HCL TECHNOLOGIES An Introduction

HCL Corporate Presentation April 2011

May 20, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

HCL TECHNOLOGIES

An Introduction

2

HCL – Growth Momentum at a global level

Source: HCL Strategic Intelligence Wing, Bloomberg database as on 1st March 2011Source: HCL Strategic Intelligence Wing, Bloomberg database as on 1st March 2011

There are 3240 companies in the Bloomberg database belonging to the IT Sector (Hardware, Software, and Services). Of the 3240, 440 (14% of total) recorded 3-year Revenue CAGR greater than 25%. Of the 440, only 10 (0.3% of total) had revenues greater than $2500 Mn. Of the 10, only 5 (0.2% of total) had market cap greater than $5000 Mn.

UNDERSTANDING HCL

4

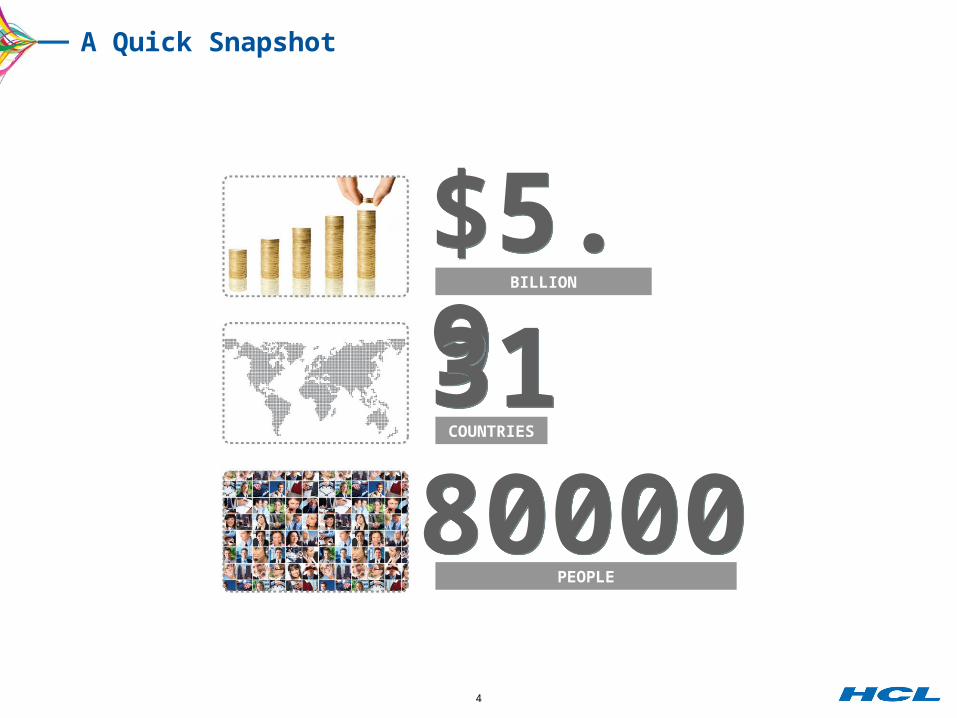

A Quick Snapshot

$5.9$5.9

31318000080000

BILLION

COUNTRIES

PEOPLE

5

Strong belief in three core values

6

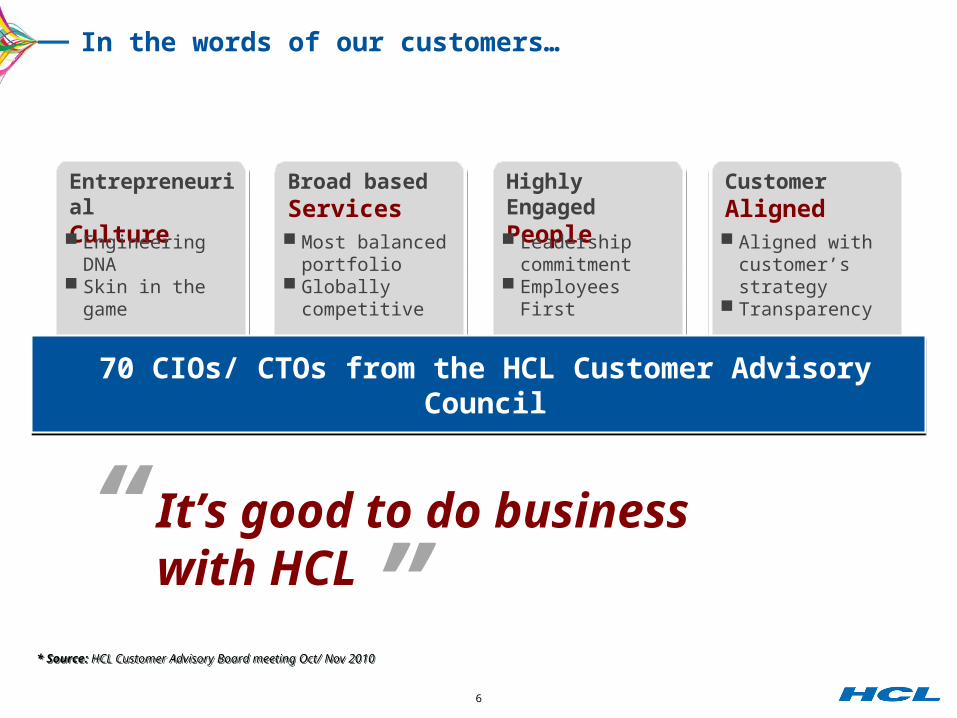

In the words of our customers…

Entrepreneurial CultureEntrepreneurial Culture

Broad basedServicesBroad basedServices

Highly Engaged PeopleHighly Engaged People

Customer AlignedCustomer Aligned

70 CIOs/ CTOs from the HCL Customer Advisory Council70 CIOs/ CTOs from the HCL Customer Advisory Council

* Source: HCL Customer Advisory Board meeting Oct/ Nov 2010* Source: HCL Customer Advisory Board meeting Oct/ Nov 2010

“ It’s good to do business with HCL ”

Engineering DNA Skin in the game

Most balanced portfolio

Globally competitive

Leadership commitment

Employees First

Aligned with customer’s strategy

Transparency

7

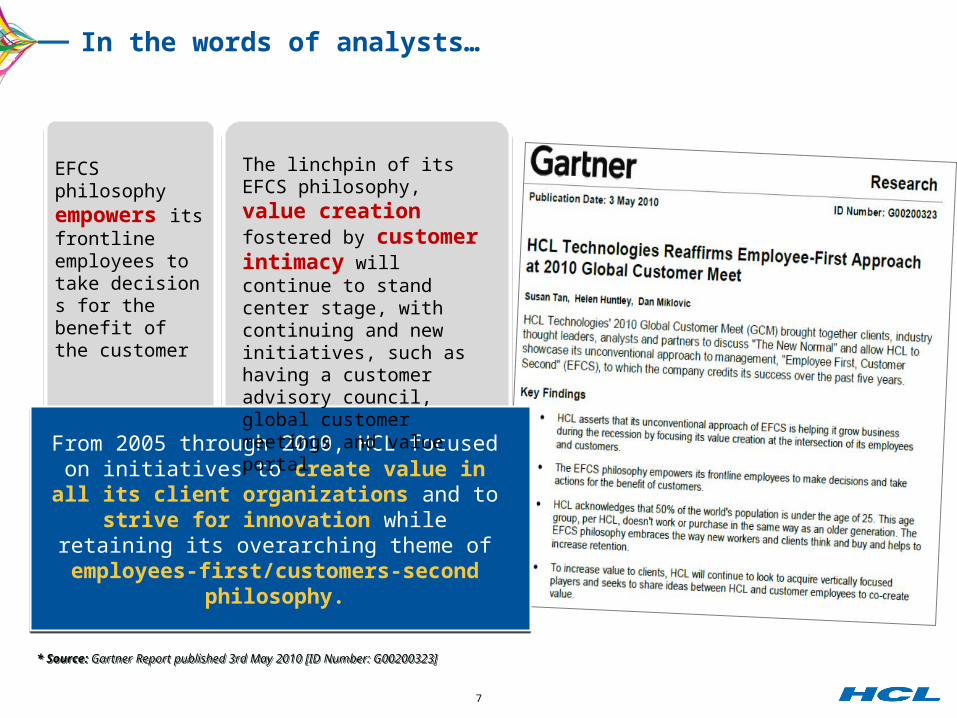

In the words of analysts…

* Source: Gartner Report published 3rd May 2010 [ID Number: G00200323]* Source: Gartner Report published 3rd May 2010 [ID Number: G00200323]

EFCS philosophy empowers its frontline employees to take decisions for the benefit of the customer

From 2005 through 2010, HCL focused on initiatives to create value in all its

client organizations and to strive for innovation while retaining its overarching

theme ofemployees-first/customers-second

philosophy.

The linchpin of its EFCS philosophy, value creation fostered by customer intimacy will continue to stand center stage, with continuing and new initiatives, such as having a customer advisory council, global customer meetings and value portal

8

In the words of thought leaders…

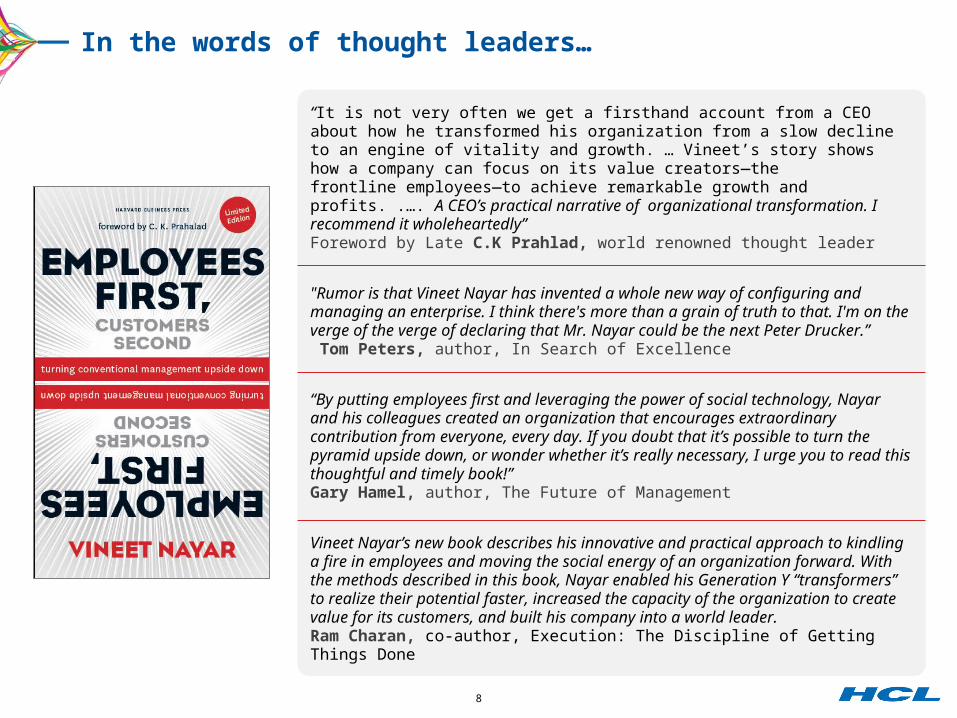

“It is not very often we get a firsthand account from a CEO about how he transformed his organization from a slow decline to an engine of vitality and growth. … Vineet’s story shows how a company can focus on its value creators—the frontline employees—to achieve remarkable growth and profits. .…. A CEO’s practical narrative of organizational transformation. I recommend it wholeheartedly”Foreword by Late C.K Prahlad, world renowned thought leader

"Rumor is that Vineet Nayar has invented a whole new way of configuring and managing an enterprise. I think there's more than a grain of truth to that. I'm on the verge of the verge of declaring that Mr. Nayar could be the next Peter Drucker.” Tom Peters, author, In Search of Excellence

“By putting employees first and leveraging the power of social technology, Nayar and his colleagues created an organization that encourages extraordinary contribution from everyone, every day. If you doubt that it’s possible to turn the pyramid upside down, or wonder whether it’s really necessary, I urge you to read this thoughtful and timely book!”Gary Hamel, author, The Future of Management

Vineet Nayar’s new book describes his innovative and practical approach to kindling a fire in employees and moving the social energy of an organization forward. With the methods described in this book, Nayar enabled his Generation Y “transformers” to realize their potential faster, increased the capacity of the organization to create value for its customers, and built his company into a world leader.Ram Charan, co-author, Execution: The Discipline of Getting Things Done

9

In the words of our investors…

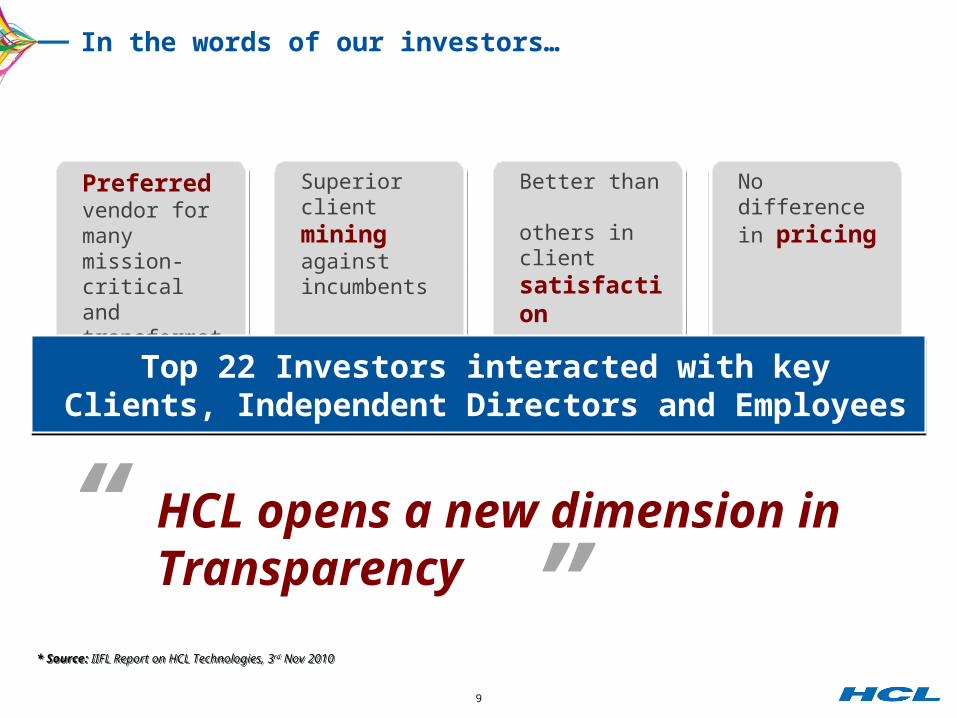

Preferred vendor for many mission-critical and transformation projects

Preferred vendor for many mission-critical and transformation projects

Superior client mining against incumbents

Superior client mining against incumbents

Better than others in client satisfaction

Better than others in client satisfaction

No difference in pricingNo difference in pricing

Top 22 Investors interacted with key Clients, Independent Directors and Employees

Top 22 Investors interacted with key Clients, Independent Directors and Employees

“ HCL opens a new dimension in Transparency”

* Source: IIFL Report on HCL Technologies, 3rd Nov 2010* Source: IIFL Report on HCL Technologies, 3rd Nov 2010

OUR BUSINESS

11

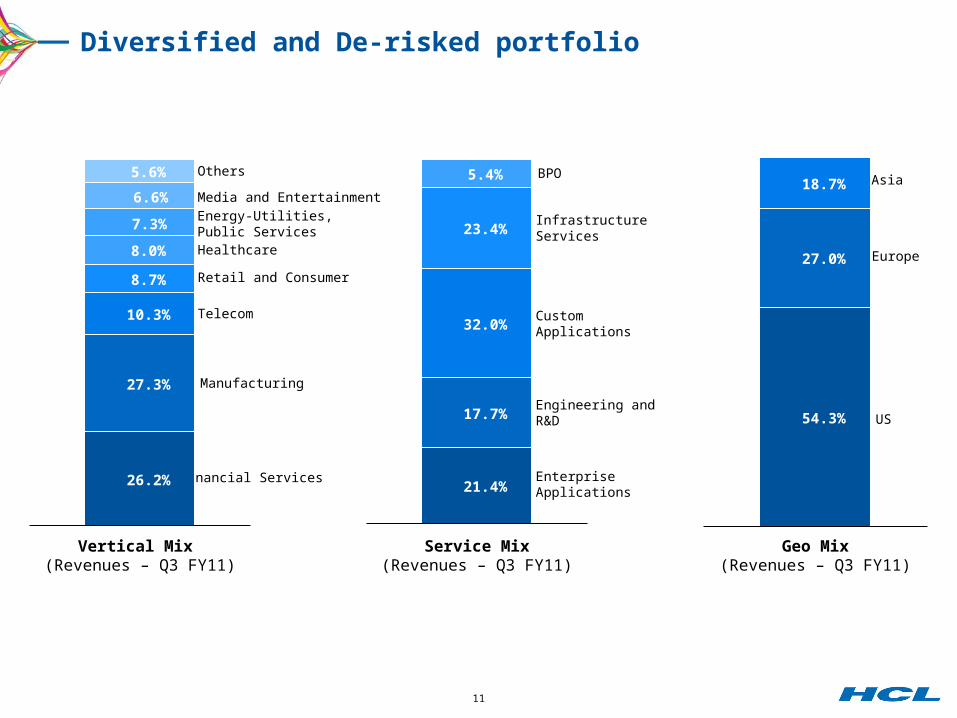

Diversified and De-risked portfolio

Asia

Europe

US

Manufacturing

Telecom

Retail and Consumer

Healthcare

Media and Entertainment

Energy-Utilities, Public Services

Financial Services Enterprise Applications

Engineering and R&D

Custom Applications

BPO

Infrastructure Services

Others

27.0%

18.7%

54.3%

27.3%

10.3%

8.0%

6.6%

7.3%

5.6%

26.2%

8.7%

17.7%

32.0%

5.4%

21.4%

23.4%

Vertical Mix (Revenues – Q3 FY11)

Service Mix(Revenues – Q3 FY11)

Geo Mix(Revenues – Q3 FY11)

12

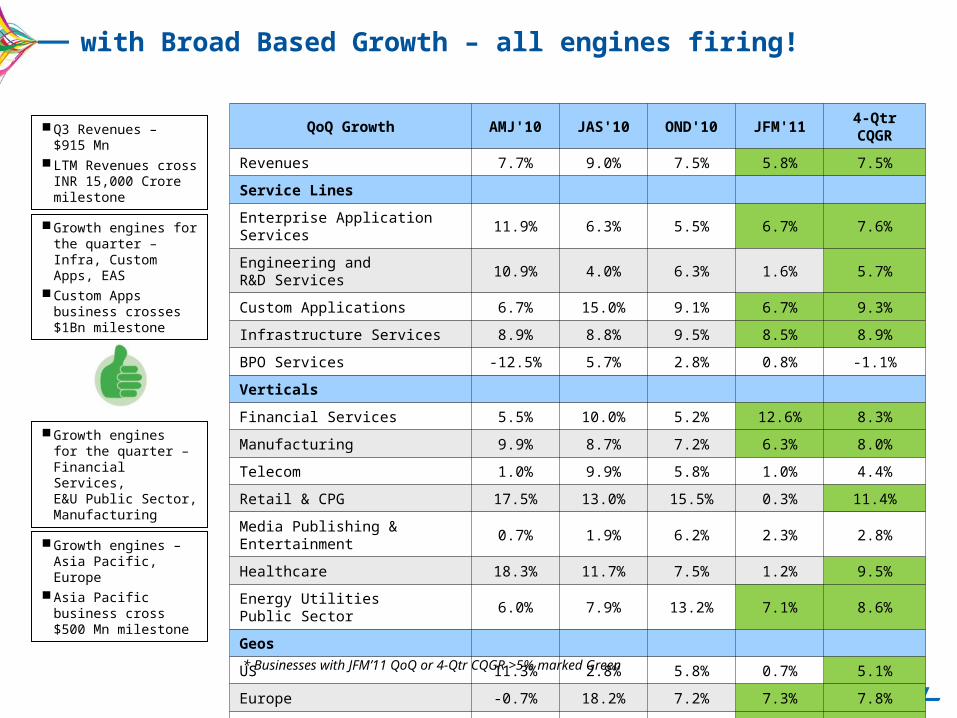

with Broad Based Growth – all engines firing!

QoQ Growth AMJ'10 JAS'10 OND'10 JFM'114-Qtr

CQGR

Revenues 7.7% 9.0% 7.5% 5.8% 7.5%

Service Lines

Enterprise Application Services 11.9% 6.3% 5.5% 6.7% 7.6%

Engineering and R&D Services 10.9% 4.0% 6.3% 1.6% 5.7%

Custom Applications 6.7% 15.0% 9.1% 6.7% 9.3%

Infrastructure Services 8.9% 8.8% 9.5% 8.5% 8.9%

BPO Services -12.5% 5.7% 2.8% 0.8% -1.1%

Verticals

Financial Services 5.5% 10.0% 5.2% 12.6% 8.3%

Manufacturing 9.9% 8.7% 7.2% 6.3% 8.0%

Telecom 1.0% 9.9% 5.8% 1.0% 4.4%

Retail & CPG 17.5% 13.0% 15.5% 0.3% 11.4%

Media Publishing & Entertainment 0.7% 1.9% 6.2% 2.3% 2.8%

Healthcare 18.3% 11.7% 7.5% 1.2% 9.5%

Energy Utilities Public Sector 6.0% 7.9% 13.2% 7.1% 8.6%

Geos

US 11.3% 2.8% 5.8% 0.7% 5.1%

Europe -0.7% 18.2% 7.2% 7.3% 7.8%

Asia Pacific 8.3% 19.8% 14.5% 21.7% 16.0%

Growth engines for the quarter – Infra, Custom Apps, EAS

Custom Apps business crosses $1Bn milestone

Growth engines for the quarter – Financial Services, E&U Public Sector, Manufacturing

Growth engines – Asia Pacific, Europe

Asia Pacific business cross $500 Mn milestone

* Businesses with JFM’11 QoQ or 4-Qtr CQGR >5% marked Green

Q3 Revenues – $915 Mn

LTM Revenues cross INR 15,000 Crore milestone

13

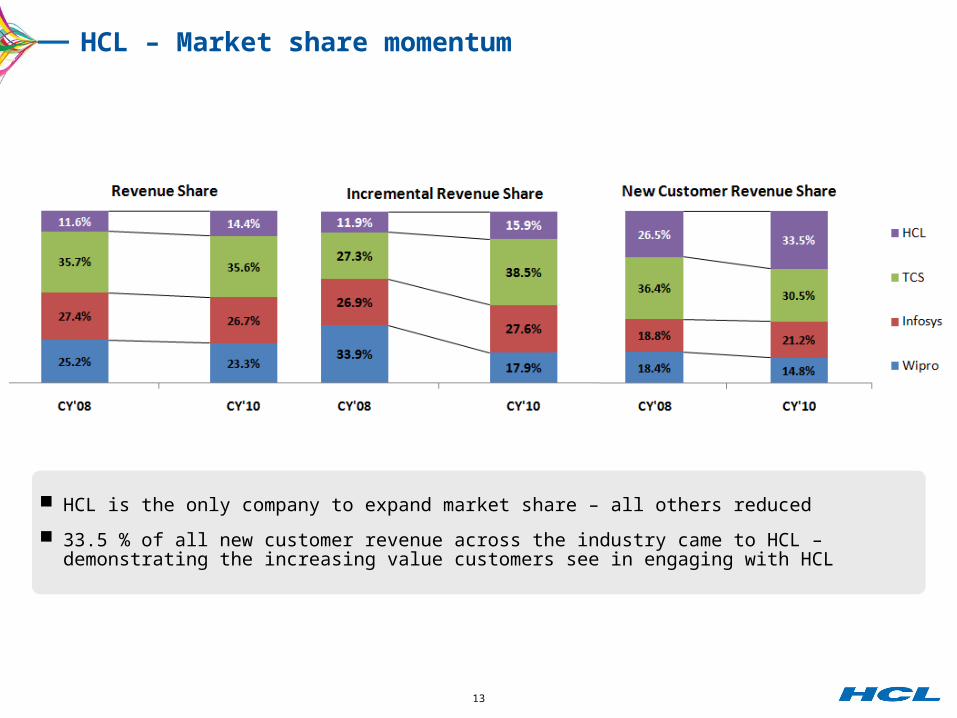

HCL – Market share momentum

HCL is the only company to expand market share – all others reduced

33.5 % of all new customer revenue across the industry came to HCL – demonstrating the increasing value customers see in engaging with HCL

14

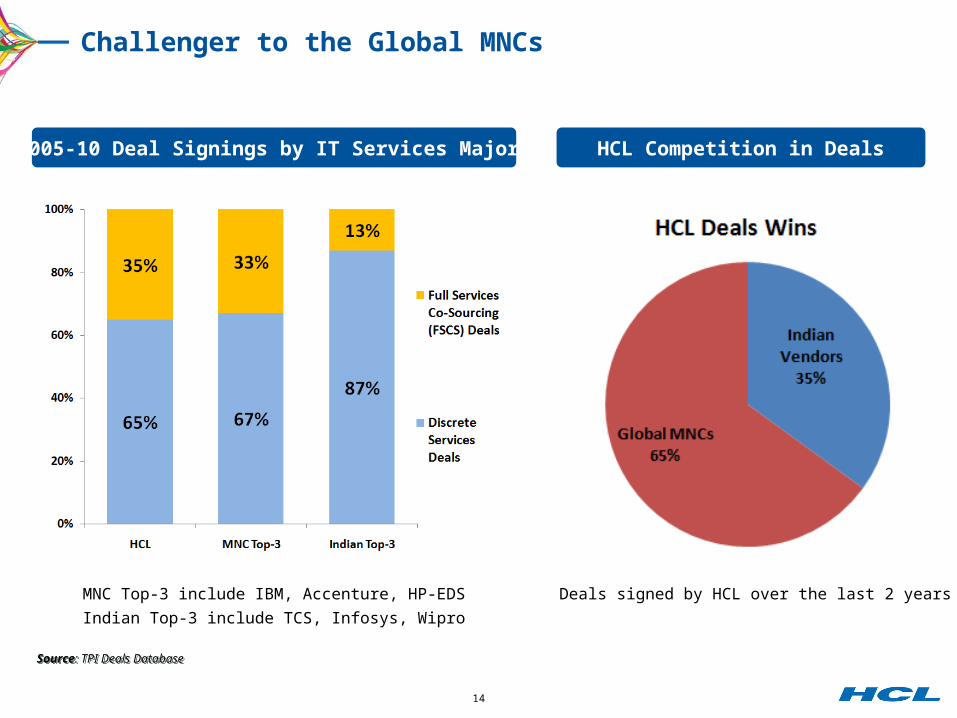

Challenger to the Global MNCs

Source: TPI Deals DatabaseSource: TPI Deals Database

MNC Top-3 include IBM, Accenture, HP-EDS

Indian Top-3 include TCS, Infosys, Wipro

Deals signed by HCL over the last 2 years

2005-10 Deal Signings by IT Services Majors HCL Competition in Deals

15

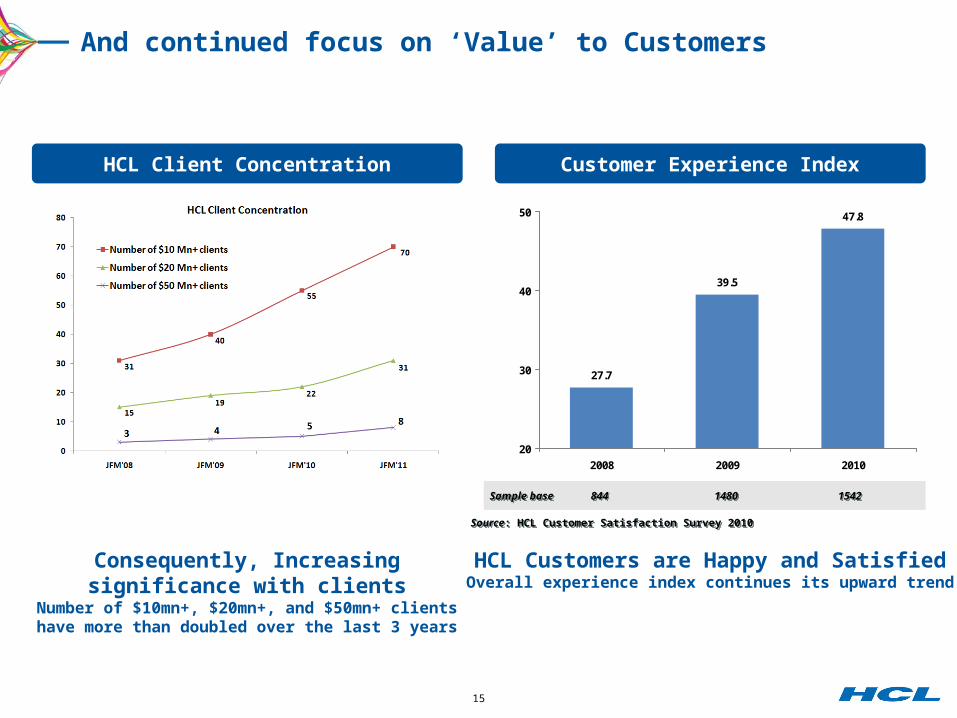

And continued focus on ‘Value’ to Customers

HCL Customers are Happy and SatisfiedOverall experience index continues its upward trend

27.7

39.5

47.8

20

30

40

50

2008 2009 2010

Sample baseSample base 844844 14801480 15421542

Source: HCL Customer Satisfaction Survey 2010Source: HCL Customer Satisfaction Survey 2010

HCL Client Concentration Customer Experience Index

Consequently, Increasing significance with clients

Number of $10mn+, $20mn+, and $50mn+ clients have more than doubled over the last 3 years

16

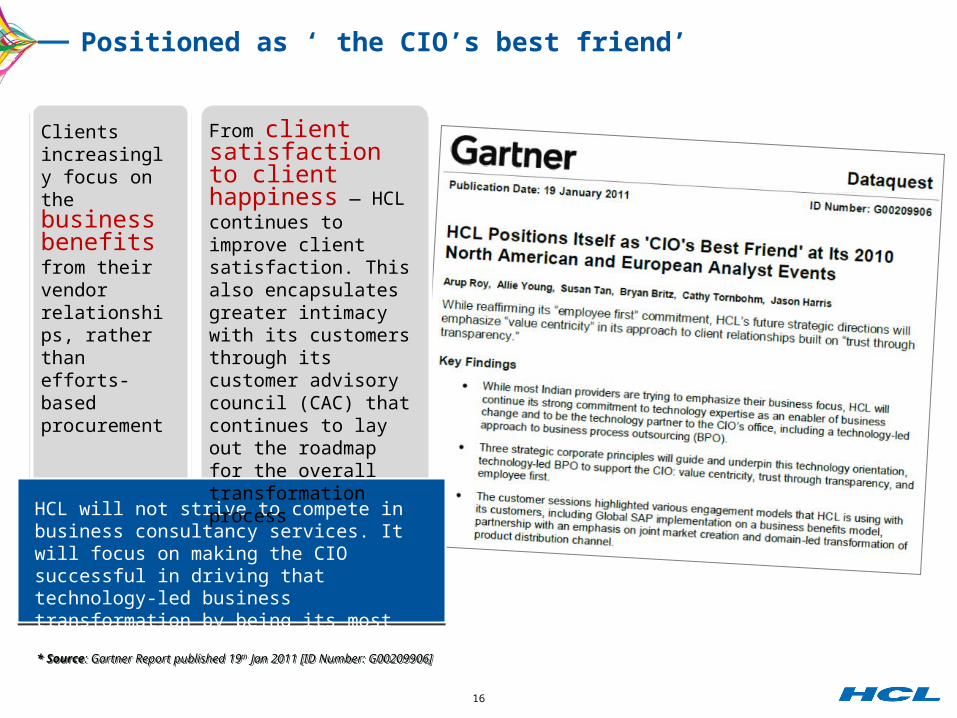

Positioned as ‘ the CIO’s best friend’

* Source: Gartner Report published 19th Jan 2011 [ID Number: G00209906]* Source: Gartner Report published 19th Jan 2011 [ID Number: G00209906]

Clients increasingly focus on the business benefits from their vendor relationships, rather than efforts-based procurement

HCL will not strive to compete in business consultancy services. It will focus on making the CIO successful in driving that technology-led business transformation by being its most trusted technology partner

From client satisfaction to client happiness — HCL continues to improve client satisfaction. This also encapsulates greater intimacy with its customers through its customer advisory council (CAC) that continues to lay out the roadmap for the overall transformation process

17

Virginia Guthrie,CIO and SVP, IT, Dr Pepper Snapple Group, since 2006

“It is important that I have a very strong business role in the organization. Outsourcing much of our IT development work to HCL affords me the time to focus on business issues.“

Chuck Ciali,CIO, Business Process and Information Technology, Teradyne

“My top concerns are cost, complexity and employee engagement. We selected HCL ISD on the basis of its breadth of experience with global customers in the hi-tech manufacturing industry, its partnership approach and the transparency in its engagement models.”

Jeff Carlson,Senior Vice President and CIO of AIG

“Like most organizations during the downturn, we had to figure out how to do more with less. HCL was instrumental in integrating the “black box” e-Signature component into the environment, making it a Web service to be accessed by other applications, and helping with production monitoring.”

Sujat Sukthankar,CTO, EndoPharma

“Flexible, scalable, cost-effective, and very agile R&D team is my focus. “We are relying on our R&D partners to create value for the organization, and they play a key role in driving our technology and R&D strategy. We believe that close collaboration with our R&D partners will drive results, and we have shown that successfully in a relatively short amount of time.”

Positioned as ‘ the CIO’s best friend’

THE ROAD AHEAD

19

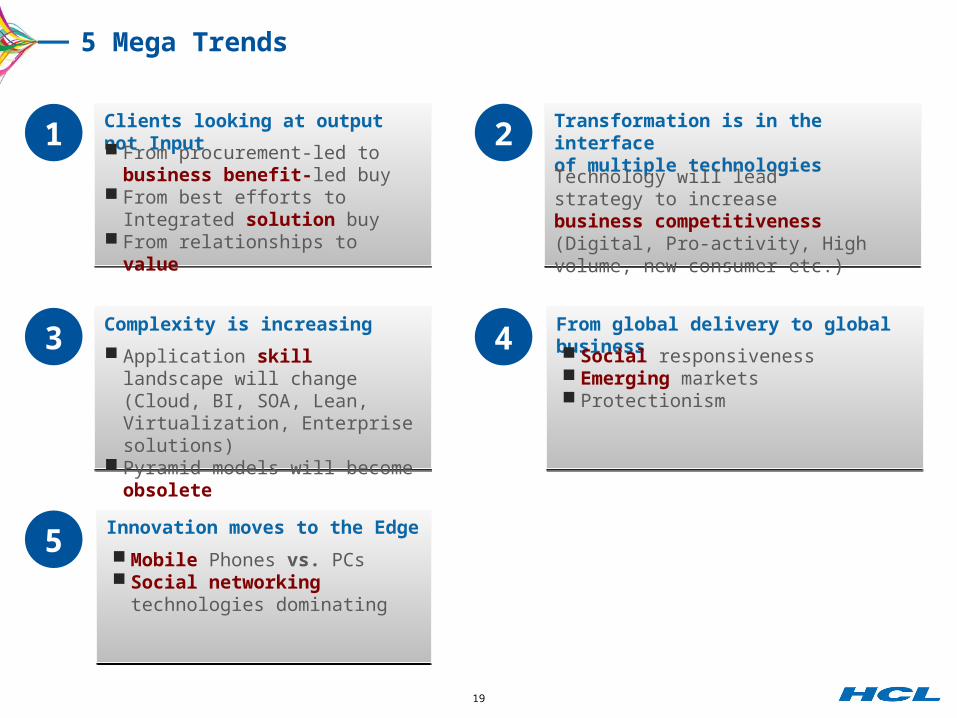

5 Mega Trends

1 Clients looking at output not InputClients looking at output not Input

From procurement-led to business benefit-led buy

From best efforts to Integrated solution buy

From relationships to value

2 Transformation is in the interface of multiple technologiesTransformation is in the interface of multiple technologies

Technology will lead strategy to increase business competitiveness (Digital, Pro-activity, High volume, new consumer etc.)

3 Complexity is increasingComplexity is increasing

Application skill landscape will change (Cloud, BI, SOA, Lean, Virtualization, Enterprise solutions)

Pyramid models will become obsolete

4 From global delivery to global businessFrom global delivery to global business

Social responsiveness Emerging markets Protectionism

5 Innovation moves to the EdgeInnovation moves to the Edge

Mobile Phones vs. PCs Social networking

technologies dominating

20

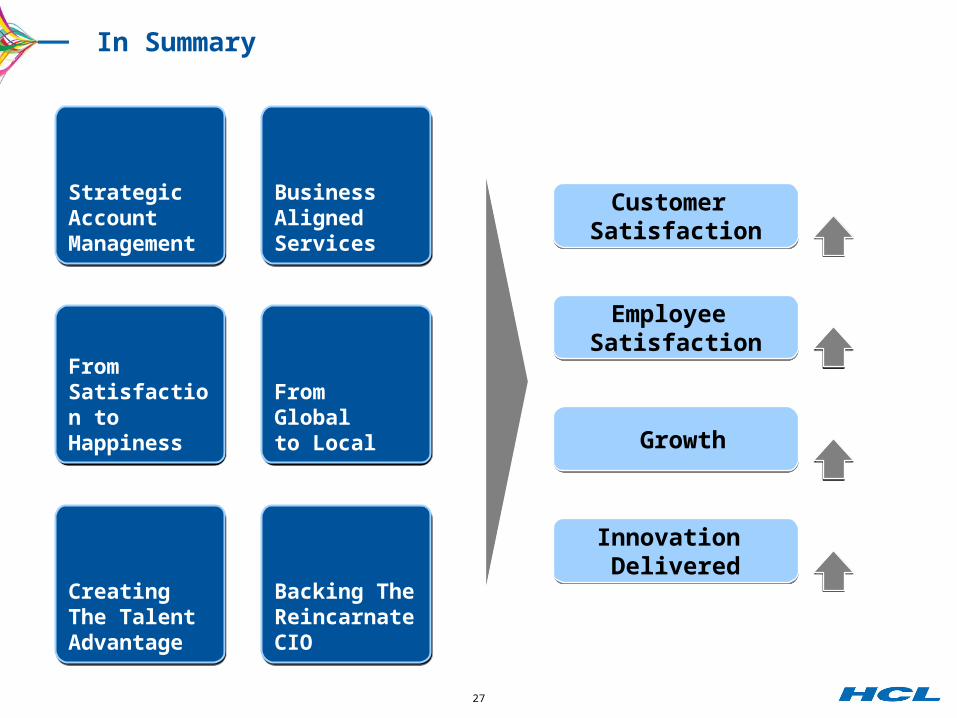

6 Areas of Departure

Strategic Account Management

Strategic Account Management

Business Aligned Services

Business Aligned Services

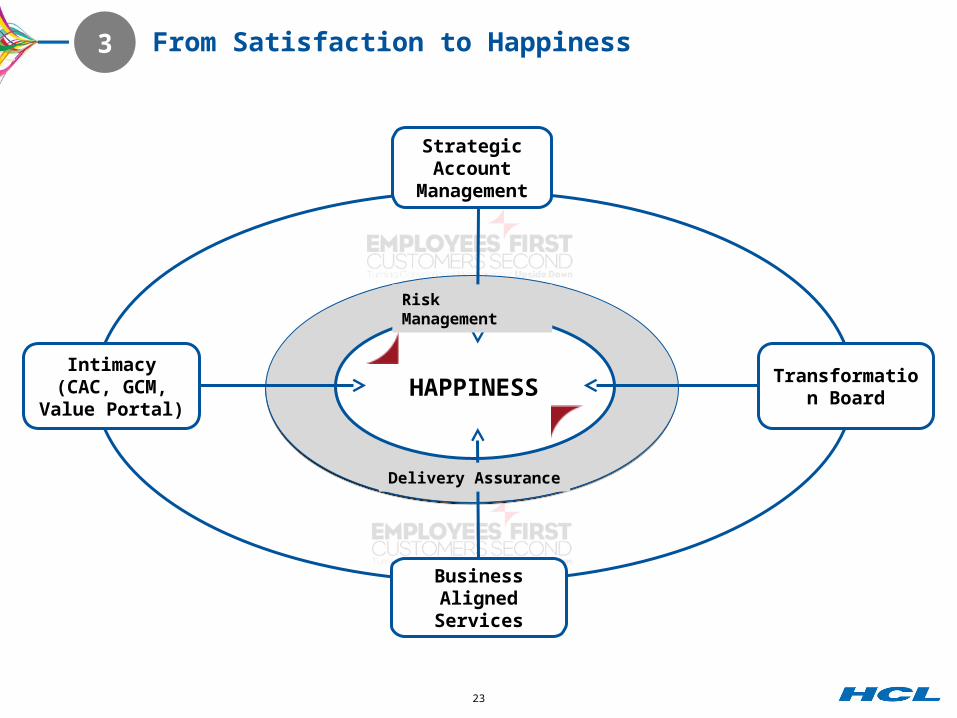

From Satisfaction to Happiness

From Satisfaction to Happiness

From Global to LocalFrom Global to Local

Creating The Talent Advantage

Creating The Talent Advantage

Backing The Reincarnate CIO

Backing The Reincarnate CIO

21

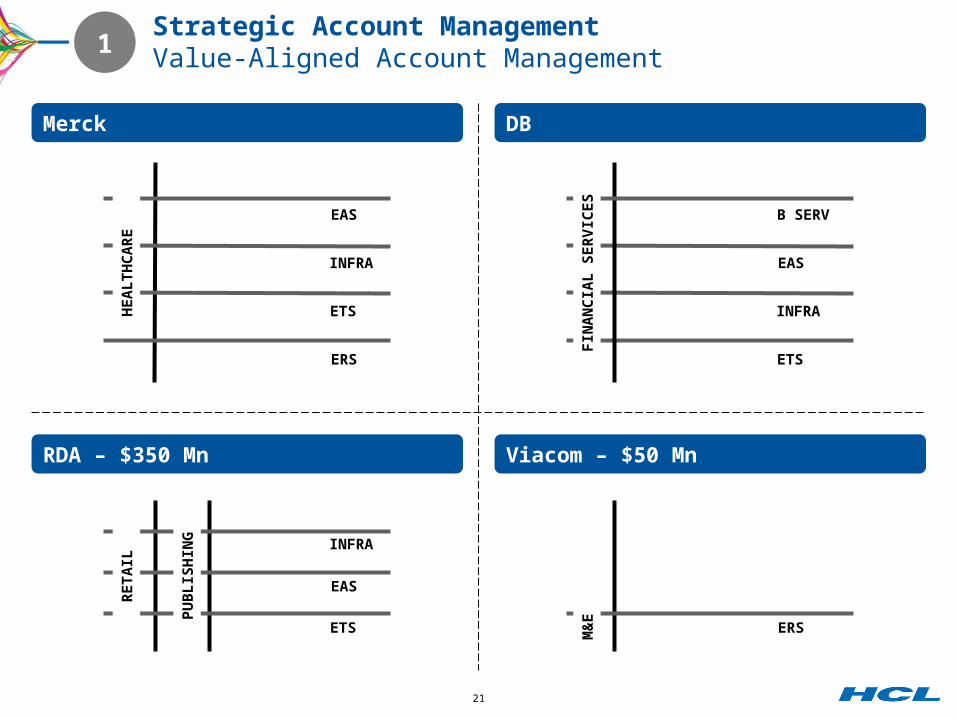

Strategic Account ManagementValue-Aligned Account Management 1

EAS

INFRA

ETS

Merck

ERS

Viacom – $50 Mn

EAS

INFRA

DB

EAS

ETS

RDA – $350 Mn

INFRA

HE

AL

TH

CA

RE

PU

BL

ISH

ING

RE

TA

IL

M&

E

ETS

B SERV

ERS

FIN

AN

CIA

L S

ER

VIC

ES

22

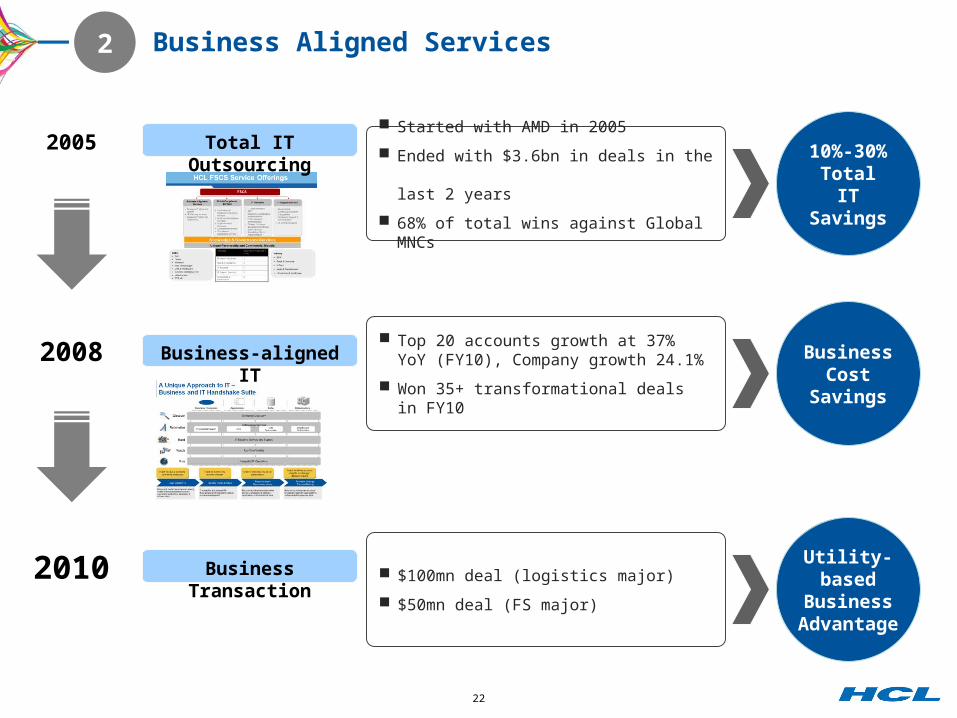

10%-30%Total IT Savings

Business Aligned Services

2005

2008

2010

Total IT Outsourcing

Business-aligned IT

Business Transaction

Started with AMD in 2005

Ended with $3.6bn in deals in the last 2 years

68% of total wins against Global MNCs

Top 20 accounts growth at 37% YoY (FY10), Company growth 24.1%

Won 35+ transformational deals in FY10

$100mn deal (logistics major)

$50mn deal (FS major)

Business Cost

Savings

Utility-based

Business Advantage

2

23

From Satisfaction to Happiness

Strategic Account

Management

Transformation Board

Business Aligned Services

Intimacy (CAC, GCM, Value Portal)

HAPPINESS

Delivery Assurance

Risk Management

3

24

CANADA

Sunnyvale

Irvine

Mexico City

Dallas

Utah

Los Angeles

Houston

Chicago

Columbia

StamfordChicago

CARY, NORTH CAROLINA

Toronto

FairfaxNew Jersey

SAO LEOPOLDO, BRAZIL

Sao PaoloSOUTH AFRICA

KRAKOW,POLAND

FINLANDSWEDEN

ITALY

SWITZERLANDFRANCE

NETHERLANDS

GERMANY

U.K.

London

Belfast

INDIA

JAPAN

SHANGHAI, CHINAHONGKONG

Perth

Melbourne

Sydney

Brisbane

Wellington

Auckland

SINGAPORE

MALAYSIA

Dubai

Israel

INDIA

PUERTO RICO

CZECH REPUBLICBelgium

SAUDI ARABIA

Beijing, China

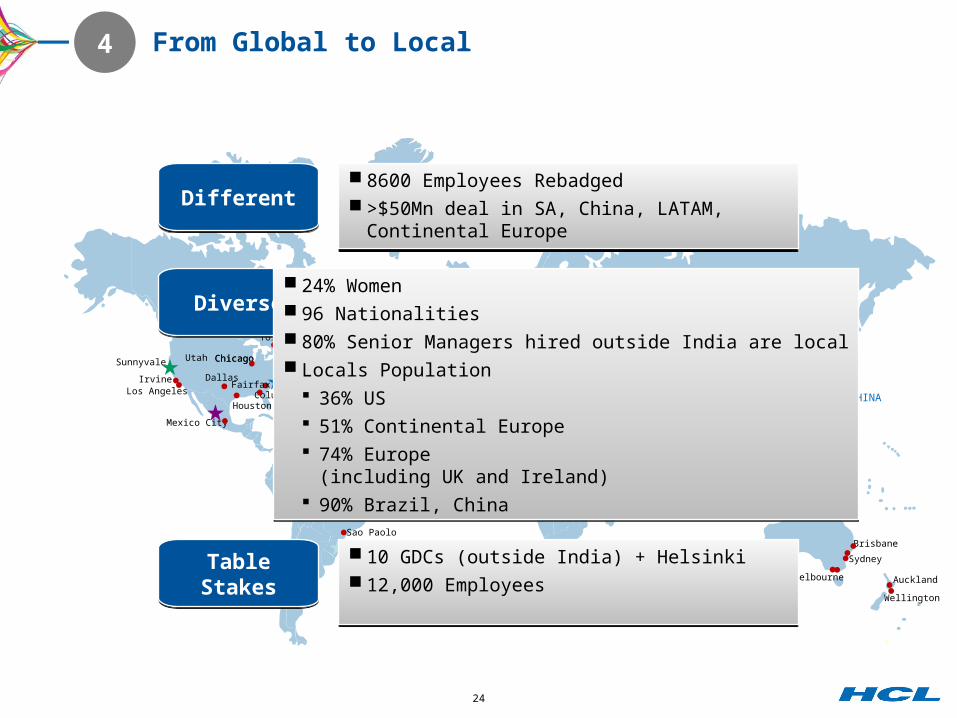

From Global to Local4

Table StakesTable

Stakes

DiverseDiverse

DifferentDifferent 8600 Employees Rebadged >$50Mn deal in SA, China, LATAM,

Continental Europe

8600 Employees Rebadged >$50Mn deal in SA, China, LATAM,

Continental Europe

24% Women 96 Nationalities 80% Senior Managers hired outside India are local Locals Population

36% US 51% Continental Europe 74% Europe

(including UK and Ireland) 90% Brazil, China

24% Women 96 Nationalities 80% Senior Managers hired outside India are local Locals Population

36% US 51% Continental Europe 74% Europe

(including UK and Ireland) 90% Brazil, China

10 GDCs (outside India) + Helsinki 12,000 Employees

10 GDCs (outside India) + Helsinki 12,000 Employees

25

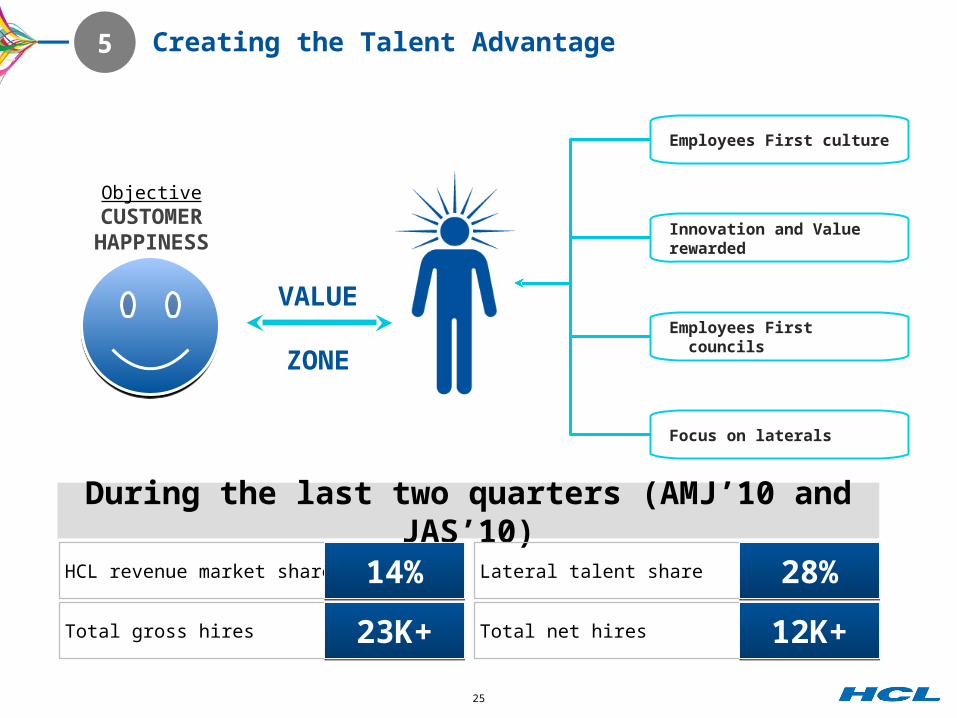

During the last two quarters (AMJ’10 and JAS’10)

Creating the Talent Advantage

HCL revenue market share Lateral talent share

Total gross hires Total net hires

14%14% 28%28%

23K+23K+ 12K+12K+

ObjectiveCUSTOMER HAPPINESS

VALUE

ZONE

Employees First culture

Innovation and Value rewarded

Employees First councils

Focus on laterals

5

26

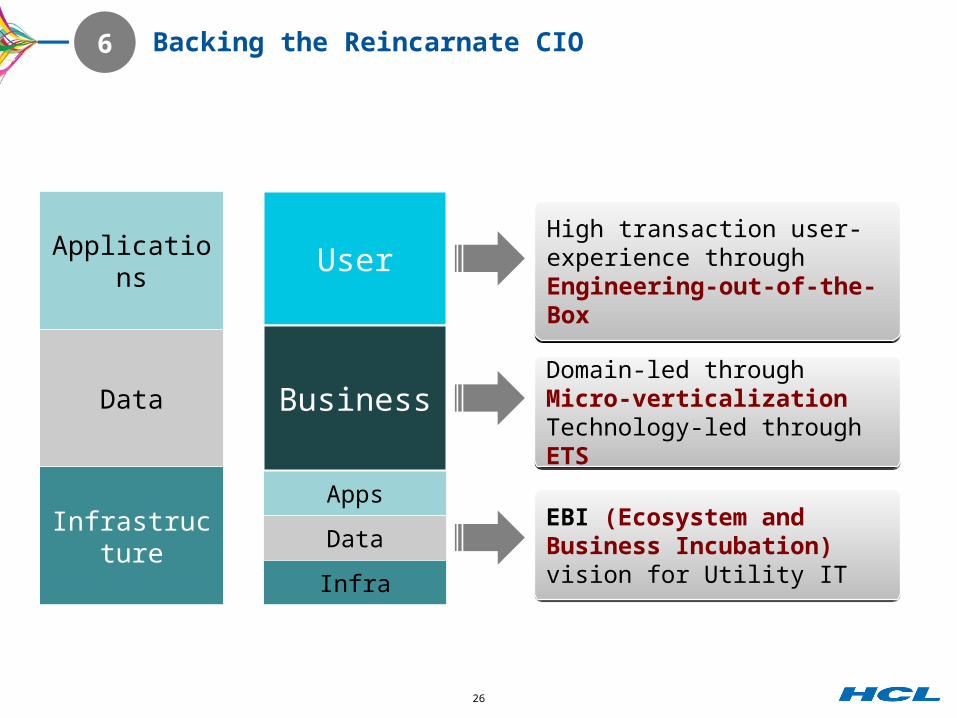

Backing the Reincarnate CIO

Applications

Data

Infrastructure

Apps

Data

Infra

User

Business

6

High transaction user-experience through Engineering-out-of-the-Box

High transaction user-experience through Engineering-out-of-the-Box

Domain-led through Micro-verticalization Technology-led through ETS

Domain-led through Micro-verticalization Technology-led through ETS

EBI (Ecosystem and Business Incubation) vision for Utility ITEBI (Ecosystem and Business Incubation) vision for Utility IT

27

In Summary

Customer SatisfactionCustomer

Satisfaction

Employee SatisfactionEmployee

Satisfaction

Growth Growth

Innovation Delivered

Innovation Delivered

Business Aligned Services

Business Aligned Services

Strategic Account Management

Strategic Account Management

From Global to Local

From Global to Local

From Satisfaction to Happiness

From Satisfaction to Happiness

Backing The Reincarnate CIO

Backing The Reincarnate CIO

Creating The Talent Advantage

Creating The Talent Advantage

28

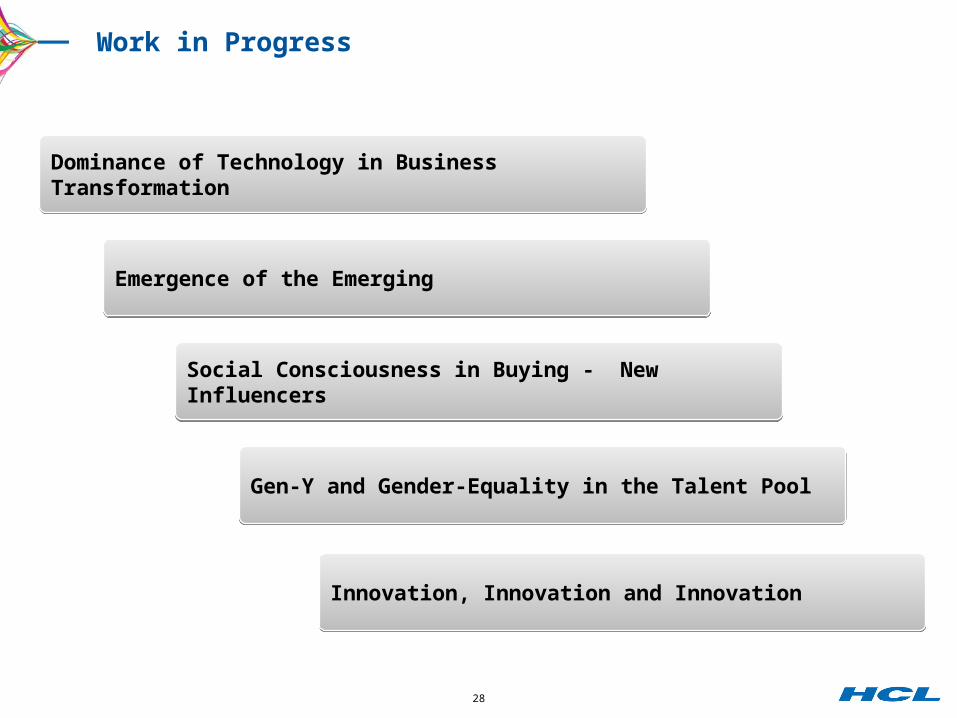

Work in Progress

Innovation, Innovation and InnovationInnovation, Innovation and Innovation

Gen-Y and Gender-Equality in the Talent PoolGen-Y and Gender-Equality in the Talent Pool

Social Consciousness in Buying - New InfluencersSocial Consciousness in Buying - New Influencers

Emergence of the EmergingEmergence of the Emerging

Dominance of Technology in Business TransformationDominance of Technology in Business Transformation

29

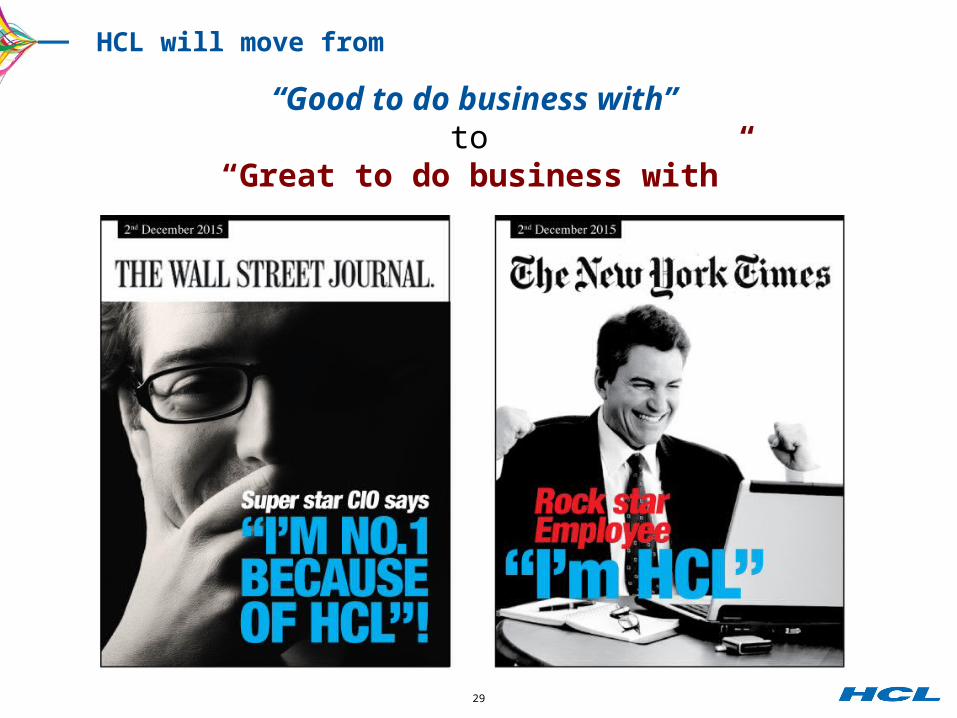

“Good to do business with” to

“Great to do business with”

HCL will move from

OUR VALUE PROPOSITIONS

IT INFRASTRUCTURE MANAGEMENT

32

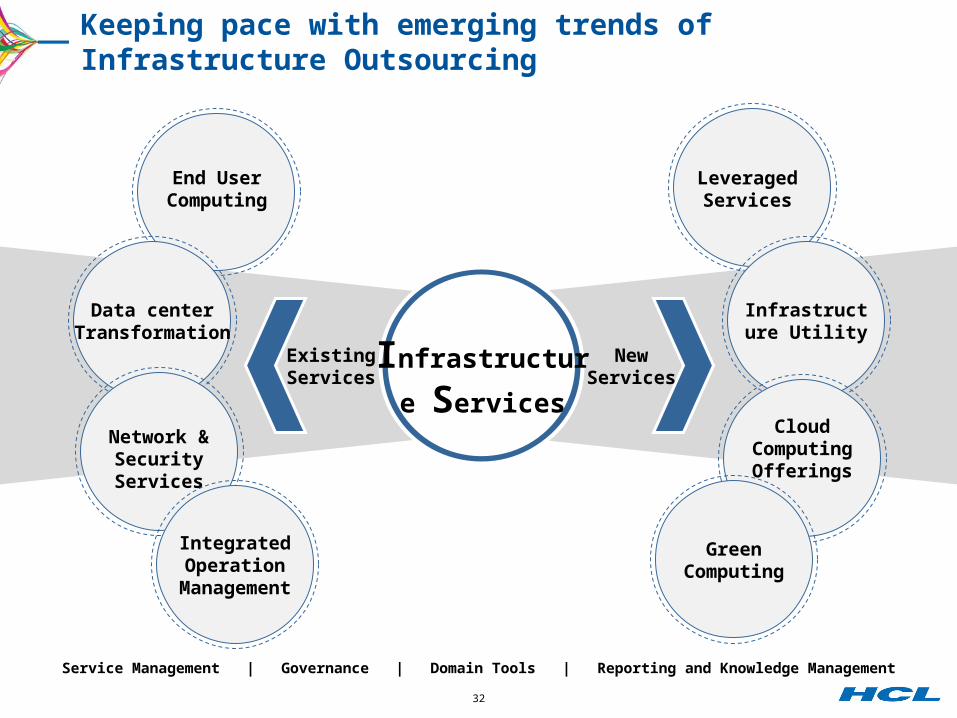

Service Management | Governance | Domain Tools | Reporting and Knowledge Management

Keeping pace with emerging trends of Infrastructure Outsourcing

Infrastructure

Services

End User Computing

Data center Transformation

Network & Security Services

Leveraged Services

Infrastructure Utility

Cloud Computing Offerings

Green Computing

Existing Services

NewServices

Integrated Operation

Management

33

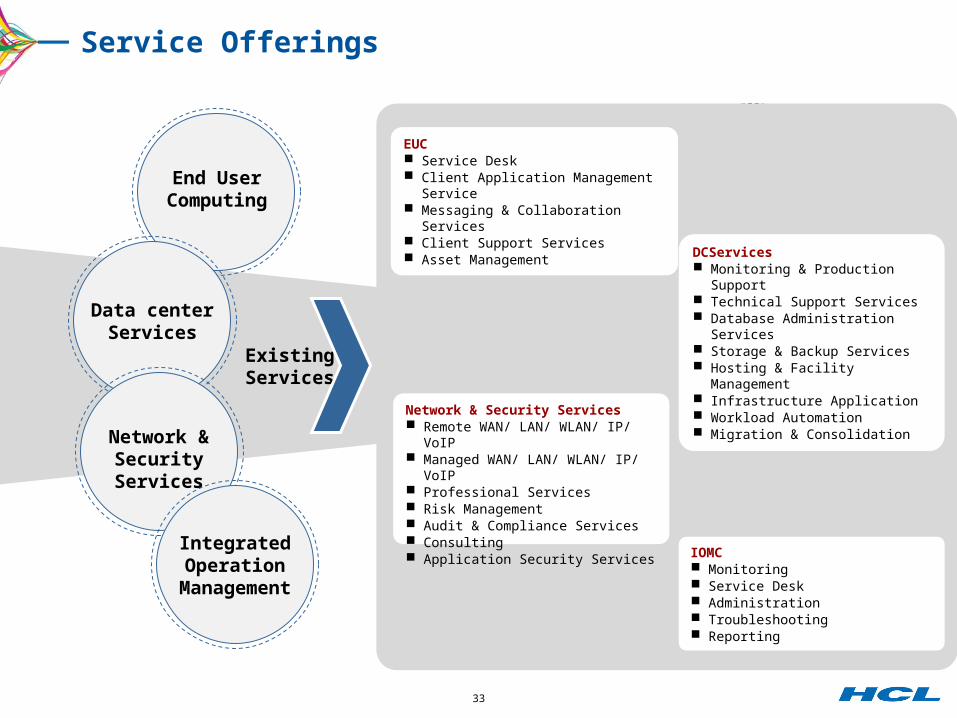

Service Offerings

Infrastructure

Services

End User Computing

Data center Services

Network & Security Services

Integrated Operation

Management

Leveraged Services

Infrastructure Utility

Cloud Computing Offerings

Green Computing

Existing Services

NewServices

EUC Service Desk Client Application Management Service Messaging & Collaboration Services Client Support Services Asset Management

Network & Security Services Remote WAN/ LAN/ WLAN/ IP/ VoIP Managed WAN/ LAN/ WLAN/ IP/ VoIP Professional Services Risk Management Audit & Compliance Services Consulting Application Security Services

IOMC Monitoring Service Desk Administration Troubleshooting Reporting

DCServices Monitoring & Production Support Technical Support Services Database Administration Services Storage & Backup Services Hosting & Facility Management Infrastructure Application Workload Automation Migration & Consolidation

34

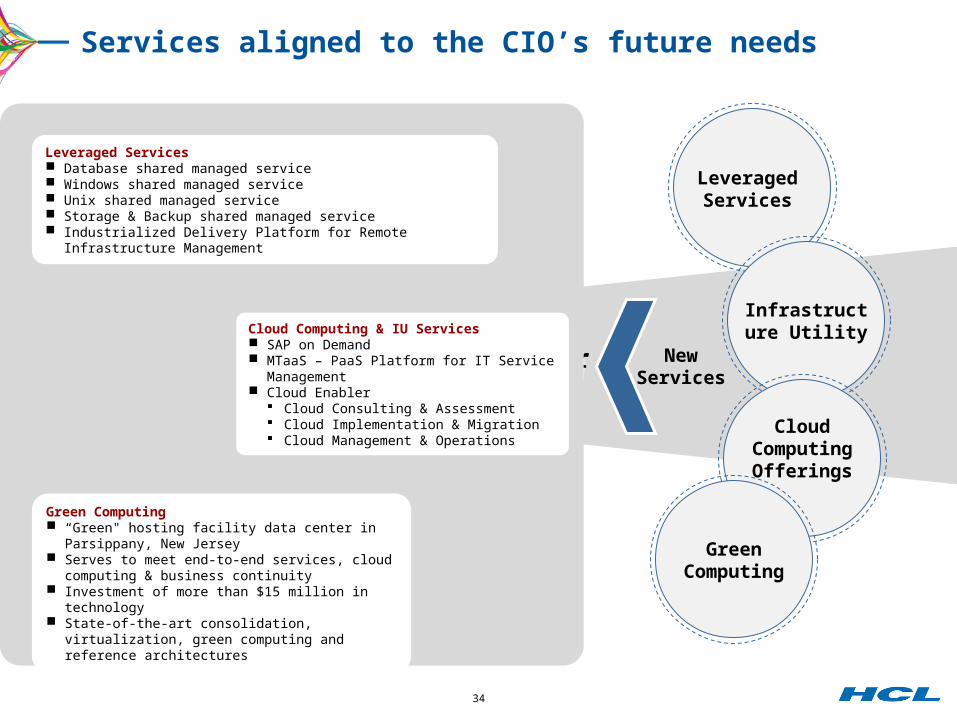

Services aligned to the CIO’s future needs

Infrastructure

Services

End User Computing

Data center Transformation

Network & Security Services

Integrated Operation

Management

Leveraged Services

Infrastructure Utility

Cloud Computing Offerings

Green Computing

NewServices

Existing Services

Leveraged Services Database shared managed service Windows shared managed service Unix shared managed service Storage & Backup shared managed service Industrialized Delivery Platform for Remote Infrastructure Management

Cloud Computing & IU Services SAP on Demand MTaaS – PaaS Platform for IT Service

Management Cloud Enabler

Cloud Consulting & Assessment Cloud Implementation & Migration Cloud Management & Operations

Green Computing “Green" hosting facility data center in Parsippany,

New Jersey Serves to meet end-to-end services, cloud computing &

business continuity Investment of more than $15 million in technology State-of-the-art consolidation, virtualization, green

computing and reference architectures

35

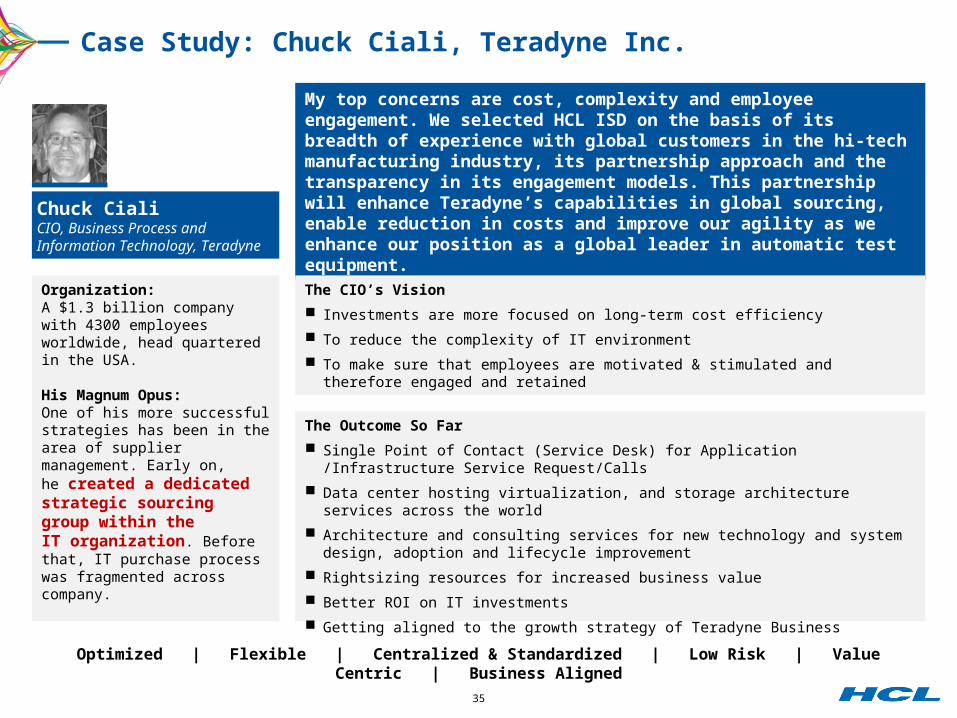

Case Study: Chuck Ciali, Teradyne Inc.

Organization:A $1.3 billion company with 4300 employees worldwide, head quartered in the USA.

His Magnum Opus:One of his more successful strategies has been in the area of supplier management. Early on, he created a dedicated strategic sourcing group within the IT organization. Before that, IT purchase process was fragmented across company.

My top concerns are cost, complexity and employee engagement. We selected HCL ISD on the basis of its breadth of experience with global customers in the hi-tech manufacturing industry, its partnership approach and the transparency in its engagement models. This partnership will enhance Teradyne’s capabilities in global sourcing, enable reduction in costs and improve our agility as we enhance our position as a global leader in automatic test equipment.

Chuck CialiCIO, Business Process and Information Technology, Teradyne

Optimized | Flexible | Centralized & Standardized | Low Risk | Value Centric | Business Aligned

The CIO’s Vision

Investments are more focused on long-term cost efficiency

To reduce the complexity of IT environment

To make sure that employees are motivated & stimulated and therefore engaged and retained

The Outcome So Far

Single Point of Contact (Service Desk) for Application /Infrastructure Service Request/Calls

Data center hosting virtualization, and storage architecture services across the world

Architecture and consulting services for new technology and system design, adoption and lifecycle improvement

Rightsizing resources for increased business value

Better ROI on IT investments

Getting aligned to the growth strategy of Teradyne Business

FINANCIAL SERVICES

37

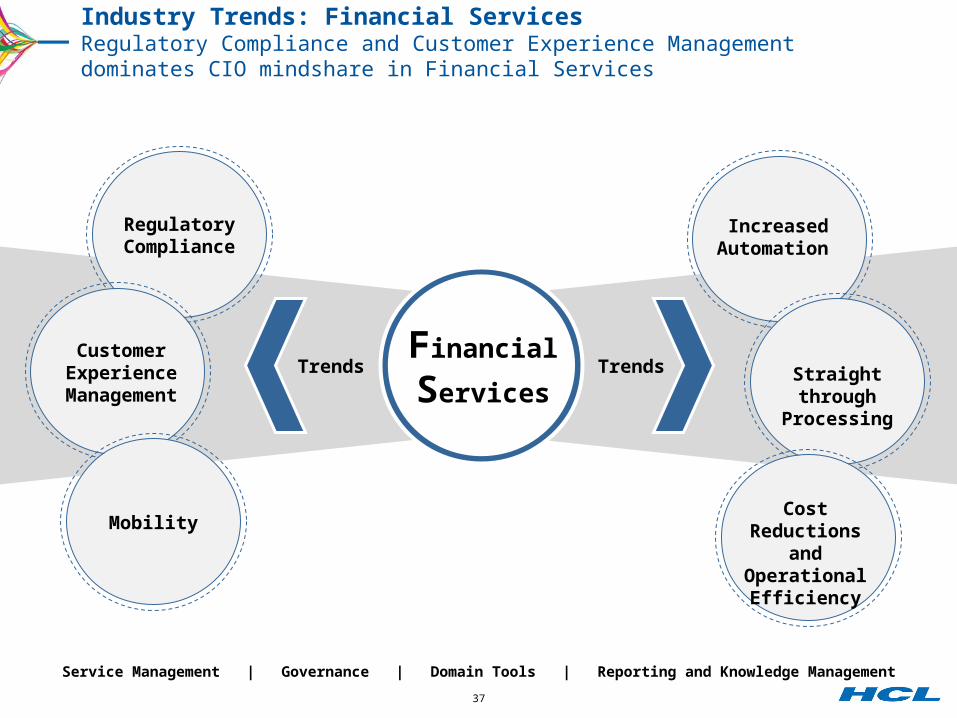

Industry Trends: Financial ServicesRegulatory Compliance and Customer Experience Management dominates CIO mindshare in Financial Services

Trends TrendsFinancial

Services

Regulatory Compliance

Customer Experience

Management

Mobility

Increased Automation

Straight through Processing

Cost Reductions and

Operational Efficiency

Service Management | Governance | Domain Tools | Reporting and Knowledge Management

38

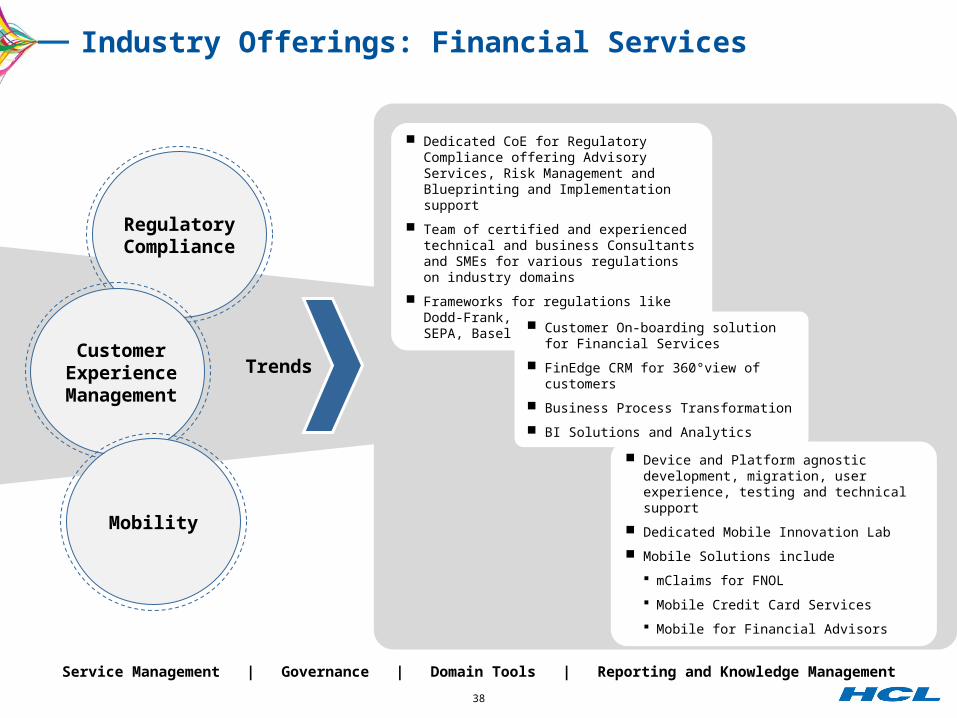

Industry Offerings: Financial Services

Service Management | Governance | Domain Tools | Reporting and Knowledge Management

Trends TrendsFinancial

Services

Regulatory Compliance

Customer Experience

Management

Mobility

Increased Automation

Straight through Processing

Cost Reductions and

Operational Efficiency

Dedicated CoE for Regulatory Compliance offering Advisory Services, Risk Management and Blueprinting and Implementation support

Team of certified and experienced technical and business Consultants and SMEs for various regulations on industry domains

Frameworks for regulations like Dodd-Frank, MiFID, Solvency II, SEPA, Basel II, Sox, Reg NMS

Device and Platform agnostic development, migration, user experience, testing and technical support

Dedicated Mobile Innovation Lab

Mobile Solutions include

mClaims for FNOL

Mobile Credit Card Services

Mobile for Financial Advisors

Customer On-boarding solution for Financial Services

FinEdge CRM for 360°view of customers

Business Process Transformation

BI Solutions and Analytics

39

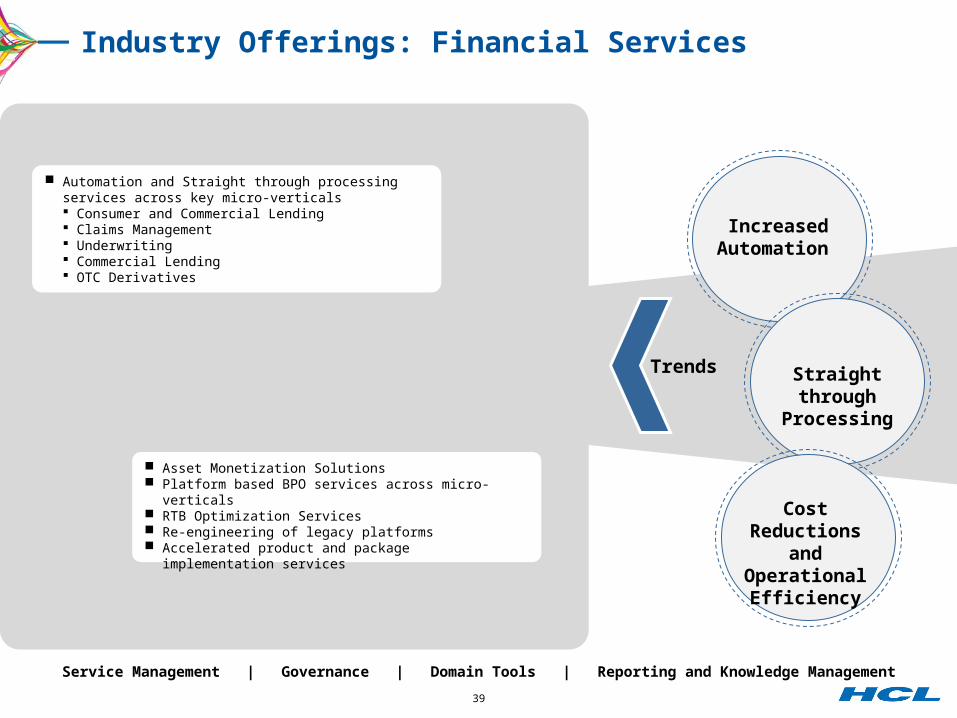

Industry Offerings: Financial Services

Service Management | Governance | Domain Tools | Reporting and Knowledge Management

Trends TrendsFinancial

Services

Regulatory Compliance

Customer Experience

Management

Mobility

Increased Automation

Straight through Processing

Cost Reductions and

Operational Efficiency

Automation and Straight through processing services across key micro-verticals Consumer and Commercial Lending Claims Management Underwriting Commercial Lending OTC Derivatives

Asset Monetization Solutions Platform based BPO services across micro-verticals RTB Optimization Services Re-engineering of legacy platforms Accelerated product and package implementation services

40

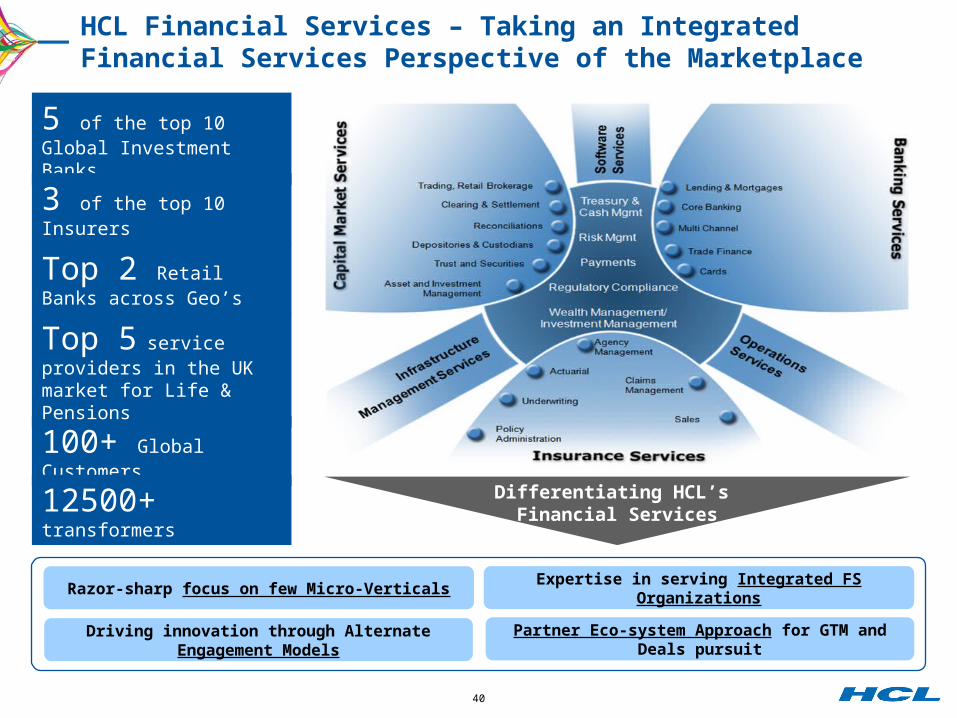

HCL Financial Services – Taking an Integrated Financial Services Perspective of the Marketplace

5 of the top 10 Global Investment Banks

100+ Global Customers

12500+ transformersDifferentiating HCL’s

Financial Services

Razor-sharp focus on few Micro-Verticals

Driving innovation through Alternate Engagement Models

Expertise in serving Integrated FS Organizations

Partner Eco-system Approach for GTM and Deals pursuit

3 of the top 10 Insurers

Top 5 service providers in the UK market for Life & Pensions

Top 2 Retail Banks across Geo’s

41

Optimized | Flexible | Centralized & Standardized | Low Risk | Value Centric | Business Aligned

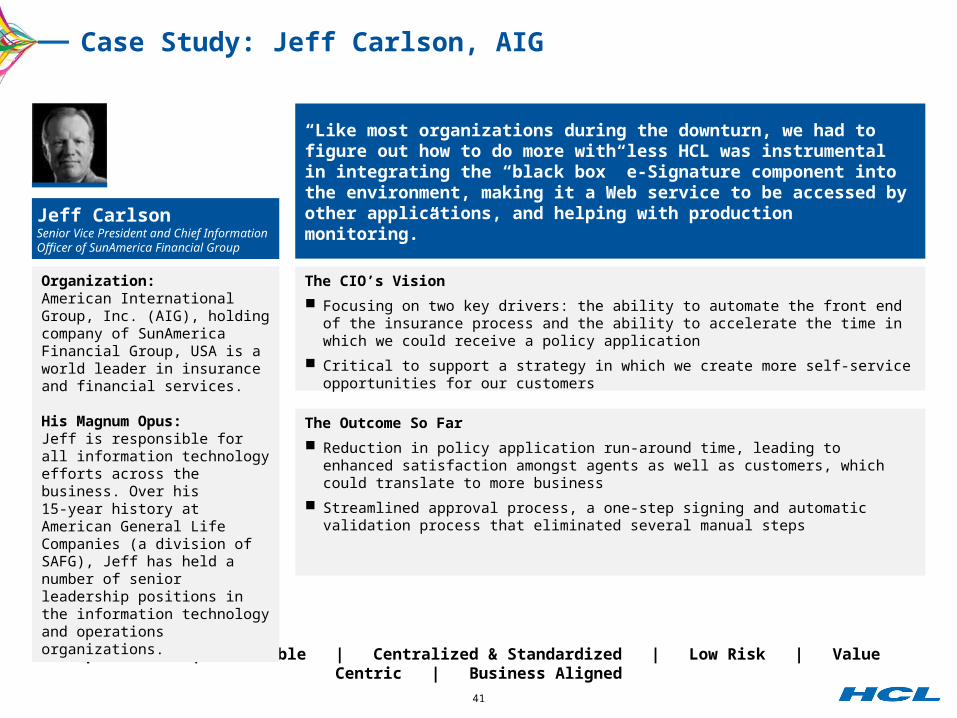

Case Study: Jeff Carlson, AIG

Organization:American International Group, Inc. (AIG), holding company of SunAmerica Financial Group, USA is a world leader in insurance and financial services.

His Magnum Opus:Jeff is responsible for all information technology efforts across the business. Over his 15-year history at American General Life Companies (a division of SAFG), Jeff has held a number of senior leadership positions in the information technology and operations organizations.

“Like most organizations during the downturn, we had to figure out how to do more with less HCL was instrumental in integrating the “black box” e-Signature component into the environment, making it a Web service to be accessed by other applications, and helping with production monitoring.”Jeff Carlson

Senior Vice President and Chief Information Officer of SunAmerica Financial Group

The CIO’s Vision

Focusing on two key drivers: the ability to automate the front end of the insurance process and the ability to accelerate the time in which we could receive a policy application

Critical to support a strategy in which we create more self-service opportunities for our customers

The Outcome So Far

Reduction in policy application run-around time, leading to enhanced satisfaction amongst agents as well as customers, which could translate to more business

Streamlined approval process, a one-step signing and automatic validation process that eliminated several manual steps

HEALTHCARE

43

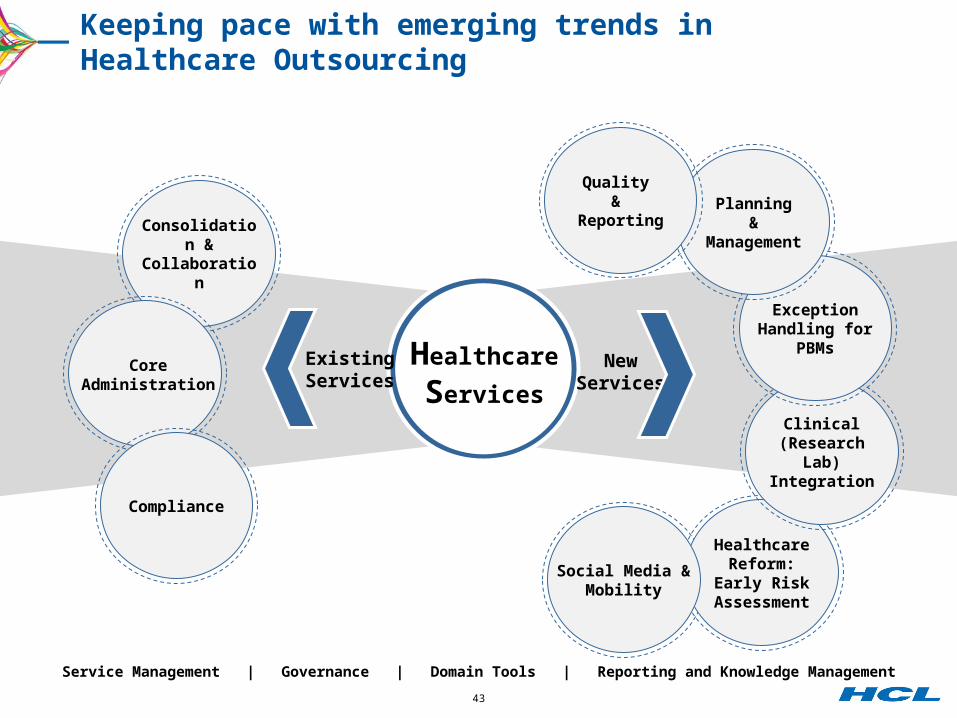

Keeping pace with emerging trends in Healthcare Outsourcing

Healthcare

Services

NewServices

Healthcare Reform:

Early Risk Assessment

Clinical (Research Lab)

Integration

Exception Handling for

PBMs

Planning&

Management

Social Media & Mobility

Quality &

Reporting

Consolidation & Collaboration

Core Administration

Compliance

Service Management | Governance | Domain Tools | Reporting and Knowledge Management

Existing Services

44

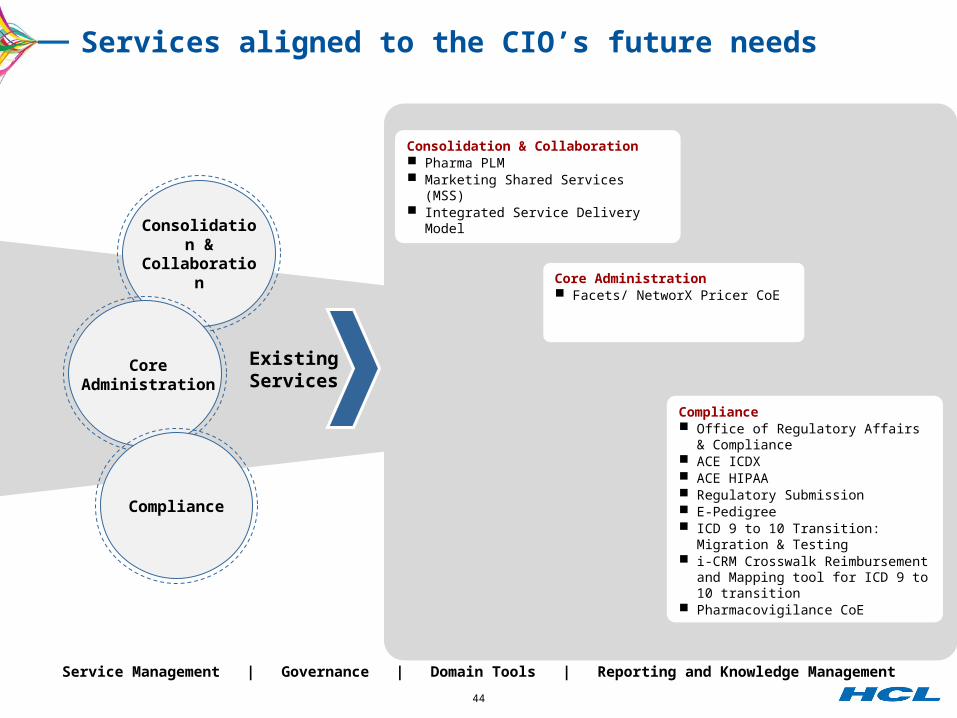

Services aligned to the CIO’s future needs

Healthcare

Services

Healthcare Reform:

Early Risk Assessment

Clinical (Research Lab)

Integration

Exception Handling for

PBMs

Planning&

Management

Social Media & Mobility

Quality &

Reporting

Service Management | Governance | Domain Tools | Reporting and Knowledge Management

Consolidation & Collaboration

Core Administration

Compliance

Existing Services

NewServices

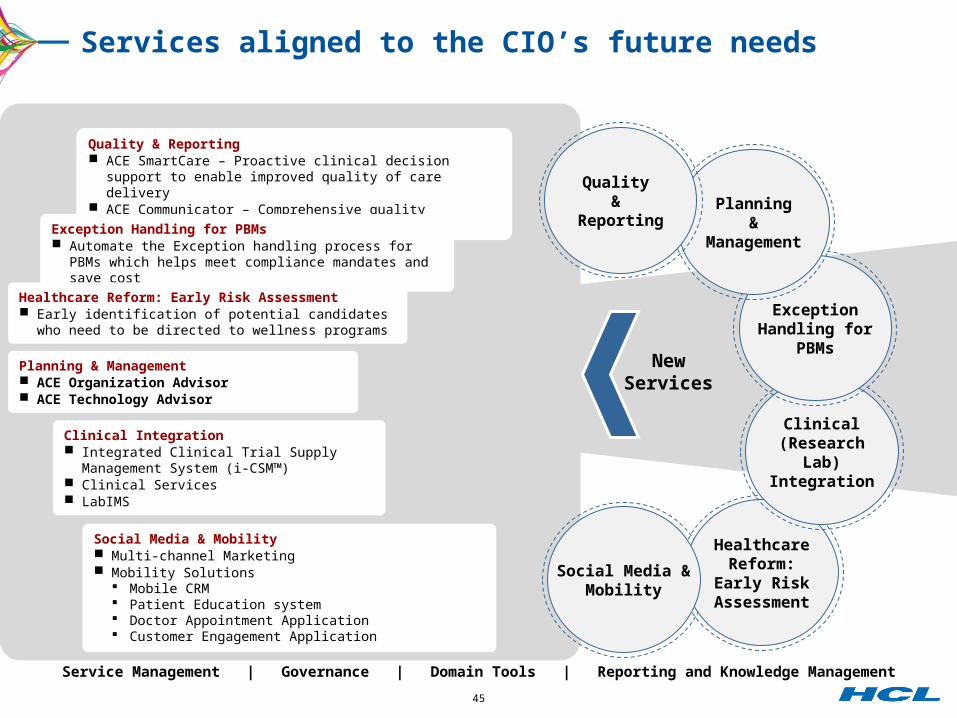

Consolidation & Collaboration Pharma PLM Marketing Shared Services (MSS) Integrated Service Delivery Model

Compliance Office of Regulatory Affairs &

Compliance ACE ICDX ACE HIPAA Regulatory Submission E-Pedigree ICD 9 to 10 Transition:

Migration & Testing i-CRM Crosswalk Reimbursement and

Mapping tool for ICD 9 to 10 transition Pharmacovigilance CoE

Core Administration Facets/ NetworX Pricer CoE

45

Services aligned to the CIO’s future needs

Healthcare

Services

Service Management | Governance | Domain Tools | Reporting and Knowledge Management

Consolidation & Collaboration

Core Administration

Compliance

Existing Services

Quality & Reporting ACE SmartCare – Proactive clinical decision support to enable

improved quality of care delivery ACE Communicator – Comprehensive quality reporting solution

Healthcare Reform:

Early Risk Assessment

Clinical (Research Lab)

Integration

Exception Handling for

PBMs

Planning&

Management

Social Media & Mobility

Quality &

Reporting

NewServices

Exception Handling for PBMs Automate the Exception handling process for PBMs which

helps meet compliance mandates and save cost

Healthcare Reform: Early Risk Assessment Early identification of potential candidates who need to be

directed to wellness programs

Planning & Management ACE Organization Advisor ACE Technology Advisor

Clinical Integration Integrated Clinical Trial Supply Management

System (i-CSM™) Clinical Services LabIMS

Social Media & Mobility Multi-channel Marketing Mobility Solutions

Mobile CRM Patient Education system Doctor Appointment Application Customer Engagement Application

46

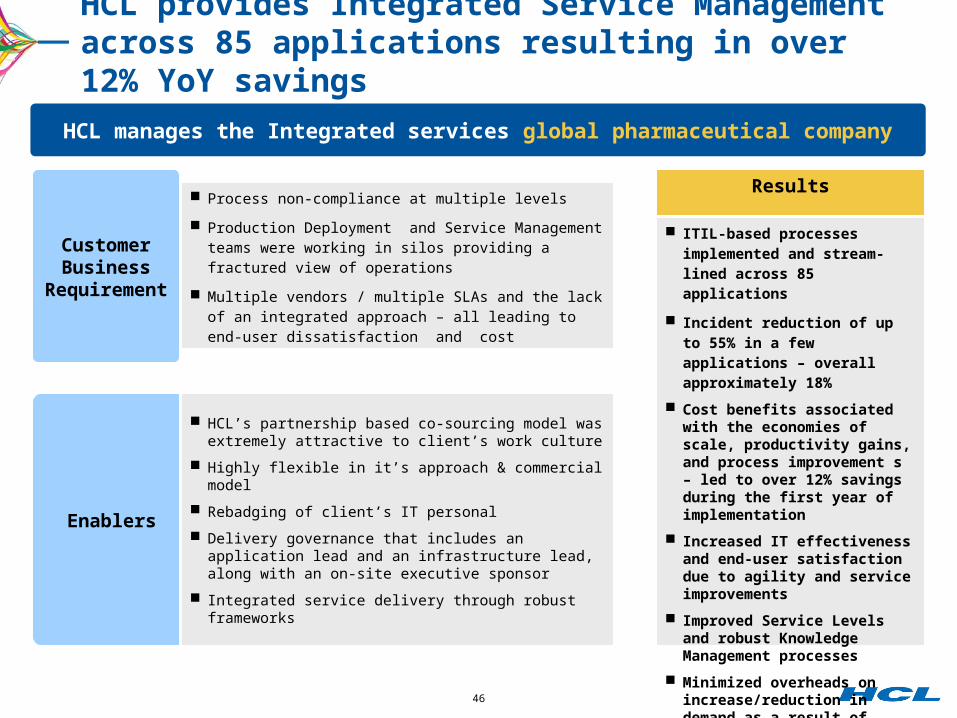

HCL provides Integrated Service Management across 85 applications resulting in over 12% YoY savings

HCL manages the Integrated services global pharmaceutical company

Enablers

HCL’s partnership based co-sourcing model was extremely attractive to client’s work culture

Highly flexible in it’s approach & commercial model

Rebadging of client’s IT personal

Delivery governance that includes an application lead and an infrastructure lead, along with an on-site executive sponsor

Integrated service delivery through robust frameworks

Customer Business

Requirement

Process non-compliance at multiple levels

Production Deployment and Service Management teams were working in silos providing a fractured view of operations

Multiple vendors / multiple SLAs and the lack of an integrated approach – all leading to end-user dissatisfaction and cost

Results

ITIL-based processes implemented and stream-lined across 85 applications

Incident reduction of up to 55% in a few applications – overall approximately 18%

Cost benefits associated with the economies of scale, productivity gains, and process improvement s – led to over 12% savings during the first year of implementation

Increased IT effectiveness and end-user satisfaction due to agility and service improvements

Improved Service Levels and robust Knowledge Management processes

Minimized overheads on increase/reduction in demand as a result of better scalability

ENTERPRISE APPLICATION SERVICES

48

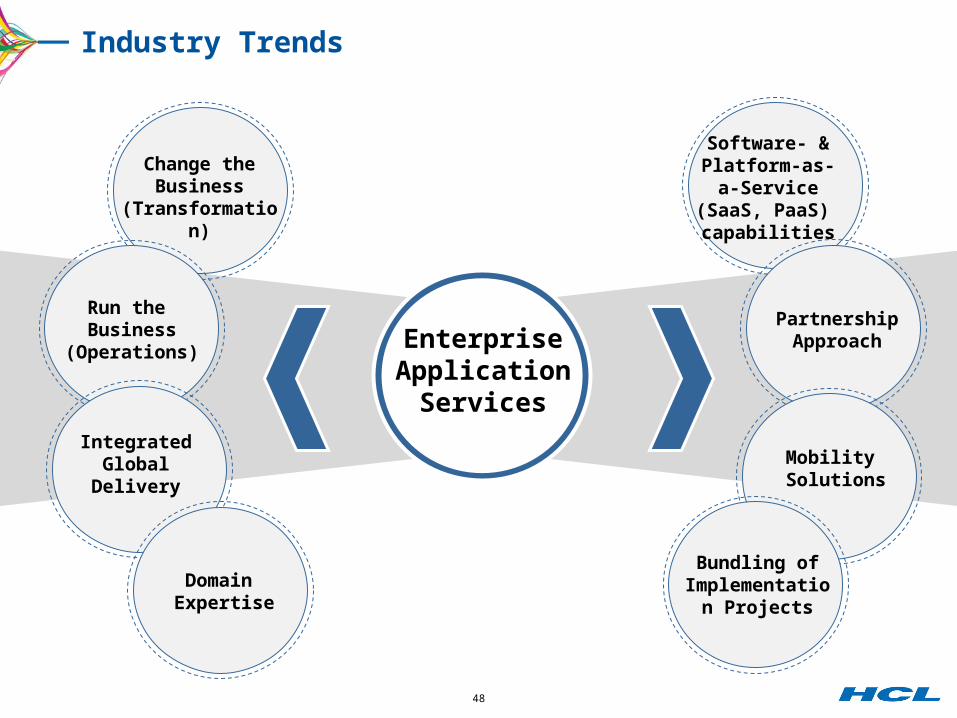

Industry Trends

EnterpriseApplication

Services

Change the Business

(Transformation)

Run the Business

(Operations)

Integrated Global

Delivery

Domain Expertise

Software- & Platform-as-a-

Service (SaaS, PaaS) capabilities

Mobility Solutions

PartnershipApproach

Bundling of Implementation

Projects

49

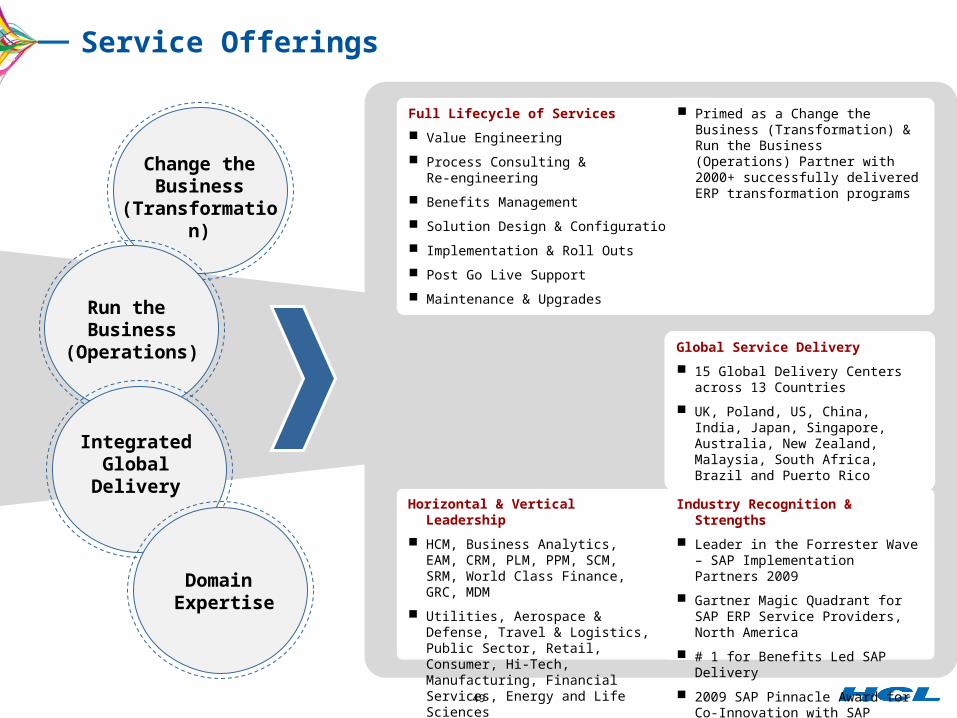

Service Offerings

Change the Business

(Transformation)

Run the Business

(Operations)

Integrated Global

Delivery

Domain Expertise

Leveraged Services

Cloud Computing Offerings

Infrastructure Utility

Green Computing

Infrastructure

Services

NewServices

Horizontal & Vertical Leadership

HCM, Business Analytics, EAM, CRM, PLM, PPM, SCM, SRM, World Class Finance, GRC, MDM

Utilities, Aerospace & Defense, Travel & Logistics, Public Sector, Retail, Consumer, Hi-Tech, Manufacturing, Financial Services, Energy and Life Sciences

Industry Recognition & Strengths

Leader in the Forrester Wave – SAP Implementation Partners 2009

Gartner Magic Quadrant for SAP ERP Service Providers, North America

# 1 for Benefits Led SAP Delivery

2009 SAP Pinnacle Award forCo-Innovation with SAP

Global Service Delivery

15 Global Delivery Centers across 13 Countries

UK, Poland, US, China, India, Japan, Singapore, Australia, New Zealand, Malaysia, South Africa, Brazil and Puerto Rico

Full Lifecycle of Services

Value Engineering

Process Consulting & Re-engineering

Benefits Management

Solution Design & Configuration

Implementation & Roll Outs

Post Go Live Support

Maintenance & Upgrades

Primed as a Change the Business (Transformation) & Run the Business (Operations) Partner with 2000+ successfully delivered ERP transformation programs

50

Service Offerings

EnterpriseApplication

Services

Change the Business

(Transformation)

Run the Business

(Operations)

Integrated Global

Delivery

Domain Expertise

Software- & Platform-as-a-

Service (SaaS, PaaS) capabilities

Mobility Solutions

PartnershipApproach

Bundling of Implementation

Projects

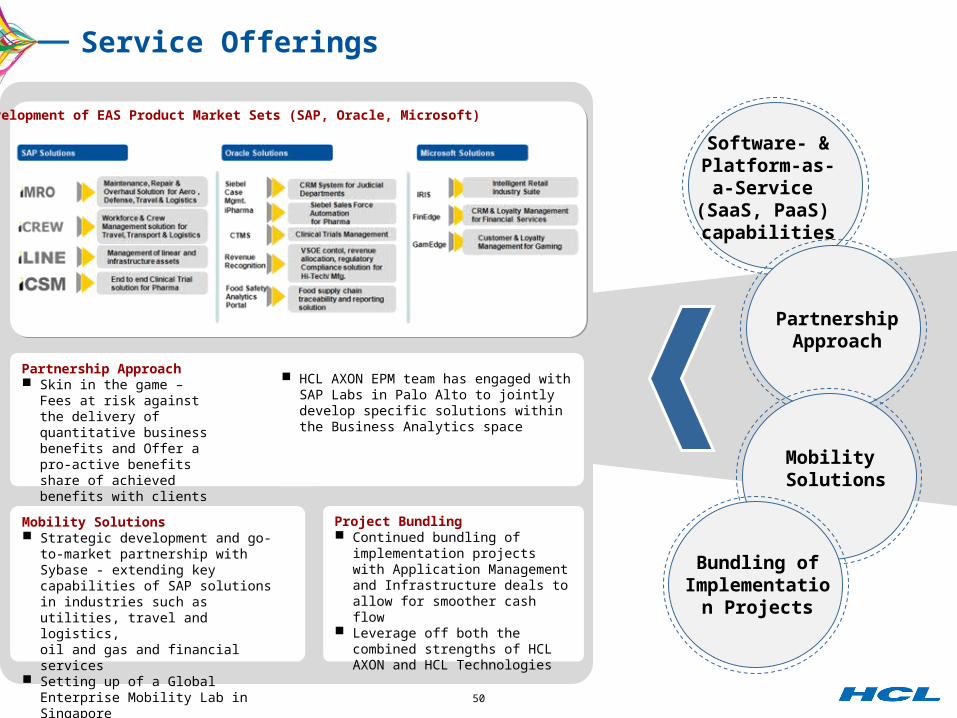

Development of EAS Product Market Sets (SAP, Oracle, Microsoft)

Partnership Approach Skin in the game –

Fees at risk against the delivery of quantitative business benefits and Offer a pro-active benefits share of achieved benefits with clients

HCL AXON EPM team has engaged with SAP Labs in Palo Alto to jointly develop specific solutions within the Business Analytics space

Mobility Solutions Strategic development and go-to-market

partnership with Sybase - extending key capabilities of SAP solutions in industries such as utilities, travel and logistics, oil and gas and financial services

Setting up of a Global Enterprise Mobility Lab in Singapore

Project Bundling Continued bundling of

implementation projects with Application Management and Infrastructure deals to allow for smoother cash flow

Leverage off both the combined strengths of HCL AXON and HCL Technologies

51

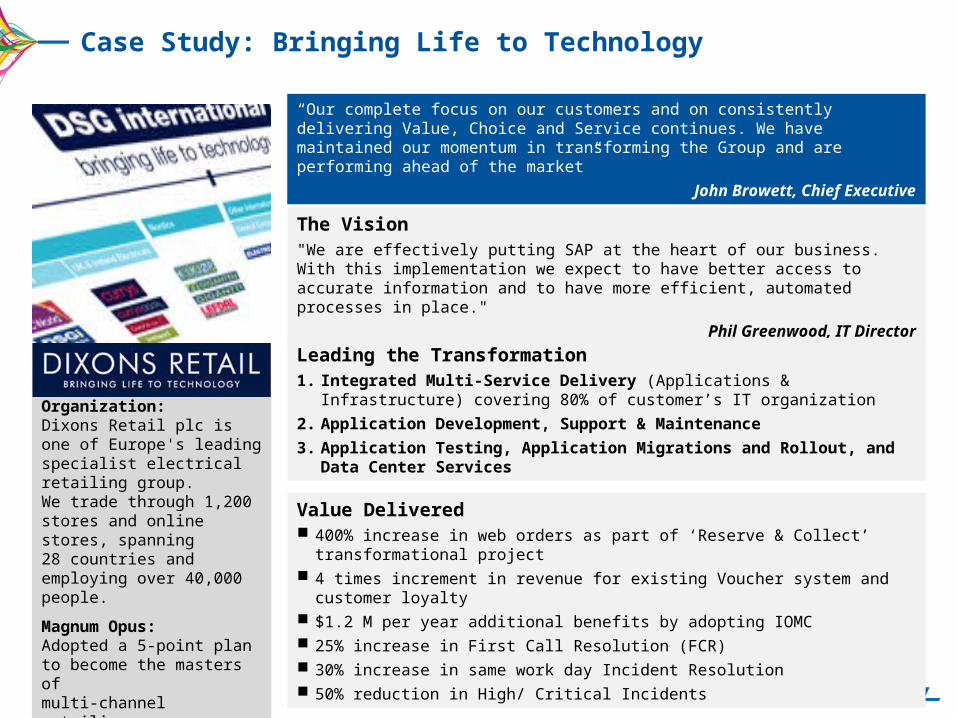

Case Study: Bringing Life to Technology

The Vision"We are effectively putting SAP at the heart of our business. With this implementation we expect to have better access to accurate information and to have more efficient, automated processes in place."

Phil Greenwood, IT Director

Leading the Transformation1. Integrated Multi-Service Delivery (Applications & Infrastructure) covering 80% of

customer’s IT organization

2. Application Development, Support & Maintenance

3. Application Testing, Application Migrations and Rollout, and Data Center Services

Organization:Dixons Retail plc is one of Europe's leading specialist electrical retailing group. We trade through 1,200 stores and online stores, spanning 28 countries and employing over 40,000 people.

Magnum Opus:Adopted a 5-point plan to become the masters of multi-channel retailing.

Renewal and Transformation

“Our complete focus on our customers and on consistently delivering Value, Choice and Service continues. We have maintained our momentum in transforming the Group and are performing ahead of the market”

John Browett, Chief Executive

Value Delivered 400% increase in web orders as part of ‘Reserve & Collect’ transformational project 4 times increment in revenue for existing Voucher system and customer loyalty $1.2 M per year additional benefits by adopting IOMC 25% increase in First Call Resolution (FCR) 30% increase in same work day Incident Resolution 50% reduction in High/ Critical Incidents

MANUFACTURING

53

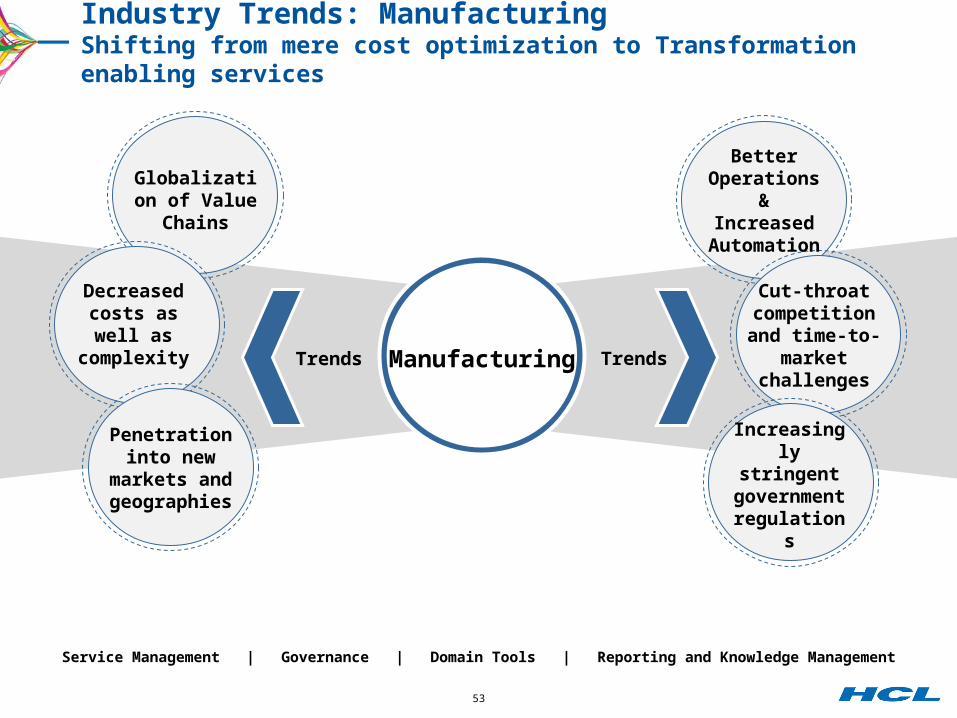

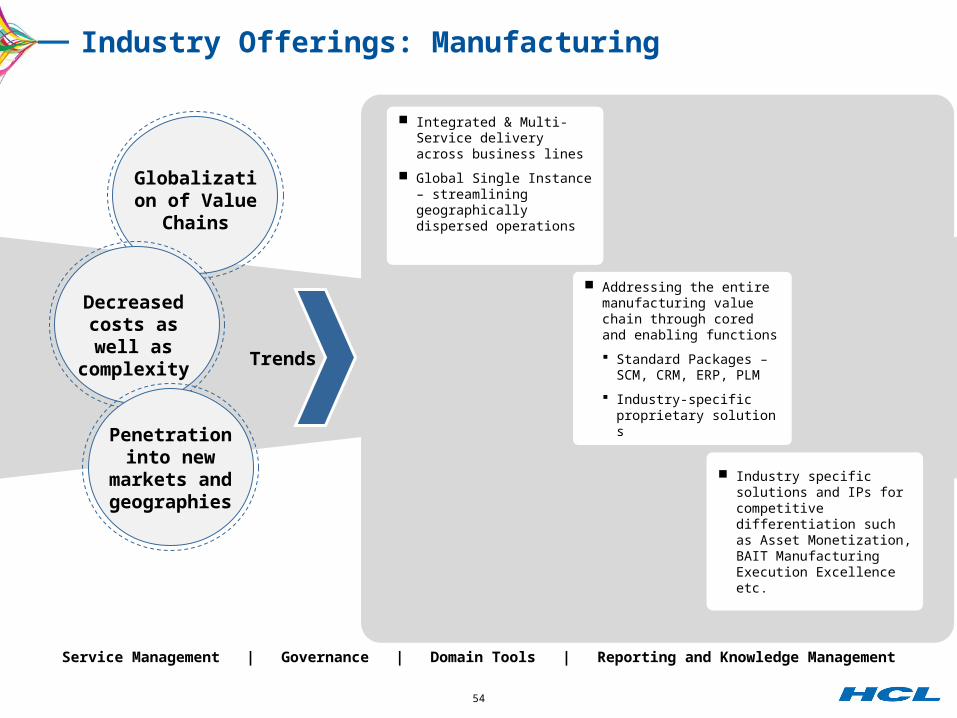

Manufacturing

Globalization of Value Chains

Decreased costs as well as complexity

Penetration into new

markets and geographies

Better Operations &

Increased Automation

Cut-throat competition and time-to-

market challenges

Increasingly stringent

government regulations

Trends Trends

Service Management | Governance | Domain Tools | Reporting and Knowledge Management

Industry Trends: ManufacturingShifting from mere cost optimization to Transformation enabling services

54

Industry Offerings: Manufacturing

Manufacturing

Globalization of Value Chains

Decreased costs as well as complexity

Penetration into new

markets and geographies

Increased Automation

Straight through

Processing

Cost Reductions

and Operational Efficiency

Trends Trends

Service Management | Governance | Domain Tools | Reporting and Knowledge Management

Industry specific solutions and IPs for competitive differentiation such as Asset Monetization, BAIT Manufacturing Execution Excellence etc.

Integrated & Multi-Service delivery across business lines

Global Single Instance – streamlining geographically dispersed operations

Addressing the entire manufacturing value chain through cored and enabling functions

Standard Packages – SCM, CRM, ERP, PLM

Industry-specific proprietary solutions

55

Industry Offerings: Manufacturing

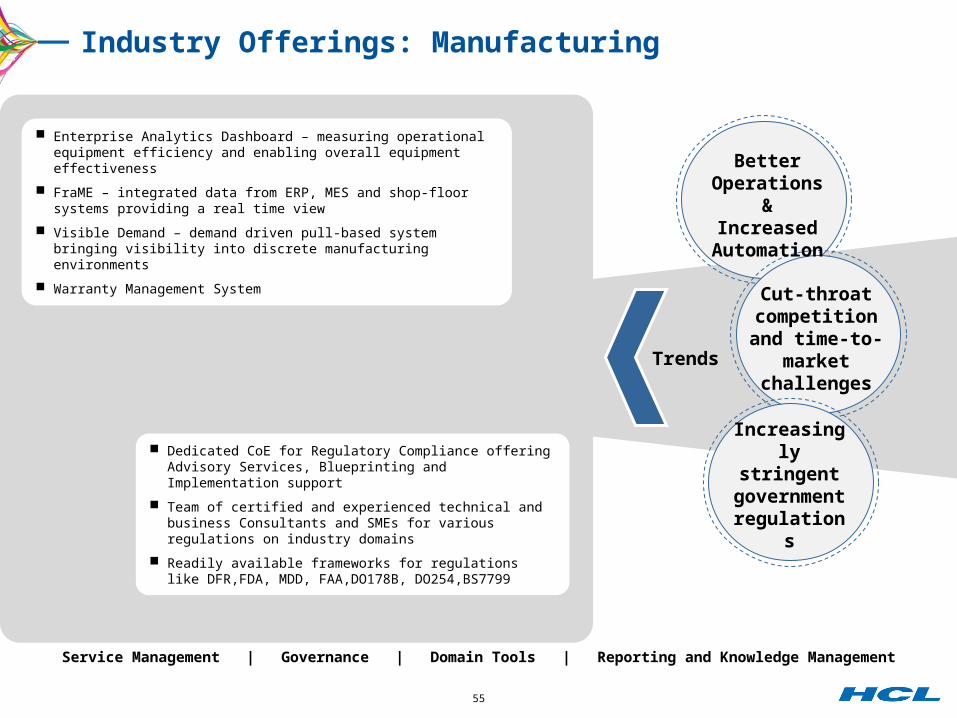

Manufacturing

Regulatory Compliance

Customer Experience

Management

Penetration into new

markets and geographies

Better Operations &

Increased Automation

Cut-throat competition and time-to-

market challenges

Increasingly stringent

government regulations

Trends Trends

Service Management | Governance | Domain Tools | Reporting and Knowledge Management

Enterprise Analytics Dashboard – measuring operational equipment efficiency and enabling overall equipment effectiveness

FraME – integrated data from ERP, MES and shop-floor systems providing a real time view

Visible Demand – demand driven pull-based system bringing visibility into discrete manufacturing environments

Warranty Management System

Dedicated CoE for Regulatory Compliance offering Advisory Services, Blueprinting and Implementation support

Team of certified and experienced technical and business Consultants and SMEs for various regulations on industry domains

Readily available frameworks for regulations like DFR,FDA, MDD, FAA,DO178B, DO254,BS7799

56

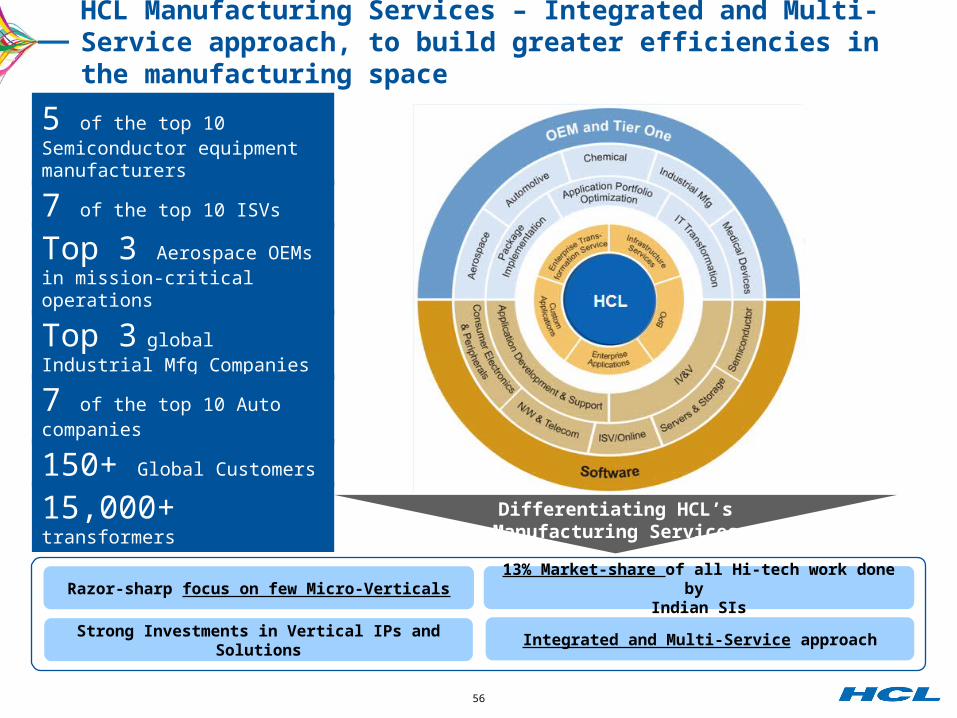

HCL Manufacturing Services – Integrated and Multi-Service approach, to build greater efficiencies in the manufacturing space

5 of the top 10 Semiconductor equipment manufacturers

150+ Global Customers

15,000+ transformersDifferentiating HCL’s Manufacturing

Services

7 of the top 10 ISVs

Top 3 global Industrial Mfg Companies

Top 3 Aerospace OEMs in mission-critical operations

7 of the top 10 Auto companies

Razor-sharp focus on few Micro-Verticals

Strong Investments in Vertical IPs and Solutions

13% Market-share of all Hi-tech work done by Indian SIs

Integrated and Multi-Service approach

57

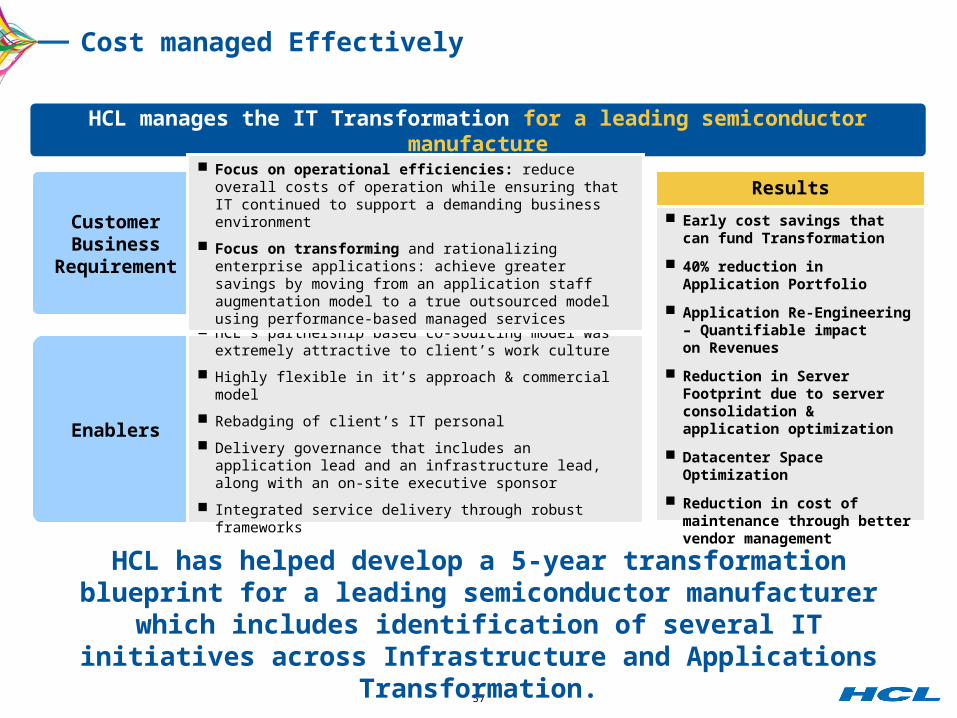

Cost managed Effectively

Enablers

HCL’s partnership based co-sourcing model was extremely attractive to client’s work culture

Highly flexible in it’s approach & commercial model

Rebadging of client’s IT personal

Delivery governance that includes an application lead and an infrastructure lead, along with an on-site executive sponsor

Integrated service delivery through robust frameworks

HCL has helped develop a 5-year transformation blueprint for a leading semiconductor manufacturer which includes identification

of several IT initiatives across Infrastructure and Applications Transformation.

HCL manages the IT Transformation for a leading semiconductor manufacture

Customer Business

Requirement

Focus on operational efficiencies: reduce overall costs of operation while ensuring that IT continued to support a demanding business environment

Focus on transforming and rationalizing enterprise applications: achieve greater savings by moving from an application staff augmentation model to a true outsourced model using performance-based managed services

Results

Early cost savings that can fund Transformation

40% reduction in Application Portfolio

Application Re-Engineering – Quantifiable impact on Revenues

Reduction in Server Footprint due to server consolidation & application optimization

Datacenter Space Optimization

Reduction in cost of maintenance through better vendor management

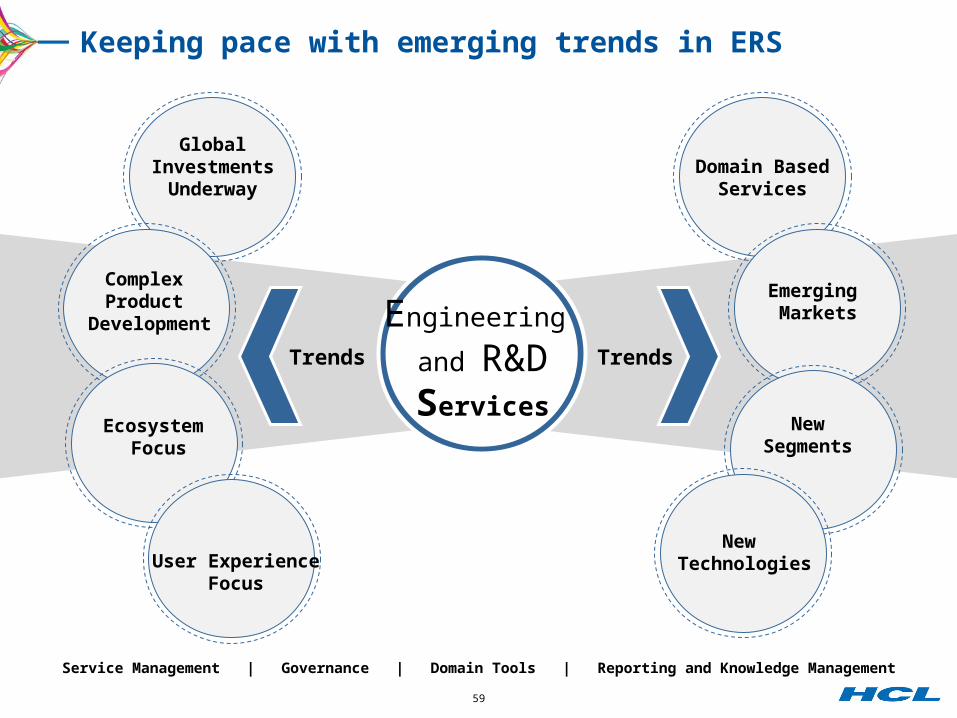

ENGINEERING AND R&D SERVICES

59

Engineering

and R&DServices

Global Investments Underway

Complex Product

Development

Ecosystem Focus

User Experience Focus

Domain Based Services

Emerging Markets

NewSegments

New Technologies

Trends Trends

Service Management | Governance | Domain Tools | Reporting and Knowledge Management

Keeping pace with emerging trends in ERS

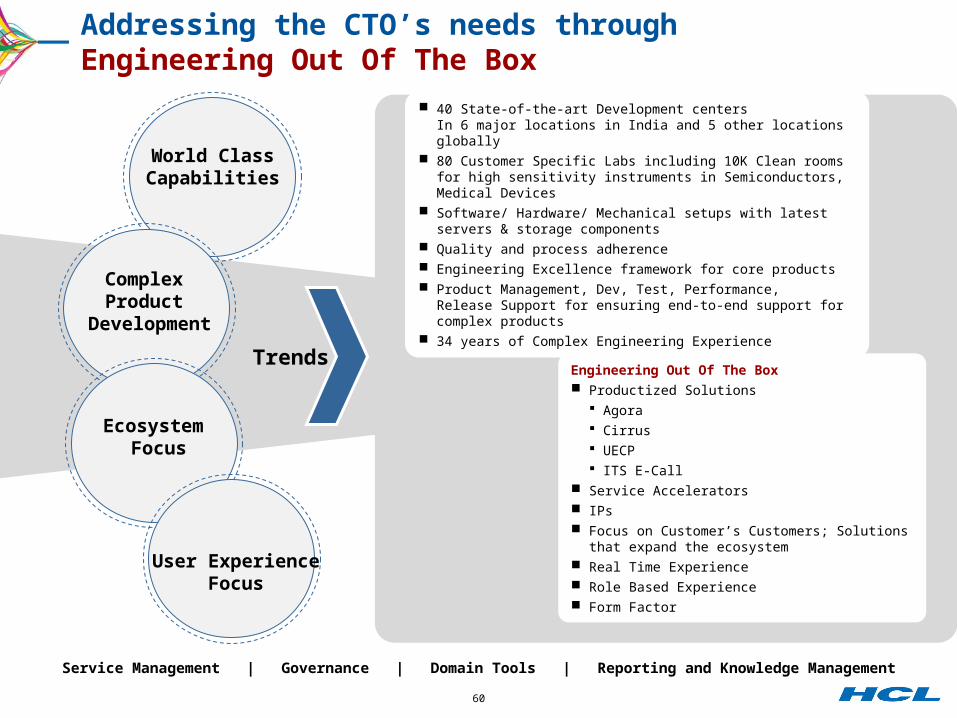

60

Engineering

and R&DServices

World Class Capabilities

Complex Product

Development

Ecosystem Focus

User Experience Focus

Domain Based Services

Emerging Markets

NewTechnologies

New Segments

Trends Trends

Service Management | Governance | Domain Tools | Reporting and Knowledge Management

Addressing the CTO’s needs through Engineering Out Of The Box

40 State-of-the-art Development centers In 6 major locations in India and 5 other locations globally

80 Customer Specific Labs including 10K Clean rooms for high sensitivity instruments in Semiconductors, Medical Devices

Software/ Hardware/ Mechanical setups with latest servers & storage components

Quality and process adherence Engineering Excellence framework for core products Product Management, Dev, Test, Performance,

Release Support for ensuring end-to-end support for complex products 34 years of Complex Engineering Experience

Engineering Out Of The Box Productized Solutions

Agora Cirrus UECP ITS E-Call

Service Accelerators IPs Focus on Customer’s Customers; Solutions that

expand the ecosystem Real Time Experience Role Based Experience Form Factor

61

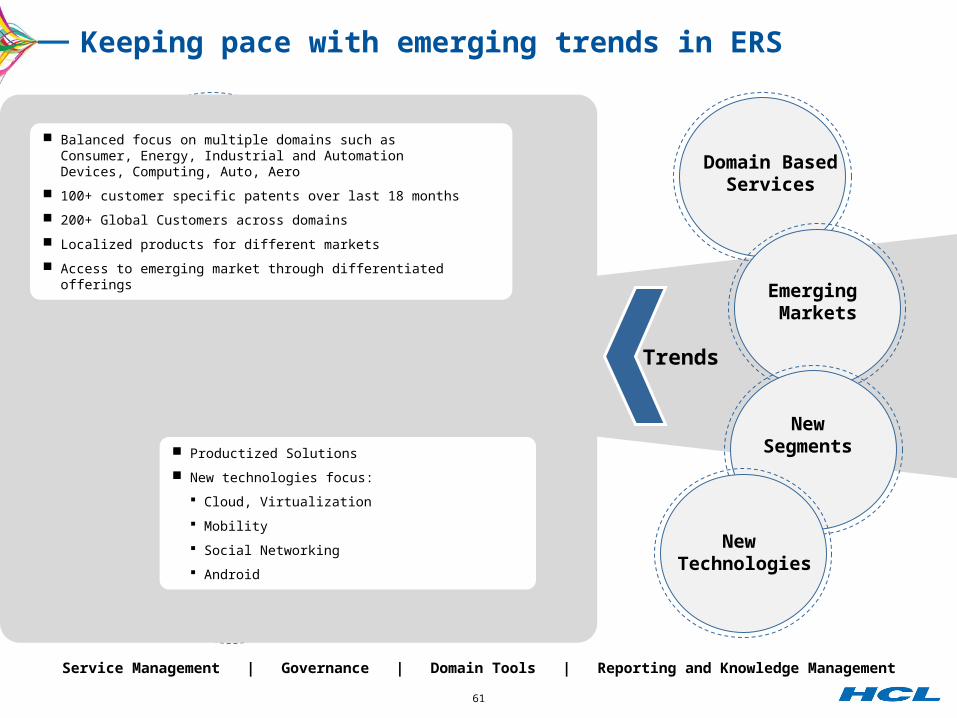

Keeping pace with emerging trends in ERS

Engineering

and R&DServices

Global Investments Underway

Complex Product

Development

Ecosystem Focus

User Experience Focus

Domain Based Services

Emerging Markets

NewSegments

New Technologies

Trends Trends

Service Management | Governance | Domain Tools | Reporting and Knowledge Management

Balanced focus on multiple domains such as Consumer, Energy, Industrial and Automation Devices, Computing, Auto, Aero

100+ customer specific patents over last 18 months

200+ Global Customers across domains

Localized products for different markets

Access to emerging market through differentiated offerings

Productized Solutions

New technologies focus:

Cloud, Virtualization

Mobility

Social Networking

Android

62

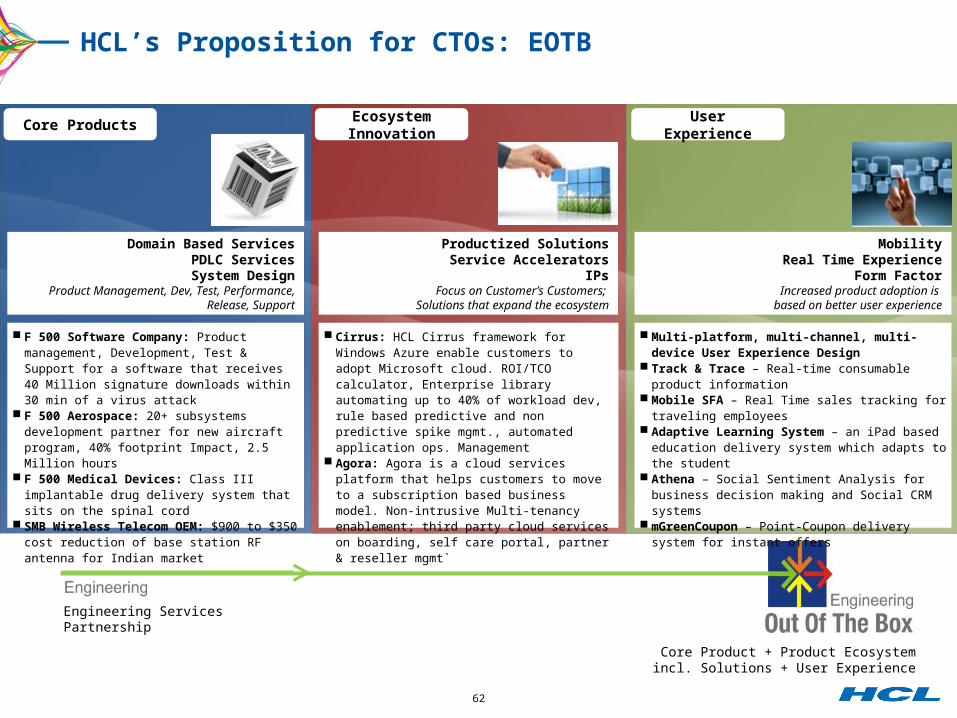

HCL’s Proposition for CTOs: EOTB

Core ProductsEcosystem Innovation

User Experience

Domain Based ServicesPDLC ServicesSystem Design

Product Management, Dev, Test, Performance, Release, Support

Productized SolutionsService Accelerators

IPsFocus on Customer’s Customers;

Solutions that expand the ecosystem

MobilityReal Time Experience

Form FactorIncreased product adoption is

based on better user experience

Engineering Services Partnership

Core Product + Product Ecosystem incl. Solutions + User Experience

F 500 Software Company: Product management, Development, Test & Support for a software that receives 40 Million signature downloads within 30 min of a virus attack

F 500 Aerospace: 20+ subsystems development partner for new aircraft program, 40% footprint Impact, 2.5 Million hours

F 500 Medical Devices: Class III implantable drug delivery system that sits on the spinal cord

SMB Wireless Telecom OEM: $900 to $350 cost reduction of base station RF antenna for Indian market

Cirrus: HCL Cirrus framework for Windows Azure enable customers to adopt Microsoft cloud. ROI/TCO calculator, Enterprise library automating up to 40% of workload dev, rule based predictive and non predictive spike mgmt., automated application ops. Management

Agora: Agora is a cloud services platform that helps customers to move to a subscription based business model. Non-intrusive Multi-tenancy enablement; third party cloud services on boarding, self care portal, partner & reseller mgmt`

Multi-platform, multi-channel, multi-device User Experience Design

Track & Trace – Real-time consumable product information

Mobile SFA – Real Time sales tracking for traveling employees

Adaptive Learning System – an iPad based education delivery system which adapts to the student

Athena – Social Sentiment Analysis for business decision making and Social CRM systems

mGreenCoupon – Point-Coupon delivery system for instant offers

63

Case Study: EndoPharma

Organization:Endo Pharmaceuticals Inc. (Endo) is specialty pharma company. Established in 1997, company focuses on pain management.

His Magnum Opus:Convert a Pharma company into a healthcare solutions company with both drug & devices to offer complete experience for physicians and care givers.

Flexible, scalable, cost-effective, and very agile R&D team is my focusSujat SukthankarVP & Head, Devices

The CIO’s Vision

Diversify to a solutions based company entailing both devices and drugs

Develop/ Leverage Semi-Virtual R&D Model to leverage on device development best practices in the industry

Focus on Urology Market space followed by launches in other markets

The Outcome So Far

“We are relying on our R&D partners to create value for the organization, and they play a key role in driving our technology and R&D strategy. We believe that close collaboration with our R&D partners will drive results, and we have shown that successfully in a relatively short amount of time. We also believe that a results-driven, semi-virtual model provides a scalable, agile, and cost-effective means of driving innovation forward.”

Consumer Services Telecom

Retail & Consumer Products Group

Media & Entertainment

65

Consumer Services

Retail Digital real estate over

Physical

Consumer Goods:Consumer Frugality

& Traceability

M&E:User Gen

content and the Long Tail

rule

Telecom:The Digital Home

gateway

Trends Trends

Trends

66

Consumer Services

Retail Digital real estate over

Physical

Consumer Goods:Consumer Frugality

& Traceability

M&E:User Gen

content and the Long Tail

rule

Telecom:The Digital Home

gateway

Trends Trends

Service Offerings

Digital Supply Chain Services (including rights, access management & royalty)

Web 2.0/ Social Networking

Micro Vertical Domain Services & Solutions – Publishing & BIS New Media- Studios, Broadcasting & Music Gaming & Hospitality

Advanced Technologies Empowerment Services

Android & New platforms app development

Ticket Lifecycle Management Span for Services Providers

Unified Communications & Mobility Services

Engineering Cost Optimization

67

Consumer Services

Retail Digital real estate over

Physical

Consumer Goods:Consumer Frugality

& Traceability

M&E:User Gen

content and the Long Tail

rule

Telecom:The Digital Home

gateway

Trends Trends

Service Offerings

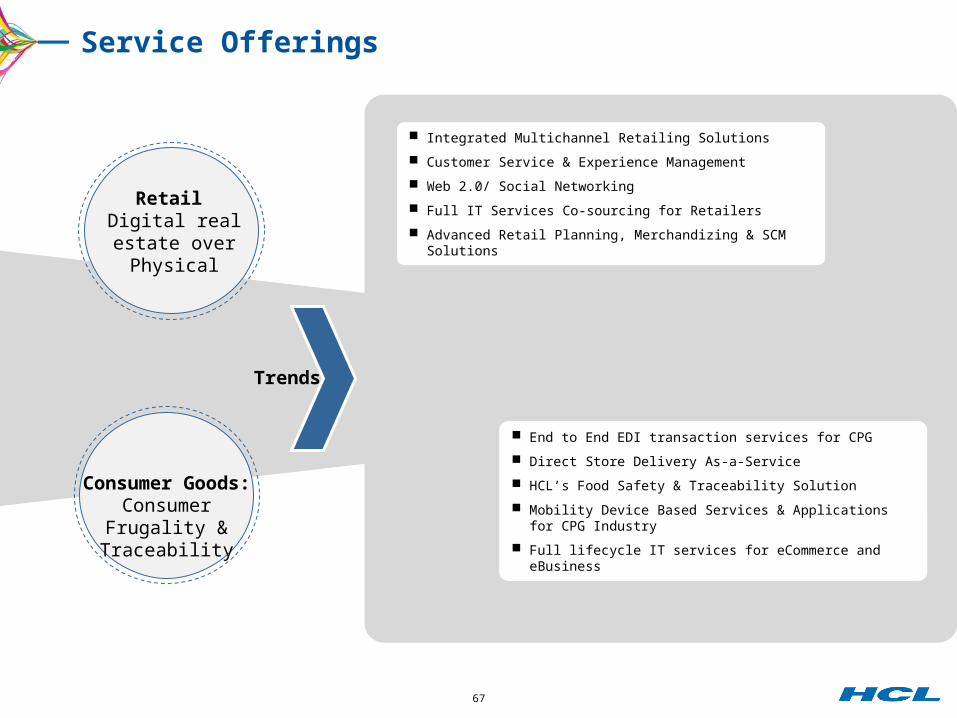

Integrated Multichannel Retailing Solutions

Customer Service & Experience Management

Web 2.0/ Social Networking

Full IT Services Co-sourcing for Retailers

Advanced Retail Planning, Merchandizing & SCM Solutions

End to End EDI transaction services for CPG

Direct Store Delivery As-a-Service

HCL’s Food Safety & Traceability Solution

Mobility Device Based Services & Applications for CPG Industry

Full lifecycle IT services for eCommerce and eBusiness

68

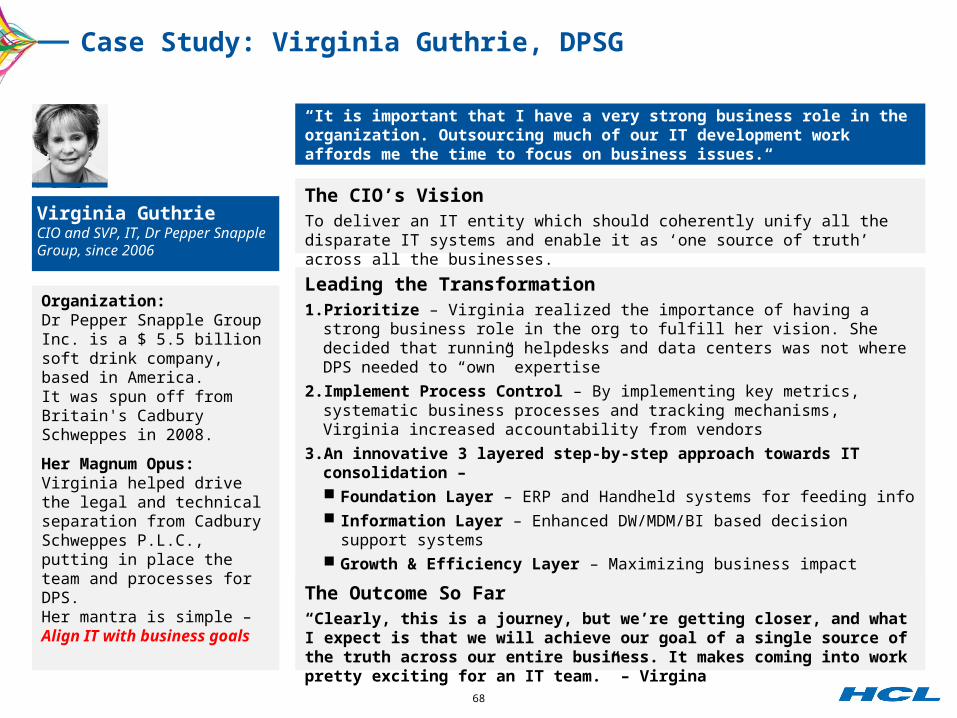

Case Study: Virginia Guthrie, DPSG

The CIO’s VisionTo deliver an IT entity which should coherently unify all the disparate IT systems and enable it as ‘one source of truth’ across all the businesses.

Leading the Transformation1. Prioritize – Virginia realized the importance of having a strong business role in the

org to fulfill her vision. She decided that running helpdesks and data centers was not where DPS needed to “own” expertise

2. Implement Process Control – By implementing key metrics, systematic business processes and tracking mechanisms, Virginia increased accountability from vendors

3. An innovative 3 layered step-by-step approach towards IT consolidation – Foundation Layer – ERP and Handheld systems for feeding info Information Layer – Enhanced DW/MDM/BI based decision support systems Growth & Efficiency Layer – Maximizing business impact

4. Alignment with business – Work hand-in-hand with business units to be an important enabler to “Grow Sales and Cut Costs”

“It is important that I have a very strong business role in the organization. Outsourcing much of our IT development work affords me the time to focus on business issues.“

The Outcome So Far“Clearly, this is a journey, but we’re getting closer, and what I expect is that we will achieve our goal of a single source of the truth across our entire business. It makes coming into work pretty exciting for an IT team.” – Virgina

Organization:Dr Pepper Snapple Group Inc. is a $ 5.5 billion soft drink company, based in America. It was spun off from Britain's Cadbury Schweppes in 2008.

Her Magnum Opus:Virginia helped drive the legal and technical separation from Cadbury Schweppes P.L.C., putting in place the team and processes for DPS. Her mantra is simple – Align IT with business goals

Virginia GuthrieCIO and SVP, IT, Dr Pepper Snapple Group, since 2006

ENTERPRISE TRANSFORMATION SERVICES

70

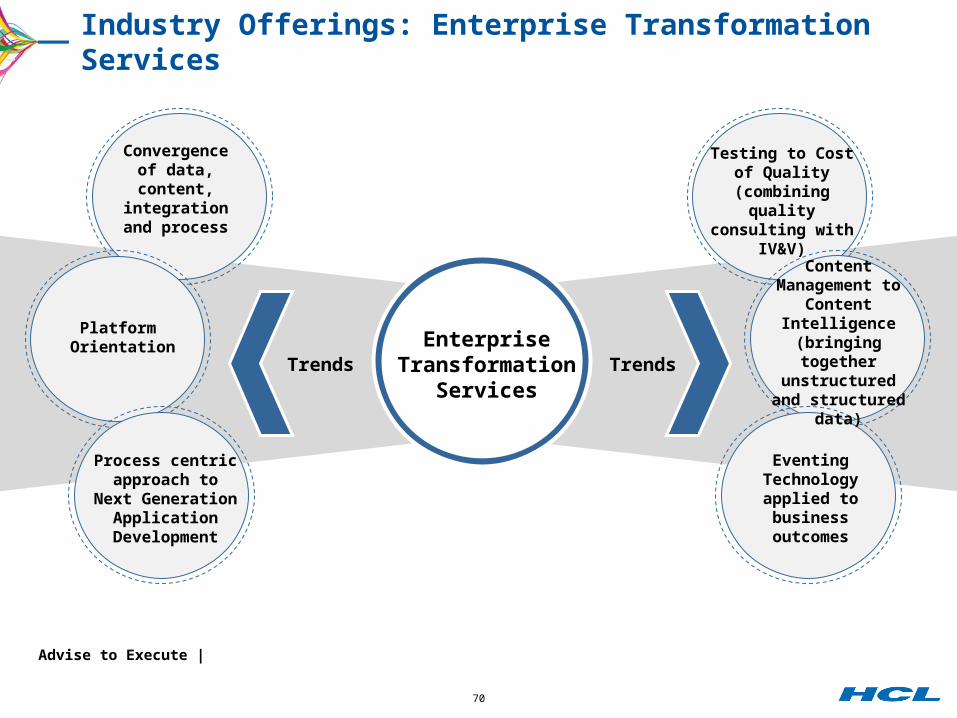

Enterprise Transformation

Services

Convergence of data, content,

integration and process

Platform Orientation

Process centric approach to

Next Generation Application

Development

Testing to Cost of Quality (combining quality consulting

with IV&V)

Eventing Technology applied

to business outcomes

Trends Trends

Industry Offerings: Enterprise Transformation Services

Content Management to

Content Intelligence (bringing together

unstructured and structured

data)

Advise to Execute |

71

Enterprise Transformation

Services

Convergence of data, content,

integration and process

Platform Orientation

Process centric approach to

Next Generation Application

Development

Testing to Cost of Quality (combining quality consulting

with IV&V)

Eventing Technology applied

to business outcomes

Trends Trends

Industry Offerings: Enterprise Transformation Services

Content Management to

Content Intelligence (bringing together

unstructured and structured

data)

Service Management | Governance | Domain Tools | Reporting and Knowledge Management

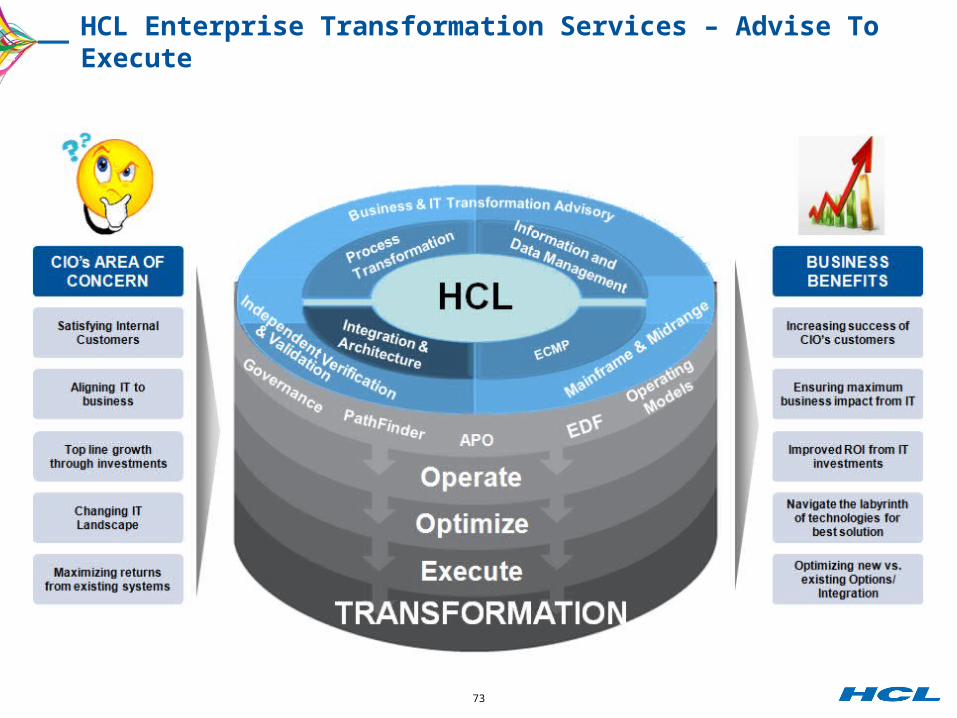

Integrated portfolio of services (Advise to Execute)

Integration Transformation Services, Data Transformation Services and Architecture Transformation Services

Business Transformation & IT Transformation Services

IT Strategy & Change Management

Cutting Edge Technologies

Process Consulting, Business Process Management

Global Visibility

Process Re-engineering

Platform Modernization & Consolidation, Legacy Modernization

Next Generation Application platform development

72

Regulatory Compliance

Customer Experience

Management

Mobility

Testing to Cost of Quality (combining quality consulting

with IV&V)

Eventing Technology applied

to business outcomes

Trends Trends

Industry Offerings: Financial Services

Content Management to

Content Intelligence (bringing together

unstructured and structured

data)

Service Management | Governance | Domain Tools | Reporting and Knowledge Management

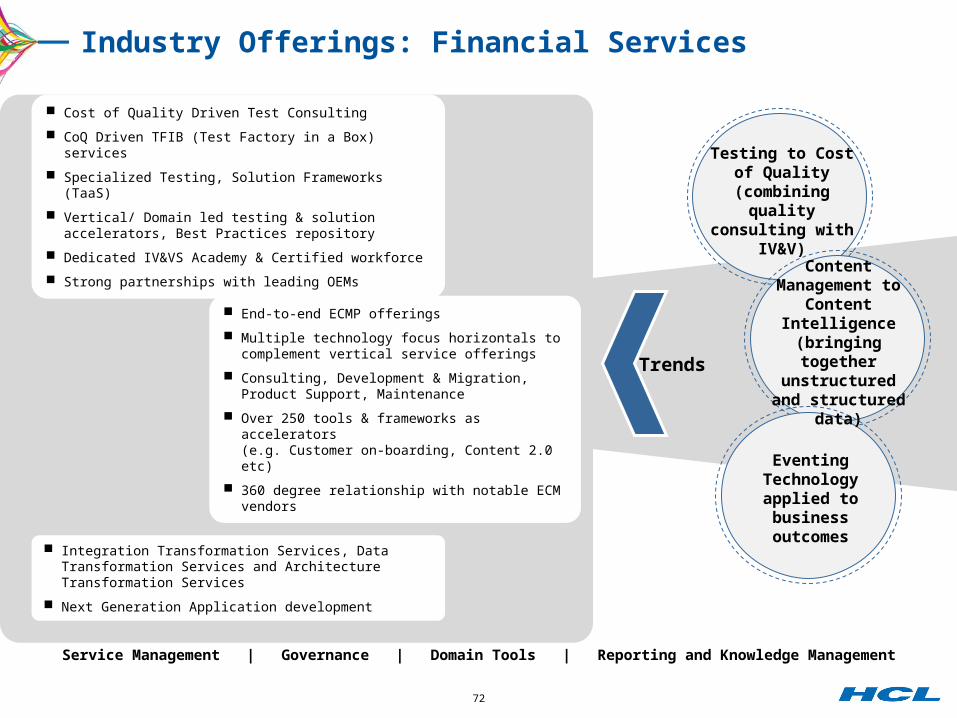

Cost of Quality Driven Test Consulting

CoQ Driven TFIB (Test Factory in a Box) services

Specialized Testing, Solution Frameworks (TaaS)

Vertical/ Domain led testing & solution accelerators, Best Practices repository

Dedicated IV&VS Academy & Certified workforce

Strong partnerships with leading OEMs

Integration Transformation Services, Data Transformation Services and Architecture Transformation Services

Next Generation Application development

Financial

Services

End-to-end ECMP offerings

Multiple technology focus horizontals to complement vertical service offerings

Consulting, Development & Migration, Product Support, Maintenance

Over 250 tools & frameworks as accelerators(e.g. Customer on-boarding, Content 2.0 etc)

360 degree relationship with notable ECM vendors

73

HCL Enterprise Transformation Services – Advise To Execute

74

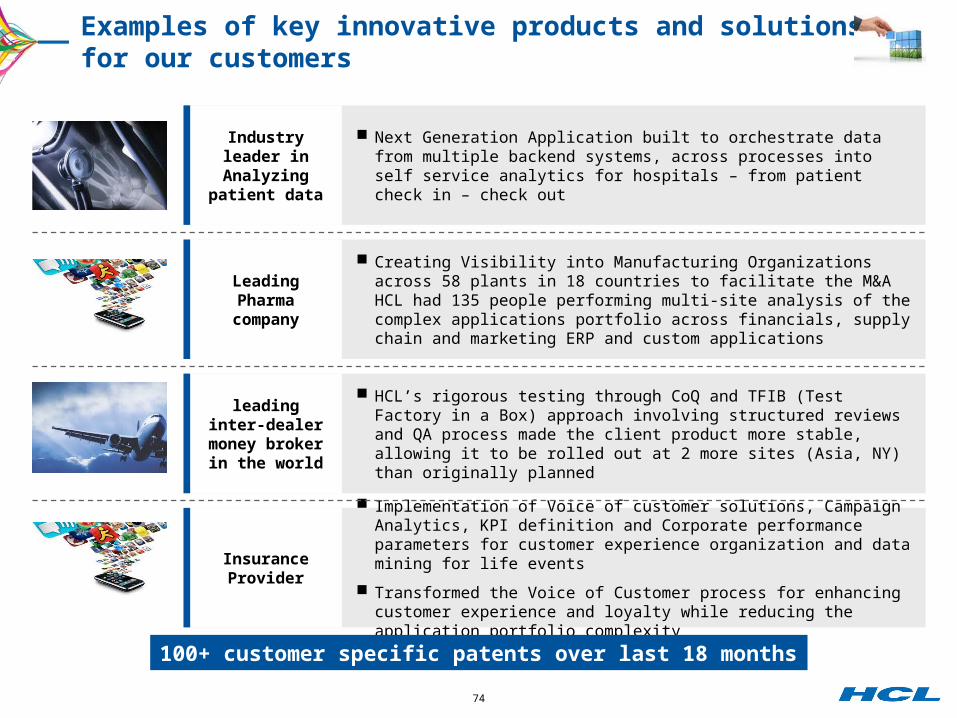

Next Generation Application built to orchestrate data from multiple backend systems, across processes into self service analytics for hospitals – from patient check in – check out

Creating Visibility into Manufacturing Organizations across 58 plants in 18 countries to facilitate the M&A HCL had 135 people performing multi-site analysis of the complex applications portfolio across financials, supply chain and marketing ERP and custom applications

HCL’s rigorous testing through CoQ and TFIB (Test Factory in a Box) approach involving structured reviews and QA process made the client product more stable, allowing it to be rolled out at 2 more sites (Asia, NY) than originally planned

Implementation of Voice of customer solutions, Campaign Analytics, KPI definition and Corporate performance parameters for customer experience organization and data mining for life events

Transformed the Voice of Customer process for enhancing customer experience and loyalty while reducing the application portfolio complexity

Examples of key innovative products and solutions for our customers

leading inter-dealer money broker in the

world

Leading Pharma company

Industry leader in Analyzing patient data

100+ customer specific patents over last 18 months

Insurance Provider

BUSINESS SERVICES

76

NeXt Generation

BPO BPO 1.0

Business Services

Cost Arbitrage

Model

Headcount Based

Discrete Process

Low Impact Risk &

Compliance

Innovation & Improvement

Output Based

Constructs

Integrated Global

Delivery

EFCS Platform

Domain Orientation

The World is changing and so are we:BPO 1.0 to Business Services

77

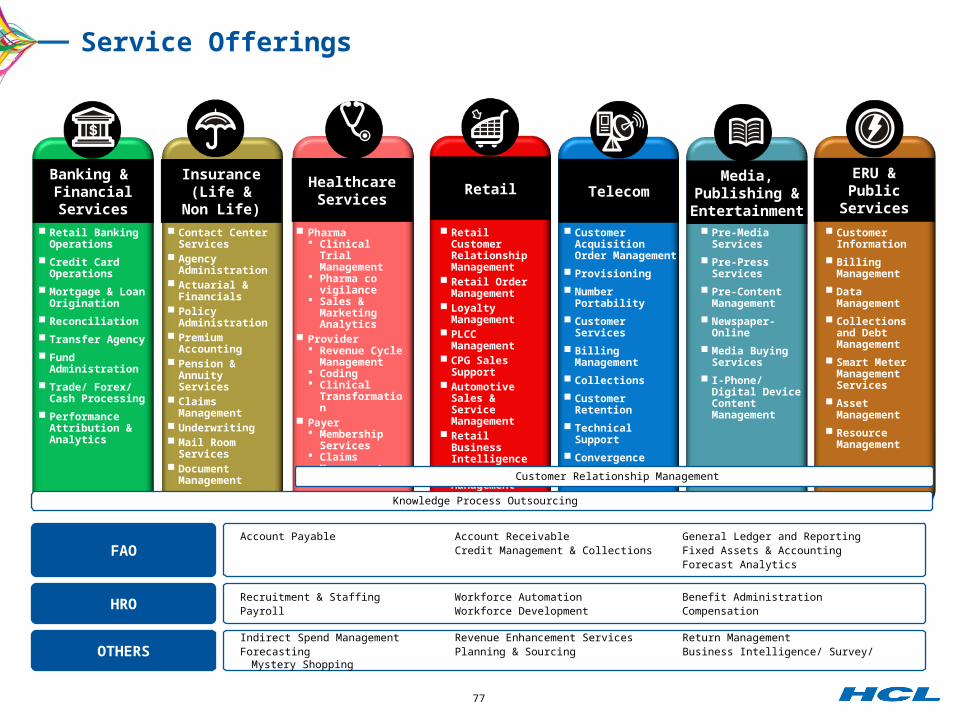

Banking & Financial Services

Retail Banking Operations

Credit Card Operations

Mortgage & Loan Origination

Reconciliation

Transfer Agency

Fund Administration

Trade/ Forex/ Cash Processing

Performance Attribution & Analytics

Insurance(Life &

Non Life) Contact Center

Services Agency

Administration Actuarial &

Financials Policy

Administration Premium

Accounting Pension & Annuity

Services Claims

Management Underwriting Mail Room

Services Document

Management

FAO

HRO

OTHERS

Account Payable Account Receivable General Ledger and ReportingCredit Management & Collections Fixed Assets & Accounting

Forecast Analytics

Recruitment & Staffing Workforce Automation Benefit AdministrationPayroll Workforce Development Compensation

Indirect Spend Management Revenue Enhancement Services Return ManagementForecasting Planning & Sourcing Business Intelligence/ Survey/ Mystery Shopping

Telecom

Customer Acquisition Order Management

Provisioning

Number Portability

Customer Services

Billing Management

Collections

Customer Retention

Technical Support

Convergence

Data Analytics

Retail Customer Relationship Management

Retail Order Management

Loyalty Management

PLCC Management

CPG Sales Support

Automotive Sales & Service Management

Retail Business Intelligence

Category Management

RetailHealthcare Services

Pharma Clinical Trial

Management Pharma co

vigilance Sales &

Marketing Analytics

Provider Revenue Cycle

Management Coding Clinical

Transformation Payer

Membership Services

Claims Management

Customer Information

Billing Management

Data Management

Collections and Debt Management

Smart Meter Management Services

Asset Management

Resource Management

ERU & Public Services

Media, Publishing &

Entertainment Pre-Media

Services

Pre-Press Services

Pre-Content Management

Newspaper-Online

Media Buying Services

I-Phone/ Digital Device Content Management

Knowledge Process Outsourcing

Customer Relationship Management

Service Offerings

78

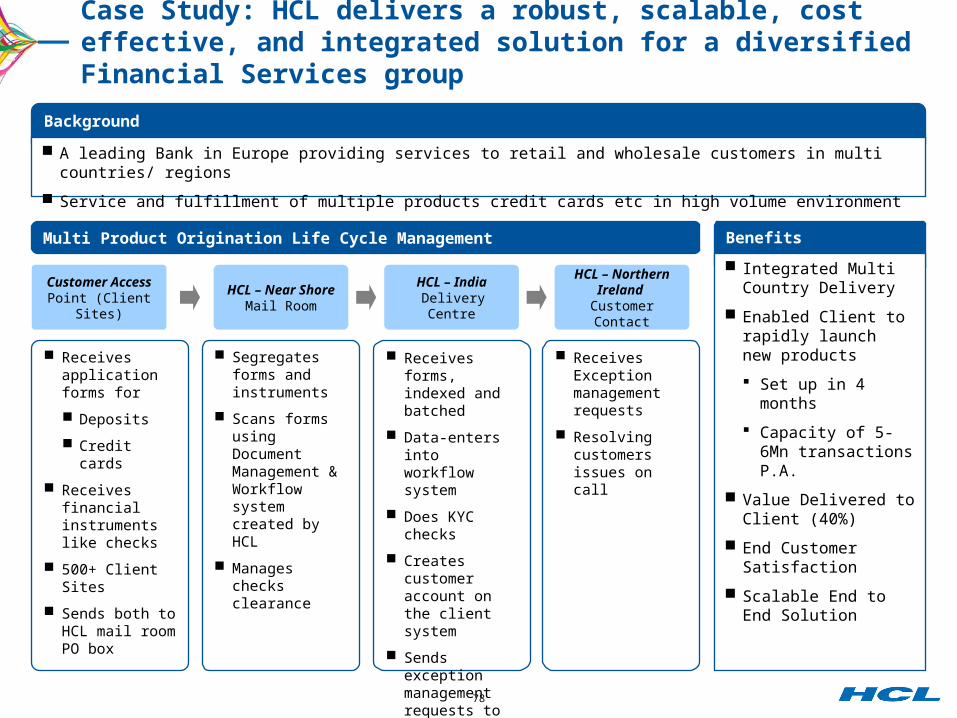

Case Study: HCL delivers a robust, scalable, cost effective, and integrated solution for a diversified Financial Services group

Background

Multi Product Origination Life Cycle Management

Receives application forms for

Deposits

Credit cards

Receives financial instruments like checks

500+ Client Sites

Sends both to HCL mail room PO box

Segregates forms and instruments

Scans forms using Document Management & Workflow system created by HCL

Manages checks clearance

Receives forms, indexed and batched

Data-enters into workflow system

Does KYC checks

Creates customer account on the client system

Sends exception management requests to HCL Ireland site

Receives Exception management requests

Resolving customers issues on call

Benefits

Integrated Multi Country Delivery

Enabled Client to rapidly launch new products

Set up in 4 months

Capacity of 5-6Mn transactions P.A.

Value Delivered to Client (40%)

End Customer Satisfaction

Scalable End to End Solution

A leading Bank in Europe providing services to retail and wholesale customers in multi countries/ regions

Service and fulfillment of multiple products credit cards etc in high volume environment

Customer Access Point (Client Sites)

HCL – Near ShoreMail Room

HCL – India Delivery Centre

HCL – Northern Ireland

Customer Contact

79

HOW CAN I HELP YOU?

Related Documents