Important disclosures appear on the last page of this report. The Henry Fund Henry B. Tippie School of Management Hannah Geyer [[email protected]] Pay TV (Cable, Satellite, Teleco) February 7, 2018 Consumer Discretionary/Communication Services - Media Industry Rating Neutral Weight Investment Thesis Key Industry Statistics We recommend a neutral weight for the pay TV (cable, satellite, and teleco) industry over the next year. The growing availability of online content, substitutes like Video on Demand (VoD), and an expanding market for connected mobile devices will continue to threaten traditional cable and satellite TV. As cable subscribers decrease year over year, companies in this industry are moving into new markets, adding new sources of revenue and shifting the shape of the industry overall. However, this movement is viable only for a relatively small number of Pay TV companies, as recent acquisitions have consolidated industry resources and market share. Drivers of Thesis • Industry-wide Cord Cutting: Cord cutting continues as more consumers opt out of traditional pay TV packages in favor of cheaper online alternatives • Increasing Programming Fees: Fees are projected to increase over the year, eroding company profits • Rivals and Substitutes: Distribution platforms for viewing and purchasing content over the internet have continued to grow, pressuring pay TV companies to aggressively compete via costly additional services and acquisitions • Regulatory Uncertainties: Policy uncertainties related to the FCC's broadband regulations (Title II) and the possibility of a nationwide 5G network could help or hurt the industry’s profits Risks to Thesis • Broadband Subscriber Growth: As the pay TV video subscribers decrease, select companies’ broadband subscribers have increased, a trend we expect to continue • Mergers & Acquisition Activity: Significant consolidation over the past few years has led to more powerful central players, decreasing rivalry within the industry Market Cap AT&T (DirecTV) Comcast Corporation (in $billions) 233.71 192.14 Charter (TWC, Bright) DISH Network Altice USA 92.28 21.82 15.18 Video ARPU AT&T (DirecTV) Comcast Corporation Charter (TWC, Bright) $118 $149 $81 DISH Network Altice USA $86 $141 Industry Statistics Price/Earnings 9.1 Price/Book Ratio 2.6 Market Cap/Total Rev Current Ratio Net Income Margin Gross Margin EBITA Margin Total Debt/Equity 2.3 .7 25.1% 65% 21.1% 203.9% 12 Month Performance Industry Description The US pay TV industry includes companies in three major segments: cable, satellite, and teleco. This industry is dominated primarily by a small number of Multiple-System Operators (MSO), companies that own and operate two or more cable TV systems. These companies bundle services including video, broadband internet, and voice, available to subscribers for monthly fees. Distribution of these services rely on networks of coaxial cables (cable), fiber-optic cables (teleco), and satellite (satellite). 8.4 13.6 5.2 21.7 24.7 5.8 9.1 27.5 4.1 0 5 10 15 20 25 30 P/E ROE ROA CMCSA Industry Sector -10% 0% 10% 20% 30% F M A M J J A S O N D J CHTR CMCSA S&P 500 Source: Yahoo Finance Source: NetAdvantage

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Important disclosures appear on the last page of this report.

The Henry Fund

Henry B. Tippie School of Management Hannah Geyer [[email protected]]

Pay TV (Cable, Satellite, Teleco) February 7, 2018

Consumer Discretionary/Communication Services - Media Industry Rating Neutral Weight

Investment Thesis Key Industry Statistics We recommend a neutral weight for the pay TV (cable, satellite, and teleco) industry over the next year. The growing availability of online content, substitutes like Video on Demand (VoD), and an expanding market for connected mobile devices will continue to threaten traditional cable and satellite TV. As cable subscribers decrease year over year, companies in this industry are moving into new markets, adding new sources of revenue and shifting the shape of the industry overall. However, this movement is viable only for a relatively small number of Pay TV companies, as recent acquisitions have consolidated industry resources and market share. Drivers of Thesis

• Industry-wide Cord Cutting: Cord cutting continues as more consumers opt out of traditional pay TV packages in favor of cheaper online alternatives

• Increasing Programming Fees: Fees are projected to increase over the year, eroding company profits

• Rivals and Substitutes: Distribution platforms for viewing and purchasing content over the internet have continued to grow, pressuring pay TV companies to aggressively compete via costly additional services and acquisitions

• Regulatory Uncertainties: Policy uncertainties related to the FCC's broadband regulations (Title II) and the possibility of a nationwide 5G network could help or hurt the industry’s profits

Risks to Thesis

• Broadband Subscriber Growth: As the pay TV video subscribers decrease, select companies’ broadband subscribers have increased, a trend we expect to continue

• Mergers & Acquisition Activity: Significant consolidation over the past few years has led to more powerful central players, decreasing rivalry within the industry

Market Cap AT&T (DirecTV) Comcast Corporation

(in $billions) 233.71 192.14

Charter (TWC, Bright) DISH Network Altice USA

92.28 21.82 15.18

Video ARPU AT&T (DirecTV) Comcast Corporation Charter (TWC, Bright)

$118 $149

$81 DISH Network Altice USA

$86 $141

Industry Statistics Price/Earnings 9.1 Price/Book Ratio 2.6 Market Cap/Total Rev Current Ratio Net Income Margin Gross Margin EBITA Margin Total Debt/Equity

2.3 .7

25.1% 65%

21.1% 203.9%

12 Month Performance Industry Description

The US pay TV industry includes companies in three major segments: cable, satellite, and teleco. This industry is dominated primarily by a small number of Multiple-System Operators (MSO), companies that own and operate two or more cable TV systems. These companies bundle services including video, broadband internet, and voice, available to subscribers for monthly fees. Distribution of these services rely on networks of coaxial cables (cable), fiber-optic cables (teleco), and satellite (satellite).

8.4

13.6

5.2

21.724.7

5.8

9.1

27.5

4.10

5

10

15

20

25

30

P/E ROE ROA

CMCSA Industry Sector

-10%

0%

10%

20%

30%

F M A M J J A S O N D J

CHTR CMCSA S&P 500

Source: Yahoo Finance

Source: NetAdvantage

Page 2

EXECUTIVE SUMMARY

Our neutral weight recommendation for the pay TV industry is driven by regulatory uncertainty, cord-cutting from subscribers without replacement, and an increasing number of competitors and substitutes.

For many years, the pay TV industry generated impressive growth, leveraging its technology, expansive reach, and popularity as the gatekeeper to cable television. With a high cost of entry and strong revenues, this was a stable environment in which to operate.

However, in recent years, Average Revenue per User (ARPU) has been steadily declining as companies face increased competition from products like Video on Demand (VoD) and over-the-top (OTT) video. These threats add value by providing original content, lower prices, and greater viewing flexibility than traditional cable would provide.

In order to compete with these new players, several pay TV companies are expanding services and shuffling current bundles. Despite these competitive adjustments, our outlook remains neutral, considering the uncertainty policy changes and acquisition rulings may have on the industry.

INDUSTRY DESCRIPTION

Cable, Satellite, and Teleco

The pay TV industry is housed within the media sub-industry of the consumer discretionary sector. Pay TV includes companies in three major areas: cable, satellite, and teleco. Primary cable companies include Comcast, (XFINITY) and Charter (Spectrum); major satellite operators include DirectTV and DISH; leading teleco companies are Verizon FiOS and AT&T U-verse. Total subscriber count for these companies is indicated below.

Source: Statista

Comcast leads the industry in terms of video subscriber base with over 22.5M subscribers. Comcast is followed by DirecTV (20.9M), Charter (17.1M), DISH (13.3M), Verizon FiOS (4.7M), AT&TU-verse (3.9M), Altice (3.5M), and Frontier (1M).13

Cable, satellite, and teleco system operators provide content to customers through different delivery platforms. Cable and teleco operators use a network of coaxial or fiber-optic cable while satellite relies on transponders transmit signals back to earth to subscribers.

These three types of pay TV companies have unique advantages and challenges, but directly impact one another, overlapping as companies merge within the industry (in the case of AT&T and DirecTV), and as customer preferences shift, impacting subscribership.

Similarly, large and small pay TV companies experience very different trends within the industry. Larger companies have been able to scale up quickly through acquisitions, thereby increasing available services to include broadband and remaining competitive in a changing industry. In contrast, smaller cable companies have faded. The chart below indicates the acquisitions made by Comcast, Time Warner Cable, Charter, Cox, and Cablevision from 2009 to 2015.14

Source: FierceCable

Page 3

Services

Historically, pay TV companies focused primarily on providing residential cable TV. However, in order to remain competitive as consumers have shifted media preferences toward broadband internet and VoD options, larger companies have increased these services to include wireless, voice, and cloud services, among others.

Both Comcast and Charter continue to invest in increasing their broadband capabilities and services in order to stay competitive in a rapidly changing environment. By providing additional services available only to established customers, these companies incentivize current subscribers to shift between bundles within the company instead of dropping the company’s services altogether.

Increasingly, companies are now focused on cloud-based applications and additional product enhancements. As a result, these players will likely continue to grow, further distancing themselves from smaller pay TV companies like Frontier and Altice USA.

High barriers to entry have traditionally buffered the industry from the threat of new entrants as companies must secure costly franchise rights from municipalities in order to operate. In addition, the cost of building out infrastructure is high, as companies develop satellite or costly fiber optic networks to reach their customers. Many of the companies that operate in these spaces are already solidly established and have substantial networks in place.

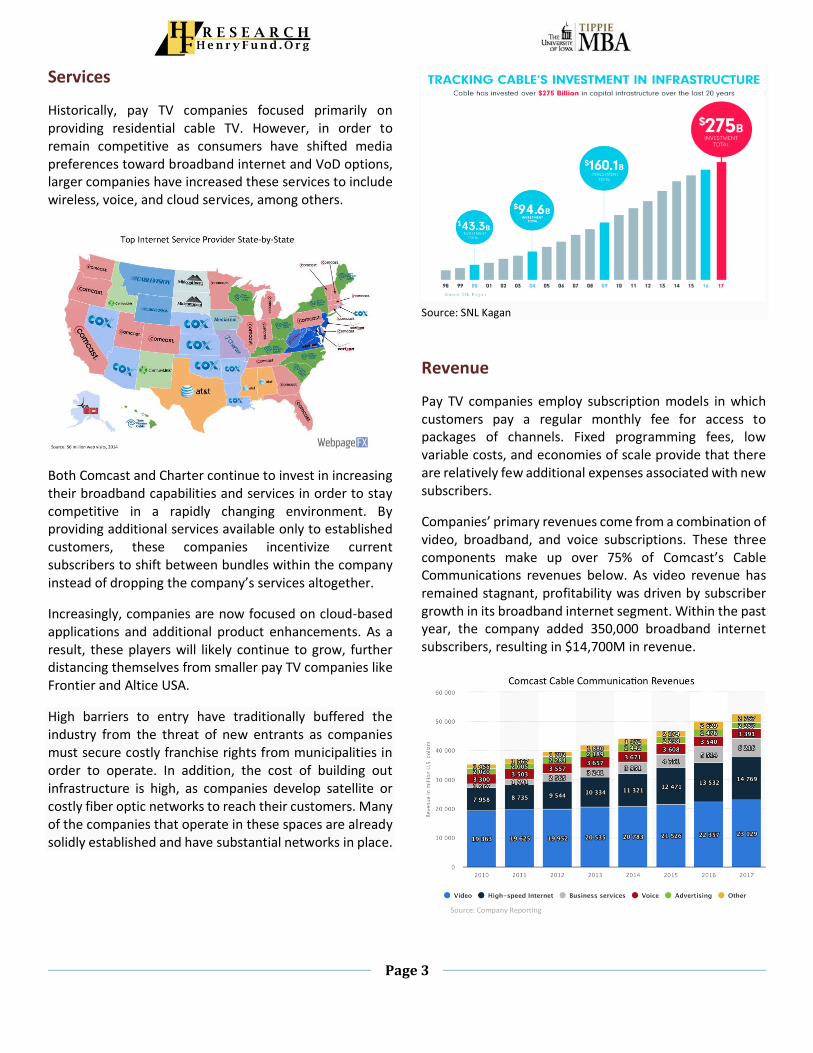

Source: SNL Kagan

Revenue

Pay TV companies employ subscription models in which customers pay a regular monthly fee for access to packages of channels. Fixed programming fees, low variable costs, and economies of scale provide that there are relatively few additional expenses associated with new subscribers.

Companies’ primary revenues come from a combination of video, broadband, and voice subscriptions. These three components make up over 75% of Comcast’s Cable Communications revenues below. As video revenue has remained stagnant, profitability was driven by subscriber growth in its broadband internet segment. Within the past year, the company added 350,000 broadband internet subscribers, resulting in $14,700M in revenue.

Source: Company Reporting

Page 4

This increase, however, is offset by increasingly high programming fees. We expect programming costs to continue to increase due to a variety of factors including annual increases, renegotiating contract renewals, and the addition of supplemental programming and services.

Cyclical Market

When analyzing the cable and satellite industry, we look at trends on a year over year basis, recognizing that this market is highly cyclical. Historically, the industry performs much higher in the first and fourth quarters of the year, due in part to seasonal programming and viewership preferences. For this reason, we compare data in correlating quarters, year over year, for the most consistent and holistic picture.

RECENT DEVELOPMENTS

The pay TV industry faces new developments in technology and policy decisions that have the potential to impact its growth in the near future. It will be crucial for players in this industry to react quickly in this changing market by developing competitive services.

Net Neutrality/Title I

In December 2017, the Federal Communications Commission (FCC) voted to reverse broadband regulations from Title I to Title II Classification, a decision that directly benefits broadband companies. This decision would remove common carrier rules, giving Internet Service Providers more leverage to control pricing and service coverage. The repeal goes into effect on April 23, after a review from the Office of Management and Budget.

However, the decision also faces a series of lawsuits from state attorneys and advocacy groups. As this decision is

very controversial among customers, it will likely have negative implications regarding consumer sentiment.

Broadband companies have stated that they do not plan to block, slow down, or prioritize web traffic as a result of the FCC's repeal, maintaining that this would damage subscriber growth.14 However, this ruling would also enable companies to serve as gatekeepers regarding how subscribers use the Internet; for example, companies could prioritize their own video-streaming services over their competitors'.

Although the Senate has enough votes to restore net neutrality, it does not currently have a two-thirds majority required to override the president’s veto.15 For this reason, we believe that the repeal will likely take effect and have a long-term impact in Comcast’s favor.

5G Spectrum Proceedings

In 2018, the FCC announced its focus on “broadband infrastructure deployment,” an initiative to transition from 4G LTE to 5G, creating a faster broadband network.14 As part of this initiative, the Trump administration announced that it is considering a government-funded 5G public utility, improving national security.

Although this buildout is unlikely due to its large scale and required capital, it would have negative implications for cable operators, since the new 5G network would become a competitor for broadband services. It remains uncertain what rules, if any, Congress and the FCC will ultimately adopt. We do not see this as a likely or immediate threat to the industry in the next two years. In the next five years, however, this decision is a more likely threat as a growing number of individual US cities begin providing Municipal Wireless Networks.

INDUSTRY TRENDS

Consumers are increasingly turning to online sources for viewing and purchasing content, which has, and likely will continue, to reduce the number of pay TV subscribers. In order to survive, companies must make up for these losses through broadband subscribers and other services.

Industry-wide Cord Cutting

Year over year, the number of industry-wide video subscribers continues to decrease at an alarming rate. The

Page 5

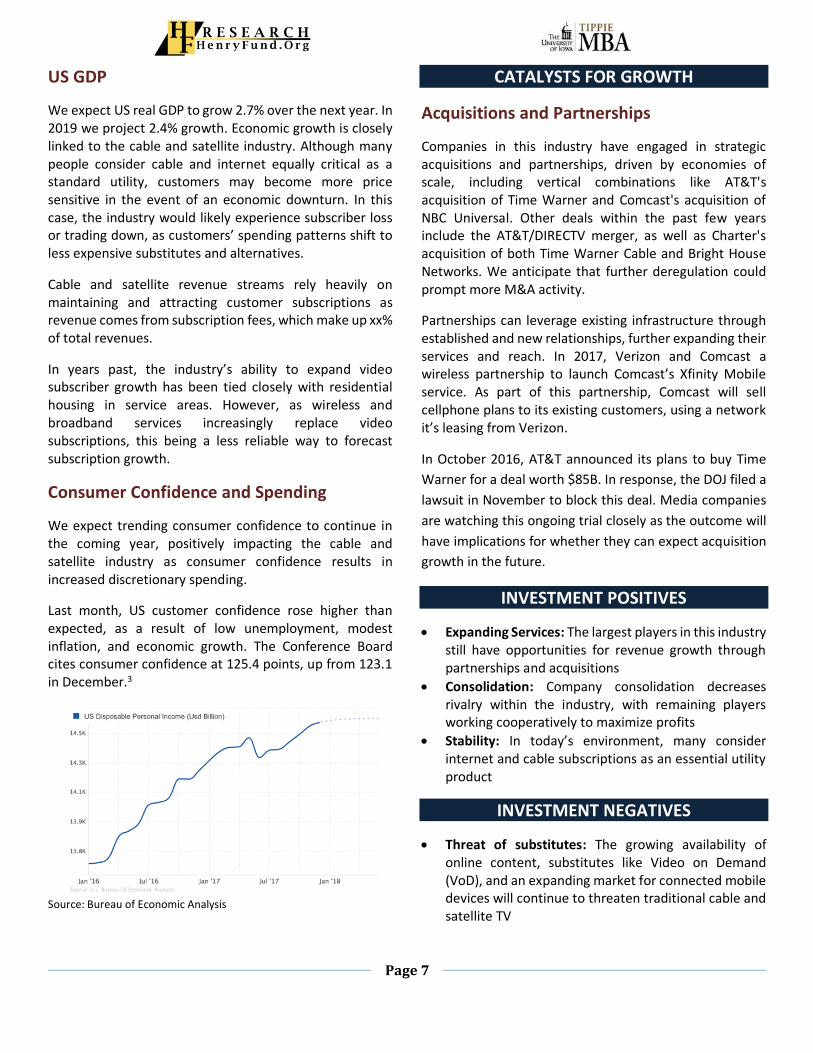

graph below includes the changing number of subscribers between twelve primary companies in the industry.

As a group, these companies lost almost 2.5 million video subscribers in the past year; they lost 1.5 million in the previous year and .5 million a year before that. As an industry, this means that the rate of cord cutting in the US is about 1 million subscribers lost per year. Although the popularity of live content in sports and events has sustained some demand for pay TV, customers are gravitating toward alternative avenues for content as companies like ESPN begin to provide more flexible online streaming options for watching live sports.

Cord Cutting by Segment

Trends emerge when we examine cord cutting by company type. From 2012-2013, teleco operators AT&T and Verizon experienced video subscriber growth as they established fiber-optic networks and positioned themselves competitively in the industry. However, building out fiber optic cable infrastructure is extremely capital intensive. After investing heavily in Texas and California, Verizon slowed its FiOS expansion, resulting in subscriber loss.

Teleco subscribers further dropped as AT&T’s 2015 acquisition of DirecTV shifted company focus from teleco toward satellite. As a result, newly-acquired DirecTV experienced video subscriber growth, boosted by AT&T’s marketing resources and energy. This growth, however, has not proven sustainable as satellite video subscribership has since dropped significantly.

Cable companies experienced subscriber growth between 2014-2016, benefiting from the teleco slump. Looked at individually, this growth in cable subscribership could look like cord cutting is slowing down; however, in the context of the entire industry, we see subscribers are shifting from one area to another, not generating new growth for the industry as a whole.

This shift is not necessarily a credit to cable company success, but in fact a response to Verizon backing away from fiber optic expansion and AT&T prioritizing growth opportunities with DirecTV.

The largest pay TV companies provide broadband internet in addition to cable; several now have more subscribers for broadband than for video, a sign that the industry definition is shifting as well.

Changes in Consumer Behavior

Mobile devices and tablets continue to gain popularity, especially in younger markets. Pay TV companies must respond in order to meet these customers. The following chart indicates the percentage of Americans who rank these four devices among the most important three: Pay-tv, video streaming, music streaming, and newspaper. For teens and young adults between the ages of 14-25, video streaming was the most likely mode with 72%.

-2500

-2000

-1500

-1000

-500

0

500

2013 2014 2015 2016 2017

YoY US Pay TV Industry Video Subscriber Growth

Subscriber Growth in ThousandsSource: Company Reporting, Jan Dawson

-2000

-1500

-1000

-500

0

500

1000

1500

2000

2013 2014 2015 2016

Video Net Subscriber Adds

Teleco Cable Satellite

Source: Company Reporting, Jackdaw Subscriber Growth in Thousands, YoY

Page 6

MARKETS AND COMPETITION

Consolidated Ownership

After a series of mergers and acquisitions within the past several years, ownership is concentrated among a small number of companies in the pay TV industry. Four companies now account for 83% of the industry’s subscriber base, which includes 78 million subscriptions. These companies are AT&T Inc. (including DIRECTV and AT&T U-verse), Comcast, Charter Communications Inc. (including Time Warner Cable Inc. and Bright House Networks LLC), and DISH.

Verizon and Altice each have about 5 million subscribers. Below them, company size gets much smaller, including Frontier with 1.6 million subscribers and Mediacom under 1 million. As of November 2016, 159 national networks were affiliated with the top six cable operators, most of which

are vertically integrated.3 In addition, six national networks were affiliated with satellite TV provider DIRECTV, owned by AT&T Inc.

The market is dominated by large companies, a trend we believe will continue as Altice begins to explore a merger with Charter.

As the four largest companies continue to grow, the rest of the market becomes less relevant and are impacted even more negatively by cord-cutting trends.

ARPU Comparison

ECONOMIC OUTLOOK

The pay TV industry is in the mature phase of its life cycle. Although consumer confidence and disposable income are expected to increase, suggesting a rise in entertainment spending, we expect online services to continue taking market share from cable operators.

AT&T

Comcast Altice USADish

Network Charter

$0

$50

$100

$150

$200

AT&T Comcast Altice USA DishNetwork

Charter

Source: Company Reporting, Q1 2017

Average Revenue Per User

Page 7

US GDP

We expect US real GDP to grow 2.7% over the next year. In 2019 we project 2.4% growth. Economic growth is closely linked to the cable and satellite industry. Although many people consider cable and internet equally critical as a standard utility, customers may become more price sensitive in the event of an economic downturn. In this case, the industry would likely experience subscriber loss or trading down, as customers’ spending patterns shift to less expensive substitutes and alternatives.

Cable and satellite revenue streams rely heavily on maintaining and attracting customer subscriptions as revenue comes from subscription fees, which make up xx% of total revenues.

In years past, the industry’s ability to expand video subscriber growth has been tied closely with residential housing in service areas. However, as wireless and broadband services increasingly replace video subscriptions, this being a less reliable way to forecast subscription growth.

Consumer Confidence and Spending

We expect trending consumer confidence to continue in the coming year, positively impacting the cable and satellite industry as consumer confidence results in increased discretionary spending.

Last month, US customer confidence rose higher than expected, as a result of low unemployment, modest inflation, and economic growth. The Conference Board cites consumer confidence at 125.4 points, up from 123.1 in December.3

Source: Bureau of Economic Analysis

CATALYSTS FOR GROWTH

Acquisitions and Partnerships

Companies in this industry have engaged in strategic acquisitions and partnerships, driven by economies of scale, including vertical combinations like AT&T's acquisition of Time Warner and Comcast's acquisition of NBC Universal. Other deals within the past few years include the AT&T/DIRECTV merger, as well as Charter's acquisition of both Time Warner Cable and Bright House Networks. We anticipate that further deregulation could prompt more M&A activity.

Partnerships can leverage existing infrastructure through established and new relationships, further expanding their services and reach. In 2017, Verizon and Comcast a wireless partnership to launch Comcast’s Xfinity Mobile service. As part of this partnership, Comcast will sell cellphone plans to its existing customers, using a network it’s leasing from Verizon.

In October 2016, AT&T announced its plans to buy Time

Warner for a deal worth $85B. In response, the DOJ filed a

lawsuit in November to block this deal. Media companies

are watching this ongoing trial closely as the outcome will

have implications for whether they can expect acquisition

growth in the future.

INVESTMENT POSITIVES

• Expanding Services: The largest players in this industry still have opportunities for revenue growth through partnerships and acquisitions

• Consolidation: Company consolidation decreases rivalry within the industry, with remaining players working cooperatively to maximize profits

• Stability: In today’s environment, many consider internet and cable subscriptions as an essential utility product

INVESTMENT NEGATIVES

• Threat of substitutes: The growing availability of online content, substitutes like Video on Demand (VoD), and an expanding market for connected mobile devices will continue to threaten traditional cable and satellite TV

Page 8

• Policy uncertainty: Pending acquisition rulings, governance regarding net neutrality, an a government 5G rollout will significantly impact how companies operate in this industry

• Industry-wide cord cutting: Subscriber loss is intensifying—especially for smaller pay TV companies

SUMMARY

Our neutral weight recommendation for the pay TV industry is driven by regulatory uncertainty, cord-cutting from subscribers without replacement, and an increasing number of competitors and substitutes.

As cable subscribers decrease year over year, companies in this industry are moving into new markets, adding or replacing sources of revenue and shifting the shape of the industry overall. However, this movement is viable only for a relatively small number of Pay TV companies, as recent acquisitions have consolidated industry resources and market share.

The firms who are best positioned to compete in this environment are large companies with sufficient capital to take on strategic acquisitions and partnerships. In addition, companies that produce their own original content have a better long-term advantage by saving costs and maintaining an independent structure, less dependent on other buyers.

Many pay TV companies are expanding services and shuffling current bundles to remain competitive and retain subscribers. Despite these adjustments, however, our outlook remains neutral, considering the uncertainty policy changes and pending acquisition rulings may have on the industry.

REFERENCES

Sources

1. FCC - https://www.fcc.gov/document/accelerating-wireline-broadband-infrastructure-deployment

2. Blooomberg - https://www.bloomberg.com/ news/features/2017-02-28/youtube-bets-it-can-convince-youngs-to-pay-for-tv

3. The Conference Board - https://www.conference-board.org/data/consumerconfidence.cfm (January 30, 2018)

4. Comcast 10-k 5. Charter Communications 10-k 6. AT&T Inc 10-k 7. Press Release - http://www.leichtmanresearch.com

/press/111517release.html 8. Factset 9. Bloomberg - https://www.bloomberg.com/news

/articles/2017-06-15/cable-tv-networks-see-a-ray-of-hope-amid-the-cord-cutting-clouds

10. CMCSA - https://www.cmcsa.com/financials/annual-reports

11. Yahoo Finance - https://finance.yahoo.com/ quote/%5ESP1500-25401025?p=%5ESP1500-25401025

12. “18th Annual Report on Video Competition” (released in January 2017) by the Federal Communications Commission (FCC).

13. Statista – The State of US Pay TV Landscape https://www.statista.com/chart/6994/pay-tv-providers-in-the-us/

14. Fierce Cable – 10 years of Consolidation - https://www.fiercecable.com/special-report/10-years-consolidation-cable-rise-comcast-twc-charter-cox-and-cablevision

IMPORTANT DISCLAIMER Henry Fund reports are created by students enrolled in the Applied Securities Management program at the University of Iowa’s Tippie College of Business. These reports provide potential employers and other interested parties an example of the analytical skills, investment knowledge, and communication abilities of our students. Henry Fund analysts are not registered investment advisors, brokers or officially licensed financial professionals. The investment opinion contained in this report does not represent an offer or solicitation to buy or sell any of the aforementioned securities. Unless otherwise noted, facts and figures included in this report are from publicly available sources. This report is not a complete compilation of data, and its accuracy is not guaranteed. From time to time, the University of Iowa, its faculty, staff, students, or the Henry Fund may hold an investment position in the companies mentioned in this report.

https://www.bloomberg.com/news/features/2017-02-28/youtube-bets-it-can-convince-youngs-to-pay-for-tv

https://www.bloomberg.com/news/features/2017-02-28/youtube-bets-it-can-convince-youngs-to-pay-for-tv

Related Documents