1 P.E.S.T.E.L. ANALYSIS OF THE MENA REGION P.E.S.T.E.L. Analysis: A Look at the Macroeconomic Environment Of the MENA Region Courtney Fenwick, Carl Schacter, Eric Rodriguez Florida Atlantic University

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1 P.E.S.T.E.L. ANALYSIS OF THE MENA REGION

P.E.S.T.E.L. Analysis:

A Look at the Macroeconomic Environment

Of the MENA Region

Courtney Fenwick, Carl Schacter, Eric Rodriguez

Florida Atlantic University

2 P.E.S.T.E.L. ANALYSIS OF THE MENA REGION

Table of Contents

Introduction to the MENA Region ....................................................................................................3

Executive Summary ............................................................................................................................4

Politics ..............................................................................................................................................5

Economic ..........................................................................................................................................9

Socio-Culture .................................................................................................................................. 12

Technology ..................................................................................................................................... 15

Environment ................................................................................................................................... 17

Legal ............................................................................................................................................... 20

Going Forward ............................................................................................................................... 23

Appendix (Graphs) ......................................................................................................................... 24

Economics .............................................................................................................................................. 24

Sociocultural .......................................................................................................................................... 27

Environmental ....................................................................................................................................... 31

Technology ............................................................................................................................................. 43

Bibliography ................................................................................................................................... 45

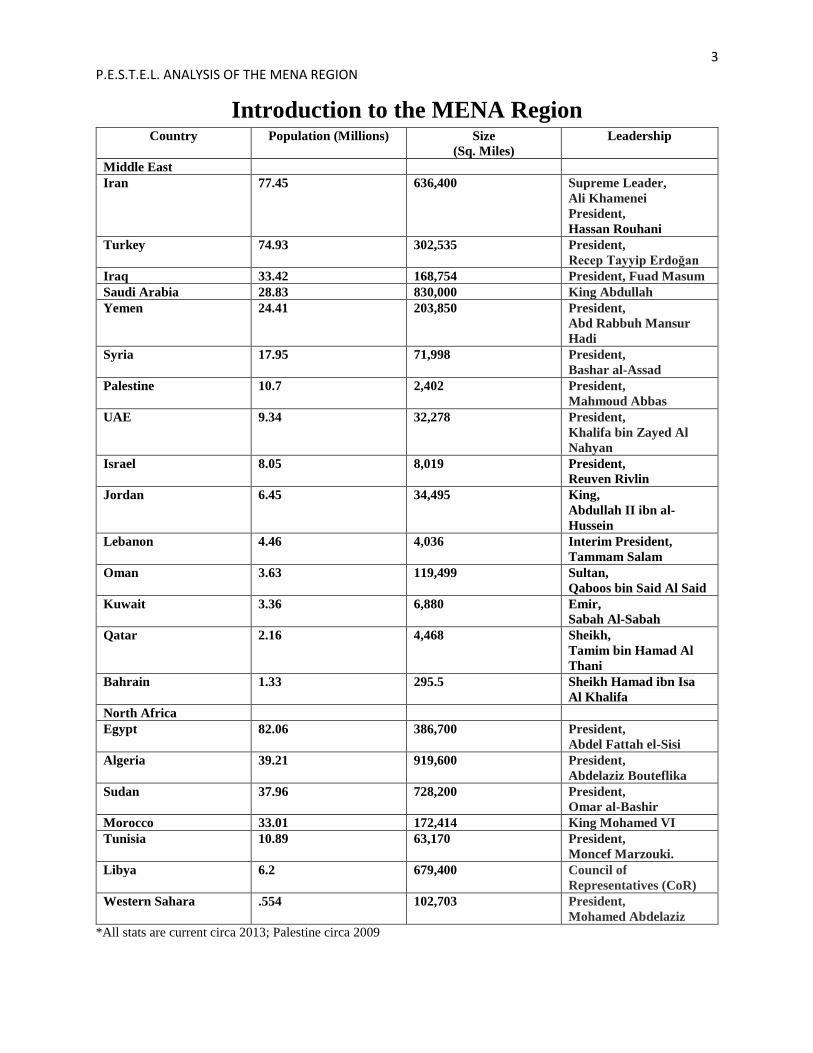

3 P.E.S.T.E.L. ANALYSIS OF THE MENA REGION

Introduction to the MENA Region Country Population (Millions) Size

(Sq. Miles)

Leadership

Middle East

Iran 77.45 636,400 Supreme Leader,

Ali Khamenei

President,

Hassan Rouhani

Turkey 74.93 302,535 President,

Recep Tayyip Erdoğan

Iraq 33.42 168,754 President, Fuad Masum

Saudi Arabia 28.83 830,000 King Abdullah

Yemen 24.41 203,850 President,

Abd Rabbuh Mansur

Hadi

Syria 17.95 71,998 President,

Bashar al-Assad

Palestine 10.7 2,402 President,

Mahmoud Abbas

UAE 9.34 32,278 President,

Khalifa bin Zayed Al

Nahyan

Israel 8.05 8,019 President,

Reuven Rivlin

Jordan 6.45 34,495 King,

Abdullah II ibn al-

Hussein

Lebanon 4.46 4,036 Interim President,

Tammam Salam

Oman 3.63 119,499 Sultan,

Qaboos bin Said Al Said

Kuwait 3.36 6,880 Emir,

Sabah Al-Sabah

Qatar 2.16 4,468 Sheikh,

Tamim bin Hamad Al

Thani

Bahrain 1.33 295.5 Sheikh Hamad ibn Isa

Al Khalifa

North Africa

Egypt 82.06 386,700 President,

Abdel Fattah el-Sisi

Algeria 39.21 919,600 President,

Abdelaziz Bouteflika

Sudan 37.96 728,200 President,

Omar al-Bashir

Morocco 33.01 172,414 King Mohamed VI

Tunisia 10.89 63,170 President,

Moncef Marzouki.

Libya 6.2 679,400 Council of

Representatives (CoR)

Western Sahara .554 102,703 President,

Mohamed Abdelaziz

*All stats are current circa 2013; Palestine circa 2009

4 P.E.S.T.E.L. ANALYSIS OF THE MENA REGION

Executive Summary

This paper is a macroeconomic analysis of the Middle East and North African (MENA) region.

It examines the Political, Economic, Socio-cultural, Technological, Environmental, and Legal

(P.E.S.T.E.L.) aspects of the MENA region. It will begin with the Political section and proceed

through the acronym in order. This paper will examine the ‘Arab Spring’ and its impacts on the

region, the role of NATO, corruption among governments, the role of the military, and the Iran

nuclear debate. Economics will examine the history of fossil fuels, foreign direct investment

(FDI), the availability of capital and credit, and the effects of national policy on wages & growth.

Socio-Cultural delves into age disparity for the youth of the MENA, religion and its influence on

government structure, the effects of emigration to escape violence, and the lack of transparency

and accountability from leaders in the region. The Technology section will discuss nuclear

development for energy security, the acceptance of popular technology into the mainstream

culture of the MENA, how the Global North is perceived, infrastructure for E-Governance, and

investments in technology. The environment is under attack from the effects of industrialization

of the MENA, pollution problems, water scarcity, and energy security through the development

of clean renewable sources. Finally, the legal section touches on the role of culture in law,

religion in law, the prolific black market and drug trade, as well as trade reform & policy.

Constant real time inflows of information from the MENA region render traditional forecasting

models unreliable. This paper will compile historic trends in an effort to establish mid to long

term outlooks for the different aspects of the PESTEL analysis. Due to the volatility of the region

this analysis will utilize verified information from peer reviewed sources at least six months or

older in order to grasp the facts and remove any speculatory journalistic bias or misinformation.

5 P.E.S.T.E.L. ANALYSIS OF THE MENA REGION

Politics

The ‘Arab Spring’ is a movement that occurred throughout the MENA. It is a cultural

awakening that began in early 2011. Protestors spoke out for human rights and ushered in an era

of ‘significant optimism’ for reformation and the proliferation of stable democracies in the

MENA region. The context of ‘Arab Spring’ mainly encompasses the predominantly peaceful

protests which influenced regime changes in Libya, Egypt, and Yemen. It also includes

incidences of military intervention (NATO in Libya), armed sectarian warfare (Syria, Yemen,

Libya) and mass mobilization of protestors. This is represented by an abundance of power

struggles with causes ranging from civil war, religious sectarian conflicts, and unstable power

transitions. Instances such as:

The regime changes in Tunisia, Egypt, and Libya

War in Syria, Iraq, and on the borders of Turkey and Iran

The ever-present conflict between Israel and Hamas in Palestine which has escalated to

missile fire and tunneling beneath the Gaza Strip

Many smaller sectarian power struggles between the population of a nation and the

struggle against their oppressive governments tenuous hold on power

The volatility of MENA has changed the security needs of visitors to the region as foreign

nationals are being abducted and beheaded with alarming frequency by terrorist organizations.

The North American Treaty Organization (NATO) has established a policy of ‘strengthening and

deepening’ its partnerships in the region to tackle these concerns head on through the shared

goals of security, stability, and peace throughout the MENA. These countries are looking to

NATO to provide direction and leadership towards practical answers to security challenges,

guarantees of security from internal and external forces that threaten the regimes currently in

power, and pro-active steps to stabilize the volatile climate that is pervasive throughout the

region. NATO’s track record has been exceptionally deficient. These areas are supposed to be

its core of expertise. Their ability to defend the MENA region is presently questionable at best

and will continue to deteriorate as financial crisis in Europe and the U.S. force spending cuts,

military shrinkage, and take NATO’s focus away from MENA and back towards domestic

issues.

It has been stated that NATO needs to begin by establishing clear and attainable goals in the

region, to send a transparent message of its partnership expectations and to define what the

phrase ‘strengthening and development’ actually means. Next, NATO must appeal to what the

MENA regions policymakers’ desires in order to establish partnerships that are more attractive

and to focus on the creation of common interests within the individual countries of MENA. The

results of its past ‘top-down’ approach have been limited at best. Most Arabs see NATO as a

powerful and aggressive alliance devoted to the political interests and security of the west.

Nations such as Israel, Egypt, and Turkey have begun to pursue their own independent policies

which are increasingly divergent from the interests of their NATO allies.

Corruption plays a major role in the politics of the MENA region. Transparency

International’s (TI) Corruptions Perceptions Index (CPI) routinely ranks MENA countries below

the world-wide average median. These findings are further bolstered by the Global Integrity

Index (GII) in which the MENA region scores very low in integrity systems and accountability

indicators. The Bartelsman Transformation Index (BTI) lends further credibility to these

6 P.E.S.T.E.L. ANALYSIS OF THE MENA REGION

negative trends. It states that all MENA countries performance regarding democratization and

market liberalization fall well below the world median. Political Transformation scores are even

lower than economic transformation rankings. The Management Index (MI) is a gauge of the

quality of the political management systems currently in use. The MI uses five major categories:

Reliable pursuit of goals by government; Effective use of resources; Governance capability;

Consensus building capacity; International cooperation. All MENA countries scored

exceptionally low in the corruption category with a rating range of 2 (Yemen, Algeria, Lebanon)

to 4 (Egypt, Jordan, Tunisia). Attributing reasons for poor performance in the Governance and

Anti-Corruption categories are:

Lack of transparency

Little or no access to information

Weak internal accountability

Few to no checks and balances in the system

Restricted freedom of the press

Elitist social classes

Excessive regulation

Significant barriers to entry

This prevalent corruption impacts many factors of government and is directly correlated to

governance indicators like: Economic growth rate; GDP per capita; Foreign Direct Investment;

Human development index; Poverty index; Health & Education spending. Corruption greatly

increases the risk of government confiscation, expropriation, and domestication due to the self

centric stance of the ruling parties in power who have little interest in social responsibility or in

serving their citizens.

A large contributor to the resistance of the adoption of democratic forms of government in

MENA is the ‘robustness’ of regime security. Robustness is the culmination of four main

factors: A countries fiscal health; international support and assistance to a nation and its military;

mobilization for popular political reform; Degree of security systems embedded in the state

policy. This leads to the role of the military in the government. There are several irregular

forms of government native to the MENA region, such as:

Oil monarchy

Civic-myth monarchy

Mukhabarat states (Syria, Tunisia, Egypt, Yemen; also known as policy/intelligence

states)

Military states

Dual military (Iran, Iraq, and Libya who have private guards and security to offset the

country’s national army)

Military democracy

Military’s in the MENA region are usually used to quell large uprisings that the police are ill

equipped to handle. When the army is summoned, it may or may not respond, as the military has

the status of autonomy with its own independent political decision maker. This further lends to

an overall un-cohesiveness and to security fears of for the different ruling governments in the

region.

Presently, the ‘X Factor’ that has grown into a significant driver of fear and change in the

MENA region is the Islamic State of Iraq and Syria (ISIS). The ISIS conflict in Syria, Iraq,

7 P.E.S.T.E.L. ANALYSIS OF THE MENA REGION

Turkey, and Iran has become the frontrunner in a host of issues ranging from the ongoing war

between Israel & Palestine to the Iran nuclear debate. Syria is now ‘ground zero’ in the war for

power and influence in the MENA region. Every country in the region has a direct stake, as well

as the outside interest of many other nations, all directly or indirectly supporting a particular

side. The underlying reasons for conflict are about the balance of power between Iran and Saudi

Arabia in addition to the overall power struggle between Iran and the U.S. & Israeli alliance.

Some key terrorism trends in 2013 include:

Evolving terrorist groups with tighter local and regional focuses from both Al- Queda

(AQ) and its partners

The rise of autonomous like-minded groups who take advantage of weak and corrupt

governments

Ayman al-Zawahi, the head of AQ, has been frequently disobeyed through AQ partners

upgrading the level of violence and attacks on the populations at large

Thousands of foreign fighters flocking to Syria to battle Assad

Meanwhile, Iran, Hizballah, and other Shia militia provide support and supplies to the

Syrian regime

Terrorism is increasingly trending to escalations of violence spurred by

sectarianmotivations in Lebanon, Pakistan, and Syria

Increased criminal activity from terrorist groups, such as kidnapping for ransom, in order

to generate capital

‘Lone Wolf’ attacks in foreign nations are escalating, an example being the Boston

Marathon bombing

The issue of Iran’s right to nuclear power versus their ability to weaponize under the pretext of

peaceful applications for the citizens of the nation is of paramount concern in the MENA region.

Fears began to escalate in 1995 at the Nuclear Non-Proliferation Treaty (NPT) convention where

the Arab League pushed for a Weapons of Mass Destruction (WMD) free zone to be established

in the middle-east. This led to over 15 years of inaction and no progress on the issue from a

disinterested NATO (mainly U.S., Britain, and Russia) who perpetually issued extensions for the

forum. The NPT conference scheduled for 2015 promises more of the same. The Arabs most

recent show of frustration on the issue came in April of 2013 when the Egyptian representatives

walked out of the NPT conference talks due to ‘unacceptable and continuous failure’. The

primary countries involved disagree on several aspects that are essential to achieving arms

control. Egypt and a few other states view the root problem as Israel, not Iran. This is not to say

that Israel is an imminent threat, but a major choke point on the path to an NPT. Not only on a

regional, but on an international level, the MENA nations are feeling pressured and threatened by

the advances in the Iranian nuclear program. Tehran is close to achieving a bomb relatively

quickly if it chooses. Iran insists that its nuclear proliferation is of a peaceful nature, but many

countries are deeply suspicious. The Iranian government states that enrichment of uranium is at

3.5% for power production and roughly 20% for medical research purposes. This is considerably

below the 95% threshold needed for a nuclear weapon. The continuous uncertainty centered on

their nuclear program and Iran’s threatening stance towards many nations, across a multitude of

issues, has led the U.S. and the gulf monarchies to closer and more correlated interdependent

relationships in an effort to curtail Iran’s ambitions. Israel is not inclined to release its nuclear

stockpile. It sees this as the major deterrent against its hostile neighbors, some of which refuse

to recognize Israel’s very existence as a sovereign nation. The recent use of chemical WMD’s

8 P.E.S.T.E.L. ANALYSIS OF THE MENA REGION

by Syria on its own population has dealt a ‘major blow’ to the NPT conference. There are many

reasons for Iran to want to prevent WMD’s in the MENA region, contrary to popular belief,

these include:

Loss of conventional superiority

WMD terrorism

The institutionalization of American presence in the region

Risk of offensive, rather than defensive, perceptions from other nations

Production vulnerability and maintenance costs

Risks inherent in weak communication and command structures

Damaging Iranian ties with regional and international allies

Religious prohibitions against WMD’s

Iran’s support of a WMD free zone would help boost other nations’ confidence in them and

allow Tehran to build trust in the greater Arab world. It would also benefit Iran by making the

region more secure and by helping to solidify their power base. Israel is in possession of

anywhere from as few as 60 to as many as 400 nuclear weapons. Jerusalem is of the mindset that

comprehensive security and peace must come before any NPT. Israel denies responsibility for

its nuclear arsenal citing that it has been empowered by the west. It seems to be a zero sum

game being played out which is un-resolvable with one side focused on WMD’s and the other on

overall regional relations between neighboring countries. This conflict is trending to continue in

its current incarnation for the foreseeable future.

9 P.E.S.T.E.L. ANALYSIS OF THE MENA REGION

Economic

Historically, the MENA region has been a fossil fuel commodity driven economy. Analyzing

both the historical and current trends in the oil industry, impacts of GDP, imports & exports,

fiscal policies, levels of foreign investment, and employment rates will allow for an effective

forecast of the region’s economic outlook.

MENA economies were prosperous in 1970’s, due in large part to the expansion of oil markets.

Initial revenues produced from oil markets in the 1970’s were largely responsible for the creation

of interventionist-redistributive economic models for oil and non-oil producing countries. These

revenues were a product of a 10 percent increase in global demand from 1976 to 1979. Welfare

structures were implemented to issue excess revenue to the citizens of the oil producing regions.

Non-oil producing countries supplied the labor force necessary to operate the drilling, wells, and

on-site machinery of the oil producing countries.

Expansion within the public sector was an effect of the booming economic progress from the

oil industry. Unemployment throughout the 1970’s was low, literacy rates increased, and life

expectancy rates were on the rise. Trends would drastically change as some countries of MENA

would become members of OPEC (Organization of the Petroleum Exporting Countries). Price

stabilization would arrive with OPEC’s output restriction enforcement in the 1980’s and oil

revenues would decline. As oil revenues declined, the economy of the MENA region would take

a downward trend as public debt increased with the various governments’ inability to answer the

public sector demands for wages and entrenched social programs. The remittance of revenues

associated with migrant labor from non-oil producing countries would decline and international

competition would intensify causing an economic crisis to the MENA region. Various

governments are undertaking initiatives to restructure their economic policies during this time to

stabilize their respective economies.

These trends show that a thriving economy which is trailed by major declines in growth and

development in the public sector are associated with countries that draw their wealth from the

exploitation natural resources. Emphasis on a natural resource like oil pulls experienced labor

from other industrial sectors and entrepreneurial endeavors which creates a pronounced

opportunity cost. Diminished growth rates in employment and investment in the public sector

are attributed to these patterns.

During the 1990’s MENA would lag in both foreign direct investment (FDI) and foreign trade

from a global perspective due to protectionist trade policies. Such policies included restrictions

on foreign majority ownership in both the public and private sectors. Oil exporting countries

were not diversified in their GDP imports and exports due to the implementation of these

policies. MENA was also a laggard globally in both foreign direct investment and foreign trade

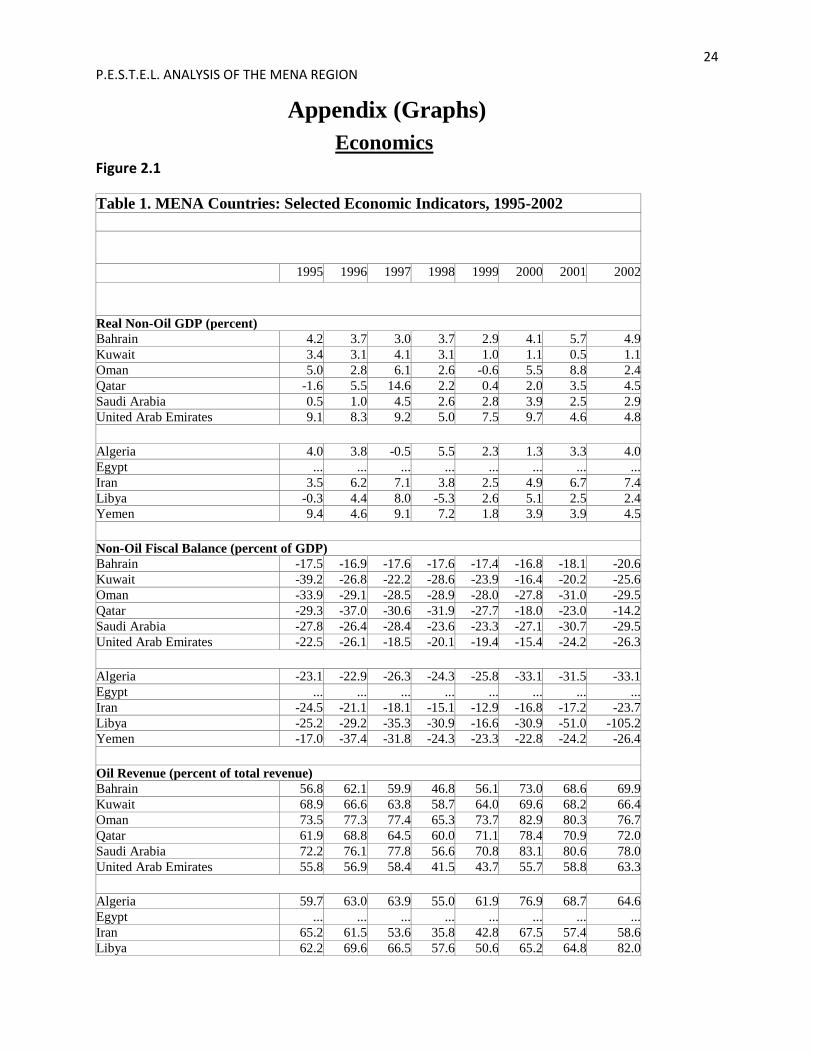

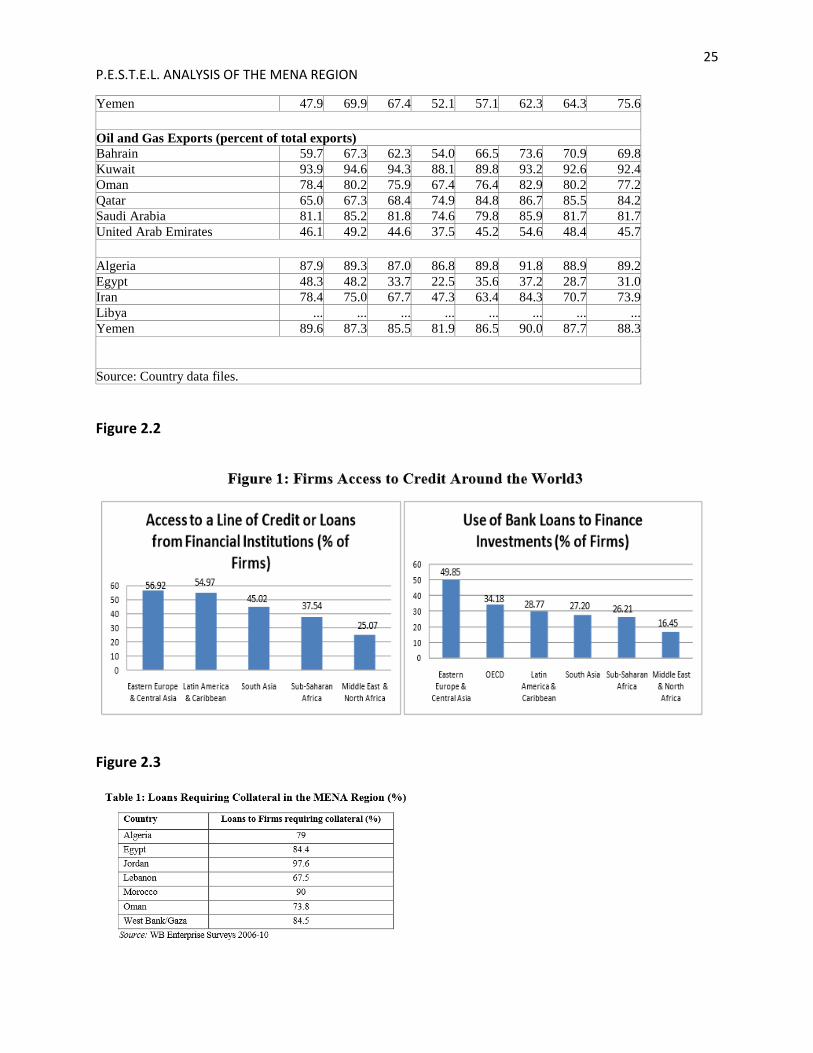

because of these closed economic systems. For example, Saudi Arabian fuels made 90 percent of

their export base during this time. (Figure 2.1)

Since the beginning of the 2000’s the Gulf States have developed some of the most attractive

private sectors outside of oil exports among the MENA region. During this time United Arab

Emirates (UAE) developed growth rates in non-oil producing sectors that represented 70 percent

of their GDP:

● Manufacturing (12.6 percent)

● Commerce and hotels (11.4 percent)

● Real estate (9.1 percent)

10 P.E.S.T.E.L. ANALYSIS OF THE MENA REGION

● Construction (8.6 percent)

● Transportation (10.9 percent)

● Finance and insurance (6.4 percent)

● Government services (11 percent)

Unfortunately these economic models are not easy to duplicate in other regions of the MENA.

Some areas have business environments that do not support entrepreneurship and often have

restrictions on attaining startup capital. Public banks govern financial systems that often show

favoritism towards businesses that are state owned and operated instead of inviting investment

from offshore firms. (Figure 2.2)

As of 2010 the MENA region falls at the bottom of the list in regards to percentage of firms

with credit lines from financial institutions (25.07%). One of the main underlying reasons why

firms have difficulty securing credit is due to insufficient collateral provided to banks. More

often than not, financial institutions have a preference towards land as collateral. Availability of

sufficient collateral isn’t the only issue as there is an inability prevalent throughout MENA firms

to make productive use of their valuable assets, such as receivables and equipment. (Figure 2.3)

FDI in the MENA region is restricted due to barriers to trade and political instability. In 2002

the Arab Development Report (UNDP) revealed that from 1975 to 1998 global FDI levels

decreased in the Middle East. From 1975 to 1980 FDI in MENA was at 2.6 percent and from

1990 to 1998 FDI declined to 0.7 percent of the global foreign investment levels. Since the end

of the 1980’s, MENA would attract the least amount of FDI inflows globally. Though FDI

inflows have been increasing as of late, the MENA still continues to lag behind other developing

countries globally.

Beginning in 2000 the Arab region received 1.9 percent of global FDI for developing countries

and was barely elevated above developing European countries that had the least FDI percentage

with .8 percent of global FDI. During this time the FDI deficiencies were attributed to both

internal and external issues. These issues can be comprised of the slow development of

entrepreneurship, political instability, restricted control of foreign ownership to below 50% to

prevent non-domestic control, and limitations on which sectors FDI can be allocated towards.

MENA countries are striving to change investment environments to realize greater inflows of

capital from FDI. New reforms are being developed toward implementing restructured

investment legislation, tax & custom incentives, and reduced foreign ownership restraints.

Enabling foreign investors to achieve majority ownership in profitable industrial sectors will

increase the amount of investment to the MENA region and achieve levels that have been

historically unreachable.

Non-oil producing economies will continue to be buoyed by rising amounts of public capital

spending and credit inflows from the private sector. The long-term challenge of decreasing

dependence on oil is on the horizon for energy producing countries of MENA. Growth in energy

efficient technology, increases in renewable energy projects, and oil supplies from alternative

sources (shale and fracking) are causing prices to decline. Last year’s tepid growth in MENA oil

exports is expected to improve as oil production and exports respond to the global economic

recovery. High levels of public capital spending and accelerating private sector credit continue

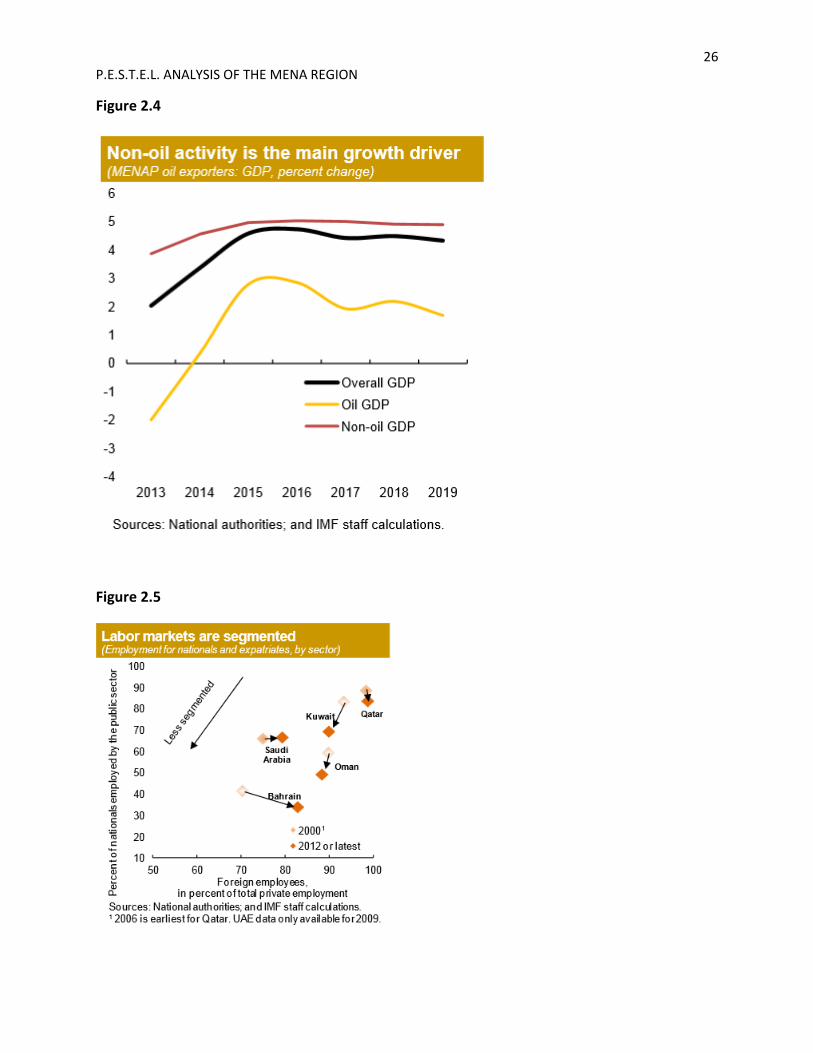

to support the non-oil economy. (Figure 2.4)

The outlook for MENA oil importing countries is modest growth and it is anticipated to

continue, but the drivers may begin to change. Resource consumption financed by industry and

large public sector wage spending, will continue to buoy growth. Planned investments in the

11 P.E.S.T.E.L. ANALYSIS OF THE MENA REGION

pipeline could start stimulating economic activity as a result of increased public spending on

infrastructure.

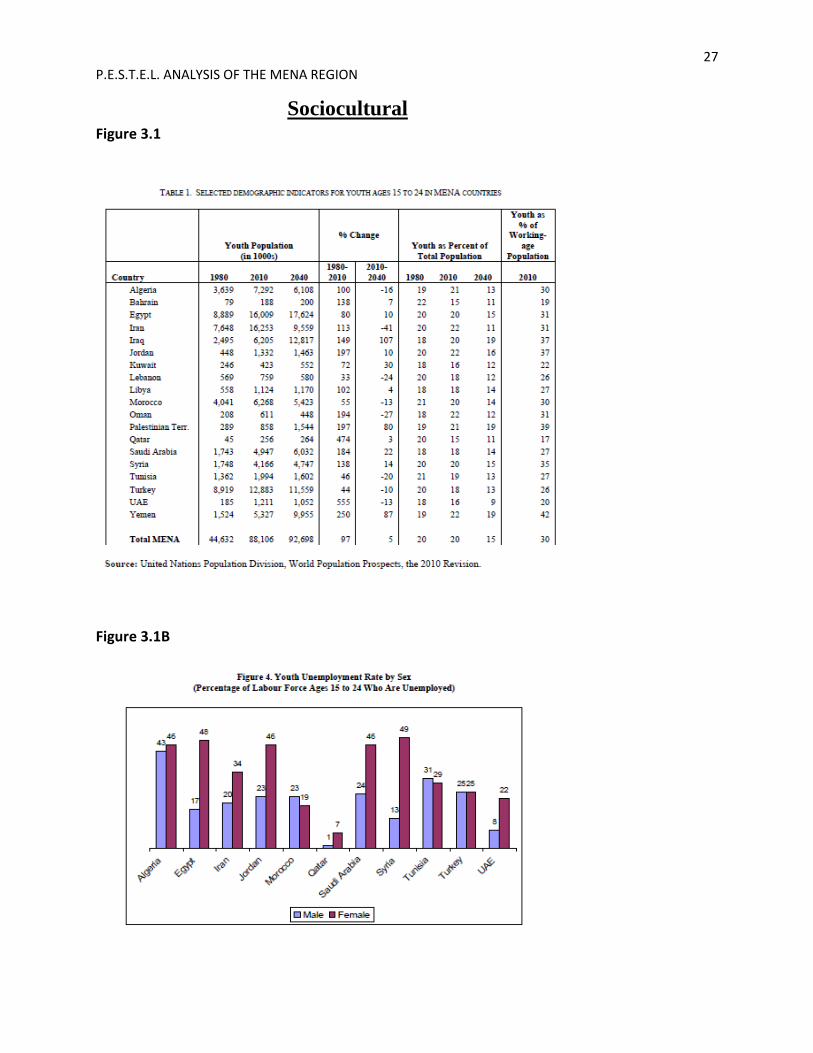

Going forward, generating jobs within the private sector for expanding populations will be a

pivotal challenge for the MENA region. A few member countries in MENA have begun taking

the appropriate measures to expand job markets as some sectors remain fragmented from the lack

of need for skilled labor. Countries can solve this issue by improving education throughout the

public sector, which would improve the need for a quality labor force. (Figure 2.5)

12 P.E.S.T.E.L. ANALYSIS OF THE MENA REGION

Socio-Culture

The age bracket of 15 to 24 represents 20% of the population in the MENA region. It is

estimated by the United Nations that over 90 million individuals in this peer group exist in the

MENA. This demographic has faced a tough job market over the past 10 years. Unemployment

levels are consistently low. Jordan has dealt with unemployment levels as high as 14% and it is

estimated that over 75% of these individuals are under the age of 30. In the nation of Egypt, it is

projected that 80% of the unemployed population is under the age of 30 and 82% of those

currently out of work have never been employed. This specific peer group in the MENA has the

highest unemployment percentage in comparison to the rest of the world. It is estimated that in

the next three decades Iraq will experience a surge in population in the 15-24 age bracket leading

to a net gain of 6 million. The “youth bulge” dilemma continues to be detrimental to the young

educated population, as their ability to find work is also on a decline. “Youth bulge” can be

attributed to those MENA countries were fertility was on a receding trend in the mid to late

1990’s. If we compare the estimated 5.6 births per woman in the 1980’s to the currenttwo births

per woman average(less than half) in 2000 in Iran, we can identify the source of the discrepancy.

This discrepancy is caused by the decrease in fertility rates during the mid to late 1990’s. Due to

this age brackets’ failed attempts to enter the workforce, the results have been:

Poverty as well as inequality,

It magnifies generational inequalities.

Leads to higher violence and mortality rates.

The youth unemployment rate is high when compared to other regions of the world, but the

labor participation rate among the youth (ages 15-24) has dropped. (Figure 3.1,B,C)

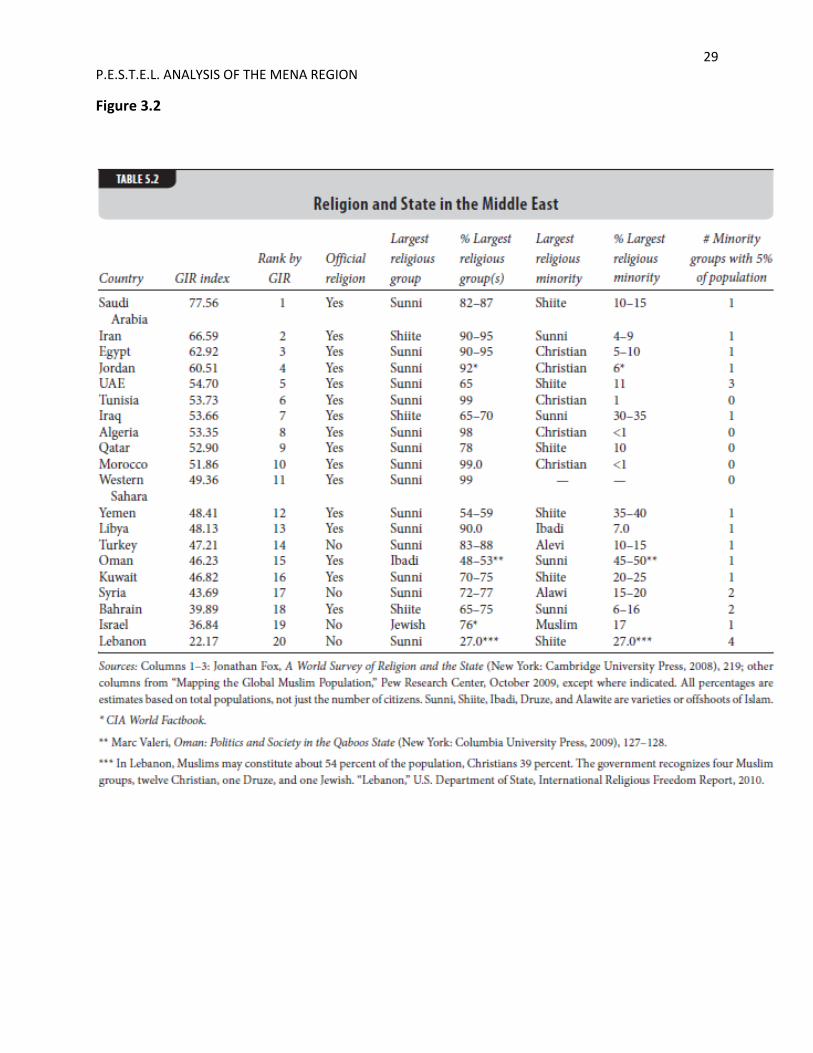

The separation of church and state is institutionalized in the western world. Within MENA, the

church and state go hand in hand. Based on table 5.2 we can determine that Islam is not the sole

decider on whether a relationship exists between the state and its dominant religion. There are a

number of states that do not consider Islam as their primary religion. These states are undeterred

by the fact that Islam is the dominant religion; this includes countries such as Turkey and

Lebanon. The Government in Religion Index (GIR) has scores ranging from 0 (low religious

influence) to 100 (high influence) and considers fivefactors to determine numerical rankings

within MENA. (Figure 3.2) Those roles consist of

State restrictions on religion

Restrictions on minority religions

Regulations on all religion

If the state legislation delegates the religion of choice

Official role of religion within the given state

A large portion of the countries have a small differential gap within their GRI rating. For

example, the UAE and Kuwait exhibit only an 8 point differential between them. Though the

scores are nearly identical the underlying values are quite far apart. In Northern Africa, Tunisia

has championed a movement to prevent religious ideals from taking over daily life. Tunisia has

looked into managing the practice of religion in the region. Their perspective contrasts to that of

13 P.E.S.T.E.L. ANALYSIS OF THE MENA REGION

the Persian Gulf which has traditionally accepted religion and law uniformly. Religion has

played a major role in the groundwork legislation of the Persian Gulf.

The fact that Syria, Israel, and Lebanon are on the bottom of the GRI does not correlate with a

decline or the acceptance of religion within politics. The reason we see this trend is, for example

in Syria, political power has belonged to the one of the Islamic religions’ larger groups (the

Sunni sect) as well as the largest religious minority, known as the Alawi (Shiite-aligned). The

state tries not to influence the practice of the different religions within its borders but religion

does not affect how political positions are distributed. A clear example if this is in Israel.

Religion showcases its influence through the country’s political parties and through the leverage

that Orthodox Judaism provides to the church as the established national religion. Israel openly

refers to itself as a Jewish state. Citizens of the region have most recently used religion as a force

to pursue political and social gains in ways that the previous generation would have not

considered. This ultimately affects the character of religion within the region.

Emigration is on a continued rise in MENA as a consequence of the Arab Spring. Egyptian

people have fled according to the International Organization for Migration (IOM) due to protests

and riots within their countries’ borders. Over 66% of individuals surveyed by the IOM who

contemplated migration were affected by events manifesting from the Arab Spring:

20% were asked to leave their employment without compensation

26% lost their jobs

19% saw working hours reduced

Libya has been host to over 1.5 million workers from other nations mainly from the Tunisian

and Egyptian regions. It is expected that these individuals will have a negative effect on the

Libyan economy once they flee the region due to consistent Arab Spring demonstrations. Over

100,000 Tunisians have returned to their home country due to ongoing threats to their personal

security within the nation of Libya. Even though the Arab Springs brought about actions

detrimental to Libya, the Libyan National Transition Council (LNTC) has allowed the UN and

other regional neighbors to have hope for the stabilization of emigration and reconstruction of

the country.

Some forces behind the Arab Springs have been high unemployment rates and low economic

opportunities. Other instigators include lack of democratic representation and the continued

corruption within governments. Even though these variables are politically sound, they

ultimately affect the economic and investment opportunities for a nation. According to the World

Economic Forum (WEF) the biggest deterrent in conducting business in the MENA region is

corruption. The concurrent abuse of political influence and increasing levels of corruption has

resulted in a 3.1 score (entire MENA region) given buy the Transparency International (TI)

Corruption Perception Index (CPI). Even though Arab Spring demonstrations have caused a

reduction in works hours, reduced compensation, and lost jobs it has brought forth some positive

changes. It has led to reforms in several MENA countries. This builds a foundation for the

chance to fight corruption and to promote the proper rule of law. Groups like the MENA-OECD

Working Group on Corporate Governance is focused on encouraging state owned enterprises to

promote full disclosure and transparency in their business practices. These goals will help lead

the MENA region down a new path. This will take time, given the amount of deep rooted

corruption that is entrenched in governments & corporations within the MENA.

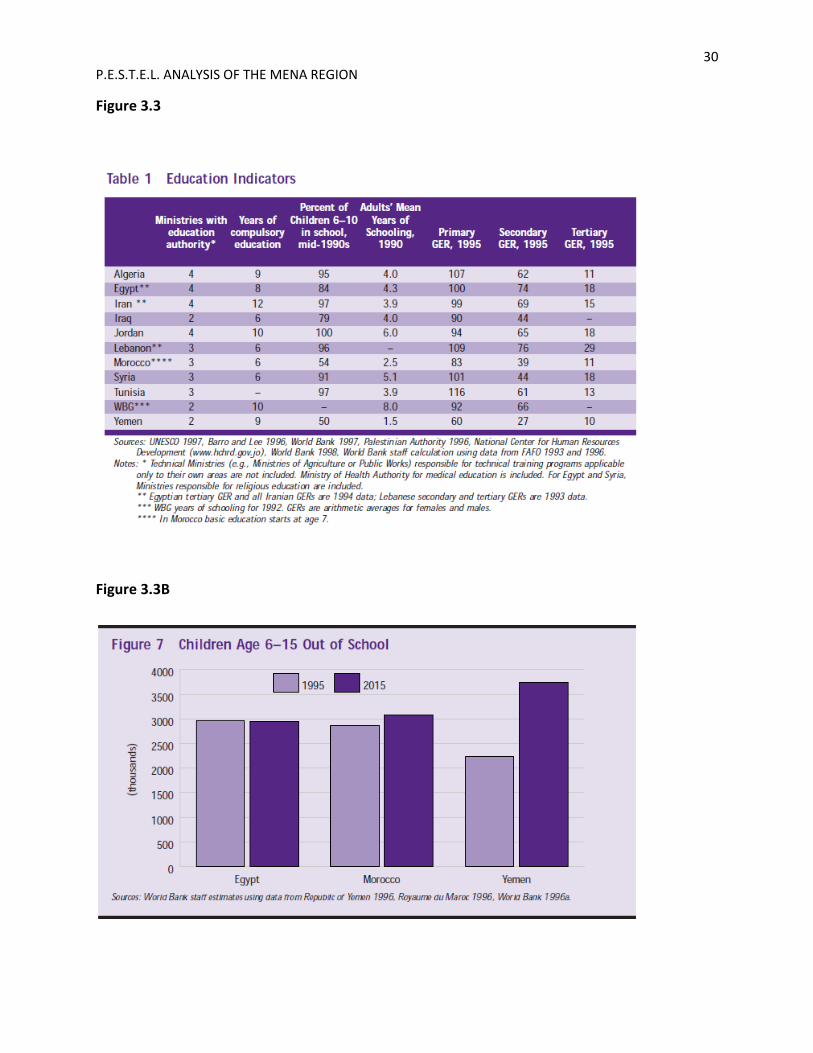

The investment in basic education within MENA is on a decline. School enrollment for the age

bracket of 5-14 is expected to drop by the year 2015. In regions such as Jordan and Iraq the

14 P.E.S.T.E.L. ANALYSIS OF THE MENA REGION

school age cohort is expected to continue to grow in the next decade. (Figure 3.3) The necessity

for higher learning within these nations will continue to rise as lower percentages of individuals

have yet to attain vocational or secondary education.

The overall quality of the education has suffered due to a growing number of students in the

region. The percentage of secondary education teachers in Iran has doubled to help meet

demands, although the amount of teachers with university degrees has dropped from 84% to

77%. Further increasing the burden for these underprepared teachers with a lack of overall

compensation will continue to discourage entrants to the field. The ongoing trend of student to

teacher disparity and the establishment of schools in rural villages leaves room for improvements

in faculty deployment, resource allocation, and in the quality of education for countries such as

Jordan, Egypt, and Morocco.

15 P.E.S.T.E.L. ANALYSIS OF THE MENA REGION

Technology

The current growth rate of nuclear energy development in the MENA region is on an

exponential rise. Nuclear development in the Middle East is entering a renaissance stage with the

proliferation of its acceptance as an alternative source of energy within the region. With

countries such as the United Arab Emirates (UAE) launching programs to initiate the

development of nuclear power, there is no indication of a decline in the quest for alternative

energy within the MENA region.

Turkey is close to acquiring the rights to develop its own nuclear energy reactor. The license is

expected by year end 2014. Egypt has announced plans to begin construction of its own nuclear

power plant by the 4th quarter of 2014. Struggles with nuclear development over the years have

been hampered by incidents like Chernobyl in 1986 and the economic struggles in 2011

coinciding with the Arab Spring. The MENA is trending to become the most ‘up and coming’

region in the development of nuclear power plants worldwide. The current estimated investment

in nuclear power is at $400billion dollars (comsan25). Saudi Arabia is expected to deplete its

crude oil resource by 2030.

The demand for electricity in the region is expected to rise from 75 Giga Watts (GW) to 120

GW by the year 2030. To help address the ongoing trend of increased energy demands in Saudi

Arabia, the King Abdullah City for Atomic Research was founded. The purpose is to focus

solely on the production of alternative energy within the region. The creation of 16 nuclear

reactors will take place in the next two decades with estimated costs of $7 billion dollars. With

this initial investment, Saudi Arabia will become the largest electricity exporter in the region.

Jordan, one of the driest countries in the region, is modifying the use and application of treated

sewage water to help cool nuclear reactors. This technology will be applied all future nuclear

endeavors.

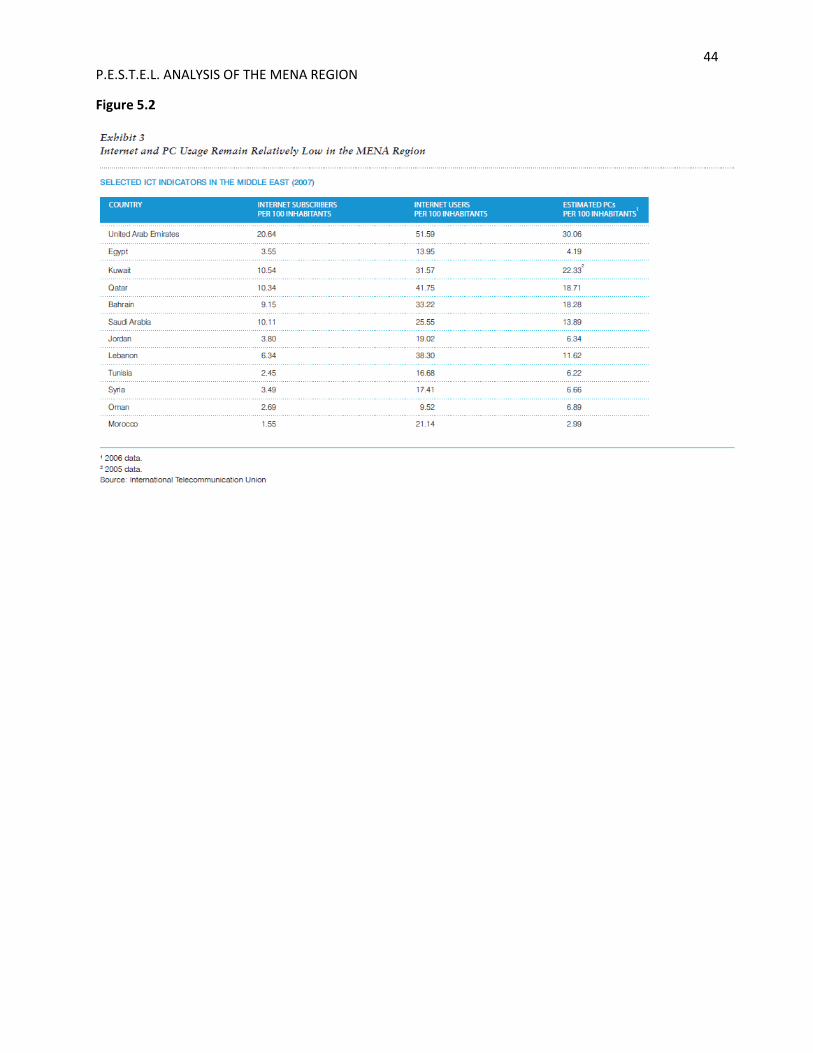

General acceptance of technology in the MENA region has been hindered due to a lack of trust

in the Global North (North America & Europe). (Figure 5.2) Privacy and trust are intertwined in

the culture of the MENA nations. It helps influence the reception of new technologies when the

source of the technology is an allied state. The continued advancement of technology is seen as a

direct threat to the social and cultural norms of the region. The rapid development of technology

like the internet has caused older generations to struggle with its acceptance. The knowledge that

is usually disseminated by the elderly to the younger generation is on a decline. A significant

factor that new technological trends must overcome in the region is the stranger in our midst

dilemma. Stranger in our midst refers to the imposition of spy and malware believed to be

ingrained into the programming of technology sourced from the Global North.

Having a figure that is trusted within the culture to sponsor and promote new technological

trends will allow for the proliferation of acceptance within the elderly population. The

governments in power within the MENA countries have a strong effect on positive technological

reception. A combination of influential factors determine technological adoption rates in the

region: Government encouragement of technological adoption, government sponsored trust

towards the Global North, or the trust that the Global North has in the use of its technology

within the MENA. Most MENA countries place significant barriers on the introduction of

technology from the Global North. This is due to the potential exposure to spyware and malware

believed to be in these systems. The slow adoption of internet access in Syria is an example of

government intervention. The market share is insufficient to lure tech companies into the MENA

region for fear of the empowerment of these nations and the militarization of their shared

16 P.E.S.T.E.L. ANALYSIS OF THE MENA REGION

technology. Continued trends in the MENA will focus on development of technology that will

not necessarily benefit the population in everyday functionality, but rather as force to help

control this specific region of the world.

A challenge faced over the last 10 years is the inconsistent growth and advancement within the

technological infrastructure. The only growth that has been present is factor accumulation labor:

land, capital, and entrepreneurship. Factor productivity, the workplace incorporation of

technology, has remained stagnant. Stagnation has resulted in slower technological growth and

acceptance within government structures. MENA is characterized as having large public sectors,

governments that are centralized, and a complex regulatory system. This is evidenced by the

lack of the modernization of public and governmental institutions. By introducing the

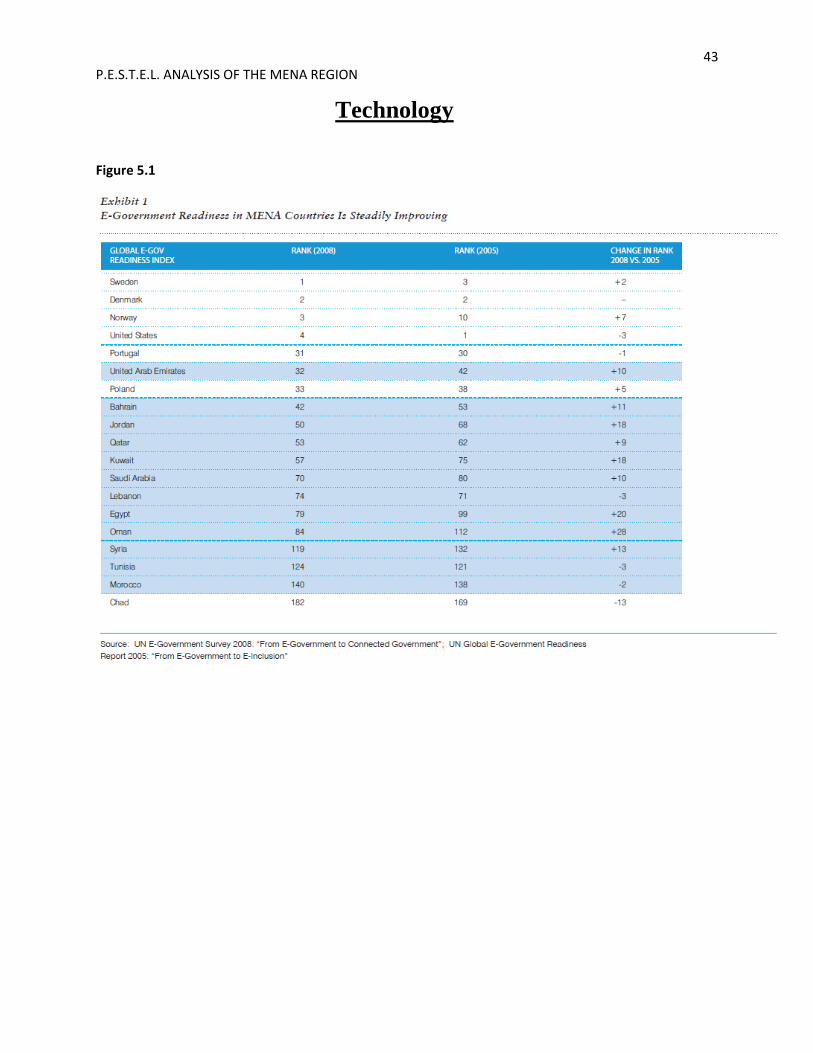

technological infrastructure to local governments, E-Governance is established. (Figure 5.1) E-

Governance has allowed for the removal of obstacles permitting a streamlined flow of

government information for local and central governmental institutions. E- Governance allows

for the optimization of small business through the ability to access services online 24 hours a day

while reducing the hindrances of distance and hours of operation. It will help reduce some causes

of corruption and potential bribery due to the transparency of governmental policies.

Though leaders in the Mena region have taken steps to achieve E-governance, it is up to the

citizens to embrace these new technologies to make E-Governance a viable source of

information. The implementation of E-Governance in MENA relies on a well versed customer

service approach to government amenities. The continued adoption is key in maintaining the

competitive edge in a global environment. E-Governance readiness in the MENA region is on a

constant rise (Exhibit 1). Governments can access global vendor marketplaces allowing the

procurements of products and services at the most competitive price. An established E-

Government will allow for the use of E-Commerce and global trade. To have a successful

implementation of E-Governance several factors must be considered:

Is the existing government stable enough to develop this program

Is the infrastructure ready

Is the population open to adoption

Egypt enhanced its telecom infrastructure to support this advancement. Over $1 billion has

been invested and Egypt currently boasts an over 65% increase in internet user subscribers. It is

important to have awareness and education to understand and take advantage of these services.

With the continued trend of development, the implementation of a standardized E-Government

across the countries in the MENA region will be swift and successful. E-Governance application

will create fundamentals through accountability, transparency, and responsiveness to the needs

of its citizens leading to a more proactive and democratic system.

17 P.E.S.T.E.L. ANALYSIS OF THE MENA REGION

Environment

The environment in the MENA has been at the bottom of the list of priorities for almost every

country in the region until recently. Industrialization, modernization, expansion of the electric

power grid, and population growth are some of the major factors garnering new attention from

the leaders and citizens of MENA alike. A significant increase in the regions renewable energy

market is being driven by a number of factors including energy security, demand growth due to

population expansion, urbanization, economic progress, and water scarcity. Hydroelectric power

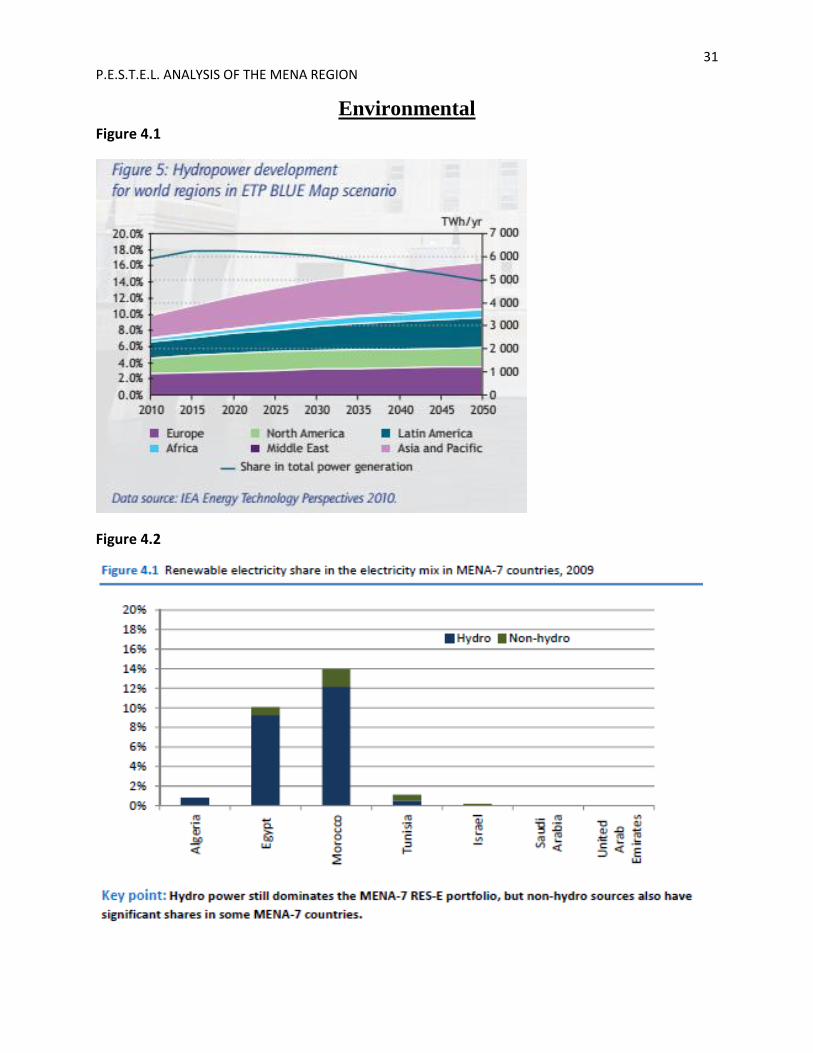

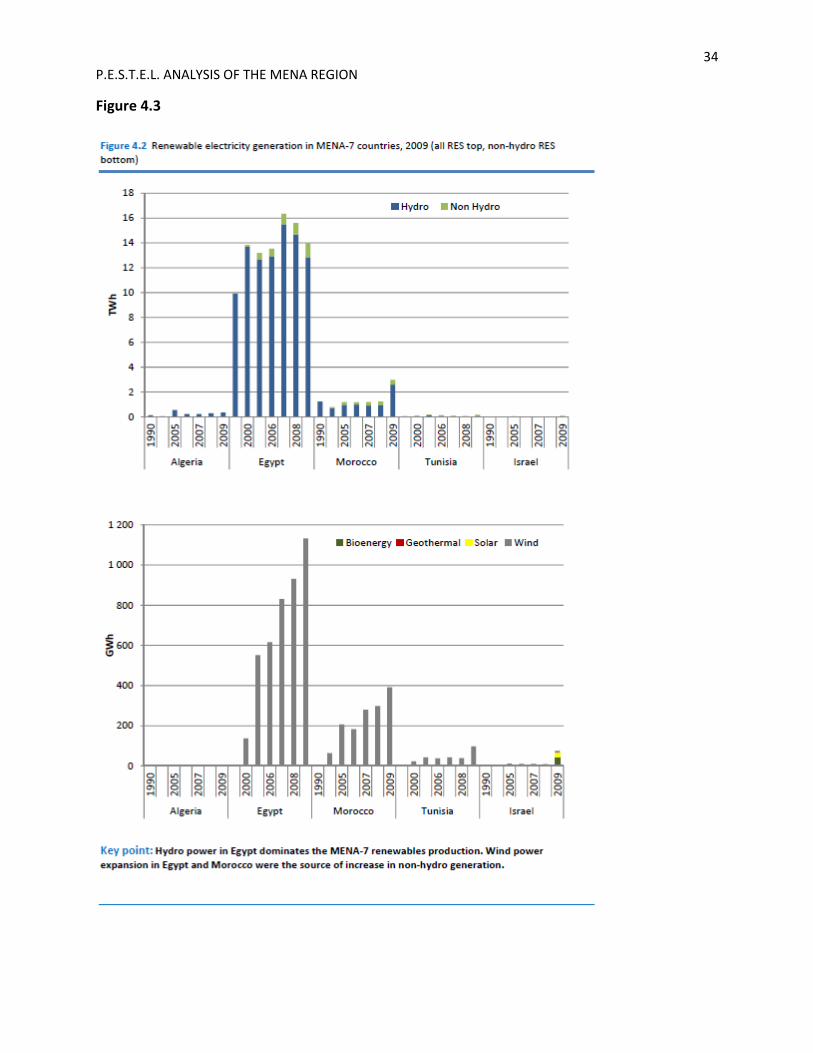

is the major producer of renewable energy supplies currently in the MENA. In the middle-east

alone, hydroelectric power plants are producing 1,000 Terra Watt Hours (TWH) of power per

year. (Figure 4.1) Unfortunately these numbers are stagnate and projected to remain so through

2015 with only a small increase, due largely to upgrades in technology, through 2050. Non-

hydroelectric renewable power generation almost doubled from 2008-2011 to 3 TWH. This

growth has outpaced traditional carbon based energy sources. Within this category wind has

become the largest supplier of renewable energy (8 MENA countries with capacity totaling 1.2

Giga Watts as of 2012) after hydro. Solar power has seen rapid adoption as well through solar

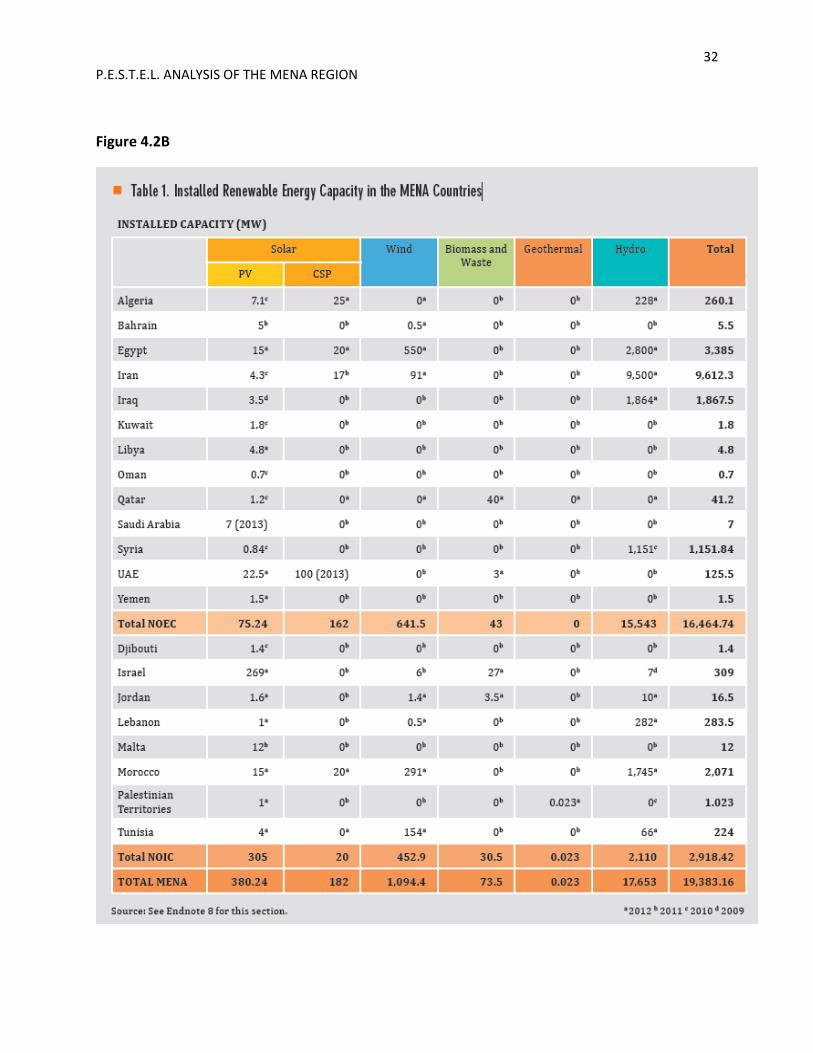

farms called Concentrated Solar Power (CSP) plants. Algeria, Egypt, Iran, and Morocco have all

established CSP plants with the UAE recently completing construction of the world’s largest

CSP plant. (Figure 4.2, B, C)

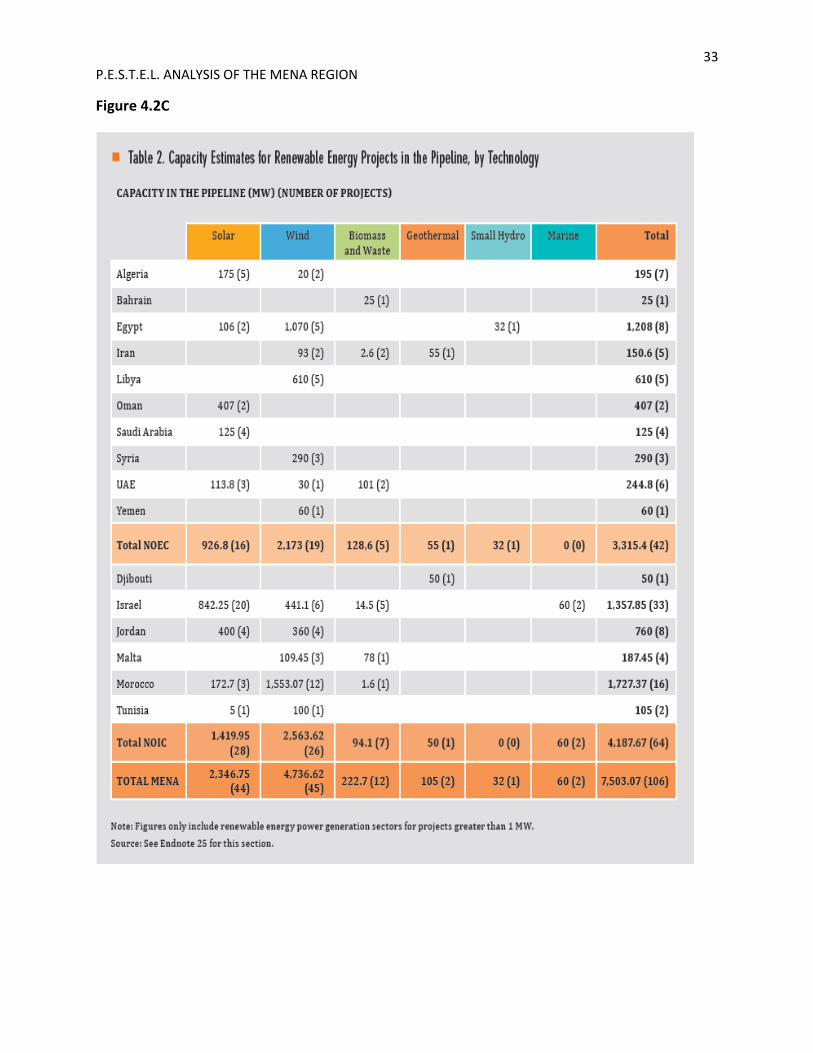

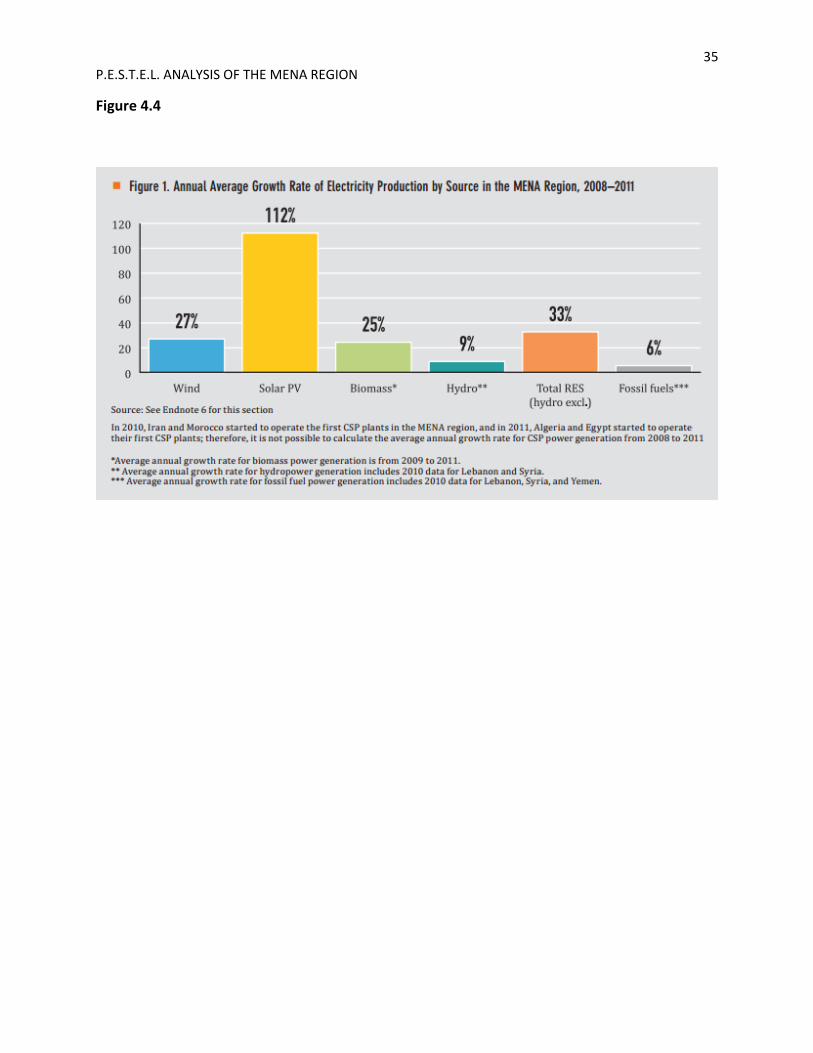

There are 106 renewable energy projects planned for the region as of April 2013. These

projects will produce 7.5 GW of new capacity which is a 450% increase over existing non-hydro

renewable power generation current output, of which wind and solar constitute 85%. (Figure 4.4)

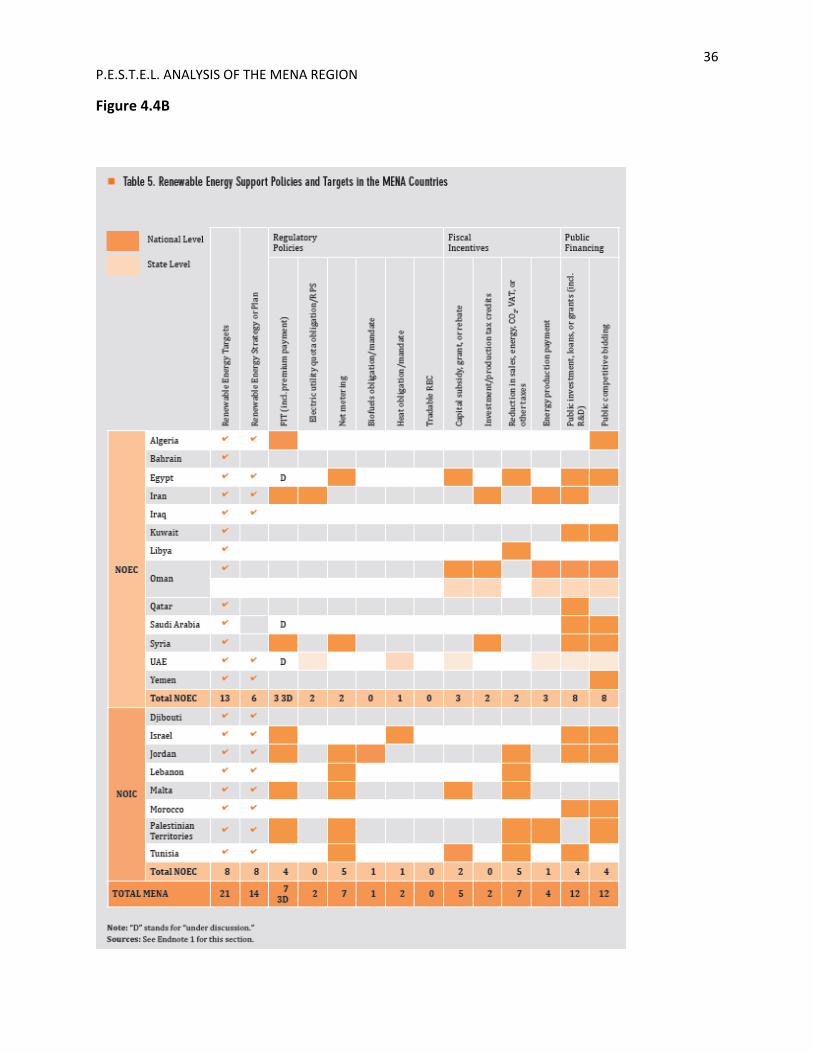

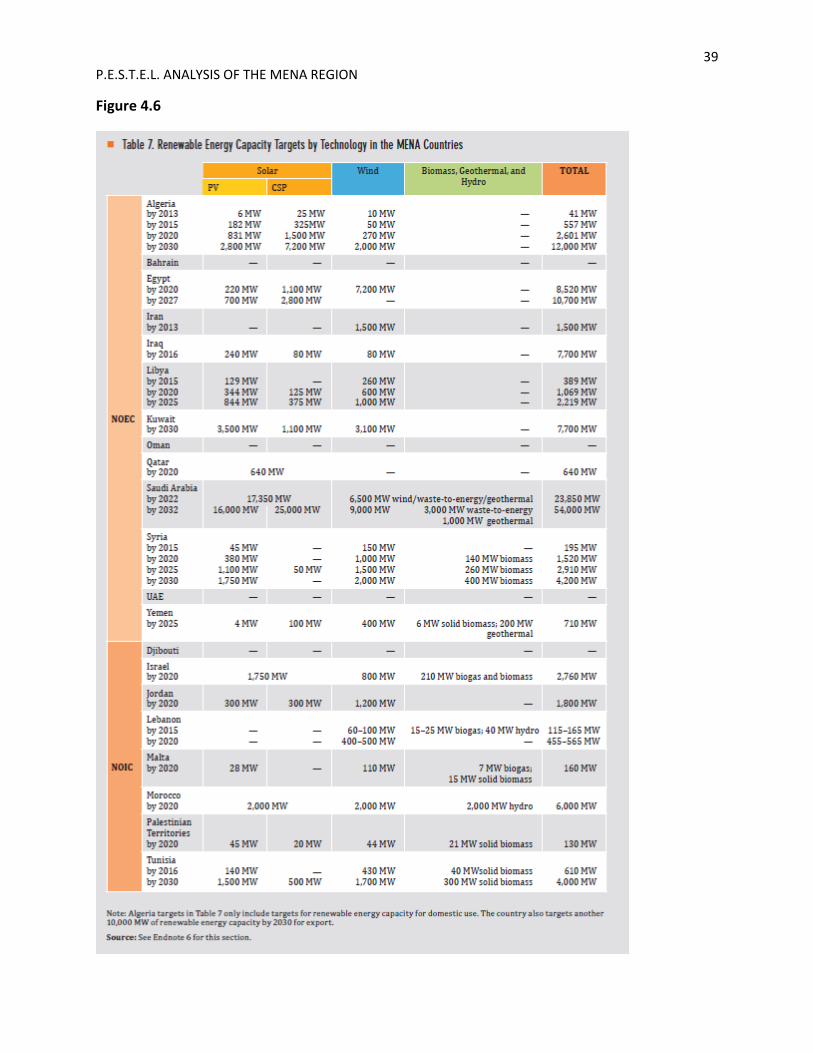

Just five MENA countries as of 2007 even had renewable energy goals. As of May 2013, all of

the countries in the region now have a target for renewable energy production. (Figure 4.4 B) If

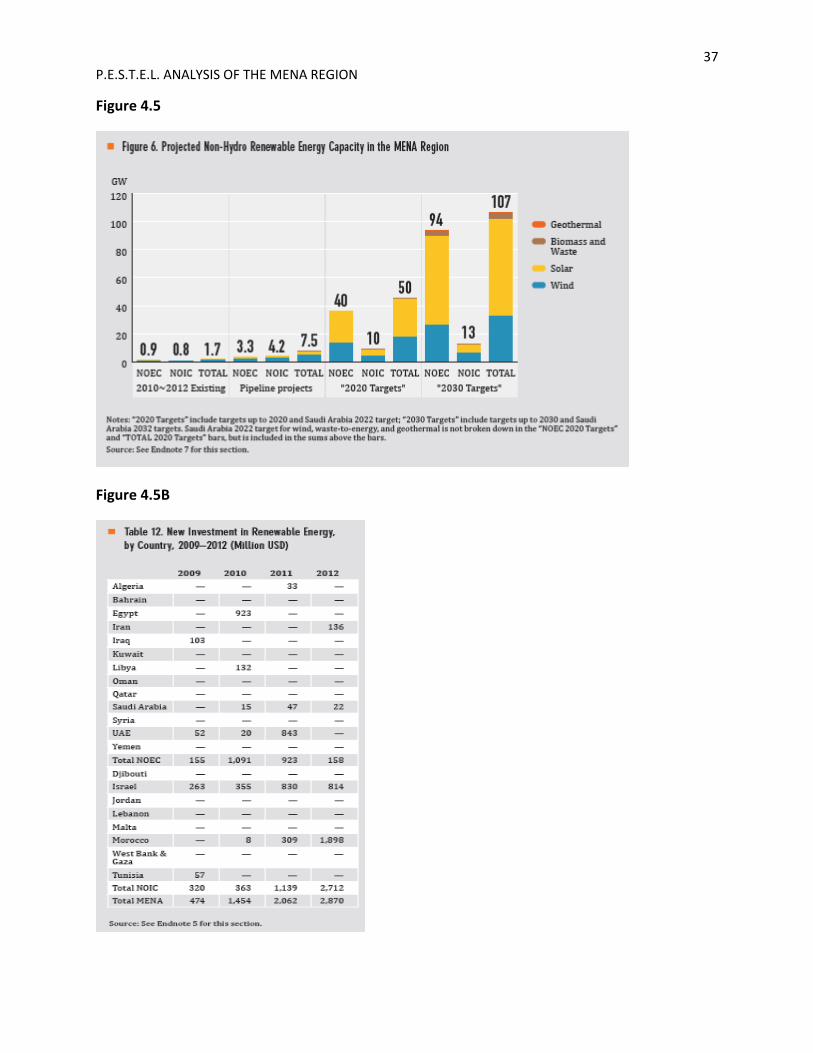

attained, the effect would be 107 GW of increased capacity by 2030. The global economic crisis

appears to be absent from renewable energy investments in the MENA region. New investments

in renewable energy reached $2.9 billion dollars in 2012 (Figure 4.5 B), a 40% increase over

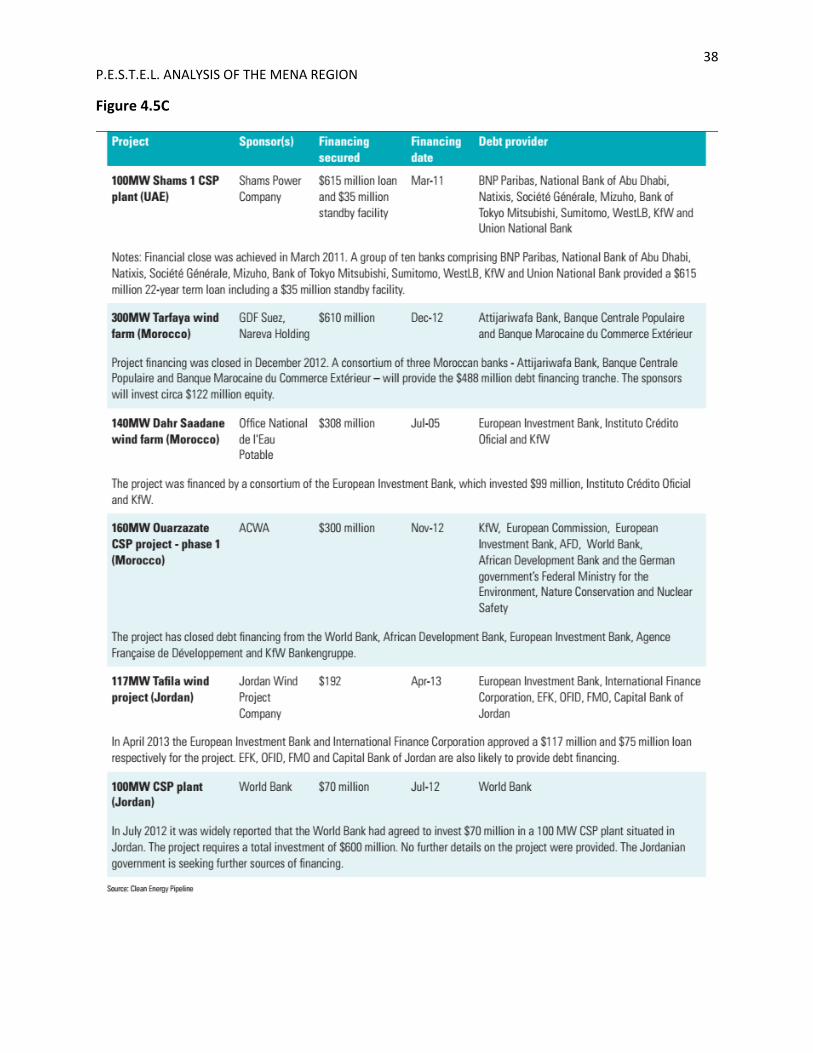

2011, and that is a 650% increase since 2004. (Figure 4.5 C)

The electric grid in the MENA region now reaches 99% or more of the population in over half

of the countries (11 out of 19) for which there is data available. There are 28 million people in

rural areas still without electricity, with 8% relying on alternative bio-fuels as their main source

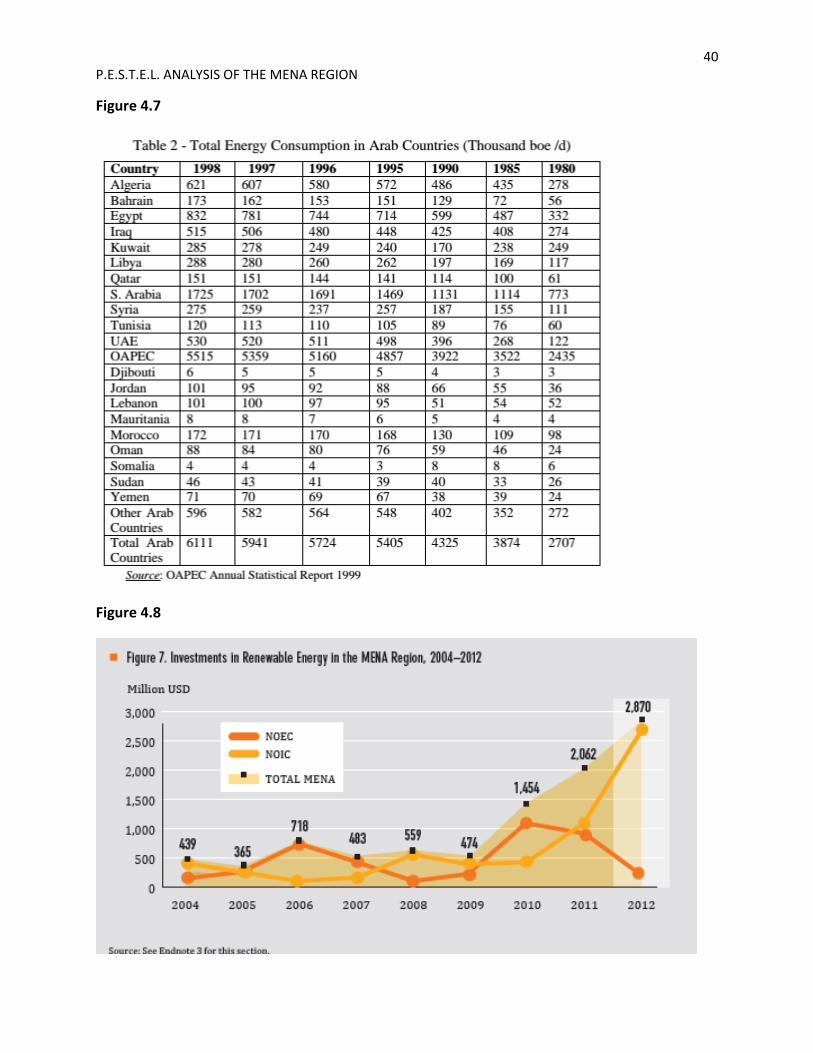

of energy. The total Primary Energy Supply for the MENA region in 2010 was up 14.9% from

2007 and achieved an average annual growth of 4.7%. Increased consumption is attributed

largely to population growth through the use of electricity to power machinery, heating &

cooling, and water desalinization. In comparison, renewable energy supplies increased 27.6%, or

at almost double the rate of current primary energy supply sources. This trend is expected to

continue as increasing consumer and industrial demands for power show no signs of slowing.

(Figure 4.7)

For Net Oil Importing Countries (NOIC) adoption of renewable energy is attributed to energy

security and the avoidance of having to continue to import expensive oil in the future. (Figure

4.8) Net Oil Exporting Countries (NOEC) recognize that production capacity has peaked and

that there is an opportunity cost related to oil and gas in a domestic context. Rapid increases in

demand for energy from air conditioning, desalination, and technological adoption are caused by

rising GDP, urbanization, and expanding population levels that are not going to be sustainable

with the current dwindling carbon based fuel supply. Leaders and policymakers in MENA are

realizing the positives to be gained from renewable energy adoption. Greenhouse gas reduction,

18 P.E.S.T.E.L. ANALYSIS OF THE MENA REGION

improved health, urban rural development, job creation, manufacturing, and power independence

& security are some examples of areas of concentration by governments. Seven MENA

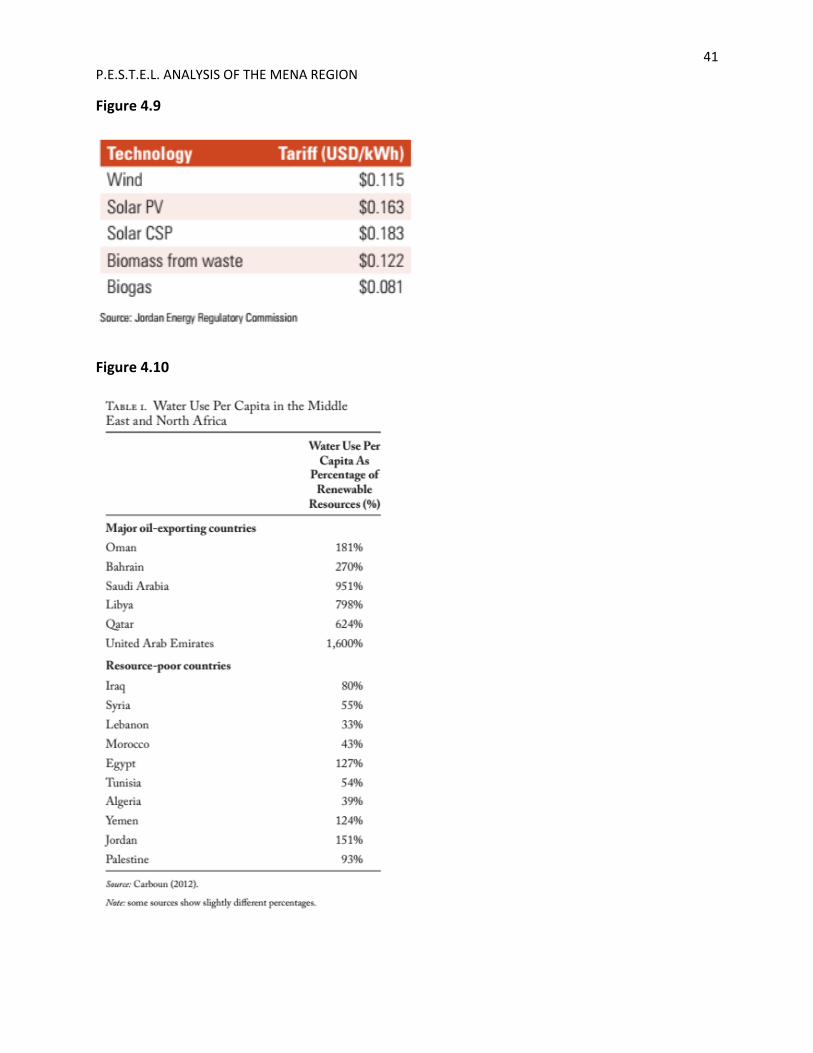

countries have adopted ‘Feed in Tariffs’ (FIT’s) as a way to help meet their lofty energy

expansion goals. (Figure 4.9) Qatar Airways has undertaken development of bio-fuels in

partnership with related industry companies such as Rolls Royce (jet engines) and Air Bus.

Government parliaments and publicly owned electric companies are also pioneering renewable

energy initiatives with financing and incentives from institutions such as the World Bank Group.

The presence of water in a region has determined the development of settlements for people in

the MENA since the beginnings of recorded history. According to the Maplecroft Waterstress

Index of 2011, the MENA region contains some of the highest ratings for ‘extreme risk’ of

insufficient and un-renewable water supplies versus the stresses of demand. These countries

include Bahrain, Libya, Qatar, Yemen, Kuwait, Saudi Arabia, Israel, Jordan, and the Western

Sahara. The index measures domestic, industrial, and agricultural uses of water against

renewable reservoirs in rivers, groundwater, and from precipitation. There are five main bodies

of fresh water in the MENA:

Tigris and Euphrates basin

Jordan River basin

Arabian Peninsula basin

Nubian Sandstone aquifer

Nile basin

Average water availability per person globally is 7,000 𝑚3/person/year. In MENA however,

that availability drops to 1,200 𝑚3/person/year. A predicted increase in population from 300

million (2012) to 500 million (2025) would bring the availability of water per person to half of

the current amount by 2050. (Figure 4.10) MENA contains roughly 6.3% of the global

population and has access to only 1.4% of the world’s renewable fresh water. The UAE and

Libya receive their fresh water from ancient underground aquifers and from the desalinization of

seawater. The aquifers are referred to as paleo-ground-water and can be up to 30,000 years old.

They are practically non-renewable by natural means. Desalinization is a short term solution, but

it is costly to energy supplies to produce. Using fossil fuels to remove salt from seawater is

unsustainable in the long term.

Extreme heat, low precipitation, harsh geography, and massive dust storms have become an

accepted part of life to some residents of the MENA. The region is characterized by is arid and

hyper-arid climates which encompass more than 78% of the total land mass. Rainfall in the

region is seasonally erratic with much deviation in amounts from year to year, ranging from

50mm-500mm. The Arab region consists of 54.8% barren land, 26.8% rangelands, 10.3%

cultivated land, and 3.9% forested area. Drought negatively impacts a region in many ways:

Reductions in productivity

Degradation of natural resources

Degraded humanitarian & social conditions

Downgraded economy

Decreased agricultural capacity

Depletion of livestock

Significant adverse effects on economic activity include increased spending on food and water,

import/export imbalance, price volatility, market failure, depleted surpluses of commodities, and

19 P.E.S.T.E.L. ANALYSIS OF THE MENA REGION

lower income levels. Different socioeconomic factors for individuals determine the degree to

which they are affected by drought related famine situations.

Air pollution is becoming an ever worsening problem in the MENA region. High levels of

suspended particulates, sulfur dioxide, and increasingly violent dust storms are beginning to take

their toll. (Figure 4.11) Air quality is recognized as one of the most important factors affecting

sustained growth on a regional scale. In addition to economic limitations, air quality greatly

impacts human health leading to inefficiency and decreased productivity. Dust storms and acid

rain cause excessive deterioration of raw materials, assets, and may give rise to new degenerative

sicknesses. MENA countries must work together to combat ever increasing air and water quality

issues. Large scale gas and oil exploitation, processing, and reformulation coupled with

industries like power plants, petrochemicals, fertilizers, steel, and aluminum all represent large

contributions to pollution and are loosely regulated. The transportation sector accounts for 70-

80% of hydro carbon emissions. (Figure 4.12) The lead in gasoline accounts for 100% of lead

particulates in urban areas. The more developed gulf countries like the UAE account for

approximately 50% of CO2 emissions (254 million metric tons of carbon) in the MENA region.

While awareness of environmental issues is on the rise, with the exception of renewable energy,

not much progress is being made towards combating the accumulating environmental deficit the

MENA is currently experiencing.

20 P.E.S.T.E.L. ANALYSIS OF THE MENA REGION

Legal

Cultures and traditions vary throughout MENA, the legal impact on the regions macro

environment effects governments and its citizensthrough multiple variables. Analyzing the

structures of:

Judicial systems

Impacts of religion on law

Women’s civil rights

International trade regulation

Organized crime and the black markets

Understanding these variables will allow for accurate forecasting of the level of influence that

governments and their institutions have on the macro environment.

Developing an analysis of MENA’s legal systems is integral in understanding the political

atmosphere and its ability to influence and shape actions on human rights. The court system can

act either as an enforcer of human rights claims or abuse its power by ignoring them. Progress

can be made with more responsive behaviors or regress and transform towards more suppressive

conduct concerning advancement.

There are two kinds of judiciary structures, dual and unified, that are prevalent in the MENA

region. Countries with dual structured systems, like Tunisia and Lebanon, are split between the

civil and administrative courts. MENA countries like United Arab Emirates and Yemen believe

in unified judiciary systems. Both forms do accept appeals cases before the courts and in some

instances separate civil litigious pursuits from administrative ones.

Judiciary systems do have their share of issues as they face structural problems that often force

both defendants and prosecutors to avoid use of the courts. These issues are comprised of:

slowness in court settlements, increased costs of litigation, and the ineffectiveness of

implementing decisions. Lebanon and Tunisian judicial systems suffer from low numbers of

acting judges in relation to the amount of cases received throughout the courts. This scenario

creates a logjam of impending cases.

Continued inefficiencies throughout the courts create civil distrust in the judiciary system and its

litigants, who are forced to exercise the option of a tribal means for conflict resolution.

MENA’s legal systems have historically been intertwined with religious or tribal law, which can

often be qualified as outdated, though gender inequality is prevalent within legislation across the

region. In comparison to other nations across the globe, the MENA region has lagged in matters

of gender inequality. Cingranelli and Richards (CIRI) a Human Rights Dataset illustrates MENA

attaining the lowest global scores regarding both the values of economic, political, and women

rights.

Historically, religious fundamentalism has played a key deterrent in the improvement of female

participation within the legal system throughout the region. Another barrier to advancement is

the complexity of the legal system. Courts are divided by the various religious groups they have

jurisdiction over.

Interfaith marriage is a topic that comes into light under the context of religious involvement in

the courts. Multiple countries in MENA have made the act illegal. As a result of such

arrangements, religious segregation becomes embedded within the MENA state’s policies. Such

policies make forecasting the legal spectrum throughout the MENA region difficult, as there is

21 P.E.S.T.E.L. ANALYSIS OF THE MENA REGION

currently little to no separation between state and religion.

Exploring MENA’s trade policies will allow for an understanding of the region’s openness to

global exchange and their impacts relative to growth in the business environment. MENA’s

trade behaviors could historically be categorized as closed or protectionist based. Such policies

have been factors in MENA’s decline in both foreign investment and growth within the public

sector.

Traditionally, foreign ownership has been hedged substantially as regulations have been in place

since the 1990’s to reduce foreign majority ownership in business. Due to a downward trend in

local economies, member countries have developed political reform that encourages such

ownership structures. In 2000 Qatar approved legislation that allowed full ownership to foreign

investment groups in the industrial, agricultural, education, tourism, and health sectors. MENA

states like Bahrain, Egypt, United Arab Emirates, Jordan and Morocco incentivize foreign

investment with free trade zones.

International trade reform & policy, which spurs foreign direct investment (FDI), is integral to

the progress of MENA countries expansion of new businesses to create competition and new

employment opportunities. Continuing this trend throughout the MENA would allow for

increased FDI capital flows that would initiate expansion throughout the public sector and help

to institute long-term economic stability.

The MENA can be viewed as a region where the relationships between geography and political

structure heavily influence its economy. For the region to form a thriving economic environment

the judicial and legal components of authority need to be updated drastically. Lack of

implementation of enhanced corporate governance and anti-corruption laws will have a

pronounced negative fiscal effect on the business environment, which will continue to decline

without such vital measures in place.

Aside from of economic benefit, MENA must strengthen its authority over member countries

that partake in organized crime. The majority of organized crime revolves around drug

trafficking, arms dealing & transport, and money laundering. Recently, this type of activity has

become increasingly widespread throughout the region and will continue to trend this direction if

accountability measures are not enforced.

Of concern is the illicit and lucrative drug trade & trafficking routes that criss-cross the MENA

region. Due to the illegal nature of these substances, high profit margins, and the unquenchable

demand from the back market, terrorist organizations and governments alike via for their piece

of the multi-billion dollar industry. Irregardless if its opium & heroin (19 metric tons annually)

produced in Iran, poppy seed transport from neighboring Afghanistan & Pakistan, or cannabis

resin produced (38 metric tons annually) in Algeria, there is ample money to be made. Every

year thousands of tons of drugs are sized throughout the MENA, but hundreds of thousands of

tons get through U.N. dragnets. Large seizures of illegal narcotics are not rare and amount to a

small fraction of the true tonnage moving through or produced in an area. Examples such as:

12.8 tons of amphetamines in Saudi Arabia

936 tons of marijuana in Africa

221.9 tons of marijuana in Morocco

1 ton of marijuana in Israel

561,272 kilograms of opiates in Iran

22 P.E.S.T.E.L. ANALYSIS OF THE MENA REGION

The financing from these illicit sources of fast cash are used for terrorism, private armies, and

personal gain. These relationships are easy to perpetuate throughout bureaucraciesdue to the

constant and pervasive corruption of the MENA countries as shown by the TI Corruption Index.

As long as there is a world-wide market willing to pay premium prices for banned substances,

this trend will continue to increase for the foreseeable future.

23 P.E.S.T.E.L. ANALYSIS OF THE MENA REGION

Going Forward

Wars and infighting have been an institutionalized way of life in the MENA region for

thousands of years. From the first recorded clashes between the Israelites and the Egyptian

Pharos, the Carthaginians, Philistines, Hittites, Persians, etc, there has been generations of

mistrust, ingrained hatred, and bloodshed. This region has come a long way in the last 100 years

through the discovery of vast amounts of commodity wealth. To break the cycle of violence and

hatred prevalent in the MENA, these countries must achieve what has rarely been accomplished

in the annals of history. They must strive to put their differences aside and realize that each

country’s fate is intertwined with that of its neighbors. The MENA must look past religion and

language to ensure a secure future for everyone in the region. MENA countries must develop

socially through:

Incorporation of youth and elimination of gender disparity

Removal of barriers between rural and urban residents

Transparency and accountability from government and leadership

Upgraded infrastructure

Energy security and independence for the future

FDI and fair distribution of capital and credit

Some individual nations may make advancements in these areas, but until the people of the

MENA realize that everything they do affects everyone around them and learns to work together

towards common goals, then they are invariably entrenched in the unending cycle of war, death,

and misery that has plagued the region incrementally for thousands of years.

24 P.E.S.T.E.L. ANALYSIS OF THE MENA REGION

Appendix (Graphs)

Economics Figure 2.1

Table 1. MENA Countries: Selected Economic Indicators, 1995-2002

1995 1996 1997 1998 1999 2000 2001 2002

Real Non-Oil GDP (percent) Bahrain 4.2 3.7 3.0 3.7 2.9 4.1 5.7 4.9 Kuwait 3.4 3.1 4.1 3.1 1.0 1.1 0.5 1.1 Oman 5.0 2.8 6.1 2.6 -0.6 5.5 8.8 2.4 Qatar -1.6 5.5 14.6 2.2 0.4 2.0 3.5 4.5 Saudi Arabia 0.5 1.0 4.5 2.6 2.8 3.9 2.5 2.9 United Arab Emirates 9.1 8.3 9.2 5.0 7.5 9.7 4.6 4.8 Algeria 4.0 3.8 -0.5 5.5 2.3 1.3 3.3 4.0 Egypt ... ... ... ... ... ... ... ... Iran 3.5 6.2 7.1 3.8 2.5 4.9 6.7 7.4 Libya -0.3 4.4 8.0 -5.3 2.6 5.1 2.5 2.4 Yemen 9.4 4.6 9.1 7.2 1.8 3.9 3.9 4.5 Non-Oil Fiscal Balance (percent of GDP) Bahrain -17.5 -16.9 -17.6 -17.6 -17.4 -16.8 -18.1 -20.6 Kuwait -39.2 -26.8 -22.2 -28.6 -23.9 -16.4 -20.2 -25.6 Oman -33.9 -29.1 -28.5 -28.9 -28.0 -27.8 -31.0 -29.5 Qatar -29.3 -37.0 -30.6 -31.9 -27.7 -18.0 -23.0 -14.2 Saudi Arabia -27.8 -26.4 -28.4 -23.6 -23.3 -27.1 -30.7 -29.5 United Arab Emirates -22.5 -26.1 -18.5 -20.1 -19.4 -15.4 -24.2 -26.3 Algeria -23.1 -22.9 -26.3 -24.3 -25.8 -33.1 -31.5 -33.1 Egypt ... ... ... ... ... ... ... ... Iran -24.5 -21.1 -18.1 -15.1 -12.9 -16.8 -17.2 -23.7 Libya -25.2 -29.2 -35.3 -30.9 -16.6 -30.9 -51.0 -105.2 Yemen -17.0 -37.4 -31.8 -24.3 -23.3 -22.8 -24.2 -26.4 Oil Revenue (percent of total revenue) Bahrain 56.8 62.1 59.9 46.8 56.1 73.0 68.6 69.9 Kuwait 68.9 66.6 63.8 58.7 64.0 69.6 68.2 66.4 Oman 73.5 77.3 77.4 65.3 73.7 82.9 80.3 76.7 Qatar 61.9 68.8 64.5 60.0 71.1 78.4 70.9 72.0 Saudi Arabia 72.2 76.1 77.8 56.6 70.8 83.1 80.6 78.0 United Arab Emirates 55.8 56.9 58.4 41.5 43.7 55.7 58.8 63.3 Algeria 59.7 63.0 63.9 55.0 61.9 76.9 68.7 64.6 Egypt ... ... ... ... ... ... ... ... Iran 65.2 61.5 53.6 35.8 42.8 67.5 57.4 58.6 Libya 62.2 69.6 66.5 57.6 50.6 65.2 64.8 82.0

25 P.E.S.T.E.L. ANALYSIS OF THE MENA REGION

Yemen 47.9 69.9 67.4 52.1 57.1 62.3 64.3 75.6 Oil and Gas Exports (percent of total exports) Bahrain 59.7 67.3 62.3 54.0 66.5 73.6 70.9 69.8 Kuwait 93.9 94.6 94.3 88.1 89.8 93.2 92.6 92.4 Oman 78.4 80.2 75.9 67.4 76.4 82.9 80.2 77.2 Qatar 65.0 67.3 68.4 74.9 84.8 86.7 85.5 84.2 Saudi Arabia 81.1 85.2 81.8 74.6 79.8 85.9 81.7 81.7 United Arab Emirates 46.1 49.2 44.6 37.5 45.2 54.6 48.4 45.7 Algeria 87.9 89.3 87.0 86.8 89.8 91.8 88.9 89.2 Egypt 48.3 48.2 33.7 22.5 35.6 37.2 28.7 31.0 Iran 78.4 75.0 67.7 47.3 63.4 84.3 70.7 73.9 Libya ... ... ... ... ... ... ... ... Yemen 89.6 87.3 85.5 81.9 86.5 90.0 87.7 88.3

Source: Country data files.

Figure 2.2

Figure 2.3

26 P.E.S.T.E.L. ANALYSIS OF THE MENA REGION

Figure 2.4

Figure 2.5

27 P.E.S.T.E.L. ANALYSIS OF THE MENA REGION

Sociocultural Figure 3.1

Figure 3.1B

28 P.E.S.T.E.L. ANALYSIS OF THE MENA REGION

Figure 3.1C

29 P.E.S.T.E.L. ANALYSIS OF THE MENA REGION

Figure 3.2

30 P.E.S.T.E.L. ANALYSIS OF THE MENA REGION

Figure 3.3

Figure 3.3B

31 P.E.S.T.E.L. ANALYSIS OF THE MENA REGION

Environmental Figure 4.1

Figure 4.2

32 P.E.S.T.E.L. ANALYSIS OF THE MENA REGION

Figure 4.2B

33 P.E.S.T.E.L. ANALYSIS OF THE MENA REGION

Figure 4.2C

34 P.E.S.T.E.L. ANALYSIS OF THE MENA REGION

Figure 4.3

35 P.E.S.T.E.L. ANALYSIS OF THE MENA REGION

Figure 4.4

36 P.E.S.T.E.L. ANALYSIS OF THE MENA REGION

Figure 4.4B

37 P.E.S.T.E.L. ANALYSIS OF THE MENA REGION

Figure 4.5

Figure 4.5B

38 P.E.S.T.E.L. ANALYSIS OF THE MENA REGION

Figure 4.5C

39 P.E.S.T.E.L. ANALYSIS OF THE MENA REGION

Figure 4.6

40 P.E.S.T.E.L. ANALYSIS OF THE MENA REGION

Figure 4.7

Figure 4.8

41 P.E.S.T.E.L. ANALYSIS OF THE MENA REGION

Figure 4.9

Figure 4.10

42 P.E.S.T.E.L. ANALYSIS OF THE MENA REGION

Figure 4.11

Figure 4.12

43 P.E.S.T.E.L. ANALYSIS OF THE MENA REGION

Technology

Figure 5.1

44 P.E.S.T.E.L. ANALYSIS OF THE MENA REGION

Figure 5.2

45 P.E.S.T.E.L. ANALYSIS OF THE MENA REGION

Bibliography

Al-Ani, B., & Redmiles, D. (2007). EGovernment: Technology for Good Governance,

Development and Democracy in the MENA countries.

Http://www.ics.uci.edu/~redmiles/publications/C076-Al-AR08.pdf. Retrieved December

1, 2014, from http://www.ics.uci.edu/~redmiles/publications/C076-Al-AR08.pdf

Brydan, J., Riahi, L., & Zissler, R. (2013). MENA Renewables Status Report 2013.

Retrieved December 1, 2014, from

http://www.ren21.net/Portals/0/documents/activities/Regional

Reports/MENA_2013_lowres.pdf

Chêne, M. (2007). Overview of Corruption in MENA Countries. Retrieved December 1,

2014, from http://www.u4.no/publications/overview-of-corruption-in-mena-countries/

Comsan, M. (2013). NUCLEAR ENERGY PERSPECTIVES IN MENA COUNTRIES.

Retrieved November 1, 2014, from http://www.afaqscientific.com/icest2013/2-

Comsan25.pdf

Dervis, K. (2014). Education in the Middle East & North Africa: A Strategy Towards

Learning for Development. Retrieved March 1, 1998, from

http://www.worldbank.org/education/strategy/MENA-E.pdf

Karakosta, C., Doukas, H., & Psarras, J. (2009). EU–MENA

energytechnologytransferundertheCDM:Israelasa frontrunner? Energy Policy, 38, 2455–

2462-2455–2462. Retrieved December 1, 2014, from

ideas.repec.org/a/eee/enepol/v38y2010i5p2455-2462.html

Khlopkov, A. (2012). Prospects for nuclear power in the Middle Eastern after Fukushima

and the Arab Spring. Retrieved November 1, 2014, from http://www.isn.ethz.ch/Digital-

Library/Publications/Detail/?lng=en&id=156051

Lee, R., & Shitrit, L. (2014). Religion, Society, and Politics in the Middle East. Retrieved

December 1, 2014, from http://www.cqpress.com/docs/college/Lust_Middle East 13e.pdf

Moisavian,S. (2012). The Iran Nuclear Dilemma: The Peaceful Use of Nuclear Energy

and NPT’s Main Objectives. Retrieved December 1, 2014, from

http://www.nonproliferation.eu/documents/backgroundpapers/mousavian.pdf

46 P.E.S.T.E.L. ANALYSIS OF THE MENA REGION

Müller, S., Marmion, A., & Beerepoot, M. (2011). RENEWABLE ENERGY MARKETS

AND PROSPECTS BY REGION. Deploying Renewables 2011: Best and Future Policy

Practice. Retrieved December 1, 2014, from

http://www.iea.org/publications/freepublications/publication/renewable-energy-markets-

and-prospects-by-regions.html

O'Sullivan, A., Rey, M., & Mendez, J. (2011). Opportunities and Challenges in the

MENA Region. Retrieved November 1, 2014, from

http://www.oecd.org/mena/49036903.pdf

Rahmetov, A. (2012). Authoritarian collapse: Concepts, causes and knowledge

accumulation. Retrieved December 1, 2014, from

http://www.sisp.it/files/papers/2012/anvar-rahmetov-1448.pdf

Reichborn-Kjennerud, E. (2014). NATO's Problematic Partnerships in the MENA

Region.Mediterranean Quarterly, 25(2). Retrieved December 1, 2014, from

http://mq.dukejournals.org/content/25/2/6.abstract?related-urls=yes&legid=ddmq;25/2/6

Saidi, N., & Yared, H. (2002). EGovernment: Technology for Good Governance,

Development and Democracy in the MENA countries. Retrieved November 1, 2014,

from http://www.mafhoum.com/press4/114E13.pdf

Shehadi, R. (2009). Customer-Centric E-Government Modernizing the MENA Region’s

Public Sector. Retrieved November 1, 2014, from

http://www.strategyand.pwc.com/global/home/what-we-think/reports-white-

papers/article-display/customer-centric-government-modernizing-mena

Tessler, M., & Nachtwey, J. (1998). Islam and attitudes toward international conflict:

Evidence from survey research in the arab world. The Journal of Conflict Resolution,

42(5), 619-636. Retrieved Dec 1, 2014 from

http://ezproxy.fau.edu/login?url=http://search.proquest.com/docview/224562066?account

id=10902 York

Air Quality and Atmospheric Pollution In the Arab Region. (2003). Retrieved December

1, 2014, from http://www.un.org/esa/sustdev/csd/csd14/escwaRIM_bp1.pdf

Country Reports on Terrorism 2013. (2014, April 1). Retrieved December 1, 2014, from

http://www.state.gov/j/ct/rls/crt/2013/

47 P.E.S.T.E.L. ANALYSIS OF THE MENA REGION

(2010, January). Middle East and North Africa. Retrieved December 1, 2014, from

https://www.unodc.org/unodc/en/drug-trafficking/middle-east-and-north-africa.html

Regional Report on The Business Legal environment in the MENA Region: Status and

Reform Challenges (Lebanon, Tunisia, Yeman and the UAE). (2009). Arab Center for the

Development of the Rule of Law and Integrity-ACRLI, 3-39. Retrieved December 1,

2014, from http://www.arabruleoflaw.org/compendium/Files/MENA-CLS-

RegionalReport-En.pdf

Renewable Energy Essentials: Hydropower. (2010, January 1). Retrieved December 1,

2014, from

http://www.iea.org/publications/freepublications/publication/hydropower_essentials.pdf

THE FUTURE FOR RENEWABLE ENERGY IN THE MENA REGION. (2013). Clean

Energy Pipeline. Retrieved December 1, 2014, from http://www.squiresanders.com/the-

future-for-renewable-energy-in-the-mena-region/

UNICEF, (October 2011) Regional Overview For The Middle East And North Africa:

MENA Gender Equality Profile Status of Girls and Women in the Middle East and North

Africa. Retrieved December 1, 2014, from:

http://www.unicef.org/gender/files/REGIONAL-Gender-Eqaulity-Profile-2011.pdf

UNODC, World Drug Report (2010) United Nations Publication, Sales No. E.10.XI.13

http://www.unodc.org/documents/wdr/WDR_2010/World_Drug_Report_2010_lo-res.pdf

Water Use and Rights (Middle East and North Africa). (2012). THE BERKSHIRE

ENCYCLOPEDIA OF SUSTAINABILITY: AFRO-EURASIA: ASSESSING

SUSTAINABILITY. Retrieved December 1, 2014, from

http://www.academia.edu/3487069/Water_Use_and_Rights_Middle_East_and_North_Af

rica_

Related Documents