© Hamburger Hafen und Logistik AG HAMBURGER HAFEN UND LOGISTIK AG Investor Presentation Sixth German Corporate Conference Munich, 19 September 2017

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

© Hamburger Hafen und Logistik AG

HAMBURGERHAFEN UND LOGISTIK AG

Investor Presentation

Sixth German Corporate Conference

Munich, 19 September 2017

© Hamburger Hafen und Logistik AG

Disclaimer

The facts and information contained herein are as up to date as is reasonably possible and are subject to revision in the future. Neither the Company nor any of its parent

or subsidiary undertakings nor any of such person’s directors, officers, employees or advisors nor any other person makes any representation or warranty, express or

implied as to, and no reliance should be placed on, the accuracy or completeness of the information contained in this presentation. Neither the Company, nor any of its

parents or subsidiary undertakings nor any of their directors, employees and advisors nor any other person shall have any liability whatsoever for loss howsoever arising,

directly or indirectly, from any use of this presentation. The same applies to information contained in other material made available at the presentation.

While all reasonable care has been taken to ensure that the facts stated herein are accurate and that the opinions contained herein are fair and reasonable, this document

is selective in nature. Where any information and statistics are quoted from any external source, such information or statistics should not be interpreted as having been

adopted or endorsed by the Company as being accurate.

This presentation contains forward-looking statements relating to the business, financial performance and results of the Company and/or the industry in which the

Company operates. These statements generally are identified by words such as “believes”, “expects”, “predicts”, “intends”, “projects”, “plans”, “estimates”, “aims”,

“foresees”, “anticipates”, “targets” and similar expressions. The forward-looking statements, including but not limited to assumptions, opinions and views of the Company

for information from third party sources, contained in this presentation are based on current plans, estimates, assumptions and projections and involve uncertainties and

risks. Various factors could cause actual future results, performance or events to differ materially from those described in these statements. The Company does not

represent or guarantee that the assumptions underlying such forward-looking statements are free from errors and the Company does not accept any responsibility for the

future accuracy of the opinions expressed in this presentation. No obligation is assumed to update any forward-looking statements.

By accepting this presentation you acknowledge that you will be solely responsible for your own assessment of the market and the market position of the Company and

that you will conduct your own analysis and be solely responsible for forming your own view of the potential future performance of the Company’s business.

This presentation is not a prospectus and does not constitute an offer or an invitation or solicitation to subscribe for, or purchase, any shares of the Company and neither

this presentation nor anything contained herein shall form the basis of, or be relied on in connection with, any offer or commitment whatsoever.

Sixth German Corporate Conference - Munich, 19 September 2017 2

© Hamburger Hafen und Logistik AG

Agenda

Company Profile and Strategy

Business Update and Financial Performance 1H2017

Outlook 2017

Appendix

3Sixth German Corporate Conference - Munich, 19 September 2017

© Hamburger Hafen und Logistik AG

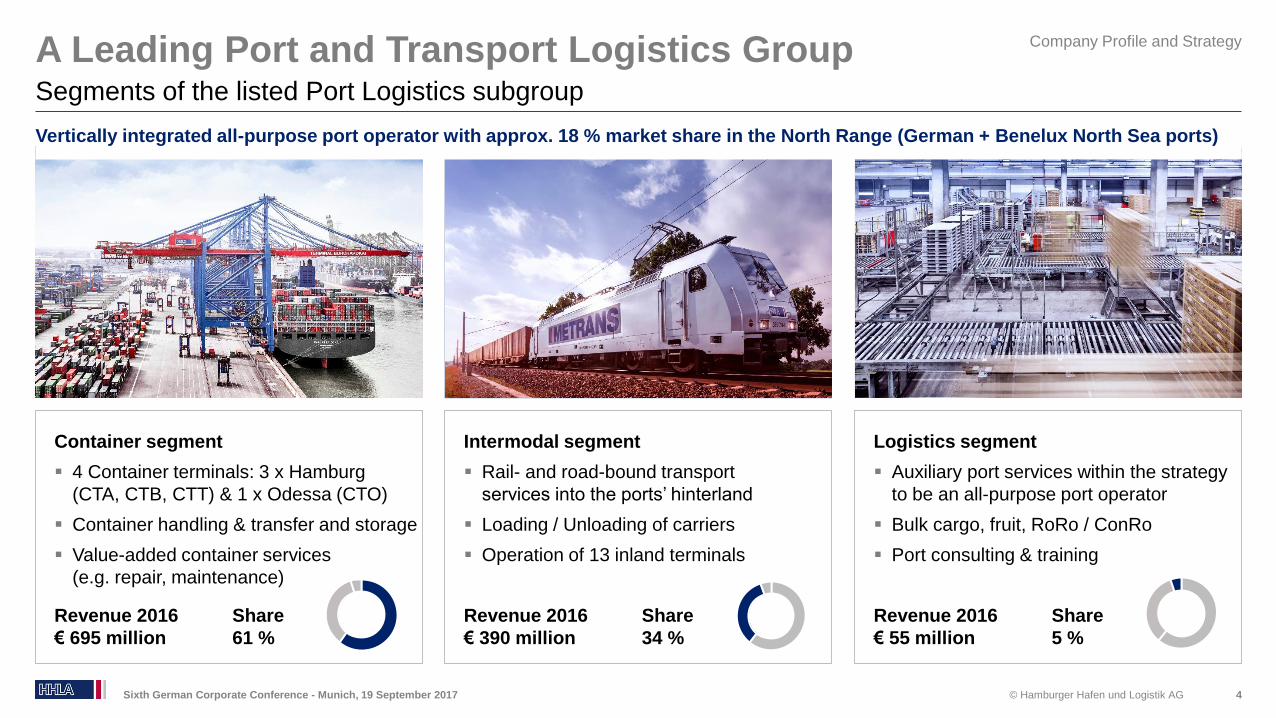

A Leading Port and Transport Logistics Group

4

Segments of the listed Port Logistics subgroup

Company Profile and Strategy

Sixth German Corporate Conference - Munich, 19 September 2017

Logistics segment

Auxiliary port services within the strategy

to be an all-purpose port operator

Bulk cargo, fruit, RoRo / ConRo

Port consulting & training

Revenue 2016 Share

€ 55 million 5 %

Container segment

4 Container terminals: 3 x Hamburg

(CTA, CTB, CTT) & 1 x Odessa (CTO)

Container handling & transfer and storage

Value-added container services

(e.g. repair, maintenance)

Revenue 2016 Share

€ 695 million 61 %

Intermodal segment

Rail- and road-bound transport

services into the ports’ hinterland

Loading / Unloading of carriers

Operation of 13 inland terminals

Revenue 2016 Share

€ 390 million 34 %

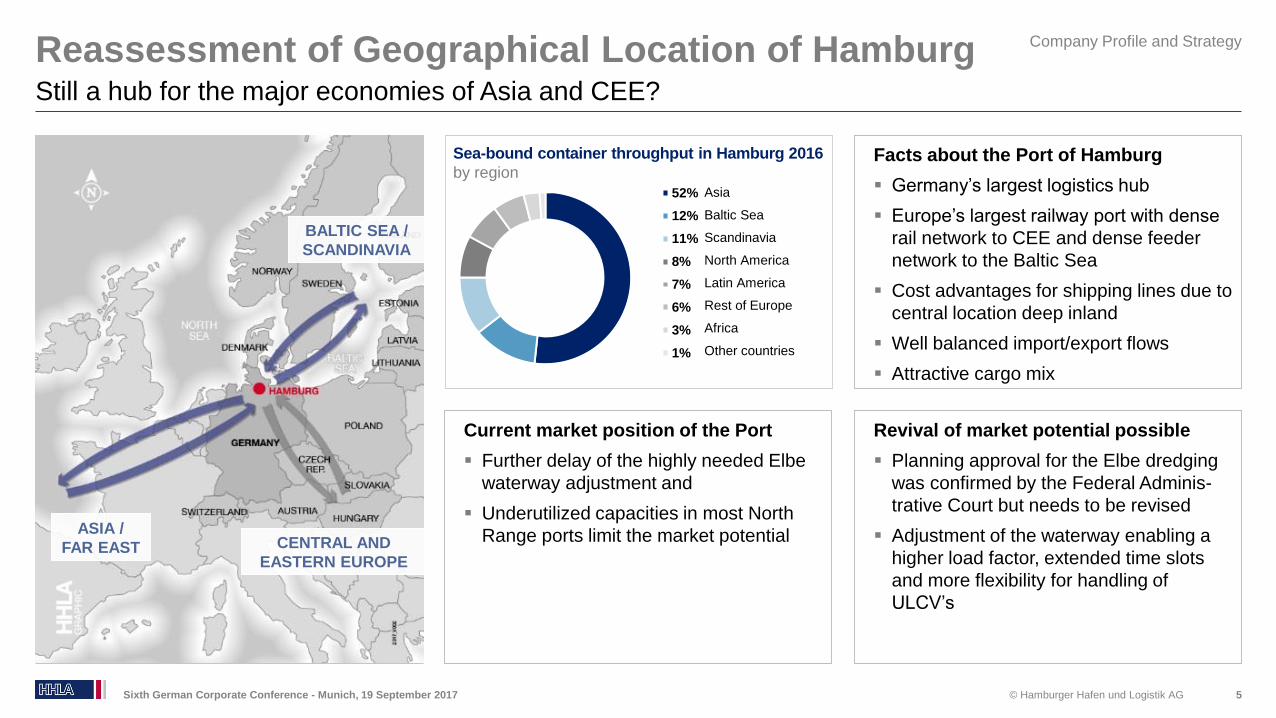

Vertically integrated all-purpose port operator with approx. 18 % market share in the North Range (German + Benelux North Sea ports)

© Hamburger Hafen und Logistik AG

52%

12%

11%

8%

7%

6%

3%

1%

Reassessment of Geographical Location of Hamburg

5

Still a hub for the major economies of Asia and CEE?

Company Profile and Strategy

Sixth German Corporate Conference - Munich, 19 September 2017

Current market position of the Port

Further delay of the highly needed Elbe

waterway adjustment and

Underutilized capacities in most North

Range ports limit the market potential

Facts about the Port of Hamburg

Germany’s largest logistics hub

Europe’s largest railway port with dense

rail network to CEE and dense feeder

network to the Baltic Sea

Cost advantages for shipping lines due to

central location deep inland

Well balanced import/export flows

Attractive cargo mix

Revival of market potential possible

Planning approval for the Elbe dredging

was confirmed by the Federal Adminis-

trative Court but needs to be revised

Adjustment of the waterway enabling a

higher load factor, extended time slots

and more flexibility for handling of

ULCV’s

BALTIC SEA /

SCANDINAVIA

CENTRAL AND

EASTERN EUROPE

ASIA /

FAR EAST

Sea-bound container throughput in Hamburg 2016

by region

Asia

Baltic Sea

Scandinavia

North America

Latin America

Rest of Europe

Africa

Other countries

© Hamburger Hafen und Logistik AG

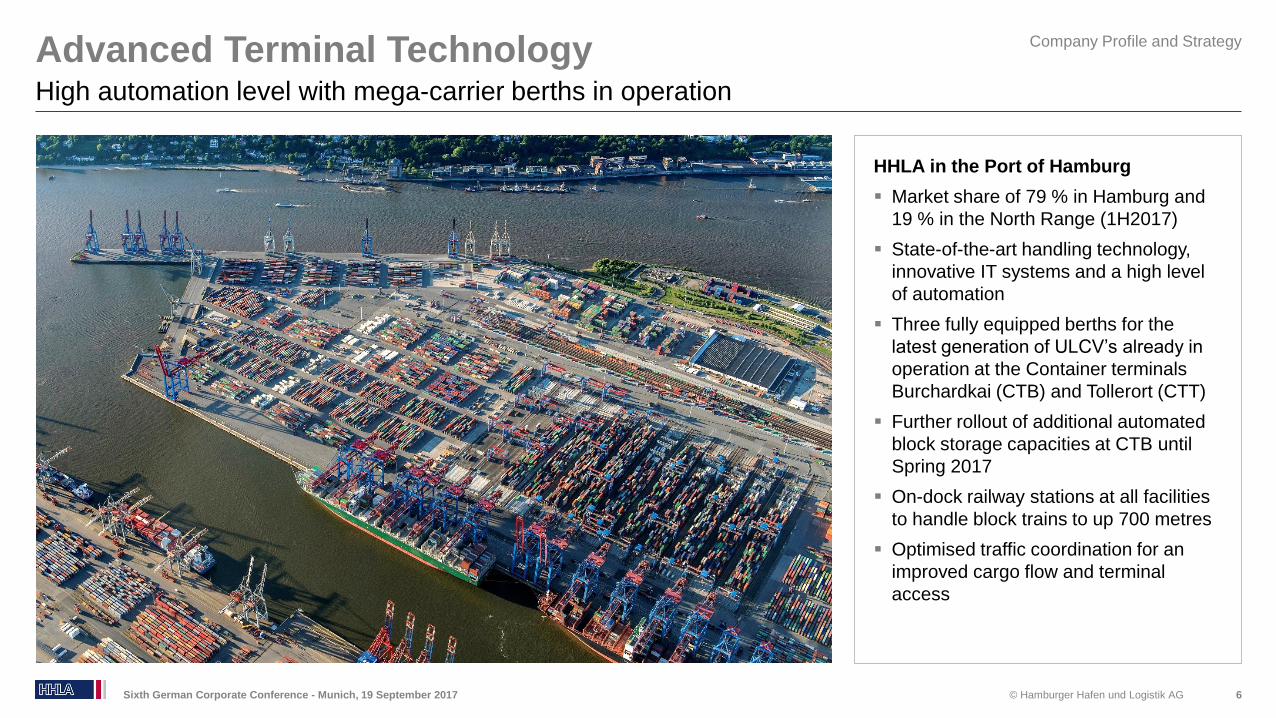

Advanced Terminal Technology

6

High automation level with mega-carrier berths in operation

Sixth German Corporate Conference - Munich, 19 September 2017

HHLA in the Port of Hamburg

Market share of 79 % in Hamburg and

19 % in the North Range (1H2017)

State-of-the-art handling technology,

innovative IT systems and a high level

of automation

Three fully equipped berths for the

latest generation of ULCV’s already in

operation at the Container terminals

Burchardkai (CTB) and Tollerort (CTT)

Further rollout of additional automated

block storage capacities at CTB until

Spring 2017

On-dock railway stations at all facilities

to handle block trains to up 700 metres

Optimised traffic coordination for an

improved cargo flow and terminal

access

Company Profile and Strategy

© Hamburger Hafen und Logistik AG

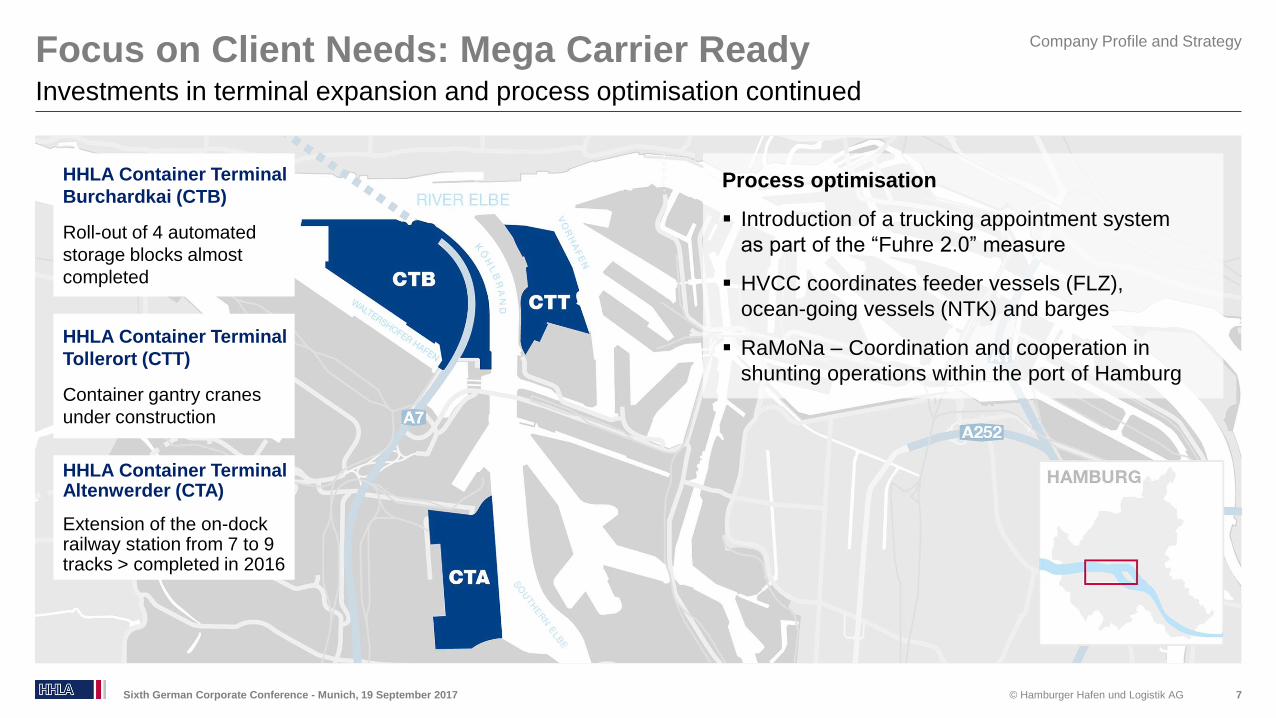

Focus on Client Needs: Mega Carrier Ready

7

Investments in terminal expansion and process optimisation continued

Sixth German Corporate Conference - Munich, 19 September 2017

HHLA Container Terminal Altenwerder (CTA)

Extension of the on-dock railway station from 7 to 9 tracks > completed in 2016

HHLA Container Terminal

Burchardkai (CTB)

Roll-out of 4 automated

storage blocks almost

completed

HHLA Container Terminal

Tollerort (CTT)

Container gantry cranes

under construction

Process optimisation

Introduction of a trucking appointment system

as part of the “Fuhre 2.0” measure

HVCC coordinates feeder vessels (FLZ),

ocean-going vessels (NTK) and barges

RaMoNa – Coordination and cooperation in

shunting operations within the port of Hamburg

Company Profile and Strategy

© Hamburger Hafen und Logistik AG

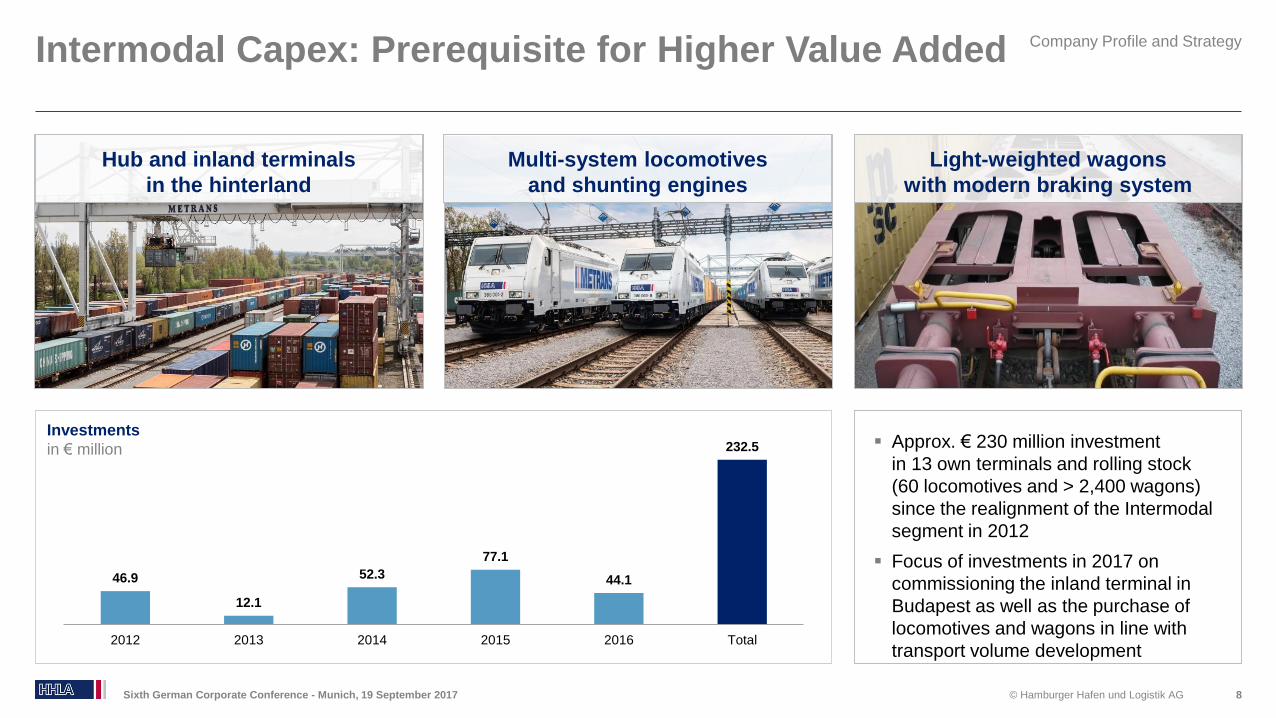

46.9

12.1

52.3

77.1

44.1

232.5

2012 2013 2014 2015 2016 Total

Intermodal Capex: Prerequisite for Higher Value Added

8

Company Profile and Strategy

Sixth German Corporate Conference - Munich, 19 September 2017

Approx. € 230 million investment

in 13 own terminals and rolling stock

(60 locomotives and > 2,400 wagons)

since the realignment of the Intermodal

segment in 2012

Focus of investments in 2017 on

commissioning the inland terminal in

Budapest as well as the purchase of

locomotives and wagons in line with

transport volume development

Hub and inland terminals

in the hinterland

Multi-system locomotives

and shunting engines

Light-weighted wagons

with modern braking system

Investments

in € million

© Hamburger Hafen und Logistik AG

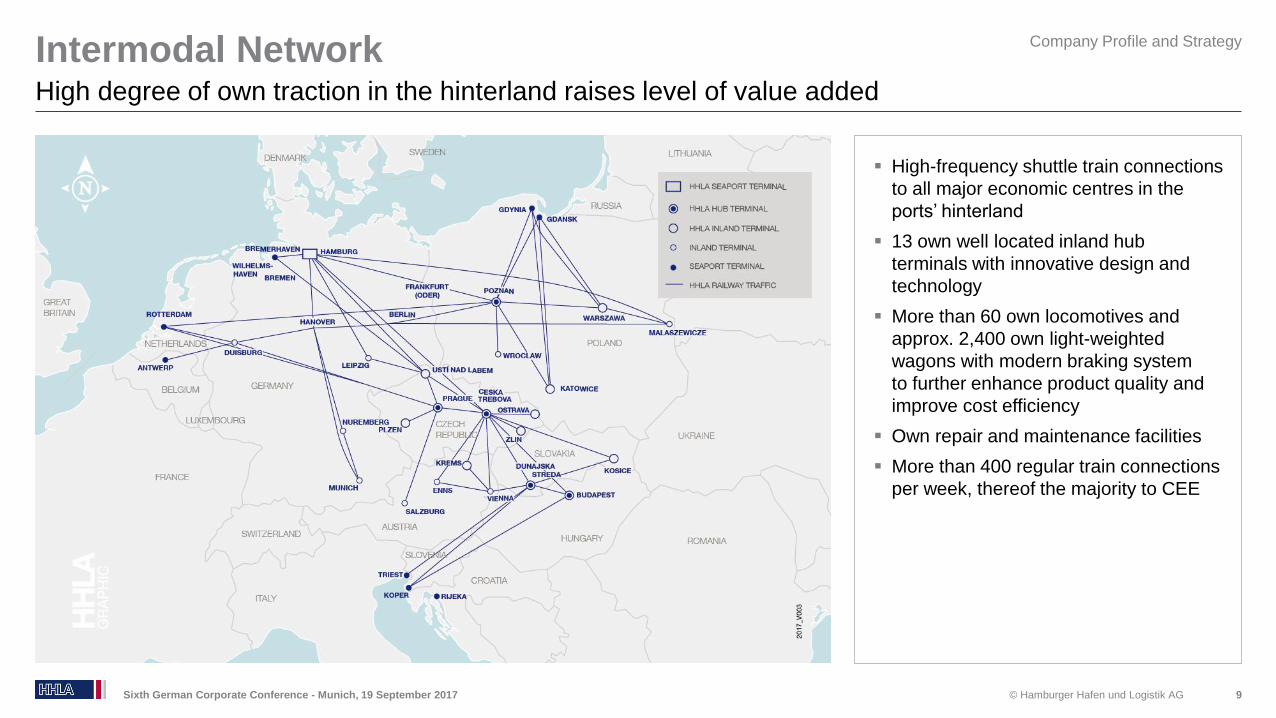

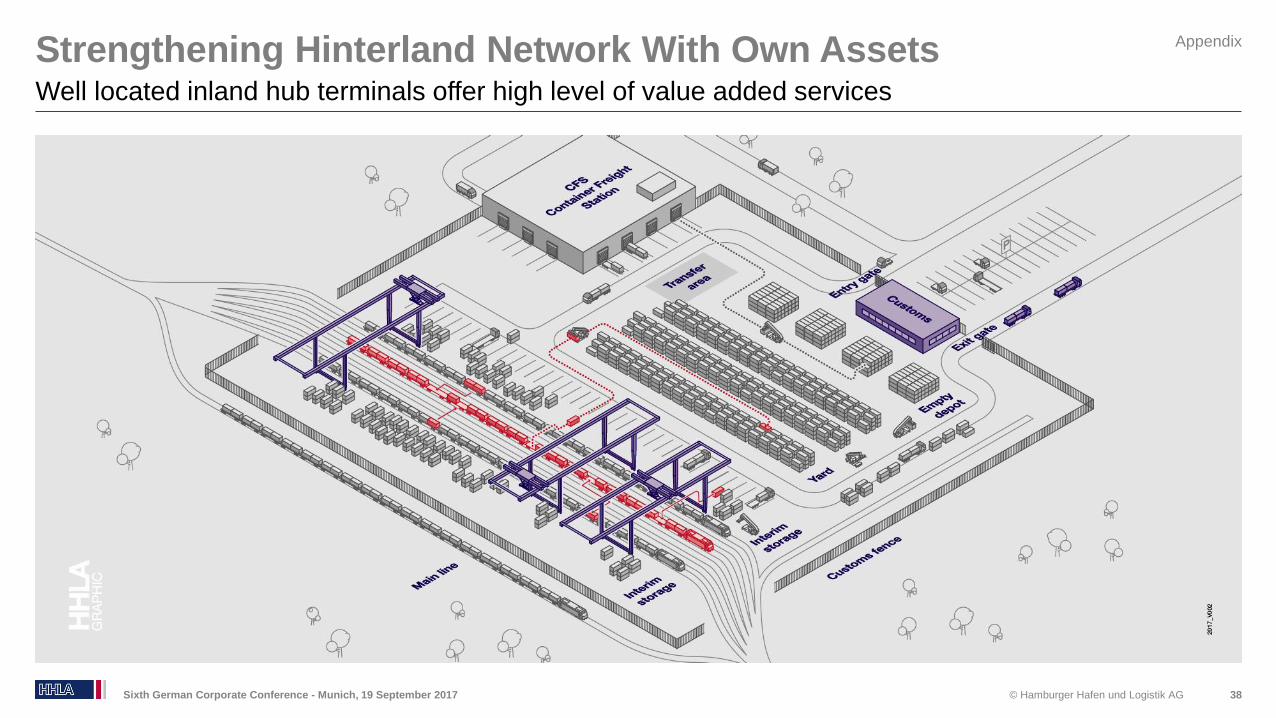

Intermodal Network

9

High degree of own traction in the hinterland raises level of value added

Company Profile and Strategy

Sixth German Corporate Conference - Munich, 19 September 2017

High-frequency shuttle train connections

to all major economic centres in the

ports’ hinterland

13 own well located inland hub

terminals with innovative design and

technology

More than 60 own locomotives and

approx. 2,400 own light-weighted

wagons with modern braking system

to further enhance product quality and

improve cost efficiency

Own repair and maintenance facilities

More than 400 regular train connections

per week, thereof the majority to CEE

© Hamburger Hafen und Logistik AG

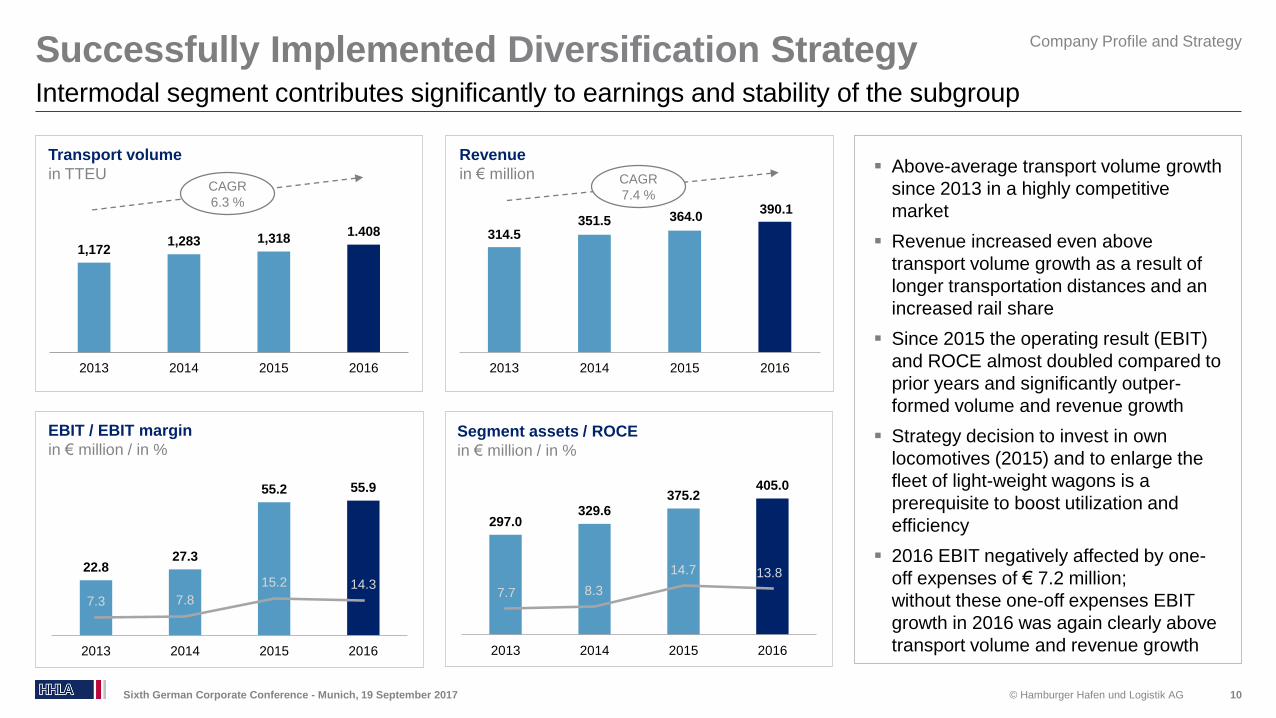

Successfully Implemented Diversification Strategy

10

Intermodal segment contributes significantly to earnings and stability of the subgroup

Company Profile and Strategy

Sixth German Corporate Conference - Munich, 19 September 2017

Above-average transport volume growth

since 2013 in a highly competitive

market

Revenue increased even above

transport volume growth as a result of

longer transportation distances and an

increased rail share

Since 2015 the operating result (EBIT)

and ROCE almost doubled compared to

prior years and significantly outper-

formed volume and revenue growth

Strategy decision to invest in own

locomotives (2015) and to enlarge the

fleet of light-weight wagons is a

prerequisite to boost utilization and

efficiency

2016 EBIT negatively affected by one-

off expenses of € 7.2 million;

without these one-off expenses EBIT

growth in 2016 was again clearly above

transport volume and revenue growth

22.827.3

55.2 55.9

7.3 7.8

15.2 14.3

2013 2014 2015 2016

EBIT / EBIT margin

in € million / in %

314.5351.5 364.0

390.1

2013 2014 2015 2016

Revenue

in € million

1,1721,283 1,318

1.408

2013 2014 2015 2016

Transport volume

in TTEU

297.0329.6

375.2405.0

2013 2014 2015 2016

Segment assets / ROCE

in € million / in %

CAGR

6.3 %

CAGR

7.4 %

7.7 8.3

14.7 13.8

© Hamburger Hafen und Logistik AG

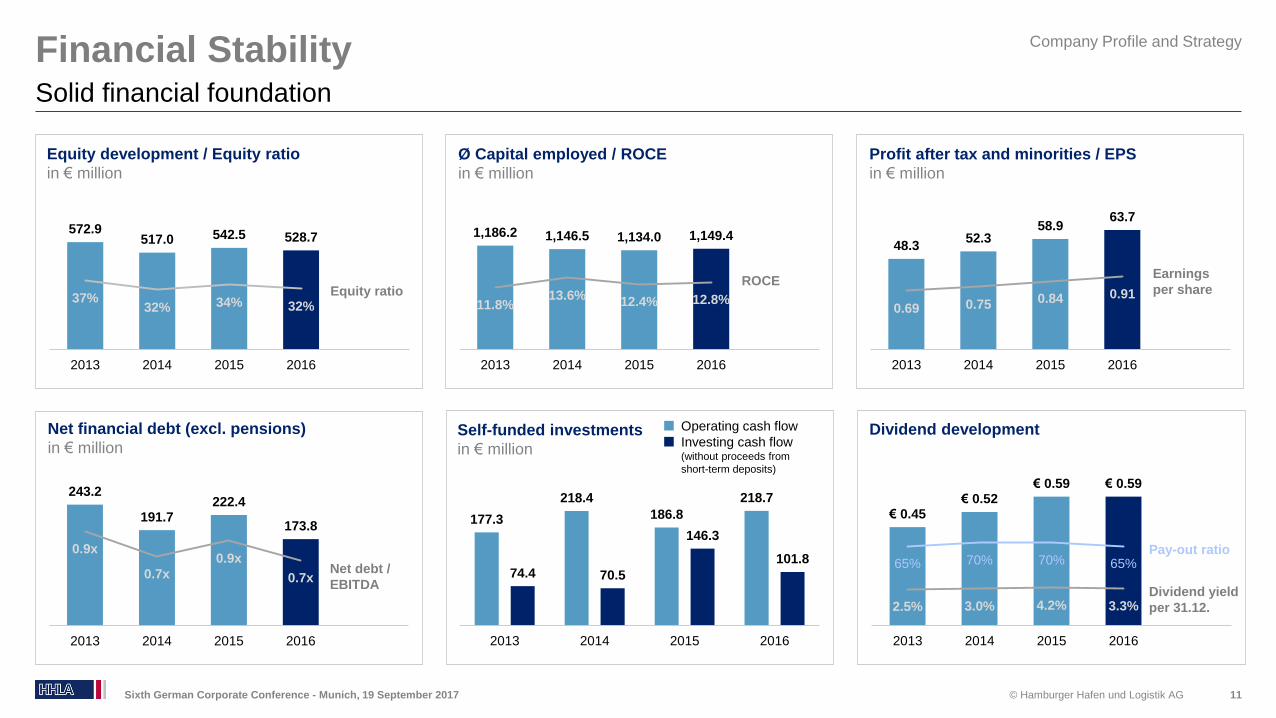

Financial Stability

Sixth German Corporate Conference - Munich, 19 September 2017 11

Solid financial foundation

48.352.3

58.963.7

0.69 0.75 0.84 0.91

2013 2014 2015 2016

Profit after tax and minorities / EPS

in € million

572.9517.0 542.5 528.7

37%32% 34% 32%

2013 2014 2015 2016

Equity development / Equity ratio

in € million

177.3

218.4

186.8

218.7

74.4 70.5

146.3

101.8

2013 2014 2015 2016

Self-funded investments

in € million

243.2

191.7222.4

173.8

0.9x

0.7x

0.9x

0.7x

2013 2014 2015 2016

Net financial debt (excl. pensions)

in € million

Equity ratio

Operating cash flow

Investing cash flow (without proceeds from

short-term deposits)

Earnings

per share

Net debt /

EBITDA

€ 0.45€ 0.52

€ 0.59 € 0.59

2.5% 3.0% 4.2% 3.3%

65% 70% 70% 65%

2013 2014 2015 2016

Dividend development

Dividend yield

per 31.12.

1,186.2 1,146.5 1,134.0 1,149.4

11.8%13.6%

12.4% 12.8%

2013 2014 2015 2016

Ø Capital employed / ROCE

in € million

ROCE

Pay-out ratio

Company Profile and Strategy

© Hamburger Hafen und Logistik AG

Agenda

Company Profile and Strategy

Business Update and Financial Performance 1H2017

Outlook 2017

Appendix

12Sixth German Corporate Conference - Munich, 19 September 2017

© Hamburger Hafen und Logistik AG

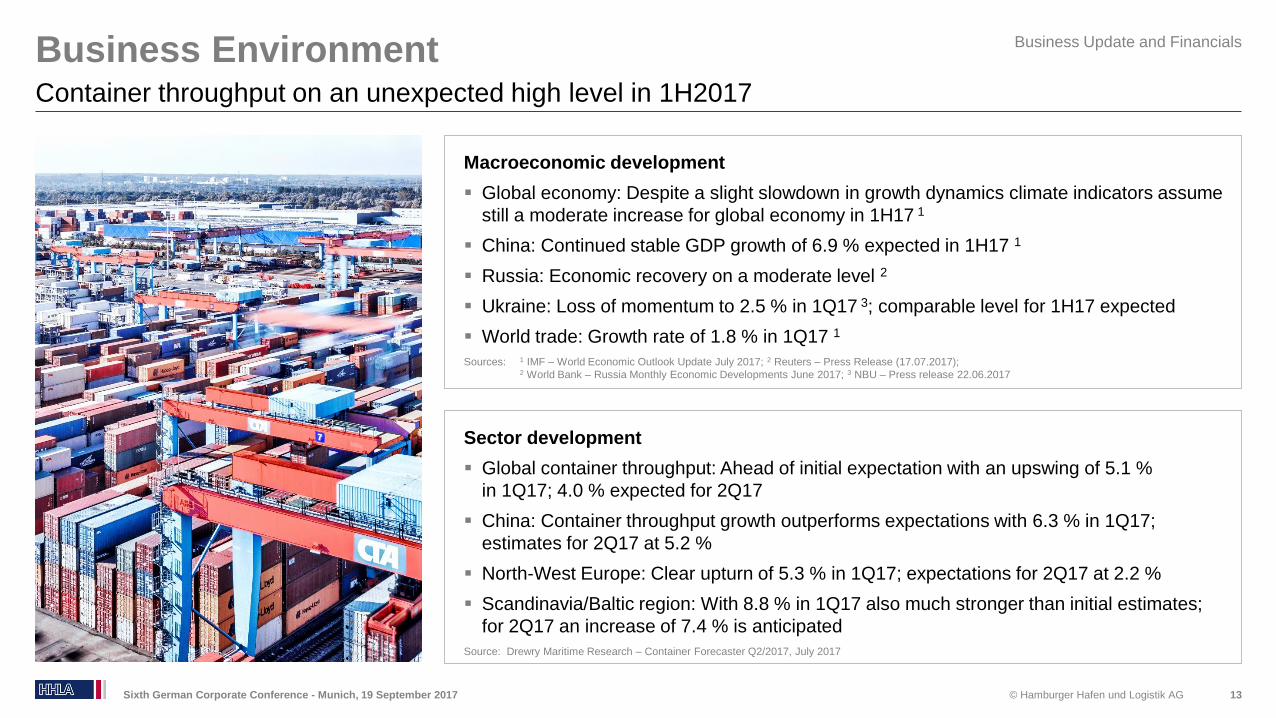

Macroeconomic development

Global economy: Despite a slight slowdown in growth dynamics climate indicators assume

still a moderate increase for global economy in 1H17 1

China: Continued stable GDP growth of 6.9 % expected in 1H17 1

Russia: Economic recovery on a moderate level 2

Ukraine: Loss of momentum to 2.5 % in 1Q17 3; comparable level for 1H17 expected

World trade: Growth rate of 1.8 % in 1Q17 1

Sources: 1 IMF – World Economic Outlook Update July 2017; 2 Reuters – Press Release (17.07.2017); 2 World Bank – Russia Monthly Economic Developments June 2017; 3 NBU – Press release 22.06.2017

Business Environment

13

Container throughput on an unexpected high level in 1H2017

Sixth German Corporate Conference - Munich, 19 September 2017

Sector development

Global container throughput: Ahead of initial expectation with an upswing of 5.1 %

in 1Q17; 4.0 % expected for 2Q17

China: Container throughput growth outperforms expectations with 6.3 % in 1Q17;

estimates for 2Q17 at 5.2 %

North-West Europe: Clear upturn of 5.3 % in 1Q17; expectations for 2Q17 at 2.2 %

Scandinavia/Baltic region: With 8.8 % in 1Q17 also much stronger than initial estimates;

for 2Q17 an increase of 7.4 % is anticipated

Source: Drewry Maritime Research – Container Forecaster Q2/2017, July 2017

Business Update and Financials

© Hamburger Hafen und Logistik AG

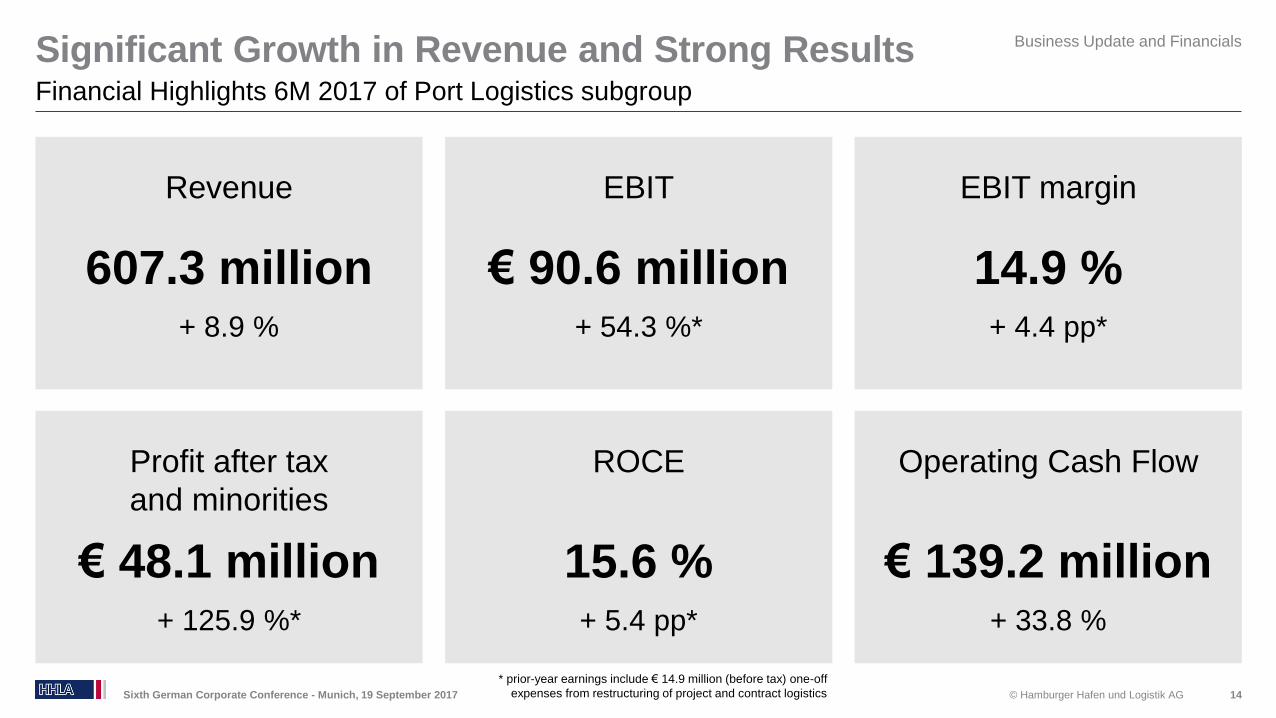

Significant Growth in Revenue and Strong Results

14

Financial Highlights 6M 2017 of Port Logistics subgroup

Business Update and Financials

Sixth German Corporate Conference - Munich, 19 September 2017

Profit after tax

and minorities

€ 48.1 million+ 125.9 %*

Revenue

607.3 million+ 8.9 %

EBIT

€ 90.6 million+ 54.3 %*

EBIT margin

14.9 %+ 4.4 pp*

* prior-year earnings include € 14.9 million (before tax) one-off

expenses from restructuring of project and contract logistics

ROCE

15.6 %+ 5.4 pp*

Operating Cash Flow

€ 139.2 million+ 33.8 %

© Hamburger Hafen und Logistik AG

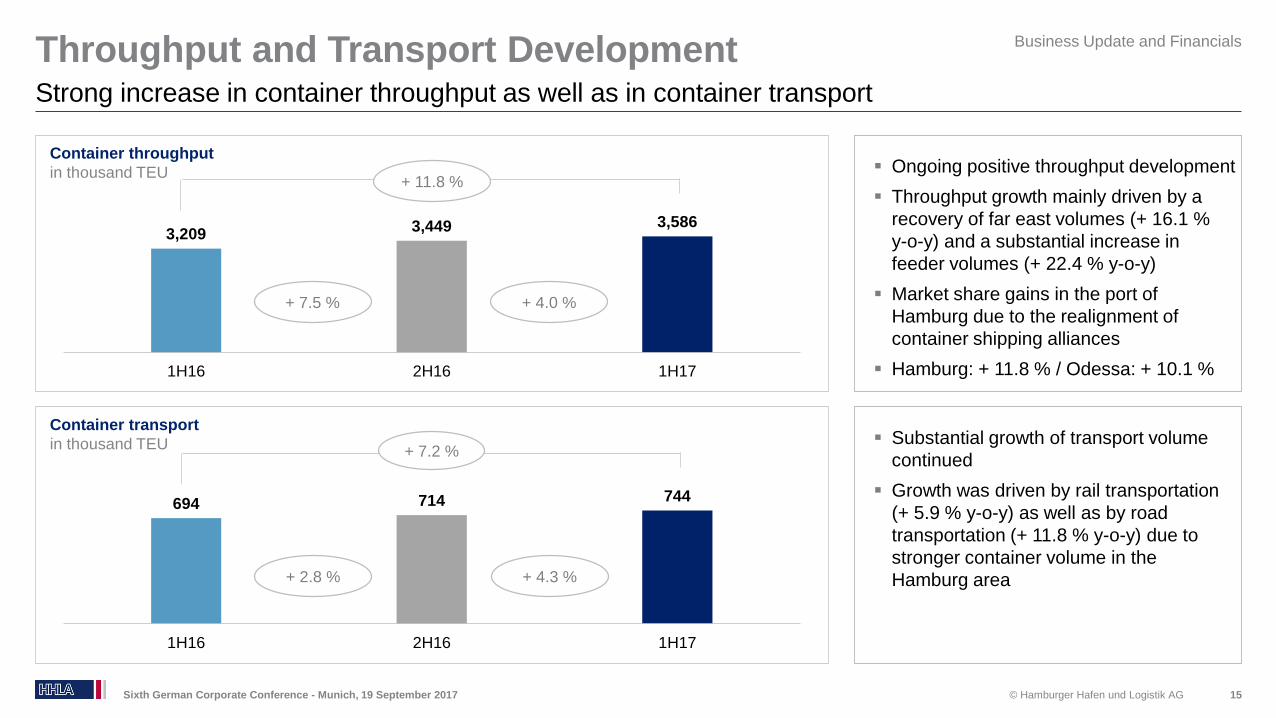

Throughput and Transport Development

15

Strong increase in container throughput as well as in container transport

Business Update and Financials

Sixth German Corporate Conference - Munich, 19 September 2017

Ongoing positive throughput development

Throughput growth mainly driven by a

recovery of far east volumes (+ 16.1 %

y-o-y) and a substantial increase in

feeder volumes (+ 22.4 % y-o-y)

Market share gains in the port of

Hamburg due to the realignment of

container shipping alliances

Hamburg: + 11.8 % / Odessa: + 10.1 %

3,2093,449 3,586

1H16 2H16 1H17

Container throughput

in thousand TEU+ 11.8 %

694 714 744

1H16 2H16 1H17

Container transport

in thousand TEU Substantial growth of transport volume

continued

Growth was driven by rail transportation

(+ 5.9 % y-o-y) as well as by road

transportation (+ 11.8 % y-o-y) due to

stronger container volume in the

Hamburg area

+ 7.5 % + 4.0 %

+ 2.8 % + 4.3 %

+ 7.2 %

© Hamburger Hafen und Logistik AG

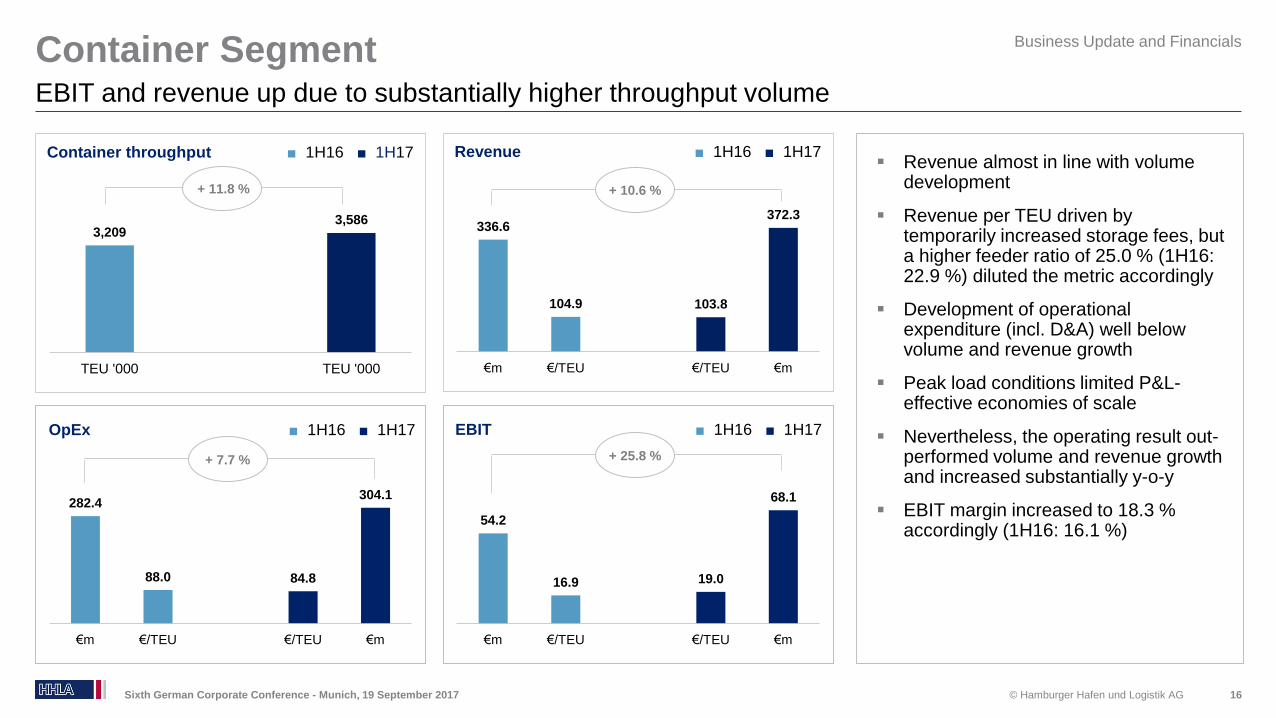

282.4

88.0 84.8

304.1

€m €/TEU €/TEU €m

54.2

16.9 19.0

68.1

€m €/TEU €/TEU €m

3,2093,586

TEU '000 TEU '000

Revenue almost in line with volume development

Revenue per TEU driven by temporarily increased storage fees, but a higher feeder ratio of 25.0 % (1H16: 22.9 %) diluted the metric accordingly

Development of operational expenditure (incl. D&A) well below volume and revenue growth

Peak load conditions limited P&L-effective economies of scale

Nevertheless, the operating result out-performed volume and revenue growth and increased substantially y-o-y

EBIT margin increased to 18.3 % accordingly (1H16: 16.1 %)

Container Segment

Sixth German Corporate Conference - Munich, 19 September 2017 16

EBIT and revenue up due to substantially higher throughput volume

EBIT ■ 1H16 ■ 1H17

Container throughput ■ 1H16 ■ 1H17

+ 11.8 %

+ 7.7 % + 25.8 %

OpEx ■ 1H16 ■ 1H17

336.6

104.9 103.8

372.3

€m €/TEU €/TEU €m

Revenue ■ 1H16 ■ 1H17

+ 10.6 %

Business Update and Financials

© Hamburger Hafen und Logistik AG

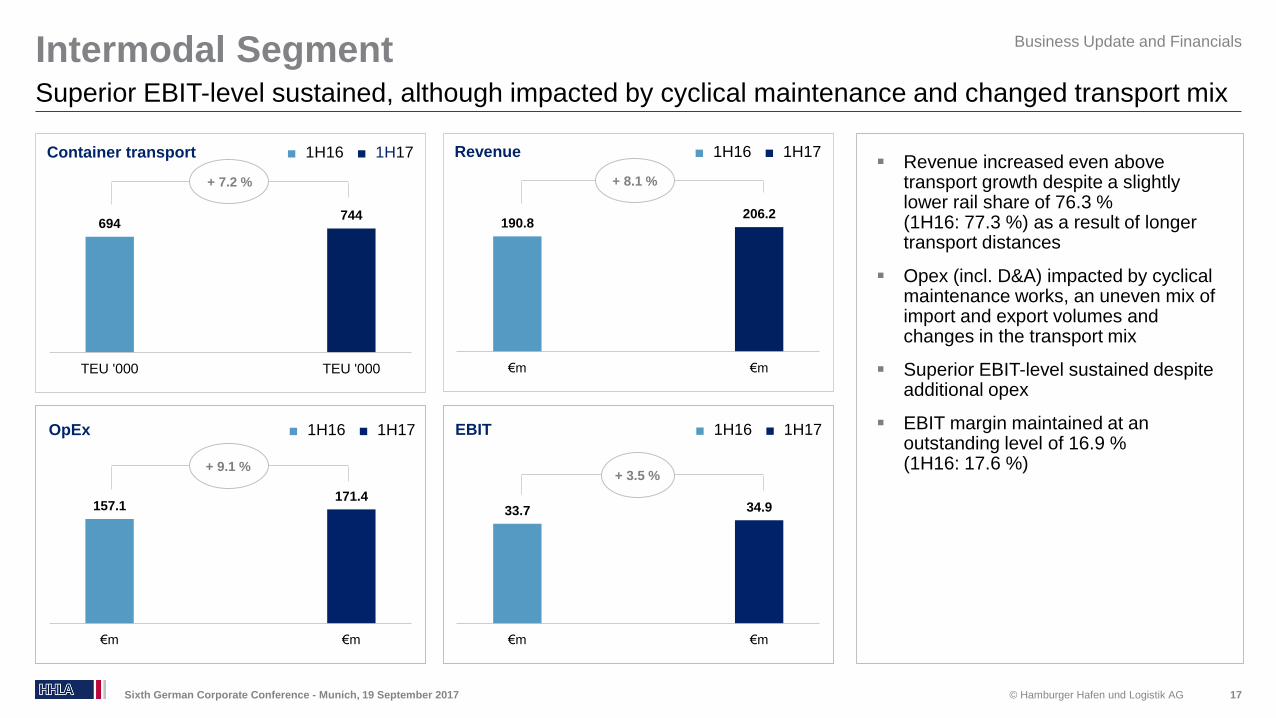

157.1171.4

€m €m

33.7 34.9

€m €m

694744

TEU '000 TEU '000

Revenue increased even above transport growth despite a slightly lower rail share of 76.3 % (1H16: 77.3 %) as a result of longer transport distances

Opex (incl. D&A) impacted by cyclical maintenance works, an uneven mix of import and export volumes and changes in the transport mix

Superior EBIT-level sustained despite additional opex

EBIT margin maintained at an outstanding level of 16.9 % (1H16: 17.6 %)

Intermodal Segment

Sixth German Corporate Conference - Munich, 19 September 2017 17

Superior EBIT-level sustained, although impacted by cyclical maintenance and changed transport mix

EBIT ■ 1H16 ■ 1H17

Business Update and Financials

Container transport ■ 1H16 ■ 1H17

+ 7.2 %

+ 9.1 %+ 3.5 %

OpEx ■ 1H16 ■ 1H17

190.8206.2

€m €m

Revenue ■ 1H16 ■ 1H17

+ 8.1 %

© Hamburger Hafen und Logistik AG

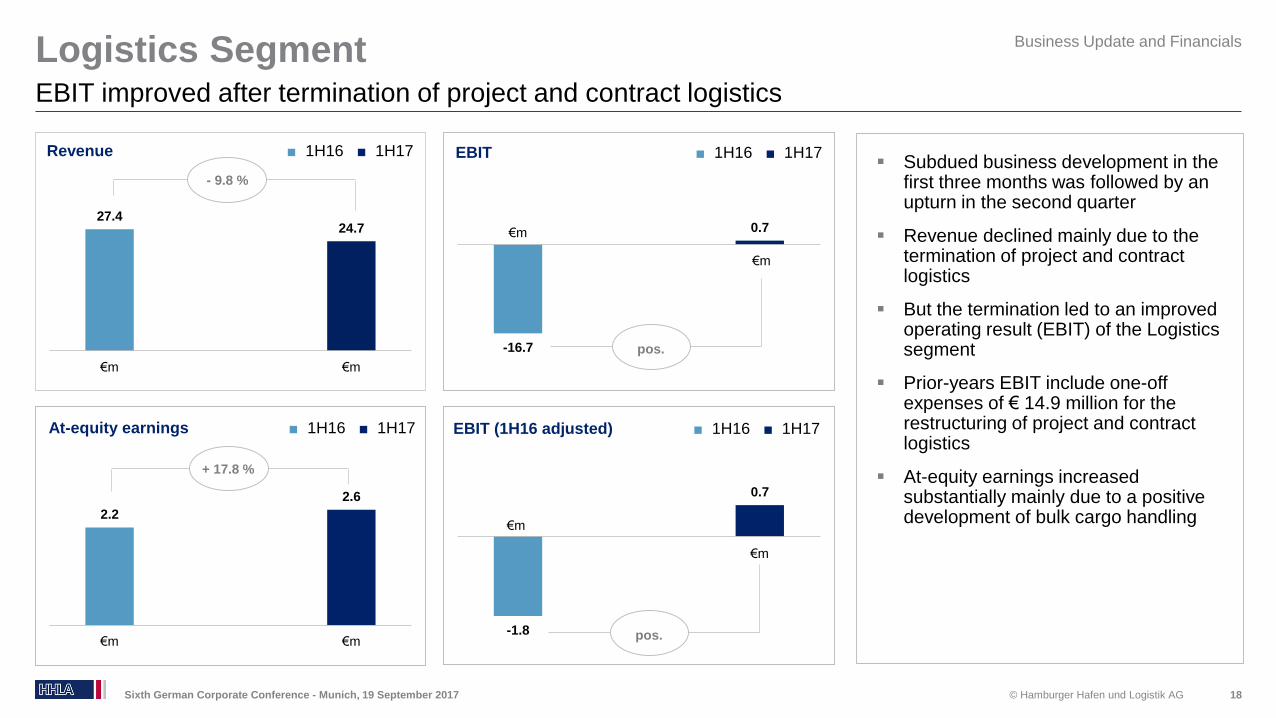

2.2

2.6

€m €m

-16.7

0.7

Subdued business development in the first three months was followed by an upturn in the second quarter

Revenue declined mainly due to the termination of project and contract logistics

But the termination led to an improved operating result (EBIT) of the Logistics segment

Prior-years EBIT include one-off expenses of € 14.9 million for the restructuring of project and contract logistics

At-equity earnings increased substantially mainly due to a positive development of bulk cargo handling

Logistics Segment

Sixth German Corporate Conference - Munich, 19 September 2017 18

EBIT improved after termination of project and contract logistics

EBIT ■ 1H16 ■ 1H17

Business Update and Financials

+ 17.8 %

pos.

At-equity earnings ■ 1H16 ■ 1H17

27.424.7

€m €m

Revenue ■ 1H16 ■ 1H17

- 9.8 %

€m

€m

-1.8

0.7

EBIT (1H16 adjusted) ■ 1H16 ■ 1H17

pos.

€m

€m

© Hamburger Hafen und Logistik AG

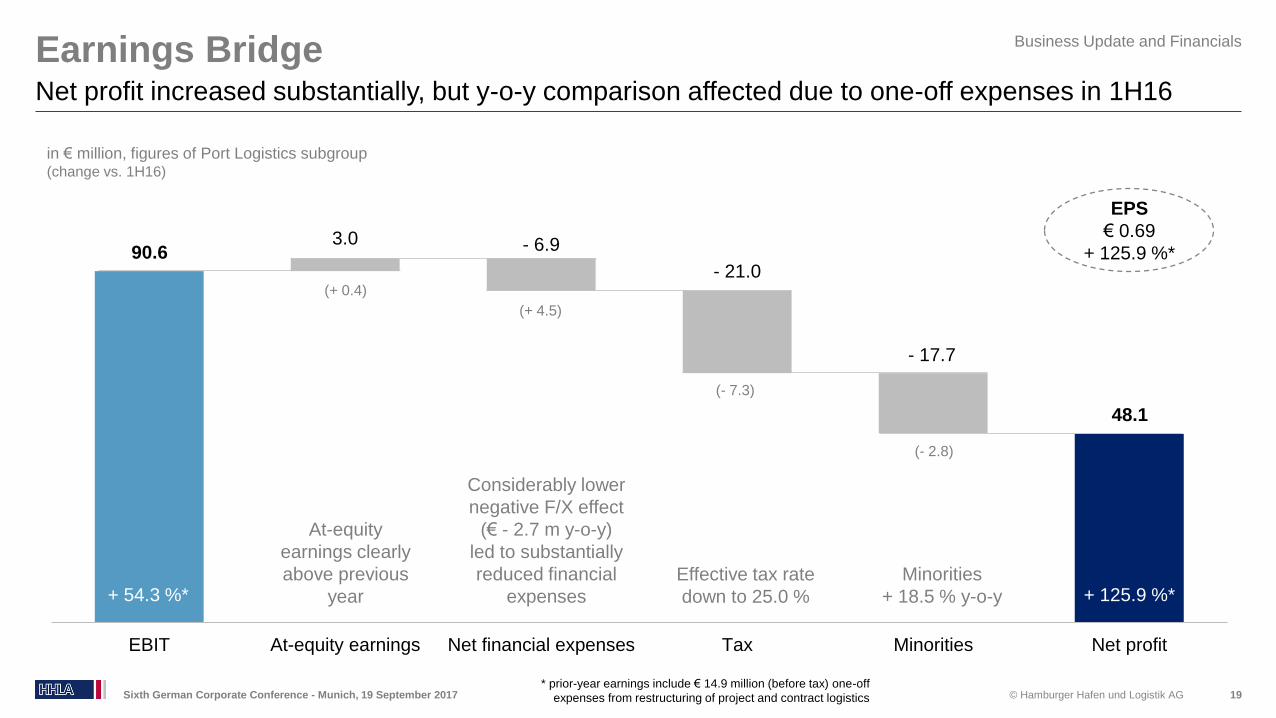

Earnings Bridge

19

Net profit increased substantially, but y-o-y comparison affected due to one-off expenses in 1H16

Business Update and Financials

Sixth German Corporate Conference - Munich, 19 September 2017

90.63.0 - 6.9

- 21.0

- 17.7

48.1

EBIT At-equity earnings Net financial expenses Tax Minorities Net profit

EPS

€ 0.69

+ 125.9 %*

in € million, figures of Port Logistics subgroup(change vs. 1H16)

(+ 0.4)

(+ 4.5)

(- 7.3)

(- 2.8)

At-equity

earnings clearly

above previous

year

Considerably lower

negative F/X effect

(€ - 2.7 m y-o-y)

led to substantially

reduced financial

expenses

Effective tax rate

down to 25.0 %

Minorities

+ 18.5 % y-o-y+ 54.3 %* + 125.9 %*

* prior-year earnings include € 14.9 million (before tax) one-off

expenses from restructuring of project and contract logistics

© Hamburger Hafen und Logistik AG

Agenda

Company Profile and Strategy

Business Update and Financial Performance 1H2017

Outlook 2017

Appendix

20Sixth German Corporate Conference - Munich, 19 September 2017

© Hamburger Hafen und Logistik AG

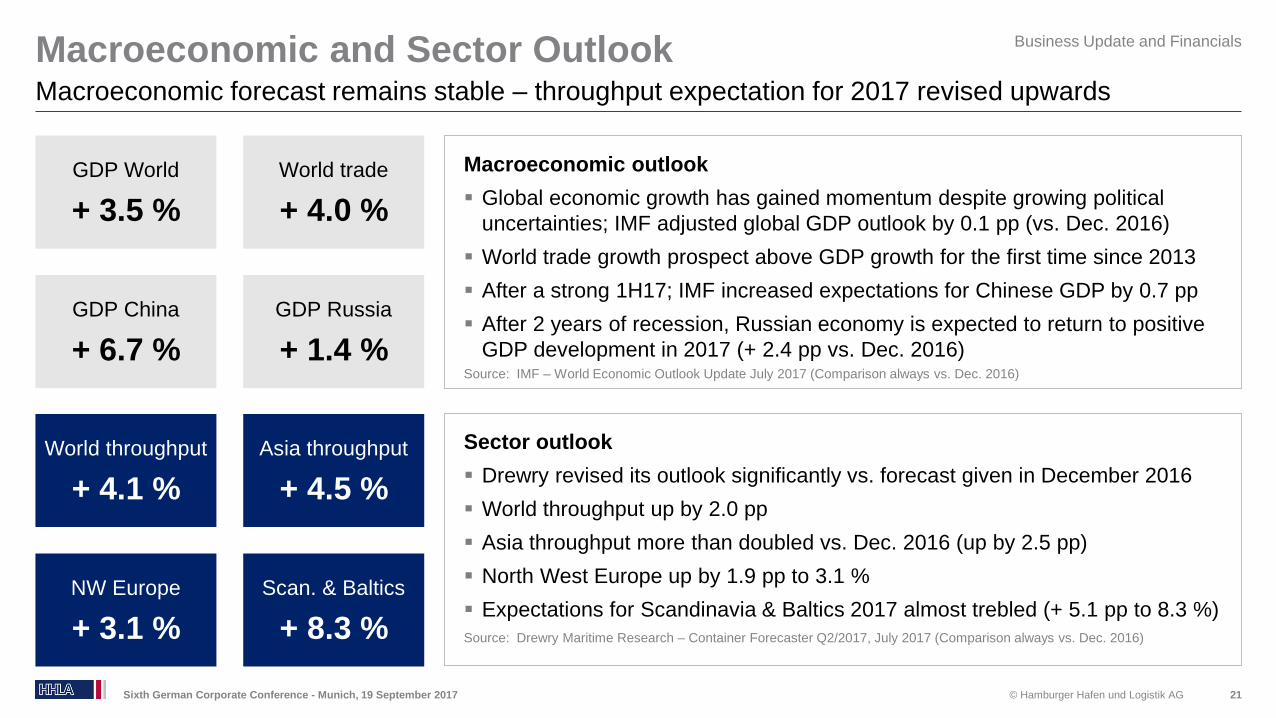

Macroeconomic outlook

Global economic growth has gained momentum despite growing political

uncertainties; IMF adjusted global GDP outlook by 0.1 pp (vs. Dec. 2016)

World trade growth prospect above GDP growth for the first time since 2013

After a strong 1H17; IMF increased expectations for Chinese GDP by 0.7 pp

After 2 years of recession, Russian economy is expected to return to positive

GDP development in 2017 (+ 2.4 pp vs. Dec. 2016)Source: IMF – World Economic Outlook Update July 2017 (Comparison always vs. Dec. 2016)

Macroeconomic and Sector Outlook

21

Macroeconomic forecast remains stable – throughput expectation for 2017 revised upwards

Business Update and Financials

Sixth German Corporate Conference - Munich, 19 September 2017

Sector outlook

Drewry revised its outlook significantly vs. forecast given in December 2016

World throughput up by 2.0 pp

Asia throughput more than doubled vs. Dec. 2016 (up by 2.5 pp)

North West Europe up by 1.9 pp to 3.1 %

Expectations for Scandinavia & Baltics 2017 almost trebled (+ 5.1 pp to 8.3 %)

Source: Drewry Maritime Research – Container Forecaster Q2/2017, July 2017 (Comparison always vs. Dec. 2016)

GDP China

+ 6.7 %

GDP Russia

+ 1.4 %

GDP World

+ 3.5 %

World trade

+ 4.0 %

NW Europe

+ 3.1 %

Scan. & Baltics

+ 8.3 %

World throughput

+ 4.1 %

Asia throughput

+ 4.5 %

© Hamburger Hafen und Logistik AG

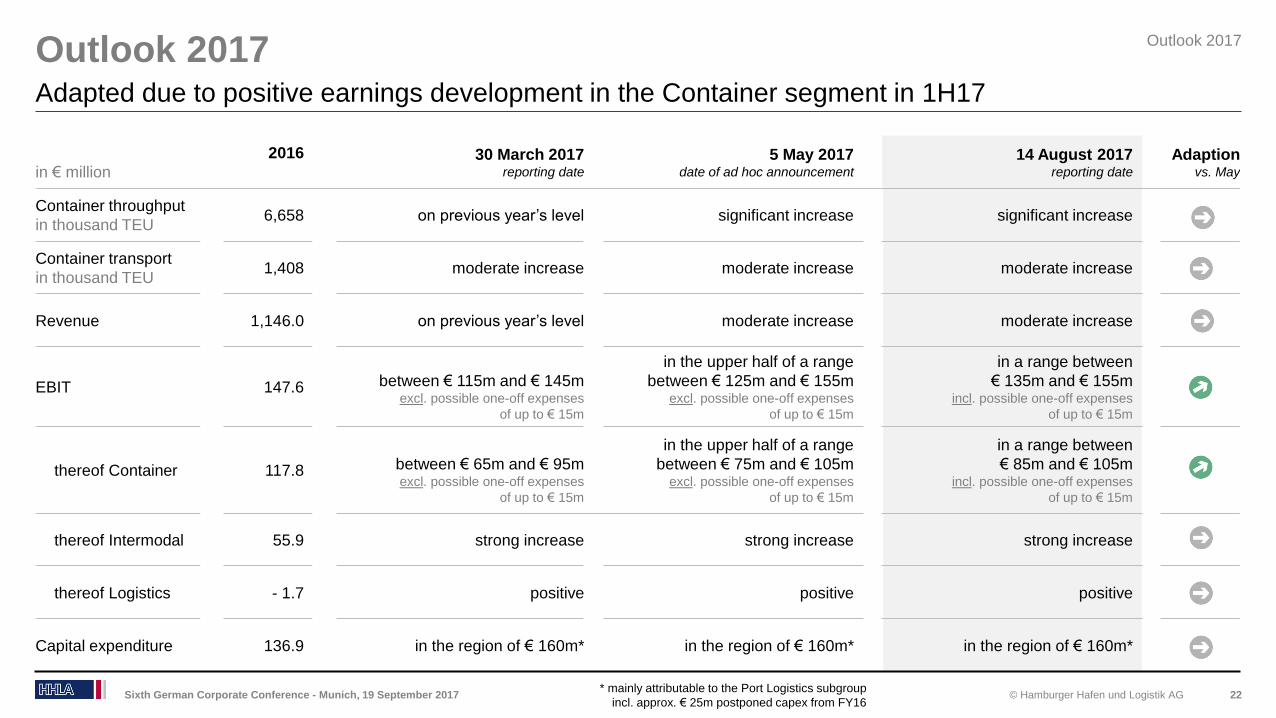

Outlook 2017

Sixth German Corporate Conference - Munich, 19 September 2017 22

Adapted due to positive earnings development in the Container segment in 1H17

Outlook 2017

in € million

2016 30 March 2017reporting date

5 May 2017date of ad hoc announcement

14 August 2017reporting date

Adaption vs. May

Container throughput

in thousand TEU6,658 on previous year’s level significant increase significant increase

Container transport

in thousand TEU1,408 moderate increase moderate increase moderate increase

Revenue 1,146.0 on previous year’s level moderate increase moderate increase

EBIT 147.6 between € 115m and € 145mexcl. possible one-off expenses

of up to € 15m

in the upper half of a range

between € 125m and € 155mexcl. possible one-off expenses

of up to € 15m

in a range between

€ 135m and € 155mincl. possible one-off expenses

of up to € 15m

thereof Container 117.8 between € 65m and € 95mexcl. possible one-off expenses

of up to € 15m

in the upper half of a range

between € 75m and € 105mexcl. possible one-off expenses

of up to € 15m

in a range between

€ 85m and € 105mincl. possible one-off expenses

of up to € 15m

thereof Intermodal 55.9 strong increase strong increase strong increase

thereof Logistics - 1.7 positive positive positive

Capital expenditure 136.9 in the region of € 160m* in the region of € 160m* in the region of € 160m*

* mainly attributable to the Port Logistics subgroup

incl. approx. € 25m postponed capex from FY16

© Hamburger Hafen und Logistik AG

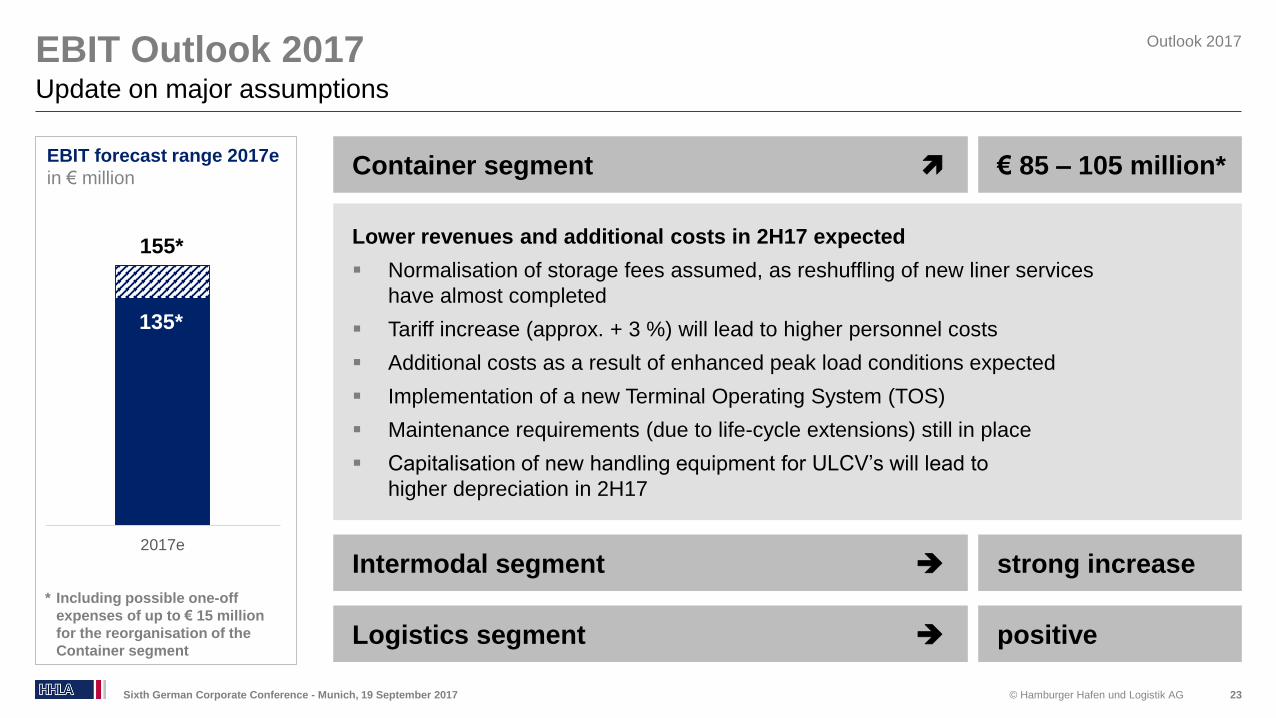

EBIT Outlook 2017

23

Update on major assumptions

Outlook 2017

Sixth German Corporate Conference - Munich, 19 September 2017

115*

2017e

* Including possible one-off

expenses of up to € 15 million

for the reorganisation of the

Container segment

EBIT forecast range 2017e

in € million

155*

135*

Lower revenues and additional costs in 2H17 expected

Normalisation of storage fees assumed, as reshuffling of new liner services

have almost completed

Tariff increase (approx. + 3 %) will lead to higher personnel costs

Additional costs as a result of enhanced peak load conditions expected

Implementation of a new Terminal Operating System (TOS)

Maintenance requirements (due to life-cycle extensions) still in place

Capitalisation of new handling equipment for ULCV’s will lead to

higher depreciation in 2H17

Container segment

Intermodal segment

Logistics segment

€ 85 – 105 million*

strong increase

positive

© Hamburger Hafen und Logistik AG

Agenda

Company Profile and Strategy

Business Update and Financial Performance 1H2017

Outlook 2017

Appendix

24Sixth German Corporate Conference - Munich, 19 September 2017

© Hamburger Hafen und Logistik AG

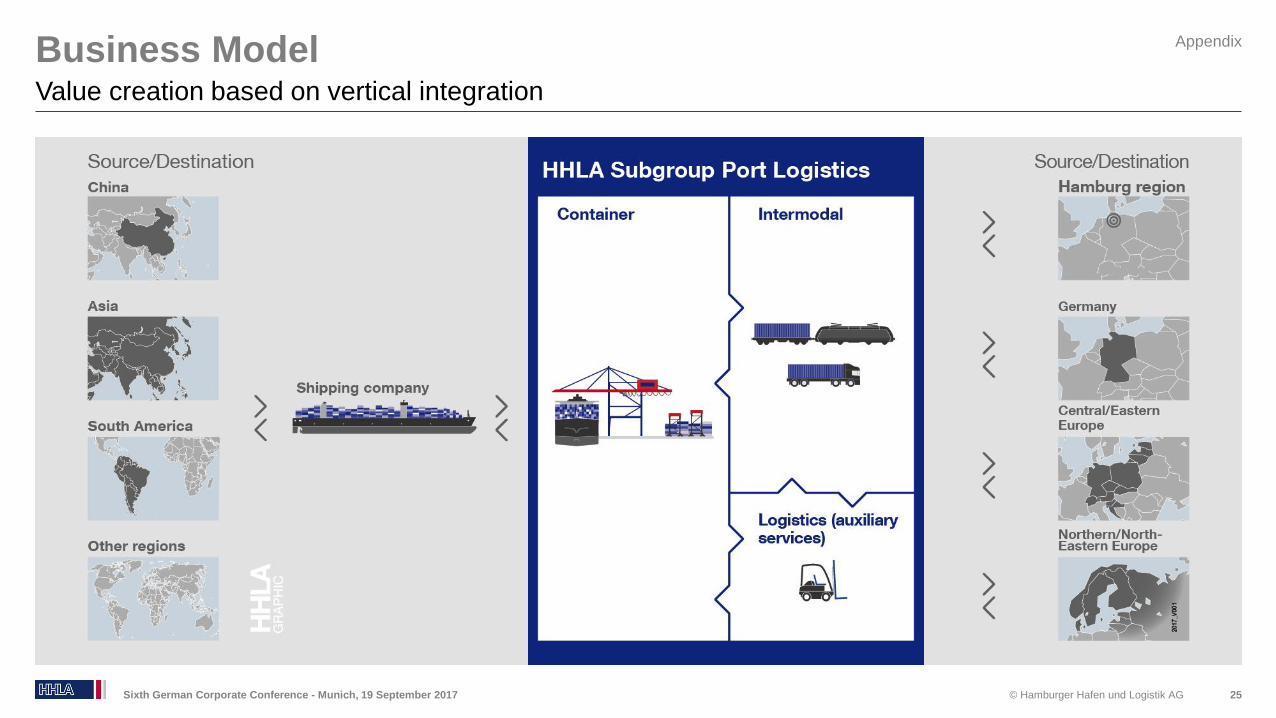

Business Model

25

Value creation based on vertical integration

Appendix

Sixth German Corporate Conference - Munich, 19 September 2017

© Hamburger Hafen und Logistik AG

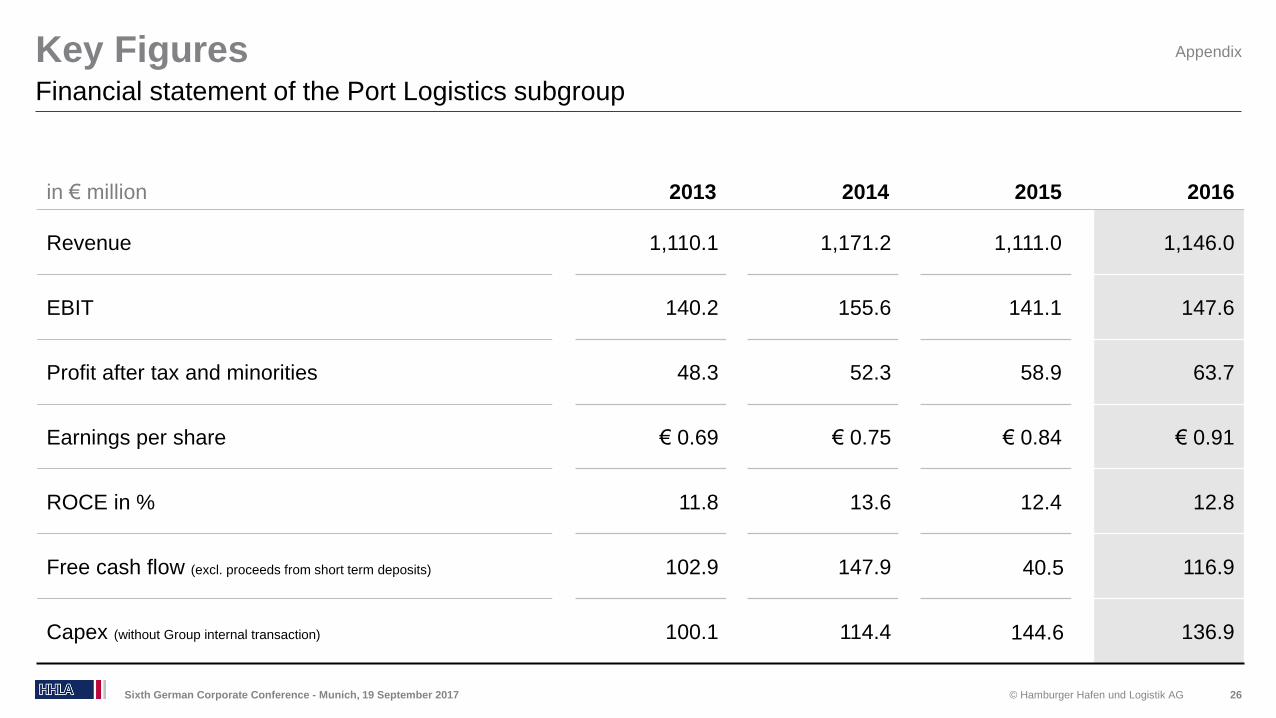

in € million 2013 2014 2015 2016

Revenue 1,110.1 1,171.2 1,111.0 1,146.0

EBIT 140.2 155.6 141.1 147.6

Profit after tax and minorities 48.3 52.3 58.9 63.7

Earnings per share € 0.69 € 0.75 € 0.84 € 0.91

ROCE in % 11.8 13.6 12.4 12.8

Free cash flow (excl. proceeds from short term deposits) 102.9 147.9 40.5 116.9

Capex (without Group internal transaction) 100.1 114.4 144.6 136.9

Key Figures

Sixth German Corporate Conference - Munich, 19 September 2017 26

Financial statement of the Port Logistics subgroup

Appendix

© Hamburger Hafen und Logistik AG

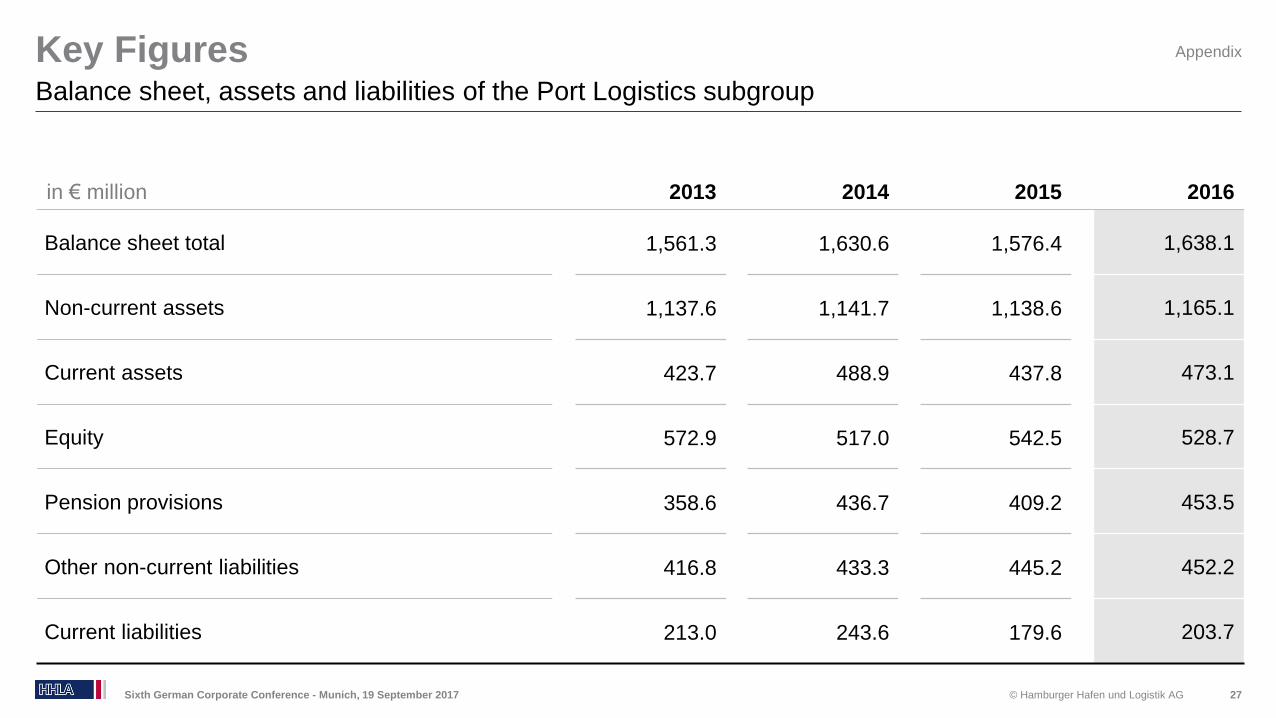

in € million 2013 2014 2015 2016

Balance sheet total 1,561.3 1,630.6 1,576.4 1,638.1

Non-current assets 1,137.6 1,141.7 1,138.6 1,165.1

Current assets 423.7 488.9 437.8 473.1

Equity 572.9 517.0 542.5 528.7

Pension provisions 358.6 436.7 409.2 453.5

Other non-current liabilities 416.8 433.3 445.2 452.2

Current liabilities 213.0 243.6 179.6 203.7

Key Figures

Sixth German Corporate Conference - Munich, 19 September 2017 27

Balance sheet, assets and liabilities of the Port Logistics subgroup

Appendix

© Hamburger Hafen und Logistik AG

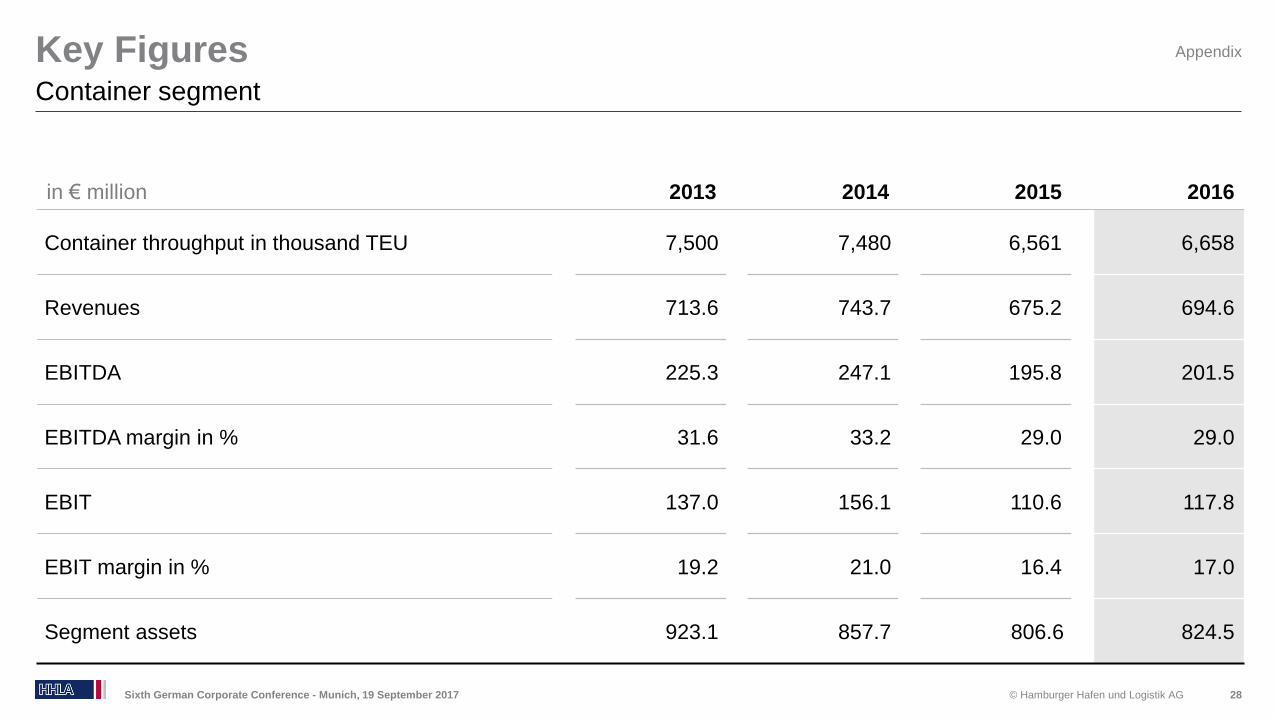

in € million 2013 2014 2015 2016

Container throughput in thousand TEU 7,500 7,480 6,561 6,658

Revenues 713.6 743.7 675.2 694.6

EBITDA 225.3 247.1 195.8 201.5

EBITDA margin in % 31.6 33.2 29.0 29.0

EBIT 137.0 156.1 110.6 117.8

EBIT margin in % 19.2 21.0 16.4 17.0

Segment assets 923.1 857.7 806.6 824.5

Key Figures

Sixth German Corporate Conference - Munich, 19 September 2017 28

Container segment

Appendix

© Hamburger Hafen und Logistik AG

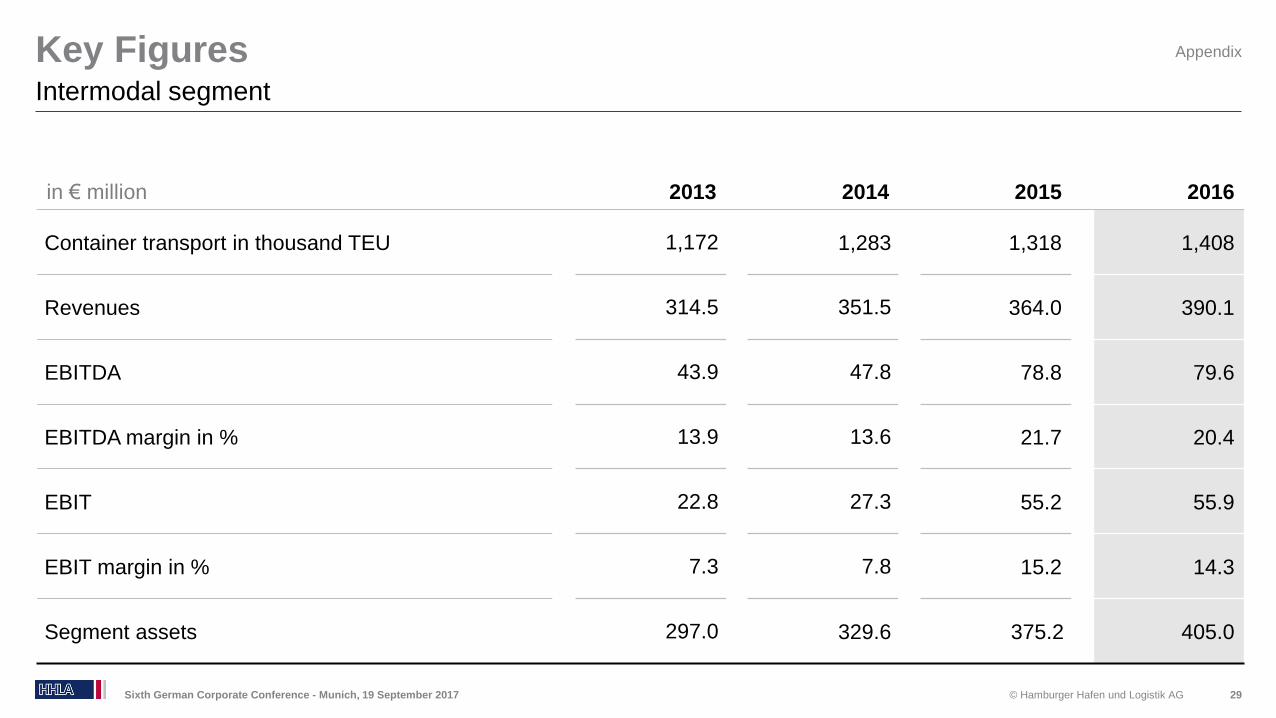

in € million 2013 2014 2015 2016

Container transport in thousand TEU 1,172 1,283 1,318 1,408

Revenues 314.5 351.5 364.0 390.1

EBITDA 43.9 47.8 78.8 79.6

EBITDA margin in % 13.9 13.6 21.7 20.4

EBIT 22.8 27.3 55.2 55.9

EBIT margin in % 7.3 7.8 15.2 14.3

Segment assets 297.0 329.6 375.2 405.0

Key Figures

Sixth German Corporate Conference - Munich, 19 September 2017 29

Intermodal segment

Appendix

© Hamburger Hafen und Logistik AG

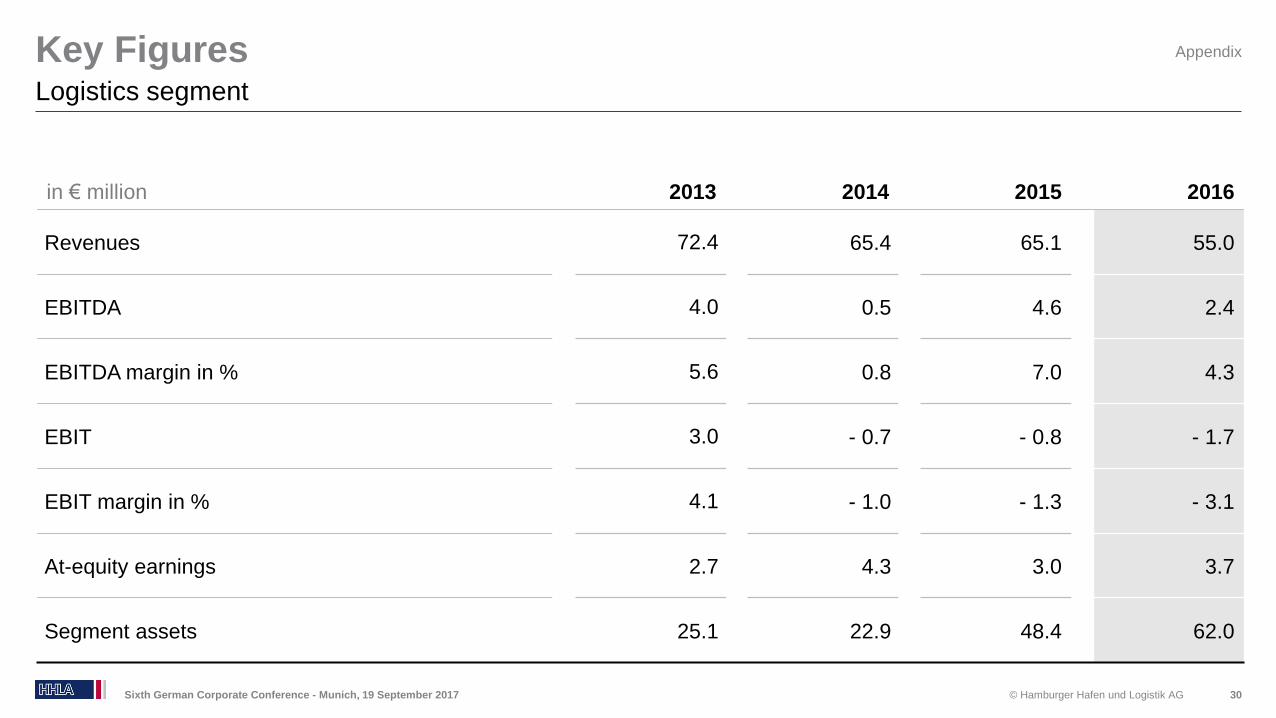

in € million 2013 2014 2015 2016

Revenues 72.4 65.4 65.1 55.0

EBITDA 4.0 0.5 4.6 2.4

EBITDA margin in % 5.6 0.8 7.0 4.3

EBIT 3.0 - 0.7 - 0.8 - 1.7

EBIT margin in % 4.1 - 1.0 - 1.3 - 3.1

At-equity earnings 2.7 4.3 3.0 3.7

Segment assets 25.1 22.9 48.4 62.0

Key Figures

Sixth German Corporate Conference - Munich, 19 September 2017 30

Logistics segment

Appendix

© Hamburger Hafen und Logistik AG

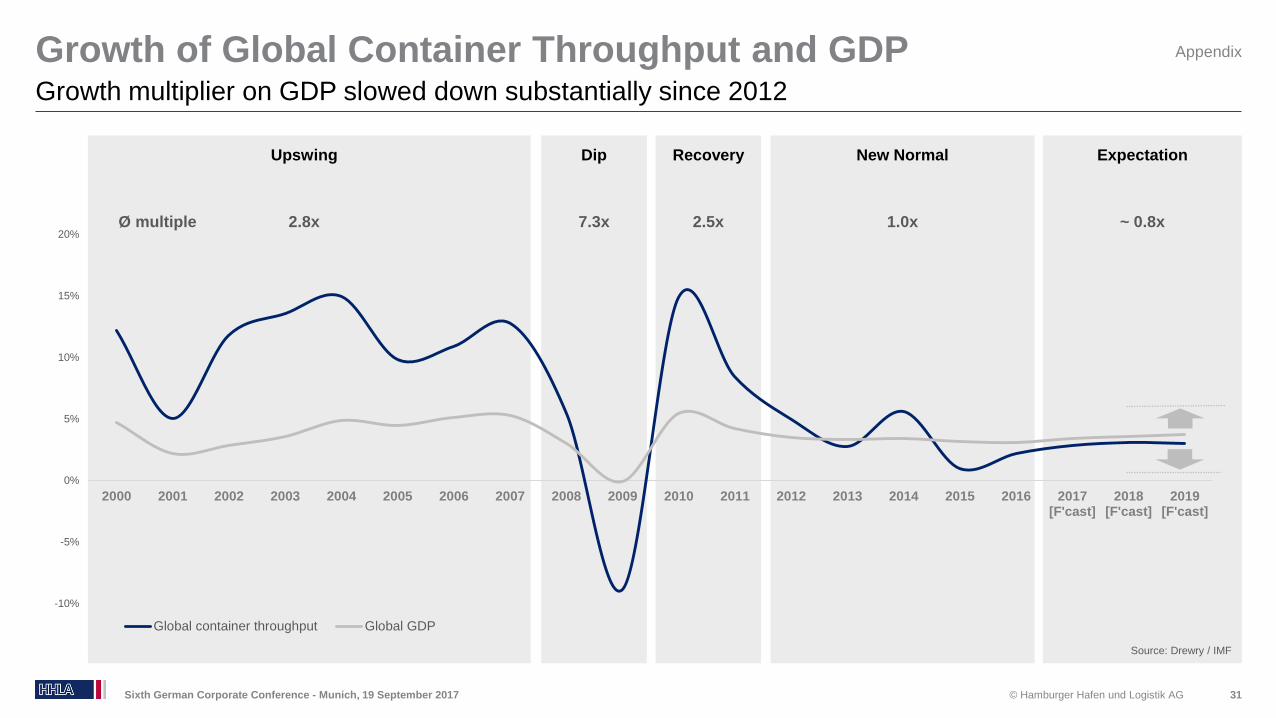

Growth of Global Container Throughput and GDP

Sixth German Corporate Conference - Munich, 19 September 2017 31

Growth multiplier on GDP slowed down substantially since 2012

Upswing Dip Recovery New Normal

-10%

-5%

0%

5%

10%

15%

20%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017[F'cast]

2018[F'cast]

2019[F'cast]

Global container throughput Global GDP

2.5x2.8x 7.3x

Expectation

1.0x ~ 0.8xØ multiple

Source: Drewry / IMF

Appendix

© Hamburger Hafen und Logistik AG

in TEU million

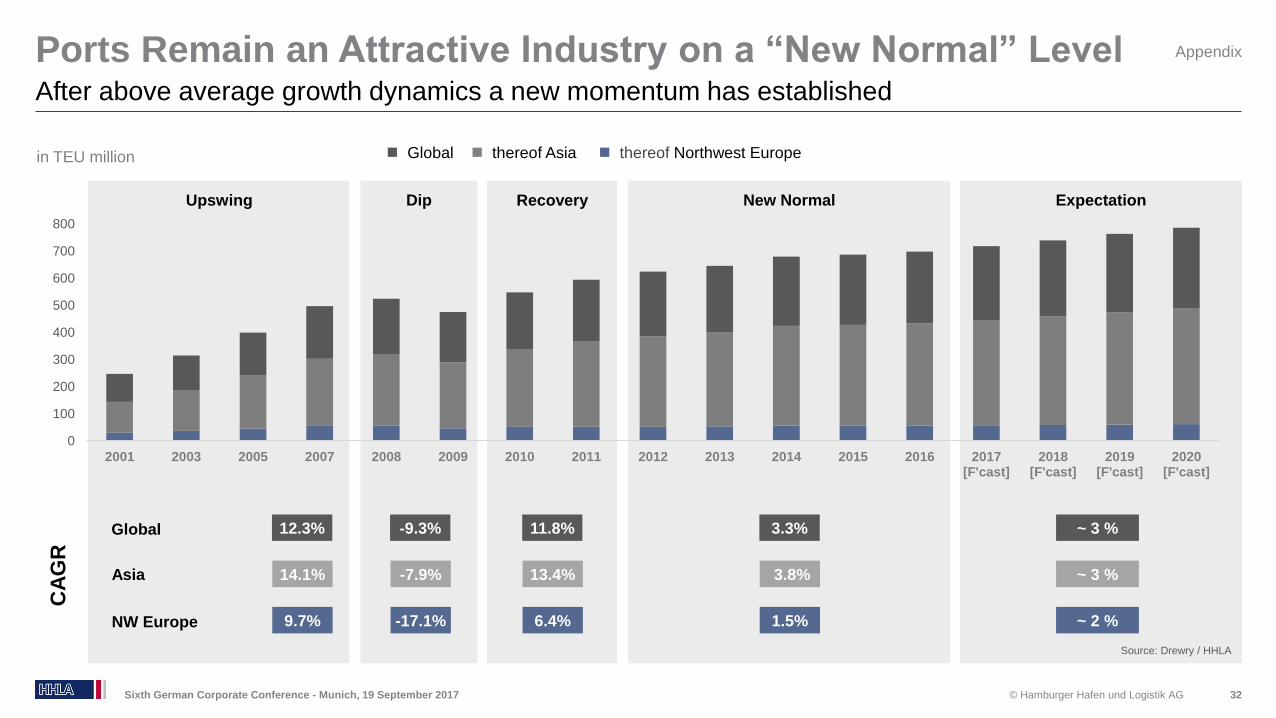

Ports Remain an Attractive Industry on a “New Normal” Level

Sixth German Corporate Conference - Munich, 19 September 2017 32

After above average growth dynamics a new momentum has established

Global thereof Asia thereof Northwest Europe

Source: Drewry / HHLA

Upswing Dip Recovery New Normal Expectation

14.1% -7.9% 13.4% 3.8% ~ 3 %

9.7% -17.1% 6.4% 1.5% ~ 2 %

CA

GR

12.3% -9.3% 11.8% 3.3% ~ 3 %

Asia

NW Europe

Global

0

100

200

300

400

500

600

700

800

2001 2003 2005 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017[F'cast]

2018[F'cast]

2019[F'cast]

2020[F'cast]

Appendix

© Hamburger Hafen und Logistik AG

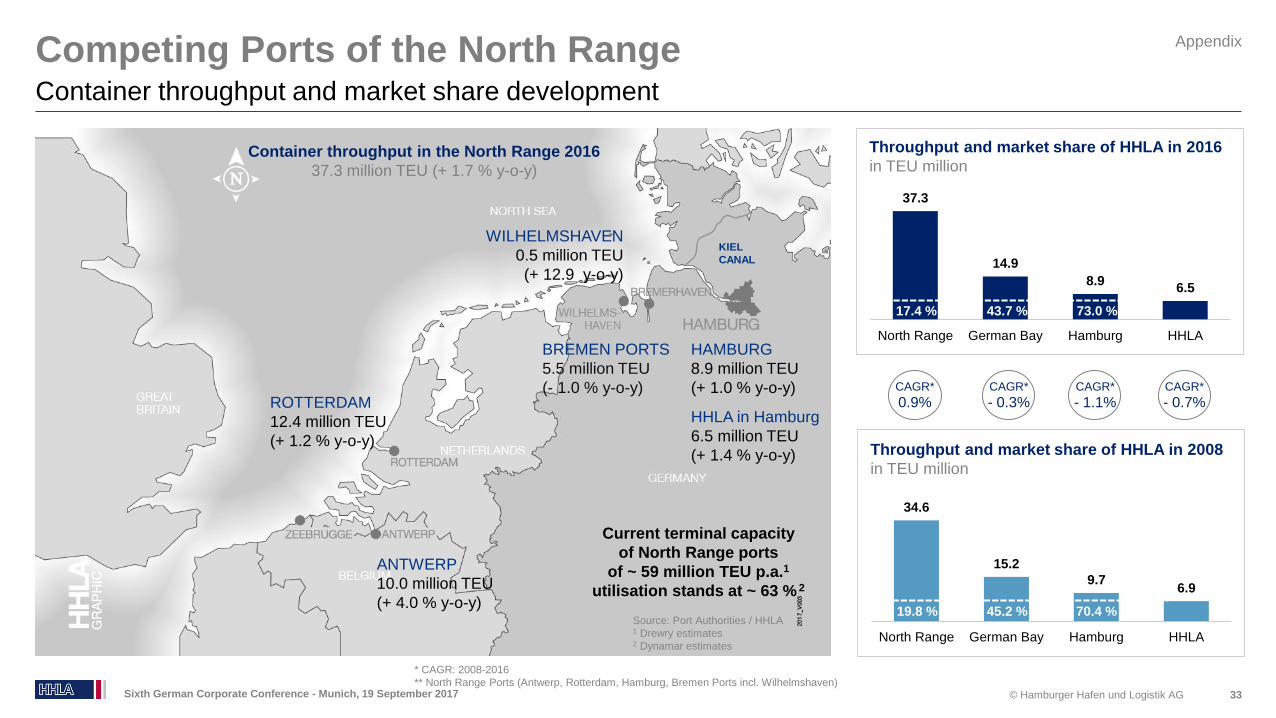

Competing Ports of the North Range

33

Container throughput and market share development

Sixth German Corporate Conference - Munich, 19 September 2017

WILHELMSHAVEN

0.5 million TEU

(+ 12.9 y-o-y)

ROTTERDAM

12.4 million TEU

(+ 1.2 % y-o-y)

ANTWERP

10.0 million TEU

(+ 4.0 % y-o-y)

BREMEN PORTS

5.5 million TEU

(- 1.0 % y-o-y)

HAMBURG

8.9 million TEU

(+ 1.0 % y-o-y)

KIEL

CANAL

HHLA in Hamburg

6.5 million TEU

(+ 1.4 % y-o-y)

Current terminal capacity

of North Range ports

of ~ 59 million TEU p.a.1

utilisation stands at ~ 63 % 2

Container throughput in the North Range 2016

37.3 million TEU (+ 1.7 % y-o-y)

37.3

14.9

8.96.5

North Range German Bay Hamburg HHLA

Throughput and market share of HHLA in 2016

in TEU million

34.6

15.2

9.76.9

North Range German Bay Hamburg HHLA

Throughput and market share of HHLA in 2008

in TEU million

70.4 %45.2 %19.8 %

CAGR*

0.9%CAGR*

- 0.3%CAGR*

- 1.1%CAGR*

- 0.7%

73.0 %43.7 %17.4 %

Source: Port Authorities / HHLA1 Drewry estimates2 Dynamar estimates

Appendix

* CAGR: 2008-2016

** North Range Ports (Antwerp, Rotterdam, Hamburg, Bremen Ports incl. Wilhelmshaven)

© Hamburger Hafen und Logistik AG

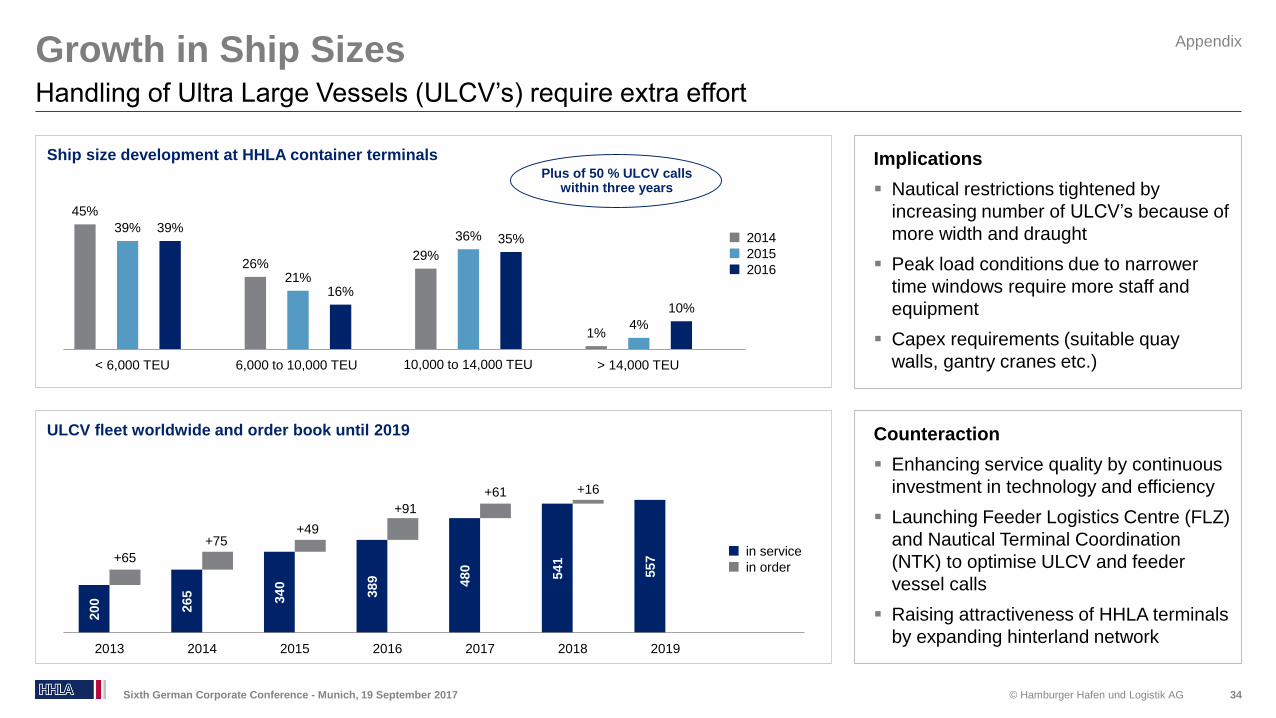

Growth in Ship Sizes

34

Handling of Ultra Large Vessels (ULCV’s) require extra effort

Sixth German Corporate Conference - Munich, 19 September 2017

Counteraction

Enhancing service quality by continuous

investment in technology and efficiency

Launching Feeder Logistics Centre (FLZ)

and Nautical Terminal Coordination

(NTK) to optimise ULCV and feeder

vessel calls

Raising attractiveness of HHLA terminals

by expanding hinterland network

Implications

Nautical restrictions tightened by

increasing number of ULCV’s because of

more width and draught

Peak load conditions due to narrower

time windows require more staff and

equipment

Capex requirements (suitable quay

walls, gantry cranes etc.)

45%

39% 39%

26%21%

16%

29%

36% 35%

1%4%

10%

Ship size development at HHLA container terminals

200

265 340

389 480

541

557+65

+75+49

+91

+61 +16

2013 2014 2015 2016 2017 2018 2019

> 14,000 TEU< 6,000 TEU 6,000 to 10,000 TEU

ULCV fleet worldwide and order book until 2019

in service

in order

2014

2015

2016

10,000 to 14,000 TEU

Plus of 50 % ULCV calls within three years

Appendix

© Hamburger Hafen und Logistik AG

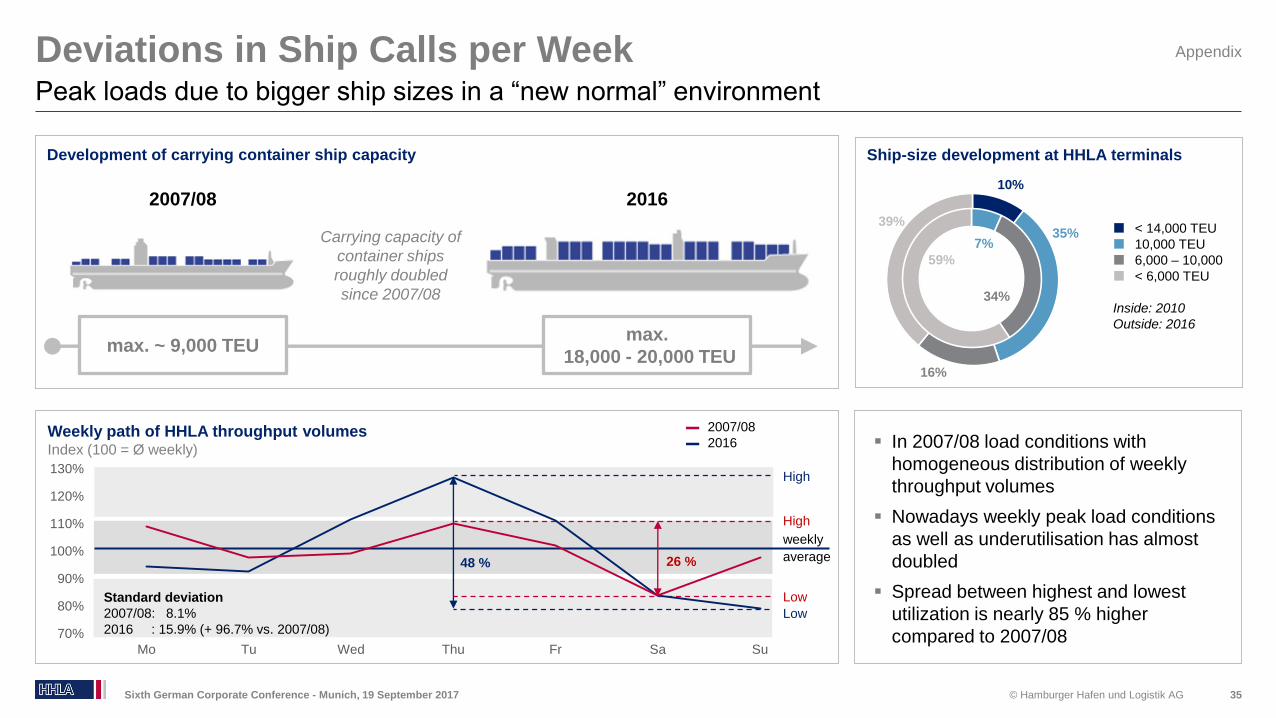

High

Low

Low

48 % 26 %

weekly

average

High

Standard deviation

2007/08: 8.1%

2016 : 15.9% (+ 96.7% vs. 2007/08)

10%

35%

16%

39%

Deviations in Ship Calls per Week

Sixth German Corporate Conference - Munich, 19 September 2017 35

Peak loads due to bigger ship sizes in a “new normal” environment

Carrying capacity of

container ships

roughly doubled

since 2007/08

2007/08 2016

In 2007/08 load conditions with

homogeneous distribution of weekly

throughput volumes

Nowadays weekly peak load conditions

as well as underutilisation has almost

doubled

Spread between highest and lowest

utilization is nearly 85 % higher

compared to 2007/08

max. ~ 9,000 TEUmax.

18,000 - 20,000 TEU

Development of carrying container ship capacity

Weekly path of HHLA throughput volumesIndex (100 = Ø weekly)

▬ 2007/08

▬ 2016

Ship-size development at HHLA terminals

< 14,000 TEU

10,000 TEU

6,000 – 10,000

< 6,000 TEU

Inside: 2010

Outside: 2016

7%

34%

59%

Appendix

70%

80%

90%

100%

110%

120%

130%

Mo Tu Wed Thu Fr Sa Su

© Hamburger Hafen und Logistik AG

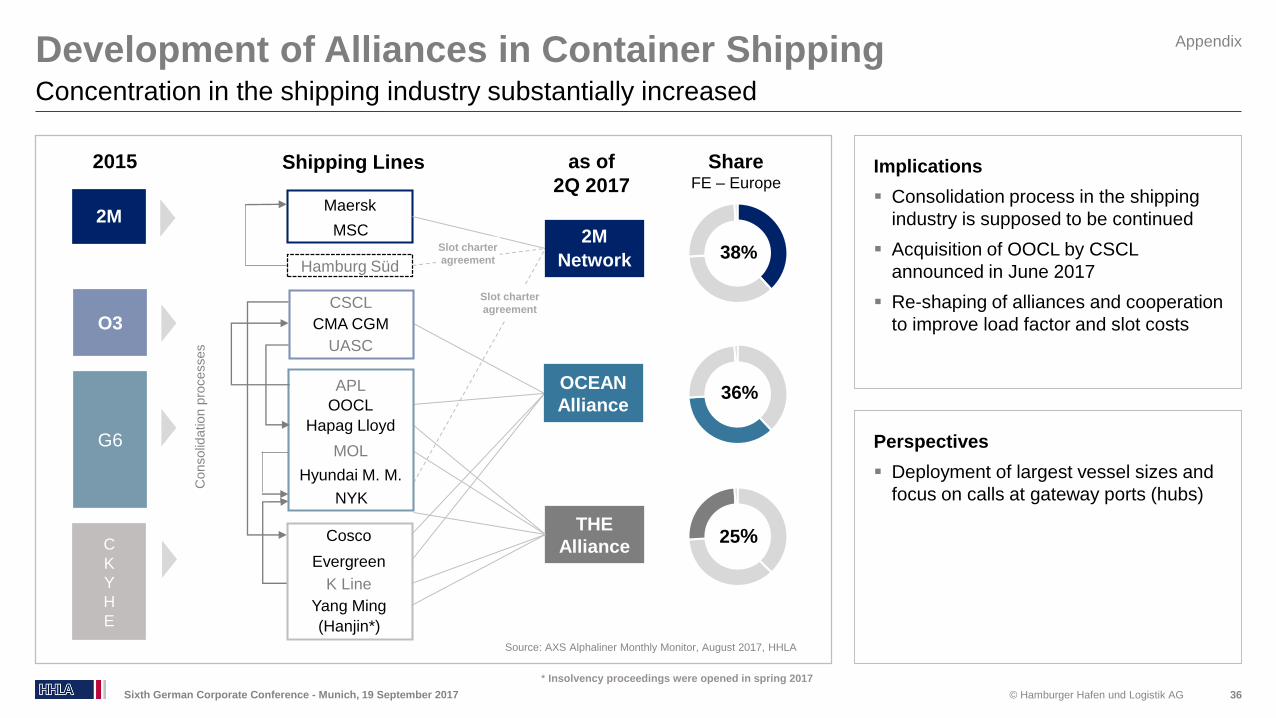

Shipping Lines

Development of Alliances in Container Shipping

36

Concentration in the shipping industry substantially increased

Sixth German Corporate Conference - Munich, 19 September 2017

70.4 %45.2 %

Perspectives

Deployment of largest vessel sizes and

focus on calls at gateway ports (hubs)

Implications

Consolidation process in the shipping

industry is supposed to be continued

Acquisition of OOCL by CSCL

announced in June 2017

Re-shaping of alliances and cooperation

to improve load factor and slot costs

THE

Alliance

2015 as of

2Q 2017

38%

36%

25%

ShareFE – Europe

Source: AXS Alphaliner Monthly Monitor, August 2017, HHLA

Hapag Lloyd

OOCL

MOL

APL

Hyundai M. M.

Cosco

K Line

Yang Ming

Evergreen

CMA CGM

CSCL

UASC

2M

O3

G6

C

K

Y

H

E

Consolid

ation p

rocesses

Slot charter

agreement

(Hanjin*)

Hamburg Süd

NYK

Slot charter

agreement

Maersk

MSC

Appendix

* Insolvency proceedings were opened in spring 2017

OCEAN

Alliance

2M

Network

© Hamburger Hafen und Logistik AG

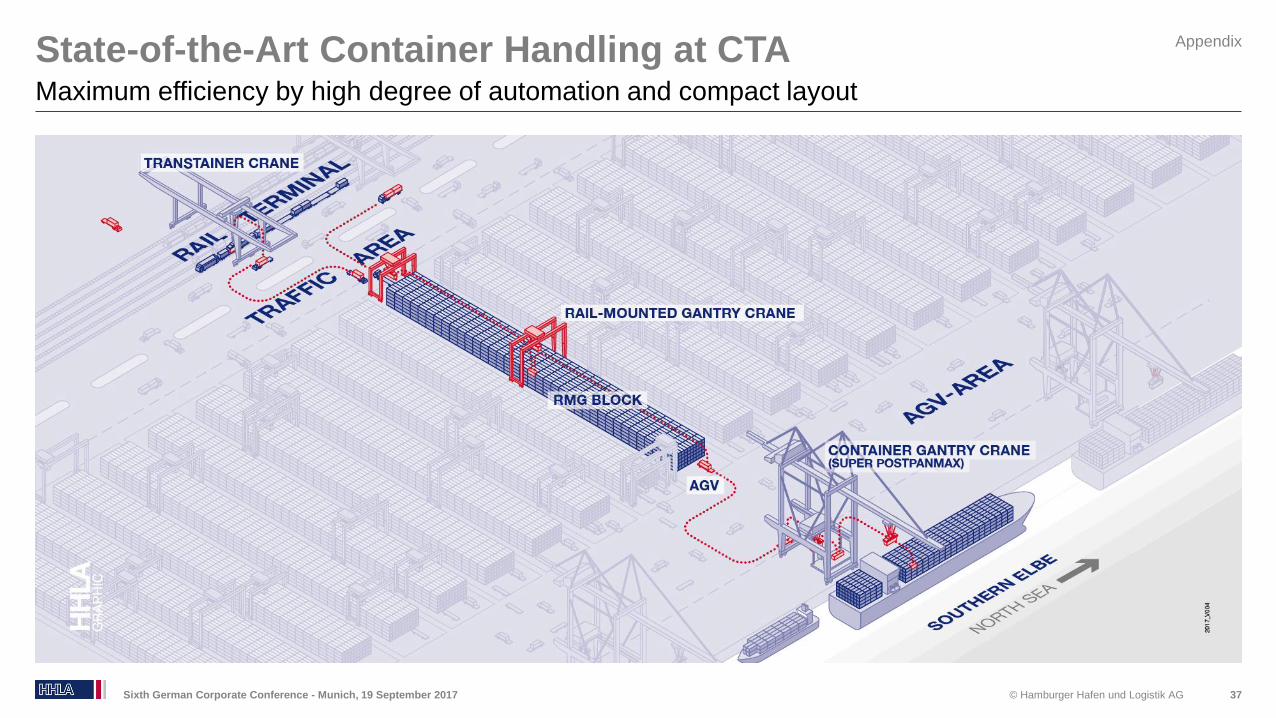

State-of-the-Art Container Handling at CTA

37

Maximum efficiency by high degree of automation and compact layout

Sixth German Corporate Conference - Munich, 19 September 2017

Appendix

© Hamburger Hafen und Logistik AG

Strengthening Hinterland Network With Own Assets

38

Well located inland hub terminals offer high level of value added services

Sixth German Corporate Conference - Munich, 19 September 2017

Appendix

© Hamburger Hafen und Logistik AG

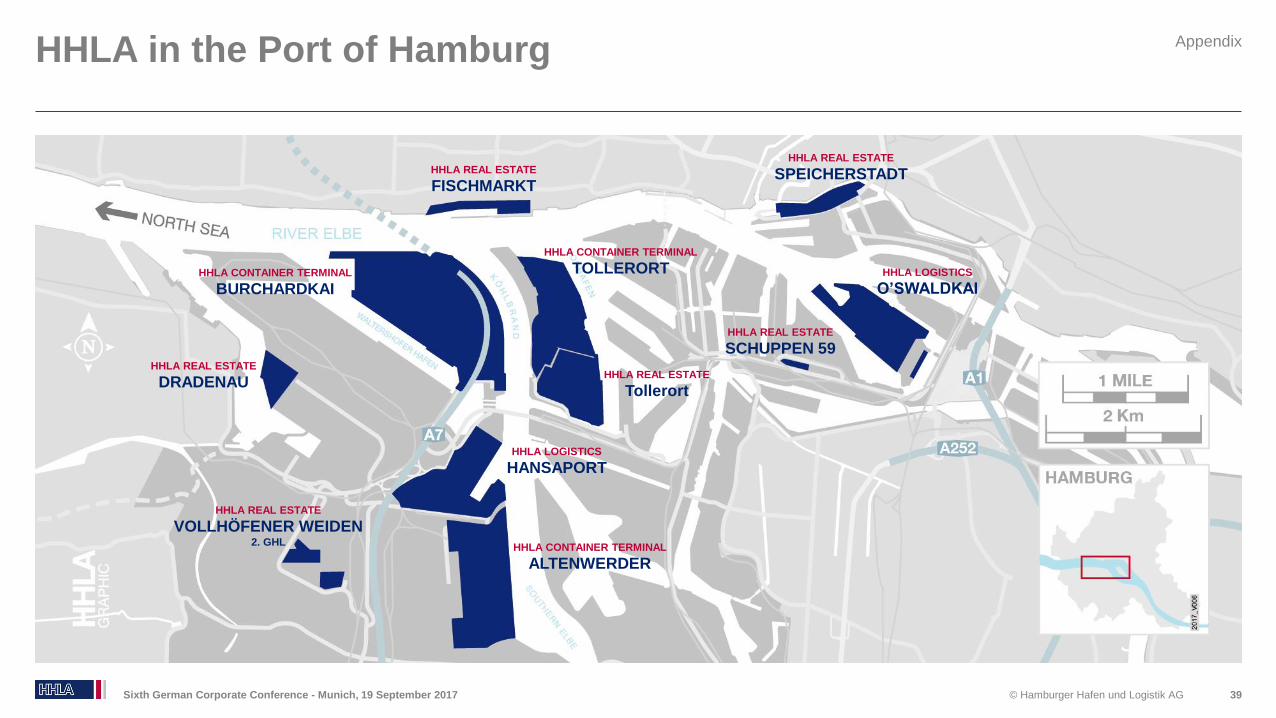

HHLA in the Port of Hamburg

39Sixth German Corporate Conference - Munich, 19 September 2017

Appendix

HHLA CONTAINER TERMINAL

BURCHARDKAI

HHLA CONTAINER TERMINAL

ALTENWERDER

HHLA LOGISTICS

HANSAPORT

HHLA CONTAINER TERMINAL

TOLLERORT

HHLA REAL ESTATE

FISCHMARKT

HHLA REAL ESTATE

SPEICHERSTADT

HHLA LOGISTICS

O’SWALDKAI

HHLA REAL ESTATE

SCHUPPEN 59

HHLA REAL ESTATE

VOLLHÖFENER WEIDEN2. GHL

HHLA REAL ESTATE

DRADENAUHHLA REAL ESTATE

Tollerort

© Hamburger Hafen und Logistik AG

Elbe Waterway Adjustment

40

Administrative steps by the public authorities in charge

Sixth German Corporate Conference - Munich, 19 September 2017

Adjustment of navigation channel

Enabling a higher load factor, extended time slots and more flexibility for mega carriers

14.50 m tidal dependent / 13.50 m tidal independent, widening boxes

Main hearings

on legal

objections

Federal

Administrative

Court (FAC)

Initiation and final

plan approval

Sep 2006 –

Apr 2012 July 2014

ECJ judgement

on the EU Water

Framework

Directive

European Court

of Justice (ECJ)

1 July 2015

Decision on

the planning

supplement

9 Feb 2017

Federal Water and

Shipping Authority /

Hamburg Port Authority

Fulfilment of

judicial obligations

Appendix

in progress

Present depth

Planned depth14.50 m tidal dependent / 13.50 m tidal independent, widening boxes

Federal

Administrative

Court (FAC)

Federal Water

and Shipping

Authority

“There is legal certainty. This means irrevocable:

the adjustment of the navigation channel comes.”

Olaf Scholz, Mayor of Hamburg

“The accessibility of the port and its hinterland

connections will improve significantly. [...]

Infrastructure projects are secured and financed.

This includes the dredging of the river Elbe.”

Enak Ferlemann, Parliamentary State Secretary

of transport and digital infrastructure

“Today's verdict has confirmed: The Elbe dredging

will come. We will now carefully analyse the

reasoning behind the decision and adapt the plans

as quickly as possible.”

Alexander Dobrindt, Federal Transport Minister

“Today's decision unfortunately takes time again.

Now we will plan and implement the next steps

as soon as possible.”

Frank Horch, Senator for Economics in Hamburg

© Hamburger Hafen und Logistik AG

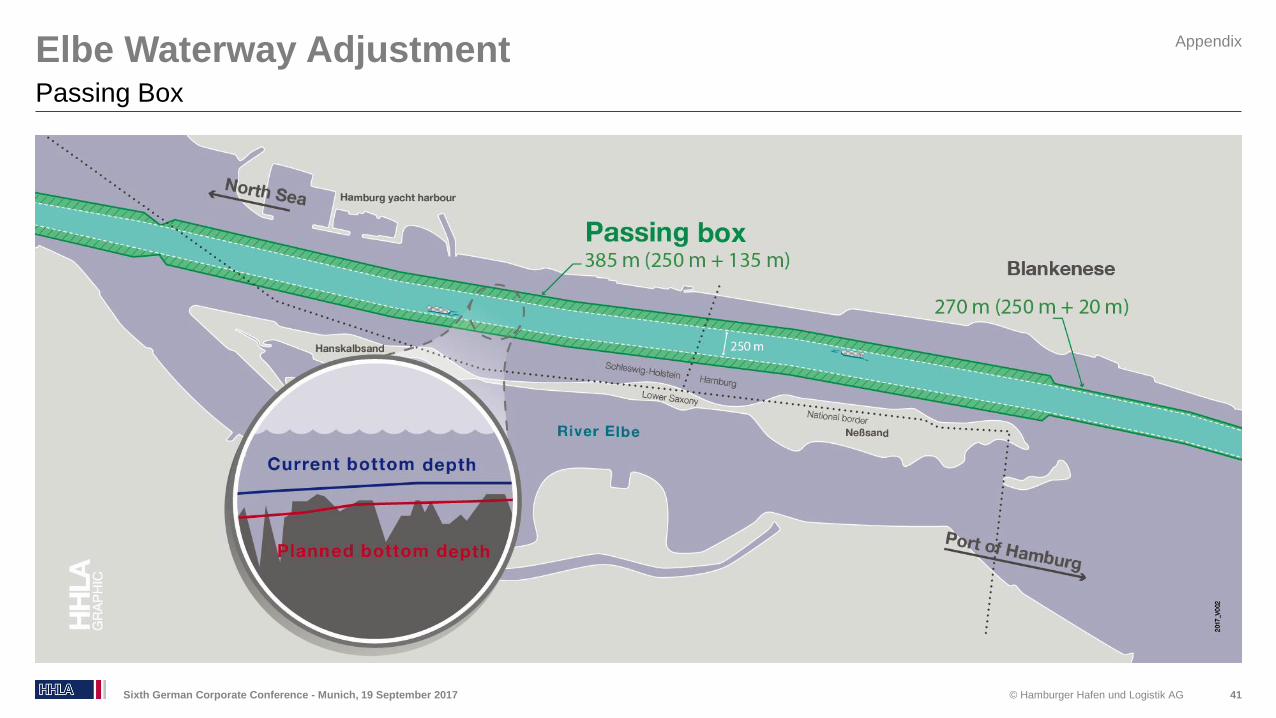

Elbe Waterway Adjustment

41

Passing Box

Sixth German Corporate Conference - Munich, 19 September 2017

Appendix

© Hamburger Hafen und Logistik AG

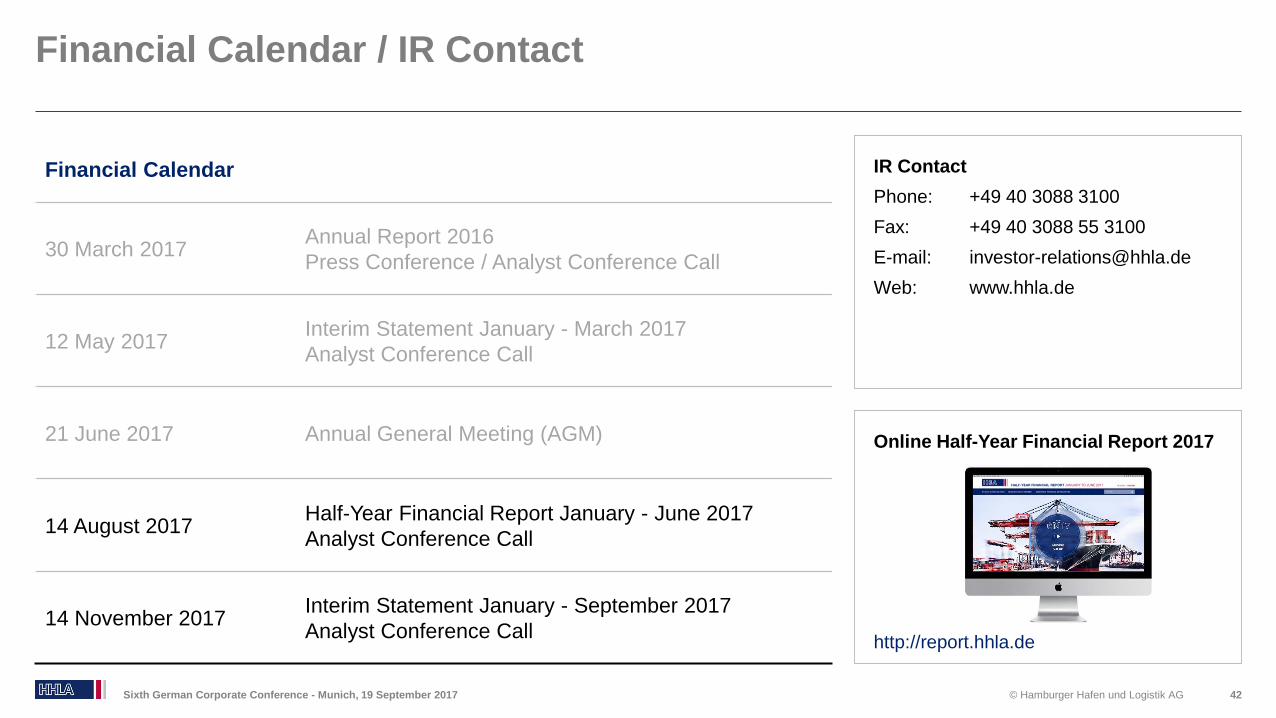

Financial Calendar / IR Contact

42Sixth German Corporate Conference - Munich, 19 September 2017

Online Half-Year Financial Report 2017

IR Contact

Phone: +49 40 3088 3100

Fax: +49 40 3088 55 3100

E-mail: [email protected]

Web: www.hhla.de

Financial Calendar

30 March 2017Annual Report 2016

Press Conference / Analyst Conference Call

12 May 2017Interim Statement January - March 2017

Analyst Conference Call

21 June 2017 Annual General Meeting (AGM)

14 August 2017Half-Year Financial Report January - June 2017

Analyst Conference Call

14 November 2017Interim Statement January - September 2017

Analyst Conference Callhttp://report.hhla.de

HALF-YEAR FINANCIAL REPORT JANUARY TO JUNE 2017

© Hamburger Hafen und Logistik AG

Interim Statement January to June 2017 http://report.hhla.de/half-year-financial-report-2017/

Related Documents