BROKING | DEPOSITORY | DISTRIBUTION | FINANCIAL ADVISORY|MERCHANT BANKING BANDHAN BANK LTD IPO Report Issue Date 15 th Mar-19 th Mar 2018 Price Band 370-375/Share Bid Lot 40 & in multiplethereof Face Value Rs 10/Share Listing BSE, NSE Offer For Sale 21,616,584 Eq Shares Fresh Issue 97,663,910 Eq Shares Pre Issue Eq Shares 109.51Cr Eq Shares Post Issue Eq Shares 119.28 Cr Eq shares BRLM Kotak Mahindra Ltd, Axis Capital Ltd , Goldman Sachs India JM Financial, JP Morgan India Pvt Ltd Registrar Karvy Computershare Private Ltd Research Analyst : Astha Jain IPO Details Bandhan Bank Ltd ( BBL) was incorporated on December 23, 2014 and began operations on August 23, 2015 by opening a greenfield network of 501 bank branches and 50 automated teller machines (“ATMs”), which as of December 31, 2017 have increased to 887 bank branches and 430 ATMs, together serving over 2.13 million general banking customers. Bank’s distribution network is particularly strong in East and Northeast India, with West Bengal, Assam and Bihar together accounting for 56.37% and 57.58% of its branches and DSCs as of December 31, 2017, Consistent track record of growing a quality asset and liability franchise: As of December 31, 2017, bank’s percentage of Gross NPAs to Gross Advances (excluding IBPC/Assignment) (“NPAs”) was 1.67% of its portfolio. Bank’s strong NPA position is largely driven by its group-based individual lending model, its focus on income generating loans made to women, its strong systems to track loan utilization, monitor credit and ensure collection, and its extensive risk management practices, such as lending progressively higher amounts only to members who have built up a track record of good repayment, which taken together have led to low rates of default. Operating model focused on serving underbanked and underpenetrated markets: BBL is a commercial bank focused on serving underbanked and underpenetrated markets in India. Its historical strength lies in microfinance, with its group beginning operations in 2001 as an NGO providing microfinance services to socially and economically disadvantaged women in rural West Bengal. While bank’s business model has transitioned over the years, operating as an NGO and then a non-bank finance company (“NBFC”) before becoming a bank, the provision of micro loans to women has remained the core focus. Valuation: The Bank is bringing the issue at p/b multiple of 4.9-4.93 on post issue book value at price band of Rs 370-375/share. Bank with its operating model focused on serving underbanked and underpenetrated markets has consistent track record of growing a quality asset and liability franchise with extensive, low cost distribution network & customer-centric approach and experienced and professional team, backed by strong independent board. Hence, we recommend “Subscribe” on issue. www.hemsecurities.com SUBSCRIBE For Private Circulation Only HEM RESEARCH

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

BROKING | DEPOSITORY | DISTRIBUTION | FINANCIAL ADVISORY|MERCHANT BANKING

BANDHAN BANK LTD

IPO Report

Issue Date 15th Mar-19th Mar 2018

Price Band 370-375/Share

Bid Lot 40 & in multiplethereof

Face Value Rs 10/Share

Listing BSE, NSE

Offer For Sale 21,616,584 Eq Shares

Fresh Issue 97,663,910 Eq Shares

Pre Issue Eq Shares 109.51Cr Eq Shares

Post Issue Eq Shares 119.28 Cr Eq shares

BRLM Kotak Mahindra Ltd,

Axis Capital Ltd ,

Goldman Sachs India

JM Financial,

JP Morgan India Pvt Ltd

Registrar Karvy Computershare

Private Ltd

Research Analyst : Astha Jain

IPO Details

Bandhan Bank Ltd ( BBL) was incorporated on December 23, 2014 and

began operations on August 23, 2015 by opening a greenfield network of

501 bank branches and 50 automated teller machines (“ATMs”), which as of

December 31, 2017 have increased to 887 bank branches and 430 ATMs,

together serving over 2.13 million general banking customers. Bank’s

distribution network is particularly strong in East and Northeast India, with

West Bengal, Assam and Bihar together accounting for 56.37% and 57.58%

of its branches and DSCs as of December 31, 2017,

Consistent track record of growing a quality asset and liability

franchise: As of December 31, 2017, bank’s percentage of Gross NPAs to

Gross Advances (excluding IBPC/Assignment) (“NPAs”) was 1.67% of its

portfolio. Bank’s strong NPA position is largely driven by its group-based

individual lending model, its focus on income generating loans made to

women, its strong systems to track loan utilization, monitor credit and

ensure collection, and its extensive risk management practices, such as

lending progressively higher amounts only to members who have built up a

track record of good repayment, which taken together have led to low rates

of default.

Operating model focused on serving underbanked and

underpenetrated markets: BBL is a commercial bank focused on serving

underbanked and underpenetrated markets in India. Its historical strength

lies in microfinance, with its group beginning operations in 2001 as an NGO

providing microfinance services to socially and economically disadvantaged

women in rural West Bengal. While bank’s business model has transitioned

over the years, operating as an NGO and then a non-bank finance company

(“NBFC”) before becoming a bank, the provision of micro loans to women

has remained the core focus.

Valuation: The Bank is bringing the issue at p/b multiple of 4.9-4.93 on post

issue book value at price band of Rs 370-375/share. Bank with its operating

model focused on serving underbanked and underpenetrated markets has

consistent track record of growing a quality asset and liability franchise with

extensive, low cost distribution network & customer-centric approach and

experienced and professional team, backed by strong independent board.

Hence, we recommend “Subscribe” on issue.

www.hemsecurities.com

SUBSCRIBE

For Private Circulation Only HEM RESEARCH

BANDHAN BANK LTD

BROKING | DEPOSITORY | DISTRIBUTION | FINANCIAL ADVISORY|MERCHANT BANKING

www.hemsecurities.com

Company Overview

BBL (Bandhan Bank Ltd) is a commercial bank focused on serving underbanked and underpenetrated

markets in India. BBL have a banking license that permits to provide banking services pan-India across

customer segments. Bandhan Bank currently offer a variety of asset and liability products and services

designed for micro banking and general banking, as well as other banking products and services to

generate non-interest income. Its microfinance business, includes a network of 2,022 doorstep service

centres (“DSCs”) and 6.77 million micro loan customers that BFSL transferred to it, which have grown

to 2,633 DSCs and 9.86 million micro loan customers as of December 31, 2017. BBL launched its

general banking business on August 23, 2015 by opening a greenfield network of 501 bank branches

and 50 automated teller machines (“ATMs”), which as of December 31, 2017 bank have grown to 887

bank branches and 430 ATMs, together serving over 2.13 million general banking customers. Bank’s

distribution network is particularly strong in East and Northeast India, with West Bengal, Assam and

Bihar together accounting for 56.37% and 57.58% of its branches and DSCs as of December 31, 2017,

respectively, though its focus is to expand across India.

BBL currently offer a variety of asset and liability products and services designed for micro banking

and general banking. Its asset products consist of retail loans including a substantial portfolio of micro

loans, as well as micro, small and medium enterprise (“SME”) loans and small enterprise loans.

Bank’s unsecured subordinated non-convertible debenture instruments were rated CARE AA-

(Stable) by Care Ratings Limited and AA-(Positive) by ICRA. Its rating for term loans are rated AA-

(Positive) and its certificates of deposit are rated A1+ by ICRA.

For Private Circulation Only HEM RESEARCH

\

0

5000

10000

15000

20000

25000

31.03.16 31.12.16 31.03.17 31.12.17

Net Advances (Rs Cr)

Micro Loans Small Enterprise Loan SME Loan Other Retail Loan

BANDHAN BANK LTD

BROKING | DEPOSITORY | DISTRIBUTION | FINANCIAL ADVISORY|MERCHANT BANKING

www.hemsecurities.com

Investment Rationale

Consistent Financial Performance and Robust Capital Base

Its Net Interest Income in FY 2016 amounted to ₹9,328.36 million, while Net Interest Income in

FY 2017 amounted to ₹24,034.98 million. Its net interest margin for the nine months ended

December 31, 2017 was 9.86%, while bank’s return on assets and return on equity were 4.07%

and 25.55%, respectively (each on an annualised basis). Bank’s cost-to-income ratio for the nine

months ended December 31, 2017 was 35.38% (on an annualised basis). Additionally, since

beginning operations bank have generated increasing non-interest income as a percentage of its

overall income, improving from 8.66% for March 2016 to 35.38% for the nine months ended

December 31, 2017. Of bank’s total deposits, its share of retail deposits has increased from 37.95%

as of March 31, 2016 to 85.07% as of December 31, 2017. Moreover, bank’s CASA ratio has

improved from 21.55% as of March 31, 2016 to 33.22% as of December 31, 2017.

Extensive, Low Cost Distribution Network

As of December 31, 2017, bank operated in 33 States and Union Territories in India, reaching 11.99

million customers through 887 branches, 2,633 doorstep service centres and 430 ATMs, with 2.13

million of customers belonging to bank’s general banking business. Bank’s distribution network is

particularly strong in East and Northeast India, with West Bengal, Assam and Bihar together

accounting for 56.37% and 57.58% of its branches and DSCs as of December 31, 2017,

respectively, though its focus is to expand across India.

Risk factors

Bank’s limited operating history and its fast growing and rapidly evolving business make it

difficult to evaluate its business and future operating results on the basis of its past performance,

and its future results may not meet or exceed its past performance.

For Private Circulation only HEM RESEARCH

BANDHAN BANK LTD

BROKING | DEPOSITORY | DISTRIBUTION | FINANCIAL ADVISORY|MERCHANT BANKING

www.hemsecurities.com

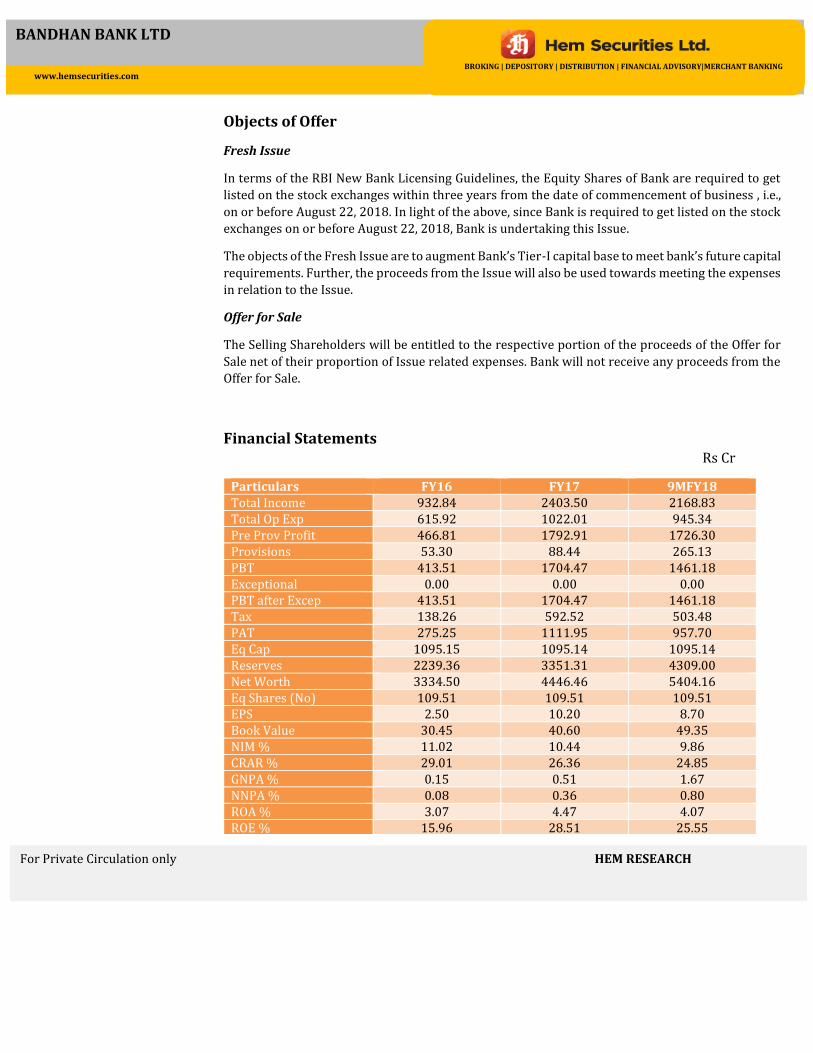

Objects of Offer

Fresh Issue

In terms of the RBI New Bank Licensing Guidelines, the Equity Shares of Bank are required to get

listed on the stock exchanges within three years from the date of commencement of business , i.e.,

on or before August 22, 2018. In light of the above, since Bank is required to get listed on the stock

exchanges on or before August 22, 2018, Bank is undertaking this Issue.

The objects of the Fresh Issue are to augment Bank’s Tier-I capital base to meet bank’s future capital

requirements. Further, the proceeds from the Issue will also be used towards meeting the expenses

in relation to the Issue.

Offer for Sale

The Selling Shareholders will be entitled to the respective portion of the proceeds of the Offer for

Sale net of their proportion of Issue related expenses. Bank will not receive any proceeds from the

Offer for Sale.

Financial Statements

Rs Cr

Particulars FY16 FY17 9MFY18 Total Income 932.84 2403.50 2168.83 Total Op Exp 615.92 1022.01 945.34 Pre Prov Profit 466.81 1792.91 1726.30 Provisions 53.30 88.44 265.13 PBT 413.51 1704.47 1461.18 Exceptional 0.00 0.00 0.00 PBT after Excep 413.51 1704.47 1461.18 Tax 138.26 592.52 503.48 PAT 275.25 1111.95 957.70 Eq Cap 1095.15 1095.14 1095.14 Reserves 2239.36 3351.31 4309.00 Net Worth 3334.50 4446.46 5404.16 Eq Shares (No) 109.51 109.51 109.51 EPS 2.50 10.20 8.70 Book Value 30.45 40.60 49.35 NIM % 11.02 10.44 9.86 CRAR % 29.01 26.36 24.85 GNPA % 0.15 0.51 1.67 NNPA % 0.08 0.36 0.80 ROA % 3.07 4.47 4.07 ROE % 15.96 28.51 25.55

For Private Circulation only HEM RESEARCH

www.hemsecurities.com

HEM SECURITIES LIMITED

MEMBER-BSE,CDSL,SEBI REGISTERED CATEGORY I MERCHANT BANKER

Sebi Registration No For Research Analyst: INH100002250

MUMBAI OFFICE: 904, A WING. 9TH FLOOR, NAMAN MIDTOWN, SENAPATI BAPAT MARG, ELPHINSTONE ROAD, LOWER PAREL ,MUMBAI -400013 PHONE- 0091 22 49060000 FAX- 0091 22 2262 5991

JAIPUR OFFICE: 203-204, JAIPUR TOWERS, M I ROAD, JAIPUR-302001 PHONE- 0091 141 405 1000 FAX- 0091 141 510 1757

GROUP COMPANIES

HEM FINLEASE PRIVATE LIMITED

MEMBER-NSE

HEM MULTI COMMODITIES PRIVATE LIMITED

MEMBER-NCDEX, MCX

HEM FINANCIAL SERVICES LIMITED

NBFC REGISTERED WITH RBI

Disclaimer & Disclosure: This document is prepared for our clients only, on the basis of publicly available information and other

sources believed to be reliable. Whilst we are not soliciting any action based on this information, all care has been taken to

ensure that the facts are accurate, fair and reasonable. This information is not intended as an offer or solicitation for the purchase

or sell of any financial instrument and at any point should not be considered as an investment advice. Reader is requested to rely

on his own decision and may take independent professional advice before investing. Hem Securities Limited, Hem Finlease Private

Limited, Hem Multi Commodities Pvt. Limited, Directors and any of its employees shall not be responsible for the content. The

person accessing this information specifically agrees to exempt Hem Securities Limited, Hem Finlease Private Limited, Hem Multi

Commodities Pvt. Limited or any of its affiliates or employees from, any and all responsibility/liability arising from such misuse

and further agrees to hold Hem Securities Limited, Hem Finlease Private Limited, Hem Multi Commodities Pvt. Limited or any of

its affiliates or employees free and harmless from all losses, costs, damages, expenses that may be suffered by the person

accessing this information due to any errors and delays. The companies and its affiliates, officers, directors, and employees,

including persons involved in the preparation or issuance of this material may from time to time, have long or short positions in,

and buy or sell the securities there of, company (ies) mentioned herein and the same have acted upon or used the information

prior to, or immediately following the publication.

Analyst Certification

The views expressed in this research report accurately reflect the personal views of the analyst(s) about the subject securities or

issues, and no part of the compensation of the research analyst(s) was, is, or will be directly or indirectly related to the specific

recommendations and views expressed by research analyst(s) in this report.

Related Documents