FOREIGN CURRENCY CONVERTIBLE BOND PRESENTED BY:- Poonam Achraya A010 Ayushi Agrawal A014 Deepashikha Godbole A029 Apeksha Narula AO42 Vidhi Agarwal A073

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

FOREIGN CURRENCY CONVERTIBLE BOND

PRESENTED BY:-

Poonam Achraya A010 Ayushi Agrawal A014 Deepashikha Godbole A029 Apeksha Narula AO42 Vidhi Agarwal A073

INTRODUCTION

• Foreign currency convertible bonds (FCCBs) are a special category of bonds.

• These bonds assume great importance for multinational corporations and in the current business scenario of globalisation, where companies are constantly dealing in foreign currencies.

• FCCBs are quasi-debt instruments and tradable on the stock exchange. Investors are hedge-fund arbitrators or foreign nationals.

• FCCBs appear on the liabilities side of the issuing company's balance sheet.

• External Commercial Borrowing (ECB) Guidelines:

• FCCB means a bond issued by an Indian company expressed in foreign currency and the principal and interest in respect of which is payable in foreign currency.

Issue of Foreign Currency Convertible Bonds and Ordinary Shares (Through Depository Receipt Mechanism) Scheme, 1993: FCCB means a bond issued in accordance with this scheme & subscribed by a non-resident in foreign currency & convertible into ordinary shares of the issuing company in any manner either in whole or in part, on the basis of any equity related warrants attached to the debt instrument.

ISSUANCE OF FCCB :

• Through Depositary Receipt Mechanism Scheme, 1993.

• GUIDELINES FOR ISSUE :a. FCCBs are hybrid instruments standing between debt and equity b. Issued by a Indian Company in foreign currencyc. Gives its holders the right to convert for a fixed no of shares at a pre-determined price d. Convertible into Equity at the option of the holder; normally at a premium of 20% to 30% over prevailing market price at the time of issuee. Cash redemption value

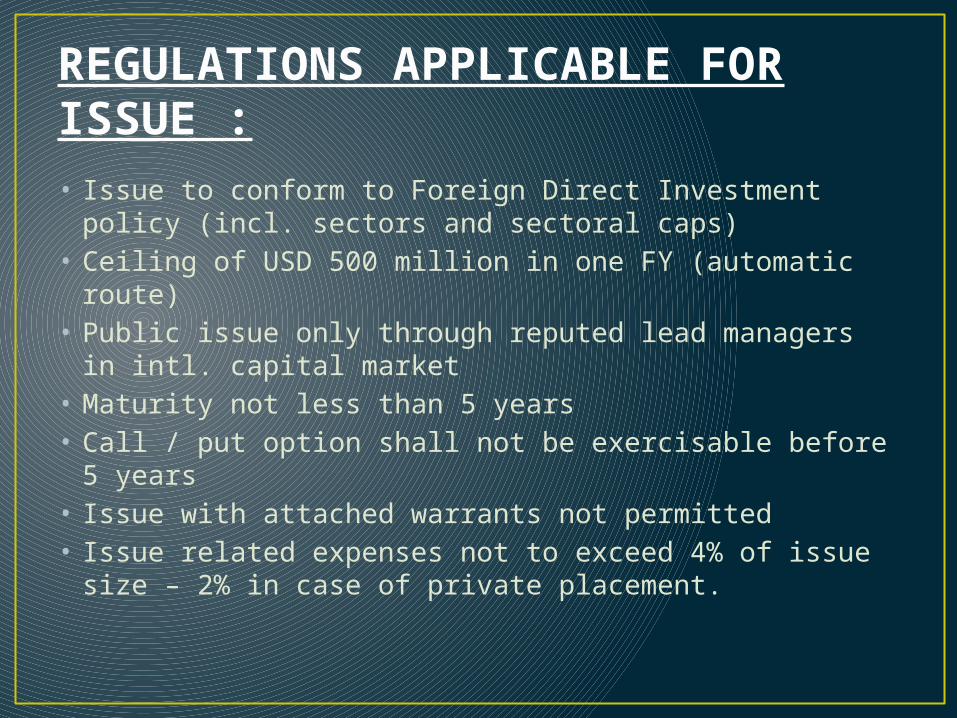

REGULATIONS APPLICABLE FOR ISSUE :

• Issue to conform to Foreign Direct Investment policy (incl. sectors and sectoral caps)

• Ceiling of USD 500 million in one FY (automatic route) • Public issue only through reputed lead managers in intl. capital

market• Maturity not less than 5 years • Call / put option shall not be exercisable before 5 years• Issue with attached warrants not permitted• Issue related expenses not to exceed 4% of issue size – 2% in

case of private placement.

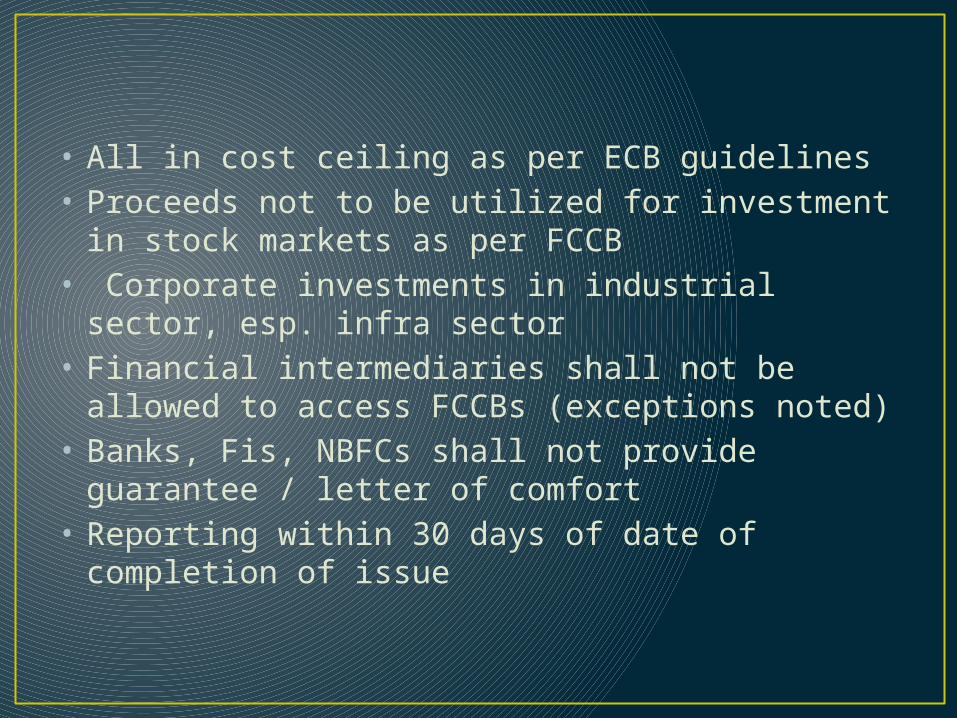

• All in cost ceiling as per ECB guidelines• Proceeds not to be utilized for investment in stock markets as

per FCCB • Corporate investments in industrial sector, esp. infra sector • Financial intermediaries shall not be allowed to access FCCBs

(exceptions noted) • Banks, Fis, NBFCs shall not provide guarantee / letter of

comfort• Reporting within 30 days of date of completion of issue

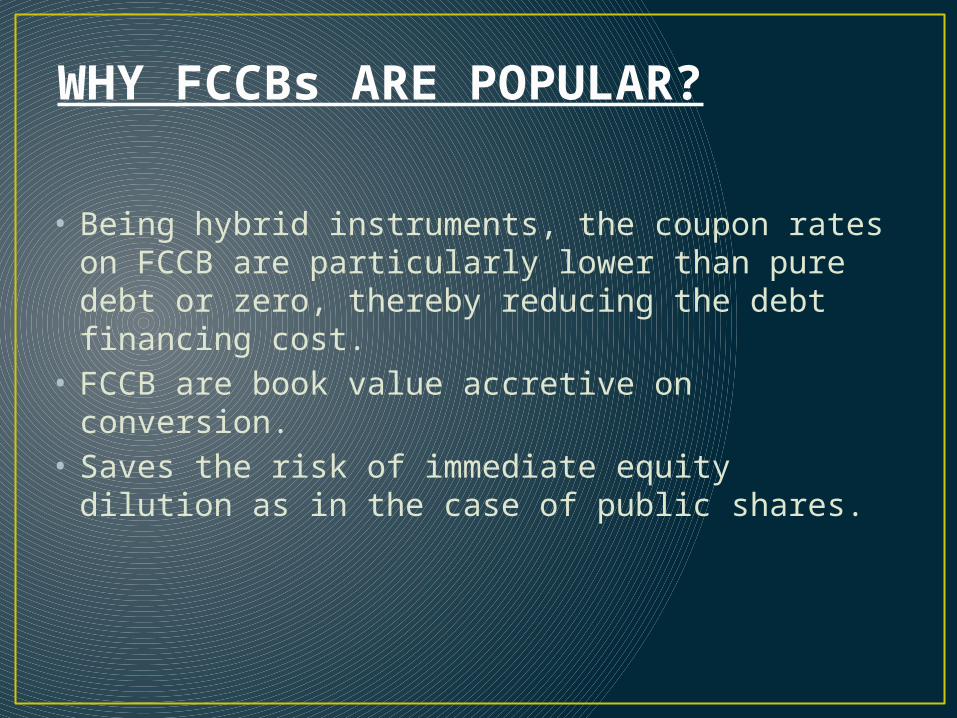

WHY FCCBs ARE POPULAR?

• Being hybrid instruments, the coupon rates on FCCB are particularly lower than pure debt or zero, thereby reducing the debt financing cost.

• FCCB are book value accretive on conversion.• Saves the risk of immediate equity dilution as in the case of

public shares.

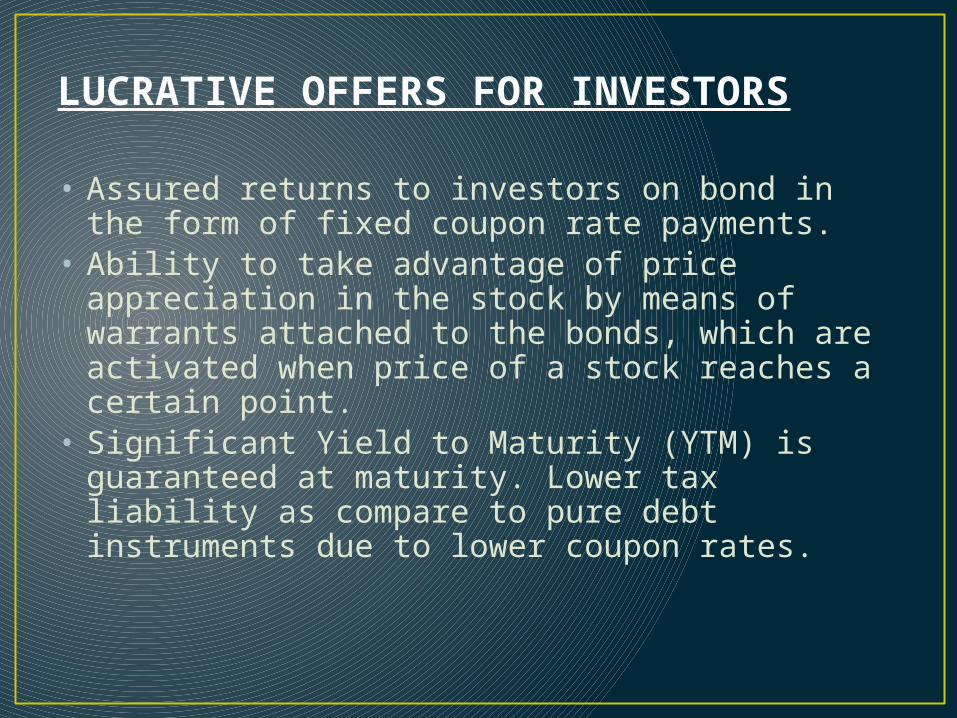

LUCRATIVE OFFERS FOR INVESTORS

• Assured returns to investors on bond in the form of fixed coupon rate payments.

• Ability to take advantage of price appreciation in the stock by means of warrants attached to the bonds, which are activated when price of a stock reaches a certain point.

• Significant Yield to Maturity (YTM) is guaranteed at maturity. Lower tax liability as compare to pure debt instruments due to lower coupon rates.

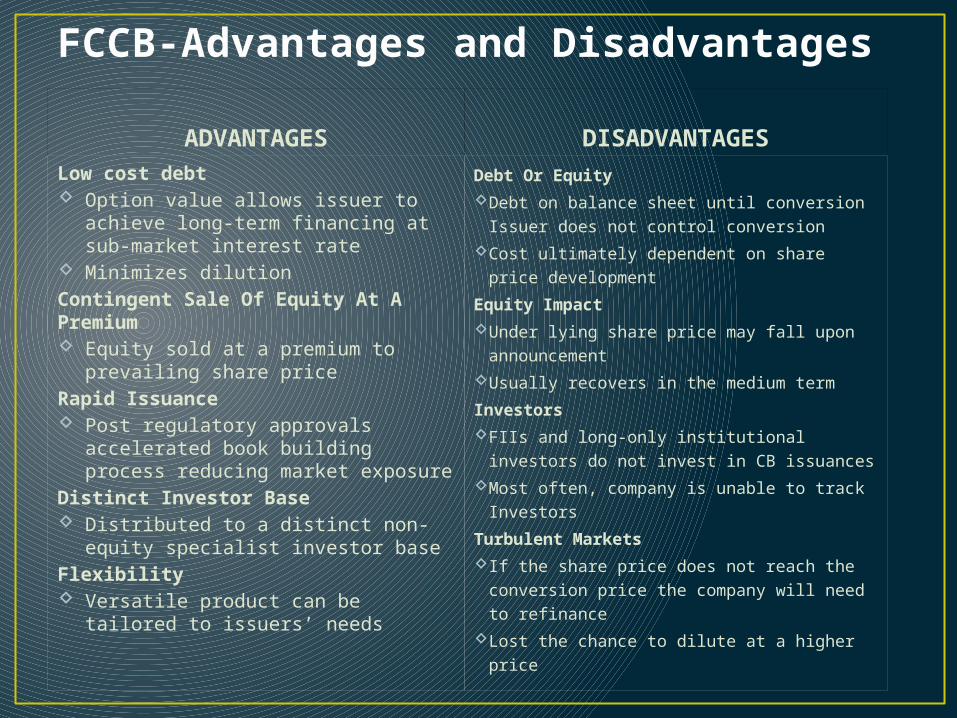

FCCB-Advantages and Disadvantages

ADVANTAGES

Low cost debt Option value allows issuer to achieve long-

term financing at sub-market interest rate Minimizes dilution

Contingent Sale Of Equity At A Premium Equity sold at a premium to prevailing share

price

Rapid Issuance Post regulatory approvals accelerated book

building process reducing market exposure

Distinct Investor Base Distributed to a distinct non-equity specialist

investor base

Flexibility Versatile product can be tailored to issuers’

needs

DISADVANTAGES

Debt Or Equity

Debt on balance sheet until conversion Issuer

does not control conversion

Cost ultimately dependent on share price

development

Equity Impact

Under lying share price may fall upon

announcement

Usually recovers in the medium term

Investors

FIIs and long-only institutional investors do not

invest in CB issuances

Most often, company is unable to track

Investors

Turbulent Markets

If the share price does not reach the conversion

price the company will need to refinance

Lost the chance to dilute at a higher price

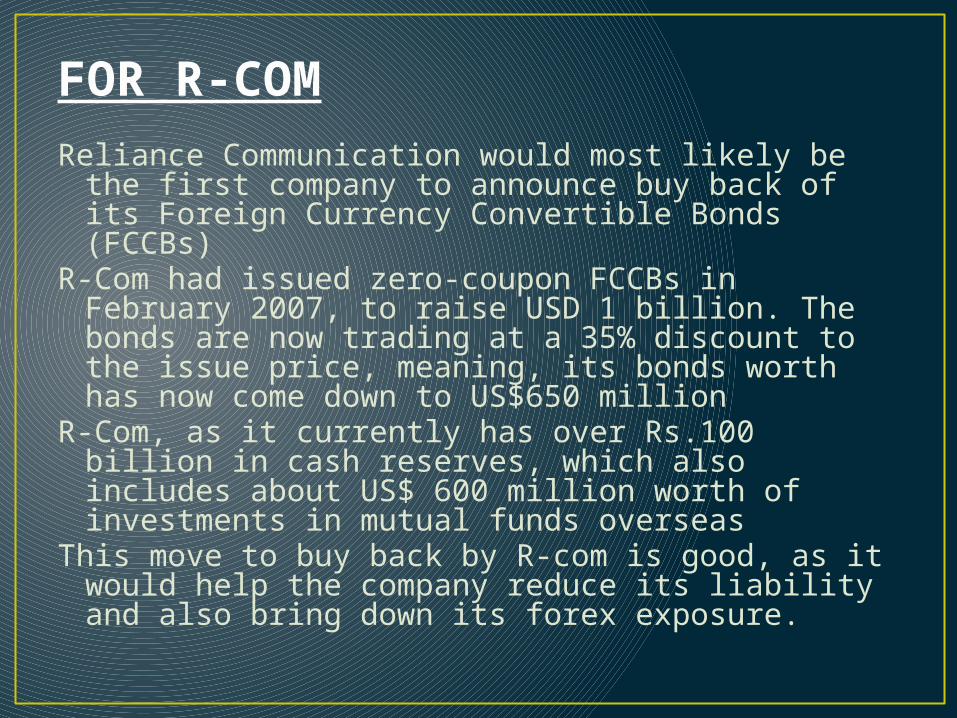

FOR R-COM

Reliance Communication would most likely be the first company to announce buy back of its Foreign Currency Convertible Bonds (FCCBs)

R-Com had issued zero-coupon FCCBs in February 2007, to raise USD 1 billion. The bonds are now trading at a 35% discount to the issue price, meaning, its bonds worth has now come down to US$650 million

R-Com, as it currently has over Rs.100 billion in cash reserves, which also includes about US$ 600 million worth of investments in mutual funds overseas

This move to buy back by R-com is good, as it would help the company reduce its liability and also bring down its forex exposure.

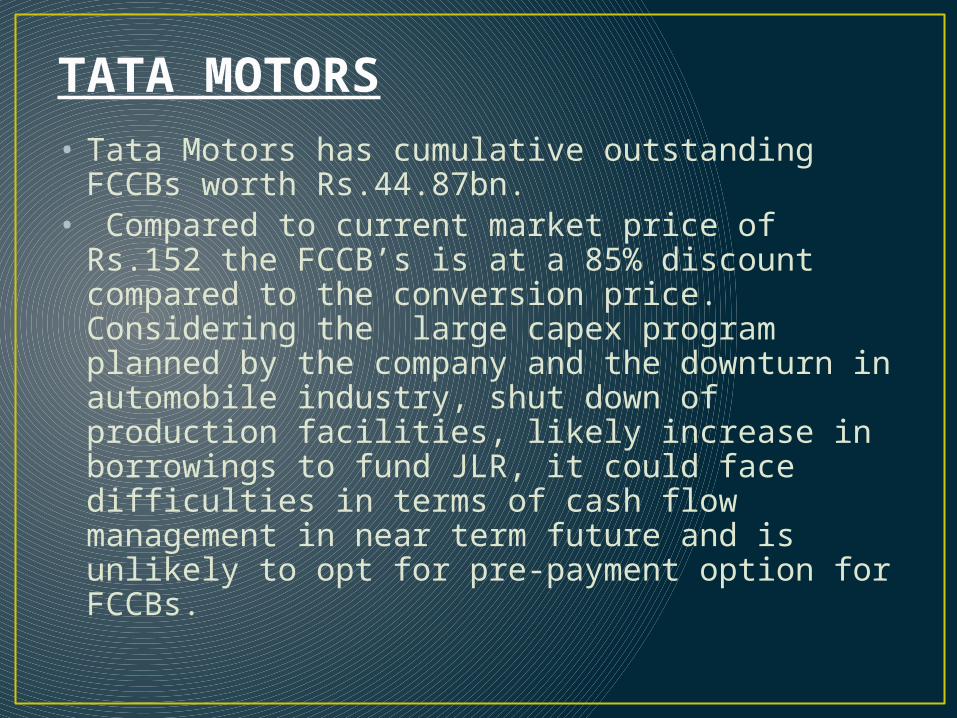

TATA MOTORS

• Tata Motors has cumulative outstanding FCCBs worth Rs.44.87bn.

• Compared to current market price of Rs.152 the FCCB’s is at a 85% discount compared to the conversion price. Considering the large capex program planned by the company and the downturn in automobile industry, shut down of production facilities, likely increase in borrowings to fund JLR, it could face difficulties in terms of cash flow management in near term future and is unlikely to opt for pre-payment option for FCCBs.

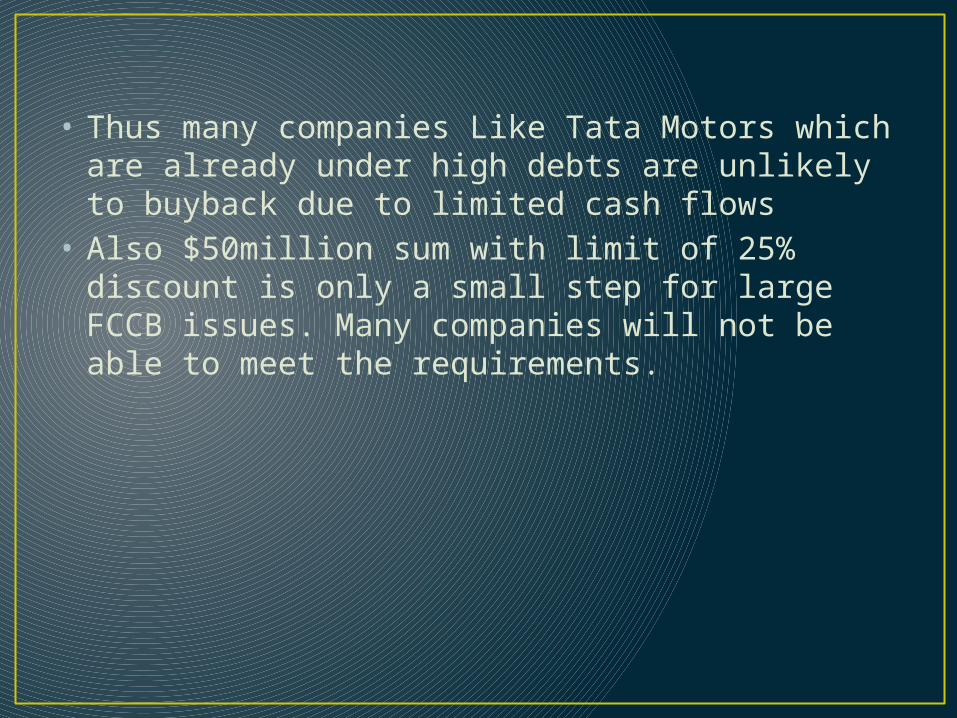

• Thus many companies Like Tata Motors which are already under high debts are unlikely to buyback due to limited cash flows

• Also $50million sum with limit of 25% discount is only a small step for large FCCB issues. Many companies will not be able to meet the requirements.

A b i t t e r P i l l

I n t o d a y ’ s fi n a n c i a l d o w n t u r n … •

C o n v e r s i o n p r i c e o f F C C B s h a s g o n e s e v e r a l t i m e s h i g h e r t h a nt h e i r c u r r e n t m a r k e t p r i c e

•I n v e s t o r s d i s i n t e r e s t e d i n c o n v e r t i n g t h e i r b o n d s i n t o e q u i t y

•R u p e e a t l o w , h i g h I N R p a y m e n t a w a i t i n g

A b i t t e r p i l l t o s w a l l o w f o r i s s u i n g c o m p a n i e s … •

S e a r c h f o r r e s o u r c e s t o r e p a y t h e d e b t w i t h f r e s h e x p e n s i v eb o r r o w i n g

•R e s e t t h e c o n v e r s i o n c l a u s e , t o b r i n g i t c l o s e r t o r e a l i t y - P o t e n t i a l

d i l u t i o n o f s h a r e h o l d i n g s1 0

W o c k h a r d t ’ s C a s e

• It is a pharmaceutical and biotechnology company headquartered in Mumbai, India.

• Given the precarious debt position that it was in, in April 2009, Wockhardt approached the domestic lenders for corporate debt restructuring (CDR) led by ICICI Bank. The lenders included domestic lenders, FCCB (foreign currency convertible bonds) holders, and other foreign lenders.

• FCCB hold an option to convert into shares or redeem the bonds

• FCCB holders filed ‘winding up petition’.

FCCB GOVERNED THROUGH RBI

• FCCB Guidelines were issued in 1993 by Ministry of Finance under the issue of Foreign Currency Convertible Bonds and Ordinary Shares (Through Depository Receipt Mechanism) Scheme, 1993.

• The RBI issues guidelines for External Commercial Borrowing(ECB) which is applicable to FCCBs.

TERMS AND CONDITIONS OF FCCB

• Initial Conversion Price: Min Conversion Price plus Conversion Premium

• – Minimum Conversion Price• – Conversion Premium: Normally 20% - 30%• Maturity Date: To meet the ECB guidelines of Average Maturity

depending• on the amount raised• Current Coupon: 0% - 5%• Yield to Maturity (YTM): Currently 6% - 8%• Redemption Price: In case the Bonds are not previously converted,

they are redeemed on the Maturity Date at principal plus YTM

• Fixed Exchange Rate: Generally fixed at the time of issuance of Bonds.

• Conversion Rights: Holder of Bonds have the right to exercise the option of conversion into Equity Share anytime before the Redemption Date.

• Conversion Price Reset: Normally linked to the market price of the Equity Shares or on every defined period; – Cannot go below the Minimum Conversion Price.

• Tax Gross Up: All payments made are generally Grossed Up.

CONCLUSION• Two to three years back Indian markets were on high growth

and FCCBs became popular for raising funds from overseas market. With the fall in the market, many FCCBs has gone down, which means no money and more problem in the market.

• Issuing companies will now have to search for resources to repay the debt along with redemption period whenever it matures. For this companies will seek to fresh borrowings, with high interest rates, which in turn would impact their profitability. Another option, which companies have is to reset the conversion clause, to bring it closer to reality.

THANK YOU!

Related Documents