Chapter 1. Growth and Investment Pakistan Economic Survey Pakistan Economic Survey 2002-03 2002-03

Pakistan Economic Survey FY03

Oct 26, 2014

A review of Pakistan's economy in year 2002-03

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Chapter 1. Growth and Investment

Pakistan Economic SurveyPakistan Economic Survey2002-032002-03

Chapter 1. Growth and Investment

1. Growth and Investment1. Growth and InvestmentThe outgoing fiscal year 2002-03 has

witnessed a sharp recovery in economic growth accompanied by equally impressive performance of agriculture and large-scale manufacturing. Other significant achievements have been the impressive growth in per capita income, both in rupee and dollar terms, and national savings reaching new heights — exceeding total investment and suggesting a large surplus in the current account balance. When viewed at the backdrop of inhospitable external environment and uncertain geo-political situation Pakistan's growth performance has been impressive in 2002-03. This year has witnessed major corporate scandals and bankruptcies in the United States, resulting in bursting of the equity market bubble; rising uncertainties in the run up to war in Iraq, causing oil prices to rise sharply, and recent outbreak of Severe Acute Respiratory Syndrome (SARS) virus badly affecting business environment in Asia. There developments on international economic scene created uncertainties. The world economic outlook remained subdued and global trade remained sluggish during the outgoing fiscal year.

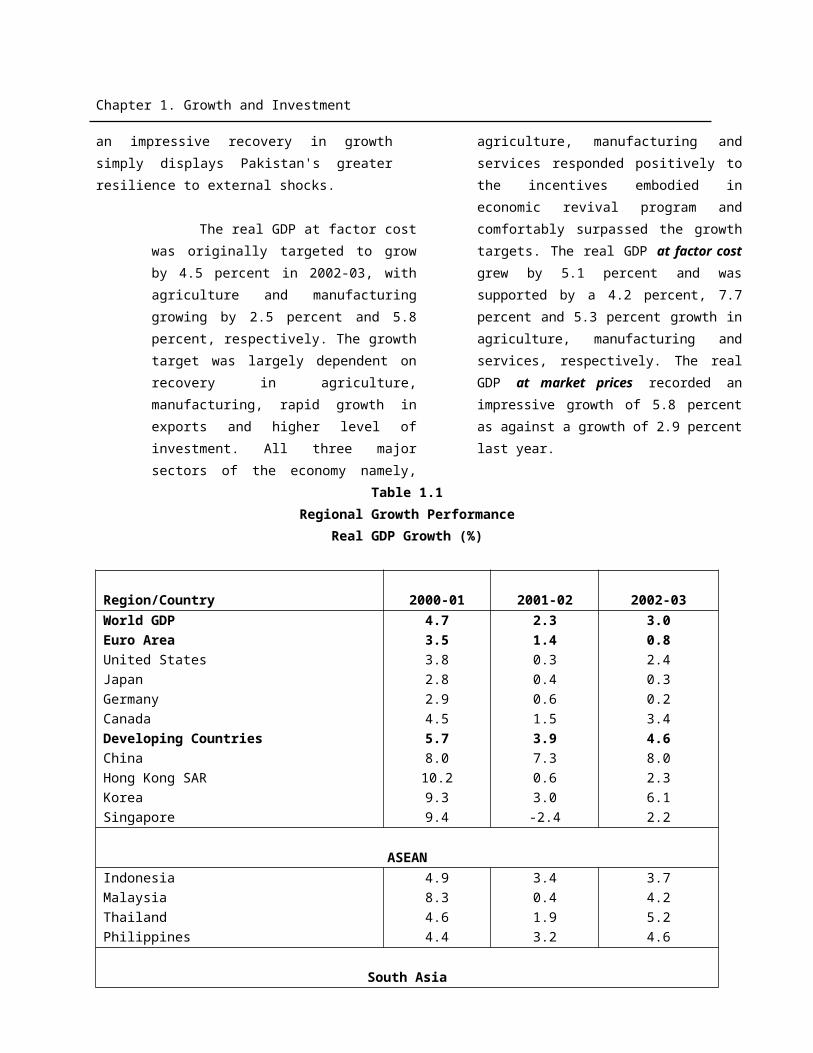

Table 1.1 documents the growth performance of selected regional economies in 2000-03. The performance of the major growth poles of the world economy (US, Japan and Euro Area) are likely to remain subdued with Japan and Euro Area economies growing by less than 1.0 percent in 2002-03. The United States is expected to perform better as compared with last year. Developing countries as a whole is expected to grow by 4.6 percent. China and Korea in Asian region are

expected to be the star performers with growth exceeding 6.0 percent. With the exception of Thailand, the other ASEAN countries are projected to grow by less than 5.0 percent. Barring Iran, the other countries in the Middle East are almost stagnating. In Africa, no country could achieve 5.0 percent growth in 2002-03. In South Asia, Pakistan is the only country which achieved more than 5.0 percent growth in 2002-03. Two points need to be noted as far as Pakistan's growth performance is concerned. Firstly, when compared with major economies of different parts of the world, Pakistan’s growth performance has been impressive. Secondly, in a subdued global economic environment, an impressive recovery in growth simply displays Pakistan's greater resilience to external shocks.

The real GDP at factor cost was originally targeted to grow by 4.5 percent in 2002-03, with agriculture and manufacturing growing by 2.5 percent and 5.8 percent, respectively. The growth target was largely dependent on recovery in agriculture, manufacturing, rapid growth in exports and higher level of investment. All three major sectors of the economy namely, agriculture, manufacturing and services responded positively to the incentives embodied in economic revival program and comfortably surpassed the growth targets. The real GDP at factor cost grew by 5.1 percent and was supported by a 4.2 percent, 7.7 percent and 5.3 percent growth in agriculture, manufacturing and services, respectively. The real GDP at market

Chapter 1. Growth and Investment

prices recorded an impressive growth of 5.8 percent as against a growth of 2.9 percent last year.

Table 1.1Regional Growth Performance

Real GDP Growth (%)

Region/Country 2000-01 2001-02 2002-03World GDP 4.7 2.3 3.0Euro Area 3.5 1.4 0.8United States 3.8 0.3 2.4Japan 2.8 0.4 0.3Germany 2.9 0.6 0.2Canada 4.5 1.5 3.4Developing Countries 5.7 3.9 4.6China 8.0 7.3 8.0Hong Kong SAR 10.2 0.6 2.3Korea 9.3 3.0 6.1Singapore 9.4 -2.4 2.2

ASEANIndonesia 4.9 3.4 3.7Malaysia 8.3 0.4 4.2Thailand 4.6 1.9 5.2Philippines 4.4 3.2 4.6

South AsiaIndia 5.4 4.2 4.4Bangladesh 5.9 5.3 4.4Sri Lanka 6.0 -1.4 3.7Pakistan 2.2 3.4 5.1

Middle EastSaudi Arabia 4.9 1.2 2.1Kuwait 1.4 -1.1 -0.9Iran 5.2 5.7 6.0Egypt 5.1 3.5 2.0

AfricaAlgeria 2.4 2.1 3.1Morocco 1.0 6.5 4.5Tunisia 4.7 5.2 1.9Nigeria 3.9 2.8 0.5Kenya -0.1 1.2 1.2South Africa 3.5 2.8 3.0

Source: World Economic Outlook (IMF), April 2003.

Chapter 1. Growth and Investment

1980's 1990-I 1990-II 2000-02 2002-030

1

2

3

4

5

6

7

8

9

10

6.1

4.9

5.7

4.2

Fig-1: Real GDP/GNP Growth

GDP Growth GNP Growth

% G

row

th

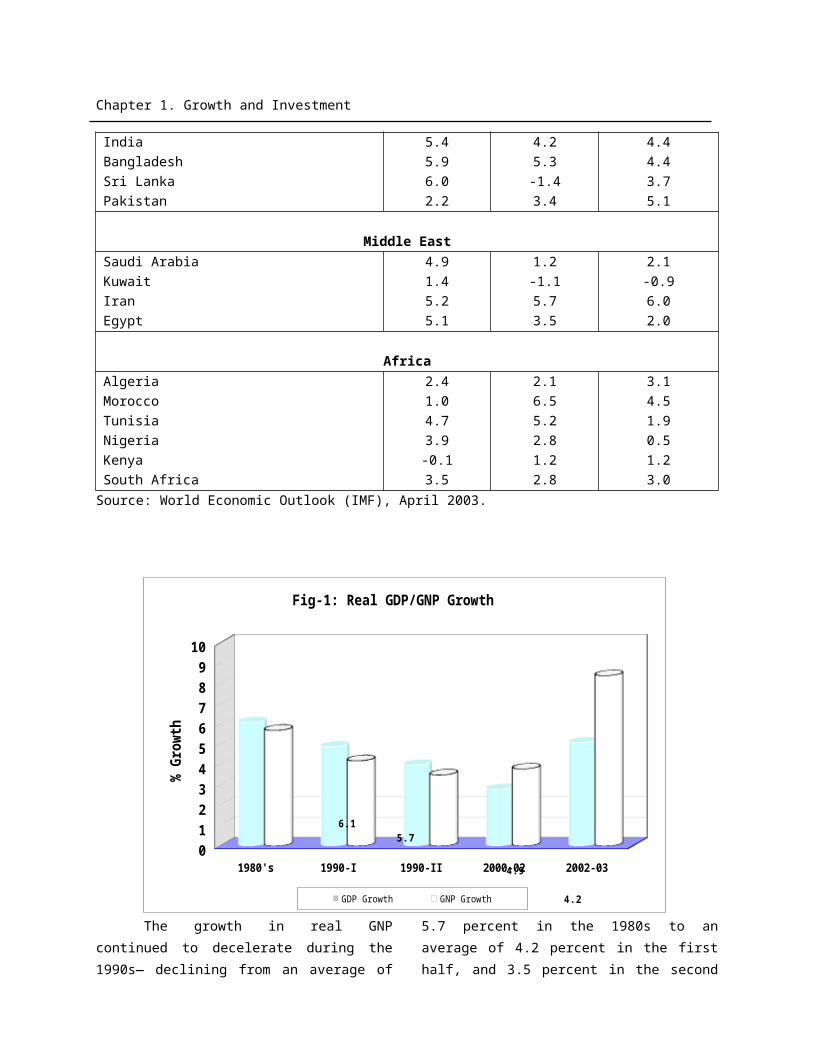

The growth in real GNP continued to decelerate during the 1990s— declining from an average of 5.7 percent in the 1980s to an average of 4.2 percent in the first half, and 3.5 percent in the second half of the 1990s. During the first three years (2000-03) of the new decade, the real GNP grew at an average of 5.4 percent. Most importantly, the real GNP registered a handsome growth of 8.4 percent in 2002-03 as against 5.3 percent last year, mainly on account of 472.2 percent increase in net factor income from abroad, which, in turn, is the result of a sharp increase in the inflow of workers remittances and foreign direct investment in the country [See Fig-1.1]. With population growing by 2.1 percent, the real per capita GNP at market price increased by 6.6 percent in 2002-03 as against an increase of 2.1 percent last year.

Notwithstanding the strong recovery

in growth to 5.1 percent in 2002-03 from 3.4 percent last year, the fact remains that Pakistan’s economic growth decelerated in the 1990s for a variety of reasons, including worsening of macroeconomic environment, serious lapses in implementation of

stabilization policies and structural reforms, adverse law and order situation, inconsistent policies, and poor governance. As against an average growth rate of 6.1 percent in the 1980s, the real GDP growth slowed to an average of 4.9 percent in the first half, 4.0 percent in the second half of the 1990s. Economic growth remained depressed for first two years (2000-02) of the new decade averaging 2.8 percent. Unprecedented drought and the events of 9/11 have been responsible for keeping the growth depressed during 2000-02. Fiscal year 2002-03 exhibits a turnaround in growth [See Fig-1]. The real challenge would now be to sustain this growth momentum.

The manufacturing sector grew by an average annual rate of 8.2 percent in the 1980s, slowed to an average of 4.7 percent in the first half and further to 2.4 percent in the second half of the 1990s. However, it performed well during last three years by growing at annual average rate of 7.0 percent per annum. In fact, over the last decade, the large-scale manufacturing lost almost three-fourth of its growth

Chapter 1. Growth and Investment

momentum. The services sector also slowed from an average of 6.6 percent in the 1980s to 5.1 percent in the first half and further to 4.0 percent in the second half of the 1990s, losing one-third of its growth momentum

during the 1990s. It started regaining its growth momentum during last three years by growing at an average rate of 4.7 percent. [See Table 1.1].

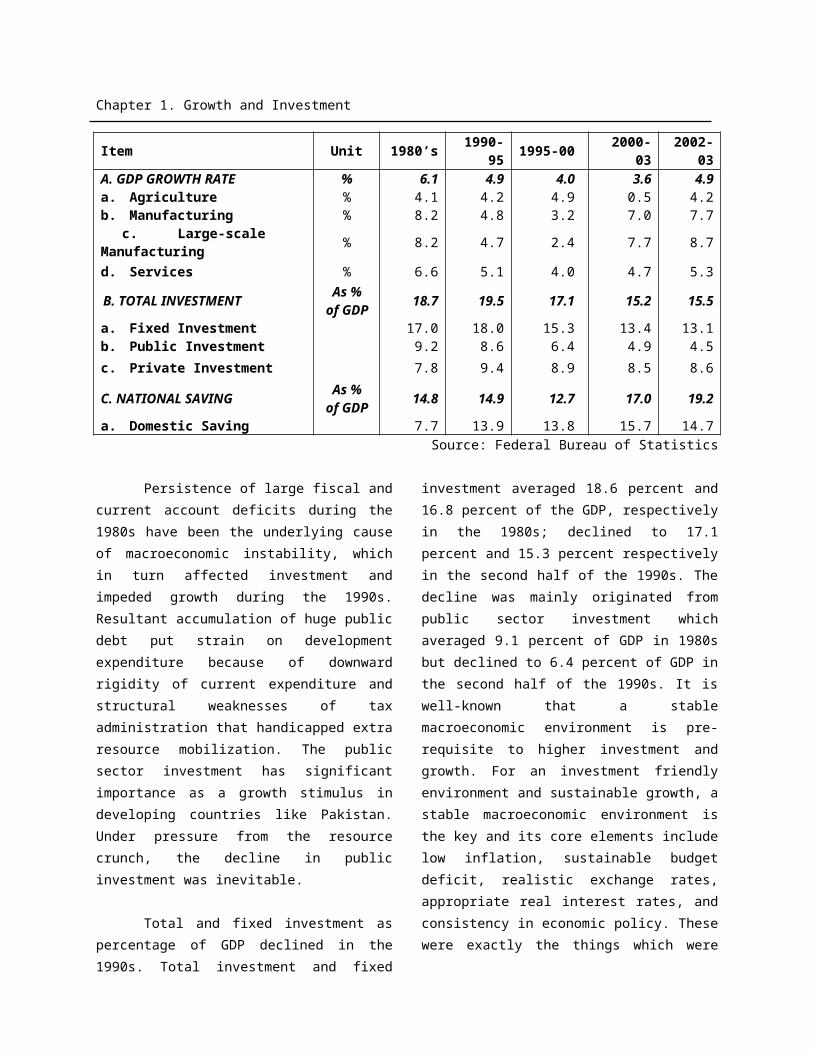

Table 1.1Growth Performance of Real Sector

Item Unit 1980’s 1990-95

1995-00

2000-03

2002-03

A. GDP GROWTH RATE % 6.1 4.9 4.0 3.6 4.9a. Agriculture % 4.1 4.2 4.9 0.5 4.2b. Manufacturing % 8.2 4.8 3.2 7.0 7.7

c. Large-scale Manufacturing

% 8.2 4.7 2.4 7.7 8.7

d. Services % 6.6 5.1 4.0 4.7 5.3

B. TOTAL INVESTMENTAs %

of GDP

18.7 19.5 17.1 15.2 15.5

a. Fixed Investment 17.0 18.0 15.3 13.4 13.1b. Public Investment 9.2 8.6 6.4 4.9 4.5

c. Private Investment 7.8 9.4 8.9 8.5 8.6

C. NATIONAL SAVINGAs %

of GDP

14.8 14.9 12.7 17.0 19.2

a. Domestic Saving 7.7 13.9 13.8 15.7 14.7Source: Federal Bureau of Statistics

Persistence of large fiscal and current account deficits during the 1980s have been the underlying cause of macroeconomic instability, which in turn affected investment and impeded growth during the 1990s. Resultant accumulation of huge public debt put strain on development expenditure because of downward rigidity of current expenditure and structural weaknesses of tax administration that handicapped extra resource mobilization. The public sector investment has significant importance as a growth stimulus in developing countries like Pakistan. Under pressure from the resource crunch, the decline in public investment was inevitable.

Total and fixed investment as percentage of GDP declined in the 1990s.

Total investment and fixed investment averaged 18.6 percent and 16.8 percent of the GDP, respectively in the 1980s; declined to 17.1 percent and 15.3 percent respectively in the second half of the 1990s. The decline was mainly originated from public sector investment which averaged 9.1 percent of GDP in 1980s but declined to 6.4 percent of GDP in the second half of the 1990s. It is well-known that a stable macroeconomic environment is pre-requisite to higher investment and growth. For an investment friendly environment and sustainable growth, a stable macroeconomic environment is the key and its core elements include low inflation, sustainable budget deficit, realistic exchange rates, appropriate real interest rates, and consistency in economic policy. These were exactly the things which were

Chapter 1. Growth and Investment

ignored in macro-economic policy making during the 1990s.

National saving rate also witnessed a decline from an average of 14.7 percent in the 1980s to 12.7 percent in the second half of the 1990s. Even with low investment rates, the current account showed large deficits during the 1990s. There was a shift by the end of the 1990s to finance investment from domestic sources instead of foreign resources. [See Table-1.1]. National savings as percent of GDP witnessed considerable improvement during the last three years (2000-03) and averaged 17.1 percent of GDP. The rise in national savings owes mainly to the significant turnaround in the current account balance.

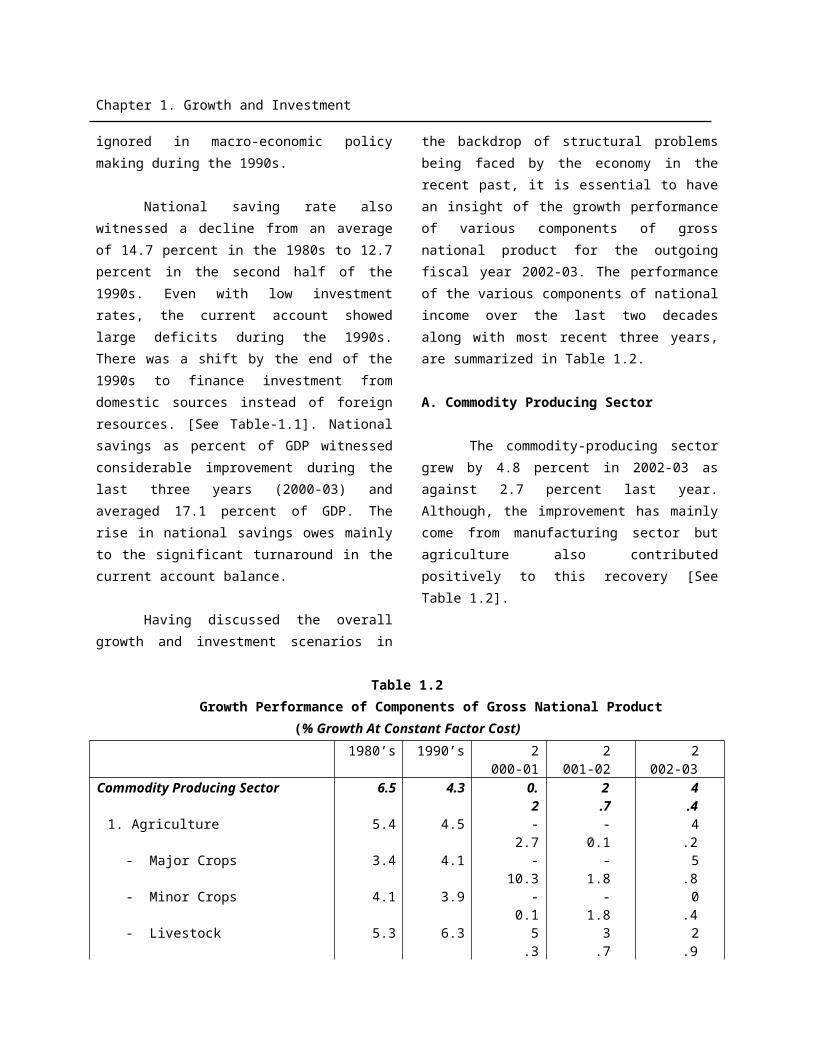

Having discussed the overall growth and investment scenarios in the backdrop of structural problems being faced by the economy in the recent past, it is essential to have an insight of the growth performance of various components of gross national product for the outgoing fiscal year 2002-03. The performance of the various components of national income over the last two decades along with most recent three years, are summarized in Table 1.2.

A. Commodity Producing Sector

The commodity-producing sector grew by 4.8 percent in 2002-03 as against 2.7 percent last year. Although, the im-provement has mainly come from manufac-turing sector but agriculture also contrib-uted positively to this recovery [See Table 1.2].

Table 1.2Growth Performance of Components of Gross National Product

(% Growth At Constant Factor Cost)1980’s 1990’s 2

000-012

001-022

002-03Commodity Producing Sector 6.5 4.3 0

.22

.74

.41. Agriculture 5.4 4.5 -

2.7-

0.14

.2- Major Crops 3.4 4.1 -

10.3-

1.85

.8- Minor Crops 4.1 3.9 -

0.1-

1.80

.4- Livestock 5.3 6.3 5

.33

.72

.9- Fishing 7.3 3.5 -

3.7-

12.01

6.6- Forestry 6.4 6.5 9

.6-

1.38

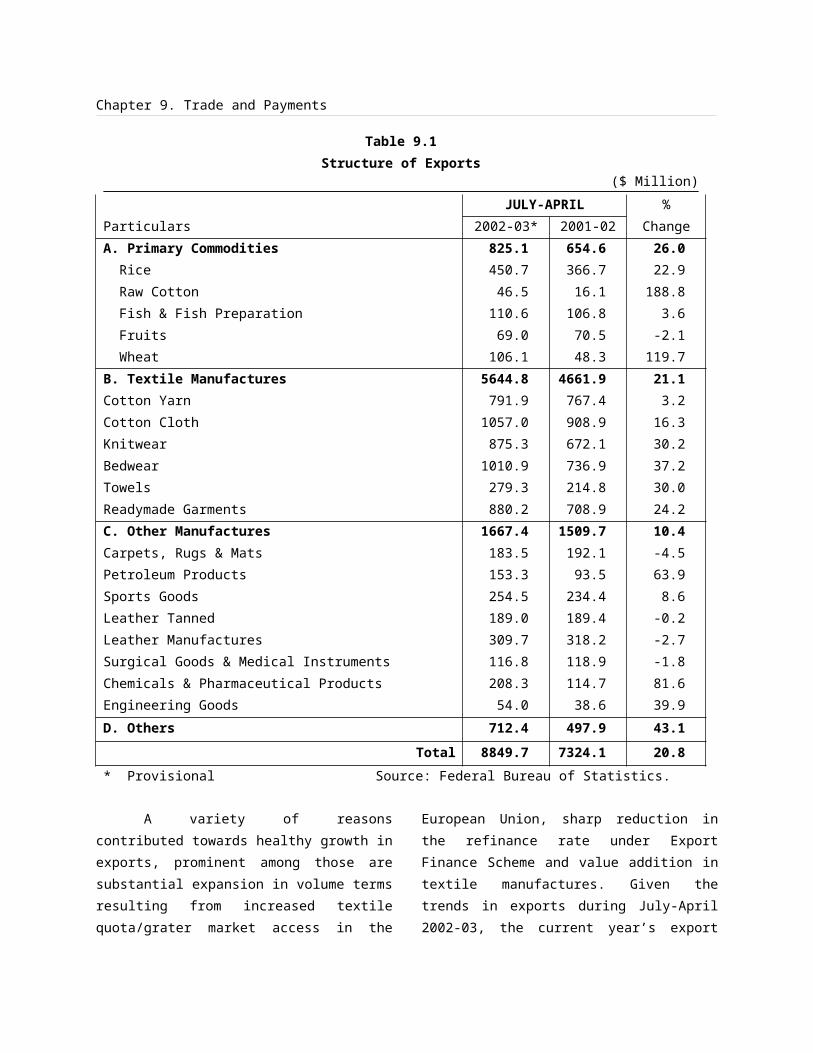

.92. Mining & Quarrying 9.5 2.9 4

.83

.79

.53. Manufacturing 8.2 4.0 8

.25

.07

.8- Large Scale 8.2 3.5 9

.54

.98

.7- Small Scale 8.4 5.3 5

.35

.35

.34. Construction 4.7 2.6 -

0.44

.33

.4

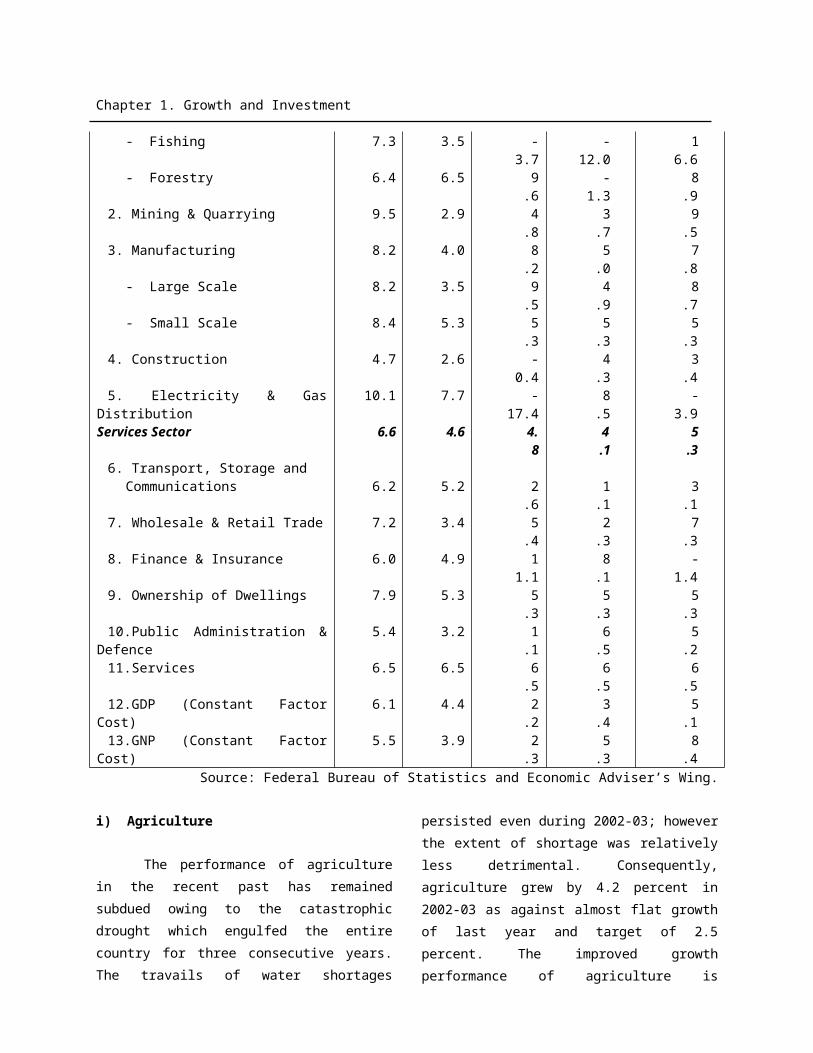

Chapter 1. Growth and Investment

5. Electricity & Gas Distribution 10.1 7.7 -17.4

8.5

-3.9

Services Sector 6.6 4.6 4.8

4.1

5.3

6. Transport, Storage and Communications 6.2 5.2 2

.61

.13

.17. Wholesale & Retail Trade 7.2 3.4 5

.42

.37

.38. Finance & Insurance 6.0 4.9 1

1.18

.1-

1.49. Ownership of Dwellings 7.9 5.3 5

.35

.35

.310.Public Administration &

Defence5.4 3.2 1

.16

.55

.211.Services 6.5 6.5 6

.56

.56

.512.GDP (Constant Factor Cost) 6.1 4.4 2

.23

.45

.113.GNP (Constant Factor Cost) 5.5 3.9 2

.35

.38

.4Source: Federal Bureau of Statistics and Economic Adviser’s Wing.

i) Agriculture

The performance of agriculture in the recent past has remained subdued owing to the catastrophic drought which engulfed the entire country for three consecutive years. The travails of water shortages persisted even during 2002-03; however the extent of shortage was relatively less detrimental. Consequently, agriculture grew by 4.2 percent in 2002-03 as against almost flat growth of last year and target of 2.5 percent. The improved growth performance of agriculture is attributable to impressive recovery in the performance of major crops.

Major crops accounting for 41 percent of agriculture value added grew by 5.8 percent as against a decline in value addition for the last two consecutive years and a target of fractional growth of 0.3 percent for 2002-03. Major crops including wheat, sugarcane, and rice witnessed increase in production by 5.5 percent, 8.3 percent, and 15.4 percent, respectively. However, the production of cotton witnessed a decline of 3.8 percent during

2002-03. This is the third year in a row when the value addition in cotton crops has declined. [See Chapter-2 for details]

The growth in value addition of Minor crops which contribute 16 percent of value addition in agriculture grew marginally by 0.4 percent in 2002-03 as against the growth target of 3.5 percent growth and decline of 1.8 percent last year. The minor crops include cereals, vegetables, fruits, condiments, oil seeds, fodder and others. Within minor crops, the production of all three major pulses witnessed tremendous growth due to introduction of new varieties of seeds. However, increase in production of important minor crops like chilies, pulses, oil seeds and onion could not boost the overall growth of minor crops.

Livestock sub-sector which account for 39 percent of overall value addition in agriculture has witnessed a modest growth of 2.9 percent in 2002-03 as compared with the target of 4.0 percent for the year and

Chapter 1. Growth and Investment

actual achievement of 3.7 percent last year. The lower growth owes to decreasing use of draught power and adjustments for inputs in the sub-sector. The production of milk, egg and mutton are estimated to have gone up by 2.9, 2.3 and 2.9 percent, respectively. The fisheries sector witnessed a growth of 16.6 percent as against a decline of 12.0 percent last year and yearly target of 4.0 percent growth. Components of fisheries such as marine fishing and inland fishing, contributed to overall increase in value added in the fisheries sub-sector. The value addition in forestry sub-sector has increased by 8.8 percent as compared to a decline of 1.3 percent last year. The production of timber and firewood also went up by 8.8 percent each.

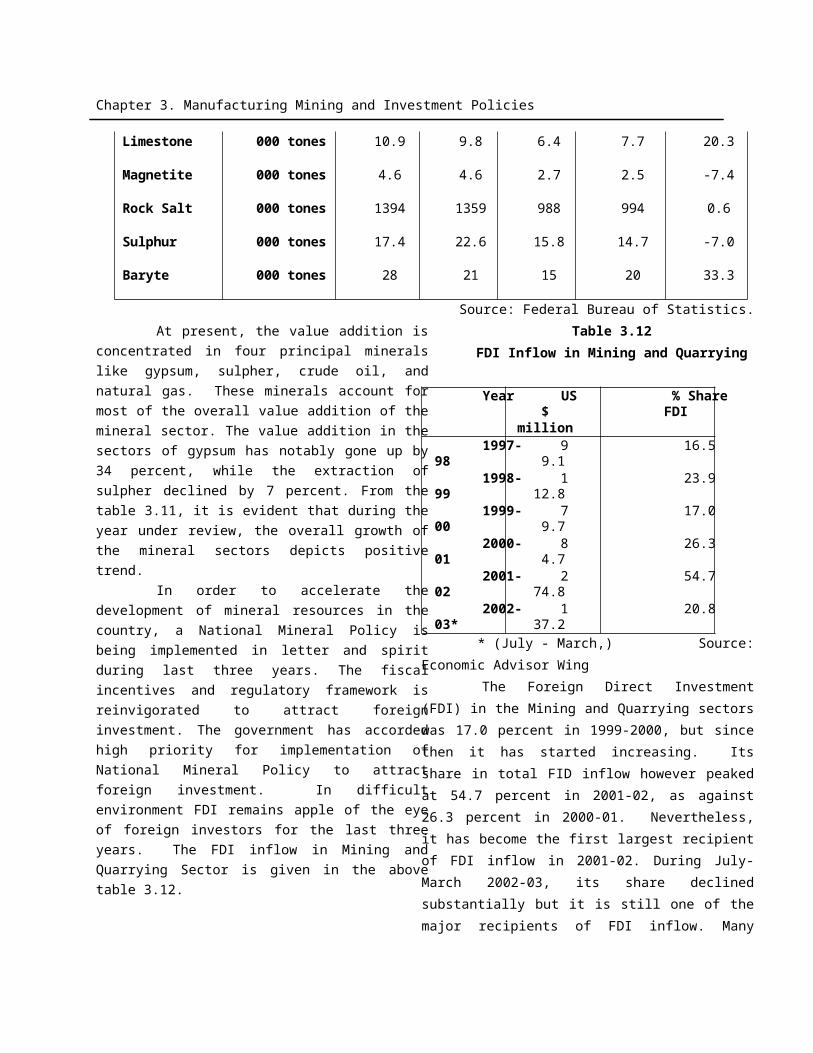

ii) Mining & Quarrying

The output in the mining and quarrying sector has surpassed the target of 2.5 percent and grew by 9.5 percent in 2002-03 as against 3.7 percent last year. The value added in crude oil increased by 2.8 percent and in natural gas it has risen by 6.5 percent. However, the value addition in coal decreased by 2.5 percent, inspite of the fact that cement industry has started using coal as a major source of energy which has fuelled the domestic demand of coal. The principal mineral which has shown enormous growth include barite (33.3 percent), lime stone (20.3 percent), gypsum (33.9 percent), and chromites (50 percent). The minerals with negative growth include sulphur (7.0 percent), dolomite (3.0 percent), and magnisite (7.4 percent).

iii) Manufacturing

The overall manufacturing sector grew by 7.7 percent as against the target of 5.8 percent and last year’s achievement of 5.0 percent. Large scale manufacturing

sector accounting for 71.2 percent of overall manufacturing, recorded an impressive and broad based growth of 8.7 percent, as against the target of 6.0 percent and last year’s growth of 4.9 percent. This is the second highest growth rate recorded during the last 13 years (the first one is 9.5 percent in 2000-01). Improvements in macroeconomic environment, sharp recovery in exports, and the availability of consumer financing at reasonable interest rates have been responsible for strong performance of large-scale manufacturing. Over the last three years (2000-03), the large-scale manufacturing has registered an average growth of 7.7 percent per annum.

Major industries that registered positive growth include sugar (13.6 percent), cement (20.5 percent), petroleum products (2.2 percent), cooking oil (6.8 percent), jeeps & cars (51.6 percent), LCV’s (57.6 percent), cotton yarn (8.1 percent), paper & board (15.7 percent), soda ash (12.9 percent), motorcycles (33.5 percent), nitrogenous fertilizer (4.2 percent) and motor tyres (16.0 percent). Ten out of eleven major industrial groups posted positive growth while only leather products group registered negative growth. The individual industries that depicted negative growth include: sulphuric acid (5.4 percent), phosphatic fertilizer (27.8 percent), paints & varnishes (63.7 percent), beverages (18.3 percent), cigarettes (7.1 percent), vegetable ghee (7.0 percent), foot wear (6.2 percent), and cotton ginned (4.7 percent). Small-scale manufacturing maintained its historical growth of 5.3 percent in 2002-03.

Construction sector grew by 3.4 percent as against 4.3 percent last year and yearly target of 4.0 percent. The government has identified housing and construction sectors as one of the major

Chapter 1. Growth and Investment

drivers of growth and likely to announce various measures in the Federal Budget 2003-04 to encourage activities in this sector. Electricity and gas distribution sector registered a decline of 3.9 percent as against an impressive growth of 8.5 percent last year and yearly target of 4.3 percent. This is the only sub-sector in commodity producing sector which registered a negative growth.

B. Services SectorThe Services Sector has been

growing at a faster pace than commodity producing sector of the economy for quite sometime. The trend remained unchanged even during 2002-03 as the services sector grew by 5.3 percent as against 4.1 percent of last year. Within this sector, the wholesale & retail trade and transport, storage and communication sub-sectors grew by 7.3 percent and 3.1 percent, respectively as against 2.3 percent and 1.1 percent of last year.

Finance and insurance sub-sector remained depressed as far as value addition is concerned. The sub-sector registered a decline of 1.4 percent in value addition during 2002-03 as against the target of 5.0 percent positive growth and last year’s actual achievement of 8.1 percent growth. Public administration and defence has depicted a growth of 5.2 percent as against 6.5 percent last year. Two minor sectors that is, ownership of dwellings and social services, have maintained their estimated growth of 5.3 percent and 6.5 percent, respectively.

Sectoral Contribution to Real GDP Growth

The greater contribution to real GDP growth of 5.1 percent came from services sector (2.7 percentage points). Industrial

sector contributed 1.4 percentage points with major share coming from manufacturing sector (almost entire). As evident from Table 1.3, almost 53 percent contribution to growth (2.7 percentage point out of 5.1 percent of real GDP growth) has come from services sector followed by industrial sector (27 percent) and agriculture (20 percent). Last year, services sector contributed 59 percent and 41 percent contribution came from industrial sector. Agricultural contributed negatively to the last year’s growth. This suggests a balanced contribution from all the three sectors to this year’s growth. The contribution of each sector to growth is summarized in Table-1.3:

Table 1.3Sectoral Contribution to the GDP

growth(Percentage Points)

Sector 2000-01

2001-02

2002-03

Agricultue -0.7 -0.02 1.0 Industry 0.6 1.4 1.4Services 2.3 2.0 2.7Real GDP (Fc)

2.2 3.4 5.1

Source: Federal Bureau of Statistics.

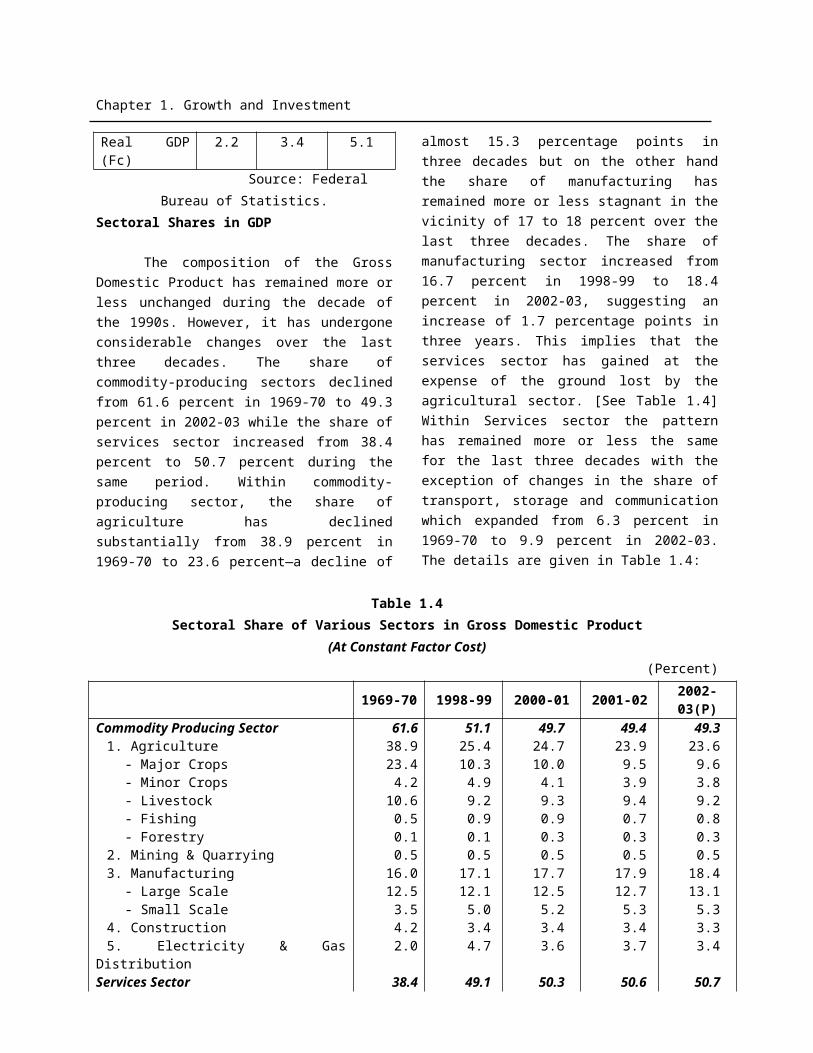

Sectoral Shares in GDP

The composition of the Gross Domestic Product has remained more or less unchanged during the decade of the 1990s. However, it has undergone considerable changes over the last three decades. The share of commodity-producing sectors declined from 61.6 percent in 1969-70 to 49.3 percent in 2002-03 while the share of services sector increased from 38.4 percent to 50.7 percent during the same period. Within commodity-producing sector, the share of agriculture has declined substantially from 38.9 percent in 1969-70 to 23.6 percent—a decline of almost 15.3 percentage points in three decades but on the other hand the

Chapter 1. Growth and Investment

share of manufacturing has remained more or less stagnant in the vicinity of 17 to 18 percent over the last three decades. The share of manufacturing sector increased from 16.7 percent in 1998-99 to 18.4 percent in 2002-03, suggesting an increase of 1.7 percentage points in three years. This implies that the services sector has gained at the expense of the ground lost by the

agricultural sector. [See Table 1.4] Within Services sector the pattern has remained more or less the same for the last three decades with the exception of changes in the share of transport, storage and communication which expanded from 6.3 percent in 1969-70 to 9.9 percent in 2002-03. The details are given in Table 1.4:

Table 1.4Sectoral Share of Various Sectors in Gross Domestic Product

(At Constant Factor Cost)(Percent)

1969-70

1998-99 2000-01 2001-02 2002-03(P)

Commodity Producing Sector 61.6 51.1 49.7 49.4 49.31. Agriculture 38.9 25.4 24.7 23.9 23.6

- Major Crops 23.4 10.3 10.0 9.5 9.6- Minor Crops 4.2 4.9 4.1 3.9 3.8- Livestock 10.6 9.2 9.3 9.4 9.2- Fishing 0.5 0.9 0.9 0.7 0.8- Forestry 0.1 0.1 0.3 0.3 0.3

2. Mining & Quarrying 0.5 0.5 0.5 0.5 0.53. Manufacturing 16.0 17.1 17.7 17.9 18.4

- Large Scale 12.5 12.1 12.5 12.7 13.1- Small Scale 3.5 5.0 5.2 5.3 5.3

4. Construction 4.2 3.4 3.4 3.4 3.35. Electricity & Gas Distribution 2.0 4.7 3.6 3.7 3.4

Services Sector 38.4 49.1 50.3 50.6 50.76. Transport, Storage and Communication

6.3 10.2 10.3 10.0 9.9

7. Wholesale and Retail Trade 13.8 15.2 15.3 15.2 15.58. Finance and Insurance 1.8 2.5 2.5 2.6 2.49. Ownership of Dwellings 3.4 5.9 6.1 6.2 6.210.Public Administration and

Defence6.4 6.1 6.4 6.6 6.6

11.Other Services 6.7 9.0 9.7 10.0 10.112.GDP (Constant Factor Cost) 100.0 100.0 100.0 100.0 100.0

P) Stands for provisional. Source: Economic Adviser’s Wing, Finance Division

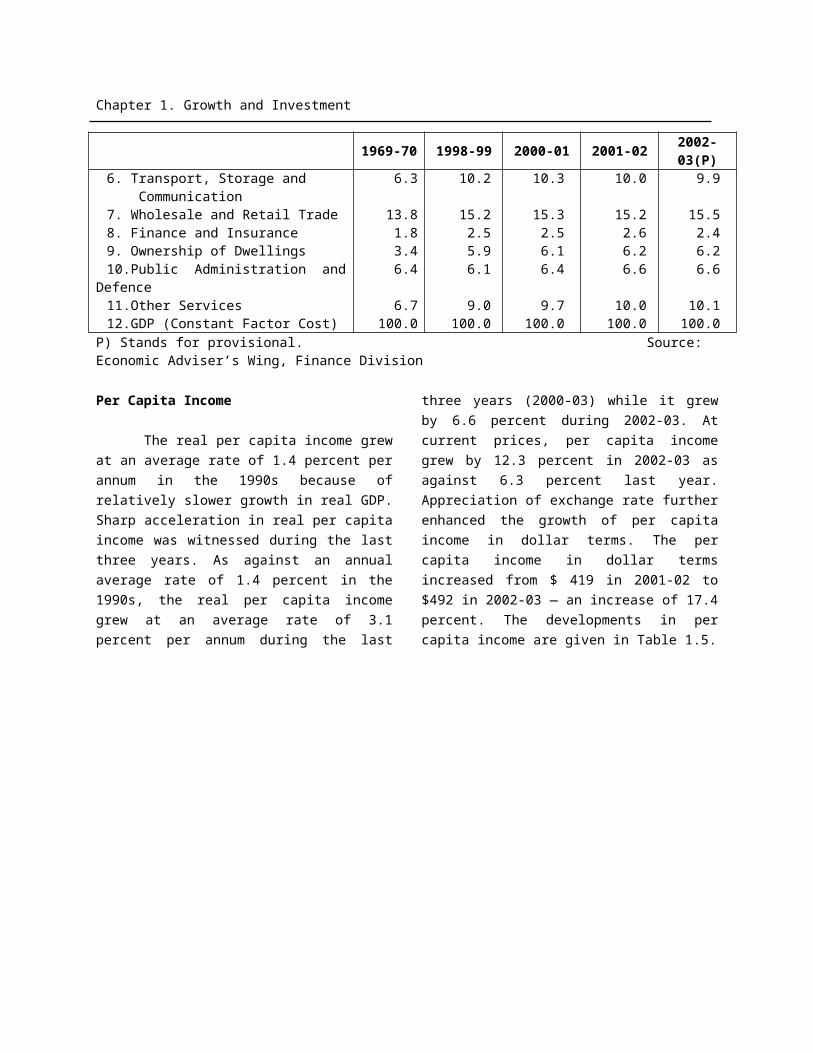

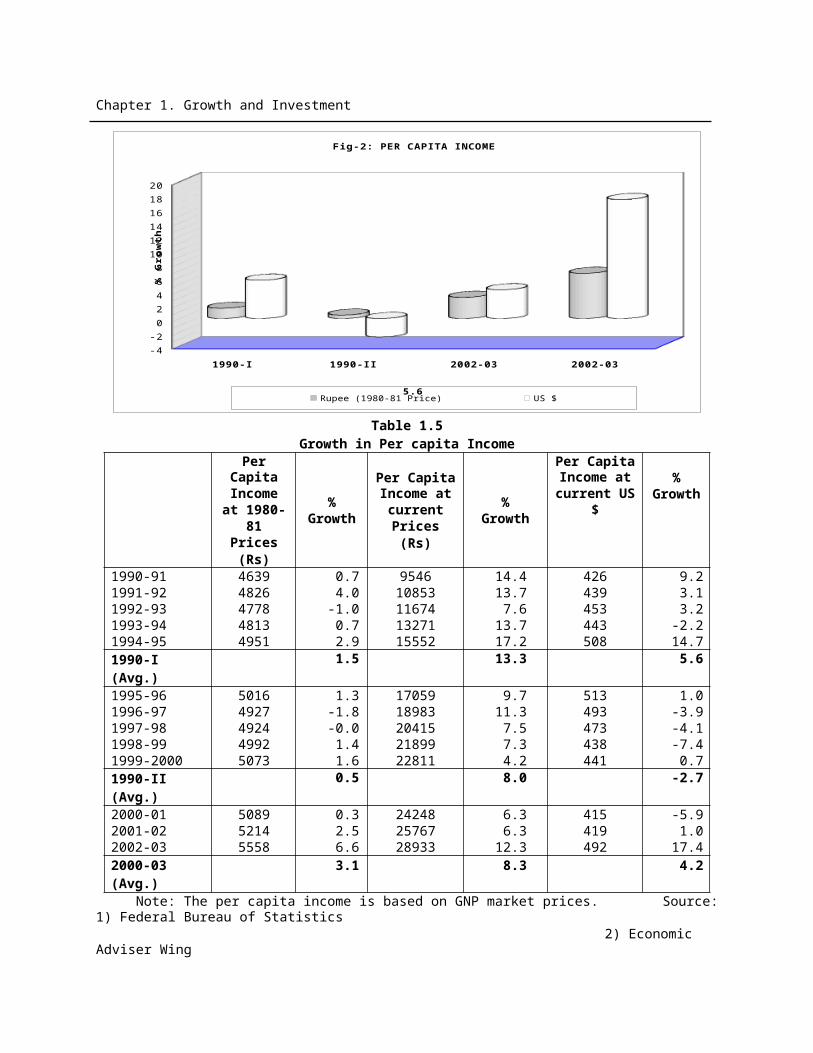

Per Capita Income

The real per capita income grew at an average rate of 1.4 percent per annum in the 1990s because of relatively slower growth in real GDP. Sharp acceleration in real per capita income was witnessed during the last three years. As against an annual average rate of 1.4 percent in the 1990s, the real per capita income grew at

an average rate of 3.1 percent per annum during the last three years (2000-03) while it grew by 6.6 percent during 2002-03. At current prices, per capita income grew by 12.3 percent in 2002-03 as against 6.3 percent last year. Appreciation of exchange rate further enhanced the growth of per capita income in dollar terms. The per capita income in dollar terms increased from $ 419 in 2001-02 to $492 in 2002-03

Chapter 1. Growth and Investment

— an increase of 17.4 percent. The developments in per capita income are

given in Table 1.5.

1990-I 1990-II 2002-03 2002-03

-4

-2

0

2

4

6

8

10

12

14

16

18

20

5.6

Fig-2: PER CAPITA INCOME

Rupee (1980-81 Price) US $

% G

row

th

Table 1.5Growth in Per capita Income

Per Capita Income at 1980-81 Prices

(Rs)

%Growth

Per Capita Income at

current Prices (Rs)

%Growth

Per Capita Income at current US

$

%Growt

h

1990-91 4639 0.7 9546 14.4 426 9.21991-92 4826 4.0 10853 13.7 439 3.11992-93 4778 -1.0 11674 7.6 453 3.21993-94 4813 0.7 13271 13.7 443 -2.21994-95 4951 2.9 15552 17.2 508 14.71990-I (Avg.)

1.5 13.3 5.6

1995-96 5016 1.3 17059 9.7 513 1.01996-97 4927 -1.8 18983 11.3 493 -3.91997-98 4924 -0.0 20415 7.5 473 -4.11998-99 4992 1.4 21899 7.3 438 -7.41999-2000 5073 1.6 22811 4.2 441 0.71990-II (Avg.)

0.5 8.0 -2.7

2000-01 5089 0.3 24248 6.3 415 -5.92001-02 5214 2.5 25767 6.3 419 1.02002-03 5558 6.6 28933 12.3 492 17.42000-03 (Avg.)

3.1 8.3 4.2

Note: The per capita income is based on GNP market prices. Source: 1) Federal Bureau of Statistics

2) Economic Adviser Wing

Chapter 1. Growth and Investment

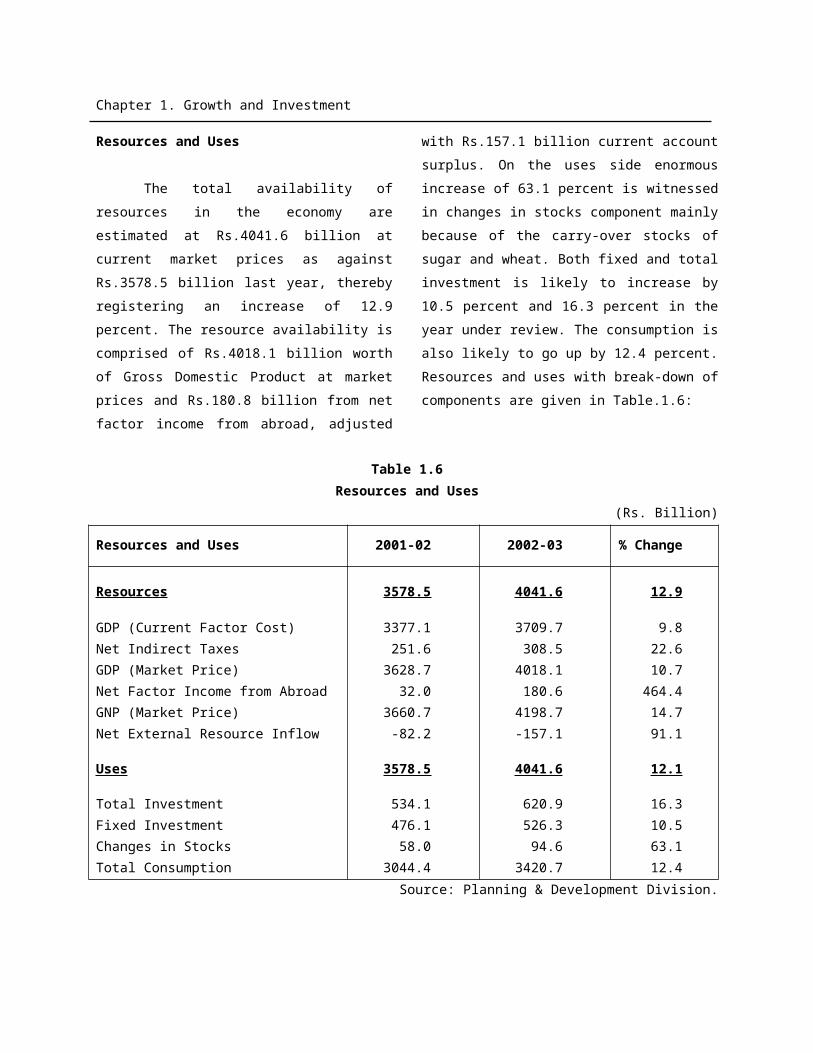

Resources and Uses

The total availability of resources in

the economy are estimated at Rs.4041.6

billion at current market prices as against

Rs.3578.5 billion last year, thereby

registering an increase of 12.9 percent. The

resource availability is comprised of

Rs.4018.1 billion worth of Gross Domestic

Product at market prices and Rs.180.8

billion from net factor income from abroad,

adjusted with Rs.157.1 billion current

account surplus. On the uses side enormous

increase of 63.1 percent is witnessed in

changes in stocks component mainly

because of the carry-over stocks of sugar

and wheat. Both fixed and total investment

is likely to increase by 10.5 percent and

16.3 percent in the year under review. The

consumption is also likely to go up by 12.4

percent. Resources and uses with break-

down of components are given in Table.1.6:

Table 1.6Resources and Uses

(Rs. Billion)

Resources and Uses 2001-02 2002-03%

Change

Resources 3578.5 4041.6 12.9

GDP (Current Factor Cost) 3377.1 3709.7 9.8Net Indirect Taxes 251.6 308.5 22.6GDP (Market Price) 3628.7 4018.1 10.7Net Factor Income from Abroad 32.0 180.6 464.4GNP (Market Price) 3660.7 4198.7 14.7Net External Resource Inflow -82.2 -157.1 91.1

Uses 3578.5 4041.6 12.1

Total Investment 534.1 620.9 16.3Fixed Investment 476.1 526.3 10.5Changes in Stocks 58.0 94.6 63.1Total Consumption 3044.4 3420.7 12.4

Source: Planning & Development Division.

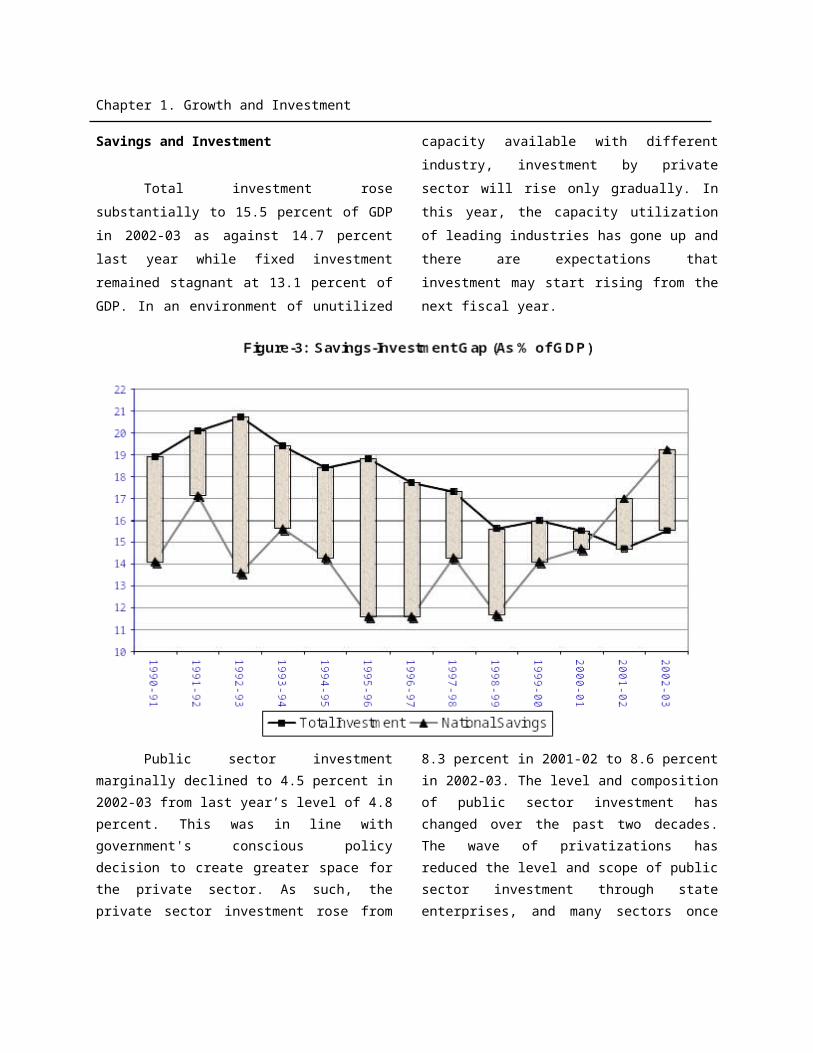

Savings and Investment

Total investment rose substantially

to 15.5 percent of GDP in 2002-03 as

against 14.7 percent last year while fixed

investment remained stagnant at 13.1

percent of GDP. In an environment of

unutilized capacity available with different

industry, investment by private sector will

rise only gradually. In this year, the

capacity utilization of leading industries has

gone up and there are expectations that

investment may start rising from the next

fiscal year.

Chapter 1. Growth and Investment

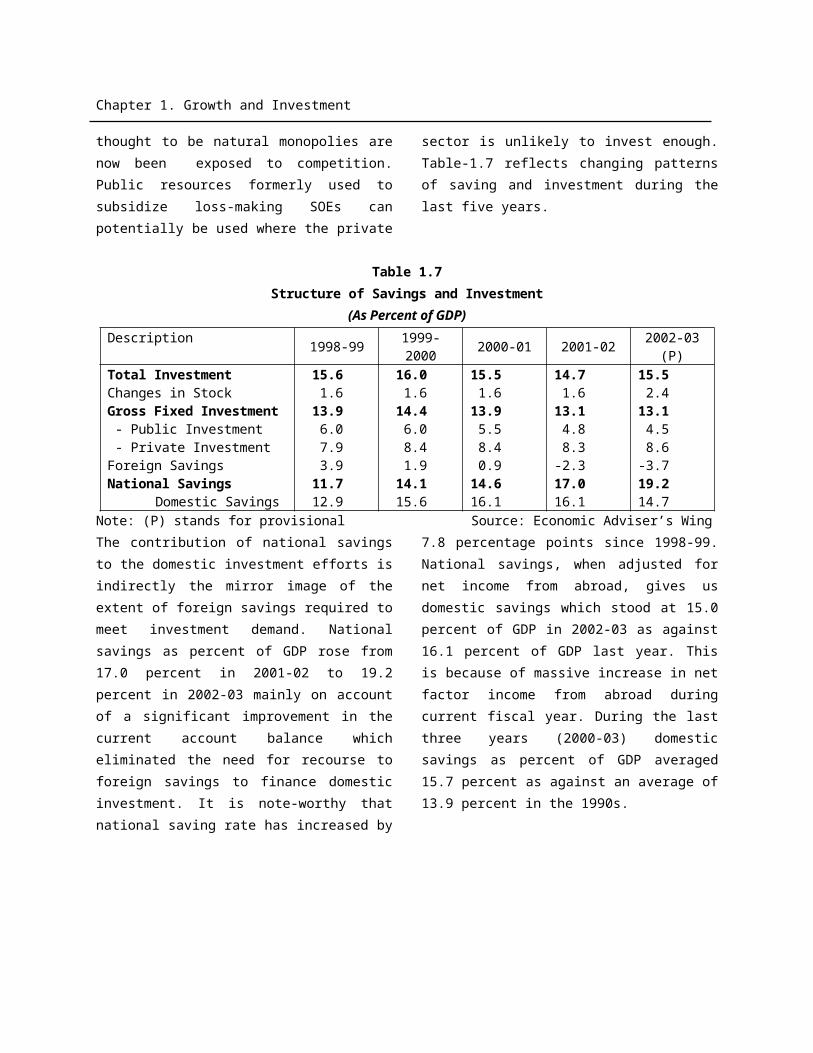

Public sector investment marginally declined to 4.5 percent in 2002-03 from last year’s level of 4.8 percent. This was in line with government's conscious policy decision to create greater space for the private sector. As such, the private sector investment rose from 8.3 percent in 2001-02 to 8.6 percent in 2002-03. The level and composition of public sector investment has changed over the past two decades. The wave of privatizations has reduced the level

and scope of public sector investment through state enterprises, and many sectors once thought to be natural monopolies are now been exposed to competition. Public resources formerly used to subsidize loss-making SOEs can potentially be used where the private sector is unlikely to invest enough. Table-1.7 reflects changing patterns of saving and investment during the last five years.

Table 1.7Structure of Savings and Investment

(As Percent of GDP)Description 1998-99 1999-

20002000-01 2001-02 2002-03

(P)Total Investment 15.6 16.0 15.5 14.7 15.5Changes in Stock 1.6 1.6 1.6 1.6 2.4Gross Fixed Investment 13.9 14.4 13.9 13.1 13.1 - Public Investment 6.0 6.0 5.5 4.8 4.5

Chapter 1. Growth and Investment

- Private Investment 7.9 8.4 8.4 8.3 8.6Foreign Savings 3.9 1.9 0.9 -2.3 -3.7National Savings 11.7 14.1 14.6 17.0 19.2

Domestic Savings 12.9 15.6 16.1 16.1 14.7Note: (P) stands for provisional Source: Economic Adviser’s WingThe contribution of national savings to the domestic investment efforts is indirectly the mirror image of the extent of foreign savings required to meet investment demand. National savings as percent of GDP rose from 17.0 percent in 2001-02 to 19.2 percent in 2002-03 mainly on account of a significant improvement in the current account balance which eliminated the need for recourse to foreign savings to finance domestic investment. It is note-worthy that national saving rate has increased by 7.8

percentage points since 1998-99. National savings, when adjusted for net income from abroad, gives us domestic savings which stood at 15.0 percent of GDP in 2002-03 as against 16.1 percent of GDP last year. This is because of massive increase in net factor income from abroad during current fiscal year. During the last three years (2000-03) domestic savings as percent of GDP averaged 15.7 percent as against an average of 13.9 percent in the 1990s.

Chapter 2. Agriculture

2. AgricultureAgriculture sector being the lynchpin

of the country’s economy continues to be the single largest sector and a dominant driving force for growth and development of the national economy. It accounts for 24 percent of the GDP and employs 48.4 percent of the total work force. Agriculture contributes to growth as a supplier of raw materials to industry as well as a market for industrial products and also contributes substantially to Pakistan’s exports earnings. Almost 67.5 percent of country’s population are living in rural areas and are directly or indirectly linked with agriculture for their livelihood. Any improvement in agriculture will not only help country’s economic growth to rise at a faster rate but will also benefit a large segment of the country’s population.

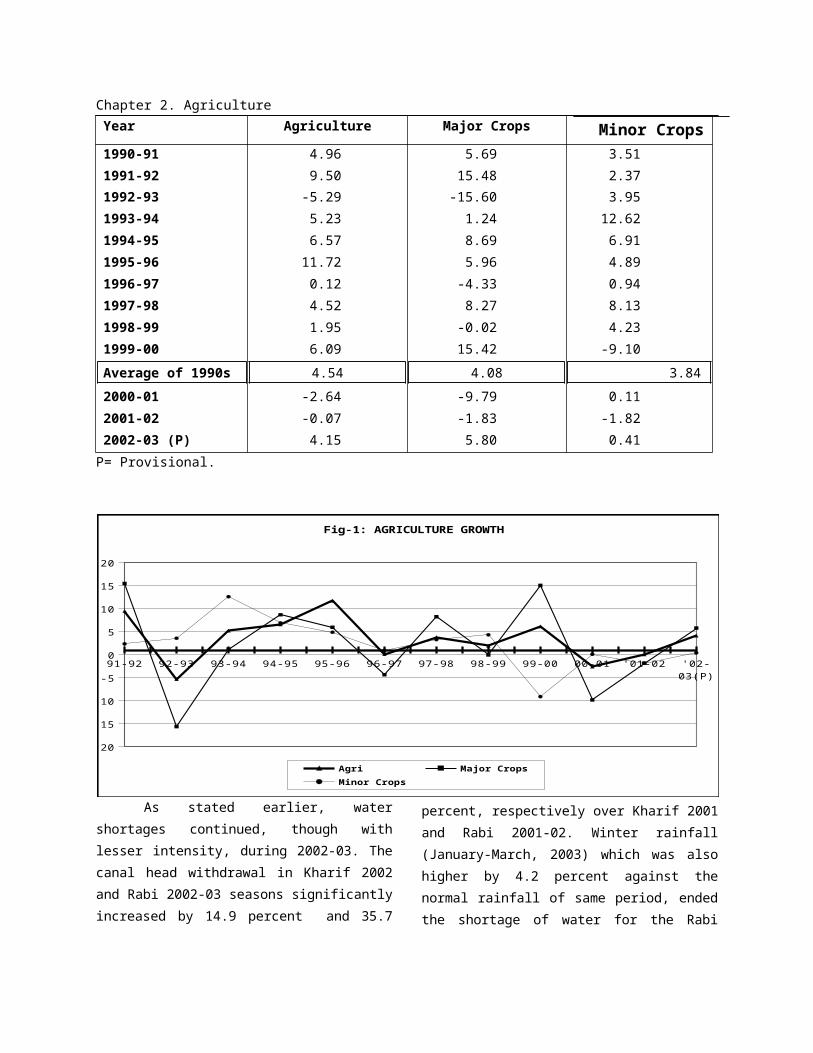

Agriculture sector has grown at an average rate of 4.5 percent per annum during the decade of the 1990s (Table-2.1) . The growth, however, has fluctuated widely – rising by as high as 11.7 percent and declining by 5.3 percent. Over the last three years in general but the first two years (2000-01 and 2001-02) of the new millennium in particular, Pakistan has witnessed crippling drought which badly affected its agriculture. Overall agricultural growth turned negative for these two years (See Table 2.1). The travails of water shortage persisted even during 2002-03, however the extent of shortage was relatively less. Notwithstanding shortage of water, Agriculture grew by 4.2 percent in 2002-03 (See Table 2.1).

Table 2.1

Agriculture Growth(Percent)

Year Agriculture Major Crops Minor Crops1990-911991-92

4.969.50

5.6915.48

3.512.37

1992-931993-941994-951995-961996-971997-981998-991999-00

-5.295.236.57

11.720.124.521.956.09

-15.601.248.695.96

-4.338.27

-0.0215.42

3.9512.62

6.914.890.948.134.23

-9.10

Chapter 2. Agriculture

Average of 1990s

2000-012001-022002-03 (P)

4.54

-2.64-0.074.15

4.08

-9.79-1.835.80

3.84

0.11-1.820.41

P= Provisional.

As stated earlier, water shortages continued, though with lesser intensity, during 2002-03. The canal head withdrawal in Kharif 2002 and Rabi 2002-03 seasons significantly increased by 14.9 percent and 35.7 percent, respectively over Kharif 2001 and Rabi 2001-02. Winter rainfall (January-March, 2003) which was also higher by 4.2 percent against the normal rainfall of same period, ended the shortage of water for the Rabi Crop 2002-03. Moreover, heavy snowfall on the mountains during winter, 2003 would help fill the country’s water reservoirs and alleviate water shortages to a greater extent for the Kharif Crops 2003. On the whole, the water situation in the current fiscal year appears better than last year but remains in short supply compared with the normal supplies. [More on this issue can be found under sub-section ‘irrigation’].

The relatively better availability of irrigation water has had positive impact on overall agricultural production this year and the agriculture growth is estimated at 4.2 percent as compared with negative 0.1 percent during 2001-02. Major crops, accounting for 41 percent of agriculture value added, registered a sharp recovery and grew by 5.8 percent against the decline of 1.8 percent last year. Minor crops, contributing 16 percent to agricultural value added, depicted positive growth of 0.4 percent against a negative growth of 1.8 percent last year. Livestock the second largest contributor to overall agriculture value added (contributing 39 percent), grew by 2.9 percent in 2002-03 as against 3.7 percent in 2001-02. Fisheries has shown a remarkable growth of 16.6 percent against the negative growth of 12 percent last year. On the other hand, forestry also registered a significant growth of 8.8 percent as against a

91-92 92-93 93-94 94-95 95-96 96-97 97-98 98-99 99-00 00-01 '01-02 '02-03(P)

-20

-15

-10

-5

0

5

10

15

20

Fig-1: AGRICULTURE GROWTH

Agri Major Crops Minor Crops

Chapter 2. Agriculturenegative growth of 1.3 percent last year. The situation of major crops for the last five years is presented inTable-2.2.

I. Crop Situation

There are two principal crop seasons in Pakistan, namely the "Kharif" the sowing season of which begins in April-June and harvesting during October-December; and the "Rabi", which begins in October-December and ends in April-May. Rice, sugarcane, cotton, maize, bajra and jowar are “Kharif" crops while wheat, gram, tobacco, rapeseed, barley and mustard are "Rabi" crops. Major crops, such as, wheat, rice, cotton and sugarcane account for 90 percent of value added in major crops. The value added in major crops accounts for 41 percent of value added in overall agriculture. Thus, the four major crops (wheat, rice, cotton, and sugarcane), on average, contribute 37 percent to value added in overall agriculture. The minor crops account for 16 percent of value added in overall agriculture. The performance of the

Chapter 2. Agriculture "Kharif" and "Rabi" crops is discussed in the ensuing pages.

Chapter 2. Agriculture

Table 2.2Production of Major Crops

(000 Tonnes)

Year Cotton(000 bales) Sugarcane Rice Maize Wheat

1998-99

1999-00

2000-01

2001-02

2002-03 (P)

8790(-4.3)

11240(27.9)

10732(-4.5)

10613(-1.1)

10211(-3.8)

55191(3.9)

46333(-16.0)

43606(-5.9)

48042(10.2)

52049(8.3)

4674(7.9)

5156(10.3)

4803(-6.8)

3882(-19.2)

4478(15.4)

1665(9.8)

1652(-0.8)

1643(-0.5)

1664(1.3)

1758(5.6)

17856(-4.5)

21079(18.0)

19024(-9.7)

18227(-4.2)

19235(5.5)

P: Provisional.(July-March) Source: Ministry of Food, Agriculture and Livestock.*: Figures in parentheses are growth rates Federal Bureau of Statistics.

a) Major Crops:

i) Cotton:

Cotton is the main cash crop which contributes substantially to the national income. It accounts for 11.7 percent of value added in agriculture and about 2.9 percent of GDP. In addition to providing raw material to the local textile industry, the surplus lint cotton is also

exported. Production of cotton is provisionally estimated at 10211 thousand bales for 2002-03, which is 3.8 percent lower than last year. The pest attack and shortage of irrigation water in the early Kharif season are mainly responsible for lower production. Cotton was cultivated on the area of 2796 thousand hectares, which was 10.3 percent lower than last year (3116 thousand hectares). Area, production and yield of cotton for the last five years are given in Table 2.3.

Table 2.3Cotton, Area, Production and Yield

Area Production Yield

Year (000 Hectare)

%Change (000 Bales)

% Change

(Kgs/Hec) %Change

1998-991999-002000-012001-022002-03

29232983292731162796

-1.22.0

-1.96.5

-10.3

879011240107321061310211

-4.327.9-4.5-1.1-3.8

511641623579621

-3.025.4-2.8-7.17.2

Chapter 2. Agriculture

(P)

P=Provisional (July-March). Source: Ministry of Food, Agriculture and Livestock Federal Bureau of

Statistics.

90-9

1

91-9

2

92-9

3

93-9

4

94-9

5

95-9

6

96-9

7

97-9

8

98-9

9

99-0

0

00-0

1

01-0

2

02-0

3(P)

5000

6000

7000

8000

9000

10000

11000

12000

13000

14000

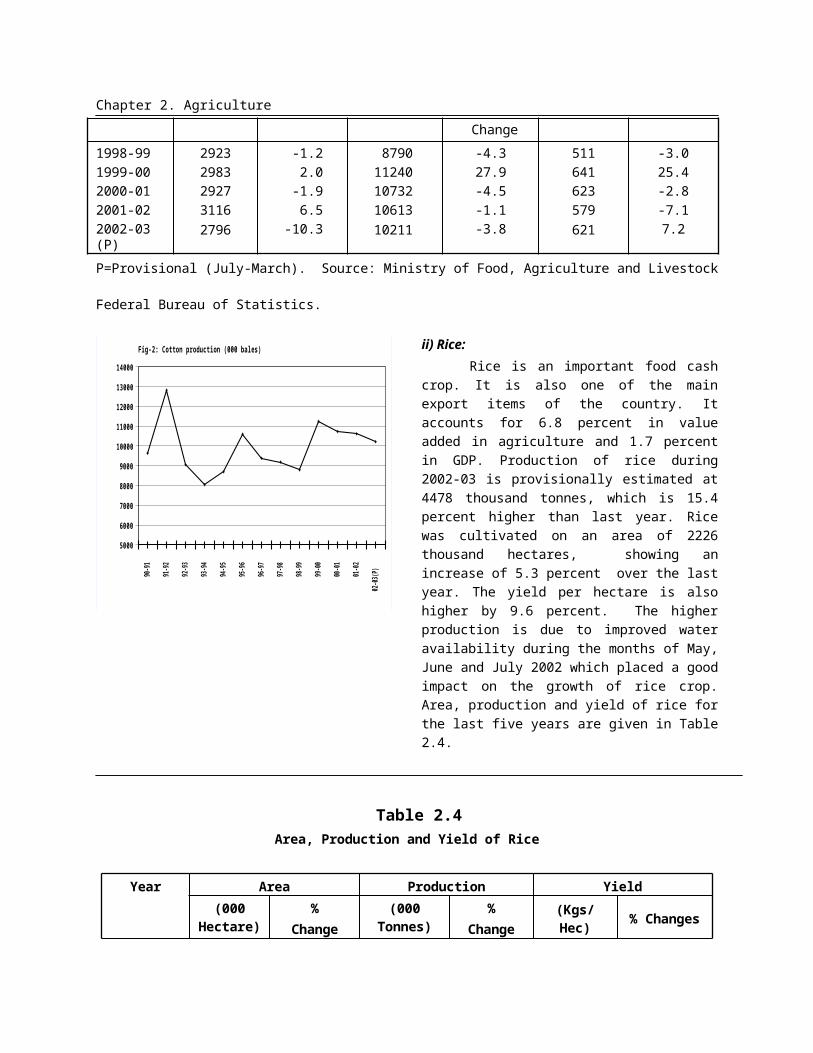

Fig-2: Cotton production (000 bales) ii) Rice:Rice is an important food cash crop. It

is also one of the main export items of the country. It accounts for 6.8 percent in value added in agriculture and 1.7 percent in GDP. Production of rice during 2002-03 is provisionally estimated at 4478 thousand tonnes, which is 15.4 percent higher than last year. Rice was cultivated on an area of 2226 thousand hectares, showing an increase of 5.3 percent over the last year. The yield per hectare is also higher by 9.6 percent. The higher production is due to improved water availability during the months of May, June and July 2002 which placed a good impact on the growth of rice crop. Area, production and yield of rice for the last five years are given in Table 2.4.

Table 2.4Area, Production and Yield of Rice

Year Area Production Yield(000

Hectare)%

Change(000

Tonnes)%

Change(Kgs/Hec)

% Changes

1998-991999-002000-012001-022002-03 (P)

24242515237721142226

4.63.8-5.5-11.15.3

46745156480338824478

7.910.3-6.8-19.215.3

19282050202118362012

3.16.3-1.4-9.19.6

P: Provisional (July-March). Source: Ministry of Food, Agriculture and Livestock.

Federal Bureau of Statistics.

Chapter 2. Agriculture

90-9

1

91-9

2

92-9

3

93-9

4

94-9

5

95-9

6

96-9

7

97-9

8

98-9

9

99-0

0

00-0

1

01-0

2

'02-0

3(P)

2000

2500

3000

3500

4000

4500

5000

5500

Fig-3: Rice production (000 Tonnes)

iii) Sugarcane:

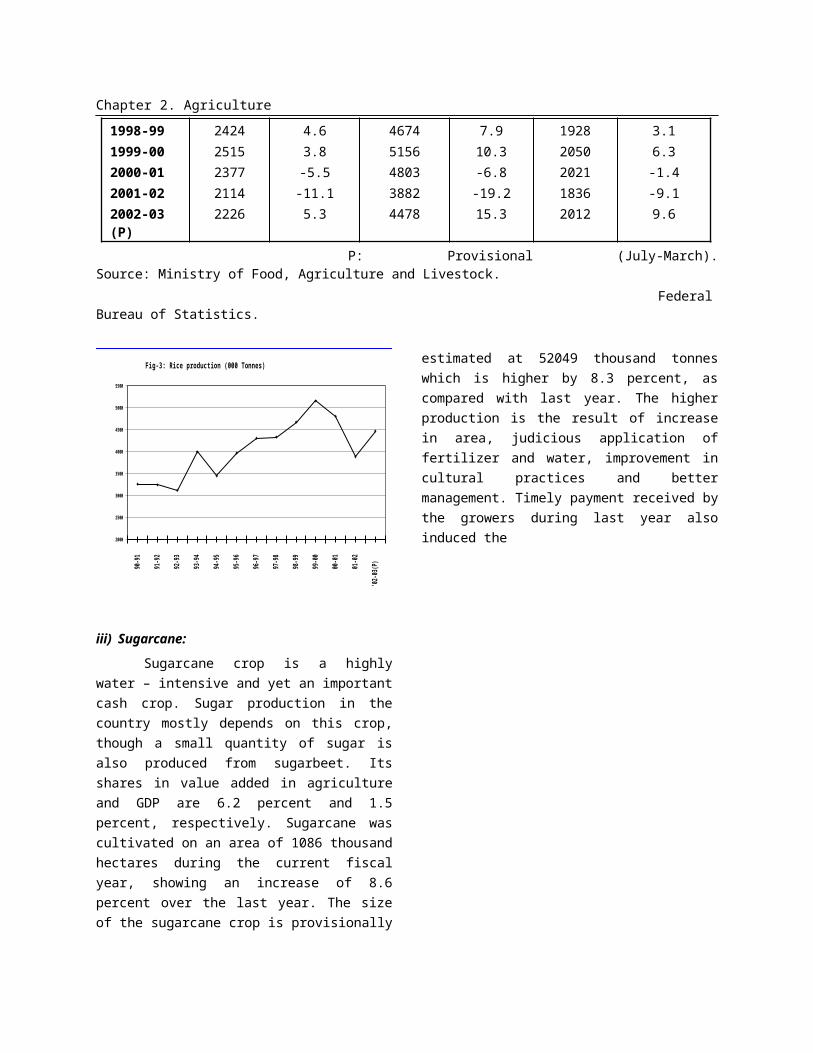

Sugarcane crop is a highly water – intensive and yet an important cash crop. Sugar production in the country mostly depends on this crop, though a small quantity of sugar is also produced from sugarbeet. Its shares in value added in agriculture and GDP are 6.2 percent and 1.5 percent, respectively. Sugarcane was cultivated on an area of 1086 thousand hectares during the current fiscal year, showing an increase of 8.6 percent over the last year. The size of the sugarcane crop is provisionally estimated at 52049 thousand tonnes which is higher by 8.3 percent, as compared with last year. The higher production is the result of increase in area, judicious application of fertilizer and water, improvement in cultural practices and better management. Timely payment received by the growers during last year also induced the

farmers to grow more sugarcane. The area, production and yield per hectare for the last five years are given in Table 2.5.

Table 2.5Area, Production and Yield of Sugarcane

Year Area Production Yield(000

Hectare%

Change(000

Tonnes)%

Change(Kgs/Hec.) %

Change1998-991999-002000-012001-022002-03 (P)

11551010961

10001086

9.4-12.6-4.94.18.6

5519146333436064804252049

3.9-16.0-5.910.28.3

4778445874453764804247927

-5.0-3.9-1.15.9-0.2

Chapter 2. AgricultureP: Provisional. (July-March) Source: Ministry of Food, Agriculture and Livestock.

Federal Bureau of Statistics.90

-91

91-9

2

92-9

3

93-9

4

94-9

5

95-9

6

96-9

7

97-9

8

98-9

9

99-0

0

00-0

1

01-0

2

'02-

03(P

)

30000

35000

40000

45000

50000

55000

60000

Fig-4: Sugarcane production (000 Tonnes)

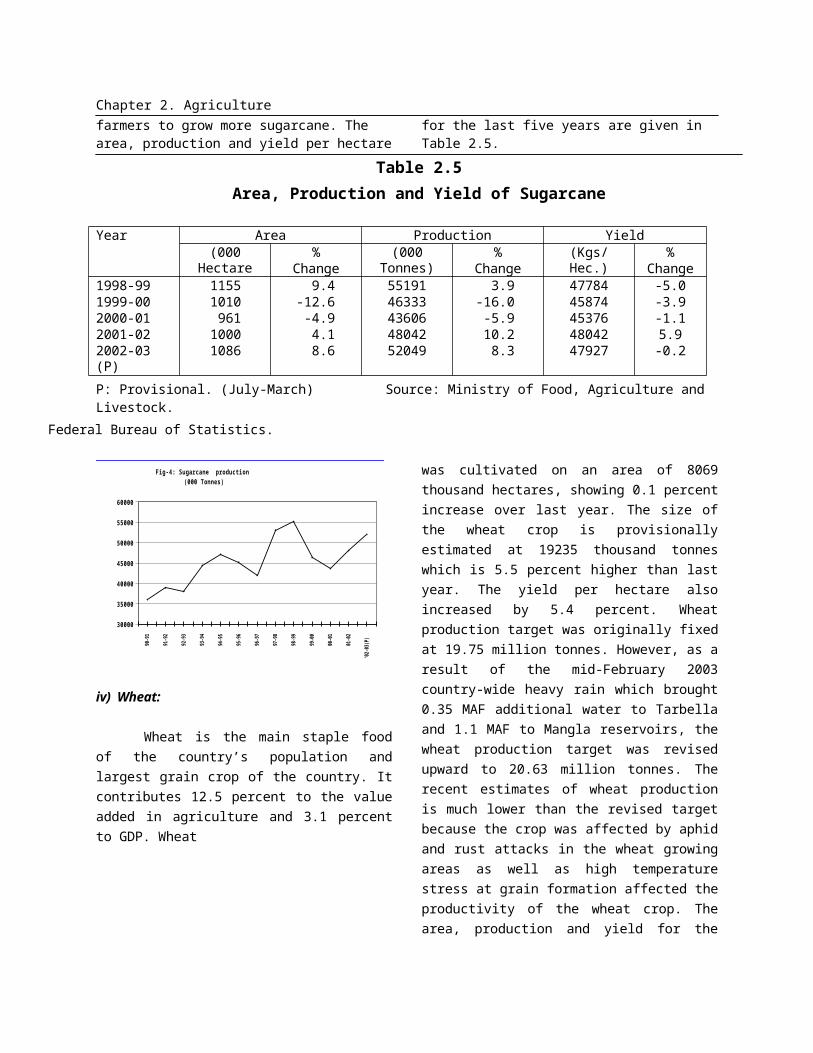

iv) Wheat:

Wheat is the main staple food of the country’s population and largest grain crop of the country. It contributes 12.5 percent to the value added in agriculture and 3.1 percent to GDP. Wheat

was cultivated on an area of 8069 thousand hectares, showing 0.1 percent increase over last year. The size of the wheat crop is provisionally estimated at 19235 thousand tonnes which is 5.5 percent higher than last year. The yield per hectare also increased by 5.4 percent. Wheat production target was originally fixed at 19.75 million tonnes. However, as a result of the mid-February 2003 country-wide heavy rain which brought 0.35 MAF additional water to Tarbella and 1.1 MAF to Mangla reservoirs, the wheat production target was revised upward to 20.63 million tonnes. The recent estimates of wheat production is much lower than the revised target because the crop was affected by aphid and rust attacks in the wheat growing areas as well as high temperature stress at grain formation affected the productivity of the wheat crop. The area, production and yield for the last five years are given in Table 2.6.

Table 2.6Area, Production and Yield of Wheat

YearArea Production Yield

(000 hectares)

%Change

(000 tonnes)

%Change

(Kgs/Hec.) % Changes

1998-991999-002000-012001-022002-03 (P)

82308463818180588069

-1.52.8

-3.3-1.50.1

1785821079190241822719235

-4.518.0-9.7-4.25.5

21702491232522622384

-3.014.8-6.7-2.75.4

P= Provisional.(July-March). Source: Ministry of Food, Agriculture and Livestock. Federal Bureau of Statistics

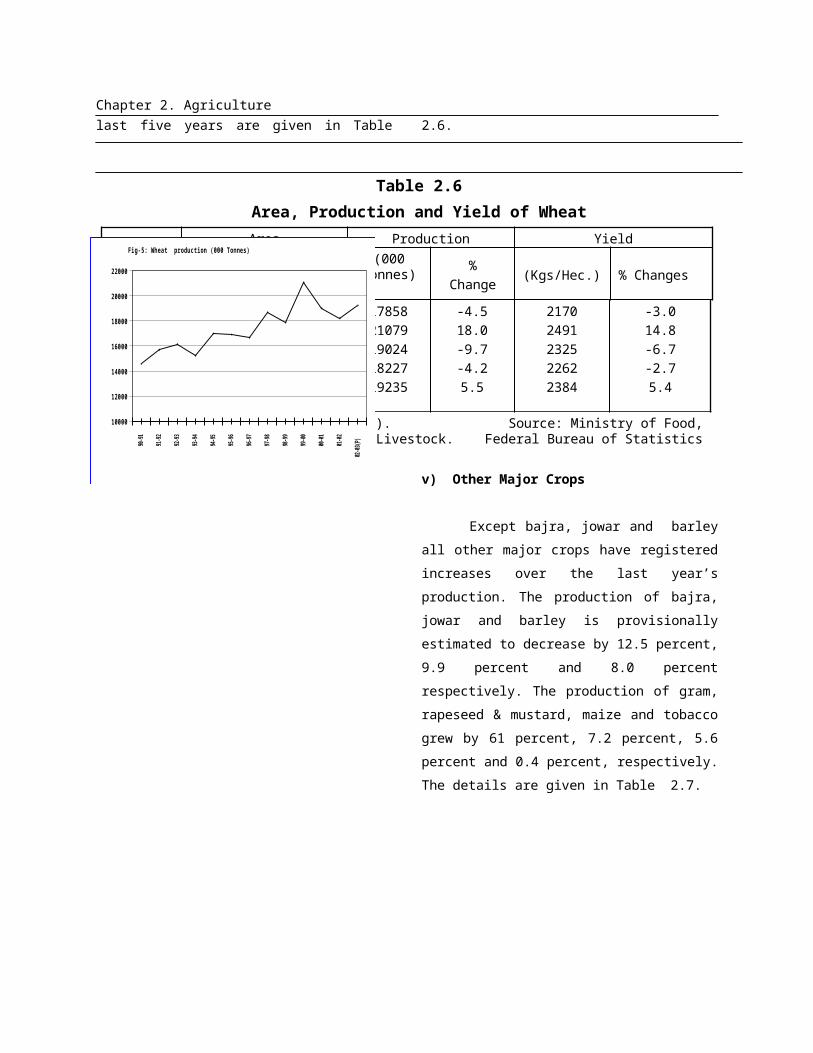

Chapter 2. Agriculturev) Other Major Crops

Except bajra, jowar and barley all

other major crops have registered increases

over the last year’s production. The

production of bajra, jowar and barley is

provisionally estimated to decrease by 12.5

percent, 9.9 percent and 8.0 percent

respectively. The production of gram,

rapeseed & mustard, maize and tobacco

grew by 61 percent, 7.2 percent, 5.6 percent

and 0.4 percent, respectively. The details

are given in Table 2.7.

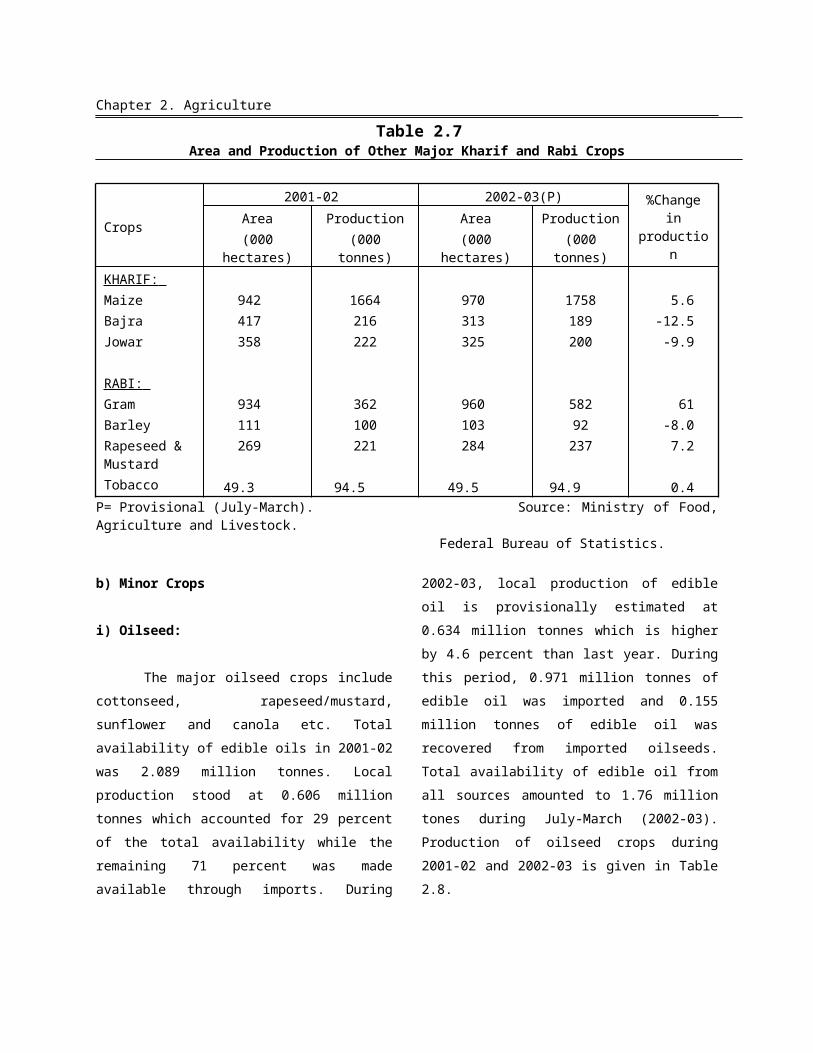

Table 2.7Area and Production of Other Major Kharif and Rabi Crops

Crops

2001-02 2002-03(P) %Change

in production

Area(000

hectares)Production

(000 tonnes)Area

(000 hectares)

Production(000

tonnes)KHARIF: MaizeBajraJowar

RABI: GramBarleyRapeseed & MustardTobacco

942417358

934111269

49.3

1664216222

362100221

94.5

970313325

960103284

49.5

1758189200

58292237

94.9

5.6-12.5-9.9

61-8.07.2

0.4P= Provisional (July-March). Source: Ministry of Food, Agriculture and Livestock. Federal Bureau of Statistics.

b) Minor Crops

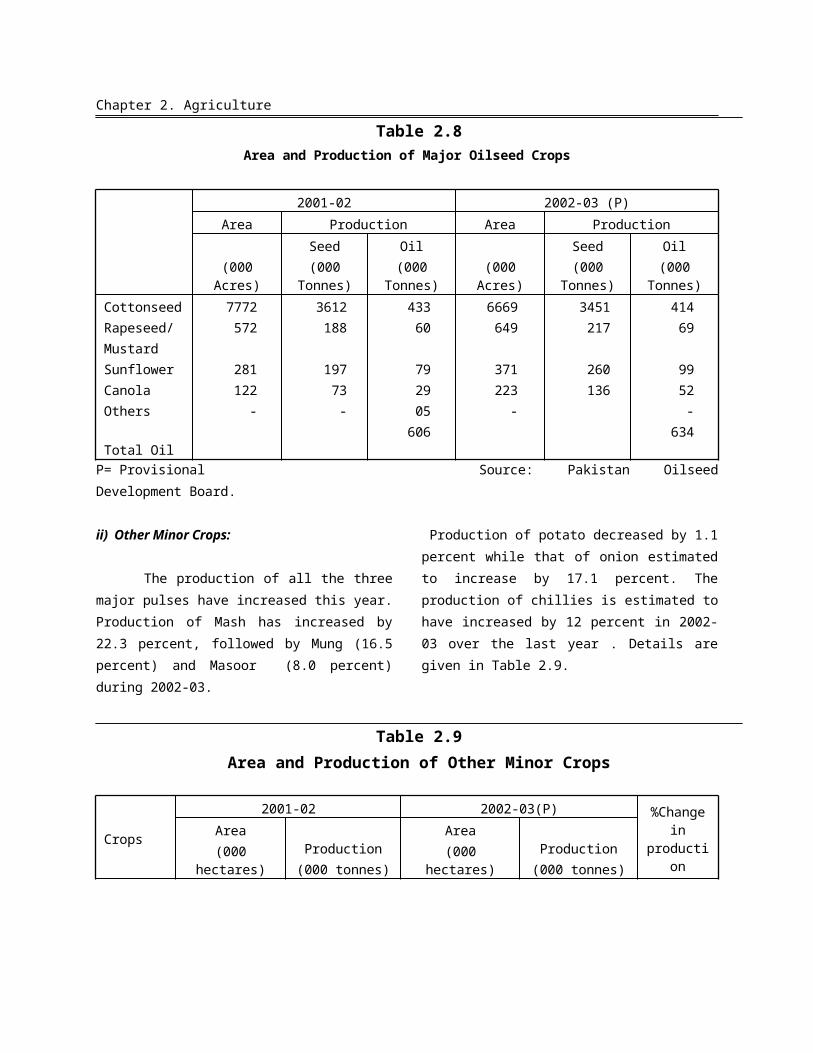

i) Oilseed:

The major oilseed crops include

cottonseed, rapeseed/mustard, sunflower

and canola etc. Total availability of edible oils

in 2001-02 was 2.089 million tonnes. Local

production stood at 0.606 million tonnes

which accounted for 29 percent of the total

availability while the remaining 71 percent

was made available through imports. During

2002-03, local production of edible oil is

provisionally estimated at 0.634 million

90-91

91-92

92-93

93-94

94-95

95-96

96-97

97-98

98-99

99-00

00-01

01-02

02-03

(P)

10000

12000

14000

16000

18000

20000

22000

Fig-5: Wheat production (000 Tonnes)

Chapter 2. Agriculturetonnes which is higher by 4.6 percent than

last year. During this period, 0.971 million

tonnes of edible oil was imported and 0.155

million tonnes of edible oil was recovered

from imported oilseeds. Total availability of

edible oil from all sources amounted to 1.76

million tones during July-March (2002-03).

Production of oilseed crops during 2001-02

and 2002-03 is given in Table 2.8.

Table 2.8Area and Production of Major Oilseed Crops

2001-02 2002-03 (P)Area Production Area Production

(000 Acres)

Seed(000

Tonnes)

Oil(000

Tonnes)(000

Acres)

Seed(000

Tonnes)

Oil(000

Tonnes)CottonseedRapeseed/MustardSunflowerCanolaOthers Total Oil

7772572

281122

-

3612188

19773

-

43360

792905

606

6669649

371223

-

3451217

260136

41469

9952

-634

P= Provisional Source: Pakistan Oilseed Development Board.

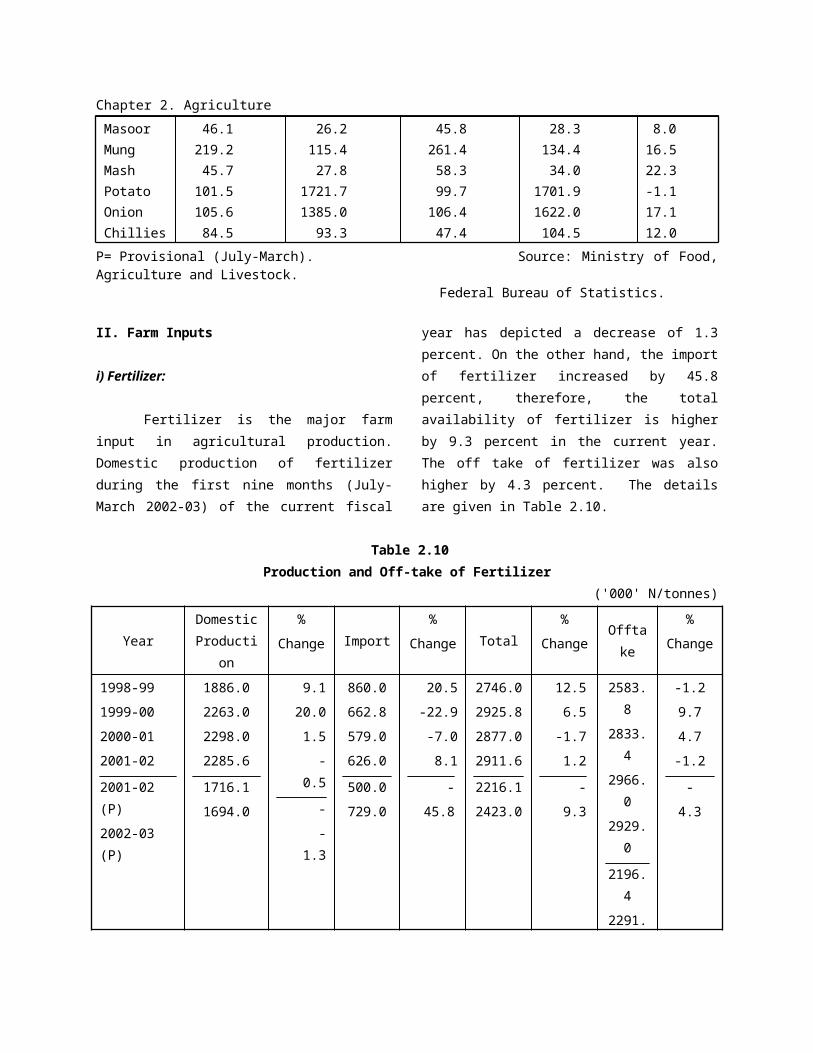

ii) Other Minor Crops:

The production of all the three major pulses have increased this year. Production of Mash has increased by 22.3 percent, followed by Mung (16.5 percent) and Masoor (8.0 percent) during 2002-03.

Production of potato decreased by 1.1 percent while that of onion estimated to increase by 17.1 percent. The production of chillies is estimated to have increased by 12 percent in 2002-03 over the last year . Details are given in Table 2.9.

Table 2.9Area and Production of Other Minor Crops

Crops

2001-02 2002-03(P) %Change in

production

Area(000

hectares)Production

(000 tonnes)Area

(000 hectares)Production

(000 tonnes)MasoorMungMashPotatoOnion

46.1219.245.7

101.5105.6

26.2115.427.8

1721.71385.0

45.8261.458.399.7

106.4

28.3134.434.0

1701.91622.0

8.016.522.3-1.117.1

Chapter 2. Agriculture

Chillies 84.5 93.3 47.4 104.5 12.0

P= Provisional (July-March). Source: Ministry of Food, Agriculture and Livestock. Federal Bureau of Statistics.

II. Farm Inputs

i) Fertilizer:

Fertilizer is the major farm input in agricultural production. Domestic production of fertilizer during the first nine months (July-March 2002-03) of the current fiscal year has

depicted a decrease of 1.3 percent. On the other hand, the import of fertilizer increased by 45.8 percent, therefore, the total availability of fertilizer is higher by 9.3 percent in the current year. The off take of fertilizer was also higher by 4.3 percent. The details are given in Table 2.10.

Table 2.10Production and Off-take of Fertilizer

('000' N/tonnes)

YearDomestic Productio

n

%

Change

Import

%

Change Total

%

Change

Offtake

%

Change

1998-99

1999-00

2000-01

2001-02

2001-02 (P)

2002-03 (P)

1886.0

2263.0

2298.0

2285.6

1716.1

1694.0

9.1

20.0

1.5

-0.5

-

-1.3

860.0

662.8

579.0

626.0

500.0

729.0

20.5

-22.9

-7.0

8.1

-

45.8

2746.0

2925.8

2877.0

2911.6

2216.1

2423.0

12.5

6.5

-1.7

1.2

-

9.3

2583.8

2833.4

2966.0

2929.0

2196.4

2291.0

-1.2

9.7

4.7

-1.2

-

4.3

P= Provisional (July-March). Source: National Fertilizer Development Centre.

ii) Improved Seed:

Quality seed of improved varieties is the key to enhance agricultural productivity. Seed has the unique position among the various agricultural inputs because the effectiveness of all other inputs mainly depend on the production potential of seeds.

Federal Seed Certification & Registration Department regulates the quality during flow of seed from breeder to growers. The Department performs its functions through seventeen Seed Testing Laboratories and Field Offices, established in various ecological zones of the country.

Chapter 2. AgricultureTo provide certified crop seeds to the

growers in public sector, Seed Corporation in Punjab and Sindh, Departments of Agriculture in Baluchistan and NWFP have been entrusted the task of seed production, processing and marketing. In private sector 394 seed companies including five multinationals have been allowed for certified seed production, processing and marketing.

With the induction of private sector into seed business, improved seed availability has increased by 16.5 percent over the seed requirement in 2001-02. During (July-March) 2002-03, 197.5 thousand tones of improved seed was procured while 147.6 thousand tones of improved seed was distributed, which was 11.9 percent higher than the same period of 2001-02.

iii) Mechanization:

Pakistan food security and agriculture surpluses for export at competitive prices require efficient development and utilization of agricultural resources. Cost of production

of various crops are not competitive due to low productivity mainly due to inefficient farming practices. Farm operations being time specific, demand precision to optimize the efficiencies of agriculture inputs for higher productivity. The future challenges of free market economy and faster globalisation have further necessitated modernization of agricultural machinery through transfer of latest, efficient and cost effective technology to farming system. Efficient use of scarce agriculture resources and accelerated agriculture mechanization is, therefore, vital and demands for a comprehensive strategic planning for the future.

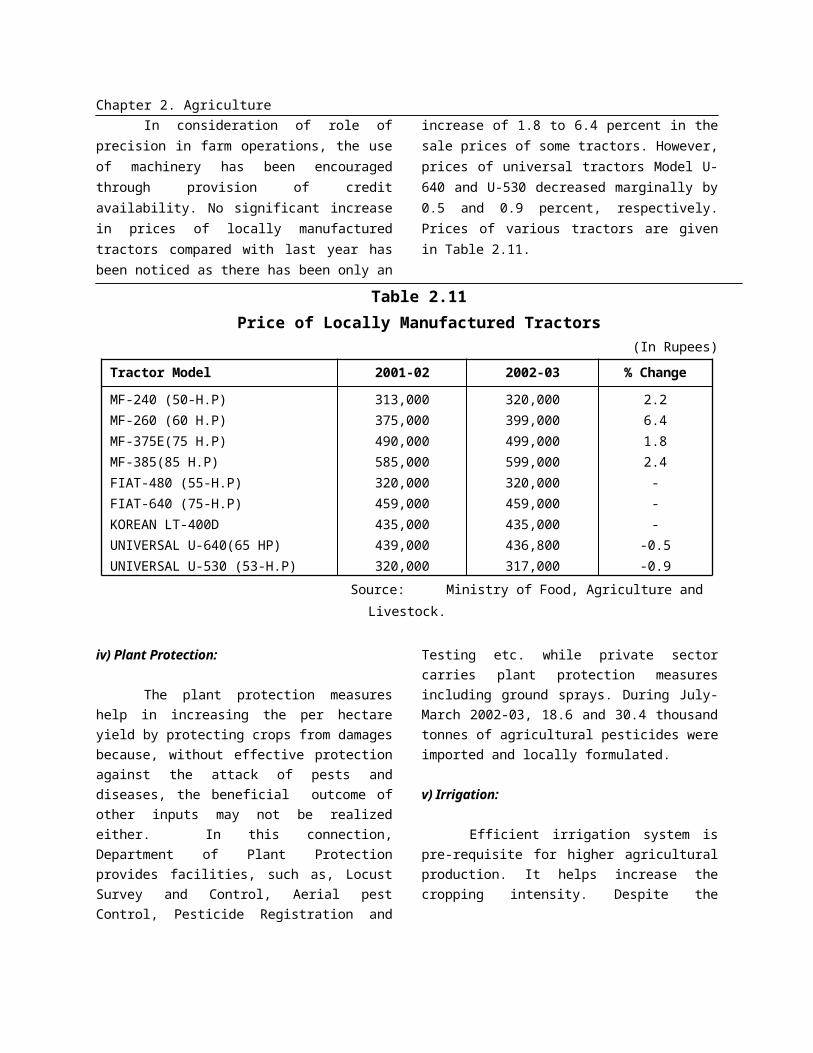

In consideration of role of precision in farm operations, the use of machinery has been encouraged through provision of credit availability. No significant increase in prices of locally manufactured tractors compared with last year has been noticed as there has been only an increase of 1.8 to 6.4 percent in the sale prices of some tractors. However, prices of universal tractors Model U-640 and U-530 decreased marginally by 0.5 and 0.9 percent, respectively. Prices of various tractors are given in Table 2.11.

Table 2.11Price of Locally Manufactured Tractors

(In Rupees)

Tractor Model 2001-02 2002-03 % Change

MF-240 (50-H.P)MF-260 (60 H.P)MF-375E(75 H.P)MF-385(85 H.P)FIAT-480 (55-H.P)FIAT-640 (75-H.P)KOREAN LT-400DUNIVERSAL U-640(65 HP)UNIVERSAL U-530 (53-H.P)

313,000375,000490,000585,000320,000459,000435,000439,000320,000

320,000399,000499,000599,000320,000459,000435,000436,800317,000

2.26.41.82.4---

-0.5-0.9

Source: Ministry of Food, Agriculture and Livestock.

iv) Plant Protection: The plant protection measures help in increasing the per hectare yield by protecting

Chapter 2. Agriculturecrops from damages because, without effective protection against the attack of pests and diseases, the beneficial outcome of other inputs may not be realized either. In this connection, Department of Plant Protection provides facilities, such as, Locust Survey and Control, Aerial pest Control, Pesticide Registration and Testing etc. while private sector carries plant protection measures including ground sprays. During July-March 2002-03, 18.6 and 30.4 thousand tonnes of agricultural pesticides were imported and locally formulated.

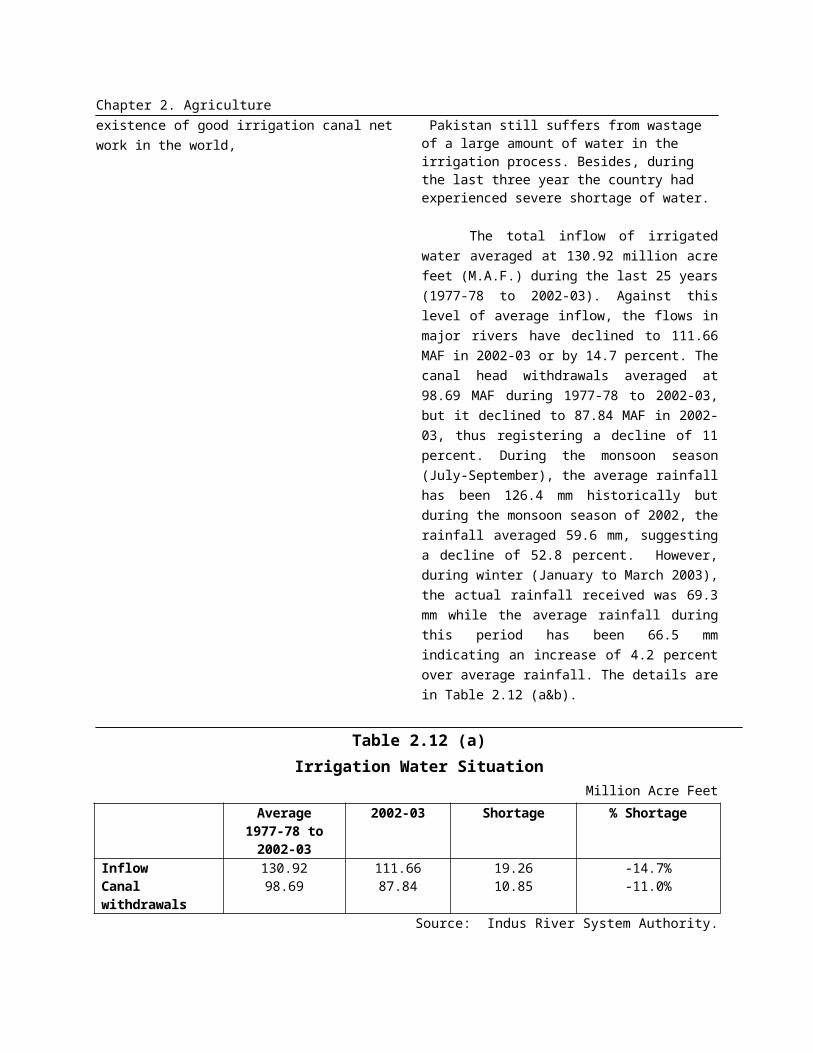

v) Irrigation:

Efficient irrigation system is pre-requisite for higher agricultural production. It helps increase the cropping intensity. Despite the existence of good irrigation canal net work in the world,

Pakistan still suffers from wastage of a large amount of water in the irrigation process. Besides, during the last three year the country had experienced severe shortage of water.

The total inflow of irrigated water averaged at 130.92 million acre feet (M.A.F.) during the last 25 years (1977-78 to 2002-03). Against this level of average inflow, the flows in major rivers have declined to 111.66 MAF in 2002-03 or by 14.7 percent. The canal head withdrawals averaged at 98.69 MAF during 1977-78 to 2002-03, but it declined to 87.84 MAF in 2002-03, thus registering a decline of 11 percent. During the monsoon season (July-September), the average rainfall has been 126.4 mm historically but during the monsoon season of 2002, the rainfall averaged 59.6 mm, suggesting a decline of 52.8 percent. However, during winter (January to March 2003), the actual rainfall received was 69.3 mm while the average rainfall during this period has been 66.5 mm indicating an increase of 4.2 percent over average rainfall. The details are in Table 2.12 (a&b).

Table 2.12 (a)Irrigation Water Situation

Million Acre FeetAverage

1977-78 to 2002-03

2002-03 Shortage % Shortage

InflowCanal withdrawals

130.9298.69

111.6687.84

19.2610.85

-14.7%-11.0%

Source: Indus River System Authority.

Chapter 2. Agriculture

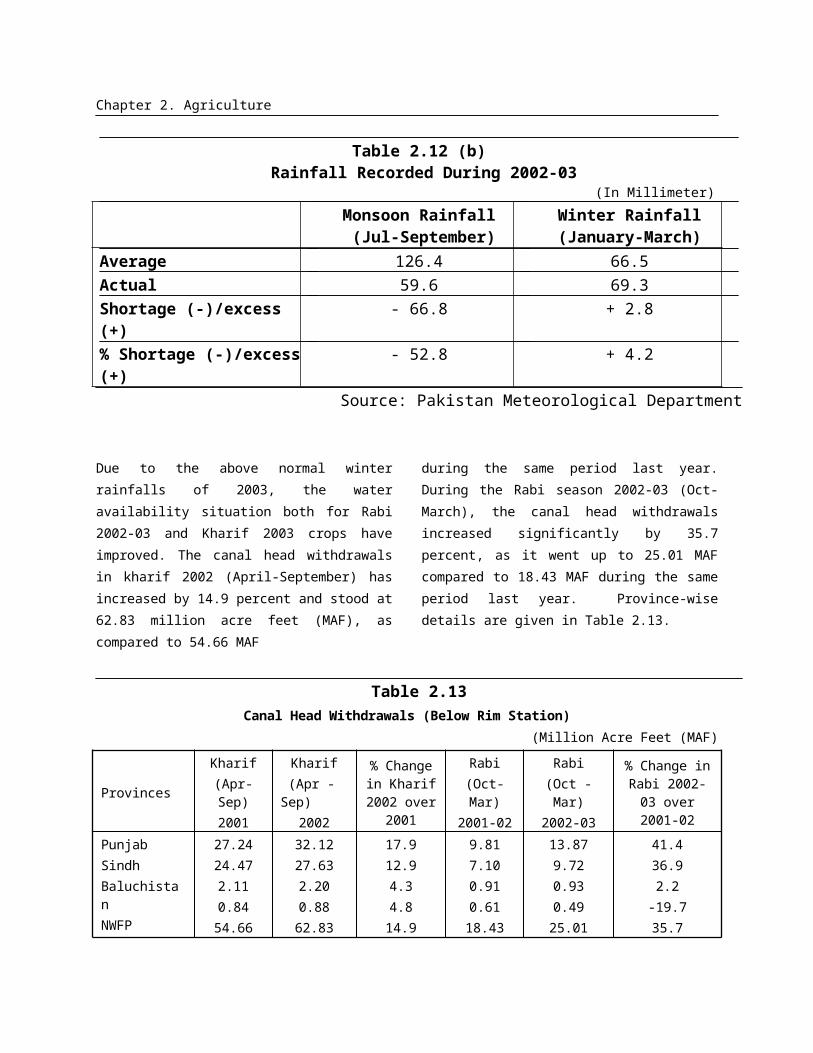

Table 2.12 (b) Rainfall Recorded During 2002-03

(In Millimeter)

Monsoon Rainfall (Jul-September)

Winter Rainfall (January-March)

Average 126.4 66.5Actual 59.6 69.3Shortage (-)/excess (+) - 66.8 + 2.8% Shortage (-)/excess (+)

- 52.8 + 4.2

Source: Pakistan Meteorological Department

Due to the above normal winter rainfalls of 2003, the water availability situation both for Rabi 2002-03 and Kharif 2003 crops have improved. The canal head withdrawals in kharif 2002 (April-September) has increased by 14.9 percent and stood at 62.83 million acre feet (MAF), as compared to 54.66 MAF

during the same period last year. During the Rabi season 2002-03 (Oct-March), the canal head withdrawals increased significantly by 35.7 percent, as it went up to 25.01 MAF compared to 18.43 MAF during the same period last year. Province-wise details are given in Table 2.13.

Table 2.13Canal Head Withdrawals (Below Rim Station)

(Million Acre Feet (MAF)

ProvincesKharif

(Apr-Sep)2001

Kharif (Apr -Sep)

2002

% Change in Kharif

2002 over 2001

Rabi(Oct-Mar)2001-02

Rabi(Oct -Mar)2002-03

% Change in Rabi 2002-03 over 2001-02

PunjabSindhBaluchistanNWFP (CRBC)Total

27.2424.472.110.8454.66

32.1227.632.200.8862.83

17.912.94.34.814.9

9.817.100.910.6118.43

13.879.720.930.4925.01

41.436.92.2

-19.735.7

Source: Indus River System Authority.

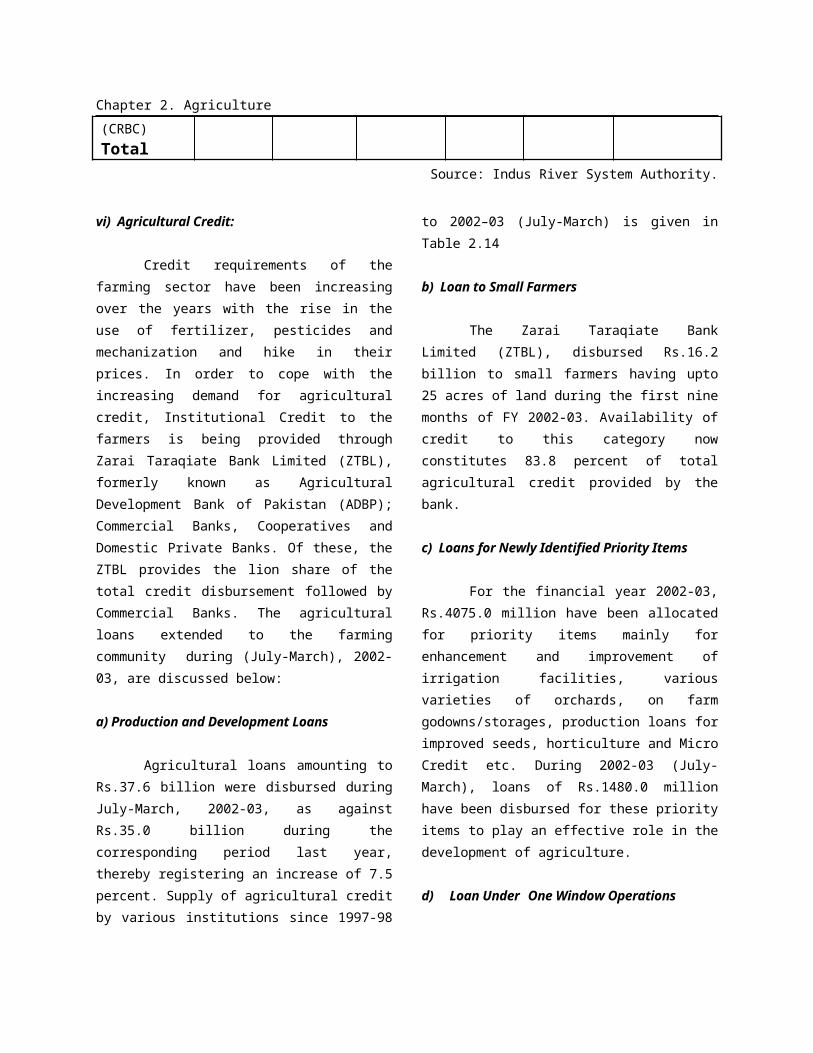

vi) Agricultural Credit:

Credit requirements of the farming sector have been increasing over the years with the rise in the use of fertilizer, pesticides and mechanization and hike in their prices. In order to cope with the increasing demand for

agricultural credit, Institutional Credit to the farmers is being provided through Zarai Taraqiate Bank Limited (ZTBL), formerly known as Agricultural Development Bank of Pakistan (ADBP); Commercial Banks, Cooperatives and Domestic Private Banks. Of these, the ZTBL provides the lion share of the

Chapter 2. Agriculturetotal credit disbursement followed by Commercial Banks. The agricultural loans extended to the farming community during (July-March), 2002-03, are discussed below:

a) Production and Development Loans

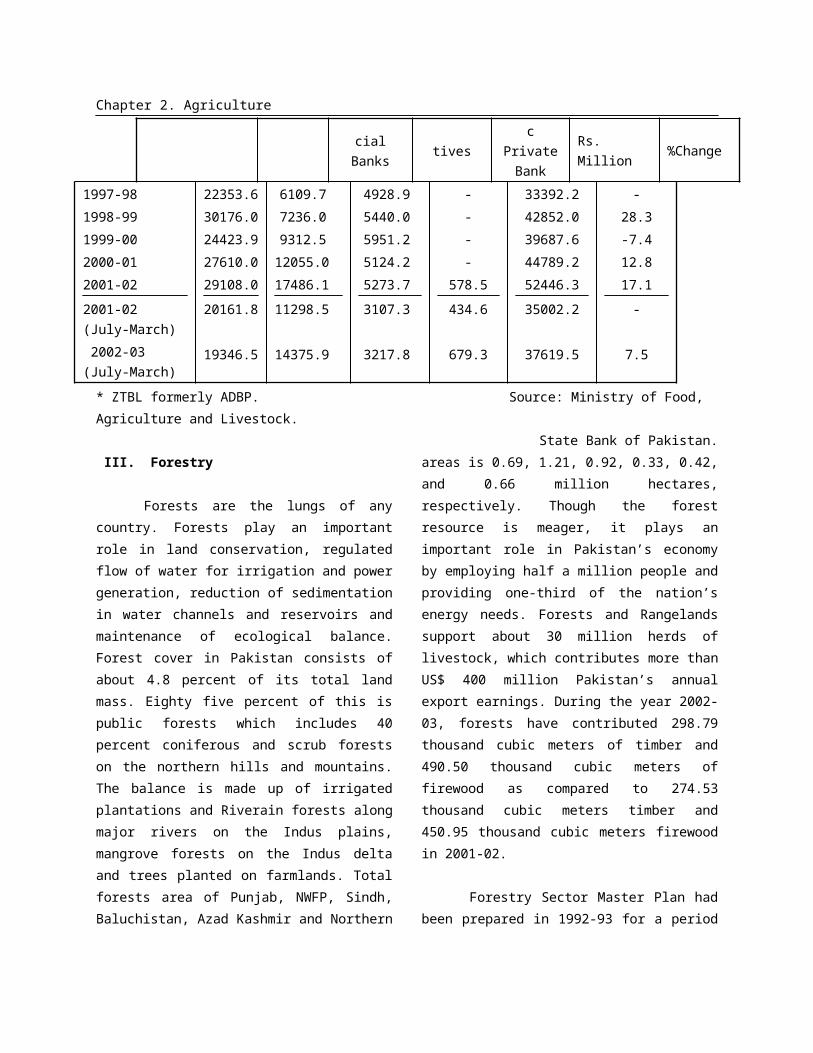

Agricultural loans amounting to Rs.37.6 billion were disbursed during July-March, 2002-03, as against Rs.35.0 billion during the corresponding period last year, thereby registering an increase of 7.5 percent. Supply of agricultural credit by various institutions since 1997-98 to 2002–03 (July-March) is given in Table 2.14

b) Loan to Small Farmers

The Zarai Taraqiate Bank Limited (ZTBL), disbursed Rs.16.2 billion to small farmers having upto 25 acres of land during the first nine months of FY 2002-03. Availability of credit to this category now constitutes 83.8 percent of total agricultural credit provided by the bank.

c) Loans for Newly Identified Priority Items

For the financial year 2002-03, Rs.4075.0 million have been allocated for priority items mainly for enhancement and improvement of irrigation facilities, various varieties of orchards, on farm godowns/storages, production loans for improved seeds, horticulture and Micro Credit etc. During 2002-03 (July-March), loans of Rs.1480.0 million have been disbursed for these priority items to play an effective role in the development of agriculture.

d) Loan Under One Window Operations

Since 1997, ZTBL has launched One

Chapter 2. AgricultureWindow Operation to provide credit facilities, particularly to small farmers, to cater for input requirements at their door step. Thus, during peak sowing season of both Rabi and Kharif Crops, One Window Operation is launched with the collaboration of Provincial Governments, Revenue Officials and Postal Authorities. Agriculture Pass Books are issued at spot to the intending borrowers, their land record is entered and loans are sanctioned at focal points whereas payments are released on the very next day from the concerned branch. During 2002-03 (July-March), loans of Rs.2565.6 million have been disbursed through One Window Operation.

e) Revolving Finance Scheme

Under this scheme, an annual loan limit is sanctioned to a borrower, based on his input credit requirements for both Rabi and Kharif Crops. This limit remains operative for a period of 3 years (six cropping season) without any afresh procedural requirement and documentation. Under this scheme Rs.7386.6 million was disbursed during (July-March) 2002-03. Thus 48% of total production loan i.e Rs.15374.6 million has been disbursed through this scheme.

Table 2.14Supply of Agricultural Credit by Institutions

(Rs. in million)

Year ZTBL*Commer-cial Banks

Coopera-tives

Domestic Private Bank

Total

Rs. Million %Change

1997-98

1998-99

1999-00

2000-01

2001-02

2001-02 (July-March)

2002-03 (July-March)

22353.6

30176.0

24423.9

27610.0

29108.0

20161.8

19346.5

6109.7

7236.0

9312.5

12055.0

17486.1

11298.5

14375.9

4928.9

5440.0

5951.2

5124.2

5273.7

3107.3

3217.8

-

-

-

-

578.5

434.6

679.3

33392.2

42852.0

39687.6

44789.2

52446.3

35002.2

37619.5

-

28.3

-7.4

12.8

17.1

-

7.5

* ZTBL formerly ADBP. Source: Ministry of Food, Agriculture and Livestock.

State Bank of Pakistan. III. Forestry

Forests are the lungs of any country. Forests play an important role in land conservation, regulated flow of water for irrigation and power generation, reduction of sedimentation in water channels and reservoirs and maintenance of ecological balance. Forest cover in Pakistan consists of about 4.8 percent of its total land mass.

Eighty five percent of this is public forests which includes 40 percent coniferous and scrub forests on the northern hills and mountains. The balance is made up of irrigated plantations and Riverain forests along major rivers on the Indus plains, mangrove forests on the Indus delta and trees planted on farmlands. Total forests area of Punjab, NWFP, Sindh, Baluchistan, Azad Kashmir and Northern areas is 0.69,

Chapter 2. Agriculture1.21, 0.92, 0.33, 0.42, and 0.66 million hectares, respectively. Though the forest resource is meager, it plays an important role in Pakistan’s economy by employing half a million people and providing one-third of the nation’s energy needs. Forests and Rangelands support about 30 million herds of livestock, which contributes more than US$ 400 million Pakistan’s annual export earnings. During the year 2002-03, forests have contributed 298.79 thousand cubic meters of timber and 490.50 thousand cubic meters of firewood as compared to 274.53 thousand cubic meters timber and 450.95 thousand cubic meters firewood in 2001-02.

Forestry Sector Master Plan had been prepared in 1992-93 for a period of 25 years which is being updated through Asian Development Bank assisted project. Forestry data is being updated through field oriented studies which will be useful in future strategic planning for the Development of forestry in the country. Tree planting campaigns are launched every year in the spring and monsoon season. During spring and monsoon season year 2002, 106.46 million saplings (Spring 66.75 and Monsoon 39.71 million) were planted.

In order to promote efficient utilization and assessment to recover the full utilization of goods and services provided by the forests, Government of Pakistan has prepared National Forest Policy 2002 which covers all renewable natural resources i.e. forests, watersheds, rangelands, biodiversity and their habitats. The policy envisages to eliminate the fundamental causes of forests depletion through active participation of all the stakeholders. The goal of this national forest policy is to foster sustainable development of natural resources, rehabilitation of its environment and

enhancement of sustainable livelihoods of communities.

A mega project in forestry sector named “Rachna Doab Afforestation Project” was started in July 1995 at a cost of Rs.485.4 million. The main objective of this project is afforestation for the purpose of camouflage and concealment which is very important for strategic point of view. During 2002-03, Rs.60.0 million were allocated to conclude the on-going activities towards achievements of afforestation targets.

Tarbela Watershed Management Project sponsored by the Ministry of Environment is an on-going project at a total cost of Rs.689.0 million, to which Rs.34.188 million were allocated during FY 2002-03.The main objectives of the project include; soil and water conservation, extension of forests, appropriate land use, improvement of environment and uplift of socio-economic conditions of people. During the fiscal year 2002-03, 14.5 acres of nurseries have been raised, 2576 acres planted, 7,086 acres afforestation maintained and 27 management/utilization plans have been prepared with the total expenditure of Rs.23.932 million till March, 2003.

IV. Livestock and Poultry

a) Livestock

Livestock is an important sector of agriculture in Pakistan, which accounts for 39 percent of agricultural value added and about 9.4 percent of the GDP. Its net foreign exchange earnings were to the tune of Rs.51.5 billion in 2001-02, which is almost 11.4 percent of the overall export earnings of the country. The role of livestock in rural economy may be realized from the fact that

Chapter 2. Agriculture30-35 million rural population is engaged in livestock raising, having household holdings of 2-3 cattle/buffalo and 5-6 sheep/goat per family

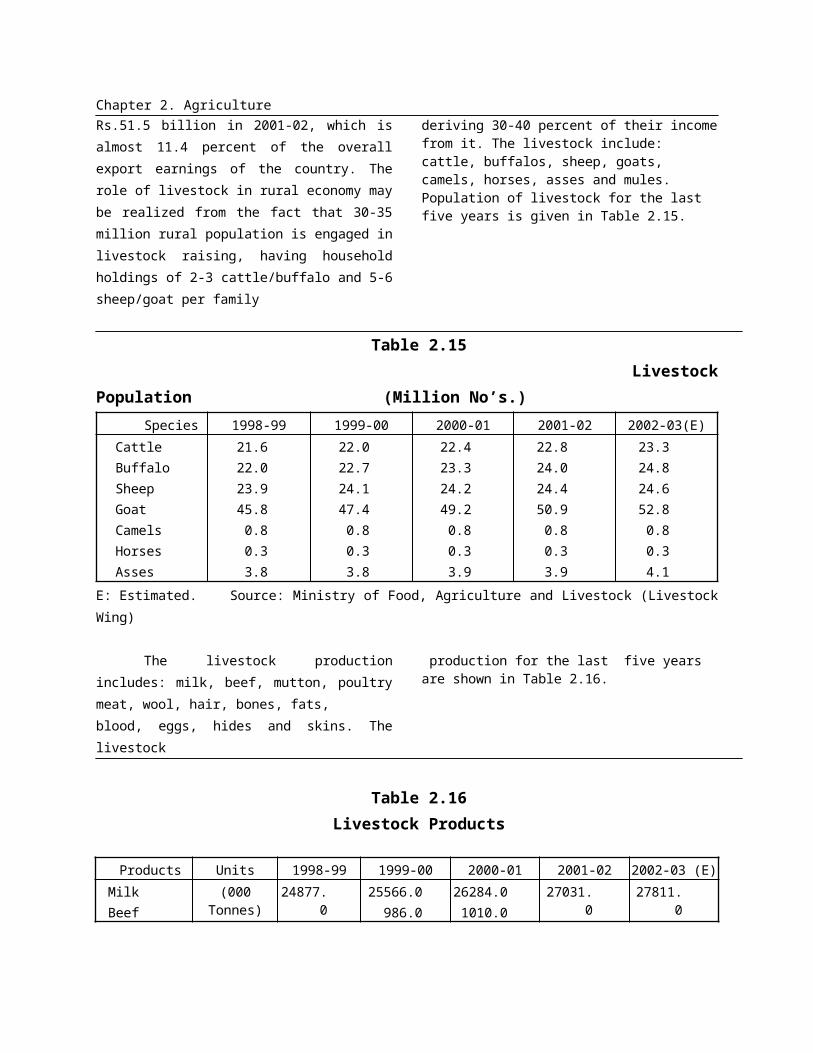

deriving 30-40 percent of their income from it. The livestock include: cattle, buffalos, sheep, goats, camels, horses, asses and mules. Population of livestock for the last five years is given in Table 2.15.

Table 2.15 Livestock Population (Million No’s.)

Species 1998-99 1999-00 2000-01 2001-02 2002-03(E)CattleBuffaloSheepGoatCamelsHorsesAsses

21.622.023.945.80.80.33.8

22.022.724.147.40.80.33.8

22.423.324.249.20.80.33.9

22.824.024.450.90.80.33.9

23.324.824.652.80.80.34.1

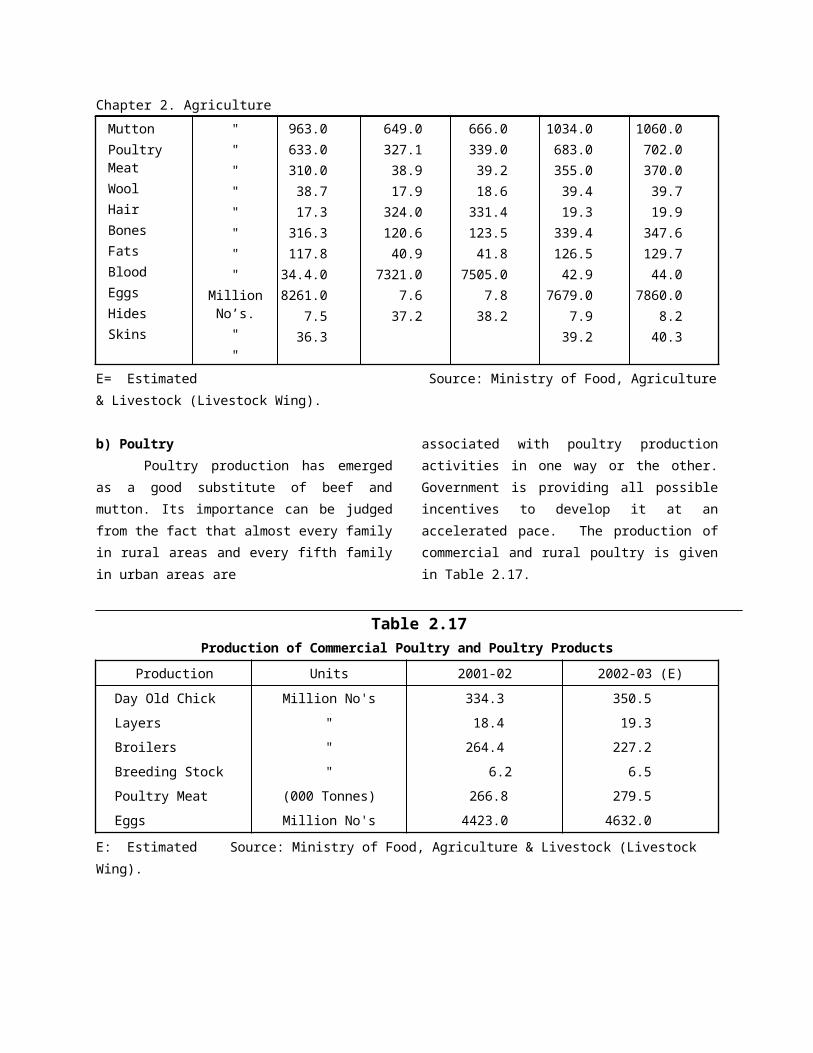

E: Estimated. Source: Ministry of Food, Agriculture and Livestock (Livestock Wing)

The livestock production includes: milk, beef, mutton, poultry meat, wool, hair, bones, fats,blood, eggs, hides and skins. The livestock

production for the last five years are shown in Table 2.16.

Table 2.16Livestock Products

Products Units 1998-99 1999-00 2000-01 2001-02 2002-03 (E)MilkBeefMuttonPoultry MeatWoolHairBonesFatsBloodEggsHidesSkins

(000 Tonnes)

""""""""

Million No’s.""

24877.0

963.0633.0310.038.717.3

316.3117.834.4.08261.0

7.536.3

25566.0986.0649.0327.138.917.9

324.0120.640.9

7321.07.6

37.2

26284.01010.0666.0339.039.218.6

331.4123.541.8

7505.07.8

38.2

27031.0

1034.0683.0355.039.419.3

339.4126.542.9

7679.07.9

39.2

27811.0

1060.0702.0370.039.719.9

347.6129.744.0

7860.08.2

40.3

E= Estimated Source: Ministry of Food, Agriculture & Livestock (Livestock Wing).

Chapter 2. Agricultureb) Poultry

Poultry production has emerged as a good substitute of beef and mutton. Its importance can be judged from the fact that almost every family in rural areas and every fifth family in urban areas are

associated with poultry production activities in one way or the other. Government is providing all possible incentives to develop it at an accelerated pace. The production of commercial and rural poultry is given in Table 2.17.

Table 2.17Production of Commercial Poultry and Poultry Products

Production Units 2001-02 2002-03 (E)

Day Old Chick

Layers

Broilers

Breeding Stock

Poultry Meat

Eggs

Million No's

"

"

"

(000 Tonnes)

Million No's

334.3

18.4

264.4

6.2

266.8

4423.0

350.5

19.3

227.2

6.5

279.5

4632.0

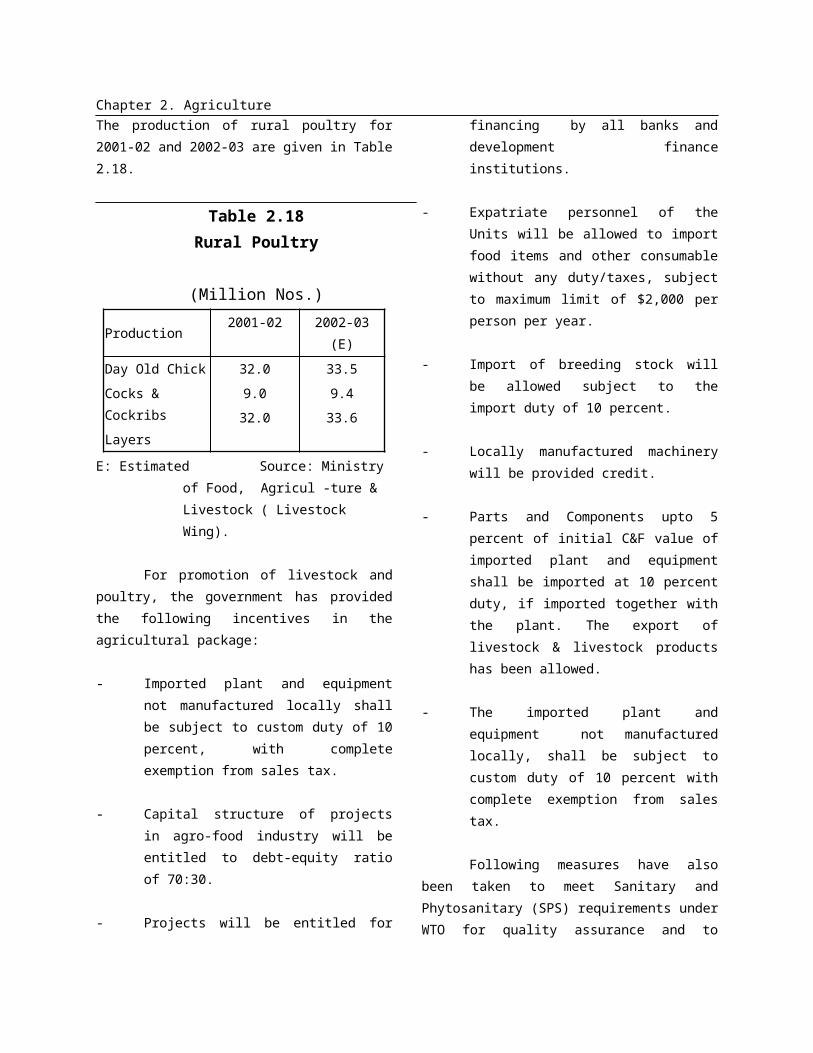

E: Estimated Source: Ministry of Food, Agriculture & Livestock (Livestock Wing). The production of rural poultry for 2001-02 and 2002-03 are given in Table 2.18.

Table 2.18Rural Poultry

(Million Nos.)

Production 2001-02 2002-03 (E)

Day Old Chick

Cocks & Cockribs

Layers

32.0

9.0

32.0

33.5

9.4

33.6

E: Estimated Source: Ministry of Food, Agricul -ture & Livestock ( Livestock Wing).

For promotion of livestock and poultry, the government has provided the following incentives in the agricultural package:

- Imported plant and equipment not manufactured locally shall be subject

to custom duty of 10 percent, with complete exemption from sales tax.

- Capital structure of projects in agro-food industry will be entitled to debt-equity ratio of 70:30.

- Projects will be entitled for financing by all banks and development finance institutions.

- Expatriate personnel of the Units will be allowed to import food items and other consumable without any duty/taxes, subject to maximum limit of $2,000 per person per year.

- Import of breeding stock will be allowed subject to the import duty of 10 percent.

- Locally manufactured machinery will be provided credit.

- Parts and Components upto 5 percent

Chapter 2. Agricultureof initial C&F value of imported plant and equipment shall be imported at 10 percent duty, if imported together with the plant. The export of livestock & livestock products has been allowed.

- The imported plant and equipment not manufactured locally, shall be subject to custom duty of 10 percent with complete exemption from sales tax.

Following measures have also been taken to meet Sanitary and Phytosanitary (SPS) requirements under WTO for quality assurance and to improve exports of livestock and livestock products:

- Establishment of abattoirs are encouraged in the private sector;

- The National Veterinary Laboratory is under construction for drug residue testing in the livestock products. This will ensure quality in exported products;

- Steps have been taken to improve sanitary and hygiene conditions of animal casing processing units in the country;

- A project titled ‘Strengthening of

Veterinary Services in Pakistan – Rinderpest Eradication

Program” has been launched during the fiscal year 2002-03.

V. Fisheries

Fishery plays an important role in Pakistan's economy and is considered to be an important source of livelihood for the coastal inhabitants. Apart from marine fisheries, inland fisheries (comprising of

rivers, lakes, ponds, dams etc) are also very important source of animal protein. Fisheries' share in GDP, though very little contributes substantially to the national income through export earnings. During the period July-March 2002-03, 58356 m. tonnes valued at Rs.5.2 billion fish and fishery products were estimated to be exported to Japan, USA, UK, Germany, Middle East, Sri Lanka, China etc. During the same period,

Chapter 2. Agriculturethe total fish production is estimated at 665,850 m. tonnes. Of which, share of marine sector is 480,000 m. tonnes and inland contribution is 185,850 m. tonnes.

The Government is taking a number of steps to improve fisheries sector. A number of initiatives are also being taken by the Federal and Provincial Fisheries Departments which, inter-alia, include strengthening of extension services, diversification of fishing efforts, development of value added products, enhancement of per capita consumption and up-gradation of socio-economic condition of the fishermen's community. Marine Fisheries Department is

also executing a project, namely, "Establishment of a Hatchery Complex for Production of Fish/Shrimp Seeds" which will play a vital role for the development of fish/ shrimp farming.

The total number of persons engaged in fisheries sector during 2002-03 is estimated at 365,000. Out of which, 138,000 persons (37.8 percent) were engaged in marine sector and 227,000 persons (62.2 percent) in inland fisheries, whereas the persons engaged in fisheries sector in 2001-02 were 363,000 persons137,000 (37.7 percent) in marine and 226,000 (62.3 percent) in inland fisheries.

_____________________________

Chapter 3. Manufacturing Mining and Investment Policies

3.Manufacturing, Mining and Investment Policies

Manufacturing sector is the second largest individual sector of the economy accounting for 18 percent of the Gross Domestic Product (GDP). The activity in the manufacturing sector is comprised of large-scale and small & medium manufacturing sector. The performance of this very important sector in general and large-scale manufacturing in particular, has been lackluster at best in 1990s owing to host of problems like tariff reforms and escalating utility prices. In the backdrop of higher growth of 8.2 percent in the 1980s, the growth rate of 4.0 percent in 1990s was disappointing. Fiscal year 2002-03 besides 2000-01 has become the best performing year for manufacturing sector since 1987-88. This year has seen manufacturing registering a stellar growth of 7.7 percent with major contribution coming from large-scale manufacturing which recorded 8.7 percent growth. The industry seems to have adjusted itself with the challenges emanated from trade and tariff rationalization of the 1990s and increased input cost due to escalating utility tariff.

The large-scale manufacturing was originally targeted to grow by 6.5 percent in 2002-03 but the target was surpassed by a wide margin. Pakistan’s overall manufacturing sector registered a growth of 7.7 percent and large-scale manufacturing grew by 8.7 percent during the current fiscal year. The improvement in the domestic demand and better macroeconomic environment have caused in significant turnaround in the manufacturing sector.

The turnaround in the large-scale manufacturing which started in 2000-01 continued to exhibit a rising trend barring brief interval in the last fiscal years (October ,November and February 2001-02). The events of September 11 and their aftermath adversely affected the performance of this sector during this period. With the exception of these three months the growth performance depicted smart recovery during the last three years. One of the significant development in the current fiscal year has been that the growth is broad-based and touched almost all industrial groups.

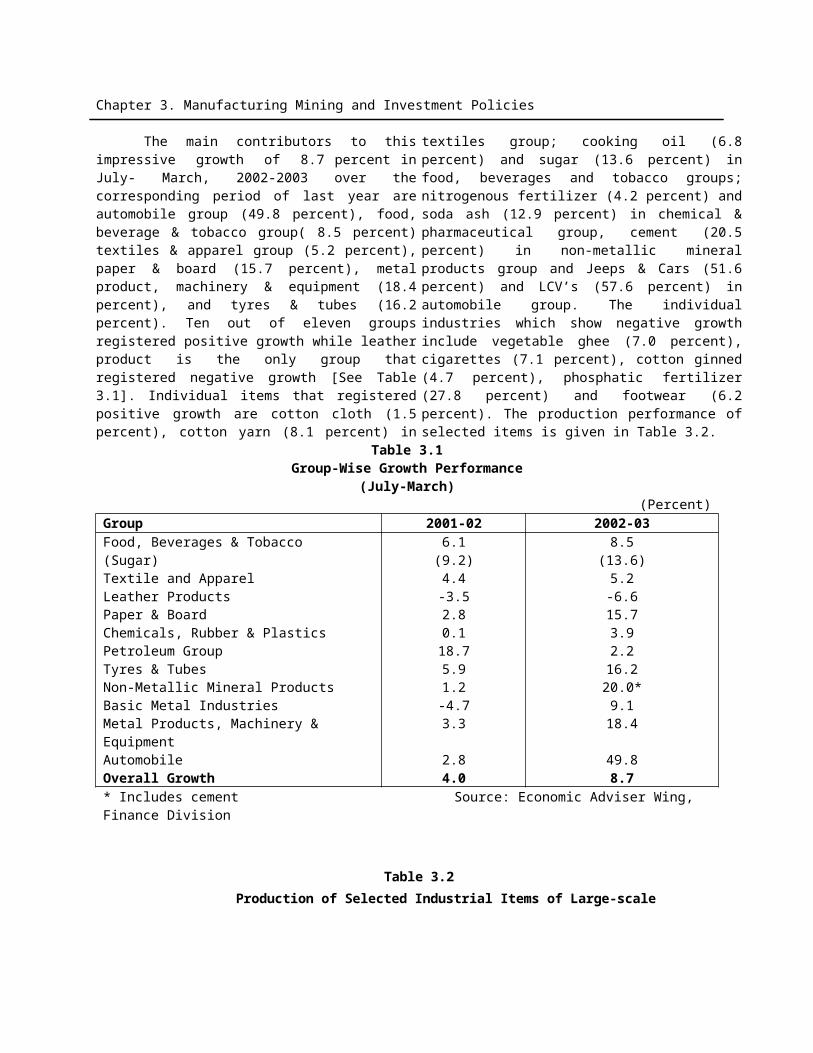

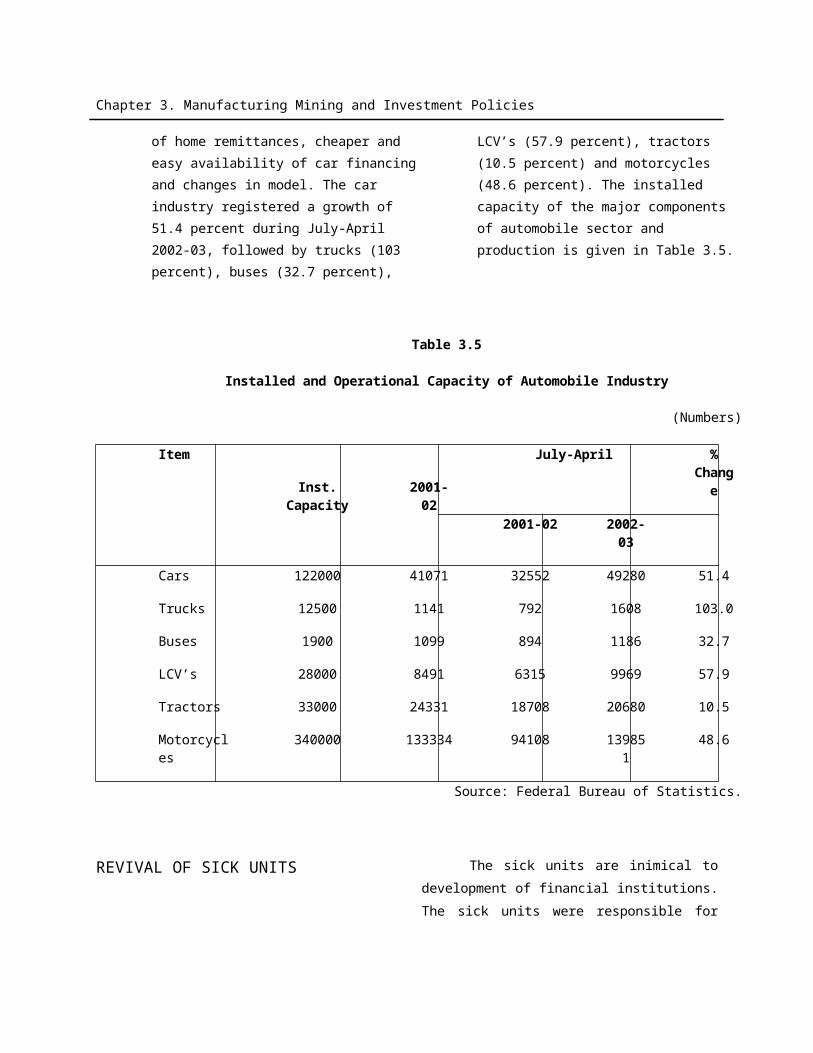

The main contributors to this impressive growth of 8.7 percent in July- March, 2002-2003 over the corresponding period of last year are automobile group (49.8 percent), food, beverage & tobacco group( 8.5 percent) textiles & apparel group (5.2 percent), paper & board (15.7 percent), metal product, machinery & equipment (18.4 percent), and tyres & tubes (16.2 percent). Ten out of eleven groups registered positive growth while leather product is the only group that registered negative growth [See Table 3.1]. Individual items that registered positive growth are cotton cloth (1.5 percent), cotton yarn (8.1 percent) in textiles group; cooking oil (6.8 percent) and sugar (13.6 percent) in food, beverages and tobacco groups; nitrogenous fertilizer (4.2 percent) and soda ash (12.9 percent) in chemical & pharmaceutical group, cement (20.5 percent) in non-metallic mineral products group and Jeeps & Cars (51.6 percent) and LCV’s (57.6 percent) in automobile group. The individual industries which show negative growth include vegetable ghee (7.0 percent), cigarettes (7.1 percent), cotton ginned (4.7 percent), phosphatic fertilizer (27.8 percent) and footwear (6.2 percent). The production performance of selected items is given in Table 3.2.

Table 3.1Group-Wise Growth Performance

(July-March)(Percent)

Group 2001-02 2002-03Food, Beverages & Tobacco 6.1 8.5(Sugar) (9.2) (13.6)Textile and Apparel 4.4 5.2Leather Products -3.5 -6.6Paper & Board 2.8 15.7

Chapter 3. Manufacturing Mining and Investment Policies

Chemicals, Rubber & Plastics 0.1 3.9Petroleum Group 18.7 2.2Tyres & Tubes 5.9 16.2Non-Metallic Mineral Products 1.2 20.0*Basic Metal Industries -4.7 9.1Metal Products, Machinery & Equipment 3.3 18.4Automobile 2.8 49.8Overall Growth 4.0 8.7* Includes cement Source: Economic Adviser Wing, Finance Division

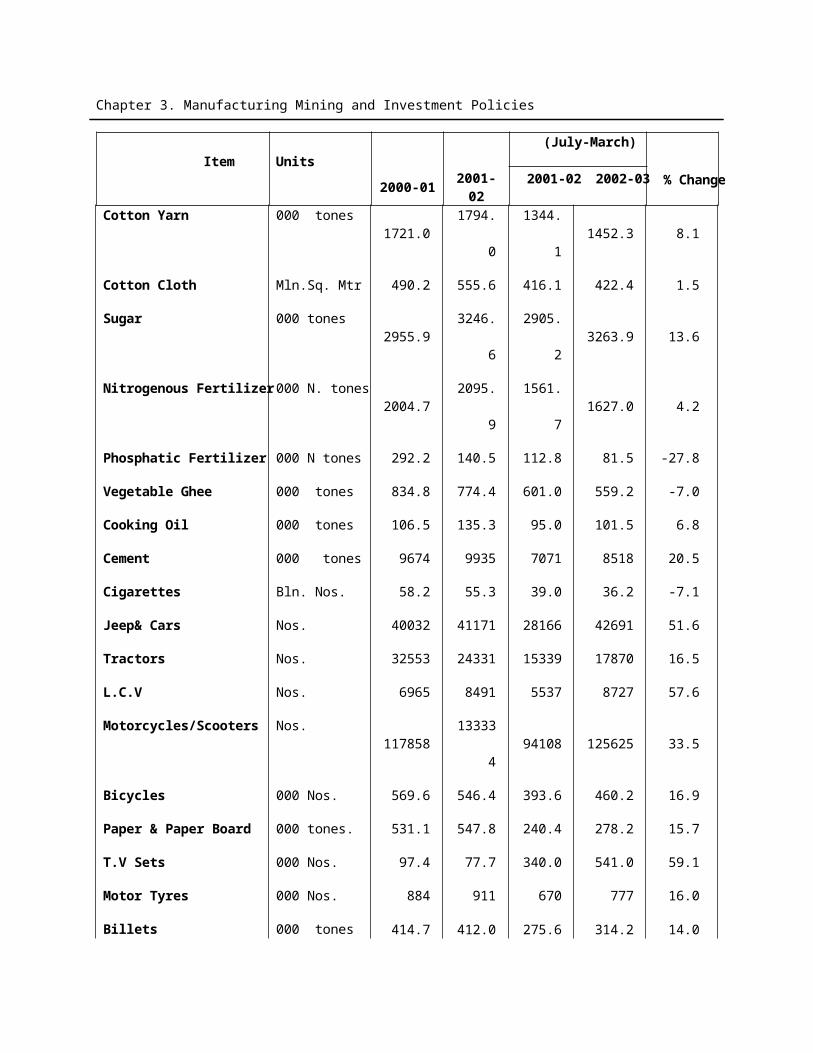

Table 3.2Production of Selected Industrial Items of Large-scale

Item Units2000-

012001-

02

(July-March)

% Change2001-02 2002-03

Cotton Yarn 000 tones 1721.0 1794.0 1344.1 1452.3 8.1

Cotton Cloth Mln.Sq. Mtr 490.2 555.6 416.1 422.4 1.5

Sugar 000 tones 2955.9 3246.6 2905.2 3263.9 13.6

Nitrogenous Fertilizer 000 N. tones 2004.7 2095.9 1561.7 1627.0 4.2

Phosphatic Fertilizer 000 N tones 292.2 140.5 112.8 81.5 -27.8

Vegetable Ghee 000 tones 834.8 774.4 601.0 559.2 -7.0

Cooking Oil 000 tones 106.5 135.3 95.0 101.5 6.8

Cement 000 tones 9674 9935 7071 8518 20.5

Cigarettes Bln. Nos. 58.2 55.3 39.0 36.2 -7.1

Jeep& Cars Nos. 40032 41171 28166 42691 51.6

Tractors Nos. 32553 24331 15339 17870 16.5

L.C.V Nos. 6965 8491 5537 8727 57.6

Motorcycles/Scooters Nos.117858

13333

494108 125625 33.5

Bicycles 000 Nos. 569.6 546.4 393.6 460.2 16.9

Chapter 3. Manufacturing Mining and Investment Policies

Paper & Paper Board 000 tones. 531.1 547.8 240.4 278.2 15.7

T.V Sets 000 Nos. 97.4 77.7 340.0 541.0 59.1

Motor Tyres 000 Nos. 884 911 670 777 16.0

Billets 000 tones 414.7 412.0 275.6 314.2 14.0

Refrigerators 000 Nos. 272.3 313.8 195.0 240.0 23.1

Soda Ash 000 tones 217.9 215.2 187.6 211.8 12.9

Source: Federal Bureau of Statistics

EVALUATION OF SELECTED INDUSTRIES OF

LARGE SCALE MANUFACTURING (LSM).

Textile Industry

Textile products are a basic human

requirement next only to food. Inspite of the

government’s efforts to diversify export as well

as industrial base, the textile remains the

backbone of industrial activity in the country. Its

share in the economy, in terms of GDP, exports,

employment, foreign exchange earnings,

investment and contribution to the value added

in industry; make it the single largest

determinant of the growth in manufacturing

sector with 46 percent share in overall

manufacturing activity. The demand for textiles

in the world is around $18 trillion. Pakistan has

emerged as one of the major cotton textile

product supplier in the world market and its

share in world yarn trade is about 30 percent

while its share in cotton cloth trade is about 8

percent. However, overall share of textile

exports from Pakistan is around one percent. The

share of textile in Pakistan’s exports earnings is

68 percent at its present worth of exports is

around $ 7 billion. The value addition in the

sector account for 9 percent of GDP and it

employ 38 percent of industrial workers. During

the last three years, Pakistan’s textile sector is

preparing itself to face the challenges of the

post-quota regime in 2005.

Investment Trend in Textile Sector

The year under review witnessed

tremendous inflow of investment in value added

expansion and BMR. The textile vision 2005

besides providing a road map to enhance

exports of textile products, also set benchmark

investment requirements for the creation of new

capacity and up-gradation of the existing

production base. The textile vision 2005

maintained that at the initial phase heavy

investment will be needed to create additional

capacity in the apparel industry; however, the

apparel sector only received 36 percent of the

targeted investment during last three years. Bulk

of the investment to the extent of 56 percent

went to the traditional spinning sector which is

three times higher than envisaged in the textile

vision 2005. The textile sector received $ 1.5

billion worth of investment during the last three

years.

The brighter side of the investment in this

sector is the heavy investment in the air jet

Chapter 3. Manufacturing Mining and Investment Policies

weaving segment where actual disbursement

has already surpassed the target with a fair

margin of 55 percent. Such investment would

not only modernize this sector but would likely to

fuel value addition in the coming years.

However, grey area of the whole investment

composition has been below target inflows in the

water jet weaving sector. The tremendous inflow

of investment in the sector is likely to enable

Pakistan textile industry to face formidable

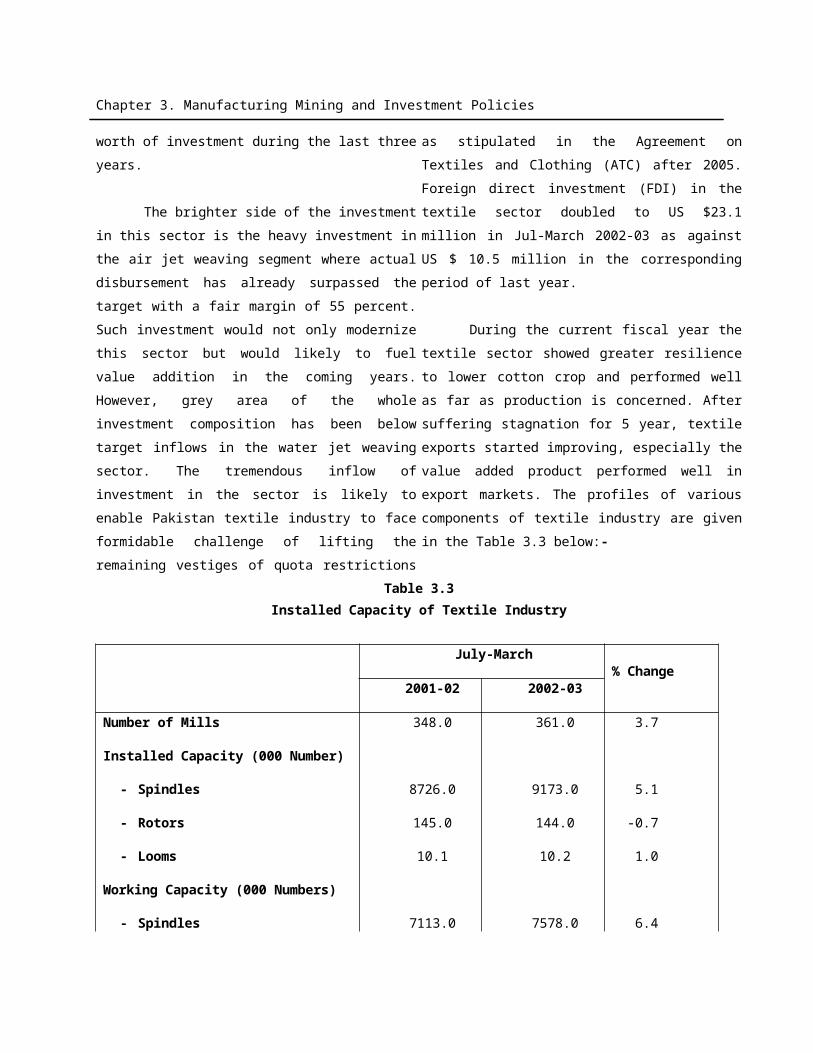

challenge of lifting the remaining vestiges of