Offices across Africa, Asia and Latin America www.MicroSave.net info@MicroSave.net Trainers Manual Planning Conducting and Monitoring Pilot Tests (Loan Products) Based on “A Toolkit for Planning Conducting and Monitoring Pilot Tests” Michael McCord, David Cracknell, Graham A.N. Wright and Henry Sempangi April 2004

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Offices across Africa, Asia and Latin America

www.MicroSave.net [email protected]

Trainers Manual

Planning Conducting and Monitoring Pilot Tests

(Loan Products)

Based on

“A Toolkit for Planning Conducting and Monitoring Pilot Tests” Michael McCord, David Cracknell, Graham A.N. Wright and Henry Sempangi

April 2004

Trainer’s Manual Planning, Conducting & Monitoring Pilot Tests - Loans

MicroSave – Market-led solutions for financial services

1

Acknowledgements Evelyn Stark prepared much of this Trainer’s Manual. Elsie Mukasa did much of the layout and design work on the manuals and workbook and additional editing work was done by Benjamin Eaglin. Greta Greathouse put together the PowerPoint presentation. This good work was then taken by the MicroSave and subjected to additional editing and extension. This training manual needs comments from trainers to provide additional training tips, examples and ideas! Your thoughts and comments are anticipated and welcomed for the next version. Table of Contents

Acknowledgements ....................................................................................................................... 1

Table of Contents .......................................................................................................................... 1

Trainer’s Guide ............................................................................................................................. 2

Preparation For Training ............................................................................................................ 5

Alternative Lesson Planning ........................................................................................................ 6

Session One: Participants Introduction and Overview ............................................................. 7

Session Two: Introduction to Pilot Testing .............................................................................. 11

Session Three: The No Pilot Test Case .................................................................................... 19

Session Four: Step 1- Composing the Pilot Test Team........................................................... 21

Session Five: Step 2 - Developing the Testing Protocol ........................................................... 32

Session Six - Step 3: Defining the Objectives ........................................................................... 42

Session Seven - Step 4: Preparing All Systems......................................................................... 56

Session Eight - Step 5: Modelling Financial Projections ......................................................... 65

Session Nine: Step 6 - Documenting the Product Definitions & Procedures ........................ 75

Session Ten: Step 7 - Training the Relevant Staff ................................................................... 86

Session Eleven: Step 8 - Developing Customer Marketing Materials and Methods ............ 93

Session 12: Step 9 – Launch: Commencing the Pilot Test .................................................... 106

Session 13: Step 10 – Monitoring and Evaluating the Test ................................................... 110

Selected Bibliography ............................................................................................................... 118

Trainer’s Manual Planning, Conducting & Monitoring Pilot Tests - Loans

MicroSave – Market-led solutions for financial services

2

Trainer’s Guide Welcome to the MicroSave Planning, Conducting and Monitoring Pilot Tests Training Curriculum. This guide is meant for those people who have taken the MicroSave Pilot Testing training course and are going to reproduce the training elsewhere – or are going to “live it” by piloting a new product within their own organisation. The guide provides comprehensive session plans and also offers the experiences of some of our research partners, staff members and trainers who have used the information herein to pilot test new products.

It is intended that the trainer delivering this course will be familiar with pilot testing as well as being a capable trainer. However, for those who may want to brush up on their training skills, there is an accompanying manual (or Microsoft Word file on CD) specifically discussing training skills and training issues. There are many other training manuals which the trainer may consult, including the “Participatory Learning & Action: A Trainer’s Guide” of the IIED Participatory Methodology Series.1

There’s already a Pilot Testing Manual on the MicroSave Website. Why is there a training curriculum also?

Several of the “Ice Breakers, Refreshers, etc.” come from these manuals.

Some people will read the Pilot Testing manual that is on our website and find that to be enough for their organisation to go forward with a pilot test. However, we have had many people and organisations who asked for a training course as well. Some people feel that it is faster and easier to train all the members of a pilot test team in the pilot testing process at once. This way they will literally all be “reading from the same page”. Who Should I be training? You may choose (or be chosen) to train this course for different types of participants. Each will have different positives and challenges. Training an MFI’s potential pilot test team: Training the potential members of the pilot testing team in one MFI is the ideal training situation. All exercises will be directly relevant and useful in the immediate future – they will be developing the actual work product needed by the MFI. For the trainer, all examples would require tailoring to directly address the needs of the one MFI. However, because the MFI team will be using the training as also an actual worksite, it may take slightly longer than the timings given here. Training potential pilot test team members – multiple MFIs: It may not be feasible (cost, time, number of requests) to train just one organisation. The trainer should insist – as much as possible – that the MFIs must send at least three or four members of the “inner core” of the product team to the training. Training the key members of the team will show that the MFIs are serious about the training and will allow the teams to breakout into their own organisations, performing the exercises as relevant to their own MFIs. It may also provide for interesting and rich discussion between MFIs as to why/how their responses to the various exercises differ. But, beware – if your clients are in the same market, they are not likely to go into the details of their product and the testing protocols – it simply wouldn’t make sense to give your competitors such an edge! Training individuals: It will be more difficult to provide this training to many individuals from many different organisations. If this is the case, the training should be handled more like a Training of Trainers as these individuals should be responsible for taking back the information to their organisation in order to train up the Pilot Testing Team and management how to plan, conduct and monitor a pilot test. What do I need to tell my participants need to bring with them? The trainer must insist –and ensure- that the participants to the course are coming to learn and “do”. They are not coming to learn how to do it later, when they return to their MFIs. Therefore, this course is limited to MFIs and participants who have a product ready – or almost ready – to be pilot tested. The

1 They can be reached at International Institute for Environment and Development/ 3 Endsleigh Street, London, WC1H ODD, UK

Trainer’s Manual Planning, Conducting & Monitoring Pilot Tests - Loans

MicroSave – Market-led solutions for financial services

3

amount of information “lost” in the long delay between the training course and an actual product to be tested dictates that this training follows directly on an actual product development process. In addition, the participants must bring with them laptops that ideally have been loaded with all the information that they may need. This will include, among others, contact lists, product information for the new product being tested, financial projections (as much as may have already been done, and possibly with as much detailed costing information as the organisation is comfortable providing) etc.

What do I need from MicroSave for the Training? These manuals are intended to be utilised with several accompanying documents, all of which are located on the MicroSave resource CD or website www.MicroSave.org .

Manuals:

Participants’ Manual: MicroSave’s Planning, Conducting and Monitoring Pilot Tests manual.

Participants’ Workbook:

The planning workbook is a short, step by step guide for participants to ensure that they plan, conduct and monitor the pilot test in the most efficient and effective manner. The workbook provides matrices, examples and checklists for each step in the pilot test process. The trainer should make sure that the workbook can be downloaded to the participant’s laptops (or sent via email).

Extra Material for Participants: Handouts:

An electronic folder of handouts is included. It should be noted that several of the handouts are in a Workbook that is designed to help participants leave the training with much of the initial planning for the their pilot-test completed. Ideally all handouts should be made available in soft copy so that they can be used by participants when they return to their institutions. Whenever possible, participants should bring their own computers so that they can complete this initial planning on their own machines.

Exercises:

An electronic folder of handouts is also included. These are primarily for the financial projection exercise (on an Excel spreadsheet) and computers are essential for running this exercise.

Extra Material for Trainer…and Participants Slideshows:

The slideshow folder is again separated by suggested training days. This course can be trained in several ways, as discussed herein. Ensure that you have the slideshow in the format most useful to you.

Slides can be printed onto overhead slides and utilised with an overhead projector. However, due to the number of slides, the amount of text, and the “animation” of slides, it is highly recommended that the trainer utilises an LCD projector, if one can be located (and electricity is available, etc.). Many participants request that they are provided with a copy of the slideshows at the end of the course, which the trainer is free to provide to them.

Practical Examples Practical examples have been provided throughout the course based on the experience of MicroSave with its Action Research Partners. The trainer should review the practical examples and where possible supplement or replace the examples given on the basis of his / her experience.

Trainer’s Manual Planning, Conducting & Monitoring Pilot Tests - Loans

MicroSave – Market-led solutions for financial services

4

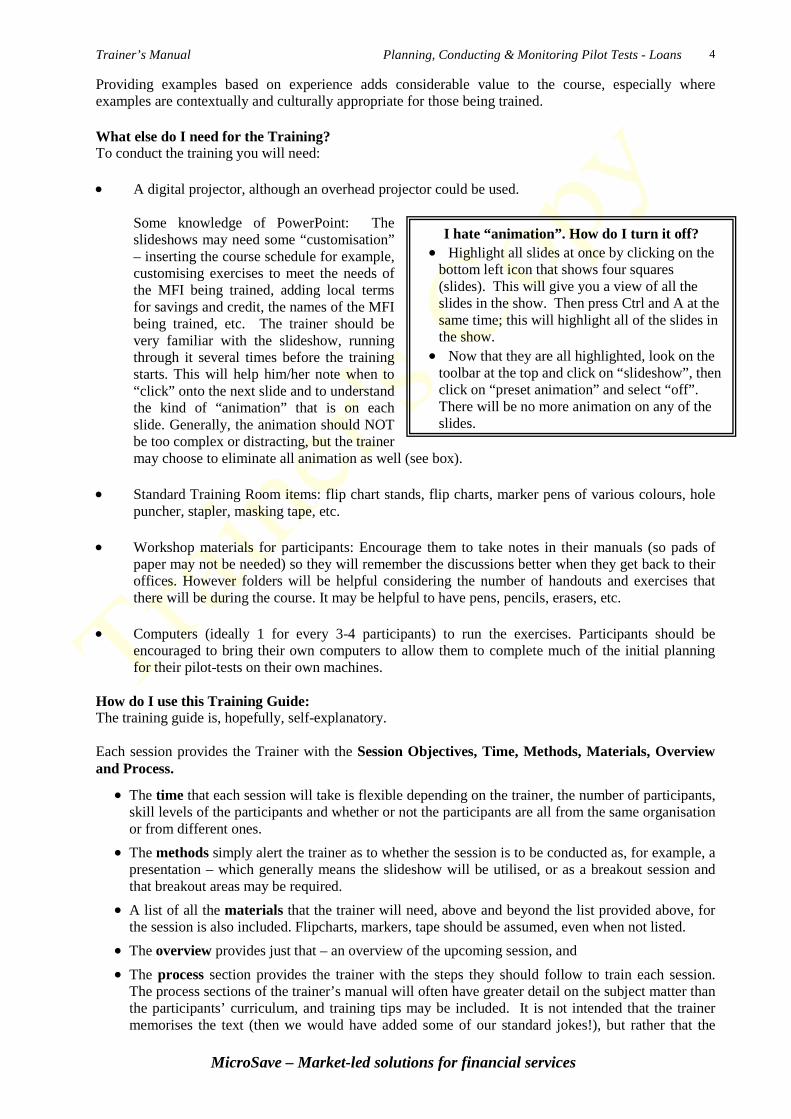

I hate “animation”. How do I turn it off? • Highlight all slides at once by clicking on the

bottom left icon that shows four squares (slides). This will give you a view of all the slides in the show. Then press Ctrl and A at the same time; this will highlight all of the slides in the show.

• Now that they are all highlighted, look on the toolbar at the top and click on “slideshow”, then click on “preset animation” and select “off”. There will be no more animation on any of the slides.

Providing examples based on experience adds considerable value to the course, especially where examples are contextually and culturally appropriate for those being trained. What else do I need for the Training? To conduct the training you will need:

• A digital projector, although an overhead projector could be used.

Some knowledge of PowerPoint: The slideshows may need some “customisation” – inserting the course schedule for example, customising exercises to meet the needs of the MFI being trained, adding local terms for savings and credit, the names of the MFI being trained, etc. The trainer should be very familiar with the slideshow, running through it several times before the training starts. This will help him/her note when to “click” onto the next slide and to understand the kind of “animation” that is on each slide. Generally, the animation should NOT be too complex or distracting, but the trainer may choose to eliminate all animation as well (see box).

• Standard Training Room items: flip chart stands, flip charts, marker pens of various colours, hole

puncher, stapler, masking tape, etc. • Workshop materials for participants: Encourage them to take notes in their manuals (so pads of

paper may not be needed) so they will remember the discussions better when they get back to their offices. However folders will be helpful considering the number of handouts and exercises that there will be during the course. It may be helpful to have pens, pencils, erasers, etc.

• Computers (ideally 1 for every 3-4 participants) to run the exercises. Participants should be

encouraged to bring their own computers to allow them to complete much of the initial planning for their pilot-tests on their own machines.

How do I use this Training Guide: The training guide is, hopefully, self-explanatory. Each session provides the Trainer with the Session Objectives, Time, Methods, Materials, Overview and Process.

• The time that each session will take is flexible depending on the trainer, the number of participants, skill levels of the participants and whether or not the participants are all from the same organisation or from different ones.

• The methods simply alert the trainer as to whether the session is to be conducted as, for example, a presentation – which generally means the slideshow will be utilised, or as a breakout session and that breakout areas may be required.

• A list of all the materials that the trainer will need, above and beyond the list provided above, for the session is also included. Flipcharts, markers, tape should be assumed, even when not listed.

• The overview provides just that – an overview of the upcoming session, and

• The process section provides the trainer with the steps they should follow to train each session. The process sections of the trainer’s manual will often have greater detail on the subject matter than the participants’ curriculum, and training tips may be included. It is not intended that the trainer memorises the text (then we would have added some of our standard jokes!), but rather that the

Trainer’s Manual Planning, Conducting & Monitoring Pilot Tests - Loans

MicroSave – Market-led solutions for financial services

5

Idea:

trainer feels confident discussing the issues at hand. The trainer should bring in relevant examples from her own MFI experiences and encourage participants to discuss their own experiences. Adults generally learn better from “real life” rather than theoretical discussions.

Finally, the trainer will find the following SYMBOLS in the manual to signify different things.

The idea symbol means that you will find comments from our experienced staff and certified trainers. More comments, questions and ideas can be directed to MicroSave, their research partners or their trainers by using the e-mail addresses on the front of this manual, or accessing the website.

This symbol helps the trainer find the exercises that are in each session.

Preparing Your Slideshow MicroSave has “hidden” slides within each training. These will not appear when you are doing the slide presentation, but they provide additional details and more information from the toolkit. It is your job as a trainer to go through the slide presentation and decide which slides to “unhide” for greater depth in a particular session. Likewise, you may choose to hide some slides that are not as relevant to your audience. See the box at right for the steps to hide or unhide a slide. Also, when printing out the slides you need to be careful to uncheck the box that says “Print Hidden Slides.” Otherwise all the slides will be printed for your participants and they will have a difficult time following your presentation (because you will skip over several slides). Preparation For Training You have chosen your participants for the course (or they have chosen you!) and you have:

• COSTED and CONTRACTED the training and agreed with the MFI the number of days for training and follow-up; you have sub-contracted additional trainers and assured that all contracts and TORs are prepared.

• Sent, via e-mail or hard-copy, all the “pre-course” handout files to your participants, if there are going to be any.

• Sent via e-mail and/or hard copy, a letter requesting that the participants bring laptops, MFI financial statements and all relevant information from the market research/product concept testing to ensure that the training is as useful and “real-life” as possible.

• Chosen an appropriate venue (steady supply of electricity, enough room for “breakout groups”, etc.) and seating plan for the number of participants you will have (a “U” shaped seating arrangement; 6 tables angled towards the front, etc.)

• Ensured that participants are all in the process of completing, or have completed the product development process and have the appropriate information available to them on the laptops that they will be bringing with them.

• Copied, bound and prepared all the manuals and handouts. • Practiced with the slideshow so that you are confident how to use it.

Offers training suggestions – trainer could try brainstorming, trainer could lecture, etc.

Hiding and Un-hiding Slides

1. On the Slides tab in normal view, select the slide you want to hide.

2. On the Slide Show menu, click Hide Slide. The hidden slide icon appears (or disappears to unhide) with the slide number inside, next to the slide you have hidden

Trainer’s Manual Planning, Conducting & Monitoring Pilot Tests - Loans

MicroSave – Market-led solutions for financial services

6

Alternative Lesson Planning Especially if you are working with only one MFI, you may be called on to deliver this training in stages. For example, you may want to train “Day 1” on a Monday and allow them the rest of the week to complete the Steps covered in Day 1. The following Monday you may train “Day 2”, etc. If you do choose to train in this way, be aware of timing issues. You will need to take some time in the morning to review the work of the participants in the prior week. You may need to provide an hour or so to allow them to finalise the information that they produced over the prior week. This will necessitate some changes in the timing of each training “Day”. It is not recommended that the training be compressed into a very short time period nor overly extended. The “Days” have been calculated to allow the team plenty of time to work in detail on their MFI’s own needs for pilot testing. Compressing this time may lead to confusion, and extending it may mean that the group is spending too much time in an “academic” setting and not enough time “doing it”.

Trainer’s Manual Planning, Conducting & Monitoring Pilot Tests - Loans

MicroSave – Market-led solutions for financial services

7

Session One: Participants Introduction and Overview2

Session Objectives: • Get to know all participants, their organisations and their roles within their MFIs • Understand what is expected of them, and what they expect from the course • Have an overview of course, outline/schedule

Time: 30 minutes Methods: Presentation Materials: Slide Show: PowerPoint presentation entitled

“Session One” – customised by the trainer with the course content pages. This session consists of approximately 5 slides (including 2 introduction)

Handouts:

• Handout 1.1 Timetable Overview: This session welcomes the participants to the course and gives them an idea of

what to expect over the next three days. 1. Opening Remarks

Time: 5 minutes Slides: 3 (including 2 introduction)

Welcome participants and introduce facilitators Read the session objectives – as you will do in each of the sessions. The slideshow will guide you on this, as well. 2. Suggested Ground Rules

Time: <5 minutes Slides: 1

The trainer may choose to add/subtract ground rules from the list on the Power point show. The trainer may ask the participants what their expectations are for this course. However, as the selection process should be quite rigorous, the participants should know what to expect – and be ready to start working!

3. Overview of Course/ Course Outline

Time: 10 – 20 minutes Slides: 1 Handout: Course Schedule (Handout 1.1) or the timetable that you have created yourself.

2 The authors is indebted to staff and management of the Kenya Post Office Savings Bank, Tanzania Postal Bank, and the Elgon Cooperative Society Limited, FINCA Uganda and Equity Building Society, Kenya at which institutions this methodology was extensively discussed and applied to their product testing process.

Trainer’s Manual Planning, Conducting & Monitoring Pilot Tests - Loans

MicroSave – Market-led solutions for financial services

8

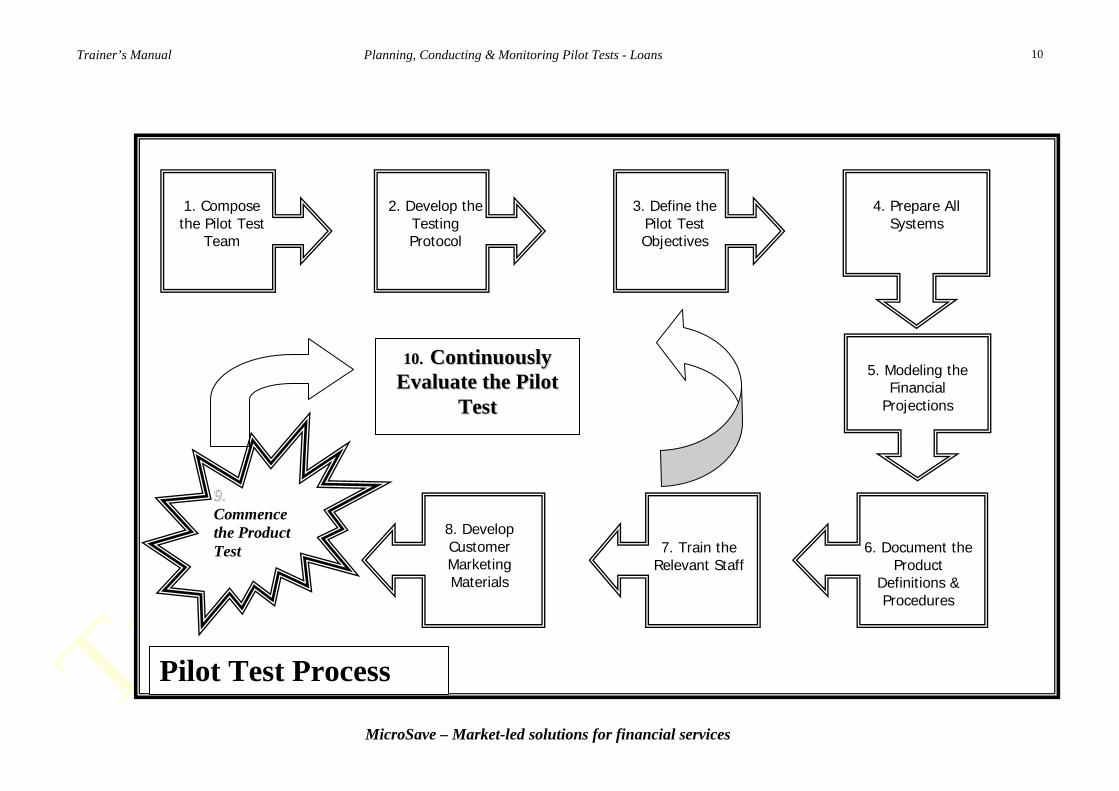

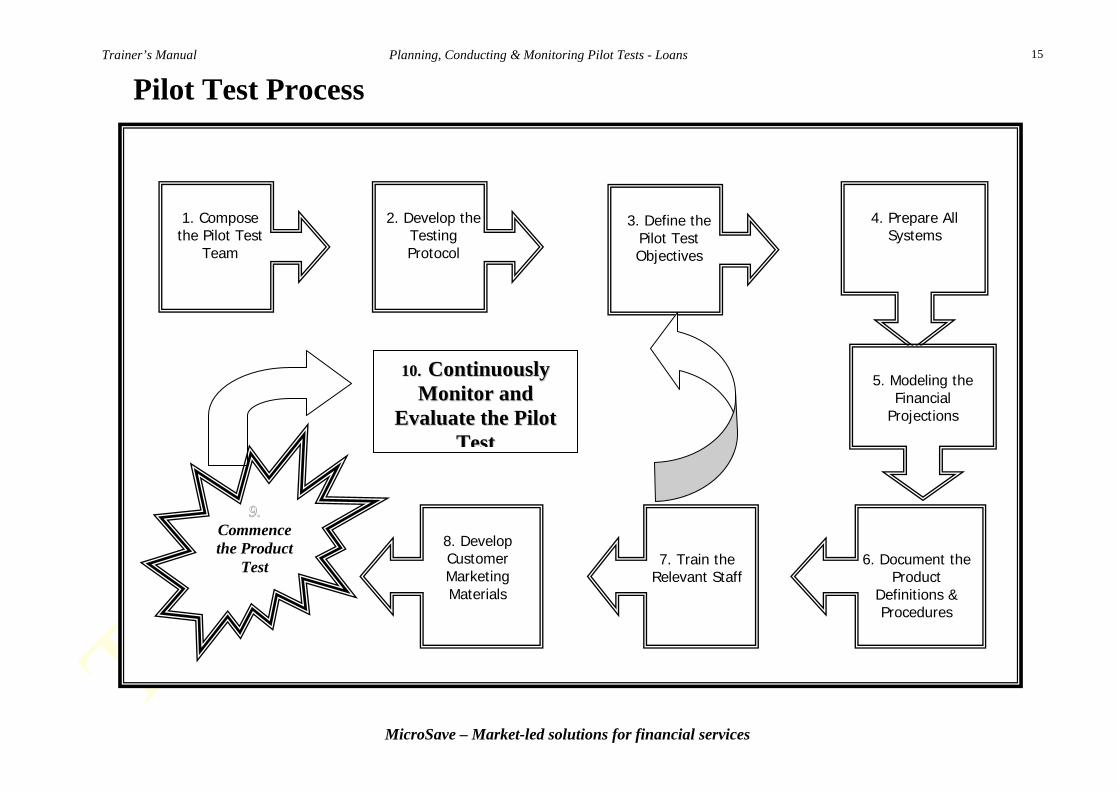

Course Overview: This course will be covering the various stages of planning, conducting and monitoring a pilot test. We have broken the pilot test process down into ten steps, and we have arranged the training sessions along the ten steps. We will have an exercise in each of the sessions to ensure that we all understand the concepts being discussed. Participants can choose to work on a loans or savings product (especially if they have brought the actual product information which the MFI plans to pilot test after this training). The trainer should ensure that the participants realise that the lessons in this course will apply to a broad range of microfinance products, not just the specific one being tested today. The ten steps of pilot testing are shown in a flow chart/diagram on the following page. We will be going into each of these steps throughout the course, and we will be going Introducing Pilot Testing in more detail in the next session.

Do not go into detail here, this will be gone over in much more depth in the next session, and then in detail step by step throughout the training.

For now, let us simply look at the flow chart and realise that at the end of these steps (Step 10: Evaluation), the pilot test team will have to make an important decision:

However, pilot testing is rarely that smooth. In many cases, we will discover upon evaluation that there are changes that need to be made in the product, putting us back into the middle of the process (re-doing the financial projections, making some changes to the delivery mechanisms, re-training staff in how to market and deliver the product, etc.).

Either ending may be considered a success!

Q: What are the Ten Steps of Pilot Testing? These steps complement each other in a comprehensive manner:

1. Composing the Pilot Test Team 2. Developing the Testing Protocol 3. Defining the Objectives 4. Preparing All Systems 5. Modelling the Financial Projections 6. Documenting the Product Definitions & Procedures 7. Training the Relevant Staff 8. Developing Customer Marketing Materials 9. Commencing the Product Test 10. Monitoring and Evaluating the Test

Either the pilot test has shown that the product is successful and we will roll out the product to our other MFI branches….

Or Not Sometimes, we will go through the entire pilot test process and realise: This product isn’t

going to be good for our institution.

Let’s stop and re-think our whole product idea.

The man who makes no mistakes does not usually make anything.

Bishop WC Magee

Trainer’s Manual Planning, Conducting & Monitoring Pilot Tests - Loans

MicroSave – Market-led solutions for financial services

9

By following these steps, your MFI will be able to control the process of pilot testing. It enables full participation, the potential for rapid trouble-shooting, effective and efficient feedback, and professional management of the product.

Q: How Do We Use the Information in this Training Manual and the Workbook?

The following sections will describe each step in detail and offer examples and worksheets so that your MFI can begin the product testing process right away. We suggest that management read through all the steps carefully before beginning the pilot testing process. Use the Workbook (or make photocopies of the worksheets) as you go along, modifying, where necessary, for your institution’s particular needs. Use the checklists (in the manual and the workbook) at the end of each step to be sure you have covered all the steps completely. Once the pilot testing team is formed, members will generally be assigned to different steps for completion. Some steps or parts of steps must be completed before others. For example, you need to know generally what systems your institution will use before you can complete the projections. But, you would not buy the required fixed assets until the time when you had to in order to have them in place one month prior to the planned test commencement date. During this time, several other steps would have been substantially completed.

Trainer’s Manual Planning, Conducting & Monitoring Pilot Tests - Loans

MicroSave – Market-led solutions for financial services

10

4. Prepare All

Systems

1. Compose the Pilot Test

Team

2. Develop the

Testing Protocol

3. Define the

Pilot Test Objectives

8. Develop Customer Marketing Materials

7. Train the Relevant Staff

6. Document the Product

Definitions & Procedures

999... Commence the Product Test

1100.. CCoonnttiinnuuoouussllyy EEvvaalluuaattee tthhee PPiilloott

TTeesstt

5. Modeling the

Financial Projections

Pilot Test Process

Trainer’s Manual Planning, Conducting & Monitoring Pilot Tests - Loans

MicroSave – Market-led solutions for financial services

11

Session Two: Introduction to Pilot Testing Session Objectives: • Understanding what Pilot Testing means and how it fits into the product development

cycle. • Ensuring that our MFI has the capacity to pilot test

Time: 45 minutes Methods: Presentation Materials: Slide Show: This session consists of approximately 16 slides “Session Two” Handouts:

•

•

Handout 2.1 Briefing Note # 14: Systematic Approach to Product Development Handout 2.2 10 Steps of Pilot Testing (Workbook)

• Handout 2.3 Briefing Note # 9: Questions that should Precede Product Development

• Handout 2.4 Briefing Note # 24: Lessons from Pilot-Testing

Overview: This session gives a deeper introduction to Pilot Testing. 1. Introduction to Pilot Testing: What, Why and Why not? Time: 15 minutes Slides: 7 (including 3 Introduction)

Q: What is a Pilot Test? Definitions: According to Collins Paperback English Dictionary, a “pilot” is a person who is qualified to operate an aircraft, or steer a ship in and out of port. In other words, a pilot acts as a guide. A “test” is defined as something that measures the worth of a person or thing by trying it out, or an examination of a person, substance, material or system. Combining these two words, we can say that a pilot test is something that measures the worth of a thing, in such a way that the test itself acts as a guide. When applied to a new product or service, a pilot test is something that measures its worth on a limited scale and scope so that the results of the test guide management decision-making about a broader rollout of the product. By pilot testing a new product before rollout, the company avoids errors on a large scale that could be corrected based on the lessons from the small-scale test.

Q: Why Pilot Testing? Whenever a new product is being developed, whether in manufacturing, business or banking, it is prudent to test the product.

Trainer’s Manual Planning, Conducting & Monitoring Pilot Tests - Loans

MicroSave – Market-led solutions for financial services

12

Take shoes, for example. At Acme Shoes, market research showed that customers wanted yellow canvas shoes with rubber toes. But, before the company commences manufacturing 2 or 3 million pairs, they want to be sure that the shoes will sell and make a profit. So, the company runs a “pilot test.” The pilot test consists of :

• making 1,000 pairs of the new yellow canvas shoes with rubber toes • test-marketing (selling) them

in a limited geographical area, for a limited period of time,

• Selling them at an initial price that covers costs3

• Analysing the results plus yield a profit.

All this is done to see if the new product is worth producing on a larger scale. Acme manufactures 1,000 shoes, trains the sales people in one store (limiting the geographic area) and starts selling them at a carefully calculated price. The store manager collects data on the sales.

From its pilot test, Acme Shoe management wants to know several things:

• Will customers buy and wear yellow canvas shoes with rubber toes (or will they buy only Acme’s traditional leather shoes)?

• Is the new shoe profitable? How much will customer’s pay for yellow canvas shoes with rubber toes (is it enough to cover all costs plus yield a profit)?

• Do these yellow canvas shoes with rubber toes satisfy customer desires?

• Are the shoes of good quality? Do they hold up to consumer use?

Throughout the testing period, data is collected and analysed. Through ongoing refinement of the shoes during the pilot test, the company becomes reasonably knowledgeable about the likely market response to the shoes, and should have maximized the potential for market appeal. By the end of the testing period, the company will be able to make a reasonable and educated decision about whether or not to launch the product on a larger scale. Without a pilot test, the company could end up manufacturing 2 million pairs of yellow canvas shoes with rubber toes, only to find that there was no market for them.

Q: What does this have to do with Microfinance and banking? The connection between them lies in the importance of pilot testing new products. The process of pilot testing is as important in banking and microfinance institutions as it is in manufacturing and other business enterprises. Market research may have shown that your Microfinance customers want a new savings – or loan - product. The product has been developed from concept to prototype, and the prototype has been refined. But it is important for institutional management to know if this new product is something that the customers will really use, with terms that result in a net positive yield to the MFI. Your bank or MFI can gather this information through designing, conducting, monitoring and evaluating an appropriate and effective pilot test of the product – a test that will accurately measure customer needs and desires, and will produce the information needed for effective institutional decision making. This Toolkit outlines a process of pilot testing products.

3 These testing prices would be calculated based on large volume projections with an amortization of research and development costs. They would not try to recoup the cost of R&D and manufacturing of a small lot in the price of that first batch of product.

Trainer’s Manual Planning, Conducting & Monitoring Pilot Tests - Loans

MicroSave – Market-led solutions for financial services

13

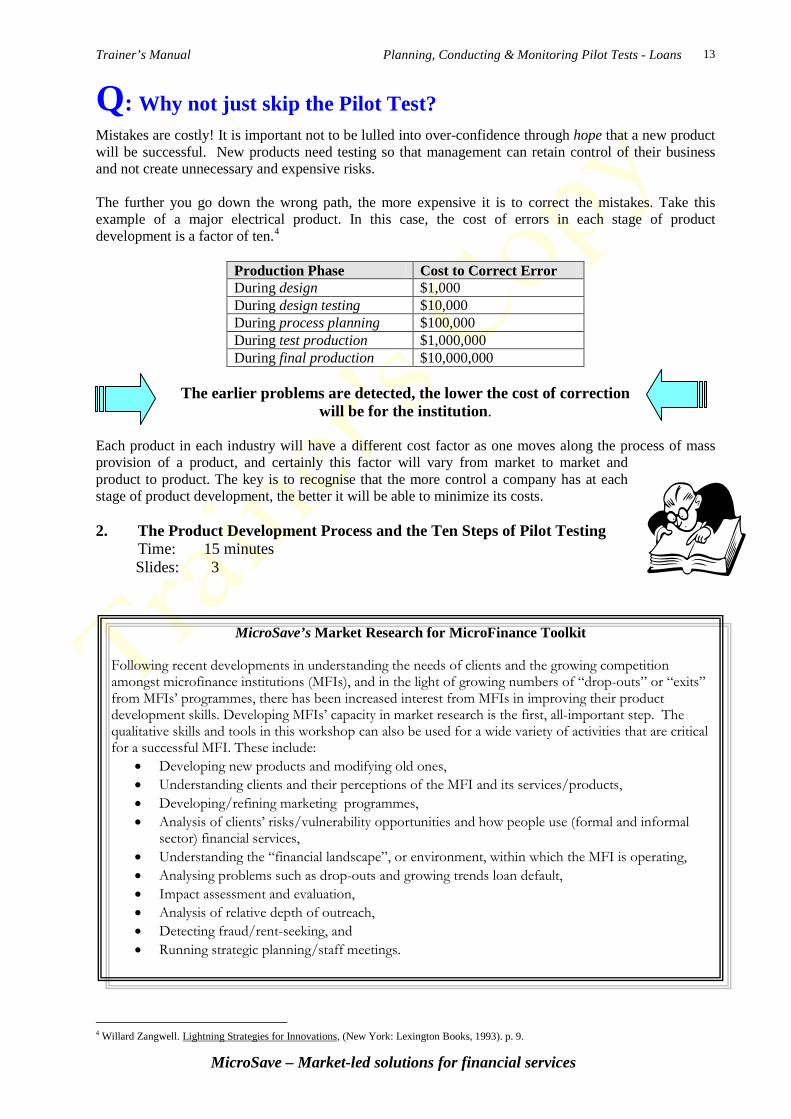

Q: Why not just skip the Pilot Test? Mistakes are costly! It is important not to be lulled into over-confidence through hope that a new product will be successful. New products need testing so that management can retain control of their business and not create unnecessary and expensive risks. The further you go down the wrong path, the more expensive it is to correct the mistakes. Take this example of a major electrical product. In this case, the cost of errors in each stage of product development is a factor of ten.4

Production Phase Cost to Correct Error During design $1,000 During design testing $10,000 During process planning $100,000 During test production $1,000,000 During final production $10,000,000

The earlier problems are detected, the lower the cost of correction

will be for the institution. Each product in each industry will have a different cost factor as one moves along the process of mass provision of a product, and certainly this factor will vary from market to market and product to product. The key is to recognise that the more control a company has at each stage of product development, the better it will be able to minimize its costs. 2. The Product Development Process and the Ten Steps of Pilot Testing Time: 15 minutes Slides: 3

4 Willard Zangwell. Lightning Strategies for Innovations, (New York: Lexington Books, 1993). p. 9.

MicroSave’s Market Research for MicroFinance Toolkit Following recent developments in understanding the needs of clients and the growing competition amongst microfinance institutions (MFIs), and in the light of growing numbers of “drop-outs” or “exits” from MFIs’ programmes, there has been increased interest from MFIs in improving their product development skills. Developing MFIs’ capacity in market research is the first, all-important step. The qualitative skills and tools in this workshop can also be used for a wide variety of activities that are critical for a successful MFI. These include:

• Developing new products and modifying old ones, • Understanding clients and their perceptions of the MFI and its services/products, • Developing/refining marketing programmes, • Analysis of clients’ risks/vulnerability opportunities and how people use (formal and informal

sector) financial services, • Understanding the “financial landscape”, or environment, within which the MFI is operating, • Analysing problems such as drop-outs and growing trends loan default, • Impact assessment and evaluation, • Analysis of relative depth of outreach, • Detecting fraud/rent-seeking, and • Running strategic planning/staff meetings.

Trainer’s Manual Planning, Conducting & Monitoring Pilot Tests - Loans

MicroSave – Market-led solutions for financial services

14

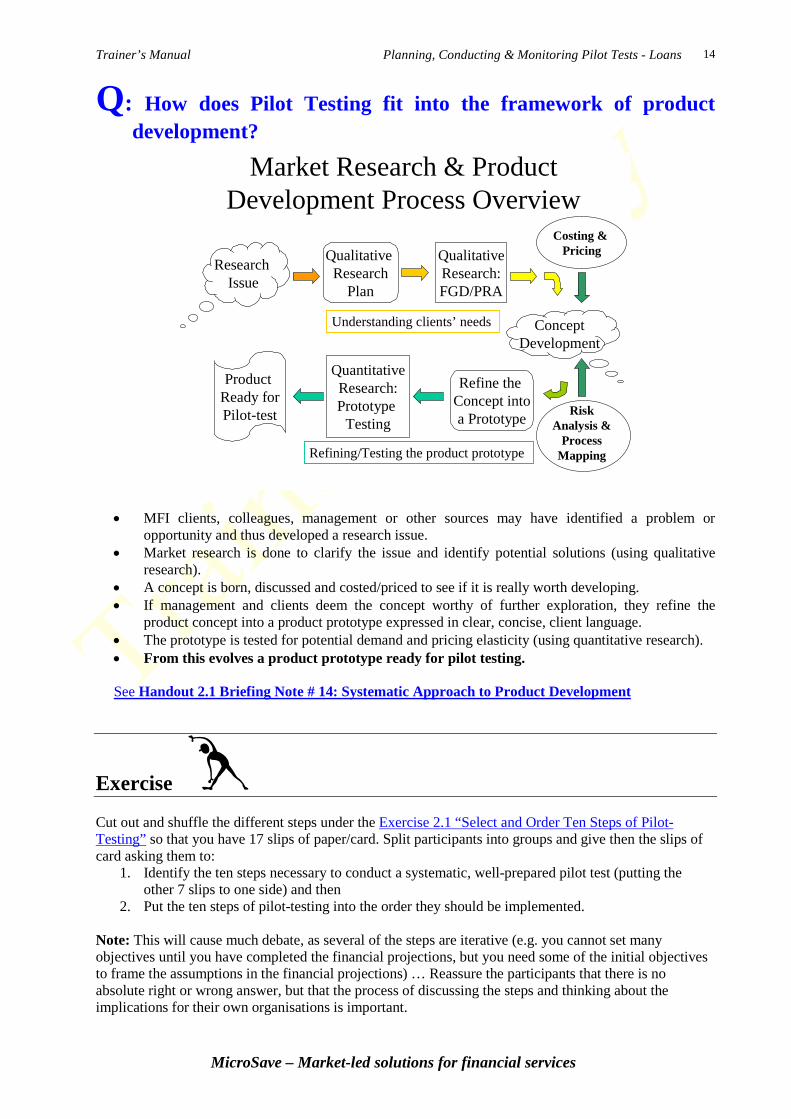

Q: How does Pilot Testing fit into the framework of product development?

• MFI clients, colleagues, management or other sources may have identified a problem or

opportunity and thus developed a research issue. • Market research is done to clarify the issue and identify potential solutions (using qualitative

research). • A concept is born, discussed and costed/priced to see if it is really worth developing. • If management and clients deem the concept worthy of further exploration, they refine the

product concept into a product prototype expressed in clear, concise, client language. • The prototype is tested for potential demand and pricing elasticity (using quantitative research). • From this evolves a product prototype ready for pilot testing. See Handout 2.1 Briefing Note # 14: Systematic Approach to Product Development

Exercise Cut out and shuffle the different steps under the Exercise 2.1 “Select and Order Ten Steps of Pilot-Testing” so that you have 17 slips of paper/card. Split participants into groups and give then the slips of card asking them to:

1. Identify the ten steps necessary to conduct a systematic, well-prepared pilot test (putting the other 7 slips to one side) and then

2. Put the ten steps of pilot-testing into the order they should be implemented. Note: This will cause much debate, as several of the steps are iterative (e.g. you cannot set many objectives until you have completed the financial projections, but you need some of the initial objectives to frame the assumptions in the financial projections) … Reassure the participants that there is no absolute right or wrong answer, but that the process of discussing the steps and thinking about the implications for their own organisations is important.

Market Research & Product Development Process Overview

QualitativeResearch:FGD/PRA

ConceptDevelopment

Qualitative Research

Plan

Refine the Concept intoa Prototype

Research Issue

QuantitativeResearch:Prototype

Testing

Product Ready forPilot-test

Understanding clients’ needs

Refining/Testing the product prototype

Costing & Pricing

Risk Analysis &

Process Mapping

Trainer’s Manual Planning, Conducting & Monitoring Pilot Tests - Loans

MicroSave – Market-led solutions for financial services

15

4. Prepare All

Systems

1. Compose the Pilot Test

Team

2. Develop the

Testing Protocol

3. Define the

Pilot Test Objectives

8. Develop Customer Marketing Materials

7. Train the Relevant Staff

6. Document the Product

Definitions & Procedures

999... Commence the Product

Test

1100.. CCoonnttiinnuuoouussllyy MMoonniittoorr aanndd

EEvvaalluuaattee tthhee PPiilloott TTeesstt

5. Modeling the

Financial Projections

Pilot Test Process

Trainer’s Manual Planning, Conducting & Monitoring Pilot Tests - Loans

MicroSave – Market-led solutions for financial services

16

The Pilot Testing Overview in the previous diagram shows how the product testing process flows from a test-ready product through testing and feedback. We’ll get to the details of all of the steps, but let’s look quickly at the Steps.

1. Assemble a team of appropriate people who 2. Develop the testing protocol (rules) 3. Ensure that the objectives are clear to all parties 4. Ensure that all systems are in place to meet the needs of the new product (the accounting system,

for example, or a staff incentive system, etc.) 5. Work with the finance staff to develop clear projections 6. Draft the policies and procedures manual and 7. Train the appropriate staff (all staff directly involved) 8. Ensure that the marketing materials are prepared and 9. Institute a feedback process for the product and start the test 10. Evaluate the results of the test

We review feedback (from clients, from staff, from Management, from MIS, accounting systems, etc.) against the objectives we have set for this product. The result of the review indicates what should happen next. In many cases, the feedback shows that the product does not meet the objectives. This is the most common scenario! In a savings product, this might mean that the interest rate must be changed, or the forms must be altered to make them easier for customers to complete or the marketing of the product inside the office –to staff - needs to be improved. In a loan product, growth may be significantly slower than projected. This might call for an adjustment to the method for determining initial loans, or a change in the application process to make it more customer-friendly, or changing the size of the groups to better fit the local culture. Adjust and Test: When the feedback indicates that the product does not meet the objectives, the product must go looping back through the process of (4) financial projections, (5) systems adjustments, (6) product definitions, (7) staff training and (8) marketing. Feedback after adjustments may still show some problems. The product must be refined until all the objectives are met.

• Roll out: Once the product finally meets the objectives, the product can be considered successful and it can move on to the roll-out phase. This hardly ever occurs the first time through the Pilot Test.

• Terminate: There are times when, no matter how much adjusting the institution does, the product simply does not satisfy the objectives. Most often such a product should simply be terminated. The feedback step is critical to making any decision about the future of the product.

After the product is rolled-out, the institution should continue to collect data and feedback from clients and internal sources. Feedback will help management to further improve the product over time.

Trainer’s Manual Planning, Conducting & Monitoring Pilot Tests - Loans

MicroSave – Market-led solutions for financial services

17

3. Capacity to Pilot Test Time: 15 minutes Slides: 4

Q: What are the Key questions that should precede new product development?

Prior to undertaking new product development the MFI should ask six essential questions. See the MicroSave paper Look Before You Leap: Key Questions That Should Precede Starting New Product Development (Wright et al.) for more details.5

1. Motivation: Are we starting product development to make our MFI more market-driven?

2. Commitment: Are we setting about product development as a process? 3. Capacity: Can our MFI handle the strains and stresses of introducing a new product? 4. Cost Effectiveness: Do we fully understand the cost structure of our products? 5. Simplicity: Can we refine, repackage and re-launch existing product (s) before we develop a new

one? 6. Complexity and Cannibalisation: Are we falling into the product proliferation trap?

Q: Do risk analysis and Pilot Testing alone provide sufficient risk management?

No. Risk analysis and management is key to developing market led financial services, whilst the pilot test is of itself a risk management tool, it is not sufficient to wait for the pilot test to identify critical risks. A more proactive approach to risk analysis and management is required. Risk analysis and management should be integrated into the product development process. A formal risk assessment should be performed by an MFI before it commences the development of new products. The risk analysis should be updated before it undertakes critical activities, such as selection of an IT system, before the commencement of the pilot test, during the pilot test itself and in the evaluation of the pilot test prior to rolling out the new product. The process of risk analysis and management has been explored and developed in the Shorebank / MicroSave Toolkit for Institutional and Product Development Risk Analysis for MFIs, as described on the following page.

It’s also important to ensure that you can minimize potential loss of control of the Test and provide valuable information that management can use to improve the product.

5 See Looking Before You Leap: Key Questions That Should Precede Starting New Product Development (Wright et al.) for more details

A Pilot Test can minimize the risk of financial loss to the institution and the clients: “We offered the loan product at a price lower than our competitors… but then we found out that we were losing a lot of money. We should have pilot tested it in one branch first”. (MFI manager) It can also guard against reputation risk: “They said they could operate savings accounts, but they are hopeless. I am taking my account elsewhere and so should you”. (Unhappy client)

Trainer’s Manual Planning, Conducting & Monitoring Pilot Tests - Loans

MicroSave – Market-led solutions for financial services

18

Q: What Must be Done Before the Pilot Test Process Begins? In addition to the steps shown in the diagram “Market Research and Prototype Development Process Overview”, an institution must ensure that it has the capacity to implement the process. Commencing the pilot testing process without adequate capacity will lead to a waste of time and money, and put the institution at risk.

Q: How do we Assess our Capacity to Pilot Test? In general, an MFI should already:6

practice the level of tracking and management analysis required of a new product with its current products;

understand the capacity requirements in all relevant departments; have reviewed and assessed as present and effective, the institution’s:

Institutional Strategy Financial viability Organisational Structure Human resources Marketing Systems

have the will of management and the Board behind the process, and the will of the staff – especially those who will be directly implementing the product; and

possess, or have available, staff that can manage, implement, and develop the new product, as well as have the available capacity to train all relevant staff.

All this should be completed before significant funds are expended on the new product development process, and certainly before the institution enters the Pilot Testing Phase.

6 Adapted from Monica Brand. Guide to New Product Development Institutional Diagnostic. Early draft. USAID/MBP

ShoreBank / MicroSave Toolkit for Institutional and Product Development Risk Analysis for MFIs

Proactive risk management is essential to the long-term sustainability of microfinance institutions (MFIs). This toolkit presents a framework for anticipating and managing risk in microfinance institutions with a particular emphasis on new product development. The toolkit is tailored to senior managers who play the most active role in setting the parameters and guidelines for managing risk.

There are two parts to this toolkit. Part 1 lays out a general framework for identifying, assessing, mitigating and monitoring risk in the MFI or bank as a whole. The document emphasizes the inter-relatedness of risks and the need for a comprehensive approach to managing them. Establishing a comprehensive risk management control structure in a financial institution is a necessary precondition to effectively managing risks related to new product development and roll-out.

Part 2 focuses on risks inherent to new product development and suggests tools to help manage the process. The toolkit’s approach to managing risk in new product development and roll-out is, by intent, conservative and time-consuming. However, sometimes it will be necessary to fast – track certain steps or maybe even take the risk of leaving some steps out for the hope of a greater gain down the line. However, ShoreBank and MicroSave caution against too much haste in rolling out new products. Being first in a market with a new product is not a sustainable competitive advantage. We recommend following and/or adapting all the steps in MicroSave’s product development process to suit your organisation’s needs, and complementing it with the risk mitigation tools provided in this toolkit. Managers should always weigh the costs of leaving out particular steps against the benefits that they might yield in preventing unnecessary cost and product failures, or increasing opportunities for new product successes down the line.

Trainer’s Manual Planning, Conducting & Monitoring Pilot Tests - Loans

MicroSave – Market-led solutions for financial services

19

Session Three: The No Pilot Test Case Session Objectives: • Understand when it is necessary to Pilot Test new products • Understanding the potential consequences of not Pilot Testing new products

Time: 45 minutes (30 min exercise)

Methods: Presentation with significant participation from group Buzz Groups Exercise and Report Back (30min) Materials: Slide Show: “Session Three” This session consists of approximately 10 slides

(including 1 introduction) Overview: This session considers where a pilot test is necessary.

Q: When should we pilot test new products?

“Pilot testing new products takes time and resources yet financial institutions developing new services are generally anxious to rollout their products quickly in order to gain higher profits and a commercial advantage over competitors. So are there occasions when a financial institution can develop new products without pilot testing?” Yes, but under specific circumstances. Where the new product is a refinement of an existing product: Where the product is a refinement of existing products it is often not necessary to pilot test the modification, as long as the modification has been properly researched and does not require major systems modifications. In October 2001, Equity received training in Market Research for Microfinance. During market research Equity discovered that although their clients were positive towards Equity that they strongly disliked the pricing of Equity’s products. Interest rates were expressed as declining balances, which were frequently misunderstood by potential clients. Furthermore, Equity imposed a range of small charges, which were not clearly communicated to clients, such as fees for photocopying or administration. In response to client criticisms Equity simplified their fee structures, and clearly communicated the new fee structure to clients. Client reactions were very positive. Where specific technical expertise is purchased: Instead of performing extensive market research and pilot testing a new housing loan. Teba Bank purchased housing loan expertise, by bringing in a team of professionals who had existing experience of offering housing loans in Teba Bank’s market. Where the product itself is low risk: Akiba Commercial Bank in Tanzania developed a successful salary loan product without pilot testing. For a commercial bank in East Africa, a salary loan product has become a “hygiene factor” - a commercial bank is expected to have a salary loan product with terms and conditions that are broadly similar to those of competitors. Secondly, salary loans are relatively low risk as employees frequently have a financial history with the institution that can be used to assess repayment ability, and the salary loan is usually secured against terminal benefits. However, for every product that is successful without a pilot test, there are many products that could have been improved with a pilot test. Several examples prove this point:

Trainer’s Manual Planning, Conducting & Monitoring Pilot Tests - Loans

MicroSave – Market-led solutions for financial services

20

Example 1. Tractor Loans: A South African bank saw that there was a high demand for tractors and decided to launch a Tractor Loan. Policies and procedures were developed, a 30% down payment was required, with 140% security, and repayments were seasonal to ensure that farmers could repay the loans from seasonal income. What happened? The loan was very popular, but ultimately failed. Many of the loan recipients were retrenched workers who used their redundancy payments to purchase tractors. Retrenched workers failed to understand the agricultural market. Loans financed second hand tractors, which proved difficult for customers to maintain. Tractors broke down and were gradually cannibalised for parts, without an income borrowers could not repay their loans. The bank found that it had insufficient staff to perform extensive field based follow up once problems started to emerge. Example 2 Too much success: Uganda Women’s Finance Trust (UWFT) was experiencing high levels of dropout and higher than acceptable levels of default. Using MicroSave market research techniques, UWFT made the decision to modify its loan products. Loan terms and amounts were increased, loan qualification periods were decreased and individual assessment of loans was introduced. Client response to the changed products was enthusiastic. In three months the portfolio outstanding increased by 50%. However, UWFT were not prepared for the rapid expansion in their portfolio and Portfolio At Risk rapidly increased. After this experience, UWFT management feel that major changes to products should be pilot tested, for several reasons; firstly, to ensure that the impact of changes to the product on the demand for the product can be properly tracked; secondly to allow the development of appropriate capacity and skills prior to the rollout of the product; thirdly to determine and plan for higher level institutional impacts such as liquidity, funding, changes in corporate image etc. Example 3 Changing Focus: When a financial institution changes its product focus, structured pilot testing becomes critical. Tanzania Postal Bank wanted to develop a micro-finance loan - it launched a small-scale, unstructured pilot test, which went reasonably well. However, as it rolled out the product the bank realised that its policies and procedures were not adequate, staffing levels were too low, and staff were not sufficiently knowledgeable in micro-finance monitoring. The bank is now addressing these problems. Example 4: Copycatting: A common way to reduce the risk of new products failing to meet the needs of the local marketplace is to copy successful products developed by other financial institutions. However, this too can be dangerous. Federal Savings a Cooperative based in Bangladesh tried to duplicate the innovative products of Safesave, which was successfully operating in Dhaka slums. However, although Federal Savings could copy the features of the product it could not duplicate the organisational culture, careful management and precise reporting systems that underpinned Safesave. With popular products, Federal Savings expanded rapidly became dangerously undercapitalised and eventually collapsed.”

Exercise Participants split into groups and consider the following questions. Time for exercise 15 minutes with 15 minutes for presentations

The no pilot case In three groups decide on two products that were not pilot tested one a success the other a failure. Provide the following information

• A very brief description of the product • What happened? • Reasons for success or failure • What could have been done better

Develop a five minute presentation in power point format

Trainer’s Manual Planning, Conducting & Monitoring Pilot Tests - Loans

MicroSave – Market-led solutions for financial services

21

Session Four: Step 1- Composing the Pilot Test Team Session Objectives: • Identifying the Pilot Test Team • Understanding the Activities of the Various Team Members • Terms of Reference for the Pilot Test Team

Time: 90 minutes (45 min exercise)

Methods: Presentation with significant participation from

group Buzz Groups Exercise and Report Back (45min) Materials: Slide Show: This session consists of approximately 25 slides (including 3

introduction) “Session Four” Handouts: The participants should all have their workbooks and CD-ROMs (or diskettes).

• Handout 4.1 Pilot Test Team Skill Areas (Workbook) • •

Handout 4.2 Team Member Specific Activities (Workbook) Handout 4.3 Sample ToRs for Pilot Test Team

Overview: This session starts participants on the Pilot Testing Process. They should be

thinking about how they are going to organise their pilot testing team within their own organisations.

1. Composing the Pilot Test Team Time: 15 minutes Slides: 9 (including 1 introduction) Your MFI has determined through market research using surveys, focus groups or Participatory Rapid Appraisal (PRA) that a new loan or savings product is needed, and has developed a product concept management believes will satisfy that need.7

7 This is commonly done in the research and design phase, which is preparatory to the pilot testing phase. An excellent guide for this research is MicroSave’s “Market Research for Microfinance.”

Key management and staff, perhaps even with the Board of Directors, have ascertained key features for this product and have a prototype design of how they want it to look and act. Now is the time for a Pilot Test Team to be organized, and the pilot testing process to begin.

Trainer’s Manual Planning, Conducting & Monitoring Pilot Tests - Loans

MicroSave – Market-led solutions for financial services

22

The first step to conducting a successful pilot test is to draw together a formal Pilot Test Team, which is ideally made up of individuals from each major area or department of the institution.

Q: Who Composes the Pilot Test Team?

This depends on the overall size of your MFI. In a large MFI, the person who puts together the Pilot Test Team may be the head of Research or the head of Marketing. In a very large institution it may be the head of New Product Development. In a medium-sized or small MFI it might be the Managing Director, Credit Manager, or a member of the Board of Directors. Oftentimes the central person drawing the team together is the “Product Champion.” This is the person with excitement and energy for the product who will pull it through all the problems and push for its success. The Product Champion also frequently serves as the “Team Leader” who must be prepared to lead his/her team, much like the Captain of a Football Team, through all the steps of pilot testing the product. S/he must be able to recognise the value of each Team member and maximize Team contributions for the value of the product and ultimately the company.

Q: How large should the Pilot Test Team be? The size of the Team depends on the size of the MFI. Generally there are between 4 and 10 members on the team. If your MFI has three to five key employees, then probably all of them will have roles to play and tasks to accomplish in the pilot testing process, and collectively will make up the Pilot Test Team. If your MFI is very large, then as many as ten key people may come together as the Pilot Test Team. Too many people on the team may hinder, rather than help, the process. What is most important is that the composition of the Team represents all major departments of the MFI, and is thus a representational

Pilot Test Team.

Q: Why do we need a representational Pilot Test Team? There are three reasons why a Pilot Test Team that represents all departments in an MFI is crucial to the success of a pilot test:

A Strong Pilot Test Team Is crucial to the success of the pilot test

Conducting a pilot test and then launching a new product is similar to a team sport in that individuals with different expertise come together, and as a group they have a single goal. In the same way that a football match is neither won nor lost by any single individual, pilot tests, and ultimately the products themselves, stand or fall on the collective efforts of many people within an institution.

The “Questions” in the manual are a good opportunity for you to engage your participants in discussion and ensure their participation.

Trainer’s Manual Planning, Conducting & Monitoring Pilot Tests - Loans

MicroSave – Market-led solutions for financial services

23

• Guidance: Team members provide guidance to the Team in their respective areas of expertise within the MFI. A Team composed of a cross-section of institutional management will be able to address most of the likely problems of the test either prior to the test, or as soon as problems arise.

• Assistance: A representational Team means that there will be someone in each department who understands the product and will be able to assist within the department whenever related issues come up.

• Ownership: A representational Team can help to generate institutional ownership and enthusiasm for the product throughout the organisation.

Q: Should the Pilot Test Team be a formal team? Yes, the Team should be formal, although many of the interactions between Team members will be informal. They should have a formal Terms of Reference (TOR) that clearly defines their role, and a Senior Manager or Board Member – someone who is not a member of the Pilot Test Team – should informally supervise them. A sample TOR is provided in Handout 4.3. The TOR clarifies the role, responsibilities, and authority of the Team, gains top management support for the test, and gives the Team clarity on what resources will be required and made available. There should be a formal meeting and communications schedule, as well as a contact list for each Team member. Finally, the TOR should identify the Team Leader, who is likely to be the Product Champion.

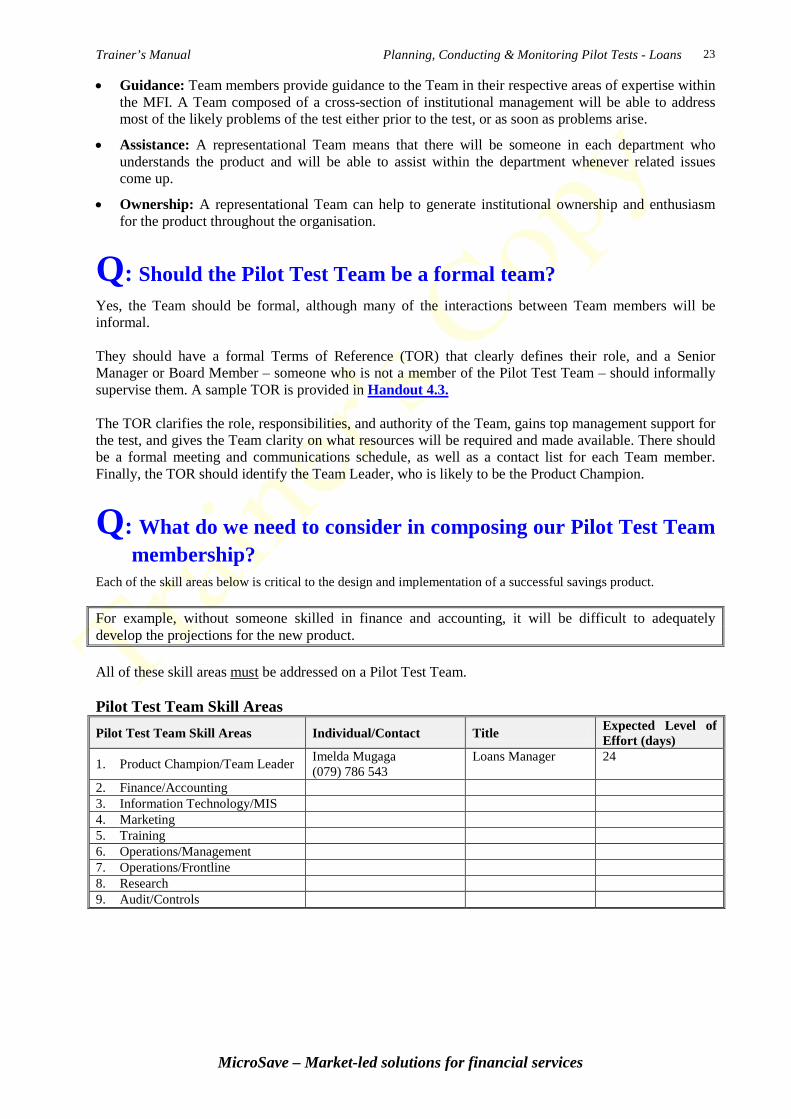

Q: What do we need to consider in composing our Pilot Test Team membership?

Each of the skill areas below is critical to the design and implementation of a successful savings product. For example, without someone skilled in finance and accounting, it will be difficult to adequately develop the projections for the new product. All of these skill areas must

be addressed on a Pilot Test Team.

Pilot Test Team Skill Areas Pilot Test Team Skill Areas Individual/Contact Title Expected Level of

Effort (days)

1. Product Champion/Team Leader Imelda Mugaga (079) 786 543

Loans Manager 24

2. Finance/Accounting 3. Information Technology/MIS 4. Marketing 5. Training 6. Operations/Management 7. Operations/Frontline 8. Research 9. Audit/Controls

Trainer’s Manual Planning, Conducting & Monitoring Pilot Tests - Loans

MicroSave – Market-led solutions for financial services

24

The days in the “level of effort” should be clearly understood. All members of the team have other work to do and therefore the level of effort should not indicate that they are “full-time” devoted to this project alone. For example, Imelda’s level of effort is 24 days, but they are spread over a much longer period. In fact, it is expected that on average she will put in 3 hours per day (a little over 2 days/week), though during the planning phase she will be putting in much more time, and then reducing her time significantly once the pilot test has begun and is in the monitoring stages. If your MFI is very large, then a sizable pool of potential Test Team members with the necessary expertise probably exists within the institution. The skill areas listed in the table above are all the basic skill areas needed for a savings or loan product. You should supplement the core team with people who have additional specific skills if those skill areas are required for a particular product. See Handout 4.1 (in the Workbook) allows participants to create own charts for their Pilot Test Team Skill Areas.

Q: What will all these people do on the team? All team members will have general and specific duties in relation to their department of representation.

The general duties relate to providing input in meetings and other pilot testing fora to reflect the needs, opinions, and resources offered by their respective departments.

The specific tasks will be related to their individual skills. The Team must be self-sufficient, covering all its needs within the Team or through co-opted members. The Team should not expect to simply delegate tasks to non-Team members and expect them to be concluded within the Team’s time frame. However, it would be advisable to ensure that the Director of Operations is asked for his input and advice in ensuring that the procedures manual is in line with the other procedures in the MFI.

For example, the Team will need to develop a procedures manual for the product. It would be unwise for the Team to simply inform the Director of Operations (a non-team member in this example) to have one prepared. First, only the Team members know the full details of the product in order to fully address the various activities of the Test. Second, only Team members are responsible (as per the TOR) for the outputs of the Test.

Give out the Workbook on diskette or CD Rom if possible. It will facilitate completion of exercises. If they are doing their “own MFI” work, it will be more useful on computer, anyway

Trainer’s Manual Planning, Conducting & Monitoring Pilot Tests - Loans

MicroSave – Market-led solutions for financial services

25

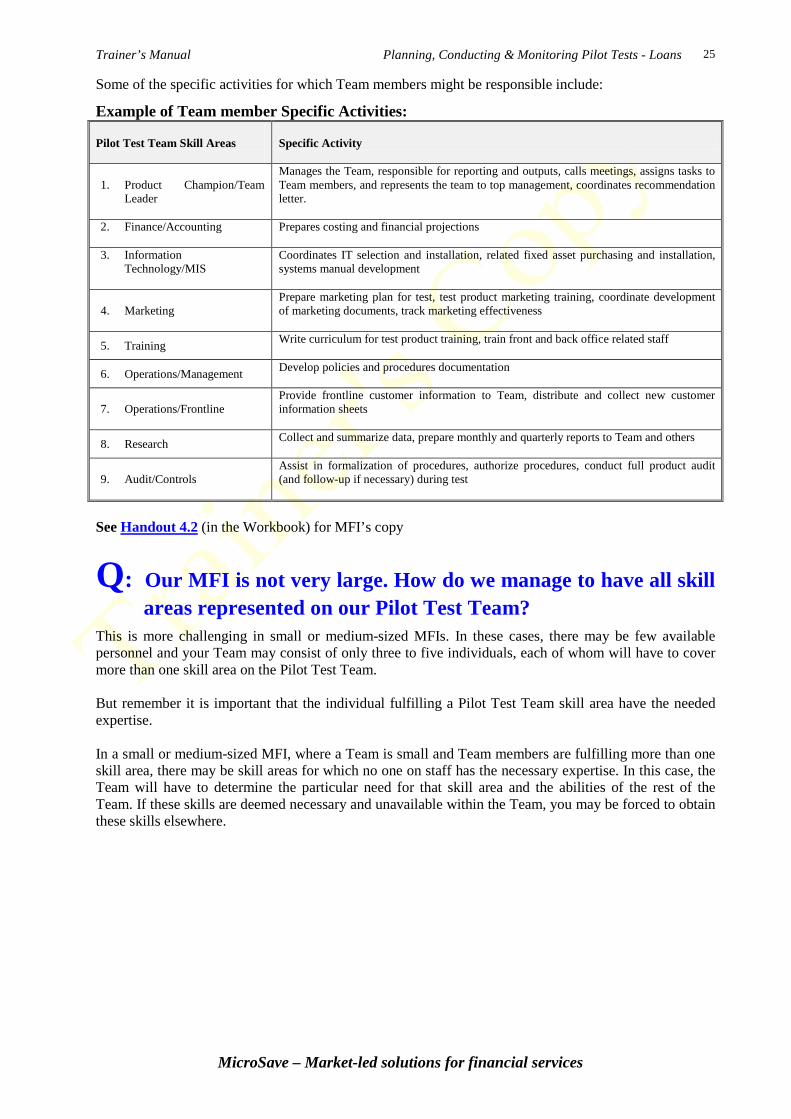

Some of the specific activities for which Team members might be responsible include:

Example of Team member Specific Activities: Pilot Test Team Skill Areas

Specific Activity

1. Product Champion/Team Leader

Manages the Team, responsible for reporting and outputs, calls meetings, assigns tasks to Team members, and represents the team to top management, coordinates recommendation letter.

2. Finance/Accounting

Prepares costing and financial projections

3. Information Technology/MIS

Coordinates IT selection and installation, related fixed asset purchasing and installation, systems manual development

4. Marketing Prepare marketing plan for test, test product marketing training, coordinate development of marketing documents, track marketing effectiveness

5. Training Write curriculum for test product training, train front and back office related staff

6. Operations/Management Develop policies and procedures documentation

7. Operations/Frontline Provide frontline customer information to Team, distribute and collect new customer information sheets

8. Research Collect and summarize data, prepare monthly and quarterly reports to Team and others

9. Audit/Controls Assist in formalization of procedures, authorize procedures, conduct full product audit (and follow-up if necessary) during test

See Handout 4.2 (in the Workbook) for MFI’s copy

Q: Our MFI is not very large. How do we manage to have all skill areas represented on our Pilot Test Team?

This is more challenging in small or medium-sized MFIs. In these cases, there may be few available personnel and your Team may consist of only three to five individuals, each of whom will have to cover more than one skill area on the Pilot Test Team. But remember it is important that the individual fulfilling a Pilot Test Team skill area have the needed expertise. In a small or medium-sized MFI, where a Team is small and Team members are fulfilling more than one skill area, there may be skill areas for which no one on staff has the necessary expertise. In this case, the Team will have to determine the particular need for that skill area and the abilities of the rest of the Team. If these skills are deemed necessary and unavailable within the Team, you may be forced to obtain these skills elsewhere.

Trainer’s Manual Planning, Conducting & Monitoring Pilot Tests - Loans

MicroSave – Market-led solutions for financial services

26

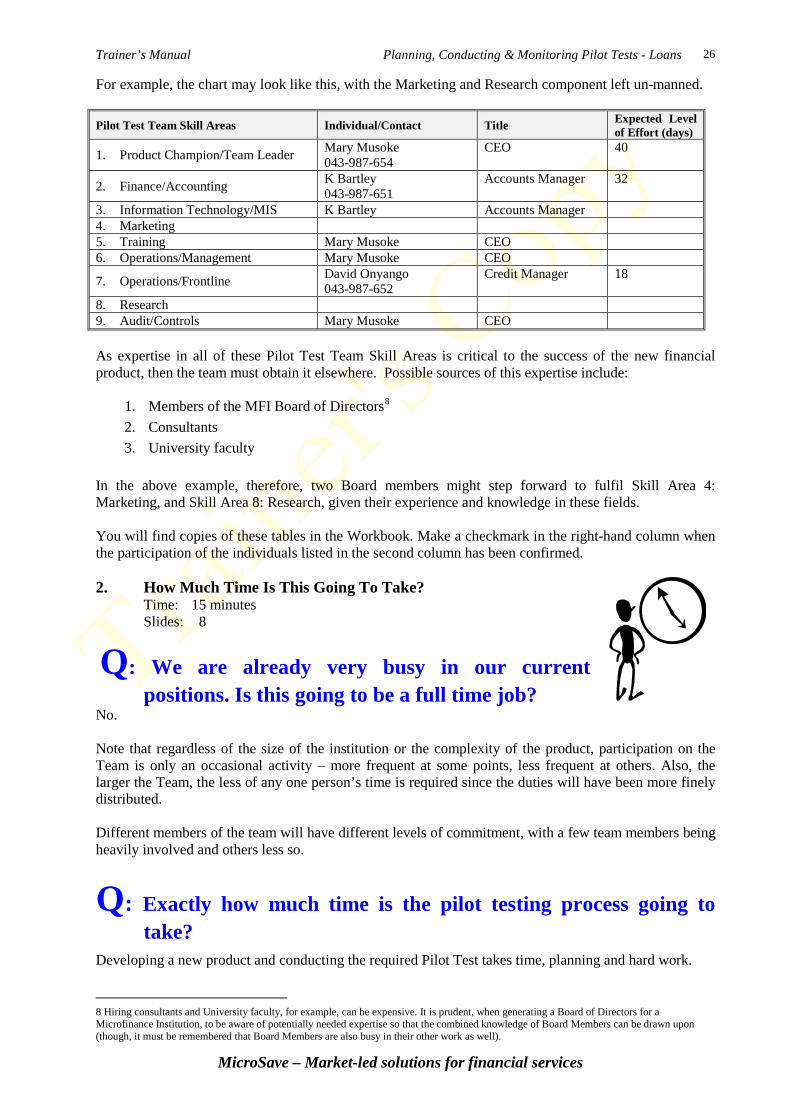

For example, the chart may look like this, with the Marketing and Research component left un-manned. Pilot Test Team Skill Areas Individual/Contact Title Expected Level

of Effort (days)

1. Product Champion/Team Leader Mary Musoke 043-987-654

CEO 40

2. Finance/Accounting K Bartley 043-987-651

Accounts Manager 32

3. Information Technology/MIS K Bartley Accounts Manager 4. Marketing 5. Training Mary Musoke CEO 6. Operations/Management Mary Musoke CEO

7. Operations/Frontline David Onyango 043-987-652

Credit Manager 18

8. Research 9. Audit/Controls Mary Musoke CEO As expertise in all of these Pilot Test Team Skill Areas is critical to the success of the new financial product, then the team must obtain it elsewhere. Possible sources of this expertise include:

1. Members of the MFI Board of Directors8

2. Consultants

3. University faculty In the above example, therefore, two Board members might step forward to fulfil Skill Area 4: Marketing, and Skill Area 8: Research, given their experience and knowledge in these fields. You will find copies of these tables in the Workbook. Make a checkmark in the right-hand column when the participation of the individuals listed in the second column has been confirmed. 2. How Much Time Is This Going To Take?

Time: 15 minutes Slides: 8

Q: We are already very busy in our current positions. Is this going to be a full time job?

No. Note that regardless of the size of the institution or the complexity of the product, participation on the Team is only an occasional activity – more frequent at some points, less frequent at others. Also, the larger the Team, the less of any one person’s time is required since the duties will have been more finely distributed. Different members of the team will have different levels of commitment, with a few team members being heavily involved and others less so.

Q: Exactly how much time is the pilot testing process going to take?

Developing a new product and conducting the required Pilot Test takes time, planning and hard work.

8 Hiring consultants and University faculty, for example, can be expensive. It is prudent, when generating a Board of Directors for a Microfinance Institution, to be aware of potentially needed expertise so that the combined knowledge of Board Members can be drawn upon (though, it must be remembered that Board Members are also busy in their other work as well).

Trainer’s Manual Planning, Conducting & Monitoring Pilot Tests - Loans

MicroSave – Market-led solutions for financial services

27

It may, or may not be a full time job for any one person, BUT it does require concentrated efforts of many individuals within an institution. Any company embarking on the development of a new product needs to dedicate substantial resources to the process. Examples of time requirements: Remember: All this is after the initial investment of 25 to 45 person-days for the market research and analysis, and before the indeterminate amount of time involved in the rollout of the new product. • The Pilot Test Team, including senior management, will need to meet frequently before the pilot test

starts probably weekly, after the pilot test starts the team should meet at least monthly (sometimes more frequently) to review the pilot testing process.

• Senior/middle management members of the Pilot Test Team and their staff will have to take the time to analyse costs and make pricing calculations

Allow: around 5-10 total person-days of the finance area representative and others depending on the state of the cost accounting system.

• Senior/middle management members of the Pilot Test Team and their staff will also have to take the

time needed to plan, conduct, and monitor the Pilot Test.

Allow: around 40-80 person-days over the 6 – 12 months of the test depending on the nature of the product, extent of revision to systems, and other particulars of the product, the MFI, and the market .

Parts of the process may have to be repeated depending on the results of the Test itself. If this is the case, it may be necessary to continue running the Test past the planned termination date. MicroSave’s action research partners spend a lot of time testing. Some have marketing/research departments tasked to do the pilot testing, while others simply task other staff members. Either way expects to spend a significant amount of time – especially the first time you do this! These are broad timing estimates. New products often require substantial adjustments to operating and management information systems, and Pilot Tests sometimes reveal important issues that require intervention. Many MFIs realise that their MIS (and other systems!) needs significant changes in order to accommodate a new product that may have a different interest rate, loan term, and repayment periods than their current product(s). Depending on the software, accommodating the new product could significantly increase time. One partner MFI was in the midst of installing a new MIS, and was thus able to ensure that the new product was incorporated immediately. Others may not be so lucky, and may have to operate “off-line” in order to get the level of detail needed to monitor the Pilot Test. Also, the particulars of each product, market, and MFI make it difficult to project the time it will take to properly prepare a product for the market. New product development is not for the faint hearted.

Q: Are you saying that release time may be needed? Yes.

Trainer’s Manual Planning, Conducting & Monitoring Pilot Tests - Loans

MicroSave – Market-led solutions for financial services

28

It must be emphasised that even though conducting a Pilot Test is an occasional activity for management and staff who are Pilot Test Team members, they will nevertheless need to be released from regular activities to perform Pilot Test related tasks. The Terms of Reference should give the Team leader authority to call for release time of the team members.

Q: It sounds like developing new products and Pilot Testing requires great institutional commitment.

It does; and it most certainly is a great institutional commitment! In fact, a significant level of commitment of resources – people, money, management – is required. Keep in mind that the lack of investment in product testing often results in failed product introductions, large costs and additional risk. Yes, it is expensive, and this is therefore a key reason why many MFIs simply allow others to lead the market with new products and then copy what is successful – this, too, can be problematic since of the three critical factors (product, market, MFI), at least one, and often more, are different from that of the copied product.

3. What Makes A Successful Pilot Test Team? Time: 5 minutes Slides: 3

Q: What makes a successful Pilot Test Team? A successful Team has the following characteristics9

• Management commitment: The Team will not be able to function without a strong commitment from institutional management, due to time and resource needs of the testing process. The Team should have at least one senior manager as a member so that they have someone who can communicate directly to the CEO and other senior managers about the product.

:

• Experienced Team leader: The product testing process requires strong leadership skills relating both to the Team itself and to the environment in which the Team works. Experienced, high quality leadership can manoeuvre a Pilot Test Team through the problems incumbent in this process.

• Proper training: The Team members must be skilled in their areas of representation. If MFI staff members do not have the necessary expertise, the MFI must obtain this expertise elsewhere.

9 Norman Reiley, The Team Based Product Development Guidebook. (Milwaukee, WI: ASQ Press, 1999) p. 9.

For example, this is often why you hear people debate about “replication” of MFI programs. A program or product that works very well in a crowded capital city may require significant changes to work well (or at all) in the more rural areas due to completely different infrastructure, economies, populations, etc. Everyone also knows stories about an MFI with a seemingly similar product to all the others but which dominates the market due to their ability to make their clients feel more satisfied than the others – a well trained, highly motivated (monetarily, and non-monetarily) staff may be the only noticeable difference… and boy, do clients notice!

Trainer’s Manual Planning, Conducting & Monitoring Pilot Tests - Loans

MicroSave – Market-led solutions for financial services

29

• Well-defined processes: The goal of the Test and the work parameters must be clear if the Team is to complete its job effectively.

• Individual and collective self-esteem: The Team and its members must have the confidence to allow for free and open discussion. Individual members or others outside the Team can and will “bully” a Team with little self-confidence. The response to bullying a weak Team often results in decisions being made that are not in the best interests of the product test, and ultimately not in the best interests of the MFI.

Other characteristics that increase the potential success of a Team include10

• 10 or fewer members: If the Team is too large, meeting schedules are complicated and expensive to manage, and it is difficult to make critical decisions.

• Enthusiastic service of members: Individuals should not be coerced to serve on the Team. A successful Pilot Test Team needs members that believe in the product and want to see it succeed, not those who serve simply for “sitting fees” or other special non-performance based remuneration.

• Membership spanning from product concept through rollout: The work of the Team will be disrupted by changes in Team membership. Consistent membership facilitates informed decision-making throughout the Test to product rollout.

• Proximate location of members: Team members will need to interact frequently on an informal basis, sometimes daily. All Team members should work within the same geographical location, to facilitate both formal and informal meetings.

4. Terms of Reference (ToR) for the Pilot Test Team

Time: 55 minutes (45 minutes exercise) Slides: 5

Q: Who drafts the Terms of Reference? Ordinarily, the Team Leader drafts the Terms of Reference for presentation to top management for approval. This approval may come from the Managing Director or Chief Executive in a large MFI, or the Board Chair in a small MFI.

Q: What are the components of Terms of Reference? A Terms of Reference (TOR) is a formal document that outlines the background of the Pilot Test activity, as well as the specific tasks, obligations and expectations of the Pilot Test Team. The Terms of Reference will be structured in several sections to clearly define the role, responsibilities and resources of the Team.

Section I: Background of the Relevant Project, Desired Results, and Activities: Section One summarizes the work that has already been completed on the road to pilot testing and explains the motivations and objectives of the product in both general and specific terms. The General Background notes the history of the product concept and product design – product development stages which should have been completed before venturing on to the pilot test. This section should specify how the general need for the new product was discerned. The Specific Background identifies the desired results for the new product in relation to both market and institutional needs. For example, it states the need for a new savings product to provide for diverse needs/desires of customers and lists those needs/desires in detail, or it might specify that

10 Preston G. Smith and Donald Reinertsen. Developing Products in Half the Time. (New York: Van Nostrand Reinhold, 1991) P.111.

Trainer’s Manual Planning, Conducting & Monitoring Pilot Tests - Loans

MicroSave – Market-led solutions for financial services

30