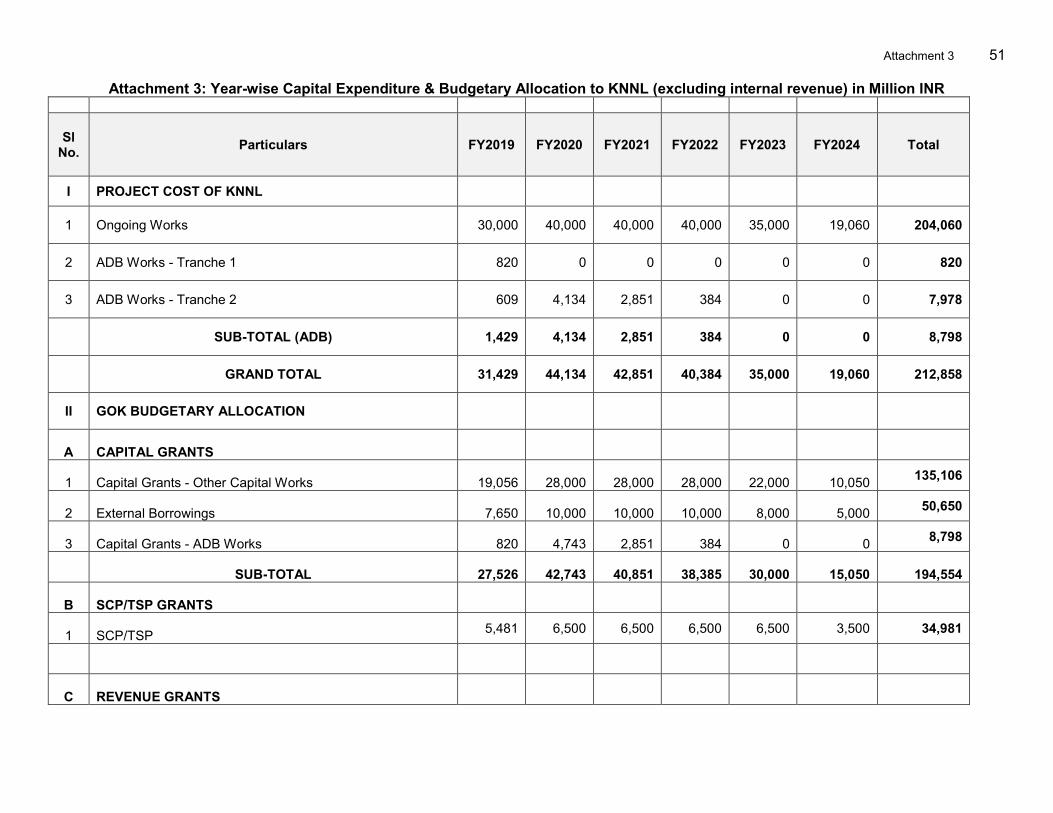

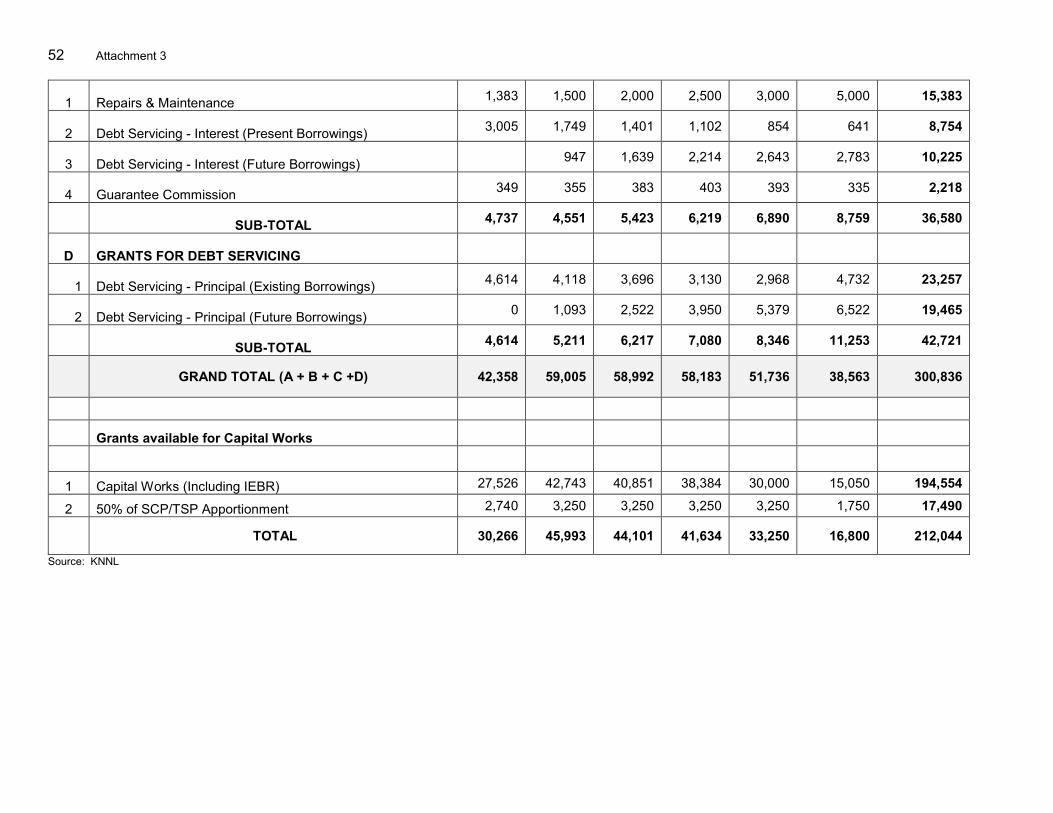

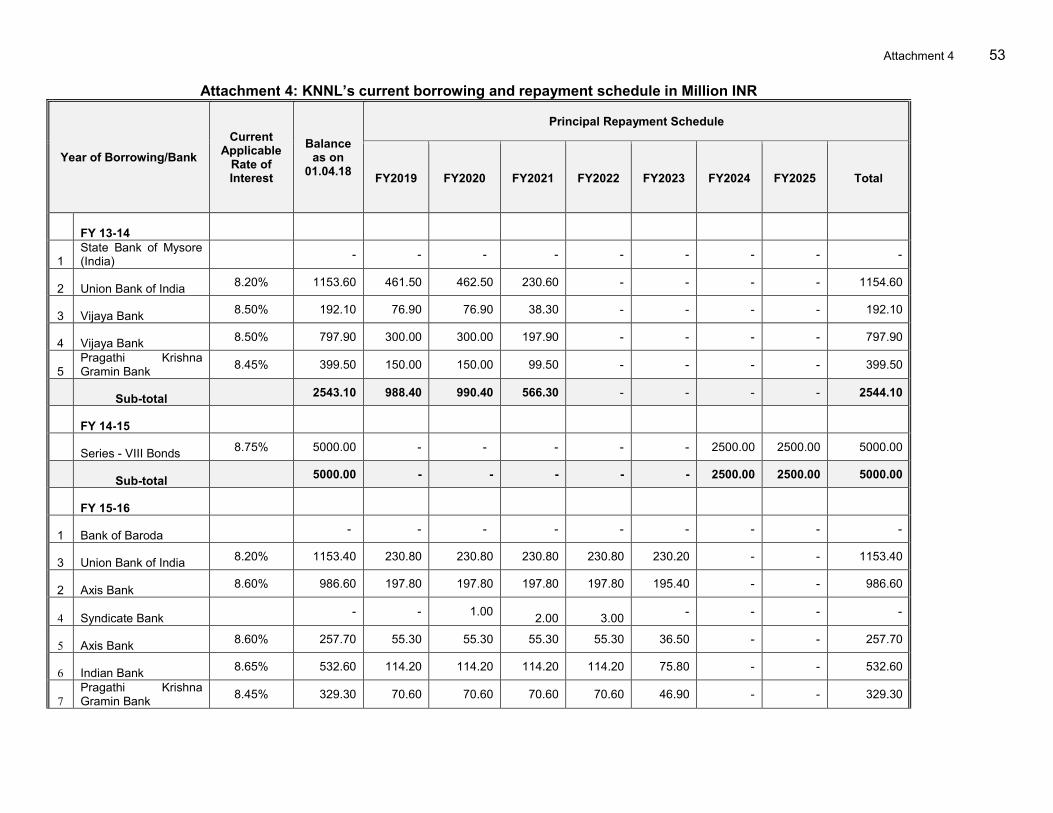

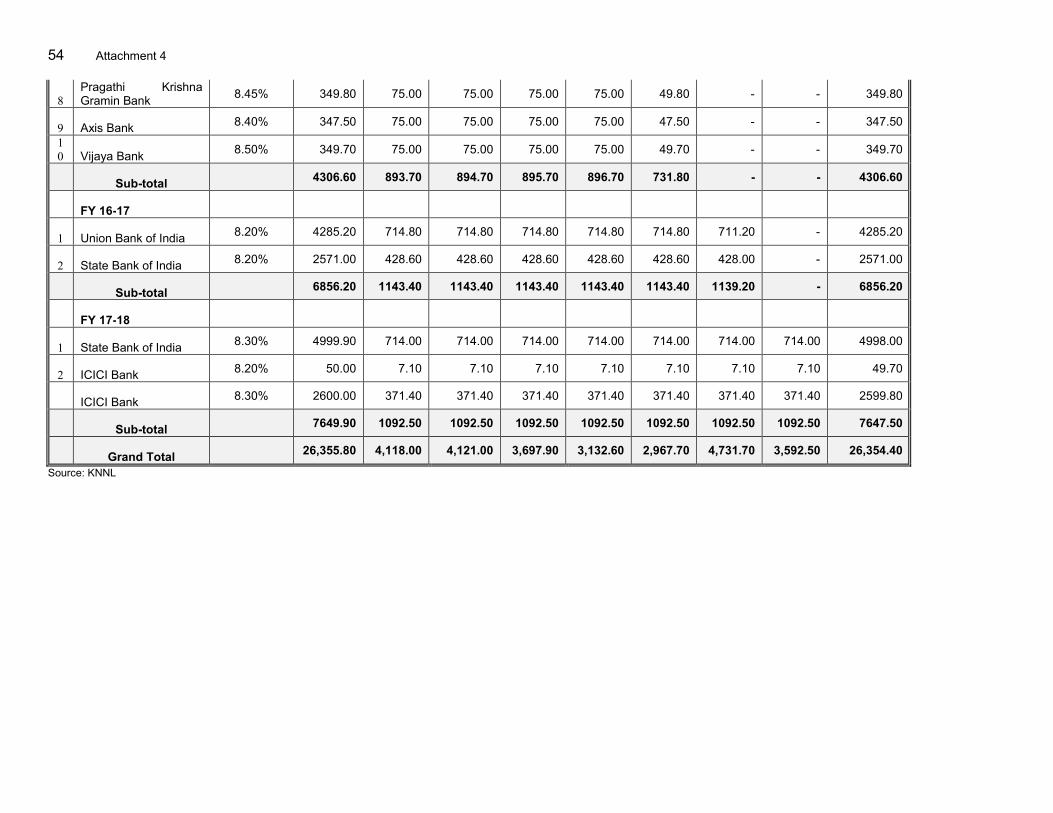

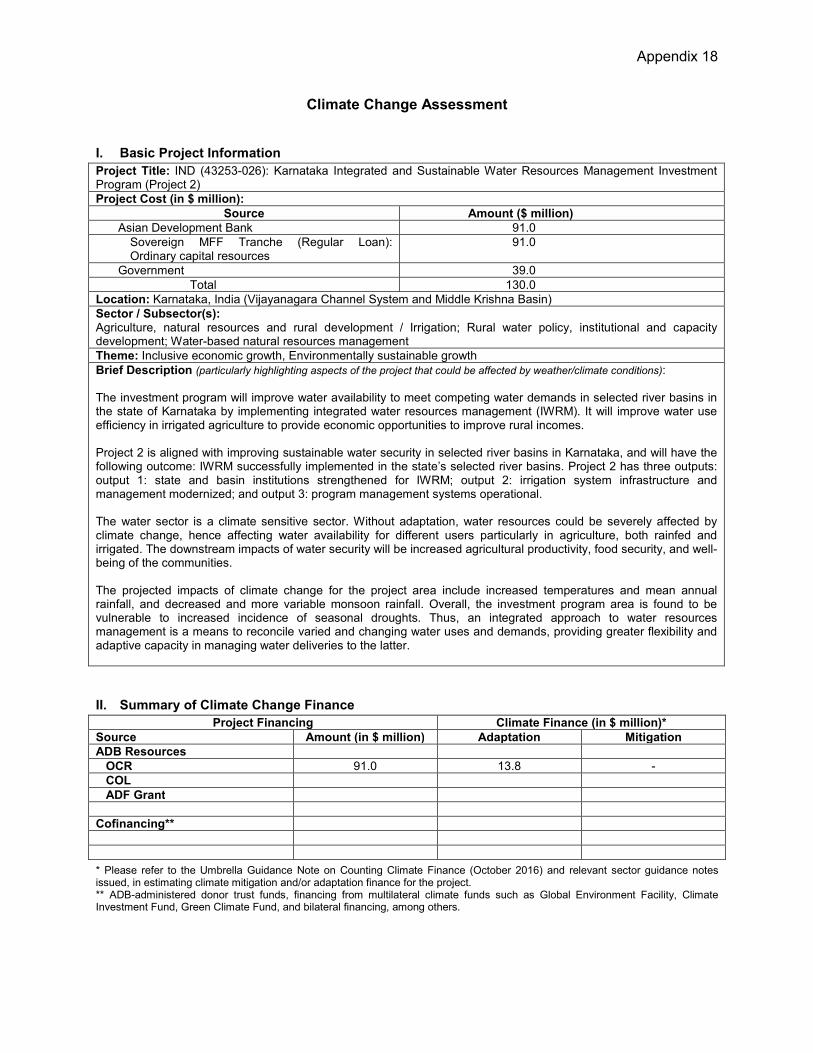

Project Number: 43253-026 MFF Number: 0085 September 2019 India: Karnataka Integrated and Sustainable Water Resources Management Investment Program (Tranche 2) (Part 2) This document is being disclosed to the public in accordance with ADB’s Access to Information Policy. Periodic Financing Request Report

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

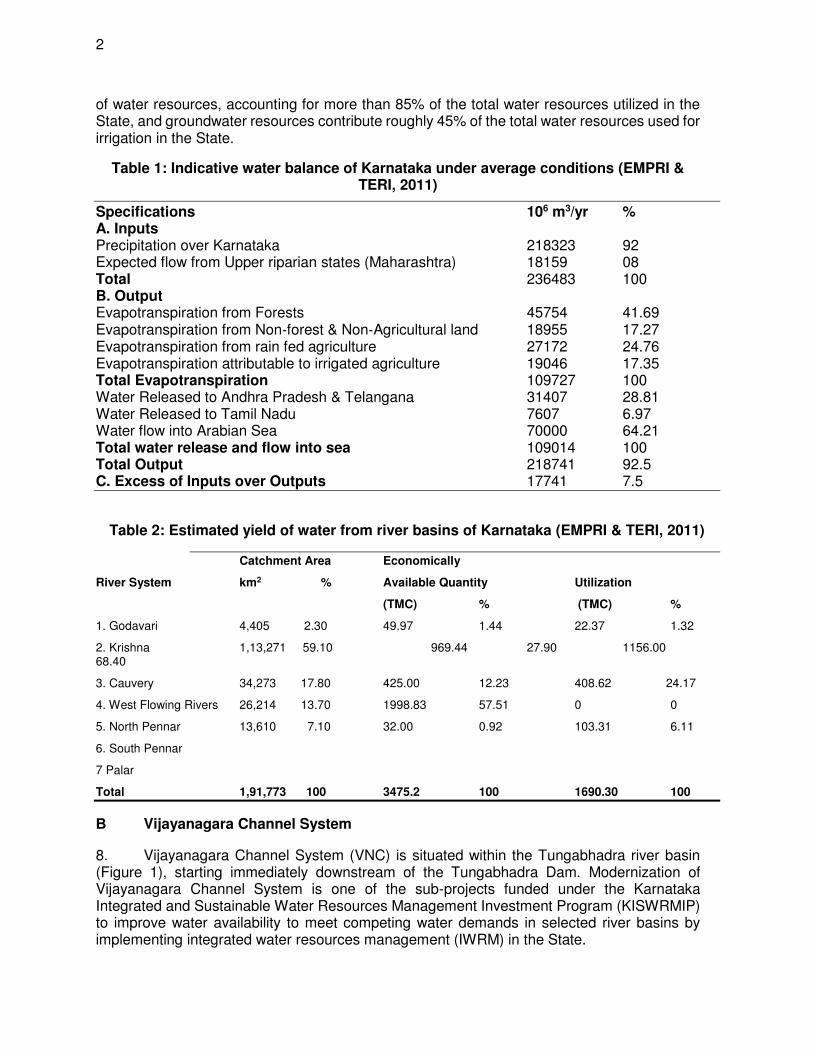

Project Number: 43253-026 MFF Number: 0085 September 2019

India: Karnataka Integrated and Sustainable Water Resources Management Investment Program (Tranche 2) (Part 2) This document is being disclosed to the public in accordance with ADB’s Access to Information Policy.

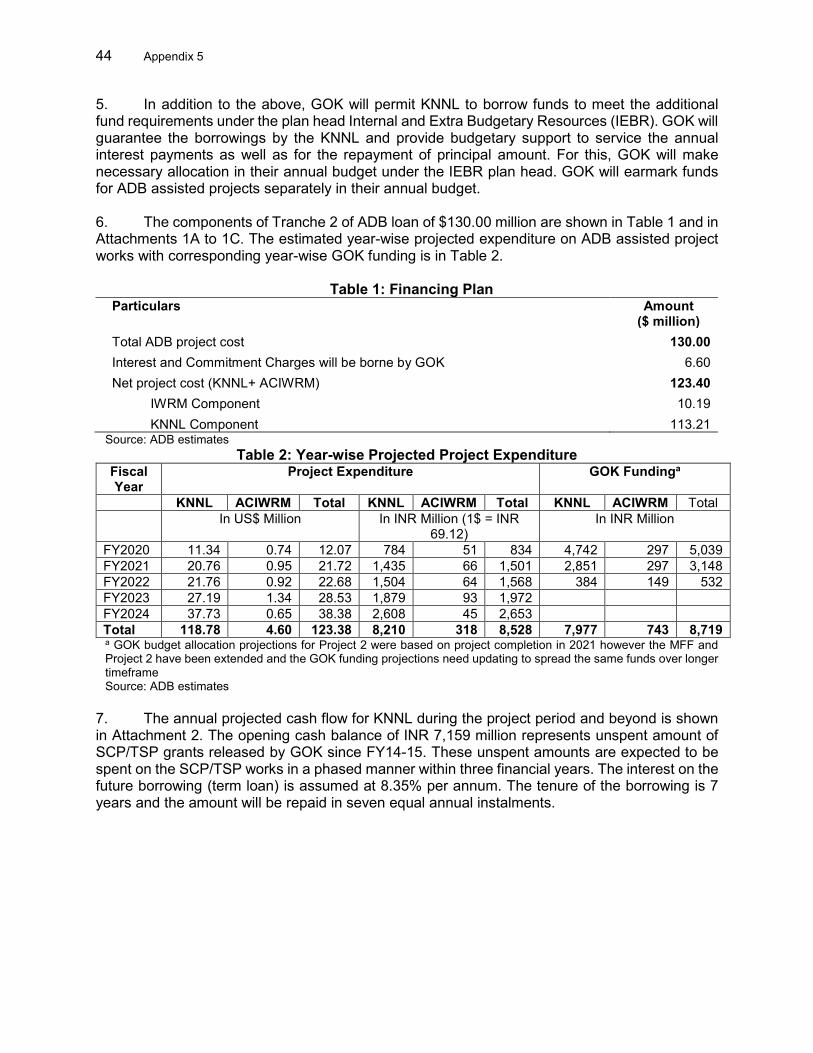

Periodic Financing Request Report

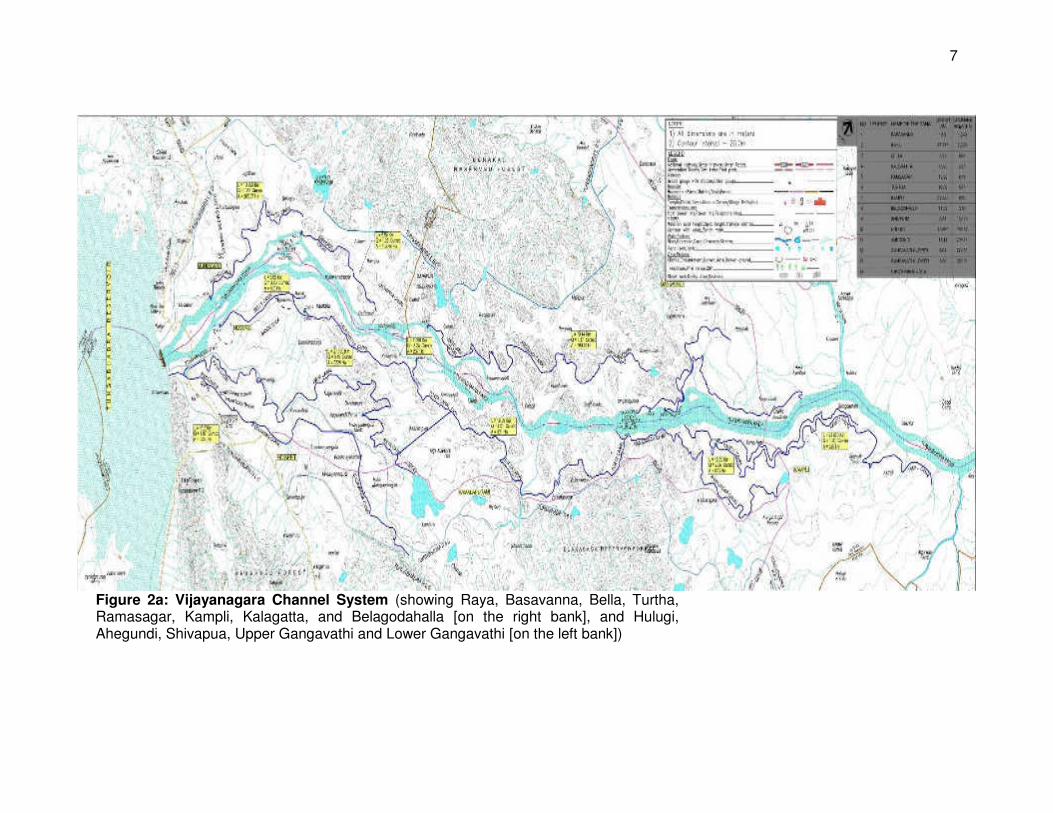

Appendix 14

KARNATAKA INTEGRATED AND SUSTAINABLE WATER RESOURCES MANAGEMENT INVESTMENT PROGRAM - TRANCHE 2

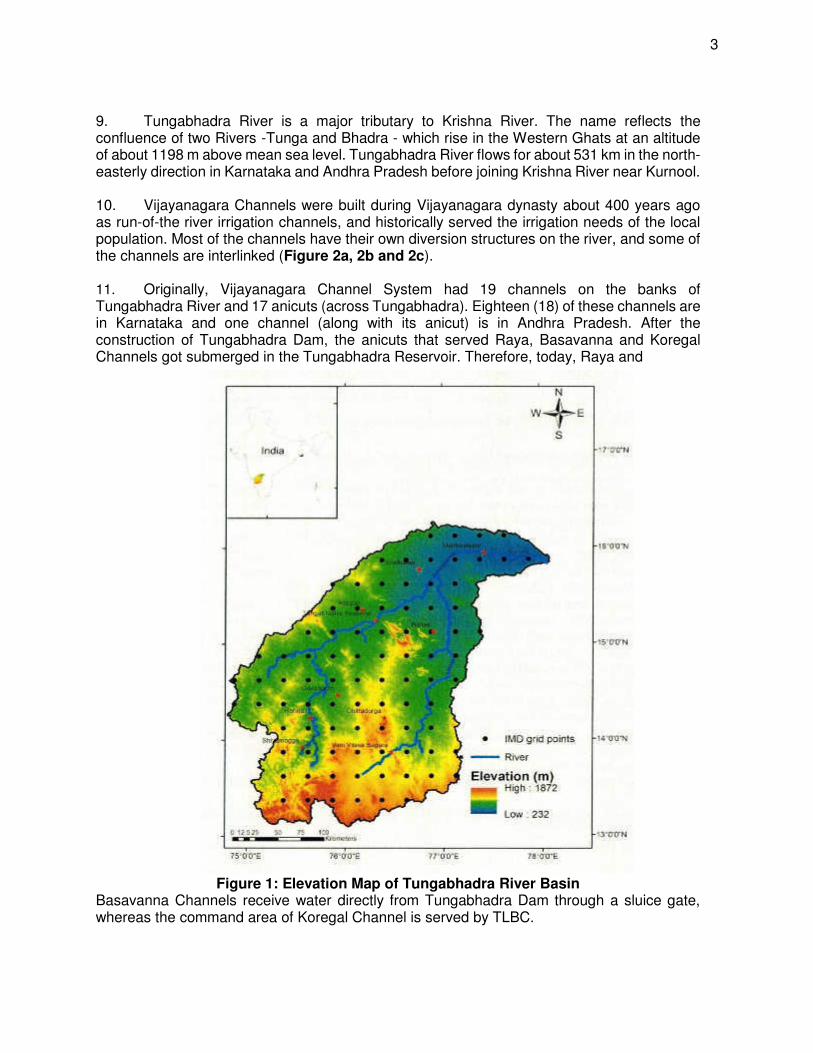

PROCUREMENT CAPACITY ASSESSMENT

September 2019

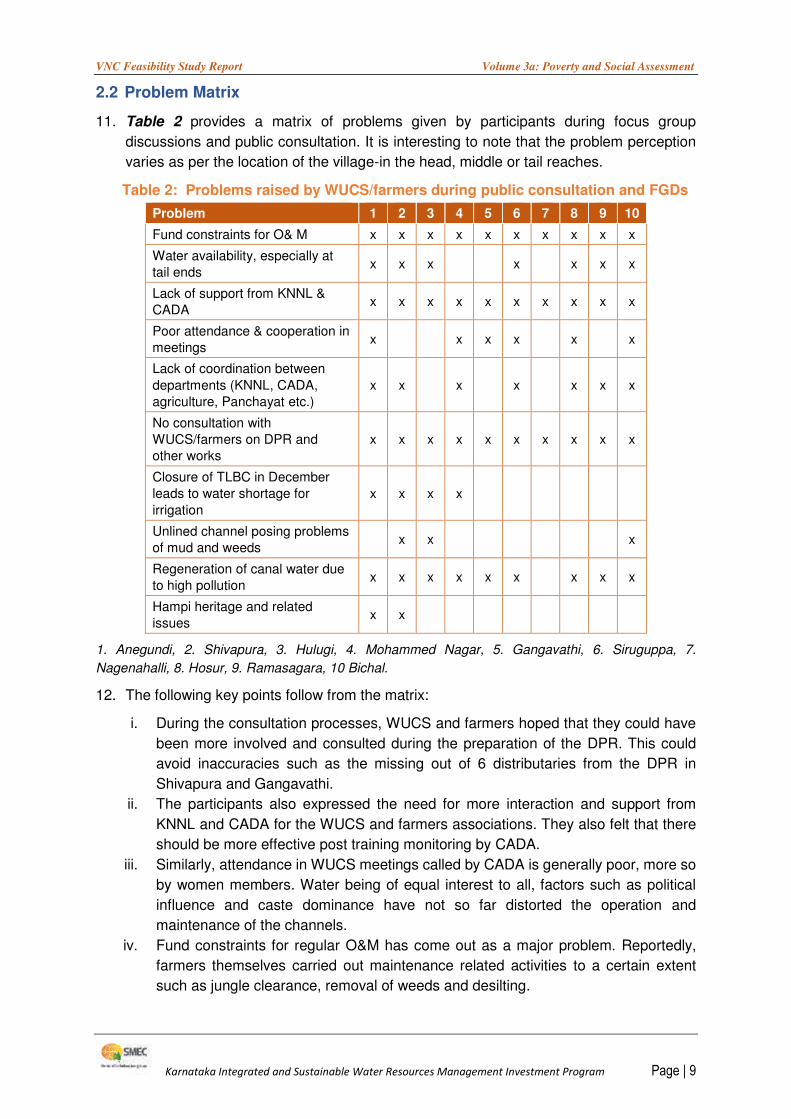

ABBREVIATIONS

ACIWRM – Advanced Centre for Integrated Water Resources Management ADB – Asian Development Bank CAD – command area development CADA – Command Area Development Authority CAG – Comptroller and Auditor General of India CE – Chief Engineer CPP – community procurement packages EA – Executing Agency EE – executive engineer EMD – earnest money deposit GFR – General Financial Rules GOK – Government of Karnataka ha – hectares ICB – international competitive bidding INR – Indian Rupees IWRM – Integrated Water Resources Management KISWRMIP – Karnataka Integrated and Sustainable Water Resources

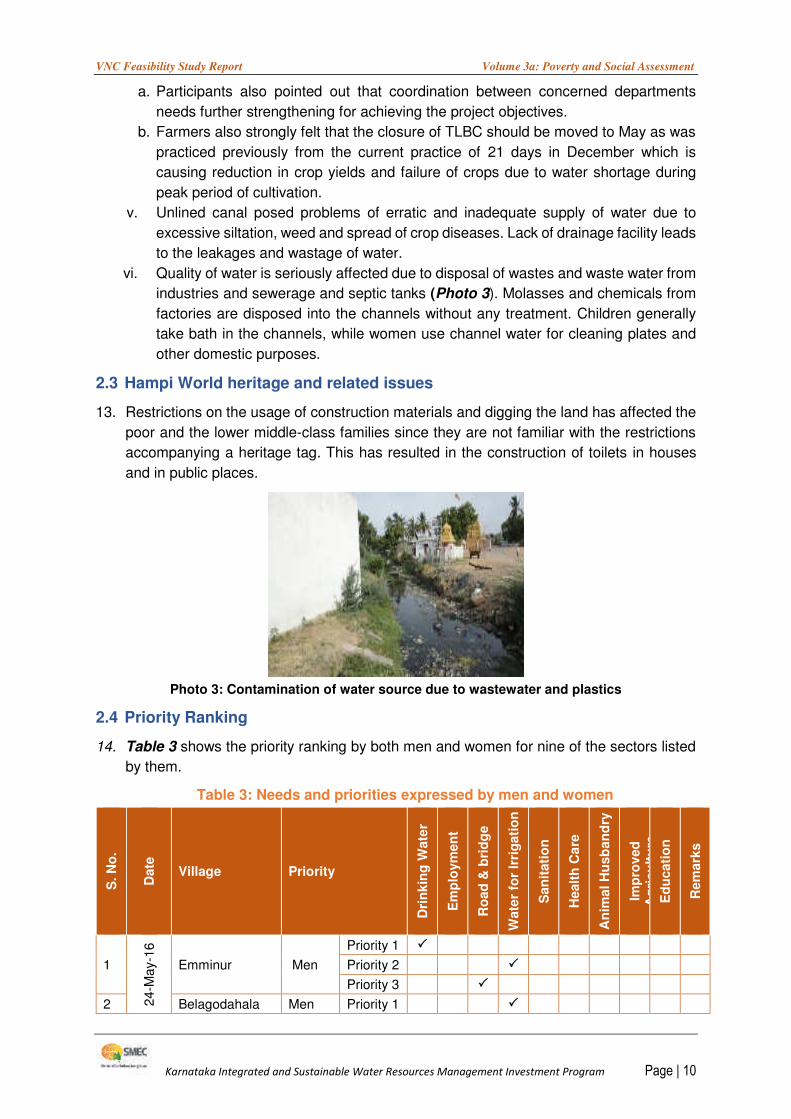

Management Investment Program KNNL – Karnataka Neeravari Nigam Limited KTPPA – Karnataka Transparency in Public Procurements Act MFF – Multi-tranche Financing Facility NA Not applicable NCB – national competitive bidding NGO – non-governmental organization PCA – procurement capacity assessment PMU – Program Management Unit P-RAMP – Procurement Risk Assessment and Management Plan PIO – Project Implementation Office PSC – Project Support Consultants SE – Superintending Engineer SBD – standard bidding documents TLBC – Tungabhadra Left Bank Canal TEC – Tender Evaluation Committee TSC – Technical Sub-Committee US$ or $ – United States Dollar VNC – Vijayanagara Channels WALMI – Water and Land Management Institute WB – World Bank WRD – Water Resources Department WUCS – Water Users Co-operative Societies

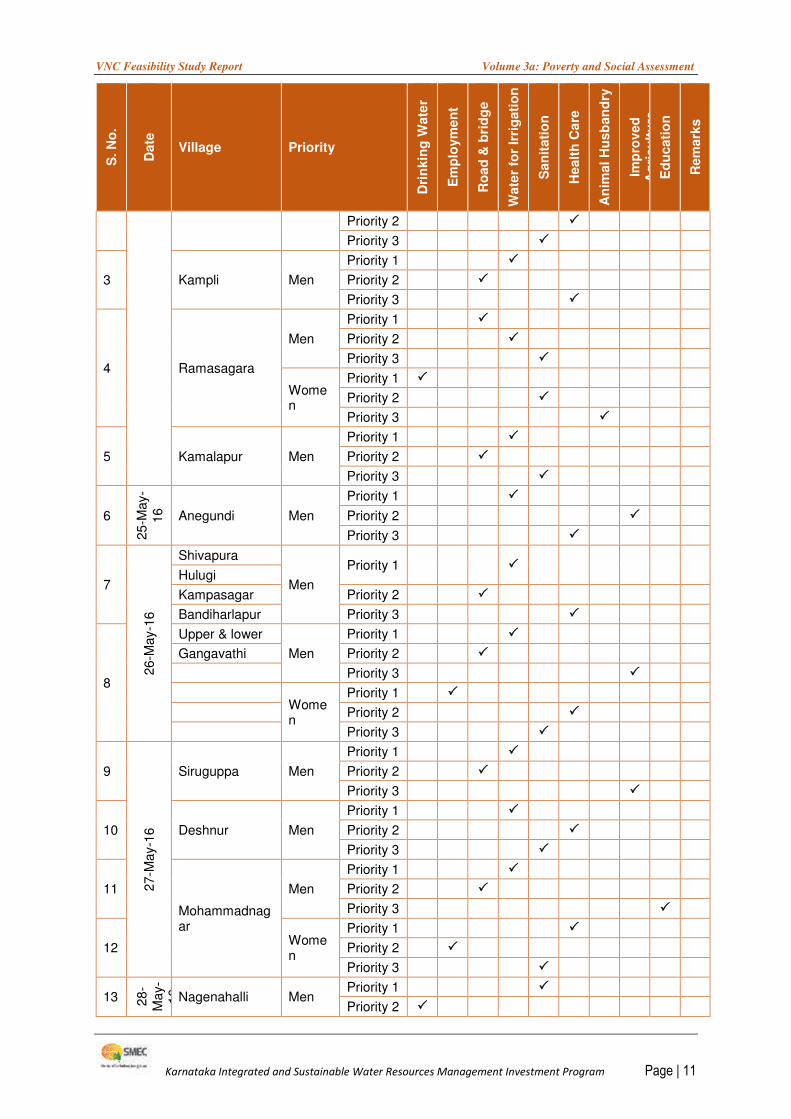

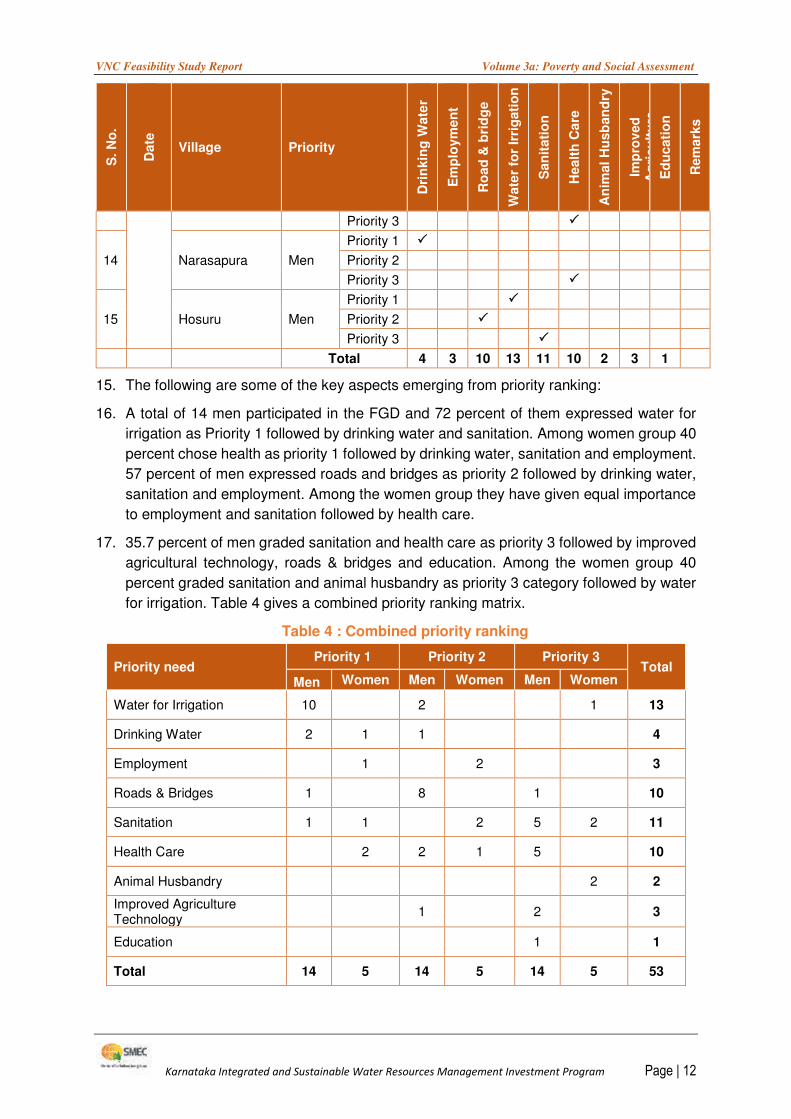

TABLE OF CONTENTS

Page No. EXECUTIVE SUMMARY iv

I. INTRODUCTION 1

A. Description of the Investment Project 1

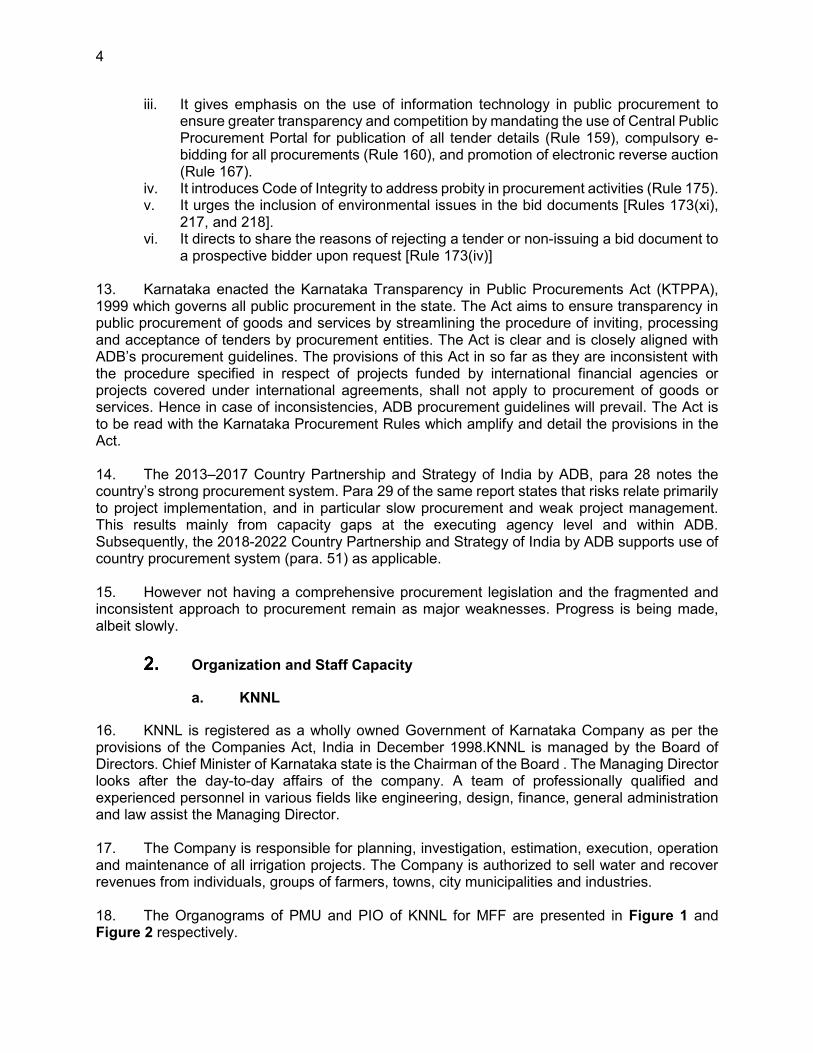

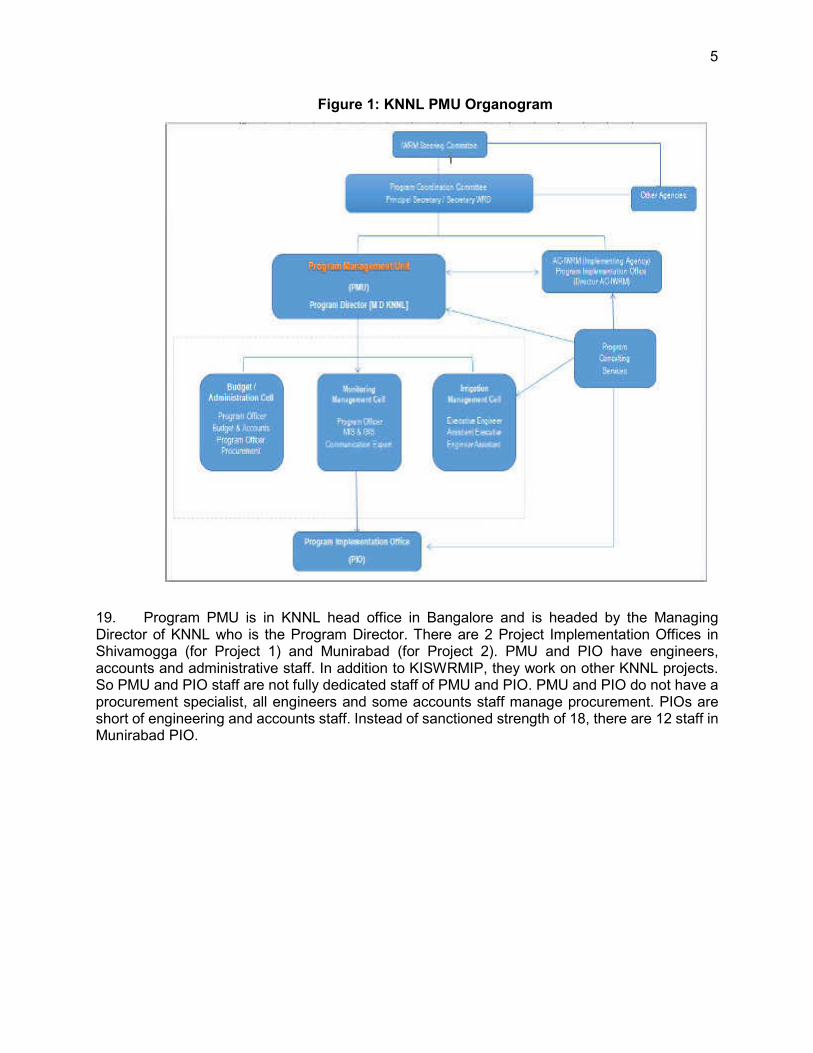

II. PROJECT PROCUREMENT RISK ASSESSMENT 3

A. Overview and Assessment 3

1. Legislative and Regulatory Framework 3

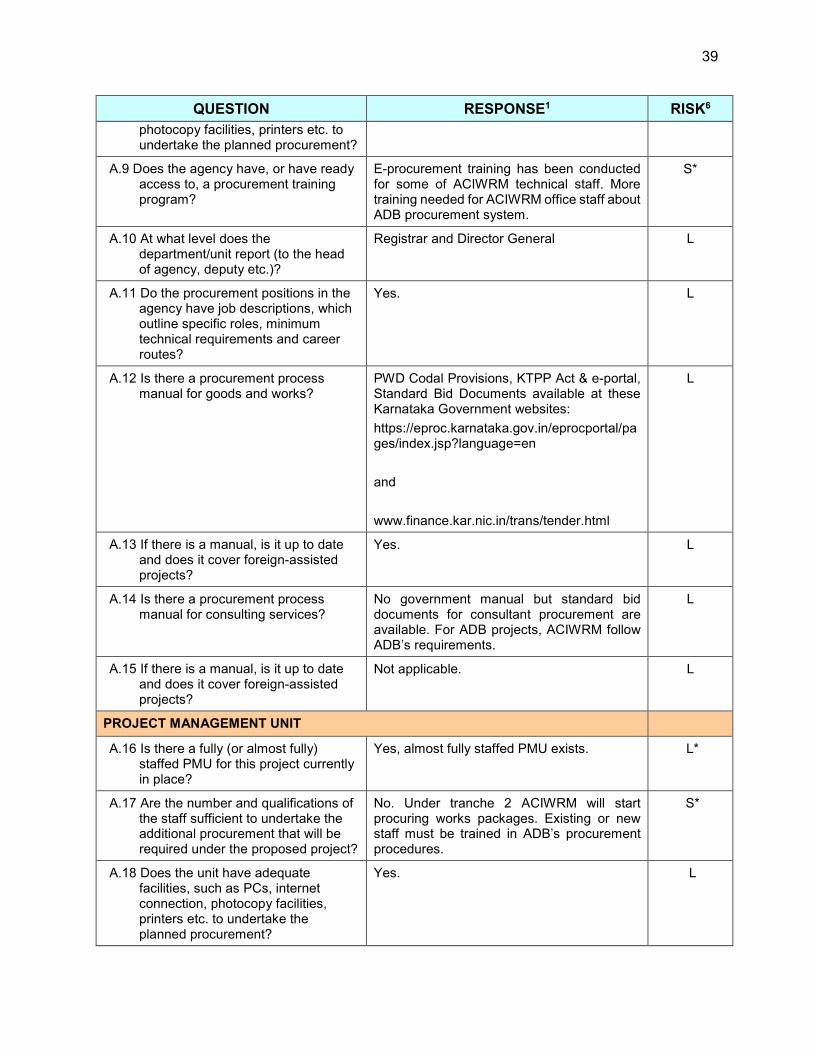

2. Organization and Staff Capacity 4

3. Information Management 11

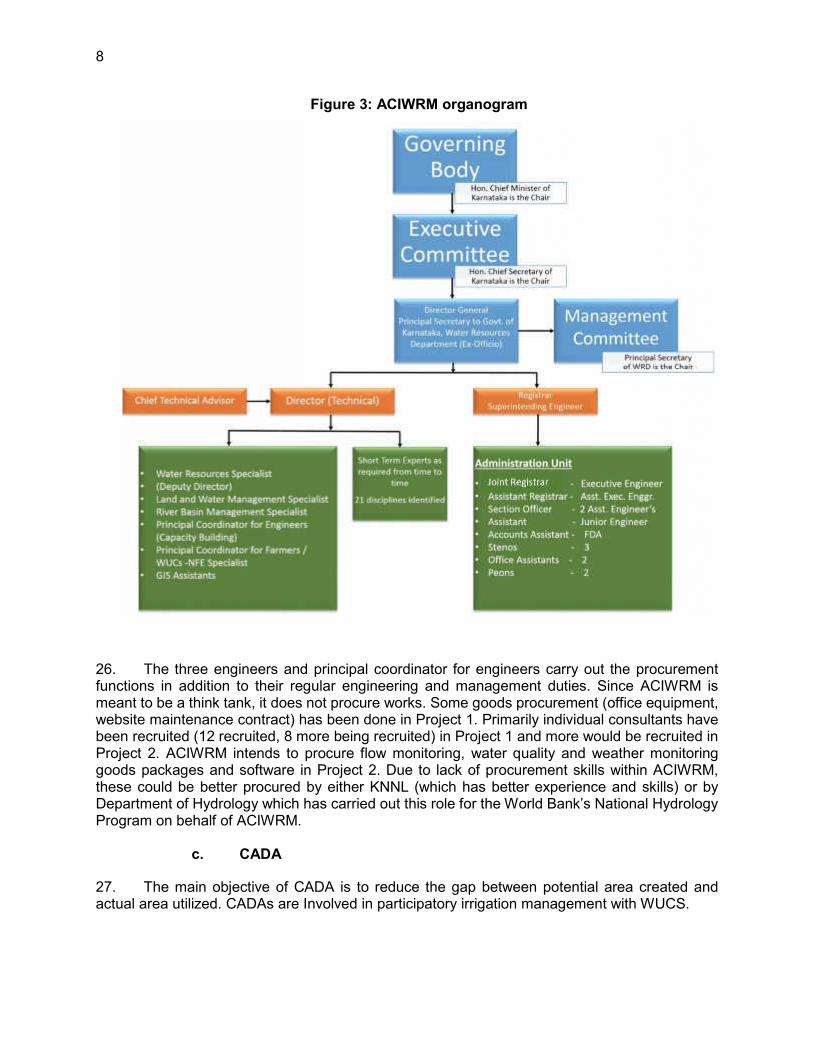

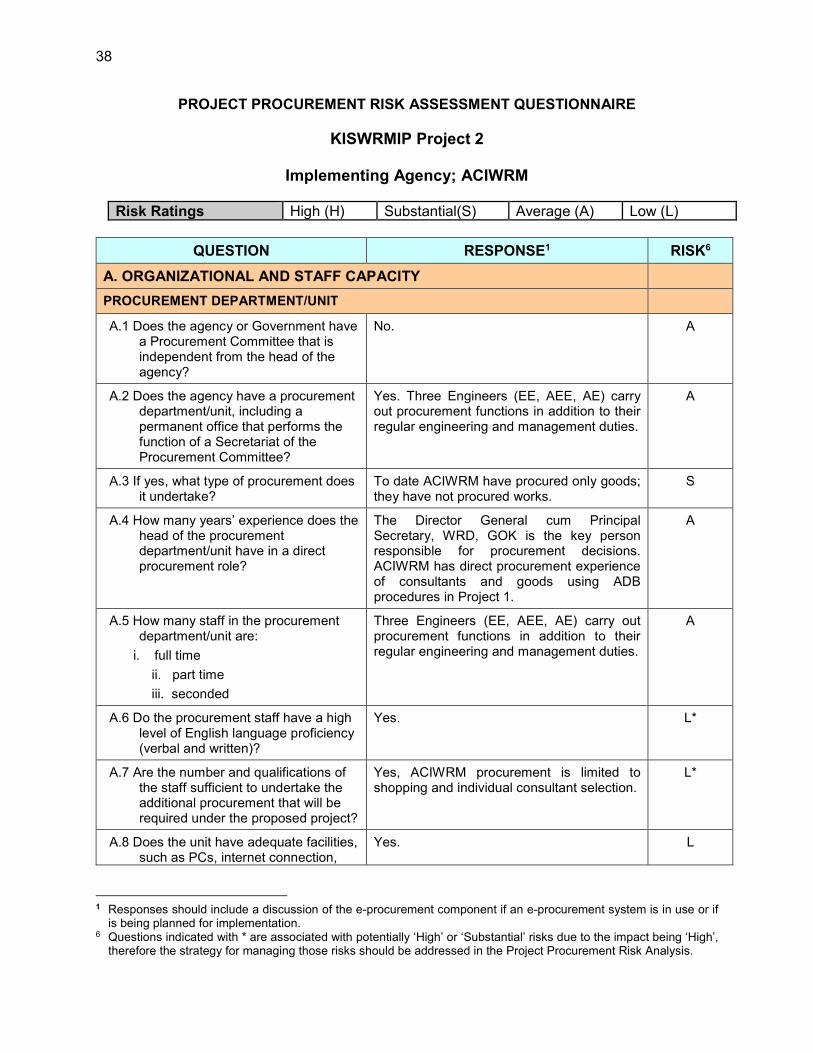

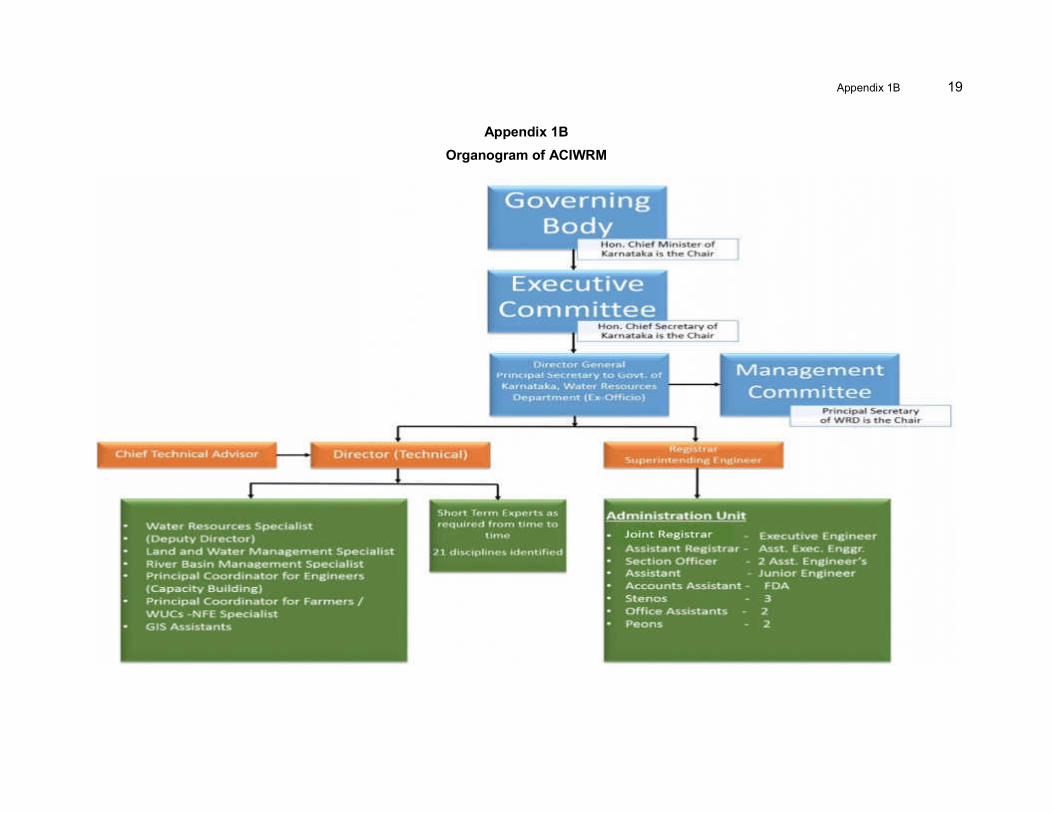

4. Procurement Practices 12

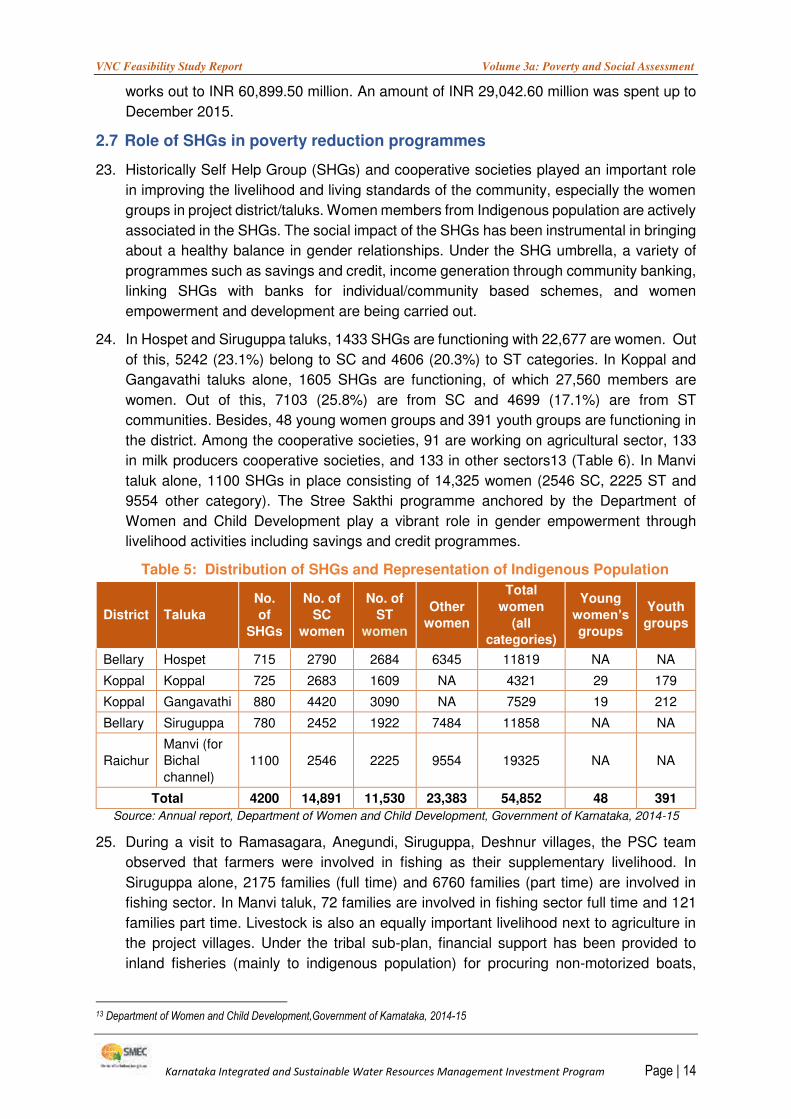

5. E-Procurement 21

6. Effectiveness 22

7. Accountability Measures 22

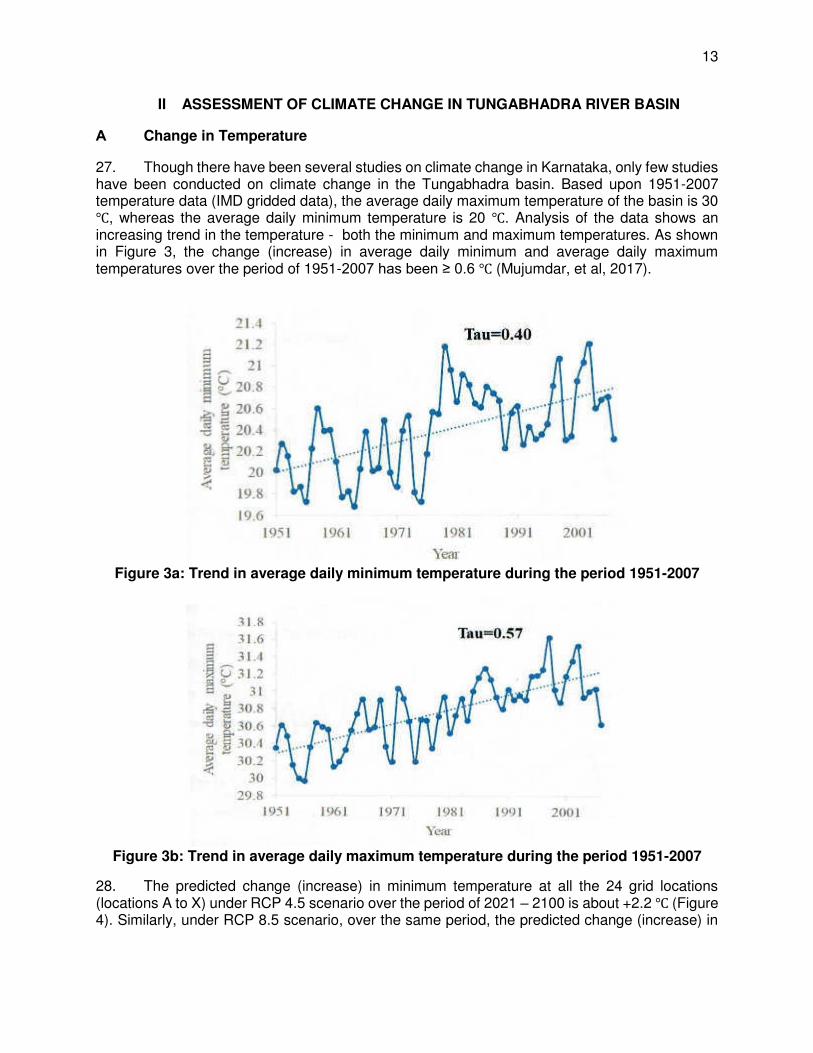

B. Strengths 23

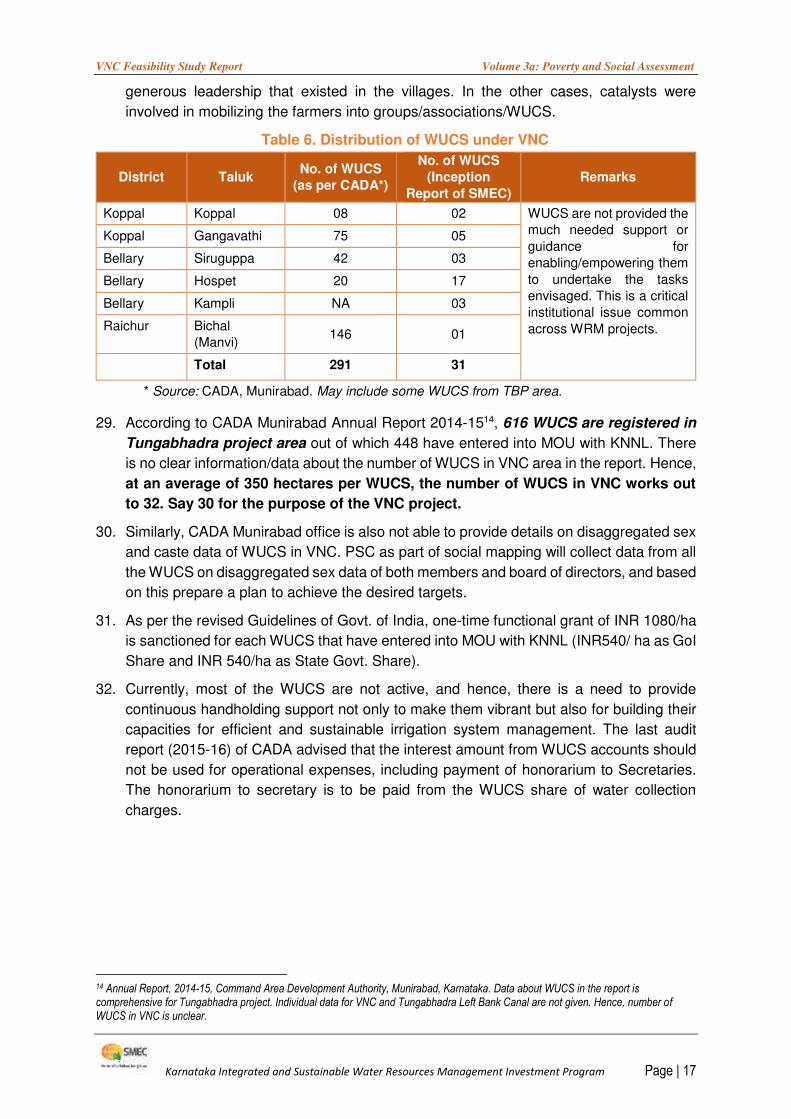

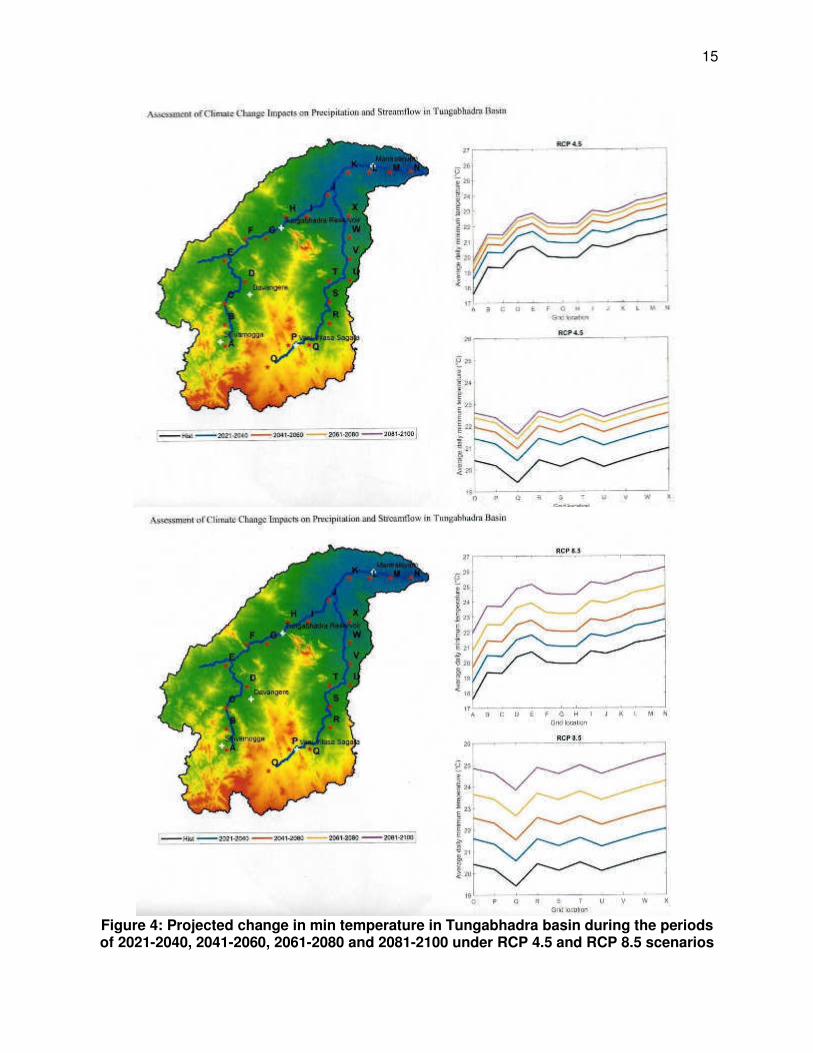

C. Weaknesses 23

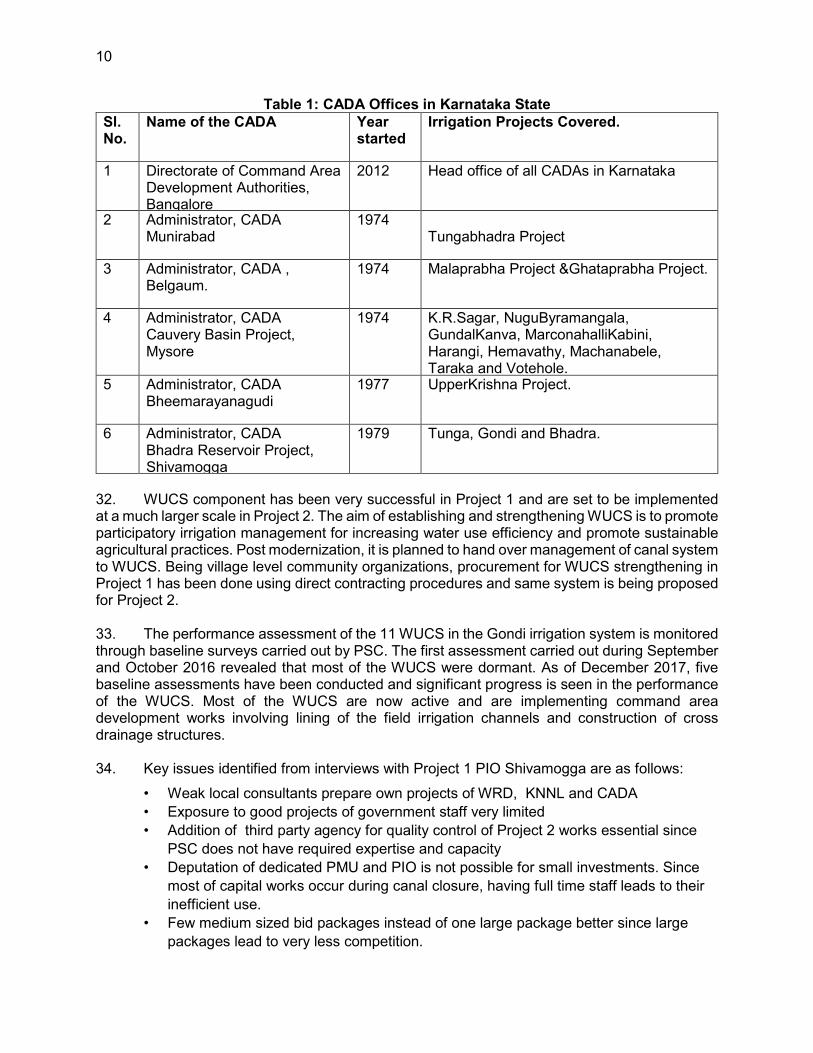

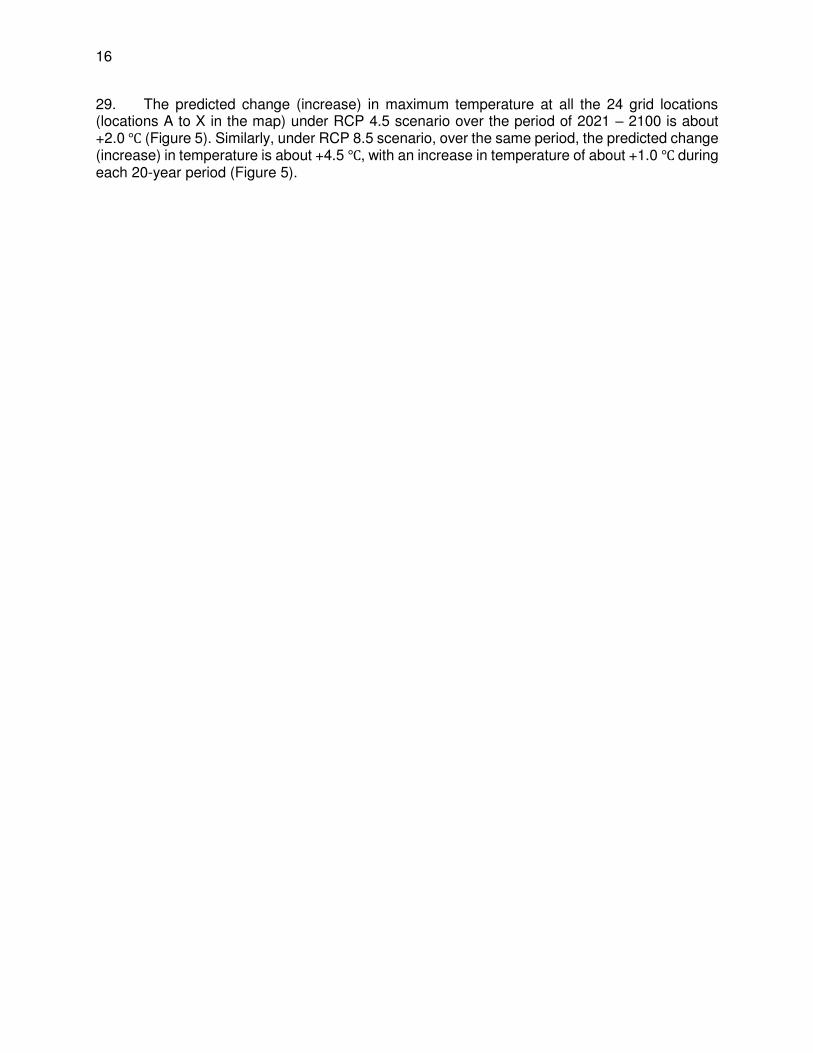

D. Procurement Risk Assessment and Management Plan (P-RAMP) 24

III. PROJECT SPECIFIC PROCUREMENT THRESHOLDS 26

IV. PROCUREMENT PLANS 27

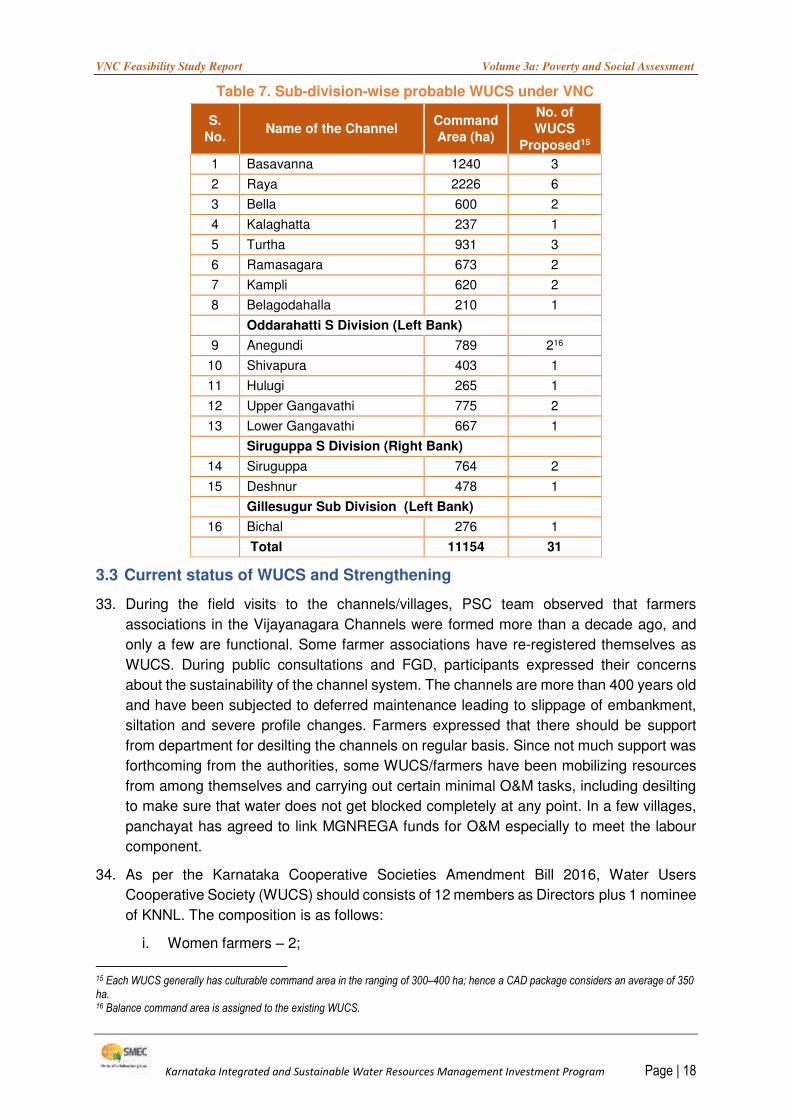

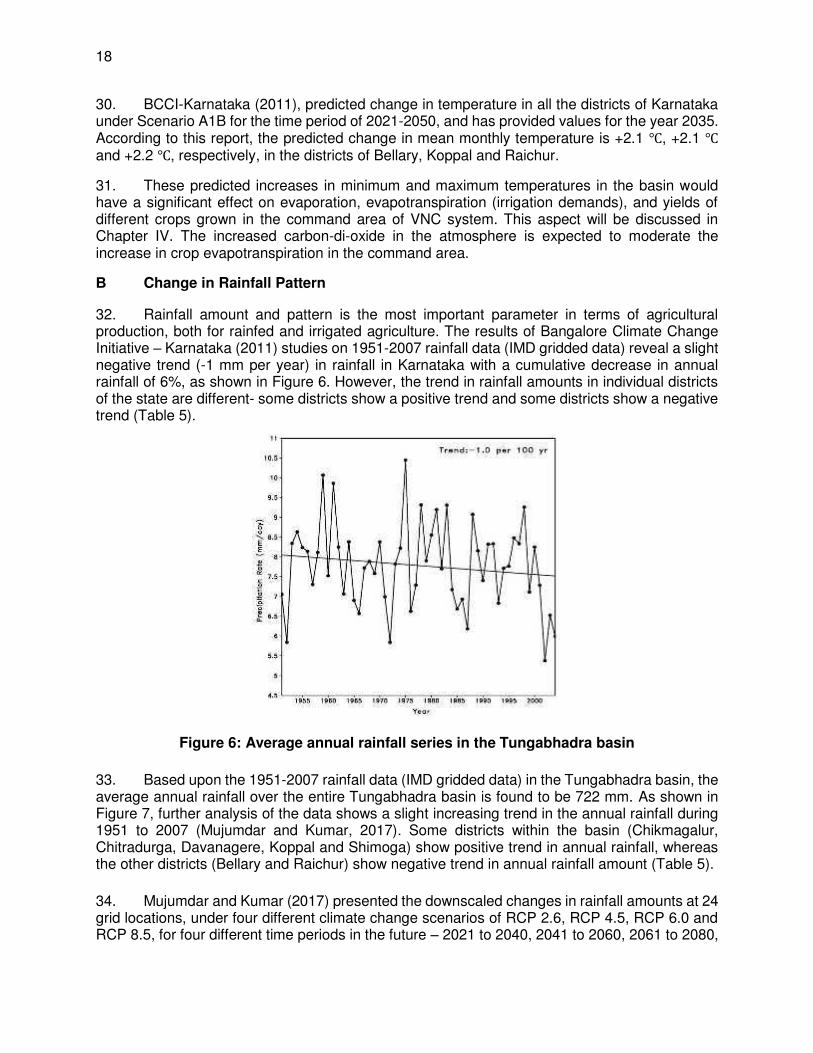

V. CONCLUSIONS 28

ANNEXES Annex 1: Completed PCA questionnaires of KNNL and ACIWRM. 37 Annex 2: Project Procurement Classification 56 Annex 3: Draft Procurement Plan of KISWRMIP Project 2 57

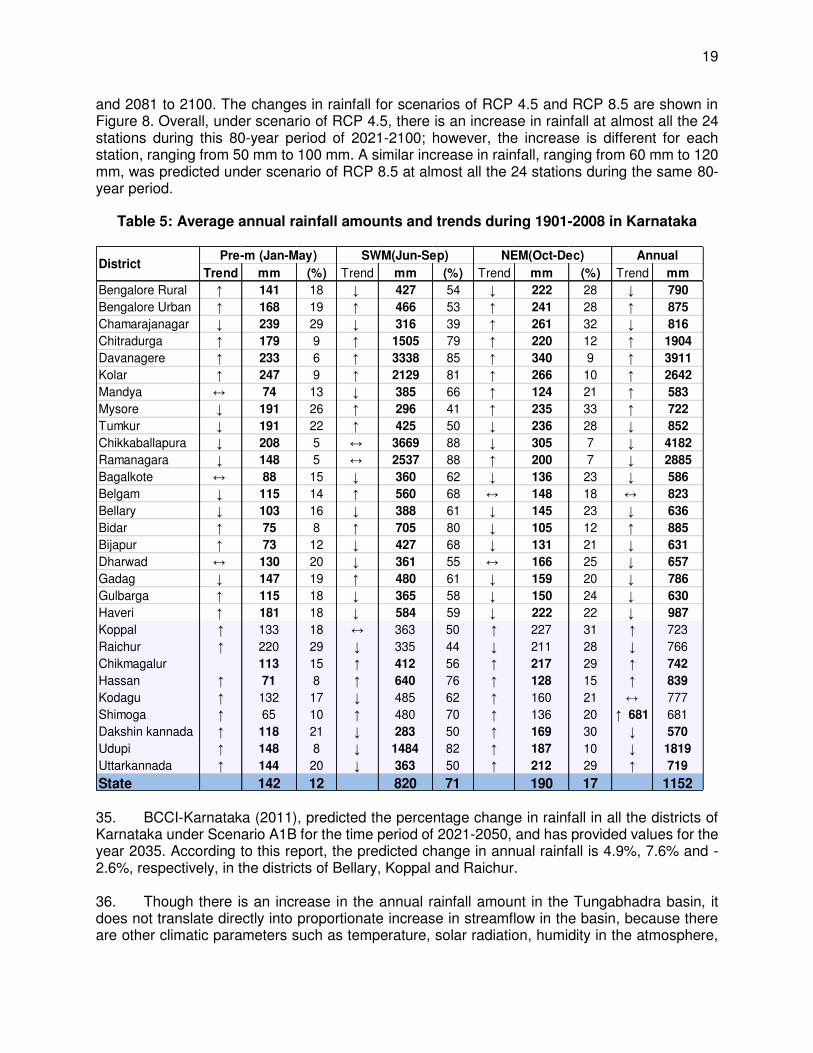

EXECUTIVE SUMMARY A. Overall assessment of Project-2 procurement risk and classification

1. Karnataka Integrated and Sustainable Water Resources Management Investment Program (KISWRMIP) – Project 2 is proposed for financing by the Asian Development Bank (ADB). A procurement capacity assessment has been undertaken for Karnataka Neeravari Nigam Ltd. (KNNL, the executing agency) and the Advanced Center for Integrated Water Resources Management (ACIWRM). The assessment was carried out following ADB’s guide on assessing Procurement Risks and Determining Project Procurement Classification. It has determined that, for Project 2, the procurement risk is moderate, and the procurement classification is category B.

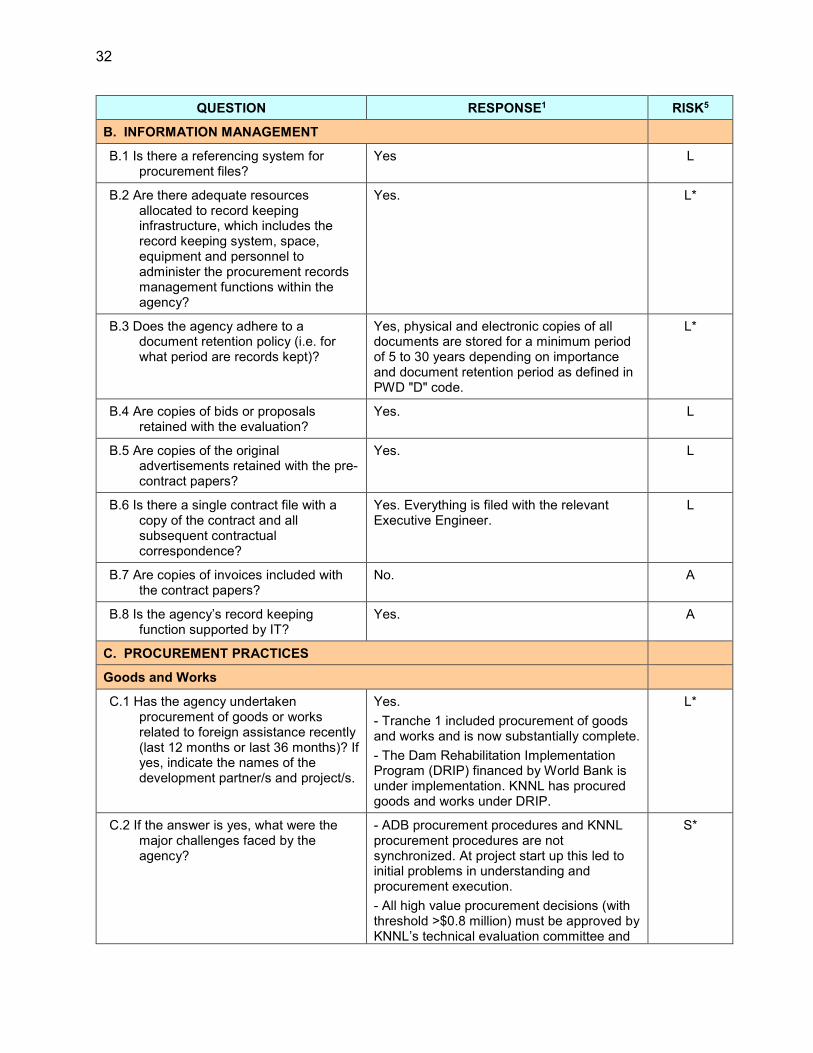

2. The completed procurement capacity assessment questionnaires for KNNL and ACIWRM are presented in Annex 1 and the completed project procurement classification is at Annex 2. Based on the procurement capacity assessment carried out and the current thresholds for India, it is recommended that prior review limits and procurement thresholds for KISWRMIP Project 2 be retained as for Project 1, and this is reflected in draft Procurement Plan in Annex 3.

B. Summary of identified weaknesses and risks

3. KNNL and ACIWRM have the benefit of having substantially completed Project 1 of the same investment program. However, there were substantial delays in procuring a works package and consultant selection during the startup of Project 1.

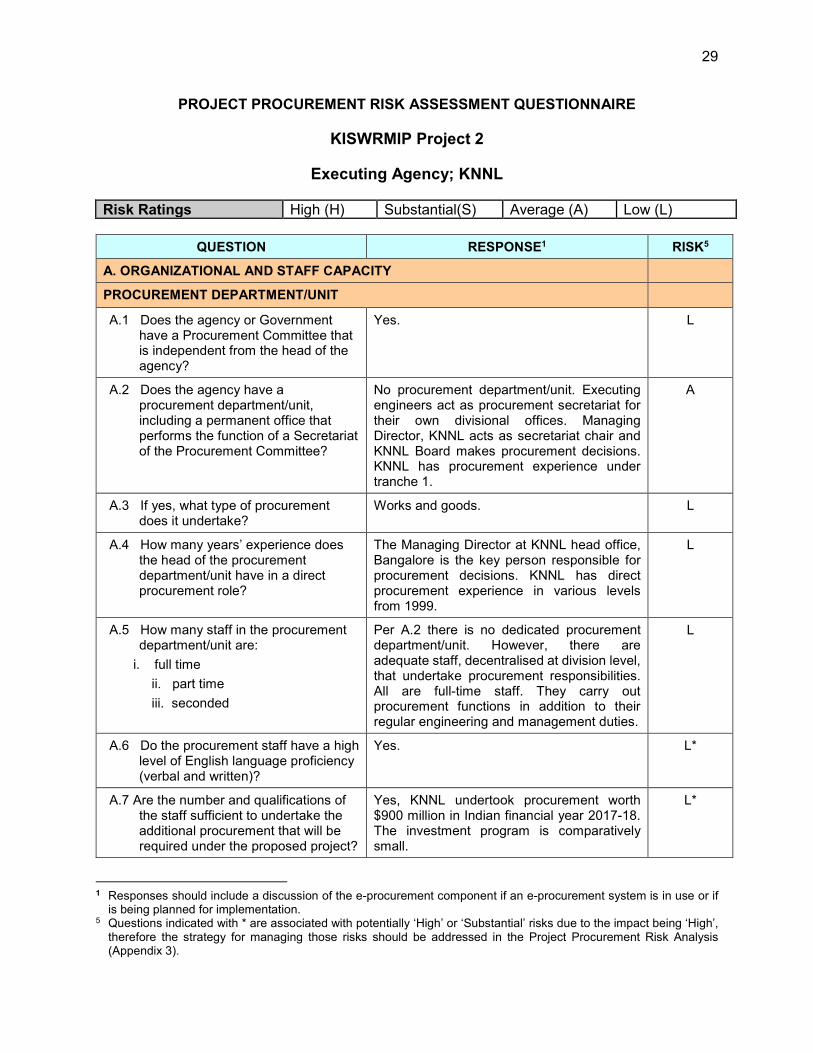

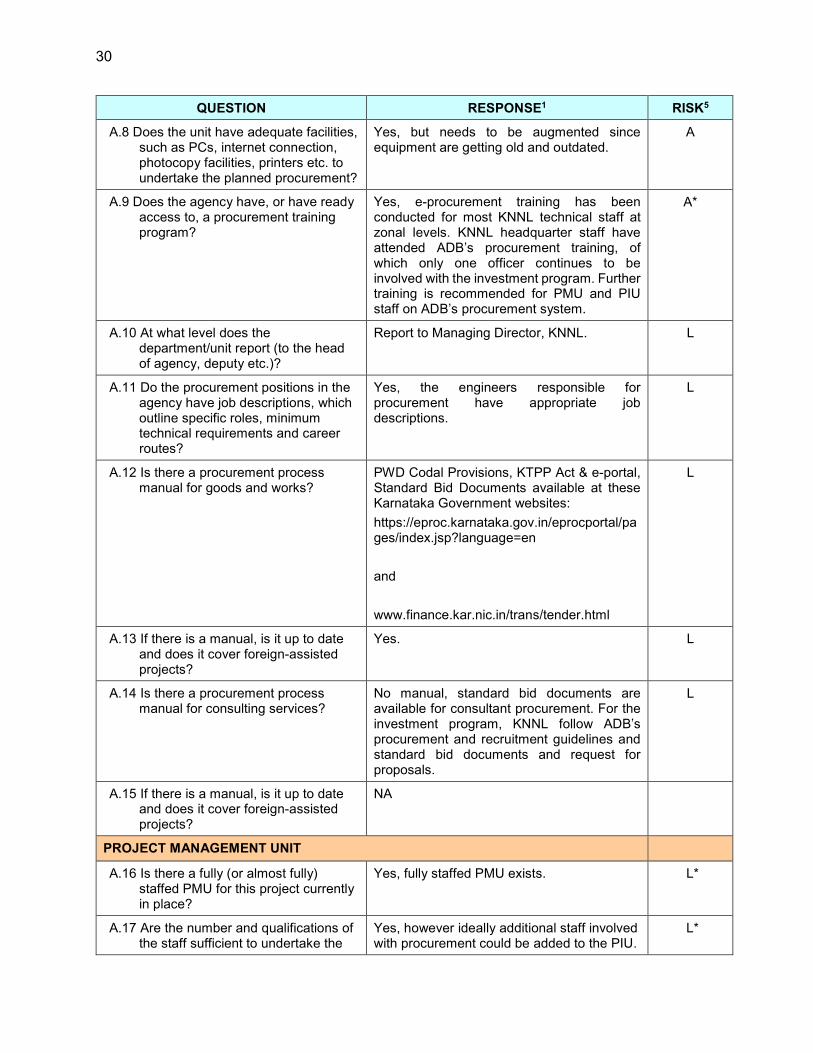

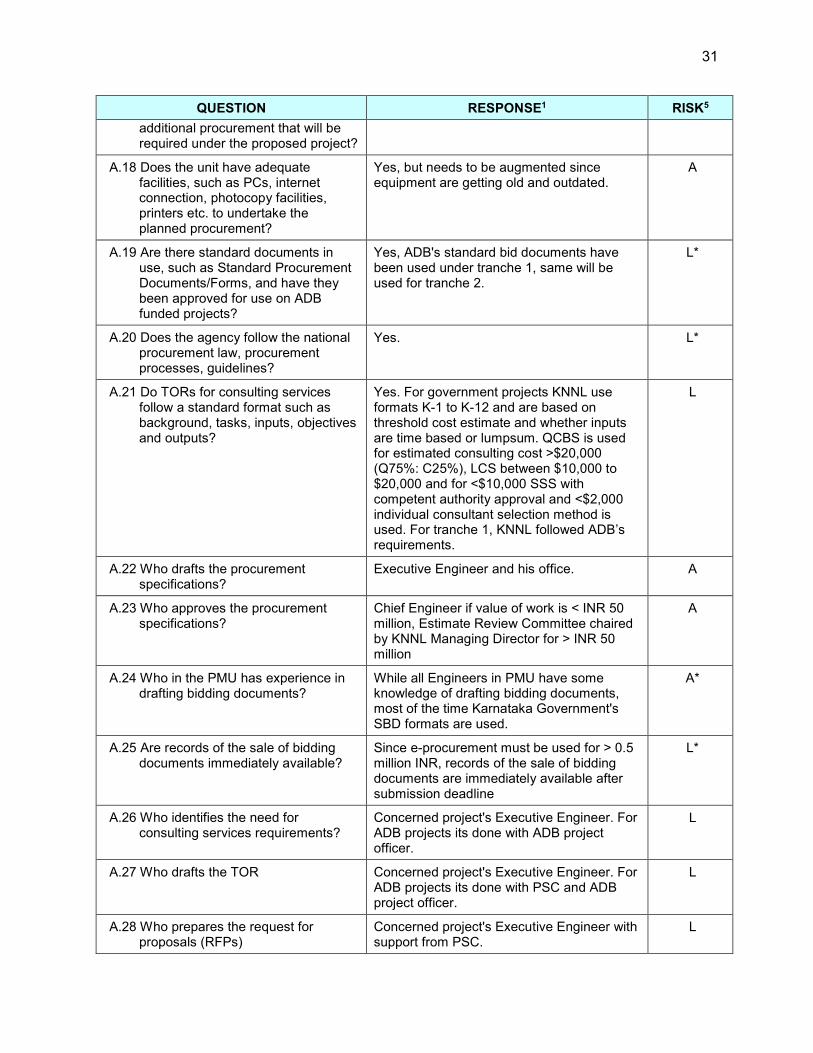

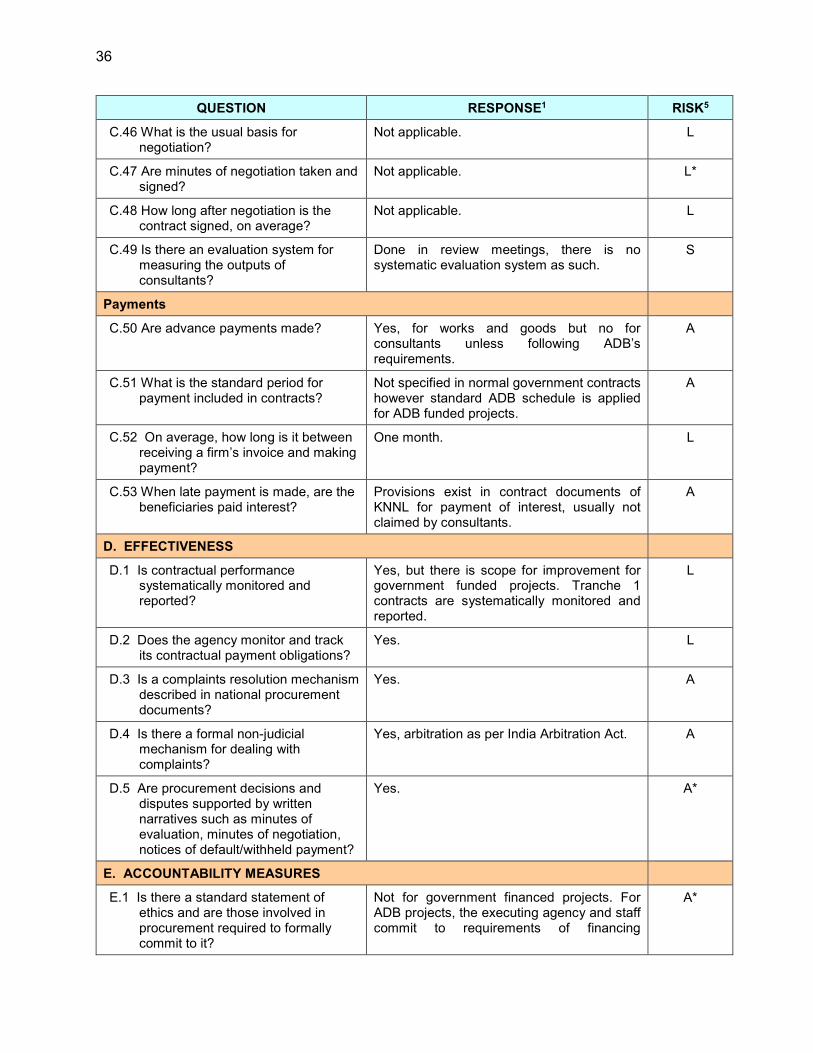

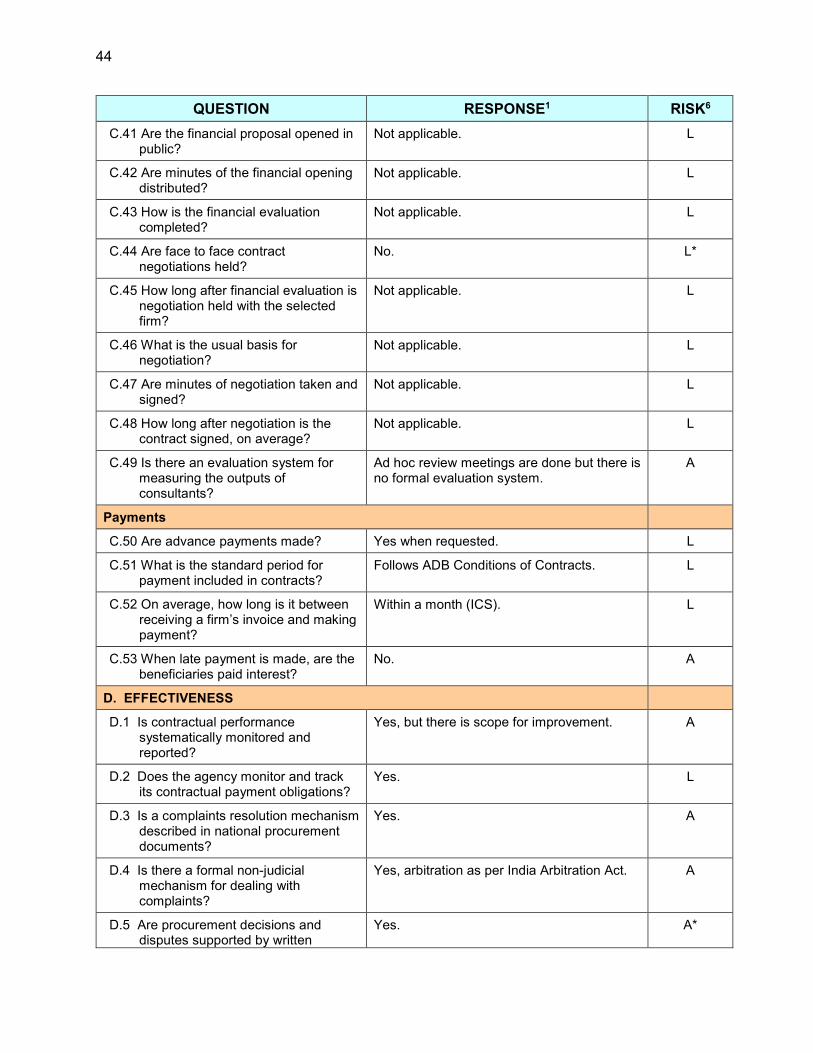

4. Faulty or delayed procurement due to lack of adequate and relevant procurement training and experience within PMU and ACIWRM is a risk. Procurement of some key packages was delayed in Project 1. There are no procurement specialists in PMU, PIO and ACIWRM. Mostly Engineering staff with little consultant support manage procurement functions which is less efficient than having full time procurement staff. All staff in PMU (except one part time consultant) and PIO comprise people seconded from government, most of them are not well versed with ADBs procurement processes. No clear separation of engineering, procurement and regulatory functions exist within PMU, PIO and ACIWRM.

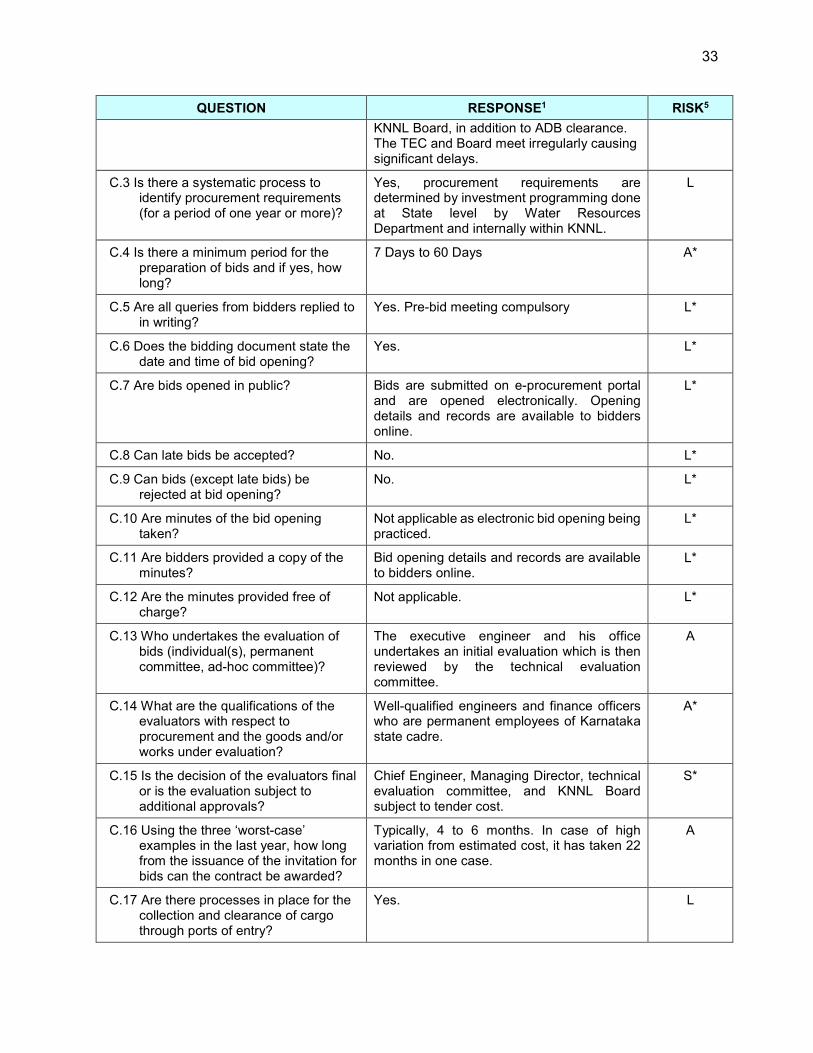

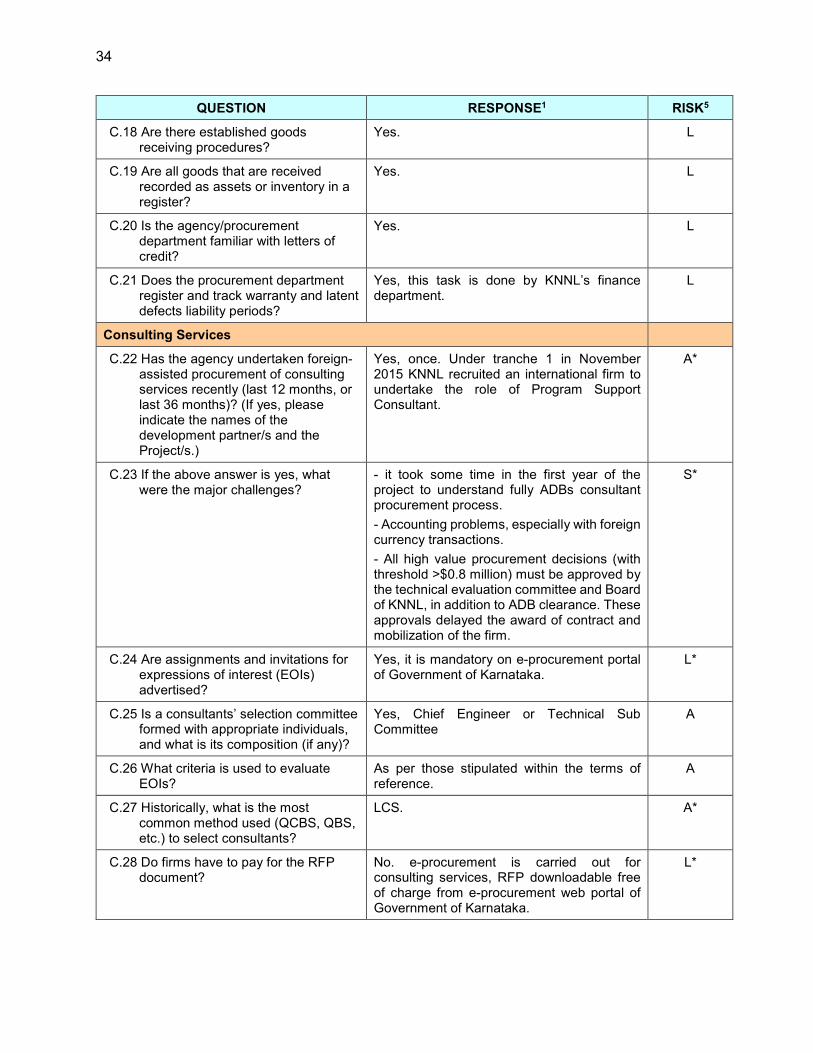

5. Low thresholds of bid evaluation and contract award approval authority of Project Directors of KNNL and ACIWRM have led to many approval levels through which procurement approvals move up and down, resulting in delays in procurement decision making. There are 3 three levels of approval for large contracts in KNNL (TEC, TSC, and KNNL Board) due to which delays occur. Decisions on contract variations, processing invoices get delayed. Experienced PMU & PIO staff get transferred leading to loss of program institutional memory.

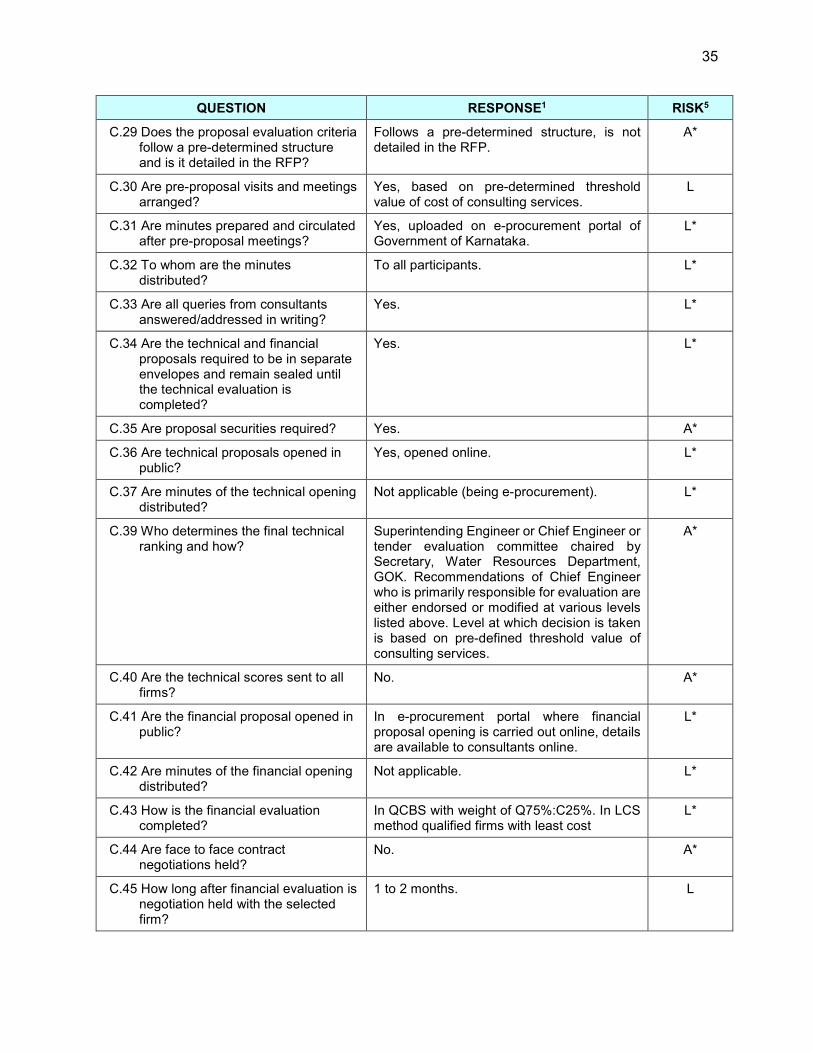

6. Below par performance of PSC related to procurement expert deployment and support to PMU, due to absence of systematic evaluation system for measuring the outputs of consultants by PMU is a risk. PSC has resorted to multiple replacements of experts.

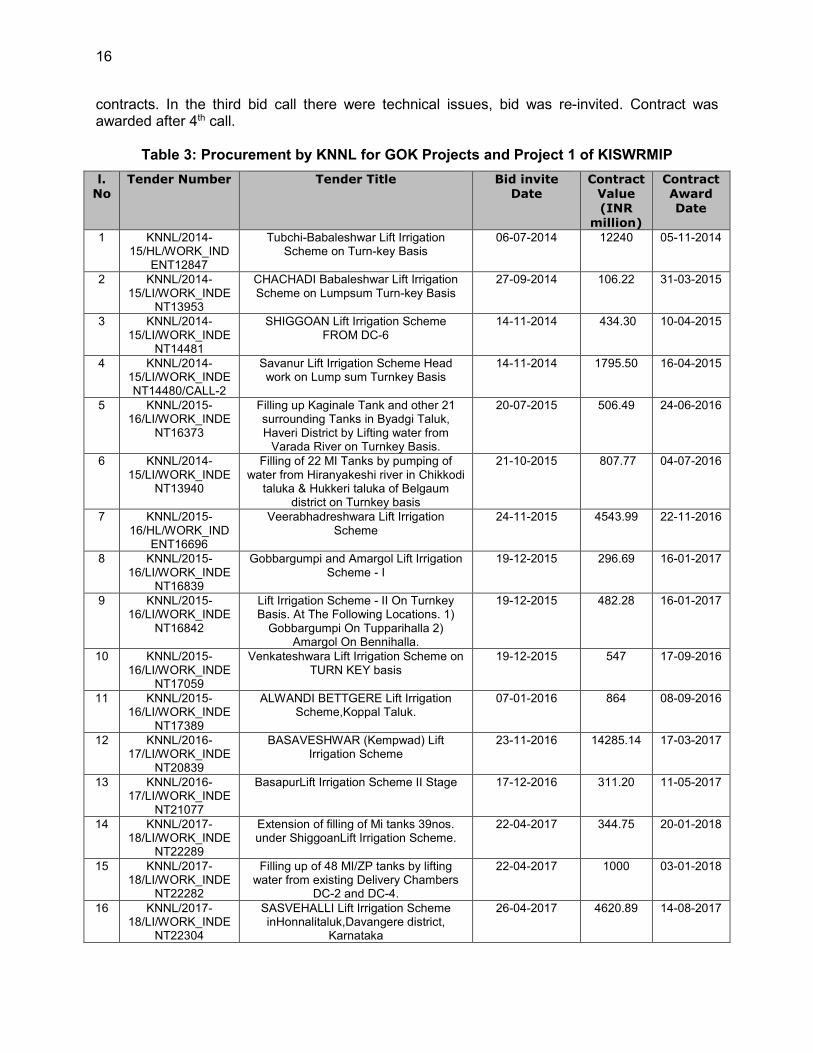

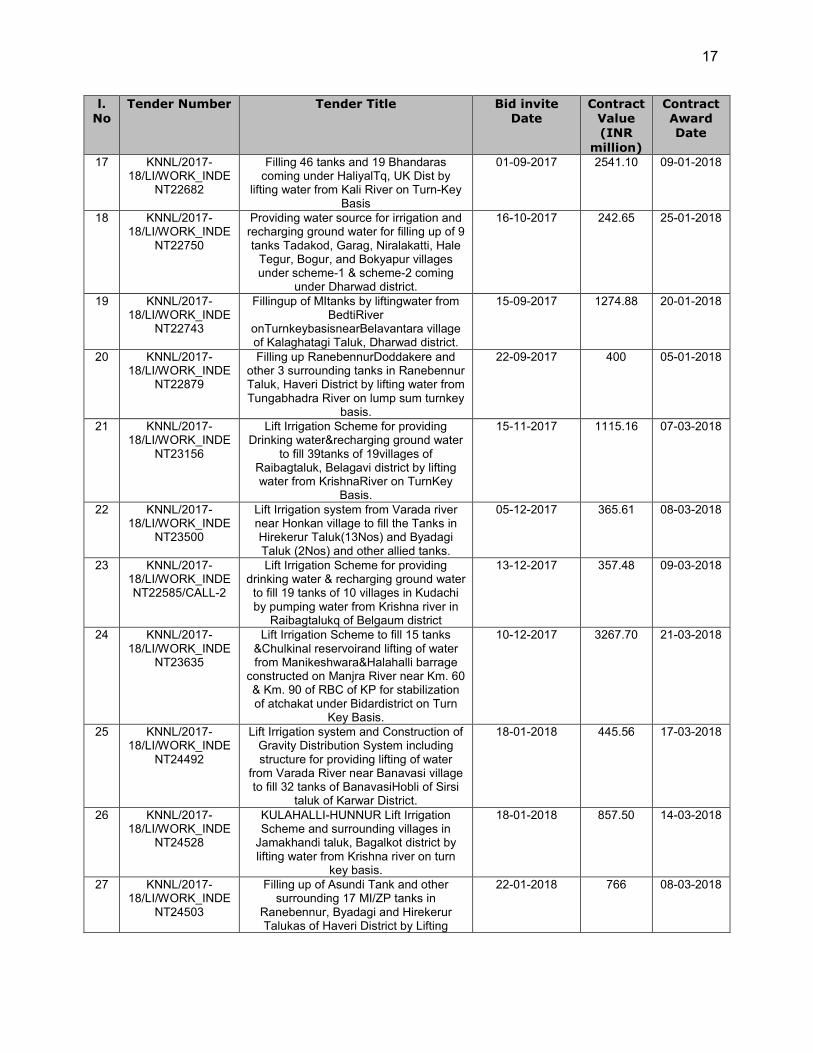

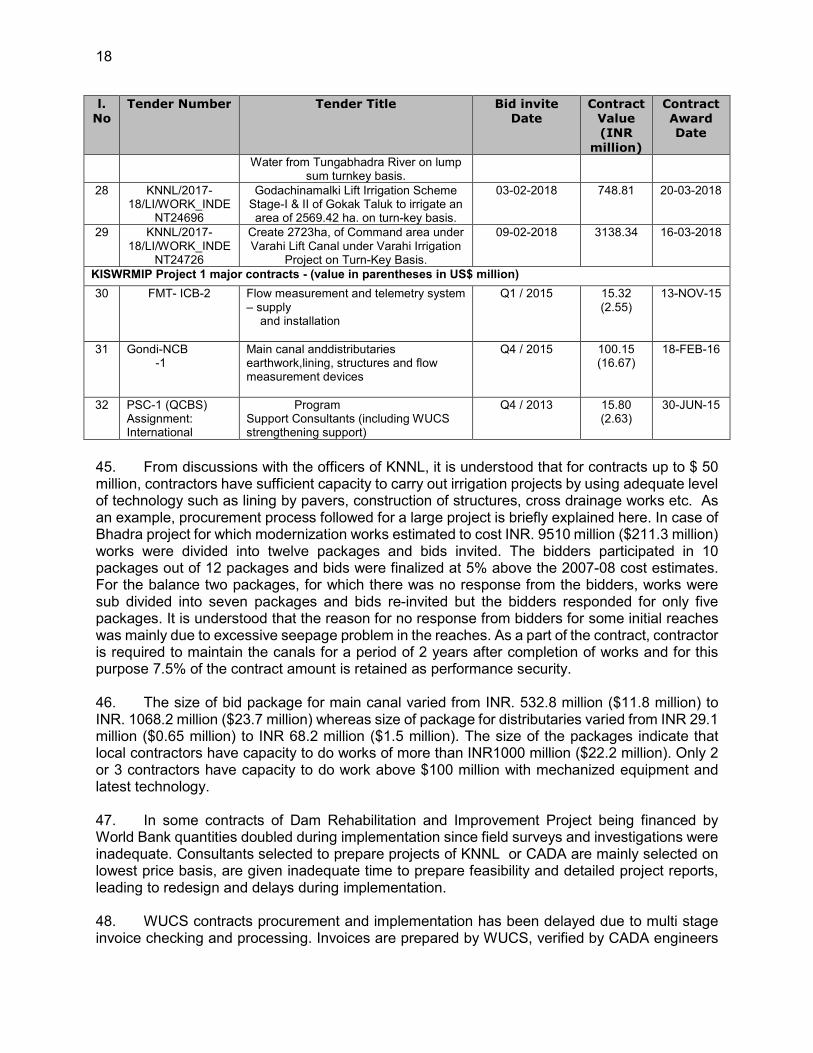

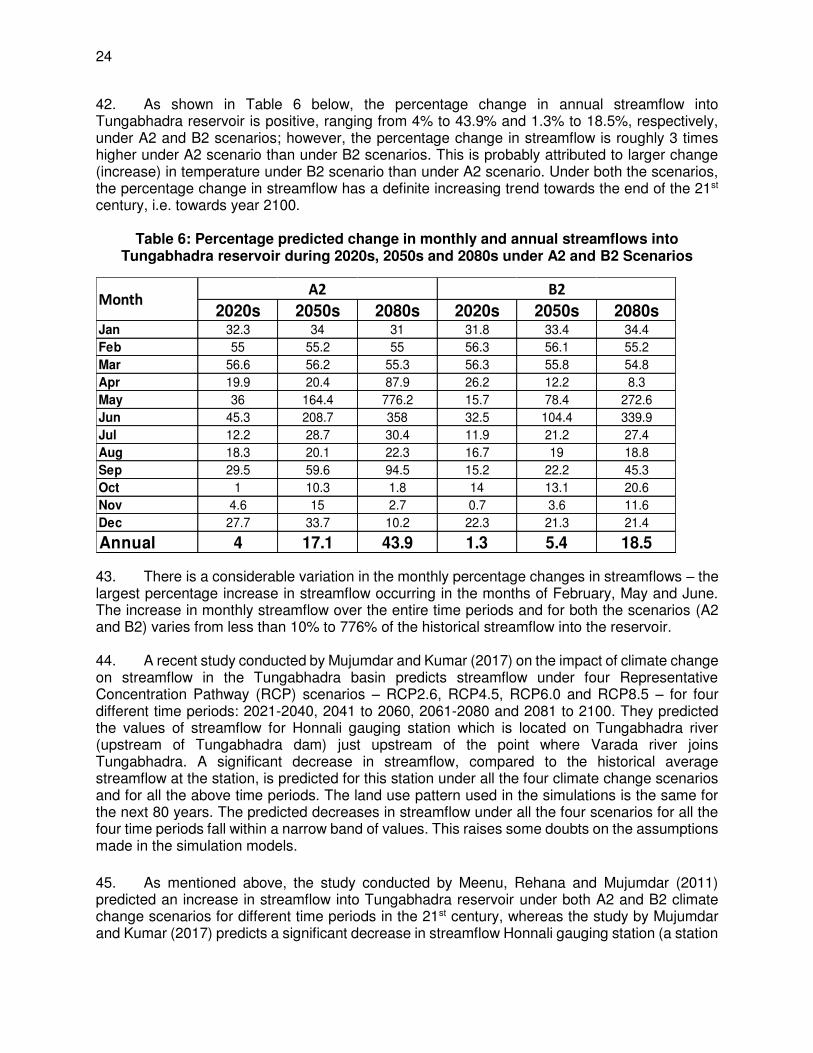

7. No requirement exists in KTPPA for those involved in procurement to formally commit to standard statement of ethics leading to lack of accountability.

C. Summary of Mitigation and Management Measures to be Adopted

8. To mitigate delayed or faulty procurement due to inadequate training and experience of staff carrying out procurement tasks, PMU needs to ensure trained and experienced (in ADB or WB projects) staff are posted to PMU, PIO and ACIWRM and are retained till substantial completion of project. Regular and tailor made procurement and contract management training of PMU, PIO and ACIWRM staff to be involved in Project 2 is be carried out. Training budget for procurement and related aspects is to be provided Project 2. Training to be provided by ADB and institutions specialized in procurement training (such as Administrative Staff College of India, Hyderabad). Increased procurement oversight and support from ADB is proposed.

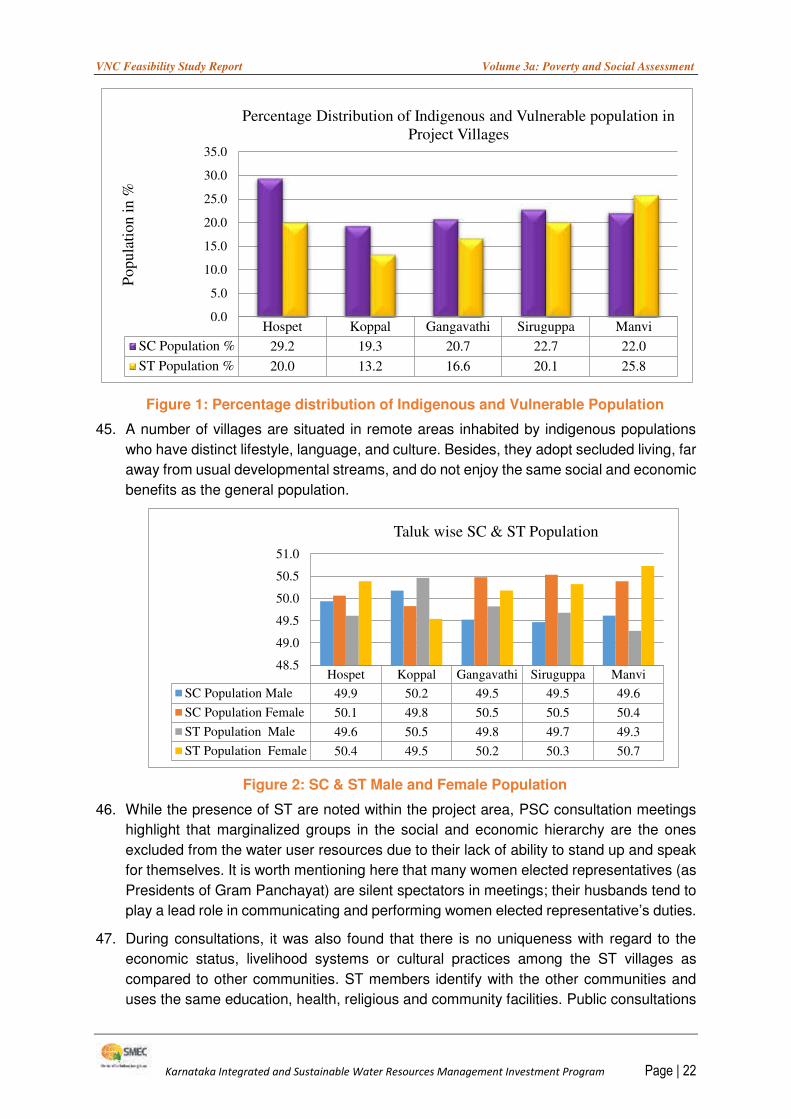

9. PMU reports to KNNL Board and obtaining KNNL’s Board approval on procurement matters has taken considerable time under Tranche 1. It is recommended that the State make similar arrangements to those for other ADB-financed projects in Karnataka, such as the Karnataka State Highways Improvement Project (financed by ADB and World Bank) by issuing a government order that delegates decision making to the State IWRM Steering Committee and have the PMU report directly to the State IWRM Steering Committee. The steering committee should be responsible for taking decisions on procurement matters. This arrangement is to be in place prior to Tranche 2 effectiveness.

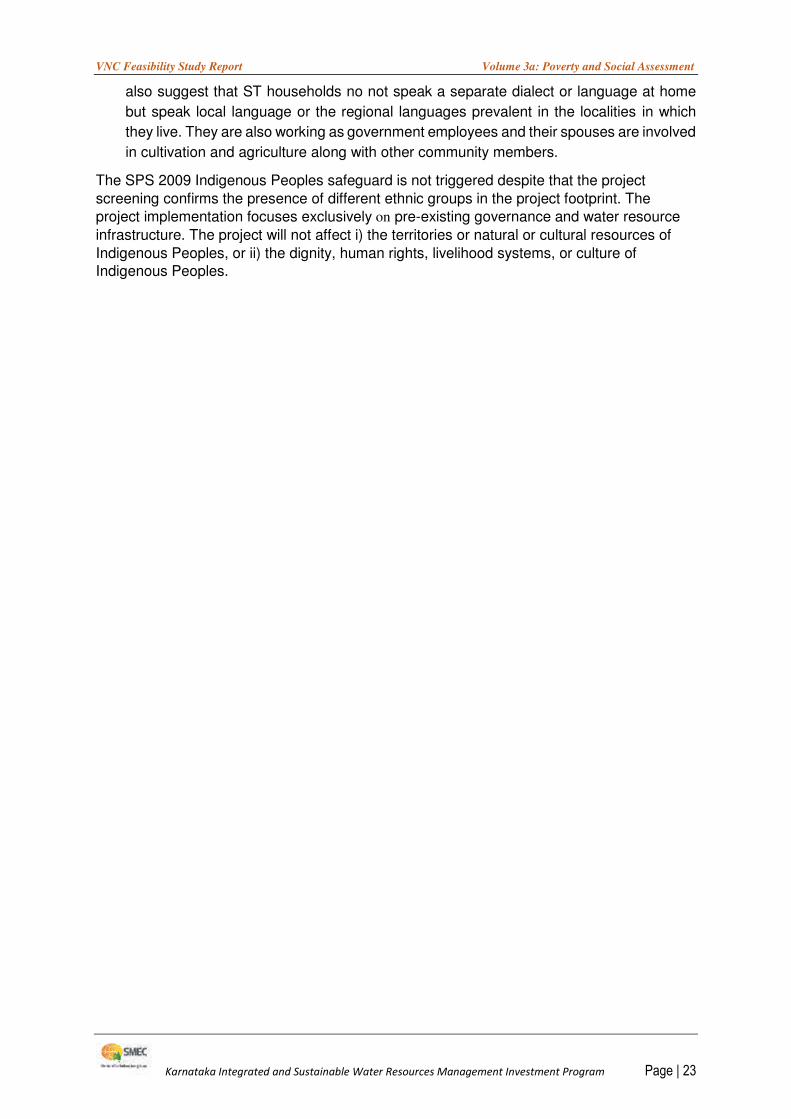

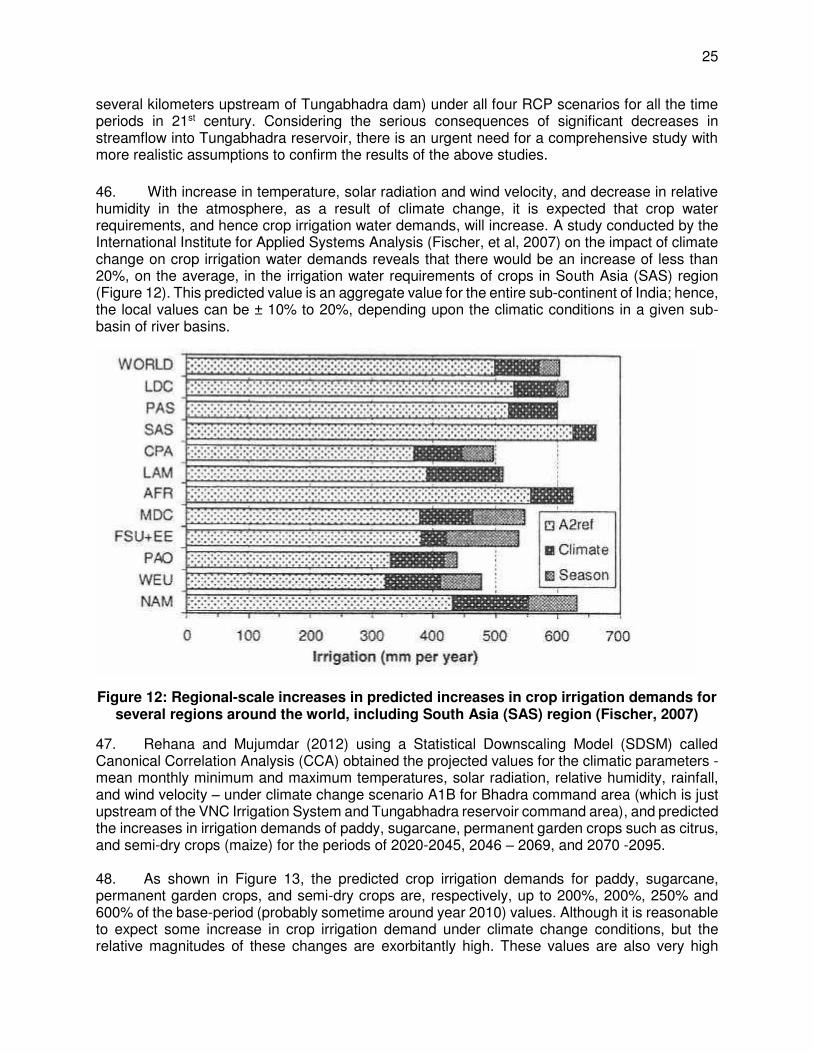

10. At present, the Program Director is also the Managing Director of KNNL and he has much wider responsibilities beyond Project 2. It is recommended that the Project Director role be assigned to a senior KNNL staff member on a full-time basis, to ensure speedy decisions on procurement.

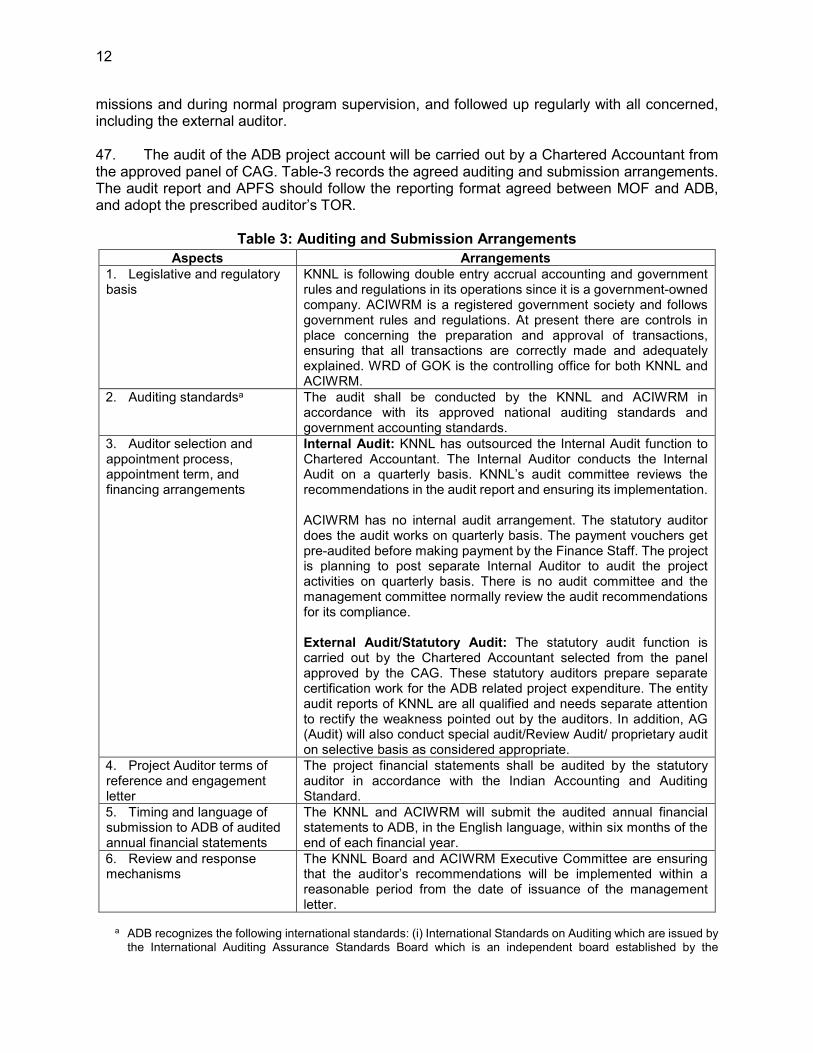

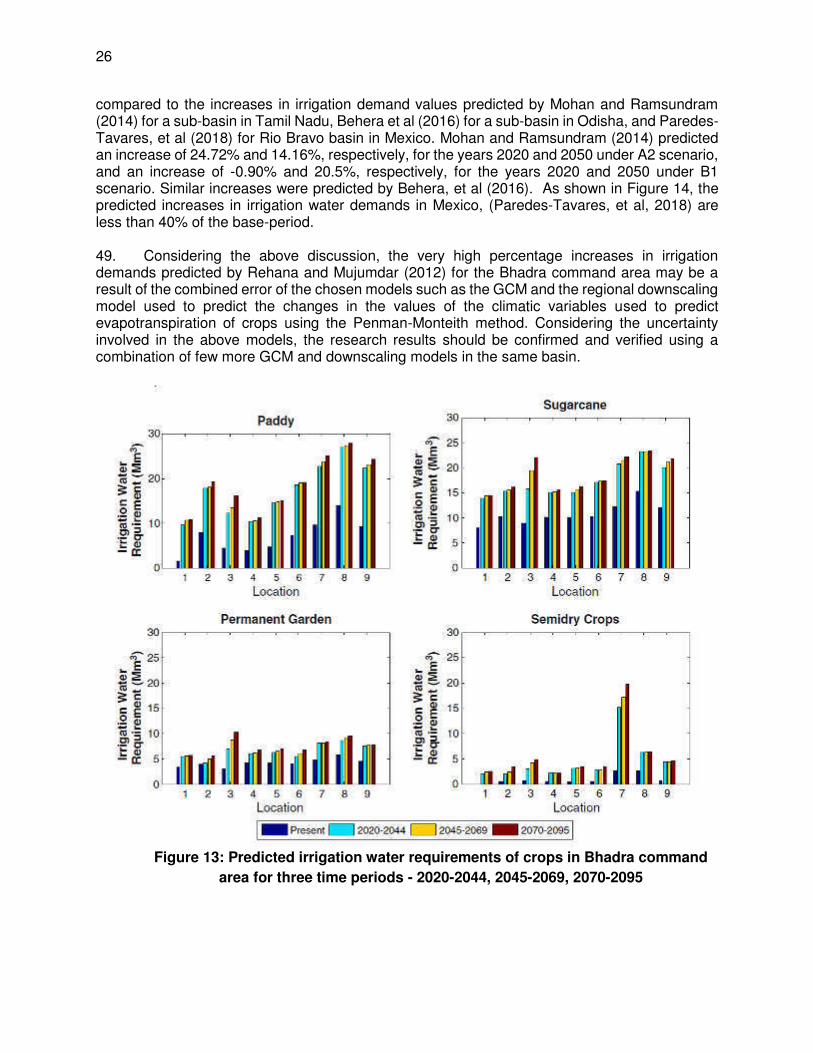

11. To ensure Consultants (PSC and individuals) are delivering value, it is required to administer to PMU and ACIWRM training programs to provide specific guidance on consultant performance evaluation and discuss case studies on consultant performance evaluation. Since multiple consultants could be working simultaneously in Project 2, a dedicated person in PMU to be devoted to evaluation and monitoring of consultants. PMU has to monitor consultant performance at regular interval and ensure PSC's procurement expert is available when required by the project

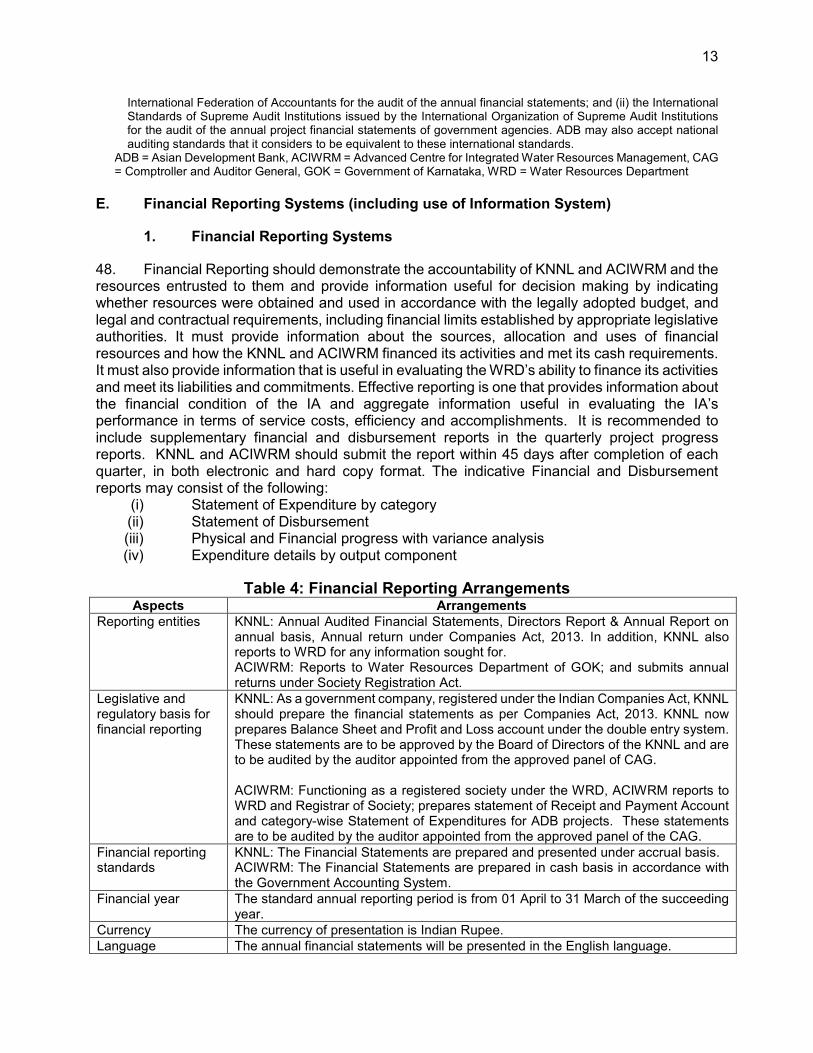

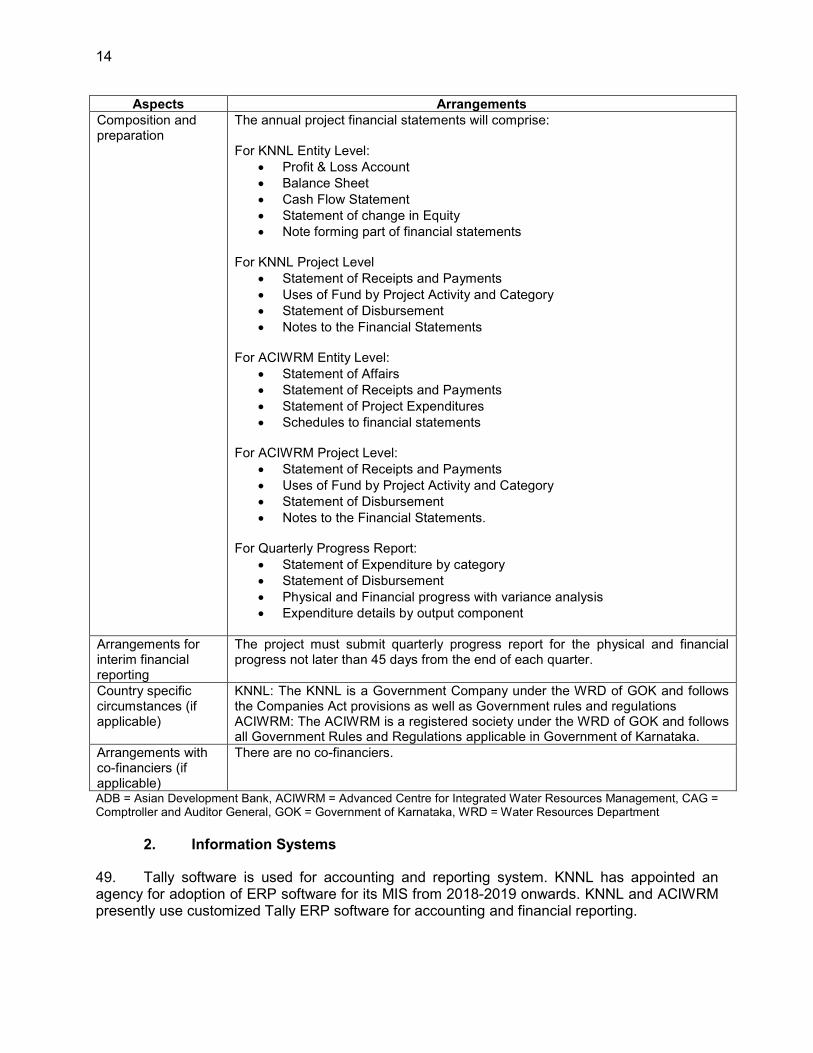

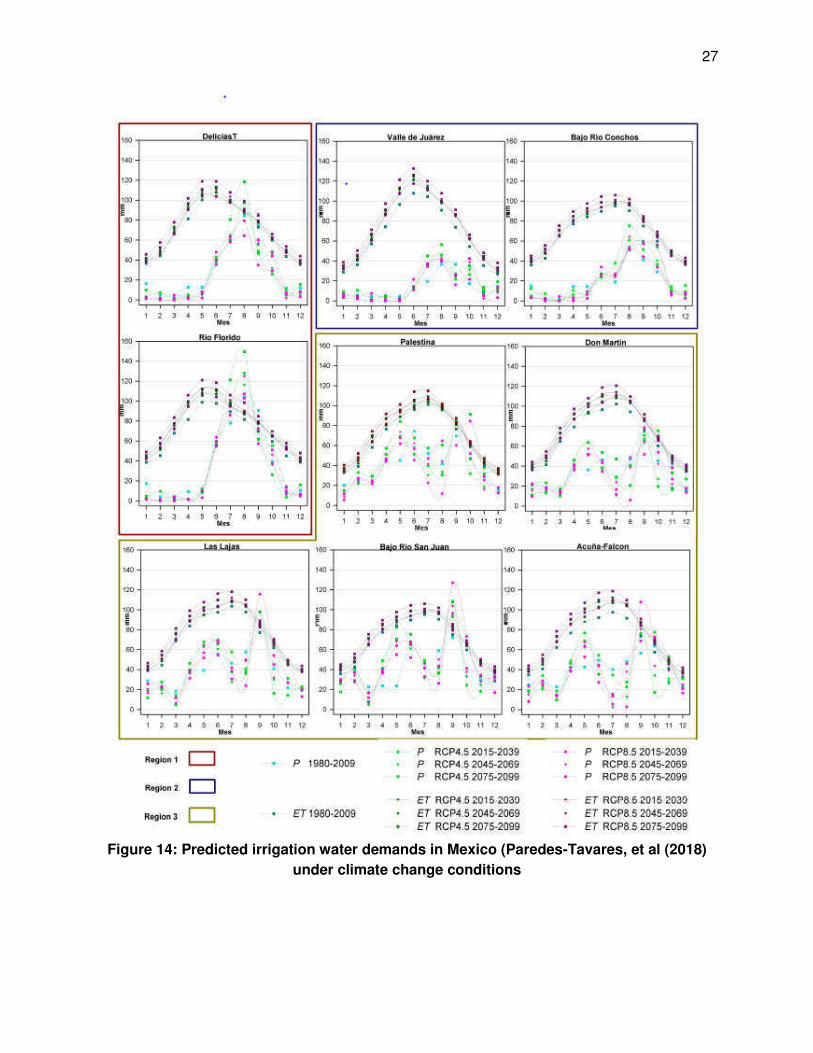

12. The absence of requirement for those involved in procurement to formally commit to standard statement of ethics is mitigated by following ADB procurement and consultant selection procedures.

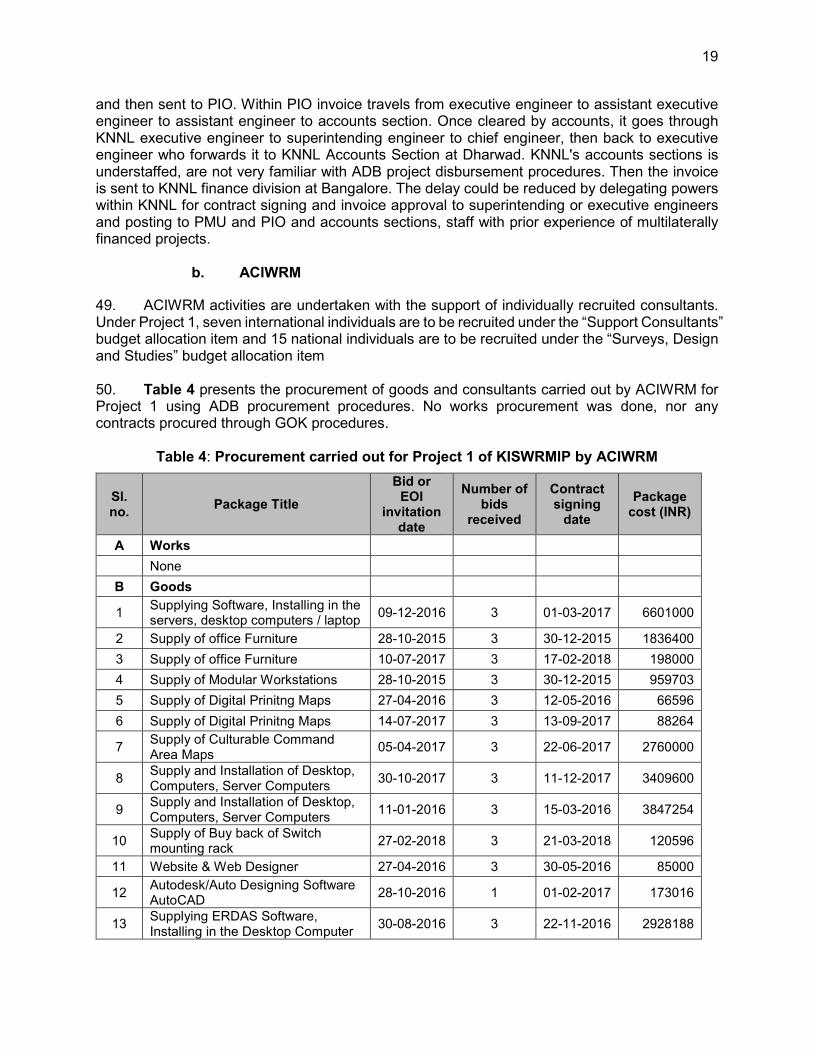

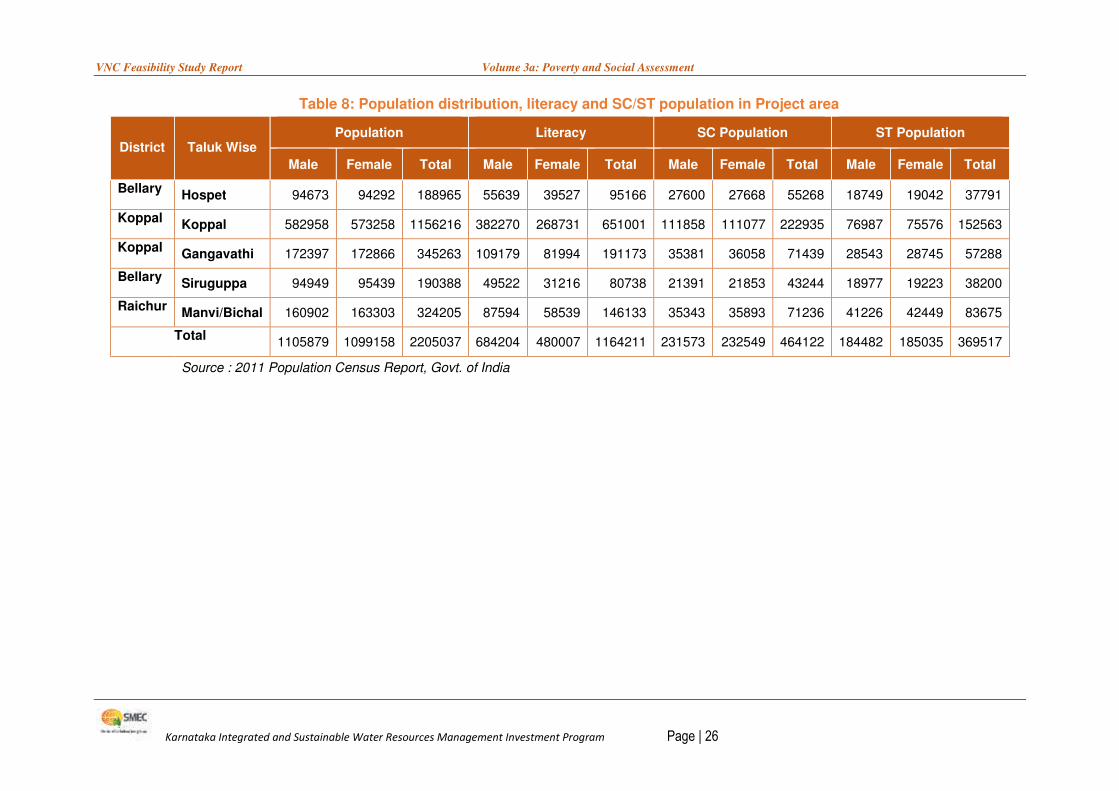

I. INTRODUCTION

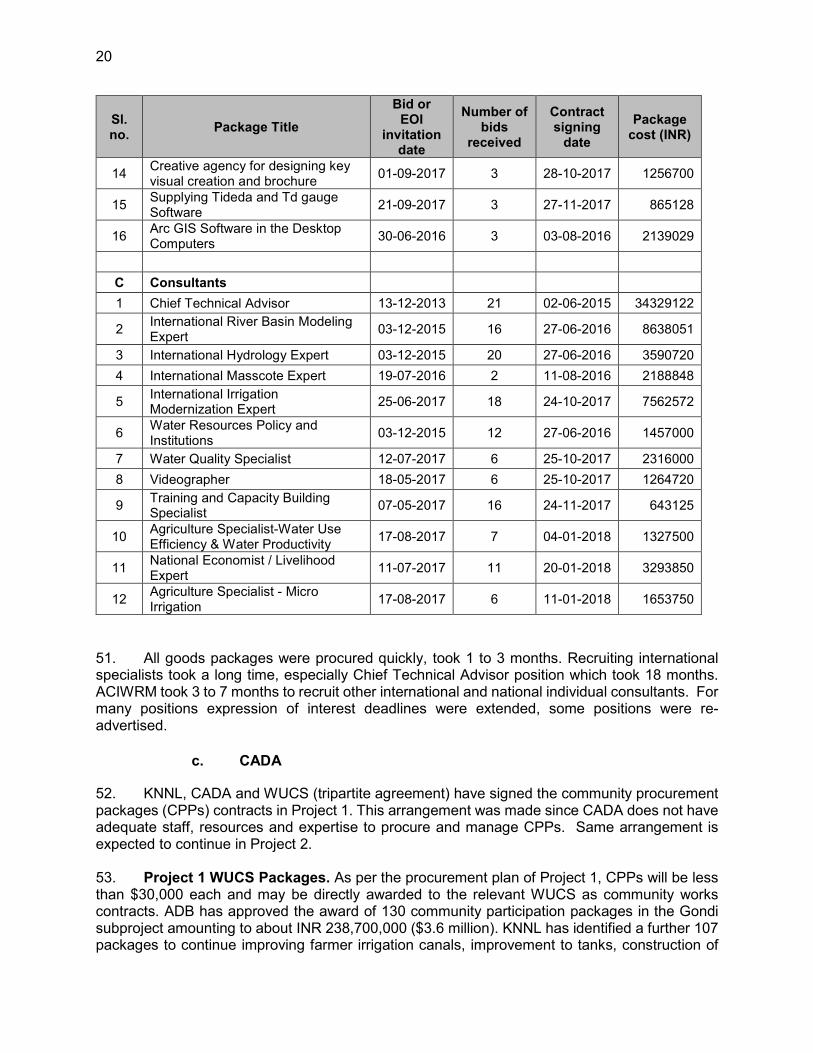

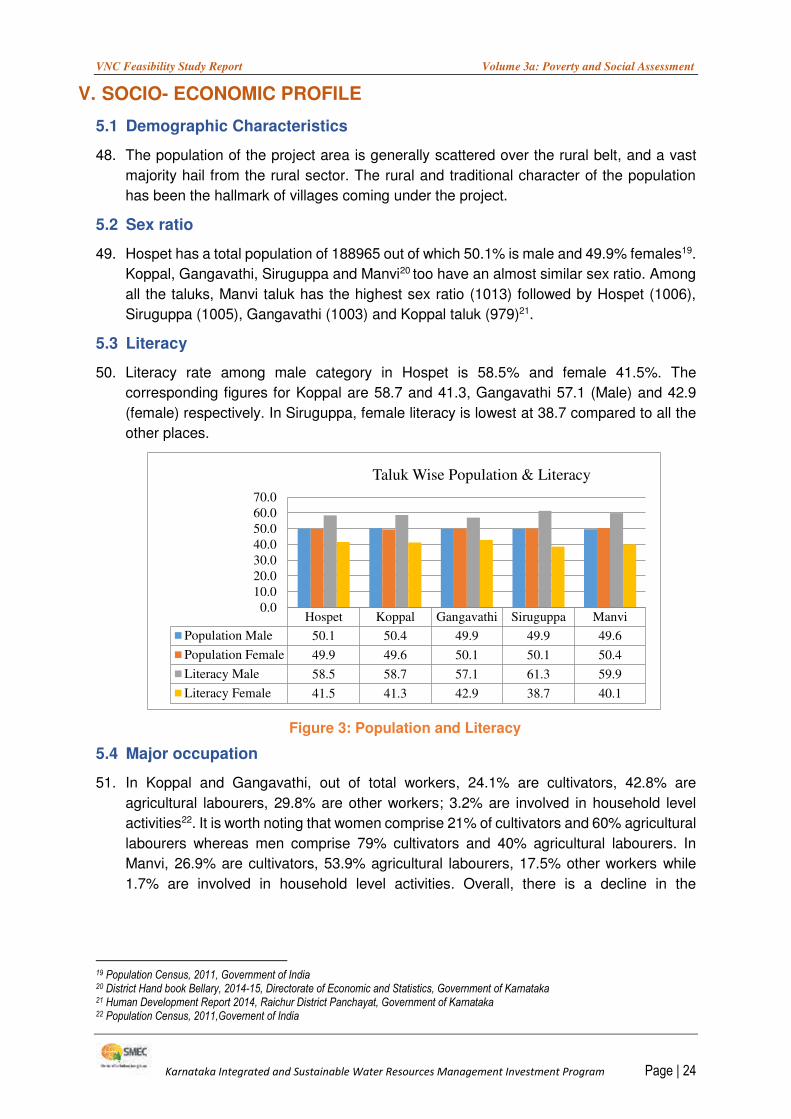

1. Project procurement capacity assessment (PCA) for the Karnataka Integrated and Sustainable Water Resources Management Investment Program (KISWRMIP) – Project 2 investment, Karnataka State, India, was prepared in accordance with Asian Development Bank's (ADB) “Guide on Assessing Procurement Risks and Determining Project Procurement Classification1”.The Asian Development Bank (ADB) financed Multi-tranche Financing Facility (MFF) for KISWRMIP for an amount of $150 million has a duration of 7 years (September 2014 to September 2021). KISWRMIP Project 1 is being implemented by Karnataka Neeravari Nigam Limited (KNNL), the executing agency (EA), and Advanced Centre for Integrated Water Resources Management (ACIWRM) the Implementing agency, from year 2014 and is scheduled for completion in March 2019. Both KNNL and ACIWRM were assessed for their procurement capacity. 2. KNNL and ACIWRM would be the executing agency and implementing agency for project 2 proposed to be implemented during 2018 to 2021. Registered under the under Indian Companies Act, KNNL established in 1999, is a wholly owned company of the Government of Karnataka (GOK) under its Water Resources Department (WRD). Established in 2012, ACIWRM is registered under Societies Registration Act, India and is anchored to the WRD of the State. 3. The PCA was undertaken during March 2018 to July 2018 during ADB’s project preparation of KISWRMIP Project 2. Meetings and discussions were carried out with KNNL, ACIWRM officials and Project Support Consultants (PSC) in Bangalore. Field visit to Shivamogga was made and discussions held with KNNL's Project Implementation Office (PIO) of Shivamogga and Munirabad, Command Area Development Authority (CADA) and PSC. Preparation activities included reviewing documents, review of reports and information from internet (KNNL, ACIWRM and CADA websites), ADB's Country Partnership Strategies (2013–2017 and 2018–2022) and KISWRMIP Project 1 portfolio experience. Information in Part A. i. has been extensively excerpted from (a) "India: Probity in Public Procurement, 2013" by United Nations Office on Drugs and Crime (b) "Working Paper No. 204. Public Procurement in India: Assessment of Institutional Mechanism, Challenges, and Reforms, July 2017" by National Institute of Public Finance and Policy, New Delhi and (c) "Karnataka Transparency in Public Procurements Act (KTPPA), 1999." 4. The program management unit (PMU) for the investment program is within KNNL headquarters (located in Bangalore). The Managing Director of KNNL is the Program Director. The PMU provides coordination, implementation, and monitoring assistance for the entire MFF. ACIWRM, an implementing agency, is based in Bangalore and is tasked to implement output 1 of the program, which focuses on institutional strengthening for Integrated Water Resources Management (IWRM). For irrigation system modernization, KNNL's divisional project implementation offices (PIO) have been established in Shivamogga (for Gondhi canals) and in Munirabad (for Vijayanagara canals) near each subproject location. The PIO comprises engineering,. accounts and administrative staff of KNNL and CADA staff. The PMU and PIOs are being provided with technical guidance and field implementation support by PSC. A. Description of the Investment Project

5. The Asian Development Bank (ADB) approved an MFF of $150 million and its Project 1 loan for $31 million was declared effective from 13 July 2015. The Project 2 loan ($91 million ) of the MFF is currently being prepared by ADB.

1 ADB. August 2015. Guide on Assessing Procurement Risks and Determining Project Procurement Classification.

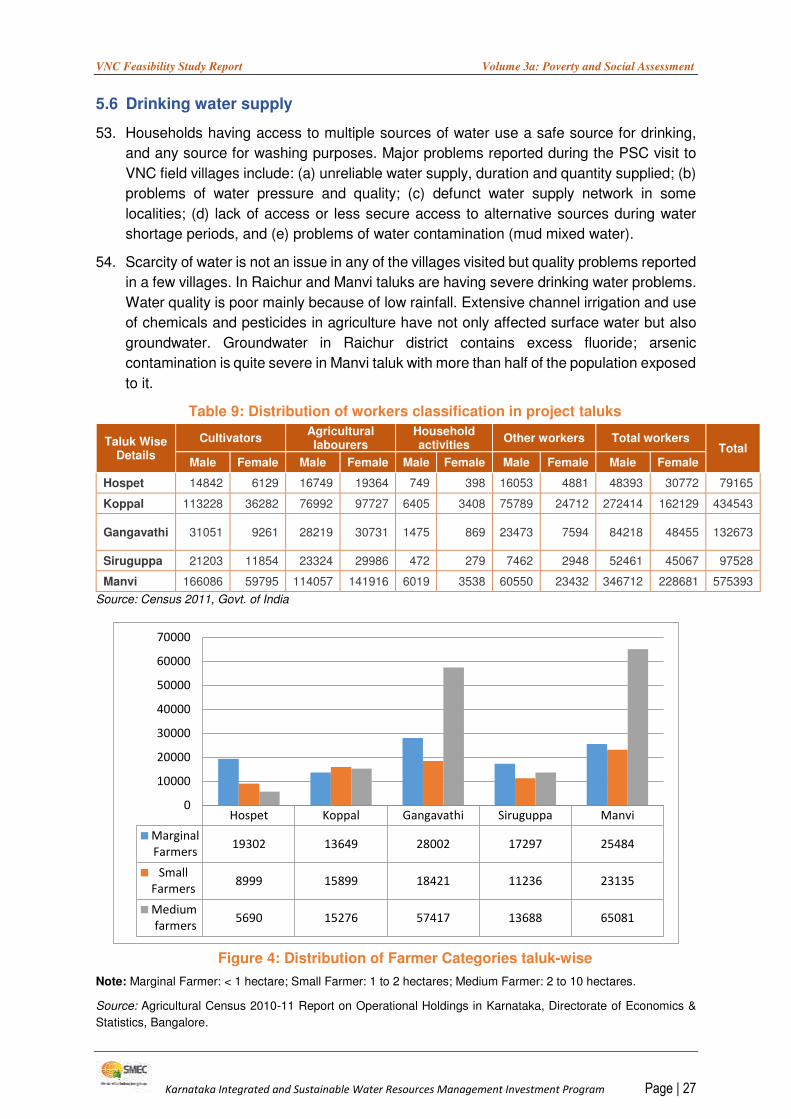

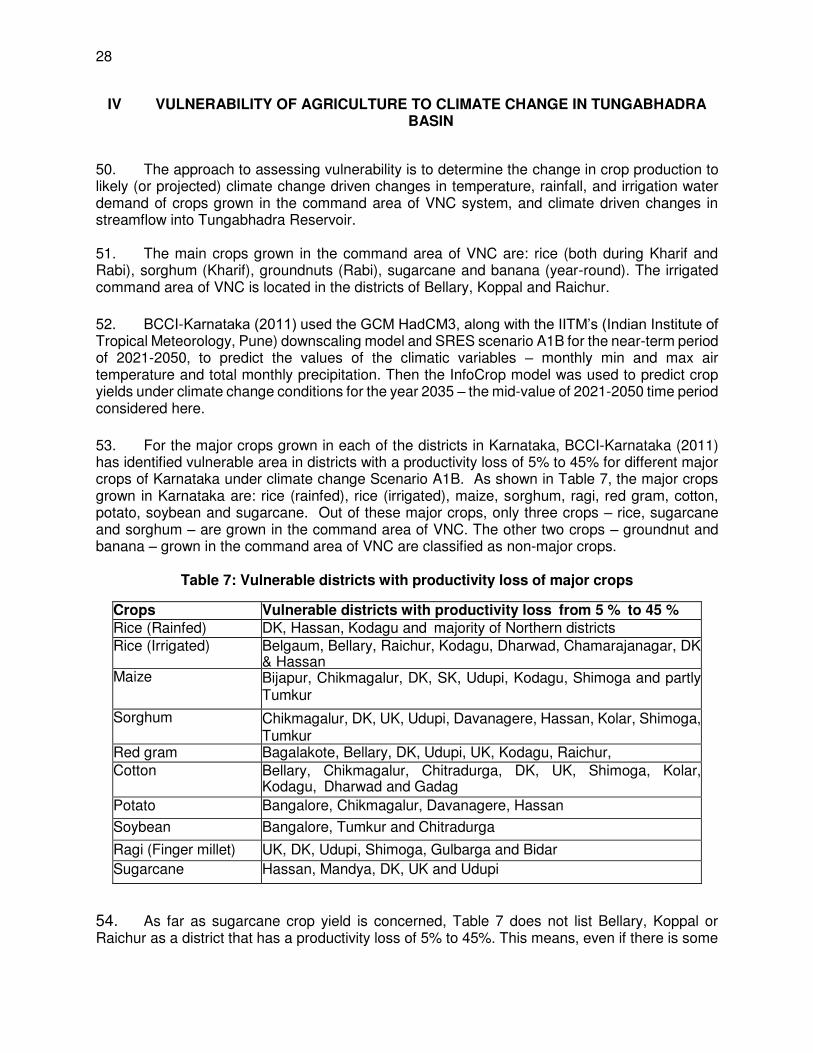

2

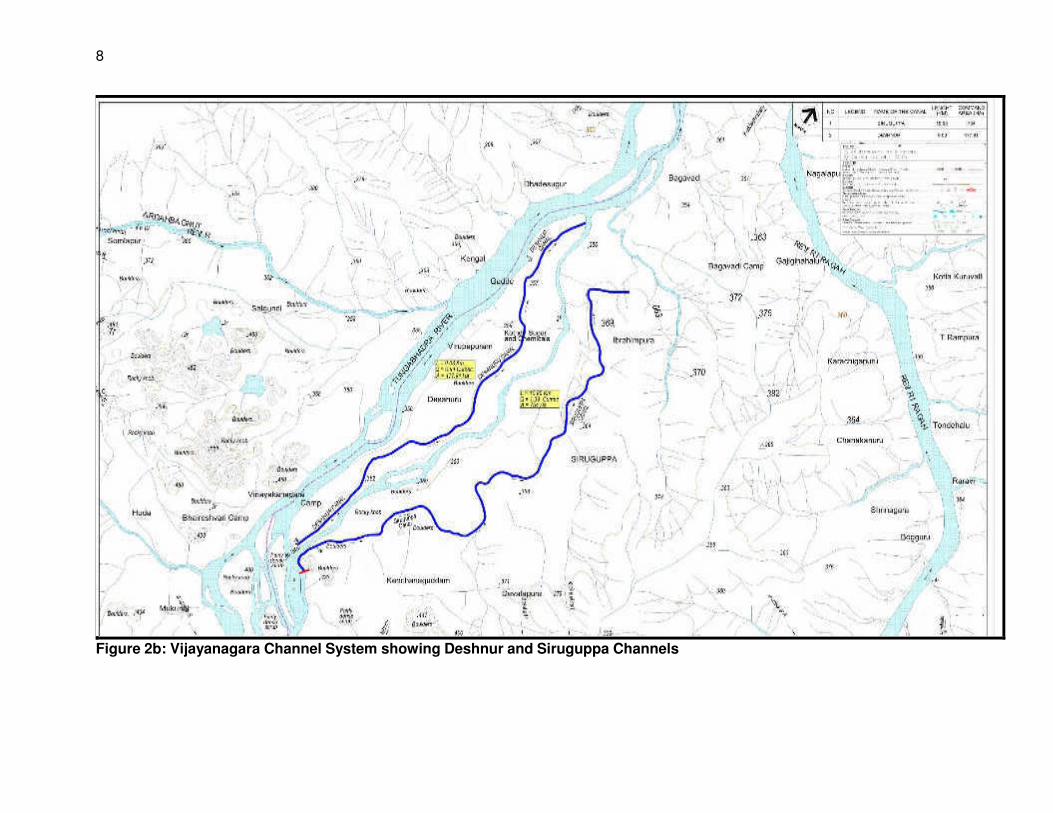

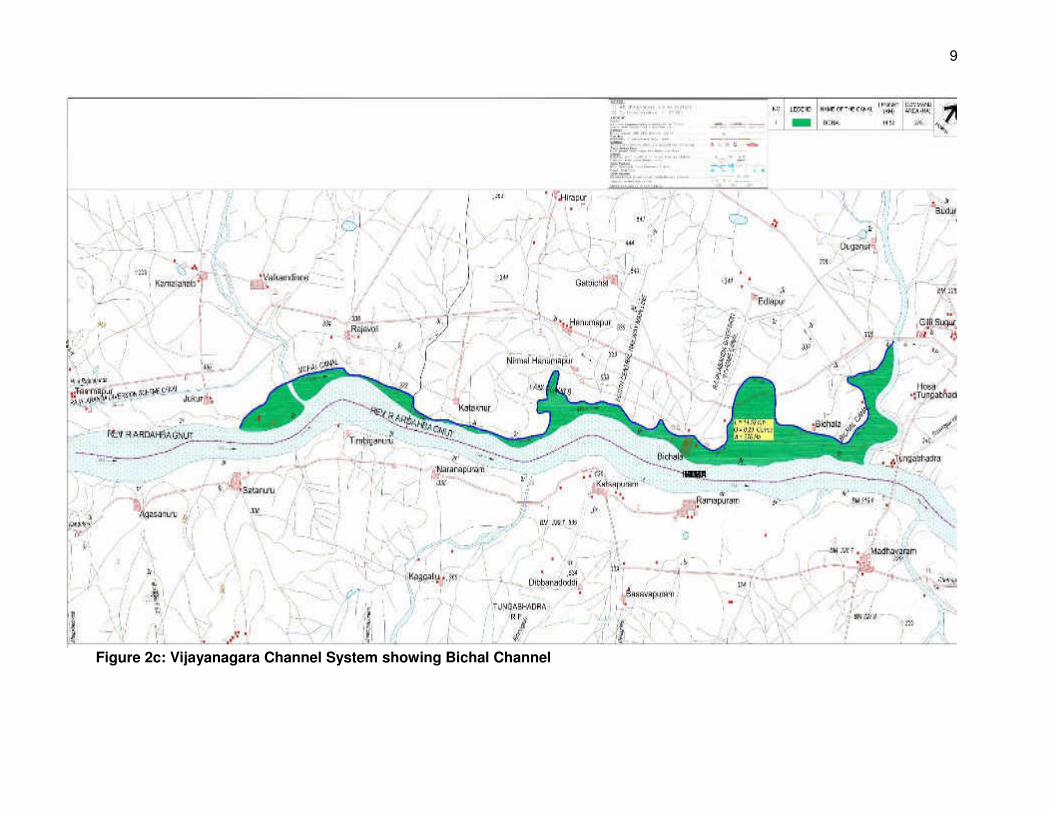

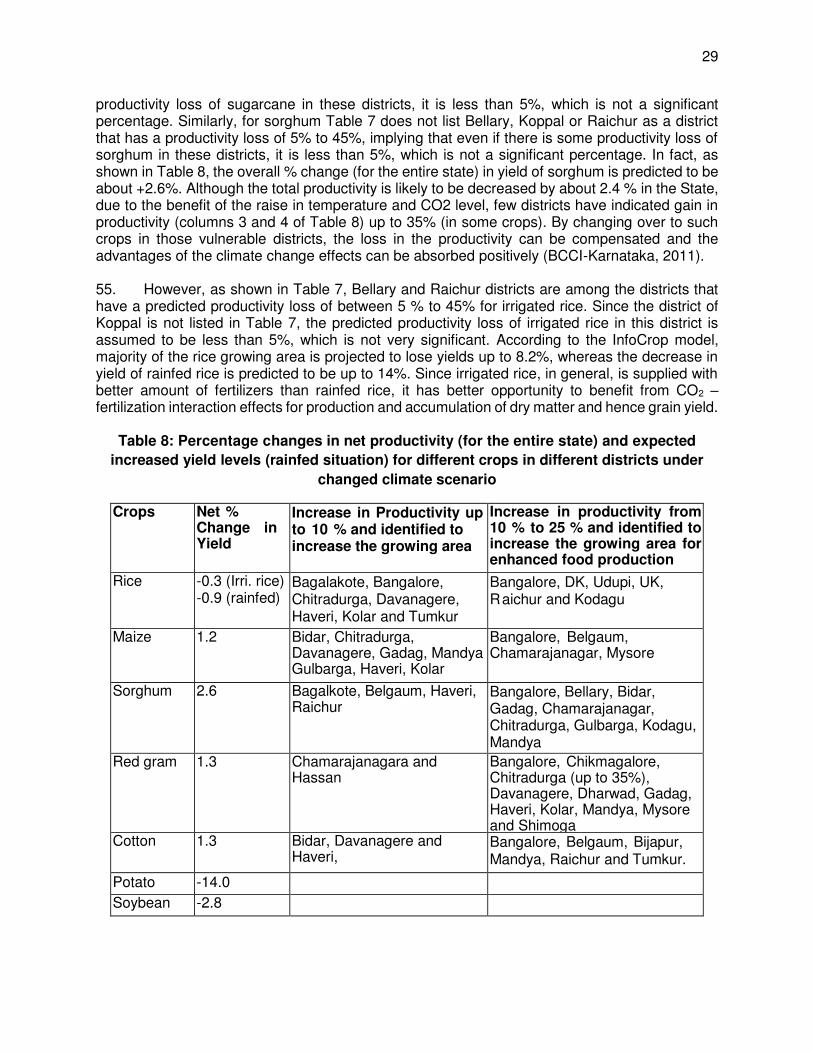

6. The Project 2 comprises three outputs. Output 1: Strengthening State and Basin Institutions for IWRM. (i) preparing the middle Krishna Basin Plan (for sub-basins K2 to K4); (ii) expanding the Karnataka Water Resources Information System; and (iii) continuing with strengthening WRD staff with IWRM training. 7. Output 2: Modernization of Irrigation System Infrastructure and Management. Project 2 will modernize the Vijayanagara Channels (VNC) subproject including repairing 16 anicuts and intake structures and about 442 kilometers of main, distributaries and minor canals. The project will establish and strengthen 30 Water User Cooperative Societies located within the project area that will then be responsible for improving their farmer irrigation canals. Project 2 will also provide farmers with extension services to improve on-farm water management and crop production, and develop an asset database and management plan. 8. Output 3: Operationalization of Program Management Systems. The main activities to be undertaken include (i) establishing a fully staffed project implementation office (PIO) with an appointed project implementation officer,(ii) procuring works and equipment financed under Project 2, (iii) coordinating with ACIWRM and managing the project support consultant, (iv) coordinating with CADA and other agencies responsible for command area development and on-farm improvement activities; (v) maintaining the program management information system database that was established under Project 1, (vi) meeting annual disbursement projections, (vii) conducting periodic safeguard and performance monitoring reviews; (viii) preparing the technical, economic and safeguard due diligence for proposed Project 3 and preparing the associated draft periodic financing request; and (ix) undertaking advanced procurement actions for proposed Project 3. 9. Project 1 is being implemented from 2014 to 2019 and implementation is slightly behind schedule. In consideration of the limited period left in the MFF (i.e. September 2021 completion target), quick procurement and contract implementation would be critical for completion of Project 2.

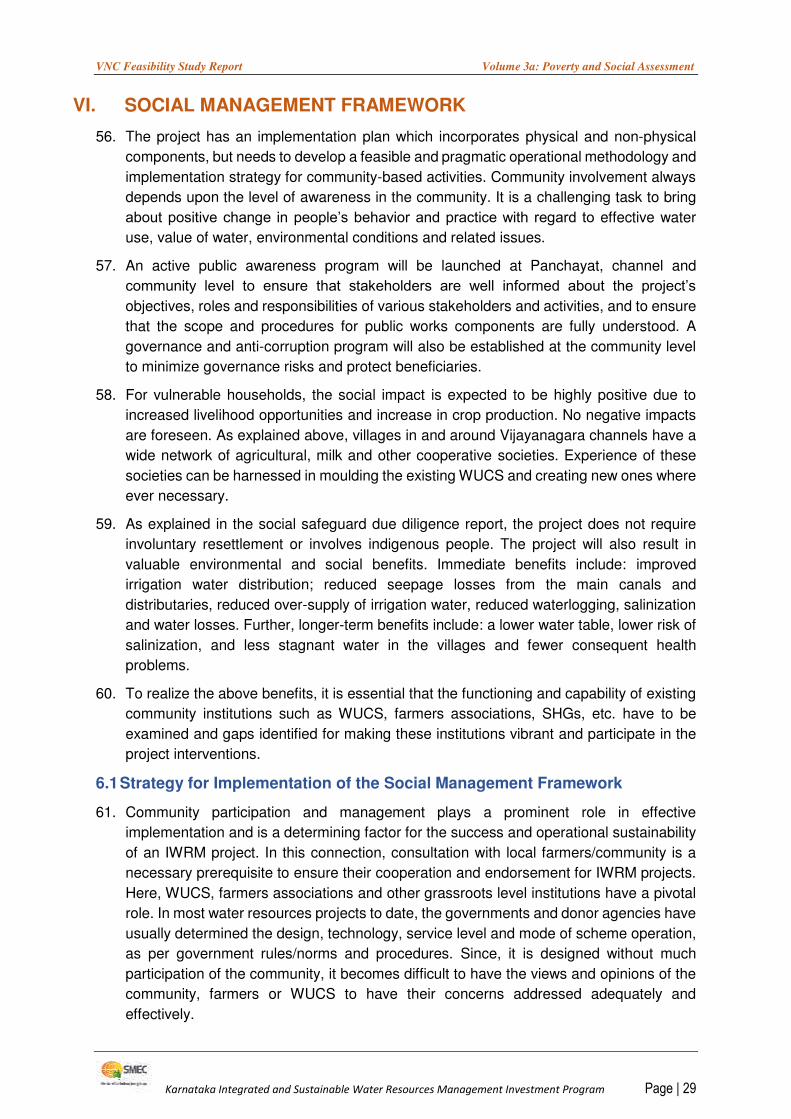

3

II. PROJECT PROCUREMENT RISK ASSESSMENT

A. Overview and Assessment

Legislative and Regulatory Framework2

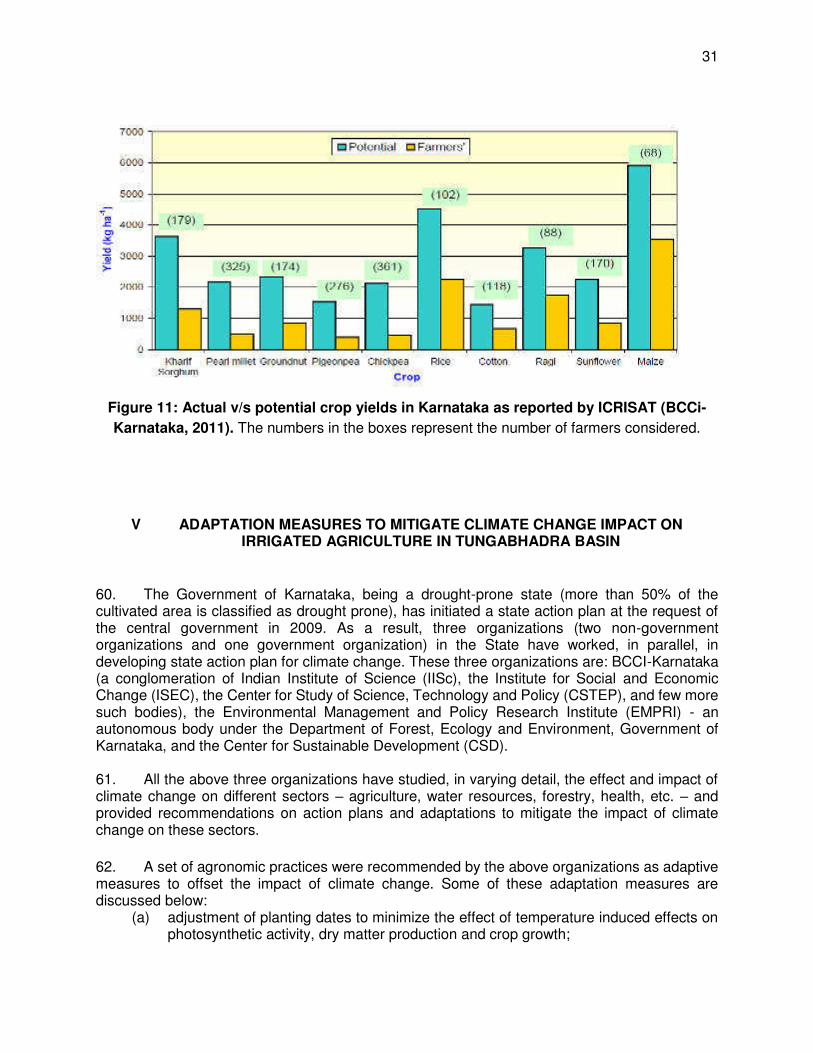

10. India does not have a comprehensive procurement legislation, and the procurement regime in the country appears to be fragmented and inconsistent in terms of rules, regulations, and procedures. The public procurement framework in India has four broad features namely constitutional provisions, legislative provisions, administrative guidelines, and overseers. Within the constitutional provisions, Articles 298, 299, 300 and 300A authorize the governments to contract for goods and services. Similarly, Article 246 specifies the legislative powers in the federal structure of India into three lists namely Union List, State List, and Concurrent List. While Article 355 specifies the executive power, Article 282 directs the financial autonomy in public spending. Beyond that, it does not provide any guidance on public procurement principles, policies, and procedures. Apart from these, a few states such as Tamil Nadu, Karnataka, Andhra Pradesh, Rajasthan and Assam follow their own procurement acts to carry out public procurement at state level. 11. General Financial Rules (GFR) of the Ministry of Finance, government of India, prescribe the use of standard procurement methods (limited tender enquiry, advertised or open tender enquiry, single tender enquiry, two-stage bidding, or electronic reverse auctions) depending on type (works, goods, services) and volume of procurement (in monetary terms). The open tender enquiry is prescribed as the preferred method. In a few special cases such as urgency or single source of supply, single tender is called with proper justification and approval of the competent authority. Similarly, limited tender can be called instead of open tender on urgency given that there will be at least three bids. On the other hand, low value procurements are done without calling a tender by the authority or a purchase committee of the procuring entity. 12. While GFR 2017 has kept intact the monetary threshold limits for a few categories as given in GFR 2005, it enhances the threshold limits for others. For example, GFR 2017 has kept intact the threshold limit for the procurement of original works through limited tender. However, it has enhanced the upper threshold limit for open tender enquiry from INR one million(~US$15,000) to 3million (~US$45,000). Similarly, it has increased the upper threshold limit for procurement of goods by the purchasing committee from INR 0.1million (~US$1,500) to INR 0.25 million (~US$3,750). While GFR 2005 perceived procurement of all kinds of services to be similar, GFR 2017 has segregated procurement of services into two broad categories viz., ‘consulting services’ and ‘non-consulting services’. In addition to these changes, GFR 2017 also includes a few important provisions as below to streamline the public procurement activities in the country.

i. GFR 2017 recommends two-stage bidding where a procuring entity holds discussions with the bidder community to finalize the technical specifications in the first stage. The financial bid is called from those whose ideas were accepted, and the bid is awarded to the bidder with the best quality-price ratio. (Rule 164).

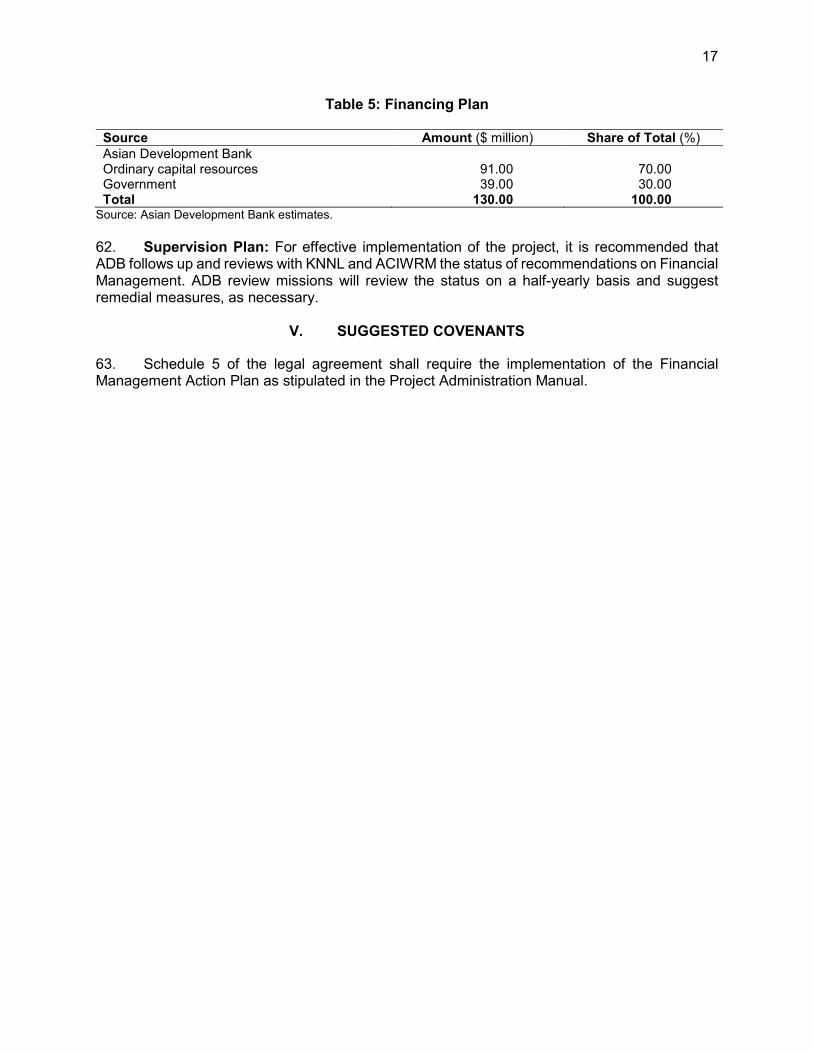

ii. It directs to assign higher weight to quality as compared to the price especially in procurement of services through the quality and cost-based selection (Rule 192).

2 This section mostly based on information from "Working Paper No. 204. Public Procurement in India: Assessment of

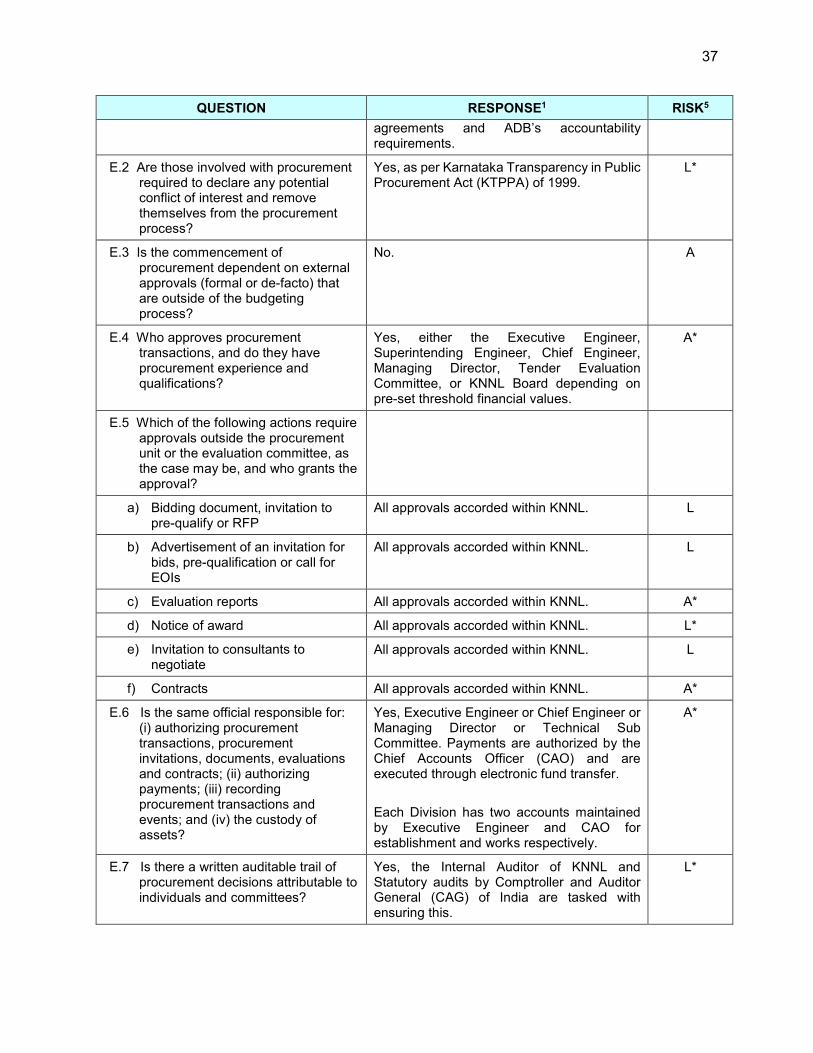

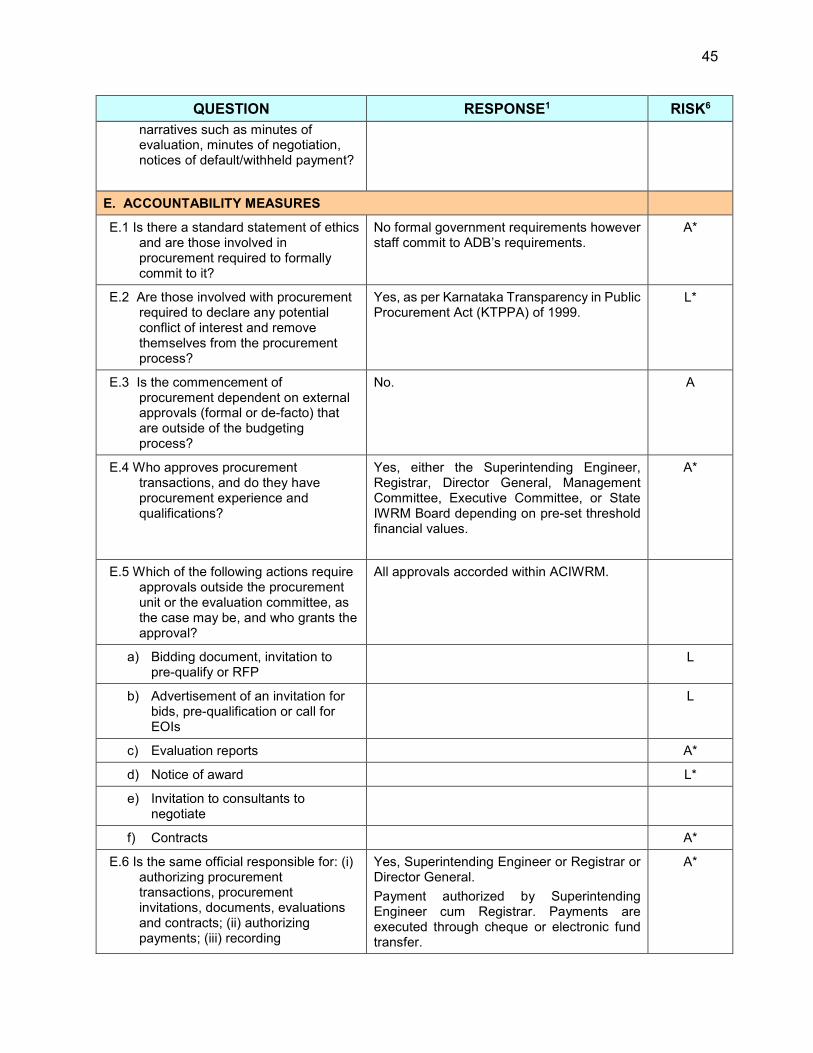

Institutional Mechanism, Challenges, and Reforms", July 2017 by National Institute of Public Finance and Policy, New Delhi, India

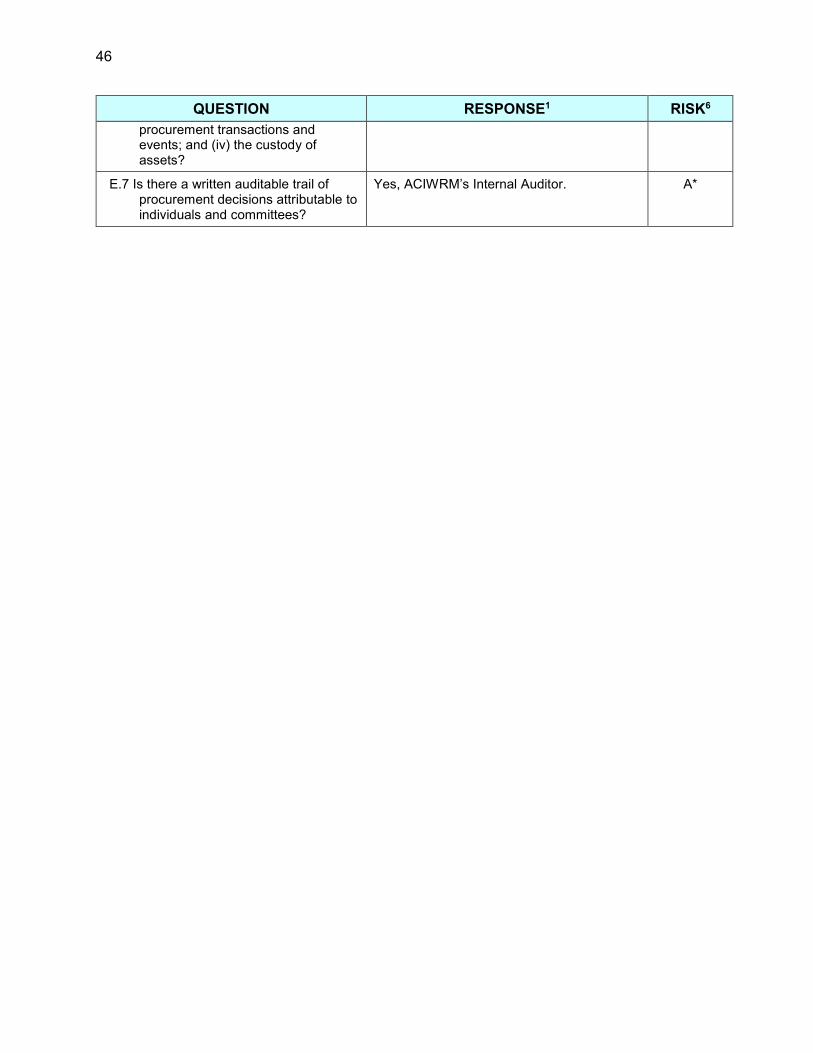

4

iii. It gives emphasis on the use of information technology in public procurement to ensure greater transparency and competition by mandating the use of Central Public Procurement Portal for publication of all tender details (Rule 159), compulsory e-bidding for all procurements (Rule 160), and promotion of electronic reverse auction (Rule 167).

iv. It introduces Code of Integrity to address probity in procurement activities (Rule 175). v. It urges the inclusion of environmental issues in the bid documents [Rules 173(xi),

217, and 218]. vi. It directs to share the reasons of rejecting a tender or non-issuing a bid document to

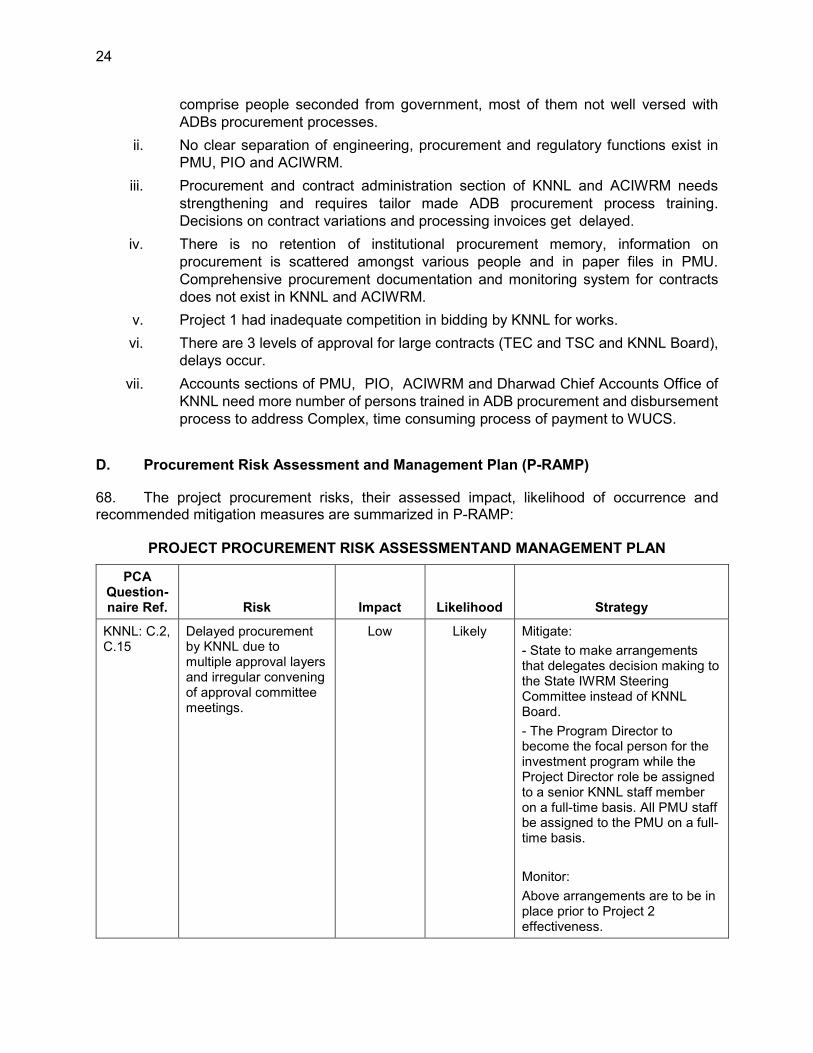

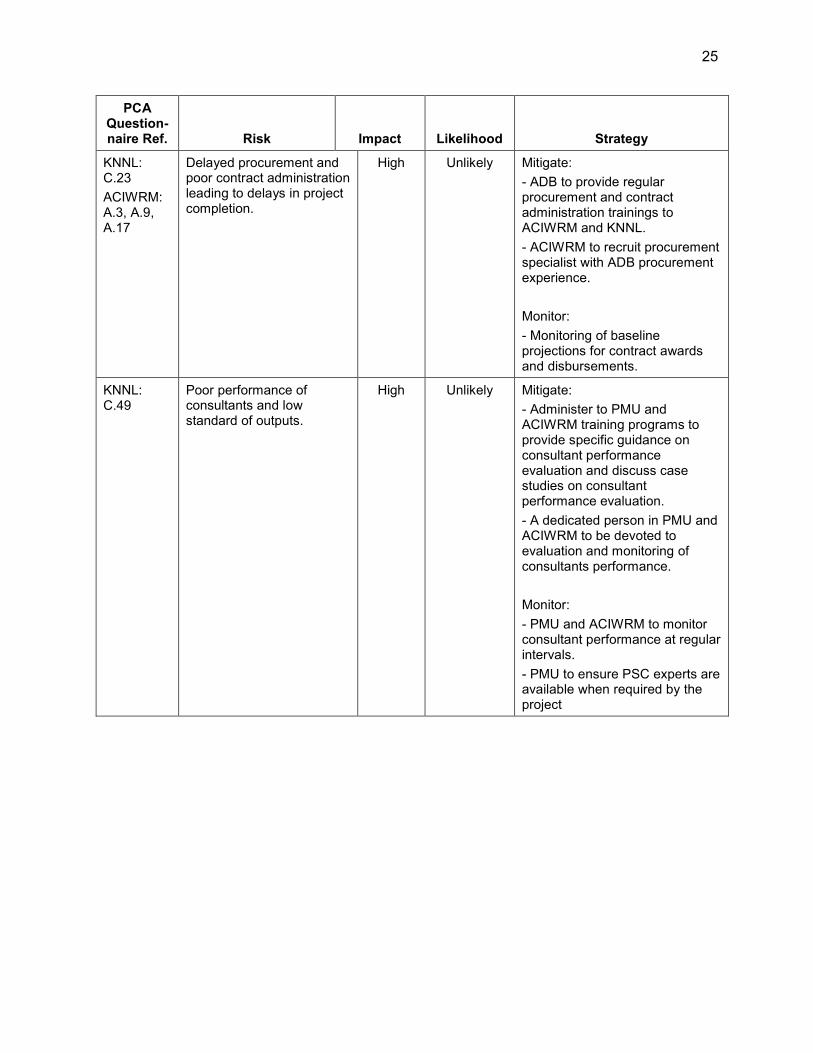

a prospective bidder upon request [Rule 173(iv)]

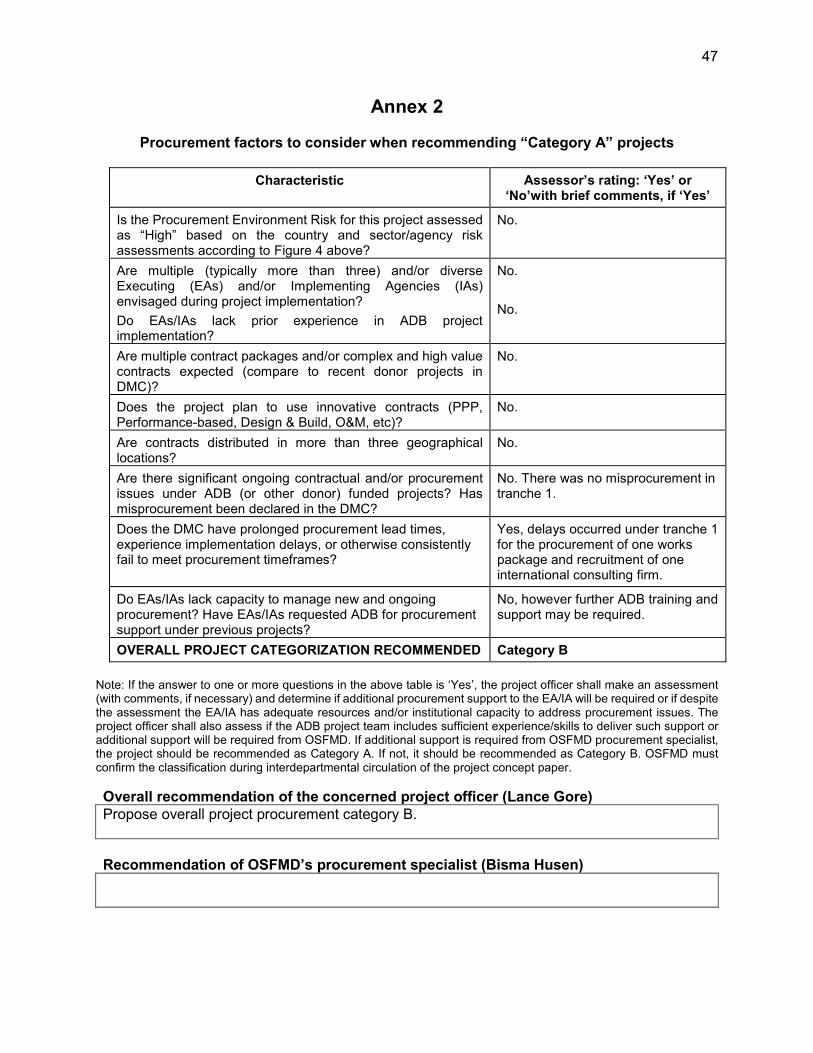

13. Karnataka enacted the Karnataka Transparency in Public Procurements Act (KTPPA), 1999 which governs all public procurement in the state. The Act aims to ensure transparency in public procurement of goods and services by streamlining the procedure of inviting, processing and acceptance of tenders by procurement entities. The Act is clear and is closely aligned with ADB’s procurement guidelines. The provisions of this Act in so far as they are inconsistent with the procedure specified in respect of projects funded by international financial agencies or projects covered under international agreements, shall not apply to procurement of goods or services. Hence in case of inconsistencies, ADB procurement guidelines will prevail. The Act is to be read with the Karnataka Procurement Rules which amplify and detail the provisions in the Act. 14. The 2013–2017 Country Partnership and Strategy of India by ADB, para 28 notes the country’s strong procurement system. Para 29 of the same report states that risks relate primarily to project implementation, and in particular slow procurement and weak project management. This results mainly from capacity gaps at the executing agency level and within ADB. Subsequently, the 2018-2022 Country Partnership and Strategy of India by ADB supports use of country procurement system (para. 51) as applicable. 15. However not having a comprehensive procurement legislation and the fragmented and inconsistent approach to procurement remain as major weaknesses. Progress is being made, albeit slowly.

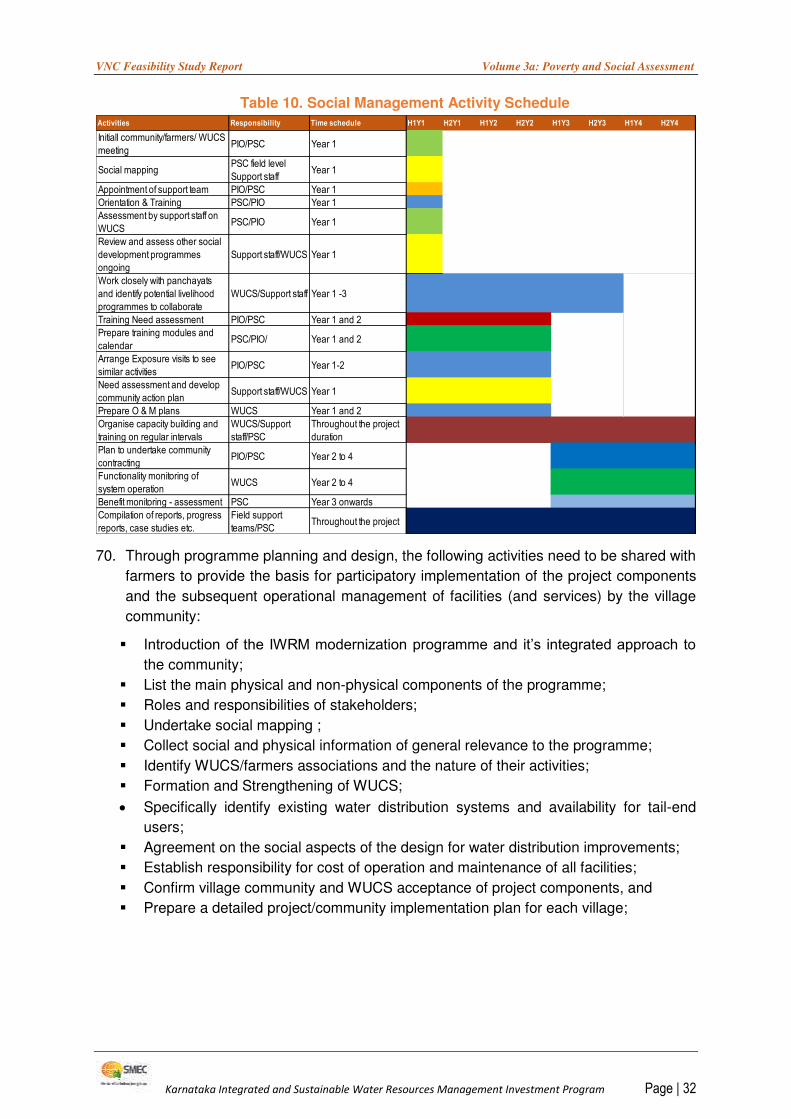

Organization and Staff Capacity

a. KNNL

16. KNNL is registered as a wholly owned Government of Karnataka Company as per the provisions of the Companies Act, India in December 1998.KNNL is managed by the Board of Directors. Chief Minister of Karnataka state is the Chairman of the Board . The Managing Director looks after the day-to-day affairs of the company. A team of professionally qualified and experienced personnel in various fields like engineering, design, finance, general administration and law assist the Managing Director. 17. The Company is responsible for planning, investigation, estimation, execution, operation and maintenance of all irrigation projects. The Company is authorized to sell water and recover revenues from individuals, groups of farmers, towns, city municipalities and industries. 18. The Organograms of PMU and PIO of KNNL for MFF are presented in Figure 1 and Figure 2 respectively.

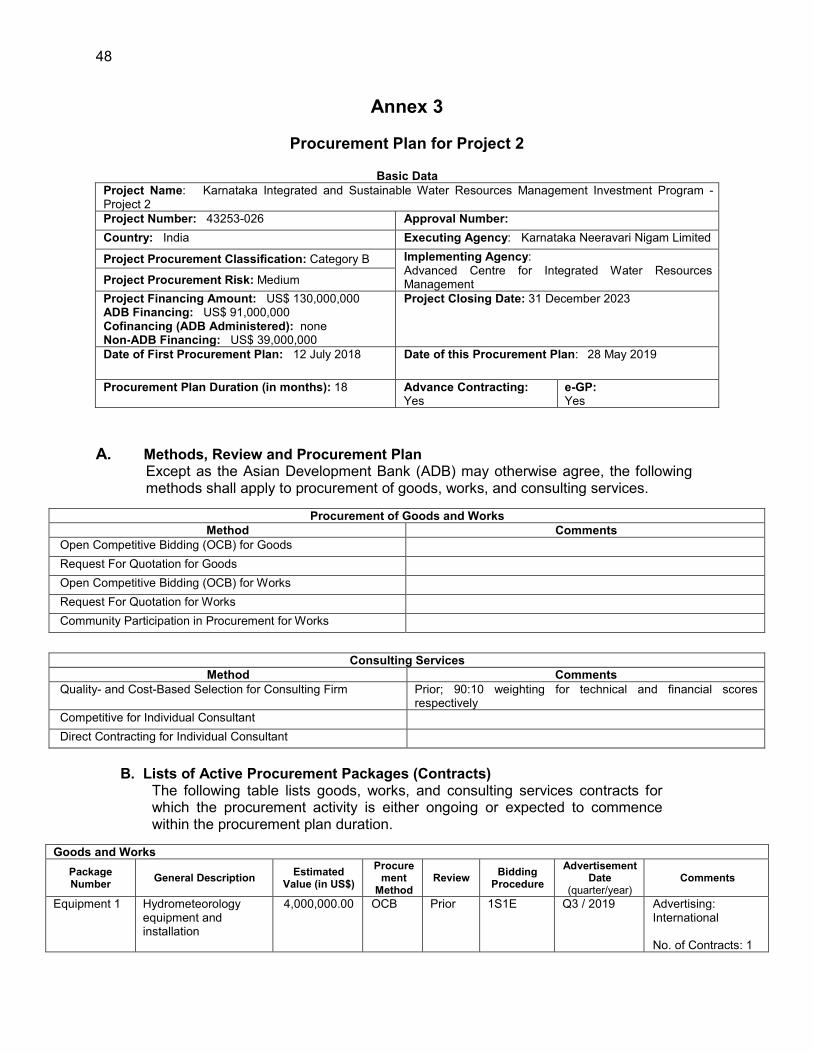

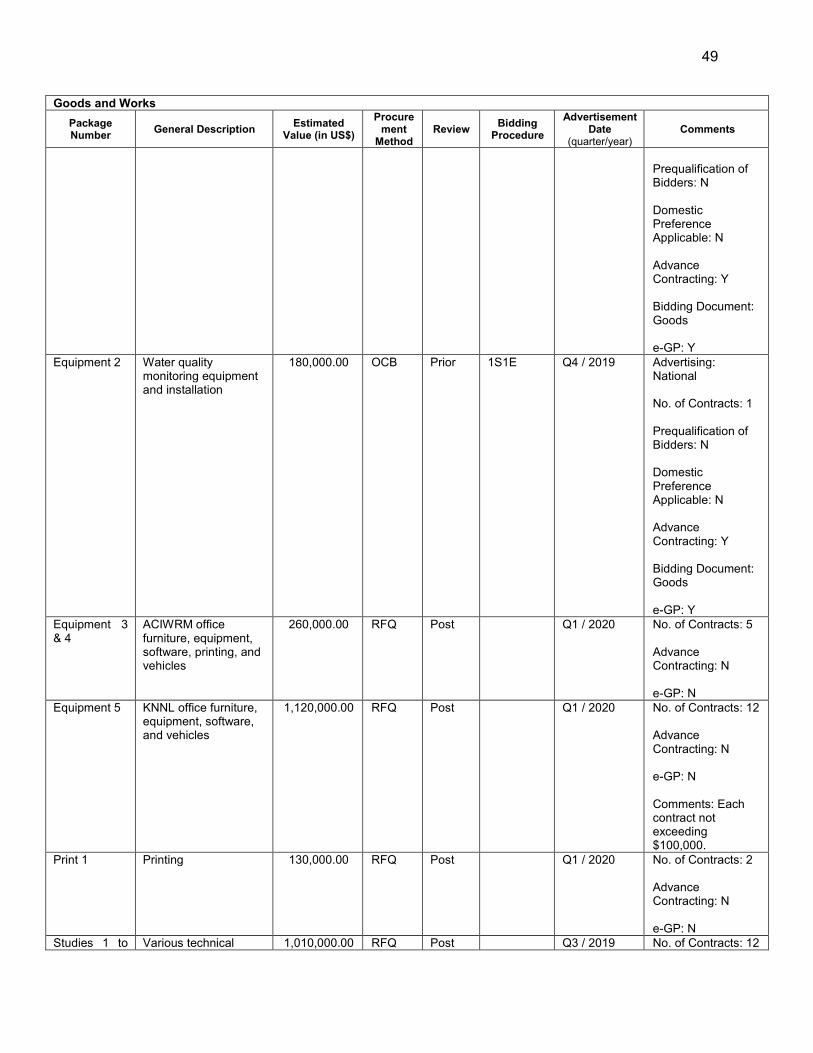

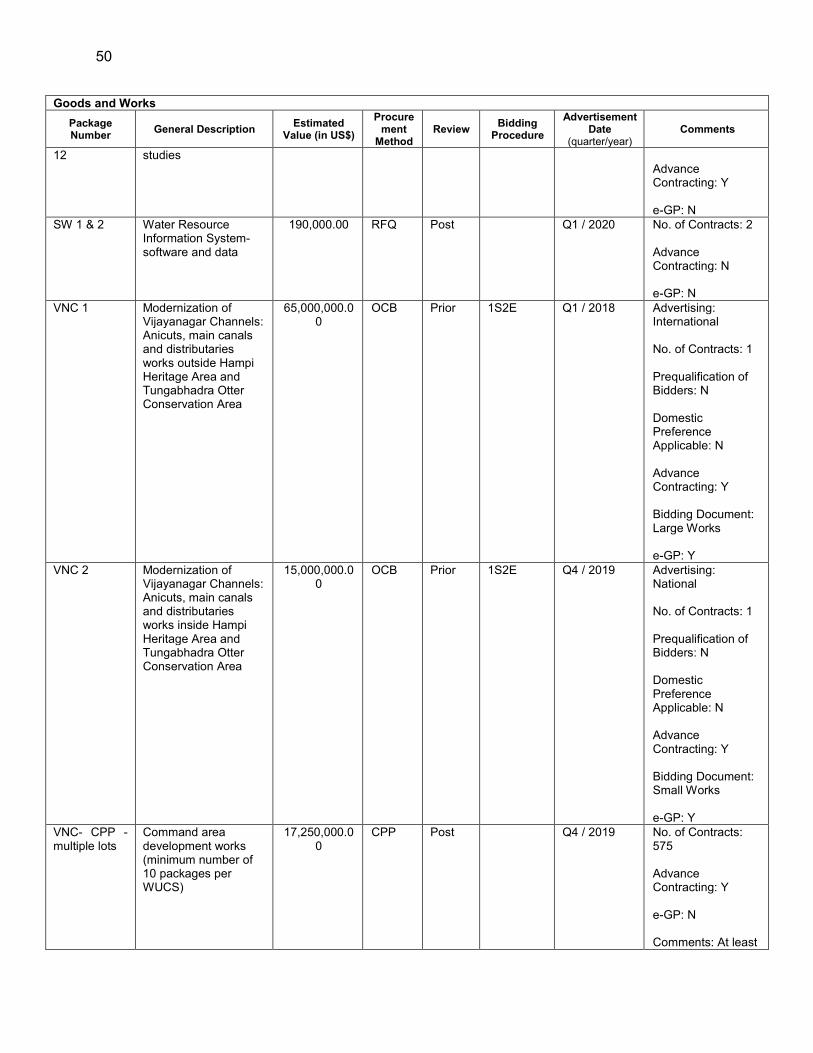

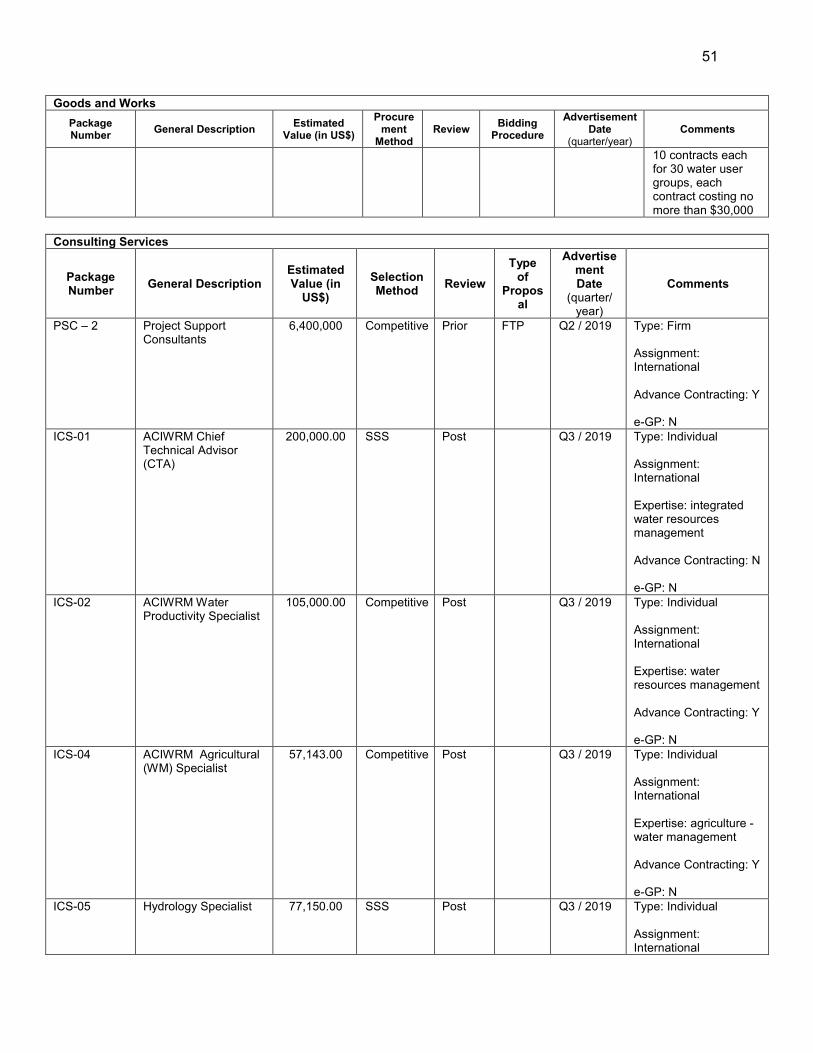

5

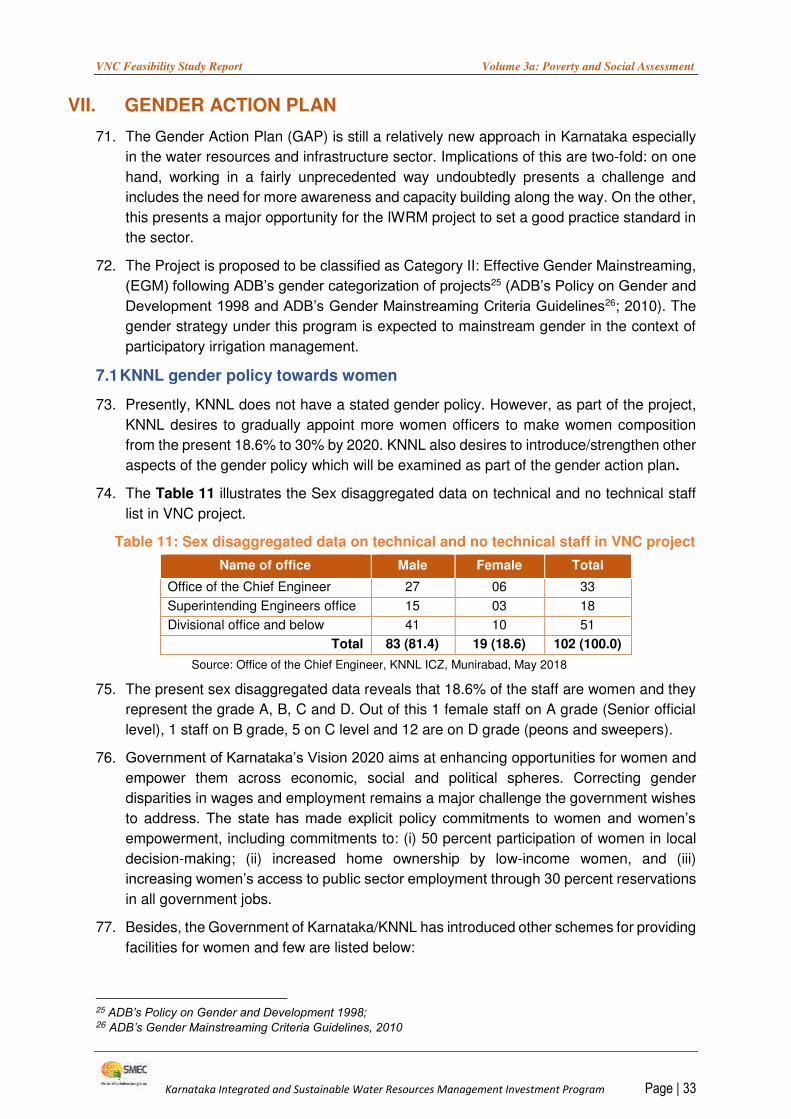

Figure 1: KNNL PMU Organogram

19. Program PMU is in KNNL head office in Bangalore and is headed by the Managing Director of KNNL who is the Program Director. There are 2 Project Implementation Offices in Shivamogga (for Project 1) and Munirabad (for Project 2). PMU and PIO have engineers, accounts and administrative staff. In addition to KISWRMIP, they work on other KNNL projects. So PMU and PIO staff are not fully dedicated staff of PMU and PIO. PMU and PIO do not have a procurement specialist, all engineers and some accounts staff manage procurement. PIOs are short of engineering and accounts staff. Instead of sanctioned strength of 18, there are 12 staff in Munirabad PIO.

6

Figure 2: KNNL PIO Organogram

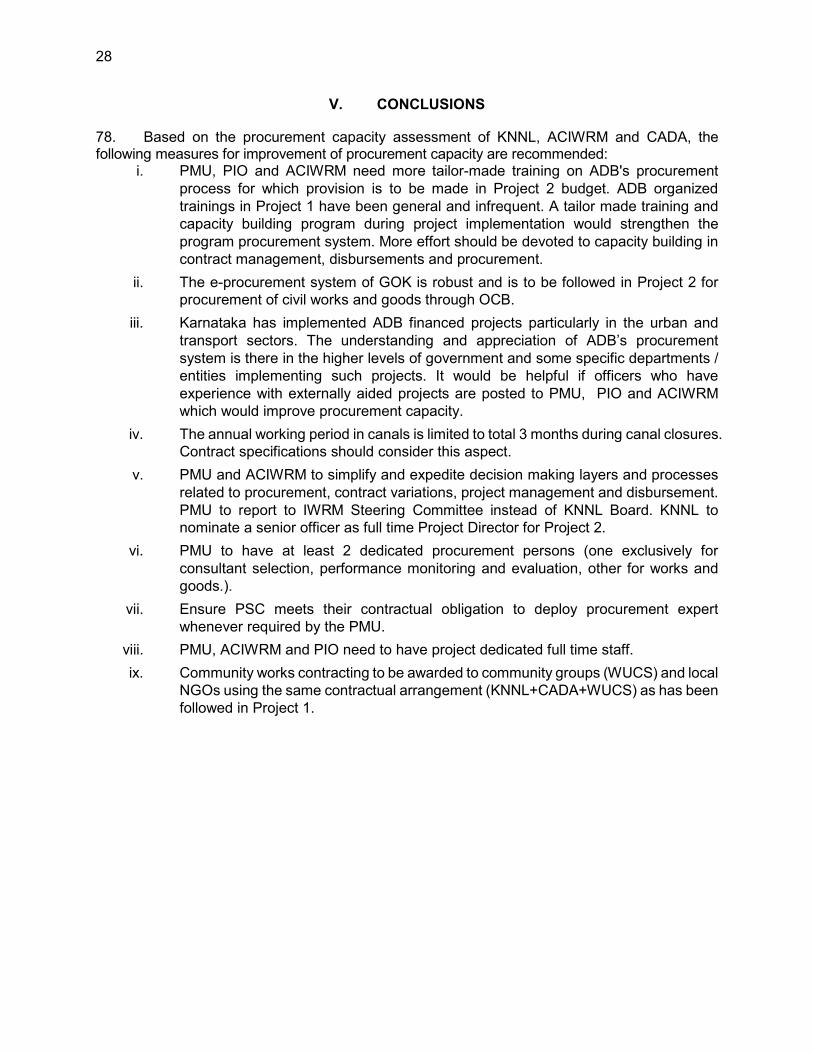

20. Dedicated PMU and Decision Making. The ADB Mission agreed during the Fact Finding Mission for Project 2 in June 2018 with KNNL and Secretary WRD that PMU and ACIWRM would report directly to IWRM Steering Committee. Under Project 1 this was never fully implemented and instead PMU has been reporting to KNNL Board. A government order is expected to be issued enabling PMU and ACIWRM to IWRM Steering Committee. The need for KNNL Board clearance has been a main cause of delays during Project 1 (during evaluations, approvals for contract variations, etc.) so it should help to expedite processes under Project 2. 21. Few PMU and PIO staff have attended ADB procurement procedures training. More focused and extensive procurement training is needed for PMU and PIO. 22. Tender Evaluation Committee (TEC) members are drawn from within PMU, are usually 4 or 5 in number. The members of TEC are appointed by WRD Secretary. The key point is there is no position of procurement specialist dedicated to KISWRMIP in PMU or PIO. Since PSC's

7

procurement expert inputs too are intermittent and are not available sometimes when required, PMU has been having difficulties with procurement issues. Overall, it is inferred that procurement and contract management section of KISWRMIP needs strengthening since Project 2 (and Project 3) are to be implemented in a tight timeframe.

b. ACIWRM

23. The ACIWRM is the first of its kind in India. The IWRM framework provides the opportunity to integrate the land and water related management aspects at the sub-basin and river basin levels. ACIWRM is a think tank of the WRD. It engages in policy analysis, research, planning, capacity building and development of knowledge base. ACIWRM works with the various departments, NGOs, civil society, private sector, farmers and water user associations and other organizations to produce integrated advice to the WRD for managing the state’s water resources. 24. ACIWRM comprises a Government Procedures and Administration Division under the management of the ACIWRM Registrar, and a Technical Division under the leadership of the Technical Director. There are six full time staff comprising training and capacity building; farmer and stakeholder involvement; river basin management; hydrology and irrigation; land and water management; and water resource information systems. Most of the experts are short term contract staff recruited for particular projects. ACIWRM is financed by GOK and supported by ADB financed KISWRMIP. ACIWRM organogram is in Figure 3. 25. Main activities of ACIWRM are:

Karnataka Water Resources Information System

IWRM training and Capacity Building

River Basin Plans in Selected River Basins

State IWRM policy and strategy

Water use efficiency and productivity

Participative land and water management plans

Communication, awareness raising and participation

Preparation of state specific action plan on climate change for water sector

National groundwater management improvement program

River basin modelling

8

Figure 3: ACIWRM organogram

26. The three engineers and principal coordinator for engineers carry out the procurement functions in addition to their regular engineering and management duties. Since ACIWRM is meant to be a think tank, it does not procure works. Some goods procurement (office equipment, website maintenance contract) has been done in Project 1. Primarily individual consultants have been recruited (12 recruited, 8 more being recruited) in Project 1 and more would be recruited in Project 2. ACIWRM intends to procure flow monitoring, water quality and weather monitoring goods packages and software in Project 2. Due to lack of procurement skills within ACIWRM, these could be better procured by either KNNL (which has better experience and skills) or by Department of Hydrology which has carried out this role for the World Bank’s National Hydrology Program on behalf of ACIWRM.

c. CADA

27. The main objective of CADA is to reduce the gap between potential area created and actual area utilized. CADAs are Involved in participatory irrigation management with WUCS.

9

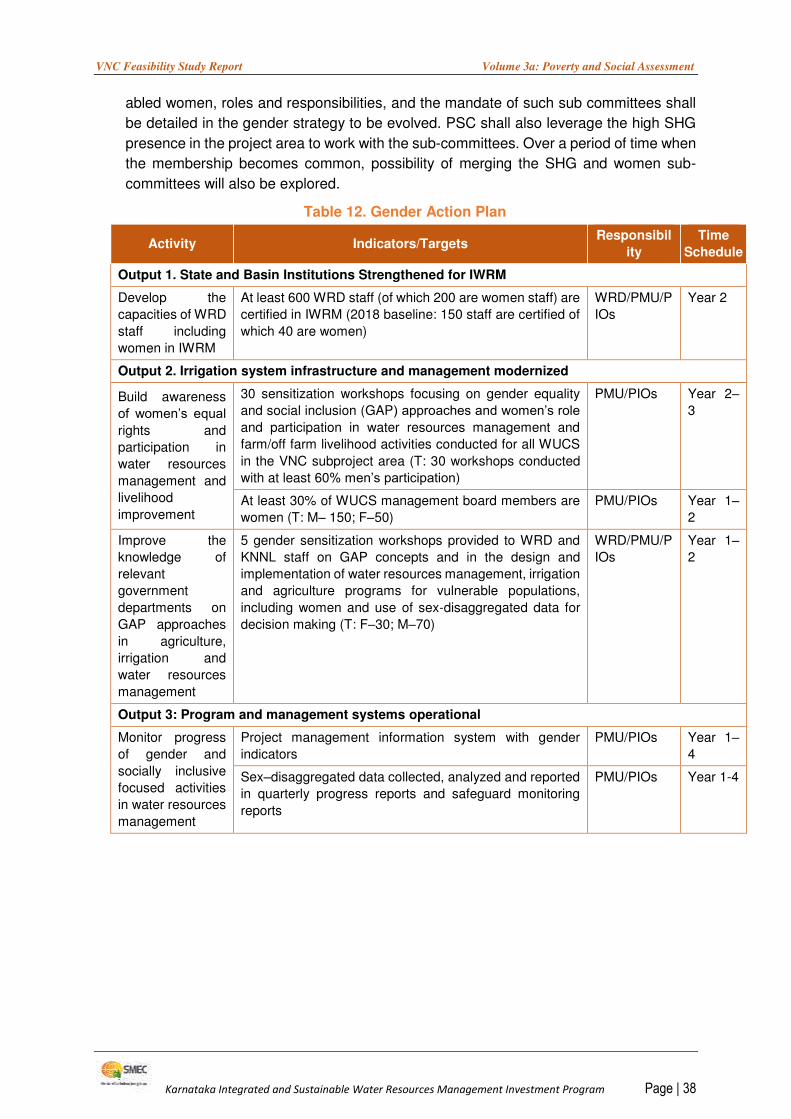

28. The Government of India provides central assistance on matching basis for carrying out central sector command area development schemes. The schemes which are covered under central sector are administration, construction of field irrigation and distribution channels; regulation of field outlets, surveys, adoptive trails, land development training, subsidy to marginal and small farmers, management subsidy for WUCS, evaluation studies and land reclamation. The other schemes viz, access roads, construction of go downs, housing, special component plan and tribal sub-plans etc., are covered under state sector schemes which do not attract any central assistance. 29. CADA Directorate has been established in 2012 to coordinate among the various CADA’s and WUCS of the state to reduce the gap between planned and created irrigation potential. The following CADAs have been formed in Karnataka to carry out CAD Programs. 30. Two recently-tabled Comptroller and Auditor General of India (CAG) audit reports3 in Karnataka assembly (a performance review of numerous irrigation projects by three irrigation corporations including KNNL and an audit of Command Area Development Projects) point out that the deficiencies plaguing these projects ranged from faulty survey and design, erroneous estimates, irregularities in tendering, violations in land acquisition processes and tardy execution of works. Severe shortage of staff compounds the problem in CADAs. Out of 2831 WUCs formed, 981 (i.e. 34 percent) were non-functional. 31. It can be inferred that CADAs institutional capacity and implementation capability is limited. Substantial number of field positions are vacant, i.e., in Munirabad office of CADA, as of June 2018 out of 8 engineer positions, only 4 are filled.

3 CAG Audit Report, Karnakata, Report 8 of 2014, Chapter 2 and Report 9 of 2014, Chapter 2.

10

Table 1: CADA Offices in Karnataka State Sl. No.

Name of the CADA

Year started

Irrigation Projects Covered.

1 Directorate of Command Area Development Authorities, Bangalore

2012 Head office of all CADAs in Karnataka

2 Administrator, CADA Munirabad

1974

Tungabhadra Project

3 Administrator, CADA , Belgaum.

1974

Malaprabha Project &Ghataprabha Project.

4 Administrator, CADA Cauvery Basin Project, Mysore

1974

K.R.Sagar, NuguByramangala, GundalKanva, MarconahalliKabini, Harangi, Hemavathy, Machanabele, Taraka and Votehole.

5 Administrator, CADA Bheemarayanagudi

1977

UpperKrishna Project.

6 Administrator, CADA Bhadra Reservoir Project, Shivamogga

1979

Tunga, Gondi and Bhadra.

32. WUCS component has been very successful in Project 1 and are set to be implemented at a much larger scale in Project 2. The aim of establishing and strengthening WUCS is to promote participatory irrigation management for increasing water use efficiency and promote sustainable agricultural practices. Post modernization, it is planned to hand over management of canal system to WUCS. Being village level community organizations, procurement for WUCS strengthening in Project 1 has been done using direct contracting procedures and same system is being proposed for Project 2. 33. The performance assessment of the 11 WUCS in the Gondi irrigation system is monitored through baseline surveys carried out by PSC. The first assessment carried out during September and October 2016 revealed that most of the WUCS were dormant. As of December 2017, five baseline assessments have been conducted and significant progress is seen in the performance of the WUCS. Most of the WUCS are now active and are implementing command area development works involving lining of the field irrigation channels and construction of cross drainage structures. 34. Key issues identified from interviews with Project 1 PIO Shivamogga are as follows:

• Weak local consultants prepare own projects of WRD, KNNL and CADA

• Exposure to good projects of government staff very limited

• Addition of third party agency for quality control of Project 2 works essential since

PSC does not have required expertise and capacity

• Deputation of dedicated PMU and PIO is not possible for small investments. Since

most of capital works occur during canal closure, having full time staff leads to their

inefficient use.

• Few medium sized bid packages instead of one large package better since large

packages lead to very less competition.

11

• WUCS contracts to be treated as techno social contracts since social organization

and participation of farmers is as important as physical works..

• PMU & PIO need longer duration, tailormade procurement training

• Many PSC team members quit leading to so many replacements. Strengthen

technical / engineering side of PSC.

35. Key issues identified from interviews with PSC are as follows; .

• Strengthen PMU and PIO by adding consultants and contract employees. Strengthen

accounting section of KNNL PMU by posting ADB or WB projects experienced

people

• Processing of payments consists of several review and approval layers: from and is

SMEC - EE - AE - AEE - Accounts Section - EE - SE - CE - EE - Accounts Section -

CAO Dharwad - KNNL finance - SMEC. Find ways to simplify and expedite.

• Project design and bid document preparation of KNNL needs improvement. For

example, gates and grooves for the gates not provided in VNC-1 bidding document,

would lead to contract variations right after contract award. Canal outlets not

provided for in bid document since they have not been identified, left to be done

later. Better to ask farmers first where they want canal outlets and incorporate in cost

estimate and bid document.

• In CAD packages division of flow structures to be part of scope of work. Presently

they are not.

• Water and Land Management Institute (WALMI) to collaborate with ACIWRM and

PSC for large scale farmer training and extension

Information Management

36. Procurement documentation, referencing and monitoring system for all types of contracts exist in KNNL and ACIWRM. Information is in paper files, procurement and project information is available on KNNL website www.http://knnlindia.com in the quarterly progress reports. PSC assists KNNL and ACIWRM with all project documentation, disclosures, preparation and submission of reports to KNNL management, WRD and ADB. 37. Adequate resources are allocated to record keeping infrastructure. Physical and electronic copies of all documents are stored for a minimum period of 5 to 30 years depending on importance and document retention period as defined in Karnataka Public Works Department's "D" code. Contract file with a copy of the contract and all subsequent contractual correspondence is with relevant Executive Engineer, but copies of invoices and payments are maintained separately by the accounts section. 38. As required by the ADB guidelines, all required notices for bids and consultancies are posted on ADB, KNNL or ACIWRM and GOK's e-procurement portal. Bids are advertised on procurement portal on ADB website, Karnataka Government e-procurement portal, Indian newspapers in English and Kannada languages, Indian Trade Journal, State Tender Bulletin, and District Tender Bulletin. Information on procurement opportunities, amendments to the bidding documents, call for expression of interest from consultants is posted on KNNL or ACIWRM websites. In addition, the notification on award of contracts is posted on KNNL or ACIWRM websites.

12

Procurement Practices

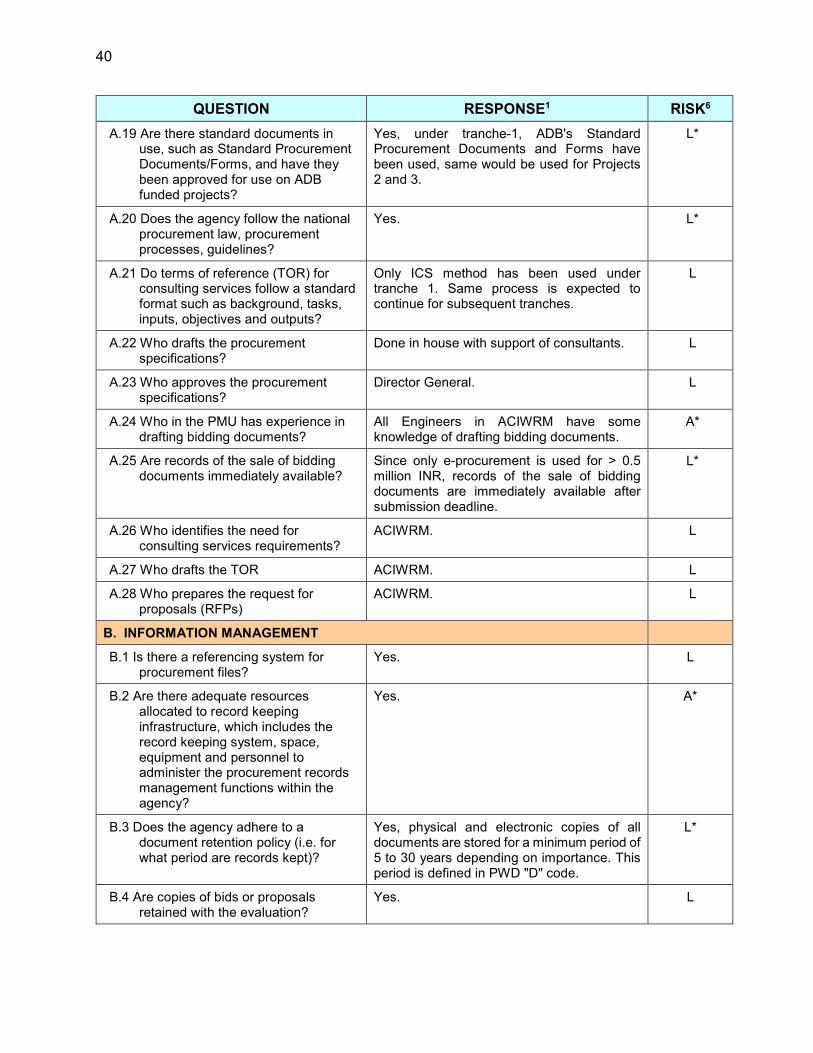

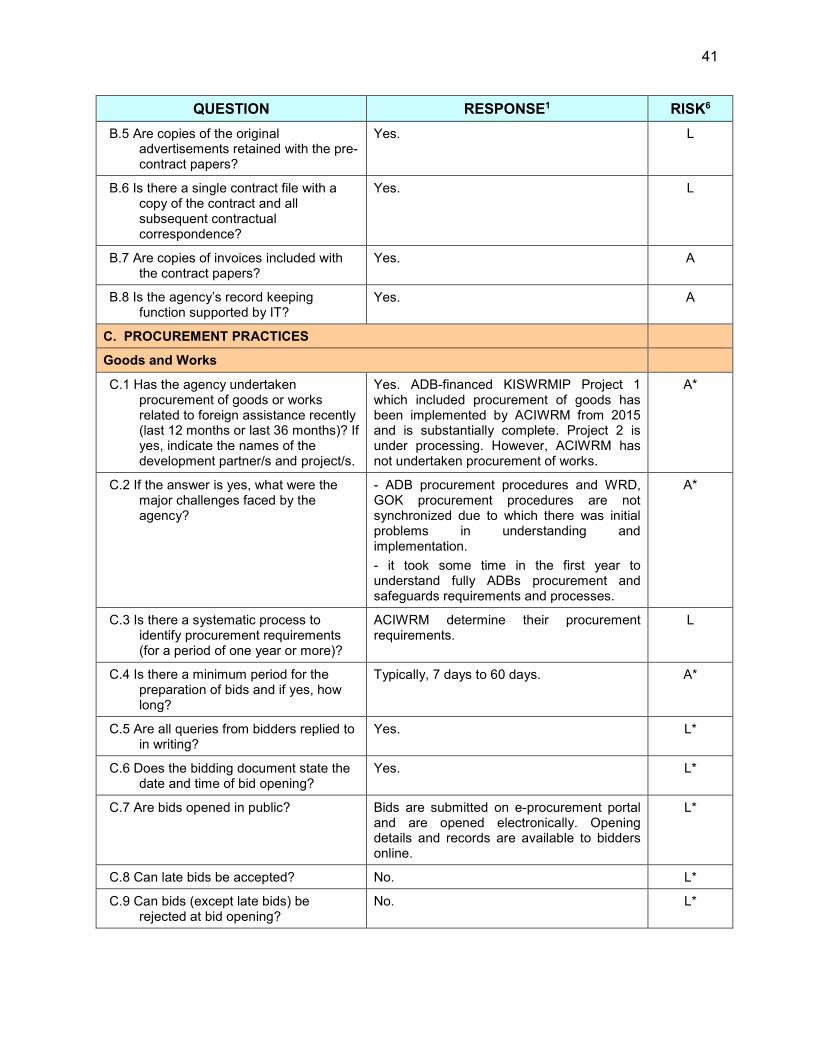

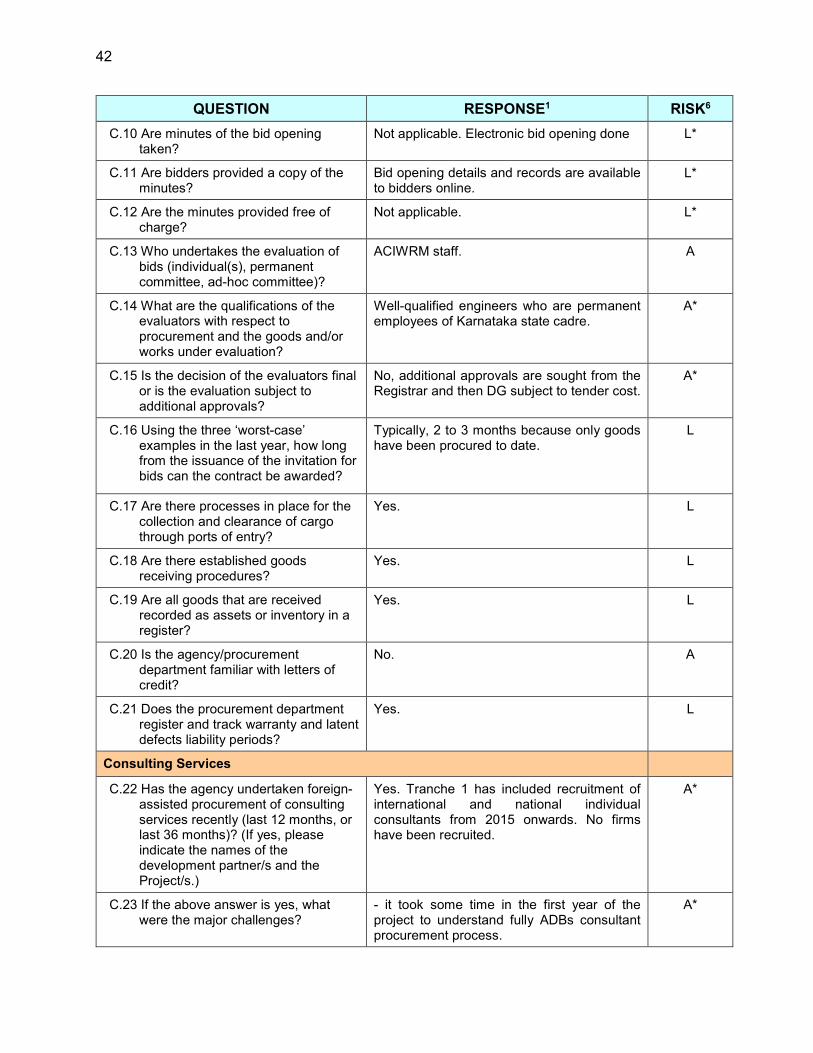

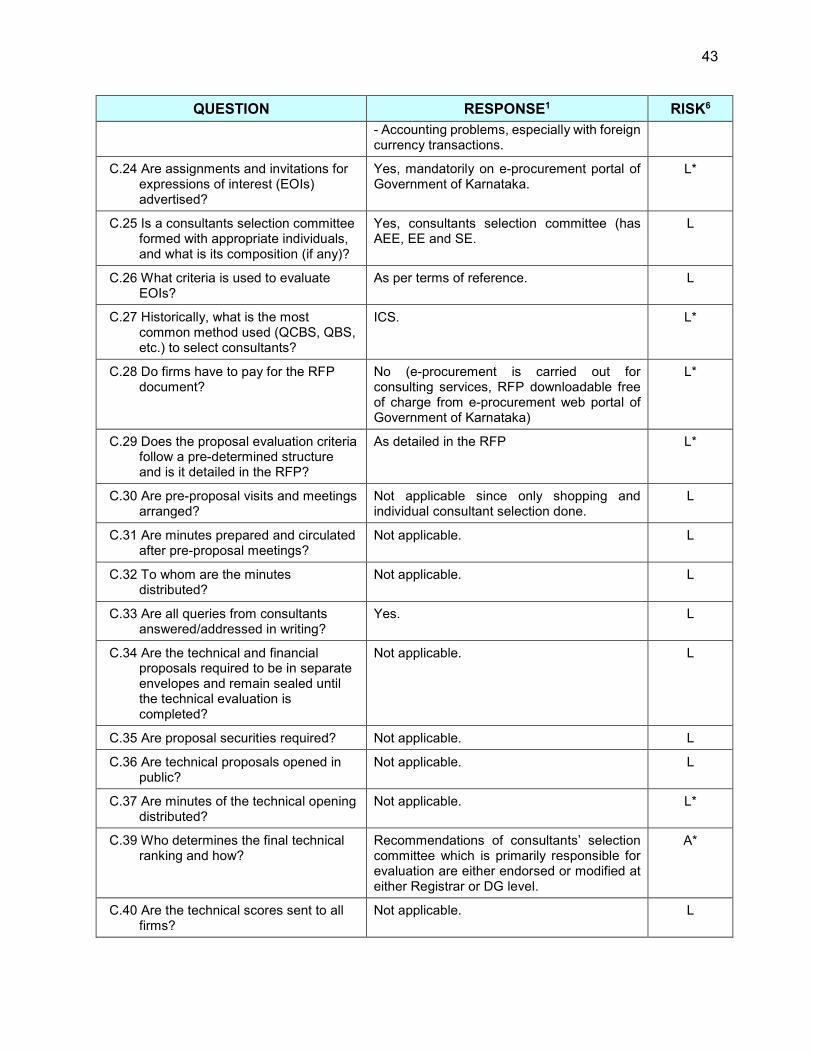

39. Filled in project procurement capacity assessment questionnaires of KNNL and ACIWRM are in Annex 1.

a. KNNL

40. Based on discussions with KNNL officers and conditions included in invitation to bids, details of procurement process of KNNL followed for government financed projects are given below.

KNNL has recent procurement experience for ADB and World Bank projects. KNNL has procured and implemented large contract packages through state financing.

The largest contract awarded till date by KNNL is INR 14285.14 million (~ US$216 million) using national competitive bidding (NCB)for turnkey contract Basaveshwar (Kempwad) Lift Irrigation Scheme. This bid was invited on 23 Dec 2016 and awarded on 17 March 2017 (less than 4 months). Longest times taken from bid invitation to contract award is about 22 months4. In case of modernization project, the largest contract package awarded is for about INR 1060 million (about US$21 million) for Bhadra project canal lining. All contracts of KNNL are procured using NCB. KNNL is following the KTPPA for all procurement. As per the Act e-procurement is mandatory for all procurements above INR. 0.2million (~ $3000) but KNNL is using e-procurement for packages of any value.

KNNL does not have a separate procurement unit. Bidding process is initiated in the field by the executive engineer (EE). The finance unit of KNNL with the support of the technical section (engineers) oversee the bidding process at KNNL central office.

Bidding process

EE prepares the draft tender papers and submits to Technical Sub-Committee (TSC) for approval through concerned (field) superintending engineer (SE) and (field) chief engineer (CE). Once approved, bids are invited by the field EE. Bids are invited either on unit rate or turnkey basis.

EE completes the technical evaluation and submits technical bid evaluation report to CE through SE for approval. CE approves technical bid evaluation report and authorizes opening of financial bids.

Financial bids are opened, evaluated and submitted to the CE for approval for bids up to $0.5 million. Bids between $0.5 million to $1.0 million are submitted to technical subcommittee through SE and CE for examination and recommendation for approval by the managing director KNNL. Bids above $1.0 million are sent for decision to the KNNL Board. KNNL is generally inviting percentage rate tenders and bidders quote above or below the estimated cost which is updated based on latest schedule of rates (SOR) for financial bid evaluation purpose.

4 The three works of upper Bhadra project entrusted on EPC turn key contract basis are: Package 1- Lifting 15 TMC

water from Tunga river to Bhadra reservoir (awarded to M/s SEW-Jyoti (JV), India, for INR. 3240 million at 17% above the estimated cost- 2007-08 SOR), Package 2-Lifting 21.5 TMC water from Bhadra reservoir to Ajjampura tunnel (awarded to M/s RNSIL (JV), Bangalore for Rs. 10320 million at 17.74% above estimated cost) and Package 3-Ajjampura tunnel (awarded to M/s SNC Power,Bangalore for Rs. 2240 million at 19.76% above estimated cost). Bids for all the packages were invited on 22 Dec 2006 and works awarded in Oct 2008.

13

As per KTPPA, bids above 10% of the estimated cost are generally considered as high which may go for rebidding. However in case of KNNL, TSC of KNNL fixes the range of percent variation which is acceptable for accepting the bids. Time taken from bid invitation to bid award is about 4-6 months in normal cases. Exceptionally, bids upto 20% above estimated cost have been awarded. Due to high competition resulting from adoption of e-procurement, it is rare that lowest bids exceed 10% above estimated cost. The bid prices depend on location and access to work site, among other factors.

Single stage single envelope procedure is followed for procurement of works below $100,000 and all goods packages. Single stage two envelope procedure is used for works between $100,000 to $2 million. Works costing above $2 million require prequalification of contractors. Technical bid is evaluated on the basis of pre-qualification criteria (turnover, similar experience, availability of man and machinery, cash flow, etc.).

KNNL specifies class of contractor who can submit the bid in the bid invitation. (Super Class, Class I, Class II and Class III registered with KNNL or other specified organisations) Super Class contractor is eligible for bidding for any contract size.

As per e-procurement procedure, earnest money deposit (EMD) or bid deposit up to INR 0.1 million is submitted online through credit or debit card, bank transfer etc. and the remaining EMD (in case EMD is more than INR 0.1 million) through demand draft or banker’s cheque or bank guarantee.

The bidder has to upload the scanned copy of the necessary certificates and documents included in support of eligibility criteria including proof for remaining EMD. The original certificates and documents are required to be produced before opening of tender containing technical bid for verification.

Dispute resolution is at two levels at present - Initial resolution at CE or Managing Director level failing which contractor can move the court for redress.

41. The standard bidding documents (SBD) of the GOK for goods, works and consultants were reviewed. Standard bid documents for works, goods and consultants have been standardized by GOK, Ministry of Finance, Procurement Cell and are used by GOK departments including KNNL and ACIWRM. Same SBD is used for national or international bidding. Process of procurement of consultants is similar to that of works or goods and requires consultants to provide bid document fee and bid guarantee. The SBD and the GOK circulars governing procurement are available in Department of Finance, GOK website www.finance.kar.nic.in/trans/tender.htm. The GOK SBDs are substantially aligned with ADB SBDs except for few key differences which are presented in Table 2.

Table 2: Summary of features and Variations - Karnataka Standard Bid Documents and ADB SBD

Procurement Type

Karnataka Standard Bid Document

ADB Standard Bid Document

Variations

Goods KG-1, for estimated cost less than $20,000

Compatible with single stage two envelope goods SBD

Karnataka SBD clause references; Section II Instruction to tenderers Clause 1.1 Tenderers not blacklisted by GOK Clause 4.1 tender language Kannada (local language) Clause 11.3 bid guarantee from nationalized or scheduled banks

14

Procurement Type

Karnataka Standard Bid Document

ADB Standard Bid Document

Variations

Clause 19.3 in case of words and figures discrepancy, lower value prevails Clause 23.1 can vary purchase quantities during contract signing up to 25% Dispute resolution is departmental.

KG-2, for estimated cost more than $20,000 up to $100,000

Compatible with single stage two envelope goods SBD

Variations as for KG-1 except that the tender language is English. Dispute resolution is departmental.

KG-3, for computer systems estimated cost less than $100,000

Compatible with single stage single envelope goods SBD

Differences same as for KG-1 except that the tender language is English. Additional clauses and price of annual maintenance contract and service centre requirements re included.

KQ-1 for shopping of goods all items together less than $2,000

No equivalent (previously known as shopping)

For low value goods. Quotation validity of 30 days.

KQ-2 for shopping of goods all items evaluated separately, total cost less than $2,000

No equivalent (previously known as shopping)

For low value goods. Quotation validity of 30 days.

KSO for shopping, ready to use items, cost less than $2,000

No equivalent

Works KW-1, for item rate works less than $40,000

Item rate small works, single stage single envelope

Tenders from JV not accepted. Bid validity 90 days. Value of work declared in notice inviting tender. Bid security varies as follows; 2.5% for cost up to INR 20 lakhs 2% for cost INR 20 lakhs – INR 100 lakhs 1.5% for cost INR 100lakhs – INR 1,000 lakhs and 1% for cost more than INR 1,000 lakhs. Dispute resolution is with the procuring department.

KW-2, for estimated cost more than $20,000 up to $100,000

Item rate small works, single stage single envelope

Same as KW-1

KW-3for estimated cost more than $100,000 up to $200,000

Item rate small works, single stage two envelope

Bid security of 1.5% of estimated cost. Dispute resolution is departmental.

KW-4 estimated cost more than $200,000 up to $2,000,000

Item rate large works, single stage two envelope

Bid security of 1.5% of estimated cost. Arbitration clause in GOK SBD provided.

KW-5 estimated cost more than $2,000,000. Prequalification required, JV not permitted

Prequalification followed by single stage single envelope

Bid security of 1% of estimated cost. Arbitration clause in GOK SBD provided.

KW-6 estimated cost more than $2,000,000. Prequalification required, JV permitted

Prequalification followed by single stage single envelope

Bid security of 1% of estimated cost. Arbitration clause in GOK SBD provided.

Consultants

15

Procurement Type

Karnataka Standard Bid Document

ADB Standard Bid Document

Variations

KC-1 time based, less than $20,000, for firms or NGOs or organizations QCBS, 75% : 25%

QCBS FTP The consultant selection process substantially similar to ADB QCBS process.

KC-2 time based, more than $20,000, for firms or NGOs or organizations QCBS, 75% : 25%

QCBS FTP

KC-3 lumpsum less than $20,000, for firms or NGOs or organizations QCBS, 75% : 25%

QCBS FTP

KC-4 lumpsum more than $20,000, for firms or NGOs or organizations QCBS, 75% : 25%

QCBS FTP

KC-5 time based, less than $20,000, for firms or NGOs or organizations LCS

LCS The consultant selection process substantially similar to ADB LCS process.

KC-6 time based, more than $20,000, for firms or NGOs or organizations LCS

LCS

KC-7 LCS lumpsum less than $20,000

LCS

KC-8 LCS lumpsum more than $20,000

LCS

KC-9 SSS time based, less than $10,000

SSS The consultant selection process substantially similar to ADB LCS process.

KC-10SSS lumpsum, less than $10,000

SSS

KC-11, Individual, less than $2,000, time based

QCBS BTP The consultant selection process substantially similar to ADB QCBS BTP process

KC-12, Individual, less than $2,000, lumpsum

QCBS BTP

42. Table 3 shows procurement carried out by KNNL for GOK projects and Program PMU for Project 1 of KISWRMIP. KNNL has experience in procurement of works, goods and consultants. 43. Following inferences can be drawn from analysis of information in Table 3:

All GOK financed works contracts are procured through National Competitive Bidding. Contract invitation to award durations ranged from 5 weeks to 13 months. Large

number of contracts (17 out of 29) were awarded in last quarter of financial year 2017-18.

PMU is experienced in recruiting international consultants using ADB's Quality and Cost Based Selection.

Most contracts are lift irrigation schemes, procured on turnkey basis including operation and maintenance for 3 to 5 years.

Contract award costs range between $ 1.6 to $ 216m million.

44. NCB Gondhi contract of Project 1 had only one qualified bidder (during second call for bids, first call had no response) who backed out from contract signing. Qualified bidder from the 2nd call refused to sign contract until KNNL settled his arbitration claims from earlier GOK financed

16

contracts. In the third bid call there were technical issues, bid was re-invited. Contract was awarded after 4th call.

Table 3: Procurement by KNNL for GOK Projects and Project 1 of KISWRMIP

l.

No Tender Number Tender Title Bid invite

Date Contract

Value

(INR

million)

Contract

Award

Date

1 KNNL/2014-15/HL/WORK_IND

ENT12847

Tubchi-Babaleshwar Lift Irrigation Scheme on Turn-key Basis

06-07-2014 12240 05-11-2014

2 KNNL/2014-15/LI/WORK_INDE

NT13953

CHACHADI Babaleshwar Lift Irrigation Scheme on Lumpsum Turn-key Basis

27-09-2014 106.22 31-03-2015

3 KNNL/2014-15/LI/WORK_INDE

NT14481

SHIGGOAN Lift Irrigation Scheme FROM DC-6

14-11-2014 434.30 10-04-2015

4 KNNL/2014-15/LI/WORK_INDENT14480/CALL-2

Savanur Lift Irrigation Scheme Head work on Lump sum Turnkey Basis

14-11-2014 1795.50 16-04-2015

5 KNNL/2015-16/LI/WORK_INDE

NT16373

Filling up Kaginale Tank and other 21 surrounding Tanks in Byadgi Taluk, Haveri District by Lifting water from

Varada River on Turnkey Basis.

20-07-2015 506.49 24-06-2016

6 KNNL/2014-15/LI/WORK_INDE

NT13940

Filling of 22 MI Tanks by pumping of water from Hiranyakeshi river in Chikkodi

taluka & Hukkeri taluka of Belgaum district on Turnkey basis

21-10-2015 807.77 04-07-2016

7 KNNL/2015-16/HL/WORK_IND

ENT16696

Veerabhadreshwara Lift Irrigation Scheme

24-11-2015 4543.99 22-11-2016

8 KNNL/2015-16/LI/WORK_INDE

NT16839

Gobbargumpi and Amargol Lift Irrigation Scheme - I

19-12-2015 296.69 16-01-2017

9 KNNL/2015-16/LI/WORK_INDE

NT16842

Lift Irrigation Scheme - II On Turnkey Basis. At The Following Locations. 1)

Gobbargumpi On Tupparihalla 2) Amargol On Bennihalla.

19-12-2015 482.28 16-01-2017

10 KNNL/2015-16/LI/WORK_INDE

NT17059

Venkateshwara Lift Irrigation Scheme on TURN KEY basis

19-12-2015 547 17-09-2016

11 KNNL/2015-16/LI/WORK_INDE

NT17389

ALWANDI BETTGERE Lift Irrigation Scheme,Koppal Taluk.

07-01-2016 864 08-09-2016

12 KNNL/2016-17/LI/WORK_INDE

NT20839

BASAVESHWAR (Kempwad) Lift Irrigation Scheme

23-11-2016 14285.14 17-03-2017

13 KNNL/2016-17/LI/WORK_INDE

NT21077

BasapurLift Irrigation Scheme II Stage 17-12-2016 311.20 11-05-2017

14 KNNL/2017-18/LI/WORK_INDE

NT22289

Extension of filling of Mi tanks 39nos. under ShiggoanLift Irrigation Scheme.

22-04-2017 344.75 20-01-2018

15 KNNL/2017-18/LI/WORK_INDE

NT22282

Filling up of 48 MI/ZP tanks by lifting water from existing Delivery Chambers

DC-2 and DC-4.

22-04-2017 1000 03-01-2018

16 KNNL/2017-18/LI/WORK_INDE

NT22304

SASVEHALLI Lift Irrigation Scheme inHonnalitaluk,Davangere district,

Karnataka

26-04-2017 4620.89 14-08-2017

17

l.

No Tender Number Tender Title Bid invite

Date Contract

Value

(INR

million)

Contract

Award

Date

17 KNNL/2017-18/LI/WORK_INDE

NT22682

Filling 46 tanks and 19 Bhandaras coming under HaliyalTq, UK Dist by

lifting water from Kali River on Turn-Key Basis

01-09-2017 2541.10 09-01-2018

18 KNNL/2017-18/LI/WORK_INDE

NT22750

Providing water source for irrigation and recharging ground water for filling up of 9 tanks Tadakod, Garag, Niralakatti, Hale

Tegur, Bogur, and Bokyapur villages under scheme-1 & scheme-2 coming

under Dharwad district.

16-10-2017 242.65 25-01-2018

19 KNNL/2017-18/LI/WORK_INDE

NT22743

Fillingup of MItanks by liftingwater from BedtiRiver

onTurnkeybasisnearBelavantara village of Kalaghatagi Taluk, Dharwad district.

15-09-2017 1274.88 20-01-2018

20 KNNL/2017-18/LI/WORK_INDE

NT22879

Filling up RanebennurDoddakere and other 3 surrounding tanks in Ranebennur Taluk, Haveri District by lifting water from Tungabhadra River on lump sum turnkey

basis.

22-09-2017 400 05-01-2018

21 KNNL/2017-18/LI/WORK_INDE

NT23156

Lift Irrigation Scheme for providing Drinking water&recharging ground water

to fill 39tanks of 19villages of Raibagtaluk, Belagavi district by lifting water from KrishnaRiver on TurnKey

Basis.

15-11-2017 1115.16 07-03-2018

22 KNNL/2017-18/LI/WORK_INDE

NT23500

Lift Irrigation system from Varada river near Honkan village to fill the Tanks in Hirekerur Taluk(13Nos) and Byadagi Taluk (2Nos) and other allied tanks.

05-12-2017 365.61 08-03-2018

23 KNNL/2017-18/LI/WORK_INDENT22585/CALL-2

Lift Irrigation Scheme for providing drinking water & recharging ground water to fill 19 tanks of 10 villages in Kudachi by pumping water from Krishna river in

Raibagtalukq of Belgaum district

13-12-2017 357.48 09-03-2018

24 KNNL/2017-18/LI/WORK_INDE

NT23635

Lift Irrigation Scheme to fill 15 tanks &Chulkinal reservoirand lifting of water from Manikeshwara&Halahalli barrage

constructed on Manjra River near Km. 60 & Km. 90 of RBC of KP for stabilization of atchakat under Bidardistrict on Turn

Key Basis.

10-12-2017 3267.70 21-03-2018

25 KNNL/2017-18/LI/WORK_INDE

NT24492

Lift Irrigation system and Construction of Gravity Distribution System including structure for providing lifting of water

from Varada River near Banavasi village to fill 32 tanks of BanavasiHobli of Sirsi

taluk of Karwar District.

18-01-2018 445.56 17-03-2018

26 KNNL/2017-18/LI/WORK_INDE

NT24528

KULAHALLI-HUNNUR Lift Irrigation Scheme and surrounding villages in

Jamakhandi taluk, Bagalkot district by lifting water from Krishna river on turn

key basis.

18-01-2018 857.50 14-03-2018

27 KNNL/2017-18/LI/WORK_INDE

NT24503

Filling up of Asundi Tank and other surrounding 17 MI/ZP tanks in

Ranebennur, Byadagi and Hirekerur Talukas of Haveri District by Lifting

22-01-2018 766 08-03-2018

18

l.

No Tender Number Tender Title Bid invite

Date Contract

Value

(INR

million)

Contract

Award

Date

Water from Tungabhadra River on lump sum turnkey basis.

28 KNNL/2017-18/LI/WORK_INDE

NT24696

Godachinamalki Lift Irrigation Scheme Stage-I & II of Gokak Taluk to irrigate an area of 2569.42 ha. on turn-key basis.

03-02-2018 748.81 20-03-2018

29 KNNL/2017-18/LI/WORK_INDE

NT24726

Create 2723ha, of Command area under Varahi Lift Canal under Varahi Irrigation

Project on Turn-Key Basis.

09-02-2018 3138.34 16-03-2018

KISWRMIP Project 1 major contracts - (value in parentheses in US$ million)

30 FMT- ICB-2 Flow measurement and telemetry system – supply

and installation

Q1 / 2015 15.32 (2.55)

13-NOV-15

31 Gondi-NCB -1

Main canal anddistributaries earthwork,lining, structures and flow measurement devices

Q4 / 2015 100.15 (16.67)

18-FEB-16

32 PSC-1 (QCBS) Assignment: International

Program Support Consultants (including WUCS strengthening support)

Q4 / 2013 15.80 (2.63)

30-JUN-15

45. From discussions with the officers of KNNL, it is understood that for contracts up to $ 50 million, contractors have sufficient capacity to carry out irrigation projects by using adequate level of technology such as lining by pavers, construction of structures, cross drainage works etc. As an example, procurement process followed for a large project is briefly explained here. In case of Bhadra project for which modernization works estimated to cost INR. 9510 million ($211.3 million) works were divided into twelve packages and bids invited. The bidders participated in 10 packages out of 12 packages and bids were finalized at 5% above the 2007-08 cost estimates. For the balance two packages, for which there was no response from the bidders, works were sub divided into seven packages and bids re-invited but the bidders responded for only five packages. It is understood that the reason for no response from bidders for some initial reaches was mainly due to excessive seepage problem in the reaches. As a part of the contract, contractor is required to maintain the canals for a period of 2 years after completion of works and for this purpose 7.5% of the contract amount is retained as performance security. 46. The size of bid package for main canal varied from INR. 532.8 million ($11.8 million) to INR. 1068.2 million ($23.7 million) whereas size of package for distributaries varied from INR 29.1 million ($0.65 million) to INR 68.2 million ($1.5 million). The size of the packages indicate that local contractors have capacity to do works of more than INR1000 million ($22.2 million). Only 2 or 3 contractors have capacity to do work above $100 million with mechanized equipment and latest technology. 47. In some contracts of Dam Rehabilitation and Improvement Project being financed by World Bank quantities doubled during implementation since field surveys and investigations were inadequate. Consultants selected to prepare projects of KNNL or CADA are mainly selected on lowest price basis, are given inadequate time to prepare feasibility and detailed project reports, leading to redesign and delays during implementation. 48. WUCS contracts procurement and implementation has been delayed due to multi stage invoice checking and processing. Invoices are prepared by WUCS, verified by CADA engineers

19

and then sent to PIO. Within PIO invoice travels from executive engineer to assistant executive engineer to assistant engineer to accounts section. Once cleared by accounts, it goes through KNNL executive engineer to superintending engineer to chief engineer, then back to executive engineer who forwards it to KNNL Accounts Section at Dharwad. KNNL's accounts sections is understaffed, are not very familiar with ADB project disbursement procedures. Then the invoice is sent to KNNL finance division at Bangalore. The delay could be reduced by delegating powers within KNNL for contract signing and invoice approval to superintending or executive engineers and posting to PMU and PIO and accounts sections, staff with prior experience of multilaterally financed projects.

b. ACIWRM

49. ACIWRM activities are undertaken with the support of individually recruited consultants. Under Project 1, seven international individuals are to be recruited under the “Support Consultants” budget allocation item and 15 national individuals are to be recruited under the “Surveys, Design and Studies” budget allocation item 50. Table 4 presents the procurement of goods and consultants carried out by ACIWRM for Project 1 using ADB procurement procedures. No works procurement was done, nor any contracts procured through GOK procedures.

Table 4: Procurement carried out for Project 1 of KISWRMIP by ACIWRM

Sl. no.

Package Title

Bid or EOI

invitation date

Number of bids

received

Contract signing

date

Package cost (INR)

A Works

None

B Goods

1 Supplying Software, Installing in the servers, desktop computers / laptop

09-12-2016 3 01-03-2017 6601000

2 Supply of office Furniture 28-10-2015 3 30-12-2015 1836400

3 Supply of office Furniture 10-07-2017 3 17-02-2018 198000

4 Supply of Modular Workstations 28-10-2015 3 30-12-2015 959703

5 Supply of Digital Prinitng Maps 27-04-2016 3 12-05-2016 66596

6 Supply of Digital Prinitng Maps 14-07-2017 3 13-09-2017 88264

7 Supply of Culturable Command Area Maps

05-04-2017 3 22-06-2017 2760000

8 Supply and Installation of Desktop, Computers, Server Computers

30-10-2017 3 11-12-2017 3409600

9 Supply and Installation of Desktop, Computers, Server Computers

11-01-2016 3 15-03-2016 3847254

10 Supply of Buy back of Switch mounting rack

27-02-2018 3 21-03-2018 120596

11 Website & Web Designer 27-04-2016 3 30-05-2016 85000

12 Autodesk/Auto Designing Software AutoCAD

28-10-2016 1 01-02-2017 173016

13 Supplying ERDAS Software, Installing in the Desktop Computer

30-08-2016 3 22-11-2016 2928188

20

Sl. no.

Package Title

Bid or EOI

invitation date

Number of bids

received

Contract signing

date

Package cost (INR)

14 Creative agency for designing key visual creation and brochure

01-09-2017 3 28-10-2017 1256700

15 Supplying Tideda and Td gauge Software

21-09-2017 3 27-11-2017 865128

16 Arc GIS Software in the Desktop Computers

30-06-2016 3 03-08-2016 2139029

C Consultants

1 Chief Technical Advisor 13-12-2013 21 02-06-2015 34329122

2 International River Basin Modeling Expert

03-12-2015 16 27-06-2016 8638051

3 International Hydrology Expert 03-12-2015 20 27-06-2016 3590720

4 International Masscote Expert 19-07-2016 2 11-08-2016 2188848

5 International Irrigation Modernization Expert

25-06-2017 18 24-10-2017 7562572

6 Water Resources Policy and Institutions

03-12-2015 12 27-06-2016 1457000

7 Water Quality Specialist 12-07-2017 6 25-10-2017 2316000

8 Videographer 18-05-2017 6 25-10-2017 1264720

9 Training and Capacity Building Specialist

07-05-2017 16 24-11-2017 643125

10 Agriculture Specialist-Water Use Efficiency & Water Productivity

17-08-2017 7 04-01-2018 1327500

11 National Economist / Livelihood Expert

11-07-2017 11 20-01-2018 3293850

12 Agriculture Specialist - Micro Irrigation

17-08-2017 6 11-01-2018 1653750

51. All goods packages were procured quickly, took 1 to 3 months. Recruiting international specialists took a long time, especially Chief Technical Advisor position which took 18 months. ACIWRM took 3 to 7 months to recruit other international and national individual consultants. For many positions expression of interest deadlines were extended, some positions were re-advertised.

c. CADA

52. KNNL, CADA and WUCS (tripartite agreement) have signed the community procurement packages (CPPs) contracts in Project 1. This arrangement was made since CADA does not have adequate staff, resources and expertise to procure and manage CPPs. Same arrangement is expected to continue in Project 2. 53. Project 1 WUCS Packages. As per the procurement plan of Project 1, CPPs will be less than $30,000 each and may be directly awarded to the relevant WUCS as community works contracts. ADB has approved the award of 130 community participation packages in the Gondi subproject amounting to about INR 238,700,000 ($3.6 million). KNNL has identified a further 107 packages to continue improving farmer irrigation canals, improvement to tanks, construction of

21

WUCS offices and provision of furniture and equipment, and installation of water control gates. The additional packages will amount to about INR 187,100,000 ($2.8 million)..Signing of the contracts (between KNNL, CADA and WUCS) happened between 30 January 2017 and 28 August 2017. As per the contracts, works were to be completed within 3 months, however, construction could not be finished on time due largely to delayed release of mobilization payments. Construction period was also limited due to canal closures in June and December 2017. 54. Project 2 WUCS Packages. About 575 WUCS packages will be shared amongst the VNC WUCS. Each package will be less than $30,000. The total amount allocated for this activity is about $20 million equivalent. Like those implemented at Gondi in Project 1, the packages will improve the field irrigation canals, construct WUCS offices where necessary, and provide the WUCS offices with furniture and equipment. Packages may also be used to establish and strengthen the WUCS federation.

E-Procurement

55. E-Procurement has become the default mode of procurement in Karnataka. Karnataka Unified End-to-End e-Procurement System is implemented by Centre for e-Governance, GOK. About 200+ government departments, parastatals, universities, few government of India agencies and some private sector clients are using the e-Procurement services. e-Procurement started in 2007 with 9 clients and has quickly grown to be the dominant procurement mode of GOK. Two full-fledged training units at Bangalore and Dharwad train client and contractor staff. 56. The technology used is enterprise level software designed and developed on open source platform. System is flexible enough to address unique process and functional requirements. The platform is hosted in State Data Centre of GOK. There are 6 modules of e-Procurement which are chosen by the user agency as per its requirement:

- e-indents and e-estimates

- e-Tendering

- e-Contract Management

- e-Catalogue Management

- e-Auction

- e-Payment

57. Complete security of bids is ensured by asymmetric bid encryption / decryption using private key infrastructure. Transfer of data is through SSL tunnel. Documents are encrypted by bidder prior to uploading his bid. Bid can be decrypted only with the private key of the bid official after the scheduled time of bid opening. Confidentiality of identity of bidders is maintained and time stamping of all transactions and workflows is carried out. Digital signature certificates are used for bid submission and opening. Use of the system is free of charge for all government departments and parastatals. Options are available for electronic payment and refund of bid security. 58. The unified e-Procurement platform has been incorporated by an amendment (Section 18-A. E-Procurement) to the KTPP Act, 1999 to enable legal validity. The e-Procurement system has been instrumental in substantial increase in bidder participation, decrease in bid premium and steep reduction of time in bidding cycle.

22

59. The system has been set up and is run under public private partnership mode with GOK and a private sector firm as partners with transaction based revenue model for sharing revenues. Centre for e-Governance is the implementing agency for e-Procurement. Centre for e-Governance Chairman is the Principal Secretary of Department of Personnel and Administrative Reforms, GOK and day to day operations are overseen by a Chief Executive Officer and Project Director. 60. E-procurement portal of GOK used by KNNL https://eproc.karnataka.gov.in/eprocportal/pages/index.jsp?language=en. This E-procurement system has been evaluated by ADB during Project 1 preparation and found fit for use in ADB financed projects.

Effectiveness

61. Contractual performance is monitored and reported but there is scope for improvement, there are delays in reporting. PMU monitors systematically its contractual payment obligations. ADB's standard bidding documents are followed, arbitration is provided for as per India Arbitration Act. Procurement decisions are supported by written narratives such as minutes of evaluation, meeting, negotiation and contract variation. The procurement appeals process has been laid out in Chapter II, Clause 16, Appeals of KTPPA. Chapter IV details Offenses and penalties. detailed rules, orders, notifications and circulars have been issued by GOK regarding KTPPA to ensure proper compliance of the procurement law. 62. No mis-procurement has been declared by ADB in Project 1.One package (Gondi-NCB -1) was rebid four times in Project 1 due to no bids received or bidders bid security lapsing before contract signing. None of the contracts have been cancelled. PSC performance related to participatory irrigation management and WUCS is deemed highly successful. PSC however has replaced many key staff multiple times, has been unable to deploy procurement expert when required, has no staff to effectively assure construction quality. So PMU desires to recruit a new third party quality assurance consulting firm for Project 2 which would enhance implementation effectiveness.

Accountability Measures

63. There are five major government bodies to check procurement probity issue in India namely Procurement Policy Division, Comptroller and Auditor General (CAG), Central Vigilance Commission (CVC), Competition Commission of India (CCI), and Central Bureau of Investigation (CBI). While the CAG and CVC address the probity issues, the CCI takes on the anti-competitive elements. The CVC has urged for adopting Integrity Pact towards enhancing transparency, equity, and competitiveness in the public procurement system. Accordingly, it approved the appointment of Independent External Monitors in 132 procuring entities in 2016 (CVC, 2017). However, CVC or the CAG do not have the power of prosecution to take disciplinary action against the procurement irregularities. Instead, they only advise or recommend disciplinary actions. Apart from probity issue, CVC and CAG also release guidelines on public procurement, which are mostly advisory in nature, but not binding on the procuring entities. At state level, Karnataka has vigilance officers in every major organization or department, Anticorruption Bureau and Karnataka Lokayukta are tasked with investigating corruption cases. 64. Procurement transactions are decided upon in case of KNNL by Estimates Review Committee and TSC and KNNL Board, the approval process therefore takes time. In case of ACIWRM, most decisions are taken inhouse with endorsement of Secretary, WRD.

23

Commencement of procurement is not dependent on any external approvals but in both KNNL and ACIWRM there is a clear separation of procurement functions. Procurement transactions and payments are authorized by managing director of KNNL while recording procurement transactions and events and custody of assets is the responsibility of designated officers in PMU and PIO. External independent audit (not specifically of procurement, but subsumed in financial audit) is periodically carried out. Statutory audits by CAG are done. Written auditable trail of the procurement decisions are available. 65. Perceived weakness in accountability measures is that there is no standard statement of ethics requirement for those involved in procurement. The rate of conviction in corruption cases is low. However those involved with procurement are required to declare any potential conflict of interest and remove themselves from the procurement process. Commencement of procurement and its approval are not dependent on external approvals.

B. Strengths

66. The strengths of KNNL and ACIWRM related to procurement are summarized as follows:

i. All procurement actions, decisions and approvals are taken within KNNL and ACIWRM.

ii. KNNL and ACIWRM being a company and a Society respectively are largely insulated from cumbersome and unclear procurement practices of the state.

iii. The PMU and PIO comprise of some staff who have experience of procurement and contract management in ADB financed Project 1 of KISWRMIP. In addition KNNL is an implementing agency under the ongoing World Bank financed Dam Rehabilitation and Improvement Project. They would be able to leverage the experience for Project 2 and Project 3 of KISWRMIP and other future projects.

iv. WUCS component which has numerous small community contracts has been well managed by KNNL by resorting to co-signing contract agreement with CADA, involving CADA in monitoring and processing payments to WUCS.

v. E-procurement by using GOK portal, KNNL or ACIWRM websites and open and widespread advertising is used well for all bid invitation.

vi. Karnataka has an excellent KTPPA which is followed by KNNL or ACIWRM, thereby strengthening the complaints redress and accountability measures.

vii. KNNL has long and strong experience of procuring and implementing irrigation sector projects, many of them large ones. ACIWRM has a good mix of government staff on deputation and consultants which works well for the kind of work they do.

C. Weaknesses

67. The weaknesses of KNNL and ACIWRM related to procurement are summarized as follows:

i. There are no procurement specialists in PMU, PIO and ACIWRM. Mostly Engineering staff with consultant support manage procurement functions which is less efficient than having full time procurement staff. PMU & PIO staff get transferred leading to loss of program institutional memory. PSC too has resorted to multiple replacements of experts. All staff in PMU (except one part time consultant) and PIO

24

comprise people seconded from government, most of them not well versed with ADBs procurement processes.

ii. No clear separation of engineering, procurement and regulatory functions exist in PMU, PIO and ACIWRM.

iii. Procurement and contract administration section of KNNL and ACIWRM needs strengthening and requires tailor made ADB procurement process training. Decisions on contract variations and processing invoices get delayed.

iv. There is no retention of institutional procurement memory, information on procurement is scattered amongst various people and in paper files in PMU. Comprehensive procurement documentation and monitoring system for contracts does not exist in KNNL and ACIWRM.

v. Project 1 had inadequate competition in bidding by KNNL for works.

vi. There are 3 levels of approval for large contracts (TEC and TSC and KNNL Board), delays occur.

vii. Accounts sections of PMU, PIO, ACIWRM and Dharwad Chief Accounts Office of KNNL need more number of persons trained in ADB procurement and disbursement process to address Complex, time consuming process of payment to WUCS.

D. Procurement Risk Assessment and Management Plan (P-RAMP)

68. The project procurement risks, their assessed impact, likelihood of occurrence and recommended mitigation measures are summarized in P-RAMP:

PROJECT PROCUREMENT RISK ASSESSMENTAND MANAGEMENT PLAN

PCA Question-naire Ref. Risk Impact Likelihood Strategy

KNNL: C.2, C.15

Delayed procurement by KNNL due to multiple approval layers and irregular convening of approval committee meetings.

Low Likely

Mitigate:

- State to make arrangements that delegates decision making to the State IWRM Steering Committee instead of KNNL Board.

- The Program Director to become the focal person for the investment program while the Project Director role be assigned to a senior KNNL staff member on a full-time basis. All PMU staff be assigned to the PMU on a full-time basis.

Monitor:

Above arrangements are to be in place prior to Project 2 effectiveness.

25

PCA Question-naire Ref. Risk Impact Likelihood Strategy

KNNL: C.23

ACIWRM: A.3, A.9, A.17

Delayed procurement and poor contract administration leading to delays in project completion.

High Unlikely Mitigate:

- ADB to provide regular procurement and contract administration trainings to ACIWRM and KNNL.

- ACIWRM to recruit procurement specialist with ADB procurement experience.

Monitor:

- Monitoring of baseline projections for contract awards and disbursements.

KNNL: C.49

Poor performance of consultants and low standard of outputs.

High Unlikely Mitigate:

- Administer to PMU and ACIWRM training programs to provide specific guidance on consultant performance evaluation and discuss case studies on consultant performance evaluation.

- A dedicated person in PMU and ACIWRM to be devoted to evaluation and monitoring of consultants performance.

Monitor:

- PMU and ACIWRM to monitor consultant performance at regular intervals.

- PMU to ensure PSC experts are available when required by the project

26

III. PROJECT SPECIFIC PROCUREMENT THRESHOLDS

69. Procurement classification for the project investment is assessed as Moderate (Category B). The completed Project Procurement Classification checklist is provided in Annex 2. 70. The reason for Moderate (Category B) classification is that in Project 1, both KNNL and ACIWRM had long procurement lead times and experienced implementation delays. Substantial delay occurred in one works package procurement of Project 1 and in PSC recruitment. However, the experience of Project 1 would improve the situation for Project 2. 71. Based on the procurement capacity assessment carried out and the current thresholds for India, it is recommended that prior review limits and procurement thresholds for Project 2 of KISWRMIP be retained as follows. In Project 2, civil works procurement will be through open competitive bidding (OCB) per the ADB Procurement Regulations for ADB Borrowers (2017, as amended from time to time). Civil works contracts above $40 million will use international advertisement and those costing less than $40 million will use national advertisement. Single-stage two-envelope bidding with post-qualification will be adopted for all civil works contracts under the project. ADB review of bid documents and evaluation shall be prior for all OCB contracts. Domestic preference is not applicable. 72. For the procurement of goods and related services, international advertisement will be used for contracts of at least $1.0 million and national advertisement for contracts of less than $1.0 million. For contracts valued at less than $100,000 ADB’s procedures on request for quotations will be followed. ADB review of procurement of goods through request for quotations will be on post facto basis. Works by government owned entities (for activities which cannot be done by competitive bidding) shall be done by Force Account method. Community works contracting (each contract not exceeding $30,000) would be awarded to community groups (WUCS) and local NGOs using the same contractual arrangement (KNNL+CADA+WUCS) as has been followed in Project 1. Procurement for the Project 2 will conform to ADB’s Procurement Regulations for ADB Borrowers (2017, as amended from time to time).

27

IV. PROCUREMENT PLANS

73. An 18-month draft procurement plan showing threshold and review procedures, goods, works, and consulting service contract packages is shown in Annex 3. 74. All advance contracting and retroactive financing will be undertaken in conformity with ADB’s Procurement Regulations for ADB Borrowers (2017, as amended from time to time). 75. The issuance of invitations to bid under advance contracting and retroactive financing will be subject to ADB approval. The borrower and KNNL have been advised that approval of advance contracting and retroactive financing does not commit ADB to finance the project. 76. Advance contracting is required. PMU, ACIWRM and PIO expenses (remuneration, office equipment, vehicles and personnel) would also be part of advance contracting and retroactive financing. Process for recruitment of a construction quality assurance firm by KNNL, individual consultants by ACIWRM are underway. PSC package will be advertised. VNC-1 works package has been awarded in March 2019. The intention is to award the other packages (except construction quality assurance firm which would take more time) after completing all procurement steps concurrent with loan effectiveness. 77. Retroactive financing. A maximum amount of eligible expenditures up to the equivalent of 20% of the total ADB loan, incurred before loan effectiveness, could be made, but not more than 12 months before the signing of the loan agreement.

28

V. CONCLUSIONS

78. Based on the procurement capacity assessment of KNNL, ACIWRM and CADA, the following measures for improvement of procurement capacity are recommended:

i. PMU, PIO and ACIWRM need more tailor-made training on ADB's procurement process for which provision is to be made in Project 2 budget. ADB organized trainings in Project 1 have been general and infrequent. A tailor made training and capacity building program during project implementation would strengthen the program procurement system. More effort should be devoted to capacity building in contract management, disbursements and procurement.

ii. The e-procurement system of GOK is robust and is to be followed in Project 2 for procurement of civil works and goods through OCB.

iii. Karnataka has implemented ADB financed projects particularly in the urban and transport sectors. The understanding and appreciation of ADB’s procurement system is there in the higher levels of government and some specific departments / entities implementing such projects. It would be helpful if officers who have experience with externally aided projects are posted to PMU, PIO and ACIWRM which would improve procurement capacity.

iv. The annual working period in canals is limited to total 3 months during canal closures. Contract specifications should consider this aspect.

v. PMU and ACIWRM to simplify and expedite decision making layers and processes related to procurement, contract variations, project management and disbursement. PMU to report to IWRM Steering Committee instead of KNNL Board. KNNL to nominate a senior officer as full time Project Director for Project 2.