Mobile Insurance: Past, Present & Future 13 November 2014 Peter Gross Regional Director – MicroEnsure Africa

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Mobile Insurance:

Past, Present & Future

13 November 2014

Peter Gross

Regional Director – MicroEnsure Africa

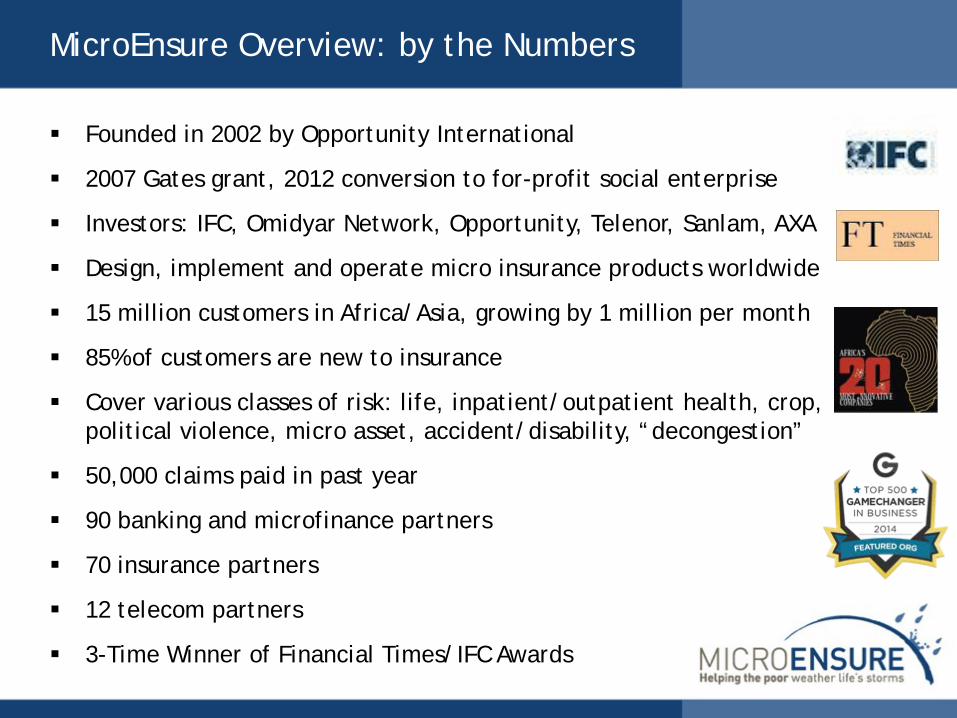

MicroEnsure Overview: by the Numbers

Founded in 2002 by Opportunity International

2007 Gates grant, 2012 conversion to for-profit social enterprise

Investors: IFC, Omidyar Network, Opportunity, Telenor, Sanlam, AXA

Design, implement and operate micro insurance products worldwide

15 million customers in Africa/Asia, growing by 1 million per month

85% of customers are new to insurance

Cover various classes of risk: life, inpatient/outpatient health, crop, political violence, micro asset, accident/disability, “decongestion”

50,000 claims paid in past year

90 banking and microfinance partners

70 insurance partners

12 telecom partners

3-Time Winner of Financial Times/IFC Awards

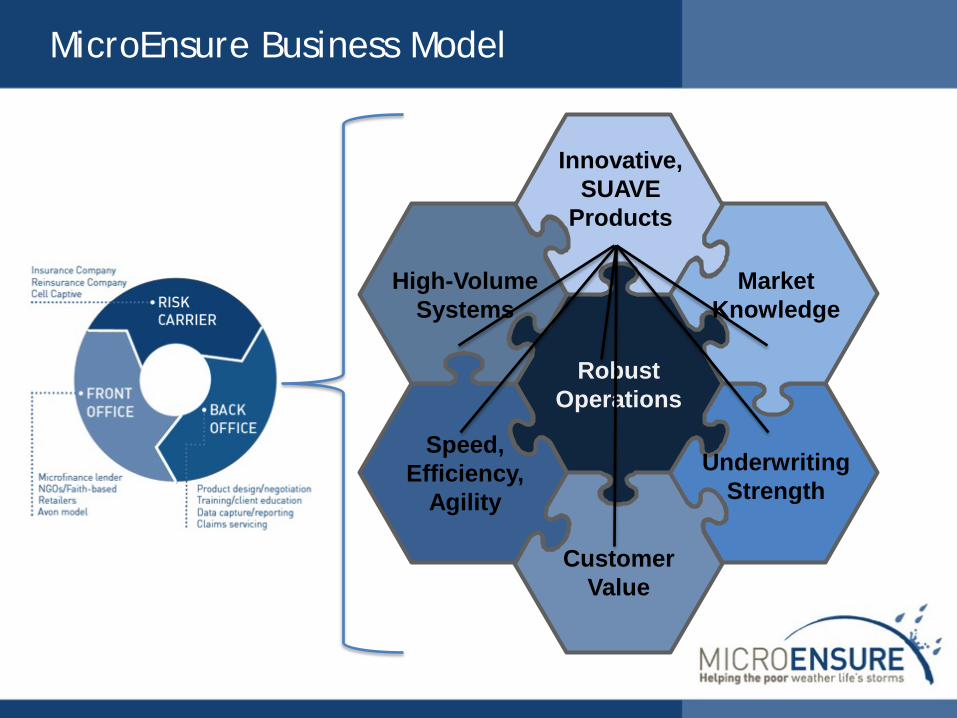

Innovative, SUAVE

Products

High-Volume Systems

Underwriting Strength

Market Knowledge

Speed, Efficiency,

Agility

Customer Value

Robust Operations

MicroEnsure Business Model

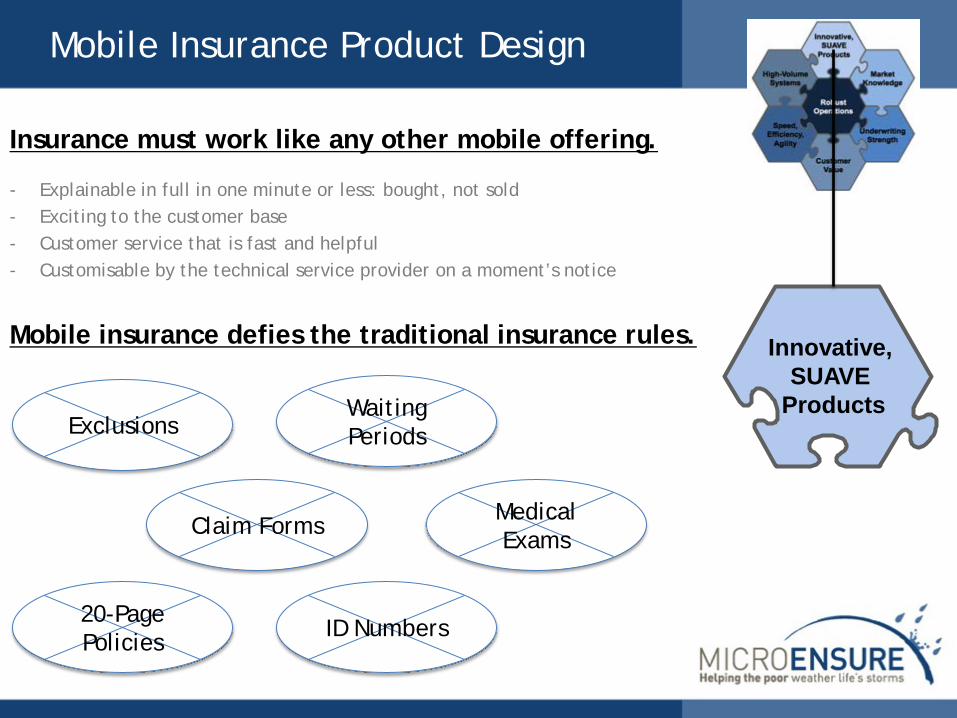

Mobile Insurance Product Design

Innovative, SUAVE

Products

Insurance must work like any other mobile offering.

- Explainable in full in one minute or less: bought, not sold - Exciting to the customer base - Customer service that is fast and helpful - Customisable by the technical service provider on a moment’s notice

Mobile insurance defies the traditional insurance rules.

Claim Forms

Exclusions

Medical Exams

Waiting Periods

ID Numbers 20-Page Policies

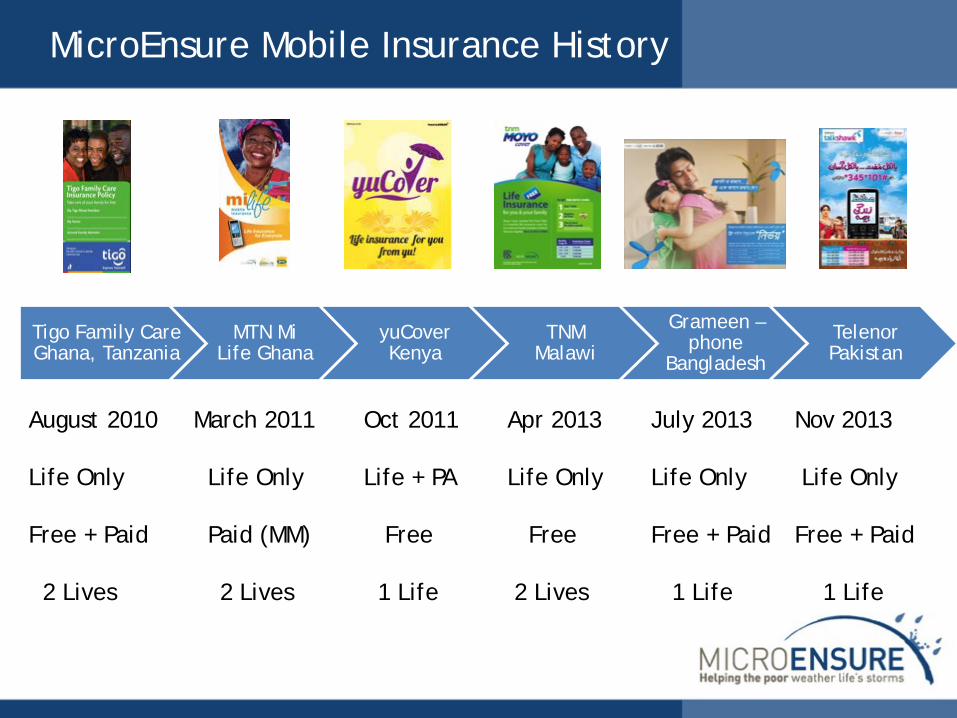

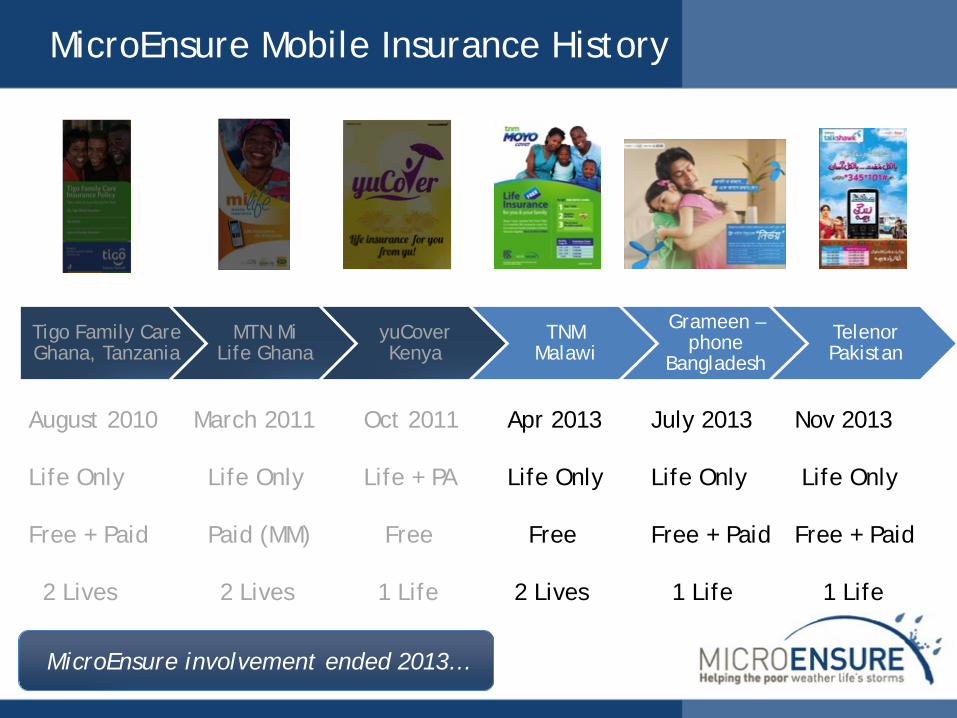

MicroEnsure Mobile Insurance History

Tigo Family Care Ghana, Tanzania

MTN Mi Life Ghana

yuCover Kenya

TNM Malawi

Grameen – phone

Bangladesh

Telenor Pakistan

August 2010 March 2011 Oct 2011 Apr 2013 July 2013 Nov 2013 Life Only Life Only Life + PA Life Only Life Only Life Only Free + Paid Paid (MM) Free Free Free + Paid Free + Paid 2 Lives 2 Lives 1 Life 2 Lives 1 Life 1 Life

MicroEnsure Mobile Insurance History

Tigo Family Care Ghana, Tanzania

MTN Mi Life Ghana

yuCover Kenya

TNM Malawi

Grameen – phone

Bangladesh

Telenor Pakistan

August 2010 March 2011 Oct 2011 Apr 2013 July 2013 Nov 2013 Life Only Life Only Life + PA Life Only Life Only Life Only Free + Paid Paid (MM) Free Free Free + Paid Free + Paid 2 Lives 2 Lives 1 Life 2 Lives 1 Life 1 Life

MicroEnsure involvement ended 2013…

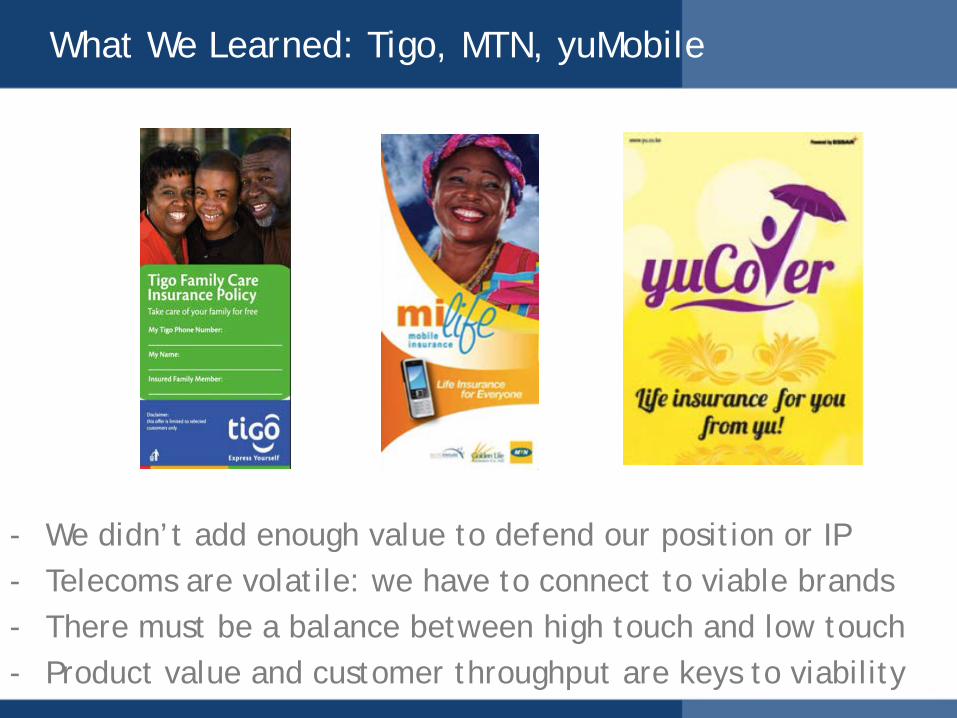

What We Learned: Tigo, MTN, yuMobile

- We didn’t add enough value to defend our position or IP - Telecoms are volatile: we have to connect to viable brands - There must be a balance between high touch and low touch - Product value and customer throughput are keys to viability

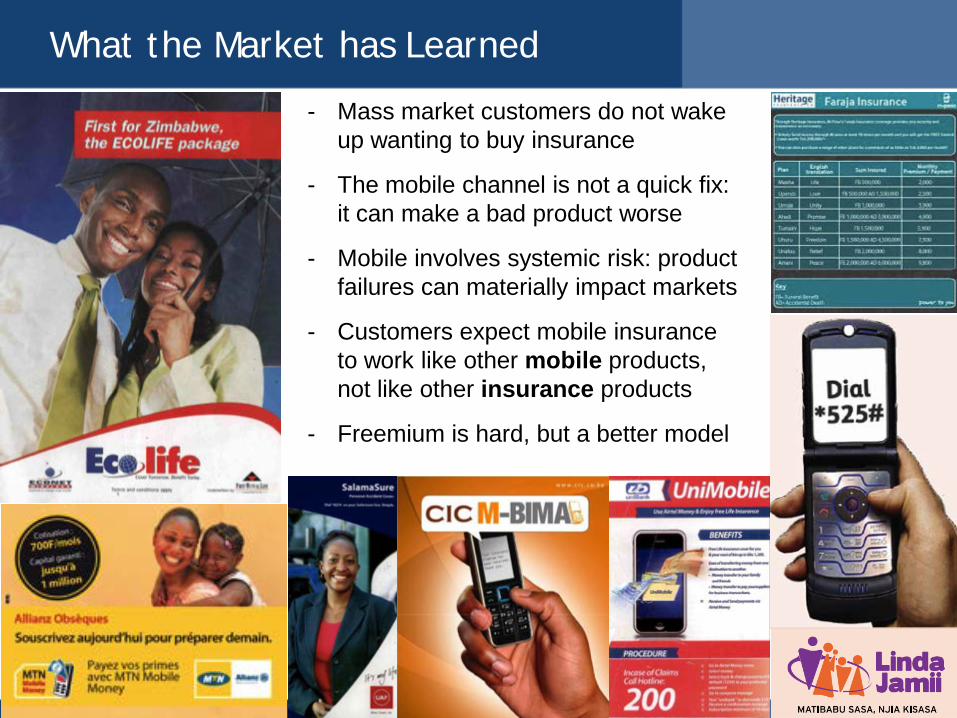

What the Market has Learned

- Mass market customers do not wake up wanting to buy insurance

- The mobile channel is not a quick fix: it can make a bad product worse

- Mobile involves systemic risk: product failures can materially impact markets

- Customers expect mobile insurance to work like other mobile products, not like other insurance products

- Freemium is hard, but a better model

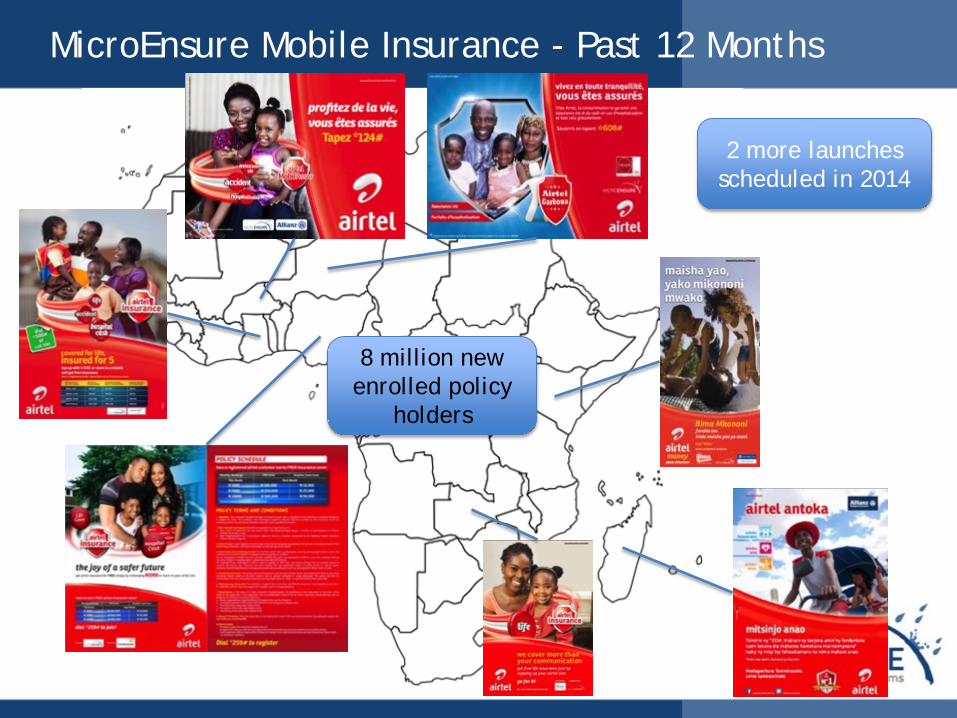

MicroEnsure Mobile Insurance - Past 12 Months

8 million new enrolled policy

holders

2 more launches scheduled in 2014

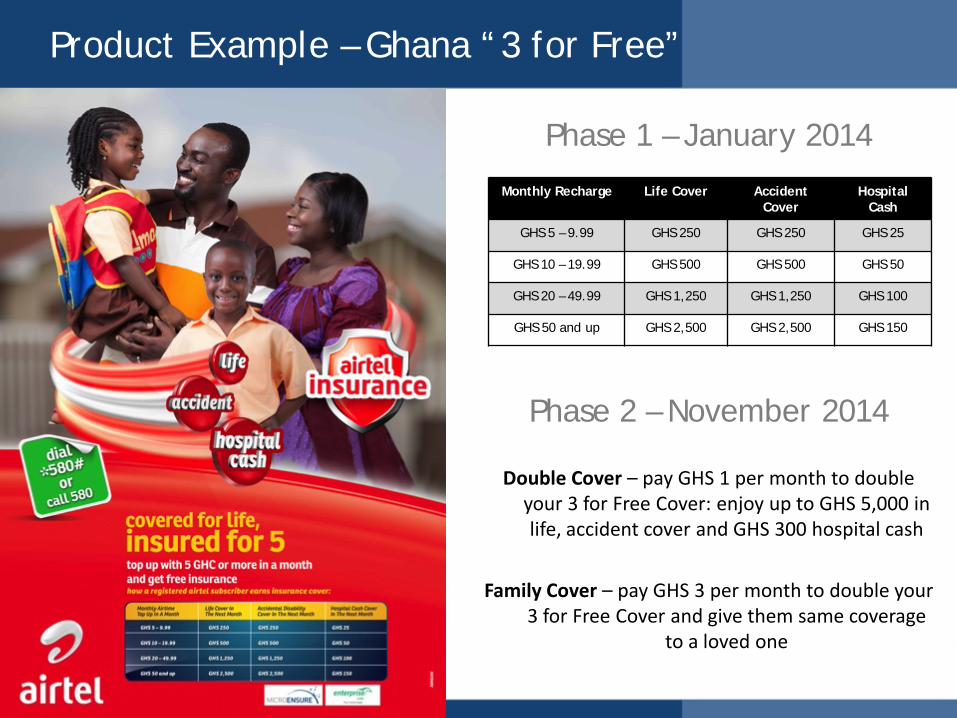

Product Example – Ghana “3 for Free”

Phase 1 – January 2014

Phase 2 – November 2014

Double Cover – pay GHS 1 per month to double your 3 for Free Cover: enjoy up to GHS 5,000 in life, accident cover and GHS 300 hospital cash

Family Cover – pay GHS 3 per month to double your 3 for Free Cover and give them same coverage

to a loved one

Monthly Recharge Life Cover Accident Cover

Hospital Cash

GHS 5 – 9.99 GHS 250 GHS 250 GHS 25

GHS 10 – 19.99 GHS 500 GHS 500 GHS 50

GHS 20 – 49.99 GHS 1,250 GHS 1,250 GHS 100

GHS 50 and up GHS 2,500 GHS 2,500 GHS 150

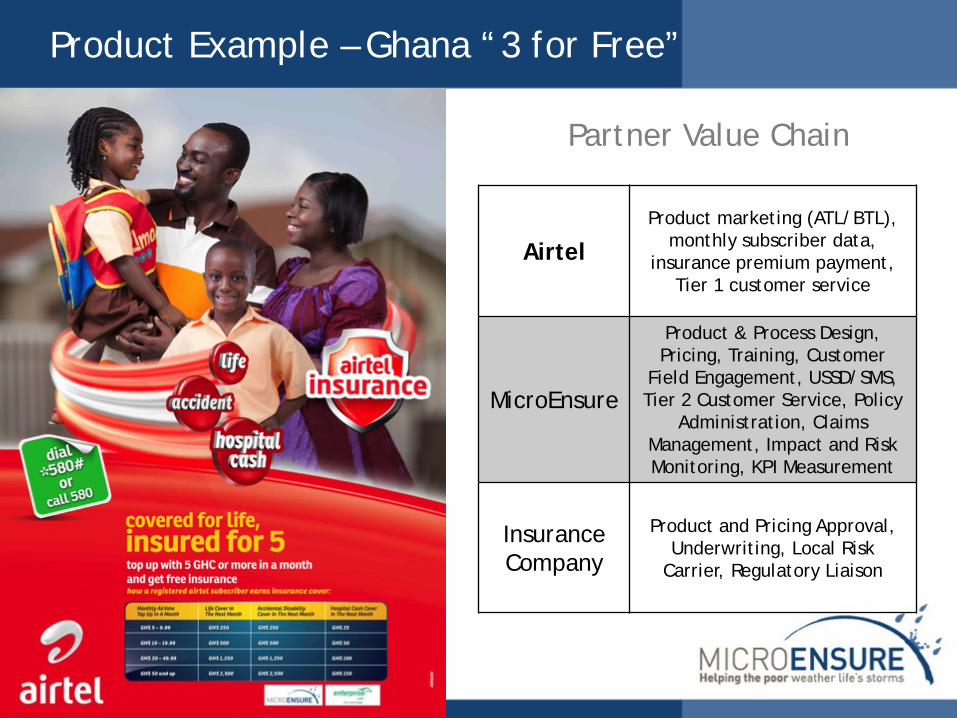

Product Example – Ghana “3 for Free”

Partner Value Chain

Airtel Product marketing (ATL/BTL),

monthly subscriber data, insurance premium payment,

Tier 1 customer service

MicroEnsure

Product & Process Design, Pricing, Training, Customer

Field Engagement, USSD/SMS, Tier 2 Customer Service, Policy

Administration, Claims Management, Impact and Risk Monitoring, KPI Measurement

Insurance Company

Product and Pricing Approval, Underwriting, Local Risk

Carrier, Regulatory Liaison

Product Example – Ghana “3 for Free”

A few insights after 1 year:

• 1,000% increase in claims*

• 450% increase in policy volumes*

• 80% Reduction in Technical Service Provider (TSP) Expense*

• Sustained ARPU and Churn Value • ATL Marketing = Wide Awareness • Multiple risk coverage is in more

demand than single risk coverage • Claims payments in 78 minutes

* As compared to a similar product in Senegal

Airtel Nigeria – TV Commercial

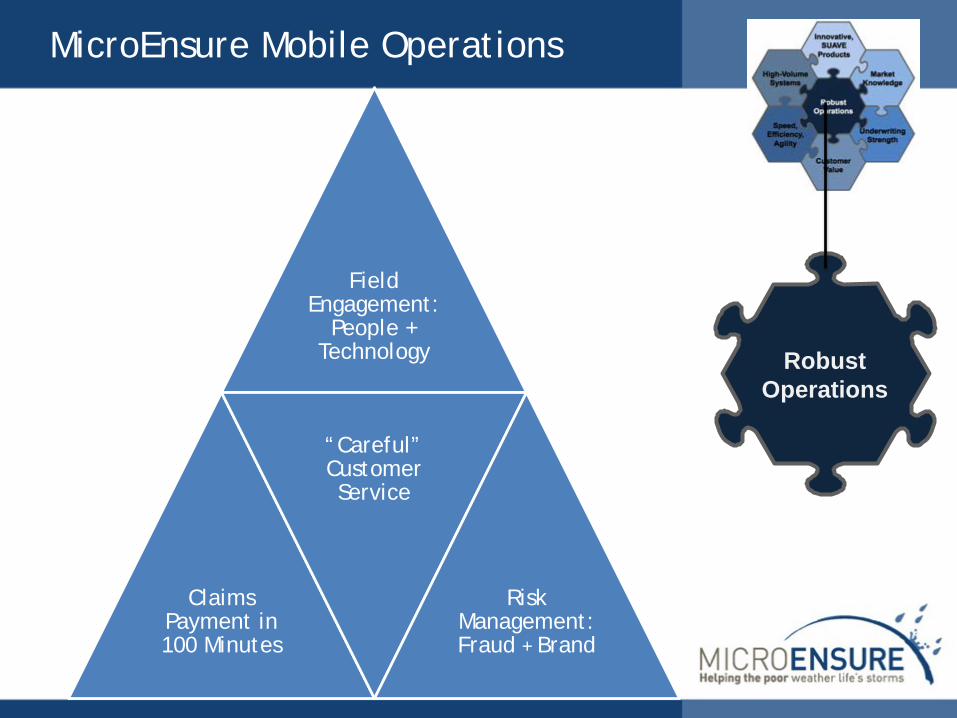

MicroEnsure Mobile Operations

Robust Operations

Field Engagement:

People + Technology

Claims Payment in 100 Minutes

“Careful” Customer Service

Risk Management: Fraud + Brand

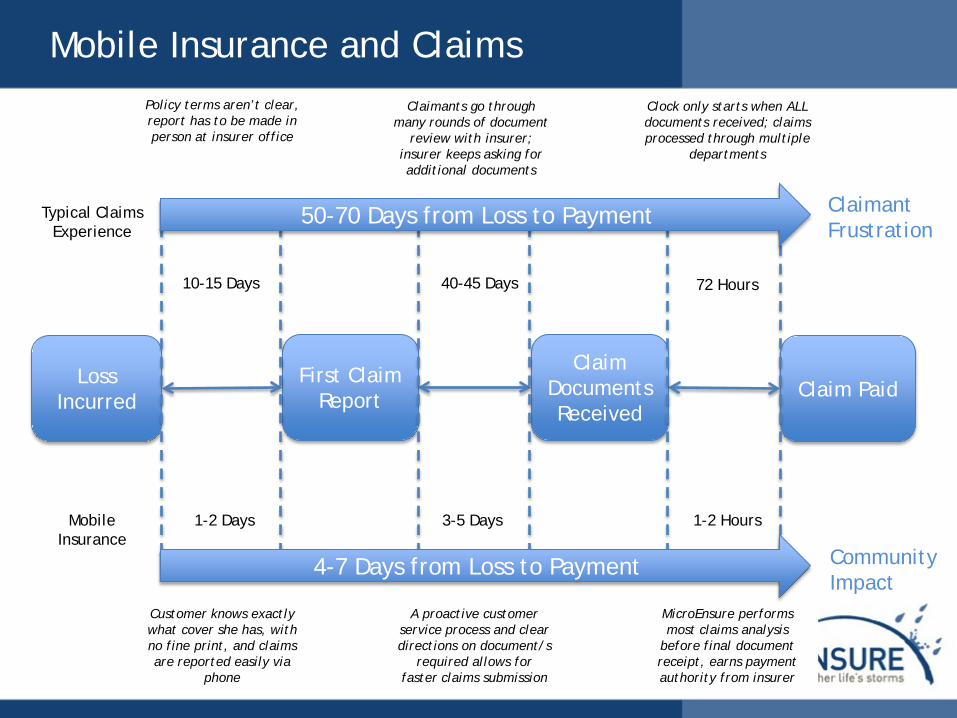

Mobile Insurance and Claims

Loss Incurred

First Claim Report

Claim Documents Received

Claim Paid

Mobile Insurance

Typical Claims Experience

1-2 Days 3-5 Days 1-2 Hours

10-15 Days 40-45 Days 72 Hours

Policy terms aren’t clear, report has to be made in person at insurer office

Claimants go through many rounds of document

review with insurer; insurer keeps asking for additional documents

Clock only starts when ALL documents received; claims processed through multiple

departments

Customer knows exactly what cover she has, with no fine print, and claims are reported easily via

phone

A proactive customer service process and clear directions on document/s

required allows for faster claims submission

MicroEnsure performs most claims analysis

before final document receipt, earns payment authority from insurer

50-70 Days from Loss to Payment

4-7 Days from Loss to Payment Community Impact

Claimant Frustration

Building Trust and Education through Claims

Designing benefit-rich products, and paying 1,000’s of claims, while mitigating fraud, requires deep technical knowledge of insurance, the low-income market, and robust operations.

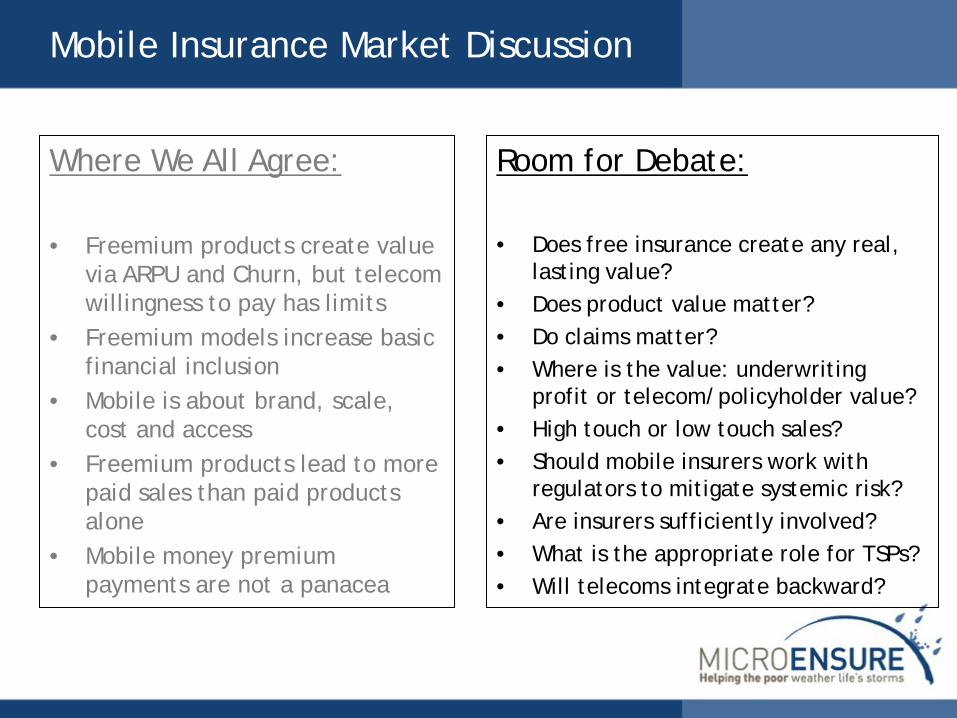

Mobile Insurance Market Discussion

Where We All Agree: • Freemium products create value

via ARPU and Churn, but telecom willingness to pay has limits

• Freemium models increase basic financial inclusion

• Mobile is about brand, scale, cost and access

• Freemium products lead to more paid sales than paid products alone

• Mobile money premium payments are not a panacea

Room for Debate: • Does free insurance create any real,

lasting value? • Does product value matter? • Do claims matter? • Where is the value: underwriting

profit or telecom/policyholder value? • High touch or low touch sales? • Should mobile insurers work with

regulators to mitigate systemic risk? • Are insurers sufficiently involved? • What is the appropriate role for TSPs? • Will telecoms integrate backward?

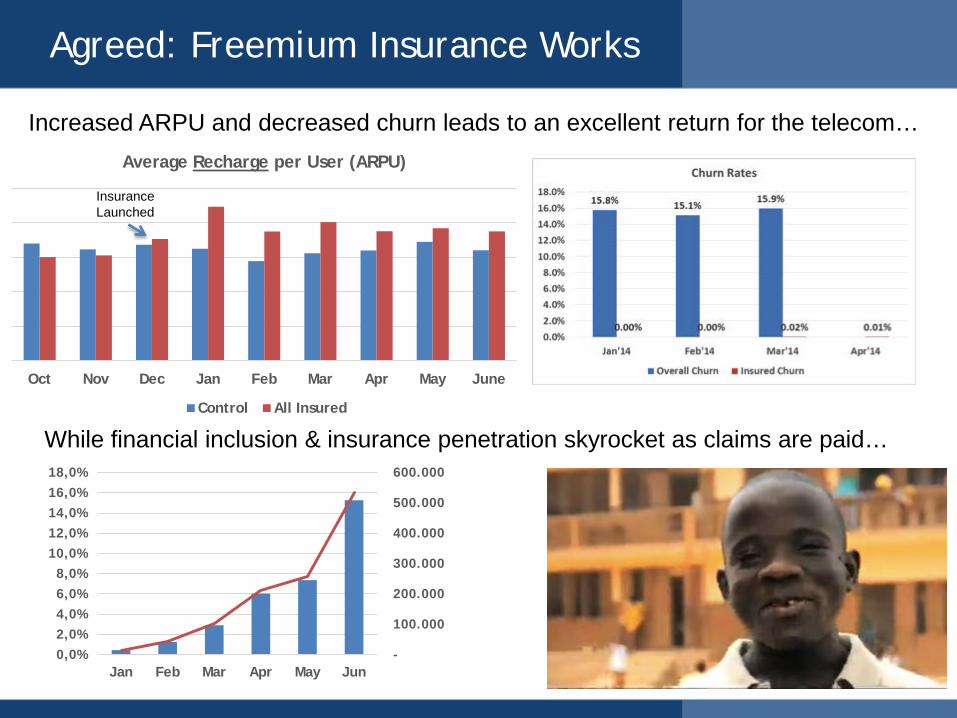

Agreed: Freemium Insurance Works

Increased ARPU and decreased churn leads to an excellent return for the telecom…

While financial inclusion & insurance penetration skyrocket as claims are paid…

-

100.000

200.000

300.000

400.000

500.000

600.000

0,0% 2,0% 4,0% 6,0% 8,0%

10,0% 12,0% 14,0% 16,0% 18,0%

Jan Feb Mar Apr May Jun

Oct Nov Dec Jan Feb Mar Apr May June

Average Recharge per User (ARPU)

Control All Insured

Insurance Launched

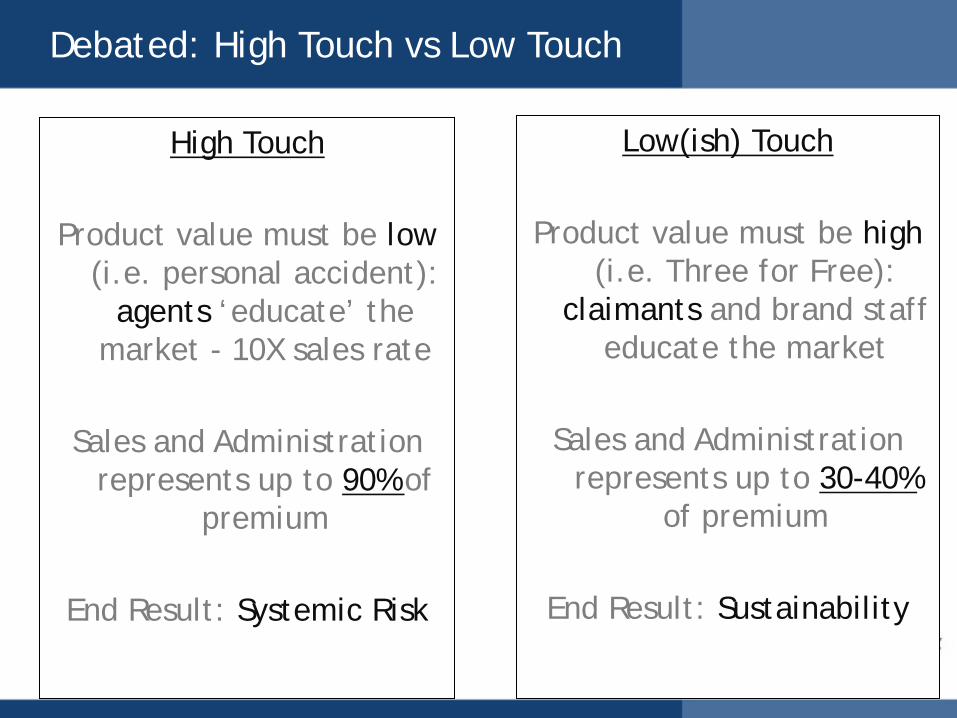

Debated: High Touch vs Low Touch

High Touch

Product value must be low (i.e. personal accident):

agents ‘educate’ the market - 10X sales rate

Sales and Administration

represents up to 90% of premium

End Result: Systemic Risk

Low(ish) Touch

Product value must be high (i.e. Three for Free):

claimants and brand staff educate the market

Sales and Administration

represents up to 30-40% of premium

End Result: Sustainability

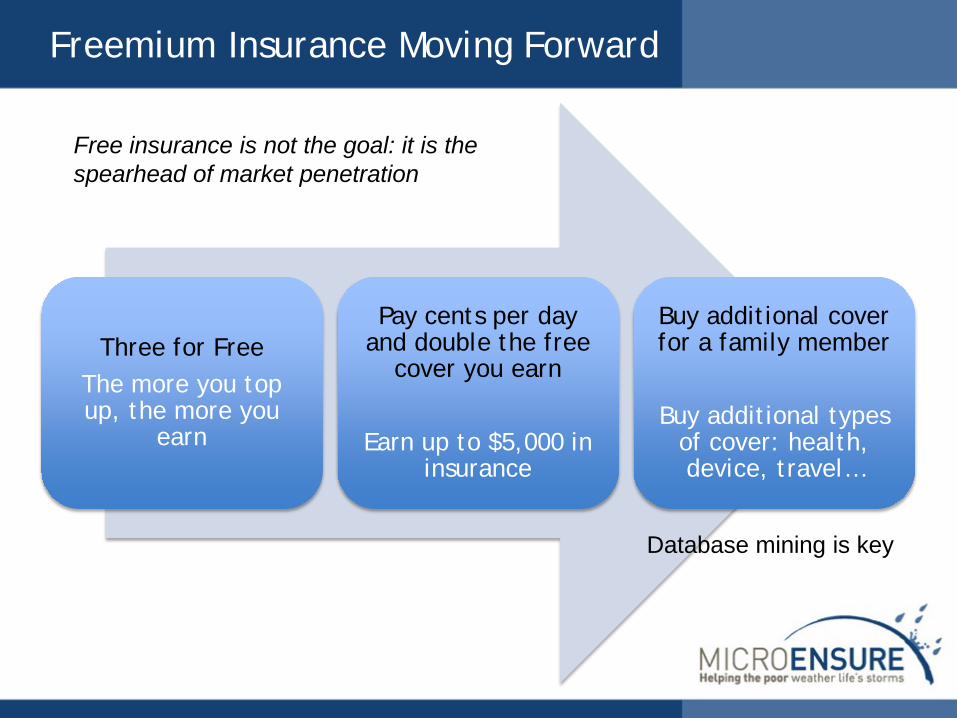

Freemium Insurance Moving Forward

Three for Free The more you top up, the more you

earn

Pay cents per day and double the free

cover you earn

Earn up to $5,000 in insurance

Buy additional cover for a family member

Buy additional types

of cover: health, device, travel…

Free insurance is not the goal: it is the spearhead of market penetration

Database mining is key

Beyond Mobile: The Future is Bright

Twitter: @microensure [email protected] [email protected] +254 786 499 100

Barclays Salary Accounts WWBG Deposit Accts

NWK Zambia Agricultural Loans

Opportunity Int’l Micro Loans

Related Documents