1 Insurance Telematics A Long-term Antidote? Insurers in numerous countries are looking to telematics as they seek to control claims costs, enhance pricing, increase profitability and differentiate and personalise their products and services. The UK now leads the world market in telematics adoption by both take up per capita and adoption rates by Insurers with both sides of the UK Government encouraging telematics politically. Since the launch of price comparison sites in the UK market a decade ago, multimillion pound advertising campaigns that highlight the benefits to customers of searching for the best price deal online are the norm, and these sites have become increasingly popular with UK consumers. This was layered upon what was already the most competitive motor insurance market place in the world. The effect of intense online competition, together with rising fraud levels and a legal environment that encourages claims farming, has resulted in a cut throat and largely unprofitable market. It is a market where fluctuating prices and uncertainty of returns prevail. UK Insurers have been frantically searching for the antidote. This search has led to a period of innovation in UK motor insurance pricing techniques. Portfolio pricing, optimisation tools and data enrichment (including leveraging credit scores) have been presented as solutions; however with the majority of the market now using these, the competitive advantage of the early adopters has worn off and the past two years has seen UK Insurers starting to turn to Telematics or Usage Based Insurance (UBI). UBI for Insurers represents a shift away from pricing based on an approximation of individual risk to pricing based on individual risk (pricing on a sample of one). In addition to pricing innovation UBI offers self-selection, deeper customer engagement, more effective channel management and reduced fraud exposure which is partly why it is being presented as a long-term antidote, rather than a shorter term pricing quick-win. Increased customer awareness and significantly lower cost data acquisition thanks to smartphone applications will assist UBI in the UK to spread from the niche high risk areas out into the lower risk mass market from 2014. The UK innovations in telematics will ripple out into international markets with early adopting Insurers and Brokers in these markets benefiting. THINKING OUTSIDE OF THE BOX For too long now Insurers have been trapped inside the ‘hamster wheel’ of market underwriting cycles, hoping that today’s customers are more profitable than yesterday’s, yet knowing that they can’t be certain of this until tomorrow. Can telematics help us break out of this cycle and what might global Insurers learn from developments in the UK? Paul Stacy R&D Director David Neave Non - Executive Director What is Insurance Telematics? Vehicle telematics is the technology of recording, sending, receiving and storing information via telecommunication devices in vehicles. Insurance telematics, better known by consumers as ‘Blackbox’ Insurance has many other names within the industry such as; ‘Pay As You Drive’, ‘Pay How You Drive’ and more recently ‘Usage Based Insurance’ (UBI). Issue 1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

Insurance Telematics

A Long-term Antidote? Insurers in numerous countries are looking to telematics as they seek to control claims costs, enhance pricing, increase profitability and differentiate and personalise their products and services. The UK now leads the world market in telematics adoption by both take up per capita and adoption rates by Insurers with both sides of the UK Government encouraging telematics politically. Since the launch of price comparison sites in the UK market a decade ago, multimillion pound advertising campaigns that highlight the benefits to customers of searching for the best price deal online are the norm, and these sites have become increasingly popular with UK consumers. This was layered upon what was already the most competitive motor insurance market place in the world. The effect of intense online competition, together with rising fraud levels and a legal environment that encourages claims farming, has resulted in a cut throat and largely unprofitable market. It is a market where fluctuating prices and uncertainty of returns prevail. UK Insurers have been frantically searching

for the antidote. This search has led to a period of innovation in UK motor insurance pricing techniques. Portfolio pricing, optimisation tools and data enrichment (including leveraging credit scores) have been presented as solutions; however with the majority of the market now using these, the competitive advantage of the early adopters has worn off and the past two years has seen UK Insurers starting to turn to Telematics or Usage Based Insurance (UBI). UBI for Insurers represents a shift away from pricing based on an approximation of individual risk to pricing based on individual risk (pricing on a sample of one). In addition to pricing innovation UBI offers self-selection, deeper customer engagement, more effective channel management and reduced fraud exposure which is partly why it is being presented as a long-term antidote, rather than a shorter term pricing quick-win. Increased customer awareness and significantly lower cost data acquisition thanks to smartphone applications will assist UBI in the UK to spread from the niche high risk areas out into the lower risk mass market from 2014. The UK innovations in telematics will ripple out into international markets with early adopting Insurers and Brokers in these markets benefiting.

THINKING OUTSIDE OF THE BOXFor too long now Insurers have been trapped inside the ‘hamster wheel’ of market underwriting cycles, hoping that today’s customers are more profitable than yesterday’s, yet knowing that they can’t be certain of this until tomorrow. Can telematics help us break out of this cycle and what might global Insurers learn from developments in the UK?

Paul StacyR&D Director

David NeaveNon - ExecutiveDirector

What is Insurance Telematics?

Vehicle telematics is the technology of recording, sending, receiving and storing information via telecommunication devices in vehicles. Insurance telematics, better known by consumers as ‘Blackbox’ Insurance has many other names within the industry such as; ‘Pay As You Drive’, ‘Pay How You Drive’ and more recently ‘Usage Based Insurance’ (UBI).

Issue 1

2

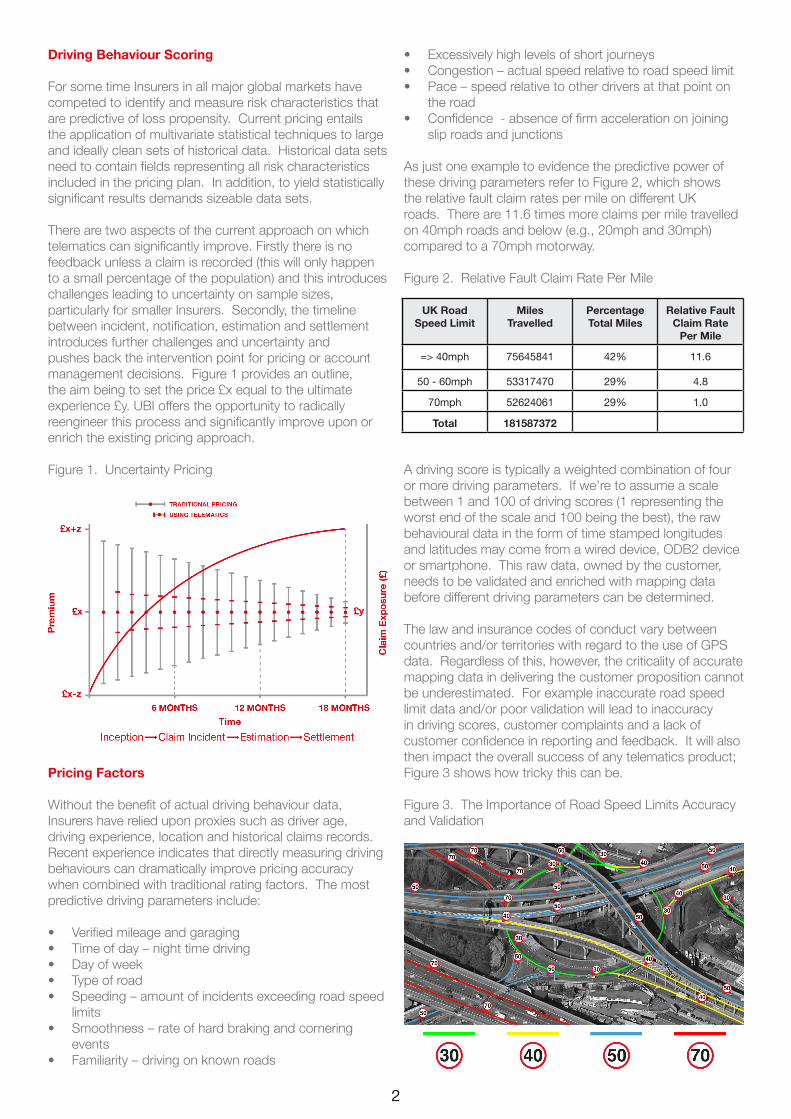

Driving Behaviour Scoring For some time Insurers in all major global markets have competed to identify and measure risk characteristics that are predictive of loss propensity. Current pricing entails the application of multivariate statistical techniques to large and ideally clean sets of historical data. Historical data sets need to contain fields representing all risk characteristics included in the pricing plan. In addition, to yield statistically significant results demands sizeable data sets. There are two aspects of the current approach on which telematics can significantly improve. Firstly there is no feedback unless a claim is recorded (this will only happen to a small percentage of the population) and this introduces challenges leading to uncertainty on sample sizes, particularly for smaller Insurers. Secondly, the timeline between incident, notification, estimation and settlement introduces further challenges and uncertainty and pushes back the intervention point for pricing or account management decisions. Figure 1 provides an outline, the aim being to set the price £x equal to the ultimate experience £y. UBI offers the opportunity to radically reengineer this process and significantly improve upon or enrich the existing pricing approach.

Figure 1. Uncertainty Pricing

Pricing Factors Without the benefit of actual driving behaviour data, Insurers have relied upon proxies such as driver age, driving experience, location and historical claims records. Recent experience indicates that directly measuring driving behaviours can dramatically improve pricing accuracy when combined with traditional rating factors. The most predictive driving parameters include: • Verified mileage and garaging• Time of day – night time driving• Day of week• Type of road• Speeding – amount of incidents exceeding road speed

limits• Smoothness – rate of hard braking and cornering

events• Familiarity – driving on known roads

• Excessively high levels of short journeys• Congestion – actual speed relative to road speed limit• Pace – speed relative to other drivers at that point on

the road• Confidence - absence of firm acceleration on joining

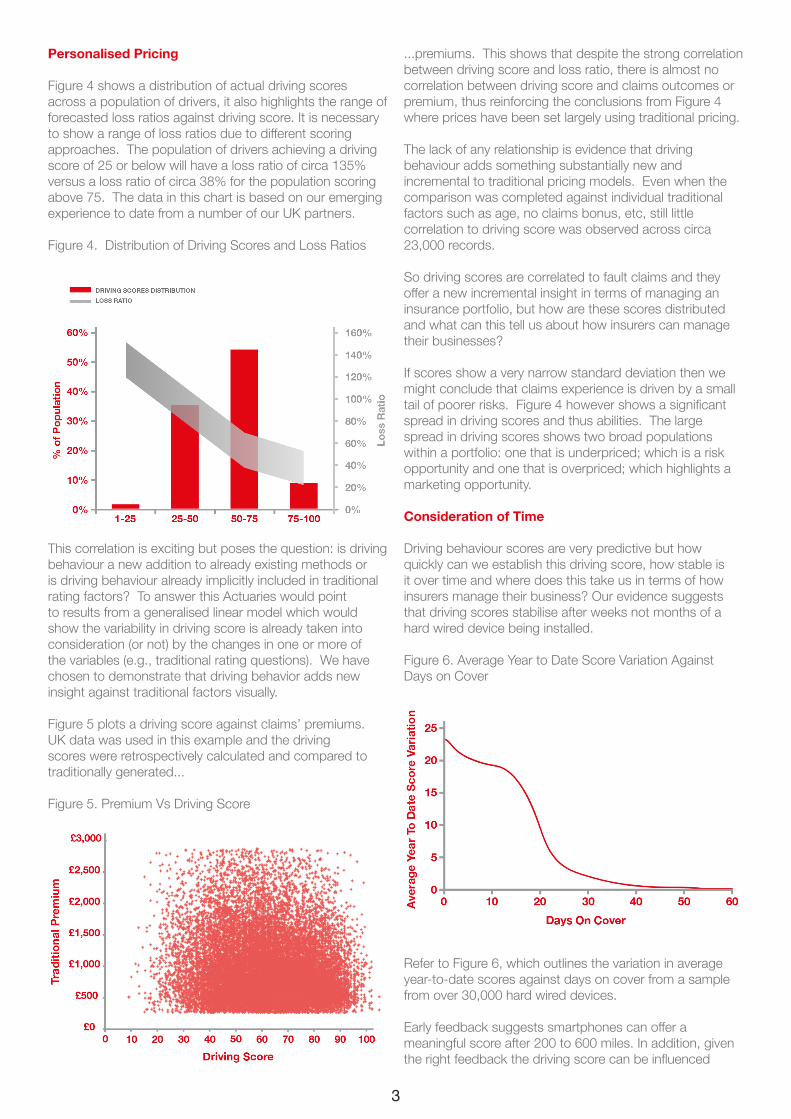

slip roads and junctions As just one example to evidence the predictive power of these driving parameters refer to Figure 2, which shows the relative fault claim rates per mile on different UK roads. There are 11.6 times more claims per mile travelled on 40mph roads and below (e.g., 20mph and 30mph) compared to a 70mph motorway.

Figure 2. Relative Fault Claim Rate Per Mile

A driving score is typically a weighted combination of four or more driving parameters. If we’re to assume a scale between 1 and 100 of driving scores (1 representing the worst end of the scale and 100 being the best), the raw behavioural data in the form of time stamped longitudes and latitudes may come from a wired device, ODB2 device or smartphone. This raw data, owned by the customer, needs to be validated and enriched with mapping data before different driving parameters can be determined.

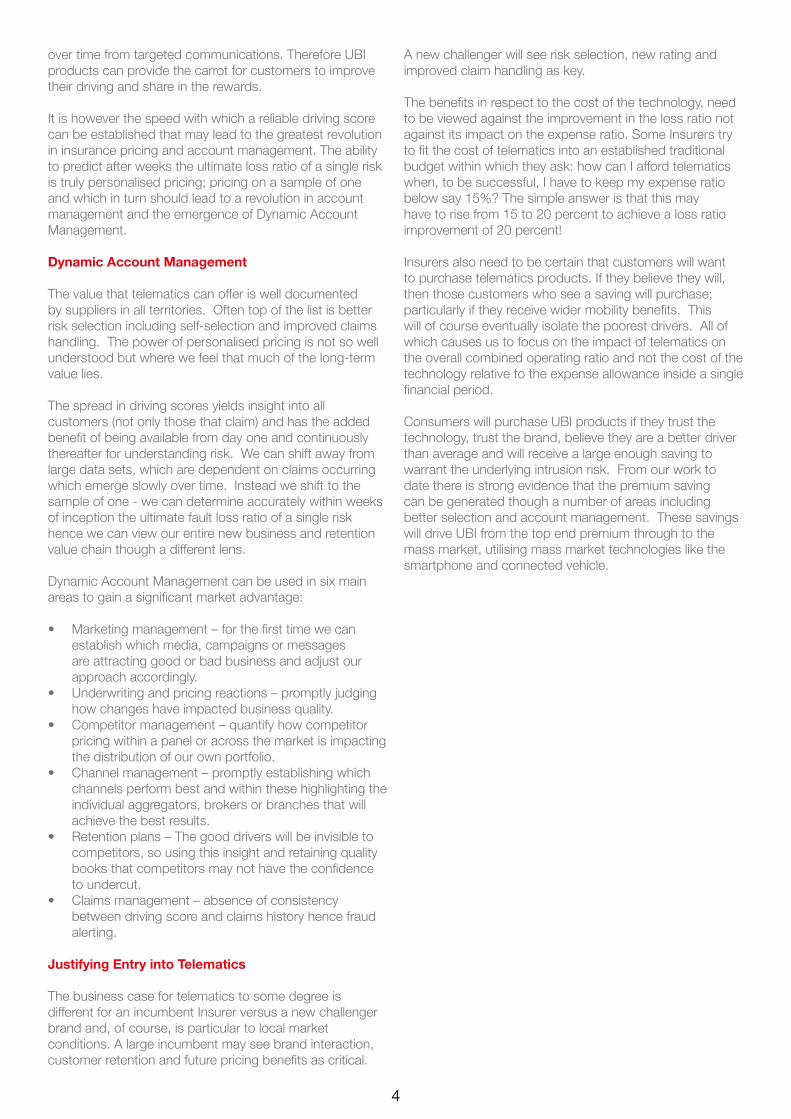

The law and insurance codes of conduct vary between countries and/or territories with regard to the use of GPS data. Regardless of this, however, the criticality of accurate mapping data in delivering the customer proposition cannot be underestimated. For example inaccurate road speed limit data and/or poor validation will lead to inaccuracy in driving scores, customer complaints and a lack of customer confidence in reporting and feedback. It will also then impact the overall success of any telematics product; Figure 3 shows how tricky this can be.

Figure 3. The Importance of Road Speed Limits Accuracy and Validation

UK Road Speed Limit

Miles Travelled

Percentage Total Miles

Relative Fault Claim Rate

Per Mile

=> 40mph 75645841 42% 11.6

50 - 60mph 53317470 29% 4.8

70mph 52624061 29% 1.0

Total 181587372

3

Personalised Pricing Figure 4 shows a distribution of actual driving scores across a population of drivers, it also highlights the range of forecasted loss ratios against driving score. It is necessary to show a range of loss ratios due to different scoring approaches. The population of drivers achieving a driving score of 25 or below will have a loss ratio of circa 135% versus a loss ratio of circa 38% for the population scoring above 75. The data in this chart is based on our emerging experience to date from a number of our UK partners.

Figure 4. Distribution of Driving Scores and Loss Ratios

This correlation is exciting but poses the question: is driving behaviour a new addition to already existing methods or is driving behaviour already implicitly included in traditional rating factors? To answer this Actuaries would point to results from a generalised linear model which would show the variability in driving score is already taken into consideration (or not) by the changes in one or more of the variables (e.g., traditional rating questions). We have chosen to demonstrate that driving behavior adds new insight against traditional factors visually.

Figure 5 plots a driving score against claims’ premiums. UK data was used in this example and the driving scores were retrospectively calculated and compared to traditionally generated...

Figure 5. Premium Vs Driving Score

...premiums. This shows that despite the strong correlation between driving score and loss ratio, there is almost no correlation between driving score and claims outcomes or premium, thus reinforcing the conclusions from Figure 4 where prices have been set largely using traditional pricing. The lack of any relationship is evidence that driving behaviour adds something substantially new and incremental to traditional pricing models. Even when the comparison was completed against individual traditional factors such as age, no claims bonus, etc, still little correlation to driving score was observed across circa 23,000 records. So driving scores are correlated to fault claims and they offer a new incremental insight in terms of managing an insurance portfolio, but how are these scores distributed and what can this tell us about how insurers can manage their businesses? If scores show a very narrow standard deviation then we might conclude that claims experience is driven by a small tail of poorer risks. Figure 4 however shows a significant spread in driving scores and thus abilities. The large spread in driving scores shows two broad populations within a portfolio: one that is underpriced; which is a risk opportunity and one that is overpriced; which highlights a marketing opportunity. Consideration of Time Driving behaviour scores are very predictive but how quickly can we establish this driving score, how stable is it over time and where does this take us in terms of how insurers manage their business? Our evidence suggests that driving scores stabilise after weeks not months of a hard wired device being installed.

Figure 6. Average Year to Date Score Variation Against Days on Cover

Refer to Figure 6, which outlines the variation in average year-to-date scores against days on cover from a sample from over 30,000 hard wired devices.

Early feedback suggests smartphones can offer a meaningful score after 200 to 600 miles. In addition, given the right feedback the driving score can be influenced

4

over time from targeted communications. Therefore UBI products can provide the carrot for customers to improve their driving and share in the rewards. It is however the speed with which a reliable driving score can be established that may lead to the greatest revolution in insurance pricing and account management. The ability to predict after weeks the ultimate loss ratio of a single risk is truly personalised pricing; pricing on a sample of one and which in turn should lead to a revolution in account management and the emergence of Dynamic Account Management. Dynamic Account Management The value that telematics can offer is well documented by suppliers in all territories. Often top of the list is better risk selection including self-selection and improved claims handling. The power of personalised pricing is not so well understood but where we feel that much of the long-term value lies. The spread in driving scores yields insight into all customers (not only those that claim) and has the added benefit of being available from day one and continuously thereafter for understanding risk. We can shift away from large data sets, which are dependent on claims occurring which emerge slowly over time. Instead we shift to the sample of one - we can determine accurately within weeks of inception the ultimate fault loss ratio of a single risk hence we can view our entire new business and retention value chain though a different lens. Dynamic Account Management can be used in six main areas to gain a significant market advantage: • Marketing management – for the first time we can

establish which media, campaigns or messages are attracting good or bad business and adjust our approach accordingly.

• Underwriting and pricing reactions – promptly judging how changes have impacted business quality.

• Competitor management – quantify how competitor pricing within a panel or across the market is impacting the distribution of our own portfolio.

• Channel management – promptly establishing which channels perform best and within these highlighting the individual aggregators, brokers or branches that will achieve the best results.

• Retention plans – The good drivers will be invisible to competitors, so using this insight and retaining quality books that competitors may not have the confidence to undercut.

• Claims management – absence of consistency between driving score and claims history hence fraud alerting.

Justifying Entry into Telematics The business case for telematics to some degree is different for an incumbent Insurer versus a new challenger brand and, of course, is particular to local market conditions. A large incumbent may see brand interaction, customer retention and future pricing benefits as critical.

A new challenger will see risk selection, new rating and improved claim handling as key. The benefits in respect to the cost of the technology, need to be viewed against the improvement in the loss ratio not against its impact on the expense ratio. Some Insurers try to fit the cost of telematics into an established traditional budget within which they ask: how can I afford telematics when, to be successful, I have to keep my expense ratio below say 15%? The simple answer is that this may have to rise from 15 to 20 percent to achieve a loss ratio improvement of 20 percent! Insurers also need to be certain that customers will want to purchase telematics products. If they believe they will, then those customers who see a saving will purchase; particularly if they receive wider mobility benefits. This will of course eventually isolate the poorest drivers. All of which causes us to focus on the impact of telematics on the overall combined operating ratio and not the cost of the technology relative to the expense allowance inside a single financial period.

Consumers will purchase UBI products if they trust the technology, trust the brand, believe they are a better driver than average and will receive a large enough saving to warrant the underlying intrusion risk. From our work to date there is strong evidence that the premium saving can be generated though a number of areas including better selection and account management. These savings will drive UBI from the top end premium through to the mass market, utilising mass market technologies like the smartphone and connected vehicle.

For more information contact the Wunelli office at

t: 02392 985 430e: [email protected]

w: www.wunelli.com

Paul Stacy - R&D Director

Paul is both an Australian and British citizen and founded Wunelli in 2008 with the aim of understanding the data and technology involved in Usage Based Insurance and making it work for both individuals and insurance companies.

Prior to Wunelli, Paul studied Engineering and completed his Masters of Mathematics. After his studies Paul worked in Insurance in Australia and for the past decade in the United Kingdom.

Paul lives in Hampshire, England with his wife and two sons, both of whom will have telematics devices installed in their vehicles!

David Neave - Non-Executive Director

David joined our board in October 2013 and brings to Wunelli over three decades’ experience within the personal insurance sector, including senior executive roles at RSA and as MD at Co-Operative Insurance. David is also

currently Non-Executive Director at Parabis and LV.

Adding to his industry experience, David has also been Chairman of the Insurance Fraud Bureau, fulfilled directorships at the Motor Insurers Bureau, ICMIF and Co-operative Legal Services and was on the ABI’s General

Insurance Committee, the Insurance Data Initiatives Board and the Financial Crime Committee.

The information and opinions contained in this publication are for general information purposes only. They do not constitute definitive professional advice and should not be relied on or treated as a substitute for specific advice relevant to particular circumstances. Wunelli does not accept or

assume any liability, responsibility or duty of care for any loss which may arise from reliance on information or opinions published in the publication or for any decision based on it. Wunelli would be pleased to advise on how to apply the principles set out in this publication to your specific

circumstances. Copyright 2014 Wunelli.com.

About Us

Wunelli is a data services company dedicated to enabling the industry to create Usage Based Insurance products. Our energy is entirely devoted to helping you understand your customers’ driving behaviour with the industry’s most

accurate driving data and trusted driving scores.

Our services and products are specifically designed so that you’re able to reassess risk, discount safer drivers and manage the relationship with your customers more effectively.

We provide clear results that make sense to help your business innovate, compete and grow.

Related Documents