Pergamon 0956-5221(95)00025-9 Scand. J. Mgmt, Vol. 11, No. 3, pp. 283-293, 1995 Copyright © 1995 Elsevier Science Ltd Printed in Great Britain. All rights reserved 0956-5221/95 $9.50 + 0.00 MANAGERIAL FOCUS IN CHANGING ENVIRONMENTS KJELL GRI~NHAUG and RUNE LINES* The Norwegian School of Economics and Business Administration, Norway (First received July 1992; accepted in revised form September 1994) Abstract -- This paper explores the way top managers attend to their ever-changing environments. A longitudinal study including top managers from two organizations, a large national bank and an industrial finn operating worldwide, was conducted. Analysis of the top-managers environmental attributions revealed several interesting findings. The managers in the two organizations differed in their environmental foci. Dramatic changes in environmental focus were observed when the top managers in the two firms were replaced. The findings indicate that top managers' environmental foci are selective, and tend to be rather rigid. Implications are highlighted. INTRODUCTION The purpose of the present paper is to explore the way in which top managers attend to their environments. In particular we examine the impact of environmental changes on the managers' environmental focus. The importance of this type of study can be motivated as follows. Managers are in charge of organizations embedded in ever-changing environments. The open system metaphor underlying this perspective implies that organizations depend on their environments, and may -- under specific circumstances also influence these environments themselves (cf. Thompson, 1967). To survive and prosper, organizations must be effective, i.e. they must be able to create acceptable outcomes for their constituencies in such a way as to retain sufficient resources (Pfeffer and Salancik, 1978, p. 11). For example, if business firms -- an important subset of organizations (Dill, 1965) -- are unable to attract and satisfy their customers with product offerings at prices which at least cover costs, they will be forced to exit the market. In order to succeed, organizational activities must be relevant and continuously adjusted to changing organizational environments. Leading textbooks in disciplines such as management, organization theory, marketing and corporate strategy also emphasize the crucial importance of exploiting "opportunities" foreseeing "threats" and taking precautions (cf. Porter, 1980). To do so, relevant information about the organizational environments is needed. But managers are not omniscient. Probably the most prevalent assumption in contemporary social science is that of lim- ited cognitive capacity, i.e. man has limited capacity to notice, seek, store, handle and make sense of data (Simon, 1957). Management can at best only react to stimuli which have been noticed and interpreted. How top managers allocate their limited attention capacity is of crucial importance, *The authors gratefully acknowledge the very constructive comments of the Editor, Professor Sten Jtnsson and three anonymous reviewers on earlier versions of the paper. Nancy Adler's improvement of the language is also appreciated. 283

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Pergamon

0956-5221(95)00025-9

Scand. J. Mgmt, Vol. 11, No. 3, pp. 283-293, 1995 Copyright © 1995 Elsevier Science Ltd

Printed in Great Britain. All rights reserved 0956-5221/95 $9.50 + 0.00

MANAGERIAL FOCUS IN CHANGING ENVIRONMENTS

K JELL GRI~NHAUG and RUNE LINES*

The Norwegian School of Economics and Business Administration, Norway

(First received July 1992; accepted in revised form September 1994)

Abstract - - This paper explores the way top managers attend to their ever-changing environments. A longitudinal study including top managers from two organizations, a large national bank and an industrial finn operating worldwide, was conducted. Analysis of the top-managers environmental attributions revealed several interesting findings. The managers in the two organizations differed in their environmental foci. Dramatic changes in environmental focus were observed when the top managers in the two firms were replaced. The findings indicate that top managers' environmental foci are selective, and tend to be rather rigid. Implications are highlighted.

INTRODUCTION

The purpose of the present paper is to explore the way in which top managers attend to their environments. In particular we examine the impact of environmental changes on the managers' environmental focus. The importance of this type of study can be motivated as follows. Managers are in charge of organizations embedded in ever-changing environments. The open system metaphor underlying this perspective implies that organizations depend on their environments, and may - - under specific circumstances also influence these environments themselves (cf. Thompson, 1967). To survive and prosper, organizations must be effective, i.e. they must be able to create acceptable outcomes for their constituencies in such a way as to retain sufficient resources (Pfeffer and Salancik, 1978, p. 11). For example, if business firms - - an important subset of organizations (Dill, 1965) - - are unable to attract and satisfy their customers with product offerings at prices which at least cover costs, they will be forced to exit the market.

In order to succeed, organizational activities must be relevant and continuously adjusted to changing organizational environments. Leading textbooks in disciplines such as management, organization theory, marketing and corporate strategy also emphasize the crucial importance of exploiting "opportunities" foreseeing "threats" and taking precautions (cf. Porter, 1980). To do so, relevant information about the organizational environments is needed. But managers are not omniscient. Probably the most prevalent assumption in contemporary social science is that of lim- ited cognitive capacity, i.e. man has limited capacity to notice, seek, store, handle and make sense of data (Simon, 1957). Management can at best only react to stimuli which have been noticed and interpreted. How top managers allocate their limited attention capacity is of crucial importance,

*The authors gratefully acknowledge the very constructive comments of the Editor, Professor Sten Jtnsson and three anonymous reviewers on earlier versions of the paper. Nancy Adler's improvement of the language is also appreciated.

283

284 K. GRONHAUG and R. LINES

since their attention will determine the signals that are detected and how those that are noticed are then interpreted, all of which then affects subsequent actions and performance outcomes (cf. Huff, 1990; Thomas et al., 1993).

Studies of managerial work have also demonstrated great pressure on management's attention capacity. The tasks are multiple, forcing management to "select" what to attend (cf. Mintzberg, 1973). As G.A. Yukle put it: "There are always more problems than a manager can handle at any given time" (Yukle, 1989, p. 55).

The nature of managerial work thus serves to emphasize the importance of the research ques- tion addressed here, namely: "how do managers attend to their environment?" From this very general question several other more specific questions can be derived, such as: "does attention focus on some environmental aspects (or sectors) more than on others?" "What factors influence the noticing of environmental signals and the attention paid to them?" These questions are in no way meant as an exhaustive list, but are simply examples of the kind of questions arising from the general issue raised at the beginning of this paper. The paper proceeds as follows. First, we discuss the concepts of environment and environmental focus. On the basis of this discussion some tentative questions are then raised and used as pointers in our empirical investigation. The methodology underlying this contribution to research is reported, after which the empirical find- ings are presented and discussed.

ENVIRONMENT AND MANAGEMENT FOCUS

The concept of the "environment", however, frequently it may be employed, is in no way unproblematic. We will not add here to the discussion about what constitutes the organizational environment (see Aldrich and Marsden, 1988, for a recent review of earlier research). For our present purpose it is sufficient to explain the environment as "what is outside the actor". In con- sidering the organization as the focal unit, the environment may thus be conceived as what is "outside" this unit. If management-- as here - - is regarded as the focal unit, then even elements inside the organization can be conceived as part of management' s environment, often termed "the internal organizational environment". Earlier research has shown that managers often pay great attention to their internal organizational environment (of. Mintzberg, 1973; Peters and Waterman, 1982).

Classification of environments In the vast literature on management, organization theory, marketing and corporate strategy,

organizational environments have been classified in several ways. A common distinction has been between the internal and the external environment.

This is the distinction that will be used here. Various classifications of the external environ- ment have been proposed, e.g. the distinction between micro- and macroenvironments. To cap- ture external factors directly influencing the organizations the term "task environment" is often used (cf. Thompson, 1967). Many attempts have been made to define the environments as con- sisting of a set of mutually exclusive segments. Such segments are usually indicated by specific organizations or institutions (e.g. regulatory agents) and populations of individuals or organiza- tions (e.g. suppliers, customers and competitors, see e.g. Dill, 1958; Porter, 1980). The number of categories or segments included varies in different classifications, as do the classification cri- teria used. Here we will adopt this kind of segment or category approach, and will distinguish between:

CHANGING ENVIRONMENTS 285

- regulatory agents - customers/buyers - competitors (and their actions) - suppliers, and - industry factors and forces.

This classification, albeit not necessarily more "right" than any other builds on classifications and research findings in disciplines such as management, organization theory, marketing, and corporate strategy. Moreover, the designation of the segment come close to the everyday lan- guage of managers. For example, managers talk about and use such concepts as "supplier", "mar- ket" and "competitors". For our present research purpose a classification closely related to the vocabulary used by managers is an advantage.*

Environmental focus and understanding Firms, like other organizations, are context-bound. Business firms operate and compete within

industries (Porter, 1980, 1990). To exhibit purposeful behavior-- as managers and organizations are both supposed to do, in order to become effective - - they must understand their surrounding context. According to attribution theories, managers like other human beings, are inclined to seek (causal) understanding in order to exhibit purposeful behavior. Central to the concept of "attri- bution" is the inferred relationship between "cause" and "consequence". It is assumed that by making such inferences people achieve greater understanding of, and hence greater control over, their environments (Harvey and Weary, 1984, p. 428). Sanford (1987) also claims that " . . . expla- nations [i.e. attributions] revolve around chains of connected events, either real or imaginary, and occur either in response to a demand for an explanation or because something is not understood" (p. 99).

Managers behaving in a purposeful way will thus attend to those parts of their environments that they perceive to be relevant, i.e. they influence the performance of their organizations. What they observe and the inferences they make will influence their attributions, and their under- standing. Because the environments they are embedded in may vary from one firm to another, it seems reasonable to assume that managements in different firms may also differ in their envi- ronmental focus. Earlier research has shown that managers do not distribute their limited atten- tion capacity "objectively", rather they are influenced by factors such as experiences, the struc- ture of their organizations and the activities they are involved in (see Pfeffer and Salancik, 1978).

A management's environmental focus may change as their environments change, so that they can make adequate adjustments. However, attribution research has demonstrated that positive outcomes tend to be attributed to internal, controllable causes, while negative outcomes are more likely to be attributed to external, uncontrollable causes (for an overview of research findings, see Harvey and Weary, 1984; Fiske and Taylor, 1991). Some researchers have claimed that such attribution patterns are "self-serving" or "hedonistic" (cf. Miller and Ross, 1975). This explana- tion has been questioned, however. Chapham and Schwenk (1991), for example, suggest that the tendency to attribute negative outcomes to external, uncontrollable causes can be explained by attempts "to develop new and better understanding of the variables affecting company perfor-

*An interesting observation is that most of the classification schemes used are imposed by researchers. It may well be that the classification schemes used by managers may differ from those imposed, and that managers may differ among themselves in their classifications of the environment.

286 K. GRONHAUG and R. LINES

mance. . . " (p. 220). It can equally well be argued that a management's environmental focus may not change, for the following two reasons. First, if the environmental changes are incremental, they are difficult to detect, while if they are sudden and dramatic they are more likely to be noticed (Kiesler and Sproull, 1982). Lewitt (1960) in his classical article "Marketing Myopia" in the Harvard Business Review shows, for example, that whole industries faded away because man- agement did not discover the eroding changes that occurred. Second, established beliefs, and thus the managers' environmental focus and their reality constructions (cf. Berger and Luckman, 1966) tend to be rather stable. Sherman et al. (1989) also claim that "New information is typi- cally assimilated into existing (cognitive) structures..." (p. 311), which suggests a certain rigid- ity in management is environmental focus. Thus, two interesting questions that have not been fully addressed in prior research are: does management's environmental focus change when the environment changes, and does the manager' s environmental focus vary with the performance of their organizations? A further question which has not previously been examined, is: do present managers differ from their predecessors in their environmental focus? Intuitively this seems likely. New managers are often recruited into organizations which are deterioriating or which are not performing well, in order to bring about a hoped for positive change which not only allows for but even requires a new and different management.

We have raised four questions about (1) variations in environmental focus across industries, (2) whether management focus changes when environments change, (3) whether the focus varies with the organizational performance, and (4) whether present managers and their predecessors differ in their environmental focus. These exploratory questions will serve as guidelines in our investigation.

RESEARCH METHODOLOGY

The following is a description of the research methodology underlying this study. To explore the questions raised above, the following research requirements should be met:

- the study should capture the environmental focus of managers, - it should be longitudinal and include both environmental changes and changes in organiza-

tional performance, - it should cover more than one industry, and - it should also capture change at top management level.

Data The way managers attend to environmental data, and how they notice and interpret it, are all

connected with their cognitive processes. A variety of methods are used to study such processes (see Huff, 1990, for a recent overview). Any method has its strengths and limitations. Here we sought to capture managerial attention - - paying through the managers' own verbalized expres- sion of it. More precisely, we analyzed the content of secondary data. This was chosen primarily to cover a sufficiently long period so that changes in the environment and in organizational per- formance could be identified.

In the present study we sought to capture managers' attributions as a way of explaining orga- nizational performance as the expression of their environmental focus. Such attributions tell us not only that the various sectors have been attended to, but also that they have been noticed and interpreted. Thus, whatever has been attended to, but not noticed and/or interpreted is left out.

CHANGING ENVIRONMENTS 287

Since we have captured many attributions (see below), we believe that these can reveal a fairly relevant picture of the attention-paying of the managers involved.

The data analyzed consisted of interviews with top managers taken from the two most impor- tant newspapers which report business news, and interviews with managers as reported in annual reports and newsletters in their organizations. An important question is whether such data really reflects management's attention-paying. There is no doubt that the statements do reflect think- ing, and probably also prior observations. But people other than the top managers interviewed may have influenced the reported statements. Top managers are generally assumed to guide and to be alert. The top managers included in this study were recognized during the period covered as being strong and dominant, leading us to believe that it is at least partially their own focus and attributions that have been caught. This conviction is supported by the fact that multiple inter- views covering a substantial period have been used, even though it has to be admitted that such data are "noisy" (cf. Holsti, 1969; Weber, 1985; Huff, 1990). It should also be noted that such data have been extensively used in earlier studies of various aspects of managerial cognition (see e.g. Bettman and Weitz, 1993; Bowman, 1984). Chapman and Schwenk (1991) even claim that such statements " . . . provide some of the best data on the cognitive aspects of strategic manage- ment" (p. 219).

In our study we first identified the relevant data sources (newspapers, annual reports, etc.), from which we then selected the articles containing interviews with the managers included in the study. Finally, statements implying attributions were extracted from the articles. The abstracted attributions represent our unit of analysis. In addition we used data from stock exchange prices and profit data taken from annual reports and internal newsletters, to assess changes in environ- ments and performance.

Setting The present study covers a period of approximately four years, capturing the attributions of

top managers in two large Norwegian firms - - a commercial bank, and an industrial firm pro- ducing aluminum and ferro-alloy products. The studied bank operates primarily on the domestic market. The banking industry changed dramatically during the period studied. At the beginning of the period the banking industry was strictly regulated, but it was later deregulated and suffered a severe crisis (for an overview of these developments, see Reve, 1990). The industrial firm oper- ates worldwide. Most of its products are sold outside Norway. Even though the firm is large when measured in terms of number of employees and turnover, its market share on the world market is modest. It operates in markets characterized as "very competitive", and is unable to influence market prices. In both organizations the top manager was replaced during the period covered by the study.

Coding and measurements A coding scheme was constructed. After thorough pre-testing the scheme was used to classify

the attributions (Appendix A gives examples of codings). A total of 1,322 attributions were coded by one person and were included in the study. To assess the reliability of the coding, a random subset of 10 per cent of the total number of attributions was coded by a second person, who was instructed in the coding rules. The degree of agreement measured by the product moment corre- lation coefficient, was found to be r = .91 (p < 0.001).

Management focus has been assessed here by the relative frequency of attributions related to the various environmental segments, a method which accords with prior research practices, for example in Aguilar's study of environmental scanning (Aguilar, 1967). The attributions in the

288 K. GR~NI-IAUG and R. LINES

present study refer primarily to four people, namely the present and former top managers in the two companies. The number of attributions per subject exceeds by far the number of attributions per person in previous studies. In the often quoted study by Bettman and Weitz (1983), only five attributions per subject were used. This data intensity, i.e. the high number of attributions per sub- ject, makes us confident that we have captured management's environmental focus more ade- quately than most earlier studies have done.

FINDINGS

In this section we report the empirical findings as follows. We first report performance and environmental changes and then findings that allow us to explore the guiding questions raised above.

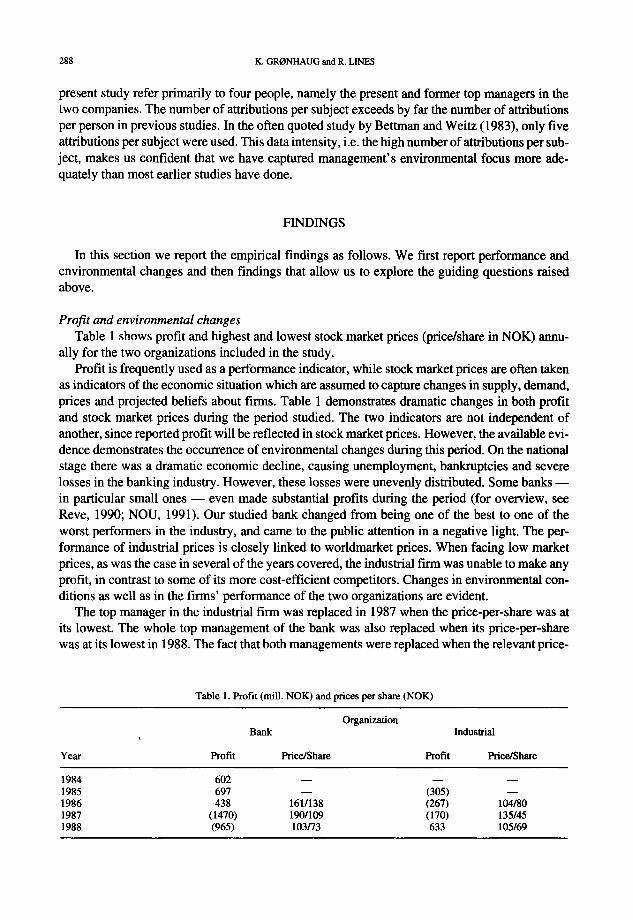

Profit and environmental changes Table 1 shows profit and highest and lowest stock market prices (price/share in NOK) annu-

ally for the two organizations included in the study. Profit is frequently used as a performance indicator, while stock market prices are often taken

as indicators of the economic situation which are assumed to capture changes in supply, demand, prices and projected beliefs about firms. Table 1 demonstrates dramatic changes in both profit and stock market prices during the period studied. The two indicators are not independent of another, since reported profit will be reflected in stock market prices. However, the available evi- dence demonstrates the occurrence of environmental changes during this period. On the national stage there was a dramatic economic decline, causing unemployment, bankruptcies and severe losses in the banking industry. However, these losses were unevenly distributed. Some banks in particular small ones - - even made substantial profits during the period (for overview, see Reve, 1990; NOU, 1991). Our studied bank changed from being one of the best to one of the worst performers in the industry, and came to the public attention in a negative light. The per- formance of industrial prices is closely linked to woddmarket prices. When facing low market prices, as was the case in several of the years covered, the industrial firm was unable to make any profit, in contrast to some of its more cost-efficient competitors. Changes in environmental con- ditions as well as in the firms' performance of the two organizations are evident.

The top manager in the industrial finn was replaced in 1987 when the price-per-share was at its lowest. The whole top management of the bank was also replaced when its price-per-share was at its lowest in 1988. The fact that both managements were replaced when the relevant price-

Table 1. Profit (mill. NOK) and prices per share (NOK)

Organization Bank Industrial

Year Prof i t Price/Share Profit Price/Share

1984 602 -- -- - - 1985 697 -- (305) - - 1986 438 1611138 (267) 104/80 1987 (1470) 190/109 (170) 135145 1988 (965) 103/73 633 105/69

CHANGING ENVIRONMENTS 289

per-share was the lowest, and that both firms sustained severe losses, indicates that organizational performance tends to be attributed to management by the shareholders and other influential con- stituencies (cf. March, 1984).

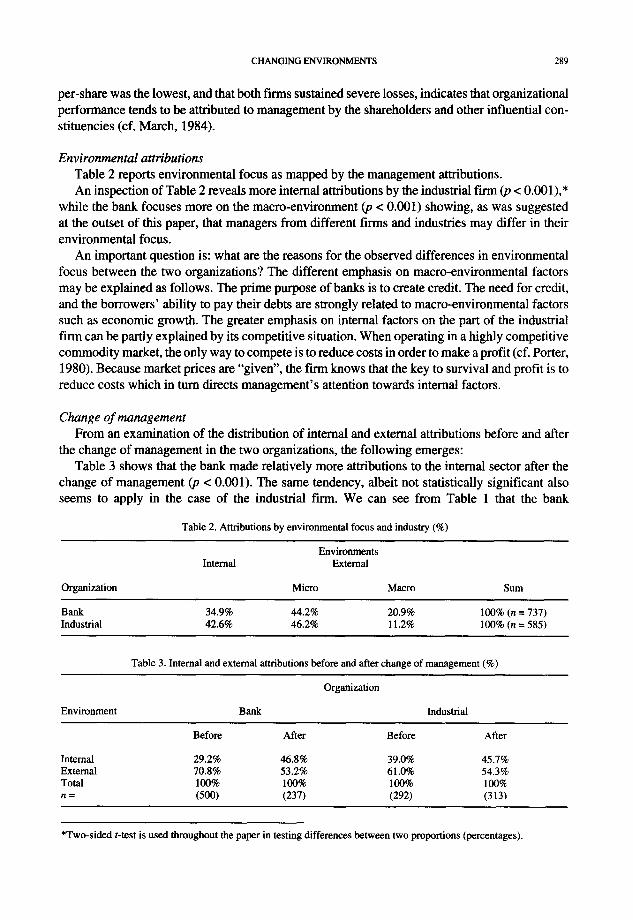

Environmental attributions Table 2 reports environmental focus as mapped by the management attributions. An inspection of Table 2 reveals more internal attributions by the industrial firm (p < 0.001),*

while the bank focuses more on the macro-environment (p < 0.001) showing, as was suggested at the outset of this paper, that managers from different firms and industries may differ in their environmental focus.

An important question is: what are the reasons for the observed differences in environmental focus between the two organizations? The different emphasis on macro-environmental factors may be explained as follows. The prime purpose of banks is to create credit. The need for credit, and the borrowers' ability to pay their debts are strongly related to macro-environmental factors such as economic growth. The greater emphasis on internal factors on the part of the industrial firm can be partly explained by its competitive situation. When operating in a highly competitive commodity market, the only way to compete is to reduce costs in order to make a profit (cf. Porter, 1980). Because market prices are "given", the firm knows that the key to survival and profit is to reduce costs which in turn directs management 's attention towards internal factors.

Change of management From an examination of the distribution of internal and external attributions before and after

the change of management in the two organizations, the following emerges: Table 3 shows that the bank made relatively more attributions to the internal sector after the

change of management (p < 0.001). The same tendency, albeit not statistically significant also seems to apply in the case of the industrial firm. We can see from Table 1 that the bank

Table 2. Attributions by environmental focus and industry (%)

Environments Internal External

Organization Micro Macro Sum

Bank 34.9% 44.2% 20.9% 100% (n = 737) Industrial 42.6% 46.2% 11.2% 100% (n = 585)

Table 3. Internal and external attributions before and after change of management (%)

Organization

Environment Bank Industrial

Before After Before After

Internal 29.2% 46.8% 39.0% 45.7% External 70.8% 53.2% 61.0% 54.3% Total 100% 100% 100% 100% n = (500) (237) (292) (313)

*Two-sided t-test is used throughout the paper in testing differences between two proportions (percentages).

290 K. GRONHAUG and R. LINES

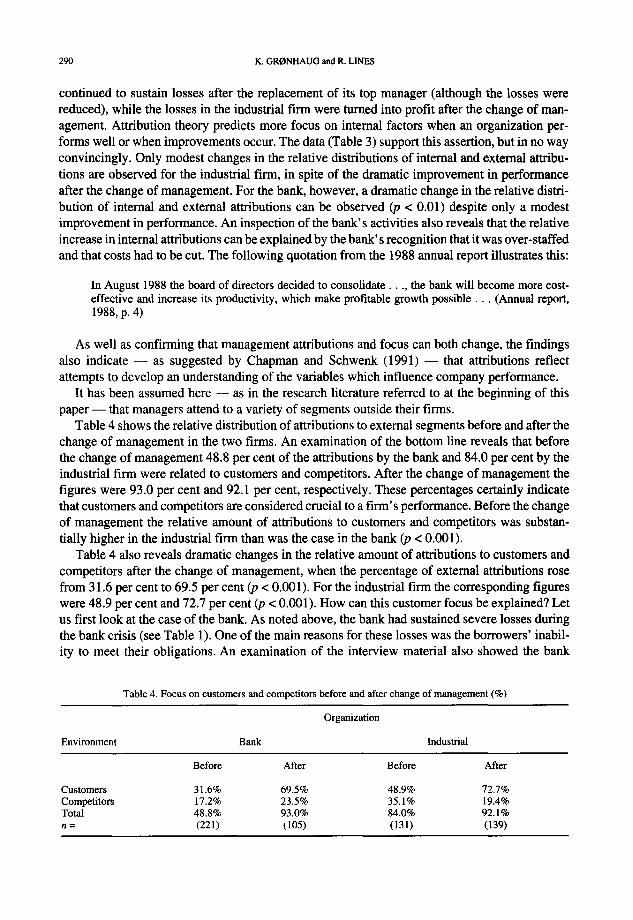

continued to sustain losses after the replacement of its top manager (although the losses were reduced), while the losses in the industrial firm were turned into profit after the change of man- agement. Attribution theory predicts more focus on internal factors when an organization per- forms well or when improvements occur. The data (Table 3) support this assertion, but in no way convincingly. Only modest changes in the relative distributions of internal and external attribu- tions are observed for the industrial firm, in spite of the dramatic improvement in performance after the change of management. For the bank, however, a dramatic change in the relative distri- bution of internal and external attributions can be observed (p < 0.01) despite only a modest improvement in performance. An inspection of the bank's activities also reveals that the relative increase in internal attributions can be explained by the bank' s recognition that it was over-staffed and that costs had to be cut. The following quotation from the 1988 annual report illustrates this:

In August 1988 the board of directors decided to consolidate . . . . the bank will become more cost- effective and increase its productivity, which make profitable growth possible.. . (Annual report, 1988, p. 4)

As well as confirming that management attributions and focus can both change, the findings also indicate - - as suggested by Chapman and Schwenk (1991) - - that attributions reflect attempts to develop an understanding of the variables which influence company performance.

It has been assumed here - - as in the research literature referred to at the beginning of this paper - - that managers attend to a variety of segments outside their firms.

Table 4 shows the relative distribution of attributions to external segments before and after the change of management in the two firms. An examination of the bottom line reveals that before the change of management 48.8 per cent of the attributions by the bank and 84.0 per cent by the industrial firm were related to customers and competitors. After the change of management the figures were 93.0 per cent and 92.1 per cent, respectively. These percentages certainly indicate that customers and competitors are considered crucial to a firm's performance. Before the change of management the relative amount of attributions to customers and competitors was substan- tially higher in the industrial firm than was the case in the bank (p < 0.001).

Table 4 also reveals dramatic changes in the relative amount of attributions to customers and competitors after the change of management, when the percentage of external attributions rose from 31.6 per cent to 69.5 per cent (p < 0.001). For the industrial firm the corresponding figures were 48.9 per cent and 72.7 per cent (p < 0.001). How can this customer focus be explained? Let us first look at the case of the bank. As noted above, the bank had sustained severe losses during the bank crisis (see Table 1). One of the main reasons for these losses was the borrowers' inabil- ity to meet their obligations. An examination of the interview material also showed the bank

Table 4. Focus on customers and competitors before and after change of management (%)

Organization

Environment Bank Industrial

Before After Before After

Customers 31.6% 69.5% 48.9% 72.7% Competitors 17.2% 23.5% 35.1% 19.4% Total 48.8% 93.0% 84.0% 92.1% n = (221) (105) (131) (139)

CHANGING ENVIRONMENTS 291

openly admitting that it must improve its routines for credit evaluation, and watch the borrowers more closely to allow for precautionary actions if it was to reduce its losses. For example, it was claimed: "when customers are in trouble (i.e. have difficulty in meeting their obligations) we must go in and help (e.g. to assist customer in making a budget).*

But how can we explain the more customer-oriented focus in the industrial firm after the change of management? An analysis of the material did not immediately assist us here. The fol- lowing seems, however, to shed some light on the matter. The new manager had a degree in busi- ness administration and had also had substantial experience in marketing - - an area in which cus- tomers are believed to be the key source of profit (cf. the content of "market orientation", Kohli and Jaworski, 1990). It could also be observed that the firm focused more consciously on build- ing up customer relationships, e.g. by adding new services, the firm attempted to generate more customers.

These findings indicate that managers attend to what they believe is important to their firm's performance. Their belief may be based on their own or other people's attributions, and are thus "attributional", i.e. they build on prior attributional inferences (cf. Kelley and Michela, 1980). Our discussion in connection with Table 4 also shows as we hypothesized at the outset, that cur- rent managers and their predecessors may differ in their environmental focus.

DISCUSSION

The findings reported above call for some further comment. Our observations, guided by a set of tentative questions, show that managers can differ in their environmental focus, and that their focus may change when organizational performance and environments change. In addition, our findings indicate that managers holding the same top position within the same company may also differ in their environmental focus. This is an example of the way a change of management may introduce a new perspective, which can lead to changes in the organizational activities as well.

Competitors and customers represented the segments in the external environments which were attended most. Similar findings have been reported in previous research (e.g. Aguilar, 1967; Daft et al., 1988). Other environmental sectors such as regulators and their activities were also attended to. The present study shows that managers allocate an important part of their limited attention capacity to the internal organization - - a finding that accords with earlier observations of managerial behavior (cf. Mintzberg, 1973; Peters and Waterman, 1982), but which has been largely disregarded in studies of managerial attention and scanning activities (cf. Aguilar, 1967; Daft et al., 1988). There is an indication here that preconceptions and methodological biases may obscure research findings.

Earlier research has shown that managers' environmental beliefs and foci tend to be rather rigid (cf. Sherman et al., 1989). The dramatic changes in environmental focus observed here in connection with a change of management (cf. Tables 3 and 4) also suggest that this kind of rigid- ity may have been present in the individual manager's environmental focus. If managers' men- tal models tend to remain fairly stable, this can represent a serious threat to organizations since

*This was confirmed in a detailed study of the way the bank's focus and behavior changed during the bank crisis. Instead of selling simply credit, the banks evaluated their customers more carefully before giving credit, as well as watching bor- rowers more closely (Gronhaug and Kleppe, 1991).

292 K. GRONHAUG and R. LINES

these menta l mode ls wil l inf luence attention, and de termine what envi ronmenta l data is not iced

and interpreted, all o f which together const i tute a ma jo r factor in guiding and direct ing organi-

zat ional activities.

R E F E R E N C E S

Aguilar, F. J., Scanning the Business Environments (London: The Macmillan Company, 1976). Aldrich, H. E. and Marsden, P. V., Environments and organizations. In: N. Smelser (Ed.), Handbook of Sociology (New

York: Rand McNally, 1988). Berger, P. L. and Luckman, T., The Social Construction of Reality (Garden City, NY: Doubleday, 1966). Bettman, J. R. and Weitz, B. A., Attribution in the board room: causal reasoning in corporate annual reports,

Administrative Science Quarterly (1983), Vol. 28, No. 2, pp. 165-183. Bowman, E. H., Content analysis of annual reports for corporate strategy and risk, Interfaces (1984), 14(1), 61-71. Chapham, S. E. and Schwenk, C. R., Self-servicing attributions, managerial cognition, and company performance,

Strategic Management Journal (1991), Vol. 12, No. 3, pp. 219-229. Dill, W. R., Environments as an influence on managerial autonomy, Administrative Science Quarterly (1958), Vol. 2, pp.

409--443. Daft, R. L., Sormunen, J. and Parks, D., Chief executive scanning, environmental characteristics, and company perfor-

mance. An empirical study, Strategic Management Journal (1988), Vol. 9, pp. 123-139. Fiske, S. T. and Taylor, S. E., Social Cognition (New York: McGraw Hill, 2nd ed., 1991). GrCnhaug, K. and K16ppe, A. I., Micro and Macro Changes in Bank-Client Relationships Due to Unforeseen Events

(Stockholm: IAREP/SASE, paper, 1990). Harvey, J. H. and Weary, G., Current issues in attribution theory and research, Annual Review of Psychology (1984), Vol.

35, pp. 427-459. Holsti, O. R., Content Analysis for the Social Sciences and Humanities (Addison-Wesley, 1969). Huff, A. S. (Ed.), Mapping Strategic Thought (New York: John Wiley and Sons, 1990). Kelly, H. H. and Miehela, J. L., Attribution theory and research, Annual Review of Psychology (1980), Vol. 31, pp.

457-501. Kiesler, S. and Sproull, L., Managerial response to changing environments: perspective on problem sensing from social

cognition, Administrative Science Quarterly (1982), 27, pp. 548-570. Kohli, A. K. and Jarworski, B. J., Market orientation: the construct, research propositions, and managerial implications,

Journal of Marketing (1990), Vol. 54, pp. 1-18. Levitt, T., Marketing myopia, Harvard Business Review (1960), July-August, pp. 27-47. March, J. G., Notes on ambiguity and executive compensation, Journal of Management Studies (1984), Vol. 1, August,

pp. 53--64. Miller, D. T. and Ross, M., Self-serving biases in attribution of causality: fact or fiction?", Psychological Bulletin (1975),

Vol. 25, pp. 129-141. Mintzberg, H., The Nature of Managerial Work (New York: Harper & Row, 1973). NOU, Penger og kreditt i en ommstillingstid, NOU (1991), p. 1. Peters, T. J. and Waterman, R. H., In Search of Excellence (New York: Harper & Row, 1982). Pfeffer, J. and Salancik, G. R., The External Control of Organizations (New York: Harper and Row, 1978). Porter, M. E., Competitive Strategy (New York: The Free Press, 1980). Porter, M. E., The Competitiveness of Nations (New York: The Free Press, 1990). Reve, T., Bankkrisen. Hva gikk gait? (Center for Applied Research, Bergen, Report No. 3/90, 1990). Sanford, A. J., The Mind of Man. Models of Human Understanding (Brighton, U.K.: Harvester, 1987). Sherman, S. J., Social cognition, Annual Review of Psychology (1987), Vol. 40, pp. 281-326. Simon, H. A., Administrative Behavior (New York: The Free Press, 2nd ed., 1957). Thomas, J. B., Clark, S. M. and Gioa, D. A., Strategic sensemaking and organizational performance: linkages among

scanning, interpretation, action and outcomes, Academy of Management Journal (1993), Vol. 36, No. 2, pp. 239-270. Thompson, J. D., Organizations in Actions (New York: McGraw Hill, 1967). Weber, R. P., Basic Content Analysis (Beverly Hills, CA: Sage, 1985). Yukle, G. A., Leadership in Organizations (Englewood Cliffs, NJ: Prentice-Hall, 1989).

CHANGING ENVIRONMENTS 293

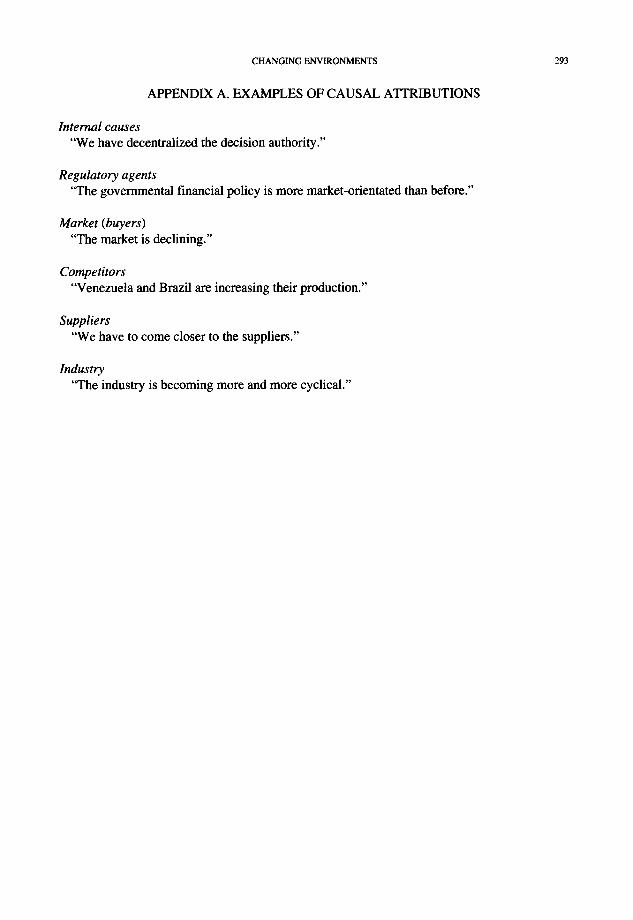

APPENDIX A. EXAMPLES OF CAUSAL ATTRIBUTIONS

Internal causes "We have decentralized the decision authority."

Regulatory agents "The governmental financial policy is more market-orientated than before."

Market (buyers) "The market is declining."

Competitors "Venezuela and Brazil are increasing their production."

Suppliers "We have to come closer to the suppliers."

Industry '"I'he industry is becoming more and more cyclical."

Related Documents