SUMMER INTERNSHIP PROJECT REPORT AT HALMA India Pvt. Ltd. A Project Report Submitted In Partial Fulfillment of the Requirements For The Award of the POST GRADUATE DIPLOMA IN MANAGEMENT TO M.S.RAMAIAH INSTITUTE OF MANAGEMENT BY HEMANTH KUMAR MEDA REG.NO. 151228 BATCH 2015-17 Under the guidance of Prof. ARUL JYOTHI M.S.RAMAIAH INSTITUTE OF MANAGEMENT NEW BEL ROAD, BANGALORE-560054 July 2016

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

SUMMER INTERNSHIP PROJECT REPORT

AT

HALMA India Pvt. Ltd.

A Project Report Submitted In Partial Fulfillment of the Requirements

For The Award of the

POST GRADUATE DIPLOMA IN MANAGEMENT

TO

M.S.RAMAIAH INSTITUTE OF MANAGEMENT

BY

HEMANTH KUMAR MEDA

REG.NO. 151228

BATCH 2015-17

Under the guidance of

Prof. ARUL JYOTHI

M.S.RAMAIAH INSTITUTE OF MANAGEMENT

NEW BEL ROAD, BANGALORE-560054

July 2016

CERTIFICATE

This is to certify that the Project Report undertaken by Hemanth Kumar Meda,

Reg. No. 151228 conducted at HALMA India Pvt. Ltd. Submitted in partial

fulfillment of the requirements for the award of the

POST GRADUATE DIPLOMA IN MANAGEMENT

TO

M.S.RAMAIAH INSTITUTE OF MANAGEMENT

Is a record of bonafide internship carried out under my supervision and guidance.

He/She has attended the required guidance sessions held. This report has not

been submitted for the award of any other degree/diploma/fellowship or similar

titles or prizes.

Guide’s Signature:

Name: Prof. Arul Jyothi

Qualification: MBA, M Phil.

STUDENT’S DECLARATION

I hereby declare that the Project Report conducted at HALMA India Pvt. Ltd. Under

the guidance of Prof. Arul Jyothi.

Submitted in Partial fulfillment of the requirements for the

POST GRADUATE DIPLOMA IN MANAGEMENT

TO

M.S.RAMAIAH INSTITUTE OF MANAGEMENT

is my original work and the same has not been submitted for the award of any other

Degree/Diploma/Fellowship or other similar titles or prizes

Signature of the Student

Place: Bangalore HEMANTH KUMAR MEDA

Date: Reg. No.:151228

ACKNOWLEDGEMENT

I extend my special gratitude to our Dean Dr.H.Muralidharan, Academic Head

Prof. V. Narayanan & Programme Head Dr. Savitha Rani Ramachandran for

inspiring me to take up this project and also for their able guidance and support

in completing this internship.

I wish to acknowledge my sincere gratitude and indebtedness to my project

guide Prof. Arul Jyothi of M.S. RAMAIAH INSTITUTE OF MANAGEMENT

Bangalore for his/her valuable guidance and constructive suggestions in the

preparation of project report.

HEMANTH KUMAR MEDA

Reg. No. 151228

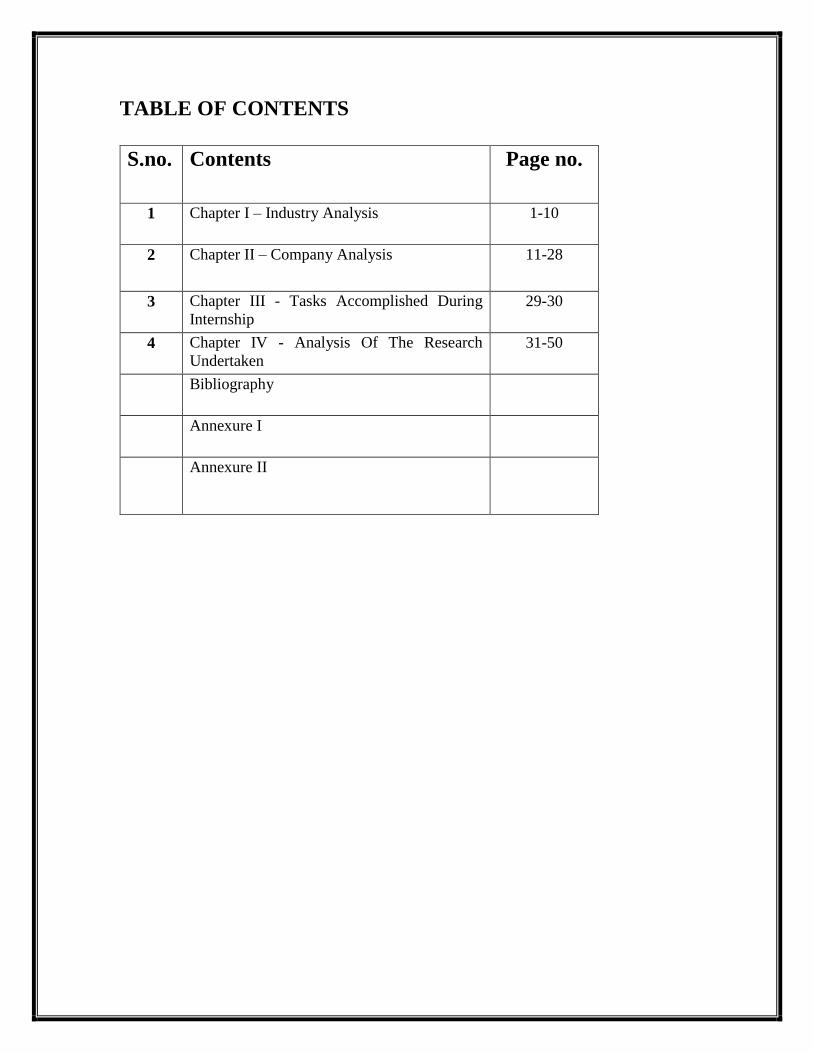

TABLE OF CONTENTS

S.no. Contents Page no.

1 Chapter I – Industry Analysis 1-10

2 Chapter II – Company Analysis

11-28

3 Chapter III - Tasks Accomplished During

Internship

29-30

4 Chapter IV - Analysis Of The Research

Undertaken

31-50

Bibliography

Annexure I

Annexure II

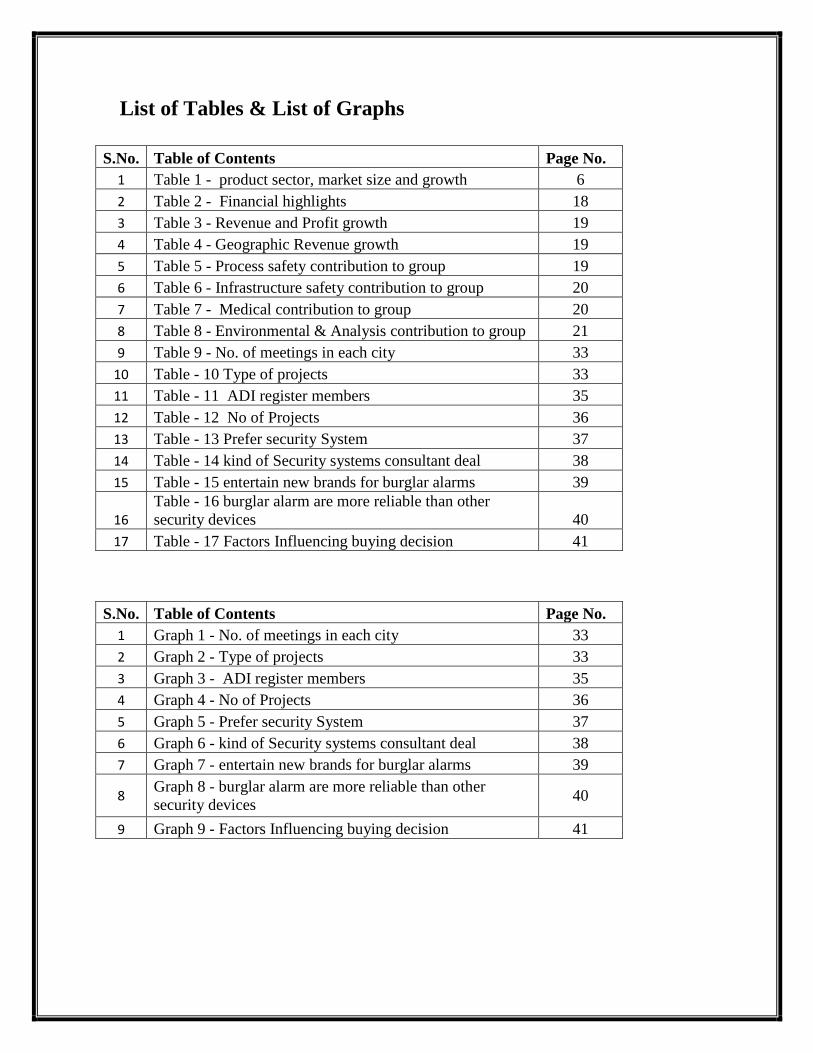

List of Tables & List of Graphs

S.No. Table of Contents Page No.

1 Table 1 - product sector, market size and growth 6

2 Table 2 - Financial highlights 18

3 Table 3 - Revenue and Profit growth 19

4 Table 4 - Geographic Revenue growth 19

5 Table 5 - Process safety contribution to group 19

6 Table 6 - Infrastructure safety contribution to group 20

7 Table 7 - Medical contribution to group 20

8 Table 8 - Environmental & Analysis contribution to group 21

9 Table 9 - No. of meetings in each city 33

10 Table - 10 Type of projects 33

11 Table - 11 ADI register members 35

12 Table - 12 No of Projects 36

13 Table - 13 Prefer security System 37

14 Table - 14 kind of Security systems consultant deal 38

15 Table - 15 entertain new brands for burglar alarms 39

16 Table - 16 burglar alarm are more reliable than other

security devices 40

17 Table - 17 Factors Influencing buying decision 41

S.No. Table of Contents Page No.

1 Graph 1 - No. of meetings in each city 33

2 Graph 2 - Type of projects 33

3 Graph 3 - ADI register members 35

4 Graph 4 - No of Projects 36

5 Graph 5 - Prefer security System 37

6 Graph 6 - kind of Security systems consultant deal 38

7 Graph 7 - entertain new brands for burglar alarms 39

8 Graph 8 - burglar alarm are more reliable than other

security devices 40

9 Graph 9 - Factors Influencing buying decision 41

Executive Summary:

India Electronic Security Industry Potential to 2020 - Growing System Integrators Market with

Real Estate Development in Upcoming Smart Cities" provides a comprehensive analysis of

electronic security market in India. The report focuses on the electronic security products sales and

solutions revenue by system integrators separately in detail. It covers market size and segmentation

of overall electronic security market by verticals (i.e. Video Surveillance - CCTV, Fire Detection,

Access Control, Intrusion Alarm and Specialty devices), by end users (residential and non-

residential - commercial, government, hospitality, transportation, education and others), by

organized and unorganized and by domestic and foreign companies operating in the sector.

Marketing research is about links the producers, customers, and end users. Collected information

used to identify and define marketing opportunities and problems, improve, and evaluate

marketing actions, monitor marketing performance, and improve understanding of marketing as a

process. This research specifies the data required to address these issues, designs the method for

collecting information, manages the data collection process, analyzes the results, and

communicates the findings and their implications.

This study contributes to understanding the architect, security consultant (Integrator) and Builder

and their role in premium residential projects, understand the challenges faced by them, factors

which are affecting the buying behavior of the customer towards intrusion alarm. Texecom under

the umbrella of HALMA group. How it penetrate in the premium residential market.

Chapter 1

Industry Profile

Introduction: India Electronic Security Industry Potential to 2020 - Growing System Integrators

Market with Real Estate Development in Upcoming Smart Cities" provides a comprehensive

analysis of electronic security market in India. The report focuses on the electronic security

products sales and solutions revenue by system integrators separately in detail. It covers market

size and segmentation of overall electronic security market by verticals (i.e. Video Surveillance -

CCTV, Fire Detection, Access Control, Intrusion Alarm and Specialty devices), by end users

(residential and non-residential - commercial, hospitality, transportation, education and others), by

organized and unorganized and by domestic and foreign companies operating in the sector.

Intrusion Prevention Systems (IPS) is a network safety technology that examines network traffic

flow to detect and prevent any malicious intrusions. Growing criminal attacks, as well as in-house

and external unethical practices, are projected to be the key aspects that lift the global intrusion

prevention system market. Growing trend of office & home security system automation is also

projected to raise the market demand. Increasing tablet and Smartphone proliferation has resulted

in increased mobility, which is also projected to boost the industry growth. In addition, increasing

disposable income, in various developed as well as developing nations, is also said to be the major

demand driving factor.

Safety has been a major concern in many sectors such as industrial commercial and residential

areas. Growing implementation of new technology in these sectors is also projected to help boost

the industry growth. Advancements in the semiconductor technology such as Liquid Crystal

Displays (LEDs) and photodiode may also boost the market growth. The advent of cable provider

& prominent telecommunication is also projected to maximize the penetration rate in the near

future.

Integration of various detection systems with intrusion prevention systems has automated various

protective measures, such as notifying police, may also help in the industry growth. Technologies

such as Biometrics provide fingerprints, palm veins, face recognition etc. and integration with such

authentication system may help fulfill the high safety needs of certain industries helping the future

market growth.

An introduction of video-based and an increase in sensitive touch-based intrusion detection

systems are also projected to boost the market demand. Increasing demand across the Banking,

Financial Services & Insurance (BFSI) sector, so as to safeguard the stored valuables, is also said

to be the major factor boosting the market growth.

All these aspects have helped boost the intrusion prevention systems market and it is projected to

grow from $2.7 billion in 2014 to $5.4 billion in 2019 with a CAG rate of 13.3%.

High safety awareness in the developed areas, such North America, may result in extensive growth.

Asia-Pacific region is said to exhibit a high growth due to increased burglary rate and consumer

disposable income. The Middle East & Africa region is also expected to witness tremendous

growth due to increasing investment in infrastructure as well as the development of data center by

major IT companies.

Page 1

1.1 Economic Reforms: The reforms launched in the early 90’s have made India an attractive place for investment. Custom

duties have been lowered, repatriation of profits made liberal and levels of foreign equity raised

considerably, (even 100 percent in case of export oriented industries). Emerging as an across the

board low cost base, the country has been found to be attractive enough to multinationals to

relocate here. More than one hundred of the Fortune 500 companies now have a presence in India.

Guidelines developed by the government in specific sectors such as Telecom, Ports, Airports,

Railways, Roads, Energy and Construction Development have been done with a view to improving

competitiveness of the Indian economy. A Special Economic Zone (SEZ) Act has also been put in

Place to facilitate this process. In 1991, when the reforms were started, India’s Forex reserves were

just US$ 2B. Today they are breaching the US$ 200B mark. The writing on the wall is very clear

- “NOBODY CAN AFFORD NOT TO ENGAGE INDIA!”

The Services Sector: The huge private manned guarding sector, estimated to comprise of more than 5,000 guard

companies employing more than 1 Million people, remains unregulated. It by and large dominates

the protection industry in India. Born in the 60’s this sector started with a handful of large players.

Today, companies like G4S, SIS, Tops, SDB CISCO, Peregrine, and Checkmate, Premier, GI

Security and some others operate through their various regional and city offices to offer protection

services nationwide. However, smaller companies dotting the landscape, in a bid to carve out a

share of the market, resort to cost-cutting, which in turn brings down the quality of service

provided. Large players, on the other hand, provide in-house training facilities, job orientation

programs which reflect in the quality of service they provide. Interestingly, the concept of Central

Monitoring Services (CMS) of alarms has not really caught on in India, as the end-user expects a

private response rather than a police or a state response. As of now, there are less than 5 companies

offering CMS and Response services, the majority of them, including G4S having started such

services in the last couple of years. The reason for the poor growth of this sector is not hard to find.

As Mr. Suresh Sawhney, the Vice President & Country Head of Ingersoll-Rand International

(India) puts it, “Inherently the Indian society is not crime prone. The general population does not

perceive this to be a threat area as also the fact that the education level of the decision makers

about security systems is low. This would change in the next 5 – 10 years.” In a bid to regulate the

manned guarding sector, the Indian Government recently passed the 2005 Private Security

Agencies Regulation Act which, in reality, is yet to take off.

The Systems Sector: The height of terrorism in the 70’s saw the birth of the systems sector with nondescript Bank Alarm

manufacturers and installers trying to outdo each other with substandard, locally-assembled

alarms. Import liberalization in the mid 80’s saw the emergence of System Integrators (SI), with

rapid acceleration in the 90’s. While most systems worth the name were imported, indigenously

assembled systems in those days too were largely import based. Further trade liberalization

resulted in the influx of global players like Honeywell, GE, BOSCH, Tyco, Siemens and HID.

Othe international companies are making their presence felt by appointing distributors, and more

recently, opening their Indian offices and offering sales and after-sales support. Large government

and infrastructure security system projects are beginning to happen as end users realize the

advantages of electronic protection.

Page 2

1.2 The Indian Electronic Protection Systems Industry The Indian market for electronic security equipment is categorized into the electronic sector and

non-electronic sectors and organized and informal sectors. While the total number of players in

the organized electronic sector is around 50, the unorganized sector accounts for about 800 units.

Many Indian companies have collaborated with foreign manufacturers and are marketing foreign

products in India. Security equipment is imported mainly from USA, UK, Germany, Singapore,

Italy, Hong Kong, Israel, Japan, Korea, China, and Taiwan.

1. 3 Some Major Brands in India As far as CCTV equipment is concerned, companies like Bosch, Honeywell, GE, Pelco, Samsung,

Yoko, Meritt Lilin, Hanse, Hi Sharp, CBC, Sanyo, American Dynamics, Vicon and more recently

Sony, Axis, DVTel, and Verint control the major portion of the market. The Access Control market

is dominated by players like HID, Europlex, Cardax, GE (Casi Rusco), Lenel, Syris, Poris,

Pegasus, Elid, IDTEK, Tyco (Sensormatic), JCI (Card Key) Solus, MBux and Kantech. The

relatively much smaller Intrusion detection systems market is catered to by names like Jablotron,

GE (Caddx), Tyco (DSC), Securico, Texecom, Magal, Senstar Stellar and Gallagher. While this

list is purely indicative, there is definitely room for more players to come in.

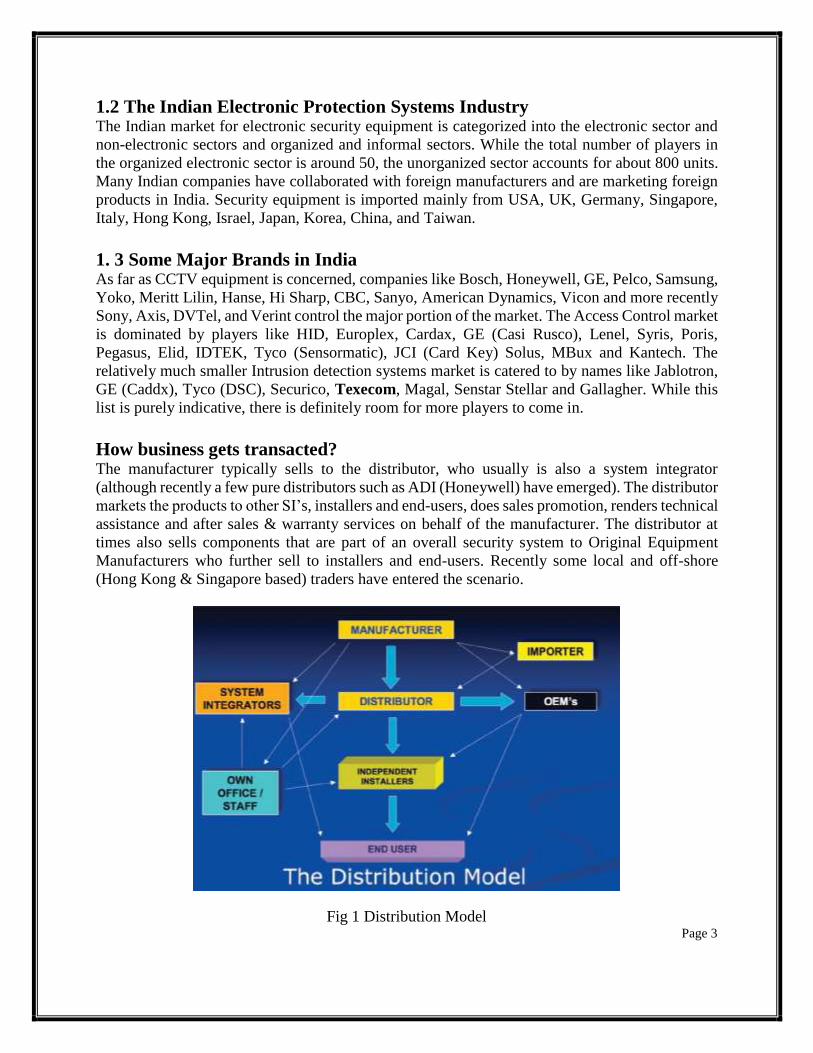

How business gets transacted? The manufacturer typically sells to the distributor, who usually is also a system integrator

(although recently a few pure distributors such as ADI (Honeywell) have emerged). The distributor

markets the products to other SI’s, installers and end-users, does sales promotion, renders technical

assistance and after sales & warranty services on behalf of the manufacturer. The distributor at

times also sells components that are part of an overall security system to Original Equipment

Manufacturers who further sell to installers and end-users. Recently some local and off-shore

(Hong Kong & Singapore based) traders have entered the scenario.

Fig 1 Distribution Model Page 3

These entities typically source, supply and often finance the transaction between the manufacturer

and the distributor. With the market expanding and looking more promising, a more recent trend

has been for manufacturers to establish their wholly owned subsidiary and open local office/s. The

Staff employed by them does product promotion with the System Integrators, Consultants,

Specifies and End-Users. Amongst the multinational brands, perhaps Honeywell has the best

broad-based and structured set-up in India. It has a software development center in Bangalore

serving its global needs, a systems integration unit (Honeywell Building Solutions) in Pune, a

dedicated distribution unit in Gurgaon (selling to big SI’s for large and middle level projects), a

general distribution unit (ADI), located on Gurgaon, Mumbai & Bangalore, selling to small and

medium level independent installers and a manufacturing unit in Gurgaon producing fire alarm

systems.

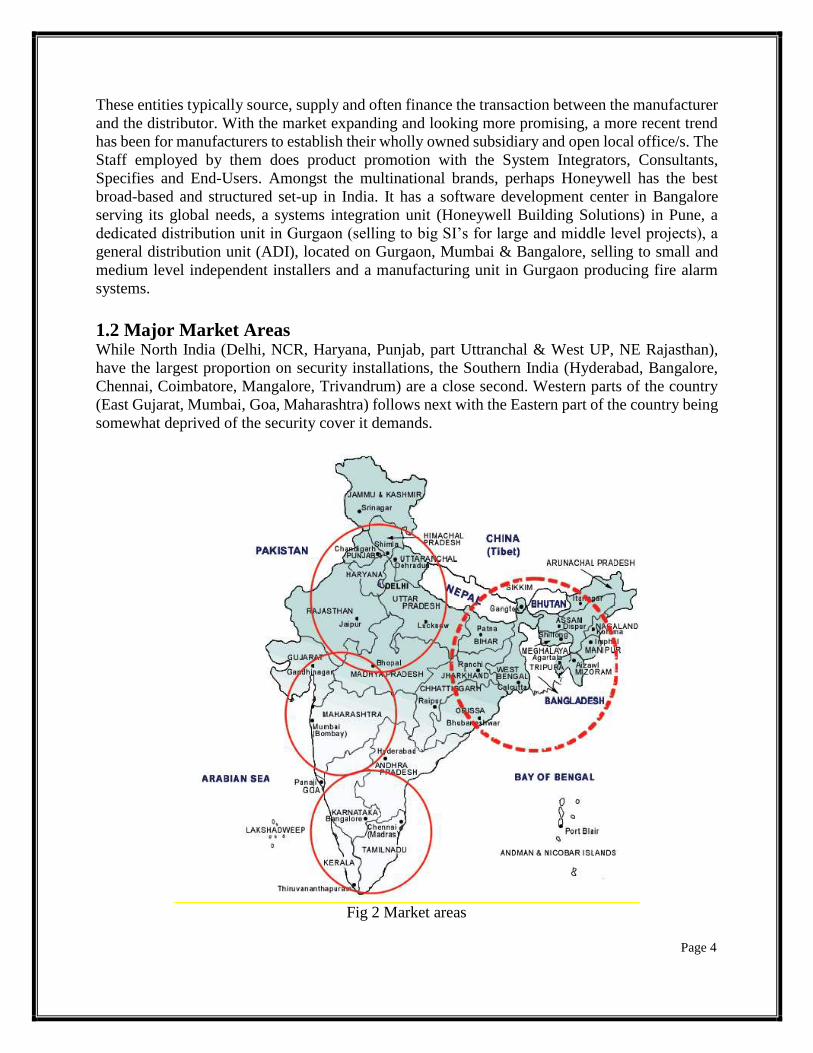

1.2 Major Market Areas While North India (Delhi, NCR, Haryana, Punjab, part Uttranchal & West UP, NE Rajasthan),

have the largest proportion on security installations, the Southern India (Hyderabad, Bangalore,

Chennai, Coimbatore, Mangalore, Trivandrum) are a close second. Western parts of the country

(East Gujarat, Mumbai, Goa, Maharashtra) follows next with the Eastern part of the country being

somewhat deprived of the security cover it demands.

Fig 2 Market areas

Page 4

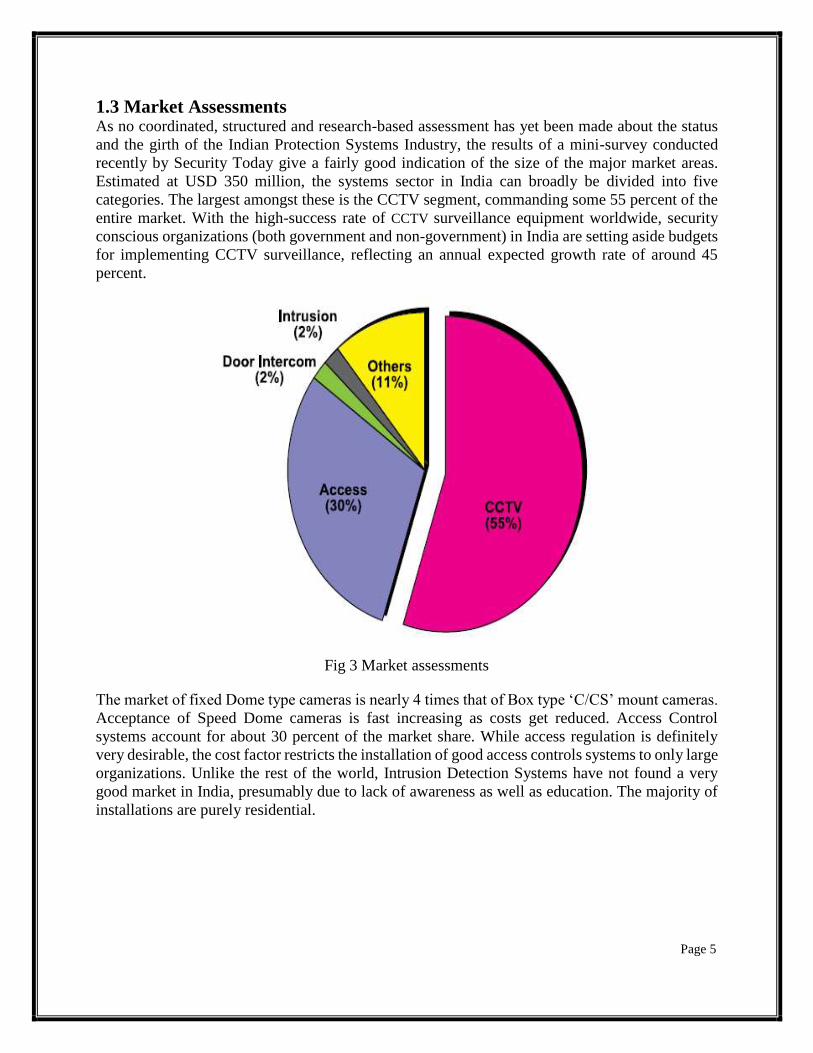

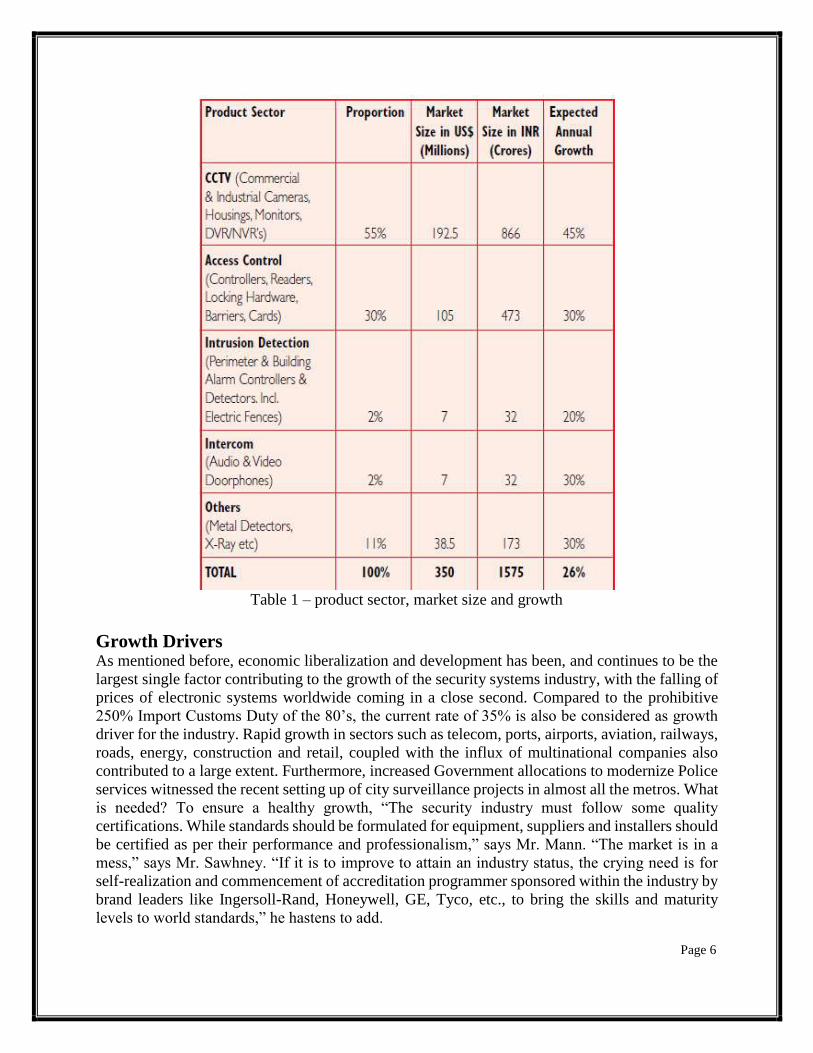

1.3 Market Assessments As no coordinated, structured and research-based assessment has yet been made about the status

and the girth of the Indian Protection Systems Industry, the results of a mini-survey conducted

recently by Security Today give a fairly good indication of the size of the major market areas.

Estimated at USD 350 million, the systems sector in India can broadly be divided into five

categories. The largest amongst these is the CCTV segment, commanding some 55 percent of the

entire market. With the high-success rate of CCTV surveillance equipment worldwide, security

conscious organizations (both government and non-government) in India are setting aside budgets

for implementing CCTV surveillance, reflecting an annual expected growth rate of around 45

percent.

Fig 3 Market assessments

The market of fixed Dome type cameras is nearly 4 times that of Box type ‘C/CS’ mount cameras.

Acceptance of Speed Dome cameras is fast increasing as costs get reduced. Access Control

systems account for about 30 percent of the market share. While access regulation is definitely

very desirable, the cost factor restricts the installation of good access controls systems to only large

organizations. Unlike the rest of the world, Intrusion Detection Systems have not found a very

good market in India, presumably due to lack of awareness as well as education. The majority of

installations are purely residential.

Page 5

Table 1 – product sector, market size and growth

Growth Drivers

As mentioned before, economic liberalization and development has been, and continues to be the

largest single factor contributing to the growth of the security systems industry, with the falling of

prices of electronic systems worldwide coming in a close second. Compared to the prohibitive

250% Import Customs Duty of the 80’s, the current rate of 35% is also be considered as growth

driver for the industry. Rapid growth in sectors such as telecom, ports, airports, aviation, railways,

roads, energy, construction and retail, coupled with the influx of multinational companies also

contributed to a large extent. Furthermore, increased Government allocations to modernize Police

services witnessed the recent setting up of city surveillance projects in almost all the metros. What

is needed? To ensure a healthy growth, “The security industry must follow some quality

certifications. While standards should be formulated for equipment, suppliers and installers should

be certified as per their performance and professionalism,” says Mr. Mann. “The market is in a

mess,” says Mr. Sawhney. “If it is to improve to attain an industry status, the crying need is for

self-realization and commencement of accreditation programmer sponsored within the industry by

brand leaders like Ingersoll-Rand, Honeywell, GE, Tyco, etc., to bring the skills and maturity

levels to world standards,” he hastens to add.

Page 6

Future Trends Trend towards one-stop shopping in the commercial and industrial markets as customers seek

to decrease their systems integration costs

Move from Analog to Digital

IP Based systems gaining ground. Players such as Axis, Sony, Verint, DVTel, Lenel increasing

awareness

Convergence of IT and Physical Security

Arrival of IT network players such as CISCO and D-Link. into the security systems arena

Intelligent Facility Management Systems

Emergence of Security Industry Publications.

More Exhibitions and Seminars

Industry Associations getting professionally active

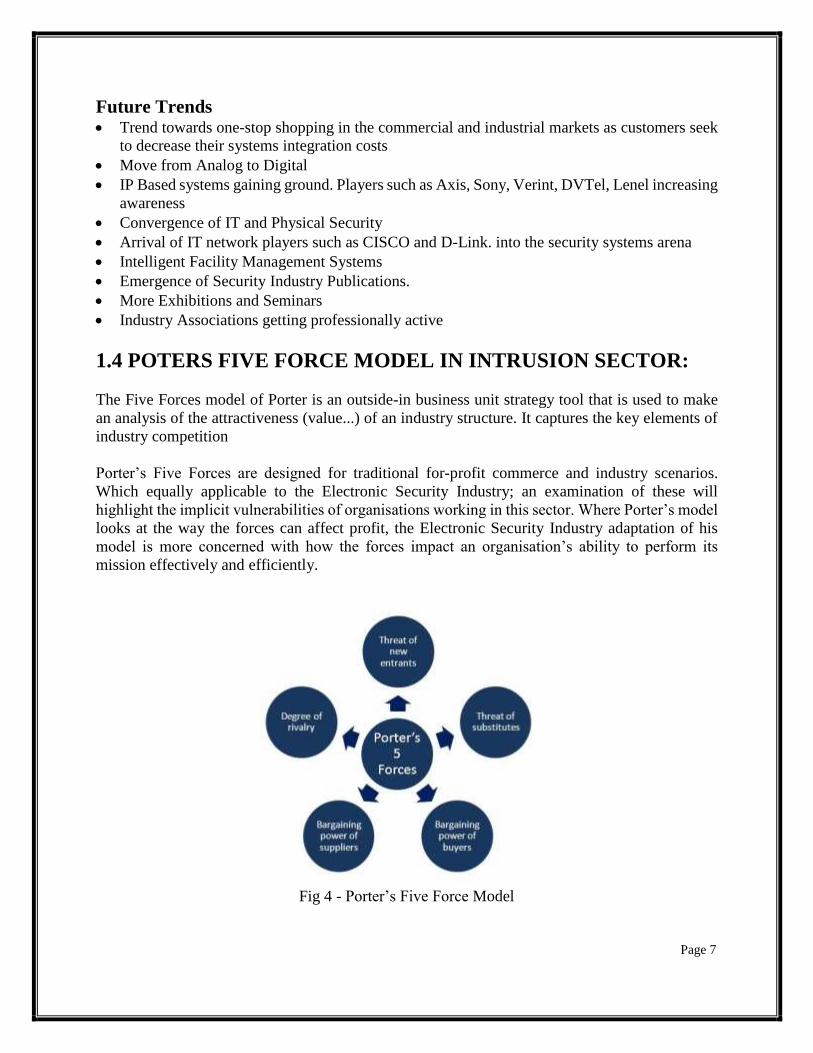

1.4 POTERS FIVE FORCE MODEL IN INTRUSION SECTOR:

The Five Forces model of Porter is an outside-in business unit strategy tool that is used to make

an analysis of the attractiveness (value...) of an industry structure. It captures the key elements of

industry competition

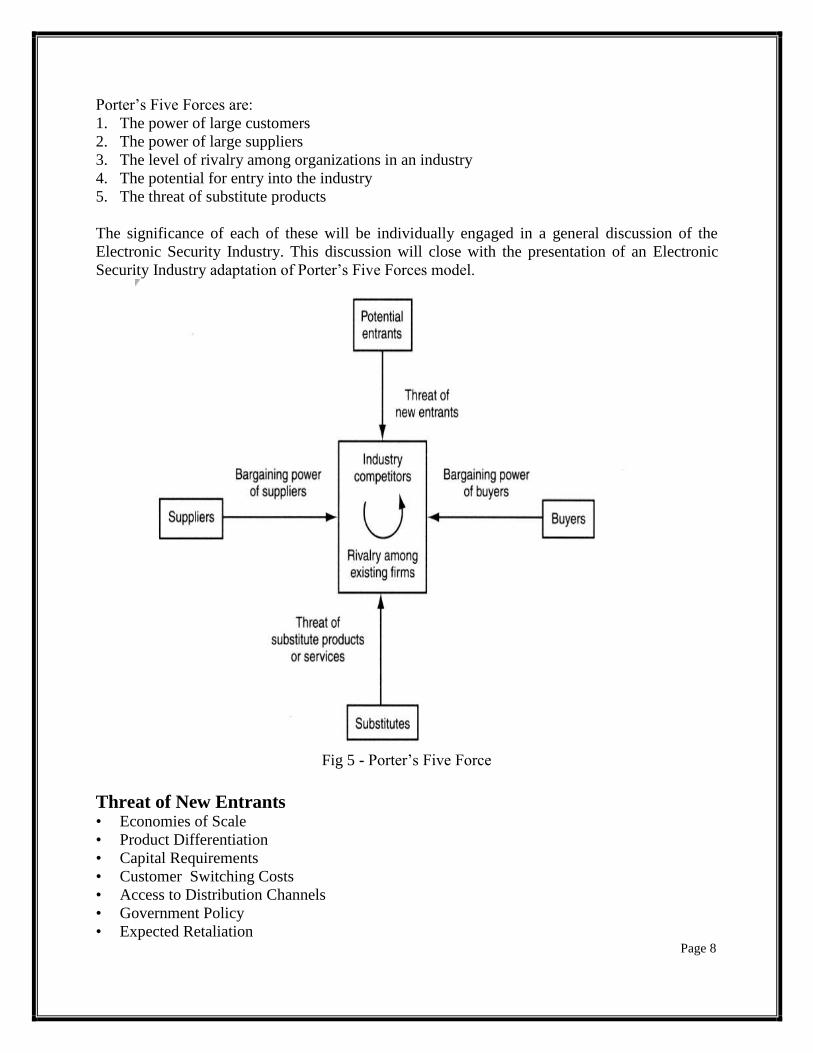

Porter’s Five Forces are designed for traditional for-profit commerce and industry scenarios.

Which equally applicable to the Electronic Security Industry; an examination of these will

highlight the implicit vulnerabilities of organisations working in this sector. Where Porter’s model

looks at the way the forces can affect profit, the Electronic Security Industry adaptation of his

model is more concerned with how the forces impact an organisation’s ability to perform its

mission effectively and efficiently.

Fig 4 - Porter’s Five Force Model

Page 7

Porter’s Five Forces are:

1. The power of large customers

2. The power of large suppliers

3. The level of rivalry among organizations in an industry

4. The potential for entry into the industry

5. The threat of substitute products

The significance of each of these will be individually engaged in a general discussion of the

Electronic Security Industry. This discussion will close with the presentation of an Electronic

Security Industry adaptation of Porter’s Five Forces model.

Fig 5 - Porter’s Five Force

Threat of New Entrants • Economies of Scale

• Product Differentiation

• Capital Requirements

• Customer Switching Costs

• Access to Distribution Channels

• Government Policy

• Expected Retaliation Page 8

Power of Suppliers

Suppliers exert power in the industry by: Threatening to raise, prices or to reduce quality, Powerful

suppliers can squeeze industry profitability if firms are unable to recover cost increases

Suppliers are likely to be powerful if: • Supplier industry is dominated by a few firms

• Suppliers’ products have few substitutes

• Buyer is not an important customer to supplier

• Suppliers’ product is an important input to buyers’ product

• Suppliers’ products are differentiated

• Suppliers’ products have high switching costs

Power of Buyers Buyers compete with the supplying industry by: Bargaining down prices, Forcing higher quality,

playing firms off of each other

Buyer groups are likely to be powerful if: • Buyers are concentrated

• Purchase accounts for a significant fraction of supplier’s sales

• Products are undifferentiated

• Buyers face few switching costs

• Buyer presents a credible threat of backward integration

• Buyer has full information

Threat of Substitute Products

• Products with similar function limit the prices firms can charge

• Keys to evaluate substitute products: Products with improving price/performance tradeoffs

relative to present industry products

Example:

• Electronic security systems in place of security guards

Rivalry among Existing Competitors

Intense rivalry often plays out in the following ways:

• Using price competition

• Staging advertising battles

• Increasing consumer warranties or service

• Making new product introductions

Page 9

Occurs when a firm is pressured or sees an opportunity:

• Price competition often leaves the entire industry worse off

• Advertising battles may increase total industry demand, but may be costly to smaller

competitors

Competitive Advantage • The Competitive Advantage model of Porter learns that competitive strategy is about taking

offensive or defensive action to create a defendable position in an industry, in order to cope

successfully with competitive forces.

• Companies can combat the pressure of the five forces and create competitive advantages.

• There are 2 basics types of Competitive Advantage :

1. Cost leadership (low cost)

2. Differentiation

Strengths of five forces model: • The model is strong tool for competitive analysis at industry level.

• It provides useful input for performing a SWOT analysis.

Page 10

Chapter II

Company Profile

2.1 Introduction:

Halma is a leading international safety, health and environmental group. Its wholly owned but

independently run companies offer advanced technology in specialised areas. These companies

make products for:

Fig 6

Halma companies make products that provide innovative solutions for many of the key problems

facing the world today. We are a remarkable success story. Without realising it, you will encounter

our products daily. We have nearly 50 businesses in 23 countries and major operations in Europe,

the USA and Asia.

At a Glance A FTSE 250 company quoted on the London Stock Exchange

Founded in 1894

Headquarters near London, United Kingdom

Around 5600 employees worldwide

Customers in 160 countries

Revenues of over £807.8 million in 2015/16

≥5% dividend growth for 35+ years

History:

Halma’s origins began in Asia in 1894. As The Nahalma Tea Estate Company Limited, it operated

in Ceylon (renamed Sri Lanka in 1972). The company later switched to rubber production and in

1937 became the Nahalma Rubber Estate Company Limited.

During the 1950s the Sri-Lankan government nationalized many of the island’s businesses,

including the rubber industry. In 1956 the Nahalma Rubber Estate Company Limited became

Halma Investments Limited. The company ended its connections with rubber and its role changed

to an investment management and industrial holding company.

Page 11

Halma was listed on the London Stock Exchange in January 1972 and became a publicly-traded

company. A series of acquisitions was made of mechanical, electrical and electronic engineering

companies and successful management generated strong organic growth. This created the basis for

the international manufacturing group that Halma is today. The company changed its name to

Halma Limited in 1973 and registered as a public limited company in 1981, becoming Halma plc.

Halma has grown to be an established FTSE 250 business and currently comprises nearly 50

subsidiary companies operating worldwide. Today, Halma’s technology centres on sensors, its

markets are primarily the protection of human and capital assets, and the Group continues to grow

through organic expansion and acquisition.

Halma Business :

Halma’s business is about protecting life and improving the quality of life for people worldwide.

Halma products provide innovative solutions for many of the key problems facing the world today.

Halma’s four specialist business sectors are:

Process safety Products which protect assets and people at work. Specialized interlocks which safely control

critical processes. Instruments which detect flammable and hazardous gases. Explosion protection

and corrosion monitoring products.

Infrastructure safety Products which detect hazards to protect assets and people in public spaces and commercial

buildings. Fire and smoke detectors, fire detection systems, security sensors and audible/visual

warning devices. Sensors used on automatic doors and elevators in buildings and transportation.

Medical Products used to improve personal and public health. Devices used to assess eye health, assist with

eye surgery and primary care applications. Fluidic components such as pumps, probes, valves and

connectors used by medical diagnostic OEMs.

Environmental & Analysis Products and technologies for analysis in safety, life sciences and environmental markets. Market-

leading opto-electronic technology and gas conditioning products. Products to monitor water

networks, UV technology for disinfecting water, and water quality testing products.

These four operating sectors offer

relatively non-cyclical markets

sustained growth underpinned by strong, resilient drivers

significant barriers to entry for potential competitors

Page 12

2.2 Organization Structure: Halma has a highly decentralised structure which delivers real competitive advantage. Halma

places its operational resources close to the customers through locally-managed, autonomous

businesses.

Halma Operating companies Operating companies have their own board of directors and are given considerable freedom for

entrepreneurial action. Research and development, manufacturing, sales and marketing, and

human resources are all managed at operating company level.

Halma subsidiary boards are empowered to make timely decisions in the best interests of their

business. With an intimate knowledge of their market dynamics and customer needs they are best

placed to make local resource allocation decisions swiftly in response to market changes.

Halma Sectors

Halma’s subsidiary companies are grouped into four operating Sectors: Process Safety,

Infrastructure Safety, Medical and Environmental & Analysis. Each sector is an autonomous

business unit responsible for its own growth organically and by acquisition.

Sectors are managed by Sector Chief Executives and Sector Vice Presidents who are Chairmen of

the subsidiaries. Their primary role is to provide insight, inspiration and leadership for the local

management boards. Sector Chief Executives understand the market needs of their companies and

contribute broadly to their strategies. They set objectives and targets, measure performance and

incentivise their managements.

Sector Chief Executives are also responsible for acquiring new businesses and the recruitment of

high calibre managers to run our companies. Sector Chief Executives are members of the Halma

Executive Board and through regular interaction between Executive Board members, common

challenges and opportunities are identified.

Head office A small head office team focuses on corporate strategy and maintains an overall framework of

financial planning, reporting and control. Head office also provides a limited range of central

financial services, including treasury, pensions, insurances and share plans, and leads Group

strategic initiatives such as driving improvements in sales processes, innovation and people

development.

Values:

Halma values help to ensure a consistent set of standards and behaviours throughout the Group.

This is particularly important given the Group’s decentralised structure.

Page 13

Halma’s core values are: Achievement

Innovation

Empowerment

Customer Satisfaction

Halma employees are required to act fairly in their dealings with fellow employees, customers,

suppliers and business partners; these principles are included within our Code of Conduct which

has been signed by each Group employee.

Halma performance culture is underpinned by the alignment of reward and incentive plans.

Acquisitions: Halma acquires companies in its existing business sectors that are successful, growing and

profitable.

Organic growth funds Halma acquisitions. Acquisitions add value to Halma’s portfolio of

businesses through new intellectual assets, new management talent and a wider technological and

geographic footprint.

Halma’s acquisition strategy is to buy businesses and intellectual assets that:

extend existing activities

fit with our entrepreneurial culture

deliver strong financial performance

Halma’s acquisitions are highly targeted. Halma usually acquire companies operating in markets

Halma are familiar with, or they may be in closely allied sectors which it understands. Halma

acquires both stand-alone businesses and ‘bolt-ons’. Halma have financial resources to invest in

acquisitions to accelerate growth.

After acquisition, companies usually operate independently under their local management within

Halma decentralized management structure. They immediately benefit from access to the

resources of a larger multinational parent. Entrepreneurs often remain and manage their business

after acquisition.

Halma CSR:

Commitment to Corporate Responsibility Halma companies are involved in the manufacture of a wide range of products that protect and

improve the quality of life for people worldwide. This section of the website focuses on areas of

progress and our performance for all areas of corporate responsibility which are considered to be

material by our stakeholders and are also important to the success of our Group’s business. Halma

has developed meaningful key performance indicators (KPIs) that reflect the importance the Group

places on corporate responsibility and enable the Board to monitor the Group’s progress in meeting

its objectives and responsibilities in these areas. Page 14

These areas of emphasis include health and safety, employee engagement and development,

human rights and ethics, corporate responsibility and sustainability.

Halma has been a member of the FTSE4Good UK index since its establishment in July 2001.

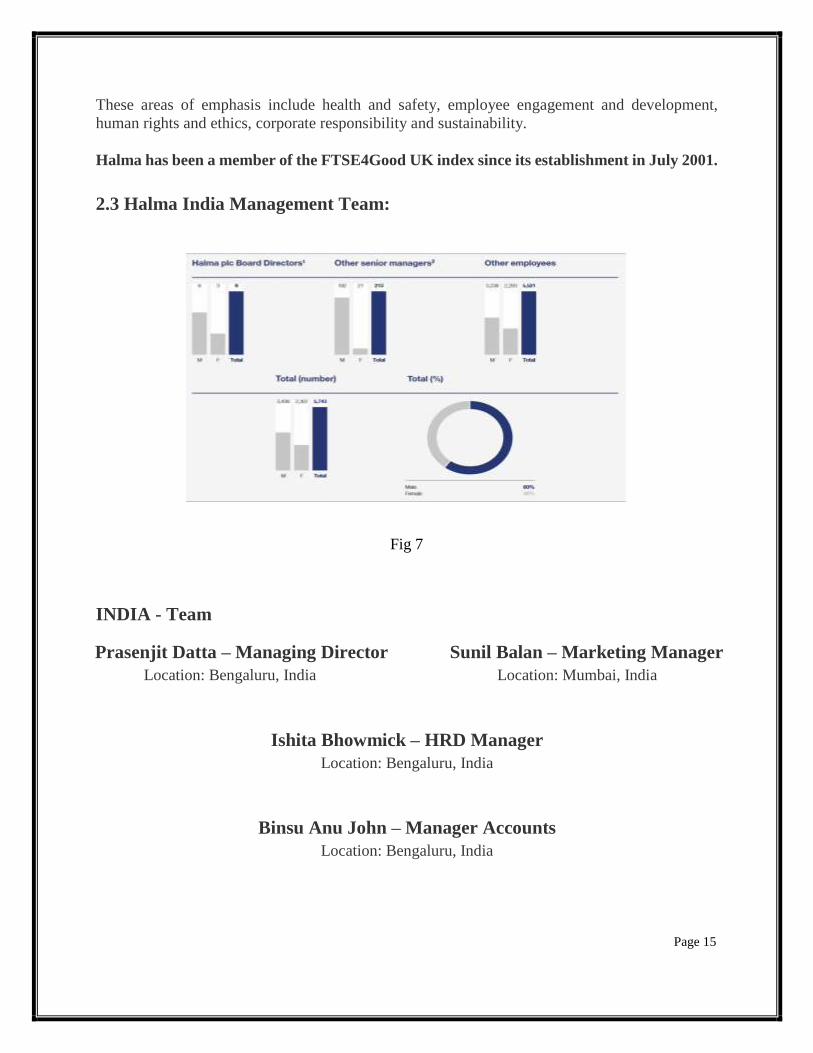

2.3 Halma India Management Team:

Fig 7

INDIA - Team

Prasenjit Datta – Managing Director

Location: Bengaluru, India

Sunil Balan – Marketing Manager

Location: Mumbai, India

Ishita Bhowmick – HRD Manager

Location: Bengaluru, India

Binsu Anu John – Manager Accounts

Location: Bengaluru, India

Page 15

Business model and strategy:

Creating long-term sustainable value

Business model objective Our objective is to double every five years. We aim to achieve this through a mix of acquisitions

and organic growth. Return on Sales in excess of 18% and Return on Capital Employed over 45%

ensure that cash generation is strong enough to sustain investment for growth and increase

dividends without the need for high levels of external funding.

What resources our business model relies on

Financial - Our strongly cash generative businesses support investment for growth

Product Innovation - Developing and delivering the right products across our markets

Human Capital - Investing in our people to enable talent leadership throughout our businesses

Intellectual Assets - Building competitive advantage through investment in R&D and new

product development

Relationships - Empowering our businesses to work closely with customers, suppliers and each

other

Sustainability - Minimising the impact that our operations have on the environment

What we do

Through innovation and acquisition, we have a portfolio of market-leading companies within our

four sectors:

Process Safety

Infrastructure Safety

Medical

Environmental & Analysis

Demand for our products is underpinned by resilient, long-term growth drivers:

Increasing health and safety regulation

Increasing demand for healthcare

Increasing demand for life-critical resources (such as energy and water)

Competitive advantage Each business builds strong application knowledge and technology by focusing on its specific

market niche where there are often barriers to entry. We place our operational resources close to

our customers through autonomous locally managed businesses. We reinvest cash into acquiring

high performance businesses in, or close to, our existing markets.

Page 16

A sustainable strategy driving value creation

Fig 8

Our strategy To acquire and grow businesses in relatively non-cyclical, specialised global niche markets. The

technology and application know-how in each company delivers strong competitive advantage to

sustain growth and high returns.

Our chosen markets have significant barriers to entry. Demand for our products is underpinned by

resilient, long-term growth drivers.

We place our operational resources close to our customers through autonomous locally managed

businesses.

We reinvest cash into acquiring high performance businesses in, or close to, our existing markets.

Our four operating sectors, Process Safety, Infrastructure Safety, Medical and Environmental &

Analysis were chosen because they offer markets where sustained growth is underpinned by

strong, resilient drivers.

Many of our markets are highly regulated. Halma products frequently satisfy demand created by

health, safety and environmental legislation. Regulation is a powerful driver which stimulates non-

discretionary purchasing.

When we acquire, we only invest in companies exposed to relatively non-cyclical markets, with

strong growth drivers, and where high barriers to entry deter new market entrants. More about

acquisitions.

Page 17

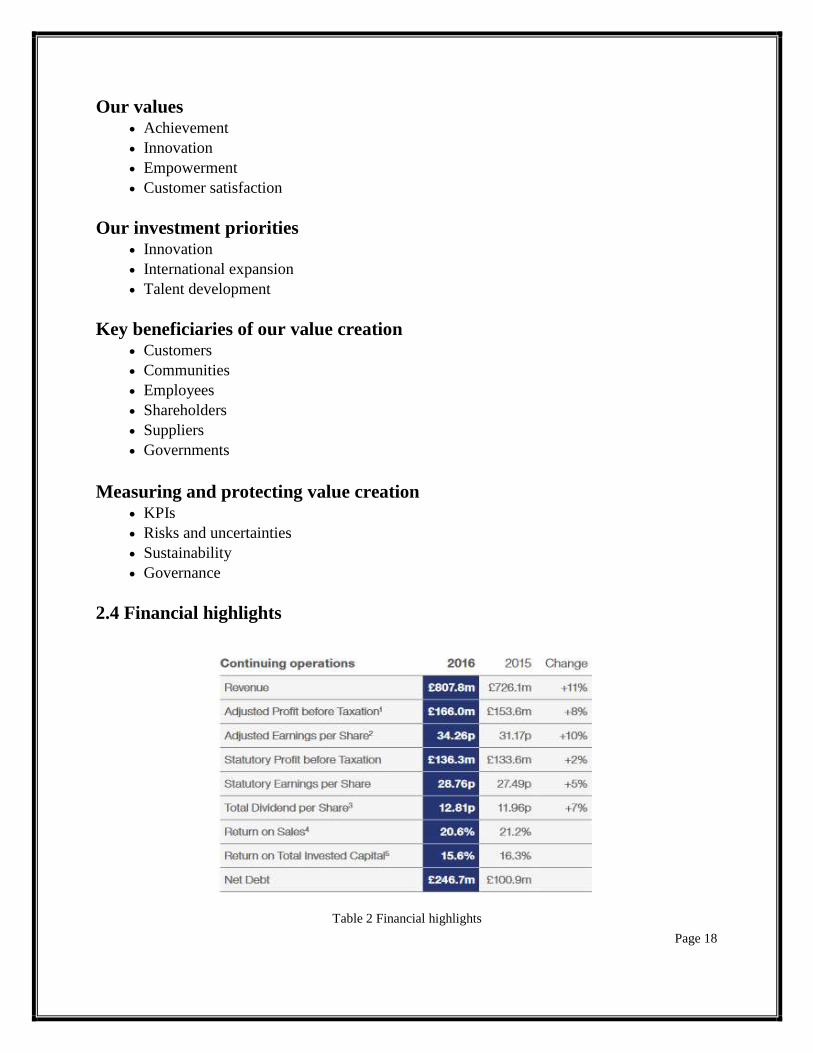

Our values Achievement

Innovation

Empowerment

Customer satisfaction

Our investment priorities Innovation

International expansion

Talent development

Key beneficiaries of our value creation Customers

Communities

Employees

Shareholders

Suppliers

Governments

Measuring and protecting value creation KPIs

Risks and uncertainties

Sustainability

Governance

2.4 Financial highlights

Table 2 Financial highlights

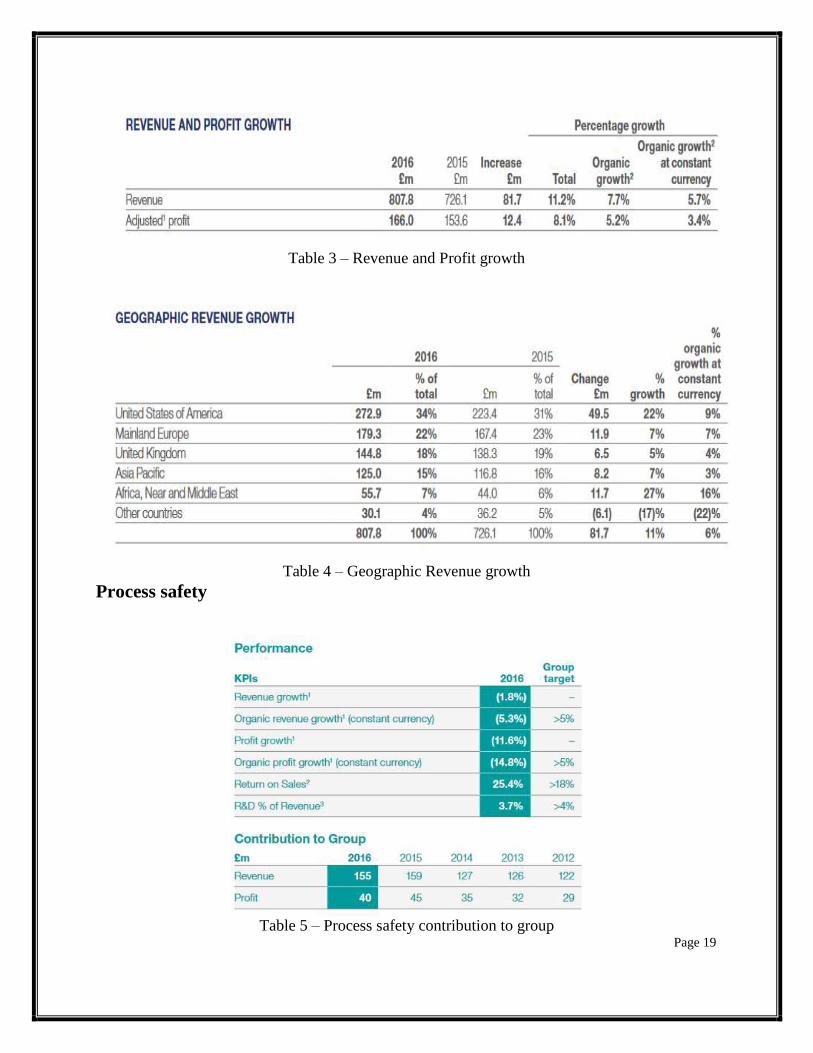

Page 18

Table 3 – Revenue and Profit growth

Table 4 – Geographic Revenue growth

Process safety

Table 5 – Process safety contribution to group

Page 19

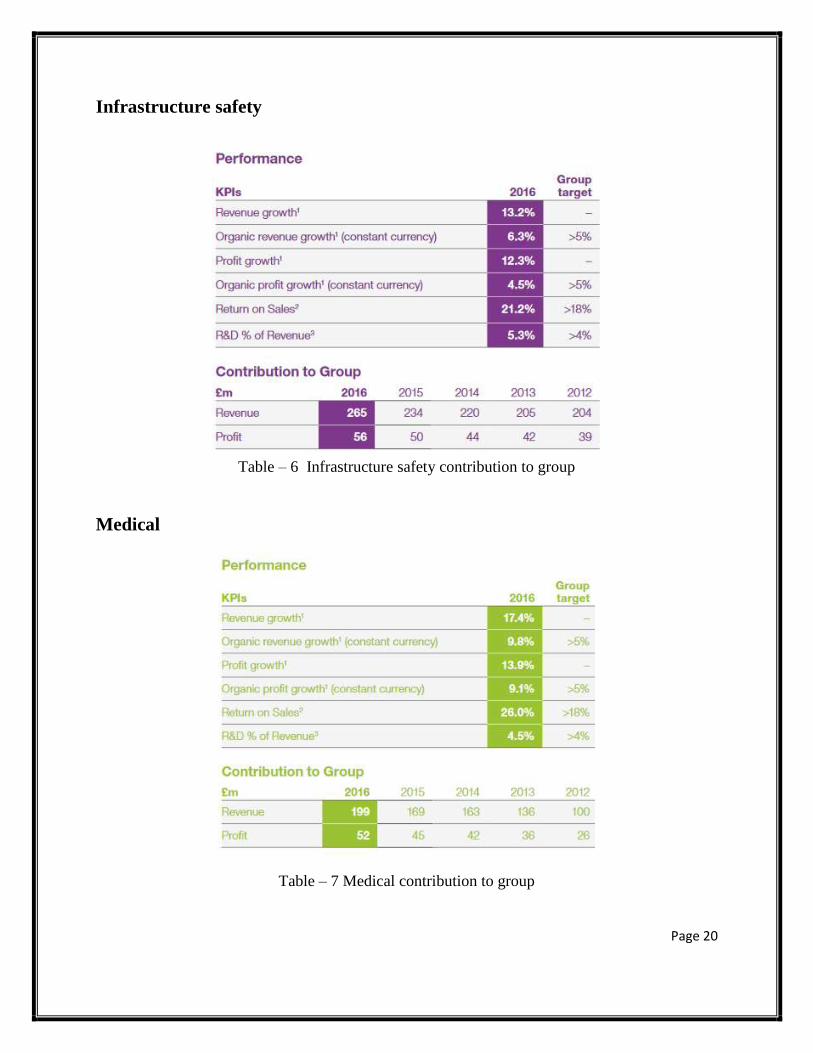

Infrastructure safety

Table – 6 Infrastructure safety contribution to group

Medical

Table – 7 Medical contribution to group

Page 20

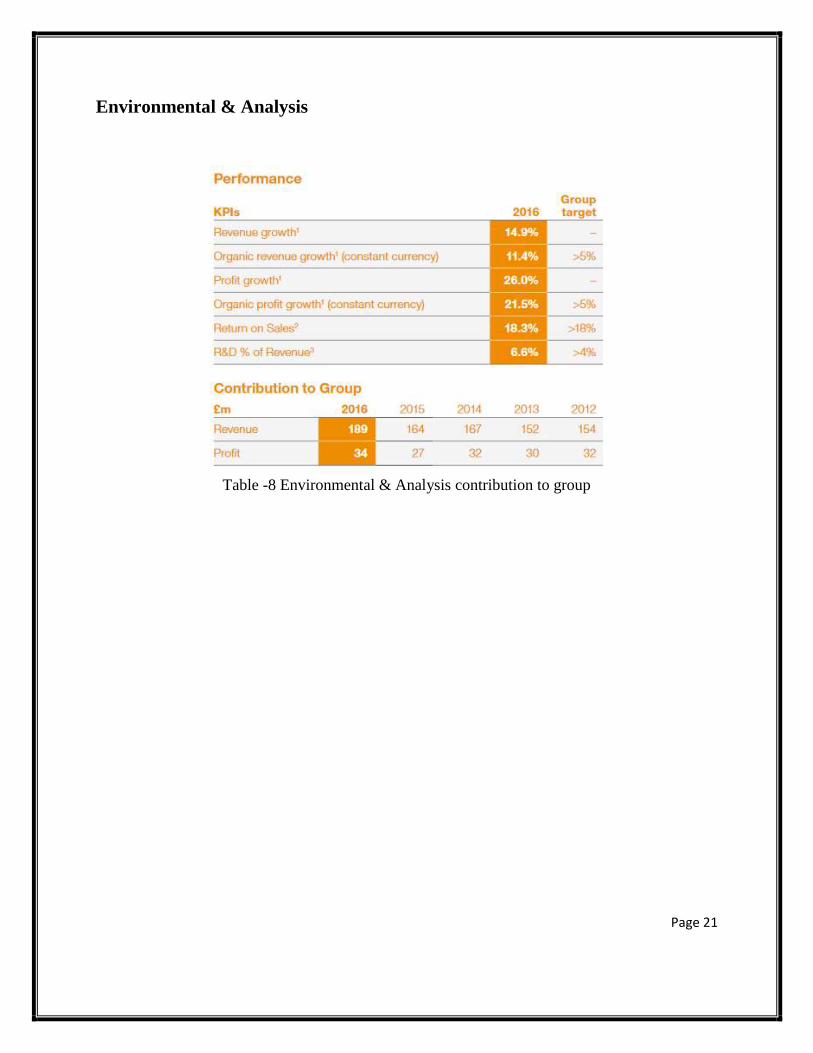

Environmental & Analysis

Table -8 Environmental & Analysis contribution to group

Page 21

2.5 Texecom

Texecom is Europe’s largest independent security alarm specialist providing bespoke design

solutions that protect people and property throughout the world.

Established in 1986, Texecom’s award-winning products cover every aspect of external and

internal security requirements.

Fig 9

Award Winning Products

Texecom’s extensive portfolio of electronic security products includes a full range of motion

detectors, control panels, perimeter protection devices, fire detectors and external sounders.

Texecom has recently launched a new ground breaking wireless technology, Ricochet mesh

networking, to universal acclaim.

Page 22

Fig 10

With a passion and a focus on performance, simplicity of operation, style and reliability, product

requirements are engineered into leading edge designs, outstanding in both quality and innovation.

Internationally Certified

Texecom is firmly committed to providing products that exceed the demands of international

standards. Texecom prides itself on producing innovative products, designed to exceed

expectations.

UK Manufacturing for Complete Control

Complete control for all aspects of development is ensured through design, manufacture and

thorough testing of all products in state-of-the-art UK facilities.

Texecom Product Range:

Wired and Wireless – Intruder Alarm Panels

GSM/IP/PSTN Communicators

Magnetic Contacts. Glass Break Detectors, Motion Sensors

External Sounders

Smoke Detectors , Panic Buttons

Central Monitoring & Diagnostics Software

Smartphone Apps (IOS & Android)

Page 23

Fig 11

Key Product Features:

Some of the Key Features of Texecom’s Range of Wired/Wireless Intruder Alarms

Advanced Control Panel Hardware for a variety of Application – 8 Zone – 640 Zone

Control Panels

Aesthetically Superior Metal and Polymer Flush and Surface Mount Keypads

Complete Control of the Security System through Mobile Apps on Android and IOS

platform

Variety of Communicators – PSTN/GSM/GPRS for faster and reliable alarm

communication

Dedicated Software for Installation, Commissioning and Maintenance

Award Winning Wireless Mesh Based technology – Ricochet in Wireless Intrusion alarm

systems

Page 24

Fig 12

Application Areas: Commercial

Banks , ATM’s,Retail Shops, Jewellery Stores, Museums

Residential:

Independent Homes, Villas, Apartments

Industrial Airports and Large Industrial Plants

Certifications: Compiance with the PD6662:2010 update.

EN Grade 2 and Grade 3 certified products

Texecom in India

Texecom products are being sold in India through various distributors since early 2000’s. Texecom

primary presence is in Mumbai and Delhi with Sales Representatives, Technical Support and

Research and Development team.

Texecom Alarm panels and accessories have been installed in thousands of locations across India

and are saving lives and property everyday

Texecom is committed to providing quality solutions in Intruder Alarm Detection for the Indian

market and will continue to invest and expand its resources and presence across India.

Page 25

2.6 Marketing

Push Strategy The term 'push strategy' describes the work a manufacturer of a product needs to perform to get

the product to the customer. This may involve setting up distribution channels and persuading

middle men and retailers to stock your product. This term now broadly encompasses most direct

promotional techniques such as encouraging retailers to stock your product, designing point of sale

materials or even selling face to face. New businesses often adopt a push strategy for their products

in order to generate exposure and a retail channel. Once your brand has been established, this can

be integrated with a pull strategy.

Distribution Channels

Company: ADI ADI has a vast distribution network and over 200 branches across the world. With our global

relationships and 30 locations across India, ADI provides a long-term trading assurance to its

customers.

ADI is dedicated to helping your business grow, and as the leading global distributor for

fire, safety & security products we have the expertise and resources to make it happen.

Product Range

Fig. 13

Services Offered

Fig. 14 Page 26

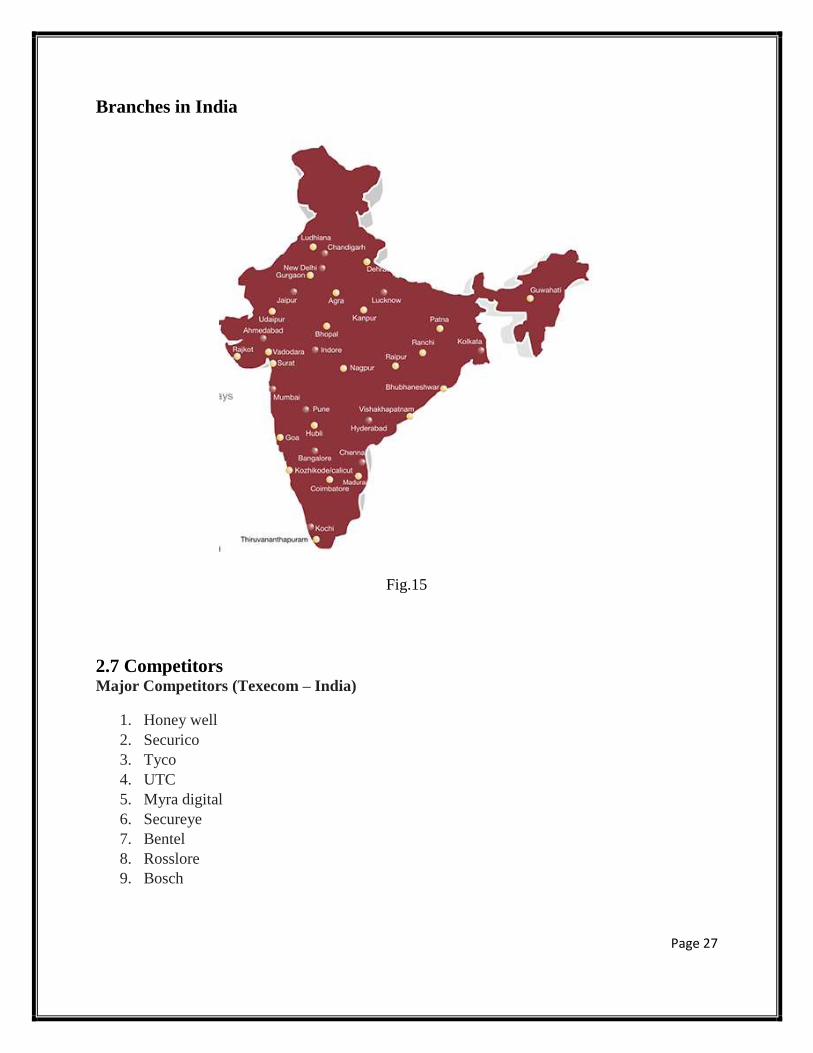

Branches in India

Fig.15

2.7 Competitors Major Competitors (Texecom – India)

1. Honey well

2. Securico

3. Tyco

4. UTC

5. Myra digital

6. Secureye

7. Bentel

8. Rosslore

9. Bosch

Page 27

Other brands:

1. DSC

2. LifeSos

3. Co- Max

4. Godrej

5. Legrand

2.8 SWOT Analysis:

Strengths High growth rate

Barriers of market entry

Weaknesses

Competitive market

Small business units

Tax structure

Productivity

Opportunities

Growth rates and profitability

Venture capital

Global markets

New acquisitions

Growing demand

Threats

Technological problems

Price changes

Growing competition and lower profitability

Increasing costs

Financial capacity

External business risks

Rising cost of raw materials

Page 28

Chapter III

Tasks Accomplished During

Internship

3.1 Roles and Responsibilities

The internship tenure at Halma India Pvt. Ltd. was chalked out for 8 weeks (4th April 2016 – 7th

June 2016). Following were the certain roles and responsibilities I had carried out during the

Internship:

To understand Security Consultants, Architect, and Builders for Texecom.

The project was about meeting the Security Consultant, Architect and Builders across India

(South & West Zone) and understanding the market penetration for Texecom in the Burglar

alarm for the premium residential projects.

Understanding the set of activities Texecom should do to gain confidence of the

infrastructure safety consultants.

Understanding what is important for the security consultants, architect and builders to get

business from the clients and also the challenges faced by them in this process.

Provide the competitive research and analysis.

Help with collected quantitative and qualitative data from the client.

Prepare a weekly report for weekly meetings.

Cold calling.

3.2 Description of Task Handled.

The project was concentrate south & west zone of India majorly concentrating on nine

different cities- Bangalore, Cochin, Coimbatore, Salem, Hyderabad, Vijayawada, Baroda,

Mumbai & Pune

Accounting mapping.

The project involved meeting Security consultant (Integrators), Architect and Builders.

Data was collected in the form of pre-defined questionnaire and personal interviews.

Out of the 53 days 40 days were spent on field for collection of data from various integrators,

architect and Builders across various cities.

Feedback collected from the existing client.

Understand the working function of the ADI Global distribution channel.

Understand the challenges face by architect, integrators and builders.

Analyze the factors contributions towards buying pattern of the intrusion market.

Page 29

3.3 Contribution to the Organization

The following recommendations were given to the organization based on the findings of the

project:-

The organization has to make the Integrators, Architect and Builders aware about

Texecom.

Research leads to account mapping of Texecom.

The company has to participate in seminars and conferences and trade shows

Analysis of the data which will helpful to take the business decisions

The company has to create tech support with sound technical knowledge person across the

nation.

Page 30

Chapter IV

Analysis of the Research

Undertaken

4.1 Introduction:

Marketing research is the process that links the producers, customers, and end users to the marketer

through information. Collected information used to identify and define marketing opportunities

and problems, improve, and evaluate marketing actions, monitor marketing performance, and

improve understanding of marketing as a process. Marketing research specifies the data required

to address these issues, designs the method for collecting information, manages the data collection

process, analyzes the results, and communicates the findings and their implications.

It is the systematic gathering, recording, and analysis of quantitative and qualitative data about

issues relating to marketing products and services. The objective of marketing research is to

identify and assess how changing elements of the marketing mix impacts customer behavior, in

that market research is concerned specifically with markets, while marketing research is concerned

specifically about marketing processes.

Marketing research is divided into two types

Target market:

1. Consumer marketing research, and

2. Business-to-business (B2B) marketing research

Methodological approach:

Qualitative marketing research, and

Quantitative marketing research

Consumer marketing research is a form of applied sociology that concentrates on understanding

the preferences, attitudes, and behaviors of consumers in a market-based economy, and it aims to

understand the effects and comparative success of marketing campaigns.

Thus, marketing research may also be described as the systematic and objective identification,

collection, analysis, and dissemination of information for the purpose of assisting management in

decision making related to the identification and solution of problems and opportunities in

marketing.

4.2 Research Design Statement of the problem: Understand the architect and security consultant and their role in premium residential market for

Texecom Ltd

Objective: 1. To study and understand the security consultants, architect and builders.

2. To understand and analyze challenges faced by the architect, builder and security

consultants while designing anti-intrusion system for the projects.

3. To identify the functionality with respect to client( architect and Security consultant)

4. To determine how sales happen through architect, builder and security consultant.

Page 31

Scope of Study:

The scope of the project is to understand the security consultant (Integrators), Architect and

Builders and their role in the premium residential market, in South and west zone of India. The

project mainly focus on the premium residential market penetration and suitably position itself on

customer. This project undergone for the period of 2 months. The geographical location chosen

for this project is south and west zone of India.

Limitation:

Place : India (West & South Zone) Period : 2 Months Focus area : Premium Buildings/villas (Anti-intrusion/ burglar alarms)

Respondents : Integrators, Architect and Builders

4.3 Methodology:

Research Method – Empirical Research

Empirical research is been used to identify the need of Security consultant, Architect and Builder

in Premium residential market for burglar alarm system.

1. Exploratory research – From the data collected we gained knowledge about the various

buying behaviors of burglar alarm through Security consultant, Architect and Builder.

2. Descriptive research – The data collected through structured questionnaire gives the

information about the factors which affected decision making when plan for security

accepts of a premium residential projects.

Target population : Security consultant (Integrators), Architect and Builders.

Sample units : Residential projects services provider from India (South and West Zone).

Sampling technique : Non-probability sampling (convenience sampling)

Sample size : 50

Place : India (West & South Zone)

Period : 2 Months

Focus area : Premium residential projects

Data collection:

Primary data – the primary data has been collected through questionnaire.

Page 32

4.4 Analysis of Data

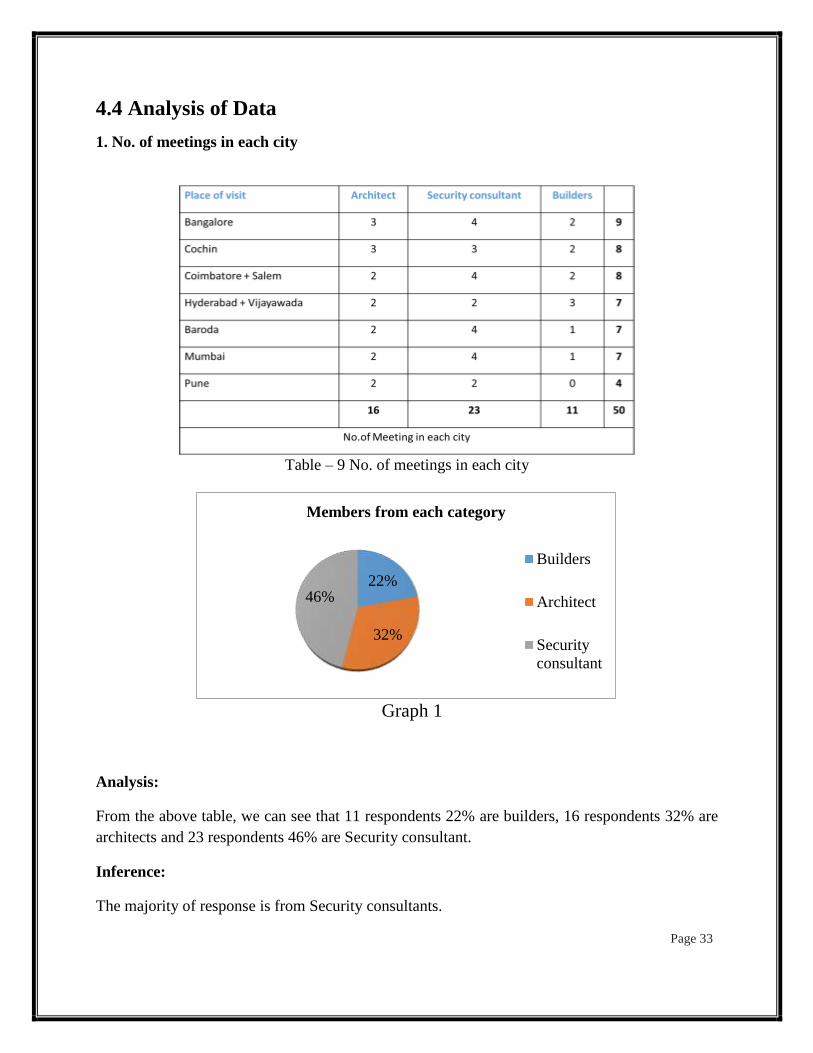

1. No. of meetings in each city

Table – 9 No. of meetings in each city

Graph 1

Analysis:

From the above table, we can see that 11 respondents 22% are builders, 16 respondents 32% are

architects and 23 respondents 46% are Security consultant.

Inference:

The majority of response is from Security consultants.

Page 33

22%

32%

46%

Members from each category

Builders

Architect

Security

consultant

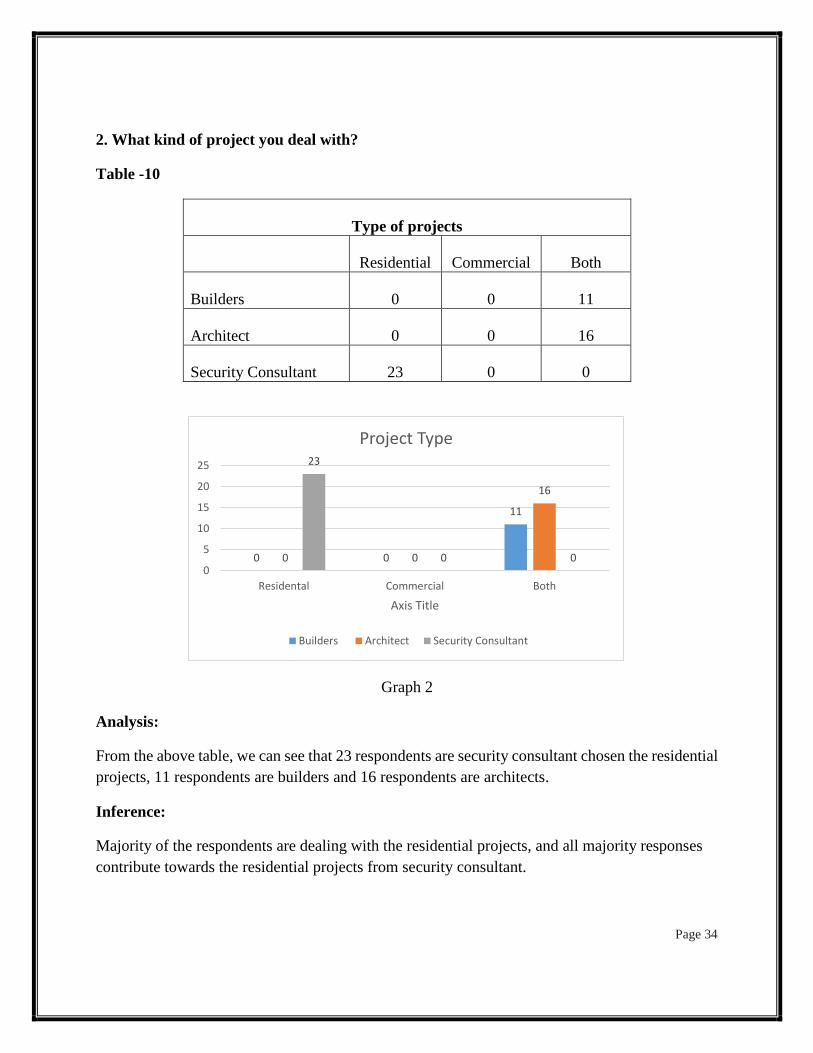

2. What kind of project you deal with?

Table -10

Type of projects

Residential Commercial Both

Builders 0 0 11

Architect 0 0 16

Security Consultant 23 0 0

Graph 2

Analysis:

From the above table, we can see that 23 respondents are security consultant chosen the residential

projects, 11 respondents are builders and 16 respondents are architects.

Inference:

Majority of the respondents are dealing with the residential projects, and all majority responses

contribute towards the residential projects from security consultant.

Page 34

0 0

11

0 0

16

23

0 00

5

10

15

20

25

Residental Commercial Both

Axis Title

Project Type

Builders Architect Security Consultant

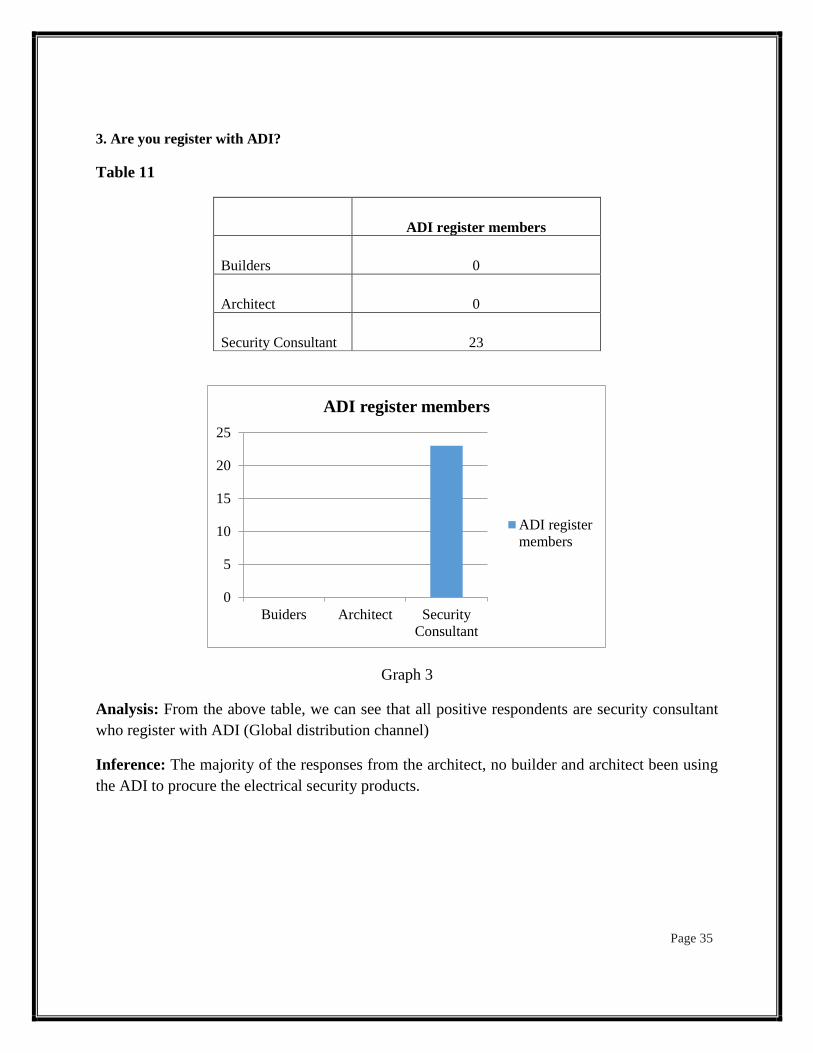

3. Are you register with ADI?

Table 11

ADI register members

Builders 0

Architect 0

Security Consultant 23

Graph 3

Analysis: From the above table, we can see that all positive respondents are security consultant

who register with ADI (Global distribution channel)

Inference: The majority of the responses from the architect, no builder and architect been using

the ADI to procure the electrical security products.

Page 35

0

5

10

15

20

25

Buiders Architect Security

Consultant

ADI register members

ADI register

members

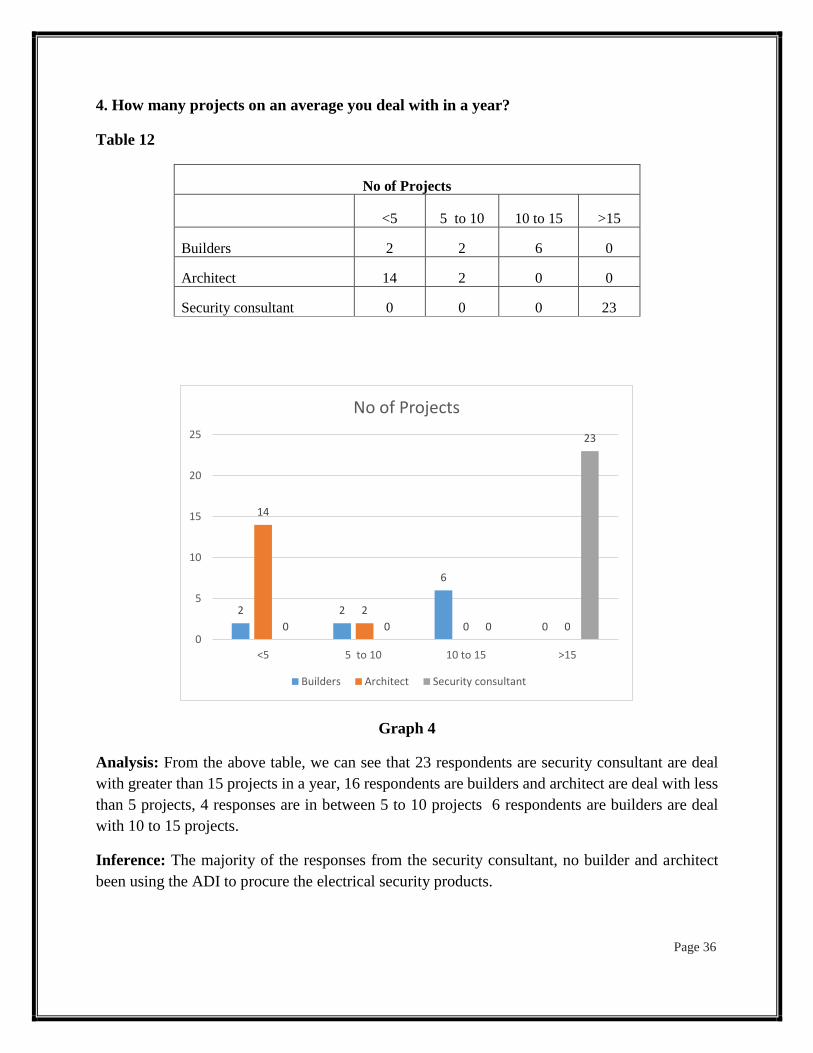

4. How many projects on an average you deal with in a year?

Table 12

No of Projects

<5 5 to 10 10 to 15 >15

Builders 2 2 6 0

Architect 14 2 0 0

Security consultant 0 0 0 23

Graph 4

Analysis: From the above table, we can see that 23 respondents are security consultant are deal

with greater than 15 projects in a year, 16 respondents are builders and architect are deal with less

than 5 projects, 4 responses are in between 5 to 10 projects 6 respondents are builders are deal

with 10 to 15 projects.

Inference: The majority of the responses from the security consultant, no builder and architect

been using the ADI to procure the electrical security products.

Page 36

2 2

6

0

14

2

0 00 0 0

23

0

5

10

15

20

25

<5 5 to 10 10 to 15 >15

No of Projects

Builders Architect Security consultant

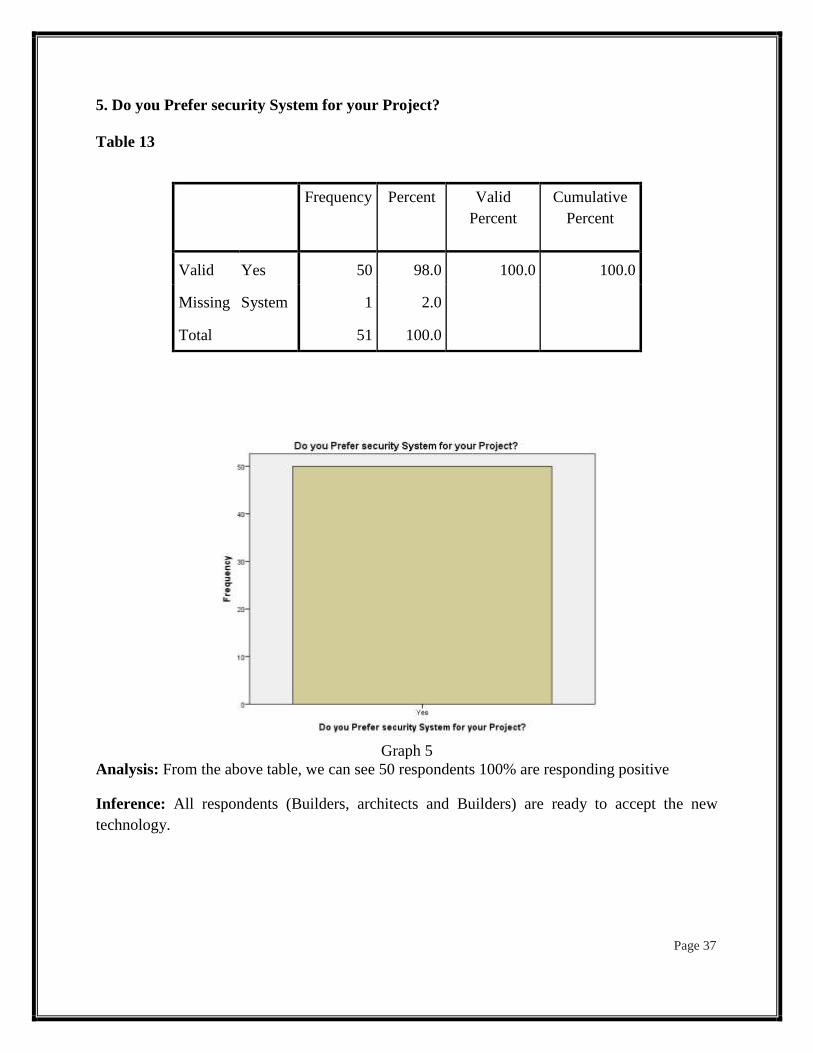

5. Do you Prefer security System for your Project?

Table 13

Frequency Percent Valid

Percent

Cumulative

Percent

Valid Yes 50 98.0 100.0 100.0

Missing System 1 2.0

Total 51 100.0

Graph 5

Analysis: From the above table, we can see 50 respondents 100% are responding positive

Inference: All respondents (Builders, architects and Builders) are ready to accept the new

technology.

Page 37

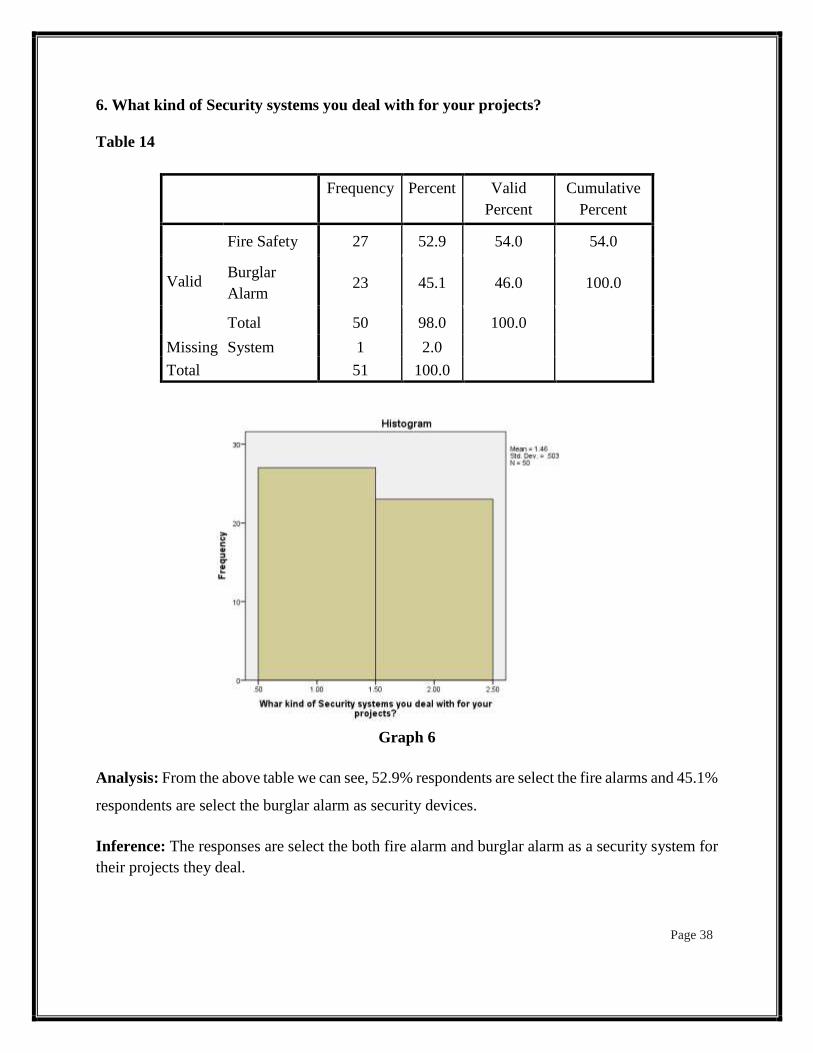

6. What kind of Security systems you deal with for your projects?

Table 14

Frequency Percent Valid

Percent

Cumulative

Percent

Valid

Fire Safety 27 52.9 54.0 54.0

Burglar

Alarm 23 45.1 46.0 100.0

Total 50 98.0 100.0

Missing System 1 2.0

Total 51 100.0

Graph 6

Analysis: From the above table we can see, 52.9% respondents are select the fire alarms and 45.1%

respondents are select the burglar alarm as security devices.

Inference: The responses are select the both fire alarm and burglar alarm as a security system for

their projects they deal.

Page 38

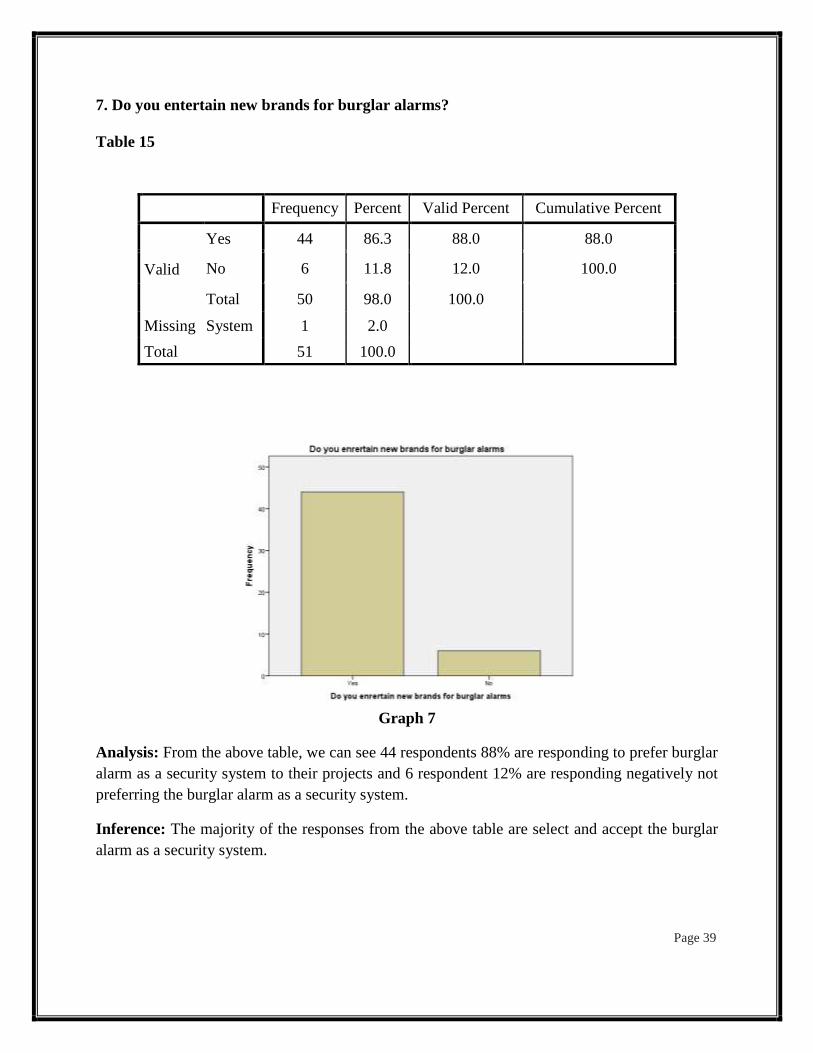

7. Do you entertain new brands for burglar alarms?

Table 15

Frequency Percent Valid Percent Cumulative Percent

Valid

Yes 44 86.3 88.0 88.0

No 6 11.8 12.0 100.0

Total 50 98.0 100.0

Missing System 1 2.0

Total 51 100.0

Graph 7

Analysis: From the above table, we can see 44 respondents 88% are responding to prefer burglar

alarm as a security system to their projects and 6 respondent 12% are responding negatively not

preferring the burglar alarm as a security system.

Inference: The majority of the responses from the above table are select and accept the burglar

alarm as a security system.

Page 39

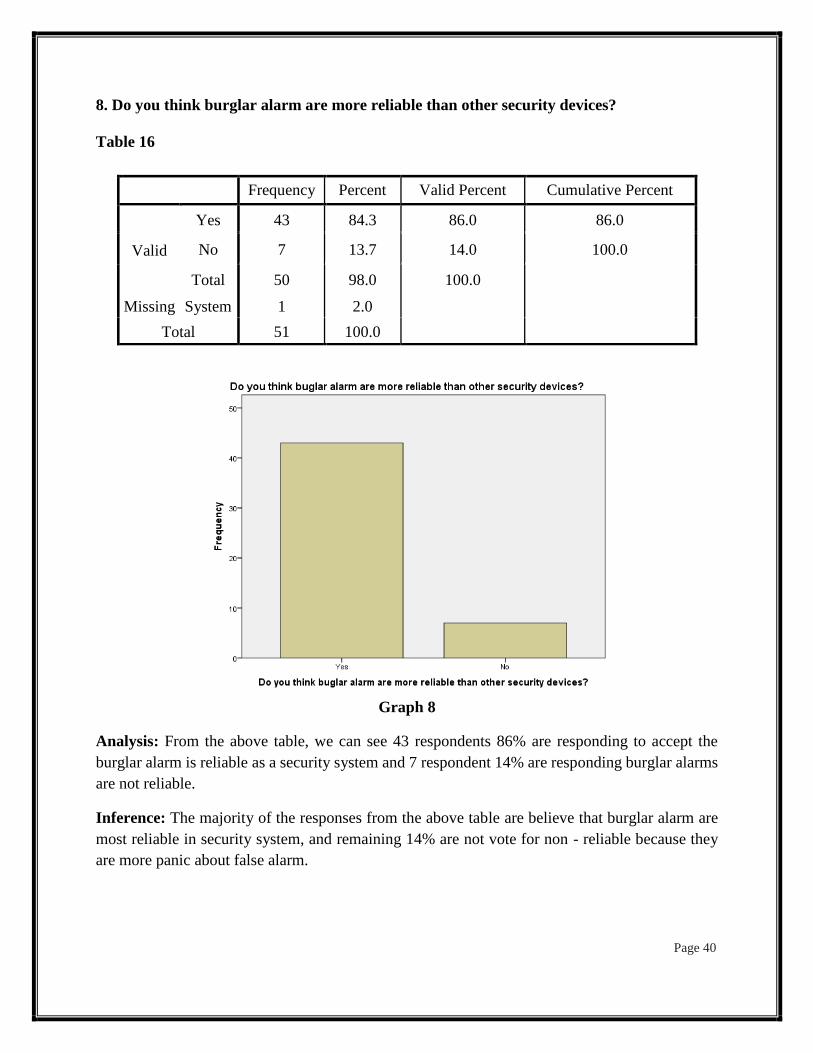

8. Do you think burglar alarm are more reliable than other security devices?

Table 16

Frequency Percent Valid Percent Cumulative Percent

Valid

Yes 43 84.3 86.0 86.0

No 7 13.7 14.0 100.0

Total 50 98.0 100.0

Missing System 1 2.0

Total 51 100.0

Graph 8

Analysis: From the above table, we can see 43 respondents 86% are responding to accept the

burglar alarm is reliable as a security system and 7 respondent 14% are responding burglar alarms

are not reliable.

Inference: The majority of the responses from the above table are believe that burglar alarm are

most reliable in security system, and remaining 14% are not vote for non - reliable because they

are more panic about false alarm.

Page 40

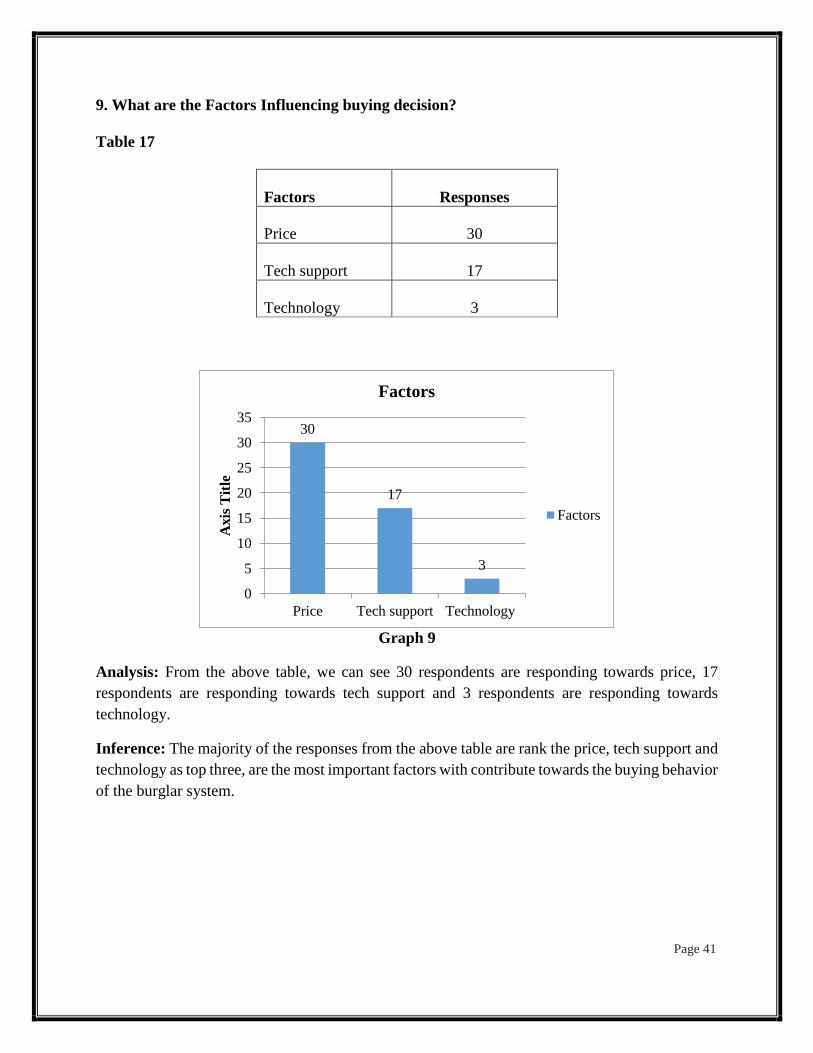

9. What are the Factors Influencing buying decision?

Table 17

Factors Responses

Price 30

Tech support 17

Technology 3

Graph 9

Analysis: From the above table, we can see 30 respondents are responding towards price, 17

respondents are responding towards tech support and 3 respondents are responding towards

technology.

Inference: The majority of the responses from the above table are rank the price, tech support and

technology as top three, are the most important factors with contribute towards the buying behavior

of the burglar system.

Page 41

30

17

3

0

5

10

15

20

25

30

35

Price Tech support Technology

Axis

Tit

le

Factors

Factors

4.5 Findings & Observations:

1. Cost of the projects architect deal, basically architect deal with project with respect to the

area of the project.

2. Integrators are take up the project with respect to the number of zone’s involved in the

projects

3. Builder are purely depending on the budget allocated to the project.

4. Texecom is a premium ended product, though it is a premium securico, DSC and Lifesos

are the major competitor for the Texecom in intrusion market.

5. Though Texecom is a UK made, customer are unaware of it.

6. Customer are more believe in the UK brand in this segment.

7. Most of the customer are unaware of the product and brands availability in this segment,

lack of technical knowledge.

8. There are three important factors which impact on the buying decision of the intrusion

alarms are price, tech support and technology.

9. Builder have dedicated team to take decision about the intrusion system, but there are not

technically sound, when it comes to installation face they depend on the Integrators.

10. Architect will recommend the intrusion, the teams who will take care of HVAC work will

lead the intrusion project as well.

11. Integrators are act as a 3rd party consultant for the architect and Builders of kin of value

added services belongs to intrusion system.

12. External appearance of the product has impact on buying decision

13. Texecom products are high price oriented compare to others brands.

14. Apart from the one minor compliant on the range issue of Texecom product, till now is

under return on sale.

15. Area cover under the sensor is more compare to the other brand of same range.

16. No of sensors used of ideal zone is less when compare to the other brands.

Builders

Decision Makers – Top level management/Finance Manager/Technical Director/Operational

director.

Basic features:

• CCTV

• Video Door Phone

• Security guard

• Intrusion System( As per Customer Preference)

Most influencing Factor

• Price

• Quality

• Look Page 42

Burglar Alarm - Mandatory

• VIP’s

• Celebrities

• Business personalities

• political background people’s

• Senior citizens – Projects

Installation by

• BMS

• Integrators

Feed back

• Good Technology

• Trust on wire Segment

• No complaints

• Looks Good

Recommendation

• Approach them with a complete solution/are a hybrid Panel, which will provide the

complete solution for the home atomisation

• Pricing – Over all pricing for complete solution is not more than Rs:30/- on an average

• Awareness about technology.

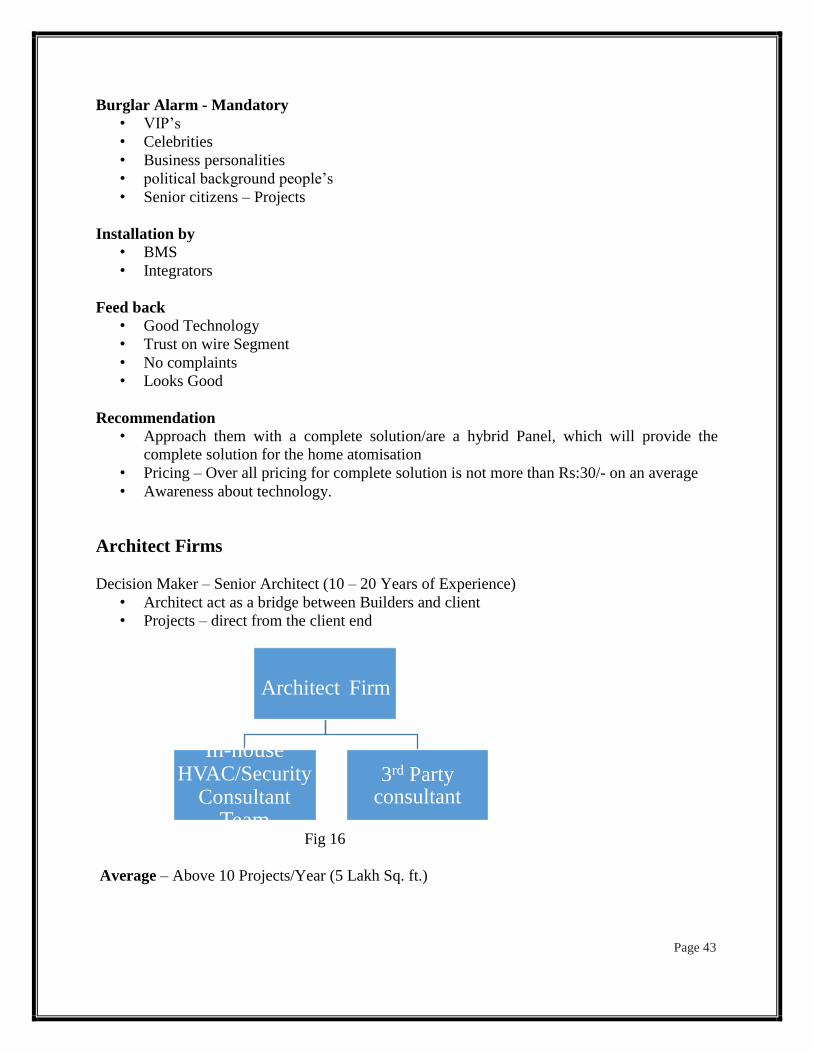

Architect Firms

Decision Maker – Senior Architect (10 – 20 Years of Experience)

• Architect act as a bridge between Builders and client

• Projects – direct from the client end

Fig 16

Average – Above 10 Projects/Year (5 Lakh Sq. ft.)

Page 43

Architect Firm

In-house HVAC/Security

ConsultantTeam

3rd Partyconsultant

Technical

• The one who is taking the decision is not the technical person, based on the experience

he/she gain the knowledge.

• HVAC department will take care of all installation’s

• Training – Integrators

Recommendation

• Registration - ADI

• Training programmes

• Support – Layout Approval

BMSS(Building Management & Security Services) Projects:

• Builders

• Architect

• Direct Client

Role: These people have the role to play from the start of the project to finishing

All safety

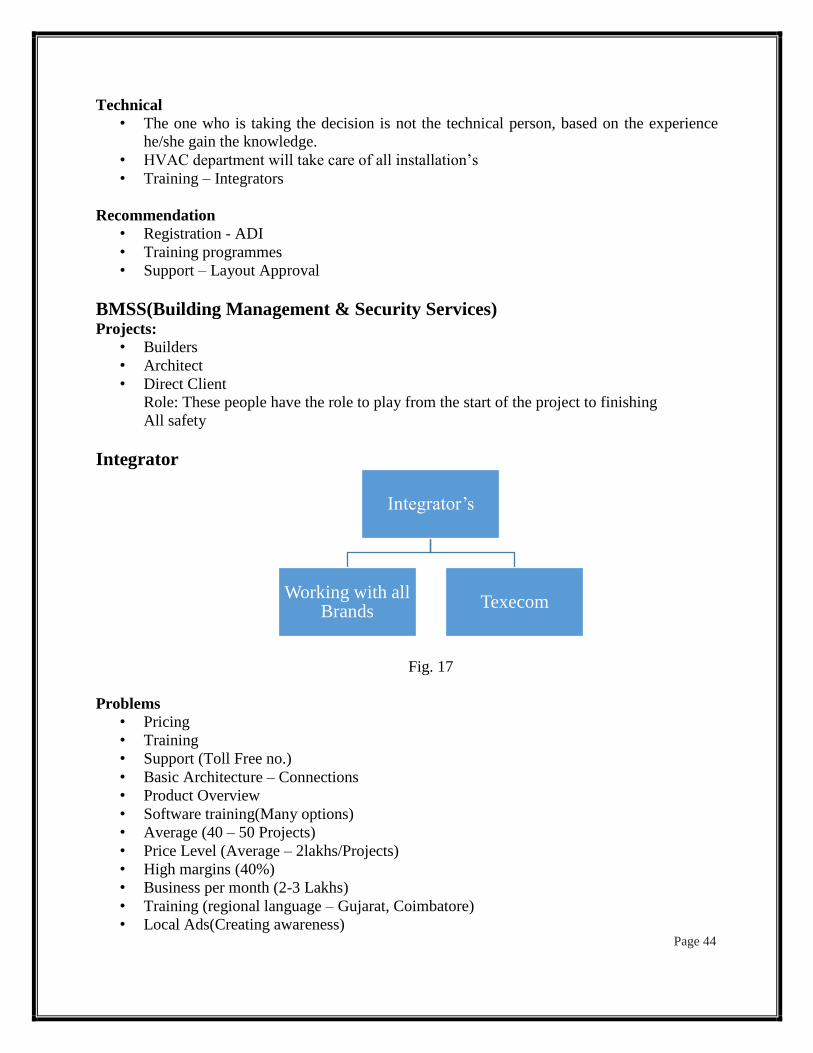

Integrator

Fig. 17

Problems

• Pricing

• Training

• Support (Toll Free no.)

• Basic Architecture – Connections

• Product Overview

• Software training(Many options)

• Average (40 – 50 Projects)

• Price Level (Average – 2lakhs/Projects)

• High margins (40%)

• Business per month (2-3 Lakhs)

• Training (regional language – Gujarat, Coimbatore)

• Local Ads(Creating awareness) Page 44

Integrator’s

Working with all Brands

Texecom

Page 45

Page 46

Fig. 18

Recommendation

• On job Training

• Demo Kit

• Product details(broaches)

• Tech support

Problems: • Pricing

• Margins

• Technical Support – Approving the layout design

• Training

• Touch Screen

• Unware of the product

• Product awareness

• Bulk Purchase

• Marketing campaign

• Online availability (www.ebay.com)

Page 47

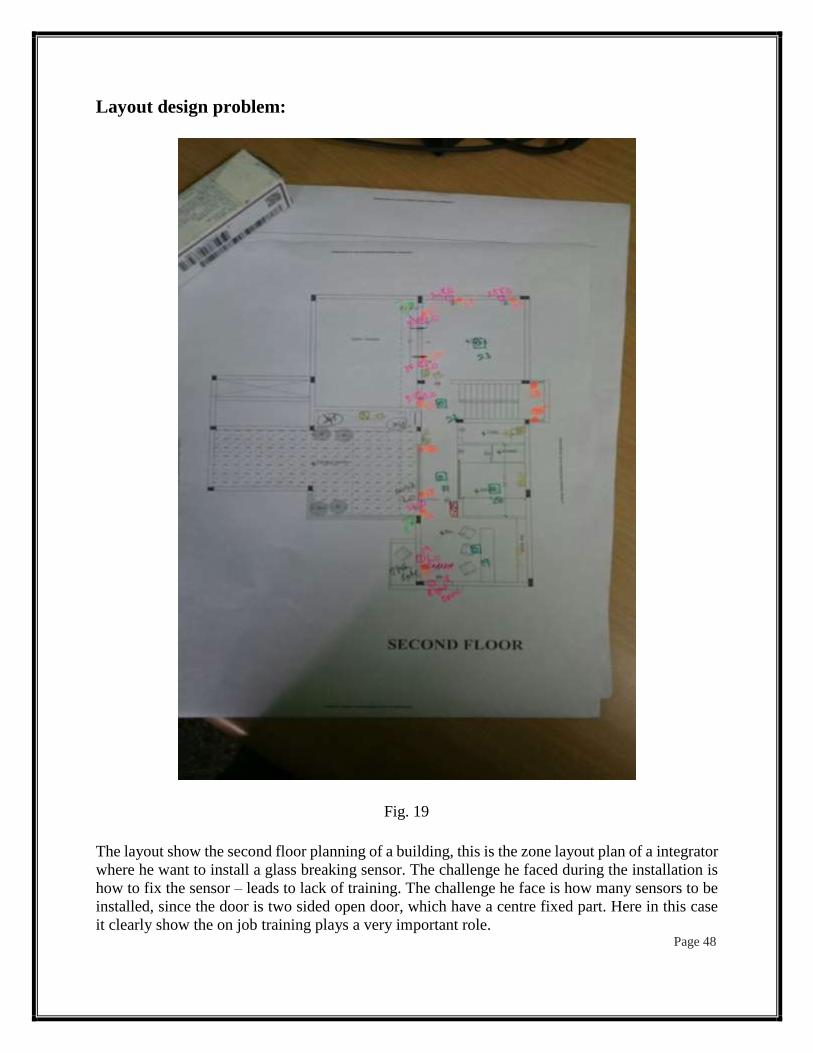

Layout design problem:

Fig. 19

The layout show the second floor planning of a building, this is the zone layout plan of a integrator

where he want to install a glass breaking sensor. The challenge he faced during the installation is

how to fix the sensor – leads to lack of training. The challenge he face is how many sensors to be

installed, since the door is two sided open door, which have a centre fixed part. Here in this case

it clearly show the on job training plays a very important role. Page 48

Solutions Required from Texecom

Texecom integrate with Crestron, RTI or any other processer

Bulk Purchase orders.

Back-up (Storage space)

All automation can be done through central panel

Touch screen

Suggestions

Broaches – Marketing

Updating about the product can be informed to all customer

Regular training

On Job Training

Free Demo kits has been distributed to all integrators

Technical Support(directly from Texecom)

Aware of UK brand recognition

Technology awareness

Distributing the T-Shirts and bags to Integrators/Security Consultants – Represent the

Texecom.

4.6 Conclusions:

This study contributes to understanding the architect, security consultant (Integrator) and Builder

and their role in premium residential projects, understand the challenges faced by them, factors

which are affecting the buying behavior of the customer towards intrusion alarm. Texecom has its

own presence on banking sectors in Indian market, there is scope for intrusion alarm in residential

projects, and the best way to penetrate in to this market is through integrators (security consultant)

because Texecom is a part of HALMA India Pvt. Ltd. Company uses push strategy of marketing

through the global distribution channel ADL. Till now only integrators are registers with ADI.

Builder and Architect looking for a complete solution but Texecom will provide a one of the input

among it.

Page 49

4.7 Recommendations:

On job Training

Free Demo Kit will install at consultant office where the customer will feel the real look

and feel it, it directly connect to emotions

Product details(brochures)

Training (regional language – Gujarat, Coimbatore), since language is the barrier to

communication of this states mention above so, local language training will give the

confidence on both customer and consultant.

Local Ads(Creating awareness)

Updating about the product

On Job Training is necessary to understand the installation in a wider side, to avid the

problem

Technical Support(directly from Texecom)

UK brand recognition

Technology awareness

Distributing the T-Shirts and bags to Integrators/Security Consultants – Represent the

Texecom.

Page 50

Bibliography

http://www.halma.com/~/media/Files/H/Halma-Plc-V2/investors/reports/2016/halma-

annual-report-2016.pdf

http://halma.in/

http://www.texe.com/int2/

http://adiglobal.in/

https://en.wikipedia.org

https://en.wikipedia.org/wiki/Market_research

Textbook: Research Methodology By Deepak Chawla & Neena Sondhi (Vikas

Publishing) 2011

Annexure I

Questionnaire

Name:

Company Name:

Phone Number:

Email Id:

Experience:

Designation:

1. What are the kind of projects you deal with?

I. Residential

Villa.

Independent Houses.

Premium Apartments.

Entry Level Apartments.

Others

_________________________________________________________________

II. Commercial.

IT Parks.

Malls.

Auditoriums.

Others ________________________________________________________.

2. How many projects on an average you deal with in a year.

Less than 5.

5-10.

10-15.

15 and above.

3. What is the cost of projects you deal with?

___________________________________________________________________________

___________________________________________________________________________

___________________________________________________________________________

_________________________________

4. Do you prefer security systems for your projects?

Yes.

No.

5. If Yes, What are the security systems you deal with for your projects?

Fire Safety.

Burglar Alarm.

Panic Button.

Smoke Detectors.

Gas detectors.

Others _________________________________________________________.

6. If Burglar Alarms, What are the brands you prefer for your projects?

___________________________________________________________________________

___________________________________________________________________________

___________________________________________________________________________

_________________________________

7. Do you entertain new brands for Burglar Alarms?

Yes.

No.

8. What are the reasons due to which you specify a particular Brand to your customers?

Multi-National.

Customer Trusted.

Popular.

Do not want to take risk.

Not aware of the New Brands.

Others ________________________________________________________________.

9. What are the set of activities a New Brand should do in order to gain confidence?

Good company profile.

Technical knowledge.

Sample of the products.

Training programs.

Incentive schemes.

List of Installation Site.

Visit of Installation Site.

Conferences.

Others

_________________________________________________________________.

10. Among the above factor which are the top 3 (descending order) in order of importance and

why?

________________________________________________________________________

________________________________________________________________________

________________________________________________________________________

________________________________________________________________________

________________________________________________________________________

________________________________________________________________________

________________________________________________________________________

____________________________

11. What are the challenges a New Brand faces to gain market share?

_______________________________________________________________________

_______________________________________________________________________

_______________________________________________________________________

_______________________________________________________________________

________________

12. Is there any third party involved who take care of the security systems for your projects? If

Yes, Name & Contact of the 3rd party.

______________________________________________________________________

______________________________________________________________________

______________________________________________________________________

______________________________________________________________________

________________________________________________

13. Do you think Burglar Alarm are more reliable than other security devices?

Yes.

Why_________________________________________________________________

_____________________________________________________________________

_____________________________________________________________________

_________________________________

No.

Why_________________________________________________________________

_____________________________________________________________________

_____________________________________________________________________

_________________________________

14. Does the external appearance of the device influence the customer to buy Burglar Alarms?

___________________________________________________________________________

___________________________________________________________________________

___________________________________________________________________________

_________________________________

15. What differentiate you from your competitors?

___________________________________________________________________________

___________________________________________________________________________

___________________________________________________________________________

___________________________________________________________________________

____________________________________________

16. What are the challenges you face for getting projects from your clients?

___________________________________________________________________________

___________________________________________________________________________

___________________________________________________________________________

___________________________________________________________________________

____________________________________________

Annexure II - Weekly reports & Attendance sheet

M. S. RAMAIAH INSTITUTE OF MANAGEMENT

PGDM - AICTE - II Semester - Batch 2015-2017

Weekly Report of SUMMER INTERNSHIP (SIP) at ___HALMA India Pvt. Ltd.____

To __Prof. Arul Jyothi

MSRIM

Sir / Madam,

The following tasks were undertaken during the week __04-04-2016_

(starting date) to ___08-04-2016___ (ending date)

Date Task Handled

Observation /

Remarks of

Faculty Guide

04-04-2016 Joining formalities, Briefing about the company

and projects they handling, Project briefing

05-04-2016 Meeting with Marking head(India) from

Texecom. Discuss about the projects, developing

objectives and task for the research study

06-04-2016 Questionnaire Preparation

07-04-2016 Discuss the Questionnaire with Marketing

Manager from Halma India Pvt. Ltd.

08-04-2016 Doing the necessary changes and getting

approval from Sunil (Marketing Manager Halma

India Pvt Ltd.)

09-04-2016 -------Holiday---------

10-04-2016 -------Holiday---------

Student Name: _______Hemanth Kumar Meda_ Reg. No.:_151228 _

Student Signature: _____________________________________________

Faculty Guide Signature: ______________________________

M. S. RAMAIAH INSTITUTE OF MANAGEMENT

PGDM - AICTE - II Semester - Batch 2015-2017

Weekly Report of SUMMER INTERNSHIP (SIP) at ______________HALMA India Pvt. Ltd. ____________

To ________Prof. Arul Jyothi____________

MSRIM

Sir / Madam,

The following tasks were undertaken during the week ___11-04-2016__

(starting date) to _______15-04-2016____ (ending date)

Date Task Handled

Observation /

Remarks of

Faculty Guide

11-04-2016 Generating the data, writing emails, cold calling

and fixing the appointment’s

12-04-2016 4 – Meeting @ Bangalore – Architects

13-04-2016 Meeting @ Bangalore – Security consultant

people, BMS(Building Management security

services)

14-04-2016 Meeting @ Bangalore – Top Builder

15-04-2016 Presenting oral to Marking Manager –

HALAMA India Pvt. Ltd. & Telephonic

Presentation to India Marketing Manager –

Texecom (UK)

16-04-2016 ----------------Holiday--------------

17-04-2016 ----------------Holiday--------------

Student Name: _Hemanth kumar Meda__________ Reg. No.:_151228 _

Student Signature: _____________________________________________

Faculty Guide Signature: ______________________________

M. S. RAMAIAH INSTITUTE OF MANAGEMENT

PGDM - AICTE - II Semester - Batch 2015-2017

Weekly Report of SUMMER INTERNSHIP (SIP) at ________HALMA India Pvt. Ltd.____________________

To ______Prof. Arul Jyothi_____________________

MSRIM

Sir / Madam,

The following tasks were undertaken during the week __18/04/2016____

(starting date) to ______22/04/2016_____ (ending date)

Date Task Handled

Observation /

Remarks of

Faculty Guide

18-04-2016

Data Mining & fix the appointment

19-04-2016 Data Mining & fix the appointment

20-04-2016 Preparing Travel Plan (Cochin, Chennai,

Hyderabad, Pune, Vijayawada…. Etc. – Study

and understand the security consultants need in

Residential Projects( Villa, Premium Independent

Houses )

21-04-2016 Generating leads in Cochin and Chennai

22-04-2016 Presentation reg: Bangalore study and getting

some inputs form both managers – study.

23-04-2016 Holiday

24-04-2016 Holiday

Student Name: ______Hemath kumar Meda_______ Reg. No.:_151228 _

Student Signature: _____________________________________________

Faculty Guide Signature: ______________________________

M. S. RAMAIAH INSTITUTE OF MANAGEMENT

PGDM - AICTE - II Semester - Batch 2015-2017

Weekly Report of SUMMER INTERNSHIP (SIP) at ________HALMA India Pvt. Ltd.____________________

To ______Prof. Arul Jyothi_____________________

MSRIM

Sir / Madam,

The following tasks were undertaken during the week __25/04/2016____

(starting date) to ______01/05/2016_____ (ending date)

Date Task Handled

Observation /

Remarks of

Faculty Guide

25-04-2016

Data Mining & fix the appointment

26-04-2016

Data Mining & fix the appointment

27-04-2016

Presentation and Generating the leads as well as

the Meeting with Global distribution channel –

ADI

28-04-2016

Generating leads in Cochin and Chennai

29-04-2016

Travel Preparation - Cochin

30-04-2016

Holiday

01-05-2016

Holiday

Student Name: ______Hemath kumar Meda_______ Reg. No.:_151228 _

Student Signature: _____________________________________________

Faculty Guide Signature: ______________________________

M. S. RAMAIAH INSTITUTE OF MANAGEMENT

PGDM - AICTE - II Semester - Batch 2015-2017

Weekly Report of SUMMER INTERNSHIP (SIP) at ________HALMA India Pvt. Ltd.____________________

To ______Prof. Arul Jyothi_____________________

MSRIM

Sir / Madam,

The following tasks were undertaken during the week __02/05/2016____

(starting date) to ______08/05/2016_____ (ending date)

Date Task Handled

Observation /

Remarks of

Faculty Guide

02-05-2016

Meeting with Builders, security Consultant and

Architect in Cochin

03-05-2016

Meeting with Builders, security Consultant and

Architect in Cochin

04-05-2016

Meeting with Builders, security Consultant and

Architect in Cochin

05-05-2016

Travel to Coimbatore

06-05-2016

Meeting with Builders, security Consultant and

Architect in Coimbatore

07-05-2016

Meeting with Builders, security Consultant and

Architect in Coimbatore

08-05-2016

Holiday

Student Name: ______Hemath kumar Meda_______ Reg. No.:_151228 _

Student Signature: _____________________________________________