George Street Review Turning Point e Iue 143

George Street Review 143

Apr 06, 2016

Â

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

� George Street Review

Turning Point The

Issue 143

� George Street Review

CONTENTS03 Chair’s Report

Courtney Olden

04 KPMG Titans of IndustrySpeaker Profiles

06 Future of Federalism Courtney Olden

07 Hidden WealthSally Moore

08Australia’s Global Future Alanna Rennie

�0 Tax & Happiness Joy Du

�2 Financial RegulationJessica Howe

�3 A Rebalancing Act Blake Nicolson

�4 Competitiveness is KeyJonathan Colak

�5 Tax Reform Jordan Kuhnemann

�6 Unemployment Update Sally Moore

�7 M&A ActivityDylan Master

�8 Taming the Excel BeastMark Johnman

20 Taming the Excel BeastMark JohnmanEditors

Mark Johnman Brigette Foot

Design Brigette Foot Charlotte Klem

Financial Regulatory SchemeEdward Langley

09

3 George Street Review

Welcome to the Semester 143 edition of the George Street Review. It’s only week 3 but the Bond Investment Group

have had an incredibly busy last few months and we are so pleased the annual Titans of Industry Forum is finally here. The following pages will provide student and staff perspectives on the overarching theme that will be discussed at the Forum: “The Turning Point: A new approach to building a globally competitive economy for Australia.” You’re in for a BIG treat with this year’s Forum set to engage, inform and motivate you.

KPMG Titans of Industry Forum 2014The annual Titans of Industry Forum is upon us! This year the Forum is proudly sponsored by KPMG and we are thrilled to be welcoming a group of talented guest speakers to Bond:• Mr Gary Wingrove – CEO, KPMG;• Dr John Laker AO – Former Chairman, APRA;• Mr Robert Jeremenko – Senior Tax Counsel, The Tax Institute; and• Mr Robert Milliken (moderator) – Australian Correspondent, The Economist.

Turn to pages 4 & 5 for more information on our speakers. We are looking forward to the opportunity to learn from some of the sharpest minds in our Australian business community and we hope you are too.

The RegularsI trust you’re staying tuned with the latest on deals, markets, economic news and business commentary in The Week Just Gone which is published on our website and Facebook page

every Saturday morning. BIG guru Dylan Master has been slaving week in week out to bring you the most up to date and relevant info in an easily-digestible format and it is definitely worth the read.

Coming up The speaker events don’t end with Titans. We’ll be bringing you another Speaker Series later in the semester and the Women in Business Evening is back in semester 151.

Getting on boardIf you like the sound/look of us, keep an eye on the Student Daily Digest and our Facebook page and website later this semester because we’ll be looking for some new recruits to join the BIG team. We’re looking for people who think BIG (last one, I promise) and have a keen interest in finance, economics or business.

FarewellBy the time the next GSR is published there’ll be a new Chair steering this ship. It has been an absolute privilege getting to know you over the past year and I have thoroughly enjoyed every attempt our BIG Committee has made to improve your student experience and prospects post-university. I am constantly amazed by just how much a small group of motivated people can achieve. Thank you to the incredible individuals I have had the pleasure of working with on the 2014 BIG Committee – you’re a talented bunch and I’m looking forward to watching your progress from afar Brisbane.

Remember, think BIG!

Courtney OldenChair, Bond Investment Group

WEBSITEPlease visit: www.bondinvestmentgroup.org

FACEBOOKFind us by searching ‘Bond Investment Group’

WANT TO CONTRIBUTE TO THE GSR? Please email: [email protected]

CHAIR’S REPORT

� George Street Review

TITANSOF INDUSTRY FO

RUM

GUE

ST S

PEA

KERS

KPMG

It is back and as BIG as ever. This year’s panel features some of Australia’s sharpest minds in the business community; true titans of the industry. The Forum will be in the form of a luncheon, followed by a panel discussion and an opportunity for Q&A.

THE TOPICThe panel will discuss current economic trends facing Australia, including regulatory movements, macroeconomic conditions and our financial architecture. The theme for this year is ‘The Turning Point: A new approach to building a globally competitive economy for Australia’.

DATE: TUESDAY 23 SEPTEMBER 2014

TIME: 12PM

WHERE: PRINCETON ROOM, BOND UNIVERSITY

04 George Street Review

5 George Street Review

GUE

ST S

PEA

KERS

GARY WINGROVECEO, KPMG

Gary was elected CEO of KPMG Australia on 1 July 2013. As CEO, he sets the firm’s strategic direction, oversees its operation and presides over the principal management body, the National Executive Committee. Gary joined another Big 4 firm in South Africa in 1988 and spent four years as an auditor, before moving into Corporate Finance. He relocated to Australia in 1994 and joined KPMG’s Corporate Finance practice in 1997. Admitted as a partner of KPMG in 2000, Gary led the Melbourne and later the National Valuations team of the firm until 2007.

In recent years he has held leadership roles as National Head of Corporate Finance, National Managing Partner of Financial Advisory Services and National Managing Partner of Advisory. He was appointed to lead the firm’s Advisory practice in July 2009 following the merger of the firm’s Financial Advisory Services and Risk Advisory Services practices.

Gary’s area of client expertise includes public fairness opinions on merger and acquisition transactions; valuations of businesses, shares and intangible assets and general corporate advice related to transactions.

ROBERT JEREMENKOSenior Tax Counsel, The Tax

Institute

Robert is Senior Tax Counsel at The Tax Institute and heads the Tax Policy and Advocacy team, leading the Institute’s advocacy activities. Robert joined The Tax Institute after five years at one of Australia’s largest banks, where he held roles including Head of International Government Affairs.

Prior to this, Robert was taxation adviser on the personal staff of the Australian Federal Treasurer, where he worked on the implementation of a broad range of taxation policy over a four-year period. Robert holds degrees in Law and Science from the Australian National University and is admitted as a Barrister and Solicitor of the High Court of Australia.

DR JOHN LAKER AO Retired Chair, APRA

Dr Laker was Chairman of the Australian Prudential Regulation Authority (APRA) over an 11–year period from 1 July 2003 to 30 June 2014. As Chairman, Dr Laker was APRA’s representative on the Payments System Board of the Reserve Bank of Australia (RBA), the Council of Financial Regulators, the Trans-Tasman Council on Banking Supervision, the Basel Committee on Banking Supervision (BCBS) and its oversight body, the Governors and Heads of Supervision (GHOS). He was also a director of the Centre for International Finance and Regulation.

Currently, Dr Laker is serving on the External Advisory Panel of the Australian Securities and Investments Commission (ASIC). He is also lecturing at the University of Sydney and undertaking advisory work for the International Monetary Fund.

Dr Laker was made an Officer of the Order of Australia in 2008 for services to the regulation of the Australian financial system and to the development and implementation of economic policies nationally and internationally.

ROBERT MILLIKEN Australian Correspondent, The

Economist

It is back and as BIG as ever. This year’s panel features some of Australia’s sharpest minds in the business community; true titans of the industry. The Forum will be in the form of a luncheon, followed by a panel discussion and an opportunity for Q&A.

THE TOPICThe panel will discuss current economic trends facing Australia, including regulatory movements, macroeconomic conditions and our financial architecture. The theme for this year is ‘The Turning Point: A new approach to building a globally competitive economy for Australia’.

Robert is a Sydney journalist and author, and a correspondent for The Economist. He writes for the magazine on Australian politics and the economy, and a wide range of issues including energy, climate and immigration, as well as for The Economist’s online Asia blog, “Banyan”, and its annual publication The World In…”. He has also moderated the Economist Group’s series of annual “Bellwether Australia” conferences. Robert Milliken is a contributor to Inside Story, Anne Summers Reports and Good Weekend.

Mod

erat

or

� George Street Review

Would Australia be better off if states were scrapped? The Federation is arguably outdated, and the three tiers of government have been labeled bloated, with huge waste and duplication issues.

The issue is that funding is the Constitution’s Achilles heel. It leaves the states legally free, but financially bound to the central government. The states’ needs are the Commonwealth’s opportunities. We’ve seen chronic problems in policy areas where Commonwealth and state roles overlap – namely hospitals and schools – and that leaves us wondering whether the states as they are serve much relevance at all.

A substantial majority of Australians agree that the current system does not work well. The Australian economy

is at a crossroads – we need to reduce our reliance on the resources sector and the state

governments might just be best placed to lead that change.

So should we fix them or should we scrap them?

Abolishing the Federation makes sense in theory, but breaking up is hard to do. It would be largely unrealistic to pursue such a big change. The only way to eliminate the states would be through a national referendum where every state agreed to the change. Abandoning federalism

wouldn’t be in the interests of the smaller states like

Tasmania, which wield greater clout, attract more funding, and

are better represented as states than they would be otherwise.

What would a non-Federalist Australia look like?

If the states were abolished, there would be only two tiers of government: a central national government; and

strengthened local governments. John Howard was all for it, opining in 2005 that “if we were starting Australia all over again, I wouldn’t support having the existing state structure. I would actually support having a national government and perhaps a series of regional governments.”

But we aren’t starting Australia all over again. The strongest argument for retaining the states is that they exist. Even though our federalist system might be second best, we may just have to find a way to make second best work as best we can.

The Future Of Federalism in

AustraliaShould Australia Scrap The States?

|Words By Courtney Olden

06 George Street Review

7 George Street Review

THE HIDDEN WEALTH IN SWITZERLAND

While most would associate Switzerland with snowy alps, good skiing and excellent chocolate, this small European nation has also long been connected with the storing of wealth. As countries’ tax systems have developed and corporations have become more far-reaching due to globalisation, the desire to reduce or avoid taxation has been broadened beyond individual asset protection. Countries around the world have responded by offering favourable tax rates with the aim of bringing large corporations onshore. Corporate tax havens have emerged in the Cayman Islands, Luxemburg, Singapore and Ireland, with technology leaders Apple and Google being based at the latter for taxation purposes. In recent times, the use of tax avoidance strategies has accelerated, driven by the digitalisation of business and increases in cross-border businesses and business practice.

Recent ATO data reveals that while Australia is a recipient of some income from tax havens, domestic companies paid $1.22 billion more to 26 offshore tax havens in 2012. However, tax evasion is beginning to be targeted globally, with the ATO’s response being Project DO IT: Disclose Offshore Income Today, which allows individuals to disclose foreign held assets without ATO or criminal investigation. Likewise, internationally, tax havens have become a hot topic of conversation. In the US, Senator Carl Levin has been a leader in reducing the utilisation of tax havens, introducing the Stop Tax Haven Abuse Act in 2013.

In May this year, Australia hosted the G20 Symposium on Tax in Tokyo. One of the key questions posed in this forum was how governments can best address this innovative and constantly changing loophole, particularly in the face of resistance from countries that benefit from holding taxable monies at low rates. Identifying the limitations of a taxation system designed for smaller and less encompassing corporations, the BEPS (base erosion and profit shifting) project aims to address some of these issues, and is currently on track, despite a demanding timeframe. It is hoped that tax reform will create a more equal system, and also eliminate double taxation. Another benefit of reform is that having an internationally accepted interpretation of taxation principles will allow clarity on what constitutes acceptable tax planning, and alternatively what amounts to illegal avoidance. Transparency around tax incentives was also identified as an area for improvement.

It seems that tax havens and tax avoidance will continue to remain a challenge, but with good reform, a tax system may emerge that realigns taxation and business profits. No system will be perfect in such a dynamic and complex area, but strong reform is certainly a step forward.

New Approaches to Taxation Challenges

|Words By Sally Moore

07 George Street Review

� George Street Review

Earlier this week, Deloitte released a statement suggesting that Australia’s financial regulation scheme is too interventionist. Claiming that Australia has been forced into “prescriptive regulation” that has bred a “compliance culture”, Deloitte submitted to the Financial Systems Inquiry that Australia’s reaction to the Global Financial Crisis (GFC), combined with the sovereign debt crisis is “not conducive to innovation”. The firm conceded that the implementation of individual changes was not large, but that the cumulative effect of those changes has been significant.

Australia largely escaped the 2009 world-wide recession. With March quarter GDP growth of 0.4% and a retention of profitability in the banking sector, we did not suffer the fate that other world economies did. However, this did not prevent concerns about financial market practices and investor protection. The pre-GFC Australian approach to financial regulation was based on disclosure, education and advice, but it didn’t prevent the marketing of high-risk financial products to wholesale investors who weren’t fully appreciative of the market.

Professor Kevin Davis, a professor of finance at the University of Melbourne, earlier this year warned that Australia cannot be complacent just because it avoided the worst of the GFC. Focussing on the issue of “ring fencing” big banks; a process that separates a portion of a company’s assets or profits for regulatory reasons, Davis suggested that Australia could not differ too far

from its peers. Banks such as the Commonwealth Bank have underplayed the need for ring fencing as it could create extra compliance costs for lenders. The discussion exemplifies the conflict between banks and governments over financial regulations; banks suggest they’ve gone too far, governments argue they are nowhere near as interventionist as those brought in overseas.

The inquiry panel, working on its final recommendations to the Abbott government, has recently faced submissions from all banks and major firms, with Deloitte’s suggestions being just the latest of many. All have claimed that the financial regulations brought in due to the GFC cannot be justified because there have not been sufficient benefits. Deloitte has asserted that “the pendulum has swung too far” without sufficient gain, but with international regulation far more interventionist than that of Australia, it is hard to see the inquiry suggesting a reduced regulatory regime.

Has The Regulatory Regime Gone Too Far?|Words By Edward Langley

08 George Street Review

9 George Street Review

The Abbott government has proposed agriculture as one of the five pillars of the Australian economy. This article discusses how the government should address the agriculture pillar to build a globally competitive economy.

Traditionally Australian agricultural exports have been amongst the most competitive in the world. Australian agriculture has existed largely unsubsidised and as a result Australian farmers have had to be innovative and develop economic farming practices to remain competitive on global markets.

The future does not look so promising. With the trend of rising wages and agricultural inputs Australian exports will not be able to compete on global markets. This is resulting in reduced farm-gate return and a disillusioned farming society. Farmers are selling off their family farms and the younger generation is being encouraged to seek jobs in other sectors.

Australian agriculture is faced with two options. We either sell our farms to foreign investors or we find markets willing to pay higher prices for our agricultural products.

Selling our farms is not an option and realistically Australia can only supply 1-2% of Asia’s food (and that is if we double our current production). The rising Asian middle class presents a timely opportunity for Australian agriculture. Faced with overwhelming issues of food safety and polluted arable land, this section of the Asian population is willing to pay premium prices for safe, clean food. Australia, having some of the cleanest and least contaminated agricultural land in the world, coupled with our geographical proximity to Asia, is arguably best situated to meet this demand.

It is crucial that Australia obtains a Free Trade Agreement (FTA) with these Asian countries so that our exports are on a level playing field with the rest of the world. In addition, it is important that we obtain FTAs that are favourable to agriculture and favourable across all agricultural sectors.

Obtaining such FTAs requires pro-active

industry marketing. Agriculture is one of the most highly protected industries for trade especially in Asia. Governments are reluctant to remove agricultural barriers to trade, in particular phytosanitary barriers, which protect against pests and disease and ensure domestic food supply. Removing agricultural barriers to trade needs to be advocated on a sector by sector basis with strong industry participation and pro-active marketing to obtain favourable terms of trade.

The Australia-Korea FTA demonstrates the need for pro-active marketing from the agricultural sector. Only a handful of agricultural sectors obtained better terms of trade, with the overall agricultural benefit being relatively low. The successful agricultural sectors were those in which farmers actively sought and petitioned for access, where farmers travelled to Korea, built business relationships and found market access for their products.

Under the current situation there is only a small fraction of Australian farmers making efforts to gain access to the Asian markets. If more efforts are not made, Australia will lose to other countries who are actively building business relations and negotiating access. On 26 June 2014 Citrus Australia signed an agreement with the Chinese Agricultural Wholesale Market Association (CAWA) to cement trade relationships. On the 24 June 2014, 21 CAWA delegates made an inaugural trip to Australia that was hosted by Citrus Australia. However, soon after when Citrus Australia held an event in collaboration with CAWA to bring together industry participants from Australia and China, there was only one Australian farmer recorded, with participation from other nations far outweighing that of Australia.

So why are a large proportion of Australian farmers not utilising this opportunity and pro-actively trying to obtain market access? Farming in Australia has traditionally been a lifestyle rather than a business. After years of drought, decreasing farm-gate return and increased competition, farming is no longer the ‘ideal’ lifestyle it once was. Family farms are being sold and the younger generation are being encouraged

to leave the family farms and seek work in other industries.

The solution is corporatisation of Australian farms. The only way this can be done is through educating the next farming generation. The role of a farmer is becoming much larger than it once was. Today farmers must produce the crops, but they also need to market the crops, sell the crops and manage the business aspect, which spans from keeping accounts to obtaining finance and addressing corporate responsibility. Entering the Asian century and accessing the markets discussed above is yet another task Australian farmers need to take on board.

We must not go down the track of selling our family farms. Instead, we need to educate our farmers and equip them with the skills to access the high-end Asian market. In educating our farmers and moving into the Asian century emphasis needs to be placed on collaboration. Rather than trying to access the markets ourselves, we should focus on collaborating with our Asian counter-parts.

This article points out that the inevitable trend of rising costs and wages will take Australian exports off global markets and force Australian farmers to sell their farms. To ensure our exports continue to be competitive we must access the high-end Asian consumer market where we can obtain premium prices by utilising our competitive advantage of supplying safe, clean food. To access these markets requires agriculturally favourable FTAs. In a highly protected industry this can only be achieved by strong Asian engagement by our farmers. Our next generation of farmers need to be equipped with the expertise, knowledge and motivation to access the Asian markets, engage with Asian counter-parts, negotiate favourable terms of trade and maintain strong business relationships. Educating our farmers to corporatize their farms and access the upcoming markets will ensure Australian agriculture is viable into the future and that it continues to be the innovative and highly developed industry it is today.

|Words By Alanna Rennie

09 George Street Review

The Answer to Australia’s Global Future

10 George Street Review

DOES TAX EQUATE TO

HAPPINESS?|Words By Joy Du

�� George Street Review

In some countries, a high tax rate really does equate to happiness. Denmark is one of the most highly taxed countries on the planet, having a top marginal tax rate of about 66%. Furthermore, they pay a 25% GST rate. Yet the Danes are one of the happiest nations despite paying such high taxes. Why is this?

Whilst forking out heaps of money may not make people happy, the benefits that a higher tax rate has might just be enough. Many Danes seem satisfied that they are getting their money’s worth – that is, they enjoy the tangible benefits of the high tax rates. This is seen through their universal health care, tuition-free education at tertiary level, employment benefits as well as security. As such, most people in Denmark think that their tax rate is appropriate, and more than one in ten think that they don’t pay enough.

Danish society is also fairly democratic, albeit without the bureaucracy that dominates many other countries with high-quality and numerous social services. What is interesting about Danish public policy, in particular the Danish health care system, is that it is clearly based on ‘social values’, with the people being motivated to pay for this system through higher taxation. Interestingly enough, various surveys have shown that Australians are prepared to pay higher taxes for their health care.

In stark contrast to Denmark, Australia has seen the toughest Federal Budget since 1997 in an effort to repair the budget. This has meant spending cuts and increased taxes to generate policy savings on a scale not seen for the better part of two decades. For example, there will be a temporary budget repair levy of 2% on the part of a person’s taxable income which exceeds $180,000, which will apply for the next three financial years. Whilst this is just one example of one of the recent tax changes, the general consensus is that the Australian population is not particularly pleased with these changes.

Maybe what Australia needs is to be able to see the tangible benefits of raised taxes. Whilst no tax system is perfect, the Australia tax system could probably learn a thing or two from the Danish one.

�� George Street Review

1� George Street Review

Now that the global financial crisis has eased, should Australia change its approach to financial regulation in a more globally competitive market?

In April this year, the Australian Securities and Investments Commission (ASIC) proposed a series of reforms to ensure that ASIC is better able to contribute to our new economy after the GFC. The comprehensive review of Australia’s financial system aimed to, according to the report released by ASIC, ensure that our financial system is able to meet the needs of Australian households and businesses into the future.

But, as the question was so adequately put by CPA Australia, why change something that isn’t broken? Australia was one of the few nations with an economy and financial structure and planning that was strong enough to survive the GFC relatively unscathed. While this may be the case, it is complacent to do nothing and merely wait until another crisis unfolds; this time with potentially more severe repercussions. ASIC’s review and evaluation of our financial system was still necessary and essential if Australia wishes to maintain a comfortable financial position in the domestic and national markets.

With the increasingly global economy, it is possible that Australia will be left behind if it does not, at some time in the future, begin to make plans to expand its current

approach to financial regulation so that it applies to a more globally competitive market. While international regulatory bodies will undoubtedly take a more dominant role in the regulation of the market, Australia must remember to act proactively in its own interests.

There is no doubt that the Australian economy fared far better during and after the GFC than others. Australia even fared better than some of the largest economies in the world. However, it would be wrong to leave the comparison at such a basic level.

One of the many, yet extremely important reasons that Australia was able to survive the GFC was because of the uniqueness of our market. Our financial market fails to reflect the same trends that are common in the larger financial markets of the world. As such, Australia cannot rely solely on international bodies for international financial regulation of the market. Despite some firms stating that national approaches to international financial regulation will cause disparities at an international level, it is essential to consider the need for smaller markets to implement their own financial regulation in a global market. The regulatory reforms that are most likely to be brought in by international regulatory agencies will be based on trends and data from the largest financial markets in the world. The Australian financial market and the financial markets of other smaller economies will not be reflected in this data. Hence, ultimately, leaving global financial regulation to international bodies could harm our economy, and work counterproductively for our financial market.

The only way Australia can attempt to determine its position in the global financial market is if Australia becomes heavily involved in international regulation of the financial markets. This is the only way to ensure that our national economy and global prospects are protected – by ensuring that all international regulatory bodies are aware of Australia’s position on financial regulation.

FINANCIAL REGULATION

FOR A GLOBAL MARKET

|Words By Jessica Howe

�2 George Street Review

�3 George Street Review

Australia’s two-speed economy has been a contentious issue over the past decade. Recent falls in commodity prices, lower demand from Asian consumers and a plateau in mining construction investment have proved detrimental for the Queensland and Western Australian economies. Times ahead will be tough for the resource and mining sector, but Australia as a nation has much more to gain then we have to lose if government action is taken to safeguard our future in other key industries.

Firstly, what damage has an overreliance on the resource and mining sector caused to our resource rich Australian states? Iron ore prices are now at a five year low, falling over 40% in the past year alone. A continuing fall in Chinese manufacturing output has equated to lower demand from Australia’s largest iron ore export partner. This fall in demand, coupled with a surge in export volumes from Australia’s three largest producers, BHP Billiton, Rio Tinto and Vale, have hit the junior miners hard. With the big three Australian iron ore producers’ break-even point relatively low, starting at a mere $44 per tonne for BHP, juniors such as Western Desert Resources and US-based Cliff Natural Resources have felt the pinch, either offloading their iron ore assets or collapsing entirely.

Conversely, the recent base metal price plummet and fatigue in demand from our Asian exports are not simply contained to big business; overreliance in the Western Australian and Queensland economies on mining and resource investment have sent these states alarmingly close to recession. Although export volumes are set to increase to levels close enough to fill the void in sale prices, a continuing slide in base metal prices, and the fact that mine production is significantly less labour exhaustive than mine construction, forecast increasing unemployment and significantly lower royalties for the western state.

Whilst mining growth and investment remain sluggish, the future is promising for Australia’s other major industries on the eastern seaboard. Record low interest rates, a buoyant property market and increases in real household disposable income are all positive signs for the New South Wales and Victorian economies. New South Wales and Victoria have reported modest growth in the retail sector, posting growth of 8.1% and 7.2% respectively. Additionally, manufacturing PMI, an indicator of manufacturing sector health, is showing some signs of a recovery with values forecast to rise to more sustainable and beneficial levels.

Although the mining and resource sectors are still ploughing ahead in Western Australia, Queensland and the Northern Territory, it is essential that current and future governments continue to emphasis growth in Australia’s other key industries, particularly manufacturing, to safeguard Australia’s future. Future governmental policy must be aimed at fostering a healthy, resilient and world-class manufacturing, education and tourism sector. Our overreliance on commodity exports will prove to be fatal to Australia’s future prosperity, unless we can strive for a balance between all of our key industries.

A Rebalancing Act Safeguarding Australia’s Future

|Words By Blake Nicolson

�3 George Street Review

1� George Street Review

CO

MPE

TITIV

ENES

SIS

KEY

As investment in Australia’s mining sector declines, government policy is critical in facilitating Australia’s competiveness on a global scale. Australia has experienced strong growth over past two decades, however strong policy decisions are required in order to maintain this growth into the future.

In order to lift competitiveness on a global scale, Australia needs to adopt a sector-based approach. This involves using government policy to maximise growth in industries identified as having a competitive advantage. According to the BCA, these core industries include agriculture, resources, tourism, highly-differentiated manufacturing and international education. These industries have the greatest potential to achieve a global presence and generate wealth.

For those industries that are not identified as having a competitive advantage, the BCA recommends removing all barriers to lowering costs in these sectors, in order to

facilitate stronger competition. While some sectors may not have a high capacity to win on a global scale, often these industries are critical as they employ a high proportion of the workforce. Ensuring that these sectors are competitive is the best way to provide job security and improve productivity.

This sector approach to growth has been successfully adopted by New Zealand, South Korea, United States and China. New Zealand in particular has created a globally competitive dairy industry by introducing targeted legislation and entering free trade agreements.

Ultimately, innovation and competitiveness is key for Australia to achieve strong ongoing growth. By reducing barriers to competitiveness and strengthening sectors with acknowledged competitive advantages, Australia will best align itself for the future.

Which sector will be able to provide sufficient impetus to offset the decline in the investment growth in the

mining sector?

|Words By Jonathan Colak

�5 George Street Review

It’s no secret that Australia’s business tax levels are amongst the highest in the developed world. CPA Australia’s Head of Business and Investment Policy, Paul Drum, is just one of many industry professionals who have put forward the notion that our country’s high business tax rate does not augur well for international competitiveness. Tony Abbott’s election promise of a shift from a 30% to 28.5% corporate tax rate is definitely a step in the right direction in regards to Australia’s international competitiveness.

However, as indicated in the Henry Tax Review (headed by Dr Ken Henry, former Treasury Secretary), since we sit near the top of the small to medium size OECD economies in regards to tax rates, we must reduce the company income tax rate to 25 percent over the short to medium term to ensure that Australia remains an attractive place to invest.

When looking at Australia’s tax regime, while it is important to consider corporate level business, as tax receipts from this sector do amount to approximately 4.5% of GDP, it is also important to look at the impact on small business. Up until recently small businesses were at the mercy of thin capitalisation rules, which are not allowing a large majority of business operators access to tax concessions, a dismally low-value asset threshold which does not allow business owners to write off assets above $5000, and exempt dividend rules, which are negatively affecting the international competitiveness of small businesses.

Much like at the corporate level the Abbott government

is now taking steps to change the legislation pertaining to tax on small business, in order to keep Australian business competitive on an international scale. However, once again according to the Henry Review, the government is still not doing enough to bring Australia on par with its international competitors.

Along with international competitiveness the concern of multinational tax avoidance and profit shifting is impossible to ignore, when speaking in regards to

Australian business tax reform. The Economics Committee of the

House of Lords in the UK and the Australian Treasury

both led inquiries and released reports that build on the OECD Action Plan on Base Erosion and Profit Shifting, which concluded that the base tax revenue that the government receives from

these corporate companies may be at

risk. The OECD report reflects that the “current

international tax standards may not have kept pace with

changes in global business practices” and “the tax practices of some multinational

companies”. One example of concern is the different treatments of debt and equity finance tax, and the effect this can have on the tax burden of some substantial multinational companies.

In summary, Australia’s current tax regime has a long way to go before becoming competitive on the world stage, with the government needing to consider many factors as they shape the future of the country’s taxation system.

A Slow Approach

To Tax Reform

|Words By Jordan Kuhnemann

�5 George Street Review

1� George Street Review

UPDATE: UNEMPLOYMENT

It could be safely said that the phrase “pleasant surprise” is not often used in relation to economic figures. However, the Australian Bureau of Statistics’ (ABS) latest release on national employment figures presented a surprising increase of 121,000, pushing the total level to 11.7 million - the largest increase in recorded history for Australia. As a result, this month’s unemployment figures have dropped to 6.1%, a significant decrease from the 6.4% figure of July.

These unexpected numbers have caused some to draw attention to the imperfections of the way employment data is collected. Doubt around the accuracy of the new figures has been expressed by ANZ’s chief economist, Warren Hogan, RBC capital market strategists, Citi economists and indeed, the Bureau itself. The ABS, however, upon looking for possible causes for the very high results, found no deficiencies in the data or the way it was collected that could account for this.

Despite questions about the exact extent of this raise, most critics have agreed that the economy is experiencing improved labour market conditions and that the figures suggest better job growth. For some however, the rosy figures have not translated into real outcomes. Youth unemployment, or employment of Australians between the ages of 15 and 24, remains at close to 15%. As ABC social affairs correspondent

Norman Hermant recently wrote, this is not the worst level in Australian history. But this is little comfort for young people looking for jobs, especially those with few skills or little training, or who have been out of employment for some time. In certain areas, particularly regional areas, levels are as high as 21%. With such high rates, and such a disparity between the national average and the average youth level, it seems that youth unemployment will remain an economic challenge for some time, as well as produce the obvious social and personal detriments.

Another concern that remains in the employment field is that of the created jobs, with a mere 14,300 being full-time positions. Coupled with increases in the number of employed people wishing to work more hours, underemployment appears to continue to be an issue. Promisingly, however, increases in job growth were not outweighed by increases in the participation rate.

Overall, Australia’s employment situation seems to be improving, especially in the face of suggestions that the US has passed its unemployment woes to Australia. However, in the cautious and hesitant post-GFC environment, we still have areas for improvement, particularly in relation to young people.

|Words By Sally Moore

�7 George Street Review

Good news, everyone. If the experts are to be believed, merger and acquisition activity is about to ramp up around the world in a big way. This means that there are share market profits on offer for investors who know where to look. Many experts say that conditions globally are in a Goldilocks zone for consolidation, especially given the low interest rate levels.

With current benign growth expectations, reasonable equity valuations and very cheap finance, there seems to be an ideal mix for merger and acquisition activity.

Picking up on this theme, Credit Suisse has singled out the Australian stocks it believes will benefit most from the uptick, in an environment where it says it is cheaper to buy than build.

It also says that investors should be tilting their portfolios toward M&A strategies as the activity heats up. The place to start, it says, is stocks that will have roles in

all of the action, such as Computershare and Macquarie Group.

Picking specific targets is a little harder, but Credit Suisse says you couldn’t do worse than focus on names that have been the subject of intense takeover speculation in the past.

For those who like to look overseas, the experts say cashed-up US corporations with offshore funds are the obvious place to look for foreign M&A. Generally speaking, without seeing significant large growth opportunities, companies will opt for the easier way to grow earnings, which could be by making acquisitions, cutting costs and synergies. Their targets will most likely be companies with clean balance sheets that are very highly rated by the bond market, thereby suggesting that these companies will be mid to large firms.

|Words By Dylan Master

Activity Means OpportunityM&A

1� George Street Review

Taming theExcel is one of the most widely used and important business tools on the planet. It has a vast array of features and functionality that can assist business professionals in many aspects of their work. However, many often find it quite difficult to use, particularly when they are unaware of its full capabilities. Here are two tips that will help make you more productive and allow you to make better use of what Excel has to offer.

|Words By Mark Johnman

Tip #1: Naming Normally when you look at formulas created in Excel, you see cell references, such as =A1 * B1. However, just by looking at these formulas, it is impossible to tell what they are calculating. As formulas get more complicated, this problem only becomes more significant. By naming cells, you can give them meaningful names that make it much easier to understand what your formulas are doing. For example, a formula such as =Quantity * Unit_Price is much easier to understand than =A1 * B1.

To name cells, highlight the selection of cells that you want to name, go to the Formulas tab and click Define Name. Spending an extra 10 seconds to do this will improve the readability of your spreadsheets and help you remember what’s going on!

Tip #2: Goal Seek

Goal Seek is a very useful tool for optimizers, consultants and forecasters. Essentially, it allows you to work backwards and find what input is needed to produce a certain answer to a formula.

For example (see opposite page), say you wanted to find out how many units of a product that you need to sell in Month 3 to generate $100,000,000 in total revenue.

By using Goal Seek, you can calculate this very quickly (assuming all of the formulas – e.g. Total Revenue = SUM(Quantity*Sales) for presales and the three months – are already in place). Firstly, go to the Data tab, What-If Analysis and click Goal Seek.

�8 George Street Review

�9 George Street Review

Excel Beast

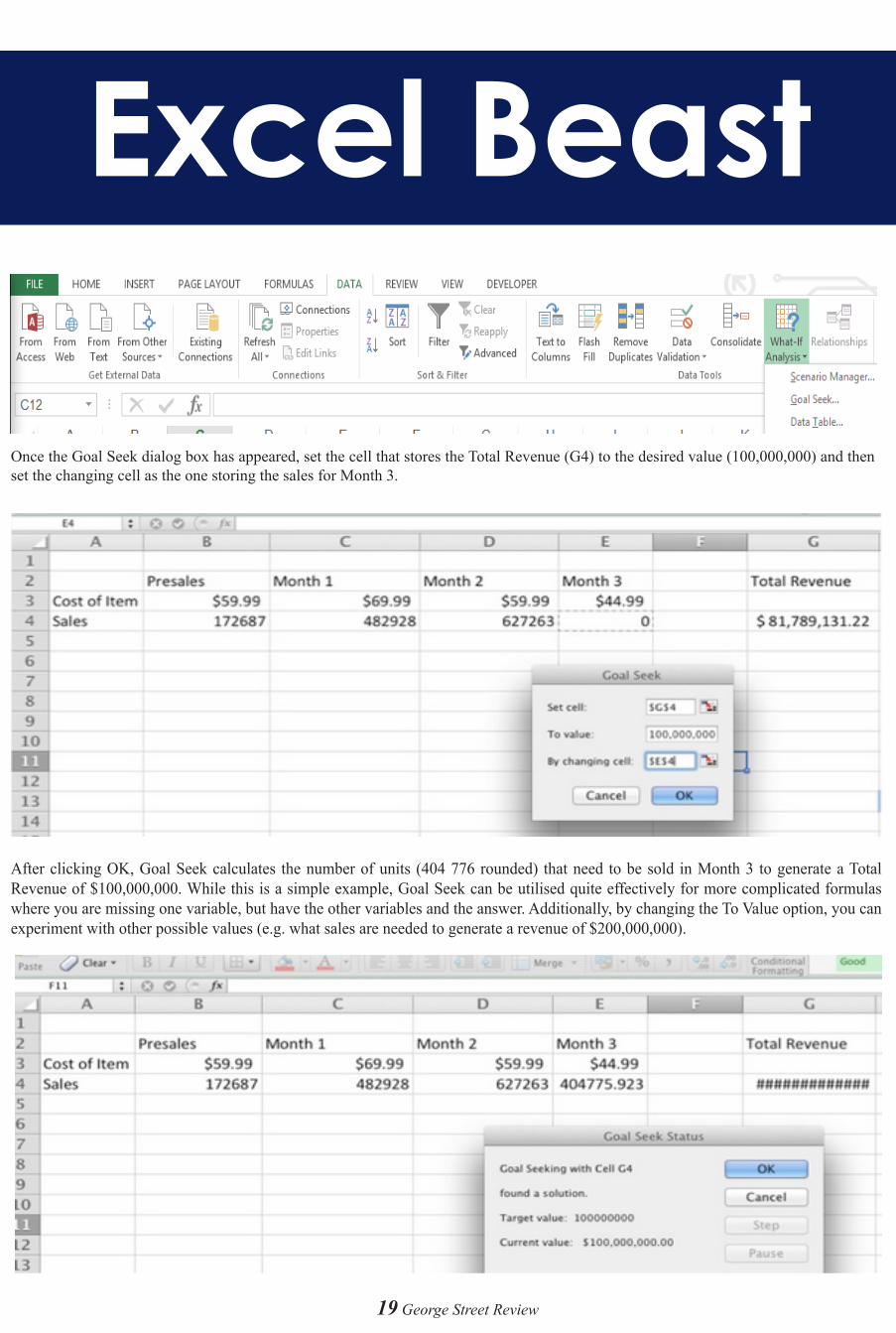

Once the Goal Seek dialog box has appeared, set the cell that stores the Total Revenue (G4) to the desired value (100,000,000) and then set the changing cell as the one storing the sales for Month 3.

After clicking OK, Goal Seek calculates the number of units (404 776 rounded) that need to be sold in Month 3 to generate a Total Revenue of $100,000,000. While this is a simple example, Goal Seek can be utilised quite effectively for more complicated formulas where you are missing one variable, but have the other variables and the answer. Additionally, by changing the To Value option, you can experiment with other possible values (e.g. what sales are needed to generate a revenue of $200,000,000).

�9 George Street Review

�0 George Street Review

BONDINVESTMENTGROUP

CHALLENGE YOUR PERCEPTIONS.think BIG.

Related Documents