

25 years old or above when you apply and under 60 at the time of maturity of the applied financing period.

Salaried person, self-employed professional or a businessman with a verifiable monthly income stream.

MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 28

PROJECT ON MCB BANK LIMITED 03143046412

Net take -Home income not less than Rs. 25,000 per month.

Have 5 years or more of business or professional experience.

Employed with the present employer for 2 years with a total employment history of 5 years.

Home Purchase Home Renovation Home Construction Tenure 3 years to 15 years 2 years to 5 years 3 years to

15 years21. MCB Virtual

MCB Virtual provides the continence of banking on internet. Whether at office or home or traveling. Log on at www.mcb.com.pk and enjoy 24 hours access of all your accounts for the largest array of service.

22. MCB Business SarmayaMCB Business Sarmaya is a running finance against your residential property. It offers running finance up to 20 millions with low markup.

23. MCB Car 4 UMCB car 4 u auto finance is a power move that gets you not only a car of your own choice but leads you best in life. It is affordable with competitive markup, flexible conditioning and easy processing and above all no hidden cost.

PLACING STRATEGIES OF MCB BANK

The location of the bank plays a vital role in making its operations profitable. If the bank is located in some business center then it will be very easy for it to MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 29

PROJECT ON MCB BANK LIMITED 03143046412

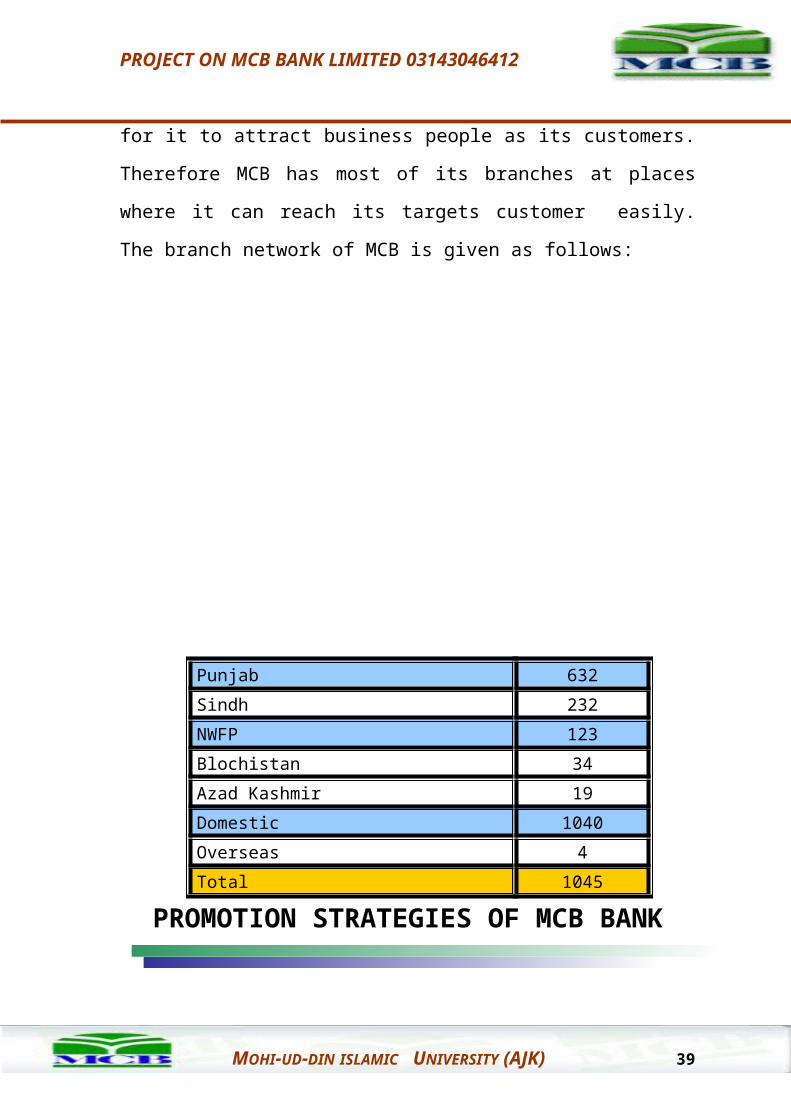

attract business people as its customers. Therefore MCB has most of its branches at places where it can reach its targets customer easily. The branch network of MCB is given as follows:

PROMOTION STRATEGIES OF MCB BANK

MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 30

Punjab 632Sindh 232NWFP 123Blochistan 34Azad Kashmir 19Domestic 1040Overseas 4Total 1045

PROJECT ON MCB BANK LIMITED 03143046412

MCB Bank is actively participating in promotion of its products and services through advertisement and other promotional schemes.Initially, the bank focused on the upper class customer’s only and offered products for a limited class of people. But now the strategy has been changed and the bank is now targeting the middle market also. The products offered are of diverse nature to cater the needs of maximum number of people.

FIELDS OF ACTIVITIES

The purpose of banks is to provide some services to the general public. And for this purpose different banks provide different services to the people in different forms. The MCB Bank is a commercial bank, in modern time commercial banks play a very important role and their functions are manifold. The main functions and services which MCB Bank Limited provides to different peoples are as follows.

1) Open Different accounts for different peoples2) Accepting various types of deposits3) Accepting various types of deposits4) Granting loans & advances5) Undertaking of agency services and also general utility

functions, few of those are as under

Collecting cheques and bill of exchange for the customers.

Collecting interest due, dividend, pensions and other sum due to customers.

Transfer of money from place to place.

MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 31

PROJECT ON MCB BANK LIMITED 03143046412

Acting an executor, trustee or attorney for the customers. ‘Providing safe custody and facilities to keep jewellery, documents or securities.

Issuing of travelers cheques and letters of credit to give credit facilities to travel.

Accepting bills of exchange on behalf of customers. Purchasing shares for the customers. Undertaking foreign exchange business. Furnishing trade information and tendering advice to

customers.

For proper functioning of branches and the over all bank has been divided in different departments. These departments handle different jobs so that division of work is there for improvement of functions and also it is easy to control the situation. The general division in a branch is as follows:

1. Cash department 2. Deposit department3. Advances & credit department4. Remittance department5. Foreign exchange department 6. Technology department (new addition in order to cop

with the growing needs of day to day technology requirements)

CASH DEPARTMENT

The following books are maintained in the Cash Department:

Receiving Cash Book Paying Cash Book Token Book Scroll Book

MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 32

PROJECT ON MCB BANK LIMITED 03143046412

Cash Balance BookWhen cash is received in counter, it is entered in the Scroll Book and Receiving Cashier Book. At the close of the day, these are balanced with each other.When the cheque or any negotiable instrument is presented at counter for payment, it is entered in the token book and token is issued to the customer. The token clerk and the Cashier make entries in the paying book and payment is made to payee. At the close of day, the Token Book and Paying Cashier Book are balanced.The consolidated figure of receipt and payment of cash is entered in the cash balance book and drawn closing balance of cash.Opening Balance + Receipts - Payments = closing Balance.This is very important department because cash is the most liquid asset and mostly frauds are made in this department, therefore, extra care is taken in this department and nobody is allowed to enter or leave the area freely. Mostly, cash area is grilled and its door is under supervision of the head of that department. All the books maintained in this department are checked by an officer.

DEPOSIT DEPARTMENT

Bank deals in money and they are merely mobilizing funds within the economy. They borrow from one person and lend to another, the difference between the rate of borrowing lending forms their spread or gross profit. Therefore we can rightly state that deposits are the blood of the bank which causes the body of an institution to get to work. These deposits are liability of the bank so from point of view of bank we can refer to them as liabilities.The total deposits of MCB are growing since its inauguration but after privatization there is a sharp incline in over all deposits of the bank. The increase in deposits is also a cause MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 33

PROJECT ON MCB BANK LIMITED 03143046412

of increase on total number of accounts; bank has progressed in both aspects.

TYPES OF DEPOSITSDeposits can be segregated on two bases, one is the duration in which there funds are expected to be with the bank and second is the cost of getting these funds. So divide deposits in two classes according to duration of deposits i.e.

1) Time deposits / liabilities2) Demand deposits / liabilities

And on the basis of the cost to acquire these funds, a deposit can be classified as any one of following four, High Cost Medium Cost, Low Cost No Cost. Banks has different kinds of deposit schemes in order to induce deposits. These schemes are a mixture of the above mentioned two types of deposits with an addition of different services & requirements such as minimum balance' requirement, mode of transaction, basis for calculation of profit, deductions, additional benefits, eligibility for different groups.In the similar fashion, MCB has a large variety of deposit schemes and some of them are as follows:

CURRENT ACCOUNTIn this type of accounts the client is allowed to deposit or withdraw money as and when he likes. He may, thus, deposits or withdraws money several times in a day if he likes. There is also no restriction of amount to be deposited or withdrawn. However, there is requirement of minimum balance maintenance of Rs. 10000/-. Usually this type of account is opened by the businessmen. No profit is paid by the bank and no service charges are deducted by the bank on current deposits account. These types of deposits are also exempt from compulsory deduction of Zakat.

PLS ACCOUNTThis type of account is for those persons who want to make small savings'. This type of account is opened with a MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 34

PROJECT ON MCB BANK LIMITED 03143046412

minimum deposit of Rs. 10000/-. Under this scheme deposits can be made only up to a-costing amount and withdrawals are allowed twice a week or 8 times a month. If a big amount is required a seven days notice is required before the withdrawal. The profit is paid on these accounts on the minimum balance during a month for the whole of That month. Zakat & other withholding taxes are deducted as per rules of the government.

KHUSHALI BACHAT ACCOUNTThis is an advance form of PLS saving a/c, in this type of account. The minimum balance requirement for this type is Rs. 10000/-. There is also restriction on the number of withdrawals as well, i.e. up to 4 times in a calendar month. For maintaining this extra balance the customer gets the benefits of profit calculation on daily product basis and also free service of standing instructions of paying utility bills and HBFC installments. All other rules of saving account are applicable.

PLS 365 GOLDThis is a special type of saving account in which customer maintains a minimum balance of Rs. 300,000- and in turn he gets the benefits of daily profit calculations and also there is no restriction on the maximum number of withdrawals as was there in the case of KBA. There is also another advantage of this scheme that if balance on a particular day falls below the minimum balance then only the product of that day is ignored whereas in KBA, if balance falls below the minimum limit then all the products for that month are ignored on in other words no profit is paid for that month.

Khaunm Bachat SchemeThis is a type of term deposit, in this type of deposit an account is deposited and monthly payments of Rs. 1000/- are made by the account holder in this account for a minimum of 10 years. After The expiry of term, he receives his funds along with profit for the tenor. The distinctive feature of this product is that profit is calculated on monthly basis and charged to account on end of each half /ear. Then profit is also calculated on that MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 35

PROJECT ON MCB BANK LIMITED 03143046412

amount of profit which is credited to the customer's account. So we can say that in this type of account there is a concept of accumulated profits on profit. This ends in getting a heavy return for the depositor at the end of tenor for his small savings. This product was actually introduced to promote saving habits in the people. Zakat and withholding taxes are deducted as per rules only at the time of maturity while making payment to the customer.

Term Deposits ReceiptsThis is a type of term deposit in which a receipt is issued for varying tenors ranging from 1 month to 5 years or more. These are in the form of receipts and profit on these receipts is paid biannually. These receipts are encashable after expiry of the period for which they were issued. Different profit rates are applied to different type of TDRs.

CLEARING DEPARTMENT

Every banker acts both as a paying as well as a collecting banker, It is however an important function of crossed cheques. A large part of this work is carried out through the bankers clearing house.A clearing house is a place where representative of all banks of the city get together and settle the receipts and payment of cheques drawn on each other. As the collecting banker runs certain risks in receipt of their ownership the law has provided certain protections to the banks.The Negotiable Instrument Act, 1881, lays down hat drawer or holder of a cheque or draft may cross the instrument generally or specially. It further lies down that a crossed cheque can only be paid to a banker, who collects it for a customer in good faith and without negligence.

Types of Cheques Transfer cheques: are those cheques, which are

collected and paid by the same branch of bank. Transfer delivery cheques: are those cheques,

which are collected and paid by two different branches of the same bank situated in the same city.

Clearing cheques: are those cheques, which are drawn on the branches of some other bank of the same

MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 36

PROJECT ON MCB BANK LIMITED 03143046412

city or of the same area, which is covered by a particular clearing house.

Collection cheques: are those cheques, which are drawn on the branches of either the same bank or of another bank, but those branches, are not in the same city or they are not the members of clearing house.

MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 37

PROJECT ON MCB BANK LIMITED 03143046412

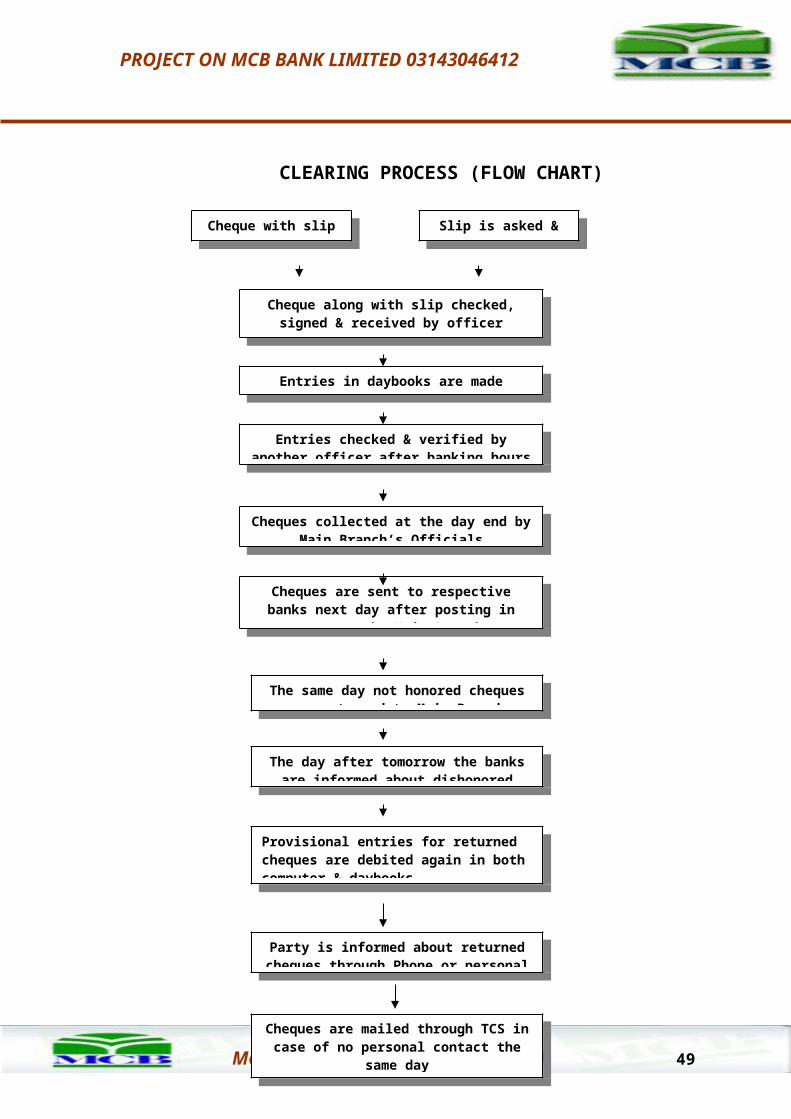

CLEARING PROCESS (FLOW CHART)

MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 38

Cheque with slip given

Cheque along with slip checked, signed & received by officer

The same day not honored cheques are returned to Main Branch

The day after tomorrow the banks are informed about dishonored cheques

Provisional entries for returned cheques are debited again in both computer & daybooks

Party is informed about returned cheques through Phone or personal contact

Cheques are mailed through TCS in case of no personal contact the same day

(If there is any availability)

Slip is asked & filled

Entries in daybooks are made

Entries checked & verified by another officer after banking hours

Cheques collected at the day end by Main Branch’s Officials

Cheques are sent to respective banks next day after posting in

computer by Main Branch

PROJECT ON MCB BANK LIMITED 03143046412

ADVANCES DEPARTMENT

Advances are the most important source of earning for the banks. MCB is also giving full attention towards this aspect and it is also obvious from the growing portfolio of advances and from very low delinquency rate. The credit portfolio of this institution is in a very much better shape than other financial institutions of Pakistan and the credit goes to the management and the staff who are concerned about the quantity and quality as well.

Loans

Cash Credits

OverdraftLOANS

Loans are monetary assistance by a financial institution to a business, individual etc. The loans are granted by the bank in lump sum, so these types called fixed or demand loans. Interest is charged on the whole amount of a fixed loan.The borrower withdraws whole the amount of loan. This type of loan is normally granted against security of gold documents.In case of demand loans against gold or documents, a demand promissory note for the amount of loan is taken from the borrower loans are granted under;LOAN AGAINST GOLDUnder this type of loan, which is granted to the borrower the Head Cashier estimates the value of Gold or Gold ornaments through an agent (Gold smith) and keeps a margin of 40 to 50 percent. After the opening the gold loan account a token is given to the borrower, which is a bank receipt.On repayment of loan, the gold or ornaments held as security for it, together with the demand promissory note duly discharged is returned to the borrower and his receipt for the gold ornament taken in the demand loan ledger. This receipts states that he ornaments returned are complete and in order. Part delivery of ornaments is given against part payment of a loan but care is taken that the ornaments still MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 39

PROJECT ON MCB BANK LIMITED 03143046412

in banks possession fully covers the balance of the loan outstanding. The interest gold loan is to be applied with quarterly.

LOAN AGAINST PLEDGE OF STOCKS In case of advancing such types of loans, the following precautions are kept in the mind:

Stock pledged must be readily saleable Products should be readily saleable Advance should be within the borrows means

REQUIREMENTS OF LOANFor granting loan to any party or individual, the bank checks following particulars of the client:

Credibility Feasibility Report

By Credibility, bank Judges the credibility of the client by his past bank record, CBI report etc. it is very important in making decision about giving him loan.Feasibility report is on the running or proposed business of the client. The report enables the bank to judge the likely return of the business.

CASH CREDITSuch cash account is opened in the name of the customer who borrows from the bank. Customer is granted a loan up to a certain limit, sanctioned by the head office, from which he can draw when he requires and interest is charged on the amount actually utilized by the customer. In order to avoid the danger of idle fund, the bank charges a certain rate of interest, even if the customer does not withdraw any amount. The rate charged by the bank on cash credit in 46 paisa per thousand on daily basis.

REMITTANCE DEPARTMENT

Remittance department performs following functions: MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 40

PROJECT ON MCB BANK LIMITED 03143046412

Mail Transfer (MT) Telegraphic Transfer (TT) Demand Drafts (DD)

MAIL TRANSFER (MT)When a customer requests the bank to transfer his money from one branch of bank to another branch of the same bank or from one city to another city to the same bank or any other bank. Customer fills the form given by bank. If the customer has an account with that amount as mentioned in the application form then concerned officer will undertake the following procedure to make the mail transfer complete.1. Branch Mail transfer form2. Receiving Branch Register copy3. Issuing branch register Copy 4. beneficiary advice 5. advice to customerIn case where the customer is not account holder of the bank then the customer will have to deposit the amount which he wants to transfer under Mail. Then the above said procedure will be done.

TELEGRAPHIC TRANSFER (TT)

This type of transfer is simple. After filling the application form the concerning officer shall fill the telegraphic transfer form. Then it is sent to the required bank which on receiving it immediately makes the payment to the customer and afterwards the voucher are sent to that bank by ordinary mail.

DEMAND DRAFT (DD)

MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 41

PROJECT ON MCB BANK LIMITED 03143046412

Demand draft is just like cheques and issued when the customer wants to take cash with him personally. The idea behind is to avoid the risk and burden of currency notes in huge quantity. Demand draft can easily be handled whatever amount it has and the money can easily be taken from the bank when it is presented. In fact, the bank persuades the customer to transfer money by drafts and avoid the risk of frauds involves in MT and T.T. Draft is only issued when the bank knows customer and bank has the confidence in himIn case of transfer of money by drafts, the customer has to fill an application form. Then the concerned officer fills the following forms:1. Customer’s advice 2. Customer’s debit form3. Register copy 4. Cover Advice

FOREIGN DEMAND DRAFTForeign Demand Draft is just like demand draft. The only difference is that a bank issues FDD to the bank of another country. It requires foreign exchange and it involves seven forms, which are to be filled.

TECHNOLOGY DEPARTMENT

Technological advancements are also affecting the banking industry. The foreign banks have a competitive edge over all local banks in their technologies' advancements and automated systems. Local banks have also realized the gravity oil this situation and are striving to add computerized systems to their branchesMCB is ahead of all other local banks in this field and now it is in a position to even compete with foreign banks. There are more than 1045 branches of MCB all over Pakistan MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 42

PROJECT ON MCB BANK LIMITED 03143046412

and out of these more than 300 branches are fully computerized Almost all .the branches of big cities are computerized; therefore, the need for a technology department at each branch is growing. Now a day, a computer division is working in each city to provide service to ad the branches of that area.MCB has also introduced the now concept of online banking. There are now more than 250 branches linked through this system and they can transact with each other directly using computer systems at their own branches. Now customers do not have to wait long for their transactions and can operate their account through all the online branches.

ATM NETWORKATM stands for Automatic Teller Machine. This machine is used to transact in one's account without intervention of humans. These machines are basically used for taking cash, confirming balances and requesting statements / cheque books.MCB has the largest ATM network in the country at the moment with almost one ATM at each online branch and also ATM terminals at International Airports. This network covers more than the 27 cities of Pakistan including the provincial capitals and large commercial cities of the country.ATMs are operated through a card issued to the valued customers and by application of Personal Identification Number (PIN number). A person can withdraw from any machine across Pakistan with having an account in only one branch of MCB. This was only possible with the help of online system. In this system all the machines are linked to central banking host at IRM division Karachi through either satellite or telephone controller. This system identifies the card holder and his PIN Number. Now MCB has also entered into a contract with Cirrus which is a subsidiary of MasterCard. This contract will enable an ATM card holder to use his account even when he is out of country at all the ATMs where Cirrus logo is displayed.

Green Cards are ordinary cards with a maximum withdrawal facility of Rs. 10,000/- in a day. The annual fee for this card is Rs. 300/- only. MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 43

PROJECT ON MCB BANK LIMITED 03143046412

Gold Cards are special cars with maximum withdrawal limit of Rs. 25000/- in a day. These cards are issued to the persons having more than Rs. 500000/- as their average balance.

International Cards are issued in collaboration with Cirrus and are useable all over the world with maximum withdrawal facility according to the standards of Cirrus.

MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 44

PROJECT ON MCB BANK LIMITED 03143046412

OTHER GENERAL INFORMATION OF THE BRANCH

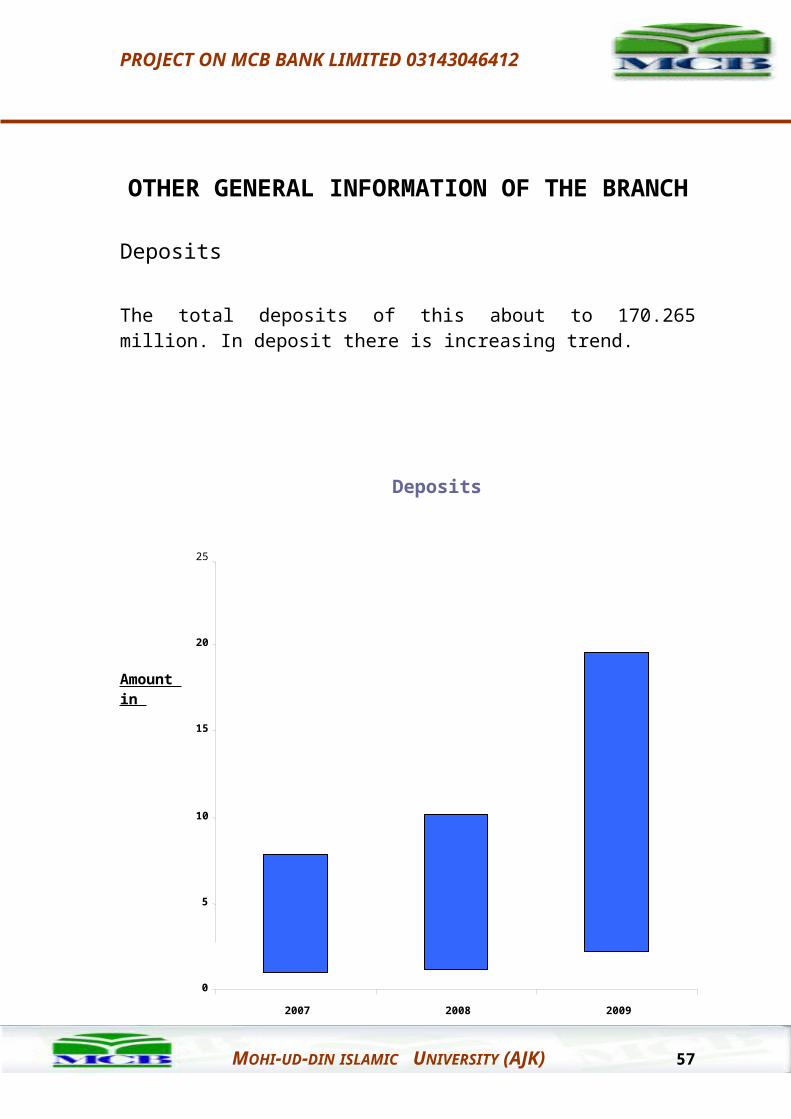

Deposits

The total deposits of this about to 170.265 million. In deposit there is increasing trend.

MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 45

Deposits

0

5

10

15

20

25

2007 2008 2009

Years

Amount in Million

PROJECT ON MCB BANK LIMITED 03143046412

ProfitTotal remittance of this branch is 220.65 million in 2009.there is also incrasing trend in profit from 2007 to 2009 because of higher mark up rate charged on the finances.

No. of vouchersThe vouchers which are transacted in this branch in 2009 are as follows:

Financing & AdvancesMainly, the short term financing such as cash finance, running finance, Demand finance, ERF II, FAFB, FBP are being dealt here.

Number of accountsAccounts in this branch of MCB are as follows:Current account Total numbers of current accounts are 435.

PLS accountTotal numbers of profit and loss accounts are 247.

Khushali bachat account:These are about to 107 accounts.

Basic Banking Account (Newly Introduced by SBP for salaried person)There are about to 126 accounts.

MCB 365 Gold AccountThere are about to 85 accounts.

MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 46

FIRST

TWO

WEEKS

PROJECT ON MCB BANK LIMITED 03143046412

ACCOUNT OPENING DEPARTMENT

Account opening and closing is the function of accounts departments. Bank’s customers may be individuals (Single or Joint), firms (partnership/proprietorship), Autonomous corporations, Limited Companies, Charitable Institutions, Associations Educational Institutions or Local Bodies.

BASICS TO OPEN AN ACCOUNT

During the span of mine internship in MCB, I learned and observed a lot of about the opening of an account. Basically I think that the opening of an account is the establishment of a contractual relationship between the banker and the customer. By opening an account at a bank a person becomes a ‘customer’ of a bank. Further I am going to express the basic requirements and steps involved in the opening of an account.

INTRODUCTION AND PRELIMINARY INVESTIGATIONBefore opening an account MCB as like the other banks in Pakistan ascertain whether or not the person who is going to open the account is a desirable customer or not. Then MCB determine the prospective customer’s integrity, respectability, occupation and the nature of business by the introductory references given at the time of account opening. Negligence in this informal preliminary investigation may result in serious consequences not only for the banker concerned directly but also for other bankers and the general public who may be affected indirectly.

In order to further strengthen and streamline this process, the Federal Ombudsman of Pakistan, vide his ruling on complaint No. II/31/5186, has directed the banks to retain with the account opening form a Photostat copy each of the National Identity Cards of the person desiring to open an MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 47

PROJECT ON MCB BANK LIMITED 03143046412

account as well as that of the introducer. As per these directions, the concerned Branch Managers are required to obtain the original National Identity Cards along with their Photostat copies and then return the original after attesting the authenticity of the retained copy.Preliminary investigation is necessary because of the following reasons:Avoid Frauds: In this regard I learned that if a banker does not make the necessary inquiries mentioned above he may enable dishonest persons to possess cheque books for fraudulent purposes. If any such person happens to be an undercharged bankrupt, the banker might be placed in an awkward position for having allowed such a person to open and open a bank account.Safeguard against unintended overdrafts: Sometimes due to a mistake an account may be given an overdraft, For instance, the ledger keeper, misreading the balance of an account honors a cheque for an amount larger than the balance. Similarly a credit entry belonging to a customer may be made by mistake in another customer’s account. In such situations the excess amount withdrawn by the customer can only be realized if the customer is a respectable person.Inquiries about clients: Being a banker I think MCB has a business obligation to respond to inquiries from other banks etc. about his customer’s financial position. Though the banker gives only a general ideal about the financial standing of his customer.

Specimen SignatureWhen an account is opened with MCB customer provides to the bank a specimen of the form of signature which would appear on all his cheques to express his authority for the payment of cheques drawn on his banker. This specimen is taken generally on a card specially designed for this purpose, and rule for the customers, full name, and account number are entered on it.If the bank has reasons to doubt the genuineness of a signature, he should either get it confirmed for his satisfaction or return the cheque with the remark ‘Signature MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 48

PROJECT ON MCB BANK LIMITED 03143046412

differs’. If the signature of the customer is forged the banker cannot escape his liability because he has actually acted on his customer’s mandate.

HOW TO OPEN AN ACCOUNT (GENERAL)Before opening an account in MCB I observed that the following points must be considered in this regard.

Another account holder of the bank should properly introduce the new customer.

The account holder should sign the account opening form in the presence of bank officer and the signature is duly verified.

A copy of identity Card is required by Bank. Against submission of the Bank’s prescribed application

form, duly introduced in the manner provided and on supplying such document, as may be required and account may be opened. The Bank reserves to itself the right to refuse to open and account without assigning any reason.

Each account shall be allotted a distinct number that is to be quoted in all correspondence with the bank relation to the account.

Minimum amount for opening and continued maintenance of various types of accounts is as follows:

Rs. Saving 10000Current 10000

The bank reserves the right to change the above mentioned minimum balance requirement at any time without any notice.

PROCEDURE TO OPEN AN ACCOUNTAccording to my practice in MCB, when a customer wants to open an account, the bank officer gives him an application form. All information, which is necessary to be known by the bank, are requirements of the application form. Form also requires the essential documents to be attached by the MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 49

PROJECT ON MCB BANK LIMITED 03143046412

customer.Basically following information is required to open an account with MCB.

Title of Account Full Name of Applicant Occupation Address Telephone No. Currency of account Nature of Business Introducer’s Name, Address & Signatures Special instruction regarding the account Initial Amount of the Deposit Signature of the applicant

DOCUMENTS TO BE ATTACHEDFurther I learned that if you wanted to open an account with MCB then you should attach the following documents with your application form which are different for different categories.SOLE PROPRIETOR’S ACCOUNTIn order to open an account with MCB Sole Proprietors have to submit their business registration certificate number.PRIVATE / JOINT ACCOUTSFor individual or private or joint accounts National Identity Card is required.

JOINT STOCK COMPANYBefore an account of a Public Limited Company is opened MCB must ask the person authorized to do so to submit the certified copies or the following documents Certified true copy of the Memorandum and Articles of Association of the company. Certified true copy of the resolution of the board of directors / managing committee / governing body regarding conduct of the account. Certified list containing names and signatures of the directors / office bearers.

MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 50

PROJECT ON MCB BANK LIMITED 03143046412

Certified true copy of the certificate of incorporation or registration. Certified true copy of the certificate of commencement of business (in case of public limited companies). Balance Sheet I.D. Card copy of each director Original is also enclosed for inspection and return List of persons authorized to operate the account. Power of Attorney in favor of the person opening account.

PARTNERSHIP FIRM ACCOUNTInformation which is required to be submitted to MCB by a partnership firm in this case is as follows:

Full Names Address Specimen of signatures of the partners Certified true copy of partnership deed Registration No. if the Partnership is registered

SOCIETIES / CLUBS AND ASSOCIATIONS ACCOUNTMCB is authorized to open the accounts of the societies/clubs and associations, These are non-trading organizations, formed for the promotion of culture, science, education, recreational activities and charitable purposes etc. some of these institution are registered under the Societies Registration Act, 1866, and are issued a certificate of registration after they have been found fit for registration.

ISSUANCE OF CHEQUE BOOKWhen a customer opens an account with the bank, he is provided with cheque book for withdrawals from account. However, the first cheque book is given to the customer only when all the required documents are checked. A cheque book contains ten, twenty five, fifty or hundred leaves. The cheque book also carries a requisition slip for the issuance of the new cheque book. This slip is duly MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 51

NEXT

TWO

WEEK

PROJECT ON MCB BANK LIMITED 03143046412

filled and singed by the customer. The signature of the customer is verified by the bank and new cheque book is issued to the customer and serial numbers of the cheque are duly entered in the book of the bank. Along with the signature, person should also write his full name & address.Usually only one cheque book is issued at a time, however big concerns who need a number of cheque books at a time, may ask the bank to stock as number of cheque books in their name and to point their name on these cheque books.The officer keeps and maintains the cheque book register Cheque book inventory and cheque books issued are recorded in this register.In case of loss of cheque book or requisition slip on cheque book the customer has to fill the Form No. 216-B to obtain a new cheque book.

UTILITY BILLS COLLECTION

I worked in the utility bills collection department as the MCB collects utility bills on behalf of WAPDA, Sui Gas Companies, and Pakistan Telecommunication Corporation Limited by putting the stamp on the utility bills “Paid”, Date of payment, Signature of the officer receiving the utility bills. After receiving utility bills a list is made on the form which is called Bills scroll form. One copy of the scroll is with the bank for evidence whereas the original copy with the receipt of the bills is sent to the billing department of the respective corporation. The bank charge commission on the bills.

MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 52

PROJECT ON MCB BANK LIMITED 03143046412

CASH MANAGEMENT

The most important department of MCB which deals in money (receiving deposits at lower rates and lend them out at higher rates of interest). This department also called as Chest Department and manager of it is called Cash Manager or Chest Manager. In those branches where this department is not separately existed, the branch manager performs the duties of the Chest Manager.

The excess cash (More than its insured limit by the insurance company) of the branches of the region is collected by the main branch. The main branch is also bound to send its excess cash (more than its insured limit) to the State Bank of Pakistan. No branch can have cash its safe more than its insurance at any time at the time of closing cash, if it is so the manager will be responsible (not the insurance company) whether or not he informed to the regional office (exception to the limit which is insured for the day).

New Notes and Prize Bonds are also part and parcel of the Cash Management. Keys of the Safe lockers are with the three authorized persons each one of them is responsible for cash as at the time of closing the cash the officers including Cash officer presented and lock the safe after counting and scrutinize the cash. The cash officer maintain its daily cash book with specification of notes (Bonds are also recorded in the books in

relation with cash) and other vouchers, after being satisfied the manager authenticates the books and vouchers regarding cash with stamp and signature. at the end I would like to conclude that the cash management is being done in the MCB very effectively.

ADVANCES DEPARTMENT

MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 53

LAST

TWO

WEEKS

PROJECT ON MCB BANK LIMITED 03143046412

On my first day of Internship, Manager gives me some advice and told me the ways to success. He told me that if some one wants to get success in banking career then he must have the knowledge of the one major department of the bank. I.e. Advances. So from very first day I was interested to work in advances department and at my request bank offer me opportunity to work in this department last two weeks Bank adopts the following procedure in order to grant a loan. A customer applies for a loan to the manager, who says him to give details of his property. The details of the proposal and the photocopies of the document to the title of property are sent to the legal advisor of bank. The legal advisor gives his legal opinion upon the documents. The branch manager, in the light of the opinion received from the legal advisor, discusses the proposal with the advancing manager whether to give or not the loan to the applicant. If manager allows granting the loan all the documents along with request letter are sent to regional office for approval. In the regional office the proposal is analyzed and if the office is satisfied a consent letter prepared which is signed by the regional controller credit. This letter is sent to the branch manager. After receiving it the manager finance reviews the consent letter, and prepares a DAC (Disbursement Authorization Certificate). DAC can be made only for people who have a bank account.The following documentation is made for loan.

An application or request letter for loan by the customer Legal opinion of the legal advisor of the bank (for the

title deeds)

Consent letter from the regional office Vetting Certificate (includes consent No., Facility

whether fund based or no-fund based, addresses etc.) Valuation of property any consultant or any panel of

consultants approved by State Bank of Pakistan Original title deed or sale deed

MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 54

PROJECT ON MCB BANK LIMITED 03143046412

Affidavit General power of attorney (made by advocate for the

person/owner taking loan for the company) Mortgage deed Mutation document made Verification of the property by the bank from the

competent authority Hypothecation of stock certificate (Running is to be

given against 75% margin of stock) IB-25R Letter of hypothecation (duly signed by the

party) IB-12 , DP Note/Promissory Note (Bank prepared itself,

duly signed by the party, revenue stamps of Rs. 100 put on it)

IB-6R Agreement of finance mark up (Contract with party for taking mark up on quarterly basis)

IB-24 (used for title deed) IB-29 (used for guarantee from party) IB-26 (used for pledge of stock, margin is different for

different goods) No. IB-28 (used for lien) etc.

After that Loan is sanctioned to the party fulfilling all the terms and conditions for the purpose. The procedure given above is for both short and long term loans.

Following finances in which Muridke Branch is dealing. Running Finance Cash Finance (Against Pledge of Stocks of wheat & rice) Demand Finance (against Lien On DSC’s) Tractor Finance Foreign Bills Purchased Finance Against Foreign Bills

MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 55

PROJECT ON MCB BANK LIMITED 03143046412

Export Refinance I Export Refinance IIThe exposure of Muridke Branch is more than 500 Million.I have learnt about the documentation required for the financing. Major focus on the financing is depending on the account turnover and collateral offered.While financing to the fresh client the credit proposal of the client is elevated to the higher office. The bank’s official get the applications form the customer and prepare the case for getting approval for the higher office.

SECURITIES HELD AGAINST FINANCING

FOR RUNNING FINANCEHypothecation of Stocks (50% Margin)Collateral security (house, land, factory etc..)

FOR CASH FINANCEPledge of stocks (20 to 25% Margin)Collateral security (house, land, factory etc..)

FOR DEMAND FINANCE

Lien over Defense Savings CertificateLien over Deposits (TDR)Lien over Foreign Currency deposits

FOR TRACTOR FINANCING

Joint ownership of the TractorCollateral security (Agri land)

MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 56

PROJECT ON MCB BANK LIMITED 03143046412

FOR EXPORT REFINANCE PART I

Lien over export bills drawn under firms order or contractsCollateral security (house, land, factory etc...)

FOR EXPORT REFINANCE PART II

Hyp & Pledge of StocksLien over EE statementCollateral security (house, land, factory etc...)

MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 57

PROJECT ON MCB BANK LIMITED 03143046412

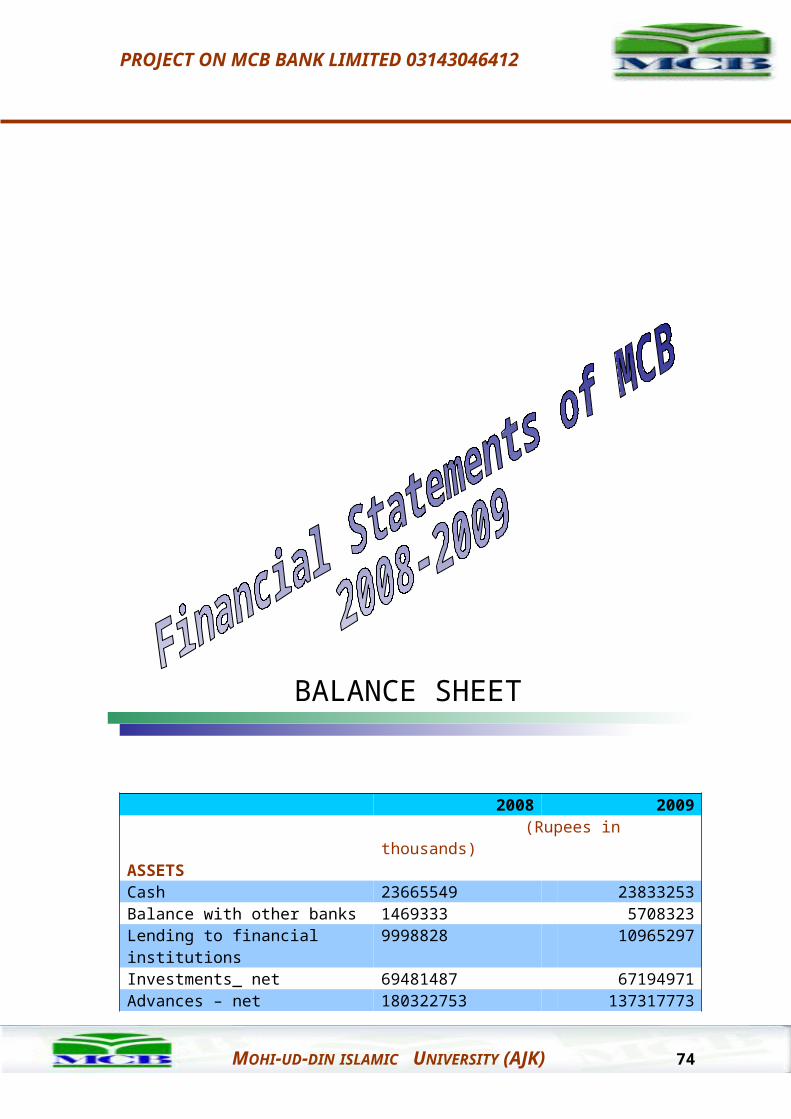

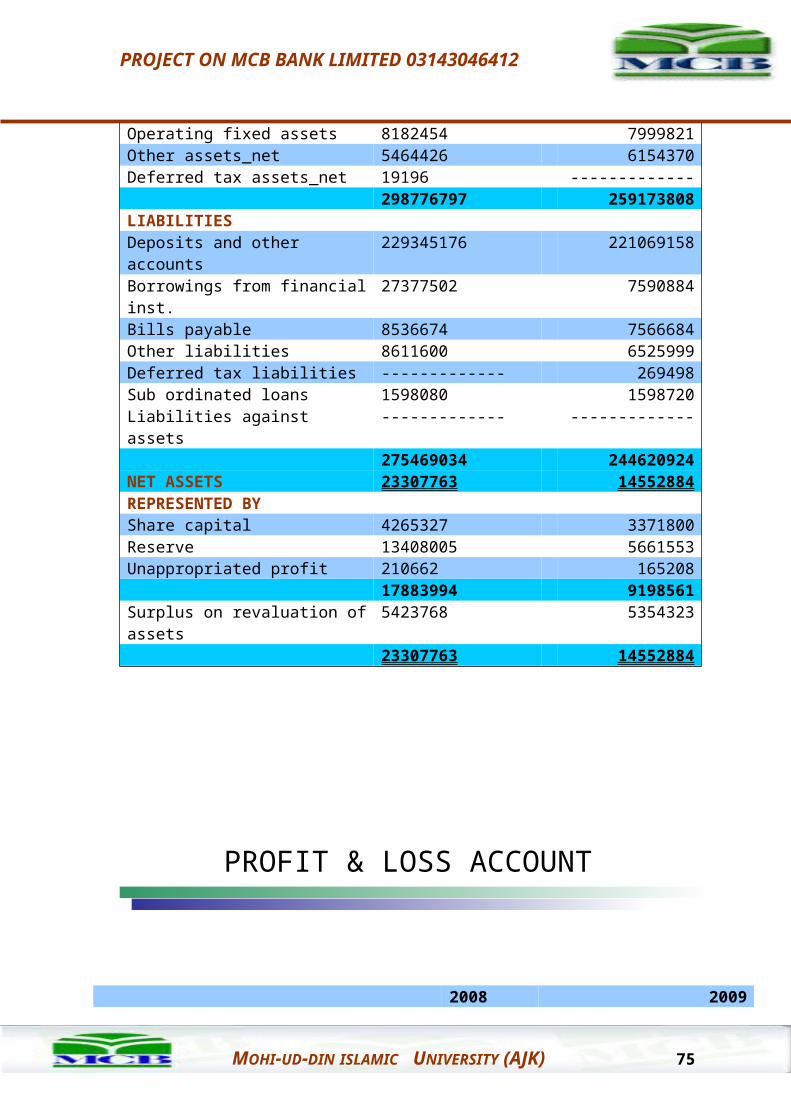

BALANCE SHEET

2008 2009 (Rupees in thousands)

ASSETSCash 23665549 23833253Balance with other banks 1469333 5708323Lending to financial institutions

9998828 10965297

Investments_ net 69481487 67194971Advances – net 180322753 137317773Operating fixed assets 8182454 7999821Other assets_net 5464426 6154370Deferred tax assets_net 19196 -------------

298776797 259173808LIABILITIESDeposits and other accounts 229345176 221069158Borrowings from financial inst.

27377502 7590884

Bills payable 8536674 7566684Other liabilities 8611600 6525999Deferred tax liabilities ------------- 269498Sub ordinated loans 1598080 1598720Liabilities against assets ------------- -------------

275469034 244620924NET ASSETS 23307763 14552884REPRESENTED BY Share capital 4265327 3371800Reserve 13408005 5661553Unappropriated profit 210662 165208

17883994 9198561Surplus on revaluation of assets

5423768 5354323

23307763 14552884

MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 58

PROJECT ON MCB BANK LIMITED 03143046412

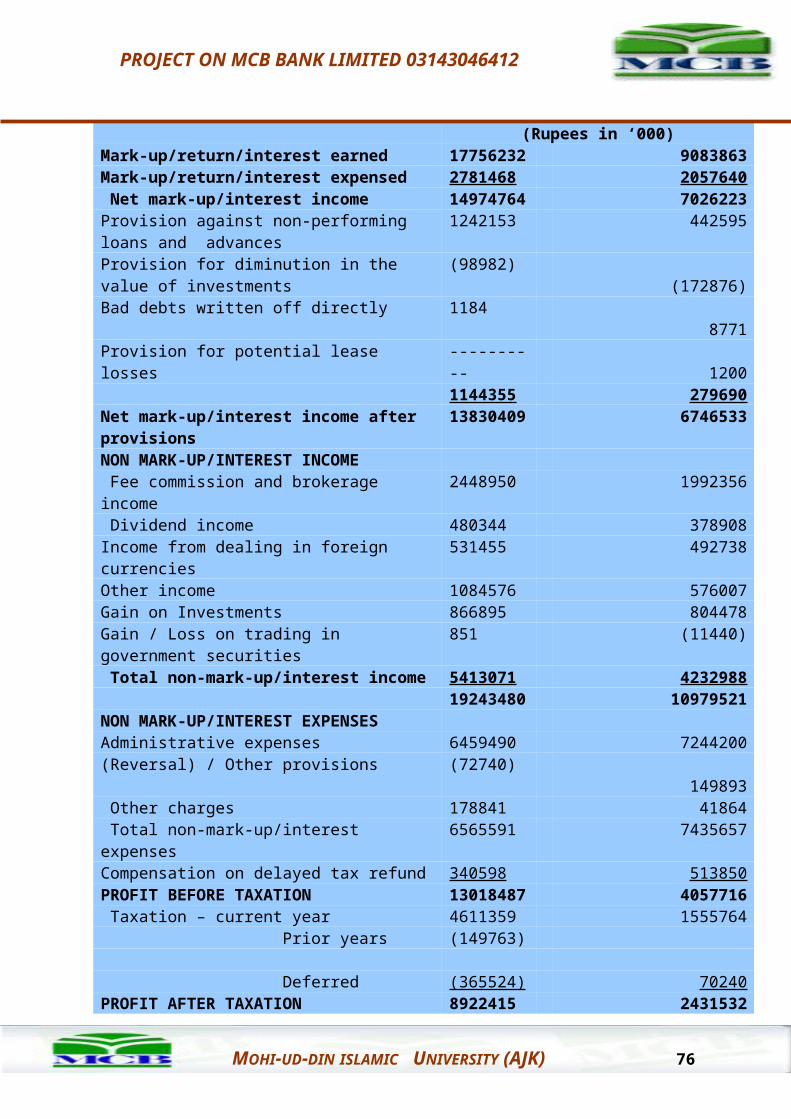

PROFIT & LOSS ACCOUNT

2008 2009(Rupees in ‘000)

Mark-up/return/interest earned 17756232

9083863

Mark-up/return/interest expensed 2781468 2057640 Net mark-up/interest income 1497476

47026223

Provision against non-performing loans and advances

1242153 442595

Provision for diminution in the value of investments

(98982) (172876)

Bad debts written off directly 1184 8771Provision for potential lease losses ---------- 1200

1144355 279690Net mark-up/interest income after provisions

13830409

6746533

NON MARK-UP/INTEREST INCOME Fee commission and brokerage income 2448950 1992356 Dividend income 480344 378908Income from dealing in foreign currencies

531455 492738

Other income 1084576 576007Gain on Investments 866895 804478Gain / Loss on trading in government securities

851 (11440)

Total non-mark-up/interest income 5413071 423298819243480

10979521

NON MARK-UP/INTEREST EXPENSESAdministrative expenses 6459490 7244200(Reversal) / Other provisions (72740) 149893 Other charges 178841 41864 Total non-mark-up/interest expenses 6565591 7435657Compensation on delayed tax refund 340598 513850PROFIT BEFORE TAXATION 1301848

74057716

Taxation – current year 4611359 1555764 Prior years (149763)

MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 59

PROJECT ON MCB BANK LIMITED 03143046412

Deferred (365524) 70240PROFIT AFTER TAXATION 8922415 2431532

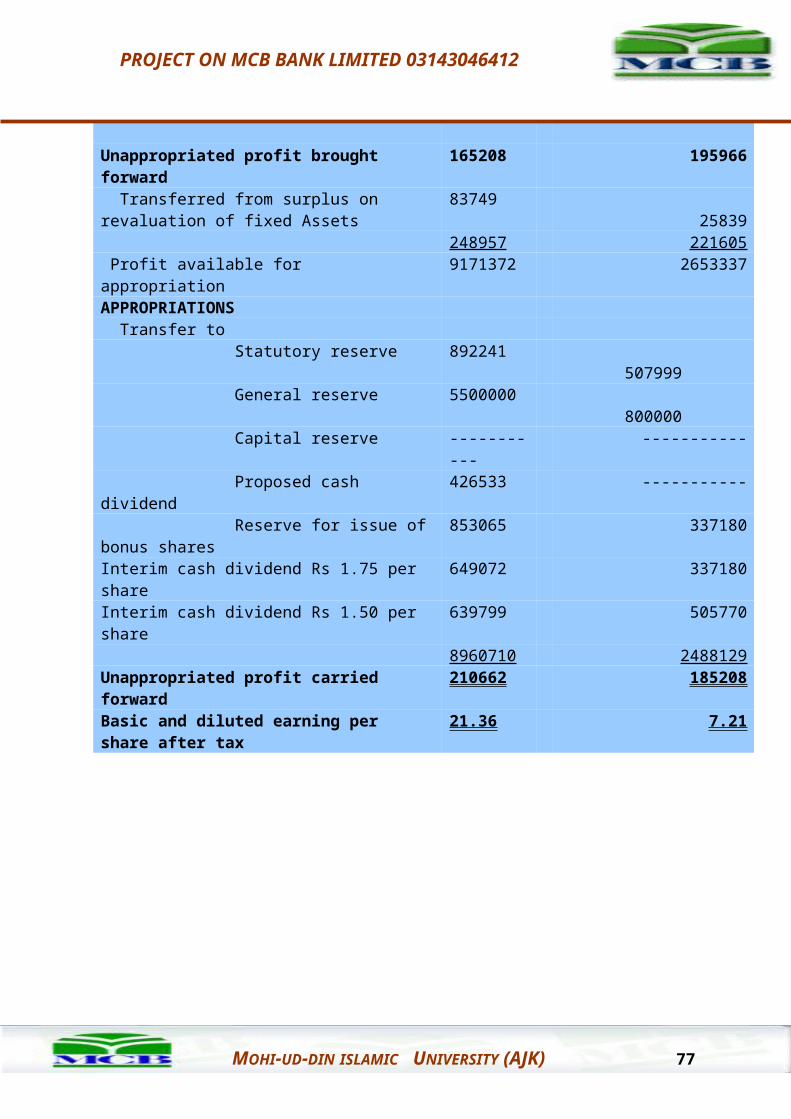

Unappropriated profit brought forward

165208 195966

Transferred from surplus on revaluation of fixed Assets

83749 25839

248957 221605 Profit available for appropriation 9171372 2653337APPROPRIATIONS Transfer to Statutory reserve 892241 507999 General reserve 5500000 800000 Capital reserve ----------- ----------- Proposed cash dividend 426533 ----------- Reserve for issue of bonus shares

853065 337180

Interim cash dividend Rs 1.75 per share 649072 337180Interim cash dividend Rs 1.50 per share 639799 505770

8960710 2488129Unappropriated profit carried forward

210662 185208

Basic and diluted earning per share after tax

21.36 7.21

MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 60

PROJECT ON MCB BANK LIMITED 03143046412

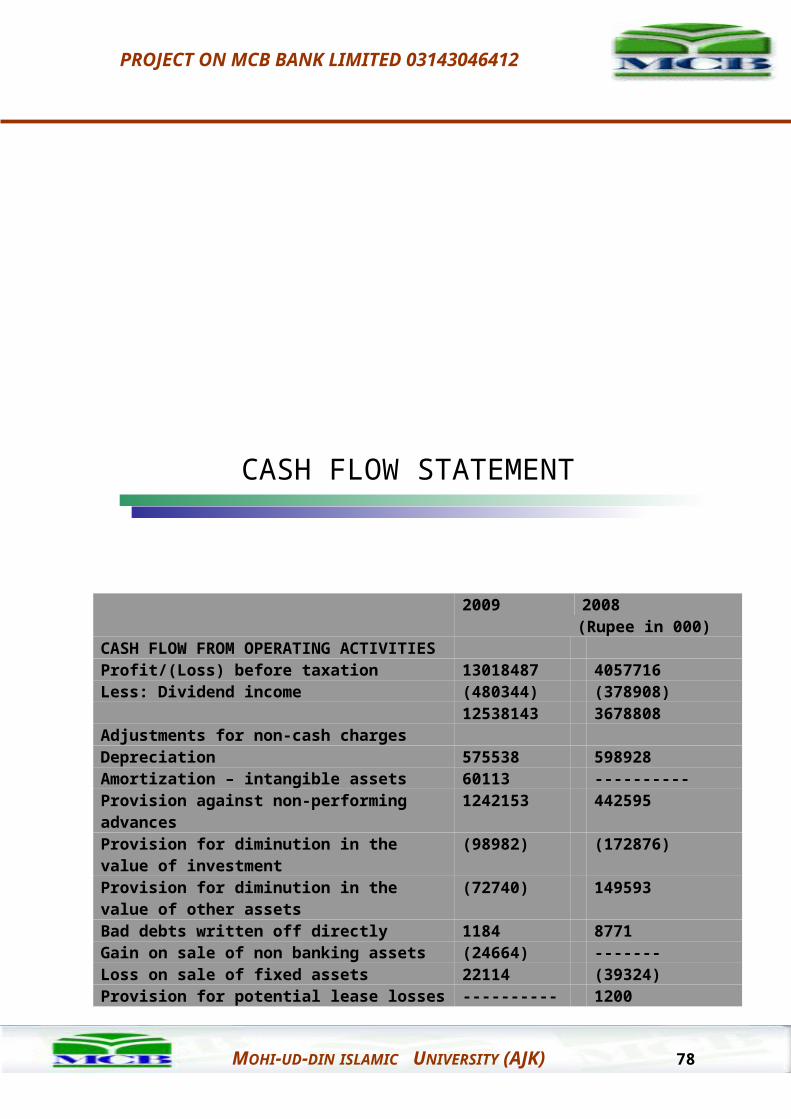

CASH FLOW STATEMENT

2009 2008 (Rupee in 000)

CASH FLOW FROM OPERATING ACTIVITIES Profit/(Loss) before taxation 13018487 4057716Less: Dividend income (480344) (378908)

12538143 3678808Adjustments for non-cash chargesDepreciation 575538 598928Amortization – intangible assets 60113 ----------Provision against non-performing advances

1242153 442595

Provision for diminution in the value of investment

(98982) (172876)

Provision for diminution in the value of other assets

(72740) 149593

Bad debts written off directly 1184 8771Gain on sale of non banking assets (24664) -------Loss on sale of fixed assets 22114 (39324)Provision for potential lease losses ----------- 1200Surplus on revaluation of held for trading securities

(1634) ----------

1703082 98888714241225 4667695

(Increase)/Decrease in operating assets Lendings to financial institutions 966469 (534847) Advances (44248317

)(40570180)

Others assets 982933 26142(455458801)

(41422187)

(Increase)/Decrease in operating assetsBills Payable 969990 (829636) Borrowings from financial institutions 19786638 (25037087) Deposits 8276020 9557765 Other liabilities 982933 26142

30015581 (16282816)

MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 61

PROJECT ON MCB BANK LIMITED 03143046412

(1289074) (53037308)Income tax paid (1152343) (683995)Income tax refund -------------- 370208Net cash flow operating activities (2441417) (53351095)CASH FLOW FROM INVESTING ACTIVITIES Net investments in available-for-sale securities

(20301953)

105292873

Net investments in held-to-maturity securities

16278483 (45878054)

Net investments in held-for trading securities

(66056) ---------------

Dividend received 588153 181258Investments in operating fixed assets (1029307) (1265675)Investment in subsidiary and associated companies

(77) --------------

Sale proceeds from non banking assets disposed of

589876 --------------

Sale proceeds of fixed assets disposed of

127254 81308

Net cash flow from investing activities (1813827) 58411710CASH FLOW FROM FINANCING ACTIVITIES Redemption of subordinated loans (640) (640)Proceeds from issue of right shares 1390868 --------Dividend paid (1545483) (818306)Net cash flow from financing activities (155255) (818946)Ex. difference in cash transactions in foreign branches

3805 (56354)

Increase/(Decrease) in cash and cash equivalents

(4406694) 4185315

Cash and cash equivalent at beginning of the year

29547922 25500460

Effects of exchange rate changes (6346) (144199)29541576 25356261

Cash and cash equivalents at end of the year

25184882 29541576

FINANCIAL ANALYSIS MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 62

PROJECT ON MCB BANK LIMITED 03143046412

"Financial statement analysis is the process of identifying of financial strengths and weaknesses of the firm by properly establishing relationship between the items of the balance sheet and the profit &loss account," and it is done through ratio analysis. RATIO ANALYSISRatio means “one number expressed in term of another a ratio is statistical yardstick by mean of which relationship between two or various figures can be compared or measured. Here we are going to explain the ratio analysis of MCB.

1. PROPRIETARY RATIO

=

Year 2009 (000) 2008 (000)Total Equity 23307763 14552884Total Assets 298776797 259173808 Ratio 0.08 0.06

2. DEBT RATIO/ SOLVENCY RATIO

=

Year 2009 (000) 2008 (000)Total Debts 275469034 244620924Total Assets 298776797 259173808 ratio 0.92 0.94

MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 63

Total equityTotal Assets

Total equity

Total Assets

PROJECT ON MCB BANK LIMITED 03143046412

3. DEBT TO EQUITY RATIO

=

Year 2009 (000) 2008 (000)Total Debts 275469034 244620924Equity 23307763 14552884 ratio 11.82 16.81

4. DEBT TO TANGIBLE NET WORTH

=

Year 2009 (000) 2008 (000)Total Debts 275469034 244620924Tangible net worth 23058725 14552884 Ratio 11.94 16.81

5. DEBT TO FUNDS RATIO

=

Year 2009 (000) 2008 (000)Long Term Debts 41318331 22455384Long Term Funds 64626094 37008268 Ratio 0.63 0.60

6. EXTERNAL INTERNAL EQUITY RATIO

=

Year 2009 (000) 2008 (000)External Equity 275469034 244620924Internal Equity 23307763 14552884 Ratio 11.82 16.81

MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 64

Total Debt

Equity

Total Debt

Equity

Long term Debt

Long Term Funds

External Equity

Internal Equity

PROJECT ON MCB BANK LIMITED 03143046412

PROFITABILITY ANALYSIS

1. RETURN ON ASSETS

= × 100

Year 2009 (000) 2008 (000)Net Profit after Tax 8922415 2431532Total Assets 298776797 259173808 return 3.0% 0.93%

2. RETURN ON EQUITY

= × 100

Year 2009 (000) 2008 (000)Net Profit after Tax 8922415 2431532Equity 23307763 14552884 return 38.28% 16.71%

3. RETURN ON INVESTMENT

= × 100

Year 2009 (000) 2008 (000)Net Profit after Tax 8922415 2431532Investment 69481487 67194971 return 12.84% 3.62%

MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 65

Net Profit after Tax

Total Assets

Net Profit after Tax

Equity

Net Profit after Tax

Investment

PROJECT ON MCB BANK LIMITED 03143046412

4. RETURN ON FIXED ASSETS

= × 100

Year 2009 (000) 2008 (000)Net Profit after Tax 8922415 2431532Fixed Assets 8182454 7999821 return 109% 30.39%

5. AVERAGE PROFIT PER BRANCH

=

Year 2009 2008Net Profit after Tax 8922415000 2431532000No. of branches 1045 1045 Average Profit 8546375 2329054

6. NET PROFIT MARGIN

= × 100

Year 2009 (000) 2008 (000)Net Profit after Tax 8922415 2431532Interest Income 17756232 9083863 return 50.25% 26.77%

7. INTEREST INCOME TO TOTAL INCOME

= × 100

Year 2009 (000) 2008 (000)Total Income 23169303 13316851Interest Income 17756232 9083863 return 76.64% 68.21%

MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 66

Net Profit after Tax

Fixed Assets

Net Profit after Tax

No. of branches

Net Profit after Tax

Interest Income

Interest Income

Total Income

PROJECT ON MCB BANK LIMITED 03143046412

8. INTEREST EXPENSE TO TOTAL EXPENSE

= × 100

Year 2009 (000) 2008 (000)Total Expense 9347059 9493097Interest Expense 2781468 2057640 return 29.76% 21.67%

9. RETURN ON ADVANCES

= × 100

Year 2009 (000) 2008 (000)Interest Income 17756232 9083863Total Advances/ Loans 180322753 137317773 return 9.85% 6.61%

MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 67

Interest Expense

Total Expense

Interest Income

Total Loans

PROJECT ON MCB BANK LIMITED 03143046412

INVESTOR ANALYSIS

Investor analysis or market analysis are related to firm market valve, as measure by its current share price to certain accounting values. Investor analysis includes:

Earning per share P/E ratio Dividend per share Dividend yield ratio Dividend payout ratio Break up value/Book value per share M/B ratio

1. EARNING PER SHARE

=

Year 2009 2008Net Profit after Tax 8922415000 2431532000No. of Shares 426532700 337180000 Earning 21 7.21

2. P/E RATIO

=

Market price per share is Rs.247.75 on 4th Jan.2009

Year 2009 2008MP Per Share 247.75 247.75EPS 21 7.21ratio 11.80 34.36

MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 68

Net Profit after Tax

No. of Shares

MP Per Share

EPS

PROJECT ON MCB BANK LIMITED 03143046412

3. DIVIDEND PER SHARE

=

Year 2009 2008Total Dividend 1288871000 842950000No. of Shares 426532700 337180000DPS 3.02 2.5

4. DIVIDEND YIELD RATIO

=

Year 2009 2008DPS 3.02 2.5MV Per Share 247.75 247.75Ratio 0.012 0.01

5. DIVIDEND PAYOUT RATIO

= × 100

Year 2009 2008DPS 3.02 2.5EPS 21 7.21Ratio 14.38% 34.67%

6. BOOK VALUE PER SHARE

=

Year 2009 2008Equity 23307763000 14552884000No. of Shares 426532700 337180000Ratio 54.64 43.16

MOHI-UD-DIN ISLAMIC UNIVERSITY (AJK) 69

Total Dividend

No, of Shares

DPS

MV Per Share

DPS

EPS

Equity

No. of Shares

PROJECT ON MCB BANK LIMITED 03143046412

7. M/B RATIO

=

Year 2009 2008BV Per Share 54.64 43.16MV Per Share 247.75 247.75Ratio 4.53 5.74

BANK SPECIAL ANALYSIS

Bank ratio analysis is little bit different from other organizations and if we want to see the real picture of a bank we have to focus on given special ratios.