Mr. Norio Usui Senior Country Economist Philippines Country Office, Asian Development Bank Mr. Norio Usui is a senior country economist in the Philippines Country Office of the Asian Development Bank. He previously worked with the Central and West Asia, and Economics and Research departments. Before joining ADB in 2005, he was an associate professor of development economics at Kansai University, Chiba University, and the University of Shizuoka in Japan. He was policy advisor for the Indonesian Government between 1998 and 2000. He obtained his master’s degree and Ph.D. from the University of Tokyo, and completed an executive education program on new thinking on growth and development policy at the Kennedy School of Government in Harvard University. His current research topics in the Philippines Country Office include: structural transformation and long-term growth performance; public support (industrial policy) for industrialization; policy options for tax reforms; impact evaluation of conditional cash transfer; and inter-governmental fiscal relations and local finance. His papers have appeared in economic journals such as World Development, Resources Policy, Singapore Economic Review, and Cambridge Journal of Economics. His latest publication is “Taking the Right Road for Inclusive Growth: Industrial Upgrading and Diversification in the Philippines.”

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Mr. Norio Usui Senior Country Economist Philippines Country Office, Asian Development Bank

Mr. Norio Usui is a senior country economist in the Philippines Country Office of the Asian Development Bank. He previously worked with the Central and West Asia, and Economics and Research departments. Before joining ADB in 2005, he was an associate professor of development economics at Kansai University, Chiba University, and the University of Shizuoka in Japan. He was policy advisor for the Indonesian Government between 1998 and 2000. He obtained his master’s degree and Ph.D. from the University of Tokyo, and completed an executive education program on new thinking on growth and development policy at the Kennedy School of Government in Harvard University. His current research topics in the Philippines Country Office include: structural transformation and long-term growth performance; public support (industrial policy) for industrialization; policy options for tax reforms; impact evaluation of conditional cash transfer; and inter-governmental fiscal relations and local finance. His papers have appeared in economic journals such as World Development, Resources Policy, Singapore Economic Review, and Cambridge Journal of Economics. His latest publication is “Taking the Right Road for Inclusive Growth: Industrial Upgrading and Diversification in the Philippines.”

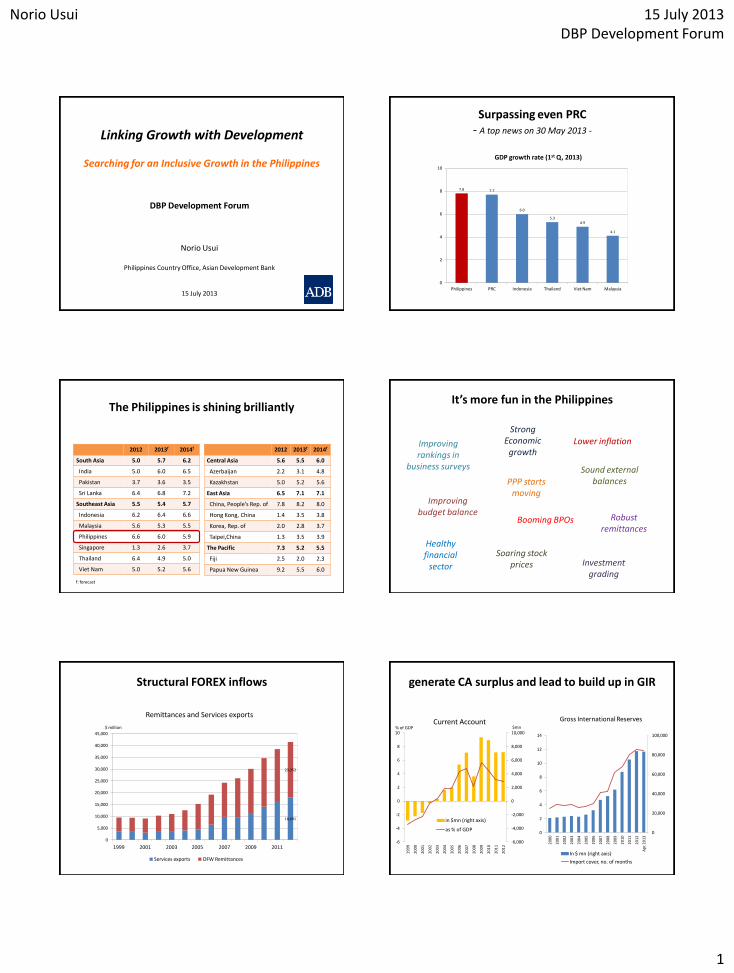

Norio Usui 15 July 2013 DBP Development Forum

1

Linking Growth with Development

Searching for an Inclusive Growth in the Philippines

DBP Development Forum

Norio Usui

Philippines Country Office, Asian Development Bank

15 July 2013

Surpassing even PRC - A top news on 30 May 2013 -

7.8 7.7

6.0

5.3 4.9

4.1

0

2

4

6

8

10

Philippines PRC Indonesia Thailand Viet Nam Malaysia

GDP growth rate (1st Q, 2013)

The Philippines is shining brilliantly

2012 2013f 2014f

South Asia 5.0 5.7 6.2

India 5.0 6.0 6.5

Pakistan 3.7 3.6 3.5

Sri Lanka 6.4 6.8 7.2

Southeast Asia 5.5 5.4 5.7

Indonesia 6.2 6.4 6.6

Malaysia 5.6 5.3 5.5

Philippines 6.6 6.0 5.9

Singapore 1.3 2.6 3.7

Thailand 6.4 4.9 5.0

Viet Nam 5.0 5.2 5.6

2012 2013f 2014f

Central Asia 5.6 5.5 6.0

Azerbaijan 2.2 3.1 4.8

Kazakhstan 5.0 5.2 5.6

East Asia 6.5 7.1 7.1

China, People’s Rep. of 7.8 8.2 8.0

Hong Kong, China 1.4 3.5 3.8

Korea, Rep. of 2.0 2.8 3.7

Taipei,China 1.3 3.5 3.9

The Pacific 7.3 5.2 5.5

Fiji 2.5 2.0 2.3

Papua New Guinea 9.2 5.5 6.0

f: forecast

It’s more fun in the Philippines

Strong Economic

growth Lower inflation

Improving budget balance

Sound external balances PPP starts

moving

Investment grading

Booming BPOs

Soaring stock prices

Healthy financial

sector

Robust remittances

Improving rankings in

business surveys

Structural FOREX inflows

18,091

23,352

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

1999 2001 2003 2005 2007 2009 2011

$ million

Remittances and Services exports

Services exports OFW Remittances

0

20,000

40,000

60,000

80,000

100,000

0

2

4

6

8

10

12

14

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

Ap

r 2

01

3

Gross International Reserves

In $ mn (right axis)

Import cover, no. of months

-6,000

-4,000

-2,000

0

2,000

4,000

6,000

8,000

10,000

-6

-4

-2

0

2

4

6

8

10

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

$mn % of GDP Current Account

in $mn (right axis)

as % of GDP

generate CA surplus and lead to build up in GIR

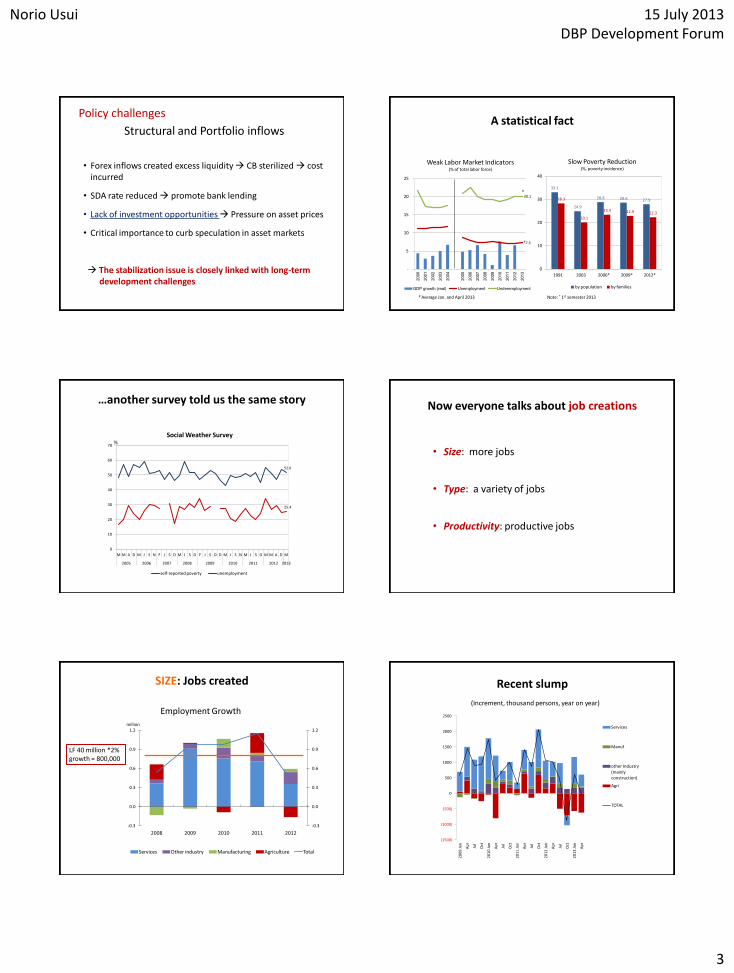

Norio Usui 15 July 2013 DBP Development Forum

2

Now, capital flows need to be watched

-1000

-500

0

500

1000

1500

2000

2007 2008 2009 2010 2011 2012 2013 May

$ mn

Net Foreign Portfolio Investment Inflow

Stock market: Net Foreign Buying

-30,000

-20,000

-10,000

0

10,000

20,000

30,000

40,000

07

/20

06

10

/20

06

01

/20

07

04

/20

07

07

/20

07

10

/20

07

01

/20

08

04

/20

08

07

/20

08

10

/20

08

01

/20

09

04

/20

09

07

/20

09

10

/20

09

01

/20

10

04

/20

10

07

/20

10

10

/20

10

01

/20

11

04

/20

11

07

/20

11

10

/20

11

01

/20

12

04

/20

12

07

/20

12

10

/20

12

01

/20

13

04

/20

13

Peso million

Sterilization

Special Deposit Account (SDA), outstanding

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

Ja

n-0

7

Ma

y-0

7

Sep-0

7

Ja

n-0

8

Ma

y-0

8

Sep-0

8

Ja

n-0

9

Ma

y-0

9

Sep-0

9

Ja

n-1

0

Ma

y-1

0

Sep-1

0

Ja

n-1

1

Ma

y-1

1

Sep-1

1

Ja

n-1

2

Ma

y-1

2

Sep-1

2

Ja

n-1

3

Ma

y-1

3

P million

Sustained credit growth

0

20

40

60

80

100

120

140

160

180

19

80

19

83

19

86

19

89

19

92

19

95

19

98

20

01

20

04

20

07

20

10

% Domestic Credit to Private Sector

% of GDP

Indonesia Malaysia

Philippines Thailand

Vietnam

• As a share of GDP, private sector credit relatively modest

0

5

10

15

20

25

Ja

n-0

8

Ma

y-0

8

Sep-0

8

Ja

n-0

9

Ma

y-0

9

Sep-0

9

Ja

n-1

0

Ma

y-1

0

Sep-1

0

Ja

n-1

1

Ma

y-1

1

Sep-1

1

Ja

n-1

2

Ma

y-1

2

Sep-1

2

Ja

n-1

3

% Bank Lending Growth

Lending for Production activities Lending to Households

Money has been flowing into….

Stock price index

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

01

JAN

07

31

MA

Y 07

28

OC

T 07

26

MA

R 0

8

23

AU

G 0

8

20

JAN

09

19

JUN

09

16

NO

V 0

9

15

AP

R 1

0

12

SEP 1

0

09

FEB 1

1

09

JUL 1

1

06

DEC

11

04

MA

Y 12

01

OC

T 12

28

FEB 1

3

INO MAL PHI THA

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

Jan 2

010

M

M

J

S

N

Jan 2

011

M

M

J

S

N

Jan 2

012

M

M

J

S

N

Jan 2

013

M

M

T-bill (91 days) rate

Pressure on the currency

37

39

41

43

45

47

49

51

01

JAN

09

06

MA

Y 09

08

SEP 0

9

11

JAN

10

16

MA

Y 10

18

SEP 1

0

21

JAN

11

26

MA

Y 11

28

SEP 1

1

31

JAN

12

04

JUN

12

07

OC

T 12

09

FEB 1

3

14

JUN

13

Peso-Dollar rate 2009- June 2013

Norio Usui 15 July 2013 DBP Development Forum

3

• Forex inflows created excess liquidity CB sterilized cost incurred

• SDA rate reduced promote bank lending

• Lack of investment opportunities Pressure on asset prices

• Critical importance to curb speculation in asset markets

The stabilization issue is closely linked with long-term development challenges

Policy challenges

Structural and Portfolio inflows

33.1

24.9

28.8 28.6 27.9 28.3

20.1

23.4 22.9 22.3

0

10

20

30

40

1991 2003 2006* 2009* 2012*

by population by families

Note: * 1st semester 2013

A statistical fact

7.3

20.1

-

5

10

15

20

25

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

GDP growth (real) Unemployment Underemployment

# Average Jan. and April 2013

#

#

Slow Poverty Reduction (%, poverty incidence)

Weak Labor Market Indicators (% of total labor force)

…another survey told us the same story

52.0

25.4

0

10

20

30

40

50

60

70

M M A D M J S N F J S D M J S D F J S O D M J S N M J S D M M A D M

2005 2006 2007 2008 2009 2010 2011 2012 2013

self-reported poverty unemployment

Social Weather Survey %

Now everyone talks about job creations

• Size: more jobs

• Type: a variety of jobs

• Productivity: productive jobs

SIZE: Jobs created

-0.3

0.0

0.3

0.6

0.9

1.2

-0.3

0.0

0.3

0.6

0.9

1.2

2008 2009 2010 2011 2012

million

Employment Growth

Services Other industry Manufacturing Agriculture Total

LF 40 million *2% growth = 800,000

Recent slump

(1500)

(1000)

(500)

0

500

1000

1500

2000

2500

20

09

Jan

Ap

r

Jul

Oct

20

10

Jan

Ap

r

Jul

Oct

20

11

Jan

Ap

r

Jul

Oct

20

12

Jan

Ap

r

Jul

Oct

20

13

Jan

Ap

r

Services

Manuf

other Industry (mainly construction)

Agri

TOTAL

(Increment, thousand persons, year on year)

Norio Usui 15 July 2013 DBP Development Forum

4

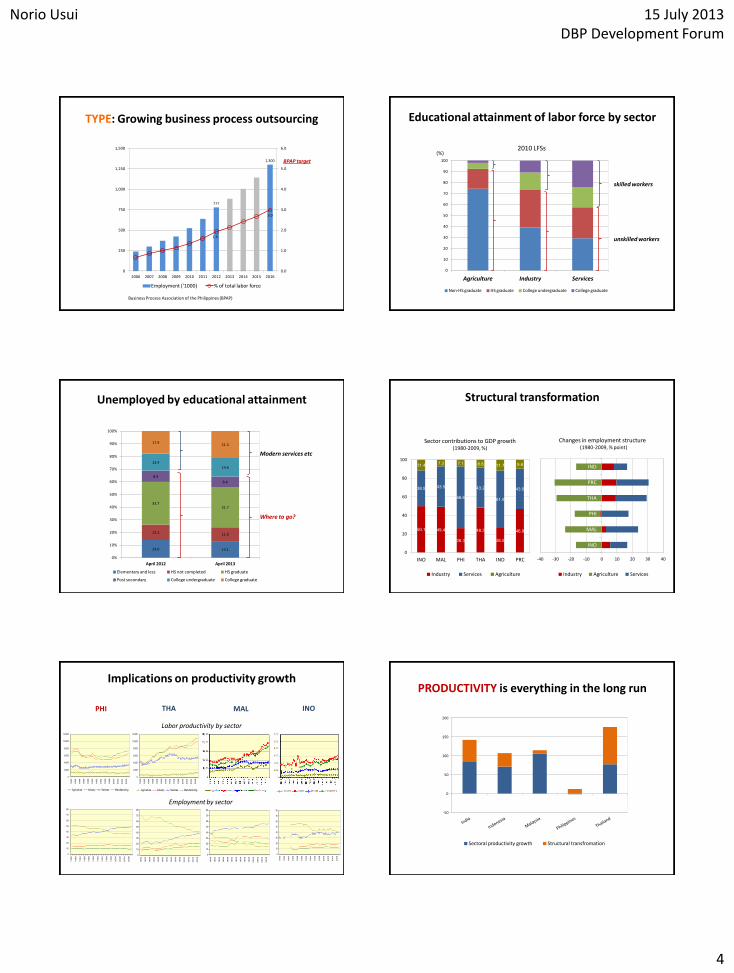

TYPE: Growing business process outsourcing

777

1,300

1.9

3.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

0

250

500

750

1,000

1,250

1,500

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Employment ('1000) % of total labor force

Business Process Association of the Philippines (BPAP)

BPAP target

Educational attainment of labor force by sector

0

10

20

30

40

50

60

70

80

90

100

Agriculture Industry Services

Non-HS graduate HS graduate College undergraduate College graduate

(%)

skilled workers

unskilled workers

2010 LFSs

Unemployed by educational attainment

14.0 13.1

12.2 11.0

33.7 31.7

8.9

8.4

13.4

14.6

17.9 21.3

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

April 2012 April 2013

Elementary and less HS not completed HS graduate

Post secondary College undergraduate College graduate

Modern services etc

Where to go?

Structural transformation

50.1 49.4

26.3

48.3

26.5

46.9

38.5 43.5

66.6

43.2

61.9

43.5

11.4 7.2 7.1 8.6 11.7 9.6

0

20

40

60

80

100

INO MAL PHI THA IND PRC

Industry Services Agriculture

-40 -30 -20 -10 0 10 20 30 40

INO

MAL

PHI

THA

PRC

IND

Industry Agriculture Services

Sector contributions to GDP growth (1980-2009, %)

Changes in employment structure (1980-2009, % point)

Implications on productivity growth

0

2,000

4,000

6,000

8,000

10,000

12,000

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

Agriculture Industry Services Manufacturing

0

2,000

4,000

6,000

8,000

10,000

12,000

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

Agriculture Industry Services Manufacturing

0

10

20

30

40

50

60

70

80

19

80

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

0

10

20

30

40

50

60

70

80

19

80

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

0

10

20

30

40

50

60

70

80

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

0

10

20

30

40

50

60

70

80

19

80

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

Employment by sector

Labor productivity by sector

PHI THA MAL INO

-50

0

50

100

150

200

Sectoral productivity growth Structural transfromation

PRODUCTIVITY is everything in the long run

Norio Usui 15 July 2013 DBP Development Forum

5

19,853

10,074

2,797

8,607 8,368

1,557 2,243

0

2,500

5,000

7,500

10,000

12,500

15,000

17,500

20,000

22,500

Indonesia Malaysia Philippines Thailand Viet Nam Cambodia Myanmar

2007

2008

2009

2010

2011

2012

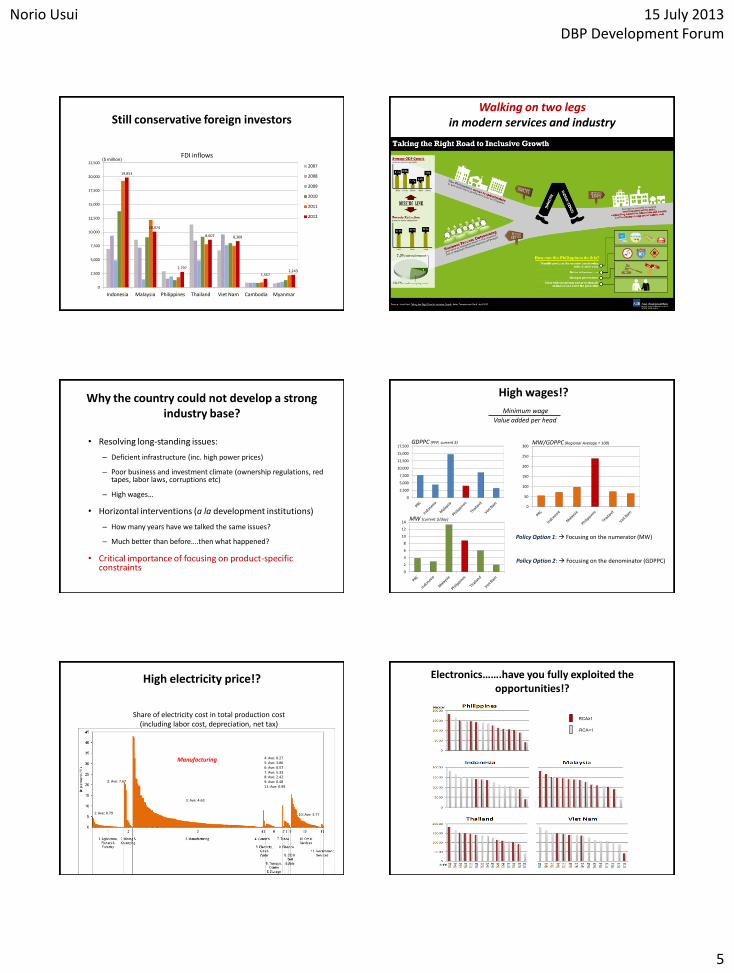

Still conservative foreign investors

($ million) FDI inflows

Walking on two legs in modern services and industry

Why the country could not develop a strong industry base?

• Resolving long-standing issues:

– Deficient infrastructure (inc. high power prices)

– Poor business and investment climate (ownership regulations, red tapes, labor laws, corruptions etc)

– High wages…

• Horizontal interventions (a la development institutions)

– How many years have we talked the same issues?

– Much better than before….then what happened?

• Critical importance of focusing on product-specific constraints

High wages!?

0

2

4

6

8

10

12

14

GDPPC (PPP, current $)

MW (current $/day)

Policy Option 1: Focusing on the numerator (MW)

Policy Option 2: Focusing on the denominator (GDPPC)

Minimum wage

Value added per head

MW/GDPPC (Regional Average = 100)

0

2,500

5,000

7,500

10,000

12,500

15,000

17,500

0

50

100

150

200

250

300

High electricity price!?

Share of electricity cost in total production cost (including labor cost, depreciation, net tax)

1: Ave: 0.79

3: Ave: 4.63

2: Ave: 7.67

4: Ave: 0.27 5: Ave: 3.86 6: Ave: 0.57 7: Ave: 5.33 8: Ave: 2.42 9: Ave: 0.48 11: Ave: 0.99

10: Ave: 3.77

Manufacturing

Electronics…….have you fully exploited the opportunities!?

RCA≥1

RCA<1

Norio Usui 15 July 2013 DBP Development Forum

6

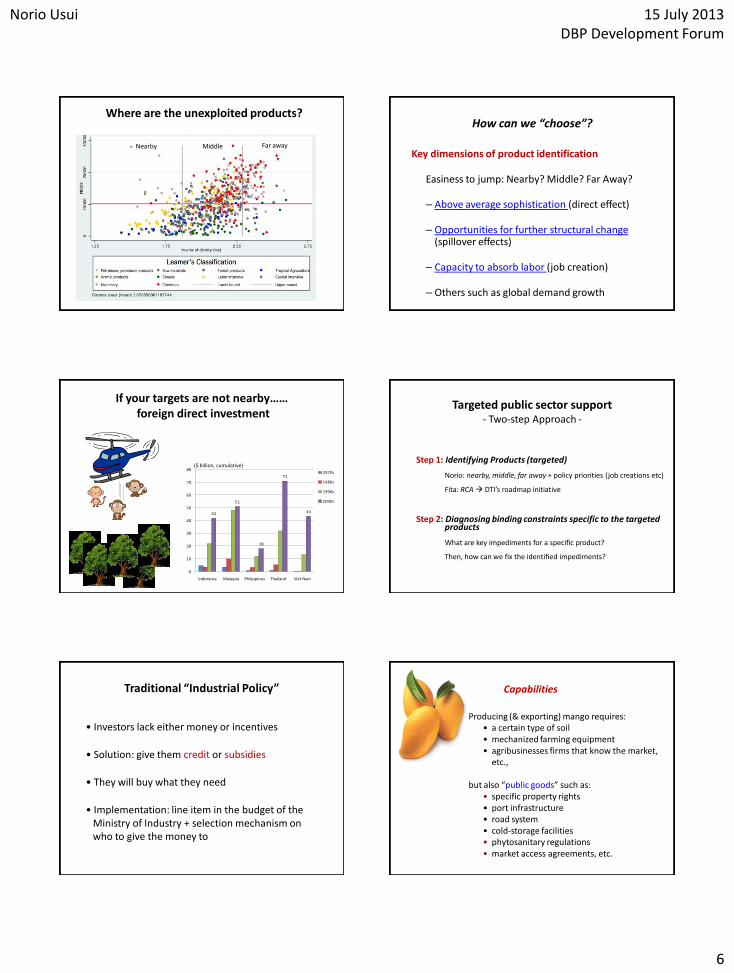

Where are the unexploited products?

Nearby Middle Far away

How can we “choose”?

Key dimensions of product identification

Easiness to jump: Nearby? Middle? Far Away?

– Above average sophistication (direct effect)

– Opportunities for further structural change (spillover effects)

– Capacity to absorb labor (job creation)

– Others such as global demand growth

If your targets are not nearby…… foreign direct investment

42

51

18

71

43

0

10

20

30

40

50

60

70

80

Indonesia Malaysia Philippines Thailand Viet Nam

1970s

1980s

1990s

2000s

($ billion, cumulative)

Targeted public sector support - Two-step Approach -

Step 1: Identifying Products (targeted)

Norio: nearby, middle, far away + policy priorities (job creations etc)

Fita: RCA DTI’s roadmap initiative

Step 2: Diagnosing binding constraints specific to the targeted products

What are key impediments for a specific product?

Then, how can we fix the identified impediments?

Traditional “Industrial Policy”

• Investors lack either money or incentives

• Solution: give them credit or subsidies

• They will buy what they need

• Implementation: line item in the budget of the Ministry of Industry + selection mechanism on who to give the money to

Producing (& exporting) mango requires: • a certain type of soil • mechanized farming equipment • agribusinesses firms that know the market,

etc.,

but also “public goods” such as: • specific property rights • port infrastructure • road system • cold-storage facilities • phytosanitary regulations • market access agreements, etc.

Capabilities

Norio Usui 15 July 2013 DBP Development Forum

7

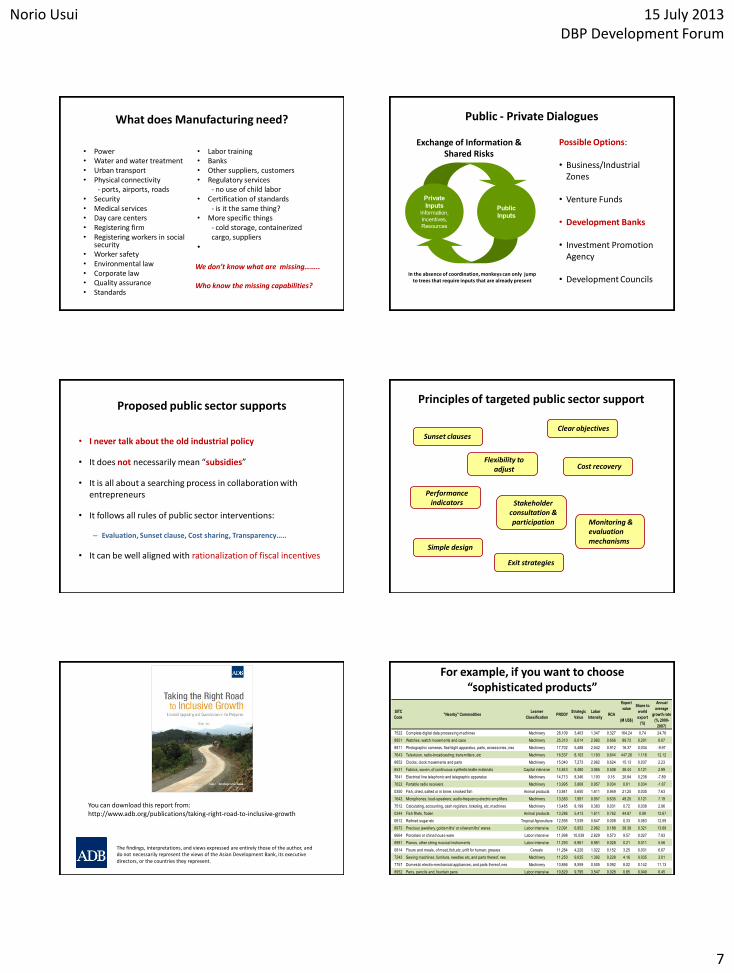

What does Manufacturing need?

• Power • Water and water treatment • Urban transport • Physical connectivity

- ports, airports, roads • Security • Medical services • Day care centers • Registering firm • Registering workers in social

security • Worker safety • Environmental law • Corporate law • Quality assurance • Standards

• Labor training • Banks • Other suppliers, customers • Regulatory services

- no use of child labor • Certification of standards

- is it the same thing? • More specific things

- cold storage, containerized cargo, suppliers

•

We don’t know what are missing…….. Who know the missing capabilities?

Public - Private Dialogues

Private

Inputs Information,

Incentives,

Resources

Public

Inputs

Exchange of Information & Shared Risks

In the absence of coordination, monkeys can only jump to trees that require inputs that are already present

Possible Options: • Business/Industrial

Zones • Venture Funds

• Development Banks

• Investment Promotion

Agency

• Development Councils

Proposed public sector supports

• I never talk about the old industrial policy

• It does not necessarily mean “subsidies”

• It is all about a searching process in collaboration with entrepreneurs

• It follows all rules of public sector interventions:

– Evaluation, Sunset clause, Cost sharing, Transparency…..

• It can be well aligned with rationalization of fiscal incentives

Principles of targeted public sector support

Sunset clauses

Exit strategies

Clear objectives

Cost recovery

Performance indicators

Simple design

Monitoring & evaluation mechanisms

Flexibility to adjust

Stakeholder consultation & participation

The findings, interpretations, and views expressed are entirely those of the author, and do not necessarily represent the views of the Asian Development Bank, its executive directors, or the countries they represent.

You can download this report from: http://www.adb.org/publications/taking-right-road-to-inclusive-growth

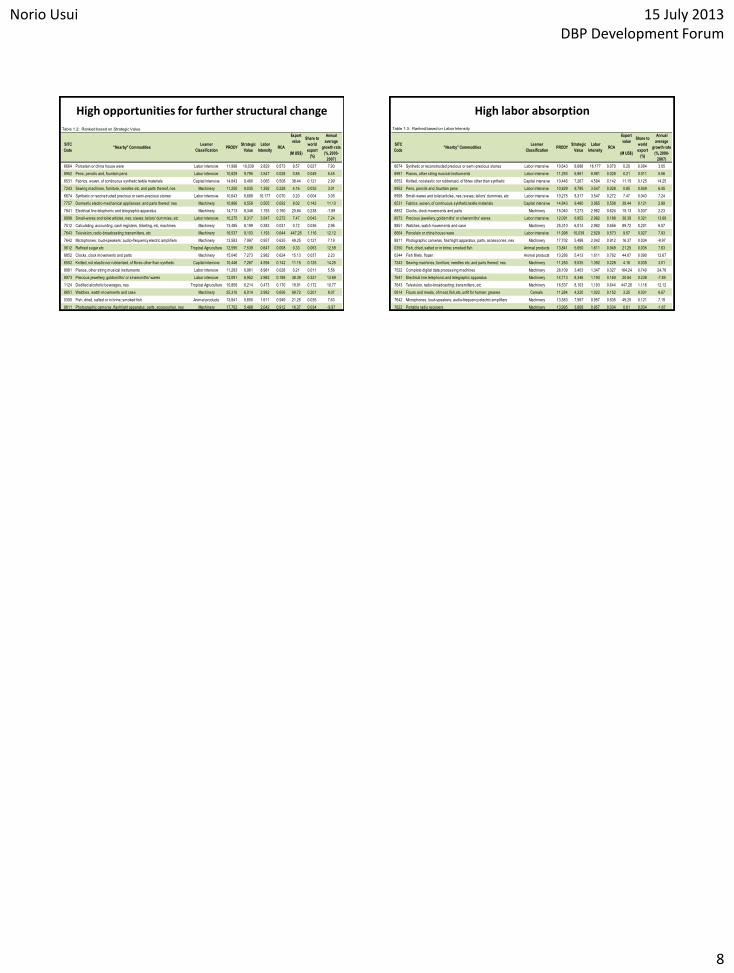

For example, if you want to choose “sophisticated products”

Export

value

(M US$)

7522 Complete digital data processing machines Machinery 28,109 3,403 1.347 0.327 164.24 0.74 24.76

8851 Watches, watch movements and case Machinery 25,310 6,014 2.982 0.656 89.72 0.201 8.07

8811 Photographic cameras, flashlight apparatus, parts, accessories, nes Machinery 17,702 5,488 2.042 0.912 16.37 0.034 -9.97

7643 Television, radio-broadcasting; transmitters, etc Machinery 16,537 8,103 1.193 0.644 447.26 1.116 12.12

8852 Clocks, clock movements and parts Machinery 15,040 7,273 2.982 0.624 15.13 0.037 2.23

6531 Fabrics, woven, of continuous synthetic textile materials Capital intensive 14,843 9,480 3.065 0.508 38.44 0.121 2.99

7641 Electrical line telephonic and telegraphic apparatus Machinery 14,713 8,346 1.193 0.16 20.84 0.238 -7.89

7622 Portable radio receivers Machinery 13,995 3,808 0.957 0.034 0.61 0.034 -1.67

0350 Fish, dried, salted or in brine; smoked fish Animal products 13,841 5,650 1.611 0.949 21.25 0.035 7.63

7642 Microphones; loud-speakers; audio-frequency electric amplifiers Machinery 13,583 7,997 0.957 0.635 49.25 0.121 7.19

7512 Calculating, accounting, cash registers, ticketing, etc, machines Machinery 13,485 8,199 0.383 0.031 0.72 0.036 2.96

0344 Fish fillets, frozen Animal products 13,286 5,413 1.611 0.762 44.87 0.09 12.67

0612 Refined sugar etc Tropical Agruculture 12,595 7,539 0.647 0.008 0.33 0.063 12.59

8973 Precious jewellery, goldsmiths' or silversmiths' wares Labor intensive 12,091 6,952 2.982 0.188 38.39 0.321 13.69

6664 Porcelain or china house ware Labor intensive 11,998 10,039 2.829 0.573 9.57 0.027 7.93

8981 Pianos, other string musical instruments Labor intensive 11,293 6,961 8.981 0.028 0.21 0.011 5.56

0814 Flours and meals, of meat, fish,etc, unfit for human; greaves Cereals 11,284 4,220 1.022 0.152 3.25 0.031 6.67

7243 Sewing machines, furniture, needles etc, and parts thereof, nes Machinery 11,250 9,035 1.392 0.228 4.16 0.035 3.01

7757 Domestic electro-mechanical appliances; and parts thereof, nes Machinery 10,866 8,559 0.505 0.092 8.02 0.142 11.13

8952 Pens, pencils and, fountain pens Labor intensive 10,829 9,795 3.547 0.028 0.85 0.049 6.45

RCA

Share to

world

export

(%)

Annual

average

growth rate

(%, 2000-

2007)

SITC

Code"Nearby" Commodities

Leamer

ClassificationPRODY

Strategic

Value

Labor

Intensity

Norio Usui 15 July 2013 DBP Development Forum

8

Table 1.2: Ranked based on Strategic Value

Export

value

(M US$)

6664 Porcelain or china house ware Labor intensive 11,998 10,039 2.829 0.573 9.57 0.027 7.93

8952 Pens, pencils and, fountain pens Labor intensive 10,829 9,795 3.547 0.028 0.85 0.049 6.45

6531 Fabrics, woven, of continuous synthetic textile materials Capital intensive 14,843 9,480 3.065 0.508 38.44 0.121 2.99

7243 Sewing machines, furniture, needles etc, and parts thereof, nes Machinery 11,250 9,035 1.392 0.228 4.16 0.035 3.01

6674 Synthetic or reconstructed precious or semi-precious stones Labor intensive 10,643 8,688 16.177 0.070 0.20 0.004 3.05

7757 Domestic electro-mechanical appliances; and parts thereof, nes Machinery 10,866 8,559 0.505 0.092 8.02 0.142 11.13

7641 Electrical line telephonic and telegraphic apparatus Machinery 14,713 8,346 1.193 0.160 20.84 0.238 -7.89

8998 Small-wares and toilet articles, nes; sieves; tailors' dummies, etc Labor intensive 10,275 8,317 3.547 0.272 7.47 0.043 7.24

7512 Calculating, accounting, cash registers, ticketing, etc, machines Machinery 13,485 8,199 0.383 0.031 0.72 0.036 2.96

7643 Television, radio-broadcasting; transmitters, etc Machinery 16,537 8,103 1.193 0.644 447.26 1.116 12.12

7642 Microphones; loud-speakers; audio-frequency electric amplifiers Machinery 13,583 7,997 0.957 0.635 49.25 0.121 7.19

0612 Refined sugar etc Tropical Agruculture 12,595 7,539 0.647 0.008 0.33 0.063 12.59

8852 Clocks, clock movements and parts Machinery 15,040 7,273 2.982 0.624 15.13 0.037 2.23

6552 Knitted, not elastic nor rubberized, of fibres other than synthetic Capital intensive 10,446 7,267 4.594 0.142 11.15 0.125 14.25

8981 Pianos, other string musical instruments Labor intensive 11,293 6,961 8.981 0.028 0.21 0.011 5.56

8973 Precious jewellery, goldsmiths' or silversmiths' wares Labor intensive 12,091 6,952 2.982 0.188 38.39 0.321 13.69

1124 Distilled alcoholic beverages, nes Tropical Agruculture 10,808 6,214 0.473 0.170 18.91 0.172 10.77

8851 Watches, watch movements and case Machinery 25,310 6,014 2.982 0.656 89.72 0.201 8.07

0350 Fish, dried, salted or in brine; smoked fish Animal products 13,841 5,650 1.611 0.949 21.25 0.035 7.63

8811 Photographic cameras, flashlight apparatus, parts, accessories, nes Machinery 17,702 5,488 2.042 0.912 16.37 0.034 -9.97

RCA

Share to

world

export

(%)

Annual

average

growth rate

(%, 2000-

2007)

SITC

Code"Nearby" Commodities

Leamer

ClassificationPRODY

Strategic

Value

Labor

Intensity

High opportunities for further structural change Table 1.3: Ranked based on Labor Intensity

Export

value

(M US$)

6674 Synthetic or reconstructed precious or semi-precious stones Labor intensive 10,643 8,688 16.177 0.070 0.20 0.004 3.05

8981 Pianos, other string musical instruments Labor intensive 11,293 6,961 8.981 0.028 0.21 0.011 5.56

6552 Knitted, not elastic nor rubberized, of fibres other than synthetic Capital intensive 10,446 7,267 4.594 0.142 11.15 0.125 14.25

8952 Pens, pencils and, fountain pens Labor intensive 10,829 9,795 3.547 0.028 0.85 0.049 6.45

8998 Small-wares and toilet articles, nes; sieves; tailors' dummies, etc Labor intensive 10,275 8,317 3.547 0.272 7.47 0.043 7.24

6531 Fabrics, woven, of continuous synthetic textile materials Capital intensive 14,843 9,480 3.065 0.508 38.44 0.121 2.99

8852 Clocks, clock movements and parts Machinery 15,040 7,273 2.982 0.624 15.13 0.037 2.23

8973 Precious jewellery, goldsmiths' or silversmiths' wares Labor intensive 12,091 6,952 2.982 0.188 38.39 0.321 13.69

8851 Watches, watch movements and case Machinery 25,310 6,014 2.982 0.656 89.72 0.201 8.07

6664 Porcelain or china house ware Labor intensive 11,998 10,039 2.829 0.573 9.57 0.027 7.93

8811 Photographic cameras, flashlight apparatus, parts, accessories, nes Machinery 17,702 5,488 2.042 0.912 16.37 0.034 -9.97

0350 Fish, dried, salted or in brine; smoked fish Animal products 13,841 5,650 1.611 0.949 21.25 0.035 7.63

0344 Fish fillets, frozen Animal products 13,286 5,413 1.611 0.762 44.87 0.090 12.67

7243 Sewing machines, furniture, needles etc, and parts thereof, nes Machinery 11,250 9,035 1.392 0.228 4.16 0.035 3.01

7522 Complete digital data processing machines Machinery 28,109 3,403 1.347 0.327 164.24 0.740 24.76

7641 Electrical line telephonic and telegraphic apparatus Machinery 14,713 8,346 1.193 0.160 20.84 0.238 -7.89

7643 Television, radio-broadcasting; transmitters, etc Machinery 16,537 8,103 1.193 0.644 447.26 1.116 12.12

0814 Flours and meals, of meat, fish,etc, unfit for human; greaves Cereals 11,284 4,220 1.022 0.152 3.25 0.031 6.67

7642 Microphones; loud-speakers; audio-frequency electric amplifiers Machinery 13,583 7,997 0.957 0.635 49.25 0.121 7.19

7622 Portable radio receivers Machinery 13,995 3,808 0.957 0.034 0.61 0.034 -1.67

RCA

Share to

world

export

(%)

Annual

average

growth rate

(%, 2000-

2007)

SITC

Code"Nearby" Commodities

Leamer

ClassificationPRODY

Strategic

Value

Labor

Intensity

High labor absorption

Related Documents