Options Futures & other Options Futures & other Derivatives Derivatives Instructor: Instructor: Ganesh Kumar N. Ganesh Kumar N.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

8/6/2019 OFD 1 Introduction

http://slidepdf.com/reader/full/ofd-1-introduction 1/32

Options Futures & other Options Futures & other DerivativesDerivatives

Instructor:Instructor:Ganesh Kumar N.Ganesh Kumar N.

8/6/2019 OFD 1 Introduction

http://slidepdf.com/reader/full/ofd-1-introduction 2/32

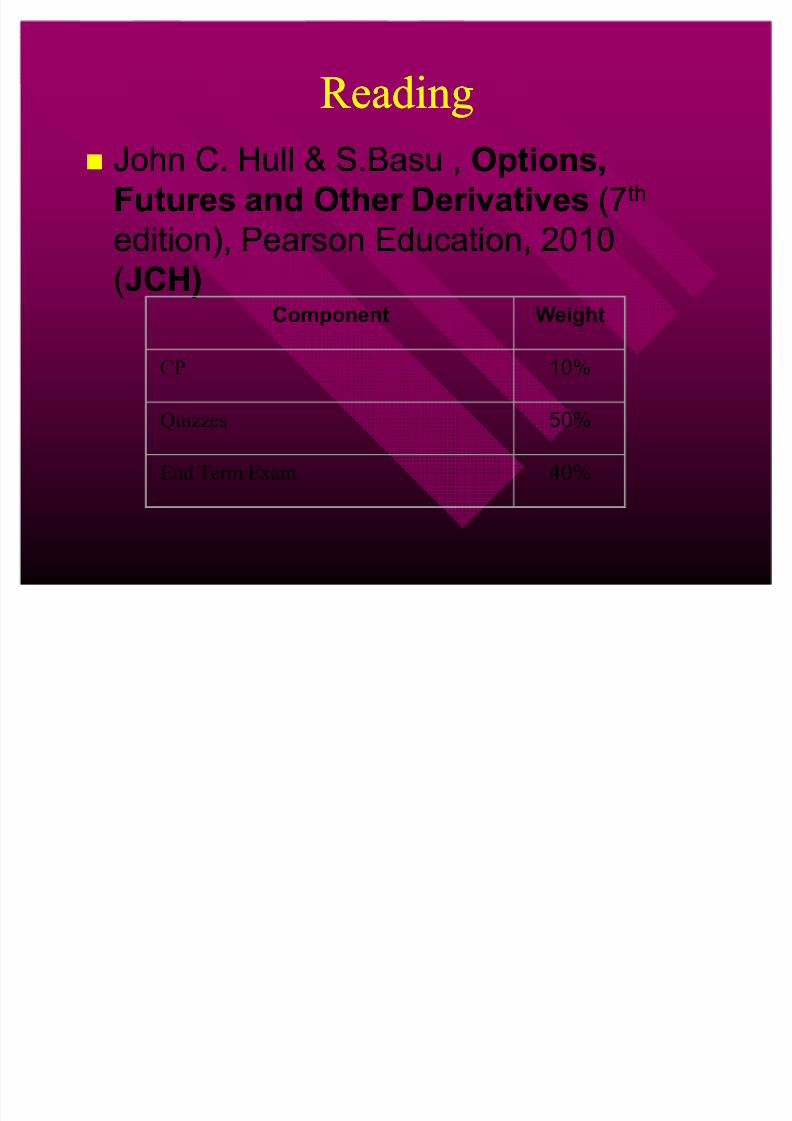

R eadingR eading

John C. Hull & S.Basu ,John C. Hull & S.Basu , Options,Options,Futures and Other DerivativesFutures and Other Derivatives (7(7thth

edition), Pearson Education, 2010edition), Pearson Education, 2010

((JCH)JCH)Component Weight

CP 10%

Quizzes 50%

End Term Exam 40%

8/6/2019 OFD 1 Introduction

http://slidepdf.com/reader/full/ofd-1-introduction 3/32

MUMBAI: Interest R ate Futures, which was inaugurated on

the National Stock Exchange (NSE) onMondayAug.31 ,

2009.

Interest rate futures was introduced in June 2003 but failed

to take off.

New derivatives in Indian market New derivatives in Indian market

8/6/2019 OFD 1 Introduction

http://slidepdf.com/reader/full/ofd-1-introduction 4/32

New derivatives in Indian market New derivatives in Indian market

Currency futures launched in August 2008Currency futures launched in August 2008

Current average turnover Current average turnover -- R s9,000 crore aR s9,000 crore a

day with NSE and MCX Stock Exchangeday with NSE and MCX Stock Exchange(MCX(MCX--SX) splitting the volumesSX) splitting the volumes

Stock based derivatives:Stock based derivatives:

± ± Index futures introduced in June 2000Index futures introduced in June 2000 ± ± July 2001: Index options,Options on securities,July 2001: Index options,Options on securities,

single stock futuressingle stock futures

8/6/2019 OFD 1 Introduction

http://slidepdf.com/reader/full/ofd-1-introduction 5/32

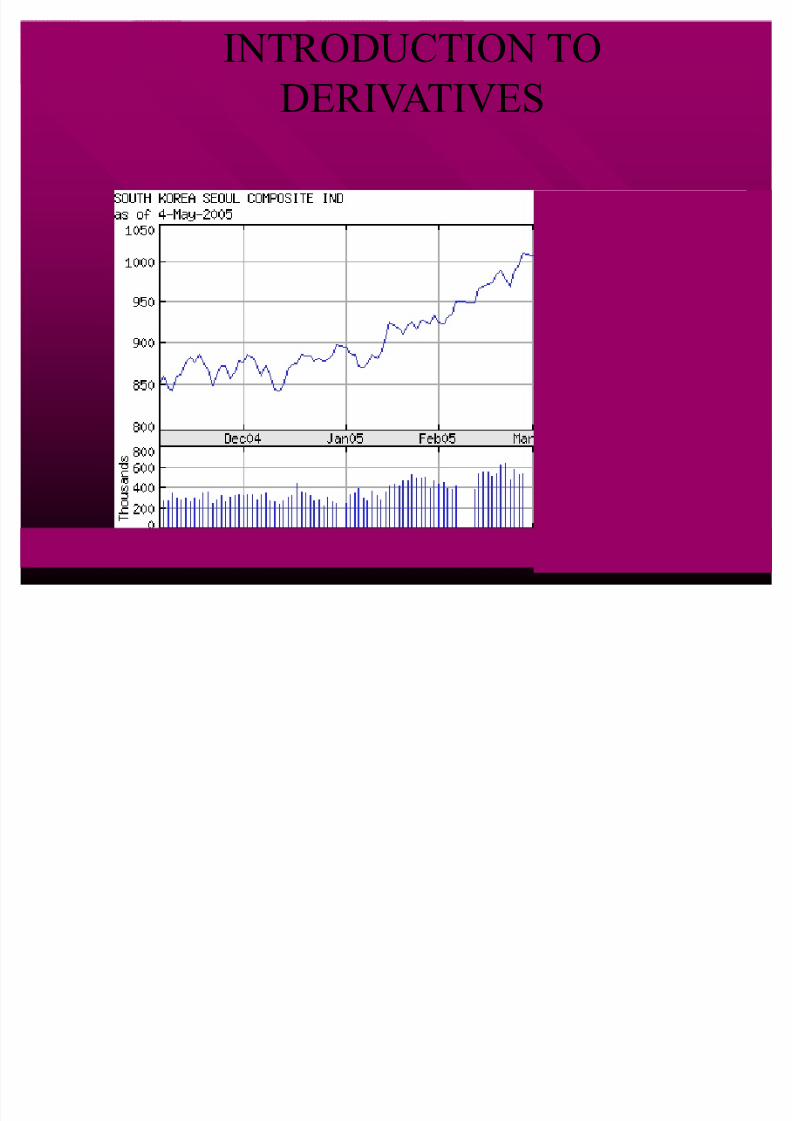

INTR ODUCTION TO

DER IVATIVES

8/6/2019 OFD 1 Introduction

http://slidepdf.com/reader/full/ofd-1-introduction 6/32

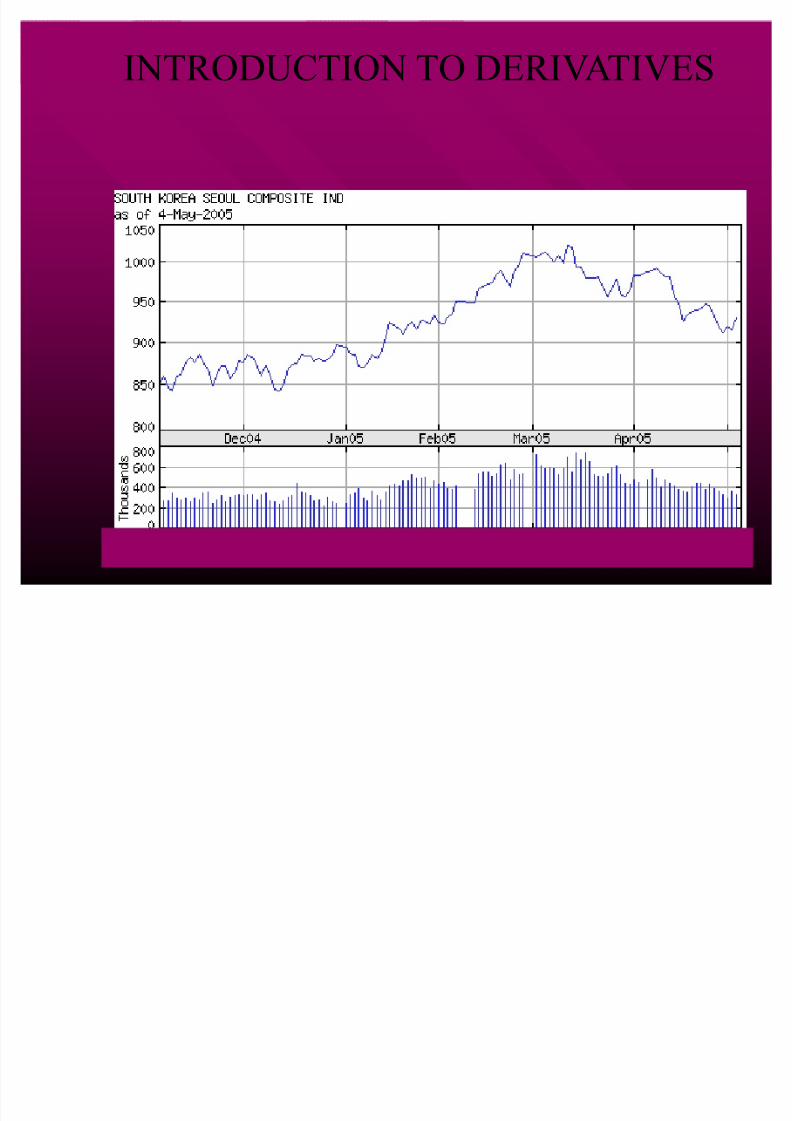

INTR ODUCTION TO DER IVATIVES

8/6/2019 OFD 1 Introduction

http://slidepdf.com/reader/full/ofd-1-introduction 7/32

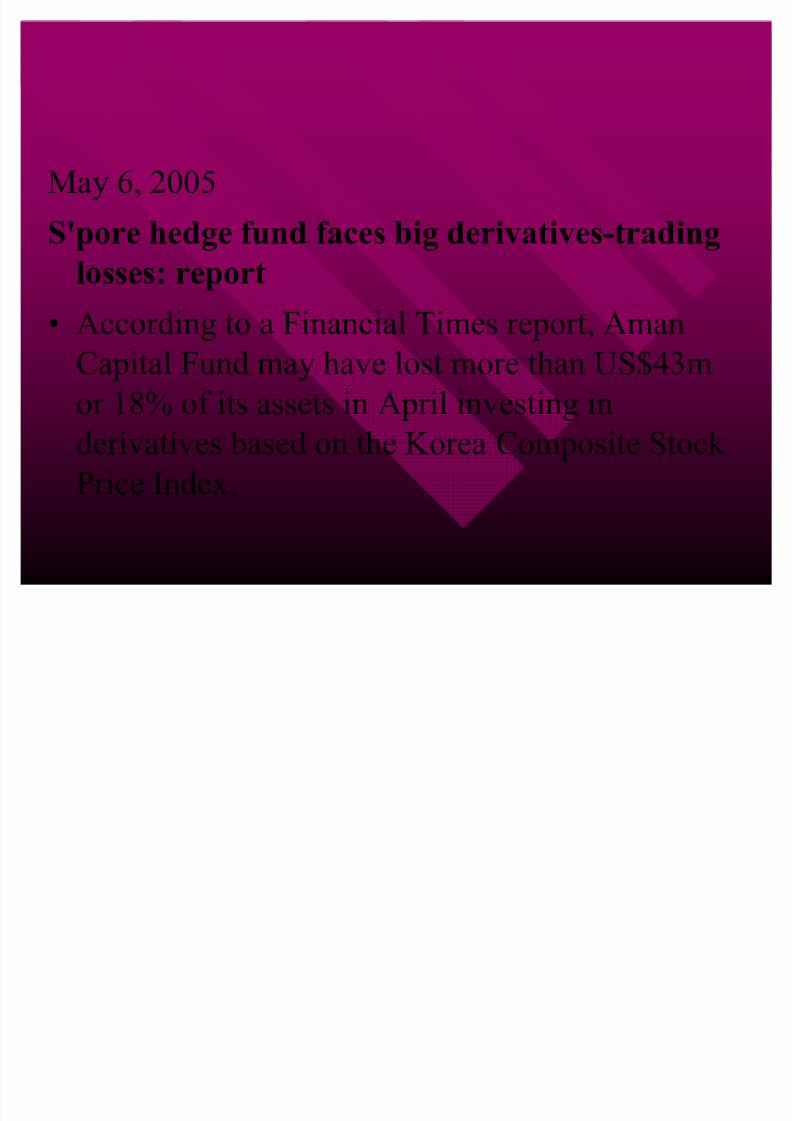

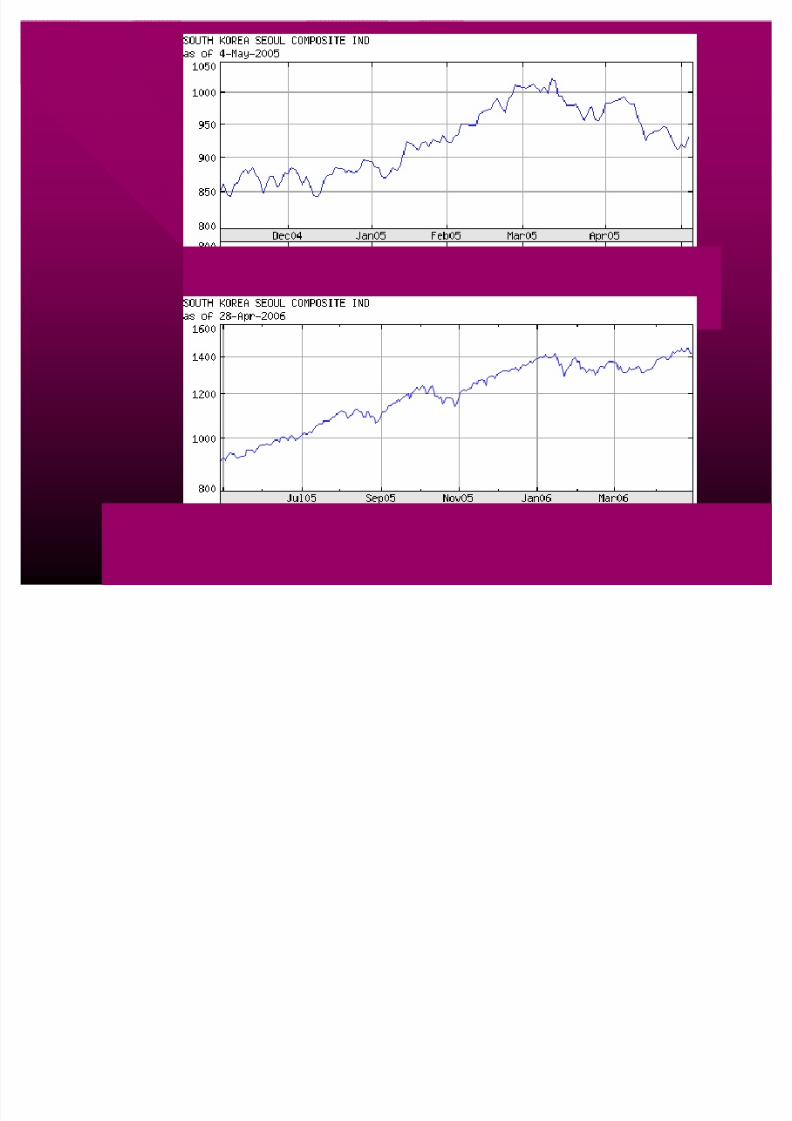

May 6, 2005

S'pore hedge fund faces big derivatives-trading

losses: report� According to a Financial Times report, Aman

Capital Fund may have lost more than US$43m

or 18% of its assets inA pril investing inderivatives based on the Korea Composite Stock

Price Index.

8/6/2019 OFD 1 Introduction

http://slidepdf.com/reader/full/ofd-1-introduction 8/32

8/6/2019 OFD 1 Introduction

http://slidepdf.com/reader/full/ofd-1-introduction 9/32

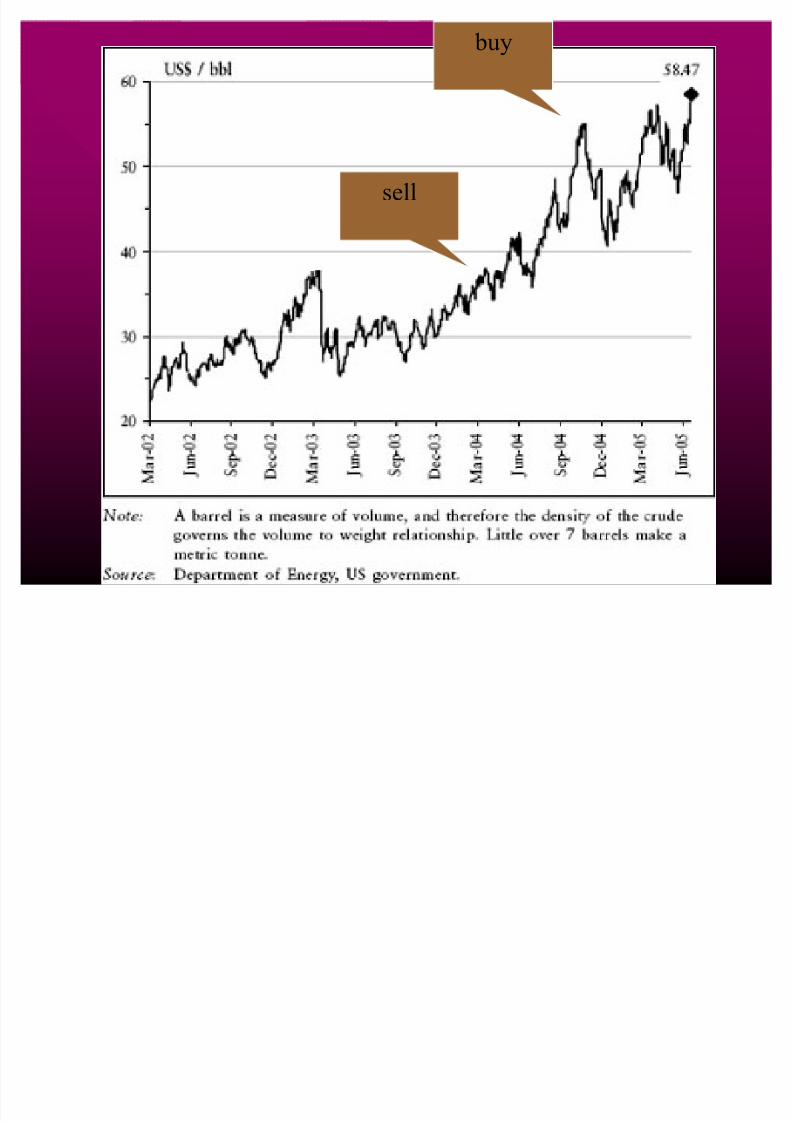

CAO and Oil futuresCAO and Oil futures

� Jet fuel trader China Aviation Oil (CAO),

which is listed in Singapore, collapsed in

November 2004 under U

S$550m inderivatives-trading losses.

� The company had sold oil futures around

$38 hoping that prices will go down but oil

prices went up.

8/6/2019 OFD 1 Introduction

http://slidepdf.com/reader/full/ofd-1-introduction 10/32

sell

buy

8/6/2019 OFD 1 Introduction

http://slidepdf.com/reader/full/ofd-1-introduction 11/32

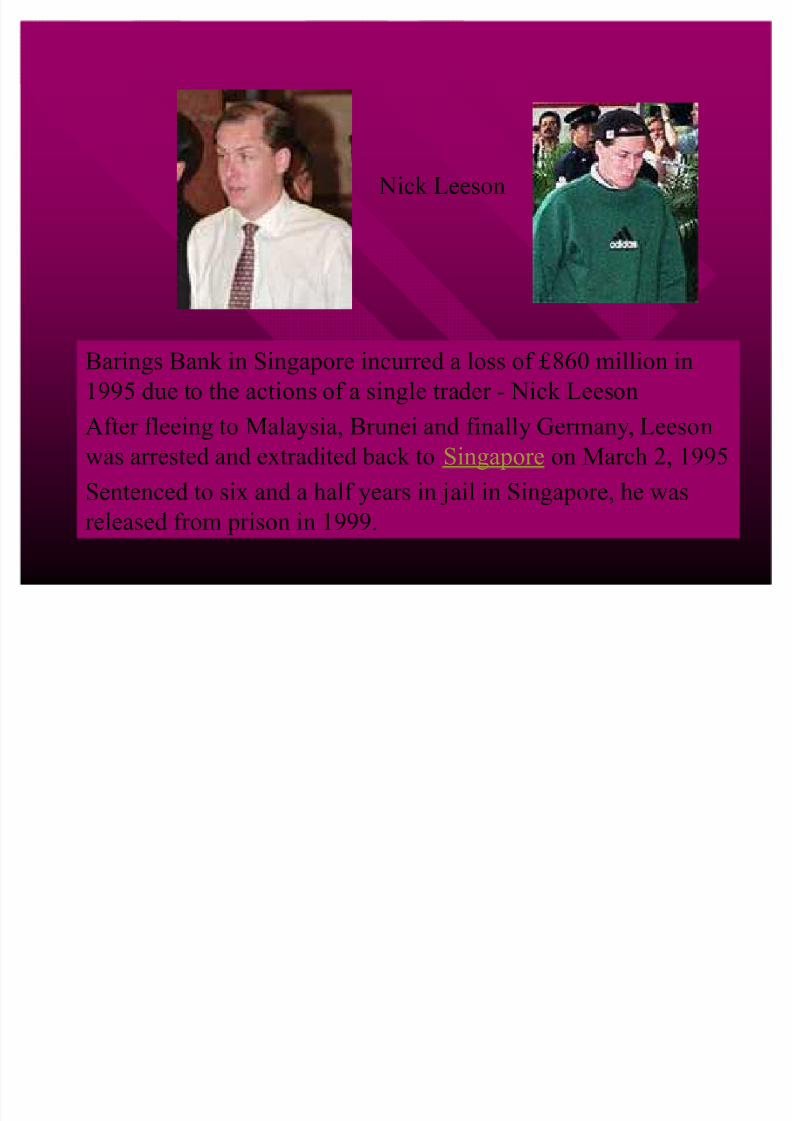

Barings Bank in Singapore incurred a loss of £860 million in

1995 due to the actions of a single trader - Nick Leeson

After fleeing to Malaysia, Brunei and finally Germany, Leeson

was arrested and extradited back to Singapore onMarch 2, 1995

Sentenced to six and a half years in jail in Singapore, he was

released from prison in 1999.

Nick Leeson

8/6/2019 OFD 1 Introduction

http://slidepdf.com/reader/full/ofd-1-introduction 12/32

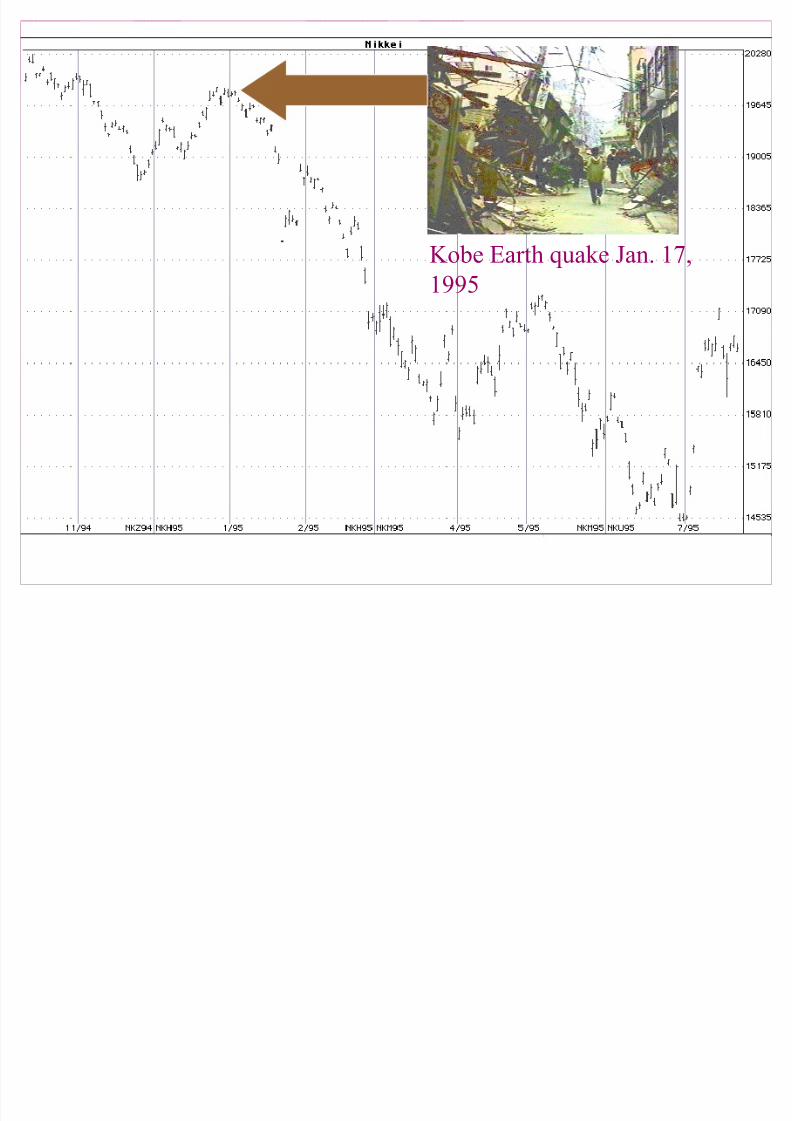

Kobe Earth quake Jan. 17,

1995

8/6/2019 OFD 1 Introduction

http://slidepdf.com/reader/full/ofd-1-introduction 13/32

Introduction to derivativesIntroduction to derivatives

A derivative is an instrument whose valueA derivative is an instrument whose valuedepends (derived from) on the values of depends (derived from) on the values of other more basic underlying variablesother more basic underlying variables

Examples:Examples:

�� Futures ContractsFutures Contracts

�� Forward ContractsForward Contracts

�� SwapsSwaps

�� OptionsOptions

8/6/2019 OFD 1 Introduction

http://slidepdf.com/reader/full/ofd-1-introduction 14/32

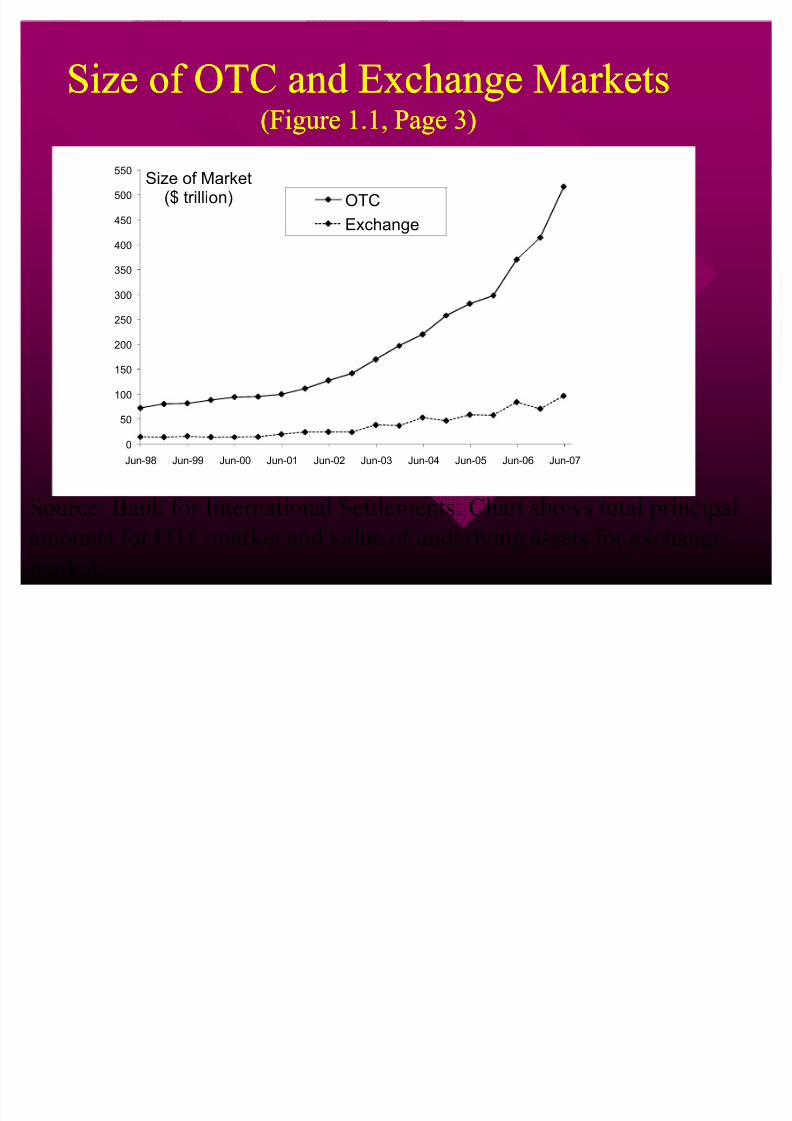

Size of OTC and ExchangeMarketsSize of OTC and ExchangeMarkets(Figure 1.1, Page 3)(Figure 1.1, Page 3)

Source: Bank for International Settlements. Chart shows total principal

amounts for OTC market and value of underlying assets for exchange

market

0

50

100

150

200

250

300

350

400

450

500

550

Jun-98 Jun-99 Jun-00 Jun-01 Jun-02 Jun-03 Jun-04 Jun-05 Jun-06 Jun-07

Size of Market($ trillion) OTC

Exchange

8/6/2019 OFD 1 Introduction

http://slidepdf.com/reader/full/ofd-1-introduction 15/32

Use of DerivativesUse of Derivatives

To hedge risksTo hedge risks

To speculate (take a view on the futureTo speculate (take a view on the future

direction of the market)direction of the market) To lock in an arbitrage profitTo lock in an arbitrage profit

To change the nature of a liabilityTo change the nature of a liability

To change the nature of an investmentTo change the nature of an investmentwithout incurring the costs of selling onewithout incurring the costs of selling one

portfolio and buying another portfolio and buying another

8/6/2019 OFD 1 Introduction

http://slidepdf.com/reader/full/ofd-1-introduction 16/32

Forward ContractsForward Contracts

It is an agreement to buy/sell as asset at a certainIt is an agreement to buy/sell as asset at a certain

future time for a certain price.future time for a certain price.

Spot contract:Agreement to buy/sell asset today.Spot contract:Agreement to buy/sell asset today.

Example: June 9. Spot INR per USD: 46.75. OneExample: June 9. Spot INR per USD: 46.75. One

month forward 46.90month forward 46.90

Forward contracts are similar to futures except thatForward contracts are similar to futures except that

they trade in the over they trade in the over--thethe--counter marketcounter market Forward contracts are particularly popular onForward contracts are particularly popular on

currencies and interest ratescurrencies and interest rates

8/6/2019 OFD 1 Introduction

http://slidepdf.com/reader/full/ofd-1-introduction 17/32

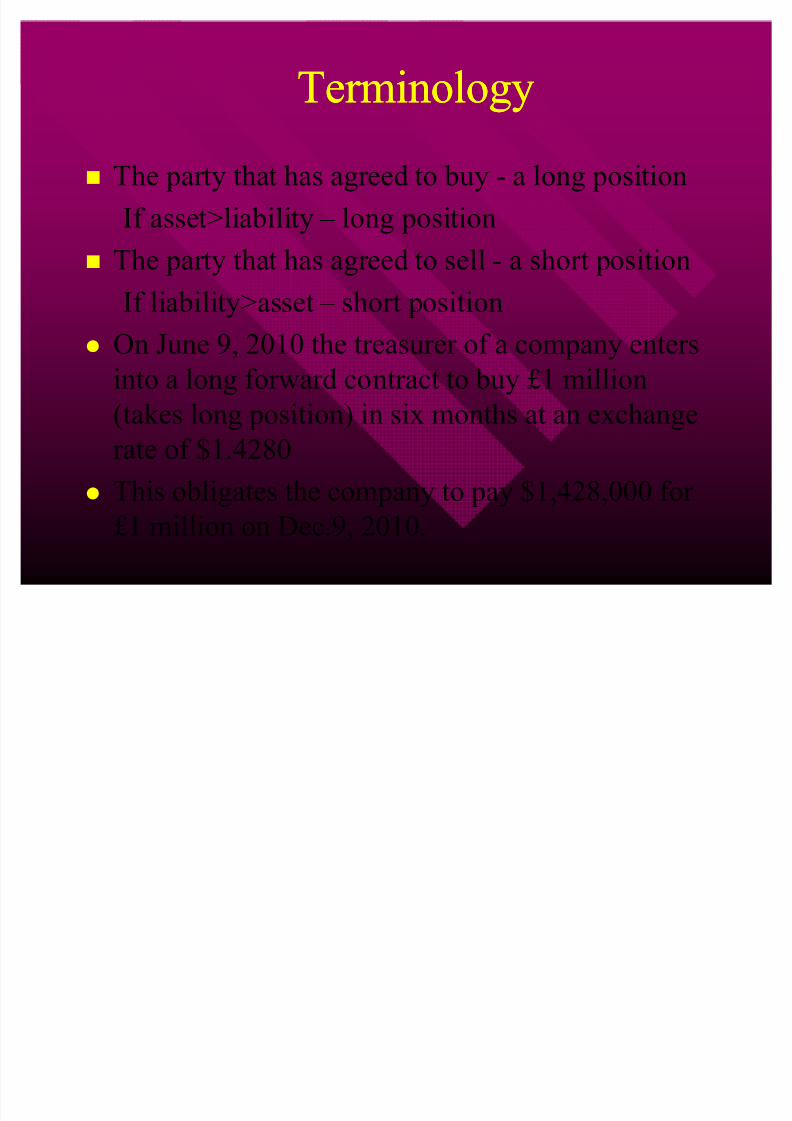

TerminologyTerminology

The party that has agreed to buy - a long position

If asset>liability ± long position

The party that has agreed to sell - a short position

If liability>asset ± short position

On June 9, 2010 the treasurer of a company enters

into a long forward contract to buy £1 million

(takes long position) in six months at an exchangerate of $1.4280

This obligates the company to pay $1,428,000 for

£1 million on Dec.9, 2010.

8/6/2019 OFD 1 Introduction

http://slidepdf.com/reader/full/ofd-1-introduction 18/32

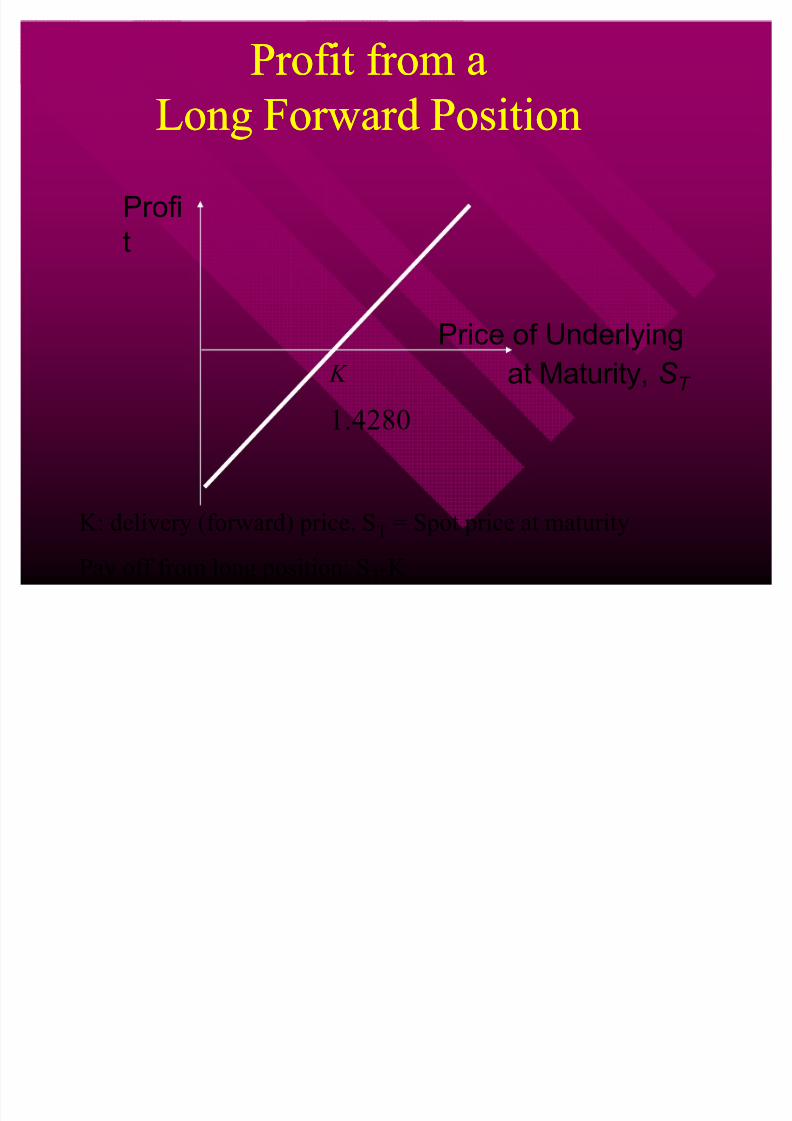

Profit from aProfit from a

Long Forward PositionLong Forward Position

Pr of it

Price of Underlying

at Maturity, S T K

K: delivery (forward) price. ST = Spot price at maturity

Pay off from long position: ST-K

1.4280

8/6/2019 OFD 1 Introduction

http://slidepdf.com/reader/full/ofd-1-introduction 19/32

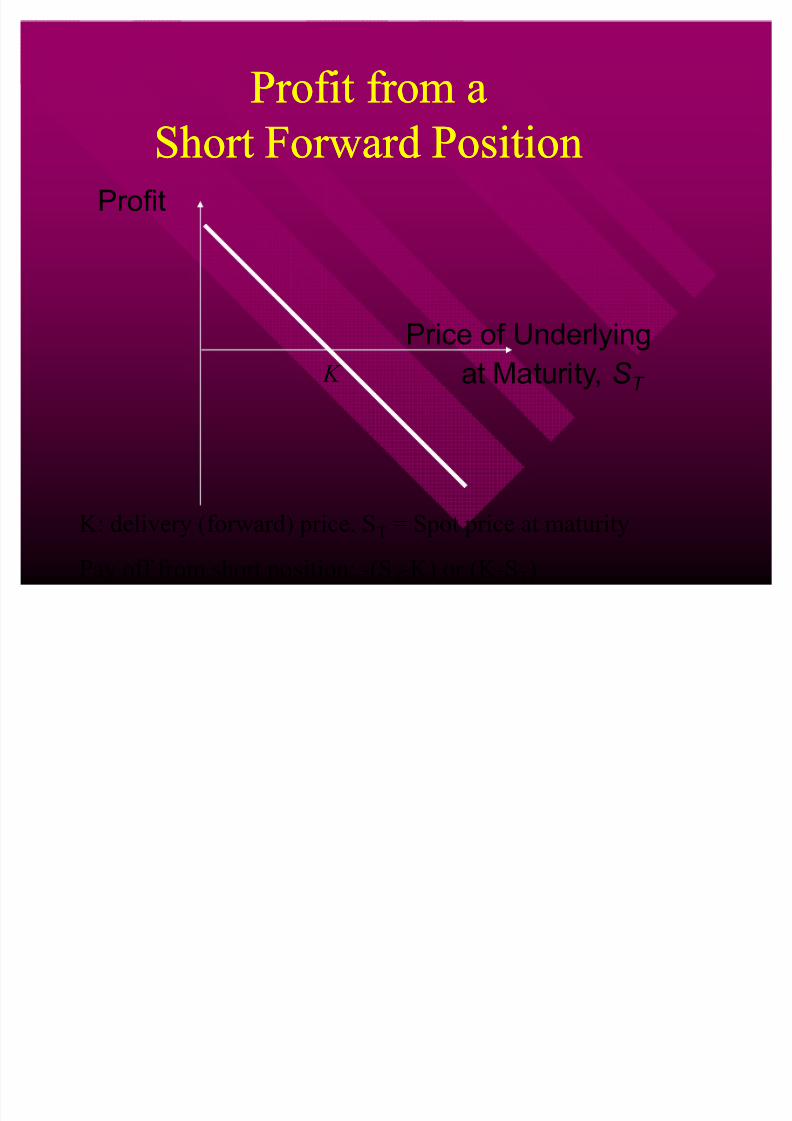

Profit from aProfit from a

Short Forward PositionShort Forward PositionPr of it

Price of Underlying

at Maturity, S T K

K: delivery (forward) price. ST = Spot price at maturity

Pay off from short position: -(ST-K) or (K-ST)

8/6/2019 OFD 1 Introduction

http://slidepdf.com/reader/full/ofd-1-introduction 20/32

OptionsOptions

yy Option gives the owner the right, but not theOption gives the owner the right, but not the

obligation to buy (call option)/ sell (put option)obligation to buy (call option)/ sell (put option)

the underlying financial asset/ commoditythe underlying financial asset/ commodityyy Exercise/Strike price is the contracted priceExercise/Strike price is the contracted price

yy Seller of an option is called option writer Seller of an option is called option writer

yy

Option premium (price of an option): the upOption premium (price of an option): the upfront payment to be made to the writer of anfront payment to be made to the writer of an

option.option.

8/6/2019 OFD 1 Introduction

http://slidepdf.com/reader/full/ofd-1-introduction 21/32

OptionsOptions

yy European option can be exercised only at maturityEuropean option can be exercised only at maturity

yy American option can be exercised before maturityAmerican option can be exercised before maturity

yy Buying (selling) a call optionBuying (selling) a call option ± ± long(short) on calllong(short) on call

yy Buying (selling) a put optionBuying (selling) a put option ± ± long(short) on putlong(short) on put

8/6/2019 OFD 1 Introduction

http://slidepdf.com/reader/full/ofd-1-introduction 22/32

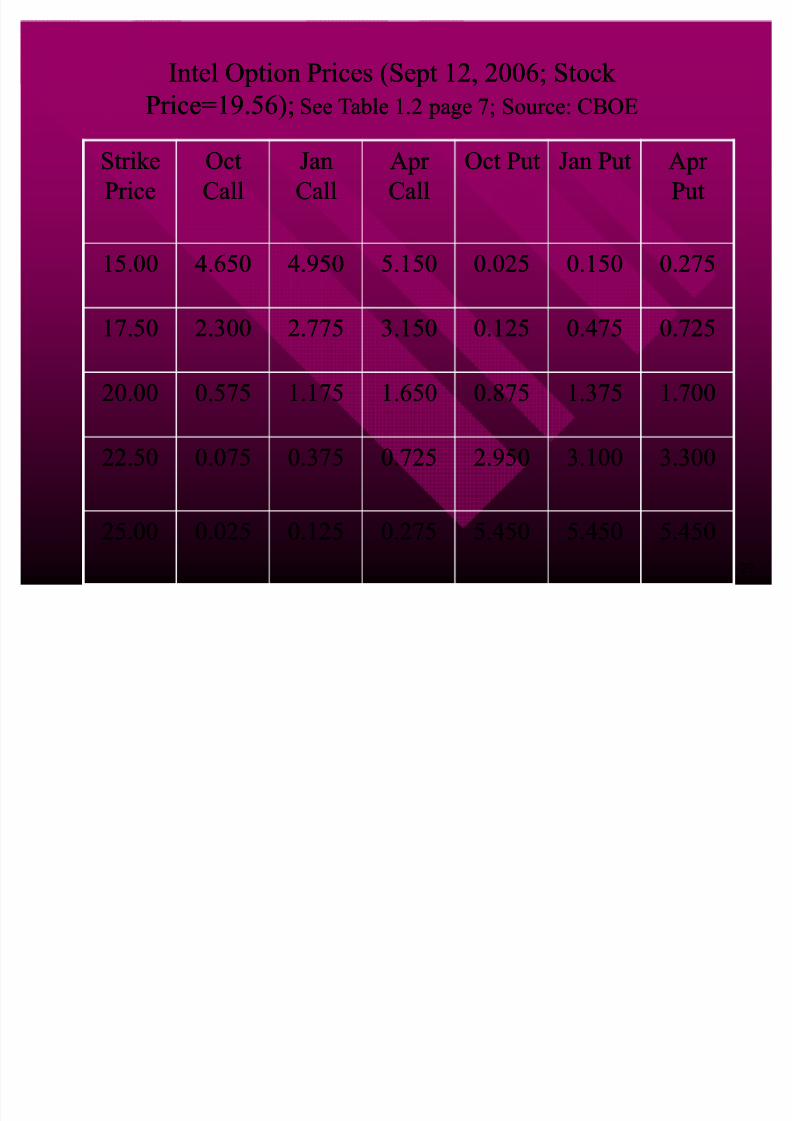

Intel Option Prices (Sept 12, 2006; Stock Intel Option Prices (Sept 12, 2006; Stock

Price=19.56);Price=19.56); See Table 1.2 page 7; Source:CBOESee Table 1.2 page 7; Source:CBOE

22

StrikeStrike

PricePrice

OctOct

CallCall

JanJan

CallCall

A pr A pr

CallCall

Oct PutOct Put Jan PutJan Put A pr A pr

PutPut

15.0015.00 4.6504.650 4.9504.950 5.1505.150 0.0250.025 0.1500.150 0.2750.275

17.5017.50 2.3002.300 2.7752.775 3.1503.150 0.1250.125 0.4750.475 0.7250.725

20.0020.00 0.5750.575 1.1751.175 1.6501.650 0.8750.875 1.3751.375 1.7001.700

22.5022.50 0.0750.075 0.3750.375 0.7250.725 2.9502.950 3.1003.100 3.3003.300

25.0025.00 0.0250.025 0.1250.125 0.2750.275 5.4505.450 5.4505.450 5.4505.450

8/6/2019 OFD 1 Introduction

http://slidepdf.com/reader/full/ofd-1-introduction 23/32

Options vs Futures/ForwardsOptions vs Futures/Forwards

In case of futures/forward the holder isIn case of futures/forward the holder is

obliged to buy or sell at a certain priceobliged to buy or sell at a certain price

An option gives the holder the right to buyAn option gives the holder the right to buyor sell at a certain priceor sell at a certain price

8/6/2019 OFD 1 Introduction

http://slidepdf.com/reader/full/ofd-1-introduction 24/32

Types of TradersTypes of Traders

� Hedgers

� Speculators

� Arbitrageurs

� Some of the largest trading losses in derivatives

have occurred because individuals who had a

mandate to be hedgers or arbitrageurs switched to being speculators

8/6/2019 OFD 1 Introduction

http://slidepdf.com/reader/full/ofd-1-introduction 25/32

Hedging exampleHedging example

A US company has to pay £10 million for A US company has to pay £10 million for imports from Britain in 3 months and decides toimports from Britain in 3 months and decides tohedge using a long position in a Pound Stg.hedge using a long position in a Pound Stg.

forward contract at $1.485 per Pound stg.forward contract at $1.485 per Pound stg. An investor owns 1,000 Microsoft sharesAn investor owns 1,000 Microsoft shares

currently worth $28 per share. A twocurrently worth $28 per share. A two--month putmonth put

with a strike price of $27.50 costs $1. Thewith a strike price of $27.50 costs $1. Theinvestor decides to hedge by buying 10 putinvestor decides to hedge by buying 10 putcontractscontracts

8/6/2019 OFD 1 Introduction

http://slidepdf.com/reader/full/ofd-1-introduction 26/32

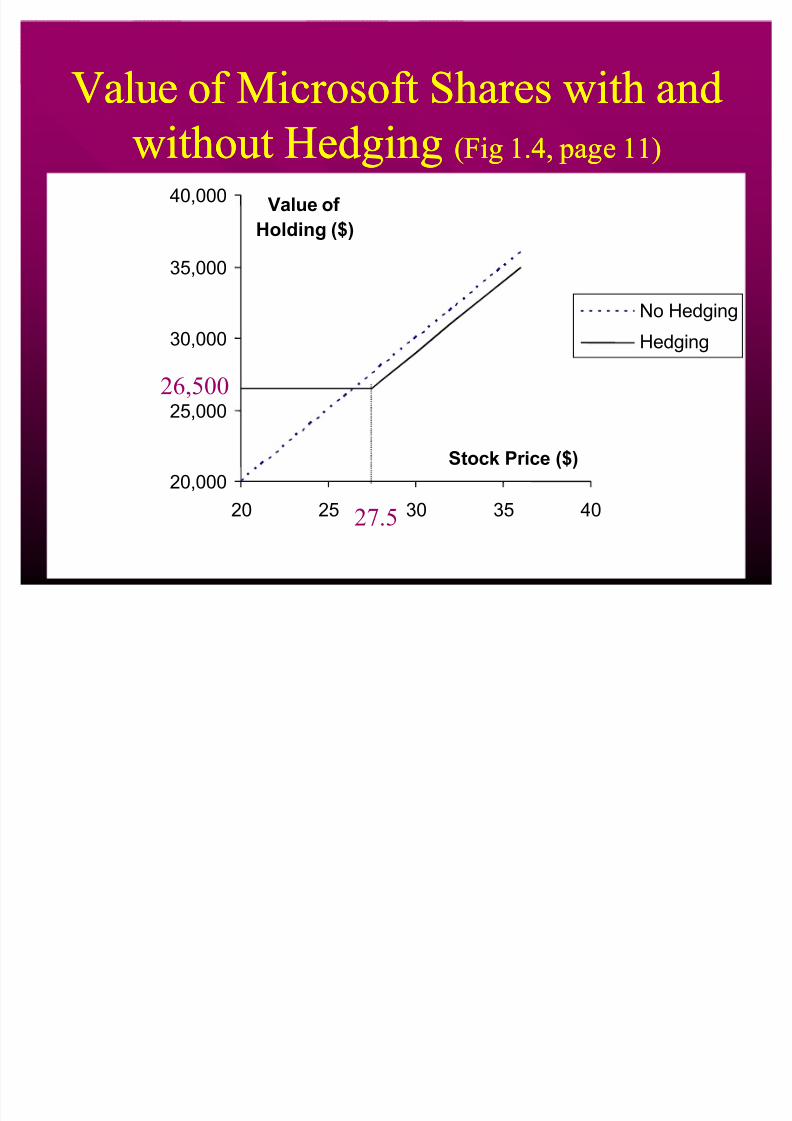

Value of Microsoft Shares with andValue of Microsoft Shares with and

without Hedgingwithout Hedging (Fig 1.4, page 11)(Fig 1.4, page 11)

20,000

25,000

30,000

35,000

40,000

20 25 30 35 40

Stock Price ($)

Value of

Holding ($)

No Hedging

Hedging

26,500

27.5

8/6/2019 OFD 1 Introduction

http://slidepdf.com/reader/full/ofd-1-introduction 27/32

Speculation ExampleSpeculation Example

An investor with R s.4,000 to invest feelsAn investor with R s.4,000 to invest feels

that ABC¶s stock price will increase over that ABC¶s stock price will increase over

the next 2 months. The current stock price isthe next 2 months. The current stock price is

R s.40 and the price of a 2R s.40 and the price of a 2--month call optionmonth call option

with a strike of 45 is R s.2with a strike of 45 is R s.2

What are the alternative strategies?What are the alternative strategies?

Buy 100 sharesBuy 100 shares

Buy 2000 call optionsBuy 2000 call options

8/6/2019 OFD 1 Introduction

http://slidepdf.com/reader/full/ofd-1-introduction 28/32

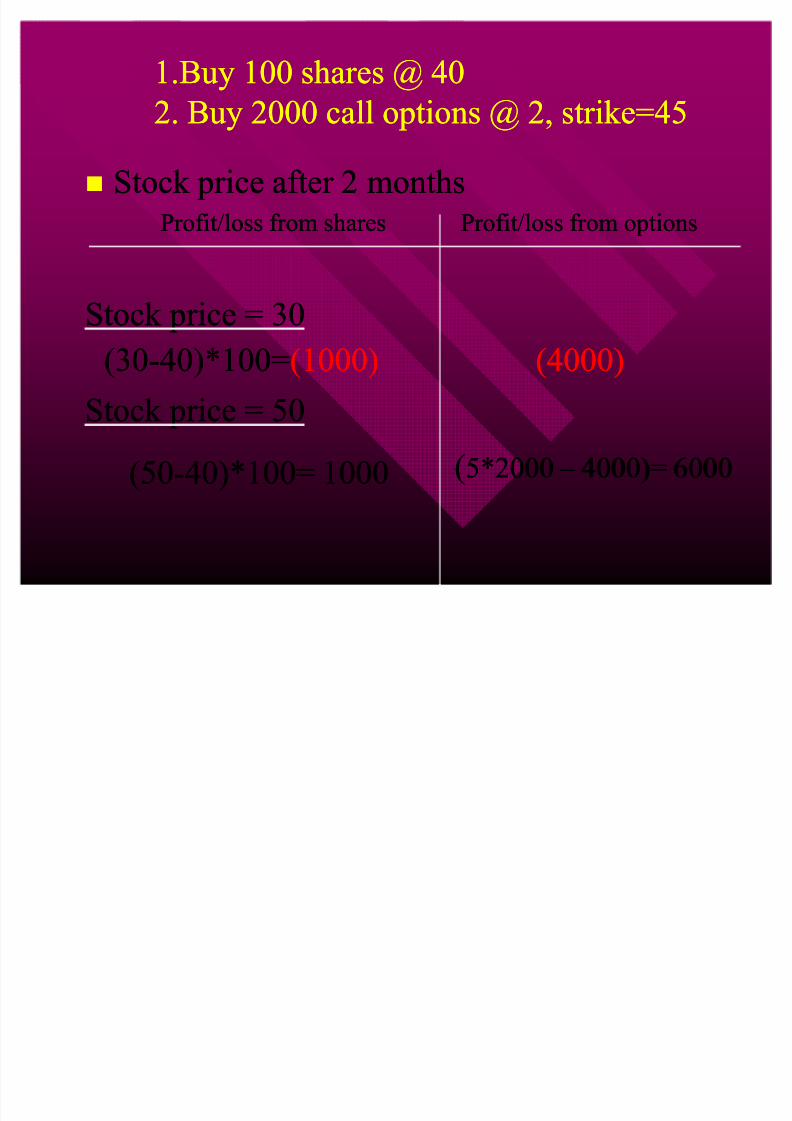

1.Buy 100 shares @ 401.Buy 100 shares @ 40

2. Buy 2000 call options @ 2, strike=452. Buy 2000 call options @ 2, strike=45

Stock price after 2 monthsStock price after 2 monthsProfit/loss from sharesProfit/loss from shares Profit/loss from optionsProfit/loss from options

Stock price = 30Stock price = 30

Stock price = 50Stock price = 50

(30(30--40)*100=40)*100=(1000)(1000) (4000)(4000)

(50(50--40)*100= 100040)*100= 1000 ((5*20005*2000 ± ± 4000)= 60004000)= 6000

8/6/2019 OFD 1 Introduction

http://slidepdf.com/reader/full/ofd-1-introduction 29/32

Arbitrage ExampleArbitrage Example

A stock price is quoted as £100 in LondonA stock price is quoted as £100 in London

and $150 in New York and $150 in New York

The current exchange rate is $1.485 per £The current exchange rate is $1.485 per £ What is the arbitrage opportunity?What is the arbitrage opportunity?

8/6/2019 OFD 1 Introduction

http://slidepdf.com/reader/full/ofd-1-introduction 30/32

Jan. 2008: SocieteJan. 2008: Societe

Generale, France¶sGenerale, France¶s

secondsecond--biggest biggest

bank, said it had been bank, said it had beenthe victim of athe victim of a

massive andmassive and

"exceptional´ fraud by"exceptional´ fraud by

a junior rogue trader a junior rogue trader resulting in losses of resulting in losses of

4.9 billion euros (over 4.9 billion euros (over

$7 billion).$7 billion).

8/6/2019 OFD 1 Introduction

http://slidepdf.com/reader/full/ofd-1-introduction 31/32

Societe GeneraleSociete Generale

The loss is the biggest caused by a singleThe loss is the biggest caused by a singletrader, dwarfing the $1.4 billion loss by trader trader, dwarfing the $1.4 billion loss by trader Nick Leeson Nick Leeson

Mr Kerviel¶s supposed job was to arbitrage smallMr Kerviel¶s supposed job was to arbitrage smalldiscrepancies between equity derivatives and cashdiscrepancies between equity derivatives and cashequity prices.equity prices.

However, starting on January 7,Mr Kerviel madeHowever, starting on January 7,Mr Kerviel made

a series of bets that Germany¶s Dax index, thea series of bets that Germany¶s Dax index, theFrench Cac40, and the Euro Stoxx 50 would rise.French Cac40, and the Euro Stoxx 50 would rise.Trade was worth an estimatedTrade was worth an estimated ¼ ¼50bn, more than50bn, more thanSocGen¶s market valueSocGen¶s market value

8/6/2019 OFD 1 Introduction

http://slidepdf.com/reader/full/ofd-1-introduction 32/32

Societe GeneraleSociete Generale

He bought futures contracts, as normal, butHe bought futures contracts, as normal, but

did not hedge against market falls.did not hedge against market falls.

Related Documents