1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 Lead Plaintiff’s Mem. Of Pts. And Auth. In Opp. To Defendant Bear, Stearns & Co.’s Motion To Dismiss Lead Plaintiff’s Third Amended And Consol. Class Action Complaint, Master File No. C-99-20743-RMW BERNSTEIN LITOWITZ BARRACK, RODOS & BACINE BERGER & GROSSMANN LLP Leonard Barrack Max W. Berger Gerald J. Rodos Daniel L. Berger M. Richard Komins Rochelle Feder Hansen Robert A. Hoffman J. Erik Sandstedt 3300 Two Commerce Square Beata Gocyk-Farber 2001 Market Street 1285 Avenue of the Americas Philadelphia, PA 19103 New York, NY 10019 Telephone: (215) 963-0600 Telephone: (212) 554-1400 - and - - and - 12730 High Bluff Drive, Suite 100 Stephen R. Basser (Cal. No. 121590) San Diego, CA 92130 402 West Broadway, Suite 850 Telephone: (858) 793-0070 San Diego, CA 92101 Telephone: (619) 230-0800 Attorneys for Lead Plaintiff The New York State Common Retirement Fund and Co-Lead Counsel for the Class UNITED STATES DISTRICT COURT NORTHERN DISTRICT OF CALIFORNIA SAN JOSE DIVISION ____________________________________ ) MASTER FILE NO. C-99-20743-RMW IN RE MCKESSON HBOC, INC. ) And Consolidated Cases SECURITIES LITIGATION ) ) The Honorable Ronald M. Whyte ____________________________________ ) Date: June 7, 2002 ) Time: 9:00 a.m. This Document Relates To: All Actions ) Courtroom: 6, Fourth Floor ____________________________________ ) LEAD PLAINTIFF’S MEMORANDUM OF POINTS AND AUTHORITIES IN OPPOSITION TO DEFENDANT BEAR, STEARNS & CO.’S MOTION TO DISMISS THE THIRD AMENDED AND CONSOLIDATED CLASS ACTION COMPLAINT

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Lead Plaintiff’s Mem. Of Pts. And Auth. In Opp. To Defendant Bear, Stearns & Co.’s Motion To DismissLead Plaintiff’s Third Amended And Consol. Class Action Complaint, Master File No. C-99-20743-RMW

BERNSTEIN LITOWITZ BARRACK, RODOS & BACINE BERGER & GROSSMANN LLP Leonard BarrackMax W. Berger Gerald J. RodosDaniel L. Berger M. Richard KominsRochelle Feder Hansen Robert A. HoffmanJ. Erik Sandstedt 3300 Two Commerce SquareBeata Gocyk-Farber 2001 Market Street1285 Avenue of the Americas Philadelphia, PA 19103New York, NY 10019 Telephone: (215) 963-0600Telephone: (212) 554-1400

- and - - and -

12730 High Bluff Drive, Suite 100 Stephen R. Basser (Cal. No. 121590)San Diego, CA 92130 402 West Broadway, Suite 850Telephone: (858) 793-0070 San Diego, CA 92101

Telephone: (619) 230-0800

Attorneys for Lead Plaintiff The New York State CommonRetirement Fund and Co-Lead Counsel for the Class

UNITED STATES DISTRICT COURTNORTHERN DISTRICT OF CALIFORNIA

SAN JOSE DIVISION

____________________________________ ) MASTER FILE NO. C-99-20743-RMW

IN RE MCKESSON HBOC, INC. ) And Consolidated CasesSECURITIES LITIGATION )

) The Honorable Ronald M. Whyte____________________________________ ) Date: June 7, 2002

) Time: 9:00 a.m.This Document Relates To: All Actions ) Courtroom: 6, Fourth Floor____________________________________ )

LEAD PLAINTIFF’S MEMORANDUM OF POINTS ANDAUTHORITIES IN OPPOSITION TO DEFENDANT BEAR,

STEARNS & CO.’S MOTION TO DISMISS THE THIRD AMENDED AND CONSOLIDATED CLASS ACTION COMPLAINT

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Lead Plaintiff’s Mem. Of Pts. And Auth. In Opp. To Defendant Bear, Stearns & Co.’s Motion To DismissLead Plaintiff’s Third Amended And Consol. Class Action Complaint, Master File No. C-99-20743-RMW 1

STATEMENT OF ISSUES PRESENTED

1. Whether the Third Amended and Consolidated Complaint adequately states a claim against

Bear Stearns for violations of Section 10(b) and Rule 10b-5 promulgated thereunder (Count IV)?

2. Whether the Third Amended and Consolidated Complaint adequately states a claim against

Bear Stearns for violations of Section 14(a) and Rule 14a-9 promulgated thereunder (Count VIII)?

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Lead Plaintiff’s Mem. Of Pts. And Auth. In Opp. To Defendant Bear, Stearns & Co.’s Motion To DismissLead Plaintiff’s Third Amended And Consol. Class Action Complaint, Master File No. C-99-20743-RMW 1

Lead Plaintiff, the New York State Common Retirement Fund (hereinafter “Lead Plaintiff”),

respectfully submits this memorandum of points and authorities in opposition to the motion of defendant

Bear Stearns & Co., Inc. (“Bear Stearns”) to dismiss the Third Amended and Consolidated Class Action

Complaint (“TAC”).

PRELIMINARY STATEMENT

The instant action arises out of a massive accounting fraud perpetrated by HBO & Company

(“HBOC”). Deloitte & Touche (“Deloitte”) initially discovered that HBOC was falsifying its financial

statements during accounting due diligence it performed in connection with the contemplated merger of

McKesson Corporation (“McKesson”) and HBOC. Deloitte disclosed the accounting improprieties to

its client, McKesson, and to Bear Stearns, the investment bank that McKesson had hired to render an

opinion as to the fairness of the merger. But rather than make Deloitte’s findings public or walk away

from the deal, McKesson chose to bury those findings. It undertook that course of action in order to

ensure that its merger with HBOC would be effectuated, believing that it could remedy HBOC’s improper

accounting practices after the deal was done. (See discussion in Lead Plaintiff’s response to McKesson’s

Motion to Dismiss.)

In order to persuade its shareholders to vote in favor of the merger, McKesson needed Bear

Stearns to conclude that the merger was fair. Accordingly, McKesson specifically instructed Bear Stearns

to rely only on the information it and HBOC provided, and not to adjust any of HBOC’s financial

information to account for Deloitte’s findings. Bear Stearns followed McKesson’s instruction and did

not consider HBOC’s true financial condition with respect to any of the work it performed in connection

with the merger. Rather, Bear Stearns considered only HBOC’s reported financial information and

historical stock prices, which it knew were false. Only as a result of the limitation imposed by McKesson

was Bear Stearns able to conclude that the Exchange Ratio was fair. Bear Stearns rendered an opinion

to that effect on October 17, 1998 (the “Fairness Opinion”). The Fairness Opinion was then incorporated

into the Joint Proxy Statement filed with the SEC on November 27, 1998 (the “Joint Proxy”), which, in

turn, was successful in convincing McKesson’s shareholders to vote in favor of the merger.

Simply stated, Bear Stearns had an obligation to the shareholders of McKesson to consider all of

the information it learned about HBOC, including the fact that its financial statements were

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

1 The facts relevant to this action are set forth in the TAC and are hereby incorporated byreference. For the Court’s convenience, however, the key facts relevant to Bear Stearns’ motion todismiss (“MTD”) are briefly highlighted below. Hereinafter, “¶ _” refers to the paragraphs of the TAC.

Lead Plaintiff’s Mem. Of Pts. And Auth. In Opp. To Defendant Bear, Stearns & Co.’s Motion To DismissLead Plaintiff’s Third Amended And Consol. Class Action Complaint, Master File No. C-99-20743-RMW 2

misrepresented, in assessing whether the merger was fair. At the very least, Bear Stearns had an

obligation to be forthcoming about the fact that Deloitte had discovered accounting irregularities in

HBOC’s financials, that McKesson had instructed it to ignore these findings, and that it had followed

McKesson’s instruction with respect to all of the work it performed in connection with the merger. Had

it fulfilled that obligation, shareholders would have known that HBOC’s stock price was based on two

and half years of overstated financial statements and, as a result, the Exchange Ratio was distorted in

HBOC’s favor. But rather than act in good faith, Bear Stearns issued the false Fairness Opinion, without

any reference to the true state of affairs at HBOC. Moreover, Bear Stearns either made or allowed

numerous false and misleading statements in the Fairness Opinion and Joint Proxy to the effect that it had

acted independently and considered all available information in evaluating the merger.

The facts of this case were not surmised by Lead Plaintiff. Rather, they are supported by direct

evidence in the form of Bear Stearns’ own internal memoranda (the “Bear Stearns Memos”), which have

been placed before this Court in the Declaration of J. Molnar (the “Molnar Decl.”). The Bear Stearns

Memos describe in great detail what Bear Stearns knew, when it knew it, and the specific instructions it

followed in assessing the fairness of the merger. Nevertheless, Bear Stearns asks this Court to dismiss

the TAC. In so doing, it recasts the particularized facts set forth in the TAC and argues that its version

of events does not support Lead Plaintiff’s claims. The Court should not accept Bear Stearns’s invitation

to disregard both the well-pled facts and the law governing the instant motion to dismiss. Rather, the

Court should consider Lead Plaintiff’s allegations, as well as the plain language of the Bear Stearns

Memos; accept those allegations as true, as is required under the law; and conclude that the TAC

adequately states claims under Sections 10(b) and 14(a) and the rules promulgated thereunder.

STATEMENT OF FACTS1

In or about July 1998, McKesson hired Deloitte to conduct accounting due diligence in connection

with a contemplated merger of McKesson and HBOC. ¶ 48. During the course of that due diligence,

Deloitte discovered that HBOC’s financial statements contained numerous violations of GAAP. See ¶

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Lead Plaintiff’s Mem. Of Pts. And Auth. In Opp. To Defendant Bear, Stearns & Co.’s Motion To DismissLead Plaintiff’s Third Amended And Consol. Class Action Complaint, Master File No. C-99-20743-RMW 3

50-56. Deloitte reported these findings to McKesson and to Bear Stearns, who McKesson had hired to

render an opinion as to the fairness of the merger for the benefit of its shareholders. ¶ 57.

In a memorandum dated July 13, 1998, from Kevin Clarke and David Blume of Bear Stearns to

the Project Titan File (the “July 13 Memo”) (Molnar Decl., Ex. B), Bear Stearns outlined the various

financial improprieties identified by Deloitte. See ¶¶ 50-56. It also quantified those improprieties and

reported that both Deloitte and McKesson’s CFO, Richard Hawkins, believed that it was likely that the

SEC would require HBOC to restate its financial statements if they ever came to light. ¶ 57. Following

discussions with representatives of McKesson, Deloitte and Bear Stearns, McKesson’s Board of Directors

chose not to pursue the merger. ¶ 58. That decision was publicly announced on July 15, 1998. Id.

In mid-October, 1998, McKesson sought to resurrect the transaction. ¶ 59. The revised deal was

more favorable to McKesson in that the revised Exchange Ratio represented a 10.2% improvement over

the ratio that had been proposed in July. ¶ 60. Nevertheless, the Exchange Ratio was still calculated

based on HBOC’s historical market price, and it still represented a significant premium – 11% – over

HBOC’s closing stock price on October 16, 1998. ¶ 59. Specifically, as set forth in the Joint Proxy, the

Exchange Ratio was based on the historical stock prices of HBOC and McKesson and their implied

market ratios over time. The implied market ratios were determined by dividing the price per share of

HBOC common stock by the price per share of McKesson common stock. Joint Proxy at 43. Bear

Stearns reviewed those ratios for the one-year, six-month and one-month periods ended October 16,

1998. Id. In view of those figures, Bear Stearns concluded that the Exchange Ratio “was within the

range of high and low implied market ratios for the observed periods.” Id.

In connection with the merger, Deloitte conducted a “bringdown” review, the results of which

were reported to Bear Stearns. ¶ 62. In a memorandum dated November 18, 1998, from Clarke and

Blume to the Project Titan File (the “November 18 Memo”) (Molnar Decl., Ex. D), Bear Stearns

confirmed that all of the improprieties that had been discovered by Deloitte in July either remained

unchanged or had worsened in the intervening period. ¶ 64.

On October 17, 1998, Bear Stearns issued the Fairness Opinion (Molnar Decl. Ex. F), which

stated as follows: “it is our opinion that the Exchange Ratio is fair, from a financial point of view, to the

shareholders of McKesson.” ¶ 249. The Fairness Opinion represented that, in reaching its conclusion,

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Lead Plaintiff’s Mem. Of Pts. And Auth. In Opp. To Defendant Bear, Stearns & Co.’s Motion To DismissLead Plaintiff’s Third Amended And Consol. Class Action Complaint, Master File No. C-99-20743-RMW 4

Bear Stearns reviewed and “relied upon,” among other things, the historical financial information of

HBOC, including HBOC’s annual reports for the fiscal years ended December 31, 1996 and 1997 and

its quarterly reports for the periods ended March 31, 1998 and June 30, 1998, as well as historical prices

and trading volumes of the common shares of McKesson and HBOC. See ¶¶ 249, 261, 294. Moreover,

the Fairness Opinion specifically stated that Bear Stearns had relied upon the representations of

McKesson and HBOC management that they were “unaware of any facts that would make [their] financial

information... incomplete or misleading.” ¶ 294(d).

The Fairness Opinion was both objectively and subjectively false. In fact, the Exchange Ratio was

not fair to McKesson shareholders. See ¶¶ 50-72, 252-253. Moreover, Bear Stearns could not have

believed the Exchange Ratio was fair, because it had been advised by Deloitte that HBOC had been, and

continued to be engaged in the falsification of its financial statements. See ¶¶ 50-72, 252-70.

Nevertheless, at McKesson’s request, Bear Stearns ignored Deloitte’s findings in evaluating the merger.

¶ 68. Thus, rather than performing a good faith analysis based on the true state of financial affairs at

HBOC, Bear Stearns relied upon HBOC’s false financial information and rendered an opinion that it knew

had no basis in fact. See ¶¶ 67-72. Only by following McKesson’s instruction to limit its analysis was

Bear Stearns able to opine that merger was fair. ¶ 69.

Bear Stearns then consented to the incorporation of the Fairness Opinion into the Joint Proxy for

the purpose of soliciting McKesson shareholders to vote in favor of the merger. ¶ 341. In lending its

name to the Joint Proxy, Bear Stearns had an independent obligation to ensure that it was not materially

false or misleading. See ¶¶ 339-358. Nevertheless, the Joint Proxy made numerous false and misleading

representations aimed at convincing investors that the merger was fair, that Bear Stearns had considered

all available information in making its determination, and that its investigation had not been restricted by

McKesson. See ¶¶ 95-97, 252-279, 339-358. Indeed, the Joint Proxy failed to make any mention of

Deloitte’s findings, or even to disclose that McKesson had hired Deloitte to conduct accounting due

diligence. Id. Most importantly, the Joint Proxy falsely stated that “McKesson did not provide specific

instructions to, or place any limitations upon, Bear Stearns with respect to the procedures to be followed

or the factors to be considered by Bear Stearns in performing its analysis or rendering [the Fairness

Opinion].” ¶¶ 96(d), 345.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Lead Plaintiff’s Mem. Of Pts. And Auth. In Opp. To Defendant Bear, Stearns & Co.’s Motion To DismissLead Plaintiff’s Third Amended And Consol. Class Action Complaint, Master File No. C-99-20743-RMW 5

In return for its actions, Bear Stearns received “success fee” of $20 million, of which $3 million

represented payment for the Fairness Opinion. See ¶¶ 280-290; Joint Proxy at 44. The remaining $17

million was contingent upon and payable at the consummation of the merger. Id. This success fee was

unusually high in view of the work Bear Stearns actually performed. Id. Moreover, Bear Stearns was

specifically advised by Hawkins that, after the merger, McKesson would attempt to remedy HBOC’s

GAAP violations over an eighteen-month period so that the improprieties would not be detected. ¶ 56,

257-258. In view of this representation, Bear Stearns had every reason to believe that the combined

entity would expunge its misconduct before it ever came to light. Id. After the merger, however,

McKesson discovered that HBOC’s fraud was actually much worse than it originally had anticipated. See

¶¶ 76-94. As a result, there was simply no way for the company to keep the fraud hidden or to avoid a

restatement. Id.

On January 28, 1999, Clarke and Blume wrote a memorandum to their superiors at Bear Stearns,

Alan Schwartz and Michael Offen (the “January 28 Memo”). In the January 28 Memo, Clarke and Blume

admit that they had discussed HBOC’s accounting irregularities with McKesson’s Board of Directors,

that the Board had discussed the irregularities with its “management team” and Deloitte, and that the

Board had decided to go forward with the merger of McKesson and HBOC. ¶ 68. The January 28

Memo also states that McKesson instructed Bear Stearns to ignore Deloitte’s findings in rendering its

Fairness Opinion. Id. According to Clarke and Blume: “we were instructed by McKesson to rely only

on the information provided to us by McKesson and HBOC and not to adjust any of this information

based on the questions raised by Deloitte.” Id. (emphasis added). Thereafter, Bear Stearns

“communicated to McKesson’s board that [it] followed these instructions with respect to all of the work

Bear Stearns performed in connection with the Transaction.” Id. (emphasis added).

The January 28 Memo could not be clearer. On its face, it proves that (i) both Bear Stearns and

McKesson’s Board had actual knowledge of the accounting irregularities discovered by Deloitte; (ii)

McKesson specifically instructed Bear Stearns to ignore those irregularities in rendering its Fairness

Opinion; (iii) Bear Stearns did ignore Deloitte’s findings in rendering its Fairness Opinion; and (iv)

McKesson’s Board knew that Bear Stearns had followed the instruction. Id.

Just three and half months after the merger, on April 28, 1999, McKesson disclosed that HBOC’s

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Lead Plaintiff’s Mem. Of Pts. And Auth. In Opp. To Defendant Bear, Stearns & Co.’s Motion To DismissLead Plaintiff’s Third Amended And Consol. Class Action Complaint, Master File No. C-99-20743-RMW 6

historical financial statements, including those published in the Joint Proxy, were materially false and had

to be restated. ¶ 76. The disclosure caused McKesson HBOC stock to drop 48% – from $67.75 to

$34.50 – in a single day. ¶ 78. Thereafter, company made additional disclosures, revealing the full scope

of the fraud that had been perpetrated by HBOC in the first instance and then continued by its successor,

the Health Care Information Technology Unit of McKesson HBOC, after the merger. See ¶¶ 76-94. As

a result of this fraud, the Plaintiff Class has suffered billions of dollars of losses.

ARGUMENT

THE TAC STATES CLAIMS AGAINST BEAR STEARNS FOR VIOLATIONS OFSECTIONS 10(b) AND 14(a) AND THE RULES PROMULGATED THEREUNDER

It is well-settled that on a motion to dismiss, all material allegations in a complaint must be taken

as true and construed in a light most favorable to the plaintiff. See In re Silicon Graphics, Inc. Sec. Litig.,

183 F.3d 970, 980 n.10, 983 (9th Cir. 1999); In re Hi/Fn, Inc. Sec. Litig., 2000 U.S. Dist. LEXIS 11631,

at *11 (N.D. Cal. Aug. 9, 2000) . Indeed, the dismissal of a complaint is appropriate only if it “appears

beyond a doubt that the plaintiff can prove no set of facts in support of his claim which would entitle him

to relief.” Conley v. Gibson, 355 U.S. 41, 45-46 (1957). The passage of the Reform Act did not change

these fundamental principles. See Silicon Graphics, 183 F.3d at 980 n.10, 983. Consequently, “[e]ven

if the face of the pleadings suggests that the chance of recovery is remote, the Court must allow the

plaintiff to develop the case at this stage of the proceedings.” Hi/Fn, 2000 U.S. Dist. LEXIS 11631, at

*11 (citing United States v. City of Redwood City, 640 F.2d 963, 966 (9th Cir. 1981)). The issue on a

motion to dismiss is not whether Lead Plaintiff will prevail, but whether it is entitled to offer evidence to

support its claim. Usher v. City of Los Angeles, 828 F.2d 556, 561 (9th Cir. 1987); In re

2THEMART.COM, Inc. Sec. Litig., 114 F. Supp. 2d 955, 959 (C.D. Cal. 2000).

The TAC alleges with particularity that the Fairness Opinion was both objectively and subjectively

false. Specifically, it alleges that the Exchange Ratio was not fair to McKesson shareholders, and that

Bear Stearns had no reason to believe it was fair. In addition, the TAC sets forth numerous specific

statements of fact – not opinion – in the Fairness Opinion and Joint Proxy to the effect that Bear Stearns

had considered all available information in assessing whether the merger was fair and that McKesson had

not placed any limitations upon Bear Stearns in reaching that conclusion.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

2 In its January 8, 2002 Order granting Bear Stearns motion to dismiss the SAC, the Courtrequired that Lead Plaintiff allege with greater particularity how the instruction given by McKesson“affected the Bear Stearns Fairness Opinion or how the accounting issues raised by Deloitte were materialor raised ‘red flags’ that would have alerted Bear Stearns to the alleged fraud of HBOC management.”The TAC addresses each of these concerns. See infra, pp. 11-16 (how it affected the opinion); 8-11(materiality); 20-22 (“red flags”).

Lead Plaintiff’s Mem. Of Pts. And Auth. In Opp. To Defendant Bear, Stearns & Co.’s Motion To DismissLead Plaintiff’s Third Amended And Consol. Class Action Complaint, Master File No. C-99-20743-RMW 7

As evidenced by the Bear Stearns Memos, each of these statements was materially false and

misleading. In truth, Bear Stearns did not perform its duties in good faith. Bear Stearns knew that

HBOC was involved in numerous fraudulent accounting practices and that its financial information was

materially misstated. As a result, Bear Stearns knew that the Exchange Ratio – which was based, in part,

on HBOC’s historical market price – was distorted in favor of HBOC shareholders and, therefore, not

fair to McKesson shareholders. Nevertheless, Bear Stearns abided by an improper instruction from

McKesson to disregard HBOC’s accounting improprieties in evaluating the Exchange Ratio. As a result,

Bear Stearns ignored the very fact that McKesson shareholders would have deemed most important in

deciding how to vote: that HBOC was “cooking its books.” Only by overlooking that key fact was Bear

Stearns able to conclude that the merger was fair.

Despite these facts, Bear Stearns now claims that Lead Plaintiff has failed to state a claim under

the federal securities laws. Specifically, Bear Stearns argues that the TAC fails to adequately allege that

(a) it made a materially false or misleading statement, or (b) that it acted with the required state of mind.

These arguments are specious. As set forth below, the TAC alleges with great particularity that both the

Fairness Opinion and the Joint Proxy were materially false and misleading, and that Bear Stearns was fully

aware of these facts. Accepting these allegations as true and drawing all reasonable inferences in favor

of Lead Plaintiff, there can be no doubt that the TAC adequately states a claim of securities fraud.2

A. The TAC Adequately Pleads that the Joint Proxy and Fairness Opinion Were MateriallyFalse and Misleading

Under the Reform Act, the TAC must “specify each statement alleged to have been misleading,

the reason or reasons why the statement is misleading, and, if an allegation regarding the statement is

made on information and belief, the complaint shall state with particularity all facts on which that belief

is formed.” 15 U.S.C. 78u-4(b)(1). Bear Stearns claims that the TAC fails to satisfy those heightened

pleading requirements. As set forth below, however, Lead Plaintiff has adequately alleged that the Joint

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Lead Plaintiff’s Mem. Of Pts. And Auth. In Opp. To Defendant Bear, Stearns & Co.’s Motion To DismissLead Plaintiff’s Third Amended And Consol. Class Action Complaint, Master File No. C-99-20743-RMW 8

Proxy and Fairness Opinion were materially false and misleading.

1. The Fairness Opinion was Materially False and Misleading

A statement or omission is “material” if “there is a substantial likelihood that a reasonable

shareholder would consider it important in deciding how to vote.” TSC Indus., Inc. v. Northway, Inc.,

426 U.S. 438, 449 (1976). Stated another way, “there must be a substantial likelihood that the disclosure

of the omitted fact would have been viewed by the reasonable investor as having significantly altered the

‘total mix’ of information made available.” Id. Materiality is a mixed question of law and fact, the

determination of which “requires delicate assessments of the inferences a ‘reasonable shareholder’ would

draw from a given set of facts and the significance of those inferences to him, and these assessments are

peculiarly ones for the trier of fact.” Id. at 450 (emphasis added). Here, the TAC identifies numerous

specific statements in the Fairness Opinion and specifies the reason or reasons why those statements were

materially false and misleading. Bear Stearns is liable for each of these statements under Section 10(b)

and Rule 10b-5.

First, the Fairness Opinion stated that the Exchange Ratio was fair. ¶ 249. In considering the

First Amended and Consolidated Complaint (“FAC”), this Court already concluded that Lead Plaintiff

has adequately alleged that this representation was objectively false. See In re McKesson HBOC, Inc.

Sec. Litig., 126 F. Supp. 2d 1248, 1273 (N.D. Cal. 2000). The TAC contains just as much, if not more

detail than the FAC. See ¶ 50-72, 249. Therefore, there can doubt that this claim is still sufficient.

The TAC also specifies several additional statements in the Fairness Opinion that were materially

false and misleading. Specifically, Bear Stearns stated that it had:

(i) reviewed the Annual Reports on Form 10-K and Quarterly Reports on Form 10-Q ofHBOC for the fiscal years ended December 31, 1996 and 1997 and the quarters endedMarch 31, 1998 and June 30, 1998; (ii) reviewed additional financial and operatinginformation relating to McKesson’s and HBOC’s businesses and prospects; (iii) met withmanagement representatives from both companies to discuss the operations, financialstatements, and future prospects of both companies; and (iv) conducted such otherstudies, analyses, inquiries, and investigations, as it deemed appropriate.

¶¶ 249, 294(a). It was materially misleading for Bear Stearns to say that it had reviewed HBOC’s 1996,

1997 and 1998 financial statements and additional financial and operating information without disclosing

that its “review” was constrained by McKesson’s instruction to ignore Deloitte’s findings with respect

to that information. See ¶¶ 50-72, 245-251, 294(a). It also was materially misleading for Bear Stearns

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Lead Plaintiff’s Mem. Of Pts. And Auth. In Opp. To Defendant Bear, Stearns & Co.’s Motion To DismissLead Plaintiff’s Third Amended And Consol. Class Action Complaint, Master File No. C-99-20743-RMW 9

to suggest that it had conducted a thorough inquiry when, in fact, Bear Stearns failed to consider all of

the facts about which it was aware – specifically, HBOC’s accounting improprieties which McKesson had

instructed it to ignore. Id.

Similarly, Bear Stearns stated that “we have further relied upon the assurances of senior

management of McKesson and HBOC that they are unaware of any facts that would make the [financial]

information... provided to us incomplete or misleading.” ¶ 294(d). Contrary to this assertion, Hawkins

– who was McKesson’s CFO and certainly one of its “senior management” – was aware of facts

establishing that HBOC’s financial information was misstated and, rather than assuring Bear Stearns of

the completeness and accuracy of that information, he advised Bear Stearns that HBOC’s financial

statements would likely need to be restated. See ¶¶ 50-72, 245-251, 294(d). Also, Bear Stearns

represented that “[i]n the course of our review, we have relied upon and assumed, without independent

verification, the accuracy and completeness of the financial information... provided to us by McKesson

and HBOC.” ¶ 294(c). As alleged in the TAC, these statements were materially misleading because they

led investors to believe that Bear Stearns did not possess any information that called HBOC’s financial

information into question when, in fact, Bear Stearns knew that HBOC’s financial information was not

accurate or complete, and that it had relied on that information only as a result of McKesson’s improper

instruction. See ¶¶ 50-72, 245-251, 294(c).

Finally, Bear Stearns represented that “[i]n arriving at our opinion, we have not performed or

obtained any independent appraisal of the assets or liabilities of McKesson or HBOC, nor have we been

furnished with any such appraisals. Our opinion is necessarily based on economic, market and other

conditions, and on the information made available to us, as of the date hereof.” Molnar Decl., Ex. F at

2 (emphasis added); ¶ 294(e). These statements were materially false and misleading because (i) at the

time it was assessing the merger, Bear Stearns had been furnished with an independent appraisal by

Deloitte of HBOC’s assets – specifically, its accounts receivable – and had concluded that they were

fraudulently inflated by millions of dollars, and (ii) the opinion was not based on all of the information

made available to Bear Stearns, but rather only the information that McKesson wanted it to consider. See

¶¶ 50-72, 245-251, 294(e).

2. The Joint Proxy was Materially False and Misleading

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Lead Plaintiff’s Mem. Of Pts. And Auth. In Opp. To Defendant Bear, Stearns & Co.’s Motion To DismissLead Plaintiff’s Third Amended And Consol. Class Action Complaint, Master File No. C-99-20743-RMW 10

The TAC alleges that Bear Stearns permitted the use of its name and its Fairness Opinion in the

Joint Proxy to solicit proxies from McKesson shareholders in favor of the merger. See ¶ 341. As set forth

in paragraphs 96 and 97 of the TAC, the Joint Proxy also contained numerous statements in addition to

the Fairness Opinion that were materially false and misleading. ¶ 353. Bear Stearns is liable for each of

these statements.

Most significantly, the Joint Proxy unequivocally stated that:

McKesson did not provide specific instructions to, or place any limitation upon, BearStearns with respect to the procedures to be followed or factors to be considered by BearStearns in performing its analysis or rendering [the Fairness Opinion].

¶ 96(d), 353 (emphasis added). This statement obviously was false. Indeed, in its own January 28

Memo, Bear Stearns admits that it was “instructed by McKesson to rely only on the information provided

to us by McKesson and HBOC and not to adjust any of this information based on the questions raised by

Deloitte.” ¶ 68; see also ¶ 345. Moreover, this representation was material. By claiming that it had not

placed any restrictions on Bear Stearns’ review of the transaction, McKesson led its shareholders to

believe that Bear Stearns had acted independently and was unfettered by any constraints in determining

whether the merger was fair. In fact, McKesson had ensured that Bear Stearns would not consider the

truth about HBOC’s accounting practices and financial statements. Thus, there can be little doubt that

this representation “implicate[d] matters at the heart of the decision confronting shareholders.” Dowling

v. Narragansett Capital Corp., 735 F. Supp. 1105, 1119 (D.R.I. 1990); see also Caruso v. Metex Corp.,

1992 WL 237299, at *12 (E.D.N.Y. July 30, 1992) (where a company withheld information from its

investment banker, Bear Stearns, and failed to disclose that limitation to shareholders, the inclusion of the

fairness opinion in the proxy statement was materially false and misleading).

Similarly, the Joint Proxy stated that the Fairness Opinion “set forth the assumptions made,

matters considered and qualifications and limitations on the review undertaken....” ¶¶ 96(e) (emphasis

added). This assertion was also materially false. The Fairness Opinion did not set forth the limitation that

McKesson had placed on Bear Stearns’ review or the fact that Bear Stearns did not consider Deloitte’s

findings, which highlighted HBOC’s improper accounting practices and called into question the accuracy

of its financial statements. Id. Moreover, this statement was material. It led investors to believe that

Bear Stearns had considered all available information in concluding that the merger was fair when, in fact,

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Lead Plaintiff’s Mem. Of Pts. And Auth. In Opp. To Defendant Bear, Stearns & Co.’s Motion To DismissLead Plaintiff’s Third Amended And Consol. Class Action Complaint, Master File No. C-99-20743-RMW 11

Bear Stearns had purposefully disregarded essential facts that all investors would have wanted to know

– i.e., that HBOC had been employing improper accounting practices for the past two and half years and,

as a result, its financial statements and stock price were fraudulently inflated.

Finally, the Joint Proxy included HBOC’s historical financial statements and pro forma financial

statements for the combined entity, as well as a representation that HBOC’s financial statements had been

prepared in conformity with GAAP. See ¶ 353. These statements obviously were materially false and

misleading, for the true state of HBOC’s financial affairs was markedly different than was represented in

those documents, and its financial statements, in fact, did not comply with GAAP.

3. Bear Stearns Decision to Follow McKesson’s Instruction and Ignore Deloitte’sFindings Affected the Fairness Opinion

Bear Stearns also claims that the TAC fails to adequately allege how McKesson’s instruction to

ignore Deloitte’s findings affected the Fairness Opinion. In making this argument, however, Bear Stearns

does not accept the well-pled allegations in the TAC as true. Rather, it recasts these facts in a light more

favorable to itself, and then argues that the inferences to be drawn from the version of events it has spun

support the dismissal of this action. This exercise is wholly improper on a motion to dismiss. Indeed, the

TAC more than adequately alleges that but for McKesson’s instruction to disregard the irregularities

discovered by Deloitte, Bear Stearns could not have concluded that the merger was fair.

Bear Stearns evaluated the Exchange Ratio based on, among other things, HBOC’s then-existing

financial information. See ¶ 262-70. Indeed, the Fairness Opinion specifically states that Bear Stearns

“relied upon” HBOC’s financial information, which included: “HBOC’s Annual Reports to Stockholders

and Annual Reports on Form 10-K for the fiscal years ended December 31, 1996 and 1997 and its

Quarterly Reports on Form 10-Q for the periods ended March 31, 1998 and June 30, 1998;” discussions

with members of senior management regarding “operations, historical financial statements and future

prospects of McKesson and HBOC;” and a review of “historical prices and trading volumes of the

common shares of McKesson and HBOC.” ¶¶ 249, 261. Bear Stearns was told by Deloitte that these

financial statements were not produced in conformity with GAAP. Further, it knew that the amounts

overstated in HBOC’s operating statements and balance sheets for 1997 and the nine months ended

September 30, 1998 were material. Nevertheless, it was instructed to – and did – ignore these findings

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Lead Plaintiff’s Mem. Of Pts. And Auth. In Opp. To Defendant Bear, Stearns & Co.’s Motion To DismissLead Plaintiff’s Third Amended And Consol. Class Action Complaint, Master File No. C-99-20743-RMW 12

“with respect to all of the work Bear Stearns performed in connection with the Transaction.” ¶ 96(d).

If Bear Stearns had considered Deloitte’s findings, it could not have concluded that HBOC was

worth what McKesson intended to pay. Id. In fact, Bear Stearns knew exactly what the necessary

adjustments would have meant, for it had quantified the impact of the improprieties on HBOC’s then-

current financial statements. See ¶ 265-267. In so doing, Bear Stearns concluded that:

• “[b]ased on Deloitte’s assessment, [HBOC’s] net income from 1997 and the first sixmonths of 1998 could each be misstated by as much as $14 million,” ¶ 265.

• “for the year ended December 31, 1997 and for the six months ended June 30, 1998 netincome was overstated by 6.9%-7.2% and 6.5%-6.8%, respectively,” ¶ 266 and

• “based on Deloitte’s assessment, [HBOC] would need to increase its balance sheetreserves by approximately $40-$55 million to adequately address the [deliberate under-reserving of accounts receivable],” ¶ 267.

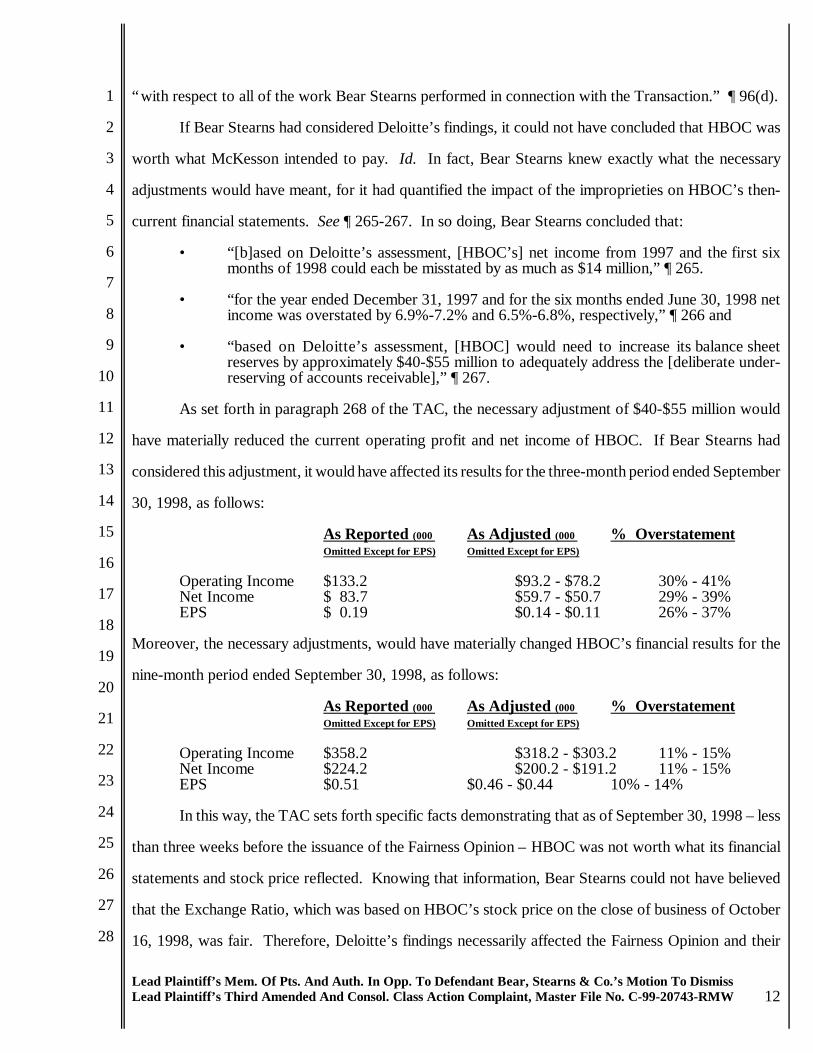

As set forth in paragraph 268 of the TAC, the necessary adjustment of $40-$55 million would

have materially reduced the current operating profit and net income of HBOC. If Bear Stearns had

considered this adjustment, it would have affected its results for the three-month period ended September

30, 1998, as follows:

As Reported (000 As Adjusted (000 % OverstatementOmitted Except for EPS) Omitted Except for EPS)

Operating Income $133.2 $93.2 - $78.2 30% - 41%Net Income $ 83.7 $59.7 - $50.7 29% - 39%EPS $ 0.19 $0.14 - $0.11 26% - 37%

Moreover, the necessary adjustments, would have materially changed HBOC’s financial results for the

nine-month period ended September 30, 1998, as follows:

As Reported (000 As Adjusted (000 % OverstatementOmitted Except for EPS) Omitted Except for EPS)

Operating Income $358.2 $318.2 - $303.2 11% - 15%Net Income $224.2 $200.2 - $191.2 11% - 15%EPS $0.51 $0.46 - $0.44 10% - 14%

In this way, the TAC sets forth specific facts demonstrating that as of September 30, 1998 – less

than three weeks before the issuance of the Fairness Opinion – HBOC was not worth what its financial

statements and stock price reflected. Knowing that information, Bear Stearns could not have believed

that the Exchange Ratio, which was based on HBOC’s stock price on the close of business of October

16, 1998, was fair. Therefore, Deloitte’s findings necessarily affected the Fairness Opinion and their

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

3 Indeed, HBOC’s historical information was essential to any determination of the merger’sfairness. ¶¶ 259-261. As set forth in the TAC, industry practice provides that “it is important for thebuyer to understand whether the target company’s financial statements depict true earnings.” ¶ 259.

Lead Plaintiff’s Mem. Of Pts. And Auth. In Opp. To Defendant Bear, Stearns & Co.’s Motion To DismissLead Plaintiff’s Third Amended And Consol. Class Action Complaint, Master File No. C-99-20743-RMW 13

implications obviously were “material” to shareholders in deciding whether to approve the merger. See

In re BankAmerica Corp. Sec. Litig., 78 F. Supp. 2d 976, 994 (E.D. Mo. 1999) (holding that information

indicating a company was overvalued in a stock-for-stock merger was material, because a reasonable

shareholder would have viewed the information as altering the “total mix” of information available).

Indeed, as discussed more fully in Lead Plaintiff’s response to McKesson’s motion to dismiss, Hawkins

conceded to Bear Stearns that the impact of these adjustments was material. Specifically, he

acknowledged that the cumulative impact on earnings of the adjustments that he would have to make to

account for the improprieties would be $29 million, which reflected a 35% and 13% overstatement of

HBOC’s reported net income for the three-months and nine-months ended September 30, 1998,

respectively. See Molnar Decl., Ex. B at 4. See also Qualitative Characteristics of Accounting

Information, Statements of Financial Accounting Concepts No. 2, App. C, ¶167 (“rule of thumb” for

materiality is 5%- 10% of net income).

Bear Stearns attempts to explain away these facts by stating that the October 16, 1998 Valuation

Committee Memorandum and its underlying exhibits (Molnar Decl., Ex. C) reflect that it did not rely on

HBOC’s historical information in rendering the Fairness Opinion. See MTD at 7 (“the underlying

financial analysis for the Fairness Opinion was based on projections provided to Bear Stearns by the

managements of McKesson and HBOC, and not on the historical financial results reflecting the

companies’ performance for 1997 and part of 1998.” (emphasis added)). Simply put, this is revisionist

history. The Fairness Opinion expressly states that Bear Stearns reviewed “and relied upon” HBOC’s

historical financial information, including its annual reports for the fiscal years ended December 31, 1996

and 1997, and its quarterly reports for the periods ended March 31, 1998 and June 30, 1998. ¶ 249, 261.

Bear Stearns cannot now walk away from those representations, which confirm that HBOC’s past

performance was a significant factor in the evaluation of the fairness of the merger. See ¶¶ 259-261.3

Bear Stearns then claims that, in fact, it did “perform[] an analysis to determine whether Deloitte’s

findings had any impact on the Fairness Opinion and concluded they did not.” MTD at 14. This new

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Lead Plaintiff’s Mem. Of Pts. And Auth. In Opp. To Defendant Bear, Stearns & Co.’s Motion To DismissLead Plaintiff’s Third Amended And Consol. Class Action Complaint, Master File No. C-99-20743-RMW 14

version of events is belied by Bear Stearns’ own January 28 Memo, which states that:

we were instructed by McKesson to rely only on the information provided to us byMcKesson and HBOC and not to adjust any of this information based on the questionsraised by Deloitte. We communicated to McKesson’s board that we followed theseinstructions with respect to all of the work Bear Stearns performed in connection with theTransaction.

¶ 68 (emphasis added).

In view of the unequivocal language of the January 28 Memo, the Court can only conclude that

Bear Stearns did not conduct any analysis of the impact of Deloitte’s findings on the fairness of the

merger. Nevertheless, Bear Stearns invites the Court to rewrite the January 28 Memo, claiming that what

it really meant was “that after Arthur Andersen reconfirmed its audit opinion (with which Deloitte

concurred), McKesson advised Bear Stearns that it could accept HBOC’s financial statements as

originally prepared without making adjustments to them.” MTD at 15. Thus, according to Bear Stearns,

“McKesson’s purported ‘instruction’ to Bear Stearns was, in reality, nothing more than a confirmation

that Bear Stearns could rely on HBOC’s financial statements as they were prepared.” Id.

Of course, that is not what the January 28 Memo says and it would be wholly improper for the

Court to accept Bear Stearns’ “spin” at this stage of the proceedings. Moreover, Bear Stearns’ version

of events is replete with false assumptions. For example, there is nothing in the record from which this

Court can conclude that “Deloitte concurred” with Andersen’s statement that HBOC’s fraud was

immaterial, or that Bear Stearns relied on such a concurrence. While Deloitte did consent to the

incorporation of its audit opinions on McKesson’s financials in the Joint Proxy, this fact does not support

a conclusion that Deloitte believed HBOC’s accounting improprieties were immaterial, as Bear Stearns

argues. See MTD at 11. Indeed, as set forth more fully in Lead Plaintiff’s response to McKesson’s

motion to dismiss, the relevant standards required only that Deloitte discuss the matter with McKesson,

which it did. See Code of Professional Conduct, ET § 203, Accounting Principles (AICPA) and AU §§

550.04-.06. Once it satisfied that obligation, there was no bar to Deloitte consenting to the inclusion in

the Joint Proxy of its opinion with respect to McKesson’s historical financial statements, the truth of

which was not impacted by HBOC’s accounting improprieties. Id. Further, Bear Stearns’ assertion is

belied by Deloitte’s express opinion that there was a “high” likelihood that the SEC would require that

HBOC’s financial statements be restated if the improper use of acquisition reserves ever became public.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Lead Plaintiff’s Mem. Of Pts. And Auth. In Opp. To Defendant Bear, Stearns & Co.’s Motion To DismissLead Plaintiff’s Third Amended And Consol. Class Action Complaint, Master File No. C-99-20743-RMW 15

¶ 54(d).

In addition, the Valuation Committee Memorandum does not state that the engagement team

made its own determination with respect to the materiality of Deloitte’s findings, as Bear Stearns now

claims. See MTD at 7. The memorandum states only that the engagement team disclosed Deloitte’s

findings to McKesson, and that it was “told by [McKesson’s] CFO that these issues have a minor impact

on [HBOC]’s historical EPS and that only a portion of the impact is recurring.” Id. at 6. Thus, rather than

suggesting that Bear Stearns performed an independent analysis with respect to Deloitte’s findings, the

Valuation Committee Memorandum actually confirms that Bear Stearns simply accepted McKesson’s

representations about the impact of HBOC’s fraud, even though it knew those representations were false.

Bear Stearns also points to the July 13 Memo, claiming that it too reflects the engagement team’s

independent assessment that Deloitte’s findings “would not adversely affect McKesson HBOC’s ability

to meet Wall Street estimates and that the impact on HBOC’s historical results would be insignificant for

purposes of the Fairness Opinion analysis.” MTD at 7. This not what the July 13 Memo says. In fact,

the July 13 Memo recognizes that the only reason the combined entity might be able to achieve its Wall

Street estimates after the merger was because it intended to ignore the impact of the corrections required

by Deloitte. ¶ 56, 257. Indeed, during the July 12, 1998 conference calls, Hawkins specifically stated

to Bear Stearns that the combined entity would not establish the reserves immediately, as required by

GAAP, but rather would phase them in over an eighteen-month period. ¶ 56. In the interim, McKesson

would deliberately publish financial statements that did not conform with GAAP and, thereby, continue

HBOC’s fraud. Id.

Finally, if nothing else, the fact that both Deloitte and Hawkins concluded that it was likely – and

in Deloitte’s view “highly” likely – that the SEC would require restatements if HBOC’s misuse of

acquisition reserves ever came to light demonstrates that Deloitte’s findings were material. ¶¶ 54(d), 254-

258. As GAAP provides, “[r]estatement is a drastic remedy. It is required, indeed, it is permitted, only

if financial statements are materially misstated.” ¶ 254 (emphasis added). As has been well-established,

a restatement of previously issued financial statements resulting from improper accounting practices

unquestionably would have had a significant impact on the price of HBOC stock and rendered the

Exchange Ratio unfair to McKesson shareholders. ¶ 255. As a sophisticated investment bank, Bear

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

4 Even if the Court were to accept Bear Stearns’ reading of the July 13 and Valuation CommitteeMemos and conclude that there is evidence to suggest that Bear Stearns had conducted an independentevaluation of Deloitte’s findings, it still would be improper for the Court to grant this motion. Indeed,at that point, there would be a factual dispute between what the January 28 and the other memoranda say.That dispute would have to be resolved by a jury, not by this Court on a motion to dismiss. SeeCampanelli v. Bockrath, 100 F.3d 1476, 1484 (9th Cir. 1996) (“[b]y comparing the merits of plaintiff’sand defendant’s characterizations, the district court impermissibly went beyond the allegations of thecomplaint to play factfinder at the 12(b)(6) stage.”)

Lead Plaintiff’s Mem. Of Pts. And Auth. In Opp. To Defendant Bear, Stearns & Co.’s Motion To DismissLead Plaintiff’s Third Amended And Consol. Class Action Complaint, Master File No. C-99-20743-RMW 16

Stearns was fully aware of that fact. Id. Thus, Bear Stearns knew that, by definition, Deloitte’s findings

would have affected the Fairness Opinion.

In sum, there can be no doubt that the TAC adequately alleges that Bear Stearns’ decision to

ignore Deloitte’s findings affected the Fairness Opinion. Indeed, only by recasting the well-pled facts in

the TAC and the Bear Stearns Memos in a light more favorable to itself can Bear Stearns argue that those

findings were not material. At trial, Bear Stearns can attempt to convince the jury of whatever facts it

wants. For the purposes of this motion, however, the Court must accept the facts in the TAC and the

Bear Stearns Memos as true and draw all reasonable inferences in favor of Lead Plaintiff. Applying this

standard, there can be no doubt that Lead Plaintiff has adequately demonstrated that McKesson’s

instruction to ignore Deloitte’s findings affected the Fairness Opinion.4

B. The TAC Adequately Pleads the Required State of Mind

Bear Stearns argues that the TAC fails to adequately plead that it acted with the required state

of mind when it issued the false Fairness Opinion and lent its name to the false Joint Proxy. However,

the facts alleged in the TAC demonstrate that Bear Stearns knew that HBOC had misrepresented its

financial statements, that the misrepresentations were material, that it had been instructed by McKesson

to disregard these facts, and that only by doing so was it able to conclude that the merger was fair. Thus,

Bear Stearns had actual knowledge that both the Fairness Opinion and Joint Proxy were materially false

and misleading. Moreover, separate and apart from pleading scienter, the TAC also specifically alleges

that Bear Stearns was negligent in allowing its name to be used in connection with the Joint Proxy.

Consequently, even if this Court were to conclude that Lead Plaintiff has failed to adequately plead

scienter, it should still sustain Lead Plaintiff’s Section 14(a) claim.

1. The TAC Pleads Particularized Facts Giving rise to a Strong Inference of Scienter

Under the Reform Act, the TAC must “state with particularity facts giving rise to a strong

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

5 In Silicon Graphics, the plaintiff alleged that “internal reports alerted the officers to seriousproduction and sales problems,” 183 F.3d at 984, however, she could not provide any “corroboratingdetails,” such as “the sources of her information with respect to the reports, how she learned of thereports, who drafted them, or which officers received them. Nor [did] she include an adequatedescription of their contents....” Id. at 985. Under such circumstances, the court concluded that theplaintiff had not adequately pled scienter.

Lead Plaintiff’s Mem. Of Pts. And Auth. In Opp. To Defendant Bear, Stearns & Co.’s Motion To DismissLead Plaintiff’s Third Amended And Consol. Class Action Complaint, Master File No. C-99-20743-RMW 17

inference that the defendant acted with the required state of mind.” 15 U.S.C. § 78u-4(b)(2). In the

context of Section 10(b), the Ninth Circuit has interpreted this to mean that Lead Plaintiff must “plead,

at a minimum, particular facts giving rise to a strong inference of deliberate or conscious recklessness.”

Silicon Graphics, 183 F.3d at 979. Scienter can be established by either direct or circumstantial evidence.

Provenz v. Miller, 102 F.3d 1478, 1490 (9th Cir. 1996). It is axiomatic that if there is direct evidence of

a defendant’s fraudulent intent, the Court need not draw any inferences to conclude that it acted with

scienter. See, e.g., County of Tuolumne v. Sonora Cmty. Hosp., 236 F.3d 1148, 1155 (9th Cir. 2001)

(direct evidence is evidence “that is explicit and requires no inferences to establish the proposition or

conclusion being asserted”). To the extent that the Court is required to draw inferences from the TAC’s

allegations, all reasonable inferences must be drawn in favor of Lead Plaintiff. See Silicon Graphics, 183

F.3d at 979. Moreover, the inference of scienter “‘must be reasonable and strong – but not irrefutable...

Plaintiffs need not foreclose all other characterizations of fact, as the task of weighing contrary accounts

is reserved for the fact finder.’” Aldridge v. A.T. Cross Corp., 284 F.3d 72, 82 (1st Cir. 2002) (quoting

Helwig v. Vencor, Inc.. 251 F.3d 540, 553 (6th Cir. 2001)).

The TAC pleads particularized facts demonstrating that Bear Stearns had actual knowledge that

the Proxy Statement and Fairness Opinion were false and misleading. These facts come from the Bear

Stearns Memos, which are recited verbatim in the TAC and have been placed before this Court by Bear

Stearns. Thus, this is not a situation like Silicon Graphics, where the plaintiff could make only vague

references to internal reports and insider sales to prove scienter.5 To the contrary, Lead Plaintiff and the

Court have access to Bear Stearns’ own internal memoranda, which outline exactly what Bear Stearns

knew, when it knew it, and the instructions it followed in preparing the Fairness Opinion. Moreover,

Lead Plaintiff has provided specific details demonstrating the reliability of the Bear Stearns Memos,

including the authors, recipients, dates and circumstances surrounding their production. Indeed, Bear

Stearns has not, and cannot question the authenticity or reliability of its own documents. Rather, as

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Lead Plaintiff’s Mem. Of Pts. And Auth. In Opp. To Defendant Bear, Stearns & Co.’s Motion To DismissLead Plaintiff’s Third Amended And Consol. Class Action Complaint, Master File No. C-99-20743-RMW 18

discussed above, Bear Stearns’ only response has been to attempt to rewrite the memoranda after-the-fact

and convince the Court to draw improper inferences in its favor. Such efforts should not be entertained.

Taken in the light most favorable to Lead Plaintiff, the Bear Stearns Memos demonstrate that Bear

Stearns knew that its Fairness Opinion was false and misleading. First, the July 13 Memo shows that Bear

Stearns was fully aware of HBOC’s GAAP violations and their effect on HBOC’s financial information.

It demonstrates that Bear Stearns had quantified the effect of HBOC’s accounting improprieties and had

been advised by Deloitte, the expert hired by McKesson to conduct accounting due diligence on HBOC,

that those improprieties were material. ¶¶ 54(d), 254-256. Moreover, the July 13 Memo reflects Bear

Stearns’ understanding that the only way HBOC’s accounting improprieties would not materially affect

the combined entity’s future operations and business prospects was if the required adjustments to conform

HBOC’s financial statements to GAAP were not made. See ¶¶ 56, 257.

All of the improprieties outlined in the July 13 Memo were reiterated in the November 18 Memo,

which was written after the “bringdown” due diligence at the time of the merger. ¶¶ 63, 264. That

memorandum demonstrates that each and every issue uncovered by Deloitte in July 1998 had either

remained unchanged or worsened by the conclusion of the quarter ended September 30, 1998. Id. It also

demonstrates that at the time Bear Stearns issued the Fairness Opinion, it was fully cognizant of the fact

that HBOC was not worth what its financial statements reflected. See ¶ 269-270. Thus, Bear Stearns

knew that the Exchange Ratio – which was based on the HBOC’s market price on the close of business

of October 16, 1998 – was not fair to McKesson shareholders. ¶¶ 269-270. Nevertheless, Bear Stearns

falsely opined that the merger was fair.

Bear Stearns also knew that other representations in the Fairness Opinion and Joint Proxy were

materially false and misleading. (See Parts (A)(1) and (A)(2) above.) Those statements were all aimed

at convincing McKesson shareholders that Bear Stearns had acted independently and considered all

available information in assessing the merger. To the contrary, the Bear Stearns Memos demonstrate that

Bear Stearns knew it had performed its duties under limitations set by McKesson. Most significantly, the

January 28 Memo proves that Bear Stearns knew that McKesson had instructed it to disregard Deloitte’s

findings in rendering the Fairness Opinion. Nevertheless, Bear Stearns signed off on the Joint Proxy,

which specifically stated that: “McKesson did not provide any specific instructions to, or place any

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Lead Plaintiff’s Mem. Of Pts. And Auth. In Opp. To Defendant Bear, Stearns & Co.’s Motion To DismissLead Plaintiff’s Third Amended And Consol. Class Action Complaint, Master File No. C-99-20743-RMW 19

limitations upon, Bear Stearns with respect to the procedures to be followed or factors to be considered

by Bear Stearns in performing its analysis or rending [the Fairness Opinion].” ¶ 96(d).

The January 28 Memo also proves that Bear Stearns knew that HBOC’s financial statements were

misstated, but that it had not taken the fact into account when evaluating the fairness of the merger.

Indeed, in drafting the January 28 Memo, Bear Stearns acknowledged that it had not considered the one

fact that McKesson’s shareholders would have wanted to know: that HBOC was “cooking its books.”

But at the same time, Bear Stearns purposefully misled investors into believing that it had no reason to

question to accuracy of HBOC’s financial information, stating, among other things, that “[i]n the course

of our review, we have relied upon and assumed, without independent verification, the accuracy and

completeness of the financial information... provided to us by McKesson and HBOC.” ¶ 293(C).

Similarly, Bear Stearns specifically stated that it had relied upon the assurances of senior management at

McKesson and HBOC “that they are unaware of any facts that would make the [financial] information...

provided to us incomplete or misleading.” ¶ 293(d). Bear Stearns knew these representations were

misleading because it knew that HBOC’s financial information was inaccurate, and it knew that

McKesson was not only aware of that fact, but had plans to continue those improprieties after the

completion of the merger. (See discussion supra.)

In addition to the direct evidence contained in the Bear Stearns Memos, the TAC pleads additional

facts that give rise to a strong inference of scienter. For example, the TAC alleges that the facts

surrounding the merger support a strong inference that Bear Stearns either knew or was deliberately

reckless in issuing the Fairness Opinion and lending its name to the Joint Proxy. See ¶¶ 181(a)-(l), 275-

279, 291-292. McKesson specifically hired Bear Stearns and Deloitte to create the impression that the

merger had been “blessed” by independent advisors. ¶¶ 291(a), 67-72. After learning about Deloitte’s

findings, however, McKesson made no effort to disclose those findings to its shareholders. Rather, it

declined to make any mention of Deloitte or the accounting due diligence in the Joint Proxy. Moreover,

McKesson specifically instructed Bear Stearns to disregard Deloitte’s findings in rendering the Fairness

Opinion, and then falsely represented in the Joint Proxy that it had not given Bear Stearns any instructions

or limitations. ¶ 291(c). Similarly, throughout the Joint Proxy, McKesson repeatedly and deliberately

conveyed the impression that Bear Stearns’ “Fairness Opinion” was independent and that it could and

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

6 This Court has recognized that an investment bank hired to render a fairness opinion should beheld to the same standards as the management it is assisting. See McKesson, 126 F. Supp. 2d at 1263(quoting Herskowitz v/ Nutri/System, Inc., 857 F.2d 179, 190 (3d Cir. 1988)).

Lead Plaintiff’s Mem. Of Pts. And Auth. In Opp. To Defendant Bear, Stearns & Co.’s Motion To DismissLead Plaintiff’s Third Amended And Consol. Class Action Complaint, Master File No. C-99-20743-RMW 20

should be relied upon. See ¶ 291(b).

Bear Stearns, in turn, agreed to follow McKesson’s instructions and ignored the fact that HBOC’s

financial statements were materially misstated when it evaluated the merger. ¶ 291(d). Nevertheless, it

specifically represented that it relied upon the accuracy of those financial statements, and that it believed

it was fair for McKesson shareholders to pay an 11% premium over HBOC’s stock price, which was

based on those false financial statements. See. e.g., Joint Proxy at 43 (demonstrating that in assessing the

Exchange Ratio, Bear Stearns analyzed HBOC’s and McKesson’s historical stock performance and

implied merger exchange ratios over time). The only inference one can draw from these facts is that Bear

Stearns knew the Fairness Opinion was false and misleading.

Bear Stearns’ purported reliance on the self-serving assertions of Andersen and HBOC that

Deloitte’s findings were immaterial also supports a strong inference of scienter. See Escott v. BarChris

Contr. Corp., 283 F. Supp. 643, 685 (S.D.N.Y. 1969) (where an officer had reason to believe expertised

portions of a prospectus were incorrect, “[h]e could not shut his eyes to the facts and rely on [the

accountants] for that portion”); Comeau v. Rupp, 810 F. Supp. 1127, 1150 (D. Kan. 1992) (corporate

directors acted recklessly as a matter of law in closing their eyes to a report of problems).6 As discussed

above, Bear Stearns knew that Andersen and HBOC’s claims had been rejected by Deloitte, who had been

hired by McKesson for the very purpose of assessing the reliability of HBOC’s books. ¶ 291(e).

Moreover, Bear Stearns knew that McKesson’s own CFO had determined that HBOC’s accounting

improprieties were material. Id. Consequently, even if true, it was at least deliberately reckless for Bear

Stearns to rely on the representations of Andersen and HBOC. Id.

Similarly, each of the accounting improprieties identified by Deloitte was a “red flag” that Bear

Stearns should have recognized and heeded. See, e.g., In re Software Toolworks, Inc., 50 F.3d 615, 623-

24 (9th Cir. 1995) (underwriter must take additional steps before relying on certified financial statements

if it becomes aware of red flag indicating problems with revenue recognition practices). The fact that

Bear Stearns ignored those red flags supports a strong inference of scienter. See In re Health Mgmt., Inc.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Lead Plaintiff’s Mem. Of Pts. And Auth. In Opp. To Defendant Bear, Stearns & Co.’s Motion To DismissLead Plaintiff’s Third Amended And Consol. Class Action Complaint, Master File No. C-99-20743-RMW 21

Sec. Litig., 970 F. Supp. 192, 203 (E.D.N.Y. 1997) (defendant acted with scienter where he ignored a

red flag, i.e., a letter from an analyst warning that the client had improperly inflated its accounts

receivable); In re Smartalk Teleservices, Inc. Sec. Litig., 124 F. Supp. 505, 520 (S.D. Ohio 2000) (finding

a red flag where independent auditor had informed client that it was reconsidering its position concerning

clients past financials, but that it was nevertheless comfortable with those financials). Specifically, as set

forth at paragraph 180 of the TAC:

C Deloitte determined that HBOC was improperly recording sales prior to granting ofrequired customer approvals in 1996 and 1997. As it turned out, this practice ofpremature recognition of revenue was, in fact, being carried out on a much larger scaleat HBOC in 1996 and 1997. Ultimately, McKesson restated $20 million in revenues forthe twelve months ended March 31, 1997 and $19 million for the twelve months endedMarch 31, 1998 because of “contingent revenues improperly recognized.”

C Deloitte determined that HBOC was improperly recording maintenance contract revenuein violation of GAAP in that it was not allocating a percentage of the total sales price tothe maintenance contract and it was not deferring the recognition of such amounts asrevenue over the life of the contract as required by GAAP. Deloitte raised this “red flag”in July. As reflected in the November 18, 1998 Memo the problem had only gotten worseby the time of the merger. This practice of improperly recording maintenance contractrevenues was also one of the GAAP violations adjusted for in the ultimate restatement.

C Deloitte found that in connection with each of the eight significant acquisitions HBOC hadcompleted since June 1995, HBOC had established “excessive” reserves and thenimproperly used those reserves to inflate earnings by charging off current operatingexpenses to those reserves. The effect was to overstate HBOC’s income by tens ofmillions of dollars. As set forth above, both Deloitte and Hawkins believed this problemwas material. This practice of reserve manipulation and excess accruals in conjunctionwith acquisitions was also one of the GAAP violations adjusted for in the restatement.

C Deloitte found that HBOC’s receivables outstanding over 90 days had increasedsubstantially from year-end 1997 and June 1998. Moreover, Deloitte indicated thatHBOC’s explanations for the enormous increases called into question the propriety ofHBOC’s revenue recognition practices. A substantial portion of the overdue receivableswas from the sale of Star Pathways products, which sales were later reversed in therestatement because HBOC’s customers (Marshall, Kaweah and Scottsdale) had noobligation to pay. See ¶ 181(l).

Despite these facts, each of which called into doubt the fairness of the merger, Bear Stearns

declined to investigate further. Instead, at the request of McKesson, it disregarded Deloitte’s findings

and their implications as to the lack of integrity of HBOC’s management. Had Bear Stearns undertaken

an appropriate inquiry, it likely would have found that the improprieties were even worse than Deloitte

had initially discovered. See ¶¶ 84-85 (recognizing that the problems identified by Deloitte were among

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

7 Bear Stearns tries to flip this fact around, claiming that it should not be liable because McKessonultimately discovered that the problems discovered by Deloitte were worse than they thought. Thisassertion is preposterous. First, the problems that Deloitte did discover were material in and ofthemselves and should have been considered in the fairness analysis and disclosed to McKesson’sshareholders. Second, as set forth in the TAC, Bear Stearns had an obligation to heed those “red flags”and undertake appropriate further inquiry before opining that the merger was fair.

8 While the Ninth Circuit has held that motive and opportunity standing alone do not satisfy theheightened pleading requirements of th Reform Act, Silicon Graphics, 183 F.3d at 980, the Court canand should consider these factors in determining whether Lead Plaintiff has alleged a strong inference ofscienter. See, e.g., Aldridge, 284 F.3d at 82.

Lead Plaintiff’s Mem. Of Pts. And Auth. In Opp. To Defendant Bear, Stearns & Co.’s Motion To DismissLead Plaintiff’s Third Amended And Consol. Class Action Complaint, Master File No. C-99-20743-RMW 22

the problems ultimately disclosed at the time of the restatement).7 Regardless, Bear Stearns’s failure to

take any action with respect to these “red flags” was at the very least deliberately reckless.

Finally, the fact that Bear Stearns had the motive and opportunity to commit the instant fraud

supports a strong inference of scienter. See ¶¶ 280-2908 Bear Stearns initial fee was $5 million, of which

$2 million was for the Fairness Opinion. ¶ 283. Bear Stearns did all of their work in July under this fee

arrangement. Id. Bear Stearns then learned of HBOC’s accounting improprieties from Deloitte, and the

deal was called off (see discussion supra). When the deal was resurrected in October, Bear Stearns did

at most two days work. ¶¶ 283, 287-90. However, Bear Stearns’s fee was increased to $20 million, of

which $3 million was for the Fairness Opinion. Id. This “success fee” was highly unusual in view of the

lack of additional work that was actually performed by Bear Stearns, but understandable in view of the

increased risk associated with rendering a Fairness Opinion without considering relevant due diligence

findings. ¶ 280. The only inference one can draw from these facts is that the success fee was a payment

for Bear Stearns’ complicity. See ¶ 282.

In addition, Bear Stearns had every reason to believe that its fraudulent intent would never come

to light. As set forth above, McKesson’s CFO had assured Bear Stearns that the combined entity would

remedy HBOC’s GAAP violations over an eighteen month period after the completion of the merger.

¶ 257-258. Indeed, it is evident from the July 13 Memo that while the parties knew the issues raised by

Deloitte were material, they also believed that those problems could be fixed. Id. As a result, Bear

Stearns had every reason to believe that the combined entity would expunge its misconduct before it had

any ramifications. In the meantime, the defendants agreed to ignore the problems, as is reflected in the

January 28 Memo.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Lead Plaintiff’s Mem. Of Pts. And Auth. In Opp. To Defendant Bear, Stearns & Co.’s Motion To DismissLead Plaintiff’s Third Amended And Consol. Class Action Complaint, Master File No. C-99-20743-RMW 23

2. At the Very Least, the TAC Adequately Pleads that Bear Stearns Was Negligent inAllowing Its Name to be Used in the Joint Proxy

This court has held that “all persons liable under Section 14 should be held to the same standard

of culpability: negligence.” McKesson, 126 F. Supp. 2d at 1264. Negligence is not a “state of mind” per

se; rather, it is a departure from the standard of care that “‘persons of ordinary prudence would use in

order to avoid injury to themselves or others under circumstances similar to those shown by the

evidence.’” USAir, Inc. v. U.S. Dep’t of Navy, 14 F.3d 1410, 1412 (9th Cir. 1994) (citations omitted).

See also Fane v. Zimmer, Inc., 927 F.2d 124, 130 n.3 (2d Cir. 1991) (“Negligence, broadly speaking, is

conduct that falls below the standard of what a reasonably prudent person would do under similar

circumstances judged at the time of the conduct at issue.”).

It is well-settled that in stating a claim for negligence, it is not necessary for a plaintiff to