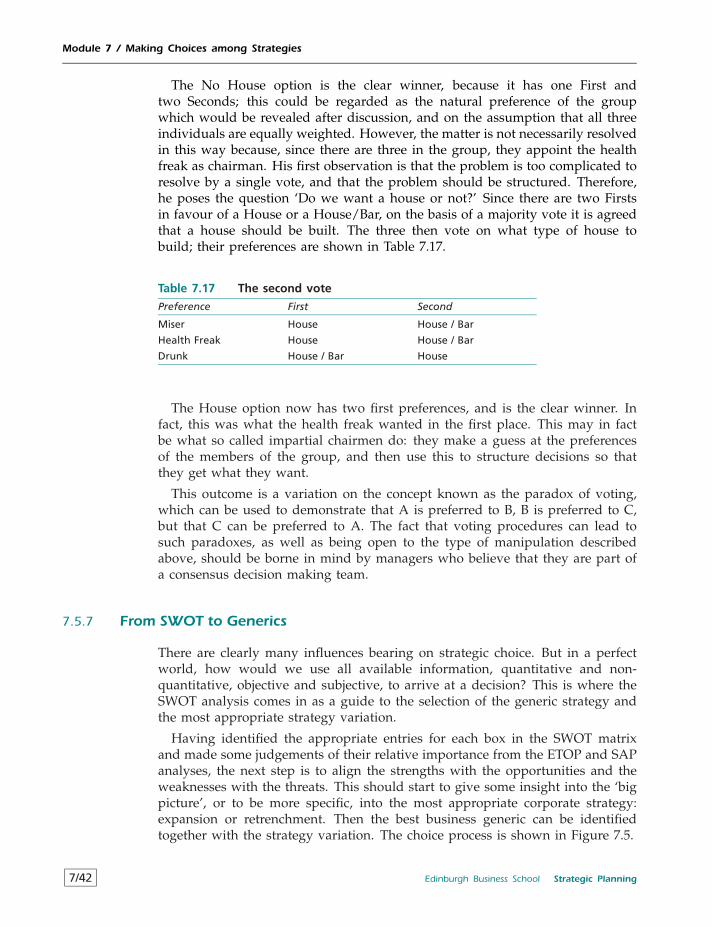

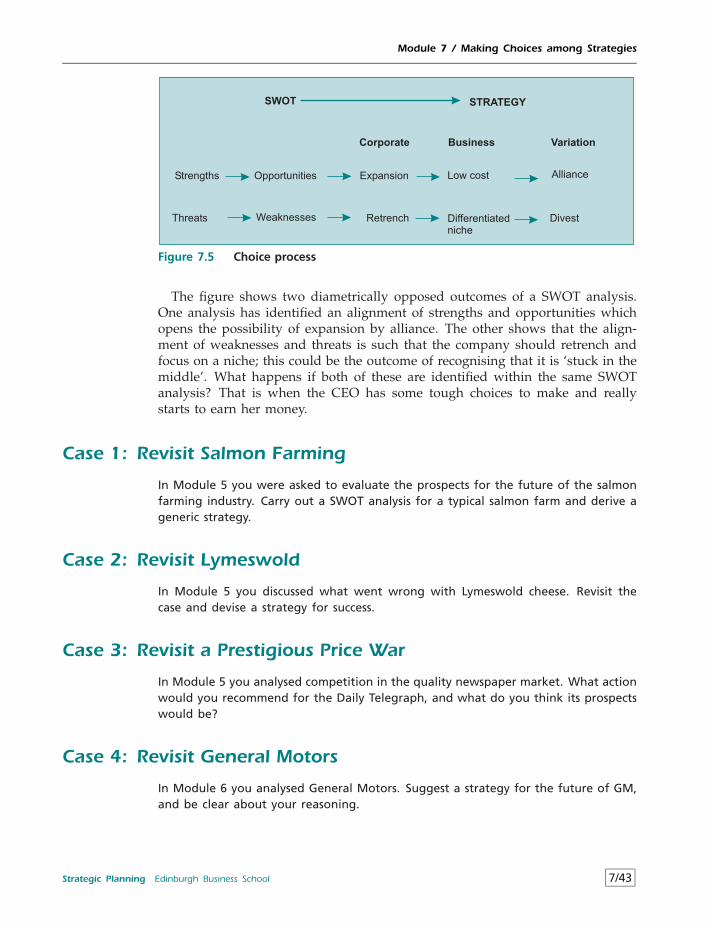

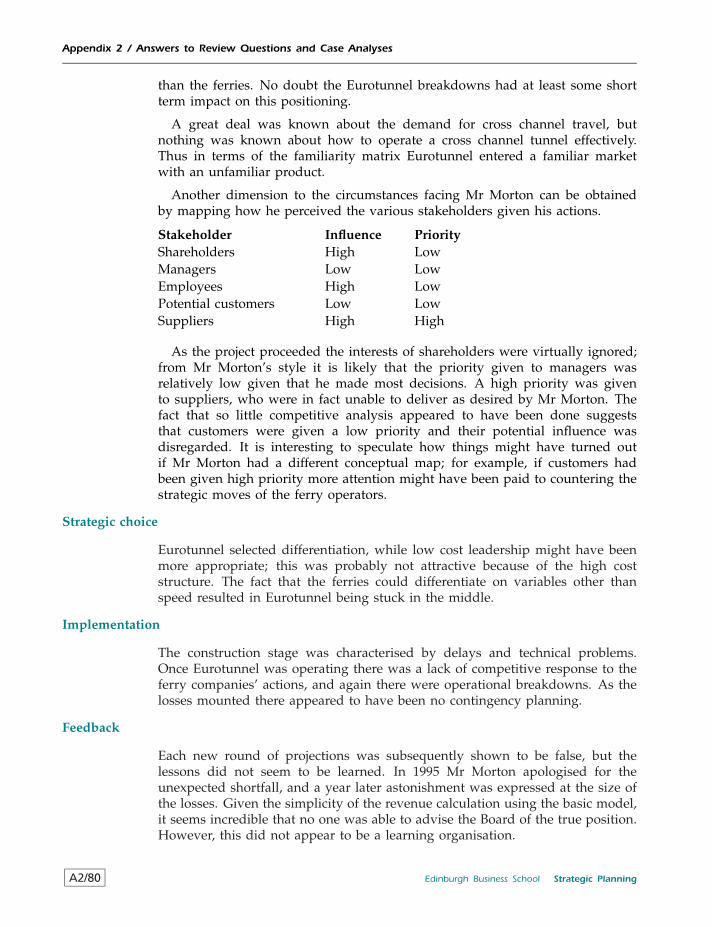

Strategic Planning Professorial Fellow of Edinburgh Business School, The Graduate School of Business, Heriot-Watt University, Alex Scott (MA, MSc, PhD) is an economist and has published over thirty research papers into efficiency in education, efficient use of energy, energy and the environment and the cost to the taxpayer of government industrial aid programmes. He is a pioneer in developing and carrying out research into new educational techniques, particularly in the field of business simulations. Professor Scott’s executive teaching includes running strategic planning sessions for groups of senior managers, widening the perspectives of functional managers, and teaching financial specialists the principles of how economies function in today’s highly complex and interdependent world. Among the companies for which he has run man- agement programmes are American Express, British Rail, British Telecom, Cathay Pacific, Fiskars, Hewlett-Packard, National Health Service, ScottishPower, Scottish Widows, Swiss Bank Corporation. Release SP-A1.3 ISBN 0 273 60924 6

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

StrategicPlanning

Professorial Fellow of Edinburgh Business School, The Graduate School of Business,Heriot-Watt University, Alex Scott (MA, MSc, PhD) is an economist and has published overthirty research papers into efficiency in education, efficient use of energy, energy andthe environment and the cost to the taxpayer of government industrial aid programmes.He is a pioneer in developing and carrying out research into new educational techniques,particularly in the field of business simulations.

Professor Scott’s executive teaching includes running strategic planning sessions forgroups of senior managers, widening the perspectives of functional managers, andteaching financial specialists the principles of how economies function in today’s highlycomplex and interdependent world. Among the companies for which he has run man-agement programmes are American Express, British Rail, British Telecom, Cathay Pacific,Fiskars, Hewlett-Packard, National Health Service, ScottishPower, Scottish Widows, SwissBank Corporation.

Release SP-A1.3

ISBN 0 273 60924 6

HERIOT-WATT UNIVERSITY

StrategicPlanning

Professor Alex Scott MA, MSc, Phd

Edinburgh Gate, Harlow, Essex CM20 2JE, United KingdomTel: +44 (0) 1279 623112Fax: +44 (0) 1279 623223

Pearson Education website: www.pearsoned-ema.com

A Pearson company

Release SP-A1.3

First published in Great Britain in 2003

c© 2003 Alex Scott

The right of Professor Alex Scott to be identified as Author of thisWork has been asserted by him in accordance with the Copyright, Designsand Patents Act 1988.

ISBN 0 273 60924 6

British Library Cataloguing in Publication DataA CIP catalogue record for this book can be obtained from the British Library.

All rights reserved; no part of this publication may be reproduced, storedin a retrieval system, or transmitted in any form or by any means, electronic,mechanical, photocopying, recording, or otherwise without the prior writtenpermission of the Publishers. This book may not be lent, resold, hiredout or otherwise disposed of by way of trade in any form of binding orcover other than that in which it is published, without the prior consentof the Publishers.

Typesetting and SGML/XML source management by CAPDM Ltd. (www.capdm.com)Printed and bound in Great Britain.

The publisher’s policy is to use paper manufactured from sustainable forests.

Contents

Using the Course Package 9

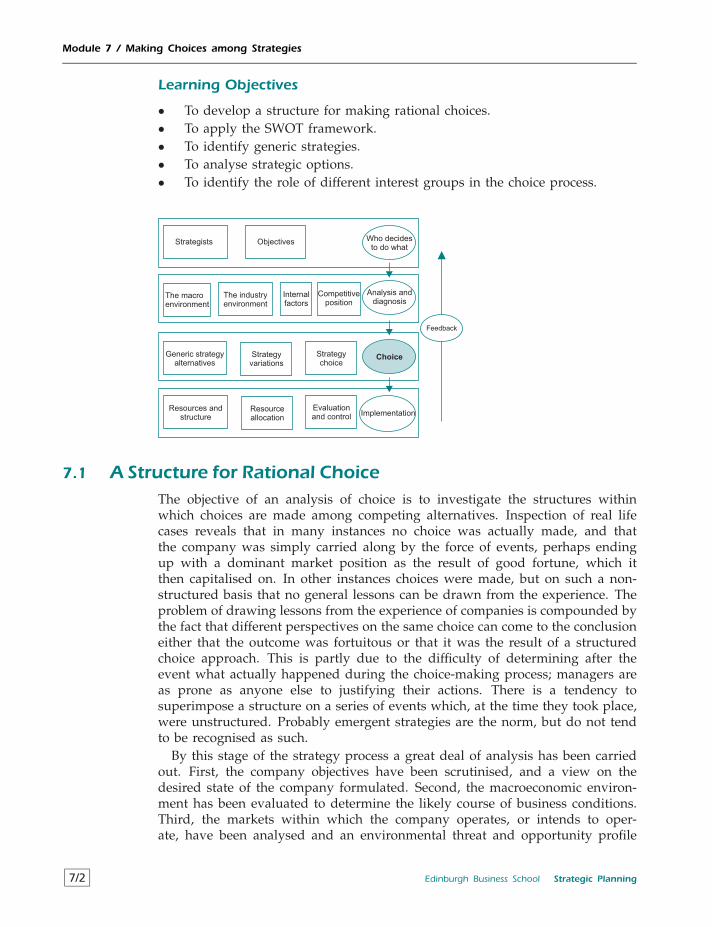

Module 1 Introduction to Strategy, Planning and Structure 1/11.1 Strategic Planning: The Context 1/21.2 What Is Strategic Planning? 1/41.3 The Process of Strategy and Decision Making 1/231.4 Business Unit and Corporate Strategy 1/401.5 Is Strategic Planning Only for Top Management? 1/47

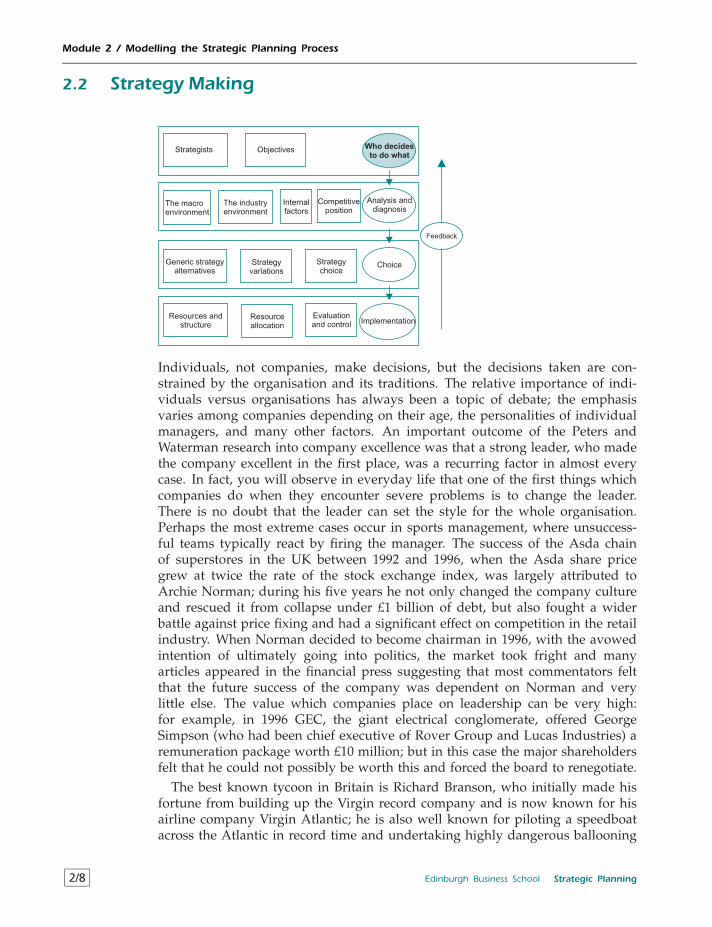

Module 2 Modelling the Strategic Planning Process 2/12.1 The Modelling Approach 2/12.2 Strategy Making 2/8

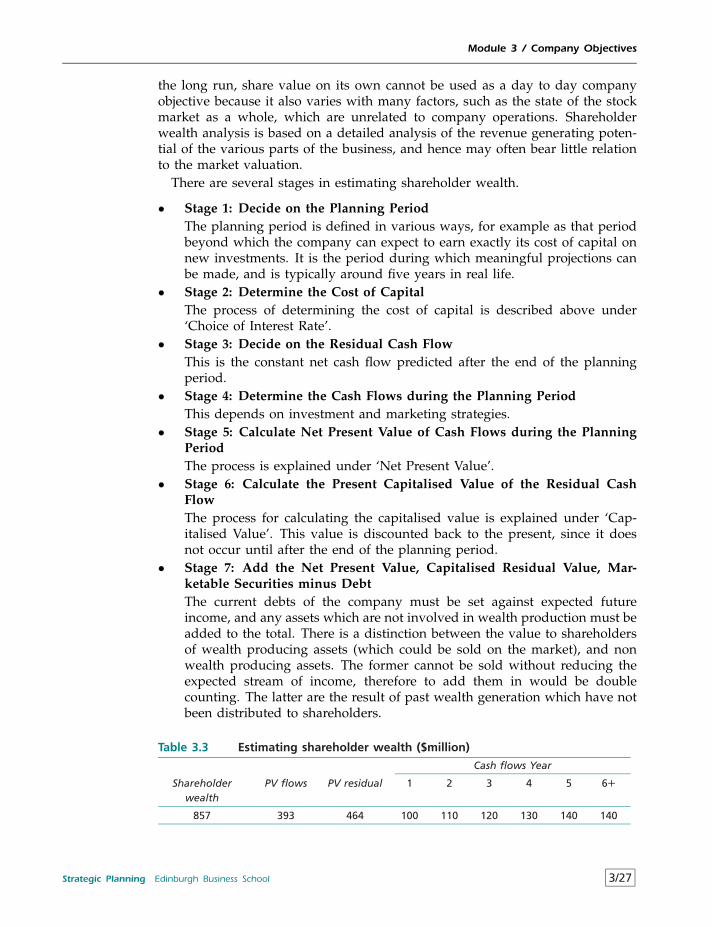

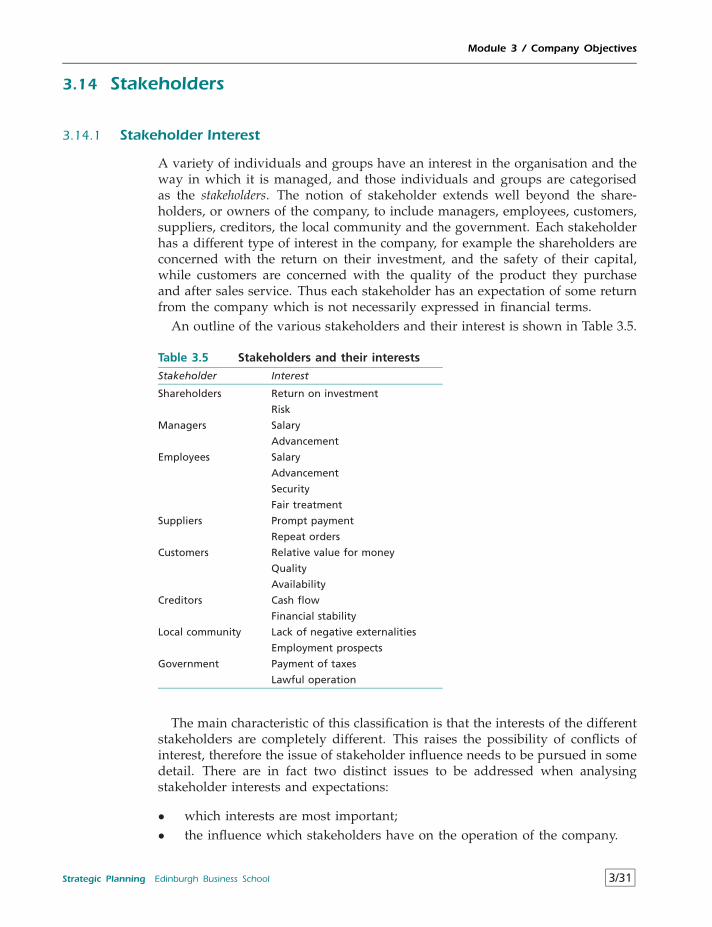

Module 3 Company Objectives 3/13.1 Setting Objectives 3/23.2 From Vision to Mission to Objectives 3/33.3 The Gap Concept 3/73.4 Credible Objectives 3/103.5 Quantifiable and Non-Quantifiable Objectives 3/113.6 Aggregate Objectives 3/133.7 Disaggregated Objectives 3/143.8 The Principal/Agent Problem 3/153.9 Means and Ends 3/173.10 Behavioural versus Economic and Financial Objectives 3/183.11 Economic Objectives 3/183.12 Financial Objectives 3/213.13 Social Objectives 3/293.14 Stakeholders 3/313.15 Ethical Considerations 3/38

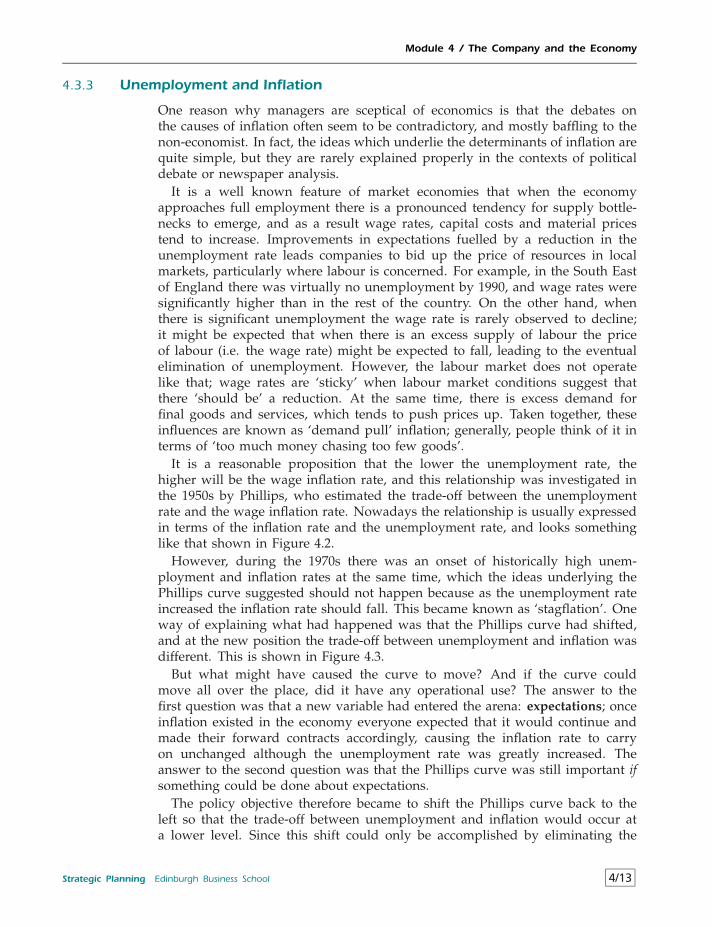

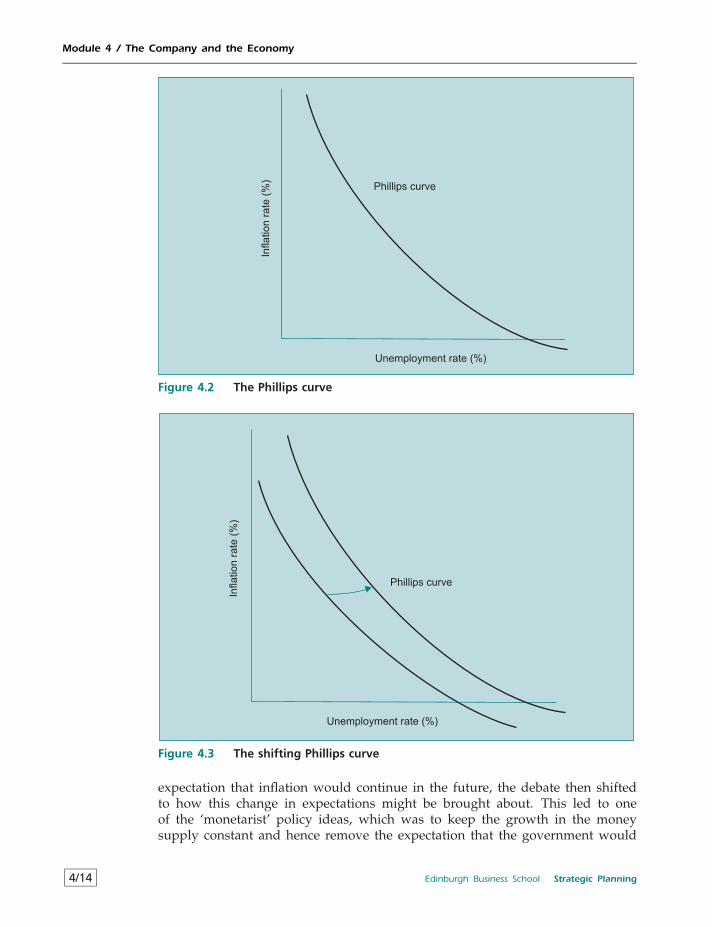

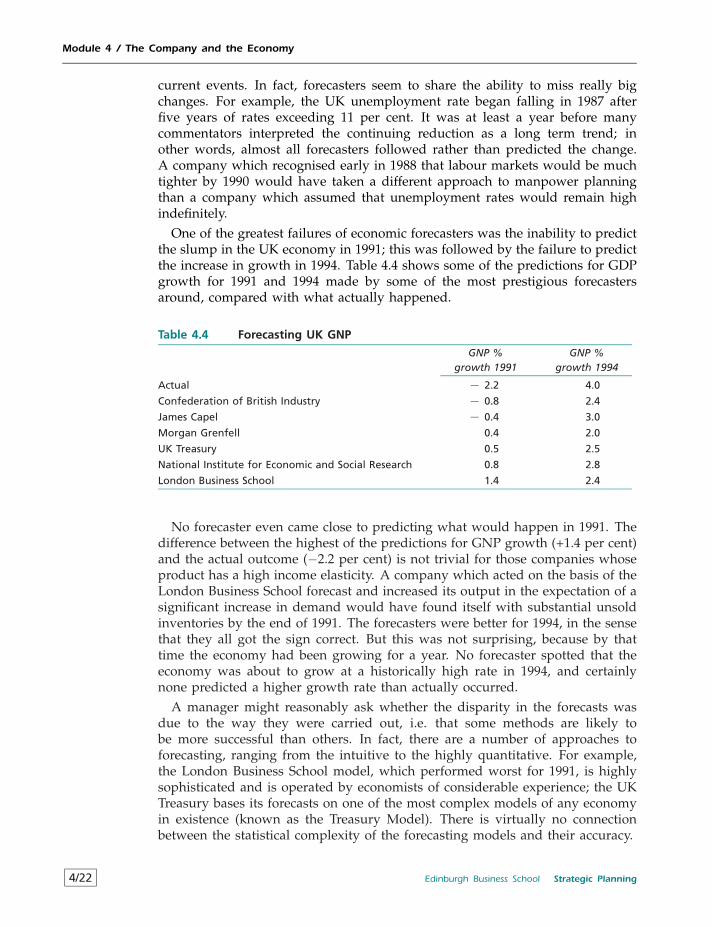

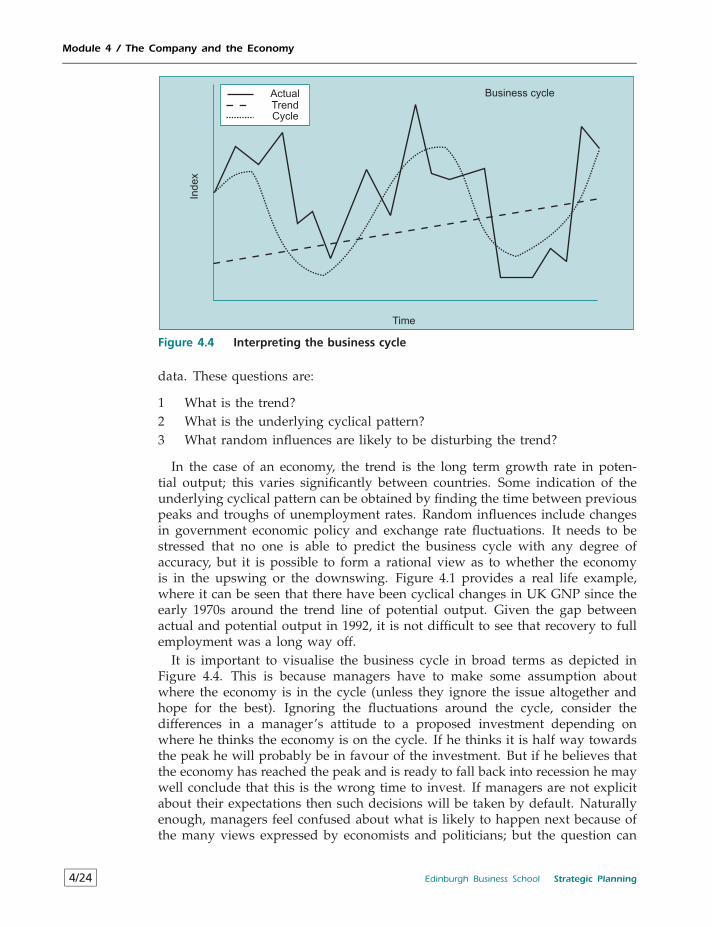

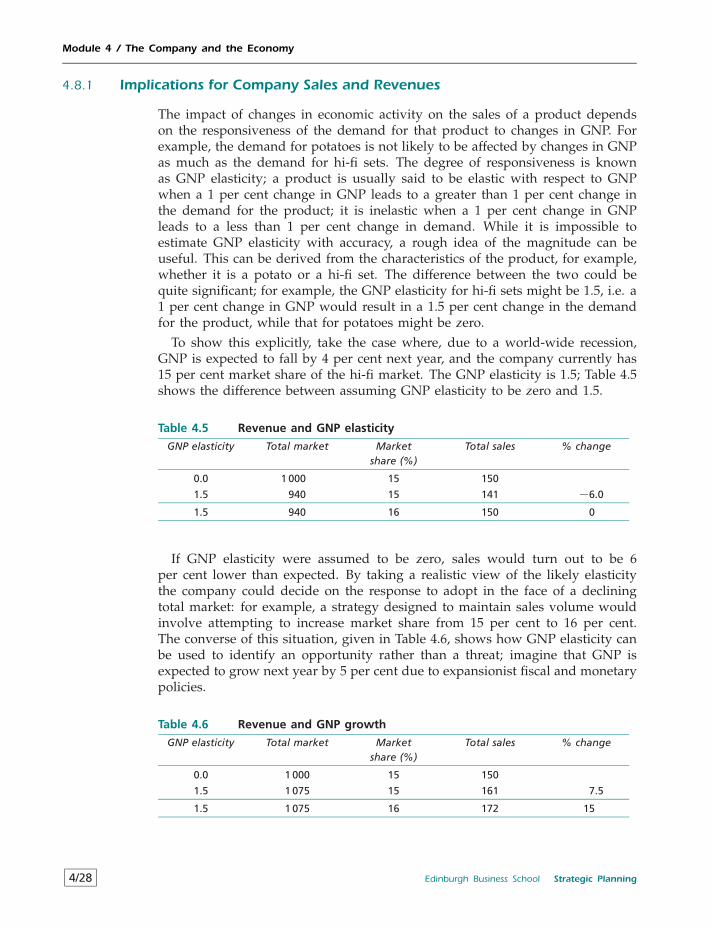

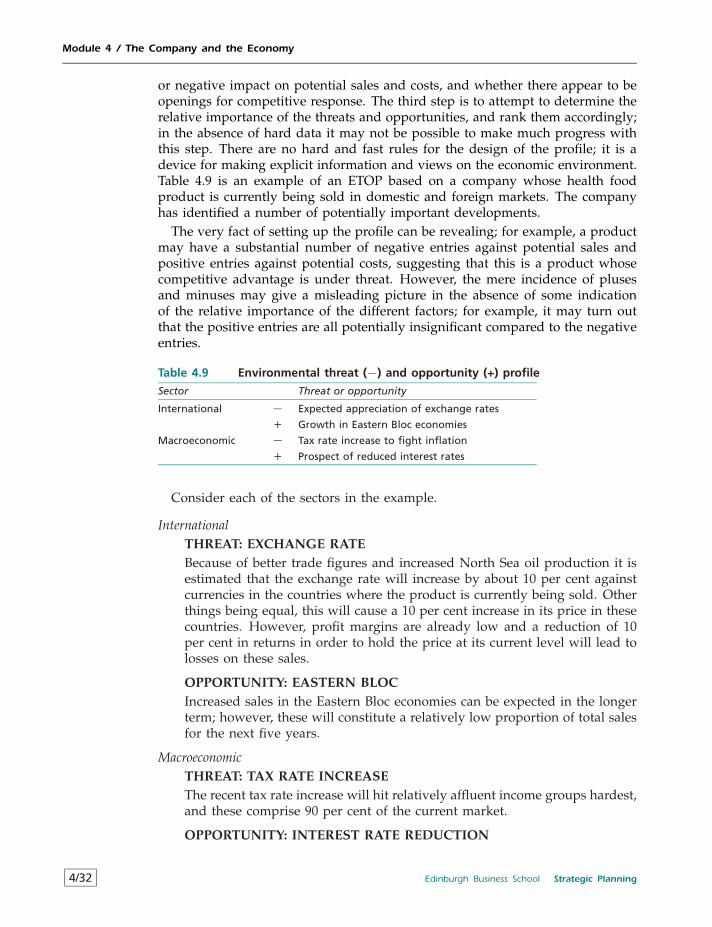

Module 4 The Company and the Economy 4/14.1 The Company in the Economic Environment 4/24.2 Revenue and Costs: The Basic Model 4/34.3 The Workings of the Economy 4/44.4 Forecasting: What Will Happen Next? 4/214.5 PEST Analysis 4/254.6 Environmental Scanning 4/264.7 Scenarios 4/274.8 The Economy and Profitability 4/274.9 Environmental Threat and Opportunity Profile: Part 1 4/31

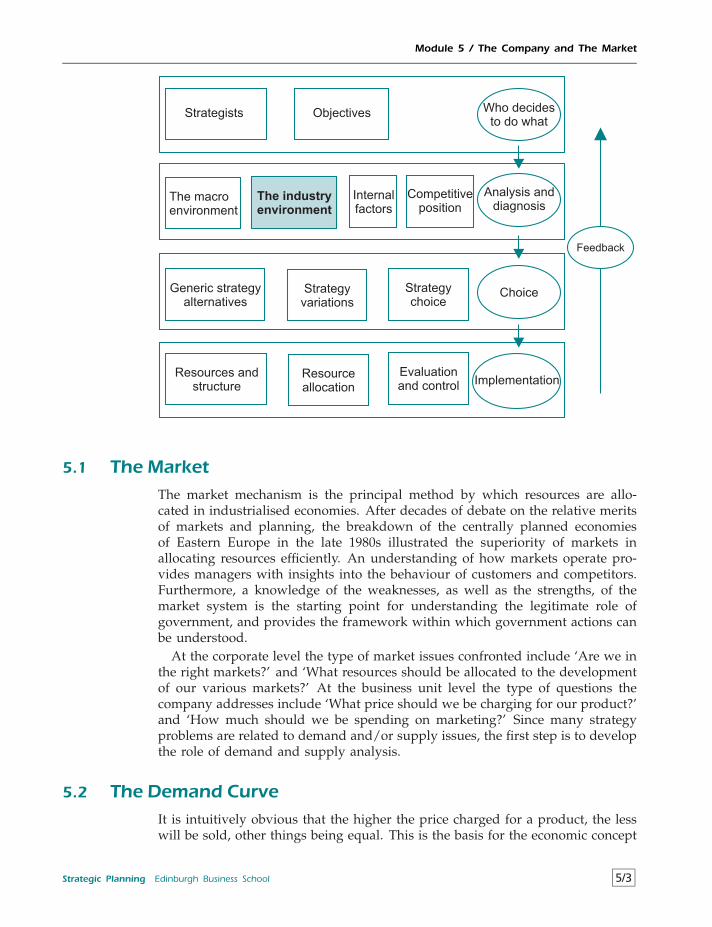

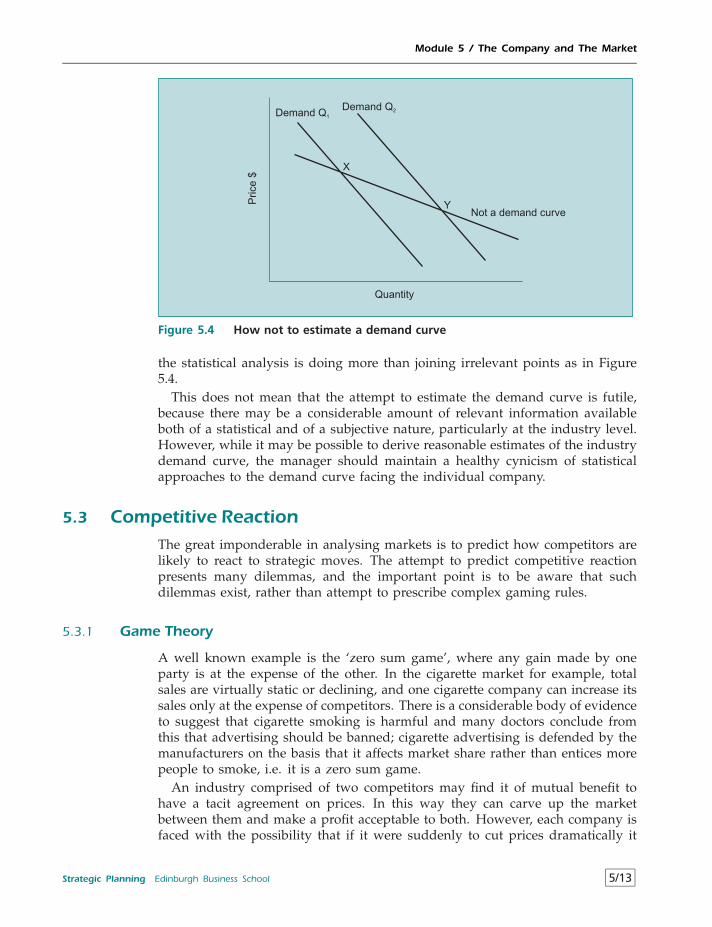

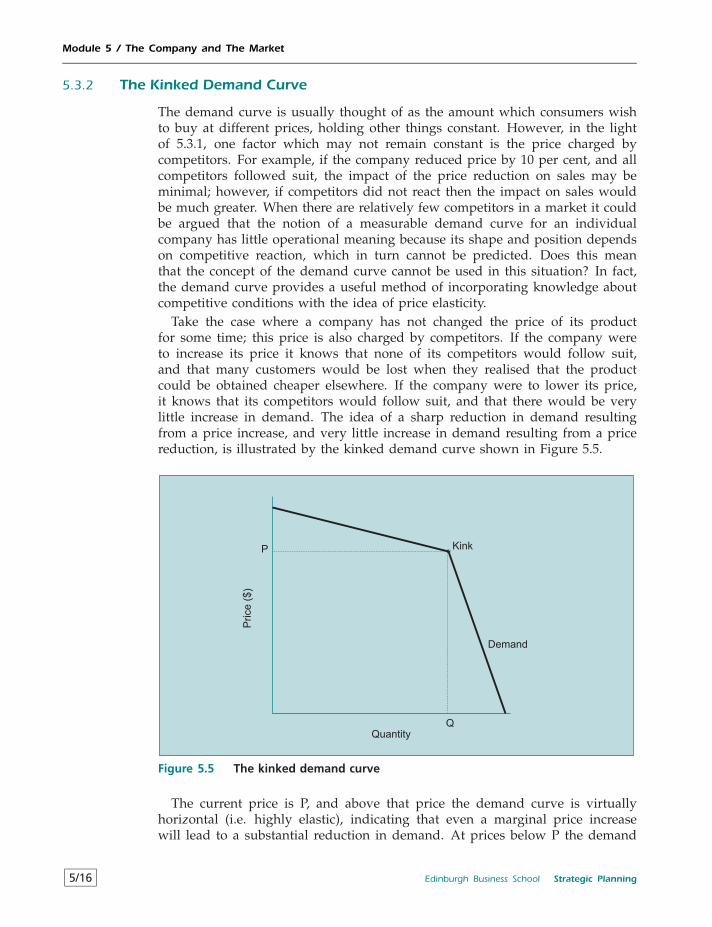

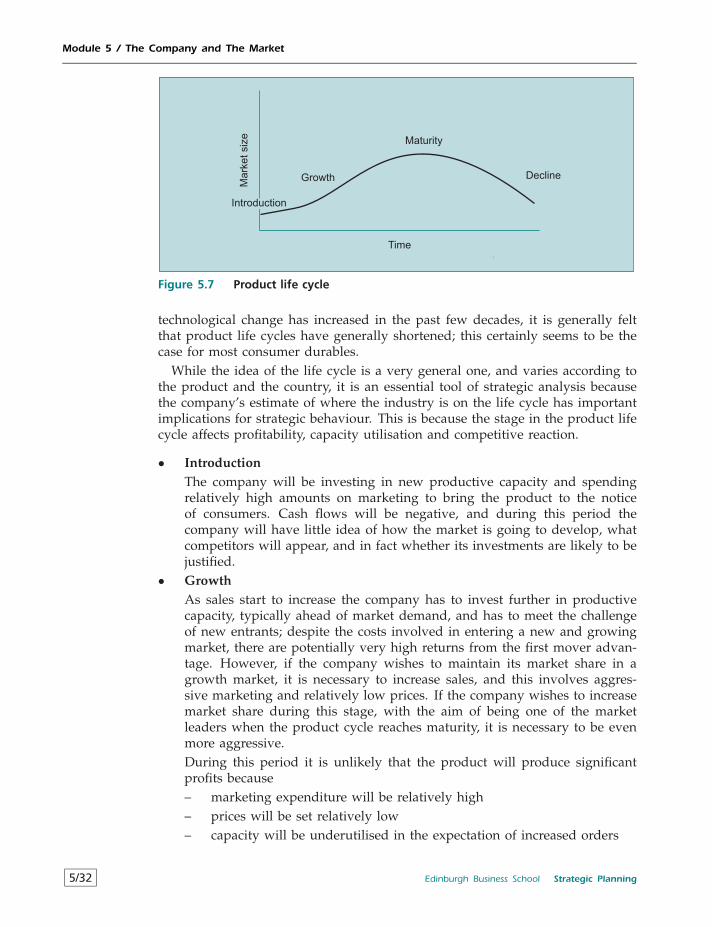

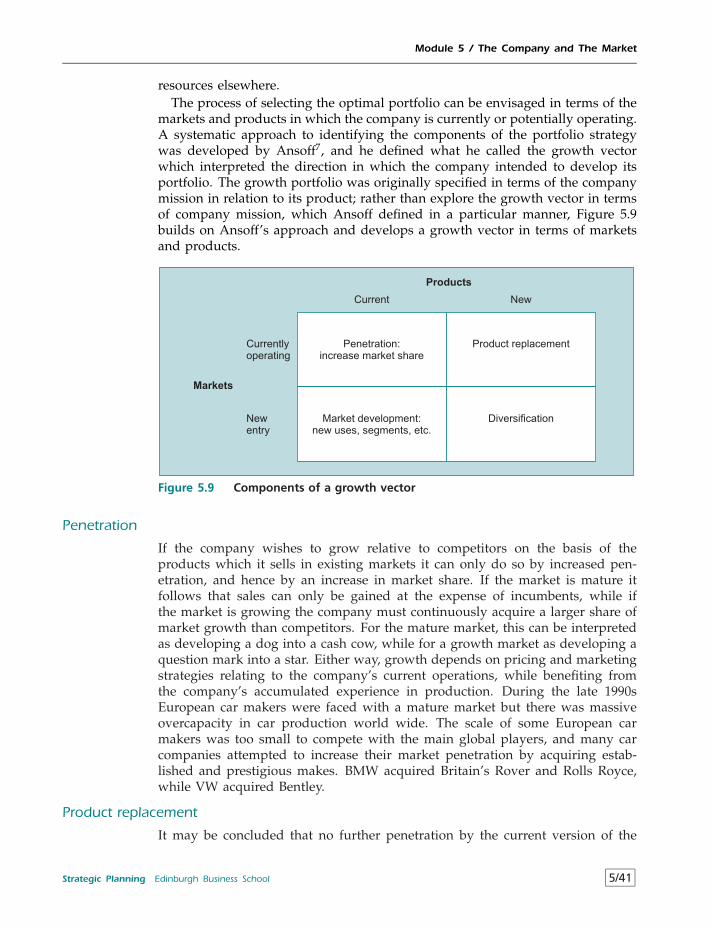

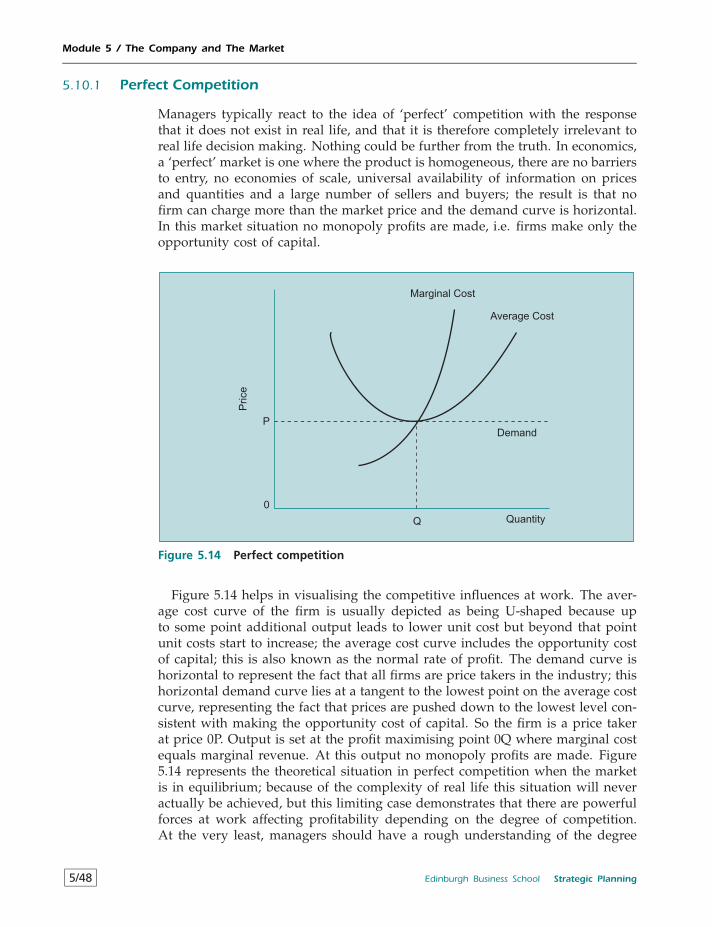

Module 5 The Company and The Market 5/15.1 The Market 5/35.2 The Demand Curve 5/3

Strategic Planning Edinburgh Business School 5

Contents

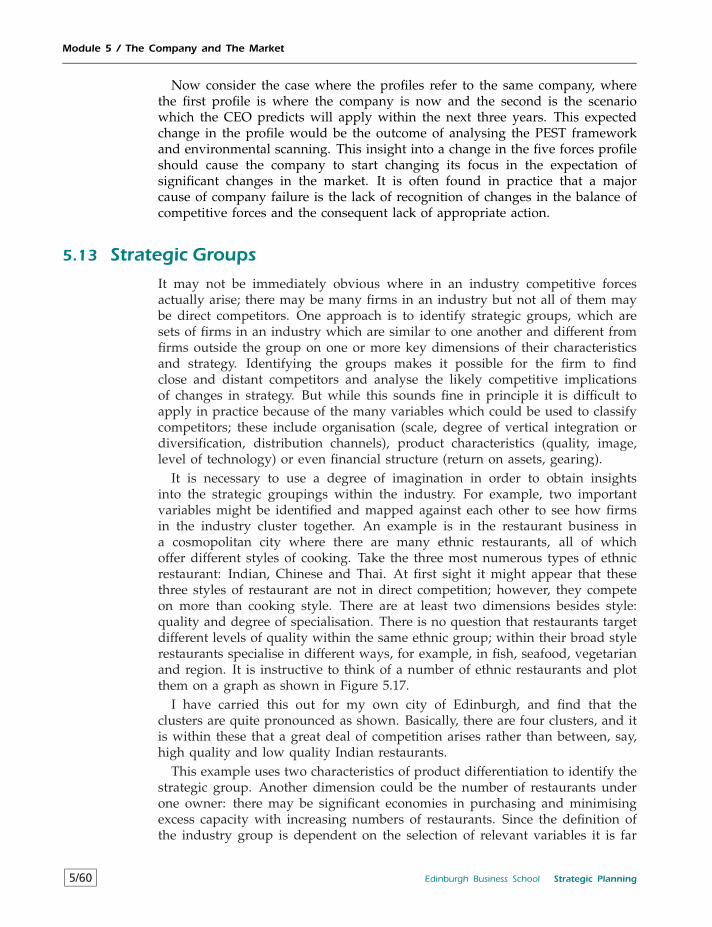

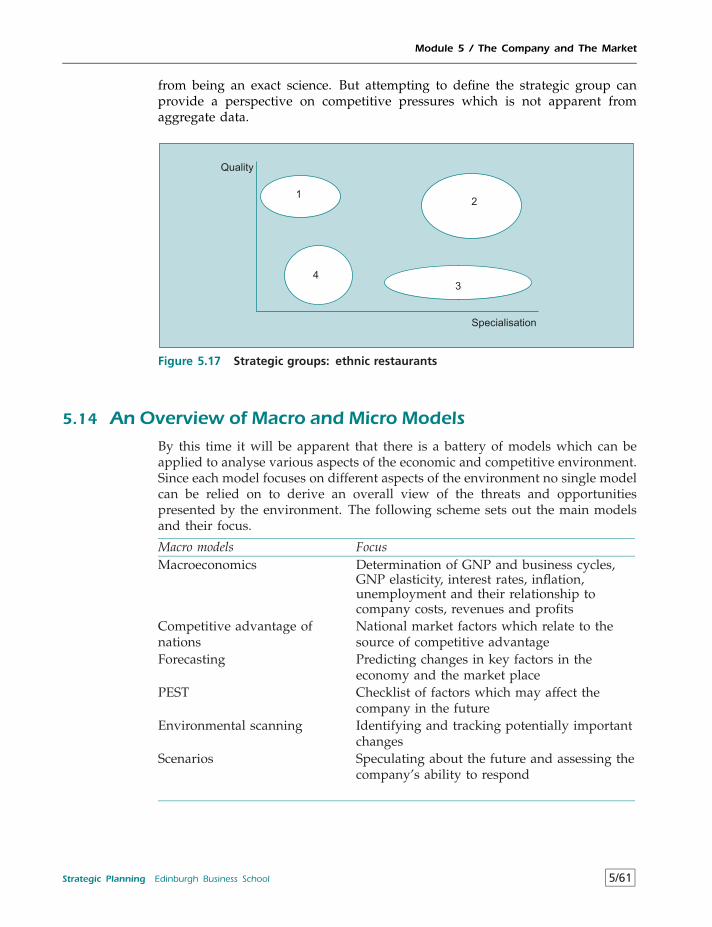

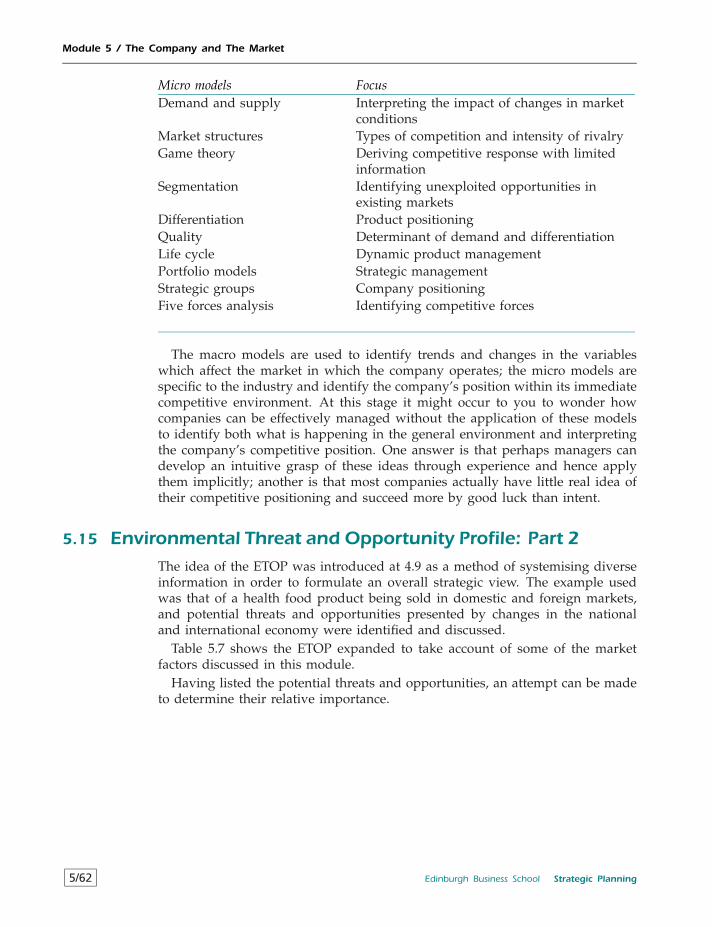

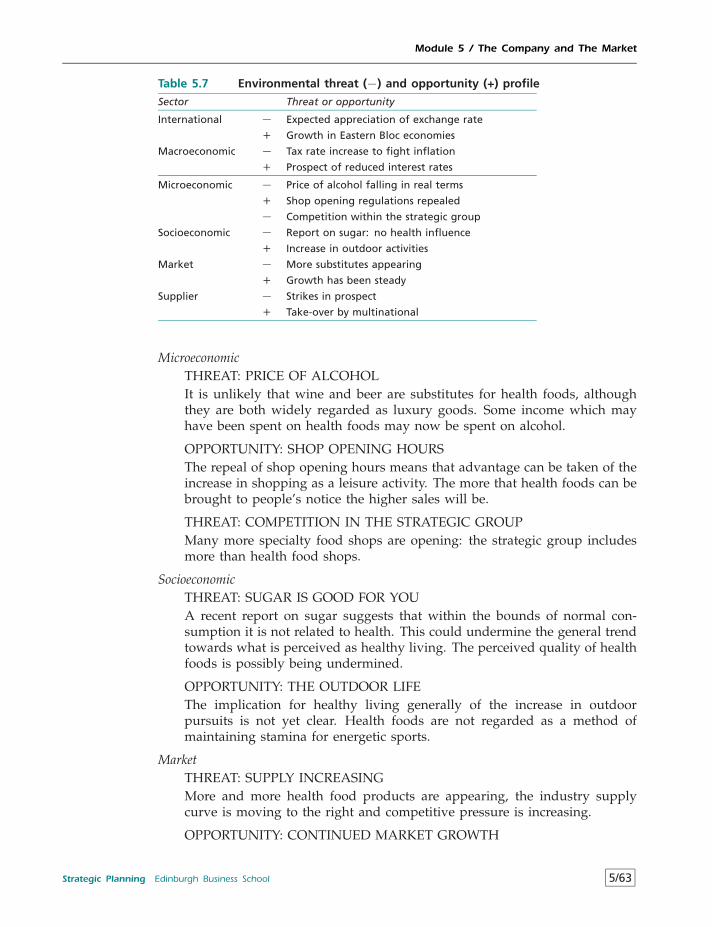

5.3 Competitive Reaction 5/135.4 Segmentation 5/185.5 Product Quality 5/245.6 Product Life Cycles 5/315.7 Portfolio Models 5/345.8 Supply 5/435.9 Markets and Prices 5/455.10 Market Structures 5/475.11 The Role of Government 5/545.12 The Structural Analysis of Industries 5/575.13 Strategic Groups 5/605.14 An Overview of Macro and Micro Models 5/615.15 Environmental Threat and Opportunity Profile: Part 2 5/62

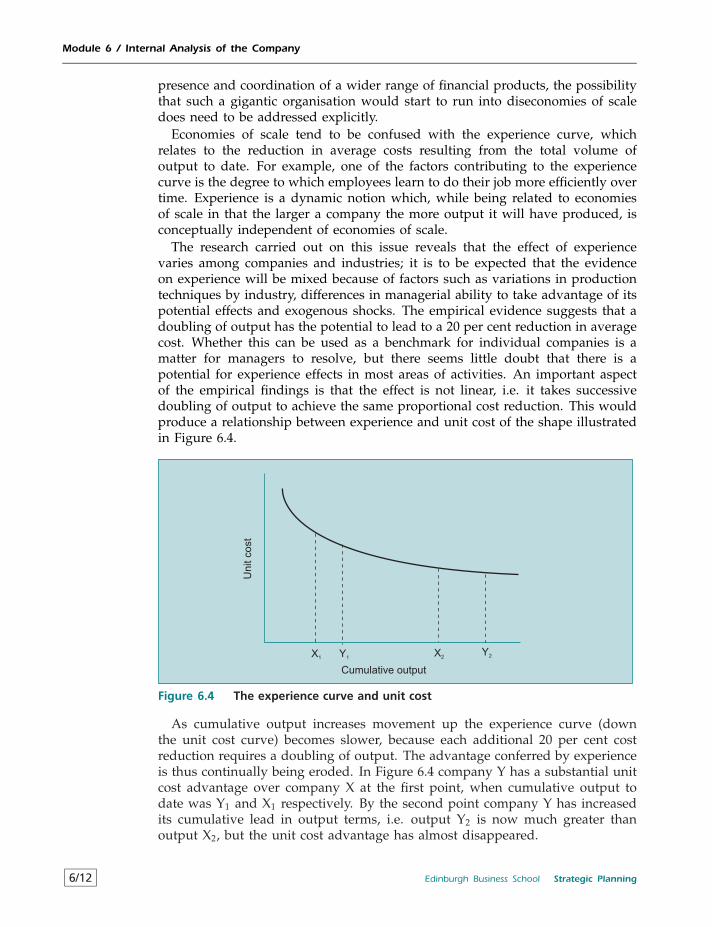

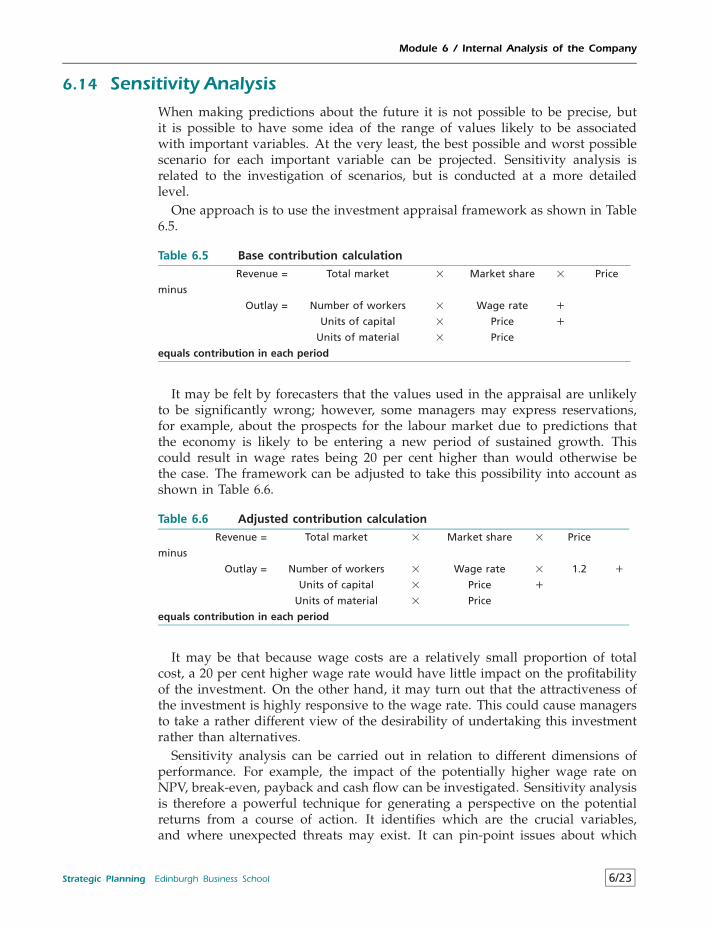

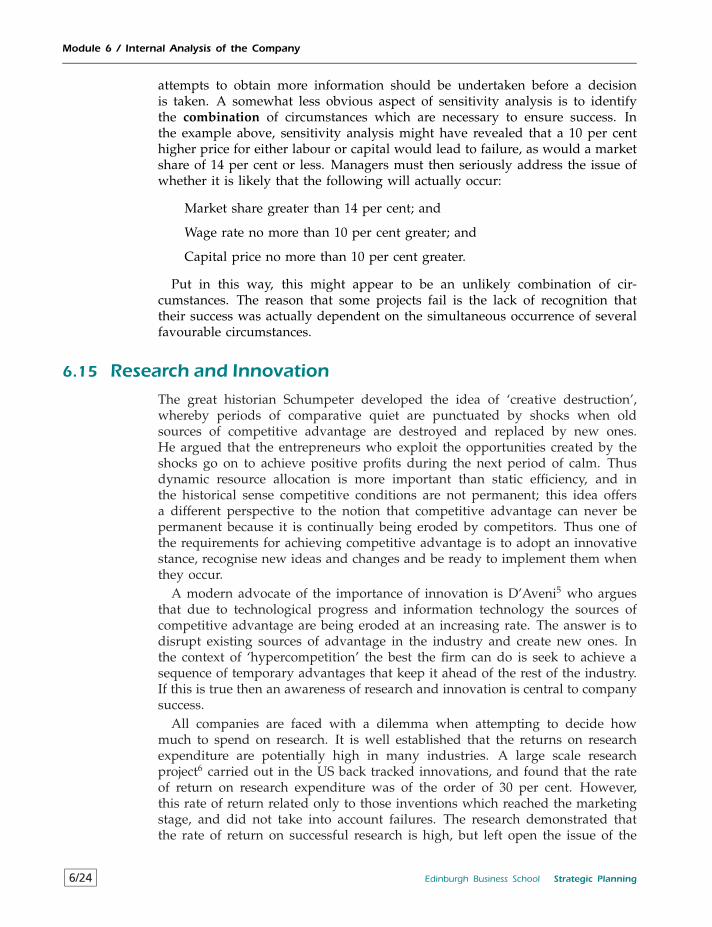

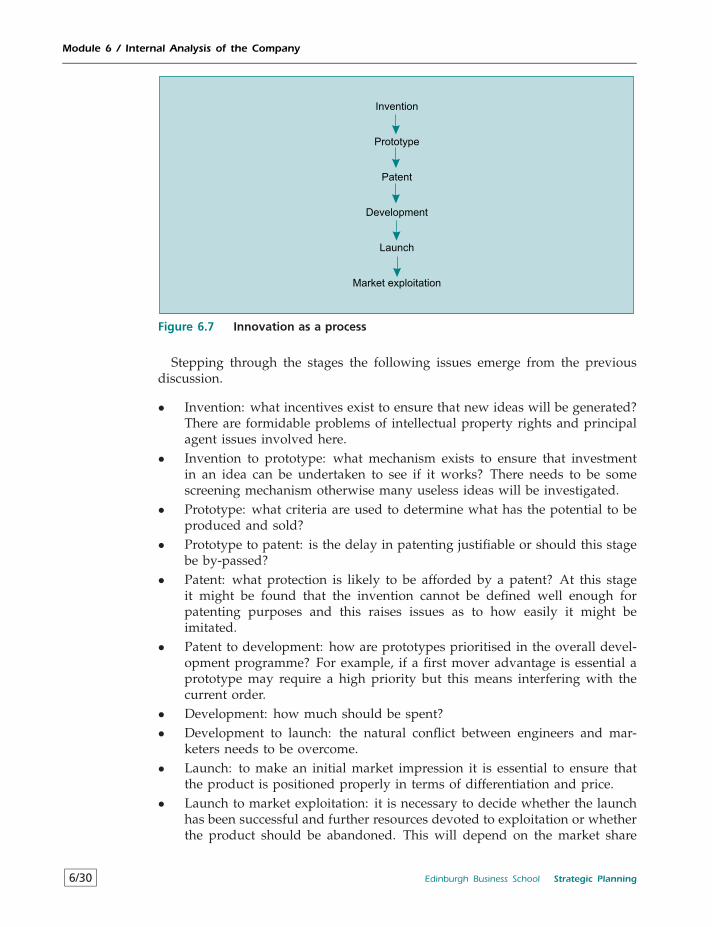

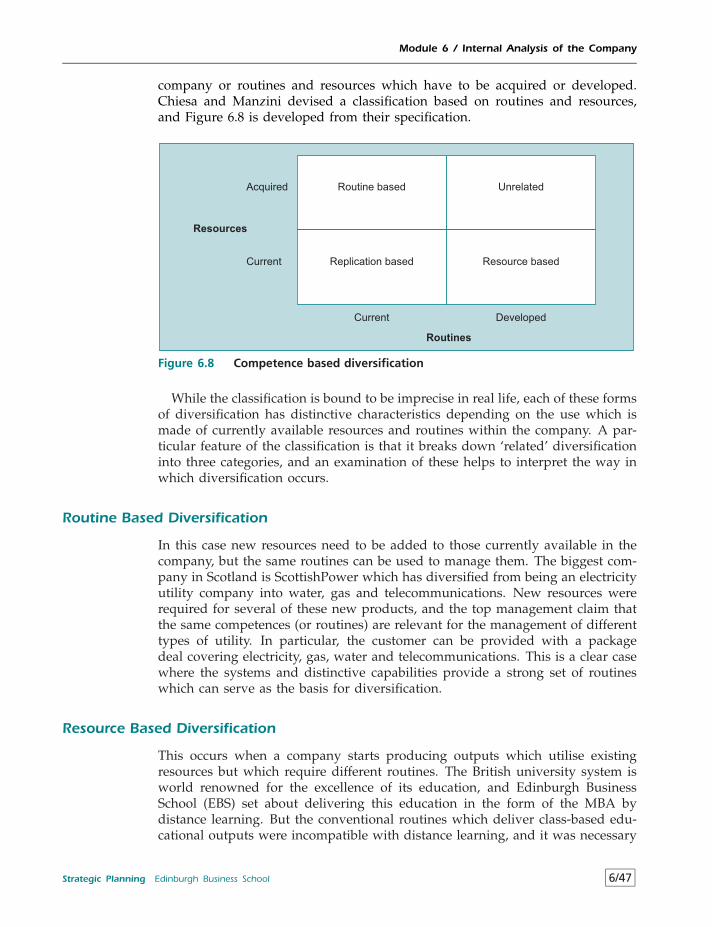

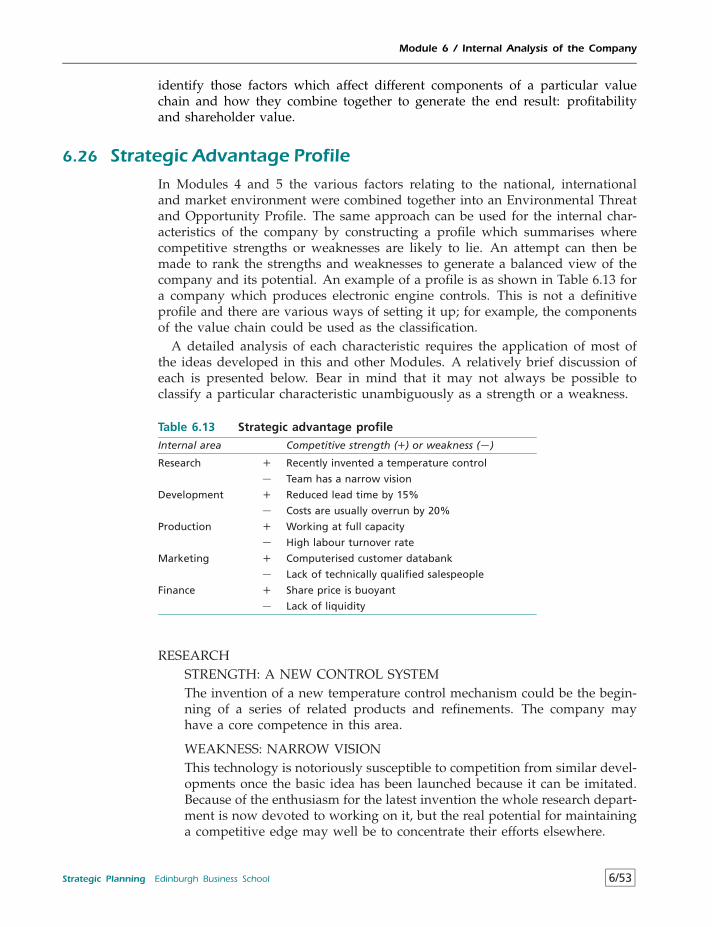

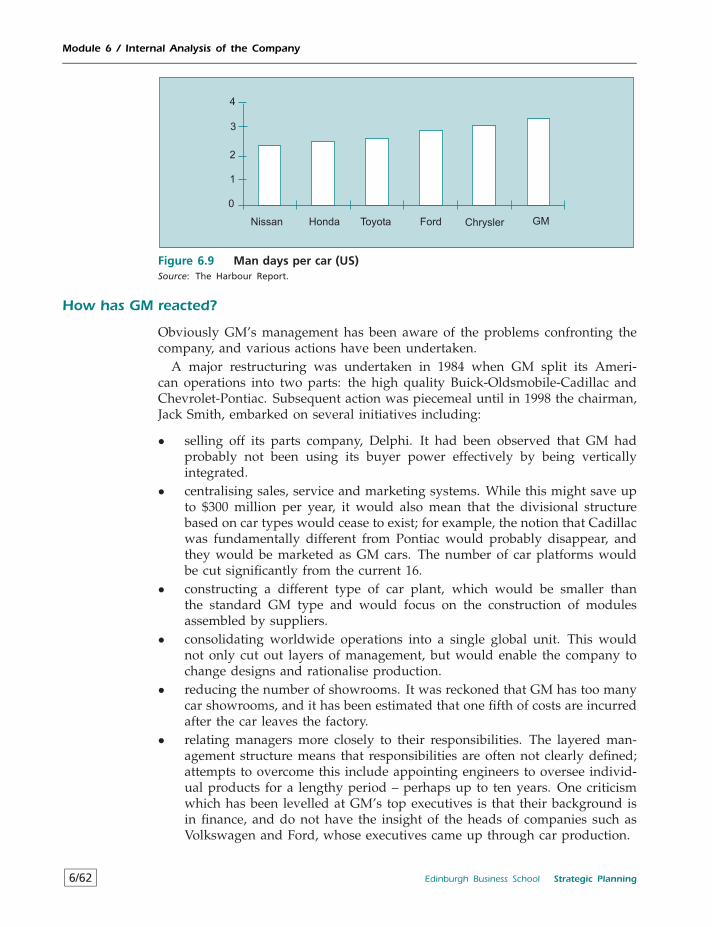

Module 6 Internal Analysis of the Company 6/16.1 Opportunity Cost 6/26.2 Fixed Costs, Variable Costs and Sunk Costs 6/46.3 Marginal Analysis 6/56.4 Diminishing Marginal Product 6/86.5 Profit Maximisation 6/106.6 Economies of Scale and the Experience Curve 6/116.7 Economies of Scope 6/136.8 Production Costs 6/146.9 Joint Production 6/156.10 Break-Even Analysis 6/166.11 Payback Period 6/176.12 Accounting Ratios 6/186.13 Benchmarking 6/216.14 Sensitivity Analysis 6/236.15 Research and Innovation 6/246.16 Development 6/266.17 Resource Management 6/316.18 Human Resource Management 6/336.19 Vertical Integration 6/356.20 The Value Chain 6/386.21 Diversification 6/406.22 Synergy 6/416.23 Competence 6/446.24 Strategic Architecture 6/496.25 The Definition of Competitive Advantage 6/506.26 Strategic Advantage Profile 6/53

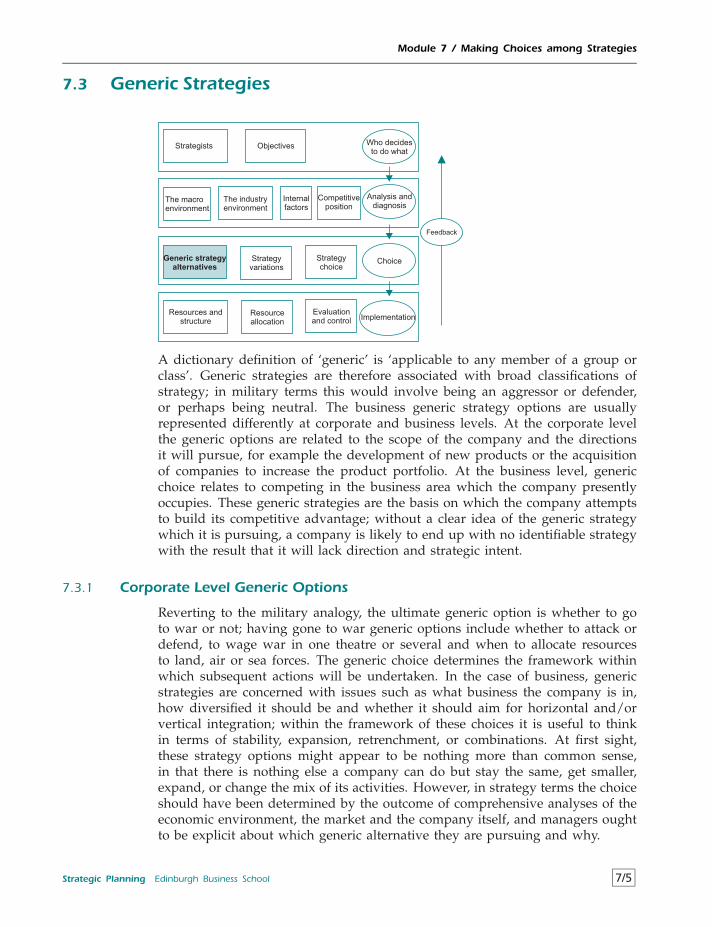

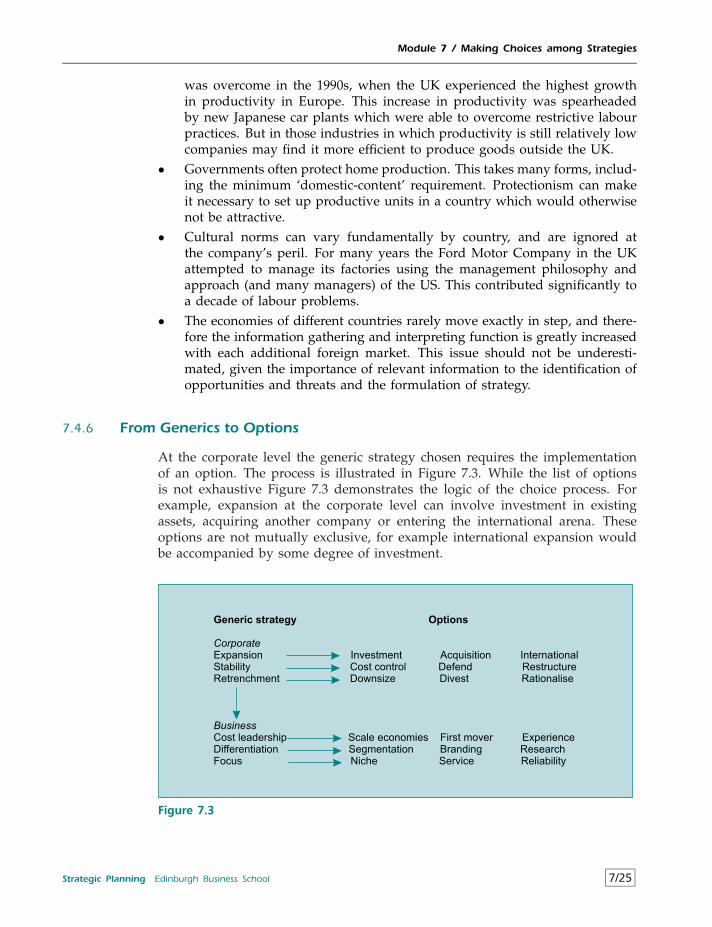

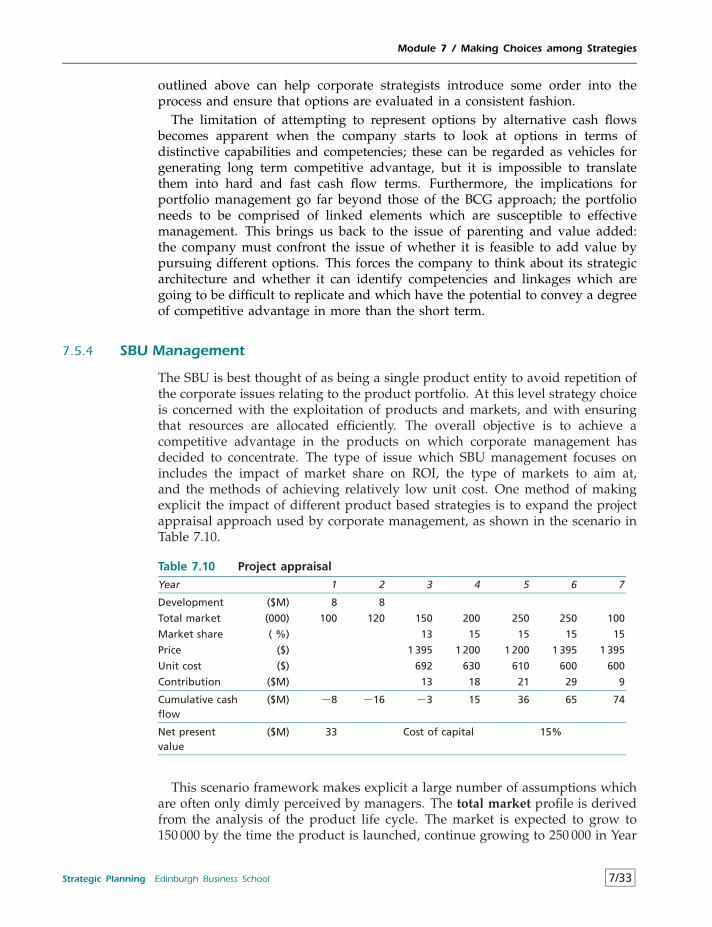

Module 7 Making Choices among Strategies 7/17.1 A Structure for Rational Choice 7/27.2 Strengths, Weaknesses, Opportunities and Threats 7/37.3 Generic Strategies 7/57.4 Identifying Strategic Variations 7/177.5 Strategy Choice 7/26

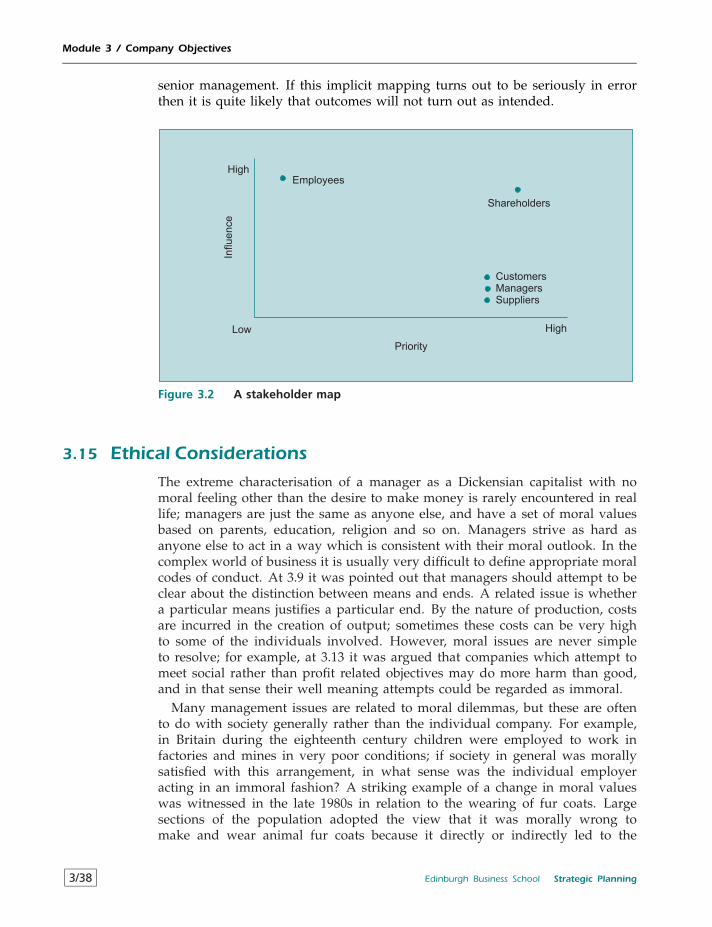

6 Edinburgh Business School Strategic Planning

Contents

Module 8 Implementing and Evaluating Strategy 8/18.1 Implementing Plans 8/28.2 Organisational Structure 8/38.3 Resource Allocation 8/68.4 Evaluation and Control 8/128.5 Feedback 8/188.6 The Augmented Process Model 8/198.7 Postscript: Strategic Planning Works 8/23

Appendix 1 Strategy Report A1/1

Appendix 2 Answers to Review Questions and Case Analyses A2/1

Appendix 3 Practice Final Examinations A3/1

Appendix 4 Guide to Strategic Planning Practice Final Examinations A4/1

Index I/1

Strategic Planning Edinburgh Business School 7

Using the Course Package

It is widely accepted that strategic planning is extremely difficult to teacheffectively. This is because, at the MBA level, it is not sufficient to know aboutthe subject – it is necessary to be able to apply ideas in order to carry outstrategic analysis of real problems. While there are many strategy models onwhich analyses can be based, the strategic approach also requires the applicationof a great many ideas and models drawn from the core business disciplines; thisis what gives substance to strategic analysis and this integrative element iswhy strategic planning is typically regarded as the capstone course in MBAprogrammes.

A further problem is that strategy solutions are to a large extent a matter ofpersonal judgement. A strategic planning analysis is judged on the structureand approach of the analysis and the justification for the policy proposals rec-ommended rather than the proposals themselves. While it may be possible torecognise that recommendations are unlikely to be successful because of mis-understandings about the basic business tools which are applied, it is usuallydifficult to judge how good or bad the results of a particular set of recommenda-tions are likely to be because no one really knows what is going to happen in thefuture. In real life strategy is undertaken in a constantly changing environmentwhich is full of uncertainty, and it is difficult to replicate these conditions in theclassroom. But it is obvious when students are using analytical ideas rather thanadopting a subjective and unstructured approach.

The approach adopted in this course is based on cases. There are some reviewexercises which are intended to reinforce your comprehension of specific topics,but the overall objective of the course is to enable you to apply strategic analysisto real life issues.

CasesThe case method is the most widely used technique for teaching strategicplanning, and was pioneered at Harvard Business School. The case is a powerfulteaching tool in class because it enables students to tackle real life examples,which have been abstracted and structured by teachers, and to present, discussand defend their analysis. The case method as used in class teaching cannotbe implemented for distance learning because it is based on interaction amongstudents and between students and teacher. In this course each case has beenanalysed fully by the professor, and many of the cases have been used in asimilar form in examinations and the analysis has benefited from the wisdomof large numbers of students. Each case has been analysed using a varietyof business models, and as you work through the course you will learn byanalysing the cases and comparing your solutions with those of the professor.It may often be the case that you consider your analysis to be superior to theprofessor’s; this is all to the good, particularly if you can justify your position.

The case method is a static approach, in that the you analyse a given situation,but cannot then experience how a plan might work out in practice, and how

Strategic Planning Edinburgh Business School 9

Using the Course Package

it might need to be adjusted as time proceeds. Strategic planning is a dynamicprocess in real life, and no case can capture this fully. A drawback of the casemethod is therefore that you will not have to live with the consequences of yourstrategy recommendations.

Feedback on student performance presents difficulties when using cases in thedistance learning mode. The professor’s analysis provides a benchmark againstwhich you can evaluate your own answer, but it cannot be regarded as a ‘perfectanswer’ to the case. This is because there can be legitimate disagreement onthe weights to ascribe to different aspects of the issue, such as the relativeimportance of different types of risk. Therefore the professor’s analysis can beregarded as an analytical framework within which you can judge the quality ofyour own thinking.

One of the difficulties in using real life cases is that they typically touch onmany issues. Several of the cases in the course attempt to focus on particulartopic areas, but the cases in the earlier Modules will be difficult to analyse fullybecause you do not have many of the analytical tools available with which totackle them. However, it is a salutory lesson to attempt cases without havingthe benefit of a full framework because there are still many lessons to be learnedfrom applying what you do know.

Because strategic planning is about applying ideas to the real world it isimportant that you tackle the exercises, in the form of cases and review questions,and assess your analysis in relation to the model answers provided. You willfind that many issues are elaborated on and reinforced in the model answersand these are an essential complement to the ideas developed in the text. Infact, the text and the exercises must be regarded as a single learning tool.

The cases, by their nature, are a snapshot at a particular time and, whilethey contain important lessons, time does march on and it is quite possible thatactual events will turn out differently to what might have been expected in thecases. Accordingly, each case is dated with the time the ‘snapshot’ was taken.An important feature of these cases is that they are not based on privilegedinformation nor in depth analysis of the organisations concerned; they havebeen constructed from the information available to everyone which is freelyavailable in the public domain, i.e. newspaper reports, magazine articles,television programmes and company reports. You will find that the cases aremuch shorter than those typically used in business school courses, and thoseof you who are familiar with Harvard Business School cases, for example, mayat first feel that they are ‘too short’. However, it is not the sheer amount ofinformation in a case which is important rather than what you can make of theinformation which is available. In fact you will find it instructive to keep trackof developments relating to the examples in the text and the cases; naturally youwill expect to keep track of developments in periodicals such as the Economistand newspapers such as the Financial Times, but you will also come uponrelevant information in the most surprising places – magazines, gossip columns,or whatever. Keep your eyes open.

10 Edinburgh Business School Strategic Planning

Using the Course Package

Your Learning StyleIt is entirely up to you how you decide to learn about strategy. Two totallydifferent learning models reported by students appear to have been equallysuccessful for them. One student worked through each Module and spenta lot of time on each case or review question both analysing the problemand comparing the outcome with the analysis provided in Appendix 2 beforeproceeding. Her intention was to build up comprehension in an incrementalfashion. Another student started by reading Modules 1 to 8 without attemptingthe cases or review exercises with the intention of gaining a general perspective;he then went back to the beginning and worked through the cases and exercises.Each felt that this approach was right for them. Whichever approach you adoptbear in mind that strategic planning is not an individual discipline which isunrelated to the core courses; when ideas from the core courses are used youmay often find it worthwhile to revisit the relevant text to refresh your mind onideas which are discussed and applied in the strategic context.

But there is one important piece of advice which you should keep in mindwhatever your learning style: do not get obsessed with detail. For example,some of the cases contain numerical information relating to company accountsand market position; you might make a computational mistake when using thesenumbers but that is not important. What is important is that the conclusions youarrive at are consistent with whatever numerical answers you have produced.Strategic planning is about the big picture and the quality of your thinking; ifyou lose sight of that you will find yourself in the classic position of not beingable to see the wood for the trees.

Strategic Planning Edinburgh Business School 11

Module 1

Introduction to Strategy, Planningand Structure

Contents

1.1 Strategic Planning: The Context 1/2

1.2 What Is Strategic Planning? 1/41.2.1 Managers’ Definitions of Strategy 1/51.2.2 Strategy in the Business Context 1/61.2.3 Three Approaches to Strategic Planning 1/81.2.4 Rittell’s Tame And Wicked Problems 1/131.2.5 The Origins of Strategy and Tactics 1/151.2.6 Strategy and the Scientific Approach 1/171.2.7 Strategic Planning and Strategic Thinking 1/21

1.3 The Process of Strategy and Decision Making 1/231.3.1 Strategy Dynamics 1/231.3.2 The Mythical Company 1/251.3.3 How Well Are We Performing? 1/251.3.4 What Should We Be Doing in the Future? 1/281.3.5 How Can We Achieve Successful Change? 1/311.3.6 Strategy and Crises 1/311.3.7 Elements of Strategic Planning 1/33

1.4 Business Unit and Corporate Strategy 1/401.4.1 Allocating Corporate Resources 1/411.4.2 Development of Corporate Strategies 1/42

1.5 Is Strategic Planning Only for Top Management? 1/471.5.1 Company Benefits of Strategic Planning 1/471.5.2 Individual Benefits of Understanding Strategic Planning 1/481.5.3 Understanding Strategic Planning: Who Should Pay? 1/48

Review Question 1 1/49

Review Question 2 1/49

Review Question 3 1/49

Review Question 4 1/49

Review Question 5 1/49

Strategic Planning Edinburgh Business School 1/1

Module 1 / Introduction to Strategy, Planning and Structure

Learning Objectives

• The meaning of strategic planning as it is used in business.• To visualise strategy as a structure of thought which can be applied to the

complex strategy process.• The different strategy concerns at the corporate and business levels.• How the major approaches to corporate strategy have developed.

1.1 Strategic Planning: The Context

It has been mentioned that strategic planning is usually the capstone course inMBA courses; it is therefore useful to look at what the core courses are concernedwith and how strategic planning fits with them. Because the core courses aretaught individually it is easy to get the impression that they are independent ofeach other, but this is far from the case. The following story tries to capture therationale for studying the core courses.

• Organisational behaviour: this subject should come at the top of the listof requirements for any management course because if you cannot handlepeople then you are not a manager. It is as simple as that. The fact isthat organisations are run by people, and if you have no understanding ofwhat motivates people and how they interact in the organisational settingthen you are unlikely to get an efficient response from the people you aremanaging. One of the most successful companies in history, IBM, appearedto lose its way in the early 1990s and reported the biggest loss in corporatehistory in 1993: it was unable to convert its inventions, such as the newRISC chips, into marketable products as fast as competitors, and it wasunable to respond quickly to changing circumstances; this was largelyattributable to the huge bureaucratic structure which had evolved and IBMwas forced to take steps to reorganise itself so that it could once againreact in a competitive manner. The people problem lay at the root of IBM’sdifficulties and this had to be sorted before real progress could be made.

• Economics: everything that happens in business is related to economic influ-ences and these operate at three levels. At the highest level it is importantto have some understanding of how the economy operates. Every businessis affected by the business cycle, the rate of interest, the exchange rate andgovernment economic policies; a manager’s view on what is happening inthe economy can greatly affect decisions on what to do next; for example,should a major investment be taken now, when all the signs are that theeconomy is heading for recession, or should it be delayed until there isan improvement? The next level concerns how markets operate and howprices are determined. What type of competitive forces prevail in yourindustry? How does market structure affect profitability? What is signalledby a change in prices? An understanding of basic economic ideas enablesyou to discuss and interpret such questions; without that understandingyou have no idea what is going on. The third level concerns ideas aboutefficiency, primarily based on marginal analysis. Rational decision making

1/2 Edinburgh Business School Strategic Planning

Module 1 / Introduction to Strategy, Planning and Structure

is based on an understanding of relevant costs and benefits, and seriousmistakes are often made because efficiency ideas are not understood.

• Marketing: there is little point to being able to manage people, interpretsurveys and make rational economic decisions if you cannot sell effectivelyin markets. Marketing is often mistakenly thought of as advertising, butadvertising is simply one of many marketing tools. Marketing is the complexprocess of relating product characteristics to market demand and attemptingto win competitive advantage in a dynamic competitive setting. Why is itthat some brands of whisky are much more successful than others, despitethe fact that the majority of people cannot tell one brand from another?Without an understanding of marketing principles and ideas it is impossibleto answer such a difficult question.

• Finance: you may be running your company well and selling effectively,but managers always have to bear in mind that perhaps they should havebeen doing something different which is more profitable. How is the choiceamong competing courses of action made in a world of uncertainty? Financetakes all available information on projected future cash flows and subjectsthem to rigorous evaluation; a company might have the choice of revampingan existing product or launching a new product which is a close substitute,and the projected cash flows both in and out are totally different while therisks associated with each are also different. The tools of financial theoryprovide you with a quantitative solution to such problems, and this takesyou a long way towards deciding on the most appropriate course of action.

• Accounting: you may have decided on the best course of action using finan-cial techniques, but it is then necessary to ensure that over time resourcesare allocated efficiently; in a company which produces more than oneproduct it is difficult to isolate relevant costs, but knowing the costs of whatyou produce is central to running a business. While finance is concernedwith deciding what should be done, accounting concentrates on how effi-ciently resources are subsequently allocated. In many ways a knowledgeof accounting helps in the same way as an understanding of quantitativemethods: you should be able to ask the correct questions and be able tointerpret the answers. Otherwise you are at the mercy of accountants, andobviously no one wants to be in that position.

• Project management: while it may appear to be a good idea to embarkon a new course of action, such as launching a new product, unless youunderstand how to implement projects effectively there is a good chancethat the launch will fail. The success of the launch will depend on meetingcriteria centred on time, cost and quality because the product will have tobe on the market by a certain date, the development and production costswill have to be maintained within budget and the quality has to be asgood as competitors’. In addition, the launch of any new product generatesrisk. Project management tools and techniques allow the risk profile to bemapped, assessed and monitored over time and any changes in risk impact,such as those due to the actions of competitors, can be tracked. As the launchprogresses tools such as earned value analysis and trade-off analysis enablethe project manager to consider different combinations of time, cost and

Strategic Planning Edinburgh Business School 1/3

Module 1 / Introduction to Strategy, Planning and Structure

performance both at present and at the projected end condition. Clearly,the lack of the project management approach can result in a haphazardproduct launch. Project management tools and techniques enable the projectmanager to plan and implement change effectively, hence increasing thelikelihood of success. A major problem confronting organisations is thatthey do not realise that their approach to managing change is haphazardbecause they are not aware that most change activities are in fact projectsin their own right and should be managed as such.

• Strategic planning: the areas covered by the six core disciplines can bedefined reasonably easily, and it is clear that they all have an important roleto play in running a company. Strategic planning is less easy to define, andthe content and role of strategic planning is what the rest of this course isabout. But one thing is certain: strategic planning is not independent of theother core disciplines.

1.2 What Is Strategic Planning?

Strategic planning is a complex activity and before attempting a definition itis useful to compare its degree of complexity with another complex activity:economic policy making, which has a general similarity with strategic planningin that strategic planning is concerned with running a company and economicpolicy is concerned with running the economy of a country. The study ofmacroeconomics reveals the complexity of fiscal and monetary policy and themany ideas and theories which are involved; furthermore, there are no com-pletely right or wrong economic policy decisions because information has to beinterpreted and conflicting theories reconciled. Although the scale of a companyis very much less than that of an industrialised country such as the UK orJapan the job of business policy making is probably just as complex. That is onereason why effective CEOs are as rare as effective Presidents, Prime Ministersand Central Bank Governors; in fact, effective CEOs are typically paid muchmore than government ministers. The complexity of economic policy becomesapparent when a list of the issues involved is compiled:

• growth of GNP• unemployment• inflation• the budget balance• the role of markets• the trade balance• the rate of interest• the exchange rate• income redistribution• pollution• government expenditure• business investment

1/4 Edinburgh Business School Strategic Planning

Module 1 / Introduction to Strategy, Planning and Structure

This list is by no means complete; in fact, the list could be extended to fill thispage. When we turn to strategic planning it is not difficult to generate a list ofequal length:

• profitability• growth in sales• market share• relative costs• competitive position• pricing• environmental scanning• human resource management• accounting ratios• investment appraisal• shareholder value• dividend policy

The theories of microeconomics and macroeconomics are used to make senseof the relationships among the many variables involved in the economy andto provide an understanding of how economies operate; this provides the basisfor interpreting government economic policy making. The approach in strategicplanning is to bring together business concepts and ideas in order to understandhow companies (and other organisations) operate in a competitive environment,develop an understanding of the inter-relationships involved, and hence providethe basis for arriving at explanations of why companies have succeeded or failedin the past and how they might operate successfully in the future.

There is an added dimension to the scope and complexity of strategic plan-ning which does not occur in economic policy making. Looking at the list ofstrategic planning issues there is an item called ‘environmental scanning’. Thisactivity is concerned with monitoring the environment within which the com-pany operates and assessing the extent to which current and potential changesin that environment are likely to impact on the company. But the macroeco-nomic environment is largely determined by the state of the economy, which inturn is greatly influenced by economic policy making. Thus to make sense ofthe macroeconomic environment it is necessary to have some understanding ofeconomic policy making and its implications. The need to understand economicpolicy making is not confined to government policy makers and it is subsumedinto strategic analysis.

1.2.1 Managers’ Definitions of Strategy

Over many years I have posed the question ‘What do you understand bystrategy?’ to experienced executives attending management programmes, andeach time the groups have responded with a wide range of answers includingthe following.

Strategic Planning Edinburgh Business School 1/5

Module 1 / Introduction to Strategy, Planning and Structure

1 Knowing where you are going and how you are going to get there.2 Setting a clear set of objectives and mobilising resources to achieve them.3 Thinking in the long rather than the short term.4 Working out how to do better in the market place than your competitors.5 Deriving and selecting a course of action.

There are some common threads running through these definitions, but indi-vidually they could lead to different courses of action. For example, definition2 focuses on objectives, but does not differentiate between short term and longterm as in definition 3; definition 4 is the only one explicitly concerned withmarkets. Definition 5 is the only one which explicitly considers choice.

It is not unusual to obtain ten different definitions from a single group. Thesemanagers are typically involved in formulating and implementing strategy so itmight appear strange that there is such apparent confusion in their minds aboutwhat is meant by the term.

1.2.2 Strategy in the Business Context

If you were to visit a large or medium sized company, chosen at random, andattempt to identify and track the formulation and implementation of a ‘strategicplan’, you may well find the task to be elusive and perplexing. In pursuing thestrategic planning process some questions which you might ask, in no particularorder, include: ‘Was the strategy ever written down?’ ‘ Where did it originate?’‘Why was it selected rather than alternatives?’ ‘Who was responsible for it?’‘Who knew if it was working or not?’ In some cases you would find it diffi-cult to elicit answers to these seemingly straightforward questions. Despite this,individual companies may consider that they have a well-developed strategicplanning process, although it is informal and subject to constant revision in thelight of circumstances. On the other hand, in some companies you would finda formal planning system complete with clearly specified objectives, responsi-bilities and control procedures. You would therefore encounter a wide diversityof activity which individual companies would consider to be strategic planning.Some additional questions might include: ‘Is there a payoff to the companyfrom the resources devoted to strategic planning?’ ‘Which is more appropriate,the informal approach or the structured formal plan?’ You would probably findthat managers offered a variety of views on both the effectiveness of planningin general and the most appropriate approach to planning.

One reason that questions relating to strategy are difficult to answer unam-biguously is that strategic planning takes place in a complex and ever-changingbusiness environment. One description of strategy is

A pattern in a stream of decisions; the pattern may not be comprehensive, unifiedor integrated1

This raises the question as to whether strategic planning is a conceptually validconcept in business; the study of strategic planning may merely be an attemptto impose a structure on events after they have occurred. The central question iswhether strategy is a rational process, in the sense that it was carefully thought

1/6 Edinburgh Business School Strategic Planning

Module 1 / Introduction to Strategy, Planning and Structure

out by senior management and then put into practice, or whether it is emergent,in the sense that it develops over a period as the result of many influences fromall levels in the organisation.

The following are some academic definitions of strategy, each with its ownparticular focus.

The decisions taken over time by top managers, which, when understood as awhole, reveal the goals they are seeking and the means used to reach these goals.Such a definition of strategy is different from common business use of the term inthat it does not refer to an explicit plan. In fact, by my definition strategy may beimplicit as well as explicit.2

the determination of the basic long term goals and objectives of an enterprise,and the adoption of courses of action and the allocation of resources necessary forcarrying out these goals.3

the pattern of objectives, purposes or goals, and the major policies and plans forachieving these goals, stated in such a way as to define what business the companyis in or should be in and the kind of company it is or should be.4

what determines the framework of a firm’s business activities and provides guide-lines for coordinating activities so that the firm can cope with and influence thechanging environment. Strategy articulates the firm’s preferred environment andthe type of organisation it is striving to become.5

Each of these quotes can be interpreted as saying different things. The firstdefinition seems to suggest that strategy can only be understood after the event,and is revealed by studying what management actually did. The second claimsthat strategy is a proactive process where long term goals are determined beforethe event and resources deployed accordingly. The third portrays strategy asa pattern of objectives which define what the company is and intends to bein a broad sense. The fourth presents strategy as a set of guidelines whichwill help it operate in a changing environment. The fact that there are suchdifferent perspectives on the issue suggests that some observers will see strategicbehaviour where others will not.

A different approach to strategy can be derived from economics: the forces ofcompetition ensure that, on average, successful companies are those which, bychance or otherwise, choose the most effective strategies. As a result it mightbe expected that such companies would tend to exhibit various characteris-tics of strategic planning contained in the definitions, such as identification ofobjectives, plans and guidelines for dealing with the unexpected, and effectiveallocation of resources. Since many companies have a record of success stretchingover decades, it is reasonable to conclude that there is scope for distilling lessonsfrom their experience and formalising these into a set of generally applicableprinciples.

However, any attempt to identify characteristics which lead to success orfailure is dependent on relating actions to outcomes, i.e. attributing cause andeffect. This is difficult in the field of business. There are numerous instancesof companies which have a record of success because they happened to bein the right market position at the right time to take advantage of favourable

Strategic Planning Edinburgh Business School 1/7

Module 1 / Introduction to Strategy, Planning and Structure

economic circumstances; investigation of such companies may reveal that theyhad little understanding of their markets and generally haphazard managementcontrols, and from this there would be little to learn about successful behaviour.However, the subsequent performance of such companies may have the potentialto generate lessons for strategic planning: do they capitalise on their goodfortune, consolidate their market position, ensure that resources are deployedefficiently and start looking forward with the objective of identifying and seizingsimilar opportunities in the future? If not, they may be caught out by the nextadverse event.

But the major problem in trying to relate cause and effect is that strategyis also concerned with the behaviour of competitors. Decisions are not onlytaken in the context of unpredictable outcomes such as market growth and thebusiness cycle, but have to take into account confrontation with other companies,each of which is trying to achieve a competitive advantage. If one company iscapable of carrying out an analysis of market conditions, it stands to reasonthat other companies can do so also, and may well have exactly the sameinformation at their disposal. Strategy decisions may then become something ofa guessing game, where managers attempt to predict what competitors will dorather than analyse options derived from financial and economic appraisal. Asa result an elaborate and sophisticated strategy based upon the latest thinkingin the business disciplines may be associated with failure because a majorcompetitor did something totally unexpected. Another way of looking at thisis that strategy is about the unknowable as well as the unpredictable. This meansthat it is necessary to go beyond the application of concepts from the individualbusiness disciplines on their own to derive effective courses of action.

Everyone should be aware that there are no simple answers to strategy issues;you only have to read the continual newspaper reports on the varying fortunesof prominent business personalities and famous companies. In internationalpublishing and communications the careers of Rupert Murdoch and the lateRobert Maxwell provide a strong contrast. The huge Bond empire based inAustralia fell apart in 1991. Richard Branson capitalised on the success of musicpublishing and is now an important player in the airline business and is movinginto the financial sector. Lord Hanson was one of the most successful take-overspecialists in the world and by 1996 had started to dismember his corporateempire. The list of successes and failures is endless, and it is a useful exerciseto write down a list of companies from your own experience, and label themsuccess or failure at the moment; then put yourself back five years and see ifyou could have predicted what has happened to them. It is obviously importantto determine whether general principles exist whose application would haveprevented the failures, and whether such principles are the underlying reasonfor the successes.

1.2.3 Three Approaches to Strategic Planning

Since strategy is such a troublesome concept to define it is to be expected thatthere are several ways of approaching the idea. Strategy can be regarded as apurely planning exercise, or a course of action which emerges over time, or asthe outcome of the resources which are available to the company.

1/8 Edinburgh Business School Strategic Planning

Module 1 / Introduction to Strategy, Planning and Structure

The Planning Approach

This approach is based on the notion that once a set of objectives have beendetermined, the business environment analysed and forecasts made, a plancan be worked out by senior management which is then passed down forimplementation; this plan is then adhered to over the planning time scale. Thisis usually thought of as the strategic planning approach, and it has been claimedby its supporters that this prescriptive form of strategy is rational and objective;but as Mintzberg6 and many others have pointed out, it makes a number ofassumptions about the world which are highly questionable.

• The future can be predicted accurately enough to make rational choices. It is infact a widespread fallacy that the future can be predicted with any realisticdegree of accuracy. At the macro level economists disagree quite markedlyon the economic prospects for any given country during the course ofthe next year; such forecasts can never take into account unforeseeableevents such as the Asian economic crisis in 1997 or the collapse of theRussian financial system in 1998. At the micro level market innovationsand the actions of competitors can have fundamental effects which are alsoimpossible to predict, such as the introduction of direct telephone insuranceselling in the UK in the early 1990s. One reason that many market changesare impossible to predict is that that they are dependent on the uniquevision of individuals; if such unique vision did not exist there would bevirtually no scope for competitive action in the first place.

• It is possible to detach strategy formulation from everyday management. In arrivingat a strategy it is necessary to have a full set of data which can be subjectedto analysis and from which conclusions can be drawn. But this assumes thatthere is some technique whereby the relevant information is extracted fromthe organisation, and from individual managers, and presented to strategymakers in a tidy bundle. This dodges the question of who is to decideon which information is relevant, and indeed whether the information isreadily available. Furthermore, as events unfold information is continuallyevolving and can go out of date very quickly. As a consequence everydaymanagement is closely tied in with strategy formulation because it is ineveryday events that information is generated.

• It is possible to forego short-term benefit in order to gain long-term advantage. Ina situation of uncertainty, and lack of knowledge about the future becauseof the difficulties of forecasting mentioned above, it may often appearpreferable to reap short-term benefits which can be achieved with a highdegree of certainty rather than waiting for highly uncertain returns. It canalso be extremely difficult to convince those who lose in the short termthat the trade-off is worthwhile. Many companies may find it virtuallyimpossible to undertake action which relates to the long term when thereare viable short term alternatives.

• The strategies proposed are capable of being managed in the way proposed. Anystrategic initiative which involves change is dependent on company person-nel adapting and working in alignment with company objectives. Changemanagement is one of the most problematical areas of strategy implemen-tation, and it can not be taken for granted. Time and again it is found in

Strategic Planning Edinburgh Business School 1/9

Module 1 / Introduction to Strategy, Planning and Structure

practice that prescriptive actions simply do not take the human dimensionadequately into account.

• The Chief Executive has the knowledge and power to choose among options. Hedoes not need to persuade anyone, nor compromise his decisions. This takesa naive view of leadership and how it is exercised. In reality, very fewbusiness leaders can behave like dictators, and certainly not for very long.It is necessary to achieve consensus and agreement at all levels of theorganisation, otherwise a prescriptive plan simply cannot be made to work.The fact of selecting one option implies that some individuals will bemade better off and some worse off (or perceive that this is the case) thanthey otherwise would have been. Compromises are inevitable during theimplementation process.

• After careful analysis, strategy decisions can be clearly specified, summarised andpresented; they do not need to be altered because circumstances outside the companyhave changed. This is perhaps one of the greatest and most potent fallacies: itis never possible to avoid ambiguity completely, and it is potentially lethalto ignore changing competitive circumstances. One of the most importantreasons for company failure is the lack of a feedback mechanism and thechannels of communication that make it possible for decision makers toadapt to changing circumstances.

• Implementation is a separate and distinctive phase that only comes after a strategyhas been agreed. This assumption is possibly a reflection of the fact that theimplementation stage of strategy has always received much less attentionthan the more glamorous and exciting areas of objective setting and strategychoice. In reality nothing ‘just happens’, and an essential part of strategymaking is to evaluate the feasibility of different courses of action. It maywell be desirable, on financial grounds, to close a factory, but the actualprocess of achieving this may have widespread and damaging effects onthe company as a whole.

During the early 1960s the notion of prescriptive planning was quite popularand many corporations set up corporate strategic planning departments. How-ever, experience has revealed that the attempt to drive corporate strategy in thisrestrictive fashion is unproductive. A major problem arises when individualsbecome committed to the strategic plan itself, and not to the success of thecompany; this can occur when performance measures have been expressed infinancial terms and the pursuit of favourable financial reports takes precedenceover longer term issues.

Emergent Strategy

This approach starts from a different premise: that people are not totally rationaland logical. The extent of this irrationality has been the subject of some researchand the general findings accord with common sense.

• Managers can only handle a relatively small number of options.• Managers are biased in their interpretation of data – in fact any data set can

be interpreted in a number of legitimate ways, and it is not surprising that

1/10 Edinburgh Business School Strategic Planning

Module 1 / Introduction to Strategy, Planning and Structure

managers often select the interpretation which backs up their previouslydetermined views.

• Managers are likely to seek a satisfactory solution rather than maximiseprofits.

• Organisations consist of coalitions of interest groups. The implementationof decisions depends on negotiation and compromise between those groups,leading to unpredictable outcomes.

• When making decisions, managers pay as much attention to a company’sculture and politics as to factors such as resource availability and externalfactors.

According to this approach strategy is not planned before the event butemerges over time in an unpredictable manner and hence may appear to havelittle structure; it is therefore argued that the claim of a cause and effect relation-ship between analysis and strategy choice and implementation is fundamentallyflawed.

There is another very good reason why there is a limited use of informationin decision making: the world is actually too complex to be understood by thehuman brain. Rationality has to be seen in the context of what is possible in thereal world, rather than what might be done in an ideal world. The term usedto describe rationality when it is impossible to take into account the complexityof real life is ‘bounded rationality’; the decision maker is rational given theinformation available, but is quite aware that more information could be obtainedat a cost. In economics it is argued that broadly speaking decision makers actin accordance with profit maximisation, but it is impossible to reconcile profitmaximisation with bounded rationality. This means that a different view ofdecision making has to be taken and the term ‘satisficing’7 was invented toreflect the fact that decision makers collect information and defer selecting acourse of action until the costs of further delay and information collection areconsidered to be greater than the potential benefits of searching out a betteroption. Thus rather than simply attempting to maximise profit, the decisionmaker satisfies himself that there is nothing more to be gained from furtherdelay. This helps to explain why decision makers are so eager to find out whatmanagement gurus have said and are continually searching for ways of makingsense of the real world. To decision makers any information is better than noinformation, and it does not matter very much to them that the information theyare acting on does not accord with accepted views of what is proper scientificenquiry.

Another way of looking at this is to make up a list of things which thecompany does not know with any certainty when about to launch a newproduct; for example

• How customers will perceive quality• How far it will be possible to meet production cost targets• How competitors will react• When a substitute will appear on the market• The impact on sales of a one year delay in launch

Strategic Planning Edinburgh Business School 1/11

Module 1 / Introduction to Strategy, Planning and Structure

It is certainly possible to collect some information on such issues, but it willnot be complete and is likely to be unreliable. In fact, it turns out that youcan not actually get hold of the really important information and it is alwaysnecessary to make assumptions and to take many things on trust.

However, it can be argued that just because the world is a complex andchanging place does not mean that decision makers should simply sit back andlet things happen and that there is still a role for the proactive approach.

• While there are bound to be adjustments to corporate objectives as timegoes on, the company can still be directed along the general lines of abroad mission. The Board need to do more than simply react to changingcircumstances.

• There is a need for efficient resource allocation; if this is not tackled resourcesmight as well be allocated randomly.

• While compromises need to be made with interest groups within the organ-isation, this is more of a constraint than a barrier to action. Decisions stillhave to be taken, and it is nonsense to avoid this simply because people aredifficult to manage.

• In many cases investments take a considerable time to reach fruition, there-fore a degree of long term planning is inevitable.

• Satisficing is in itself a rational basis for choice, since it is better to make aninformed judgement on the basis of some information than no informationat all, or to ignore information altogether.

• The act of attempting to plan at least makes the basis for managementaction clear.

Therefore there is some middle ground between trying to plan for all eventu-alities and simply reacting to events as they occur.

Resource Based Strategy

This approach lays emphasis on the internal resources available to the company.While it does not overlook the importance of the competitive environment,it starts from the basic premise that strategy is primarily concerned with thesearch for competitive advantage, and to a large extent the source of competitiveadvantage rests within the organisation’s resources. The resource based viewdoes not focus so much on the actual labour and capital deployed by thecompany, but rather on the way in which these resources are utilised. It startsfrom the premise that a successful company is not a passive collection ofresources which reacts to changes in the competitive environment, but is onethat develops the ability not only to take advantage of opportunities as theyarise, but to create the opportunities themselves by innovative behaviour.

Ways in which this might be put into practice include the idea of totalquality management, which attempts to orientate all resources in the company todelivering high quality output to customers and establishing a reputation whichis a significant competitive asset. Another is the development of distinctivecompetencies which other companies do not have and cannot imitate and whichprovide the basis for lasting competitive advantage. None of the resource based

1/12 Edinburgh Business School Strategic Planning

Module 1 / Introduction to Strategy, Planning and Structure

approaches provides a full prescription for success, and research into theireffectiveness is still at a relatively early stage; this being the case, it is notsurprising that there is a great deal of controversy surrounding the pay off fromthe resource based approach.

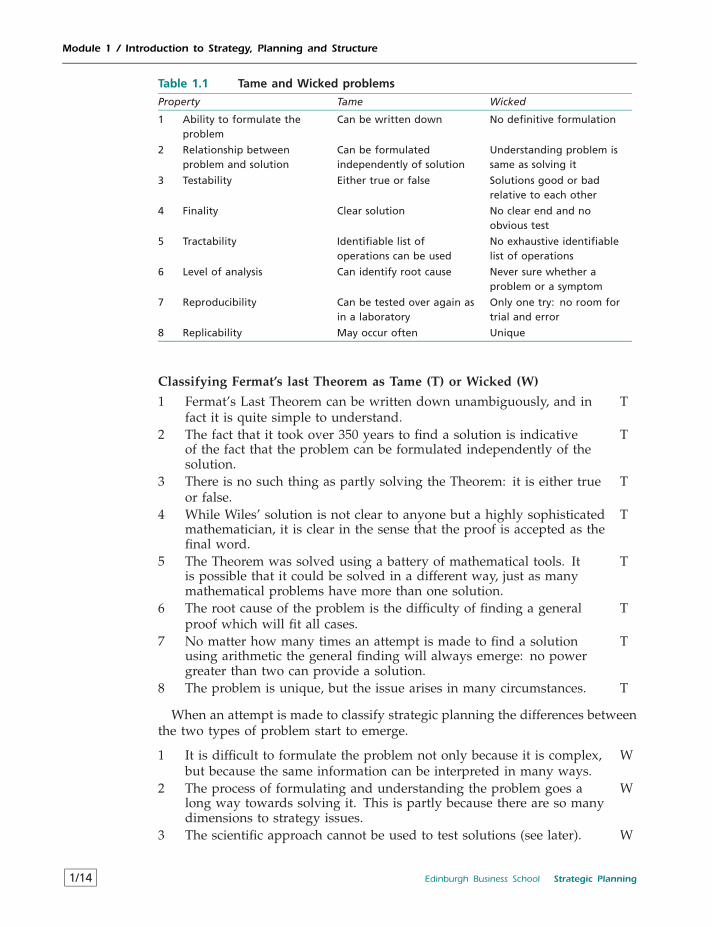

1.2.4 Rittell’s Tame And Wicked Problems

It should be clear from the preceding discussions that strategic planning, orstrategy, is a complicated subject. If you think of strategy as being a problemto solve, say for a particular company, it does not take long to realise that itis incredibly complex; the trouble is that there is a lot of confusion about whatthe terms ‘difficult’ and ‘complex’ actually mean. At one time, for example, itwas thought that the problem of running an economy efficiently was solvablein the sense that a sufficiently powerful computer program could work out allinput requirements for feasible outputs and allocate resources accordingly. Theplanners in the old Soviet economies fell into this trap, and were of the opinionthat it if you worked at it long enough it would be possible to plan the economy.But what if the basic premise were totally wrong, i.e. it is not possible even inprinciple to plan an economy or a company with any degree of precision? Theimplications of this are quite profound because if the notion that a ‘perfect’ planis mistaken in principle we move into different conceptual territory.

Here is a warning before you tackle the rest of this section. Some studentsfind this argument somewhat academic and feel that it merely defines thedifference between ‘scientific’ and ‘non-scientific’ problems. However, this is notthe case because the distinction is between different types of problem, whetherthey are defined as scientific or not. It is usually felt that strategy problemsare difficult because they are complex, but the shortcoming of focusing oncomplexity becomes clear when problems are classified as ‘tame’ or ‘wicked’in the sense used by Rittel8. In this scheme, wicked means much more thanincredibly complex. For example, consider Fermat’s Last Theorem; in about 1637the mathematician Fermat noted that he had a proof for the proposition thatthere were no three numbers which would fit the expression

xn + yn = zn, where n > 2

The trouble was that he claimed not to have sufficient room in the marginto elaborate the proof. The search for the proof occupied many mathematiciansfor the next three hundred years, and it was not until 1993 that Andrew Wiles,after many years of effort, found the solution using highly refined and abstractmathematical concepts. There is no doubt that Fermat’s Last Theorem is anincredibly complex problem, but consider it in the light of Rittell’s distinctionbetween tame and wicked characterised in Table 1.1.

Is Fermat’s Last Theorem a tame or wicked problem? The following classi-fication suggests that it is overwhelmingly a tame problem, despite its greatdifficulty and complexity. You may disagree with some of the individual classi-fications, but it is unlikely that more than two categories can be unambiguouslyclassified as wicked.

Strategic Planning Edinburgh Business School 1/13

Module 1 / Introduction to Strategy, Planning and Structure

Table 1.1 Tame and Wicked problems

Property Tame Wicked

1 Ability to formulate theproblem

Can be written down No definitive formulation

2 Relationship betweenproblem and solution

Can be formulatedindependently of solution

Understanding problem issame as solving it

3 Testability Either true or false Solutions good or badrelative to each other

4 Finality Clear solution No clear end and noobvious test

5 Tractability Identifiable list ofoperations can be used

No exhaustive identifiablelist of operations

6 Level of analysis Can identify root cause Never sure whether aproblem or a symptom

7 Reproducibility Can be tested over again asin a laboratory

Only one try: no room fortrial and error

8 Replicability May occur often Unique

Classifying Fermat’s last Theorem as Tame (T) or Wicked (W)

1 Fermat’s Last Theorem can be written down unambiguously, and infact it is quite simple to understand.

T

2 The fact that it took over 350 years to find a solution is indicativeof the fact that the problem can be formulated independently of thesolution.

T

3 There is no such thing as partly solving the Theorem: it is either trueor false.

T

4 While Wiles’ solution is not clear to anyone but a highly sophisticatedmathematician, it is clear in the sense that the proof is accepted as thefinal word.

T

5 The Theorem was solved using a battery of mathematical tools. Itis possible that it could be solved in a different way, just as manymathematical problems have more than one solution.

T

6 The root cause of the problem is the difficulty of finding a generalproof which will fit all cases.

T

7 No matter how many times an attempt is made to find a solutionusing arithmetic the general finding will always emerge: no powergreater than two can provide a solution.

T

8 The problem is unique, but the issue arises in many circumstances. T

When an attempt is made to classify strategic planning the differences betweenthe two types of problem start to emerge.

1 It is difficult to formulate the problem not only because it is complex,but because the same information can be interpreted in many ways.

W

2 The process of formulating and understanding the problem goes along way towards solving it. This is partly because there are so manydimensions to strategy issues.

W

3 The scientific approach cannot be used to test solutions (see later). W

1/14 Edinburgh Business School Strategic Planning

Module 1 / Introduction to Strategy, Planning and Structure

4 It is not clear where the problem ends because of real worlddynamics. It is impossible even to visualise the time frame overwhich a proposed solution will prevail.

W

5 There are many techniques which can be applied, and no agreementon which is most effective in which circumstances. This ischaracterised by management ‘fads’ which come and go regularly.

W

6 The cause is usually not clear, and symptoms are often confused withproblems; for example, a falling market share may be a symptom ofdiminishing competitive advantage.

W

7 Opportunities typically only present themselves once, and it isimpossible to go back in time and try again.

W

8 Each business problem is unique, although it may share commonfeatures with other situations.

W

While there is room for discussion on the extent to which each issue can beclassified as tame or wicked, there is no doubt that strategic planning emergesoverwhelmingly as a wicked problem. Managers may feel that they understandstrategy problems better than Fermat’s Last Theorem, and that they could neverremotely understand the solution to the Theorem; but in fact it is meaninglessto compare the two types of problem because they are intrinsically different.

1.2.5 The Origins of Strategy and Tactics

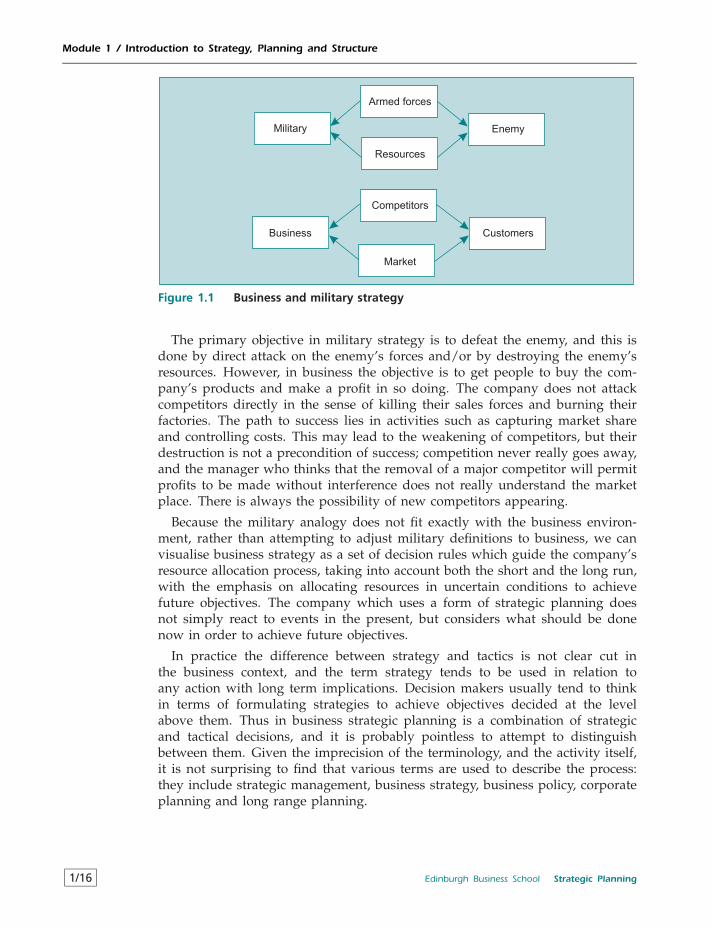

The roots of the word ‘strategy’ lie in the Greek strategio, meaning a general,stratos meaning an army, and agein meaning to lead. Some dictionaries definestrategy as the planning and implementation of military campaigns; its meaninghas widened in common use to include activities such as gaming and busi-ness, in which planning and the implementation of plans are undertaken. In theexpression ‘strategic planning’ the term ‘planning’ is therefore tautologous, sinceit is already included in the concept of strategy. Despite the tautology, the termhas now been accepted in general use, particularly in business schools and in theliterature relating to strategic activities in business. Given the origins of strategy,it is not surprising to find that many of the ideas of military strategy havebeen carried over to business strategy; these include setting objectives, identify-ing strengths and weaknesses, organising resources accordingly and evaluatingoutcomes.

Tactics is a notion which is closely related to strategy. Again, the meaningcan be clarified by the Greek roots: taktikos meaning fit for arranging, andtaktos meaning ordered. The military definition relates to the science or art ofmanoeuvring in the presence of the enemy. Thus, in the military context, strategyis deciding what is to be done, and tactics is deciding how individual objectivesare to be achieved.

The attempt to transplant these military ideas into business has led to somedegree of confusion. The basic reason for this is that running a business is nottruly analogous to fighting a war, although there are many similarities in acompetitive environment. Figure 1.1 is by no means definitive, but it gives animpression of the difference between military and business strategy.

Strategic Planning Edinburgh Business School 1/15

Module 1 / Introduction to Strategy, Planning and Structure

Armed forces

Resources

EnemyMilitary

Competitors

Business

Market

Customers

Figure 1.1 Business and military strategy

The primary objective in military strategy is to defeat the enemy, and this isdone by direct attack on the enemy’s forces and/or by destroying the enemy’sresources. However, in business the objective is to get people to buy the com-pany’s products and make a profit in so doing. The company does not attackcompetitors directly in the sense of killing their sales forces and burning theirfactories. The path to success lies in activities such as capturing market shareand controlling costs. This may lead to the weakening of competitors, but theirdestruction is not a precondition of success; competition never really goes away,and the manager who thinks that the removal of a major competitor will permitprofits to be made without interference does not really understand the marketplace. There is always the possibility of new competitors appearing.

Because the military analogy does not fit exactly with the business environ-ment, rather than attempting to adjust military definitions to business, we canvisualise business strategy as a set of decision rules which guide the company’sresource allocation process, taking into account both the short and the long run,with the emphasis on allocating resources in uncertain conditions to achievefuture objectives. The company which uses a form of strategic planning doesnot simply react to events in the present, but considers what should be donenow in order to achieve future objectives.

In practice the difference between strategy and tactics is not clear cut inthe business context, and the term strategy tends to be used in relation toany action with long term implications. Decision makers usually tend to thinkin terms of formulating strategies to achieve objectives decided at the levelabove them. Thus in business strategic planning is a combination of strategicand tactical decisions, and it is probably pointless to attempt to distinguishbetween them. Given the imprecision of the terminology, and the activity itself,it is not surprising to find that various terms are used to describe the process:they include strategic management, business strategy, business policy, corporateplanning and long range planning.

1/16 Edinburgh Business School Strategic Planning

Module 1 / Introduction to Strategy, Planning and Structure

1.2.6 Strategy and the Scientific Approach

The social sciences are concerned with analysing and explaining humanbehaviour in the areas of economics, behavioural relationships, social inter-action, and so on. The business disciplines are largely concerned with applyingthe methods of the social sciences to the running of companies. For example,the idea of economies of scale originates from economic theories relating to thecombination of the factors of production, and has been subjected to a greatdeal of empirical testing. It is well known that economies of scale can lead tolower average costs, possibly up to some point beyond which costs no longerfall; however, the theory underlying economies of scale is quite subtle and doesnot lead to the expectation that decreasing average cost with size will actuallybe observed even in those industries where economies of scale exist. This isbecause of the concepts of short run and long run adjustment to different levelsof output; economies of scale will only be observed where firms have made‘long run’ adjustments to their factor inputs. As a result, it is necessary to takea sample of firms in order to carry out statistical analysis because, for any givensize of firm, there is likely to be a range of unit cost; the statistical analysis takesaccount of the random variations from the underlying relationship between sizeand unit cost.

Those who have been trained in science will recognise elements of what isknown as the scientific method in the description of how economies of scalemight be estimated: a theory is developed based on ideas relating to costs, ahypothesis is derived from the theory (i.e. something which can be tested), dataare collected, subjected to appropriate analysis, and the hypothesis is acceptedor rejected. This rigorous approach appeals to the ordered mind, and is usuallyused as a benchmark as to whether a subject ought to be deemed scientific.Disciplines are often (explicitly or implicitly) ranked according to where theylie on the scientific spectrum on the basis of whether the scientific method isapplied. Physics lies at the top end of the scientific spectrum and the socialsciences lie near the bottom and above the arts; among the social scienceseconomics is typically regarded as the most scientific. But it is important to beaware that philosophers of science do not agree on what the scientific methodactually is. It is not necessary to go into the subject in detail, but a brief outlineof the main strands of thought gives an impression of how scientific thinkingitself has developed.

The best known view, advanced by the philosopher Karl Popper, is thathypotheses or theories can only ever be falsified; it is impossible to verifya theory because the possibility that it might be falsified always exists. Thetrouble is that, by the same token, it is not possible to falsify a theory either,because the reverse is also true. In other words, it is never possible to arrive at adefinite answer on the basis of the evidence available. A wider view, associatedwith Kalakos, is that it is not the testing of individual theories that is important,but the overall research programme; individual projects only have relevancein the context of the programme and there is no such thing as falsification.Finally, a contrary view expressed by Feyerabend is that the scientific method isunduly constrictive, and the major discoveries have not been made as a resultof following it. In fact, this view holds that discoveries are much more the

Strategic Planning Edinburgh Business School 1/17

Module 1 / Introduction to Strategy, Planning and Structure

result of lateral thinking and chance events, and that subsequently they aremade respectable by framing the discoveries in the scientific manner. ThomasKuhn pointed out that the prevailing mode of thought, or scientific paradigm,determines what is thought of as science, and the paradigm itself is subject tochange over time. The scientific paradigm that the earth is flat and is orbitedby the sun was only overturned after a great deal of controversy; similarly, thescientific approach outlined above is just a paradigm of thought, and is noteven rigorously applied in physics, a discipline in which there is a great deal ofspeculative thinking.

It is intuitively attractive to apply the scientific method to strategy makingand, by following the approach used to estimate economies of scale, identifycriteria for effectiveness which can be applied in a variety of circumstances. Butwhen attempting to apply the scientific method to the question of what courseof action is likely to lead to success for a company, we are faced with severalintractable problems.

• As indicated above, there are different views on what strategic planningactually is; for example, many studies have attempted to measure the impactof planning systems on company performance, but planning systems andstrategic planning are not necessarily closely related.

• The types of company, the environments in which they operate, and theproblems facing them, are so different that it is difficult to do more thandraw general similarities among companies and situations. In other words,the range of variables which would have to be controlled for is enormous.

• There may be significant interactions among variables; for example,economies of scale may only occur in certain circumstances, and the use ofcompany size on its own as an indicator of potential economies of scale maybe misleading. Another way of expressing this is that the company as awhole is more than the sum of its individual parts, and undue emphasis ondisaggregating the functions and characteristics of a company can obscurethe overall picture.

• Companies and their markets change with the passage of time, and com-bined with the inevitable lags between actions and outcomes, it becomesimpossible to disentangle cause and effect. In other words, it cannot beinferred with certainty that a company succeeded either because it madethe right decisions or because circumstances turned out to be favourable inrelation to what it did. It is easy to fall into the trap of post hoc, ergo propterhoc, i.e. the fallacious reasoning of being after this, therefore being becauseof this.

So there are two levels of problem in trying to find out anything about thereal world. First, the scientific method cannot provide definite answers; at bestit is a rigorous approach which identifies the necessary steps in an investigation.Second, the data available in real life do not make it possible to test hypothesesabout strategy.

The problem of dealing with large numbers of interacting variables subjectto lags is not unique to the analysis of strategic planning; research into edu-cation is another example where student, teacher and social characteristics are

1/18 Edinburgh Business School Strategic Planning

Module 1 / Introduction to Strategy, Planning and Structure

notoriously difficult to measure, and interaction effects between teachers andstudents are likely to be important. Researchers have to make a choice betweentwo approaches to educational studies: concentrate on relatively few institutionsin depth, or carry out a large scale survey on many institutions. The large scalestudy cannot take into account as many variables as the in-depth study, andmay omit many potentially important variables; furthermore, those variablesincluded in the study may not be the most important but merely those mostsusceptible to measurement. However, the results obtained in the large scalestudy are likely to be of general applicability; while the small scale study cantake into account many more variables the results cannot be generalised becausethey may be particular to the cases studied. There are therefore costs and benefitsassociated with both large scale and in-depth methodologies.

Research into strategy is dominated by the in-depth approach, which meansthat any prescription for ‘best practice’ strategy can only be corroborated byreference to relatively few cases. A feature of the strategy literature is that it isheavily spiced with anecdotes, and evidence in favour of hypotheses comes inthe form of what is sometimes known as casual empiricism. But if there is noscientific proof in favour of different courses of action, how is it that expertsin strategy command very high fees for telling companies what they should bedoing? To some extent there is a degree of fashion in strategy advice. There is nodoubt that experts have offered different prescriptions for strategy approaches:that consistency of delivery is the key issue; that striving for higher qualityis a major success factor in its own right; that diversification is an essentialaspect of company growth; that company success depends on the identificationand exploitation of core competencies; that internationalisation is the engine ofgrowth; that a strong home base is a prerequisite for international success. Thescientifically trained may find it puzzling that so much credibility is attached toprescriptions which have no empirical foundation. On the other hand, managerspoint out that they have to operate in an environment in which the scientificapproach cannot be applied, that the anecdotal approach is better than nothing,and it is necessary to use what we do know in order to introduce rationalityinto decision making. The question of whether a company strategy will work inpractice is as uncertain as an economic strategy for a country as a whole.

In 1990 the UK adopted the strategy of entering the European Exchange RateMechanism (ERM) with the objective of curing both inflation and a chronicimbalance of trade; despite the enthusiasm for this move in many quarters, byearly 1991 it was obvious that membership of the ERM was not an immediatecure for the underlying problems of relatively low productivity and overheatedlabour markets. This led to a loss of confidence in the UK economy on thepart of international speculators, and in September 1992 the UK had no optionbut to leave the ERM and the currency immediately depreciated by about 15%against the German mark. Some prominent economists gloated that they hadpredicted this outcome from the beginning; others were dumbfounded. Thepoint to ponder is that if this strategy, which was subject to so much informedanalysis, could end in utter disaster, then the same fate can well lie in store forcompany strategies.

One of the best known attempts to identify the company characteristics which

Strategic Planning Edinburgh Business School 1/19

Module 1 / Introduction to Strategy, Planning and Structure

lead to strategic success is contained in the book In Search of Excellence.9 Theirquest for the characteristics of excellent companies was based on a non-randomsample of 43 US companies which fulfilled stringent market conditions forsuccess; these included three measures of growth and long term wealth creationover a 20 year period, three measures of return on capital and sales, and the viewof industry experts on the company’s innovative track record. With the resourcesat their disposal it was possible to interview 21 of the companies in depth, andconduct less intensive studies on the remainder. The research identified eightattributes which characterised the excellent, innovative companies as defined.Without going into the details of these attributes, the authors acknowledge that‘Most of these eight attributes are not startling.’ They also acknowledge thatthe eight attributes were not present to the same degree in all of the companiesstudied; however, the authors claimed that there was a preponderance of theeight in each company, and that the general traits of the companies wereobvious. This is something which we have to take on trust. The point here isnot to criticise the research, but to use it as an example of how difficult it is tofind out anything from the experience of actual companies.

The authors also acknowledge that they cannot guarantee that the companieswill remain in the excellent category, but they do maintain that these com-panies will cope with adversity better than companies which do not have theirattributes. This brings us to the logical problem in interpreting the researchfindings: the companies were defined as being excellent on the basis of beinggood market performers and having a good innovative track record; anotherway of looking at this conclusion is to say that successful companies stand abetter chance of being successful in the future, and the attributes identified inthe research may have little to do with future success. It does seem rather oddthat all of the excellent companies exhibited the identified attributes; there isclearly a danger here of having identified companies as being excellent on thebasis of the attributes in the first place, because that was what the researcherswere looking for. Because business conditions are continually changing, it isdifficult to falsify or verify the authors’ claim of continuing success; there isno doubt that the 43 companies listed on pages 20–21 of their book have gonein different directions: Wang Laboratories failed as did Digital Equipment, andGeneral Motors’ market share in the US dropped from 55 per cent to 33 percent, the company losing $4 billion in 1991; on the other hand companies suchas Disney Productions have continued to be highly successful. But this is not thewhole story, since Disney found it extremely difficult to transplant its successfulUS operations into France – the troubled history of Euro Disney is discussed inPractice Final Examination 2.

An important issue is whether they have performed, and will continue toperform, as a group better than companies which did not exhibit the excellentattributes; this would be the subject of another research project. On balance itseems that the research did not identify all the attributes of successful com-panies, nor can we be confident that those which it did identify were relativelyimportant. For example, it may be that the history of these companies since1982 can be explained by changes in competitive conditions, and the degreeof competitive edge conferred on them by the identified attributes had only aminor impact on their performance.

1/20 Edinburgh Business School Strategic Planning

Module 1 / Introduction to Strategy, Planning and Structure

An attempt to determine whether strategy making processes rather than othercompany characteristics make a difference to company performance was carriedout by Hall and Banbury.10 This was a large scale study which obtained responsesfrom over 300 companies, and it is interesting for the light which it sheds on theproblems of carrying out research in the area rather than in the statistical findingsthemselves (which are hedged with qualifications because of the limitations ofthe study). The objective of the study was to concentrate on whether a strategyprocess was followed rather than what it was; for example, the split betweenthe rational and the incremental approaches was considered too simple to beuseful. What the authors considered important was the accumulation of strategyskills over time, or the development of a strategy making process capability;this is clearly a subjective variable and is open to interpretation based on theinformation provided by the respondents. They pointed out that the one variablewhich cannot be used as a performance measure is current profitability, becauseof lagged effects; this means it is necessary to use measures such as new productdevelopment, innovation, social responsiveness and growth, all of which are alsosubject to subjectivity and may be irrelevant in certain cases. By and large, itwas found that strategic process capability counts: that the more firms in thestudy were able to develop competence in multiple modes of strategy makingprocesses then the higher their performance. But the authors make a telling pointwhich makes it impossible to draw specific lessons from the study: the directionof causation may be the other way round, and it may be that successful firmsadopt processes which accord with the definitions of strategic process capability.This is a particular problem when looking at a cross section of companies atone time, where it is not possible to pursue the dynamics of strategy makingand performance. So even a well specified and conducted study which producesstatistically significant findings may contain little more than a description of theway the world is.

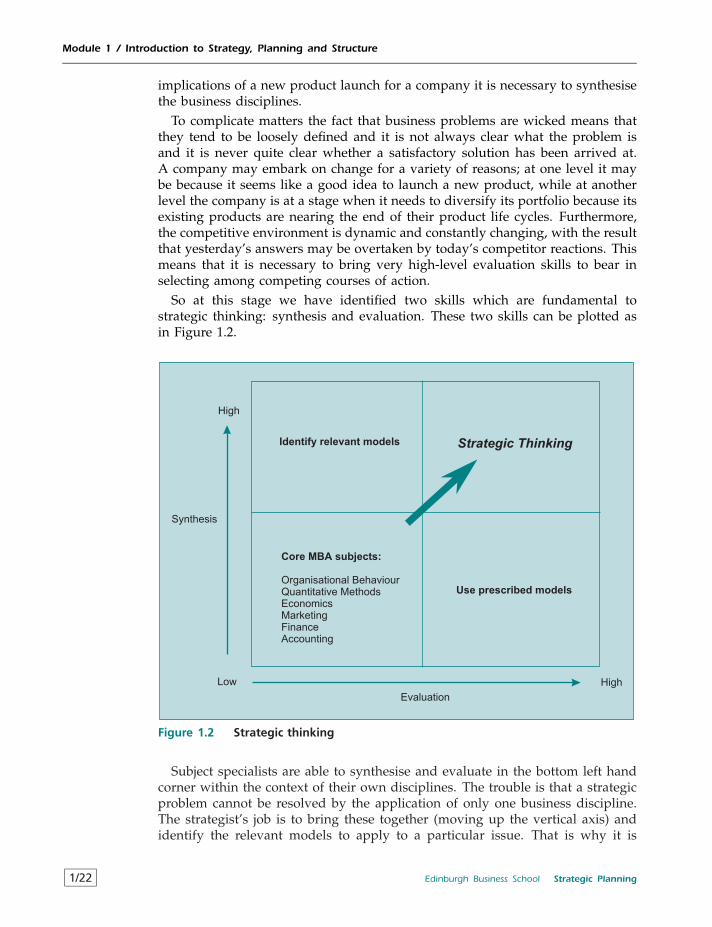

1.2.7 Strategic Planning and Strategic Thinking