Energy Sector Assessment Strategy and Roadmap Project Number: 26194 Document Stage: May 2010 Viet Nam 2010

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Energy Sector Assessment Strategy and Roadmap

Project Number: 26194 Document Stage: May 2010

Viet Nam

2010

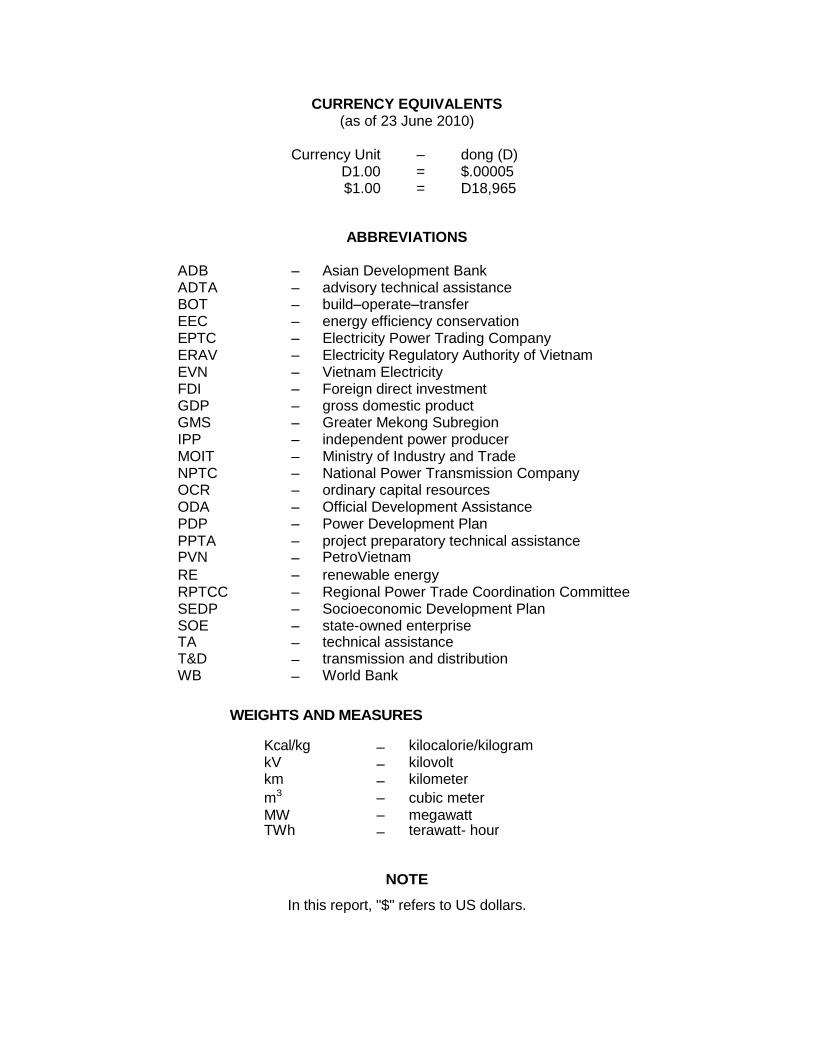

CURRENCY EQUIVALENTS (as of 23 June 2010)

Currency Unit – dong (D)

D1.00 = $.00005 $1.00 = D18,965

ABBREVIATIONS

ADB – Asian Development Bank ADTA – advisory technical assistance BOT – build–operate–transfer EEC – energy efficiency conservation EPTC – Electricity Power Trading Company ERAV – Electricity Regulatory Authority of Vietnam EVN – Vietnam Electricity FDI – Foreign direct investment GDP – gross domestic product GMS – Greater Mekong Subregion IPP – independent power producer MOIT – Ministry of Industry and Trade NPTC – National Power Transmission Company OCR – ordinary capital resources ODA – Official Development Assistance PDP – Power Development Plan PPTA – project preparatory technical assistance PVN – PetroVietnam

RE – renewable energy RPTCC – Regional Power Trade Coordination Committee SEDP – Socioeconomic Development Plan SOE – state-owned enterprise TA – technical assistance T&D – transmission and distribution WB – World Bank

WEIGHTS AND MEASURES

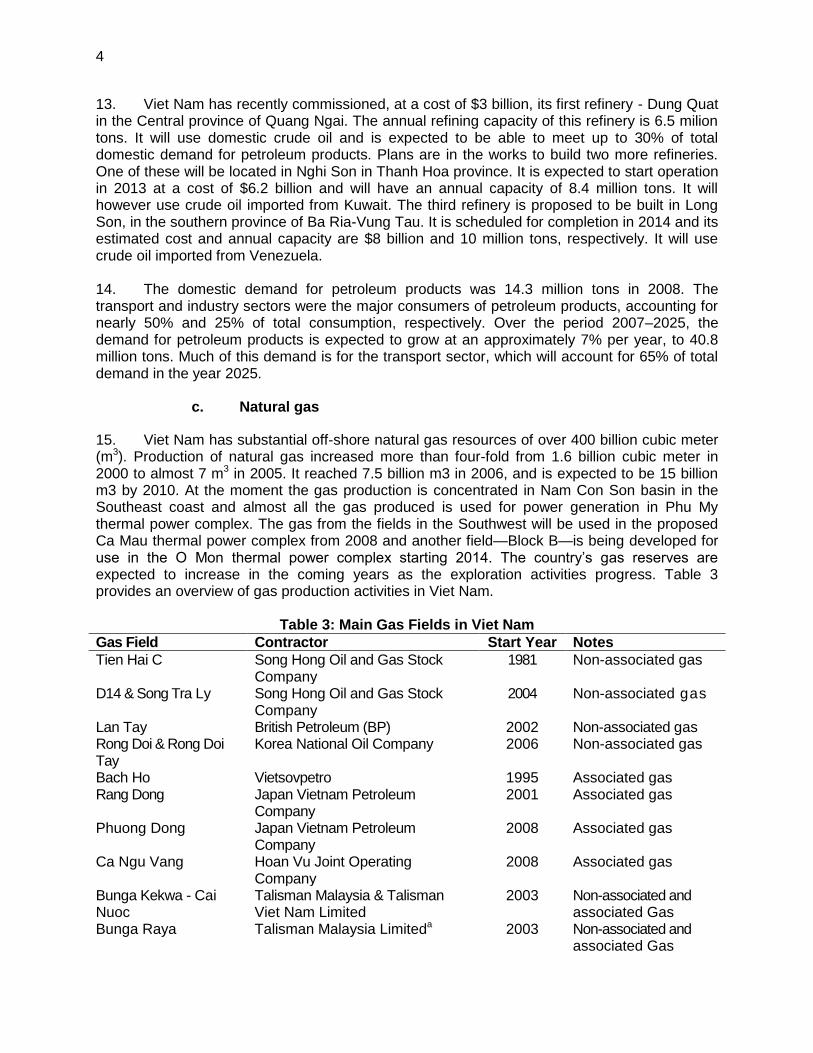

Kcal/kg – kilocalorie/kilogram kV – kilovolt km – kilometer

m3 – cubic meter MW – megawatt TWh – terawatt- hour

NOTE

In this report, "$" refers to US dollars.

In preparing any country partnership strategy, financing any project, or by making any designation of or reference to a particular territory or geographic area in this document, the Asian Development Bank does not intend to make any judgments as to the legal or other status of any territory or area.

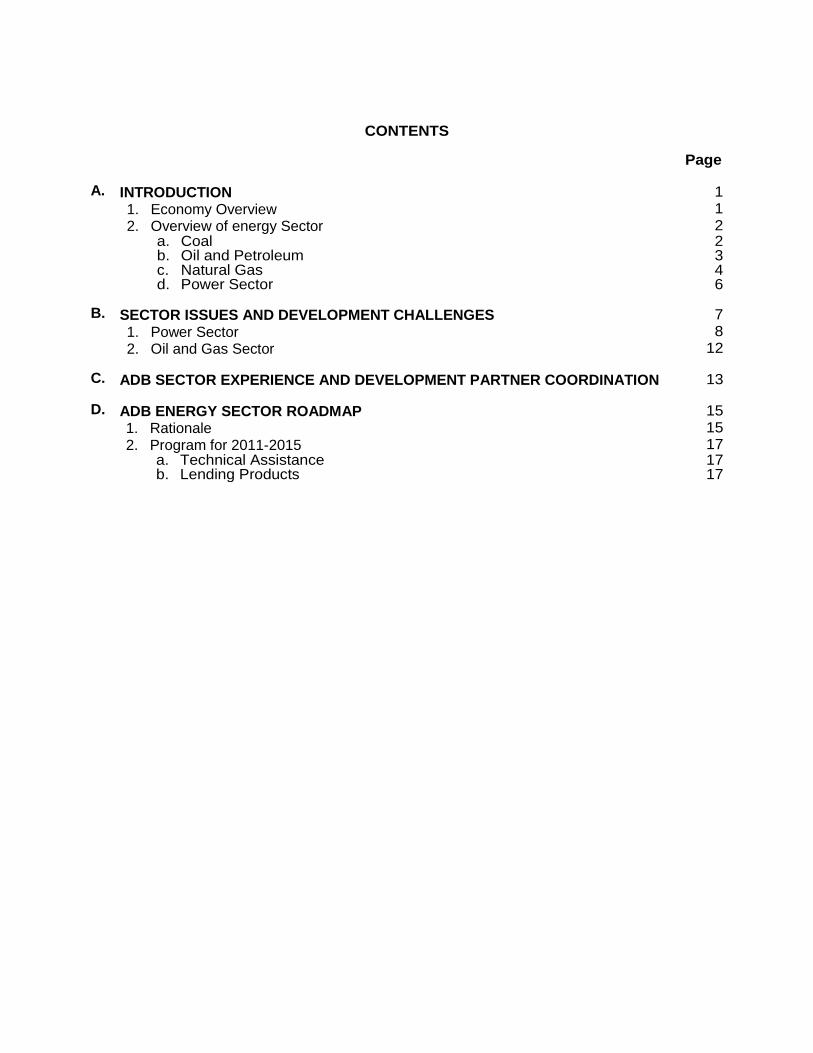

CONTENTS

Page A. INTRODUCTION 1 1. Economy Overview 1 2. Overview of energy Sector 2

a. Coal 2 b. Oil and Petroleum 3 c. Natural Gas 4 d. Power Sector 6

B. SECTOR ISSUES AND DEVELOPMENT CHALLENGES 7 1. Power Sector 8 2. Oil and Gas Sector 12

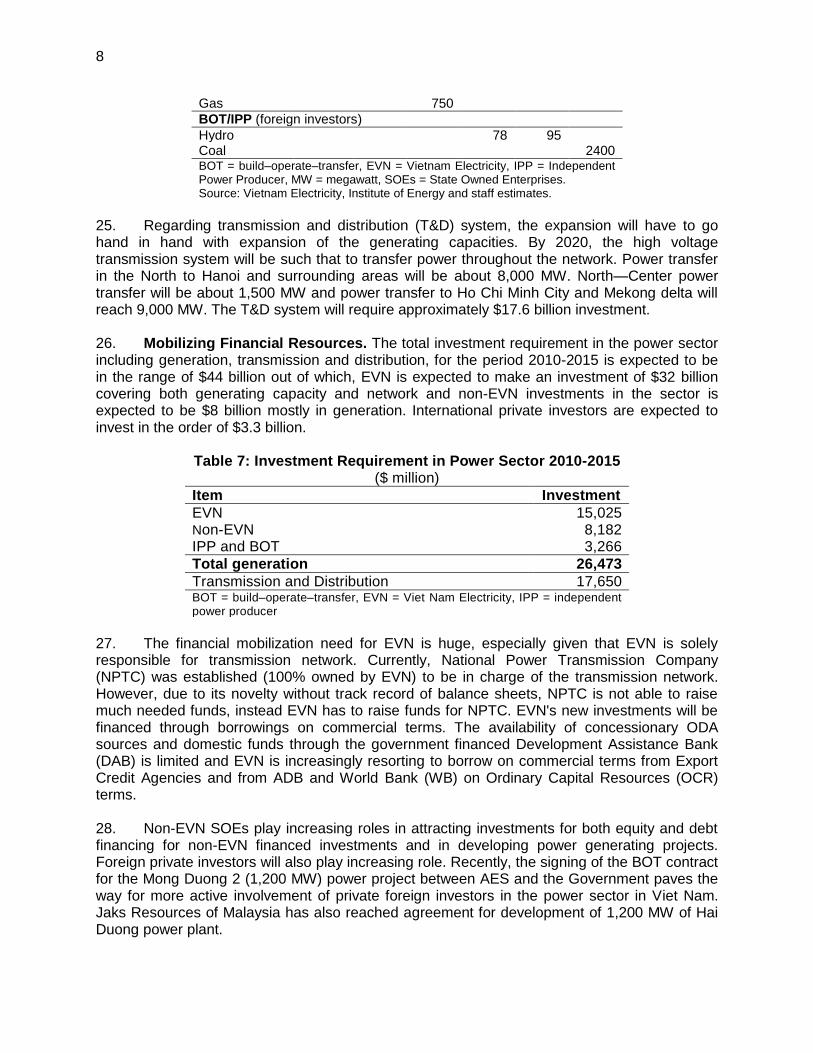

C. ADB SECTOR EXPERIENCE AND DEVELOPMENT PARTNER COORDINATION 13

D. ADB ENERGY SECTOR ROADMAP 15 1. Rationale 15 2. Program for 2011-2015 17

a. Technical Assistance 17 b. Lending Products 17

1

A. INTRODUCTION

1. Economy Overview

1. During the period 2000–2009, Viet Nam has recorded an average economic growth of 7.64% accompanied by rapid industrialization and urbanization and buoyed by increased of investment, consumer spending and Government spending. The country, however, suffered low gross domestic product (GDP) growth in 2008 and 2009 due to the impacts of the global financial crisis, thus GDP growth stood at 6.1% and 5.3% in 2008 and 2009, respectively. The growth was particularly strong for the industry, which recorded 9.7% per year for the ten-year period, followed by service sector–7.6% per annum. Agriculture also expanded with a rate of 3.9% per year. By 2009, the country managed to double its GDP of the 2000 level. Per capital GDP in 2009 reached almost $1,000 per person. 2. The structure of the economy shifted toward industry and services. By 2009, agriculture sector contributed less than 20% of GDP, while industry and construction contributed 41% and service sector accounted for 39%. Within the industry, there was a shift toward higher value–added sectors. Government’s continuation of its Doi Moi policy brings increased Official Development Assistance (ODA) funds and attracts more foreign direct investment (FDI). The country is becoming more and more integrated into regional and international markets. 3. The Government is preparing its long term socioeconomic development plan (SEDP) toward 2030. Three scenarios were developed anticipating different development possibilities in the next 20 years. The base scenario envisages relatively high growth for the next five years, 2010–2015, with GDP growing at 7.5% per annum, then slowing down to 7% per annum till 2020. The economy structure will evolve with industry reaching 48%, service will account for 40% of GDP; and agriculture share will reduce to 12.5% in 2020.

Table 1: Projection of the Economy Structure (%)

Item 2010 2015 2020 2030

Industry and construction 44.7 46.3 47.8 48.7 Agriculture 17.3 14.7 12.5 8.7 Services 38.0 38.9 39.7 42.6 Source: General Statistics Office

4. The strong growth of business and service sector coupled with industrialization was the main characteristic of the Viet Nam economy during the last decade. This set the stage for high demand for electricity and other forms of end-use energies. Due to high GDP elasticity to electricity, the projected GDP growth of 7.5% for 2006–2010 will result in an electricity demand growth of over 15%. A similar growth in demand for coal, oil and gas is expected. Availability of reliable energy resources is an essential prerequisite for maintaining Viet Nam’s enviable record of socially inclusive economic growth and creating the enabling environment for private sector investments in manufacturing and service sectors. 5. The country is mobilizing a large amount of external financial resources to meet its investment needs. Managing debts to a sustainable level becomes more and more important aspect. According to the recent debate in the National Assembly, the debt level is still below the limit (50% of GDP); 37% in 2007, 41% in 2008 and 44% in 2009; inclusive of direct borrowing, bonds and Government guarantee. The country is paying special attention in managing the

2

borrowing level as well as to make efficient utilization of the resources.

2. Overview of Energy Sector

6. Viet Nam has substantial energy resources, including all types of primary energies (coal, oil and gas, and hydropower) and renewable energy resources such as bio mass, solar and wind.

a. Coal

7. Coal is Viet Nam’s largest indigenous resource, with proven reserves estimated to be of the order of 6 billion tons. The bulk of this coal is anthracite, concentrated in the northern part of the country, especially the northeastern province of Quang Ninh. The country exports the highest quality coals, with calorific values in the range of 7,200-8,500 kilocalorie/kilogram (Kcal/kg), as metallurgical coal. Lower quality coal (3,500-5,500 Kcal/kg) is used domestically for the production of electricity, cement and construction materials. 8. Over the period 2000–2009, coal consumption in Viet Nam increased to 14.2 million tons—an annual increase of 9.2%. Electricity generation has been the most significant consumer of coal, accounting for 37% of total coal consumed in 2008. The demand for coal is expected to increase to 92 million tons by the year 2025—representing an annual increase of 11% between 2007 and 2025. Electricity generation will be responsible for much of this increase, for example, by 2025, it will account for nearly 83% of the total coal consumption. The other major user of coal is the industry sector, where coal is used primarily for steel, cement, paper and fertilizer production. 9. On the supply side, coal production increased to 39 million tons in 2008 – an annual increase of 14%. The production of coal is expected to rise to 42 million tons in 2010 and 54 million tons in 2020 and the use of coal in power generation will be increased to 15 million tons by 2010 and to 22 million tons by 2020. Up to now, Viet Nam has been an exporter of coal, exporting 32 million tons in 2008. More than 60% of coal export went to China and the rest to Japan. On account however of rapidly increasing domestic demand for coal, especially for power generation and other industries (such as cement and steel), the lack of available areas suitable for open pit mining, dearth of capital and local expertise for undertaking deep underground mining, Viet Nam is expected to become a net importer of coal in the coming years. For example, it is estimated that the annual rate of increase in coal production will decline to 3% over the period of 2007–2025 (as compared with 14% over the period 1990–2007). Overall, Viet Nam expects to import nearly 6, 15 and 55 million tons of coal by 2015, 2020 and 2025, respectively. 10. Coal mining, export and domestic distribution are dominated by the state-owned coal mining monopoly - Vinacomin (Viet Nam Mining Company). The coal mining in Viet Nam is expected to move from shallow open cast mining to deep mining to meet the increasing demand for coal. The investment requirement in the coal sector is also substantial, concentrating on development of new deep coal mines, coal washing plants, and other coal handling and transport facilities. The environmental and safety issues of increased coal production are a major concern.

b. Oil and petroleum

11. Viet Nam has substantial oil reserves. The current estimate of discovered oil reserves

3

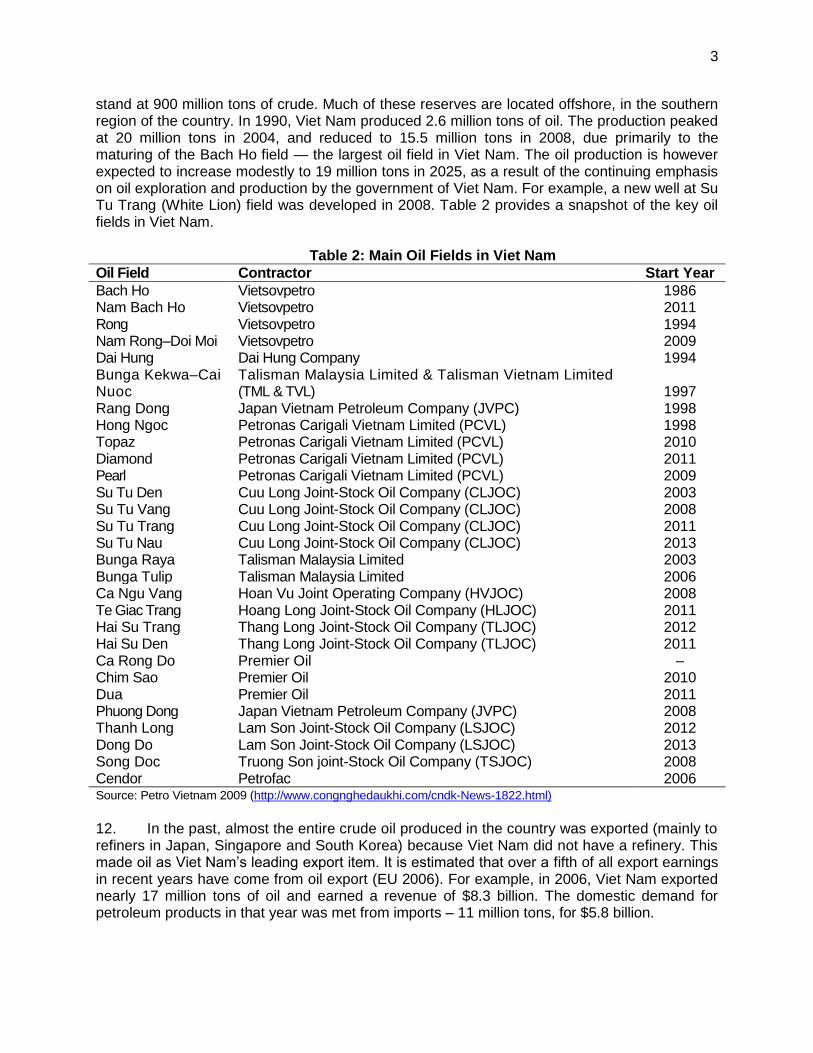

stand at 900 million tons of crude. Much of these reserves are located offshore, in the southern region of the country. In 1990, Viet Nam produced 2.6 million tons of oil. The production peaked at 20 million tons in 2004, and reduced to 15.5 million tons in 2008, due primarily to the maturing of the Bach Ho field — the largest oil field in Viet Nam. The oil production is however expected to increase modestly to 19 million tons in 2025, as a result of the continuing emphasis on oil exploration and production by the government of Viet Nam. For example, a new well at Su Tu Trang (White Lion) field was developed in 2008. Table 2 provides a snapshot of the key oil fields in Viet Nam. Table 2: Main Oil Fields in Viet Nam

Oil Field Contractor Start Year

Bach Ho Vietsovpetro 1986 Nam Bach Ho Vietsovpetro 2011 Rong Vietsovpetro 1994 Nam Rong–Doi Moi Vietsovpetro 2009 Dai Hung Dai Hung Company 1994 Bunga Kekwa–Cai Nuoc

Talisman Malaysia Limited & Talisman Vietnam Limited (TML & TVL) 1997

Rang Dong Japan Vietnam Petroleum Company (JVPC) 1998 Hong Ngoc Petronas Carigali Vietnam Limited (PCVL) 1998 Topaz Petronas Carigali Vietnam Limited (PCVL) 2010 Diamond Petronas Carigali Vietnam Limited (PCVL) 2011 Pearl Petronas Carigali Vietnam Limited (PCVL) 2009 Su Tu Den Cuu Long Joint-Stock Oil Company (CLJOC) 2003 Su Tu Vang Cuu Long Joint-Stock Oil Company (CLJOC) 2008 Su Tu Trang Cuu Long Joint-Stock Oil Company (CLJOC) 2011 Su Tu Nau Cuu Long Joint-Stock Oil Company (CLJOC) 2013 Bunga Raya Talisman Malaysia Limited 2003 Bunga Tulip Talisman Malaysia Limited 2006 Ca Ngu Vang Hoan Vu Joint Operating Company (HVJOC) 2008 Te Giac Trang Hoang Long Joint-Stock Oil Company (HLJOC) 2011 Hai Su Trang Thang Long Joint-Stock Oil Company (TLJOC) 2012 Hai Su Den Thang Long Joint-Stock Oil Company (TLJOC) 2011 Ca Rong Do Premier Oil – Chim Sao Premier Oil 2010 Dua Premier Oil 2011 Phuong Dong Japan Vietnam Petroleum Company (JVPC) 2008 Thanh Long Lam Son Joint-Stock Oil Company (LSJOC) 2012 Dong Do Lam Son Joint-Stock Oil Company (LSJOC) 2013 Song Doc Truong Son joint-Stock Oil Company (TSJOC) 2008 Cendor Petrofac 2006 Source: Petro Vietnam 2009 (http://www.congnghedaukhi.com/cndk-News-1822.html)

12. In the past, almost the entire crude oil produced in the country was exported (mainly to refiners in Japan, Singapore and South Korea) because Viet Nam did not have a refinery. This made oil as Viet Nam’s leading export item. It is estimated that over a fifth of all export earnings in recent years have come from oil export (EU 2006). For example, in 2006, Viet Nam exported nearly 17 million tons of oil and earned a revenue of $8.3 billion. The domestic demand for petroleum products in that year was met from imports – 11 million tons, for $5.8 billion.

4

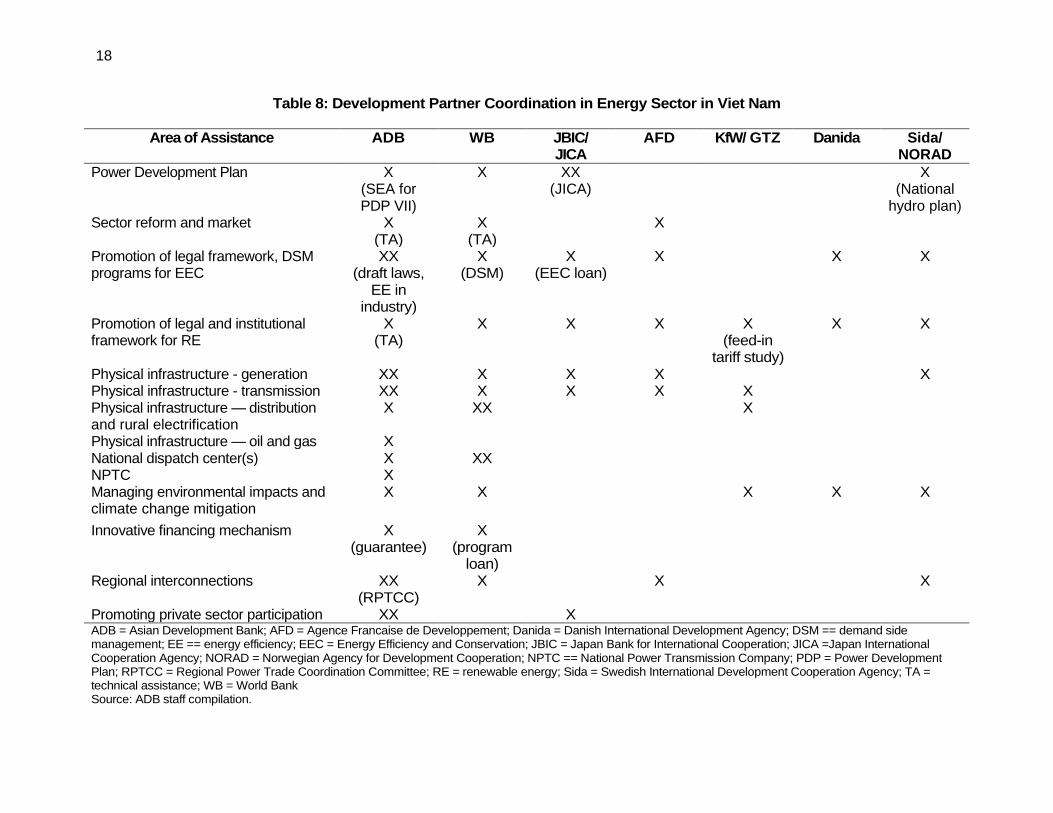

13. Viet Nam has recently commissioned, at a cost of $3 billion, its first refinery - Dung Quat in the Central province of Quang Ngai. The annual refining capacity of this refinery is 6.5 milion tons. It will use domestic crude oil and is expected to be able to meet up to 30% of total domestic demand for petroleum products. Plans are in the works to build two more refineries. One of these will be located in Nghi Son in Thanh Hoa province. It is expected to start operation in 2013 at a cost of $6.2 billion and will have an annual capacity of 8.4 million tons. It will however use crude oil imported from Kuwait. The third refinery is proposed to be built in Long Son, in the southern province of Ba Ria-Vung Tau. It is scheduled for completion in 2014 and its estimated cost and annual capacity are $8 billion and 10 million tons, respectively. It will use crude oil imported from Venezuela. 14. The domestic demand for petroleum products was 14.3 million tons in 2008. The transport and industry sectors were the major consumers of petroleum products, accounting for nearly 50% and 25% of total consumption, respectively. Over the period 2007–2025, the demand for petroleum products is expected to grow at an approximately 7% per year, to 40.8 million tons. Much of this demand is for the transport sector, which will account for 65% of total demand in the year 2025.

c. Natural gas

15. Viet Nam has substantial off-shore natural gas resources of over 400 billion cubic meter (m3). Production of natural gas increased more than four-fold from 1.6 billion cubic meter in 2000 to almost 7 m3 in 2005. It reached 7.5 billion m3 in 2006, and is expected to be 15 billion m3 by 2010. At the moment the gas production is concentrated in Nam Con Son basin in the Southeast coast and almost all the gas produced is used for power generation in Phu My thermal power complex. The gas from the fields in the Southwest will be used in the proposed Ca Mau thermal power complex from 2008 and another field—Block B—is being developed for use in the O Mon thermal power complex starting 2014. The country’s gas reserves are expected to increase in the coming years as the exploration activities progress. Table 3 provides an overview of gas production activities in Viet Nam.

Table 3: Main Gas Fields in Viet Nam

Gas Field Contractor Start Year Notes

Tien Hai C Song Hong Oil and Gas Stock Company

1981 Non-associated gas

D14 & Song Tra Ly Song Hong Oil and Gas Stock Company

2004 Non-associated gas

Lan Tay British Petroleum (BP) 2002 Non-associated gas Rong Doi & Rong Doi Tay

Korea National Oil Company 2006 Non-associated gas

Bach Ho Vietsovpetro 1995 Associated gas Rang Dong Japan Vietnam Petroleum

Company 2001 Associated gas

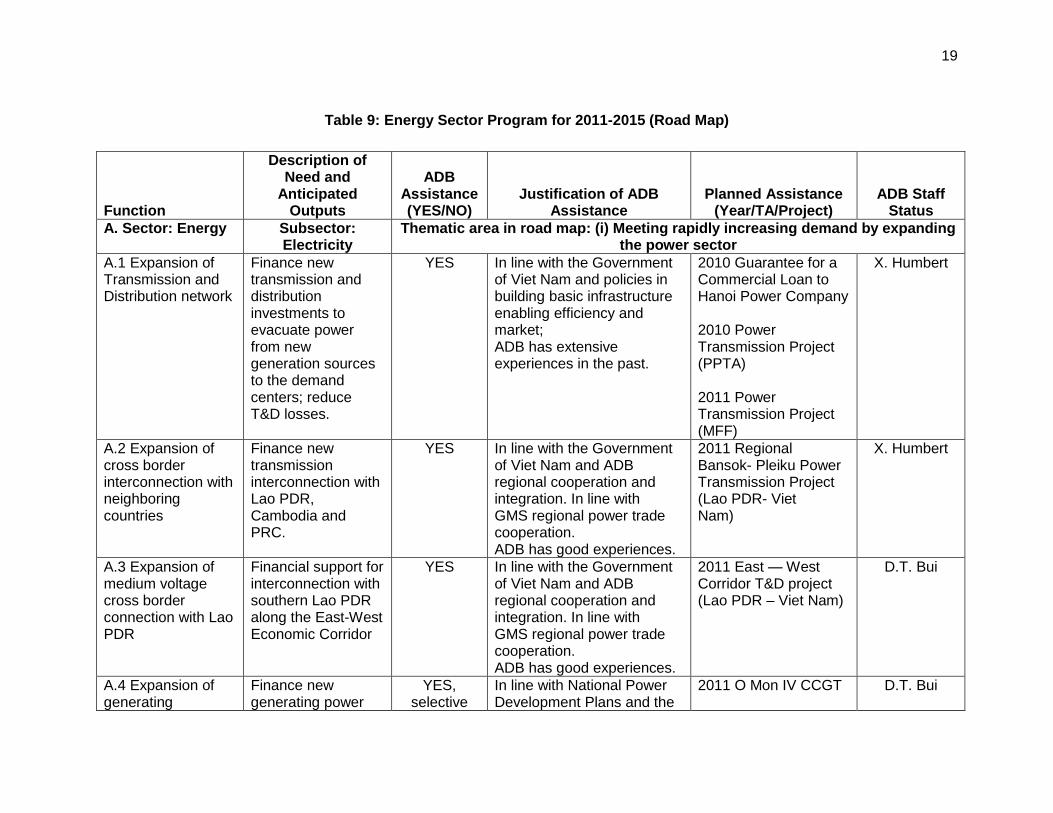

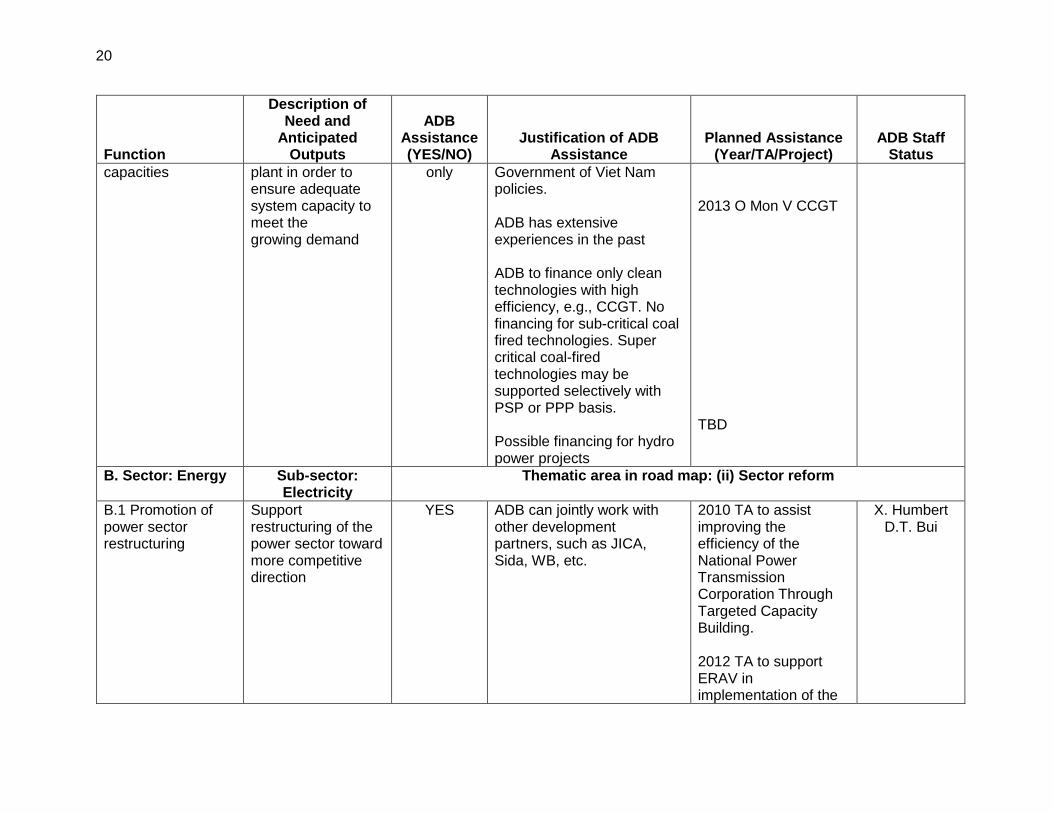

Phuong Dong

Japan Vietnam Petroleum Company

2008 Associated gas

Ca Ngu Vang Hoan Vu Joint Operating Company

2008 Associated gas

Bunga Kekwa - Cai Nuoc

Talisman Malaysia & Talisman Viet Nam Limited

2003 Non-associated and associated Gas

Bunga Raya Talisman Malaysia Limiteda 2003 Non-associated and associated Gas

5

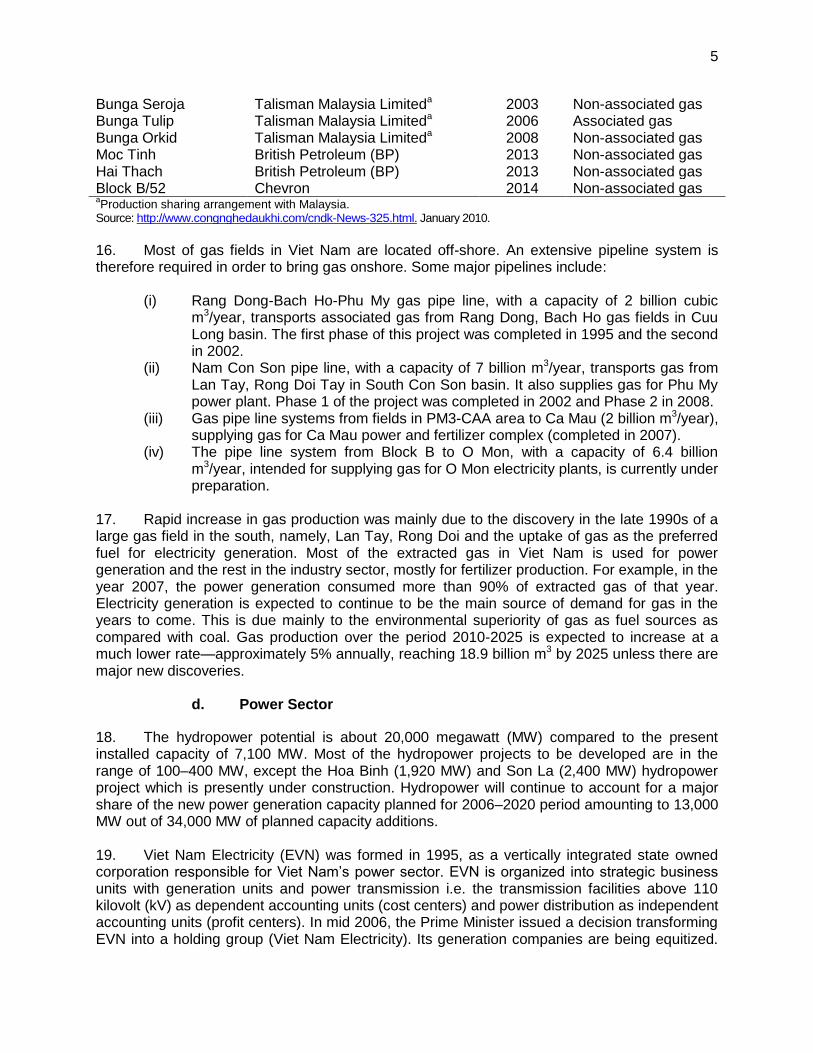

Bunga Seroja Talisman Malaysia Limiteda 2003 Non-associated gas Bunga Tulip Talisman Malaysia Limiteda 2006 Associated gas Bunga Orkid Talisman Malaysia Limiteda 2008 Non-associated gas Moc Tinh British Petroleum (BP) 2013 Non-associated gas Hai Thach British Petroleum (BP) 2013 Non-associated gas Block B/52 Chevron 2014 Non-associated gas aProduction sharing arrangement with Malaysia.

Source: http://www.congnghedaukhi.com/cndk-News-325.html. January 2010.

16. Most of gas fields in Viet Nam are located off-shore. An extensive pipeline system is therefore required in order to bring gas onshore. Some major pipelines include:

(i) Rang Dong-Bach Ho-Phu My gas pipe line, with a capacity of 2 billion cubic m3/year, transports associated gas from Rang Dong, Bach Ho gas fields in Cuu Long basin. The first phase of this project was completed in 1995 and the second in 2002.

(ii) Nam Con Son pipe line, with a capacity of 7 billion m3/year, transports gas from Lan Tay, Rong Doi Tay in South Con Son basin. It also supplies gas for Phu My power plant. Phase 1 of the project was completed in 2002 and Phase 2 in 2008.

(iii) Gas pipe line systems from fields in PM3-CAA area to Ca Mau (2 billion m3/year), supplying gas for Ca Mau power and fertilizer complex (completed in 2007).

(iv) The pipe line system from Block B to O Mon, with a capacity of 6.4 billion m3/year, intended for supplying gas for O Mon electricity plants, is currently under preparation.

17. Rapid increase in gas production was mainly due to the discovery in the late 1990s of a large gas field in the south, namely, Lan Tay, Rong Doi and the uptake of gas as the preferred fuel for electricity generation. Most of the extracted gas in Viet Nam is used for power generation and the rest in the industry sector, mostly for fertilizer production. For example, in the year 2007, the power generation consumed more than 90% of extracted gas of that year. Electricity generation is expected to continue to be the main source of demand for gas in the years to come. This is due mainly to the environmental superiority of gas as fuel sources as compared with coal. Gas production over the period 2010-2025 is expected to increase at a much lower rate—approximately 5% annually, reaching 18.9 billion m3 by 2025 unless there are major new discoveries.

d. Power Sector

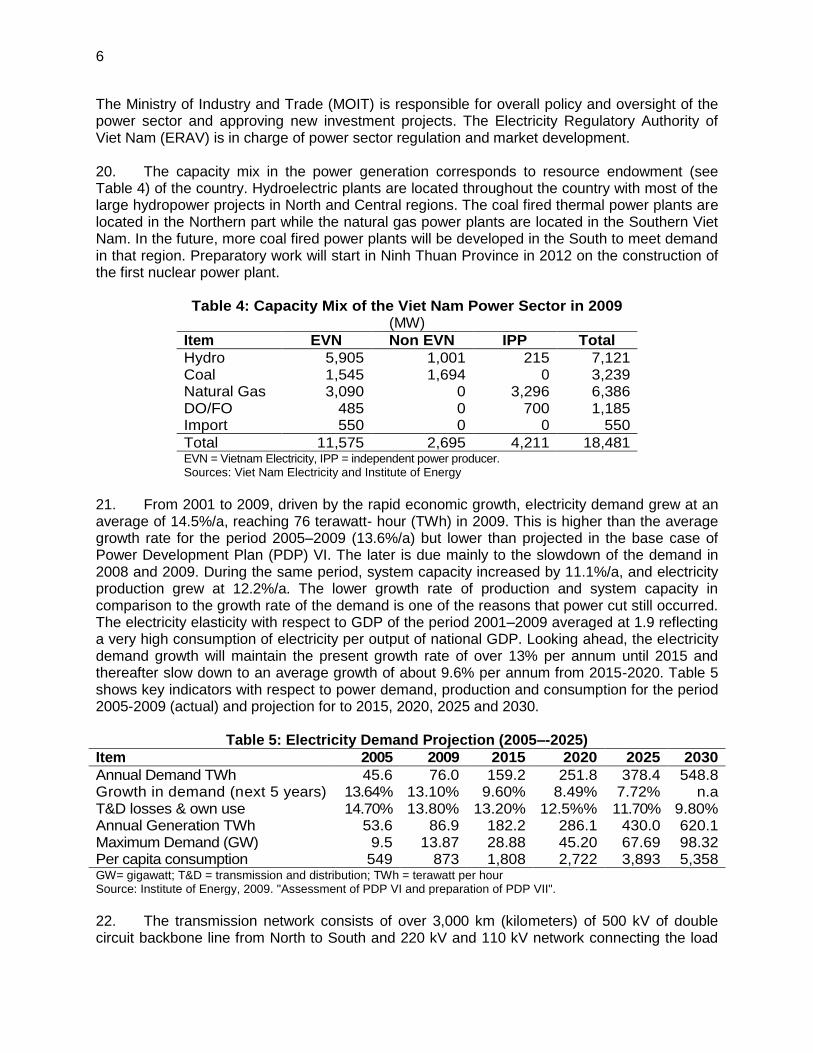

18. The hydropower potential is about 20,000 megawatt (MW) compared to the present installed capacity of 7,100 MW. Most of the hydropower projects to be developed are in the range of 100–400 MW, except the Hoa Binh (1,920 MW) and Son La (2,400 MW) hydropower project which is presently under construction. Hydropower will continue to account for a major share of the new power generation capacity planned for 2006–2020 period amounting to 13,000 MW out of 34,000 MW of planned capacity additions. 19. Viet Nam Electricity (EVN) was formed in 1995, as a vertically integrated state owned corporation responsible for Viet Nam’s power sector. EVN is organized into strategic business units with generation units and power transmission i.e. the transmission facilities above 110 kilovolt (kV) as dependent accounting units (cost centers) and power distribution as independent accounting units (profit centers). In mid 2006, the Prime Minister issued a decision transforming EVN into a holding group (Viet Nam Electricity). Its generation companies are being equitized.

6

The Ministry of Industry and Trade (MOIT) is responsible for overall policy and oversight of the power sector and approving new investment projects. The Electricity Regulatory Authority of Viet Nam (ERAV) is in charge of power sector regulation and market development. 20. The capacity mix in the power generation corresponds to resource endowment (see Table 4) of the country. Hydroelectric plants are located throughout the country with most of the large hydropower projects in North and Central regions. The coal fired thermal power plants are located in the Northern part while the natural gas power plants are located in the Southern Viet Nam. In the future, more coal fired power plants will be developed in the South to meet demand in that region. Preparatory work will start in Ninh Thuan Province in 2012 on the construction of the first nuclear power plant.

Table 4: Capacity Mix of the Viet Nam Power Sector in 2009 (MW)

Item EVN Non EVN IPP Total

Hydro 5,905 1,001 215 7,121 Coal 1,545 1,694 0 3,239 Natural Gas 3,090 0 3,296 6,386 DO/FO 485 0 700 1,185 Import 550 0 0 550

Total 11,575 2,695 4,211 18,481 EVN = Vietnam Electricity, IPP = independent power producer. Sources: Viet Nam Electricity and Institute of Energy

21. From 2001 to 2009, driven by the rapid economic growth, electricity demand grew at an average of 14.5%/a, reaching 76 terawatt- hour (TWh) in 2009. This is higher than the average growth rate for the period 2005–2009 (13.6%/a) but lower than projected in the base case of Power Development Plan (PDP) VI. The later is due mainly to the slowdown of the demand in 2008 and 2009. During the same period, system capacity increased by 11.1%/a, and electricity production grew at 12.2%/a. The lower growth rate of production and system capacity in comparison to the growth rate of the demand is one of the reasons that power cut still occurred. The electricity elasticity with respect to GDP of the period 2001–2009 averaged at 1.9 reflecting a very high consumption of electricity per output of national GDP. Looking ahead, the electricity demand growth will maintain the present growth rate of over 13% per annum until 2015 and thereafter slow down to an average growth of about 9.6% per annum from 2015-2020. Table 5 shows key indicators with respect to power demand, production and consumption for the period 2005-2009 (actual) and projection for to 2015, 2020, 2025 and 2030.

Table 5: Electricity Demand Projection (2005–-2025)

Item 2005 2009 2015 2020 2025 2030

Annual Demand TWh 45.6 76.0 159.2 251.8 378.4 548.8 Growth in demand (next 5 years) 13.64% 13.10% 9.60% 8.49% 7.72% n.a T&D losses & own use 14.70% 13.80% 13.20% 12.5%% 11.70% 9.80% Annual Generation TWh 53.6 86.9 182.2 286.1 430.0 620.1 Maximum Demand (GW) 9.5 13.87 28.88 45.20 67.69 98.32 Per capita consumption 549 873 1,808 2,722 3,893 5,358 GW= gigawatt; T&D = transmission and distribution; TWh = terawatt per hour Source: Institute of Energy, 2009. "Assessment of PDP VI and preparation of PDP VII". 22. The transmission network consists of over 3,000 km (kilometers) of 500 kV of double circuit backbone line from North to South and 220 kV and 110 kV network connecting the load

7

centers to the backbone network. The ongoing transmission augmentation is aimed at completing the 500 kV ring networks around Hanoi1 and Ho Chi Minh City. During the last five years, Viet Nam has constructed new 550 km of 500 kV lines, more than 2,300 km 220 kV lines, and almost 5,000 megavolt amperes of 500 kV substations and 9,000 megavolt amperes of 220 kV substations. In the distribution sector, EVN subsidiaries engaged in power distribution purchase bulk power from EVN at administratively fixed bulk power tariffs at 110 kV level and are responsible for power distribution to end users. The tariffs are proposed by EVN and approved by the Government for adjustment annually (effective 1 March each year). This tariff enables power companies and generation companies to achieve a reasonable profit based on their production cost structure. By the end of 2009, the number of electrified communes has exceeded 95% compared to 50% in 1995. B. Sector Issues and Development Challenges

23. The key challenge facing the energy sector is to meet the rapidly increasing energy demand in economically sustainable and environmentally friendly manner. This key challenge evolves into (i) the need for maintaining adequate investments in production capacities and the need for mobilizing sufficient financial resources to meet investment needs; (ii) the need for more competition in energy supply chain, requiring reform and market development; (iii) requirement for higher efficiency in energy production and use and energy conservation and better management of the environmental impacts; and (iv) diversification of energy supply including renewable energies, regional import/export and cooperation. The next paragraphs will elaborate these development challenges, looking at subsector level. Asian Development Bank (ADB) will not be involved in coal production sector due to its high level of potential environmental impacts. Thus, the discussion focuses on power sector and to some extent oil and gas sector.

1. Power Sector

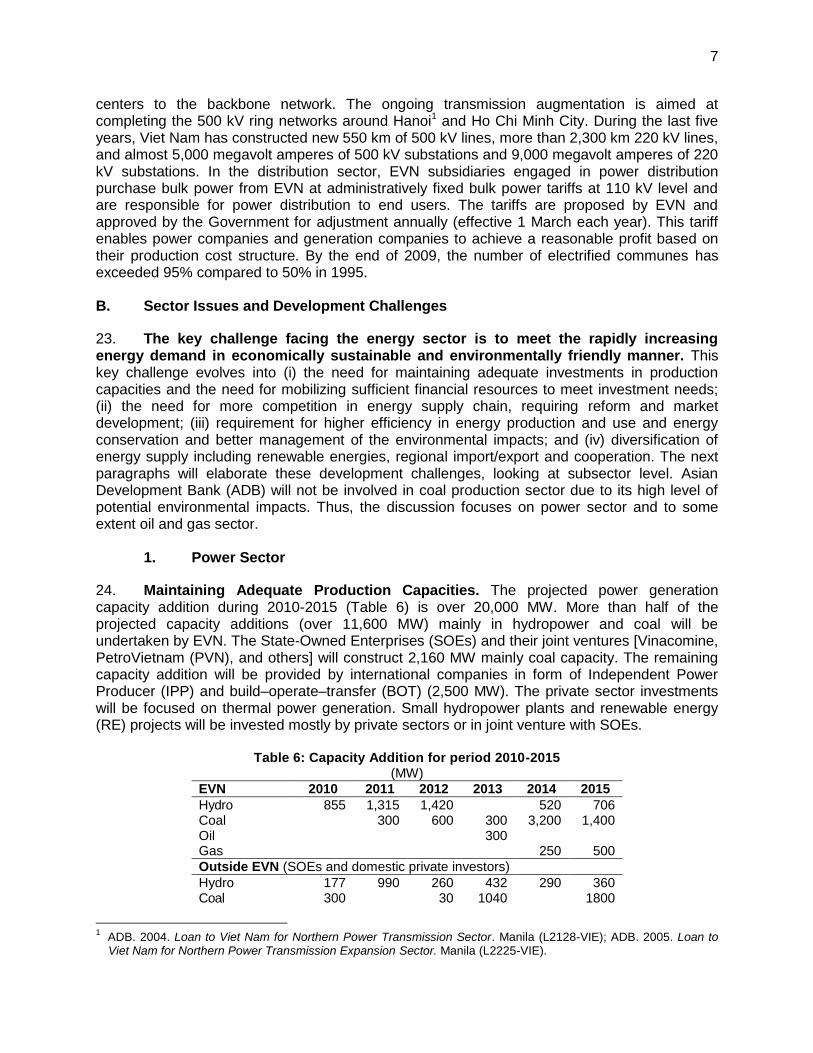

24. Maintaining Adequate Production Capacities. The projected power generation capacity addition during 2010-2015 (Table 6) is over 20,000 MW. More than half of the projected capacity additions (over 11,600 MW) mainly in hydropower and coal will be undertaken by EVN. The State-Owned Enterprises (SOEs) and their joint ventures [Vinacomine, PetroVietnam (PVN), and others] will construct 2,160 MW mainly coal capacity. The remaining capacity addition will be provided by international companies in form of Independent Power Producer (IPP) and build–operate–transfer (BOT) (2,500 MW). The private sector investments will be focused on thermal power generation. Small hydropower plants and renewable energy (RE) projects will be invested mostly by private sectors or in joint venture with SOEs.

Table 6: Capacity Addition for period 2010-2015 (MW)

EVN 2010 2011 2012 2013 2014 2015

Hydro 855 1,315 1,420 520 706 Coal 300 600 300 3,200 1,400 Oil 300 Gas 250 500

Outside EVN (SOEs and domestic private investors)

Hydro 177 990 260 432 290 360 Coal 300 30 1040 1800

1 ADB. 2004. Loan to Viet Nam for Northern Power Transmission Sector. Manila (L2128-VIE); ADB. 2005. Loan to

Viet Nam for Northern Power Transmission Expansion Sector. Manila (L2225-VIE).

8

Gas 750

BOT/IPP (foreign investors)

Hydro 78 95 Coal 2400 BOT = build–operate–transfer, EVN = Vietnam Electricity, IPP = Independent Power Producer, MW = megawatt, SOEs = State Owned Enterprises. Source: Vietnam Electricity, Institute of Energy and staff estimates.

25. Regarding transmission and distribution (T&D) system, the expansion will have to go hand in hand with expansion of the generating capacities. By 2020, the high voltage transmission system will be such that to transfer power throughout the network. Power transfer in the North to Hanoi and surrounding areas will be about 8,000 MW. North—Center power transfer will be about 1,500 MW and power transfer to Ho Chi Minh City and Mekong delta will reach 9,000 MW. The T&D system will require approximately $17.6 billion investment. 26. Mobilizing Financial Resources. The total investment requirement in the power sector including generation, transmission and distribution, for the period 2010-2015 is expected to be in the range of $44 billion out of which, EVN is expected to make an investment of $32 billion covering both generating capacity and network and non-EVN investments in the sector is expected to be $8 billion mostly in generation. International private investors are expected to invest in the order of $3.3 billion.

Table 7: Investment Requirement in Power Sector 2010-2015 ($ million)

Item Investment

EVN 15,025 Non-EVN 8,182 IPP and BOT 3,266

Total generation 26,473

Transmission and Distribution 17,650 BOT = build–operate–transfer, EVN = Viet Nam Electricity, IPP = independent power producer

27. The financial mobilization need for EVN is huge, especially given that EVN is solely responsible for transmission network. Currently, National Power Transmission Company (NPTC) was established (100% owned by EVN) to be in charge of the transmission network. However, due to its novelty without track record of balance sheets, NPTC is not able to raise much needed funds, instead EVN has to raise funds for NPTC. EVN's new investments will be financed through borrowings on commercial terms. The availability of concessionary ODA sources and domestic funds through the government financed Development Assistance Bank (DAB) is limited and EVN is increasingly resorting to borrow on commercial terms from Export Credit Agencies and from ADB and World Bank (WB) on Ordinary Capital Resources (OCR) terms. 28. Non-EVN SOEs play increasing roles in attracting investments for both equity and debt financing for non-EVN financed investments and in developing power generating projects. Foreign private investors will also play increasing role. Recently, the signing of the BOT contract for the Mong Duong 2 (1,200 MW) power project between AES and the Government paves the way for more active involvement of private foreign investors in the power sector in Viet Nam. Jaks Resources of Malaysia has also reached agreement for development of 1,200 MW of Hai Duong power plant.

9

29. Power Sector Reform and Market Development. Sector reform and market development are to liberalize the power industry with the aim to improve efficiency both at the production and at the consumption sides. Sector reform and market development will create favorable conditions for attracting investment, encouraging efficient operation of the power sector through fair and transparent competition. Ultimately, the reform will ensure reliable and competitive supply of electricity to the consumers. 30. Reform of the Viet Nam power market started in 2006 with the Government approval of the roadmap for power market reform by the Prime Minister Decision No. 26/2006/QD-TTg. The Decision stipulates the objectives of the Viet Nam power market, including: (i) ensure stable and reliable high quality electric supply; (ii) attract capital investment for the power sector from all economic sectors both domestic and foreign, gradually reducing state budget investment in the electricity industry; (iii) gradually develop a competitive electric market that operate stably; eliminate subsidy for the electricity industry and expand the choices for the buyers’ rights to select electric suppliers; (iv) improve the production and business efficiency of the electricity industry, thus easing the pressure to raise electricity tariff; and (v) ensure sustainable development of the electricity industry. The Prime Minister decision also defines three stages of the power market development: Stage 1 (2007–2014) development of a competitive power production market (pilot stage from 2007–2009); Stage 2 (2015–2022) development of a competitive wholesale electric market (pilot stage from 2015–2016); and Stage 3 (after 2024) implementation of a competitive retail electric market (pilot stage from 2022–2024). 31. To implement this reform roadmap, on 31 December 2007, the Electricity Power Trading Company (EPTC) was established in the form of a dependent-accounting unit under EVN. EPTC buys power wholesale from power plants and sells wholesale to power distributions companies. EPTC as a single buyer also buys spot delivery on the competitive power production market. Starting January 2008, EPTC has signed power purchase agreements (PPAs) with all power generating companies and with the IPPs. Every year EPTC sign sale contracts with power companies for the following year. 32. In December 2008, the ERAV put forward the Master Plan for Designing the Competitive Power Market and Restructuring of the Power Industry in Viet Nam. The Master Plan proposes the establishment of the Cost-Based-Pool competitive power market. It envisages restructuring of the power sector by separating the generation, load dispatch, transmission and distribution functions and establishing separate companies to perform these different functions: (i) establishment of four independent power generating companies, each consists of a mix of hydro, coal and gas based capacities; (ii) separation of the National Dispatch Center from EVN and establish independent System and Market Operator; (iii) separation transmission functions from EVN and establish National Transmission Company; and (iv) establishment of five power companies in charge of distributions. In December 2009, the NPTC was established. In February 2010, five power distribution companies were established: Northern Power Company, Central Power Company, Southern Power Company, Hanoi Power Company and Ho Chi Minh City Power Company. 33. Dealing with Environmental and Social Issues. The rapid expansion of Viet Nam’s energy/electricity sector is bound to result in significant environmental and social externalities. The addition of large coal power generation capacity will contribute to increased green house gas emissions. However, the current level of per capita green house gas emissions in Viet Nam is among the lowest in the world. This however does require that planning for environmental protection be taken at this stage when massive coal fired complexes are being studied. Super critical and ultra-supercritical technology can help to increase efficiency therefore reducing GHG

10

emission per kilowatt hour produced. The Government is keen on applying these advanced technologies. Some of the hydropower projects involve significant resettlement and environment impacts. The government has strengthened the approval process for environment impact assessments with the recent requirement for hydropower projects to be licensed and improved compensation arrangements for land acquisition for project affected people. 34. ADB is assisting the Government, through Institute of Energy, in applying strategic environmental impact assessment in system planning level so as to recommend the expansion plan that is environment benign. Work has already started. (Post ante assessment for PDP VI was completed, which provide experiences and lessons for the more ambitious application for PDP VII). 35. Energy Efficiency and Conservation. In 2003, the Government of Viet Nam issued the Decree on Efficient Utilization of Energy and Energy Conservation. Subsequently in 2006, the Prime Minister approved the National Targeted Program on Energy Efficiency and Conservation (EEC) for the period 2006–2015. The Program called for a concerted effort in improving energy efficiency, reducing energy losses, and instituting measures for improving energy conservation in all sectors of the economy. The Program has time-bound targeted components and projects, with specific objectives and targets to be achieved by 2015 and beyond. The Program uses economic incentives together with administrative measures to put in place day-to-day energy conservation practices in the whole society. 36. The Program aims at achieving specific targets within a timeframe, to bring about actual reductions in energy production and consumption. The specific objectives of the Program are to: (i) formulate and implement a framework for effective management of EEC within the government, enterprises, and public services, and society as a whole; (ii) establish a model for EEC management and apply the model to 40% of the designated energy consumers/enterprises during the period 2006–2010 and to the remaining 60% by 2015; (iii) formulate and enforce an energy-efficient building code for all new buildings to be constructed after 2008; (iv) achieve 3%–5% reduction of the total energy consumption in the country during 2006–2010 and 5%–8% reduction during 2011–2015 (this is equivalent to saving 5 million tone of oil equivalent (toe) and 13 million toe in the two periods, respectively, based on a business-as-usual scenario); and (v) reduce energy consumption in the industry sector by 5% in 2006–2010 and 8% in 2011-2015 (equivalent to energy savings of 2.6 and 5.0 million toe). 37. Following the implementation of the Decree and the National Target Program, legal and institutional setup was established. The EEC Office was set up within the MOIT in charge of coordinating the energy efficiency and conservation across the economy. The draft laws on EEC are being debated at the National Assembly this May. After six year of continued efforts, EEC gradually take roots in the society. A million CFL program was implemented. A five million CFL program is underway. Solar water heater program with government subsidies recorded some success in Ho Chi Minh City. However, there remain a number of obstacles in realizing energy conservation potential, namely: (i) lack of viable financial mechanism to support energy conservation projects, (ii) absence of EEC fund, and (iii) lack of professional energy service providers who are crucial links between the energy users and conservations practices. 38. ADB has been actively assisting Viet Nam in promoting EEC practices. ADB provided a technical assistance (TA) to assist MOIT in promoting energy conservation and energy-efficient best practices in the industry sector. The TA assisted MOIT in (i) designing training methods and materials for energy managers in industrial enterprises; (ii) conducting a survey of energy consumption in industrial enterprises to identify consumption patterns in industry; (iii)

11

establishing Energy Service Companies that can provide auditing services and advise industrial enterprises on energy conservation measures; (iv) piloting energy audits in selected industrial enterprises; and (v) preparing appropriate investment plans applicable for the audited enterprises to implement as well as advising them on financing so as to realize the energy-saving potential in a profitable manner. In addition, ADB assisted MOIT in upgrading the fifth draft of Energy Conservation Laws for submission to the Government. ADB is looking into the potential energy conservation not only in the industrial sector, but also in water supply and sanitation, household uses, public lighting and retrofitting of power plants. 39. Promotion of REs. Viet Nam has considerable RE resources but so far the utilization is negligible. REs for electricity production mainly consist of small and mini hydro (4,000 MW), wind (3,500 MW), and biogas cogeneration (400 MW). At the moment, the country utilizes about 150 MW cogeneration, all of this is in sugar industry. Only 7.5 MW wind power was constructed in Tuy Phong, Binh Thuan province. The obstacles to more active utilization of renewable energies are lack of: (i) a strong institutional and regulatory framework to support renewable energies; (ii) renewable feed-in tariff mechanism, lack of fund to support upfront investment; and (iii) technical capability. The Government is presently considering the draft Strategy and Master Plan for Renewable Energy Development in Viet Nam up to 2015, and an outlook up to 2025. The Master Plan shows the way ahead for the RE sector development including necessary subsidies to cover the higher costs of renewable energies. REs are best way to power remote areas and isolated islands. There are six island districts where national grid cannot reach. There are several very remote districts, to which extension of the national power grid is not economical. These are the areas that will need to be powered by off-grid electricity or with isolated local lower voltage grid. Remote location makes the cost of construction high especially the cost of transportation of equipment and installation. 40. The Government plans to increase RE capacity to about 1,400 MW in 2015 and 2,900 MW in 2020. A bulk of this renewable capacity will come from wind power in Binh Thuan and Ninh Thuan provinces. ADB assessment of possibility of construction of wind power units on islands shows that the costs will be high and more importantly that there is a need to have local technical capability to man and maintain wind facilities once built. 41. Regional Cooperation and Cross-border Power Trade. Viet Nam currently imports 400 MW power from Yunan province, People’s Republic of China and exports 200 MW to Cambodia through the ADB funded project: Tay Ninh – Sihanoukville. In the future, regional cooperation will continue to play important role. In the North, import from China will increase to about 2,000 MW. The current import uses 220 kV interconnection. The possibility of constructing 500 kV line (HVDC) is being explored. In the future, Lao PDR will become important source of power for Viet Nam. The two countries have signed MOU for power trade of 5,000 MW. Xekaman 3 power plant is under construction by a Viet Lao joint venture. To materialize the potential of Greater Mekong Subregion (GMS) power trade, development of cross border interconnections as well as development of regional power trade mechanism is very important. Currently ADB is assisting GMS countries under the Regional Power Trade Coordination Committee (RPTCC) and will continue to do so. A study for Indochina interconnection plan has started. More works will be required in this important area.

2. Oil and Gas Sector

42. Development Strategy of Oil and Gas Sector. The Oil and Gas Master Plan (2007– 2015, with outlook to 2025) approved by the Government in 2006 sets out the following goals: (i) develop the oil and gas sector comprehensively to be able to carry out a variety of activities

12

covering the entire production cycle, e.g., upstream exploration and production import and export, midstream transport, storage and processing (refineries), downstream distribution and services; (ii) intensify domestic exploration and also expand exploration abroad in joint ventures so as to increase exploitable reserves of oil and gas; (iii) ensure optimal utilization of the country's oil and gas resources to ensure long-term energy security; and (iv) develop oil and gas industry in an environmentally friendly manner, e.g., minimize the impacts on the environment due to exploration, production and transportation, and distribution processes. 43. With regard to oil and gas production and utilization, the Master Plan stresses the "rational and optimal production and use of the national oil and gas resources". In parallel with gas production, the Plan envisages development of a gas market that will use gas most efficiently, namely for power generation, fertilizer production and other industrial and commercial uses. The Plan's target is to reach annual production of 20 million tons of oil and up to 14 billion cubic meters gas by 2015. 44. In order to meet the gas production and consumption target, the Master Plan calls for construction and safe operation of a national gas pipeline network, which integrates the existing gas pipelines (e.g., PM3 – Phu My) with the new pipeline (e.g., Block B – O Mon). The national network should be ready for integration with the trans-ASEAN gas pipeline system in the future. 45. Key challenges. The Master Plan as well as the Implementation Plan (2011-2015) has identified a number of challenges that the oil and gas sector is facing. First is oil price volatility, the uncertainly of oil price represents a factor that negatively impacts PVN's ability to balance its expenditures and income, as revenue from export of crude oil is the single largest source of PVN's income. Thus, the Master Plan calls for combination of domestic production with oversea exploration activities in order to increase income from oversea production. 46. Second, in the today's world of energy insecurity, for a developing country like Viet Nam, which requires constant supply of energy, ensuring supply of the primary energies such as oil and gas is very important task shouldered by PVN. Gas is an important fuel for power generation, and relatively cleaner than coal so providing gas for power development is the key developmental objective of the sector. 47. Third challenge, relating to both of the above, is the need for a very large capital investment. It is estimated that total investment requirement of PVN for the 5 years, 2011-2015, amounts to almost $80 billion, of which, $30 billion for oil exploration, $6 billion for gas production, $22 billion for oil refineries, and the rest for investment in power and other sectors. To meet this challenge, PVN's 5-year plan devises a number of measures for mobilizing financing resources. PVN will be able to mobilize 30% of this capital need (e.g., $24 billion) by putting in its equity and borrowing from the Viet Nam Development Bank. For the large remaining capital need, PVN plans to issue domestic bonds, invite FDI, and commercial borrowings. International financial institutions are the potential source of funds that the PVN's Plan is looking at for assistance. 48. In the oil and gas sector, PVN will mobilize 30% of this capital need (e.g., $24 billion) by putting in its equity and borrowing from the Viet Nam Development Bank. For the large remaining capital need, PVN plans to issue domestic bonds, invite FDI, and commercial borrowings. International financial institutions such as ADB are the potential source of funds that the PVN's Plan is looking at for assistance. In light of this, PVN has requested ADB to assist with financing the Block B — O Mon gas pipeline project. ADB proposes the use of guarantee instruments, which is to facilitate PVN's borrowing from international commercial banks. ADB's

13

guarantee would bring down cost of the borrowing and prolong the tenure of the commercial bank loans. C. ADB Sector Experience and Development Partner Coordination

49. ADB has approved five OCR loans2 amounting to $1,800 million and four Asian Development Fund loans amounting to $320 million3 to the power sector. One guarantee in the amount of $342 million was also approved in 2009. The first three Asian Development Fund Loans were primarily for extensions and rehabilitation of distribution networks. The two OCR loans approved in 2004 and 2005 are to finance the expansion of high voltage transmission system in Northern Viet Nam. The latest financing by ADB (2007 and 2009) is to support building of a 1,000 MW Mong Duong power plant, the 156 MW Song Bung 4 hydro power plant; and to support provincial distribution companies and NPTC to rehabilitate and expand their distribution systems. ADB has also supported private sector investment in power generation4 by providing direct loans and political risk guarantees for the Phu My 2.2 and Phu My 3 power projects in 2002 and 2003, respectively. During 2005-2006, ADB has approved series of advisory technical assistance (ADTAs)5 to improve the crosscutting social and environmental issues of the power sector and two project preparatory technical assistance (PPTAs) to prepare the Song Bung 4 Hydro Power Project. Specifically in 2007, ADB approved an ADTA assisting MOIT in its effort to implement the National Program on energy efficiency and conservation. ADB has expended its assistance beyond the power sector, by providing a PPTA to study the public and private development of a gas pipeline which will transport off-shore natural gas for power generation at the O Mon power complex.6 50. Experiences on implementation of ADB support, including implementation of loan projects and TA projects are mixed. The outcomes are well achieved. But implementation delays occurred mostly in procurement. Lengthy approval process on both Government and ADB sides. Another reason is the requirement to comply with environmental and resettlement implementation plans. Usually, resettlement plans require full compensation and resettlement

2 ADB. 2004. Loan to Viet Nam for Northern Power Transmission Sector Project. Manila (L2128-VIE); ADB. 2005.

Loan to Viet Nam for Northern Power Transmission Expansion Sector Project. Manila (L2225-VIE); ADB. 2007. Loan to Viet Nam for Mong Duong 1 Thermal Power Project. Manila (L2353-VIE); ADB. 2009. Loan to Viet Nam for Mong Duong 1 Thermal Power Project t Tranche 2. Manila (L-2610-VIE); ADB. 2008. Loan to Viet Nam for Song Bung 4 Hydropower Project. Manila (L2429-VIE).

3 ADB. 1972. Loan to Viet Nam for Saigon Power Project. Manila (L0108-VIE); ADB. 1995. Loan to Viet Nam for

Power Distribution for Rehabilitation Project. Manila (L1358-VIE); ADB. 1997. Loan to Viet Nam for Central and Southern Viet Nam Power Distribution Project. Manila (L1585-VIE); ADB. 2009. Loan to Viet Nam for Renewable Energy Development and Network Expansion and Rehabilitation for Remote Communes Sector Project. Manila (L2517-VIE).

4 ADB. 2002. Loan to Mekong Energy Company Limited for Phu My 2.2 Power. Manila (PS-7176); ADB. 2002. Loan

to Viet Nam for Phu My 2.2 Power. Manila (L1906-VIE); ADB. 2002. Loan to Phu My 3 Power. Manila (PS-7178); ADB. 2002. Loan to Viet Nam for Phu My 3 Power. Manila (L1923-VIE).

5 ADB. 2005. Technical Assistance to Viet Nam for Developing Benefit Sharing Mechanism for People Adversely

Affected by Power Generation Projects. Manila (TA4689-VIE); ADB. 2005. Technical Assistance to Viet Nam for Strengthening Institutional Capacity of Local Stakeholders for Implementation of Son La Livelihood and Resettlement Plan. Manila (TA4690-VIE); ADB. 2005. Technical Assistance to Viet Nam for Capacity Building in Strategic Environmental Assessment of Hydropower Project. Manila (TA4713-VIE); ADB. 2005. Technical Assistance to Viet Nam for Implementation of the Environmental Management Plan for Son La Hydropower Project. Manila (TA4711-VIE).

6 ADB. 2007. Technical Assistance to Viet Nam for Supporting Implementation of the National Energy Efficiency

Program. Manila (TA7024-VIE); ADB. 2007. Technical Assistance to Viet Nam for Preparing the Support for the Public-Private Development of the O Mon Gas Pipeline. Manila (TA4923-VIE).

14

before the mobilization of contractors. In reality of transmission projects, even though the line route is identified, actual DMS details will be finalized only after the location of each tower will be fixed. This causes delays in implementation. Impacts of TAs are well recognized. Owing to ADB TAs, institutional reform takes place. The enactment of Electricity Law and the establishment of the ERAV and Energy Efficiency and Conservation Office of Viet Nam (EECOV) are example of success. 51. The other major development partners are the WB, Japan Bank for International Cooperation (JBIC), Agence Francaise de Developpement (AFD), KfW, GTZ, Swedish International Development Cooperation Agency (Sida), Danish International Development Agency (Danida) and Norwegian Agency for Development Cooperation (NORAD). Table 8 shows the development partners involvement in energy sector. ADB plays leading role in a number of areas, namely: (i) physical infrastructure development in generation and transmission system, (ii) promotion of EEC, (iii) regional cooperation and interconnections, and (iv) promotion of private investors. WB plays leading role in power sector reform and market development, rural distribution and rural electrification. JBIC is an important partner in physical infrastructure development in generation, while JICA continuously provides assistance in preparation of PDPs. European partners focuses their assistance in promoting renewable energies, EEC and environmental protection and climate change mitigation. In an effort to streamline the procedure in dealing with assistance by development partners, the Prime Minster has issued a decision 48/2008/QD-TTg, which provides guideline for harmonized project detailed outlines that use funds from five banks (ADB, WB, JBIC, AFD, and KfW). D. ADB Energy Sector Roadmap

1. Rationale

52. Looking ahead in the next ten years, three areas are key for development of the power sector in Viet Nam: (i) sector reform and market development, (ii) meeting demand with reliable supply in environment friendly manner, and (iii) promoting EEC and RE. Among these three, the first one is the most important. Sector reform and market development will allow reducing costs of services, optimal use or resources and higher efficiency through transparent competition, thus, attracting more investor interests. It also allows penetration of RE into the market. Therefore, sector reform and market development will facilitate achieving the goal of second and third area. 53. ADB should position itself to play instrumental role in these processes of capitalizing on its competitive advantages in resource mobilization and knowledge base and experiences in the sector and the mutual understanding and cooperation with counterparts that ADB has cultivated in energy sector in Viet Nam over the years. 54. ADB Strategy 2020 calls for socially inclusive and environmentally sustainable economic growth – a key pillar in ADB’s country strategy for Viet Nam. Under the Strategy 2020, ADB's infrastructure operations will emphasize public-private partnerships and private sector engagements. In this respect, ADB continued assistance to physical infrastructure, generation and transmission, will emphasize mobilizing private sector financing for public sector borrowers through cofinancing and credit enhancement. Generation projects to be supported by ADB will have to be state of the art technology, with low environmental impacts. No coal-fired power plants with sub-critical technology will be supported. Only more efficient coal-fired power plants implemented by private sector will be considered. Priority will be given to high efficiency combined cycle gas turbine. Even for these technologies, ADB will only provide part of the

15

investment and will call on a partner for cofinancing. ADB support for a project will also link to basic infrastructure that would facilitate private investors in the same power complex. 55. Strengthening transmission system is as much important as expansion of generating system. This is evident from the total investment needed (Table 7). Transmission system will have to be developed in synch with generation in order to evacuate power to consumers. ADB will continue its support in this area, making use of experiences learnt through two large projects, especially looking from the implementation point of view (e.g., procurement and implementation of environmental and resettlement plans). 56. ADB will deploy innovative financing instruments, such as sovereign guarantee and non–sovereign guarantee for commercial private lending to meet investment needs of the energy sector in Viet Nam. Private investor participation is a key drive of ADB operation in the next five years. This is well aligned with the new Socio-Economic Development Plan (SEDP) 2011–2015 that the Government is preparing now. The SEDP 2011–2015 places emphasis on the shift from Viet Nam being "the recipient" to "the partner" in working with ADB and other partners. The country has to strive in order to be able to gradually borrow and repay investment needs in commercial terms. Cofinancing and guarantees will be used in most of large generation and transmission investment projects in the years to come. 57. ADB has already provided a TA to assist MOIT in preparing a standardized set of tender documents for BOT projects. The TA implementation is slow. This should be accelerated building on experience of International Finance Corporation on Nghi Son project. This is believed to be of importance for MOIT as more BOT projects will be negotiated in the future following the success of Mong Duong 2 project (AES) and Hai Duong project (Jak Resources Malaysia). This will pave the way for more public-private partnership in power sector. 58. Technical assistances to facilitate power market development will be envisaged in the next few years in ADB operation. Even though WB leads in this area, ADB participation brings additional value added as ERAV will have more than one counterpart to consult difficult issues such as creation of competitive generation market, establishment of ISO, transition from competitive generation market to whole sale market etc. It is important that a TA will be developed in consultation with MOIT and ERAV to help this process. 59. EEC and RE are virtually green fields. Different assistances have been provided by all development partners to promote EEC (see Table 8). However, the impacts have not been felt. This is because assistances provided often sporadic, on piecemeal basis. Assistances were not coordinated in such manner that tackle the two most important barriers: (i) lack of viable domestic Energy Service Providers able of appraising and financing EEC projects, and (ii) lack of appropriate financing mechanism to finance EEC projects, which, though financially viable with very short payback period, are by nature, small size and scattered in many sectors of the economy. The presence of strong and viable Energy Service Companies will serve as aggregators for these EEC projects. In light of this, ADB innovative product is much needed. It has been identified that in order to kick start the mainstreaming of EEC business in Viet Nam a combination of technical assistance, risk-sharing and credit line is required. A PPTA working to operationalize this product is proposed. Such innovative product will utilize multiple venues of resources available in ADB such as, Clean Energy Financing Partnership Facility (CEFPF), Clean Technology Fund (CTF) and public sector loan. 60. In Viet Nam, the institutional and regulatory environment is not yet created to effectively facilitate the development of a RE market and industry. Various assistance has been provided

16

by all development partners to promote RE such as: (i) providing re-financing facility to commercial banks to support renewable energy investment and support the regulatory infrastructure particularly for small grid-connected hydropower (World Bank), (ii) developing a comprehensive overview for financial support mechanism and disbursement for grid-connected projects particularly with regards to a feed-in-tariff mechanism (GTZ), and (iii) creating a framework for planning, preparing, implementing and operating RE off-grid system (SIDA) (see Table 8). One critical aspect at this stage is to set up a strong and transparent central agency. An agency that is responsible for coordinating and managing all aspects related to targeted RE development in line with the country's objectives to address important energy and socio–economic development needs. Viet Nam envisions to set-up a Renewable Energy Development Office. In line with this, ADB proposes TAs and PPTAs to provide targeted support in establishing the central authority as well as building capacity by enabling this agency to translate the general RE targets into specific economic opportunities. This will be complemented with assistance for pilot wind power project to strengthen capacity and know-how for further diversification of Viet Nam's energy matrix. Continuous support will be required to establish an effective institutional and regulatory environment including guidance on grid-connection priorities, interim funding and economic support mechanism, technical standards and guidance documents as well as capacity building of all key stakeholders. MOIT should coordinate with ADB and other development partners regarding the support required to implement these additional necessary actions. Once the institutional and regulatory framework conducive to the roll-out of RE projects is established, ADB will support RE projects implemented with PSP/PPP. 61. RE lacks behind that of EEC. Unlike for EEC, there exist a Governmental decree, draft laws and an office in charge. RE has none of these. Similar to EEC, recently, various assistances have been provided by all development partners to promote RE (see Table 8). However, the impacts have not been felt. It is considered important to establish a ministerial level office in charge of RE. Legal framework development should take place immediately. Assessment of technical potential as well as market potentials will need to be undertaken. In parallel, assistance to green field projects, such as wind power, biogas, etc. cannot wait. In this light, ADB proposes a number of TAs and PPTAs to assist MOIT in promoting RE. 62. Mitigating the future adverse impacts of global climate change is one important area for Viet Nam a country known to be most vulnerable to sea level rise in Southeast Asia. Climate change mitigation will have to be streamlined into sector works. This is being proposed in the pipeline. 63. Regional cooperation is on-going and will continue. Participation of Viet Nam in GMS program as well as in other ASEAN fora will continue to be supported by ADB. Particularly under the RPTCC umbrella, cross-border interconnections will be further studied and ensuing projects will be pursued.

2. Program for 2011-2015

64. Given limited financial and staff resources, ADB should rationalize its assistance program in energy sector in Viet Nam. On the other hand, being the single most important regional development institution, ADB cannot afford losing sight of key development areas. Thus, the program for 2011-2015 should be selective but comprehensive. The program consists of "soft" assistance, meaning, technical assistance to build capacity, institutions and regulatory and legal framework, and "hard" assistance, meaning, financing of physical infrastructure using innovative financing mechanisms.

17

a. Technical Assistance

65. In the next five to ten years, evolution of power market and sector restructuring is the most important process. This will set stage for transparent competition, higher efficiency, more private investment, etc. Currently WB leads in this area. However, ADB needs to participate. It is proposed to develop a TA to assist ERAV in pushing ahead with (i) generation competitive market, establishment and functioning of ISO; (ii) mechanism for wheeling charge by NPTC; and (iii) benefit-sharing mechanism for people affected by hydropower plants. Tariff adjustment, which takes place annually, is an imperative need for ERAV. With the gradual liberalizing fuel prices (coal and oil) and with the perspective of importing fuel for power generation with international market prices, calculation of production costs — the basis for tariff adjustment — is an urgent need by ERAV. One comprehensive TA is proposed to provide methodological development for all the above is proposed (instead of numerous Small Scale TAs). 66. As discussed above, institutional and legal building for RE is the first step in promoting penetration of RE. MOIT has expressed the need for ADB's assistance in several occasions. It is proposed to develop a TA to help MOIT in setting up an RE office, preparing decree on promotion of RE, which will be developed later into RE law. The TA can also cover resource mapping and feed-in tariff institutionalization.

b. Lending products

67. In the field of EEC, a three-in-one product is proposed: a credit line (loan) combined with risk-sharing and technical assistance will meet the need of EEC market in Viet Nam. A PPTA is proposed for this purpose, which will lead to ensuing project. 68. Financing of T&D system will be undertaken mostly by guarantees. Financing of generating capacities will be selective (high efficient, environment friendly technologies only) with co-financing and also guarantees. RE (e.g., wind power) projects will be given priority. 69. Based on the above main considerations, the following program has been developed jointly by Energy Team (see Table 9).

18

Table 8: Development Partner Coordination in Energy Sector in Viet Nam

Area of Assistance ADB WB JBIC/ JICA

AFD KfW/ GTZ Danida Sida/ NORAD

Power Development Plan X (SEA for PDP VII)

X XX (JICA)

X (National

hydro plan) Sector reform and market X

(TA) X

(TA) X

Promotion of legal framework, DSM programs for EEC

XX (draft laws,

EE in industry)

X (DSM)

X (EEC loan)

X X X

Promotion of legal and institutional framework for RE

X (TA)

X X X X (feed-in

tariff study)

X X

Physical infrastructure - generation XX X X X X Physical infrastructure - transmission XX X X X X Physical infrastructure — distribution and rural electrification

X XX X

Physical infrastructure — oil and gas X National dispatch center(s) X XX NPTC X Managing environmental impacts and climate change mitigation

X X X X X

Innovative financing mechanism X (guarantee)

X (program

loan)

Regional interconnections XX (RPTCC)

X X X

Promoting private sector participation XX X ADB = Asian Development Bank; AFD = Agence Francaise de Developpement; Danida = Danish International Development Agency; DSM == demand side management; EE == energy efficiency; EEC = Energy Efficiency and Conservation; JBIC = Japan Bank for International Cooperation; JICA =Japan International Cooperation Agency; NORAD = Norwegian Agency for Development Cooperation; NPTC == National Power Transmission Company; PDP = Power Development Plan; RPTCC = Regional Power Trade Coordination Committee; RE = renewable energy; Sida = Swedish International Development Cooperation Agency; TA = technical assistance; WB = World Bank Source: ADB staff compilation.

19

Table 9: Energy Sector Program for 2011-2015 (Road Map)

Function

Description of Need and

Anticipated Outputs

ADB Assistance (YES/NO)

Justification of ADB Assistance

Planned Assistance (Year/TA/Project)

ADB Staff Status

A. Sector: Energy Subsector: Electricity

Thematic area in road map: (i) Meeting rapidly increasing demand by expanding the power sector

A.1 Expansion of Transmission and Distribution network

Finance new transmission and distribution investments to evacuate power from new generation sources to the demand centers; reduce T&D losses.

YES In line with the Government of Viet Nam and policies in building basic infrastructure enabling efficiency and market; ADB has extensive experiences in the past.

2010 Guarantee for a Commercial Loan to Hanoi Power Company 2010 Power Transmission Project (PPTA) 2011 Power Transmission Project (MFF)

X. Humbert

A.2 Expansion of cross border interconnection with neighboring countries

Finance new transmission interconnection with Lao PDR, Cambodia and PRC.

YES In line with the Government of Viet Nam and ADB regional cooperation and integration. In line with GMS regional power trade cooperation. ADB has good experiences.

2011 Regional Bansok- Pleiku Power Transmission Project (Lao PDR- Viet Nam)

X. Humbert

A.3 Expansion of medium voltage cross border connection with Lao PDR

Financial support for interconnection with southern Lao PDR along the East-West Economic Corridor

YES In line with the Government of Viet Nam and ADB regional cooperation and integration. In line with GMS regional power trade cooperation. ADB has good experiences.

2011 East — West Corridor T&D project (Lao PDR – Viet Nam)

D.T. Bui

A.4 Expansion of generating

Finance new generating power

YES, selective

In line with National Power Development Plans and the

2011 O Mon IV CCGT

D.T. Bui

20

Function

Description of Need and

Anticipated Outputs

ADB Assistance (YES/NO)

Justification of ADB Assistance

Planned Assistance (Year/TA/Project)

ADB Staff Status

capacities plant in order to ensure adequate system capacity to meet the growing demand

only Government of Viet Nam policies. ADB has extensive experiences in the past ADB to finance only clean technologies with high efficiency, e.g., CCGT. No financing for sub-critical coal fired technologies. Super critical coal-fired technologies may be supported selectively with PSP or PPP basis. Possible financing for hydro power projects

2013 O Mon V CCGT TBD

B. Sector: Energy Sub-sector: Electricity

Thematic area in road map: (ii) Sector reform

B.1 Promotion of power sector restructuring

Support restructuring of the power sector toward more competitive direction

YES ADB can jointly work with other development partners, such as JICA, Sida, WB, etc.

2010 TA to assist improving the efficiency of the National Power Transmission Corporation Through Targeted Capacity Building. 2012 TA to support ERAV in implementation of the

X. Humbert D.T. Bui

21

Function

Description of Need and

Anticipated Outputs

ADB Assistance (YES/NO)

Justification of ADB Assistance

Planned Assistance (Year/TA/Project)

ADB Staff Status

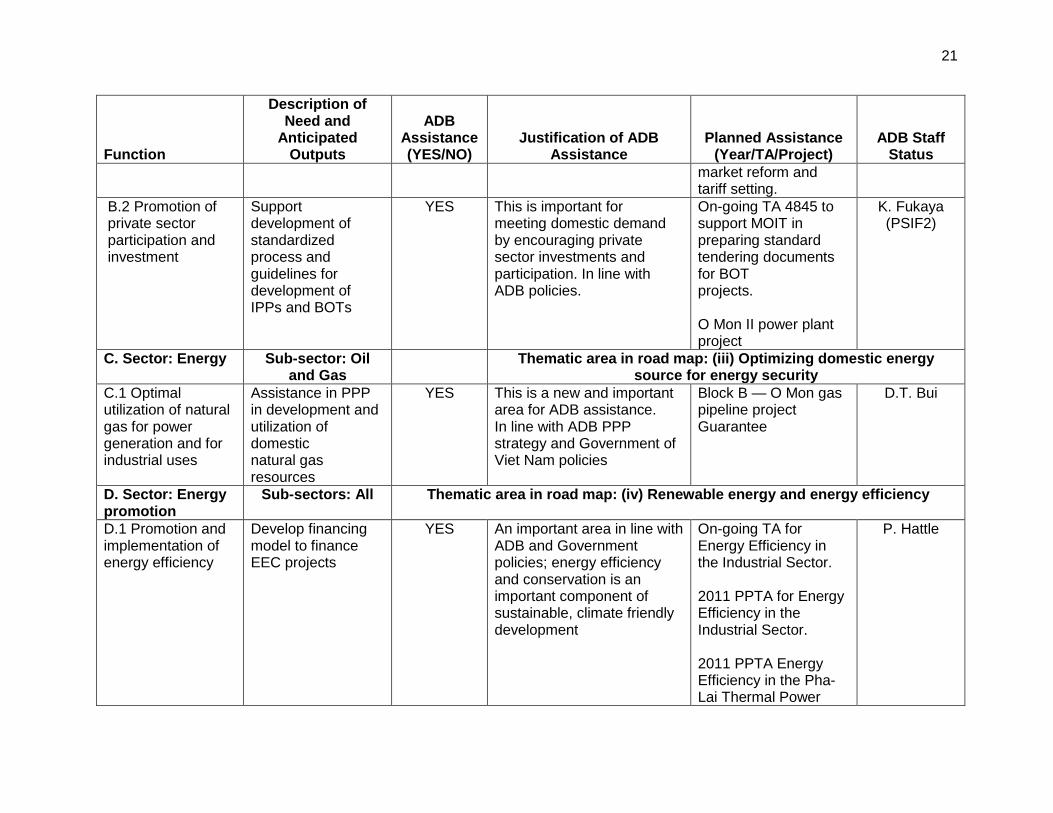

market reform and tariff setting.

B.2 Promotion of private sector participation and investment

Support development of standardized process and guidelines for development of IPPs and BOTs

YES This is important for meeting domestic demand by encouraging private sector investments and participation. In line with ADB policies.

On-going TA 4845 to support MOIT in preparing standard tendering documents for BOT projects. O Mon II power plant project

K. Fukaya (PSIF2)

C. Sector: Energy Sub-sector: Oil and Gas

Thematic area in road map: (iii) Optimizing domestic energy source for energy security

C.1 Optimal utilization of natural gas for power generation and for industrial uses

Assistance in PPP in development and utilization of domestic natural gas resources

YES This is a new and important area for ADB assistance. In line with ADB PPP strategy and Government of Viet Nam policies

Block B — O Mon gas pipeline project Guarantee

D.T. Bui

D. Sector: Energy promotion

Sub-sectors: All Thematic area in road map: (iv) Renewable energy and energy efficiency

D.1 Promotion and implementation of energy efficiency

Develop financing model to finance EEC projects

YES An important area in line with ADB and Government policies; energy efficiency and conservation is an important component of sustainable, climate friendly development

On-going TA for Energy Efficiency in the Industrial Sector. 2011 PPTA for Energy Efficiency in the Industrial Sector. 2011 PPTA Energy Efficiency in the Pha-Lai Thermal Power

P. Hattle

22

Function

Description of Need and

Anticipated Outputs

ADB Assistance (YES/NO)

Justification of ADB Assistance

Planned Assistance (Year/TA/Project)

ADB Staff Status

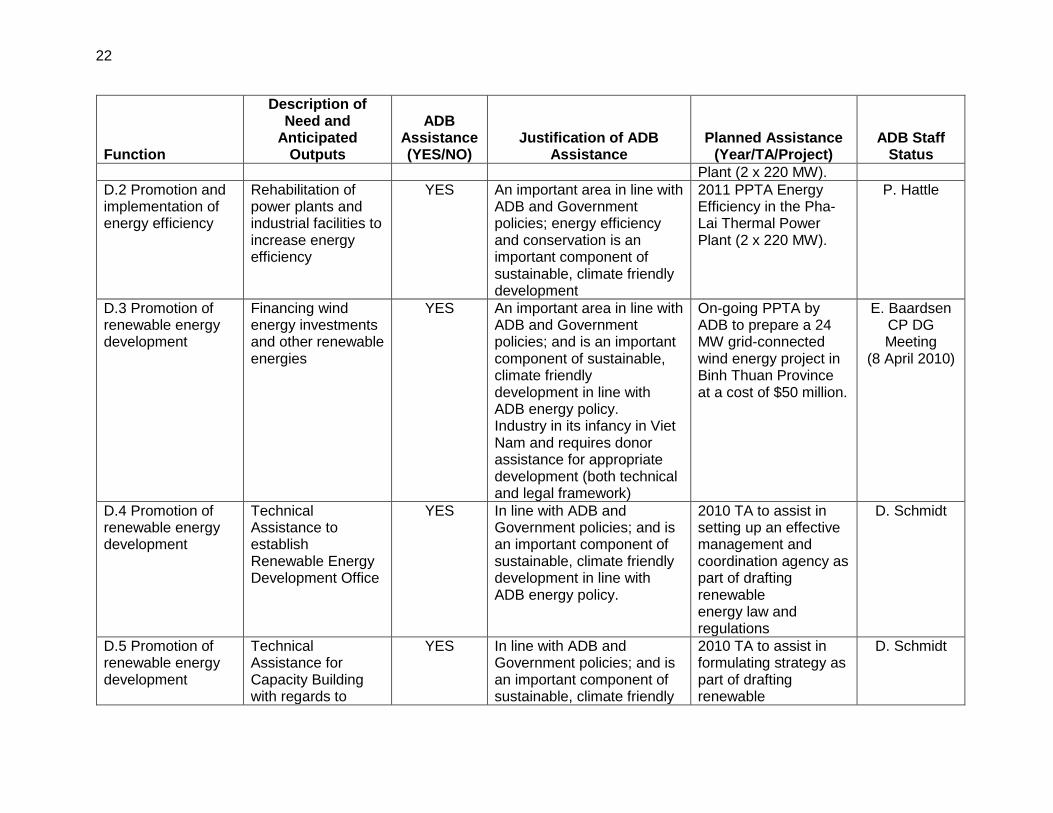

Plant (2 x 220 MW).

D.2 Promotion and implementation of energy efficiency

Rehabilitation of power plants and industrial facilities to increase energy efficiency

YES An important area in line with ADB and Government policies; energy efficiency and conservation is an important component of sustainable, climate friendly development

2011 PPTA Energy Efficiency in the Pha-Lai Thermal Power Plant (2 x 220 MW).

P. Hattle

D.3 Promotion of renewable energy development

Financing wind energy investments and other renewable energies

YES An important area in line with ADB and Government policies; and is an important component of sustainable, climate friendly development in line with ADB energy policy. Industry in its infancy in Viet Nam and requires donor assistance for appropriate development (both technical and legal framework)

On-going PPTA by ADB to prepare a 24 MW grid-connected wind energy project in Binh Thuan Province at a cost of $50 million.

E. Baardsen CP DG Meeting

(8 April 2010)

D.4 Promotion of renewable energy development

Technical Assistance to establish Renewable Energy Development Office

YES In line with ADB and Government policies; and is an important component of sustainable, climate friendly development in line with ADB energy policy.

2010 TA to assist in setting up an effective management and coordination agency as part of drafting renewable energy law and regulations

D. Schmidt

D.5 Promotion of renewable energy development

Technical Assistance for Capacity Building with regards to

YES In line with ADB and Government policies; and is an important component of sustainable, climate friendly

2010 TA to assist in formulating strategy as part of drafting renewable

D. Schmidt

23

Function

Description of Need and

Anticipated Outputs

ADB Assistance (YES/NO)

Justification of ADB Assistance

Planned Assistance (Year/TA/Project)

ADB Staff Status

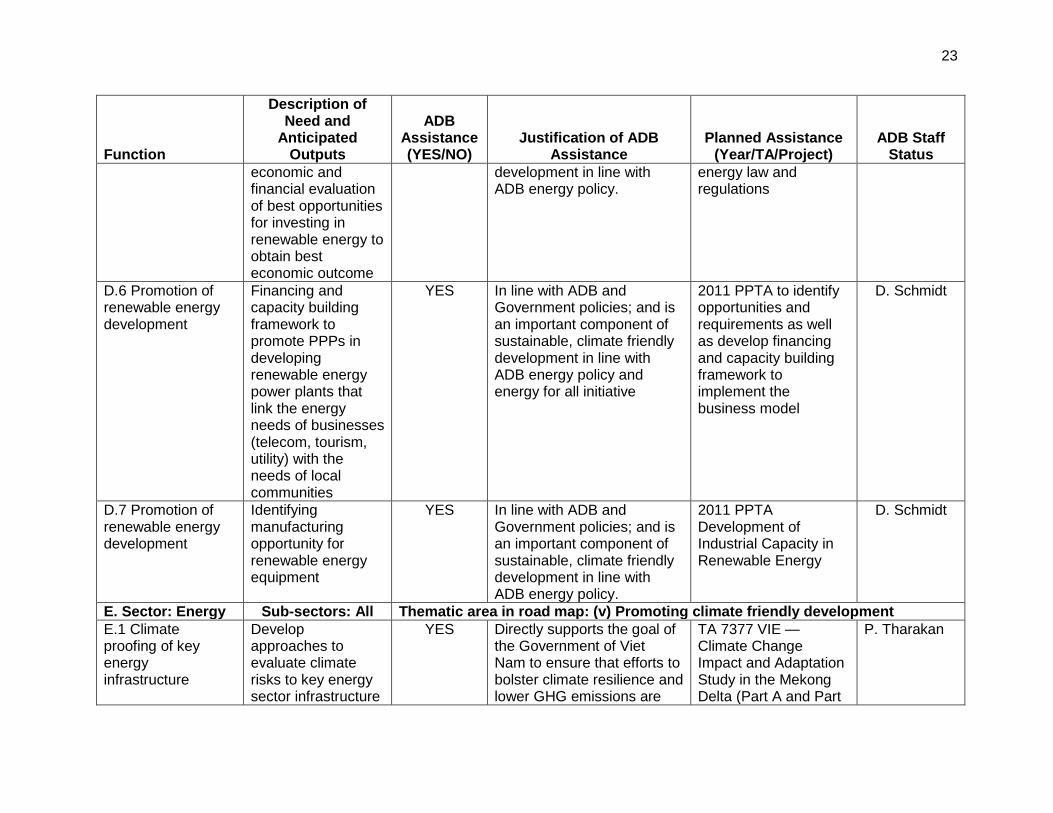

economic and financial evaluation of best opportunities for investing in renewable energy to obtain best economic outcome

development in line with ADB energy policy.

energy law and regulations

D.6 Promotion of renewable energy development

Financing and capacity building framework to promote PPPs in developing renewable energy power plants that link the energy needs of businesses (telecom, tourism, utility) with the needs of local communities

YES In line with ADB and Government policies; and is an important component of sustainable, climate friendly development in line with ADB energy policy and energy for all initiative

2011 PPTA to identify opportunities and requirements as well as develop financing and capacity building framework to implement the business model

D. Schmidt

D.7 Promotion of renewable energy development

Identifying manufacturing opportunity for renewable energy equipment

YES In line with ADB and Government policies; and is an important component of sustainable, climate friendly development in line with ADB energy policy.

2011 PPTA Development of Industrial Capacity in Renewable Energy

D. Schmidt

E. Sector: Energy Sub-sectors: All Thematic area in road map: (v) Promoting climate friendly development

E.1 Climate proofing of key energy infrastructure

Develop approaches to evaluate climate risks to key energy sector infrastructure

YES

Directly supports the goal of the Government of Viet Nam to ensure that efforts to bolster climate resilience and lower GHG emissions are

TA 7377 VIE — Climate Change Impact and Adaptation Study in the Mekong Delta (Part A and Part

P. Tharakan

24

Function

Description of Need and

Anticipated Outputs

ADB Assistance (YES/NO)

Justification of ADB Assistance

Planned Assistance (Year/TA/Project)

ADB Staff Status

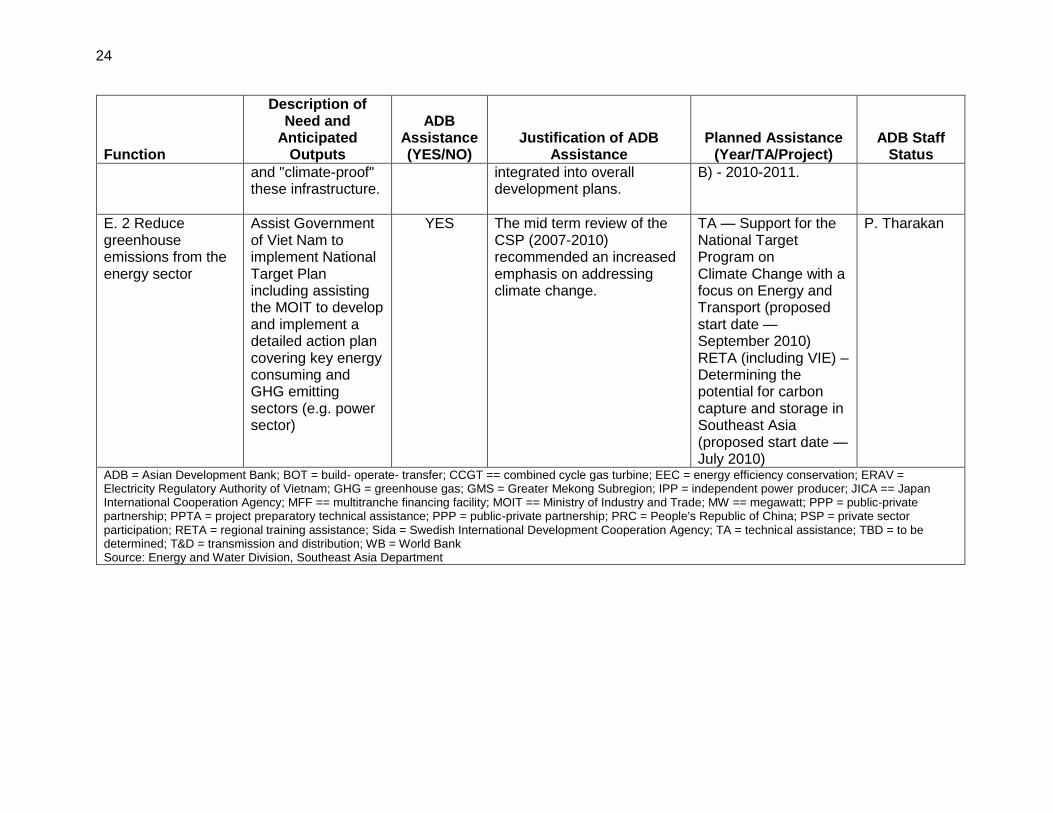

and "climate-proof" these infrastructure.

integrated into overall development plans.

B) - 2010-2011.

E. 2 Reduce greenhouse emissions from the energy sector

Assist Government of Viet Nam to implement National Target Plan including assisting the MOIT to develop and implement a detailed action plan covering key energy consuming and GHG emitting sectors (e.g. power sector)

YES The mid term review of the CSP (2007-2010) recommended an increased emphasis on addressing climate change.

TA — Support for the National Target Program on Climate Change with a focus on Energy and Transport (proposed start date — September 2010) RETA (including VIE) – Determining the potential for carbon capture and storage in Southeast Asia (proposed start date — July 2010)

P. Tharakan

ADB = Asian Development Bank; BOT = build- operate- transfer; CCGT == combined cycle gas turbine; EEC = energy efficiency conservation; ERAV = Electricity Regulatory Authority of Vietnam; GHG = greenhouse gas; GMS = Greater Mekong Subregion; IPP = independent power producer; JICA == Japan International Cooperation Agency; MFF == multitranche financing facility; MOIT == Ministry of Industry and Trade; MW == megawatt; PPP = public-private partnership; PPTA = project preparatory technical assistance; PPP = public-private partnership; PRC = People's Republic of China; PSP = private sector participation; RETA = regional training assistance; Sida = Swedish International Development Cooperation Agency; TA = technical assistance; TBD = to be determined; T&D = transmission and distribution; WB = World Bank Source: Energy and Water Division, Southeast Asia Department

Related Documents