Farmland Values and Leasing Key Questions Chapter 20 What determines the value of farmland? What are the advantages and disadvantages of owning vs. leasing? What are the common types of farm leases? How can a fair cash rent be determined?

Farmland Values and Leasing Key Questions Chapter 20 §What determines the value of farmland? §What are the advantages and disadvantages of owning vs. leasing?

Dec 14, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Farmland Values and LeasingKey QuestionsChapter 20

What determines the value of farmland?What are the advantages and disadvantages

of owning vs. leasing?What are the common types of farm leases?How can a fair cash rent be determined?

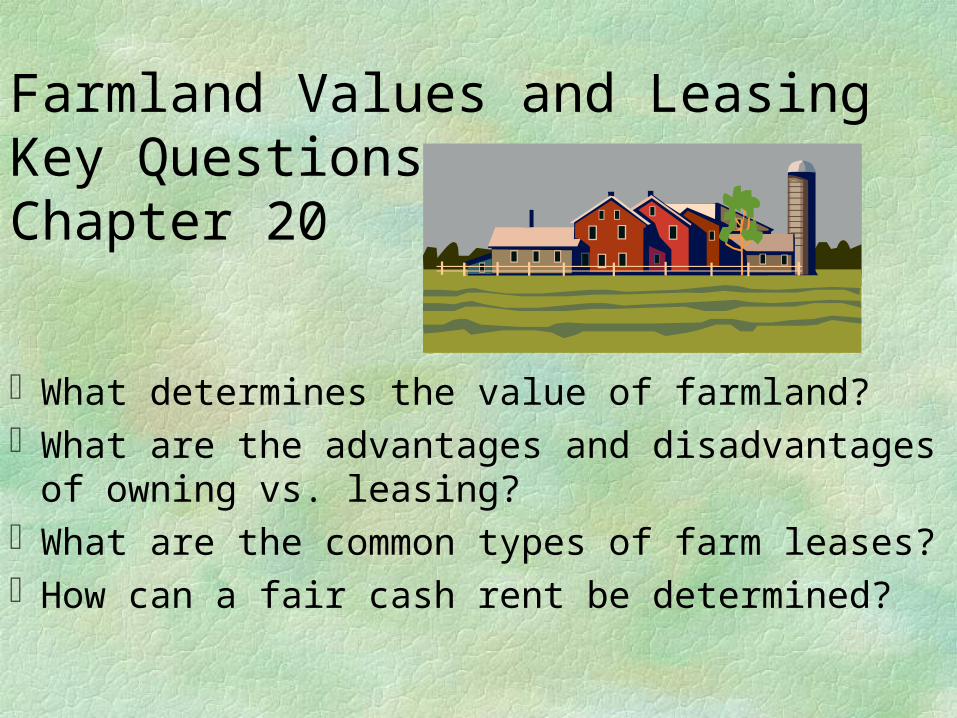

Average Iowa Farmland Value--$/acre

$0$250$500$750

$1,000$1,250$1,500$1,750$2,000$2,250$2,500$2,750$3,000$3,250

Land Value Trends in Iowa1973-1981

Increased export demand High grain prices Low interest rates High inflation rate

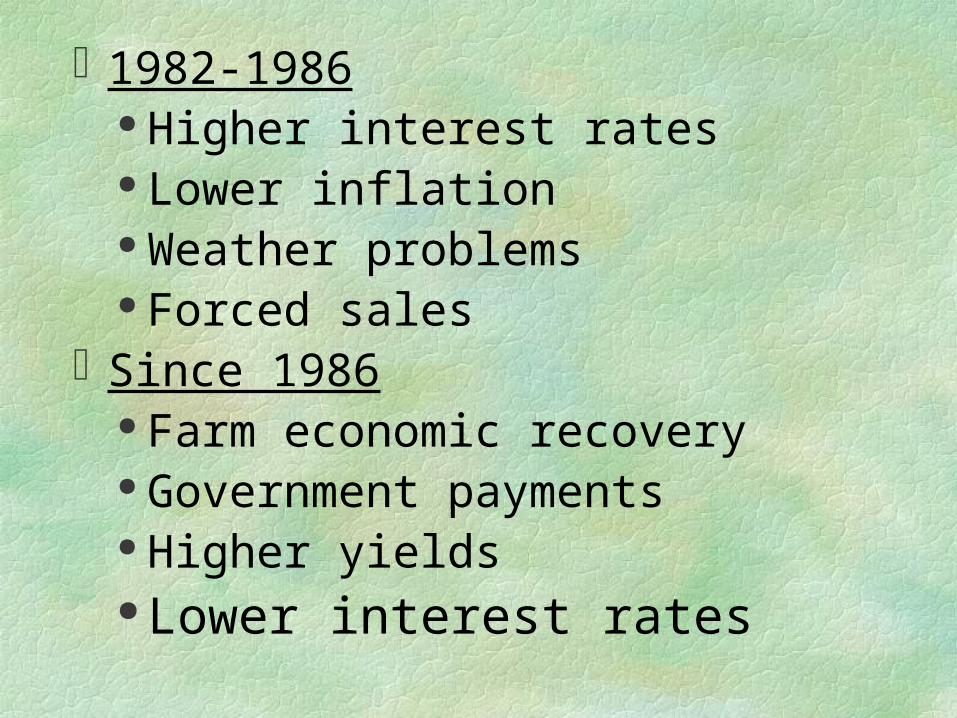

1982-1986 Higher interest rates Lower inflation Weather problems Forced sales

Since 1986 Farm economic recovery Government payments Higher yields Lower interest rates

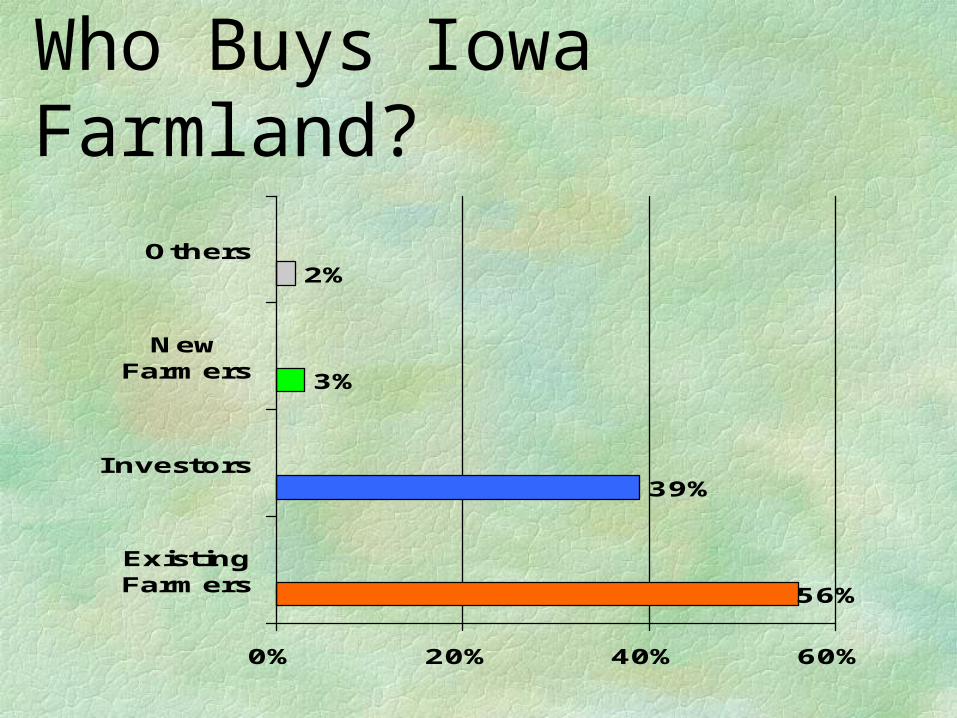

Who Buys Iowa Farmland?

56%

39%

3%

2%

0% 20% 40% 60%

ExistingFarmers

Investors

NewFarmers

Others

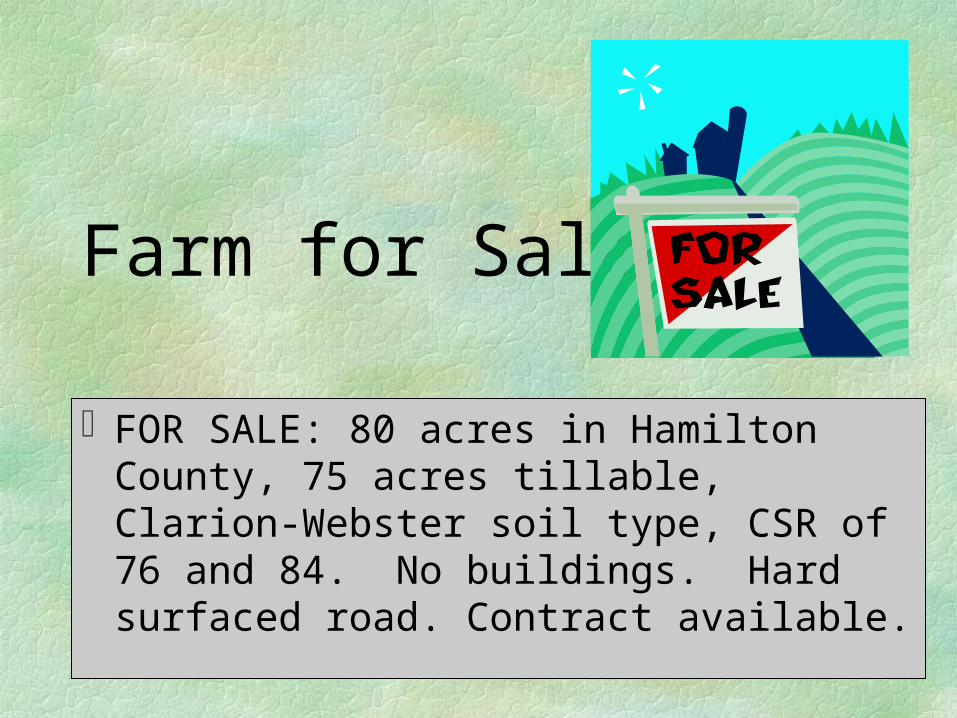

Farm for Sale

FOR SALE: 80 acres in Hamilton County, 75 acres tillable, Clarion-Webster soil type, CSR of 76 and 84. No buildings. Hard surfaced road. Contract available.

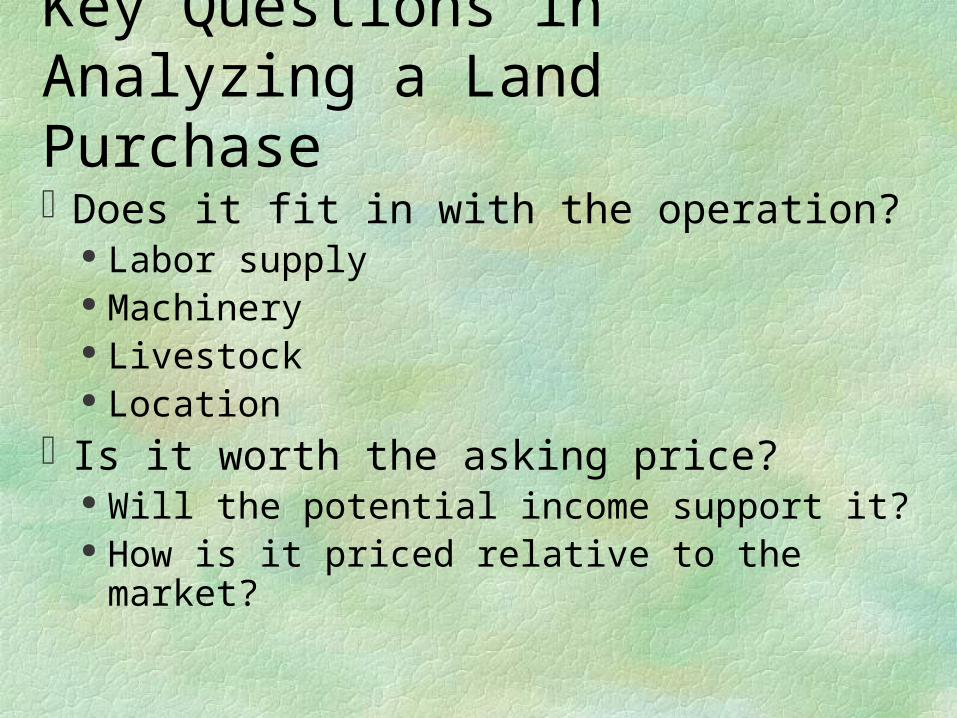

Key Questions in Analyzing a Land PurchaseDoes it fit in with the operation?

Labor supply Machinery Livestock Location

Is it worth the asking price? Will the potential income support it? How is it priced relative to the market?

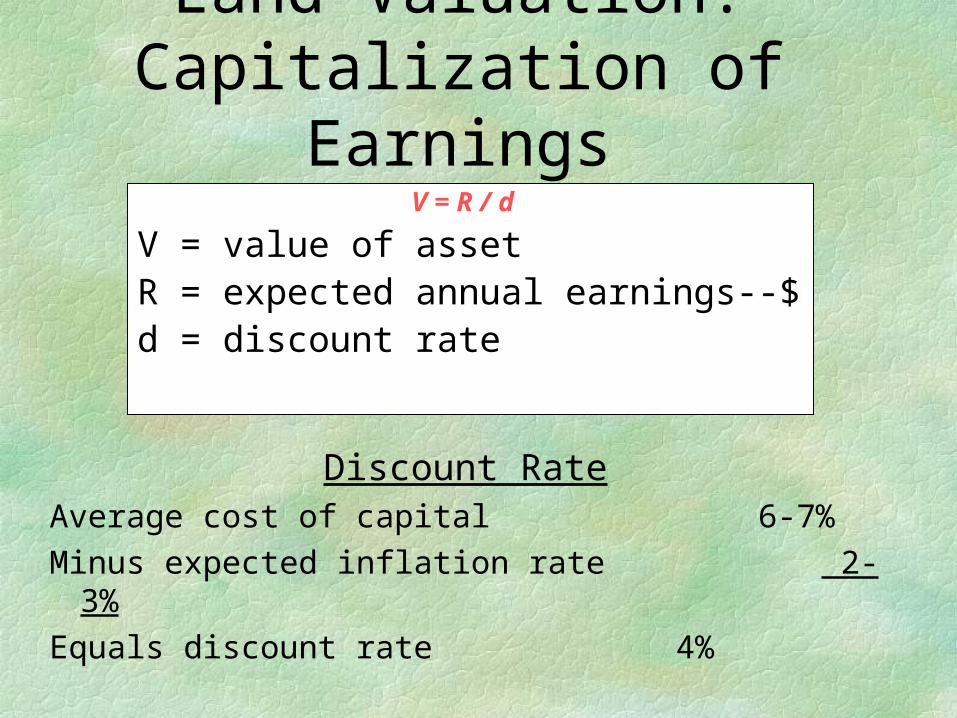

Land Valuation:Capitalization of Earnings

V = R / d

V = value of assetR = expected annual earnings--$d = discount rate

Discount RateAverage cost of capital 6-7%Minus expected inflation rate 2-3%Equals discount rate 4%

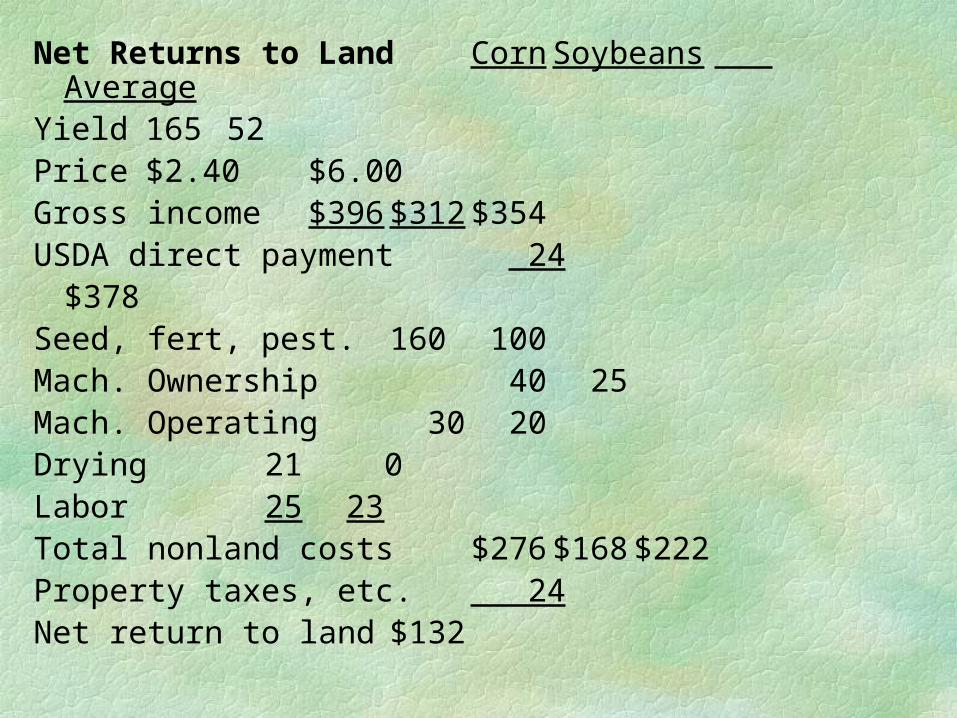

Net Returns to Land Corn Soybeans Average

Yield 165 52Price $2.40 $6.00Gross income $396 $312 $354USDA direct payment 24

$378Seed, fert, pest. 160 100Mach. Ownership 40 25Mach. Operating 30 20Drying 21 0Labor 25 23Total nonland costs $276 $168 $222Property taxes, etc. 24Net return to land $132

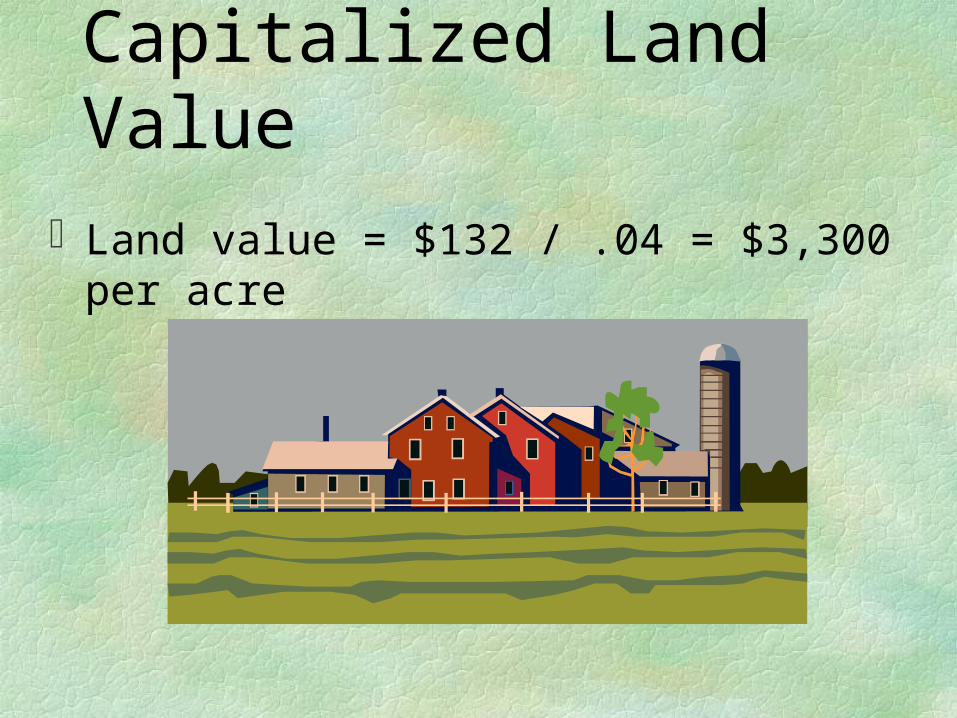

Capitalized Land Value

Land value = $132 / .04 = $3,300 per acre

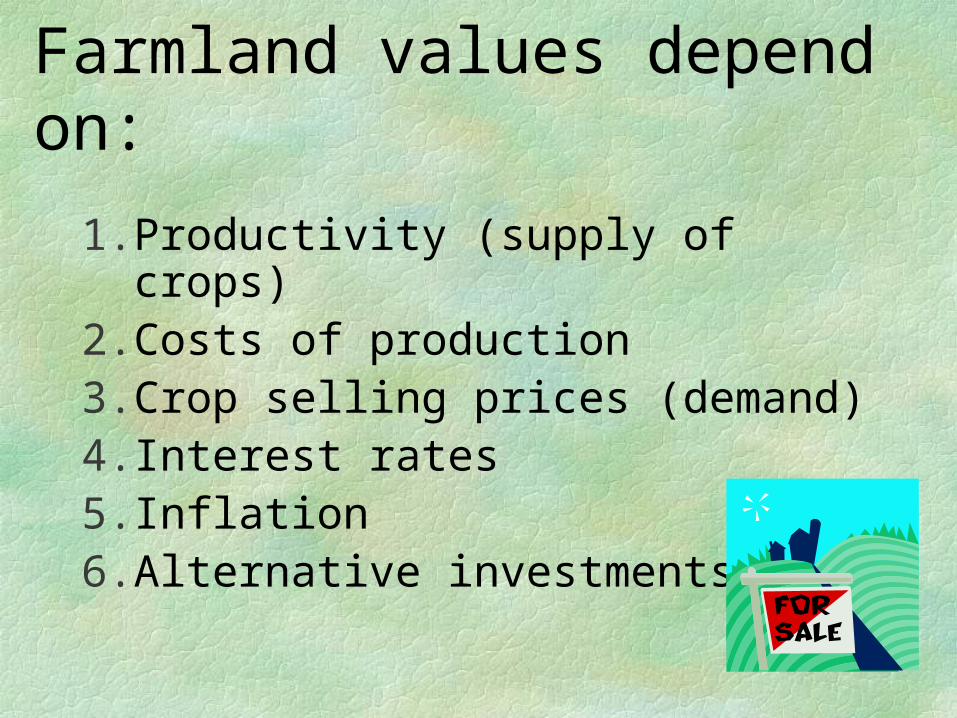

Farmland values depend on:

1. Productivity (supply of crops)2. Costs of production3. Crop selling prices (demand)4. Interest rates5. Inflation6. Alternative investments

Comparative Sales

Recent actual salesSimilar landSame area

Comparative SalesFactors to compare:Productivity +Location + or -Other uses/income + or -Family sales -Sales contract +Size of tract + or -

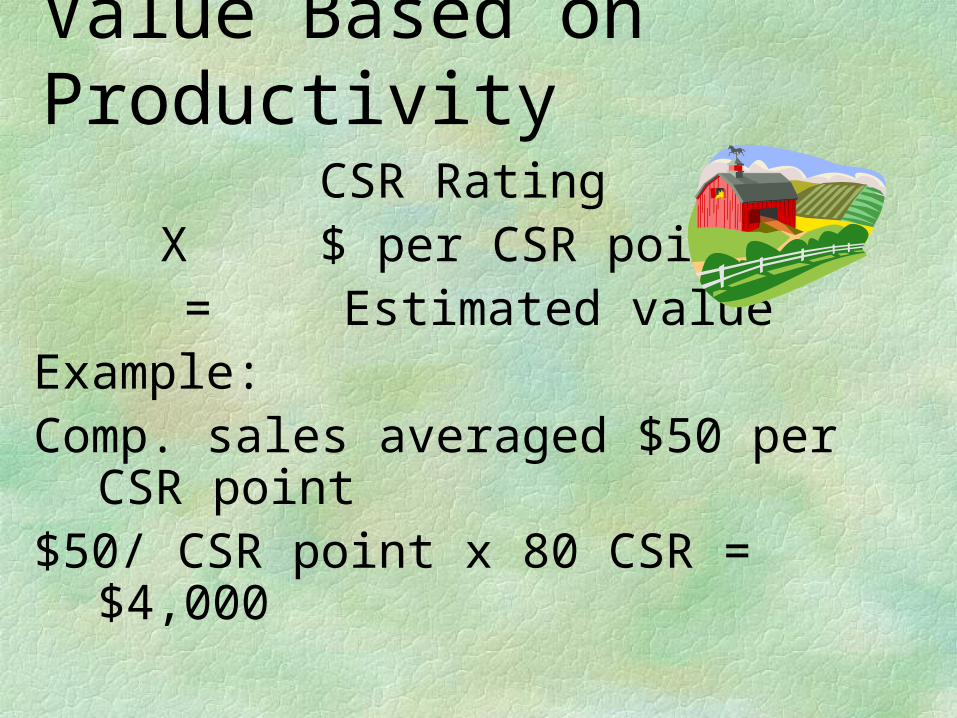

Value Based on Productivity

CSR RatingX $ per CSR point= Estimated value

Example:Comp. sales averaged $50 per CSR

point$50/ CSR point x 80 CSR = $4,000

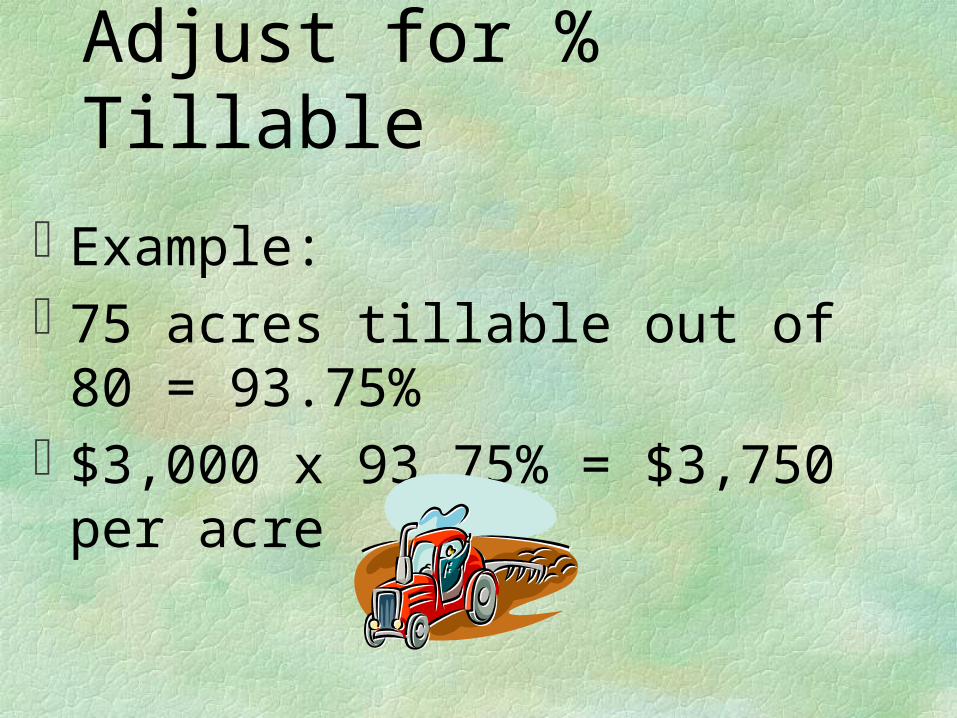

Adjust for % Tillable

Example: 75 acres tillable out of 80 =

93.75%$3,000 x 93.75% = $3,750 per

acre

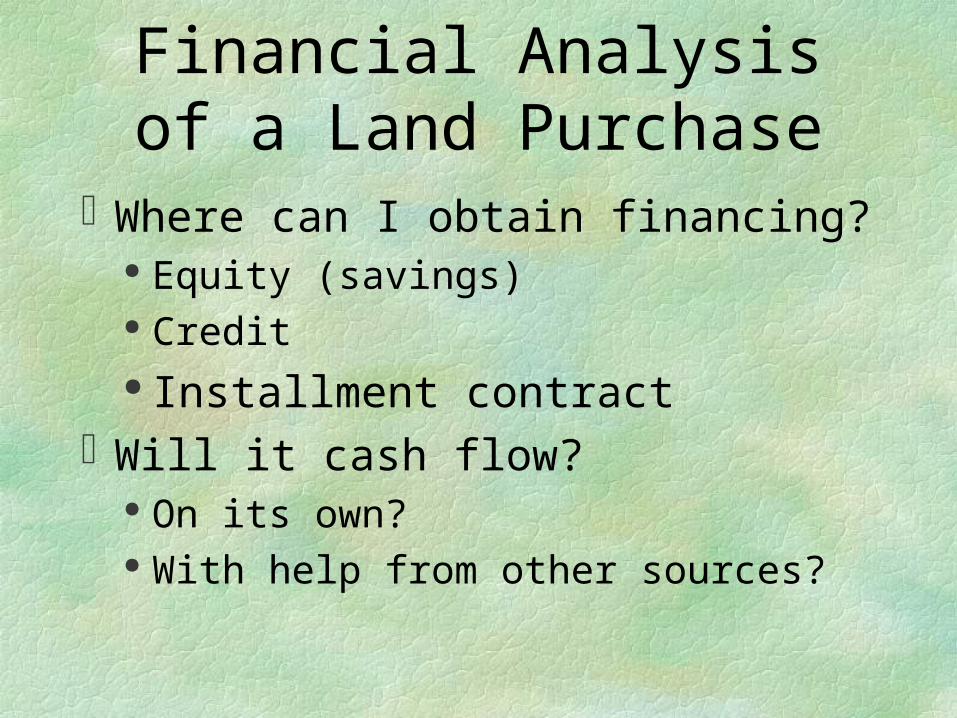

Financial Analysis of a Land Purchase

Where can I obtain financing? Equity (savings) Credit Installment contract

Will it cash flow? On its own? With help from other sources?

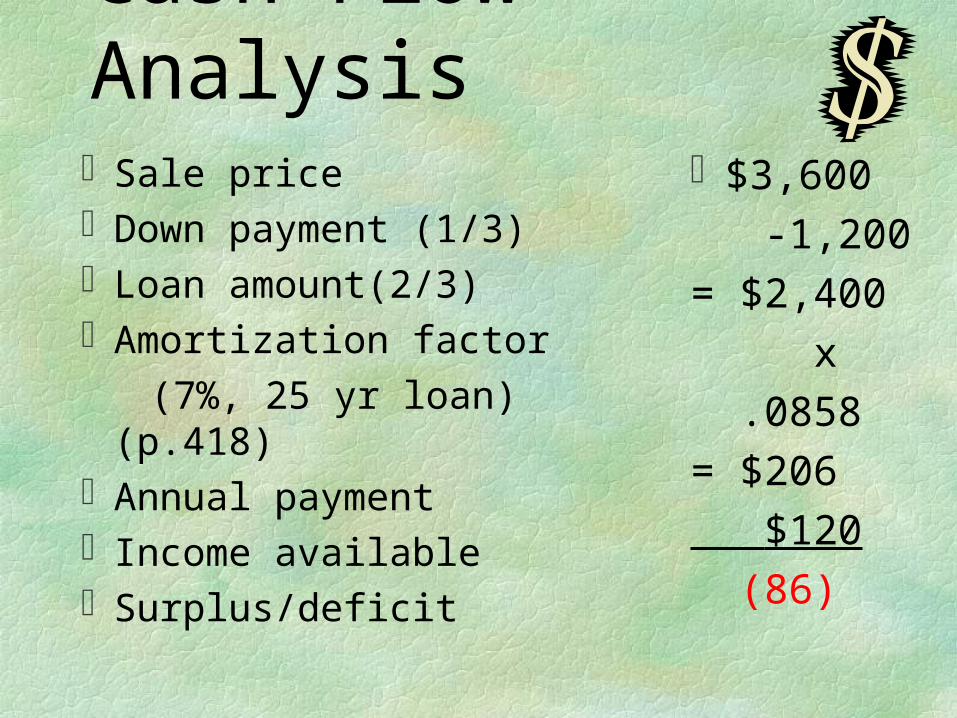

Cash Flow Analysis Sale priceDown payment (1/3)Loan amount(2/3)Amortization factor (7%, 25 yr loan) (p.418)Annual paymentIncome availableSurplus/deficit

$3,600 -1,200= $2,400 x .0858= $206 $120 (86)

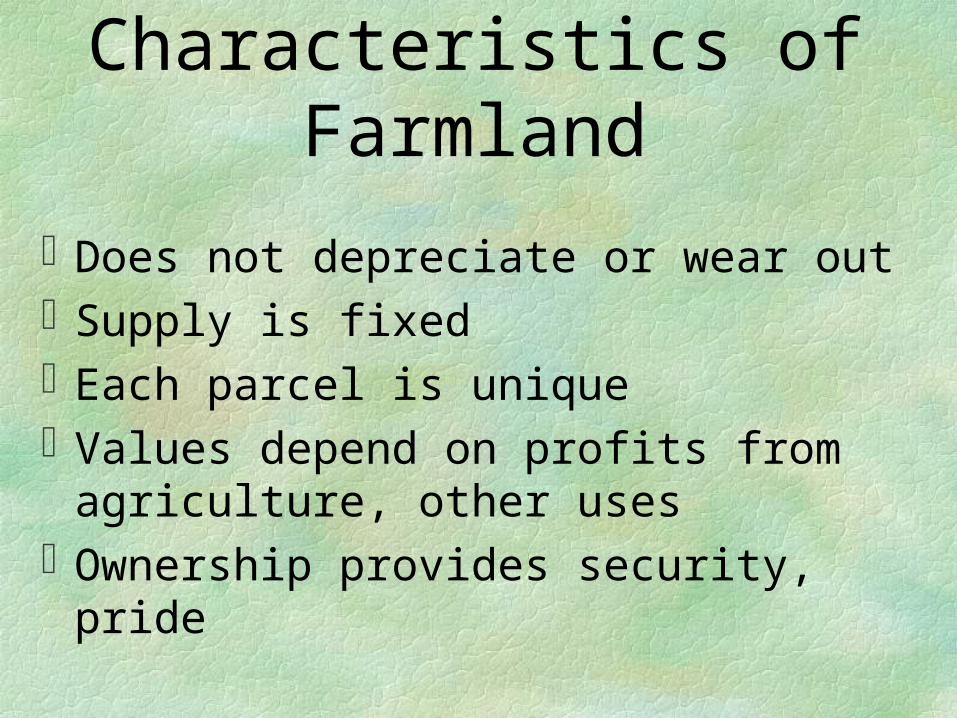

Characteristics of Farmland

Does not depreciate or wear outSupply is fixedEach parcel is uniqueValues depend on profits from

agriculture, other usesOwnership provides security, pride

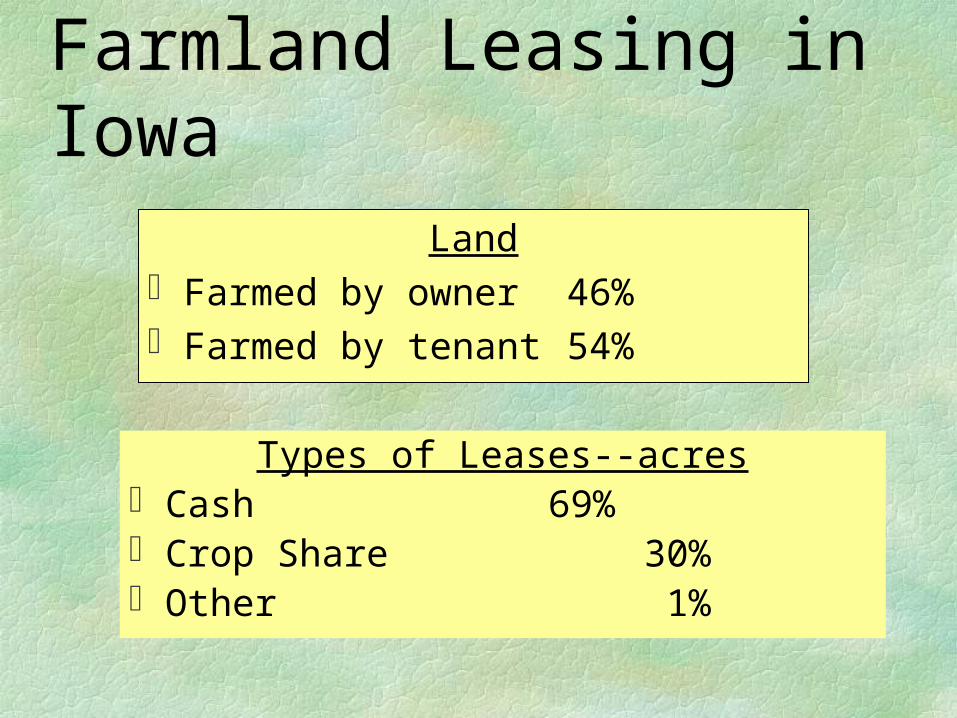

Farmland Leasing in Iowa

LandFarmed by owner 46%Farmed by tenant 54%

Types of Leases--acresCash 69%Crop Share 30%Other 1%

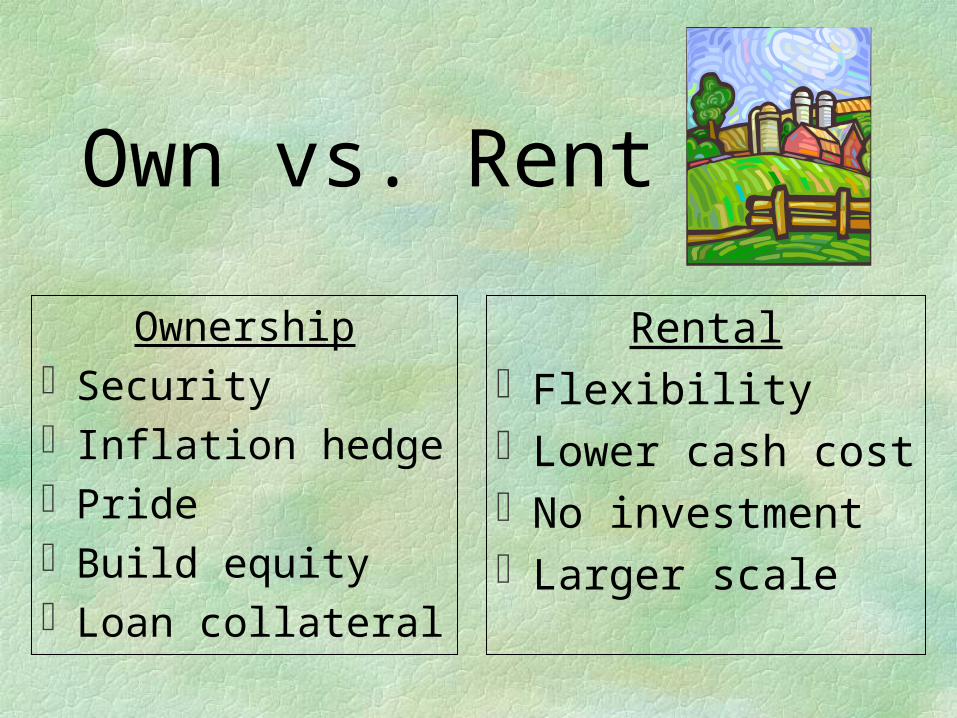

Own vs. Rent

OwnershipSecurityInflation hedgePrideBuild equityLoan collateral

RentalFlexibilityLower cash costNo investmentLarger scale

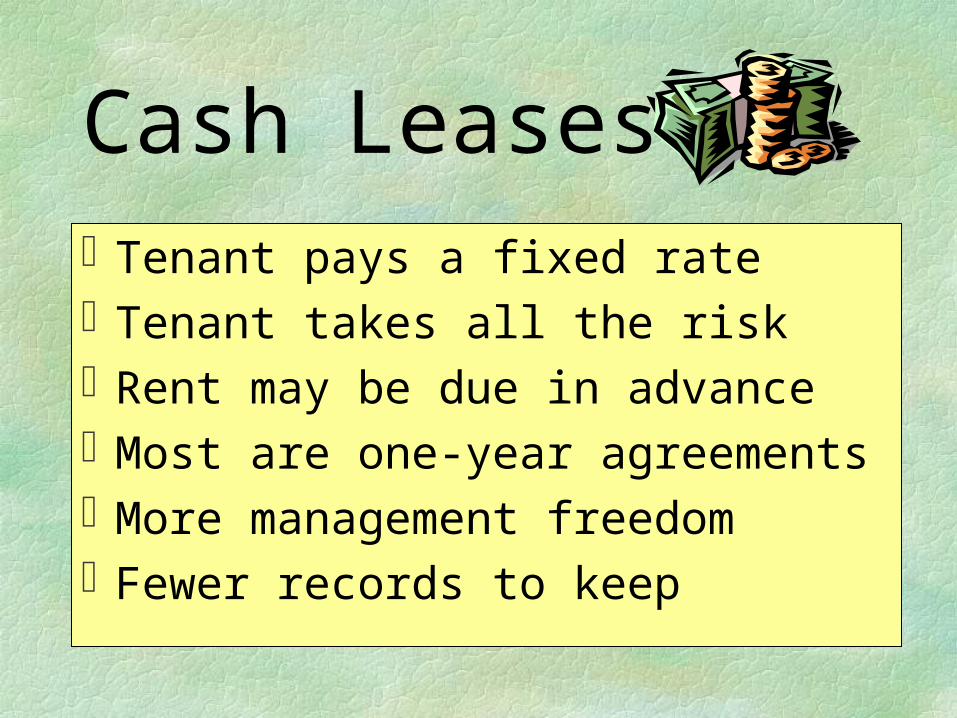

Cash LeasesTenant pays a fixed rateTenant takes all the riskRent may be due in advanceMost are one-year agreementsMore management freedomFewer records to keep

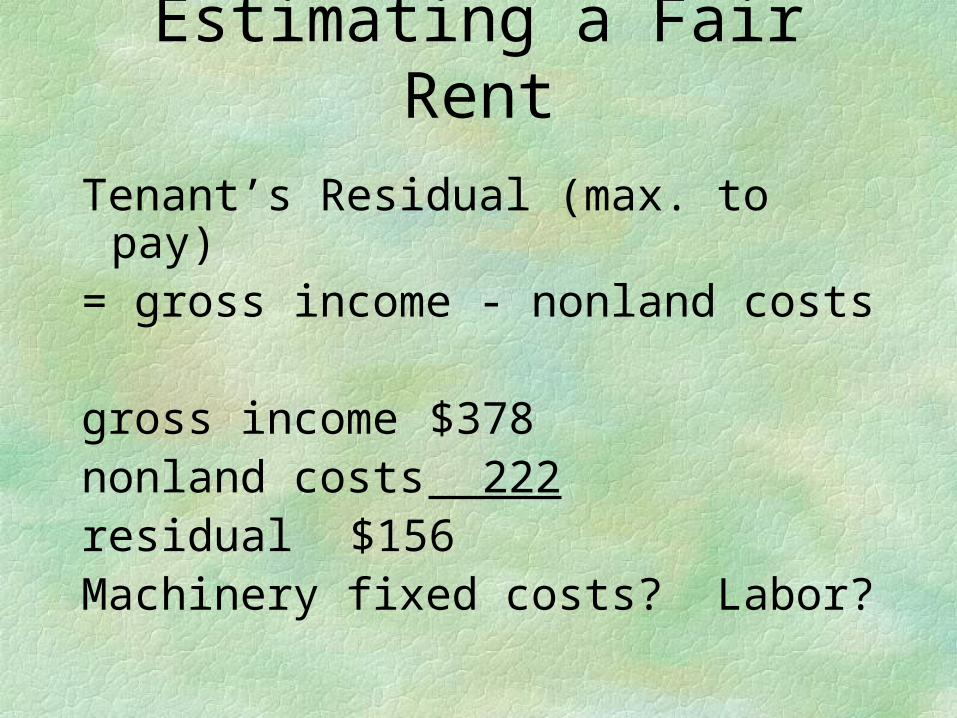

Estimating a Fair Rent

Tenant’s Residual (max. to pay)= gross income - nonland costs

gross income $378nonland costs 222 residual $156Machinery fixed costs? Labor?

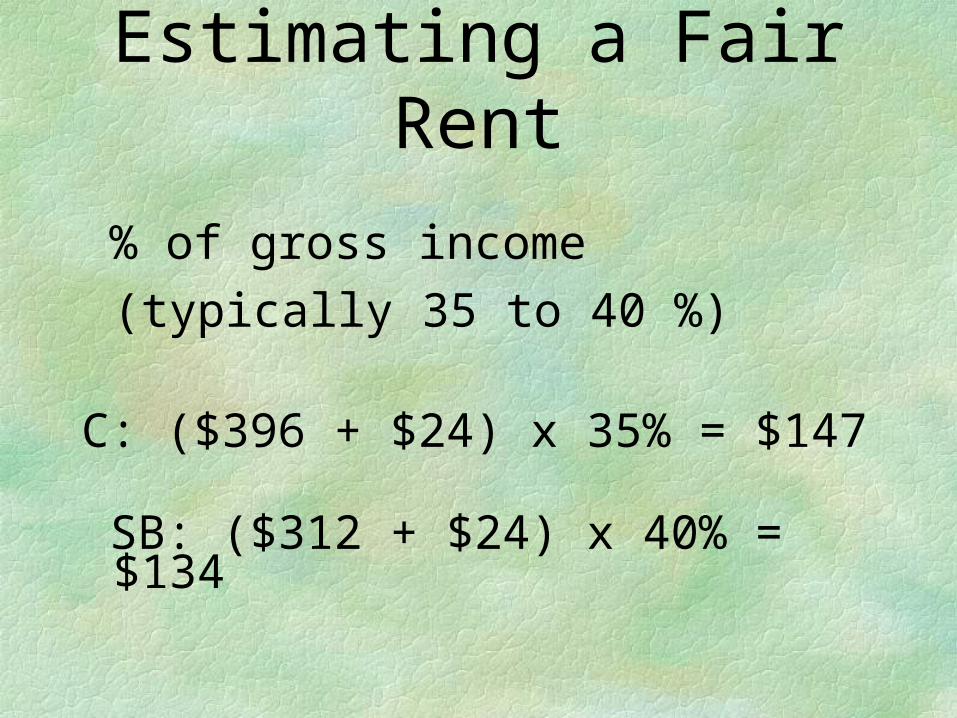

Estimating a Fair Rent

% of gross income(typically 35 to 40 %)

C: ($396 + $24) x 35% = $147

SB: ($312 + $24) x 40% = $134

Cash Rent Based on Yields

Corn: $.90 - $1.00 per bushelSoybeans: $2.70 - $3.00 per bu.Example:

Corn: 165 bu. X $.90 = $148Soybeans: 52 bu. X $2.80 = $146

Flexible Cash Leases

Rent is paid in cashAmount of rent depends on actual

prices and/or yieldsTenant pays all crop expensesTenant and owner share risksMust agree on how to calculate rent,

and how to determine actual price and yield

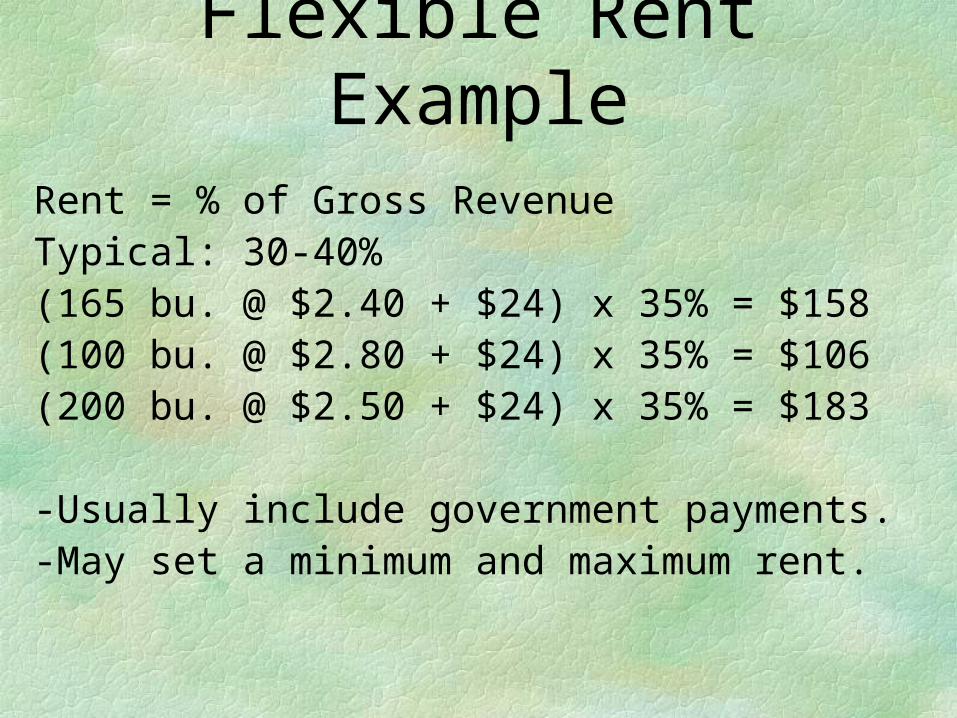

Flexible Rent Example

Rent = % of Gross RevenueTypical: 30-40% (165 bu. @ $2.40 + $24) x 35% = $158(100 bu. @ $2.80 + $24) x 35% = $106(200 bu. @ $2.50 + $24) x 35% = $183

-Usually include government payments.-May set a minimum and maximum

rent.

Crop Share LeasesTenant and owner divide crop

1/2 and 1/2 is typical

Tenant and owner share cost of crop inputs (seed, fertilizer, pesticides, drying, crop insurance)

Tenant supplies labor and machineryBoth price and production risk are

sharedLess capital is required from tenant

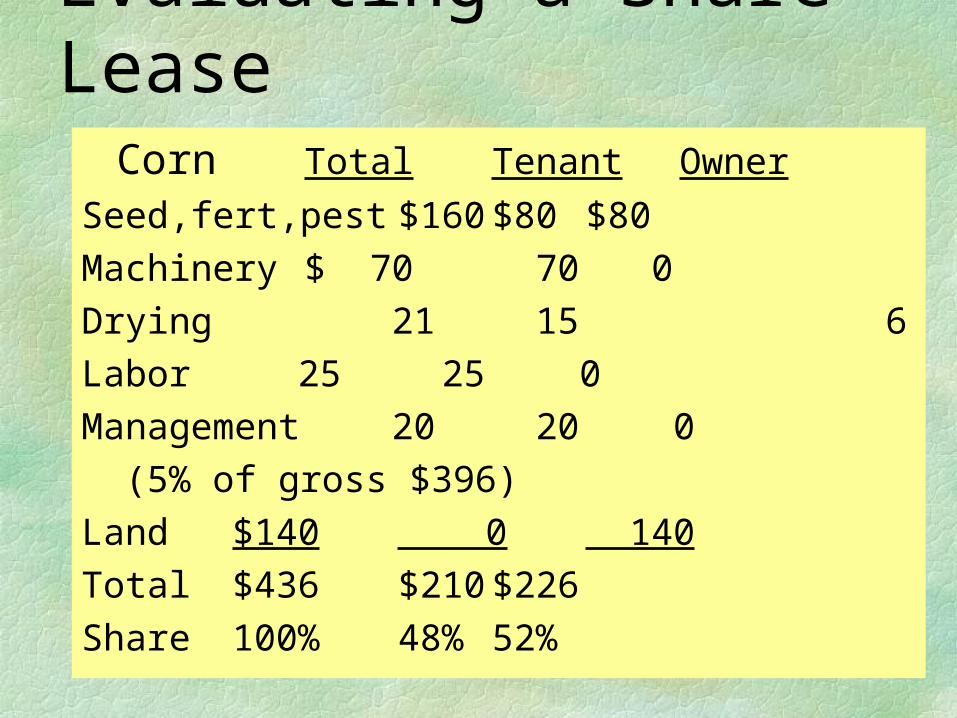

Evaluating a Share Lease

Corn Total Tenant Owner

Seed,fert,pest $160 $80 $80Machinery $ 70 70 0Drying 21 15 6Labor 25 25 0Management 20 20 0 (5% of gross $396)Land $140 0 140Total $436 $210 $226Share 100% 48% 52%

Net Returns to Tenant--Corn

(60)

(40)

(20)

0

20

40

60

80

100

120

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

$ per acre

Cash

Crop Share

Net Returns to Tenant--Soybeans

(20)

0

20

40

60

80

100

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

$ per acre

Cash

Crop Share

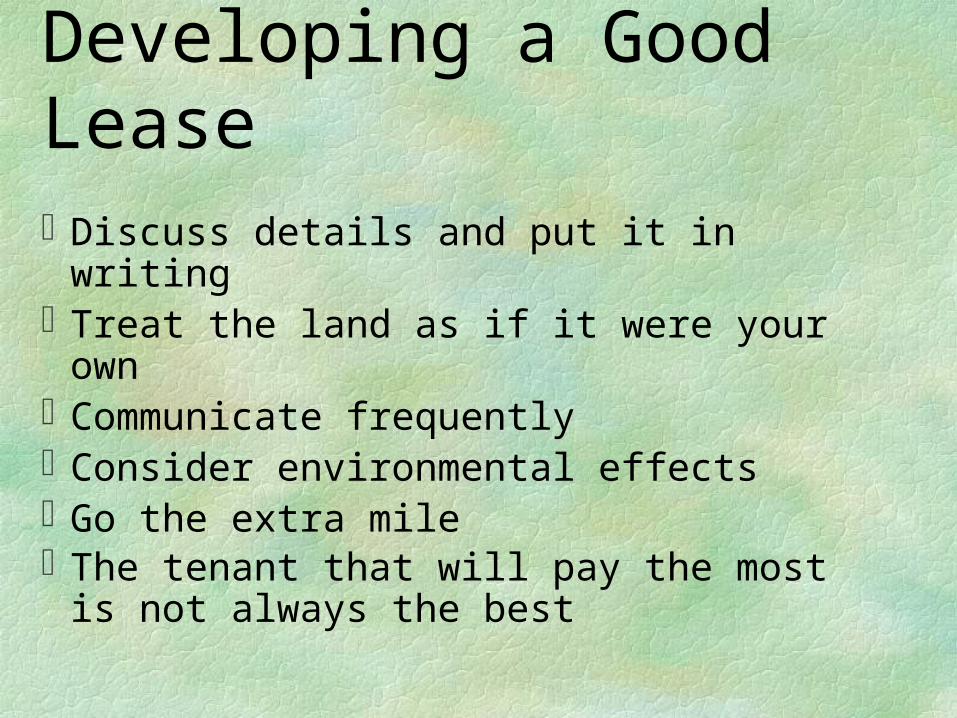

Developing a Good LeaseDiscuss details and put it in writingTreat the land as if it were your ownCommunicate frequentlyConsider environmental effectsGo the extra mileThe tenant that will pay the most is

not always the best

Custom FarmingOperator supplies labor

and machinery, onlyMay buy supplies,

choose inputs, etc.Receives a fixed

payment, sometimes a bonus or % of crop

Owner takes all the risk

Livestock Share Lease

Crop costs split same as crop-share leaseOwner provide buildings, pasture,

stationary equipmentTenant provides movable equipment, laborDivide livestock, feed, operating costsDivide income equallyNot very common now

Contract FarmingUsually involves growing specialty crops

high oil corn, seed corn, organic grains, etcMay receive a fixed paymentMay receive a guaranteed priceMust meet quality standardsManagement requirements are stricterMay need separate storageNeed a guaranteed market

Contract Finishing

Operator provides buildings, labor, operating costs

Contractor provides animals, feed, health services, marketing

Operator receives a fixed payment per animal or space. May have a bonus.

Limited risk, limited returns

Custom Feeding(mostly cattle)

Operator supplies feedlot, labor, feed, and all operating expenses

Owner of cattle pays a yardage fee ($ per head per day) plus health costs, feed costs, transportation

Related Documents