NPTEL International Finance Vinod Gupta School Managemant , IIT. Kharagpur . Module 10 Foreign Exchange Contracts: Swaps and Option s Developed b y: Dr. Prabi na Rajib As so ci ate Pro fes sor (Fi nan ce & A cc oun ts ) Vinod Gupt a Schoo l of Management IIT Kharagpur, 721 302 Email: [email protected] J oi nt In it ia t iv e IITs an d IISc – Fun d ed b y MHRD - 1 -

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

7/28/2019 Module10- forex

http://slidepdf.com/reader/full/module10-forex 1/13

NPTELInternational FinanceVinod Gupta School Managemant , IIT. Kharagpur .

Module 10Foreign Exchange Contracts:

Swaps and Options

Developed by: Dr. Prabina Rajib Associate Professor (Finance & Accounts)

Vinod Gupta School of ManagementIIT Kharagpur, 721 302

Email: [email protected]

J oint Initiative IITs and IISc – Funded by MHRD - 1 -

7/28/2019 Module10- forex

http://slidepdf.com/reader/full/module10-forex 2/13

NPTELInternational FinanceVinod Gupta School Managemant , IIT. Kharagpur .

Forex market players can trade foreign exchange in differing maturities and using

different type of instruments i.e, cash, tom , spot, forward, futures, swaps and options

contracts. In this session, foreign currency swaps and options are discussed. Though

Indian companies are buying/selling options in the OTC market (with banks as

counterparties), exchange traded options have started in India very recently. The contract

specifications of options contract trading United Stock Exchange of India has also been

discussed in detail. Indian companies have incurred major derivatives loss by entering

into zero cost derivatives. The structure of zero cost derivatives has been also discussed.

Session 10Foreign Exchange Contracts: Swaps and Options

Highlight & Motivation:

Learning Objectives

Hence the objective of this module is to understand:

• Foreign currency swaps

• Foreign currency options

o Long/short call and put options

o American and European option

o ATM/OTM/ITM options.

• Exchange traded option contact specifications : A detailed discussion

o Zero cost derivatives.

J oint Initiative IITs and IISc – Funded by MHRD - 2 -

7/28/2019 Module10- forex

http://slidepdf.com/reader/full/module10-forex 3/13

NPTELInternational FinanceVinod Gupta School Managemant , IIT. Kharagpur .

Besides spot, forward and futures contracts, companies also regularly enter into currency

swaps, and option contracts to mitigate foreign exchange risk. In the following sections,

very briefly details about foreign currency swaps and options have been discussed asthese would be discussed in greater detail in subsequent modules.

10.1: Primer to Foreign currency swaps, and options:

10.2 Foreign Currency Swaps:

Very briefly, currency swap works like this: An Indian company, XYZ Co. took anECB

(External Commercial Borrowing) loan of USD 250mn for 6 years at a fixed interest

rate of 5.5%. After two years, remaining time to maturity is 4 years. XYZ Co. wants to

shift this USD obligation and wants to pay the interest and principal in INR. The Indian

company fears that INR to depreciate – hence increasing its INR expenditure to servicethe foreign currency denominated interest as well as principal. It approaches different

banks for swapping its USD obligations. BBK bank agrees to be the counterparty for this

swap at an 8.5% per annum. Once both parties agree, the following swap payment

happens between XYZ Co. and BBK Bank.

• In the beginning of the contract, XYZ Co. gives 250mn USD to BBK Bank. BBK

Bank pays INR 11750 mn (equivalent of 250mn USD at a rate of INR 47/USD) to

XYZ CO.

• For the next 4 years, BBK bank pays USD 13.75mn (5.5% of USD 200mn) to

XYZ Co. In return, XYZ Co. pays INR 998.75mn (8.5% of INR 11750mn) to

BBK Bank.

• After the 4th year, BBK bank pays USD 250mn to XYZ Co. XYZ Co. returns

INR 11750mn to BBK Bank.

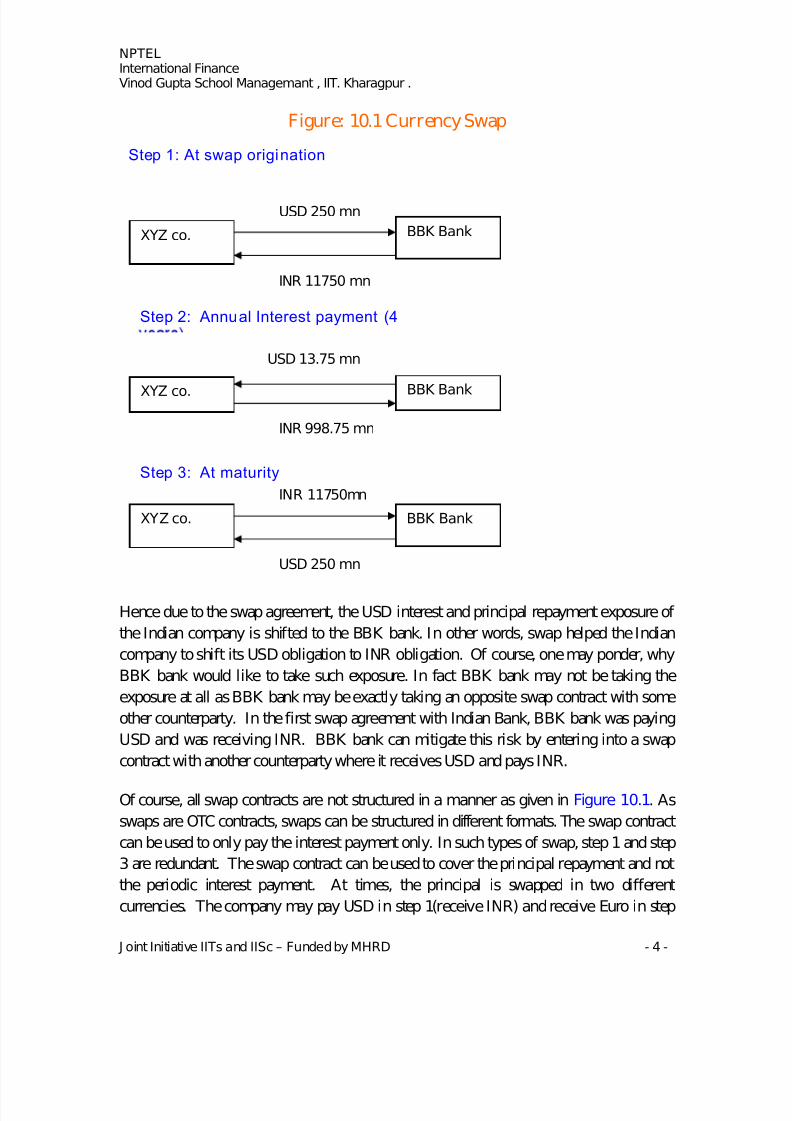

The following figure, Figure 10.1 indicates the three steps in swap contract graphically.

J oint Initiative IITs and IISc – Funded by MHRD - 3 -

7/28/2019 Module10- forex

http://slidepdf.com/reader/full/module10-forex 4/13

NPTELInternational FinanceVinod Gupta School Managemant , IIT. Kharagpur .

Figure: 10.1 Currency Swap

BBK BankXYZ co.

USD 250 mn

INR 11750 mn

XYZ co. BBK Bank

USD 13.75 mn

INR 998.75 mn

Step 1: At swap origination

Step 2: Annual Interest payment (4

Step 3: At maturity

XYZ co. BBK Bank

INR 11750mn

USD 250 mn

Hence due to the swap agreement, the USD interest and principal repayment exposure of

the Indian company is shifted to the BBK bank. In other words, swap helped the Indian

company to shift its USD obligation to INR obligation. Of course, one may ponder, why

BBK bank would like to take such exposure. In fact BBK bank may not be taking the

exposure at all as BBK bank may be exactly taking an opposite swap contract with some

other counterparty. In the first swap agreement with Indian Bank, BBK bank was paying

USD and was receiving INR. BBK bank can mitigate this risk by entering into a swap

contract with another counterparty where it receives USD and pays INR.

Of course, all swap contracts are not structured in a manner as given in Figure 10.1. As

swaps are OTC contracts, swaps can be structured in different formats. The swap contract

can be used to only pay the interest payment only. In such types of swap, step 1 and step

3 are redundant. The swap contract can be used to cover the principal repayment and not

the periodic interest payment. At times, the principal is swapped in two different

currencies. The company may pay USD in step 1(receive INR) and receive Euro in step

J oint Initiative IITs and IISc – Funded by MHRD - 4 -

7/28/2019 Module10- forex

http://slidepdf.com/reader/full/module10-forex 5/13

NPTELInternational FinanceVinod Gupta School Managemant , IIT. Kharagpur .

3 (pay INR). Depending upon the client’s requirement, banks structure swaps with

varying features.

10.3: Foreign Currency Options: Brief Introduction to Call and Put Option.

Companies buy and sell call and put options to hedge their foreign times exchange

exposure as well as at times indulge in speculative activities. Options on foreign

currency are offered by banks as OTC product or can be bought and sold in exchanges.

Before we proceed to understand foreign currency options in greater details, let us

understand the 4 building blocks of options, namely long call, short call, long put and

short put. However, if a reader has not been exposed to these concepts earlier, then it is

advisable to read a derivative text book on options to get a deeper understanding of

options before proceeding with the remaining part of this session.

In a call option, the option buyer (long call position holder) has the right to buy theunderlying currency at the maturity at the exercise price. For example, an importer

wanting to hedge the USD risk, enters into long call option for 20,000 USD at

INR 44.45/USD with contract maturing after 15 days from today. The counterparty to the

importer takes a short call option. On T+15 day, the spot rate is INR 43.80/USD.

Whether the importer will exercise his option to buy USD from the counterparty or not?

In this case, theoption will not be exercised as the importer is better off buying the USD

from spot market than from the short call position holder. The importer will exercise call

option, when the spot price is higher than INR 44.45/USD—when INR depreciates.

In a put option, the option buyer (long put position holder) has the right to sell the

underlying currency at the maturity at the exercise price. For example, an exporter

wanting to hedge the USD risk, enters into long put option for 18950 USD at

INR 44.45/USD with contract maturing after 15 days from today. The counterparty to the

exporter takes a short put option. On T+15 day, the spot rate is INR 43.80/USD.

Whether the exporter will exercise his option to sell USD to the counterparty or not? In

this case, theoption will be exercised as the exporter can sell USD at INR44.45 per USD

due to the option contract. Without the option, the exporter would have sold USD at INR

43.80/USD. The exporter will exercise his put option, when the spot price is lesser thanINR 44.45/USD—when INR appreciates.

J oint Initiative IITs and IISc – Funded by MHRD - 5 -

7/28/2019 Module10- forex

http://slidepdf.com/reader/full/module10-forex 6/13

NPTELInternational FinanceVinod Gupta School Managemant , IIT. Kharagpur .

Depending upon whether options can be exercised only on maturity date or on or before

maturity date, options are categorized as European and American respectively. An

option is in-the-money (ITM) if it is profitable to exercise. For a call option, if the spot

exchange rate is higher than the strike exchange rate, then it is an ITM option. For an

ITM put option, the spot exchange rate is lesser than the strike exchange rate.

An option is out-of-money (OTM) when it is not profitable to exercise these options.

For a call option, when the spot exchange rate is lesser than the strike exchange rate, it is

an OTM option. For a put option, when the spot exchange rate is higher than the strike

exchange rate, it is an OTM option.

Anat-the-money (ATM) option is when the exercise price is at par with the spot price.

Foreign currency options are available both in OTC market as well as traded in Indian

exchanges. OTC options are offered by banks with banks taking one taking one side in

each option contract.

10.4: Currency Options in India:

Though little dated, details given in Box 10.4 explain the call and option concepts as well

as highlight the popularity of currency options offered by Indian Banks.

J oint Initiative IITs and IISc – Funded by MHRD - 6 -

7/28/2019 Module10- forex

http://slidepdf.com/reader/full/module10-forex 7/13

NPTELInternational FinanceVinod Gupta School Managemant , IIT. Kharagpur .

A call option, on the other hand, is a right to buy - so a USD call option would give the buyer a rightbut not an obligation to buy dollars at a strike price, at a particular exercise date.

Plain vanilla options are the put or call options, which can be exercised by corporates. A putoption is a right to sell - so purchase of a USD put will give a corporate the right but not theobligation to sell dollars at a particular date, at a pre-determined rate, known as the strike price. An exporter, who would want to sell dollars if the market moves against him but does not want

to sell dollars if the market exchange rate is in his favour, would normally buy a USD put.

Not only have the plain vanilla options, active up to one year, gained popularity, options havinga time period of over a year have also seen a demand. "Deals have been struck for five-yearoptions too, with two to three years instruments also being traded in large amounts," MrChaudhary said.

According to dealers, the view on the rupee has changed, as now the expectation is of a 44.00 levelagainst the anticipation of a 47.50 level nearly two months ago. With the dollar weakening across allmajor currencies, the rupee is expected to appreciate, but this has failed to assuage sentiments giventhe high volatility in the dollar-rupee exchange market.

"Rupee options are increasing in popularity, as the view on the domestic currency is changing," said Mr Abhishek Chaudhary, forex options trader, ICICI Bank. He said ICICI Bank was an activeplayer in the rupee options market and volumes transacted by the bank had doubled recently.Over the

last couple of months, nearly a 300-per cent jump in business had been recorded with about $1.5billion worth of deals being transacted.

If an exporter books a forward contract, he is bound to fulfil it at the due date, while they arenot tied down to an exchange rate in an option. In a forward contract, merchants cannot takeadvantage of a subsequent movement of exchange rates in their favour.

According to traders, earlier a secular movement in the rupee was observed but now there is inter-day

volatility. So corporates are getting edgy about the direction of the rupee. Even with the rupeeappreciating uni-directionally to 45.04/05 levels from the 45.75 levels seen in mid-October, volatilityhas increased, as the rupee moves into the 10-15 paise band in a day.

The rupee options market has seen increased activity with leveraged options finding favour with

corporates in recent times. Daily volumes have increased by nearly 50 % to reach a turnover of about$50 million to $100 million, compared to a daily turnover of $25 million to $50 million a month ortwo back, dealers said. The reason for the popularity of these instruments over forwards is thatoptions do not confer an obligation on the buyer to perform a contract,dealers said. An option isa contract, which gives the buyer a right but not an obligation to fulfill the contract on a duedate; a premium is required to be paid to the ̀ writer' or seller of the option for this contract.

Box 10.4 Rupee options a hit among corporateshttp://www.thehindubusinessl ine.com/2004/11/23/stories/2004112303180300.htm

J oint Initiative IITs and IISc – Funded by MHRD - 7 -

7/28/2019 Module10- forex

http://slidepdf.com/reader/full/module10-forex 8/13

NPTELInternational FinanceVinod Gupta School Managemant , IIT. Kharagpur .

Besides OTC contracts, currency options for many currency pairs are available for

trading through exchanges. Annexure 10.2 highlights US Dollar INR options contracts

specifications trading at United Stock exchanges of India. In Section 10.5, the contract

specification is explained in detail. Size of each contract is for 1000 USD i.e, a long call

(put) option gives the buyer the right to buy (sell) 1000 USD. The option premium is

quoted in INR terms. All options traded areEuropean style. Theoption premium tick

size is in INR 0.0025. At a given point of time, three monthly contracts and three

quarterly contracts are available. For example, in the month of August 2011, contract

maturing on August 2011, September 2011, October 2011 as well as December 2011,

March 2012 and June 2012 contracts are available. Hence at a given point of time, a

trader can buy/sell options upto a maximum period of 9 months.Strike price indicates at

a given point of time, 12 ITM, 12 OTM and 1 ATM option will be available for trading.

Strike price interval indicates the price the difference between consecutive two strike

prices. Options strike price are in the multiple of INR 0.25. Exercise at expiry indicates

that open positions results in delivery of both currencies. For example, if a trader as 15

open long call options at an exercise price of INR 40.20, then on the maturity date, the

trader pays INR 603,000 and receives USD 15000 from the short call position holder.

Position limit indicates the maximum open position a member can take depending on the

category of the trader. Initial margin and extreme moss margin is calculated in a similar

manner as that of currency futures explained in Session 9. Settlement of premium

indicates that option premium is paid by the buyer in cash on day T and paid out to seller

on T+1 day.

Table 10.1 shows a snapshot of options order book (USD/INR) at United StockExchange of India.

J oint Initiative IITs and IISc – Funded by MHRD - 8 -

7/28/2019 Module10- forex

http://slidepdf.com/reader/full/module10-forex 9/13

NPTELInternational FinanceVinod Gupta School Managemant , IIT. Kharagpur .

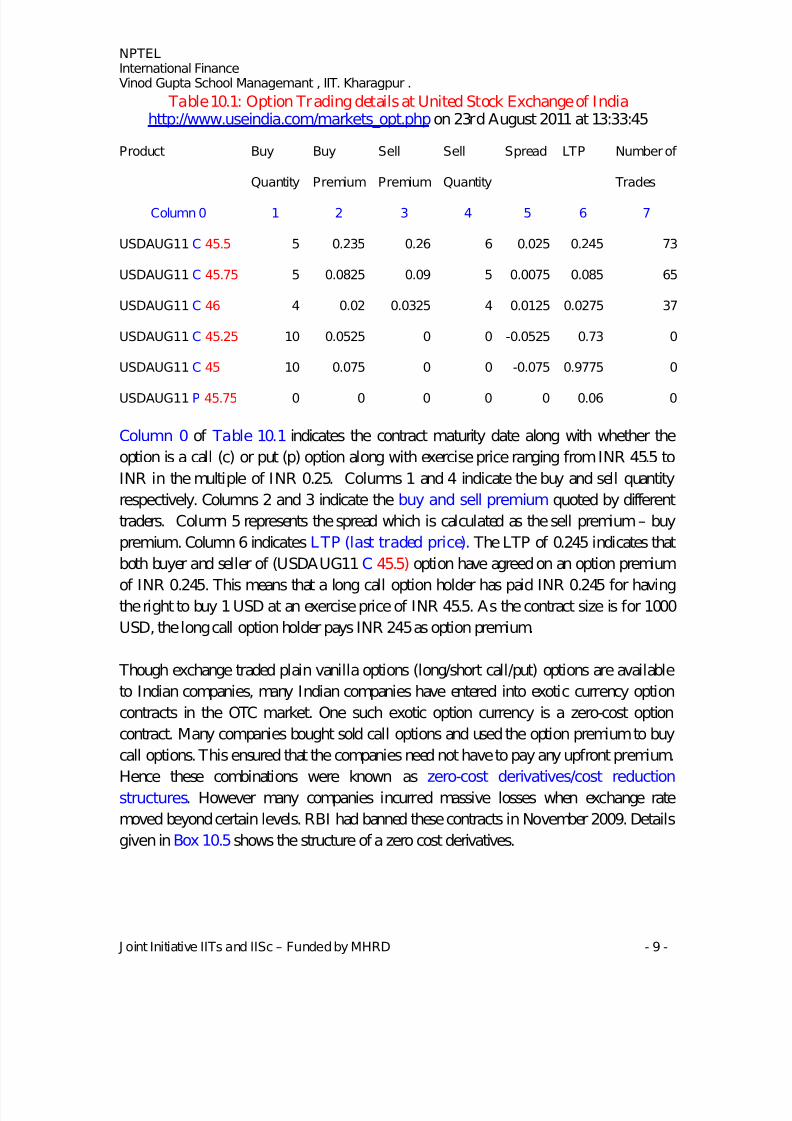

Table 10.1: Option Trading details at United Stock Exchange of Indiahttp://www.useindia.com/markets_opt.phpon 23rd August 2011 at 13:33:45

Product Buy Buy Sell Sell Spread LTP Number of

Quantity Premium Premium Quantity Trades

Column 0 1 2 3 4 5 6 7

USDAUG11 C 45.5 5 0.235 0.26 6 0.025 0.245 73

USDAUG11 C 45.75 5 0.0825 0.09 5 0.0075 0.085 65

USDAUG11 C 46 4 0.02 0.0325 4 0.0125 0.0275 37

USDAUG11 C 45.25 10 0.0525 0 0 -0.0525 0.73 0

USDAUG11 C 45 10 0.075 0 0 -0.075 0.9775 0

USDAUG11 P 45.75 0 0 0 0 0 0.06 0

Column 0 of Table 10.1 indicates the contract maturity date along with whether the

option is a call (c) or put (p) option along with exercise price ranging from INR 45.5 to

INR in the multiple of INR 0.25. Columns 1 and 4 indicate the buy and sell quantity

respectively. Columns 2 and 3 indicate the buy and sell premium quoted by different

traders. Column 5 represents the spread which is calculated as the sell premium – buy

premium. Column 6 indicates LTP (last traded price). The LTP of 0.245 indicates that

both buyer and seller of (USDAUG11C 45.5) option have agreed on an option premium

of INR 0.245. This means that a long call option holder has paid INR 0.245 for havingthe right to buy 1 USD at an exercise price of INR 45.5. As the contract size is for 1000

USD, the long call option holder pays INR 245 as option premium.

Though exchange traded plain vanilla options (long/short call/put) options are available

to Indian companies, many Indian companies have entered into exotic currency option

contracts in the OTC market. One such exotic option currency is a zero-cost option

contract. Many companies bought sold call options and used the option premium to buy

call options. This ensured that the companies need not have to pay any upfront premium.

Hence these combinations were known as zero-cost derivatives/cost reduction

structures. However many companies incurred massive losses when exchange rate

moved beyond certain levels. RBI had banned these contracts in November 2009. Details

given inBox 10.5shows the structure of a zero cost derivatives.

J oint Initiative IITs and IISc – Funded by MHRD - 9 -

7/28/2019 Module10- forex

http://slidepdf.com/reader/full/module10-forex 10/13

NPTELInternational FinanceVinod Gupta School Managemant , IIT. Kharagpur .

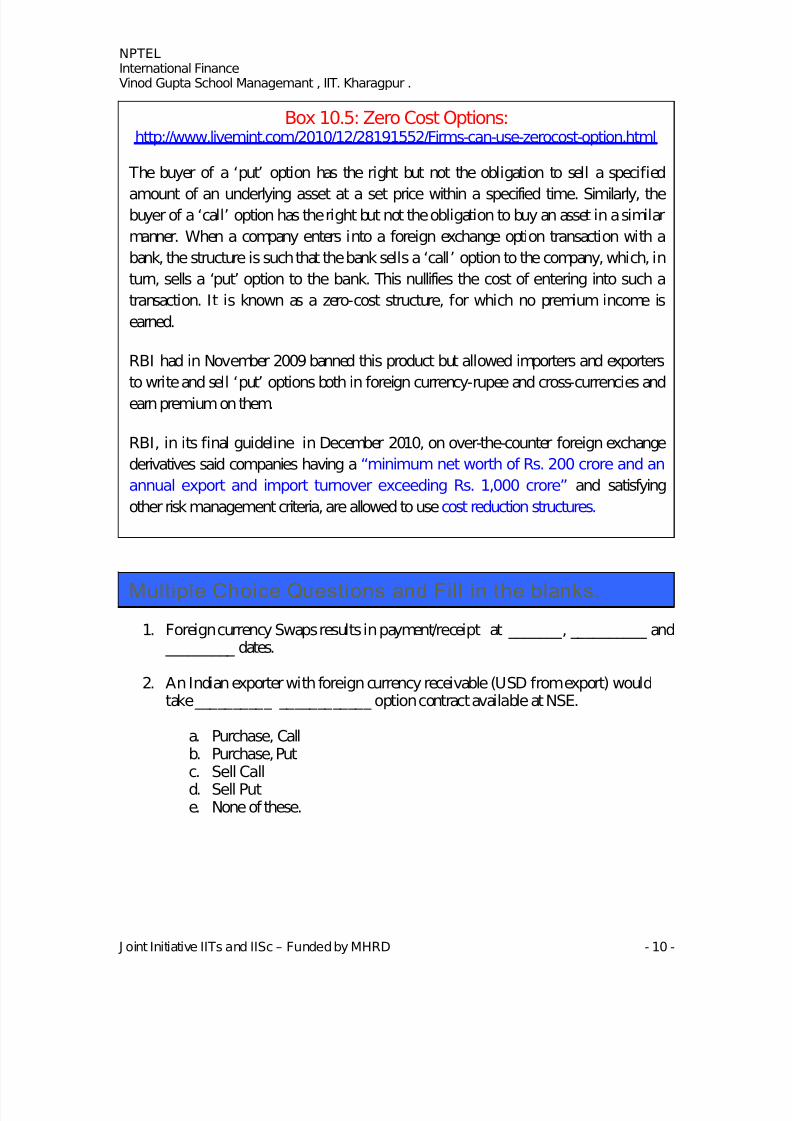

RBI, in its final guideline in December 2010, on over-the-counter foreign exchange

derivatives said companies having a “minimum net worth of Rs. 200 crore and an

annual export and import turnover exceeding Rs. 1,000 crore” and satisfying

other risk management criteria, are allowed to usecost reduction structures.

RBI had in November 2009 banned this product but allowed importers and exporters

to write and sell ‘put’ options both in foreign currency-rupee and cross-currencies and

earn premium on them.

The buyer of a ‘put’ option has the right but not the obligation to sell a specified

amount of an underlying asset at a set price within a specified time. Similarly, thebuyer of a ‘call’ option has the right but not the obligation to buy an asset in a similar

manner. When a company enters into a foreign exchange option transaction with a

bank, the structure is such that the bank sells a ‘call’ option to the company, which, in

turn, sells a ‘put’ option to the bank. This nullifies the cost of entering into such a

transaction. It is known as a zero-cost structure, for which no premium income is

earned.

Box 10.5: Zero Cost Options:http://www.livemint.com/2010/12/28191552/Firms-can-use-zerocost-option.html

Multiple Choice Questions and Fill in the blanks.

1. Foreign currency Swaps results in payment/receipt at _______, __________ and _________ dates.

2. An Indian exporter with foreign currency receivable (USD from export) wouldtake __________ ____________ option contract available at NSE.

a. Purchase, Callb. Purchase, Putc. Sell Call

d. Sell Pute. None of these.

J oint Initiative IITs and IISc – Funded by MHRD - 10 -

7/28/2019 Module10- forex

http://slidepdf.com/reader/full/module10-forex 11/13

NPTELInternational FinanceVinod Gupta School Managemant , IIT. Kharagpur .

3. If a call option has a strike price of INR 42.35/USD. If the spot rate on thematurity date is INR 43.35/USD. The call option is

a. An ITM optionb. An OTM optionc. An ATM Option

4. If a put option has a strike price of INR 42.35/USD. If the spot rate on thematurity date is INR 43.35. The put option is

a. An ITM optionb. An OTM optionc. An ATM Option

Short Questions:

1. A trader enters into long put options on USD/INR exchange rate and paid anoption premium of Rs. 0.125. The exercise price is INR 45.20. At what spot rate,

the long position holder will exercise his put options and what exchange rate, thelong put option holder will make profit.

2. What are zero cost derivatives and why a company would invest in theseinstruments?

3. Explain why forward/futures/option contracts are zero-sum game?

4. Foreign Currency swap contracts help companies to shift their liabilities from onecurrency to another currency? Give an example to justify the above statement?

Answers to Multiple Choice Questions:

1. Swap origination, Annual interest payment/receipt, At maturity.

2. Purchase a put option to sell USD at a later stage.

3. a

4. b

J oint Initiative IITs and IISc – Funded by MHRD - 11 -

7/28/2019 Module10- forex

http://slidepdf.com/reader/full/module10-forex 12/13

NPTELInternational FinanceVinod Gupta School Managemant , IIT. Kharagpur .

• Leading exporters unwinding forward contracts, The Economic Times, 23rd July

2008. http://economictimes.indiatimes.com/articleshow/msid-3266587,prtpage-1.cms

• Rupee hit by an invisible force. DNA MONEY 16th June 2008.http://sify.com/finance/fullstory.php?id=1475907

• Foreign Exchange Futures contract. http://www.nseindia.com • Foreign Exchange options contracthttp://www.useindia.com

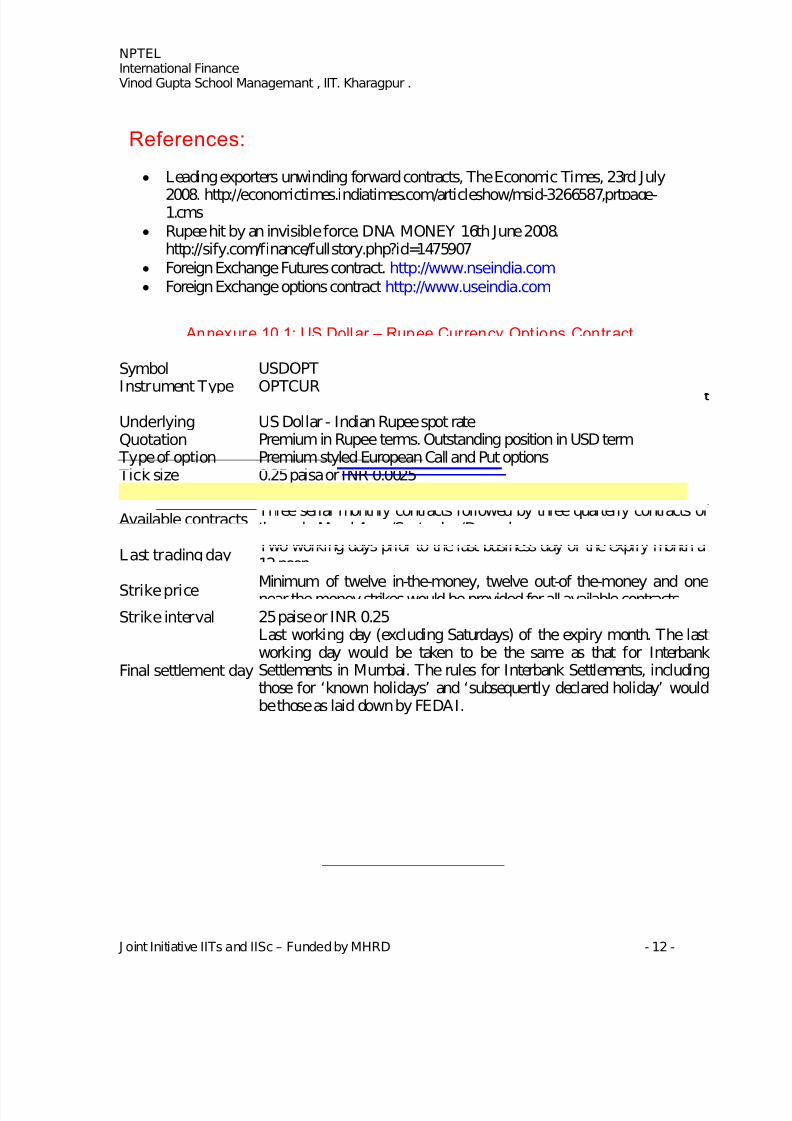

Annexure 10.1: US Dollar – Rupee Currency Opt ions Contract.http://www.useindia.com

Symbol USDOPT

Instrument Type OPTCURSize of Contract 1 contract is for 1000 USD (Lot size)Underlying US Dollar - Indian Rupee spot rateQuotation Premium in Rupee terms. Outstanding position in USD term Type of option Premium styled European Call and Put options Tick size 0.25 paisa or INR 0.0025 Trading hours Monday to Friday ( 9:00 a.m. to 5:00 p.m. )

Available contracts Three serial monthly contracts followed by three quarterly contracts of the cycle March/June/September/December

Last trading day Two working days prior to the last business day of the expiry month a12 noon.

Strike price Minimum of twelve in-the-money, twelve out-of the-money and onenear-the-money strikes would be provided for all available contractsStrike interval 25 paise or INR 0.25

Final settlement day

Last working day (excluding Saturdays) of the expiry month. The lastworking day would be taken to be the same as that for InterbankSettlements in Mumbai. The rules for Interbank Settlements, includingthose for ‘known holidays’ and ‘subsequently declared holiday’ wouldbe those as laid down by FEDAI.

References:

J oint Initiative IITs and IISc – Funded by MHRD - 12 -

7/28/2019 Module10- forex

http://slidepdf.com/reader/full/module10-forex 13/13

NPTELInternational FinanceVinod Gupta School Managemant , IIT. Kharagpur .

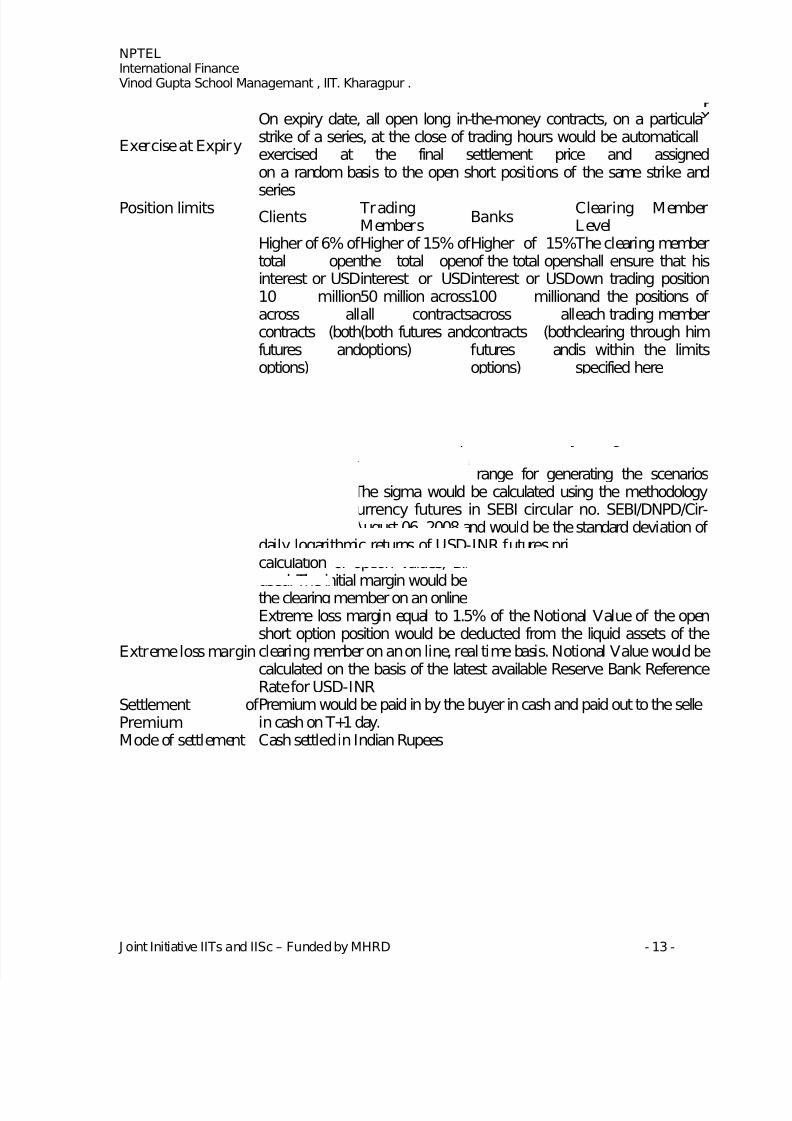

Exercise at Expiry

On expiry date, all open long in-the-money contracts, on a particulastrike of a series, at the close of trading hours would be automaticallexercised at the final settlement price and assignedon a random basis to the open short positions of the same strike and

seriesPosition limitsClients

TradingMembers

BanksClearing MemberLevel

Higher of 6% of total openinterest or USD10 millionacross allcontracts (bothfutures and

options)

Higher of 15% of the total open

Higher of 15%

interest or USDof the total open

50 million acrossinterest or USD

all contracts100 million

(both futures andacross allcontracts (both

options) futures and

The clearing membershall ensure that hisown trading positionand the positions of each trading memberclearing through himis within the limitsspecified hereoptions)

The Initial Margin requirement would be based on a worst scenario lossof a portfolio of an individual client comprising his positions in optionsand futures contracts on the same underlying across different maturitiesand across various scenarios of price and volatility changes. In order toachieve this, the price range for generating the scenarios would be 3.5standard deviation and volatility range for generating the scenarioswould be 3%. The sigma would be calculated using the methodologyspecified for currency futures in SEBI circular no. SEBI/DNPD/Cir-38/2008 dated August 06, 2008 and would be the standard deviation of daily logarithmic returns of USD-INR futures price. For the purpose of calculation of option values, Black-Scholes pricing model would be

used. The initial margin would be deducted from the liquid net worth of the clearing member on an online, real time basis.

Initial margin

Extreme loss margin equal to 1.5% of the Notional Value of the openshort option position would be deducted from the liquid assets of theclearing member on an on line, real time basis. Notional Value would becalculated on the basis of the latest available Reserve Bank ReferenceRate for USD-INR

Extreme loss margin

Settlement of Premium would be paid in by the buyer in cash and paid out to the sellePremium in cash on T+1 day.Mode of settlement Cash settled in Indian Rupees

J oint Initiative IITs and IISc – Funded by MHRD - 13 -

Related Documents